KeyBanc Capital Markets

2005 Industrial &

Automotive Investment

Conference

June 8, 2005

Charles G. “Chip” McClure

Chairman, CEO and President

James D. Donlon, III

Sr. Vice President and CFO

Rakesh Sachdev

Sr. Vice President Corporate Strategy

Cautionary Statement Concerning

Forward-Looking Statement

This presentation contains “forward-looking statements” as defined in the Private Securities

Litigation Reform Act of 1995. These forward-looking statements are based on currently available

competitive, financial and economic data and management’s views and assumptions regarding

future events. Such forward-looking statements are inherently uncertain, and actual results may

differ materially from those projected as a result of certain risks and uncertainties, including but

not limited to global economic and market conditions; the demand for commercial, specialty and

light vehicles for which the company supplies products; risks inherent in operating abroad,

including foreign currency exchange rates and potential disruption production and supply due to

terrorist attacks or acts of aggression; availability and cost of raw materials, including steel; OEM

program delays; demand for and market acceptance of new and existing products; reliance on

major OEM customers; labor relations of the company, its customers and suppliers; the financial

condition of the company’s suppliers and customers, including potential bankruptcies; successful

integration of acquired or merged businesses; achievement of the expected annual savings and

synergies from past and future business combinations; success and timing of potential

divestitures; potential impairment of long-lived assets, including goodwill; competitive product

and pricing pressures; the amount of the company’s debt; the ability of the company to access

capital markets; the credit ratings of the company’s debt; the outcome of existing and any future

legal proceedings, including any litigation with respect to environmental or asbestos-related

matters; as well as other risks and uncertainties, including but not limited to those detailed herein

and from time to time in ArvinMeritor’s Securities and Exchange Commission filings.

2

Agenda

Company Profile

Winning with the 3Rs

Profitable Growth Opportunities

Segments and Outlook

Summary

3

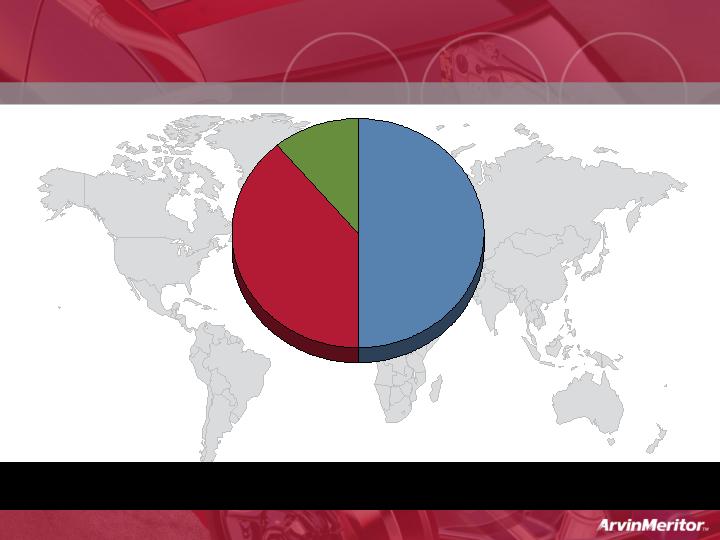

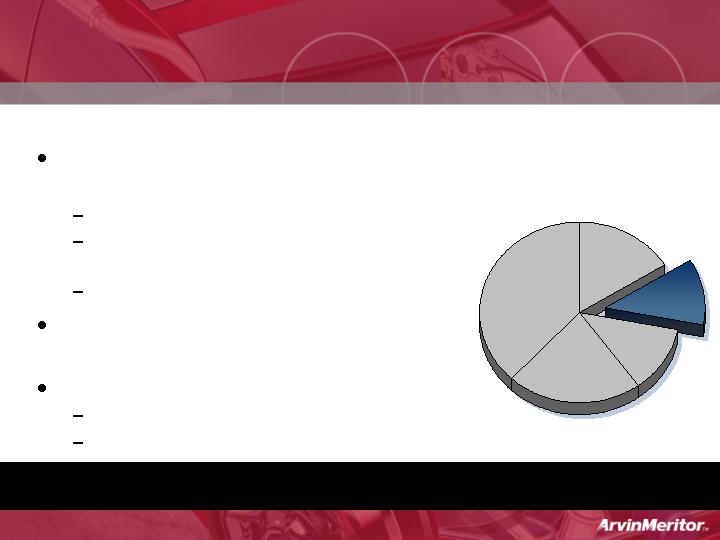

Two Focused Businesses

Market Diversity

Commercial

Vehicle

Systems

Light

Vehicle

Systems

60%

40%

Total Sales = $8.0B

Continuing Operations

FY 2004

4

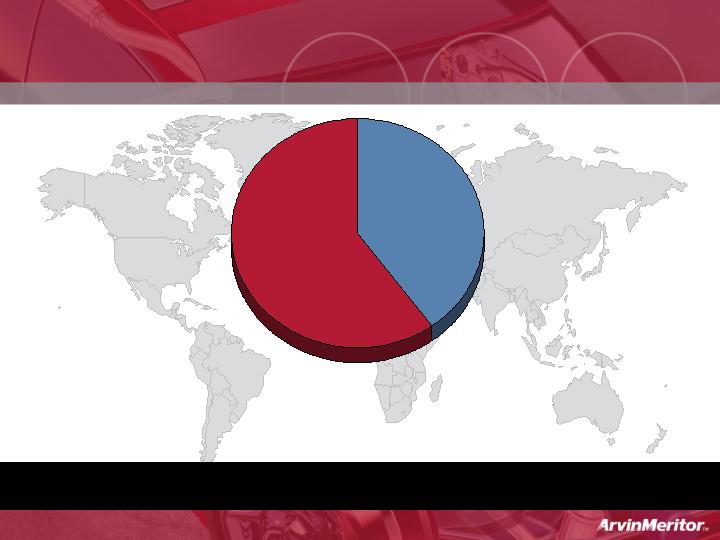

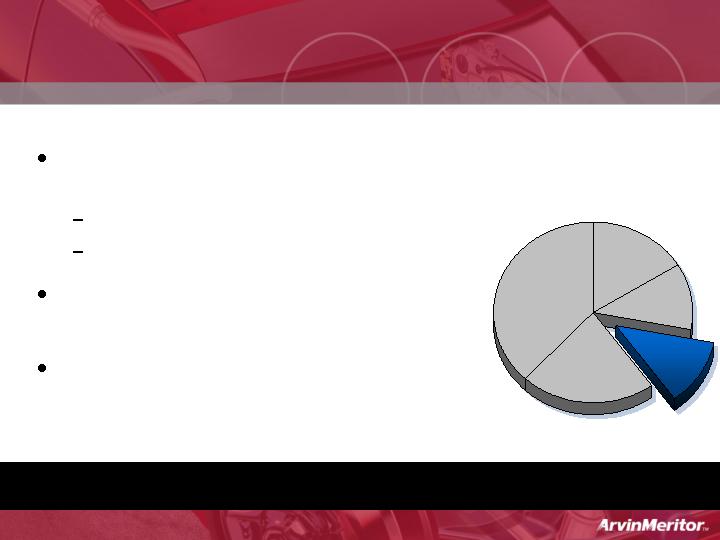

Geographic Split

Geographic Diversity

North

America

Europe

39%

50%

Total Sales = $8.0B

Continuing Operations

FY 2004

11%

Asia and

Other

5

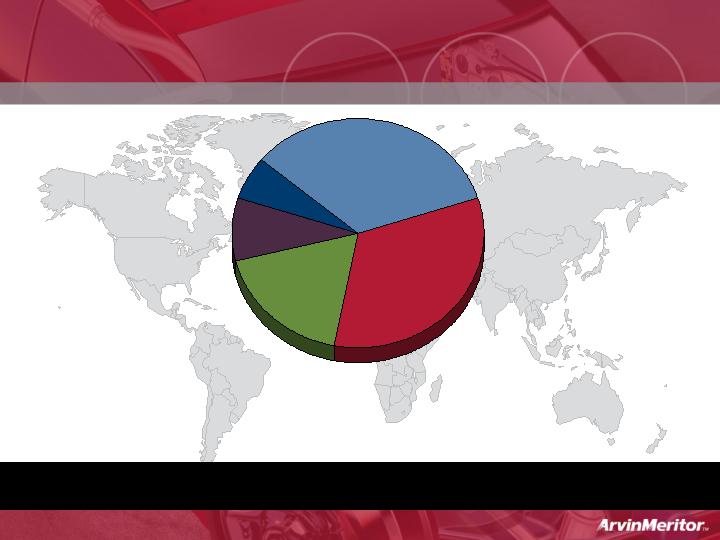

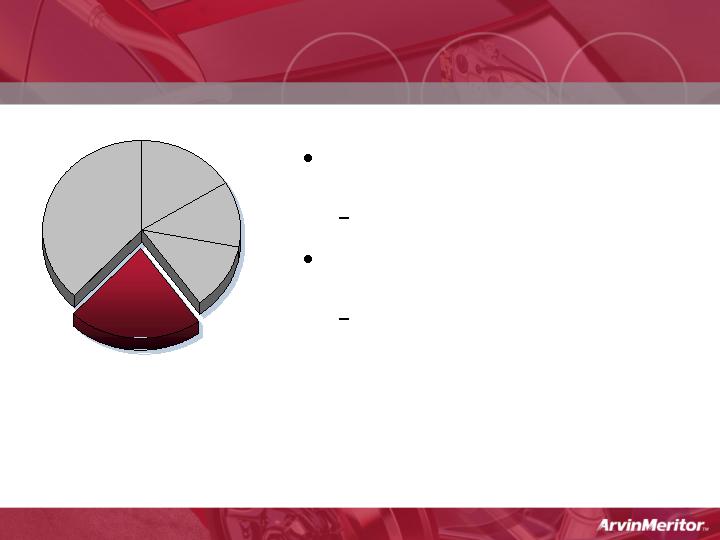

Product Line

Product Diversity

CVS –

Undercarriage

and Drivetrain

LVS –

Undercarriage

33%

34%

Total Sales = $8.0B

Continuing Operations

FY 2004

18%

9%

6%

LVS –

Emission

Technology

LVS -

Aperture

CVS -

Specialty

6

Agenda

Company Profile

Winning with the 3Rs

Profitable Growth Opportunities

Segments and Outlook

Summary

7

The 3Rs

Rationalize

Initiate

and

Execute

3Rs

Regenerate

Refocus

8

3Rs Update

Rationalize

400-500 salaried reductions

Closed 5 facilities over the

last two years

Focused and intense cost

reductions

Closing 11 facilities

Integrating and

consolidating other facilities

Efficient asset utilization

Expand margins

Align capacity to market

Higher return on assets

Refocus

Sold Roll Coater

Sold Automotive Stamping

Components

Sold Central Tubing Facility

Sold Trailer Axle Beam

Manufacturing Operation

Sell LVA (North America)

Sell LVA (Europe)

Evaluating all business lines

Sell other non-core and

non-performing businesses

Concentrate and focus on

businesses that generate

cash and strengthen

financial position

Regenerate

Volvo – RVI axles

Net new business

Hyundai doors

Strong CVA sales

On-Trac support

CVS new emission

technology contracts

Toyota emissions

Asia FAW brakes

Lexus steering (MSSC)

Fill strategic gaps

Bolt-on acquisitions,

alliances, and

partnerships

Expand global presence

China

India

Emissions 2007 - 2010

What have we done?

What are we doing now?

Where are we going?

9

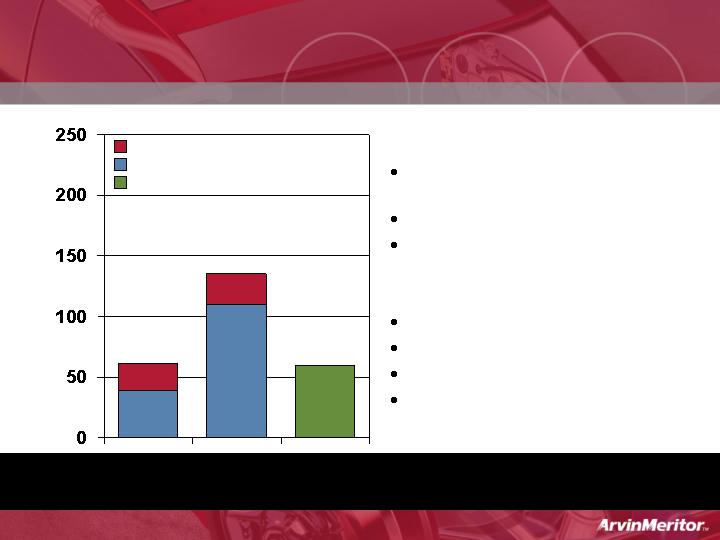

New Restructuring Actions

Summary of Plan

400-500 global salaried

employees

Close 11 facilities largely in LVS

Integration and consolidation of

other facilities

Benefits

Take out excess capacity

Improve fixed cost

Improve operational efficiencies

Improve manufacturing footprint

$23

$25

Non-Cash Costs

Cash Costs

Annual Savings

$39

$62

$110

$135

($ in millions)

Savings

Costs

2Q Charge

Remainder of Charges – Approximately $73M – to be

Incurred in the Next 12 - 18 Months

$50-$60

10

Agenda

Company Profile

Winning with the 3Rs

Profitable Growth Opportunities

Segments and Outlook

Summary

11

Expanding Our Global Presence in

Asia/Pacific

FY04 sales $397M

7 countries

24 sites

~2,100 employees

Global Strategy

12

Year-Over-Year Growth in China

Light Vehicle Systems

Commercial Vehicle Systems

Global Growth Strategy

13

Presence in Europe

FY04 sales $3.2B

12 countries

14 major

manufacturing and

distribution operations

Additional facilities

located throughout

Europe

~10,000 employees

Global Strategy

14

Presence in North America

Global Strategy

FY04 sales $4.0B

3 countries

60 sites

~15,000 employees

15

FY04 sales $312M

Three countries

Eleven sites

~2,500 employees

Global Strategy

Presence in South America

Note: Does not include discontinued operations

16

Unconsolidated joint ventures financial performance is strong

Sales $1.1B and Net Income of $56M

$600M in consolidated sales

Strong cash dividends

Total assets of unconsolidated joint ventures $454M

Twelve emerging market JVs

Taking advantage of domestic growth and export opportunities

Most are market leaders in their region

Joint Ventures Add to Success

17

Future Direction

LVS

Components:

Axles

Brakes

Suspensions

Drivelines

Controls

Sourcing

Design

Engineering

Suspension

Module

SYNERGIES

Integrated

Systems/

Modules

Total System

Design

Engineering

Expertise

Components:

Axles

Brakes

Suspensions

Drivelines

Controls

CVS

Future

Today

Undercarriage Growth Strategy

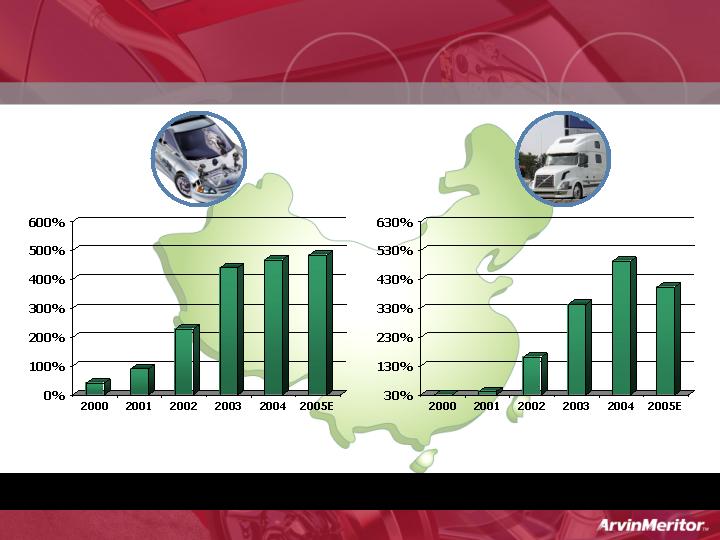

Worldwide Emissions Regulations

Emissions Growth Strategy

EPA ’98

EPA ’04

Euro IV

Euro III

Euro II

Euro I

Japan ‘05

Projected

Euro

III=

2010

Euro IV=

2006

Euro IV=

2010

Euro III= 2006

Euro IV= 2009

Euro III= 2007

Euro IV=2010

Euro IV=

20??

EPA ‘04=

2007

Euro V= 2008

Euro VI=2011

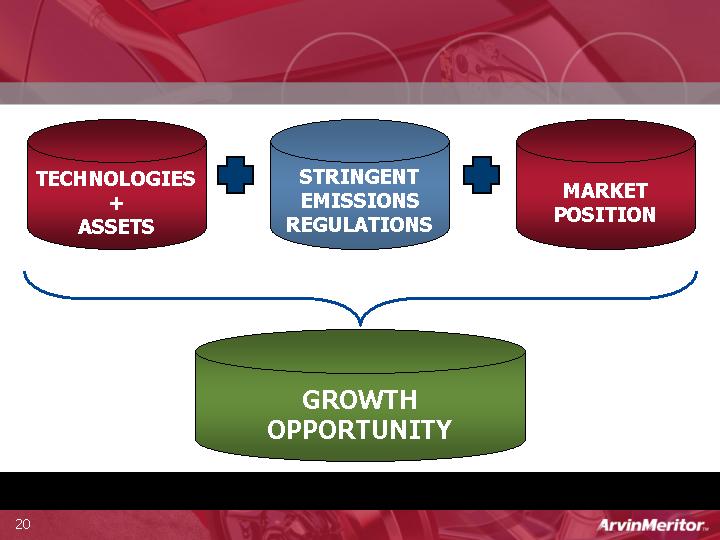

Significant Diesel Emissions Opportunity

LVS

CVS

EURO 4 & 5, US 2007 & 2010

JAPAN 2005

Emissions Growth Strategy

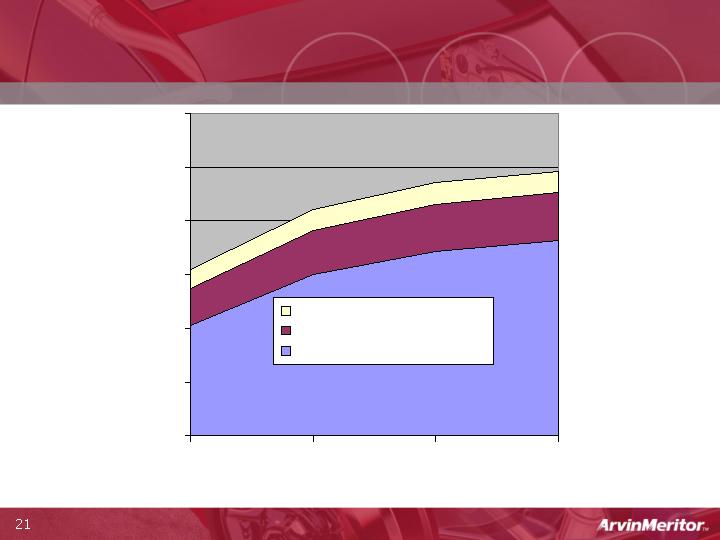

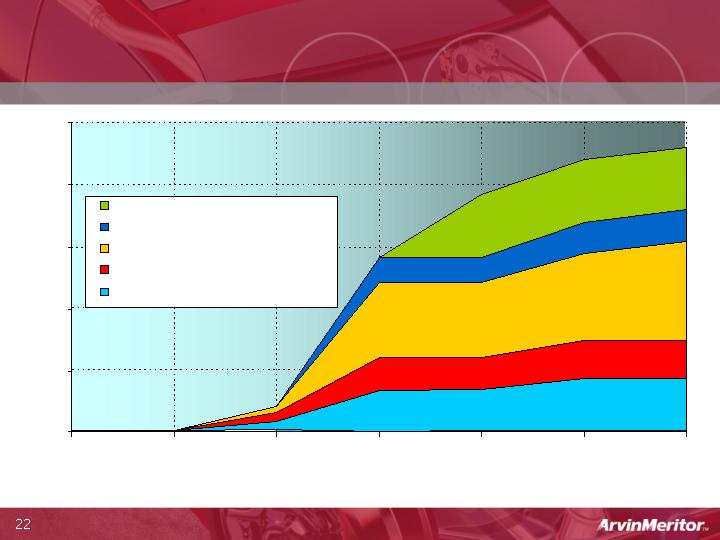

LVS Awarded Contract Volumes

Worldwide*

* Confirmed Business Only (Dec. 2004)

Calendar Years

$-

$50m

$100m

$150m

$200m

$250m

$300m

2005

2006

2007

2008

Manifold

NVH (mufflers)

DOC/DPF

CVS Awarded Contract Volumes

Europe and U.S.*

* Confirmed Business Only (Dec. 2004)

0

$50m

$100m

$150m

$200m

$250m

2003

2004

2005

2006

2007

2008

2009

Calendar Years

U.S. HD Truck PM Filter

European HD Engine PM Filter

European MD PM Filter

European HD Truck SCR

European HD/MD Truck SCR

Agenda

Company Profile

Winning with the 3Rs

Profitable Growth Opportunities

Segments and Outlook

Summary

23

Building Resilience

to Market and Customer Risk

Well-Defined Short-Term Strategies

and Actions for Each Segment

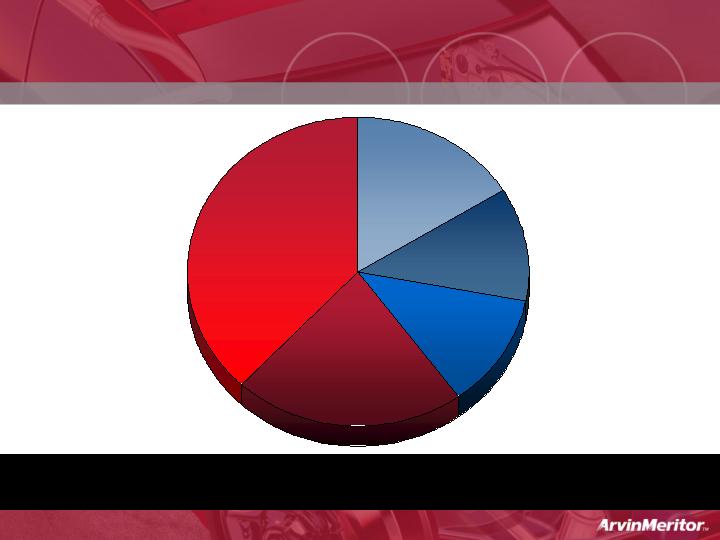

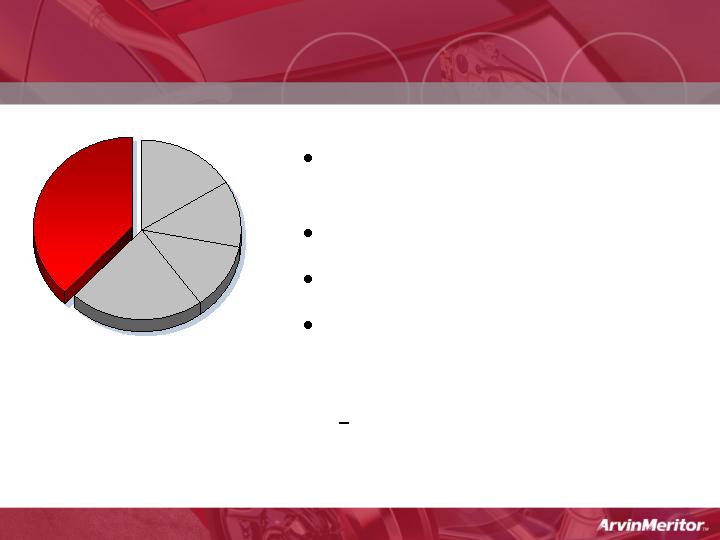

N.A. OEM

Truck & Trailer

Sales

16%

FY 2004

Europe &

ROW

OE Sales

12%

CV

Aftermarket &

Specialty

OEMs

12%

N.A. Big 3 LVS

OEM Sales

20%

Other LVS

OEM Sales

40%

Commercial

Vehicle

Systems

40%

Light

Vehicle

Systems

60%

24

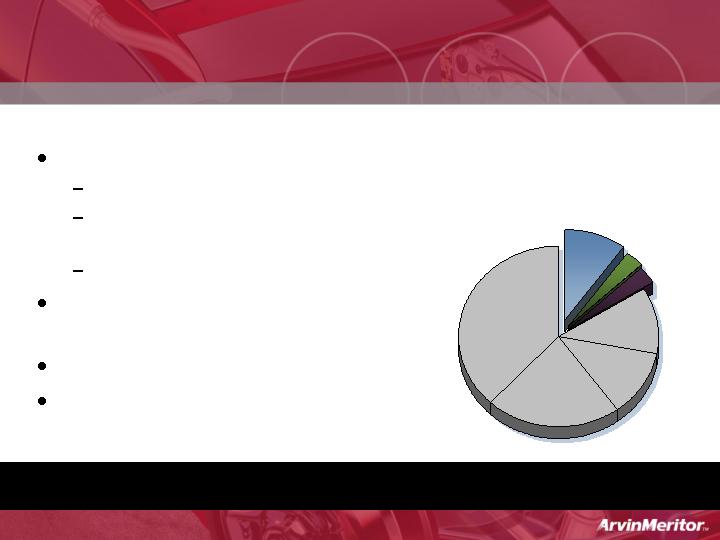

CVS N.A. OEM Truck and Trailer

Manage through economic cycles

Profitable during downturn

Layered capacity in developing

countries (Mexico, Brazil, Turkey, India)

Selling non-core assets

Leverage extensive and established

sales and service network

Seize emissions opportunity

Leverage “component” strength to

enter systems and modules business

N.A. OEM Truck

& Trailer Sales

16%

Successfully Managing Cyclicality

Class 8

10%

Class 5-7

3%

Trailers

3%

25

CVS Europe and Rest-of-World OEM

Successfully de-integrate OEMs

drivetrain business

Volvo/RVI axle and brake business

Emerging market opportunities (India

and China)

Other European OEMs

Leverage manufacturing footprint to

expand margins

CV Emissions business opportunity

SCR for Euro IV

Several contracts won

Europe & ROW

OEM Sales

12%

Continuing Growth Opportunities

26

CV Aftermarket and Specialty OEM

Leverage brand and distribution

channel to expand share and content

Growing brake business

Growing remanufacturing business

Synergies between OEM and

aftermarket

Core competencies in developing

mechanically complex and low-

volume specialty products

CV Aftermarket

& Specialty OEs

12%

Highly Stable and Profitable Business

27

Selective growth; manage for

margins

Exhaust, apertures

Selective growth; manage for

returns on invested capital

Suspension modules

N.A. Big Three Light Vehicle OEM Sales

N.A. Big Three

LVS OEM Sales

20%

28

Continue aggressive cost

reduction programs

Right-size manufacturing capacity

Flawless product launches

Continue growth in emerging

markets and with Asian OEMs in

North America

China, Korea, India

Other LVS OEM Sales

ROW LVS

OEM Sales

40%

29

CVS 2007 vs. 2001 – N.A. Truck Market

2001 Downturn

Class 8 market declined 50%

(to 150,000)

CVS OE business in NA ~ 60%

CVS business slightly profitable

(before restructuring)

ARM generated $188M in free

cash flow (lower working

capital)

2007 Downturn

Market expected to decline

less (~ 35%)

CVS OE business in NA <50%

CVS business profitability

expected to be higher

ARM free cash flow expected

to be healthy

2007 Downturn Not Expected to be as Severe When

Compared to the 2001 Downturn

30

Agenda

Company Profile

Industry Challenges

Winning with the 3Rs

Profitable Growth Opportunities

Summary

31

Financial Performance Improvement

CVS volumes and performance strong

Savings from restructuring initiatives and

productivity programs beginning to be realized

Impact of steel moderating

Managing through lower GM and Ford production

volumes

Q3 and Full Year Guidance Expected to be at the Top of

the Range

Appendix

33

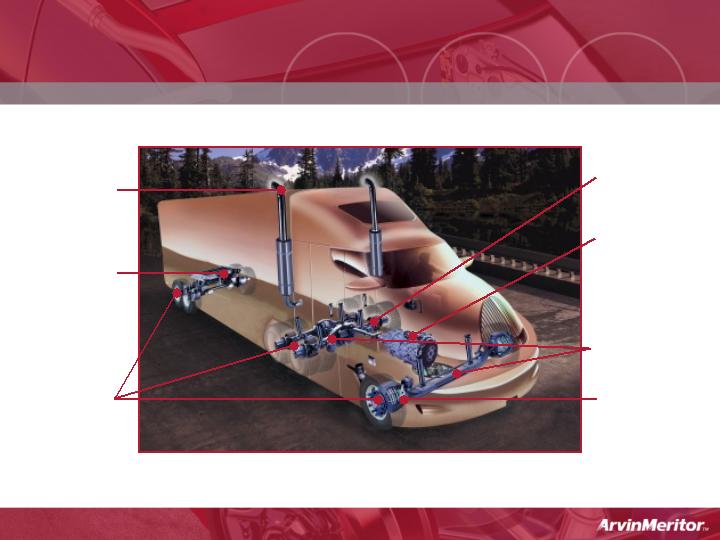

ABS, air

system and

stability

controls

Emissions

systems

Complete

Braking

systems

(wheel ends

and brakes)

Drivelines

Automated

transmissions

/clutch

Front and

rear axles

CVS Product Portfolio

Trailer and

suspension

systems

34

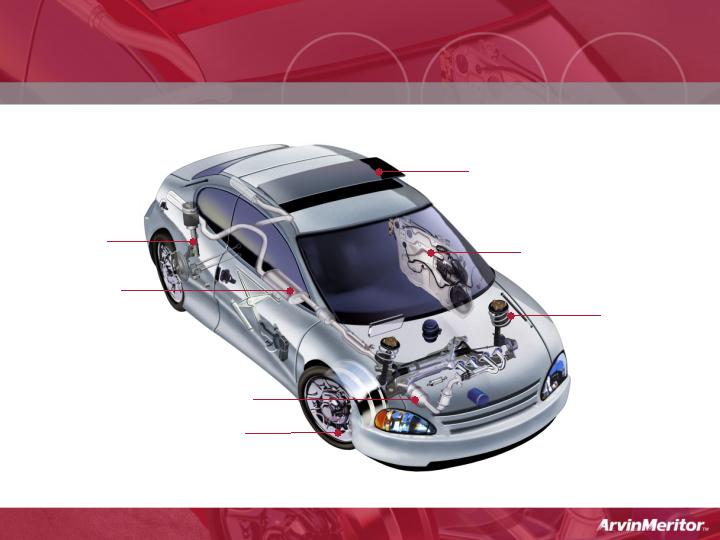

LVS Product Portfolio

Roof systems and modules

Door systems

and modules

Suspension

components

(coil

springs,

stabilizer

and torsion

bars)

Steel wheels

Emission systems

Suspension

modules

Exhaust

systems

35