8th Annual JPMorgan Harbour Auto Conference

August 1, 2005

James D. Donlon, III

Sr. Vice President and CFO

Cautionary Statement Concerning

Forward-Looking Statement

This presentation contains “forward-looking statements” as defined in the Private

Securities Litigation Reform Act of 1995. These forward-looking statements are based

on currently available competitive, financial and economic data and management’s

views and assumptions regarding future events. Such forward-looking statements are

inherently uncertain, and actual results may differ materially from those projected as

a result of certain risks and uncertainties, including but not limited to global economic

and market conditions; the demand for commercial, specialty and light vehicles for

which the company supplies products; risks inherent in operating abroad, including

foreign currency exchange rates and potential disruption production and supply due

to terrorist attacks or acts of aggression; availability and cost of raw materials,

including steel; OEM program delays; demand for and market acceptance of new and

existing products; reliance on major OEM customers; labor relations of the company,

its customers and suppliers; the financial condition of the company’s suppliers and

customers, including potential bankruptcies; successful integration of acquired or

merged businesses; achievement of the expected annual savings and synergies from

past and future business combinations; success and timing of potential divestitures;

potential impairment of long-lived assets, including goodwill; competitive product and

pricing pressures; the amount of the company’s debt; the ability of the company to

access capital markets; the credit ratings of the company’s debt; the outcome of

existing and any future legal proceedings, including any litigation with respect to

environmental or asbestos-related matters; as well as other risks and uncertainties,

including but not limited to those detailed herein and from time to time in

ArvinMeritor’s Securities and Exchange Commission filings.

2

Agenda

ArvinMeritor Business Overview

3rd Quarter Results

Outlook

3

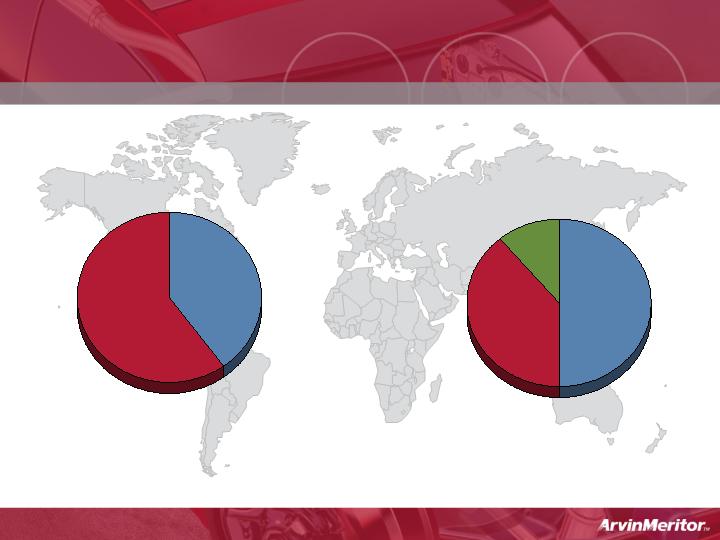

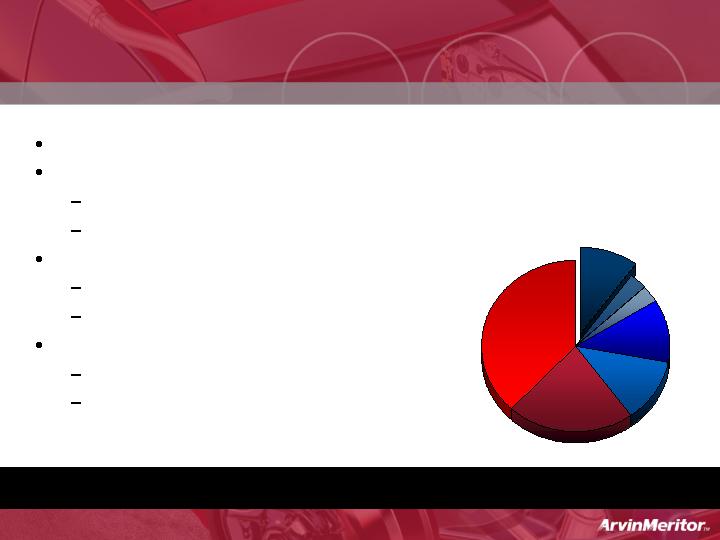

Diversified Global Company

North

America

39%

50%

11%

Asia and

Other

Europe

Commercial

Vehicle

Systems

Light

Vehicle

Systems

60%

40%

Business Segments

39%

11%

Geographic Sales

LVS sales are 55% and CVS sales are 45% for the first nine months of 2005

FY 2004

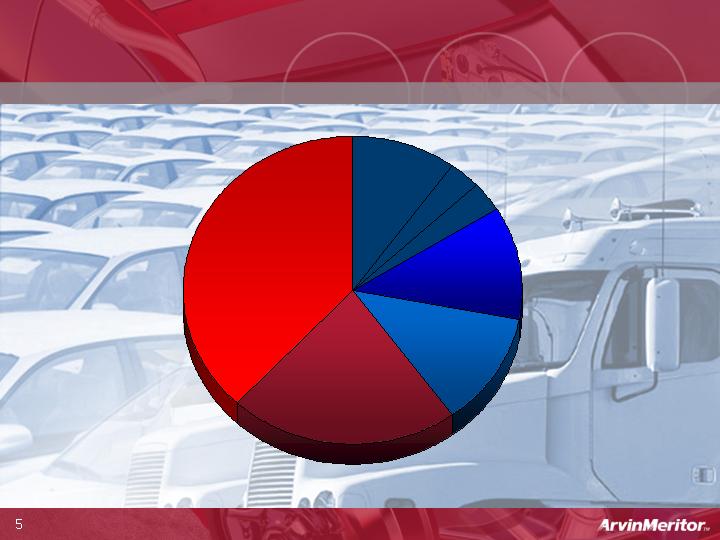

4

FY 2004

N.A. OEM Truck

& Trailer Sales

16%

Europe &

ROW

OE Sales

12%

CV Aftermarket

&

Specialty OEMs

12%

N.A. Big 3

LVS OEM

Sales

20%

Other LVS

OEM Sales

40%

Diversified Global Company

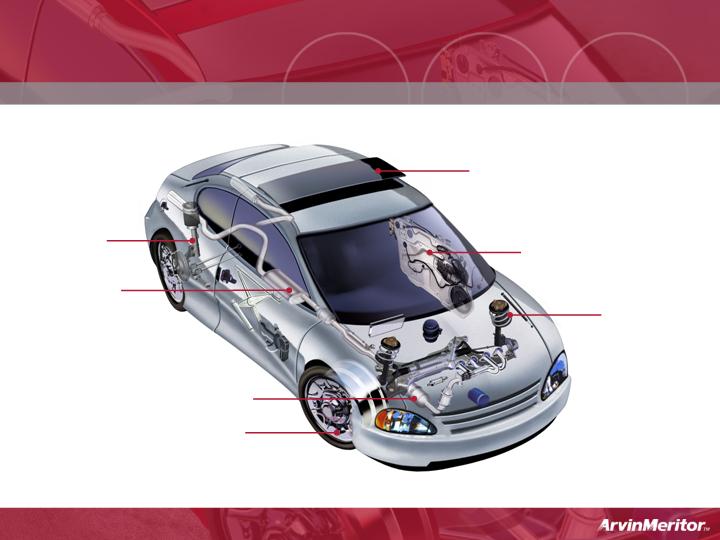

Light Vehicle Systems

Product Portfolio

Roof systems and modules

Door systems

and modules

Suspension

components

(coil

springs,

stabilizer

and torsion

bars)

Steel wheels

Emission systems

Suspension

modules

Exhaust

systems

6

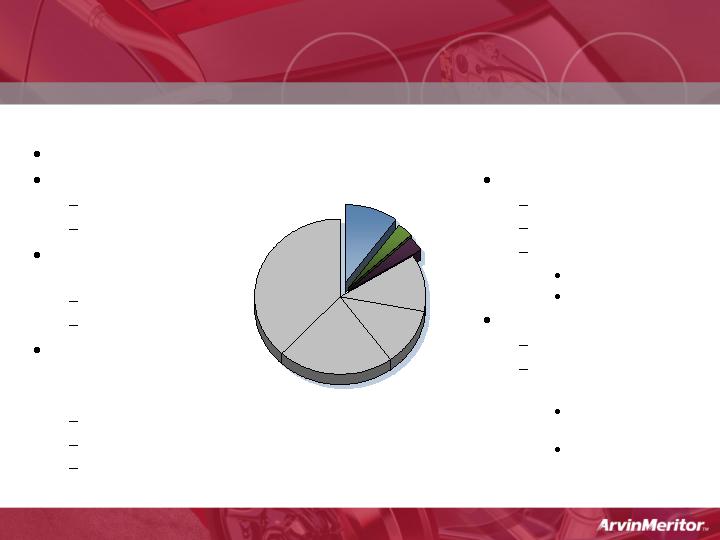

Light Vehicle Systems

Strengths

Diversified

N.A. Big 3 only 20%

of total sales

Diverse product

portfolio

LVS emissions

technology being used

in heavy truck

solutions

Issues

Low operating margins

Steel

Excess capacity

Focus of product lines

3 Rs Actions

Restructure

Eliminate excess

capacity

Refocus

Evaluate portfolio

Regenerate

Grow profitable

business product

lines

Timetable

Restructure

Refocus

Regenerate

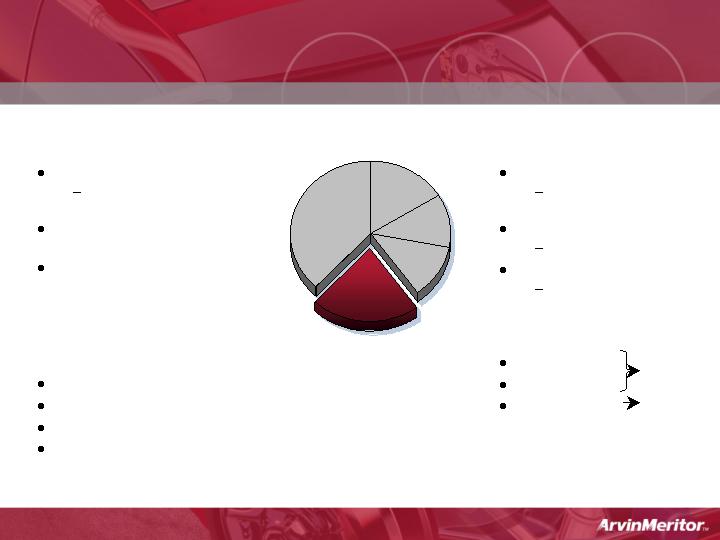

N.A. Big Three

LVS OEM Sales

20%

FY05/06

FY06/07

7

Restructuring Actions

Summary of Plan

400-500 global salaried employees

Close 11 facilities largely in LVS

1,850 additional employees

Integration and consolidation of

other facilities

Benefits

Take out excess capacity

Improve fixed cost

Improve operational efficiencies

Improve manufacturing footprint

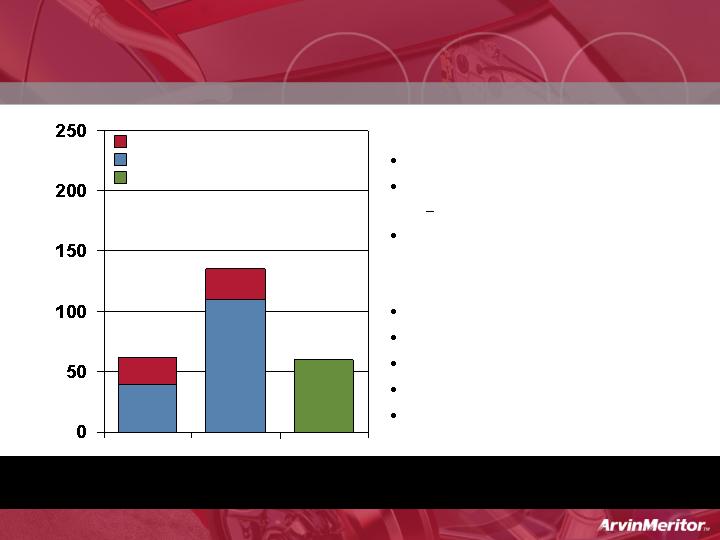

Full Year savings expected in 2007

$24

$25

Non-Cash Costs

Cash Costs

Annual Savings

$44

$68

$110

$135

($ in millions)

Savings

Costs

Q2 & Q3

Charges

$50 - $60

Remainder of Charges – Approximately $67M –

to be recorded in the Next 12 - 15 Months

8

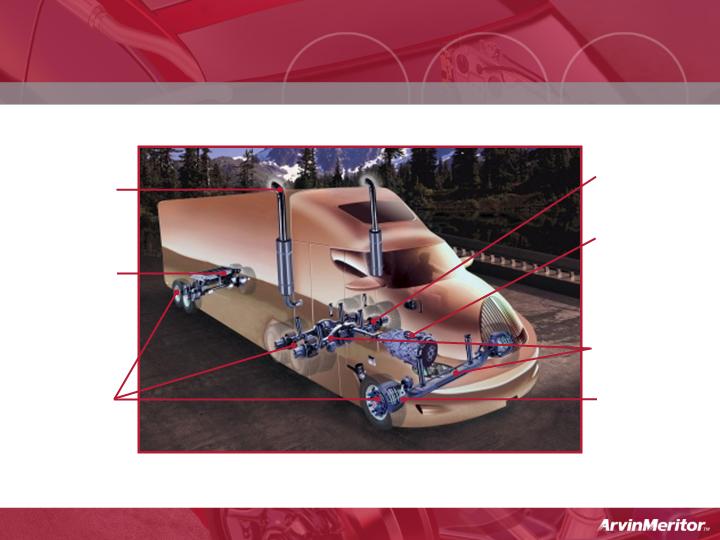

ABS, air

system and

stability

controls

Emissions

systems

Complete

Braking

systems

(wheel ends

and brakes)

Drivelines

Automated

transmissions

/clutch

Front and

rear axles

Commercial Vehicle Systems

Product Portfolio

Trailer and

suspension

systems

9

Heavy Truck Systems

Strengths:

Focused portfolio

Diversified

Customer

Geography

Strengths in “hot”

areas

Emissions

Safety

Strong global

markets

3rd Quarter, 2005

30% growth

Operating margins

6.5% (before special

items)

Issues/Opportunities:

Steel

Moderating prices

Supply good

Opportunities

Supply source

Product Design

2007 N.A. Downturn

Not as severe

ARM better

positioned

10% N.A. heavy

truck

Strong emissions

solutions

Class 8

10%

Class 5-7

3%

Trailers

3%

N.A. OEM Truck

& Trailer Sales

16%

10

Steel Impact

Basic steel costs moderating

Specialty steels still generating headwind

$20 million net impact in Q3, 2005

$100 million full year net impact

11

2007 Heavy Truck Downturn

Not as severe as 2001 downturn (30-35% vs. 50%)

Diversified customer base

Volvo JV

Hino

Diversified product portfolio

Commercial Vehicle Emissions

Aftermarket

Diversified globally

Asia

Europe

Well Positioned to Maintain Strong Performance

N.A. Class 8 Sales

10% of Company

12

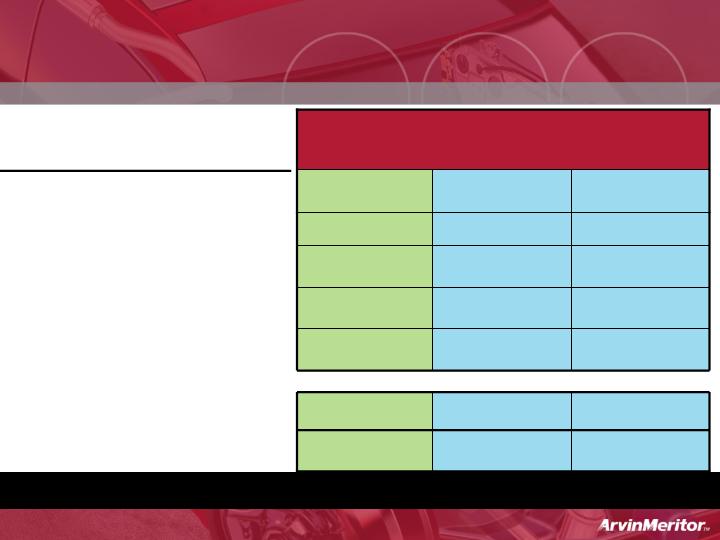

Third-Quarter Results (Before Special Items)

80 bps

5.7%

6.5%

$ 0.09

$ 0.61

$ 0.70

$ 3

$ 48

$ 51

(80)bps

2.7%

1.9%

$ 6

$ 42

$ 48

$ 14

$ 82

$ 96

$ 312

$ 2,099

$ 2,411

Increase/

(Decrease)

Third-Quarter

FY 2005 FY 2004

Continuing Operations (LVS, CVS)

Sales

Operating Income

Income

Diluted EPS

Free Cash Flow

Operating Margin

CVS

LVS

Met High End of Guidance

13

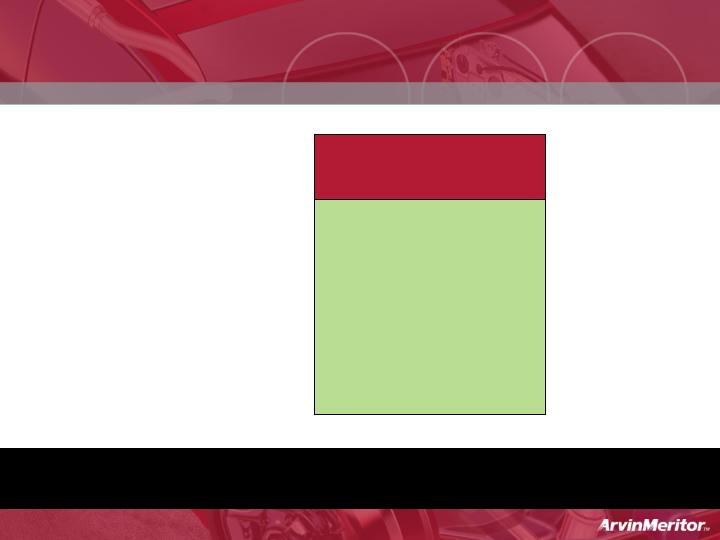

Full-Year FY 2005 Outlook

(In millions, except EPS)

$ 1.40

$ 97

2.5%

$ 8,750

Full Year

FY 2005

-

-

-

-

$ 1.60

$ 110

2.8%

$ 8,825

Diluted EPS

Income

Operating Margin

Sales

Continuing Operations (Before Special Items)

Focused on Achieving Full-Year Results at the Top End

of Earnings Range

14

2006 Outlook

Continued Strong Truck Markets Globally

Restructuring Gains Traction

Moderating Steel

Earnings Headwind from Pensions

Stronger Cash Flow

14

Appendix

1

Use of Non-GAAP Financial Information

In addition to the results reported in accordance with accounting principles generally accepted in the

United States (“GAAP”) included throughout this presentation, the Company has provided information

regarding income from continuing operations, diluted earnings per share and segment operating income

and margins before special items which are non-GAAP financial measures. These non-GAAP measures

are defined as reported income or loss from continuing operations, reported diluted earnings or loss per

share and segment operating income plus or minus special items.

Management believes that the non-GAAP financial measures used in this presentation are useful to both

management and investors in their analysis of the Company’s results of operations. In particular,

management believes that income from continuing operations, diluted earnings per share and segment

operating income and margins before special items is a better summary of the company’s results of

operations. Further, management uses these non-GAAP measures for planning and forecasting in future

periods.

These non-GAAP measures should not be considered a substitute for the reported results prepared in

accordance with GAAP. These non-GAAP financial measures, as determined and presented by the

Company, may not be comparable to related or similarly titled measures reported by other companies.

Set forth on the following slide is a reconciliation of these non-GAAP financial measures to the most

directly comparable financial measures calculated and presented in accordance with GAAP.

2

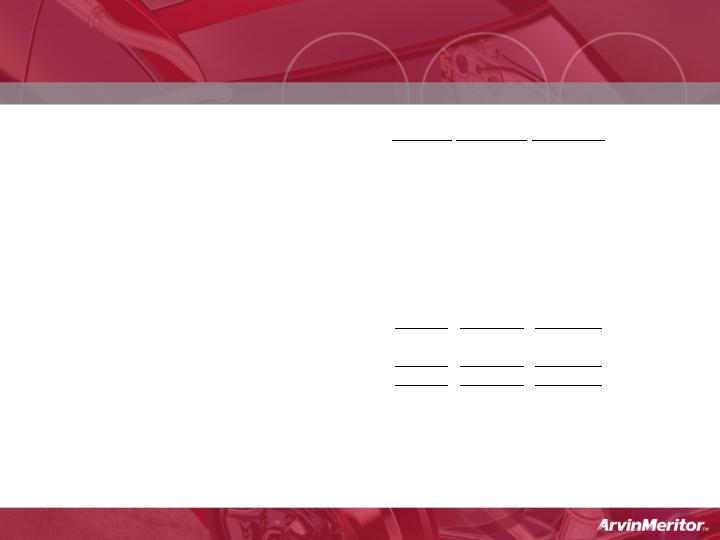

Reconciliation of GAAP Financial Information to

3rd Qtr FY 05 Results before Special Items

Q3 FY 05

Reported

Restructuring

Q3 FY05

Adjusted

Sales

2,411

$

-

$

2,411

$

Gross Margin

201

-

201

Operating Income

90

6

96

Income from Continuing Operations

44

4

48

Diluted Earnings Per Share - Continuing Operations

0.64

$

0.06

$

0.70

$

Guidance

$0.60 - $0.70

Segment Operating Income

LVS Operating Income

20

$

5

$

25

$

CVS Operating Income

72

1

73

Segment Operating Income

92

6

98

Unallocated Corporate Costs

(2)

-

(2)

Total Operating Income

90

$

6

$

96

$

Operating Margins

LVS

1.5%

1.9%

CVS

6.4%

6.5%

Segment Operating Margins

3.8%

4.1%

Total Operating Margins

3.7%

4.0%

3