Bank of America

35th Annual

Investment Conference

Sept. 22, 2005

Charles “Chip” McClure

Chairman, CEO and President

Rakesh Sachdev

Senior Vice President, Corporate Strategy

Brian Casey

Vice President and Treasurer

Cautionary Statement Concerning

Forward-Looking Statement

This presentation contains “forward-looking statements” as defined in the Private

Securities Litigation Reform Act of 1995. These forward-looking statements are based

on currently available competitive, financial and economic data and management’s

views and assumptions regarding future events. Such forward-looking statements are

inherently uncertain, and actual results may differ materially from those projected as

a result of certain risks and uncertainties, including but not limited to global economic

and market conditions; the demand for commercial, specialty and light vehicles for

which the company supplies products; risks inherent in operating abroad, including

foreign currency exchange rates and potential disruption of production and supply

due to terrorist attacks or acts of aggression; availability and cost of raw materials,

including steel; OEM program delays; demand for and market acceptance of new and

existing products; reliance on major OEM customers; labor relations of the company,

its customers and suppliers; the financial condition of the company’s suppliers and

customers, including potential bankruptcies; successful integration of acquired or

merged businesses; achievement of the expected annual savings and synergies from

past and future business combinations; success and timing of potential divestitures;

potential impairment of long-lived assets, including goodwill; competitive product and

pricing pressures; the amount of the company’s debt; the ability of the company to

access capital markets; the credit ratings of the company’s debt; the outcome of

existing and any future legal proceedings, including any litigation with respect to

environmental or asbestos-related matters; as well as other risks and uncertainties,

including but not limited to those detailed herein and from time to time in

ArvinMeritor’s Securities and Exchange Commission filings.

2

Agenda

Company profile

Light Vehicle Systems

Reshaping the business

Commercial Vehicle Systems

Capitalizing on strengths

Emissions

Diesel emissions opportunities

Summary

3

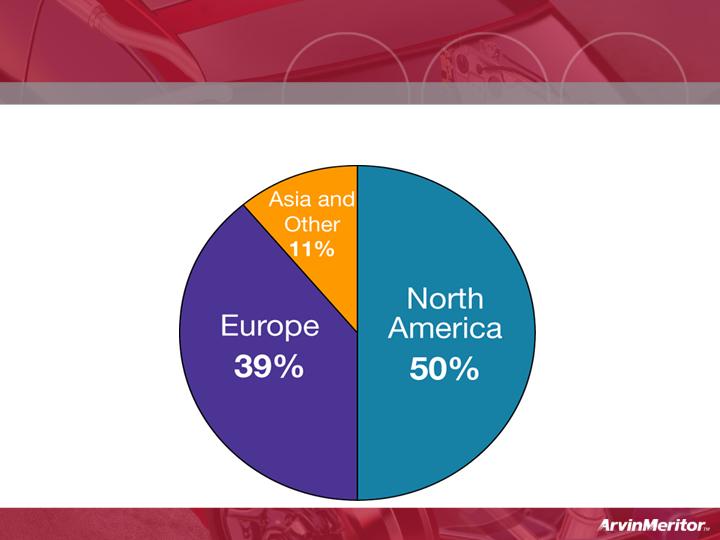

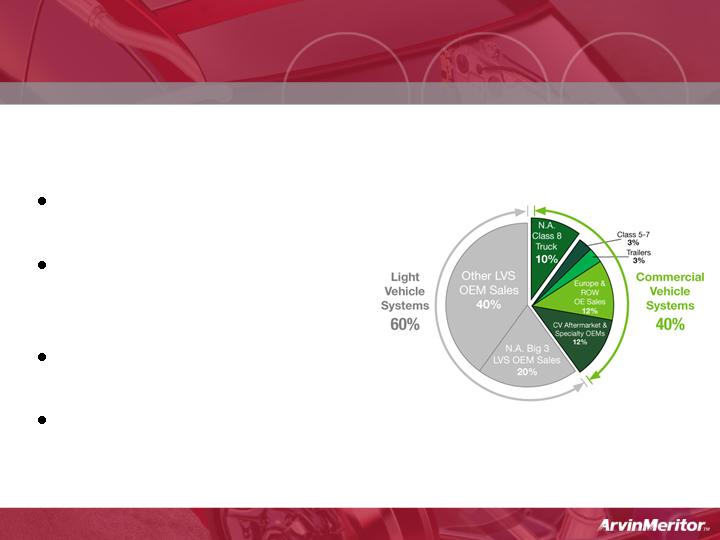

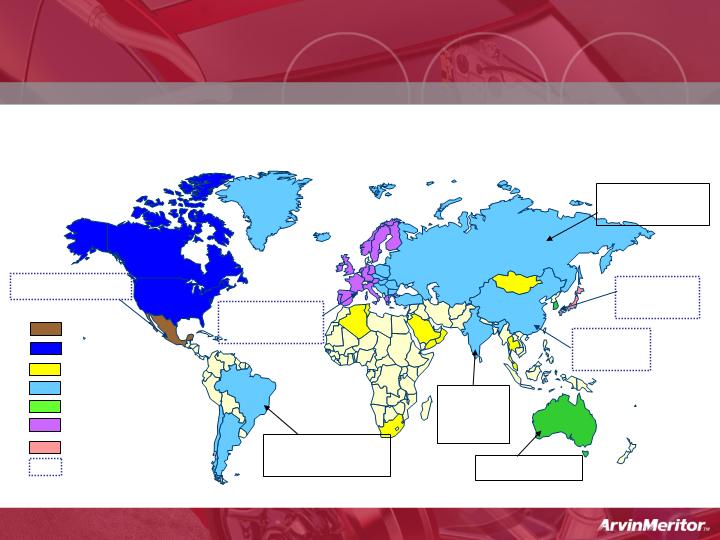

Company Profile

Global Diversification

FY 2004

4

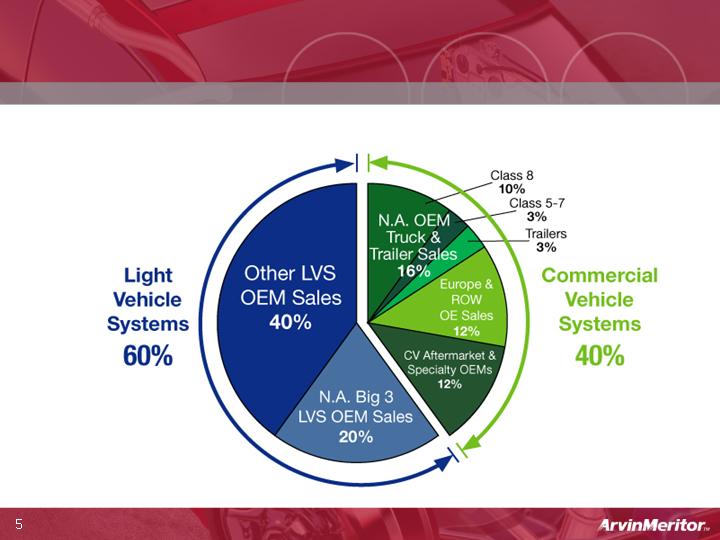

Company Profile

Note: LVS sales were 55% and CVS sales were 45% for the first nine months of 2005

Business Segment Diversification

FY 2004

5

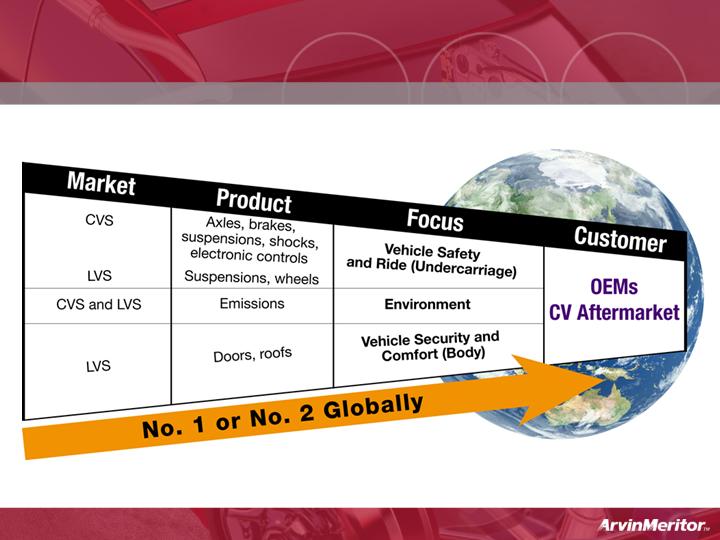

Company Profile

Market and Product Focus

6

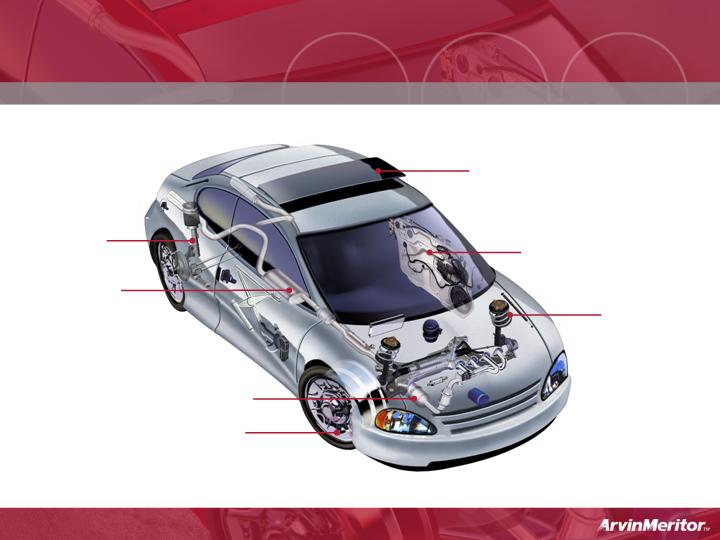

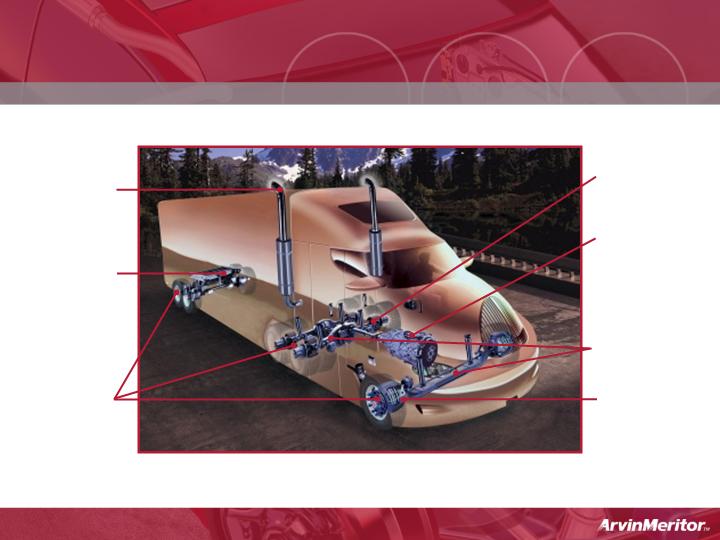

Light Vehicle Systems

Roof systems and modules

Door systems

and modules

Suspension

components

(coil

springs,

stabilizer

and torsion

bars)

Steel wheels

Emissions systems

Suspension

modules

Exhaust

systems

7

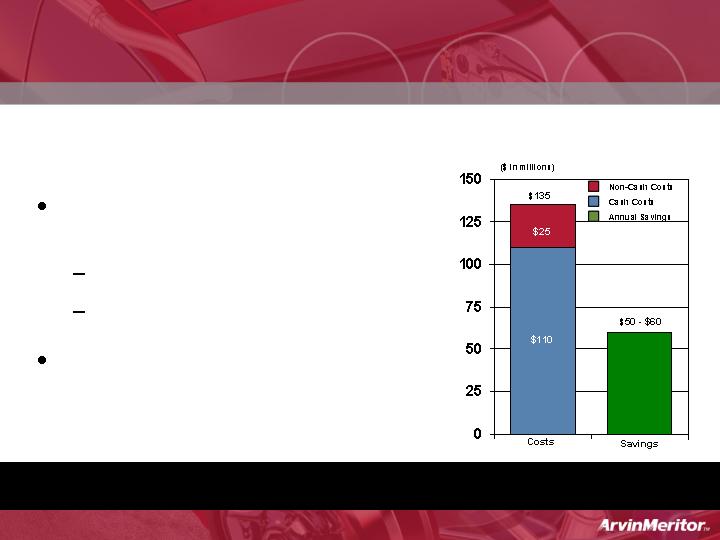

Restructuring Program

Reshaping the LVS Business

Step 1: Reducing Capacity

Closing and consolidating

11 ArvinMeritor locations

Nine in LVS business

$135 million total program cost

$50-60 million annual savings for

ArvinMeritor expected by 2007

$50-60 Million Annual Benefit

8

Reshaping the LVS Business

Step 2: Sourcing Globally

Expecting new sources to

generate savings in

immediate future

VP of LVS Purchasing

relocated to China

Building local staff to

achieve aggressive goals

Moving Rapidly to Reduce Supply Costs

9

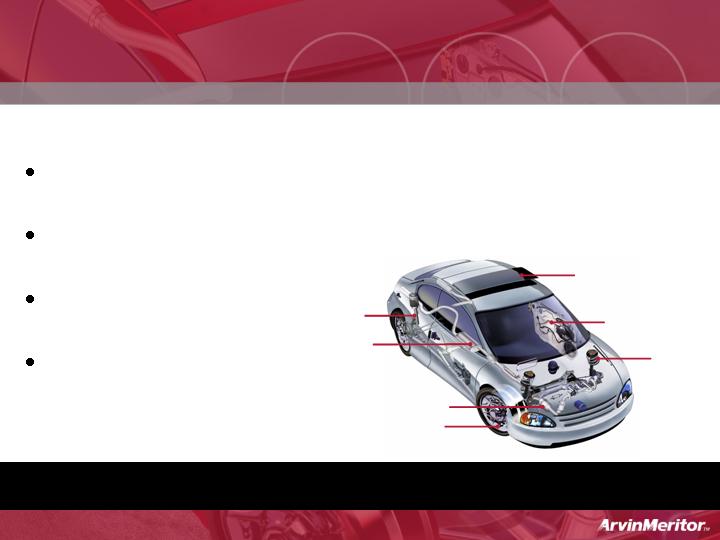

Reshaping the LVS Business

Committed to Improving Profitability

Roof systems and modules

Door systems

and modules

Suspension

components

(coil

springs,

stabilizer

and torsion

bars)

Steel wheels

Emissions systems

Suspension

modules

Exhaust

systems

Step 3: Evaluating Product Portfolio

Reducing capacity/sourcing globally

not enough for some products

Divestitures of non-core products

under consideration

Market valuations have

become pacing factor

Continue steps to capture

value throughout

evaluation process

10

Reshaping the LVS Business

Step 4: Growing Non-North America Big 3 Business

Relatively low N.A. Big 3 exposure

20 percent of total

ArvinMeritor business

Continue efforts to diversify

Established Korean

emissions joint venture

Awarded European

multi-panel sunroof contract

Began door module production

for Hyundai N.A.

Continuing to Diversify Customer Base

FY 2004

11

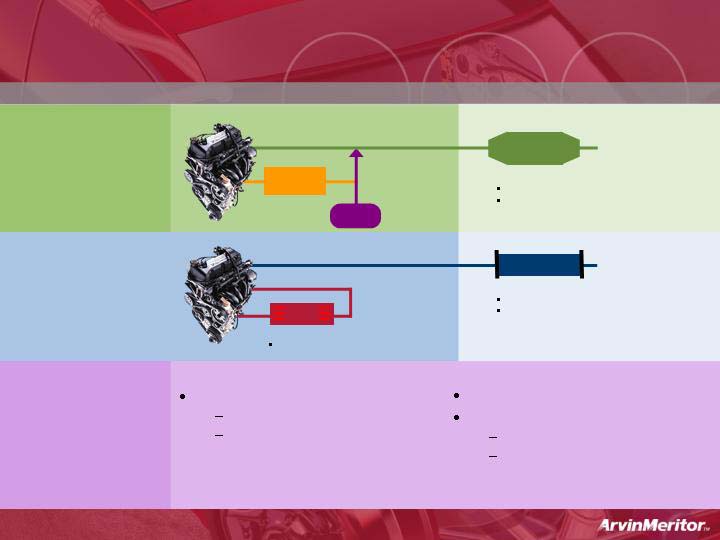

ABS, air

system and

stability

controls

Emissions

systems

Complete

Braking

systems

(wheel ends

and brakes)

Drivelines

Automated

transmissions

Front and

rear axles

Commercial Vehicle Systems

Trailer and

suspension

systems

12

Capitalizing on Strengths

Commercial Vehicle Markets are Strong Globally

Significant volume increases in North America, Europe,

South America and China (2005 vs. 2004)

+30%

+12%

+16%

+11%

13

Capitalizing on Strengths

Well-Positioned to Capture Growth

Firmly entrenched in global markets

European Volvo joint venture

First Auto Works (FAW) joint venture in China

Dynamic product portfolio in “hot” growth areas

Safety/Undercarriage

Aftermarket

Emissions

14

Capitalizing on Strengths

2007 N.A. Truck Market Cyclicality

Being Well-Managed

Only impacts 10 percent of

total ArvinMeritor business

N.A. downturn not expected

to be as severe

(30-35% vs. 50%)

Global markets expected to

remain strong in 2007

Emissions and Aftermarket

provide meaningful offset to

potential N.A. market decline

FY 2004

15

Capitalizing on Strengths

Opportunities Are Being Realized

Commercial Vehicle Aftermarket

Opportunity for global expansion

Partially offsets N.A. market decline

Commercial Vehicle Emissions

Delivering solutions to meet global emissions

requirements

Marketing new products

Capturing new business

Developing advanced technology for future solutions

16

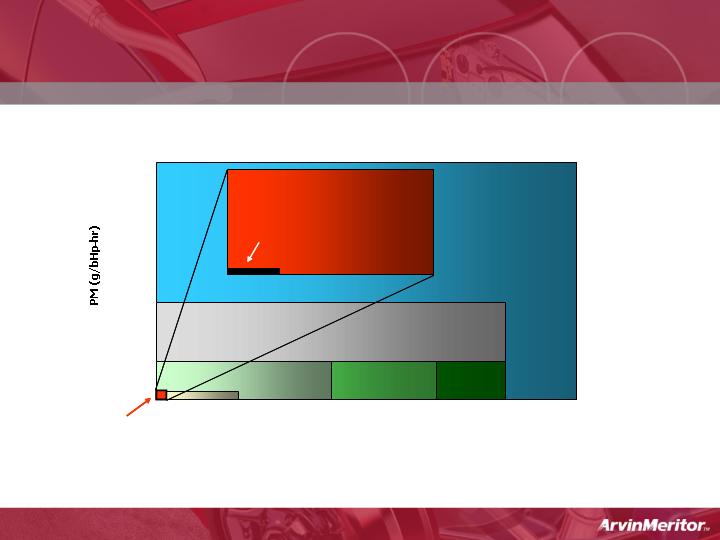

Diesel Emissions Opportunities

NOx (g/bHp

-

hr)

2010

(PM = 0.01, NOx = 0.2)

1988

1991

1994

1998

2002

0

1

4

3

2

5

6

0.1

0.2

0.3

0.4

0.5

0.6

0

1

4

3

2

5

6

0.1

0.2

0.3

0.4

0.5

0.6

NOx (g/bHp

-

hr)

2010

1988

1991

1994

1998

2002

2010

2014

0

0.05

0.2

0.1

0.002

0.004

0.006

0.008

0.01

0.15

2010

2014

(PM = 0.001, NOx = 0.05)

Sources: EPA and DieselNet

U.S. Diesel Emissions Standards

17

Diesel Emissions Opportunities

EPA ’98

EPA ’04

Euro IV

Euro III

Euro II

Euro I

Japan ‘05

Projected

Euro

III=

2010

Euro IV= 2006

Euro IV=

2010

Euro III= 2006

Euro IV= 2009

Euro III= 2007

Euro IV=2010

Euro IV=

20??

EPA ‘04= 2007

Euro V= 2008

Euro VI=2011

Global Emissions Standards are Driving

Significant Growth Opportunities for ArvinMeritor

18

Diesel Emissions Solutions

U.S. may adopt SCR solution

Improves fuel efficiency

Low sulfur diesel capacity

constraint

Lean NOx Traps

Combined PM and NOx Traps

SCRT (SCR+DPF)

Lean NOx Trap with Plasma

Fuel Reformer

2007

U.S.

Solution

2006

Europe

Solution

EGR

Exhaust Gas Recirculation (EGR)

Reduces NOx

DPF

Diesel Particulate Filter (DPF)

Reduces PM

Vocational application uses

actively regenerated filter

SCR

Urea

Control

Selective Catalytic Reduction (SCR)

Reduces NOx

Reduces PM

Beyond

2007

19

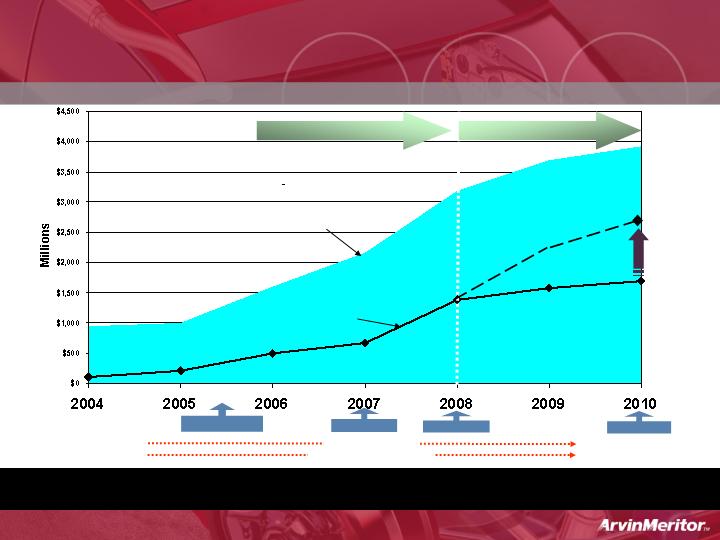

Commercial Vehicle Diesel Emissions

Global Addressable Market

$660/truck

$2,700/truck

Euro 4 / Japan

EPA 2007

Euro 5

EPA 2010

- EU: mostly SCR

US: EGR+DPF

Technology TBD

Current Tech. Prevails

(EGR + DPF)

New Tech. Required

(SCR & Active DPF)

Technology Defined

Global Market $2+ billion in 2007

ARM Addressable Market

Addressable Market Grows to $2-3 Billion in 2010

Global Solutions

ArvinMeritor Solutions

$2,000/truck

$300-360 /truck

20

Summary

Reshaping the Light Vehicle Systems business

Capitalizing on global strengths of

Commercial Vehicle Systems

Well-positioned to capture growing diesel

emissions opportunities

Light Vehicle Aftermarket divestiture progressing

21

www.arvinmeritor.com

22