Analyst Day 2005

1

Forward-Looking Statement

This presentation contains statements relating to future results of the company (including certain

projections and business trends) that are “forward-looking statements” as defined in the Private

Securities Litigation Reform Act of 1995. Forward-looking statements are typically identified by

words or phrases such as “believe,” “expect,” “anticipate,” “estimate,” “should,” “are likely to be,”

“will,” and similar expressions. Actual results may differ materially from those projected as a

result of certain risks and uncertainties, including, but not limited to, global economic and market

conditions; the demand for commercial, specialty and light vehicles for which the company

supplies products; risks inherent in operating abroad (including foreign currency exchange rates

and potential disruption of production and supply due to terrorist attacks or acts of aggression);

availability and cost of raw materials, including steel; OEM program delays; demand for and

market acceptance of new and existing products; successful development of new products;

reliance on major OEM customers; labor relations of the company, its customers and suppliers;

including potential disruptions in supply of parts to our facilities or demand for our products due

to work stoppages; the financial condition of the company’s suppliers and customers, including

potential bankruptcies; successful integration of acquired or merged businesses; the ability to

achieve the expected annual savings and synergies from past and future business combinations;

success and timing of potential divestitures; potential impairment of long-lived assets, including

goodwill; competitive product and pricing pressures; the amount of the company’s debt; the

ability of the company to access capital markets; credit ratings of the company’s debt; the

outcome of existing and any future legal proceedings, including any litigation with respect to

environmental or asbestos-related matters; as well as other risks and uncertainties, including, but

not limited to, those detailed from time to time in the filings of the company with the Securities

and Exchange Commission.

2

Chip McClure

Chairman, CEO and President

Dec. 8, 2005

3

2005 Year in Review

Steel/steel/steel

Tough actions taken

Solved supply issues

Moderating for 2006

Industry turmoil in Light Vehicle Systems (LVS)

Operational improvements

Restructuring (LVS/CVS/Corporate)

On budget and on-track

Divestitures

Completed Roll Coater/17th St.

Achieved $200M in proceeds

Light Vehicle Aftermarket in progress

Met guidance

Delivered results in tough times

4

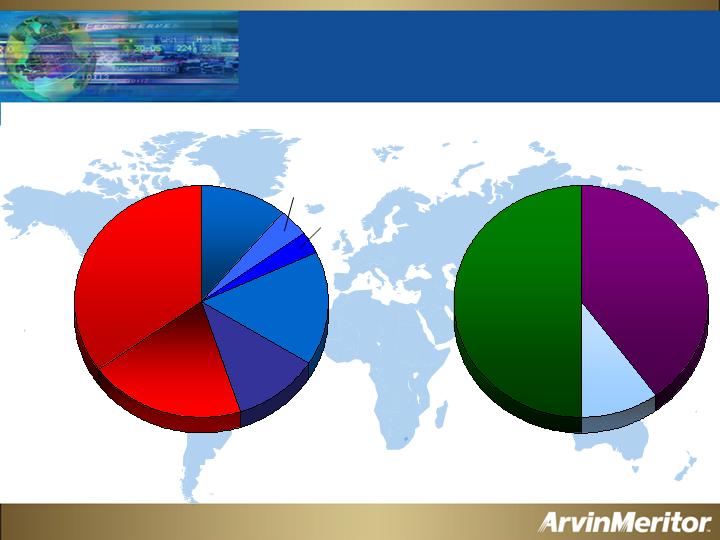

Global Business Diversity

Light

Vehicle

Systems

55%

Commercial

Vehicle

Systems

45%

North

America

50%

Europe

40%

Rest of

World

10%

Other LVS

OEM Sales

35%

N.A. Big 3

LVS OEM

Sales

20%

N.A.

Class 8

Truck

11%

CV

Aftermarket

& Specialty

OEMs

11%

Europe and

ROW OE

Sales

16%

Class 5-7

4%

Trailers

3%

5

Light Vehicle Systems

Business strategy is

being paced by

market factors

Creating value in

tough environment,

whether we

ultimately hold or sell

Continue to

capitalize on

emissions

technologies

6

Commercial Vehicle Systems

Business focused on

making 2007 a

non-event

Capitalizing on

business strengths,

including emissions

technology

solutions

Growing

aftermarket

business globally

7

Financial Review

Detailed FY06

outlook

Pension

including FY06

EPS impact

Review

financial

health

8

Business Strategy

Redefining our strategic

intent

Drive results to achieve

13-15 percent Return on

Invested Capital (ROIC)

9

Key Points

Strong leadership team

Taking the right actions today

Focused on making 2007

a non-event

Financially healthy

Driving to 13-15 percent ROIC

10

Light Vehicle Systems

Juan De La Riva

President

11

Automotive Product Range

Steel wheels

Suspension

components

Emissions controls

Door systems

and modules

Suspension

modules

Roof systems and modules

Exhaust

systems

12

LVS Geographic Footprint

North America

44%

Asia/Pacific

and Other

9%

Europe

47%

Fiscal Year 2005 Sales of $4.8 Billion

13

Limited LVS Exposure

to GM and Ford in North America

5%

10%

$3.5B

Value-Added

Sales*

* Total LVS, FY05

14

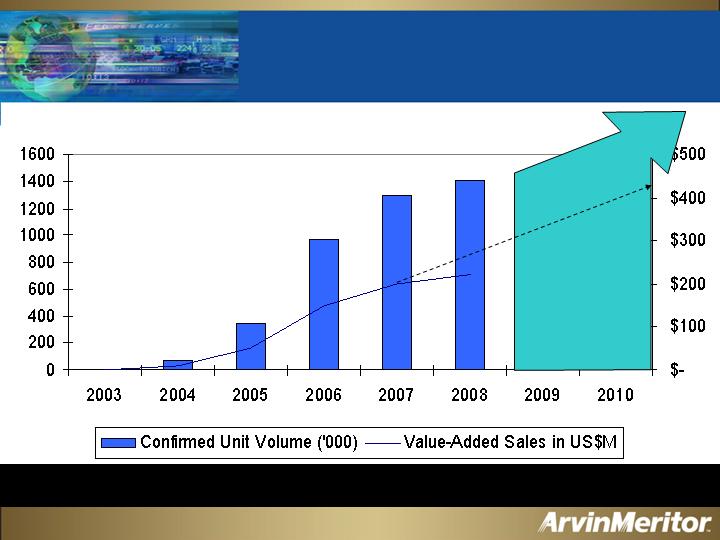

LVS Sales

17.0

17.0

16.4

16.4

European Volumes*

16.5

16.0

15.6

15.6

N. American Volumes*

$5.0

$1.5

$3.5

FY08

$4.6

$4.6

$4.8

TOTAL Sales

$1.4

$1.4

$1.3

Pass-Through

Sales

$3.2

$3.2

$3.5

Value-Added Sales

FY07

FY06

FY05

in billions

*Company estimates

15

LVS Margins

3.3%

2.0%

1.3%

0.8%

TOTAL Margin

4.7%

FY08

2.9%

1.9%

1.1%

Value-Added

Margin

FY07

FY06

FY05

(Before special items)

16

LVS Margin Improvements

17

LVS Restructuring Program

Annual run rate of ~$35M savings

beginning in 2007

May 2005 restructuring program

Downsize

16 percent salaried positions

8 percent hourly positions

Close

9 of 11 recently announced facility

closings in LVS

Divest

17th Street, Columbus, Ind., U.S.

18

Seize Procurement Opportunities

Substantial cost reductions of

raw materials and components

available

Localize supply base in

Asia/Pacific

Must have strong supplier

development in place

Strong support from

Engineering groups essential

LVS Procurement leadership

residing in Shanghai

Moving Rapidly to Reduce Supply Costs

19

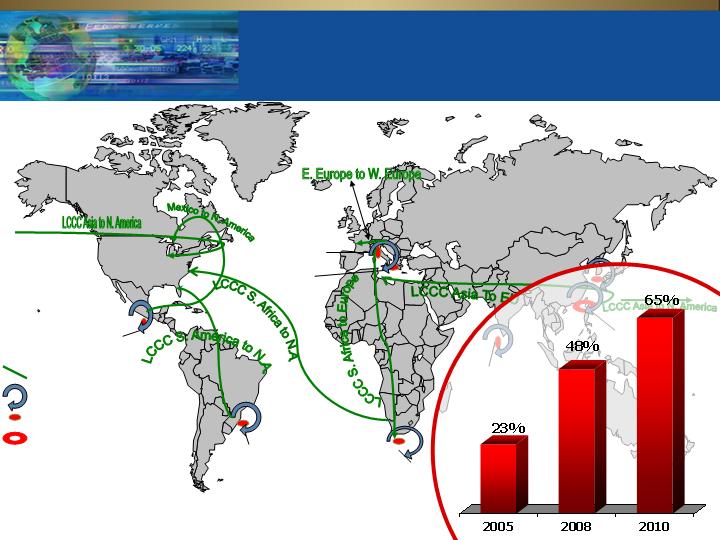

Leading Cost Competitive Country (LCCC)

Supplier Development and Management

Queretaro, Mexico

Limeira, SP Brazil

Cape Town, South Africa

Istanbul, Turkey

Liberec, Czech Republic

Bangalore, India

Shanghai, China

Asia Procurement

Headquarters

Seoul, Korea

LCCC Mexico

LCCC Brazil

LCCC South Africa

LCCC Asia

Global Purchasing Offices

Asia Procurement

Headquarters

LCCC To LCC Spend

LCCC To HCC Spend

Legend

Comprehensive Strategy to Double LCCC Spend by 2008

Leading Competitive Cost Country Sourcing Drives

Global Resource Planning

20

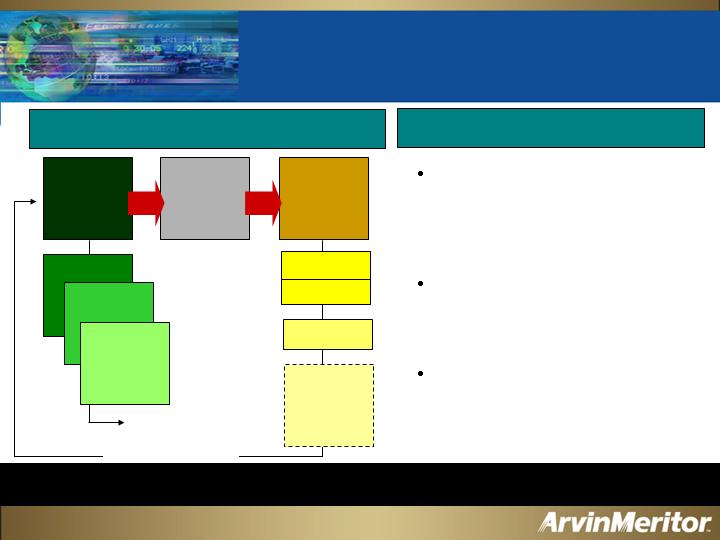

Low-Cost Producer Strategy

MOS

Metrics

Gap

Analysis

Continuous

Improvement

Global

Regional

Plant

PORs & QBRs

EI Teams

White Shirt

AMPS Tools

Plant Level

Line of Sight

to P&L

Impact

Overall Concept

Main Enablers

MOS metrics drive in-plant gap

analysis to identify Continuous

Improvement projects impacting

Performance Operating Profit

(POP) and ROIC

Robust ArvinMeritor Performance

System (AMPS) tools for driving

improvement and sharing

solutions

White Shirt culture engages

employees in self-directed

Employee Involvement teams that

focus on bottom-line results

Continuous Improvement – AMPS Tools – White Shirt Philosophy

Reset Benchmarks

21

Focus on Asia/Pacific Customers

Emissions Technologies (Korea)

Diesel Particulate Filters (DPFs)

Door Systems (Korea and India)

Door modules and components

Wheels (India and China)

Suspension Components (China)

Asia/Pacific Joint Venture Initiatives

Asia Pacific includes: Australia, China, India, Japan, Korea and Thailand

LVS Asia/Pacific Sales

22

Evaluating Product Portfolio

Reducing capacity/sourcing globally

not enough for some products

Divestures of non-core products/

processes under consideration

Market valuations have become

pacing factor

Continue steps to capture value

throughout evaluation process

23

LVS Emissions Technologies

Michael Bleidt

General Manager and Vice President

24

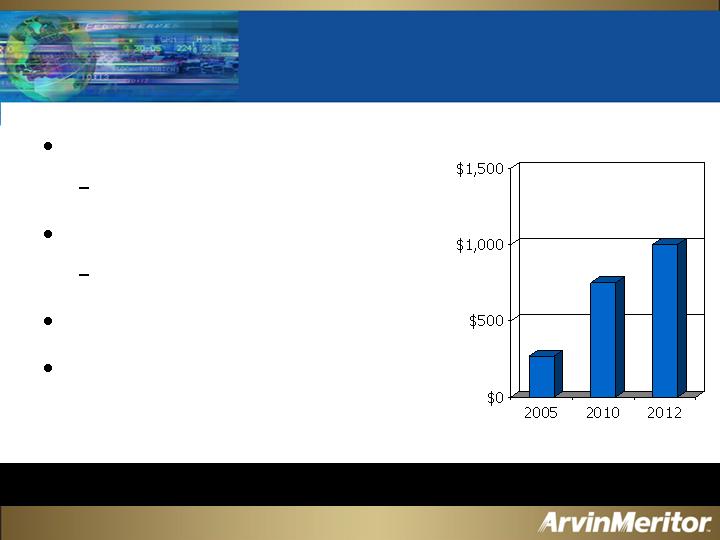

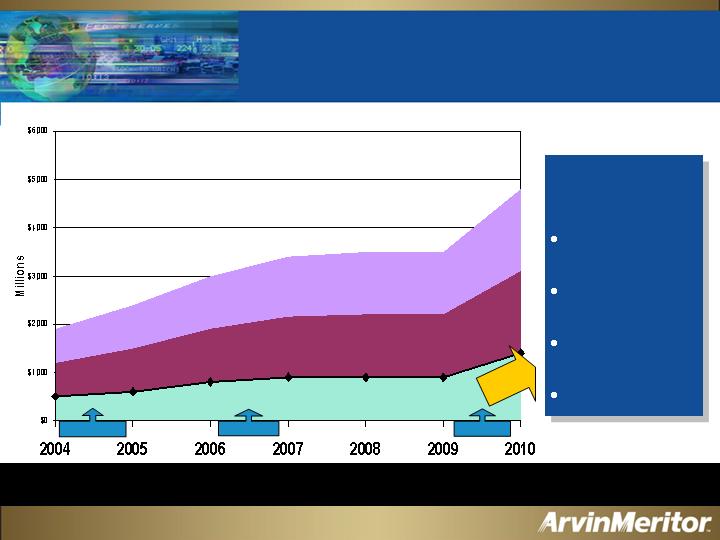

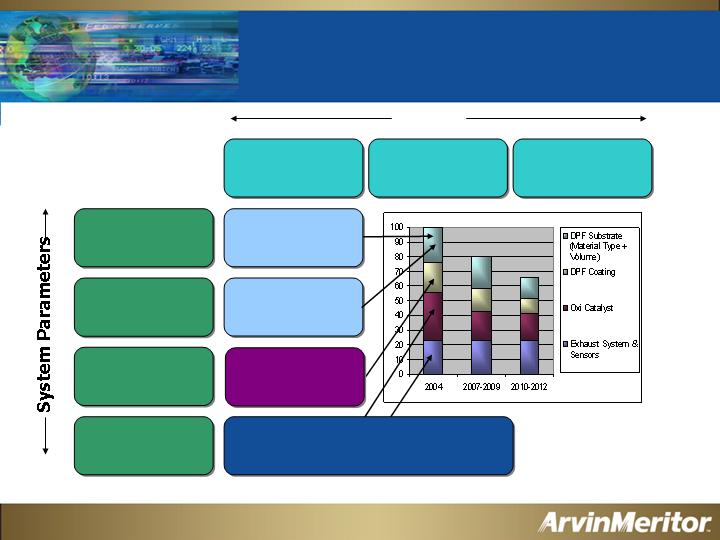

Light Vehicle Diesel After-Treatment

Global Addressable Market

Addressable Market Grows Beyond $1 Billion

Euro 4 / Japan

EPA 2007

Euro 5

Catalyzed Coatings

Ceramic Internals

ARM Value-Added Addressable Market

ArvinMeritor

Expertise

Systems design

and integration

Thermal fluid

management

Systems

optimization

Canning

25

Positioned for

Market Share Leadership

Generation 1

2003-04

Generation 2

2005-07

Generation 3

2008-09

Generation 4

2010+

Leading Product Innovation

33%+

Next

Technology Leap

Lean NOx Traps, SCR/DPF Combinations and DPNR

First

Widespread

Use

Catalyzed DPF without Additive

25%

20%

Maturing Volumes

– Emphasis

on Cost

Affordable, More Efficient Regeneration Port Injection Technology

33%

20%

DPF with Additive

Early Adopters

0%

26

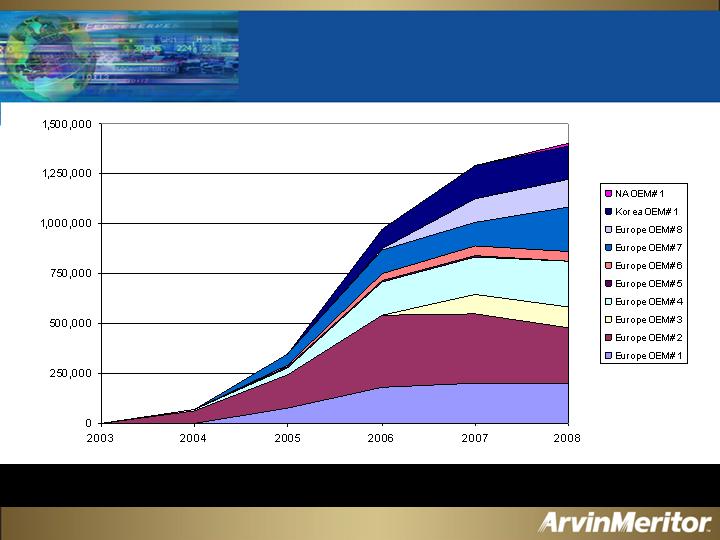

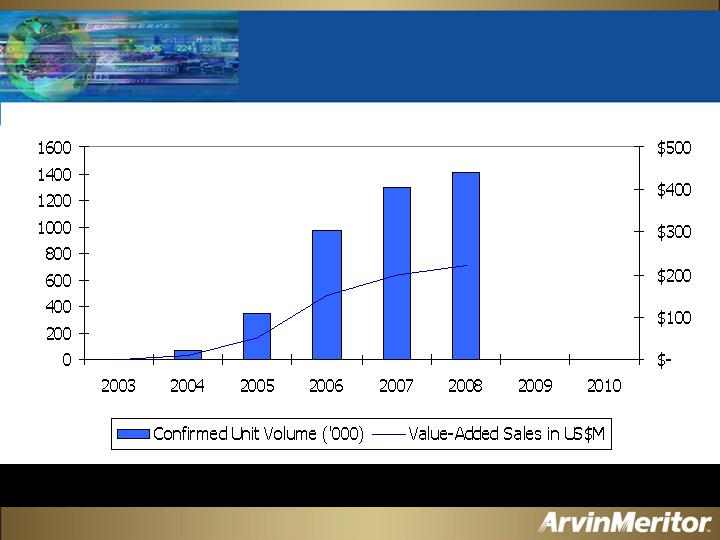

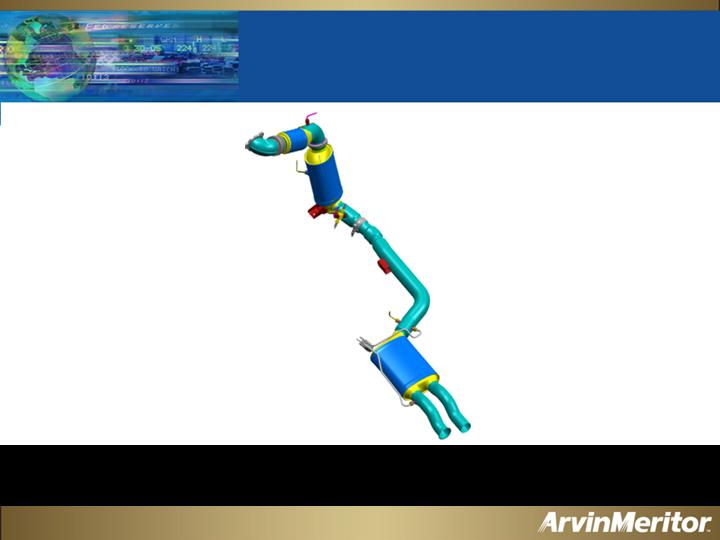

1.4 Million DPF Units Confirmed

DPF Production in Europe, Korea

and North America

27

Confirmed DPF Value-Added Sales

35 Percent Market Share of European DPFs

28

Positioned for

Market Share Leadership

Generation 1

2003-04

Generation 2

2005-07

Generation 3

2008-09

Generation 4

2010+

Leading Product Innovation

33%+

Next

Technology Leap

Lean NOx Traps, SCR/DPF Combinations and DPNR

First

Widespread

Use

Catalyzed DPF without Additive

25%

20%

Maturing Volumes

– Emphasis

on Cost

Affordable, More Efficient Regeneration Port Injection Technology

33%

20%

DPF with Additive

Early Adopters

0%

29

Diesel Market Western Europe

14.786

4.746

32,1%

0%

20

14.490

6.694

46,2%

5%

400

15.200

7.904

52,0%

38%

3.000

15.200

8.208

54,0%

100%

8.200

YEAR

Passenger Car-Market

(in 1.000 vehicles)

Passenger Car-Diesel

(in 1.000 vehicles)

Diesel-

Share

Share

Diesel Particulate

Filter

Passenger Car with

Particulate Filter

(in 1.000 vehicles)

2000

2004

2007

2010/12

EURO 4

EURO 5

* Source: Federal Environmental Agency

UBA Estimates of DPF Market

30

System Cost

Regeneration

Efficiency

Oil Dilution

Drivers

* Source: FGP, ATA Congress 09/04

Industry Desperate to Reduce

Diesel-Emissions Related Costs

DPF Volume

Exhaust System/

Layout

Filter Substrate

(Material)

DPF Coating

(Washcoat + PGM)

Reduce Size and Number of DOC;

Move to Close-Coupled DPF

Reduce DPF Size

Find New

Substrate Material

Reduce Platinum

Dependence

Customer’s technical objective

31

Focus ArvinMeritor

Expertise

and Technologies on

Reducing

System Costs

Light Vehicle

Diesel Emissions Strategy

32

Formula for Success

+

=

Vaporizer Enables 20 Percent Cost Reduction

Low-Cost

Diesel Regeneration

System

Proprietary

Port-Injection

Dosing

Technology

Proprietary

Predictive

Software

Core

Competencies

+

33

Positioned for

Market Share Leadership

Leading Product Innovation

Generation 1

2003-04

Generation 2

2005-07

Generation 3

2008-09

Generation 4

2010+

33%+

Next

Technology Leap

Lean NOx Traps, SCR/DPF Combinations and DPNR

First

Widespread

Use

Catalyzed DPF without Additive

25%

20%

Maturing Volumes

– Emphasis

on Cost

Affordable, More Efficient Regeneration Port Injection Technology

33%

20%

DPF with Additive

Early Adopters

0%

34

Generation Four in Development

UREA

Injection + diffuser

DPF

Light PGM loading

SOOT

Capacitor

SCR

Catalyst

Vaporizer

Proven Regeneration Experience

Positions ArvinMeritor as Emissions Leader

35

Strategy Propels Growth

Advanced Products Earning Higher Margins

36

Commercial Vehicle Systems

Tom Gosnell

President

37

Capitalizing on Strengths

Significant volume increases in North America, Europe,

South America and China

(2005 vs. 2004)

+30%

+12%

+16%

+11%

Commercial Vehicle Markets Are Strong Globally

38

Commercial Vehicle

Production Outlook

421

305

FY06

Heavy- and Medium-Duty

Trucks

(Western Europe)

Class 8 Trucks (North America)

Commercial Vehicle Production

(thousands of units)

-

(6%)

% Change

421

324

FY05

39

Capitalizing on Strengths

Well-positioned to capture growth

Firmly entrenched in global markets

European Volvo joint venture

First Auto Works (FAW) joint venture in China

Dynamic product portfolio in “hot” growth areas

Safety/Undercarriage

Aftermarket

Emissions

40

CVS Sales and Margins

6.0%

6.2%

5.2%

Operating Margin

$3.8

$4.0

$4.1

Sales

FY07

FY06

FY05

$ in billions

(Before special items)

41

2007 N.A. Truck Market Cyclicality

Being Well-Managed

Only impacts 11 percent of

total ArvinMeritor business

N.A. downturn not expected to

be as severe (30-35 percent vs.

50 percent)

Global markets expected to

remain strong in 2007

Emissions and aftermarket

growth provide meaningful

offset to potential North

America market decline

Operational improvements

continue in Trailer and

Specialty products

FY05

42

Commercial Vehicle Emissions

Pedro Ferro

Vice President and General Manager

43

Why ArvinMeritor…

TECHNOLOGIES

+

ASSETS

MARKET

POSITION

+

VEHICLE

DYNAMICS

STRINGENT

EMISSIONS

REGULATIONS

LIGHT VEHICLE SYSTEMS

EMISSIONS TECHNOLOGIES

COMMERCIAL

VEHICLE SYSTEMS

EURO 4 & 5, U.S. 2007 & 2010

JAPAN 2005

MAJOR

GROWTH

BUSINESS

Warton,

U.K.

Columbus,

Ind., U.S.

Troy, Mich., U.S.

44

Diesel Emissions Opportunities

NOx (g/bHp

-

hr)

2010

(PM = 0.01, NOx = 0.2)

1988

1991

1994

1998

2002

0

1

4

3

2

5

6

0.1

0.2

0.3

0.4

0.5

0.6

0

1

4

3

2

5

6

0.1

0.2

0.3

0.4

0.5

0.6

NOx (g/bHp

-

hr)

2010

1988

1991

1994

1998

2002

0

0.05

0.2

0.1

0.002

0.004

0.006

0.008

0.01

0.15

2010

2014

(PM = 0.001, NOx = 0.05)

0

0.05

0.2

0.1

0.002

0.004

0.006

0.008

0.01

0.15

2010

2014

Sources: EPA and DieselNet

U.S. Diesel Emissions Standards

45

Diesel Emissions Opportunities

EPA ’98

EPA ’04

Euro IV

Euro III

Euro II

Euro I

Japan ‘05

Projected

Euro

III=

2010

EPA ‘04= 2006

Euro IV=

2010

Euro III= 2006

Euro IV= 2009

Euro III= 2007

Euro IV=2010

Euro IV=

20??

EPA ‘04= 2007

Euro V= 2008

Euro VI=2011

Global Emissions Standards are Driving

Significant Growth Opportunities for ArvinMeritor

46

Diesel Emissions Solutions

U.S. may adopt SCR solution

Improves fuel efficiency

Low sulfur diesel capacity

constraint

Lean NOx Traps

Combined PM and NOx Traps

SCRT (SCR+DPF)

Lean NOx Trap with Plasma Fuel

Reformer

2007

U.S.

Solution

2006

Europe

Solution

EGR

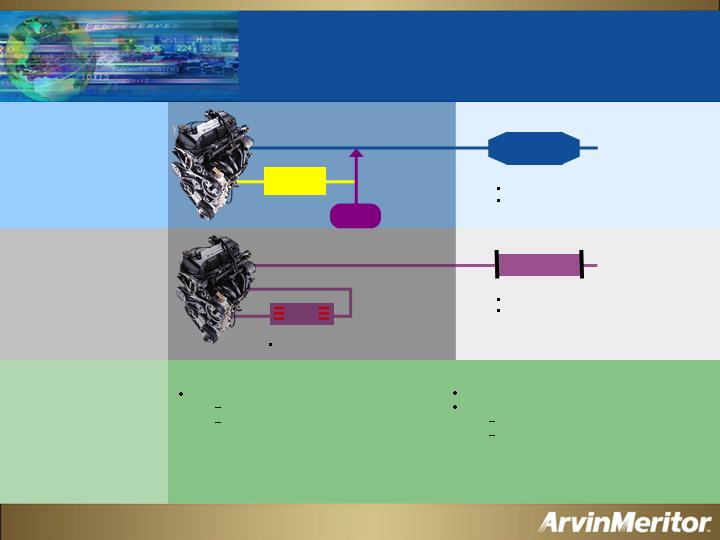

Exhaust Gas Recirculation (EGR)

Reduces NOx

DPF

Diesel Particulate Filter (DPF)

Reduces PM

Vocational application uses

actively regenerated filter

SCR

Urea

Control

Selective Catalytic Reduction (SCR)

Reduces NOx

Reduces PM

Beyond

2007

47

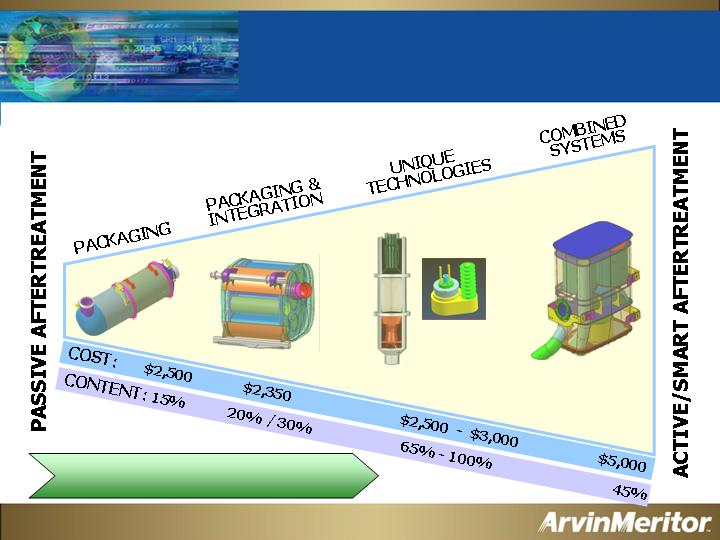

Increasing Value-Added Content

DPF

SCR

PFR

SCRT

LNT+DPF

TR

EMISSIONS REQUIREMENTS

48

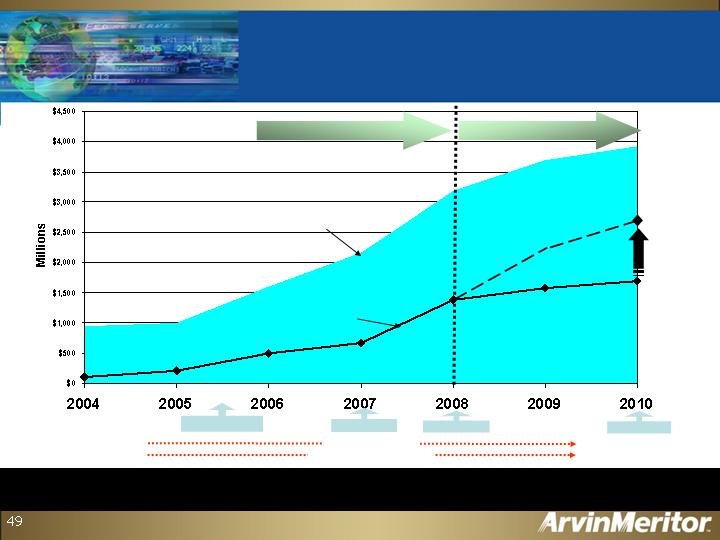

Commercial Vehicle Diesel Emissions

Global Addressable Market

$660/truck

$2,700/truck

Euro 4 / Japan

EPA 2007

Euro 5

EPA 2010

EU: mostly SCR

US: EGR+DPF

Technology TBD

Current Tech. Prevails

(EGR + DPF)

New Tech. Required

(SCR & Active DPF)

Technology Defined

Global Market $2+ billion in 2007

ARM Addressable Market

Addressable Market Grows to $2-3 Billion in 2010

Global Solutions

ArvinMeritor Solutions

$2,000/truck

$300-360 /truck

Global Volume Growth by Solution

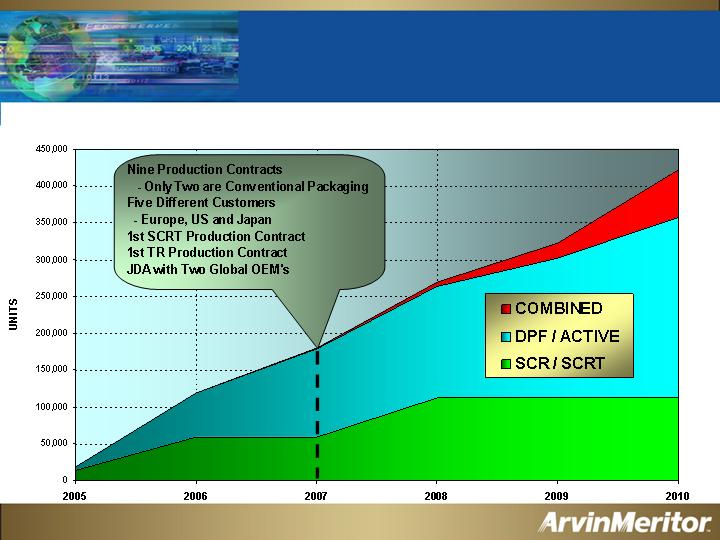

50

Positioned to Meet

Global Requirements

Diesel emissions market is growing rapidly for Commercial Vehicle

and Light Vehicle

Positioned to do more than packaging in diesel

SCR, Thermal Regenerator, Plasma Fuel Reformer

Experience in United States, Europe and Japan

“Passive” and “Active” Aftertreatment

Fuel cost and precious metals price escalation favors ArvinMeritor

technology

Addressable market is likely to grow

Active DPF Regeneration displacing Catalytic Filters

Further developing portfolio for 2010

Combined NOx and PM solution

Diesel aftertreatment has more content $ than gasoline

Problem-solving opportunities in diesel aftertreatment

Capturing new business and developing future technology

51

Financial Review

Jim Donlon

Senior Vice President and CFO

52

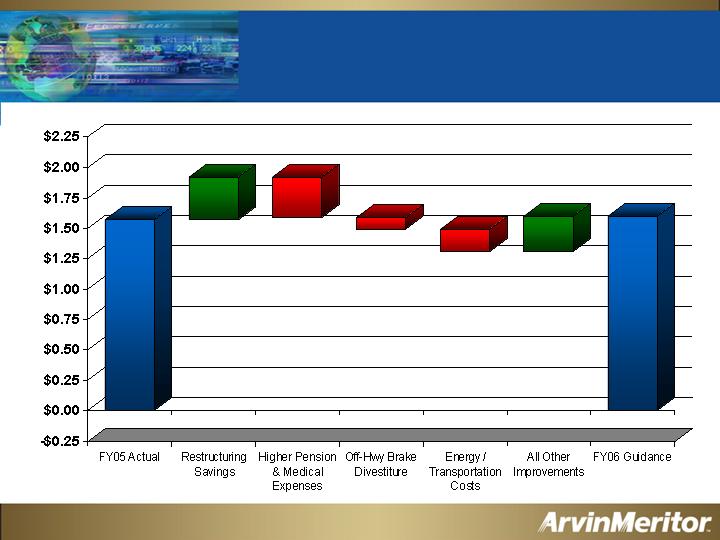

FY06 EPS Walk from FY05

(Before Special Items)

$0.30 - $0.40

($0.32) – ($0.35)

($0.10)

($0.15) – ($0.20)

$0.20 – $0.38

$1.50 – $1.70

$1.57

53

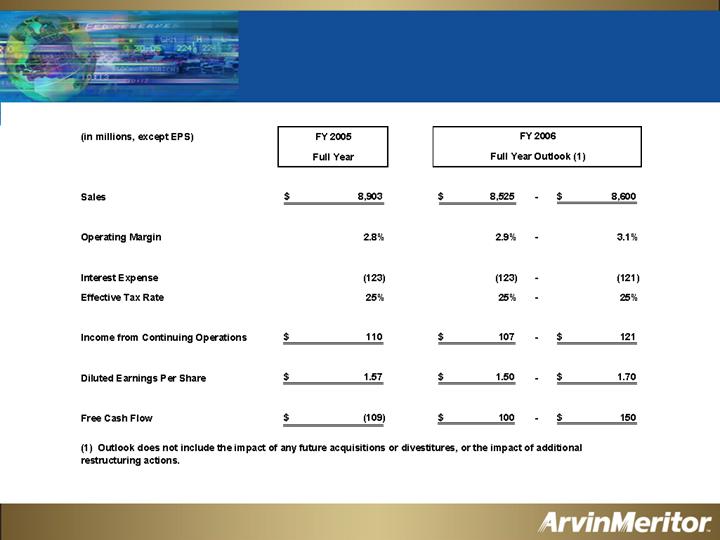

FY06 Outlook

Continuing Operations Before Special Items

54

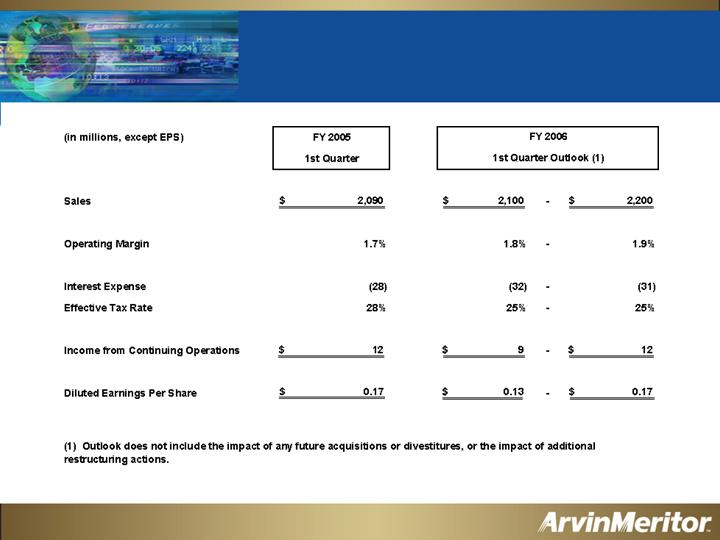

FY06 First Quarter Outlook

Continuing Operations Before Special Items

55

FY06 Free Cash Flow Walk from FY05

$100

$110

$0- $50

$100 - $150

($109)

($9)

($ millions)

56

FY06 Cash Flow Outlook Details

(in millions)

Income From Continuing Operations

85

$

-

99

$

Adjustments to Income

Depreciation and Other Amortization

180

-

185

Pension and Retiree Medical Expense

135

-

135

Pension and Retiree Medical Contributions

(175)

-

(175)

Changes in Assets and Liabilities

30

-

66

Cash Flows provided by continuing operations

255

-

310

Cash Flows provided by discontinued operations

-

-

5

Total Cash Flows Provided by Operations

255

-

315

Capital Expenditures

(155)

-

(165)

Free Cash Flow

100

$

-

150

$

Note: Does not include the effects of any changes in A/R securitization and factoring or any future

acquisitions or divestitures.

Full Year

FY 2006

57

Pension Discount Rate Trends

2005 discount rate creates headwind in 2006

Trend suggests that discount rate will create tailwind in 2007

Ten-Year Treasury Rate

Estimated spread to

Corporate AA Bond

Portfolio

58

Actions to Reduce Legacy Obligations

Changed supplemental healthcare benefits to Medicare

eligible retirees

Benefit no longer provided

Announced Aug. 3, 2004; effective Jan. 1, 2006

Reduced Accumulated Projected Benefit Obligation

(APBO) by $257M

Modified pension benefit for new employees

Defined benefit becomes defined contribution

Effective Oct. 1, 2005

59

Recent cash flow has been strong

Expecting 2006 to be much better than 2005

Pension discount rate creates 2006 headwind

Non-cash event

Rate trends suggest 2007 tailwind

Legacy cost issues addressed

Liquidity is adequate

Plans to continue improving

Financial Summary

60

Rakesh Sachdev

Senior Vice President

Corporate Strategy

61

Beginning Our Transformation with

Renewed Strategic Intent

From

To

To be the number one

supplier to the motor

vehicle industry by 2010

To be a leading global

provider of innovative

customer solutions that

enhance mobility, safety

and the environment

Transition Focus from Gaining Scale to

Sustainable Value Creation

Result

Expectation

Focused on revenue growth

CAGR >10% since spin-off

CVS + LVS

Leading positions in CVS

Undercarriage and LVS Emissions

Focus on creating valued solutions

Mobility, safety, environment

Expanded markets

Framework for differentiating our core

product for substantial profitability

62

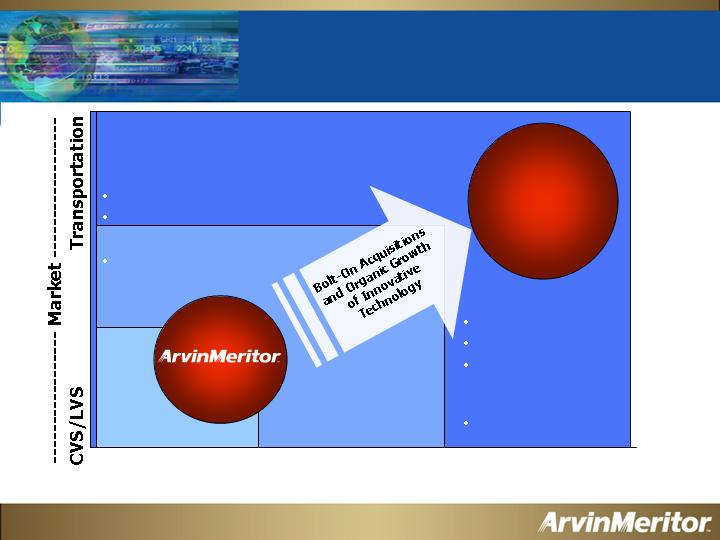

Near-Term Priorities

Reshape our portfolio

Assess strategic fit and financial viability

Complete operational turnaround of

underperformers

Drive for achieving ROIC targets in 3-5 years

Create value for additional portfolio activity

Pursue profitable expansion strategy

Emerging market

Customer service and support

Adjacent and emerging technologies

Long-Term Financial Target:

ROIC 13-15% and Operating Margin 6-7%

63

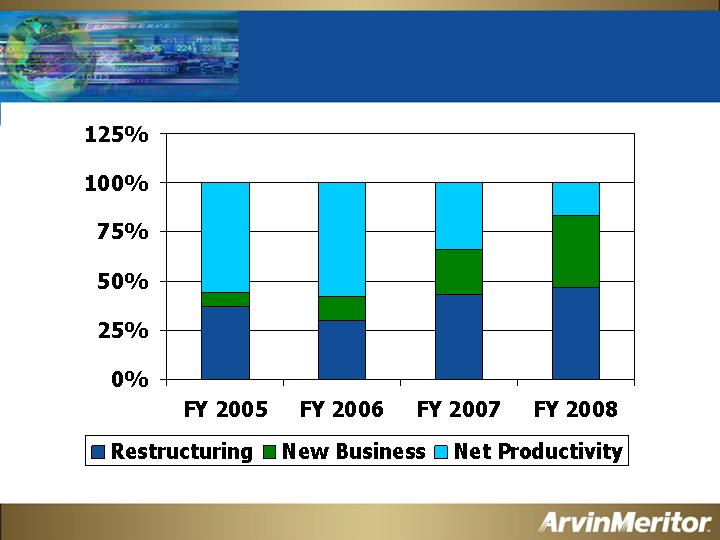

Roadmap to Long-Term Margin Target

(Five-Year Results)

6.0% - 7.0%

Long-Term Target

0.75% - 1.0%

Active Intelligent Systems

(Undercarriage and Emissions)

0.5%

Commercial Vehicle Aftermarket

0.5%

Emerging Markets

0.25% - 0.5%

Portfolio Reshaping/Divestitures

0.5% - 1.0%

Operational Improvements,

Including Supply Chain

0.5%

Restructuring

Roadmap for Improvement:

3%

Current

Operating Margin %

64

Reshaping Our Portfolio in 2006

Products:

Axles

Brakes

Suspensions

Shocks

Wheels

Roofs

Doors

Emissions

Strategic Fit

Mobility, Safety

and Environment

Value Creation

Customers:

Financial Fit

Operating Margin

and Asset Turns

Sustainable ROIC

Reshaping the Management and Content of Our Portfolio

Core

Business

65

Focused Initiatives for Expansion

CORE BUSINESSES

EXAMPLES:

Emerging

Markets

Customer Service

and Support

Adjacent and Emerging

Technologies

GROWTH

OPPORTUNITIES:

China/India

Axles

Brakes

Corporate

Shared

Services

Commercial

Vehicle

Aftermarket

Vehicle Stability Control

Driver Warning

Collision Avoidance

Active DP/NOx Control

Fuel Optimization

Active/Intelligent Systems

66

Emerging Market Business Model

Build business in emerging markets by transferring

proven solutions from the developed world

Invest in joint ventures and wholly owned subsidiaries

Greater than $10 Billion addressable market

Utilize emerging market capacity for economical export

opportunities

Evaluate Business Process Outsourcing (BPO) initiatives

* Our current addressable market >$10B

Total Returns

67

Growth Potential for

Commercial Vehicle Aftermarket

Large global market

$90 Billion ($20 Billion

undercarriage)

Leverage growth on

Expanding OE business

Channel management

experience

Emerging market presence

and infrastructure

68

Path to Differentiating Solutions

Products Solutions

---------------------------Technology -------------------------

Active and

Intelligent

Solutions

Active Ride Control

Vehicle Dynamic Control

Driver Warning

Collision Avoidance

Active Emissions

Management

Active NoX and PM

Reduction

Systems

Undercarriage Systems

Mechanical Components

Modules and Aftermarket

Emissions Systems

Aftertreatment Systems

69

Positioning ArvinMeritor for

Sustained Value Over the Cycle

In the next one to two years:

Focus on reshaping our portfolio

Create value through operational improvements

Develop emerging markets, service and support, and

accelerate technology initiatives

In the next three to five years:

Achieve and begin sustaining value creation targets –

ROIC of 13-15 percent

Pursue journey towards active/intelligent systems

through adjacent technology and market objectives

70

Chip McClure

Chairman, President and CEO

Summary

71

Key Points

Strong leadership team

Taking the right actions today

Focused on making 2007

a non-event

Financially healthy

Driving to 13-15 percent ROIC

72

www.arvinmeritor.com

73