This presentation contains statements relating to future results of the company (including certain projections

and business trends) that are “forward-looking statements” as defined in the Private Securities Litigation

Reform Act of 1995. Forward-looking statements are typically identified by words or phrases such as

“believe,” “expect,” “anticipate,” “estimate,” “should,” “are likely to be,” “will,” and similar expressions. Actual

results may differ materially from those projected as a result of certain risks and uncertainties, including, but

not limited to, global economic and market conditions; the demand for commercial, specialty and light

vehicles for which the company supplies products; risks inherent in operating abroad (including foreign

currency exchange rates and potential disruption of production and supply due to terrorist attacks or acts of

aggression); availability and cost of raw materials, including steel; OEM program delays; demand for and

market acceptance of new and existing products; successful development of new products; reliance on

major OEM customers; labor relations of the company, its customers and suppliers; potential disruptions in

supply of parts to our facilities or demand for our products due to work stoppages; the financial condition of

the company’s suppliers and customers, including potential bankruptcies; successful integration of acquired

or merged businesses; the ability to achieve the expected annual savings and synergies from past and

future business combinations; success and timing of potential divestitures; potential impairment of long-lived

assets, including goodwill; competitive product and pricing pressures; the amount of the company’s debt; the

ability of the company to access capital markets; credit ratings of the company’s debt; the outcome of

existing and any future legal proceedings, including any litigation with respect to environmental or asbestos-

related matters; as well as other risks and uncertainties, including, but not limited to, those detailed from

time to time in the filings of the company with the Securities and Exchange Commission.

Forward-Looking Statements

2

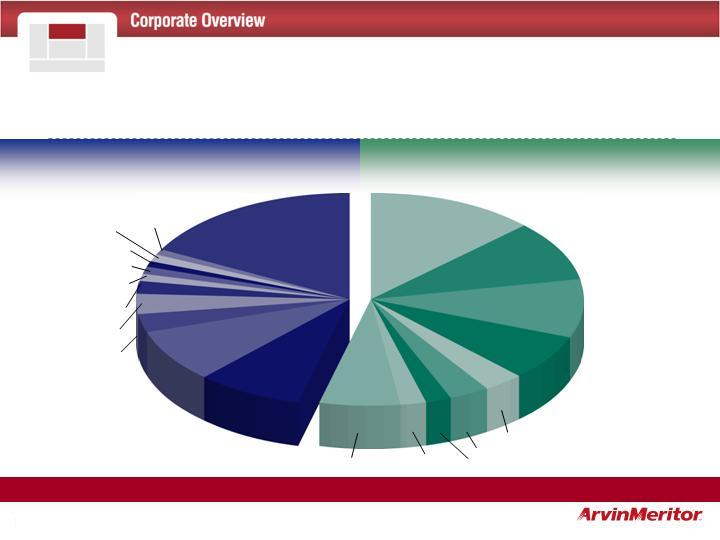

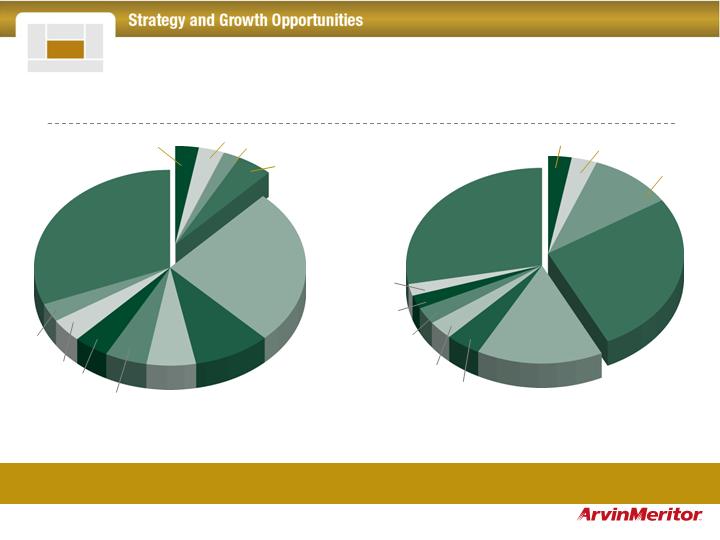

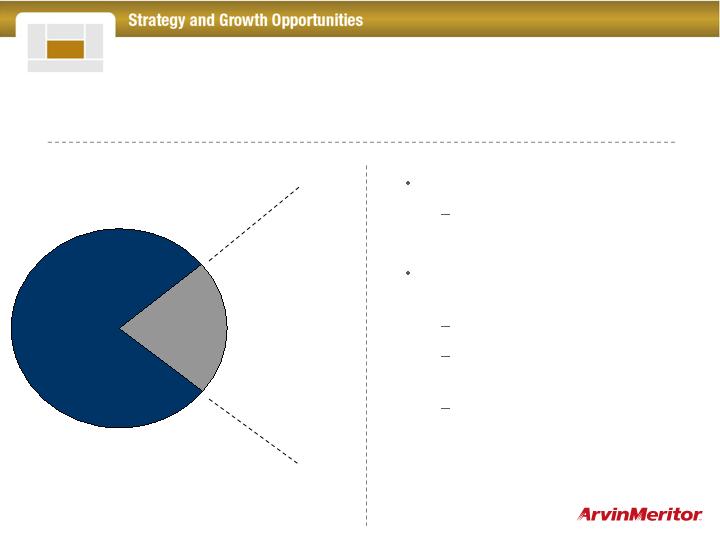

CVS Total Sales of $4.1 billion = 46%

LVS Total Sales of $4.7 billion = 54%

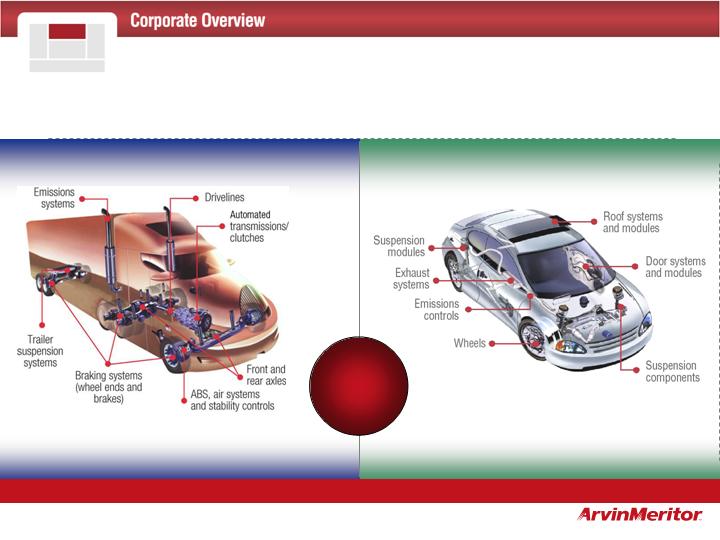

Broad Product Portfolio

Sales from Continuing Operations $8.8 Billion in FY05

#1 or #2 in

most major

markets

3

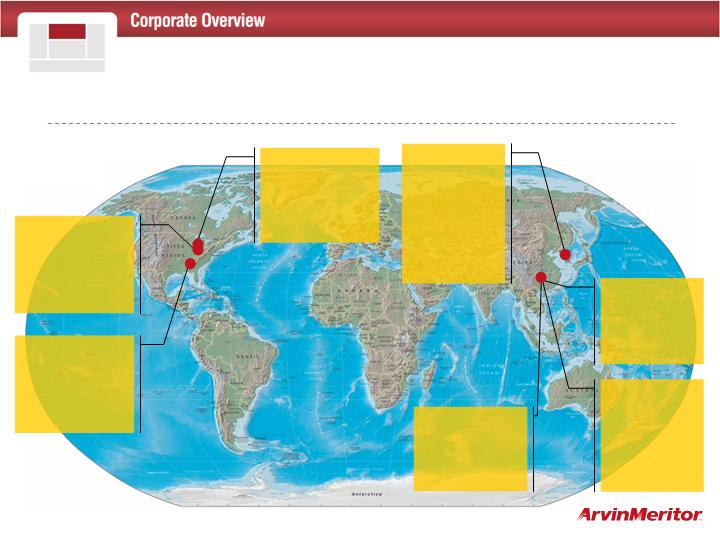

Strong Global Presence

North America – 51%

FY05 sales $4.5B

LVS – $2.0B

CVS – $2.5B

46 manufacturing facilities

7 joint ventures*

6 technical centers

Europe – 38%

FY05 sales $3.3B

LVS – $2.2B

CVS – $1.1B

43 manufacturing facilities

8 joint ventures*

12 technical centers

South America – 5%

FY05 sales $0.5B

LVS – $240M

CVS – $217M

12 manufacturing facilities

2 joint ventures*

2 technical centers

Asia Pacific & ROW – 6%

FY05 sales $0.5B

LVS – $276M

CVS – $256M

20 manufacturing facilities

9 joint ventures*

1 technical center

* Includes consolidated and non-consolidated joint ventures

121 Manufacturing

Facilities

26 Joint Ventures

21 Technical

Centers

4

Diverse Customer Base

Minimizes Reliance on Any Single Customer

CVS Customer Base

LVS Customer Base

DaimlerChrysler

13%

General Motors

9%

Volkswagen

9%

Ford 7%

Asian Based OEMs 3%

BMW 3%

PSA 2%

Fiat 2%

Other LVS 6%

Other CVS

16%

Fiat 1%

Asian Based

OEMs 1%

Ford 1%

Volkswagen 1%

General Motors 1%

PACCAR 2%

Renault 3%

International 3%

Volvo 8%

DaimlerChrysler

9%

5

Diverse Customer Base

Limited Exposure to Troubled Customers in North America

LVS exposure to

General

Motors in North

America = 7%

of total

company sales

LVS exposure to

Ford in

North America = 3%

of total

company sales

6

Diverse Customer Base

CVS Exposure to Class 8 Downturn in North America Approximately 11%

PACCAR

International

Volvo/Mack

DaimlerChrysler

7

Recent Accomplishments: Expanding Customer Base

Awarded two new

emissions

contracts with

Chinese

manufacturer

Awarded exhaust

aftertreatment

device packaging

for Daimler-

Chrysler’s heavy-

duty engines

Signed multi-

year contract to

supply door

module to the

Chinese market

Entered into

joint venture

with DongWon

Precision

Industrial Co. to

supply diesel

particulate filters

to the Korean

market

Entered into

joint venture

with First Auto

Works (FAW)

to produce

foundation

brakes

Opened Customer

Value Center in

Alabama to supply

door modules for

Hyundai’s Sonata

and Sante Fe

Selected as

standard

equipment supplier

for hub and brake

drums by Wabash

National Corp.

8

LVS:

Thomastown, Australia (Doors)

Augsburg, Germany Plant #2 (Emissions Technologies)

Asti, Italy (Ride Control)

Blackpool, U.K. (Emissions Technologies)

Pulaski, Tenn., U.S. (Shock Absorbers)

Valladolid, Spain (Doors)

Mosciano, Italy (Emissions Technologies)

Birmingham, England (Doors)

CVS:

Cleveland, Ohio, U.S. (Aftermarket distribution)

Wrexham, U.K. (Trailer Products)

Annualized Savings of $50-60 Million Beginning in 2007

Recent Accomplishments:

Restructuring in Process to Optimize Operations

9

Recent Accomplishments:

Divestitures of Non-Core Business

In process

Europe

In process

Ride Control

South Africa

In process

Motion control

In process

Ride control

Not disclosed

Sold

Exhaust

$170 million

Sale completed

Purolator filters

North America

$9 million

Sold

Equity Share in Purolator India

India

Light Vehicle Aftermarket

$43 million

Sold

Off-Highway Brakes

Commercial Vehicle Systems

Proceeds

Status

10

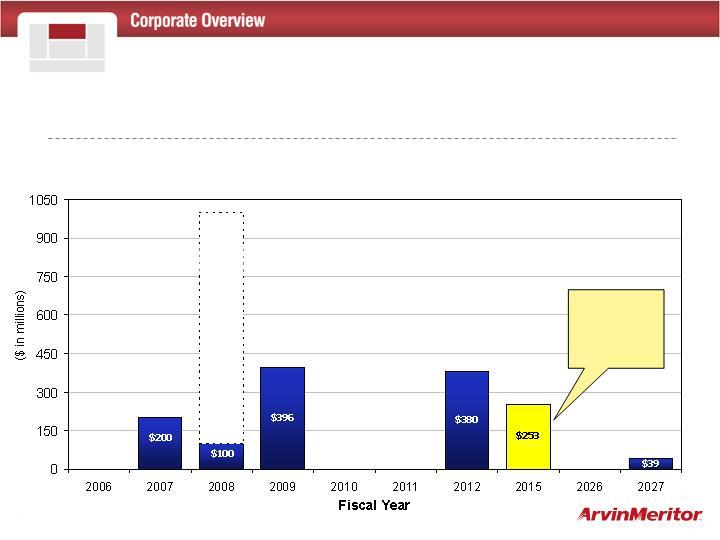

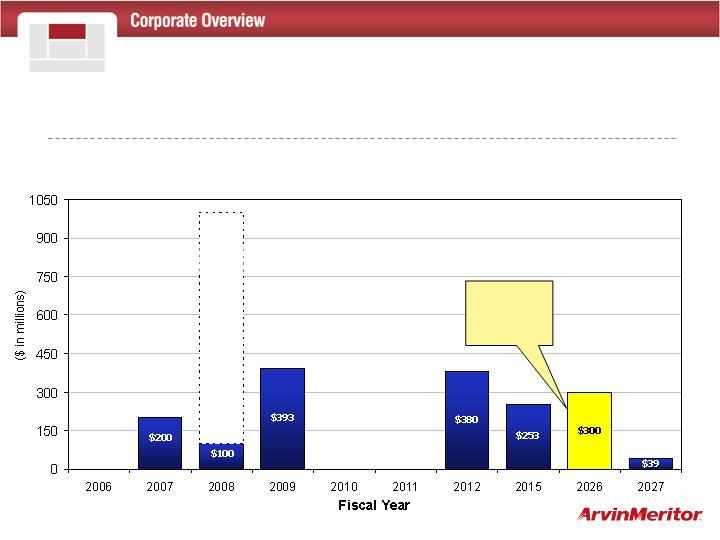

$900

Revolver

Fiscal Year ‘04 Term Debt Through 2011: $948 Million

Recent Accomplishments:

Improving the Balance Sheet

11

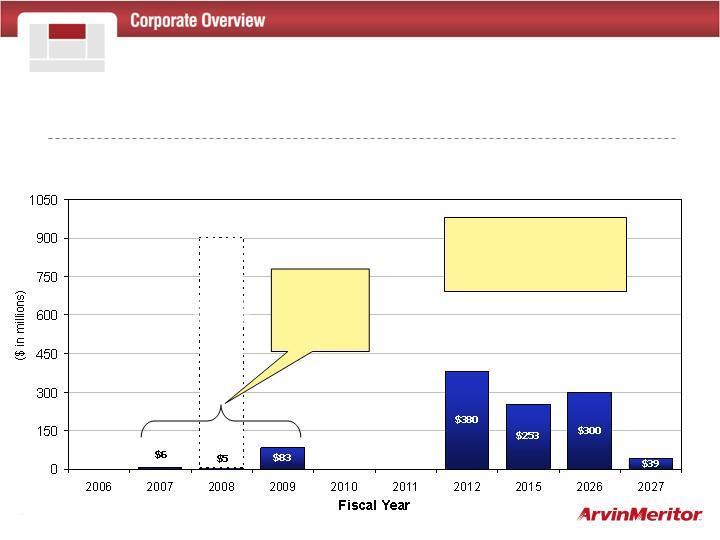

Fiscal Year ‘05 Term Debt through 2011: $696 Million

$900

Revolver

Recent Accomplishments:

Improving the Balance Sheet

September ’05:

exchanged

$253 million

term debt from

2009 to 2015

* Company repurchased $20 million in FY05

*

12

Recent Accomplishments:

Improving the Balance Sheet

March ‘06: Issued New $300 Million Convertible Bond

$900

Revolver

Demand for

new bond was

approximately

$1.2 billion

* Company repurchased $3 million in Q1 FY06

*

13

Current Term Debt Maturing through 2011 Now $94 Million

Recent Accomplishments:

Improving the Balance Sheet

$900

Revolver

Repurchased

$600 million in

Term debt

from 2007

through 2009

Funded repurchase through:

Divestiture proceeds: ~$220 million

Convertible funds: ~$300 million

Cash on hand: ~$80 million

14

Recent Accomplishments:

Improving the Balance Sheet

Net term debt reduction of $300

million

From $1.4 billion to $1.1 billion

Extended $553 million of

term debt

Now due in 10 to 20 years

No Major Debt Maturities Until 2012

15

Focusing on Core Growth Drivers

Vehicle Performance

Ride Comfort

Vehicle Stability

Collision Avoidance

Fuel Efficiency

Emissions Reduction

Mobility

Safety

Environment

16

ASSESS PRODUCT PORTFOLIO FOR STRATEGIC FIT

Pursuing Profitable Business Expansion

Mobility

Safety

Environment

STRENGTHEN AND GROW IN PROFITABLE SEGMENTS

Optimize Cash Contribution and Improve Operating Performance

ROIC Target of 15%

ASSESS PRODUCT PORTFOLIO FOR FINANCIAL FIT

17

“Activate” existing

mechanical products

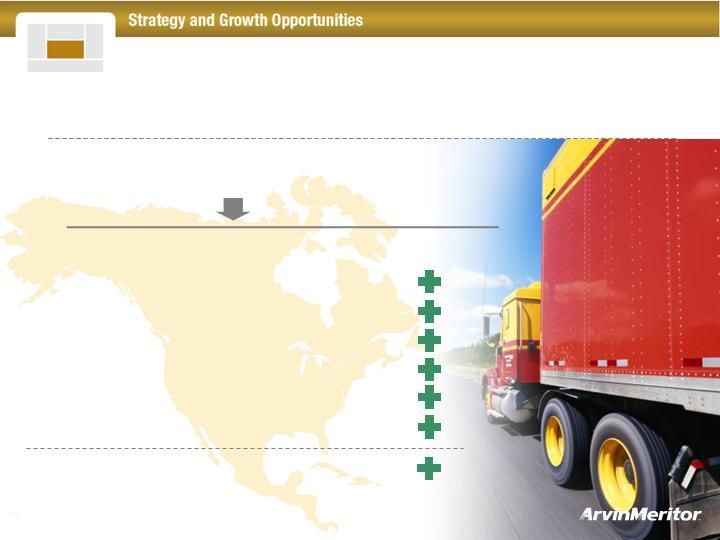

Pursuing Profitable Business Expansion

Increase presence

in emerging

markets

Grow Commercial

Vehicle Emissions

and Aftermarket

businesses

18

Source: Keystone: The World’s Top Automotive Markets in 2030

2005

2030

U.S.

26%

R.O.W.

31%

Spain

3%

U.K. 4%

Italy 5%

Germany 6%

Japan

9%

France 4%

China

27%

U.S. 15%

India 10%

Japan

4%

Germany

3%

Brazil 3%

Russia 3%

Mexico

3%

France

2%

U.K.

2%

R.O.W.

28%

12% - 43% Growth Projected in Brazil, Russia, India and China

Vehicle Registration Growth Projection in Top 10 Markets

China 4%

India 2%

Brazil 3%

Russia 3%

BRIC Markets Offer Significant Growth Potential

19

Current Operations in South America

Wholly-Owned Operations

Limeira, Brazil

Steel wheels, doors, latches, catalytic converters, emissions

technologies

Customers include DaimlerChrysler, VW, Toyota, Honda, GM,

Ford, PSA, Fiat

Osasco, Brazil

Axles, carriers, gear sets, housings, precision forgings

Customers include Volvo, VW, Ford, International, IVECO,

Agrale, Axle Tech

Distributes aftermarket axles, brakes, suspension parts

Customers include Iveco, VW, Volvo, Ford

Cordoba, Argentina; Camcari (CVC), Gravatai, Sao Bernardo do

Campo, Brazil

Manufacturer and assemble exhaust components and systems

Customers include Toyota, Honda, VW, Renault, ASA, Peugot,

GM, Ford, DaimlerChrysler

Valencia, Venezuela

Emissions and ride control

Customers include Toyota, Hyundai, GM, Ford, DaimlerChrysler

Joint Ventures

Master Sistemas Automotive Limitada, Caxias do Sul, Brazil

Brakes

Suspensys Sistemas Automotive Limitada, Caxias do Sul, Brazil

Suspensions

Operating in South America Since 1973

Nine Manufacturing Facilities

20

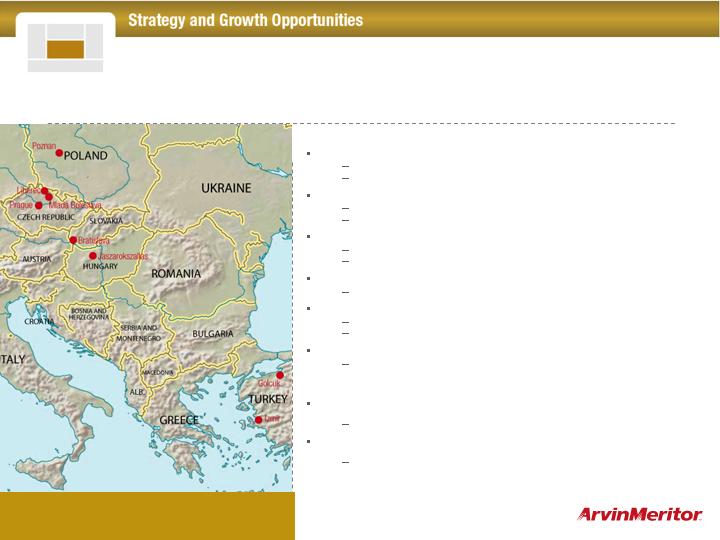

Current Operations in Eastern Europe

Wholly-Owned Operations

Liberec, Czech Republic

Complete door assemblies, door modules, window regulators

Customers include Skoda Auto, Volkswagen, Toyota/PSA

Mlada Boleslav, Czech Republic

Exhaust systems

Customers include Volkswagen Slovakia, Skoda

Jaszarokszallas, Hungary

Catalytic converters, mufflers, pipes

Customers include Porsche, Suzuki, Volkswagen, BMW, Ferrari

Poznan, Poland

Door modules for Volkswagen Poznan

Golcuk, Turkey

Cold and hot end exhaust

Customers include Ford Otosan

Bratislava, Slovakia

Sunroofs, large opening systems, modules, glass encapsulation

Joint Ventures

Ege Fren Sanayii ve Ticaret A.S., Izmir, Turkey

Brakes

Arvin Exhaust s.r.o., Prague, Czech Republic

Emissions Technologies

Operating in Eastern Europe Since Early 1990’s

Eight Manufacturing Facilities

21

Current Operations in India

Wholly-Owned Operations

Technical Center, Bangalore

Established in 1998

More than 100 employees engaged in engineering, IT and

procurement activities supporting ArvinMeritor’s light and

commercial vehicle business groups

Joint Ventures

Automotive Axles Ltd., Mysore

Joint venture partnership with Kalyani Group

Manufactures axles, brakes, housings and components for light,

medium and commercial vehicles, and technical center

Meritor HVS India Ltd., Mysore

Joint venture partnership with Bharat Forge Limited (BFL)

Product and application engineering, assembly, marketing and

sale of axle and brake products for light, medium and heavy

commercial vehicles

Arvin Exhaust India Private Ltd., Chennai and Bangalore (CVC)

Joint venture partnership with Anand Group

Manufacture, assembly and marketing of complete automotive

exhaust systems, catalytic converters, manifolds and related

components

Gabriel India Ltd., headquarters in Delhi

Joint venture partnership with Anand Group

Seven plants with total manufacturing capacity of more than 10

million shock absorbers, struts and front forks

Operating in India Since Late 1960’s

Two Technical Centers

Ten Manufacturing Facilities

22

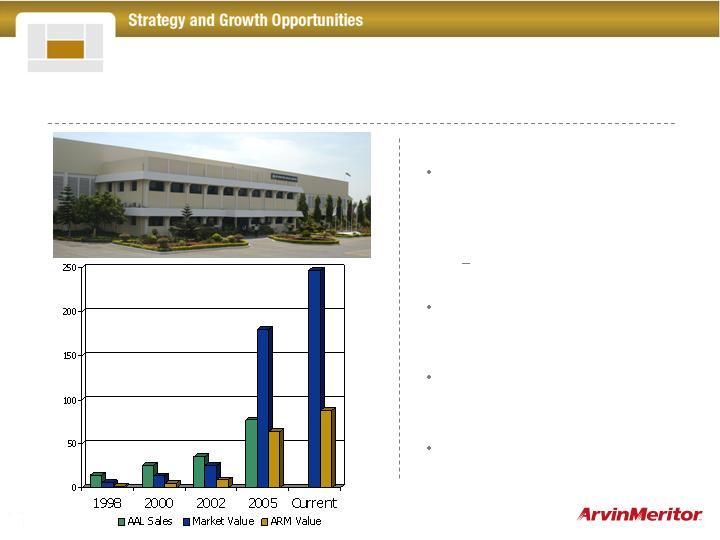

Established joint venture with

Bharat Forge in 1982 with an

investment of approximately

$3 million

ArvinMeritor has thirty-five

percent ownership

Sales have increased from

$14 million in 1998 to

$77 million in 2005

Market value during this same

period increased from $6

million to $180 million

Current market value is $250

million

Success Story: Automotive Axles – India

23

Current Operations in China

Wholly-Owned Operations

Pudong

Axle assembly

PuDong (CVC), Yantai (CVC), Anting, Chongqing (CVC) and Nanjing

Emissions technologies

Customers include VW, SAIC, GM, Ford, Jeep, SEA

Zhenjiang

Window regulators and door latches

Customers include Mazda Japan, FAW-VW, Volkswagen

Shanghai

Changchun

Door modules, CVC beginning in October 2006

Shanghai

Corporate office

Joint Ventures

Shanghai ArvinMeritor Automotive Parts Co. Ltd.

Sunroofs

Customers include Shanghai VW

ArvinMeritor FAW Sihuan (Changchun) Vehicle Brake Co. Ltd.

Brakes

Customers include FAW

Xuzhou Meritor Axle Co. Ltd.

Axles for off-highway vehicles, brakes

Customers include FAW, FOTON, Puyuan, Taian

Meritor Huayang Braking Co. Ltd. (Shanghai)

Brakes

Customers include Golden Dragon, Ankai Bus, Volvo Sunwin

Operating in China Since Late 1980’s

Doubled Presence in Past Three Years

Twelve Manufacturing Facilities

24

India And China Are Projected to Become Major

Component Producers

Source: Market research, Booz Allen IC

Total Component Part Sales from 2000 to 2010

($ Billions)

India

China

25

Global supply partners for key components

In-market conduit to customers

Continuing operations are involved in 26 joint ventures in 13

countries

Sales of unconsolidated joint ventures in 2005 were $1.5 billion

Equity earnings from joint ventures in fiscal year 2005 were $28

million

Increase of 47 percent over the prior year

Vital Element of Global Expansion and Technology Strategy

Growing through Joint Ventures

26

Sales Growth from Unconsolidated Joint Ventures

2005

2004

2003

$1.5B

$1.1B

$843M

27

Forming Joint Ventures to Grow in Emerging Markets

2005 Consolidated Sales

Including All Joint Ventures

North

America

51%

Europe

38%

Rest of

World

11%

North

America

49%

Europe

32%

Rest of

World

19%

Geographic Diversity Aided by Joint Ventures

28

Emerging Markets Offer Attractive

Shared Service Opportunities

Accounts Payable

Accounts Receivable

Database and

network

administration

Enterprise

Resource Planning

Application

development

Maintenance and

support

Call Center

Help Desk

Daily procurement

activities

Intelligent commodity

sourcing

Supplier development

and SQA

Purchase – pay

processing

FINANCIAL

SERVICES

VALUE ADDED

ENGINEERING

Above and beyond

CAD

Cost reduction –

VA/VE

Complete product

development cycle

Design, develop and

validate

24/7 virtual design

center

IT

PROJECTS

PROCUREMENT

AND

ADMINISTRATION

29

Comprehensive strategy to

double LCCC spend by 2008

Substantial cost reductions of

raw materials and components

Localize supply base in

Asia/Pacific

Procurement leadership based

in Shanghai

Emerging Markets Offer Attractive Sourcing

Opportunities

Leading Cost-Competitive Country

(LCCC) Spend

60%

43%

22%

2010

2008

2005

30

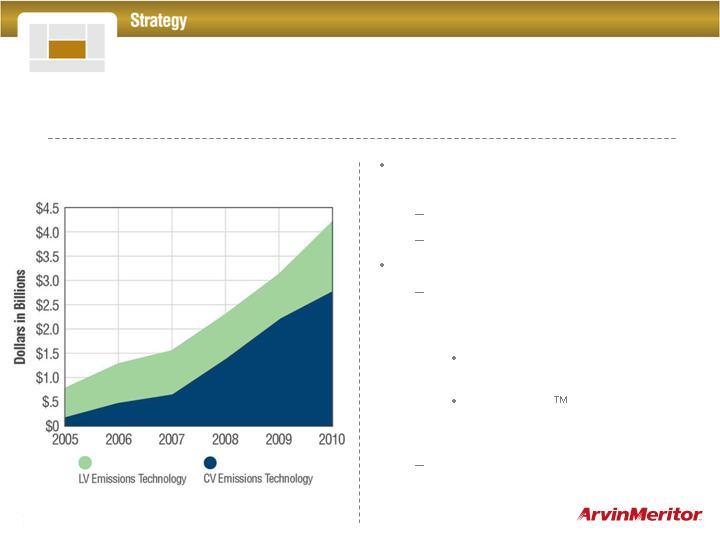

Capturing Our Share of Rapidly Growing

Global Diesel Emissions Market

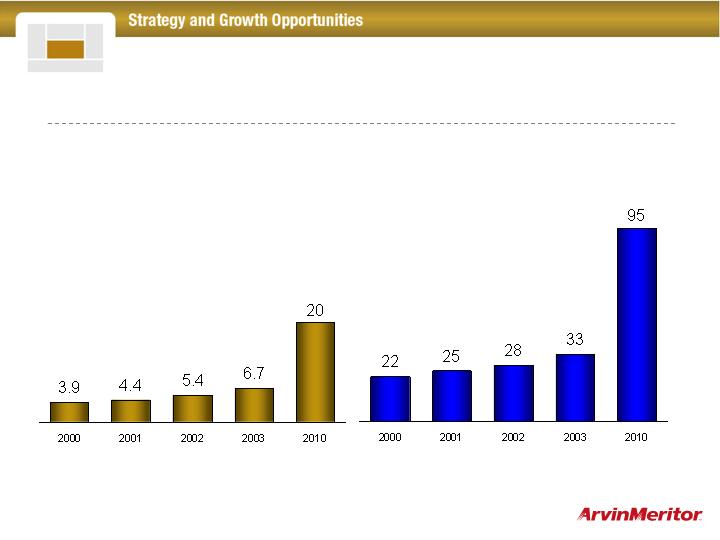

Addressable market of $750 million in

2005 grows to $4.2 billion by 2010

$2.7 billion in CVS

$1.5 billion in LVS

Significant business awards

Nine Commercial Vehicle

Emissions (CVE) contracts with

seven different customers

Exhaust aftertreatment device

packaging for DaimlerChrysler

ActiveClean Atomizer

Technology for General Engine

Products

1.4 million LV diesel particulate

filters

Diesel Emissions Addressable Market

31

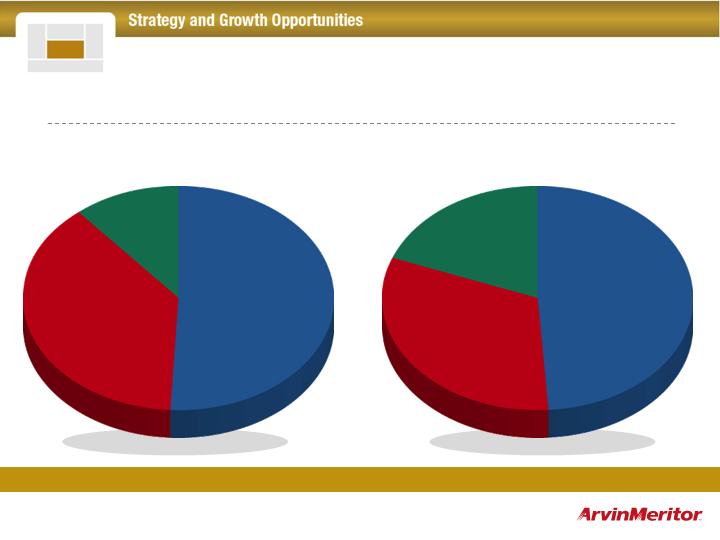

Capturing Growth in Global

Commercial Vehicle Aftermarkets

Global Market of $89 Billion

Addressable Undercarriage

Market of $20 Billion

Leverage Strengths to Grow

Business

Expanding OE Business

Channel Management

Experience

Emerging Market Presence

and Infrastructure

Global

Market

Addressable

Market

$89 billion

$20 billion

32

Plans to Mitigate the 2007 NA Class 8 Downturn

Layered Capacity

Emerging Markets

LVS Restructuring

High-Volume Premium Reduction

CVA Growth

CVE Growth

Trailer Productivity

Conversion @ 15%-20% ($45M) – ($60M)

30-35% ~($300M)

Exposure to Class 8: 11% of $8.8B ~ $900M

33

Diversified product portfolio and

customer base

Strengthened balance sheet

Leading positions in global

markets

Growing CVE and CVA

businesses

Expanding in emerging markets

Mitigating 2007 N.A. Class 8 truck

downturn

Investment Highlights

34

www.arvinmeritor.com

35