Exhibit 99

2007 AANY Conference

Chip McClure

Chairman, CEO and President

1

This presentation contains statements relating to future results of the company (including certain projections and business trends) that are “forward-looking statements” as defined in the Private Securities Litigation Reform Act of 1995. Forward-looking statements are typically identified by words or phrases such as “believe,” “expect,” “anticipate,” “estimate,” “should,” “are likely to be,” “will” and similar expressions. Actual results may differ materially from those projected as a result of certain risks and uncertainties, including but not limited to global economic and market cycles and conditions; the demand for commercial, specialty and light vehicles for which the company supplies products; risks inherent in operating abroad (including foreign currency exchange rates and potential disruption of production and supply due to terrorist attacks or acts of aggression); availability and cost of raw materials, including steel; OEM program delays; demand for and market acceptance of new and existing products; successful development of new products; reliance on major OEM customers; labor relations of the company, its suppliers and customers, including potential disruptions in supply of parts to our facilities or demand for our products due to work stoppages; the financial condition of the company’s suppliers and customers, including potential bankruptcies; possible adverse effects of any future suspension of normal trade credit terms by our suppliers; potential difficulties competing with companies that have avoided their existing contracts in bankruptcy and reorganization proceedings; successful integration of acquired or merged businesses; the ability to achieve the expected annual savings and synergies from past and future business combinations and the ability to achieve the expected benefits of restructuring actions; success and timing of potential divestitures; potential impairment of long-lived assets, including goodwill; competitive product and pricing pressures; the amount of the company’s debt; the ability of the company to continue to comply with covenants in its financing agreements; the ability of the company to access capital markets; credit ratings of the company’s debt; the outcome of existing and any future legal proceedings, including any litigation with respect to environmental or asbestos-related matters; rising costs of pension and other post-retirement benefits and possible changes in pension and other accounting rules; as well as other risks and uncertainties, including but not limited to those detailed herein and from time to time in other filings of the company with the SEC. These forward-looking statements are made only as of the date hereof, and the company undertakes no obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise, except as otherwise required by law.

Forward-Looking Statements

2

Agenda

Overview of Company and Results

Envisioning the Future of ArvinMeritor

Performance Plus Success Factors

3

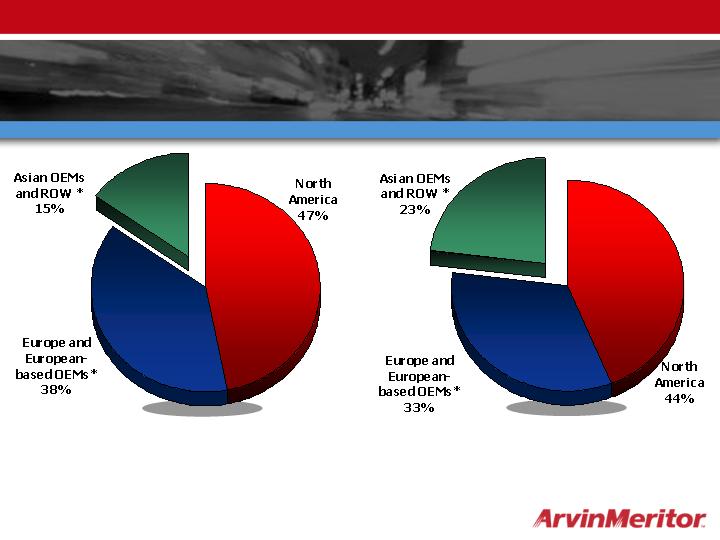

Diverse Customer Base

Commercial Vehicle Customers

Light Vehicle Customers

DaimlerChrysler

10%

General Motors

9%

Volkswagen

10%

Ford 7%

Asia-Based

OEMs 3%

BMW 2%

Fiat 3%

Other LVS

9%

Other CVS

15%

Fiat 2%

Asia-Based

OEMs 3%

Ford 3%

Volkswagen 1%

General Motors 1%

PACCAR 2%

International 3%

Volvo 9%

DaimlerChrysler

8%

47%

Commercial

Vehicles

53%

Light

Vehicles

Overview

4

Consolidated

Revenue

* Includes local operations of companies

headquartered in North America and Europe

+ Non-Consolidated

Joint Ventures

Geographic/Customer Mix

of 2006 Sales

Overview

5

Commitments Kept

$262 million

Operating income of $250 - $265 million

$284 million

Free cash flow of $100 - $150 million

$501 million

reduction in net debt

Improve balance sheet

Delivery

$1.78

$9.2 billion

EPS of $1.50 - $1.70

Sales of $8.5 - $8.6 billion

Actual Result

Goal

Overview

Goals from 2005 Analyst Day

6

Agenda

Overview of Company and Results

Envisioning the Future of ArvinMeritor

Performance Plus Success Factors

7

Today’s Portfolio of Businesses

CV Emissions

LV Emissions

Roofs

Wheels

Doors

Aftermarket

Specialty

Axles

Brakes

Trailers

Low

High

Growth

Envisioning the Future

Emerging

Markets

New

Stars

8

Vision for Growth and Profitability

Be a global systems leader

in our target markets

Develop scalable product

technologies and

capabilities, focusing on

electronics and controls

Accelerate growth in Asia

and with Asian OEMs

Accelerate growth in

Commercial Vehicle

Aftermarket

Achieve top quartile

financial performance

among peer companies

Safety

Environment

Mobility

Envisioning the Future

9

Integrated Systems Leadership

Envisioning the Future

What it is not

Full-service supplier initiative

Outsourcing of engineering from OEMs

What it is

For mature markets:

High-tech, cross-systems capability to develop new

product solutions that customers will value

More controls and electronics capability

For developing markets

Helping local OEMs gain the full cost benefits of

modularization and mechanical integration

10

Medium-Term Goals

Growth with a Purpose

Envisioning the Future

1/3 – 1/3 – 1/3 regional business mix

Triple sales in Asia and with Asian OEMs

Triple the size of Aftermarket business

Grow organically where margins are good

Achieve ROIC of 13 – 15 percent

11

Triple Asian Sales in Five Years

Envisioning the Future

ArvinMeritor is a Partner for All Phases

Success: Being the partner our growing customers need now

- Capacity for explosive growth

- Improved technology

- World-class quality

Enduring global partnership

Customer Phase

Customer Need

12

OEMs Producing in Asia

- Local consumption

- Regional export

- Global export

Transplants

Case Study: CIMC Leverages ARM Quality

and Technology For Leadership

CIMC, the world’s largest marine container company with sales

of $3.5 billion, entered the semi-trailer business in 2002

Already the #1 trailer OEM in China, aspires to be #1 globally

For about three years, ARM has supplied axles from Frankfort,

KY for trailer production in China for customers in the U.S.

(about $60 million ARM sales in 2006)

ARM delivered needed technology and quality for global exports

Pushing for the same advantages at lower cost, CIMC

encouraged ARM to build new facility in China

We opened a wholly-owned green field plant in Wuxi, Jiangsu;

customer shipments began this week

Envisioning the Future

13

Wuxi Plant: Platform for Growth

300,000 square feet and 160 employees in 2007

350 employees with full ramp-up of trailer axles

Transition all CIMC export production over 12-18 mos.

Grow local content of axles to 100% over same time

Enter market for “square” axles for domestic trailers

Lead in higher-tech axles as domestic market matures

Launch component manufacturing for axles assembled in

North America and Europe

Potential future expansion for brakes, wheels and other systems

Potential aftermarket opportunity

Envisioning the Future

14

Agenda

Overview of Company and Results

Envisioning the Future of ArvinMeritor

Performance Plus Success Factors

15

Performance Plus Success Factors

16

Industry challenges

Reason to change

Executive alignment

Agents of change

Clear strategies

Pathway to change

Fast-start actions

Momentum to change

Strong balance sheet

Resources to change

Industry Challenges Provide a

Reason to Change

Reason to Change

Commercial Vehicle Systems

2007 North America Class 8 downturn

Light Vehicle Systems

Lower production at some key customers

Industry margins below historical average

Uneven regional growth rates

Emissions Technologies

Lower production at some key customers

Industry margins below historical average

Higher stainless steel prices

17

OE/Supplier Forecasts

Calendar Year 2007

Average 211

High Est. 250

Low Est. 181

(Thousands of vehicles)

FY2007 = 235K vehicles

FY2008 = 250K vehicles

Q2 Q3 Q4 Q1

CY2007 = 200K Vehicles

North America Class 8 Volumes

85

55

45

50

50

60

70

70

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

65

35

310

220

FY2009

FY2010

Reason to Change

18

North

America

Western

Europe

South

America

Source: CSM Worldwide light vehicle production by region (2006 – 2012)

Central

Europe

Middle East

& Africa

+1.0%

Uneven Regional Growth Rates

Asia

Pacific

Reason to Change

+6.4%

+1.3%

+5.4%

+9%

+3.7%

Global Light Vehicle Production Outlook

19

Factors Affecting Fiscal Q1 Results

European Axle Launch Costs and New ERP System

Strike at VW plant in Brussels

Slightly Higher N.A. Heavy Truck Market

Significantly Reduced Big Three Production

Q1, FY 2007

RED = Decreases

GREEN = Increases

$0.17 EPS from Continuing Operations Before Special Items

Q1, FY 2006

Reason to Change

20

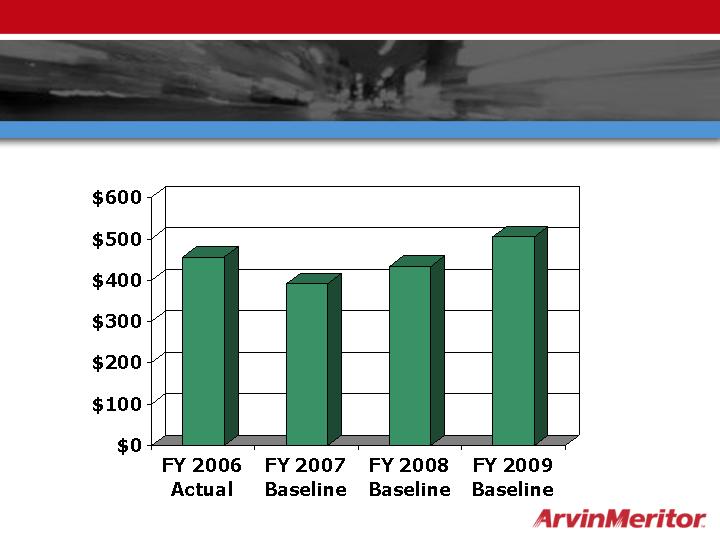

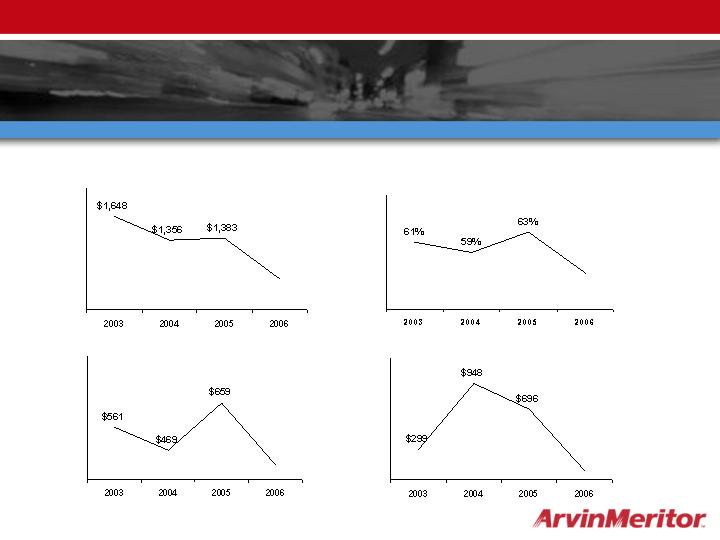

Baseline EBITDA Forecast as of Dec. 7

(Before Performance Plus)

$ Millions Before Special Items

Reason to Change

$456

$375-$405

$410-$455

$475-$535

21

Performance Plus Success Factors

22

Industry challenges

Reason to change

Executive alignment

Agents of change

Clear strategies

Pathway to change

Fast-start actions

Momentum to change

Strong balance sheet

Resources to change

Phil Martens,

President, LVS

H. H. “Buddy” Wacaser,

President, ET

Rob Ostrov,

Sr. VP HR

Jay Craig

VP and

Controller

Carsten Reinhardt,

President, CVS

Strong Leaders to Reshape Our Future

New Leadership Team

Agents of Change

23

New Leaders Drive Performance Plus

J. Craig

P. Martens

P. Martens

J. Craig

C.

Reinhardt

C.

Reinhardt

Aftermarket

Product

Growth

Overhead

Mfg.

ER&D

Materials

Commercial Excellence

Revenue Enhancement

Operational Excellence

Cost Improvements

Steering Committee

J. Craig

J. Donlon

R. Ostrov

C. Reinhardt

P. Martens

Sponsor: R. Ostrov

Talent Excellence

Sponsors: J. Craig and J. Donlon

Program Office

R. Sachdev

Sponsors

Agents of Change

Top Quartile Financial Performance Among Peer Companies

24

Performance Plus Success Factors

25

Industry challenges

Reason to change

Executive alignment

Agents of change

Clear strategies

Pathway to change

Fast-start actions

Momentum to change

Strong balance sheet

Resources to change

Talent Excellence

Pillars of Performance

Pathway to Change

26

Performance Plus Success Factors

27

Industry challenges

Reason to change

Executive alignment

Agents of change

Clear strategies

Pathway to change

Fast-start actions

Momentum to change

Strong balance sheet

Resources to change

Actions Already Underway

Momentum to Change

Category crossover

Expansion of shared services

Reengineering projects for material savings

(e.g., driveline yoke)

Rationalization of engineering footprint

Broadening of remanufacturing

ET restructuring (not included in Performance Plus targets)

28

Light Vehicles

Commercial Vehicles

Growth from Category Cross-Over

Crossing the Boundary

Leverage technology

Utilize capacity

Innovate for leadership

Future State: Eliminate Boundaries

Steel wheels

Car and light truck axles

and modules

DPFs, converters

Window regulators, door

modules

Medium truck wheels

Drive axles

Momentum to Change

Commercial diesel emissions

Truck and specialty vehicle

doors

29

Shared Services

Launched Shared Services pilot program in partnership

with HCL

Twenty Accounts Payable positions moved to Chennai,

India

Achieved two-thirds cost and productivity improvement

Based on success of pilot, ramping up additional activities

throughout 2007

Accounts Receivable, Payroll, Benefits

Boundary-less organization is an enabler

Momentum to Change

30

New Business Wins with Asian

Customers

First Auto Works

Momentum to Change

31

Performance Plus Success Factors

32

Industry challenges

Reason to change

Executive alignment

Agents of change

Clear strategies

Pathway to change

Fast-start actions

Momentum to change

Strong balance sheet

Resources to change

Debt-to-capitalization ratio

(millions)

Term debt due within 5 years

(millions)

Net debt (1)

(millions)

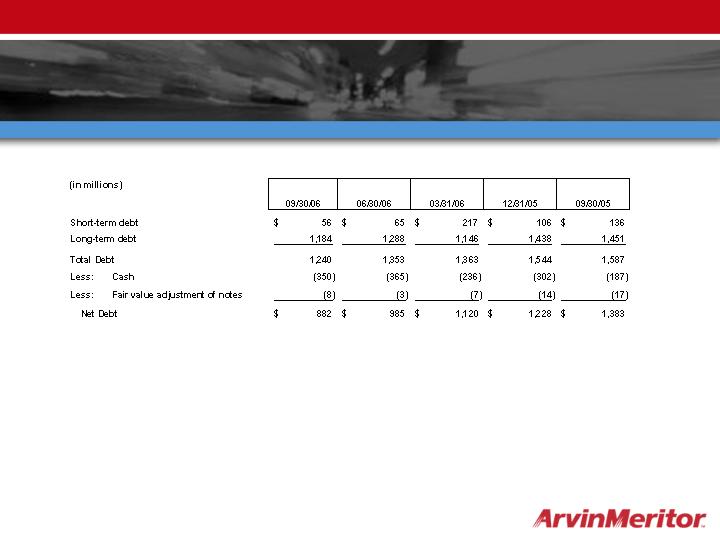

$882

55%

$93

$409

Balance Sheet Strengthening

Resources to Change

(1) See appendix for definition of net debt

33

$39 million

Sold

CVS Off-Highway Brakes

$ 227million

Total Light Vehicle Aftermarket

Other Divestitures

Light Vehicle Aftermarket

N/A

Evaluating

LVS MSSC suspension JV

Sold

Equity share in Purolator India

In Process

N.A. Ride Control

Sold

S. Africa Ride Control

Sold

N.A. Purolator filters

Sold

N.A. Exhaust

In Process

LVA Europe

Sold

N.A. Motion Control

Proceeds

Status

Divestiture Status

Resources to Change

34

Performance Plus Success Factors

Performance Plus will Transform ArvinMeritor into a

Top-Quartile Financial Performer

35

Industry challenges

Reason to change

Executive alignment

Agents of change

Clear strategies

Pathway to change

Fast-start actions

Momentum to change

Strong balance sheet

Resources to change

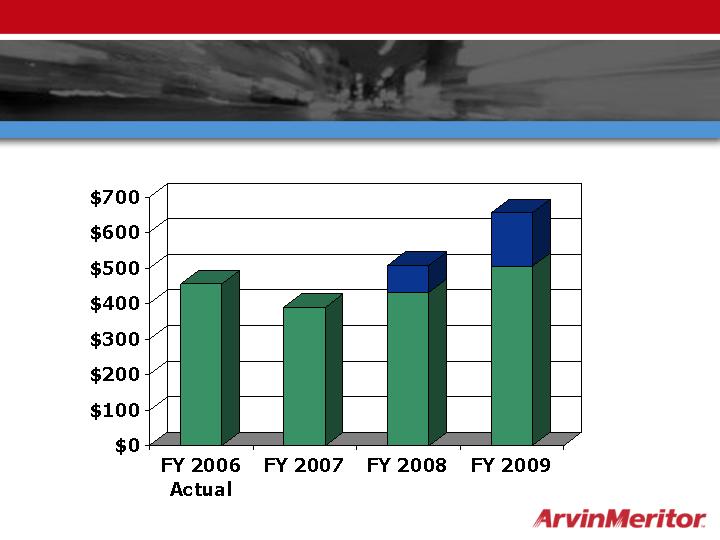

EBITDA with High Confidence

Improvement from Performance Plus

$ Millions Before Special Items

$456

$375-$405

$485-$530

$625-$685

36

Appendix

37

Use of Non-GAAP Financial Information

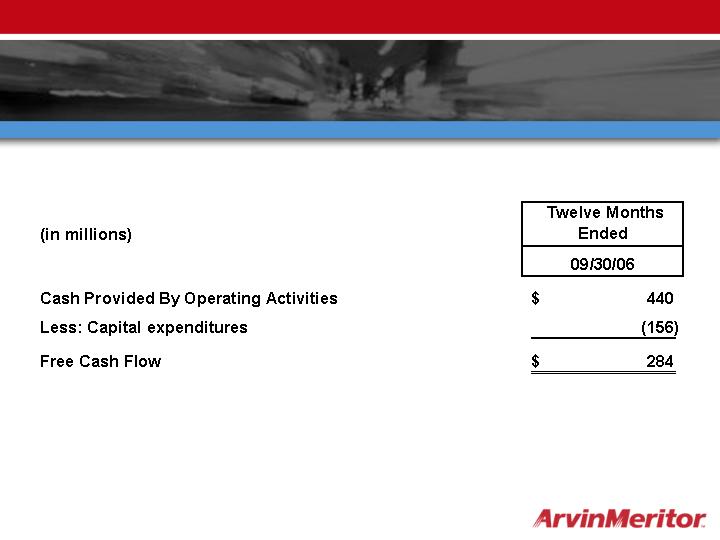

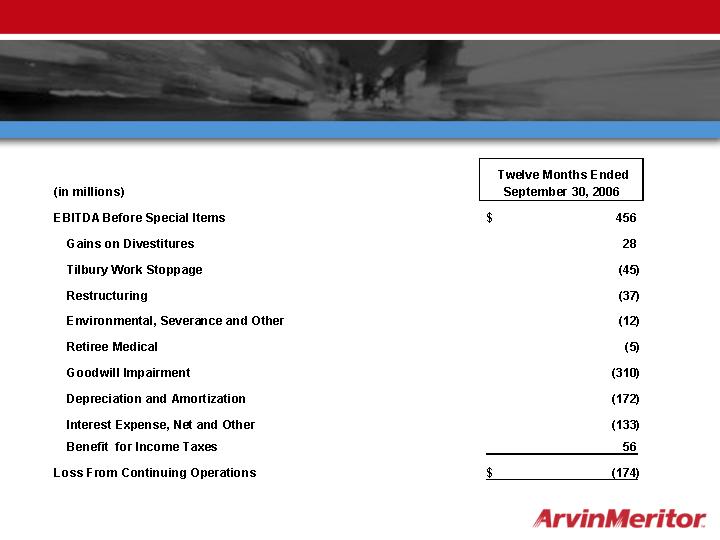

In addition to the results reported in accordance with accounting principles generally accepted in the United States (“GAAP”) included throughout this presentation, the company has provided information regarding income from continuing operations, diluted earnings per share and operating income and margins before special items, which are non-GAAP financial measures. These non-GAAP measures are defined as reported income or loss from continuing operations, reported diluted earnings or loss per share from continuing operations and operating income or loss plus or minus special items. Other non-GAAP financial measures include “EBITDA before special items” and “free cash flow”. EBITDA is defined as earnings before interest, income taxes, depreciation and amortization plus or minus special items. Free cash flow represents net cash provided by operating activities less capital expenditures.

Management believes that the non-GAAP financial measures used in this presentation are useful to both management and investors in their analysis of the Company’s financial position and results of operations. In particular, management believes EBITDA is a meaningful measure of performance as it is commonly utilized by management and investors to analyze operating performance and entity valuation. Management, the investment community and the banking institutions routinely use EBITDA, together with other measures, to measure operating performance in our industry. Management believes that free cash flow is useful in analyzing the Company’s ability to service and repay its debt. Further, management uses these non-GAAP measures for planning and forecasting in future periods.

These non-GAAP measures should not be considered a substitute for the reported results prepared in accordance with GAAP. EBITDA should not be considered as an alternative to net income as an indicator of our operating performance or to cash flows as a measure of liquidity. Free cash flow should not be considered a substitute for cash provided by operating activities or other cash flow statement data prepared in accordance with GAAP or as a measure of liquidity. In addition, the calculation of free cash flow does not reflect cash used to service debt and thus, does not reflect funds available for investment or other discretionary uses. These non-GAAP financial measures, as determined and presented by the company, may not be comparable to related or similarly titled measures reported by other companies.

Set forth on the following slides are reconciliations of these non-GAAP financial measures, if applicable, to the most directly comparable financial measures calculated and presented in accordance with GAAP.

38

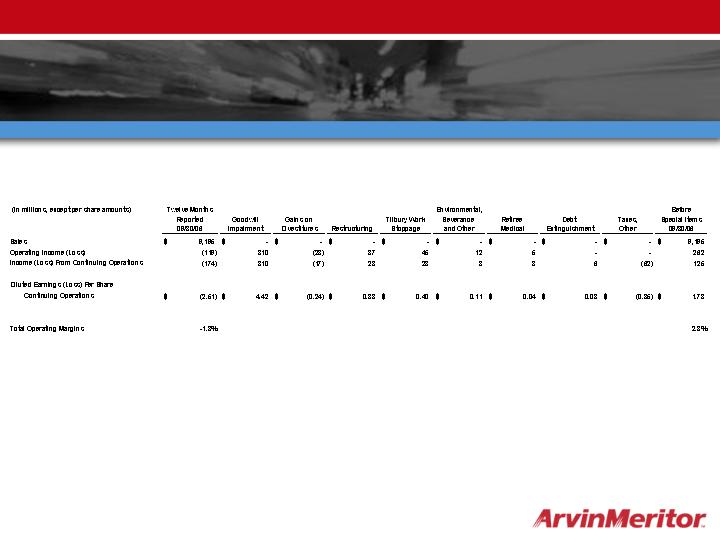

Non-GAAP Financial Information –

Full Year FY 2006 Results Before Special Items

39

Non-GAAP Financial Information –

Free Cash Flow

40

Non-GAAP Financial Information –

EBITDA – Before Special Items

41

Non-GAAP Financial Information –

Net Debt

42