FY 2007 Third Quarter

Earnings Presentation

Chip McClure, Chairman, CEO & President

Jim Donlon, Senior Vice President & CFO

July 30, 2007

1

Forward-Looking Statements

2

This presentation contains statements relating to future results of the company (including certain projections and

business trends) that are “forward-looking statements” as defined in the Private Securities Litigation Reform Act of

1995. Forward-looking statements are typically identified by words or phrases such as “believe,” “expect,”

“anticipate,” “estimate,” “should,” “are likely to be,” “will” and similar expressions. Actual results may differ

materially from those projected as a result of certain risks and uncertainties, including but not limited to global

economic and market cycles and conditions; the demand for commercial, specialty and light vehicles for which the

company supplies products; risks inherent in operating abroad (including foreign currency exchange rates and

potential disruption of production and supply due to terrorist attacks or acts of aggression); availability and cost of

raw materials, including steel; OEM program delays; demand for and market acceptance of new and existing

products; successful development of new products; reliance on major OEM customers; labor relations of the

company, its suppliers and customers, including potential disruptions in supply of parts to our facilities or demand

for our products due to work stoppages; the financial condition of the company’s suppliers and customers,

including potential bankruptcies; possible adverse effects of any future suspension of normal trade credit terms by

our suppliers; potential difficulties competing with companies that have avoided their existing contracts in

bankruptcy and reorganization proceedings; successful integration of acquired or merged businesses; the ability

to achieve the expected annual savings and synergies from past and future business combinations and the ability

to achieve the expected benefits of restructuring actions; success and timing of potential divestitures; potential

impairment of long-lived assets, including goodwill; competitive product and pricing pressures; the amount of the

company’s debt; the ability of the company to continue to comply with covenants in its financing agreements; the

ability of the company to access capital markets; credit ratings of the company’s debt; the outcome of existing and

any future legal proceedings, including any litigation with respect to environmental or asbestos-related matters;

rising costs of pension and other post-retirement benefits and possible changes in pension and other accounting

rules; as well as other risks and uncertainties, including but not limited to those detailed herein and from time to

time in other filings of the company with the SEC. These forward-looking statements are made only as of the

date hereof, and the company undertakes no obligation to update or revise the forward-looking statements,

whether as a result of new information, future events or otherwise, except as otherwise required by law.

Highlights

Earned $0.25 per share from continuing operations before special

items

LVS year-over-year margin expansion continues

CVS profitable in the trough of the 2007 downturn

Completed the sale of Emissions Technologies on May 17

Performance Plus teams on track to achieve goals

FY 2007 EPS guidance before special items of $0.75 to $0.80

compared to $0.70 to $0.80 previously

Cash flow guidance reduced to a range of $50 million to $100

million outflow reflecting working capital investments for growth

outside North America and timing of ET post-closing adjustments

3

Minimizing Impact of the Downturn

Q3 2007 Compared to FY 2001

-1.5 pts

-6.2 pts

CVS operating margin vs. prior year

Reduced CVS margin impact

Improved LVS margins

Expanded global presence

Diversified– less dependent

on North America

Downturn equally severe

+1.1 pts

-1.4 pts

LVS operating margin vs. prior year

+8%

-4%

European truck industry vs. prior year

53%

37%

ARM sales outside North America

-31%

-29%

Class 5-7 vs. prior year

-54%

-48%

Class 8 industry vs. prior year

Q3 2007

FY 2001

Better positioned for 2007 downturn

4

Accomplishments of Performance Plus

Manufacturing footprint improvements underway

Three plant closures announced (Brussels, Frankfurt, St. Thomas)

Two others proceeding in near term

Lean manufacturing implementation underway

Launched ArvinMeritor Production System

Expanding Specialty business

International and Armor Holdings contracts represent 58% of total

MRAP business awarded to date

Growing Commercial Vehicle Aftermarket

Launched trailer axle remanufacturing for North America

Entered significant JV with Chery Motors in China

Light vehicle chassis products produced in Wuhu

$150 million of business by 2010 including door modules and wheels

5

Third Quarter Income Statement from Continuing

Operations – Before Special Items (1)

(1) See Appendix – “Non-GAAP Financial Information”

-43%

$ (0.19)

$ 0.44)

$ 0.25)

Continuing Operations

Diluted Earnings Per Share

-42%

$ (13)

$ 31

$ 18)

Income from Continuing Operations

-25%

(1)

(4)

(5)

Minority Interests

58%

7)

(12)

(5)

Provision for Income Taxes

-40%

(19)

47)

28)

Income Before Income Taxes

4%

1)

(28)

(27)

Interest Expense, Net and Other

0%

-)

10)

10)

Equity in Earnings of Affiliates

-31%

(20)

65)

45)

Operating Income

4%

4

(97)

(93)

SG&A

-15%

(24)

162)

138)

Gross Margin

3%

49

(1,573)

(1,524)

Cost of Sales

-4%

$ (73)

$ 1,735)

$ 1,662)

Sales

%

$

Better/(Worse)

2006

2007

Three Months Ended June 30,

(in millions, except per share amounts)

6

0%

-

(2)

(2)

Unallocated Corporate Costs

-13%

(14)

110)

96)

Segment EBITDA

-29%

(2)

(7)

(9)

ET Corporate Allocations

-16%

$ (16)

$ 101)

$ 85)

Total EBITDA

-0.7 pts

5.8%

5.1%

Total EBITDA Margins

-0.5 pts

6.3%

5.8%

Segment EBITDA Margins

-1.5 pts

7.7%

6.2%

Commercial Vehicle System

1.1 pts

3.8%

4.9%

Light Vehicle Systems (2)

EBITDA Margins

-25%

(22)

87)

65)

Commercial Vehicle System

35%

$ 8)

$ 23)

$ 31)

Light Vehicle Systems

EBITDA

%

$

Better/(Worse)

2006

2007

Quarter Ended June 30,

(in millions)

Segment EBITDA Before Special Items (1)

7

(1)

See Appendix – “Non-GAAP Financial Information”

(2)

Adjusted to reflect the impact of reduced volumes in our Brussels operation

ET Proceeds Received to Date

$ 215

Cash Received to Date

Quarter Ended

June 30, 2007

$ 251

Cash Portion

(59)

Less Note and Assumed Liabilities

(36)

Delayed Closings (1)

$ 40 – $ 60

Memo: Pending Refund of Working Capital

$ 310

Total Consideration

(In millions)

(1) In escrow and expected to close in Q4.

8

Free Cash Flow including Divestiture Proceeds

Free Cash Flow

(42)

-- Continuing Operations

(114)

-- Discontinued Operations

$ 215

ET Proceeds Received to Date

Quarter Ended

June 30, 2007

$ 59

Free Cash Flow including Proceeds

(In millions)

9

Free Cash Flow (1)

30

50

Restructuring and Other

Quarter Ended

June 30,

(32)

(177)

Performance Working Capital (2)

$ 155

$ (156)

Free Cash Flow

78

(114)

Discontinued Operations

63

95

Off Balance Sheet Securitization and Factoring

6

(14)

Pension and Retiree Medical Net of Expense

6

8

Net Spending (D&A less Capital Expenditures)

$ 4

$ (4)

Income (Loss) from Continuing Operations

2006

2007

(1) See Appendix – “Non-GAAP Financial Information”

(2) Change in payables less changes in receivables, inventory and customer tooling

(In millions)

10

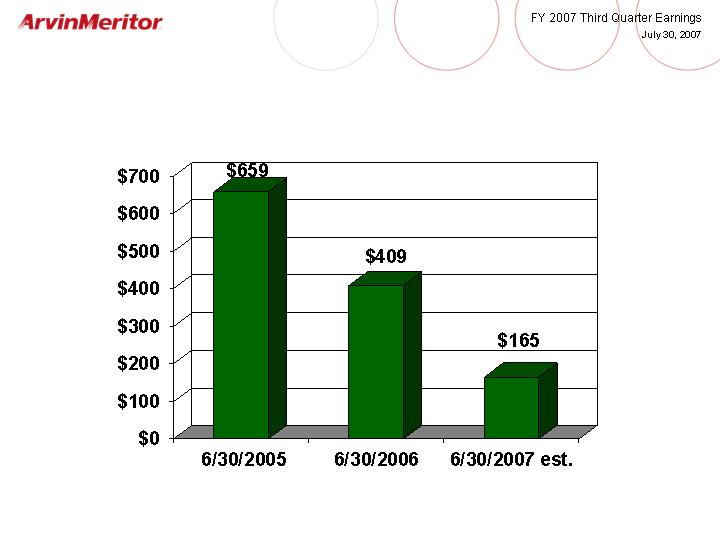

Pension Underfunded Status

(In millions)

11

Fiscal Year 2007 Outlook

Continuing Operations Before Special Items

(100)

(50)

Free Cash Flow

0.80

0.75

Diluted Earnings Per Share

$ 57

$ 54

Income from Continuing

Operations

0%

(4)%

Effective Tax Rate

(110)

(100)

Interest Expense

300

285

EBITDA

$ 6,300

$ 6,200

Sales

FY 2007

Full Year Outlook (1)

(in millions except tax rate and EPS)

(1) Excluding gains or losses on divestitures, restructuring costs, and other special items

12

(1) Excluding gains or losses on divestitures, restructuring costs, and other special items

(0.10)

–

Funding Cost of Working Capital Investments

0.05 – 0.10

100 – 200

ROW Sales Growth

0.05

–

Lower Tax Rate

$6,200 – $6,300

$6,000 – $6,200

Sales

(millions)

$0.75 – $0.80

Updated FY 2007 Guidance Range

$0.70 – $0.80

Previous Guidance

Estimated

EPS (1)

FY 2007 Outlook vs. Prior

Continuing Operations Before Special Items

13

(Thousands of vehicles)

FY2007 = 238K vehicles

FY2008 = 250K vehicles

Q2 Q3 Q4 Q1

CY2007 = 199K Vehicles

89

71

50

60

70

70

Q1

Q2

Q3

Q4

42

310

220

FY2009

FY2010

36

North America Class 8 Volumes

28*

* Previous forecast

14

Why ArvinMeritor?

Strong commercial vehicle volumes

Continuing strong industry in Europe

Continuing rapid growth in Asia and South America

2008-2009 pre-buy in North America

Performance Plus profit improvement plan

$75 million cost reductions by 2008

$150 million cost reductions by 2009

Significant growth initiatives

Continued rapid growth in Asia

New chassis JV and expanded relationship with Chery

Significant expansion of commercial vehicle axle business in India

Strong balance sheet

Track record of reducing leverage and improving liquidity

Positioned for investment opportunities

15

Appendix

16

Use of Non-GAAP Financial Information

In addition to the results reported in accordance with accounting principles generally accepted in the United States (“GAAP”)

included throughout this presentation, the Company has provided information regarding income from continuing operations

and diluted earnings per share before special items, which are non-GAAP financial measures. These non-GAAP measures

are defined as reported income or loss from continuing operations and reported diluted earnings or loss per share from

continuing operations plus or minus special items. Other non-GAAP financial measures include “EBITDA,” “net debt” and

“free cash flow”. EBITDA is defined as earnings before interest, taxes, depreciation and amortization, and losses on sales of

receivables, plus or minus special items. Net debt is defined as total debt less the fair value adjustment of notes due to

interest rate swaps, less cash. Free cash flow represents net cash provided by operating activities less capital expenditures.

Management believes that the non-GAAP financial measures used in this presentation are useful to both management and

investors in their analysis of the Company’s financial position and results of operations. In particular, management believes

that net debt is an important indicator of the Company’s overall leverage and free cash flow is useful in analyzing the

Company’s ability to service and repay its debt. EBITDA is a meaningful measure of performance commonly used by

management, the investment community and banking institutions to analyze operating performance and entity valuation.

Further, management uses these non-GAAP measures for planning and forecasting in future periods.

These non-GAAP measures should not be considered a substitute for the reported results prepared in accordance with

GAAP. Neither net debt nor free cash flow should be considered substitutes for debt, cash provided by operating activities or

other balance sheet or cash flow statement data prepared in accordance with GAAP or as a measure of financial position or

liquidity. In addition, the calculation of free cash flow does not reflect cash used to service debt and thus, does not reflect

funds available for investment or other discretionary uses. EBITDA should not be considered an alternative to net income as

an indicator of operating performance or to cash flows as a measure of liquidity. These non-GAAP financial measures, as

determined and presented by the Company, may not be comparable to related or similarly titled measures reported by other

companies.

Set forth on the following slides are reconciliations of these non-GAAP financial measures, if applicable, to the most directly

comparable financial measures calculated and presented in accordance with GAAP.

17

Announced Plant Closures

Freightliner,

Armor Holdings,

CVA

BMW, GM,

Nissan, Ford/

Land Rover,

Porsche

Volkswagen

Major Customers

Drivelines

Sunroofs and

components

Door systems

Products

17

182

128

Number of Employees

20,000

146,000

103,000

Square Footage

St. Thomas,

Ontario

Frankfurt,

Germany

Brussels,

Belgium

18

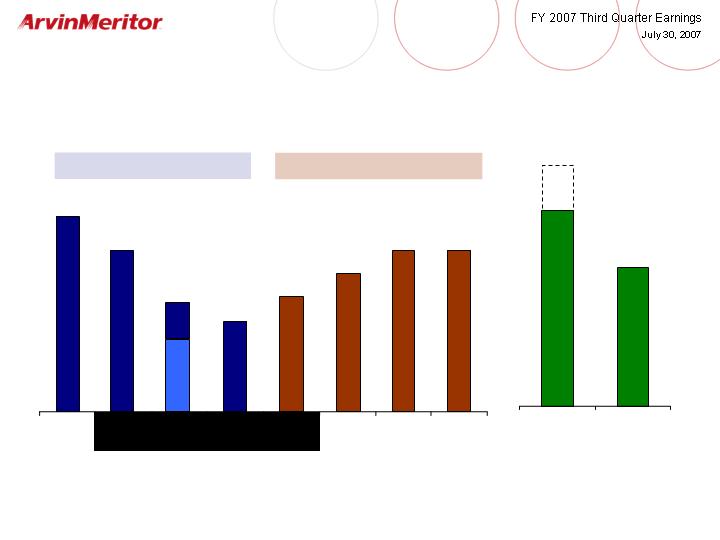

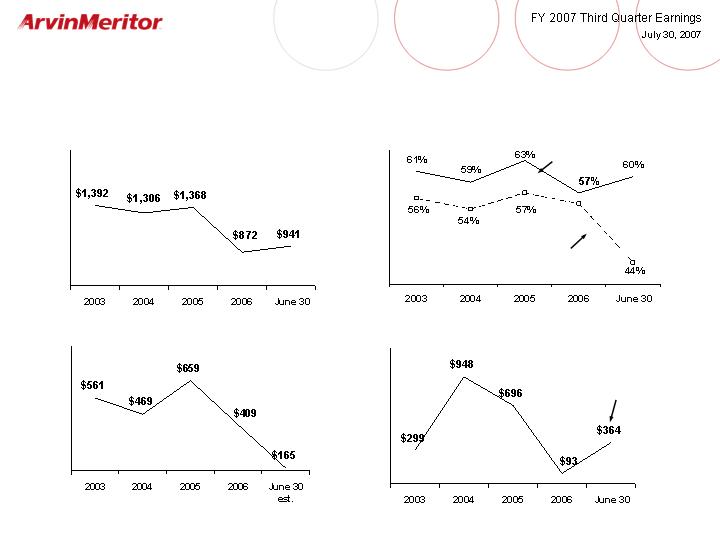

Debt-to-capitalization ratio

Unfunded pension liability

(millions)

Term debt due within 5 years

(millions)

Net debt

(millions)

Balance Sheet Strengthening

Market value

Book value

8-3/4% due

March 2012

19

Non-GAAP Financial Information

Income Statement Special Items Walk 3Q 2007

20

Product

Before

GAAP

Disruptions

Income

Special Items

Q3 2007

and Restructuring

Taxes

Q3 2007

Sales

1,662

$

-

$

-

$

1,662

$

Gross Margin

136

2

-

138

Operating Income

19

26

-

45

Income (Loss) Before Income Taxes

2

26

-

28

Income (Loss) From Continuing Operations

(4)

16

6

18

DILUTED EARNINGS (LOSS) PER SHARE

Continuing Operations

(0.06)

$

0.23

$

0.08

$

0.25

$

Diluted Shares Outstanding

70.8

71.8

71.8

71.8

EBITDA

Light Vehicle Systems

12

$

19

$

-

$

31

$

Commercial Vehicle Systems

63

2

-

65

Segment EBITDA

75

21

-

96

Unallocated Corporate Costs

(7)

5

-

(2)

ET Corporate Allocations

(9)

-

-

(9)

Total EBITDA

59

$

26

$

-

$

85

$

Non-GAAP Financial Information

Income Statement Special Items Walk 3Q 2006

21

Tilbury

Before

GAAP

Work

Taxes,

Special Items

Q3 2006

Stoppage

Sheffield

Restructuring

other

Q3 2006

Sales

1,735

$

-

$

-

$

-

$

-

$

1,735

$

Gross Margin

117

45

-

-

-

162

Operating Income

24

45

(5)

1

-

65

Income Before Income Taxes

6

45

(5)

1

-

47

Income From Continuing Operations

4

28

(3)

1

1

31

DILUTED EARNINGS (LOSS) PER SHARE

Continuing Operations

0.06

$

0.40

$

(0.04)

$

0.01

$

0.01

$

0.44

$

Diluted Shares Outstanding

70.1

70.1

70.1

70.1

70.1

70.1

EBITDA

Light Vehicle Systems

28

$

-

$

(5)

$

-

$

-

$

23

$

Commercial Vehicle Systems

41

45

-

1

-

87

Segment EBITDA

69

45

(5)

1

-

110

Unallocated Corporate Costs

(2)

-

-

-

-

(2)

ET Corporate Allocations

(7)

-

-

-

-

(7)

Total EBITDA

60

$

45

$

(5)

$

1

$

-

$

101

$

Non-GAAP Financial Information

Income Statement Special Items Walk FY 2006

22

Twelve Months

Tilbury

Environmental

Before

Reported

Gains on

Work

Severance

Retiree

Debt

Taxes,

Special Items

9/30/06

Divestitures

Restructuring

Stoppage

and Other

Medical

Extinguishment

other

9/30/06

Sales

6,415

$

-

$

-

$

-

$

-

$

-

$

-

$

-

$

6,415

$

Gross Margin

505

-

-

45

3

5

-

-

558

Operating Income

171

(28)

18

45

12

5

-

-

223

Income Before Income Taxes

72

(28)

18

45

12

5

10

-

134

Income From Continuing Operations

112

(17)

11

28

7

3

6

(57)

93

DILUTED EARNINGS (LOSS) PER SHARE

Continuing Operations

1.60

$

(0.24)

$

0.16

$

0.40

$

0.10

$

0.04

$

0.09

$

(0.81)

$

1.32

$

Diluted Shares Outstanding

70.2

70.2

70.2

70.2

70.2

70.2

70.2

70.2

70.2

EBITDA

Light Vehicle Systems

58

$

(5)

$

13

$

-

$

3

$

-

$

-

$

-

$

69

$

Commercial Vehicle Systems

293

(23)

5

45

3

5

-

-

328

Segment EBITDA

351

(28)

18

45

6

5

-

-

397

Unallocated Corporate Costs

(7)

-

-

-

6

-

-

-

(1)

ET Corporate Allocations

(31)

-

-

��

-

-

-

-

-

(31)

Total EBITDA

313

$

(28)

$

18

$

45

$

12

$

5

$

-

$

-

$

365

$

Non-GAAP Financial Information

3Q EBITDA Reconciliation

23

2007

2006

Total EBITDA - Before Special Items

$ 85

$ 101

Restructuring Costs

(24)

(1)

Product Disruptions

(2)

(45)

Gain on Divestitures

-

5

Loss on Sale of Receivables

(3)

-

Depreciation and Amortization

(32)

(30)

Interest Expense, Net

(27)

(28)

Benefit (Provision) for Income Taxes

(1)

2

Income (Loss) From Continuing Operations

(4)

$

4

$

Quarter Ended

June 30,

Non-GAAP Financial Information

Net Debt

24

(in millions)

Q3

Q2

Q1

Q4

Q3

FY 2007

FY 2007

FY 2007

FY 2006

FY 2006

Short-term Debt

108

$

17

$

137

$

56

$

65

$

Long-term Debt

1,118

1,220

1,174

1,174

1,275

Total Debt

1,226

1,237

1,311

1,230

1,340

Less:

Cash

(284)

(222)

(369)

(350)

(365)

Fair value adjustment of notes

(1)

(8)

(8)

(8)

(3)

Net Debt

941

$

1,007

$

934

$

872

$

972

$

Non-GAAP Financial Information

Free Cash Flow

25

2007

2006

Cash provided by (used for) operating activities

(127)

$

186

$

Less: Capital expenditures (1)

(29)

(31)

Free cash flow

(156)

$

155

$

(1) Includes capital expenditures of discontinued operations.

Three Months Ended

June 30,

26