Exhibit 99a

Deutsche Bank

2007 Leveraged Finance

Conference

Jim Donlon, Executive Vice President and CFO

Mary Lehmann, Sr. VP, Strategic Initiatives, and Treasurer

October 3, 2007

1

Forward-Looking Statements

This presentation contains statements relating to future results of the company (including certain projections and

business trends) that are “forward-looking statements” as defined in the Private Securities Litigation Reform Act of

1995. Forward-looking statements are typically identified by words or phrases such as “believe,” “expect,”

“anticipate,” “estimate,” “should,” “are likely to be,” “will” and similar expressions. Actual results may differ

materially from those projected as a result of certain risks and uncertainties, including but not limited to global

economic and market cycles and conditions; the demand for commercial, specialty and light vehicles for which the

company supplies products; risks inherent in operating abroad (including foreign currency exchange rates and

potential disruption of production and supply due to terrorist attacks or acts of aggression); availability and cost of

raw materials, including steel; OEM program delays; demand for and market acceptance of new and existing

products; successful development of new products; reliance on major OEM customers; labor relations of the

company, its suppliers and customers, including potential disruptions in supply of parts to our facilities or demand

for our products due to work stoppages; the financial condition of the company’s suppliers and customers,

including potential bankruptcies; possible adverse effects of any future suspension of normal trade credit terms by

our suppliers; potential difficulties competing with companies that have avoided their existing contracts in

bankruptcy and reorganization proceedings; successful integration of acquired or merged businesses; the ability

to achieve the expected annual savings and synergies from past and future business combinations and the ability

to achieve the expected benefits of restructuring actions; success and timing of potential divestitures; potential

impairment of long-lived assets, including goodwill; competitive product and pricing pressures; the amount of the

company’s debt; the ability of the company to continue to comply with covenants in its financing agreements; the

ability of the company to access capital markets; credit ratings of the company’s debt; the outcome of existing and

any future legal proceedings, including any litigation with respect to environmental or asbestos-related matters;

rising costs of pension and other post-retirement benefits and possible changes in pension and other accounting

rules; as well as other risks and uncertainties, including but not limited to those detailed herein and from time to

time in other filings of the company with the SEC. These forward-looking statements are made only as of the

date hereof, and the company undertakes no obligation to update or revise the forward-looking statements,

whether as a result of new information, future events or otherwise, except as otherwise required by law.

2

Product Portfolio

Commercial Vehicle Systems

Light Vehicle Systems

3

Customer Base After ET Divestiture

2006 Sales

Commercial Vehicle Customers

Light Vehicle Customers

DaimlerChrysler

8%

General Motors 3%

Volkswagen

7%

Ford 3%

Asian Based

OEMs 4%

BMW 1%

Other LVS 7%

Other CVS

22%

Fiat 2%

Asian Based

OEMs 4%

Ford 1%

Volkswagen 1%

General Motors 1%

PACCAR 2%

International

5%

Volvo 17%

DaimlerChrysler

12%

67%

Commercial

Vehicle

33%

Light

Vehicle

4

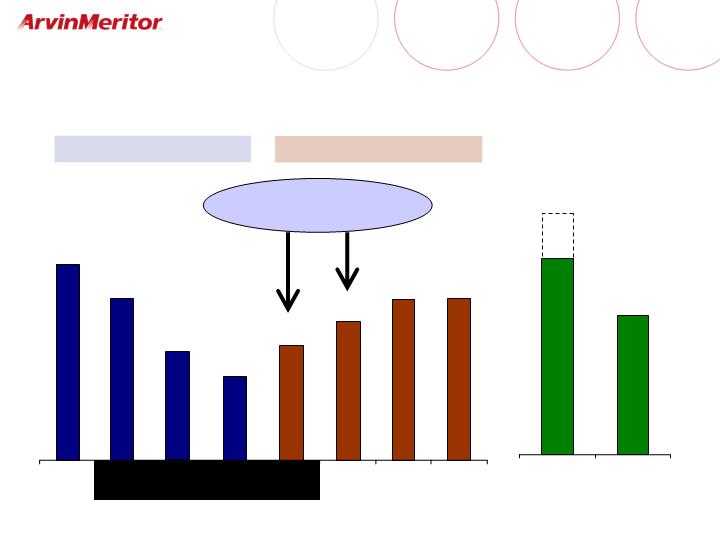

Scorecard of Downturn Offsets

Slide from June 2006 showing expected offsets to N.A. Class 8 downturn

Layered Capacity

Emerging Markets

High-Volume Premium Reduction

CVA Growth

Specialty Vehicle Market

CVE Growth

Trailer Productivity

Conversion @ 15%-20% ($45M) – ($60M)

Other Markets ~($15M)

30-35% ~($300M)

Exposure to Class 8: 11% of $8.8B ~ $900M

2007 Outcome

½

Volume shortfall

Sold Emissions

Industry contracted

Migrated to Europe

Exceeded

As estimated

June 2006

5

Credit Crunch Affects Aftermarket, Trailers and

OE Truck Sales

Scarce funding

exacerbates already poor

new home sales.

The demand for aftermarket

truck components declines as

ton-miles remain weak.

Trailer sales also suffer.

The volume of building

materials, landscaping

materials, appliances

and furniture being

shipped is down.

Class 8 truck downturn lasts

longer, and mix favors owner-

operators over large fleets.

About 20% of

all freight is

related to new

housing

construction

6

Truck Tonnage Index

Seasonally adjusted monthly index, 2000 = 100.0

Jan

2006

Apr

2006

Jul

2006

Oct

2006

Jan

2007

Apr

2007

Freight volumes were weak even before credit crunch

Source: ATA

Jul

2007

July down 4% vs July 2006

Below year-ago 12 of last 13 months

July CYTD down 3% vs 2006

August and September weaker

7

2007 CY U.S. Trailer Sales Forecast

Total U.S. trailer industry builds

Actual

September Forecast

January Forecast

Source: ACT Research

Trailer weakness continues to surprise industry analysts

August Forecast

11% miss

Lowered by 8%

one month later

8

Class 8 Truck Net New Orders

2006

2007

2005

Source: ACT Research

New order intake for heavy trucks has been weak

9

FY2007 = 224K vehicles

FY2008 = 250K vehicles

Q2 Q3 Q4 Q1

CY2007 = 185K Vehicles

89

71

50

60

70

70

Q1

Q2

Q3

Q4

42

310

220

FY2009

FY2010

36

Class 8 Production Likely to Recover Later

(Thousands of vehicles)

Downward pressure

10

Unfavorable Sales Mix

Class 8 Registrations July YTD

32%

24%

For-hire Carriers

All Other

For-hire freight carriers (where ARM share is greatest) affected most

Source: R.L. Polk

Total registrations 30% lower

2006

2007

11

Europe Medium & Heavy Truck Production

Thousands of vehicles, fiscal quarters

Nov. 2006 Forecast

Preliminary Actual

Source: Internal estimates

Europe truck volumes have taken OEMs and suppliers off-guard

FY Actual

510

FY Forecast

419

22% Surprise

15%

20%

15%

47%

12

Premium freight

CVS Europe Supply Constraints

Western

European

Suppliers

ArvinMeritor

Eastern

European &

Asian

Suppliers

Components

Systems

Assembly

Vehicle

Assembly

Capacity

Constrained

Capacity

Constrained

Capacity

Constrained

Premium freight

Scheduling

Challenged

Late changes

Qualify new

suppliers

Capacity

Constrained

Premium freight

Premium freight

Scheduling

Challenged

Capacity

Investments

Lean manu-

facturing

13

Revised Outlook for 2007

Earnings Per Share

EPS Impact

2008

2007

Element

None

($0.20)

Non-recurring items in Q4

- Supplier reorganizations

- German tax law change

1H flowthrough

($0.20)

Ongoing operational issues

- Weak U.S. economy

- Supply shortages in Europe

14

2008 Guidance Compared to 2007

Diluted EPS for Continuing Operations Before Special Items

0.25 - 0.35

Performance Plus product & growth actions

including improved customer terms

0.10 - 0.15

Pension and retiree medical

(0.20) - (0.30)

1H flowthrough of Q4 operational issues

(0.10) - (0.20)

North America CVS net volume and mix

0.70 - 0.75

Performance Plus cost savings

$1.40 - $1.60

FY 2008 Guidance

$0.75 - $0.80

July 30, 2007 Guidance – FY 2007

15

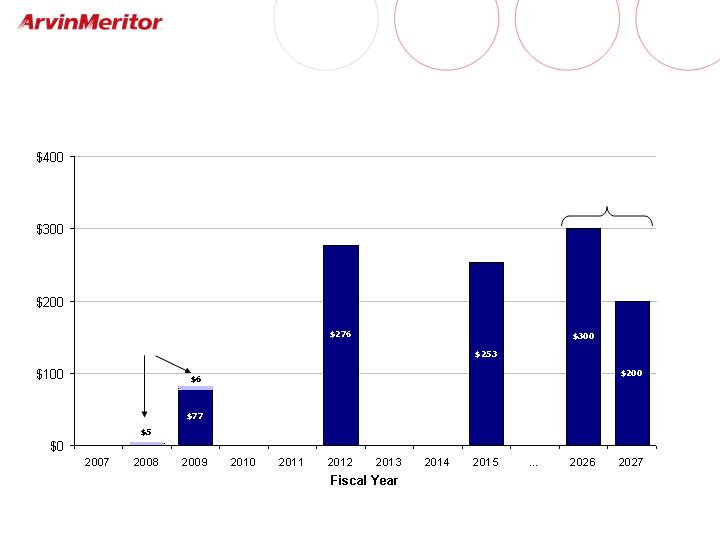

Convertible

Newest

Issue

Term Debt Profile

(Maturities in millions)

Defeased

16

Retiree Healthcare

June 30, 2007 estimate

Unfunded Position: ��

$587 million

Disputed

Amount

$168

UAW

Plants

$447

Salaried

and Other

$140

Annual spend:

$50-$55 million

expense and

cash

17

Medium-term Investment Thesis Intact

Strong commercial vehicle volumes

Solid 2H 2008 in North America, followed by 2009 pre-buy

Continuing strong industry in Europe, with improving ability

to capitalize

Continuing rapid growth in Asia

Performance Plus profit improvement plan

$75 million cost reductions in 2008 and $150 million in 2009

Significant growth initiatives

Solid balance sheet

No significant near-term maturities of term debt

Short-term credit line covenant relief granted

18