LVS Spinoff Update -

Arvin Innovation (ARVI)

May 28, 2008

Jim Donlon

Designated CFO, Arvin Innovation

Jay Craig

CFO, ArvinMeritor

Mary Lehmann

SVP, Strategic Initiatives, and

Treasurer, ArvinMeritor

1

Forward-Looking Statements

This presentation contains statements relating to future results of the company (including certain projections and

business trends) that are “forward-looking statements” as defined in the Private Securities Litigation Reform Act of

1995. Forward-looking statements are typically identified by words or phrases such as “believe,” “expect,” “anticipate,”

“estimate,” “should,” “are likely to be,” “will” and similar expressions. In addition, there are risks and uncertainties

relating to the planned spinoff of ArvinMeritor’s Light Vehicle Systems business, including the timing and certainty of

completion of the transition. Actual results may differ materially from those projected as a result of certain risks and

uncertainties, including but not limited to global and regional economic and market cycles and conditions; the demand

for commercial, specialty and light vehicles for which the company supplies products; risks inherent in operating abroad

(including foreign currency exchange rate volatility and potential disruption of production and supply due to terrorist

attacks or acts of aggression); availability and sharply rising cost of raw materials, including steel and oil and our ability

to recover steel and other commodity price increases from our customers; rising transportation costs; our ability to

implement additional productivity and cost reduction initiatives and our ability to achieve the expected benefits of past

and future restructuring actions; OEM program delays; demand for and market acceptance of new and existing

products; successful development of new products; reliance on major OEM customers; reduced sales to key

customers; changes in operations, reduced production volumes and changes in product mix and market share of our

OEM customers; competitive product and pricing pressures; labor relations of the company, its suppliers and

customers, including potential disruptions in supply of parts to our facilities or demand for our products due to work

stoppages; the financial condition of the company’s suppliers and customers, including potential bankruptcies; possible

adverse effects of any future suspension of normal trade credit terms by our suppliers; potential difficulties competing

with companies that have avoided their existing contracts in bankruptcy and reorganization proceedings; success and

timing of potential divestitures; potential impairment of long-lived assets, including goodwill; successful integration of

acquired or merged businesses; potential adjustment of the value of deferred tax assets; the amount of the company’s

debt; the ability of the company to continue to comply with covenants in its financing agreements; the ability of the

company to access capital markets; credit ratings of the company’s debt; the outcome of existing and any future legal

proceedings, including any litigation with respect to environmental or asbestos-related matters; product liability and

warranty and recall claims; rising costs of pension and other post-retirement benefits and possible changes in pension

and other accounting rules; as well as other risks and uncertainties, including but not limited to those detailed from time

to time in filings of the company with the SEC. These forward-looking statements are made only as of the date hereof,

and the company undertakes no obligation to update or revise the forward-looking statements, whether as a result of

new information, future events or otherwise, except as otherwise required by law.

2

Form 10 Process

We filed a Form 10 for Arvin Innovation on May 28, 2008.

After expected review by the Securities and Exchange

Commission, we will be filing amendments with updated

information.

3

Highlights of Spinoff

ArvinMeritor to spin off its Light Vehicle Systems segment

to shareholders

ArvinMeritor to continue as a commercial vehicle systems

supplier

Spinoff represents a major step in corporate transformation

Improves corporate clarity and management focus

Allows each company to reach its full shareholder value

potential

Allows holders to invest selectively

De-couples risk profiles

Improves customer dynamics

Unlocks shareholder value and increases focus

4

Terms of the Spinoff

Spinoff expected to be implemented through a pro rata tax-free stock

dividend to ArvinMeritor shareholders

Upon completion, ARM shareholders will own 100% of both

companies

Spinoff expected to be completed within the next 12 months

Subject to market conditions and regulatory and other customary

approvals

New company has applied to be listed as ARVI on the NASDAQ stock

exchange

Transaction time line:

FY 2008 Q3 Q4 FY 2009

Announce

File Form 10

Update the Market

Spinoff Effective

5

ARVI Investment Thesis

Global supplier with $2.1 billion of value-added sales(1)

Specialized in Body and Chassis Systems

Over 60% of revenue derived outside North America

Diverse and robust business portfolio

Global manufacturing with an expanding LCC footprint

Great brands and business building blocks

Strong book of business benefiting from emerging

market growth

Experienced and respected management team

Margin expansion from an improving cost structure

Positioned to win in the global automotive industry

(1)

Value-added sales are defined to be total sales less pass-through sales. In 2007, LVS had value-added sales including sales to affiliated companies of $2.1 billion and pass-through sales of approximately $200 million.

6

ARVI Targeted Revenue Growth

$2.3 billion of revenues in 2007 projected to grow

to $2.7 - $2.9 billion by 2010(1)

95% of assumed new business already awarded:

Global sunroof program

Global latch program

Global door module

New medium-duty wheels business

Chery business projected to grow to $150

million

Net of run-off of old business at low margins

Projected 7 – 10% annual growth rate over first two years

(1)

Based on management assumptions regarding pricing, currency exchange rates, volume and timing of vehicle production, option mix, and other factors not in the control of management.

7

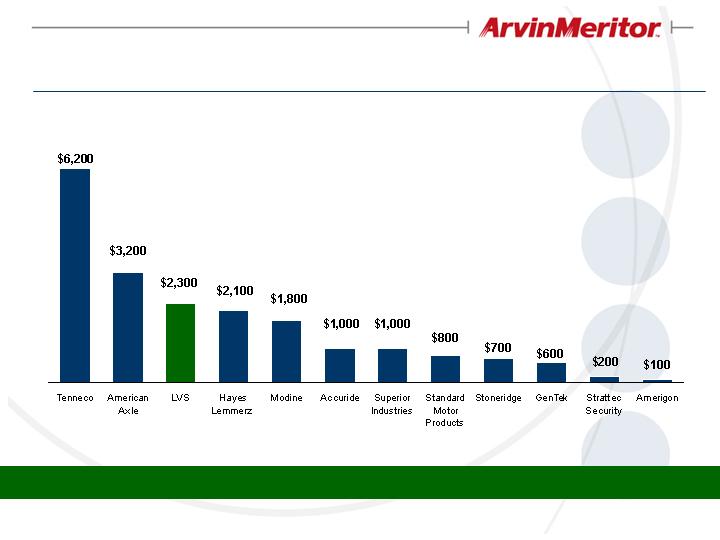

U.S. Public Comparable Suppliers

ARVI will have more than sufficient scale to compete effectively

(millions)

2007 Sales

8

Primary Competitors

Door and Access Control Systems

Brose, Intier, Kiekert, Mitsui, Valeo,

Aisin, Grupo Antolin

Roof Systems

Webasto, Inalfa, Aisin

Body Systems

Chassis Systems

Suspension Systems and Modules

ZF, Thyssen-Krupp, Delphi, Visteon,

TRW, Tenneco, Benteler, NHK Spring,

San Luis Rassini, Mubea, Sogefi

Ride Control

Tenneco, Kayaba, Sachs

Wheels

Hayes-Lemmerz, Topy, Accuride, CMW

Strong, established competitive position

9

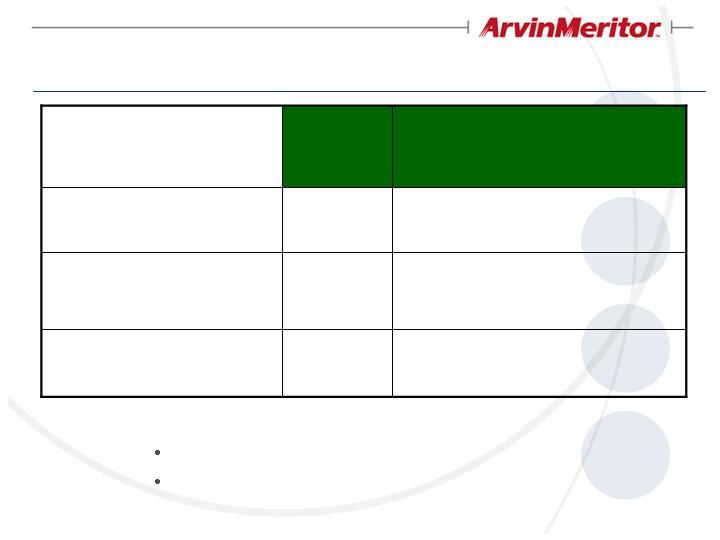

-

(10)

-

(21)

$ 35

15

$ 20

LVS

Form 10

$ (1)

-

$ (1)

Form 10

Adjustment

$ 14

$ (6)

$ 21

Total Segment EBITDA

15

-

15

Restructuring Costs

Selected Items Included Above

(3)

(6)

(18)

21

$ (6)

Preliminary

Pro Forma

Adjustmts(2)

(3)

Other Transferred Liabilities

-

Corporate Allocations

LVS Pro

Forma

LVS

Segment(1)

(millions)

(16)

Pension/OPEB

(18)

Stand-Alone Costs

$ 29

$ 36

EBITDA Before Special Items(3)

2008 1H Pro Forma EBITDA Bridge

(1)

Actual results are on the basis of the LVS segment of ArvinMeritor, Inc. and are not on the basis of LVS as a separate, stand-alone entity. Financial results for the LVS segment of ArvinMeritor will differ from, and may not be indicative of, the results of operations and financial position LVS would have had if it had operated as a separate, stand-alone entity during those periods.

(2)

See “Unaudited Pro Forma Combined Condensed Financial Statements in the Form 10 filed with the SEC on May 28, 2008. This pro forma information is for illustrative and informational purposes only and is not necessarily indicative of our performance or financial position had we been a separate, stand-alone entity at that date or of our future performance or financial position.

(3)

See Appendix – “Non-GAAP Financial Measures.”

10

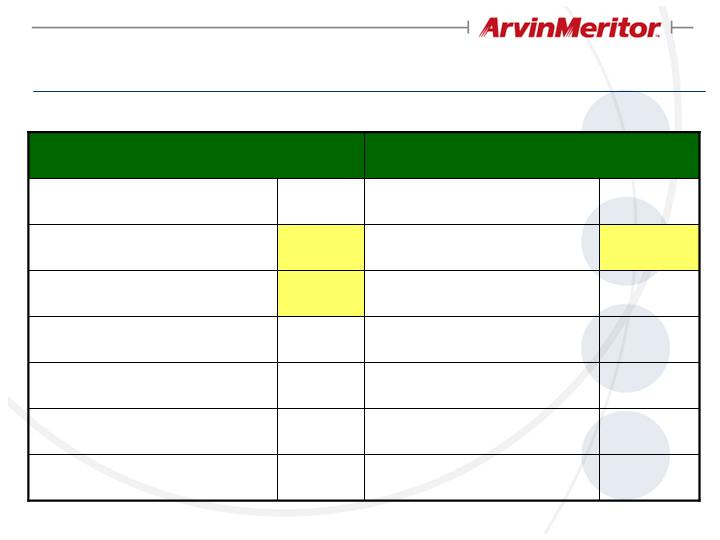

5

-

5

ET Corporate Allocations

(2)

-

(2)

Changes to Certain Benefit Programs

2008

Better/Worse

Than 2007

2007

1H

2008

1H

LVS Segment Results (millions)(1)

5

(5)

-

Adjustments to Pricing Reserves

2

-

2

Commercial Settlement with Supplier

$ 9

$ 41

$ 50

Adjusted EBITDA on Comparable Basis

9

-

9

Legal/Commercial Dispute with Customer

$ (10)

$ 46

$ 36

EBITDA Before Special Items as Reported (2)

2008 Progress on Underlying Profitability

(1)

Actual results are on the basis of the LVS segment of ArvinMeritor, Inc. and are not on the basis of LVS as a separate, stand-alone entity.

Financial results for the LVS segment of ArvinMeritor will differ from, and may not be indicative of, the results of operations and financial position LVS would have had if it had operated as a separate, stand-alone entity during those periods.

(2)

See Appendix – “Non-GAAP Financial Information”

11

ARVI To Be Positioned Solidly

Expected to launch with $100 million of cash

Includes $50 million to fund current liabilities

Expected to launch with approximately $125 million of debt

Initially drawn portion of $200 - $250 million borrowing arrangements

Low leverage ratio

Manageable interest expense

$25 million net debt(1) at launch expected to rise modestly over first quarter

of operation

We may consider placing more debt in ARVI if conditions of financial

markets allow

Unfunded pension/OPEB liabilities of $209 million

Other transferred net liabilities of $32 million

Expected payment to ARM reflecting cash in excess of $100 million

Credit profile expected to be comparable to ARM’s

(1)

Net debt equals $125 million of expected debt less $100 million of expected cash.

12

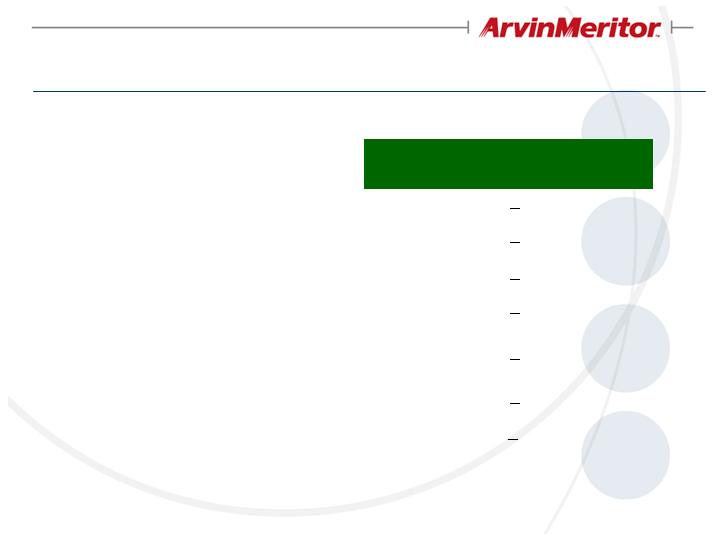

Transfer of Liabilities and Assets

(1)

6

6

-

Asbestos Liabilities, Net(2)

(1)

14

14

-

Environmental Liabilities

(1)

12

12

-

Other Employee Matters(2)

$ (6)

$ 209

$ 57

$ 152

Pension (Unfunded PBO) &

Retiree Medical (APBO)

$ (9)

$ 241

$ 89

$ 152

Total

Memo: 1H

EBITDA

Change

LVS Pro

Forma(1)

Preliminary

Amount

Transferred

at Spin

LVS

Form 10

Funded Status as of June 30, 2007 or

Net Liability as of March 31, 2008

(millions)

Enables lower-risk funding plan with less debt

(1)

See “Unaudited Pro Forma Combined Condensed Financial Statements in the Form 10 filed with the SEC on May 28, 2008. This pro forma information is for illustrative and informational purposes only and is not necessarily indicative of our performance or financial position had we been a separate, stand-alone entity at that date or of our future performance or financial position.

(2)

See Slide 18 for breakout of assets and liabilities.

13

ARM Leverage

Management’s intention is to

maintain leverage at current level or

lower

2008 fiscal year guidance of $390-

410 million before spinoff and pro

forma adjustments and continuing

improvement thereafter

Expected to be reduced after cash

payment from Arvin Innovation

Comments

318(1)

Trailing Twelve Months

EBITDA Before Special Items

March 31,

2008

(millions except ratio)

4.1x

Debt-to-EBITDA Ratio

$ 1,299

Debt

Debt Reduction Opportunities:

On balance sheet securitization ($125 million)

February 2009 debt maturity ($77 million)

(1)

See Appendix – “Non-GAAP Financial Information”

14

2008 Planning Assumptions

Calendar Year Basis

Other Regions/Metrics

North America

580-590

Europe medium & heavy

truck production (000)

220-240

Class 8 truck production

(000)

1,340

Asia medium & heavy

truck production (000)

195-210

Trailer production (000)

180-195

Europe trailer production

160-175

Class 5-7 truck production

(000)

17.1

W. Europe light vehicle

industry sales (millions)

15.2

U.S. light vehicle industry

sales (millions)

4.0

S. America light vehicle

production (millions)

14,200

MRAP production

Much

Worse

Steel price change

Flat

CV aftermarket industry

growth rate ex. pricing

1.6%

Europe GDP growth

1.4%

U.S. GDP growth

15

Fiscal Year 2008 Outlook

Continuing Operations Before Special Items

$ (125)

$ (75)

Free Cash Flow

1.60

1.40

Diluted Earnings Per Share

$ 118

$ 104

Income from Continuing

Operations

26%

22%

Effective Tax Rate

(100)

(90)

Interest Expense

410

390

EBITDA

$ 7,300

$ 7,100

Sales

FY 2008

Full Year Outlook (1)

(in millions except tax rate and EPS)

(1) Excluding gains or losses on divestitures, restructuring costs, and other special items

16

Appendix

17

Transfer of Liabilities and Assets

(6)

44

(50)

-

Asbestos

(14)

-

(14)

-

Environmental Liabilities

(12)

2

(14)

-

Other Employee Matters

$ (209)

$ 3

$ (60)

$ (152)

Pension (Unfunded PBO) &

Retiree Medical (APBO)

$ (241)

$ 49

$(138)

$ (152)

Total

LVS Pro

Forma(2)

Assets(1)

Liabilities

Assumed

LVS

Form 10

Funded Status as of June 30, 2007 or

Net Liability as of March 31, 2008

(millions)

(1)

Including indemnifications and contractual pass-through of recoveries.

(2)

See “Unaudited Pro Forma Combined Condensed Financial Statements in the Form 10 filed with the SEC on May 28, 2008. This pro

forma information is for illustrative and informational purposes only and is not necessarily indicative of our performance or financial position had we been a separate, stand-alone entity at that date or of our future performance or financial position.

18

Use of Non-GAAP Financial Information

Included in this presentation, the Company has provided information regarding segment EBITDA. ArvinMeritor uses

Segment EBITDA as the primary basis for the chief operating decision maker to evaluate the performance of each of the

company’s reportable segments. Segment EBITDA is defined as Income (Loss) from Continuing Operations before interest,

tax, depreciation and amortization and losses on sales of receivables. This presentation also includes Segment EBITDA

before special items (BSI). Segment EBITDA before special items is defined as Segment EBITDA plus or minus special

items.

Management believes that the non-GAAP financial measures used in this presentation are useful to both management and

investors in their analysis of the Company’s financial position and results of operations. Segment EBITDA is a meaningful

measure of performance commonly used by management, the investment community and banking institutions to analyze

operating performance and entity valuation. Further, management uses these non-GAAP measures for planning and

forecasting in future periods.

These non-GAAP measures should not be considered a substitute for the reported results prepared in accordance with

GAAP. Segment EBITDA should not be considered an alternative to operating income as an indicator of operating

performance or to cash flows as a measure of liquidity. These non-GAAP financial measures, as determined and presented

by the Company, may not be comparable to related or similarly titled measures reported by other companies.

Set forth on the following slide are reconciliations of Income (Loss) from Continuing Operations as reported in the

company’s Form 10-Q and Arvin Innovation’s Form 10 filed May 28, 2008 to Segment EBITDA before special items.

19

Non-GAAP Financial Information

EBITDA Before Special Items

(1)

See Slide 19 – “Non-GAAP Financial Information”

2008

2007

Total LVS Segment EBITDA - BSI (1)

36

$

46

$

Ride Control Fair Value Adjustment

-

10

Product Disruptions

-

(5)

Restructuring

(15)

(29)

Total LVS Segment EBITDA - Reported (1)

21

$

22

$

Six Months Ended March 31,

(1) Actual results are on the basis of the LVS segment of ArvinMeritor, Inc. and are

not on the basis of LVS as a separate, stand-alone entity. Financial results for the

LVS segment of ArvinMeritor will differ from, and may not be indicative of, the results

of operations and financial position LVS would have had if it had operated as a

separate, stand-alone entity during those periods.

20

Non-GAAP Financial Information

EBITDA Reconciliation

(1)

See Slide 19 – “Non-GAAP Financial Information”

Six Months Ended

March 31, 2008

Total EBITDA - Form 10

20

$

Loss on Sale of Receivables

(2)

Depreciation and Amortization

(31)

Interest Expense, net

(1)

Provision for Income Taxes

(8)

Loss from Continuing Operations

(22)

$

21

Non-GAAP Financial Information

EBITDA Reconciliation for Trailing Twelve Months

(1)

See Slide 19 – “Non-GAAP Financial Information”

Q3

Q4

Q1

Q2

Total EBITDA - BSI

85

$

47

$

82

$

104

$

318

$

Restructuring Costs

(24)

(10)

(10)

(5)

(49)

Supplier Reorganizations

-

(10)

-

-

(10)

Product Disruptions, Work Stoppages, and Other (1)

(2)

(2)

-

-

(4)

Loss on Sale of Receivables

(3)

(3)

(4)

(5)

(15)

Depreciation and Amortization

(32)

(33)

(32)

(36)

(133)

Interest Expense, Net

(27)

(22)

(27)

(20)

(96)

Benefit (Provision) for Income Taxes

(1)

10

(10)

(14)

(15)

Income (Loss) from Continuing Operations

(4)

$

(23)

$

(1)

$

24

$

(4)

$

(1) Primarily related to impact of production disruptions caused by work stoppages at a facility of one of our customers.

FY 2007

FY 2008

Trailing 12

Months

22