Deutsche Bank 2009

Leveraged Finance

Conference

September 30, 2009

Jay Craig

Senior Vice President and CFO

Forward-Looking Statements

This presentation contains statements relating to future results of the company (including certain projections and business trends) that are

“forward-looking statements” as defined in the Private Securities Litigation Reform Act of 1995. Forward-looking statements are typically

identified by words or phrases such as “believe,” “expect,” “anticipate,” “estimate,” “should,” “are likely to be,” “will” and similar expressions.

There are risks and uncertainties relating our ability to obtain any needed waiver or amendment to our credit agreement if needed in the future;

our ability to achieve anticipated or continued cost savings from reduction actions; and our ability to execute the Company’s announced plans

for the Body Systems and Chassis Systems businesses of LVS, including the timing and certainty of completion or the terms upon which any

sale agreement with respect to any portion of the business may be made and the amount of any exit costs. In addition, actual results may differ

materially from those projected as a result of certain risks and uncertainties, including but not limited to global economic and market cycles and

conditions, including the recent global economic crisis; whether we will have sufficient liquidity as we continue to be affected by declining vehicle

production volumes; the financial condition of the company’s suppliers and customers, including bankruptcies; possible adverse effects of any

future suspension of normal trade credit terms by our suppliers; the ability of the company to continue to comply with covenants in its financing

agreements; the ability of the company to access capital markets; credit ratings of the company’s debt; the demand for commercial, specialty

and light vehicles for which the company supplies products; risks inherent in operating abroad (including foreign currency exchange rates and

potential disruption of production and supply due to terrorist attacks or acts of aggression); availability and rising cost of raw materials, including

steel and oil; OEM program delays; demand for and market acceptance of new and existing products; successful development of new products;

reliance on major OEM customers; labor relations of the company, its suppliers and customers, including potential disruptions in supply of parts

to our facilities or demand for our products due to work stoppages; potential difficulties competing with companies that have avoided their

existing contracts in bankruptcy and reorganization proceedings; successful integration of acquired or merged businesses; the ability to achieve

the expected annual savings and synergies from past and future business combinations and the ability to achieve the expected benefits of

restructuring actions; potential impairment of long-lived assets, including goodwill; potential adjustment of the value of deferred tax assets;

competitive product and pricing pressures; the amount of the company’s debt; the outcome of existing and any future legal proceedings,

including any litigation with respect to environmental or asbestos-related matters; the outcome of actual and potential product liability and

warranty and recall claims; rising costs of pension and other post-retirement benefits and possible changes in pension and other accounting

rules; as well as other risks and uncertainties, including but not limited to those detailed from time to time in filings of the company with the

SEC. These forward-looking statements are made only as of the date hereof, and the company undertakes no obligation to update or revise the

forward-looking statements, whether as a result of new information, future events or otherwise, except as otherwise required by law.

All earnings per share amounts are on a diluted basis. The company's fiscal year ends on the Sunday nearest Sept. 30, and its fiscal quarters

end on the Sundays nearest Dec. 31, March 31 and June 30. All year and quarter references relate to the company's fiscal year and fiscal

quarters, unless otherwise stated.

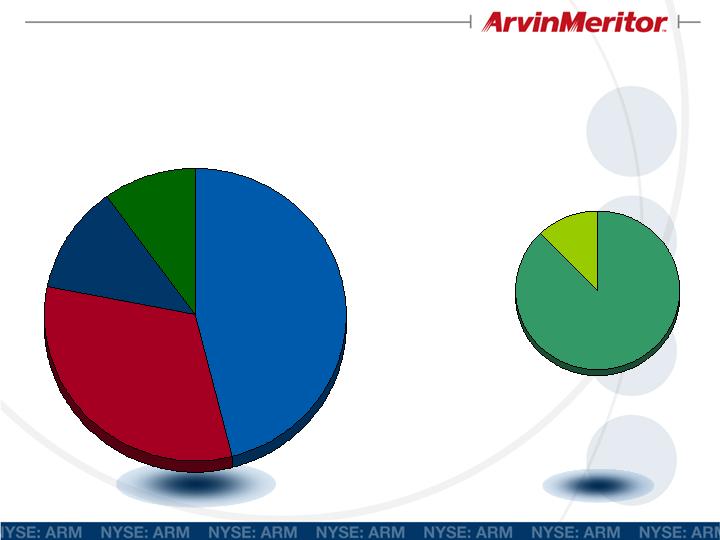

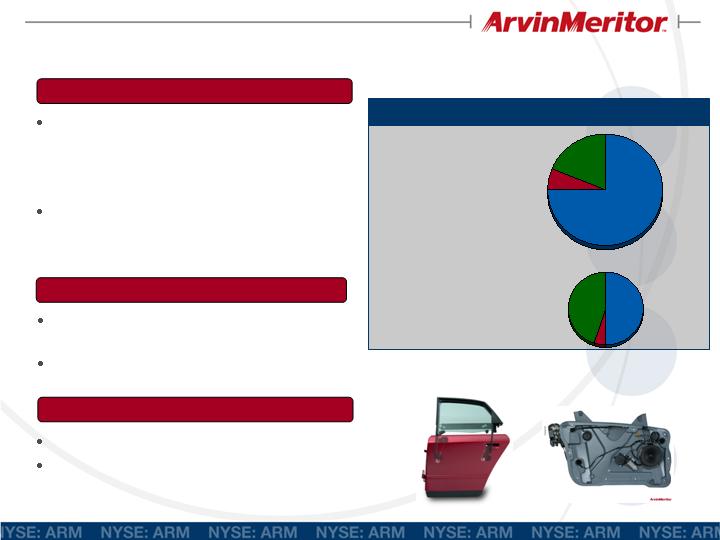

Diverse Business Portfolio

Based on2008 Sales

North

America

46%

Europe

32%

South

America

12%

Asia

Pacific

10%

CVS

Body

88%

$4.8 Billion

$1.6 Billion

LVS

Chassis

Remaining

12%

ü

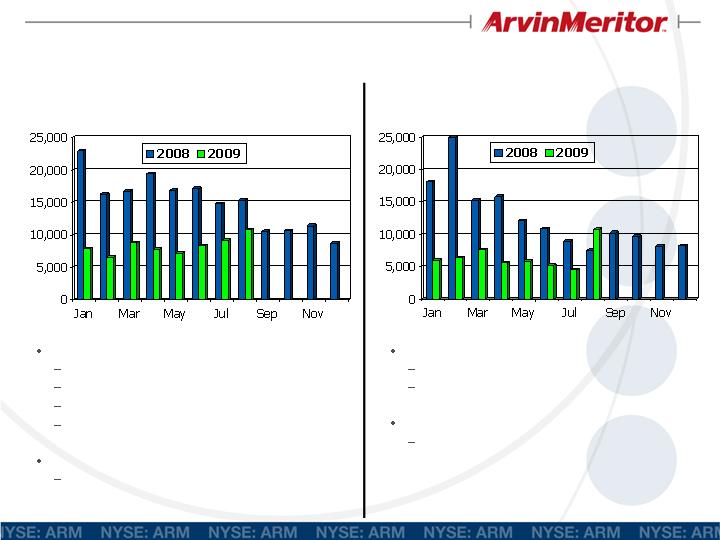

Truck Net Orders by Month

North America

August 2009 : 10,740

Highest heavy truck net orders in nine months

17% above July ’09

30% below August ’08

Credit concerns and low freight traffic continue to

hold orders down at low levels

Fiscal YTD average: 8,860

52% below FY08 period; seasonally adjusted rate

of 104,800

August 2009 : 10,810

August net orders high due to school bus orders

June and July were distorted due to GM exiting

the market

Fiscal YTD average: 7,120

54% below FY08 period; seasonally adjusted

rate of 84,300

Class 8

Class 5-7

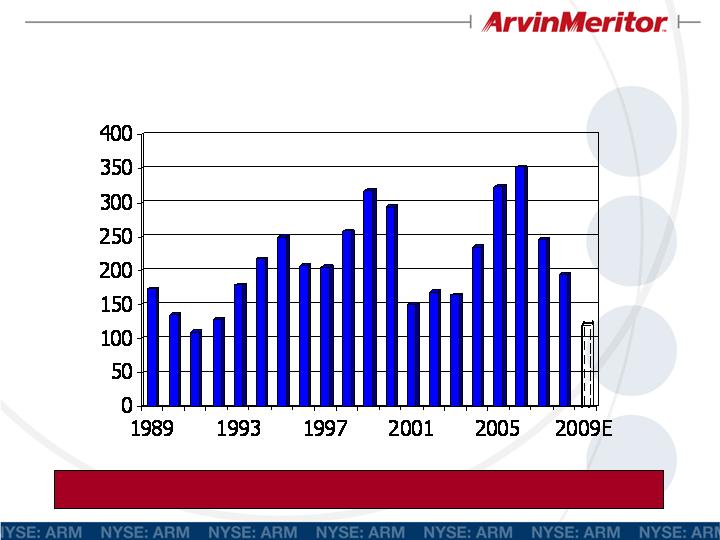

Historical Class 8 Production

North America

In bottom of trough and preparing for the upturn

Units (000)

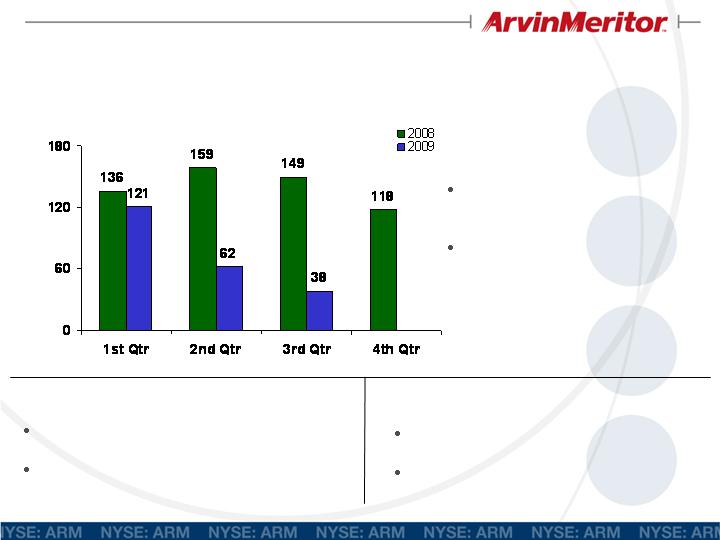

Commercial Vehicle Markets - ROW

Fiscal Quarters

Europe

Med. & Heavy Truck Production (000)

Q3 production down 74%

year-over-year and down

39% from Q2

More down time in fiscal Q4

South America

Asia Pacific

Q3 production down 36% year-over-

year, but up 9% from Q2

Could see further small increases in

upcoming quarters

Q3 production down 27% year-over-

year, but up 33% from Q2

Same industry trends hold for India and

China specifically

Strategic Priorities

1.

Ensure adequate liquidity while minimizing cost

Clear covenants

Benefit from current favorable credit agreement

2.

Continued restructuring and other cost reductions

Resist workforce and cost increases as volume returns

Tight controls on discretionary spending

Performance Plus Wave II

3.

Continue operational performance improvement

Improve global capacity flexibility

Drive inventory turns improvements

Manage the upturn

4.

Complete LVS separation

5.

Continue to grow high-margin product categories

Commercial Vehicle Aftermarket and Specialty

6.

Innovate and strengthen product development and technology

Hybrid commercial vehicles, new axle launch, fuel efficient and

high quality products

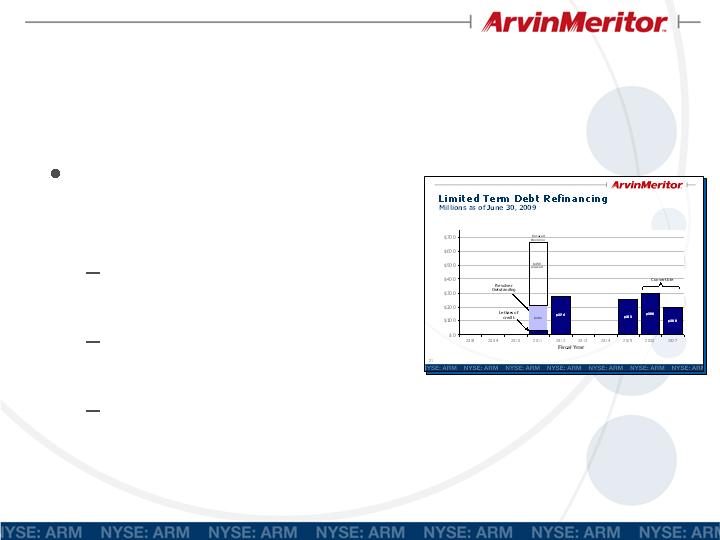

Credit Line Covenant Compliance

Completed identified actions needed to clear covenants at September

measurement

New, two-year U.S. receivables financing arrangement completed

on September 8, 2009

Total commitment under the facility is $125 million after

additional lender participation

Daily borrowing availability under the New Facility exceeds

availability under the facility it replaced

Sale of Wheels business unit was completed on September 21,

2009 with receipt of proceeds in September FY 2009

Used net proceeds of $169 million from the sale to reduce

outstanding balances on the revolving credit facility

We believe that we are in compliance with all covenants in our

revolving credit facility, including the covenant related to the ratio of

senior secured debt to EBITDA, as of the end of Q4 2009

Light Vehicle Systems

Closed sale of Wheels to lochpe-Maxion

S.A. on September 21, 2009

Received $169 million of net proceeds

Chassis divestitures

- Gabriel de Venezuela

- Gabriel Ride Control North America

- JV Mitsubishi Steel (MSSC)

Remaining Chassis business expected to

operate near break-even; modules will run

off over two years as vehicle programs end

Wheels

Chassis

Working to minimize cash requirements

Divest as business and market conditions allow

Body

LVS Chassis

$0.5 Billion

Wheels

$0.3 Billion

North

America

75%

North

America

50%

South

America

45%

Q4 Discontinued Operations

Based on 2008 Sales

Product Highlights

Meritor® TACTXTM High Mobility

Independent Suspension in production with

British TSV program

Semi-active damping shocks

Meritor® Air Suspension Height Control

Lightweight aluminum carrier assemblies

Expanding ELSA Disc Brake Platform into

North America and Asia Pacific markets

Best-in-class reliability and performance

Participating in DOE SuperTruck competition

with Meritor® Dual Mode Class 8 Hybrid

Meritor® MT-14X Tandem Axle

Superior design addresses customer

needs for reduced weight, improved

efficiency and wider ratio coverage

Expected

launch at

MATS in 2010

Strategic repositioning nearing completion

Aggressively lowered breakeven levels with the goal of

being cash flow neutral at current industry size

Well-positioned to benefit from a rebound in the

commercial vehicle industry

Current North American industry about 50% below cycle average

Sustainable competitive position

Strong growth in most profitable product categories

Aftermarket and Specialty

Investment Case

Franchise value we can sustain and grow

Frequently Asked Questions

1.

Will you be negatively impacted by the FMTV

award to Oshkosh?

2.

What is the status of your French Factoring and

Swedish Securitization programs?

3.

With the fourth quarter covenant issue behind

you, are you planning any changes to your capital

structure?

4.

What exposure do you have to higher steel

prices?

5.

Do you have any targets on where your

profitability could go relative to past cycles?

FAQ #1: Will you be negatively impacted

by the FMTV award to Oshkosh?

Oshkosh will fundamentally build the same FMTV

vehicles as BAE Systems to maintain continuity in

the military's vehicle fleet

Award currently under protest by BAE Systems

and Navistar

We expect to supply the

same components

regardless of

manufacturer

FAQ #2: What is the status of your French

Factoring and Swedish Securitization

programs?

Both facilities backed by 364-day liquidity

commitments from Nordea Bank

renewed through mid-October 2009

We expect renewal of the two facilities based

on verbal communication with Nordea

FAQ #3: With the fourth quarter covenant

issue behind you, are you planning any

changes to your capital structure?

We continue to look at

available options to address

the balance sheet, including

Renewing the 2011

revolver

Addressing the 2012

unsecured notes

Progressing towards

investment grade statistics

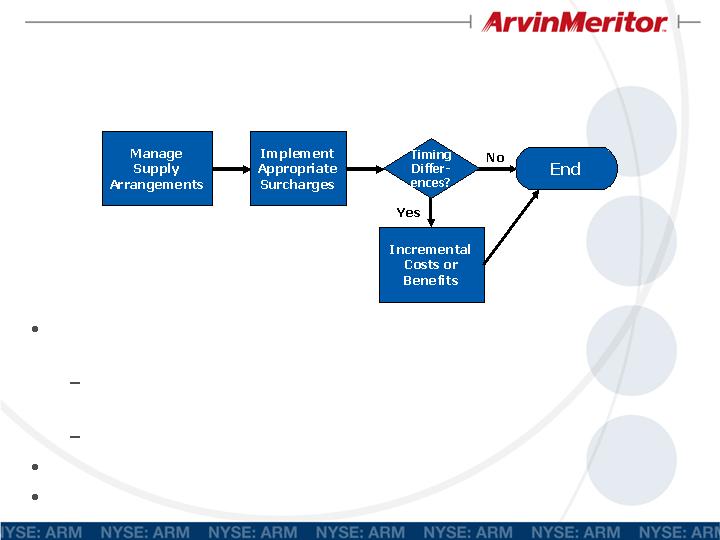

FAQ #4: What exposure do you have to

higher steel prices?

We do not expect to experience any significant impact from increasing

steel prices

Contractually recover/refund steel price differences from/to our

customers

Similar to prior periods of rising steel prices

Surcharges will increase/decrease in parallel with costs

Commodity movements not viewed as cost or profit making opportunity

FAQ #5: Do you have any targets on where

your profitability could go relative to

past cycles? (1)

We have a long-term Return on Equity target

in the mid teens or higher

Therefore, we have a long-term EBITDA

margin target of 10% average through the

cycle

We believe becoming exclusively a

commercial vehicle and industrial company

allows us to achieve that more rapidly

(1) Based on management’s current long-term planning assumptions. Please see slide 2, “Forward-Looking Statements”.