Forward-Looking Statements

This presentation contains statements relating to future results of the company (including certain projections and business trends) that are

“forward-looking statements” as defined in the Private Securities Litigation Reform Act of 1995. Forward-looking statements are typically identified

by words or phrases such as “believe,” “expect,” “anticipate,” “estimate,” “should,” “are likely to be,” “will” and similar expressions. There are risks

and uncertainties relating to the company’s announced plans to divest the Body Systems business of LVS and any of the strategic options under

which to pursue such divestiture. In the case of any sale of all or a portion of the business, these risks and uncertainties include the timing and

certainty of completion of any sale, the terms upon which any purchase and sale agreement may be entered into (including potential substantial

costs) and whether closing conditions (some of which may not be within the company’s control) will be met. In the case of any shut down of

portions of the business, these risks and uncertainties include the amount of substantial severance and other payments as well as the length of

time we will continue to have to operate the business, which is likely to be longer than in a sale scenario. There is also a risk of loss of customers

of this business due to the uncertainty as to the future of this business. In addition, actual results may differ materially from those projected as a

result of certain risks and uncertainties, including but not limited to global economic and market cycles and conditions, including the recent global

economic crisis; the demand for commercial, specialty and light vehicles for which the company supplies products; risks inherent in operating

abroad (including foreign currency exchange rates and potential disruption of production and supply due to terrorist attacks or acts of aggression);

whether our liquidity will be affected by declining vehicle production volumes in the future; availability and sharply rising cost of raw materials,

including steel and oil; OEM program delays; demand for and market acceptance of new and existing products; successful development of new

products; reliance on major OEM customers; labor relations of the company, its suppliers and customers, including potential disruptions in supply

of parts to our facilities or demand for our products due to work stoppages; the financial condition of the company’s suppliers and customers,

including potential bankruptcies; possible adverse effects of any future suspension of normal trade credit terms by our suppliers; potential

difficulties competing with companies that have avoided their existing contracts in bankruptcy and reorganization proceedings; successful

integration of acquired or merged businesses; the ability to achieve the expected annual savings and synergies from past and future business

combinations and the ability to achieve the expected benefits of restructuring actions; the ability to achieve anticipated or continued cost savings

from reduction actions; success and timing of potential divestitures; potential impairment of long-lived assets, including goodwill; potential

adjustment of the value of deferred tax assets; competitive product and pricing pressures; the amount of the company’s debt; the ability of the

company to continue to comply with covenants in its financing agreements; the ability of the company to access capital markets; credit ratings of

the company’s debt; the outcome of existing and any future legal proceedings, including any litigation with respect to environmental or asbestos-

related matters; the outcome of actual and potential product liability and warranty and recall claims; rising costs of pension and other post-

retirement benefits and possible changes in pension and other accounting rules; as well as other risks and uncertainties, including but not limited to

those detailed from time to time in filings of the company with the SEC. These forward-looking statements are made only as of the date hereof, and

the company undertakes no obligation to update or revise the forward-looking statements, whether as a result of new information, future events or

otherwise, except as otherwise required by law.

All earnings per share amounts are on a diluted basis. The company's fiscal year ends on the Sunday nearest Sept. 30, and its fiscal quarters end

on the Sundays nearest Dec. 31, March 31 and June 30. All year and quarter references relate to the company's fiscal year and fiscal quarters,

unless otherwise stated.

Agenda

Chris Snodgrass

Vice President, Worldwide Manufacturing

Manufacturing & Supply

Chain

Jay Craig

Chief Financial Officer

Financial Overview

Strategic Direction

Chip McClure

Chairman, CEO and President

Operations Strategy &

Performance Plus

Commercial Truck

Carsten Reinhardt

Chief Operating Officer

Industrial & Asia Pacific

Tim Bowes

President, Industrial

Aftermarket & Trailer

Joe Mejaly

President, Aftermarket & Trailer

Divestiture Update

Mary Lehmann

Chris Snodgrass

& Supply Chain

Manufacturing & Supply

Chain

Jay Craig

Chief Financial Officer

Financial Overview

Strategic Direction

Chip McClure

Chairman, CEO and President

Operations Strategy &

Performance Plus

Commercial Truck

Carsten Reinhardt

Chief Operating Officer

Industrial & Asia Pacific

Tim Bowes

President, Industrial & Asia Pacific

Aftermarket & Trailer

Joe Mejaly

President, Aftermarket & Trailer

Divestiture Update

Mary Lehmann

Senior Vice President, Strategic

Initiatives

2009 Priorities

Accelerate restructuring and other cost

reductions

Continue operational performance

improvement

Complete LVS separation

Continue to grow high-margin segments

Innovate and strengthen technology

Did what we said we would do

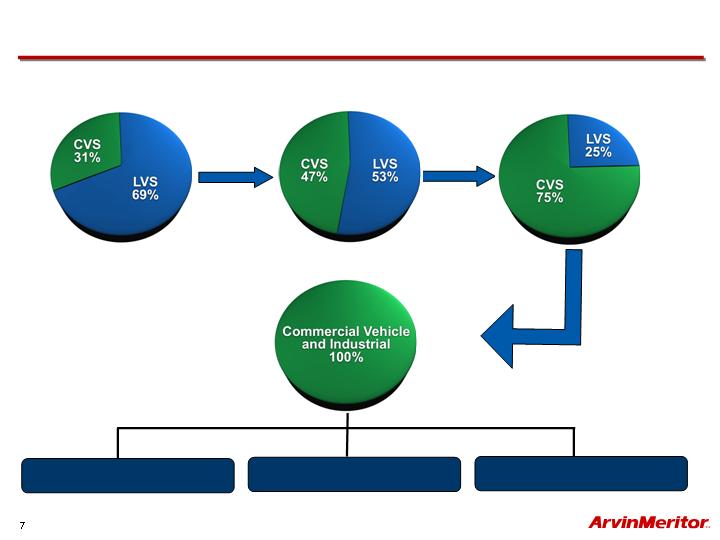

Progress Toward Transformation

FY03

FY06

Future

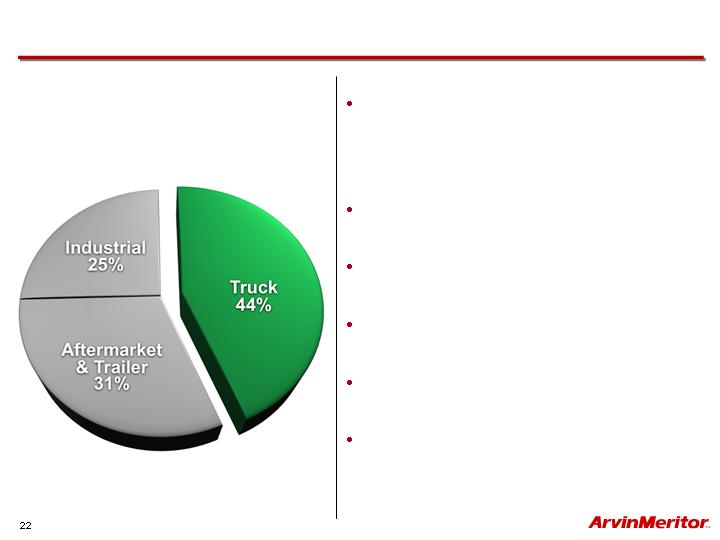

Commercial Truck

Industrial

Aftermarket & Trailer

Based on Sales

FY09

Commercial Truck

Maintain leadership position

in delivering advanced

drivetrain solutions

Expand global brake

leadership positions

Invest in advanced

technologies to improve

vehicle efficiency

Strengthen electronics and

controls capability

Strategic Priorities

Industrial

Grow global off-highway,

specialty and defense

business

Expand product and

customer portfolio

Grow market share in Asia

Pacific

Accelerate investments in

engineering and technology

capabilities in China and

India

Strategic Priorities

Aftermarket & Trailer

Grow aftermarket through

expansion of product portfolio

and remanufacturing

business

Continue to expand

aftermarket global distribution

network and systems

infrastructure

Expand into emerging

markets

Increase global share of the

growing trailer market

Strategic Priorities

Light Vehicle Systems

Continue commitment to

LVS divestiture strategy

Continue to invest and

support customers

Limit costs to carry the

business

Strategic Priorities

2010 Priorities

Remain focused on rigorous cost management to

realize improved operating leverage

Continue transformation to focus the company on

global commercial and industrial markets

Successfully execute as global markets recover

Drive innovation – accelerating new products and

advanced fuel efficient technologies

Maintain focus on sustainable profitable growth

Continue focus on balance sheet management

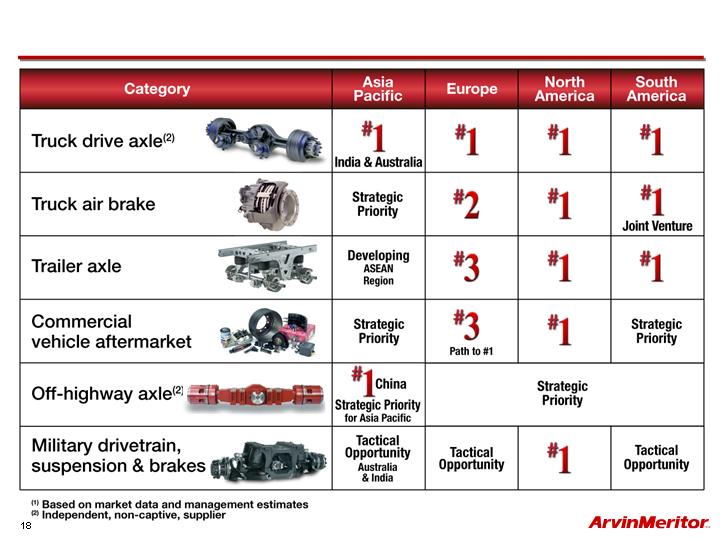

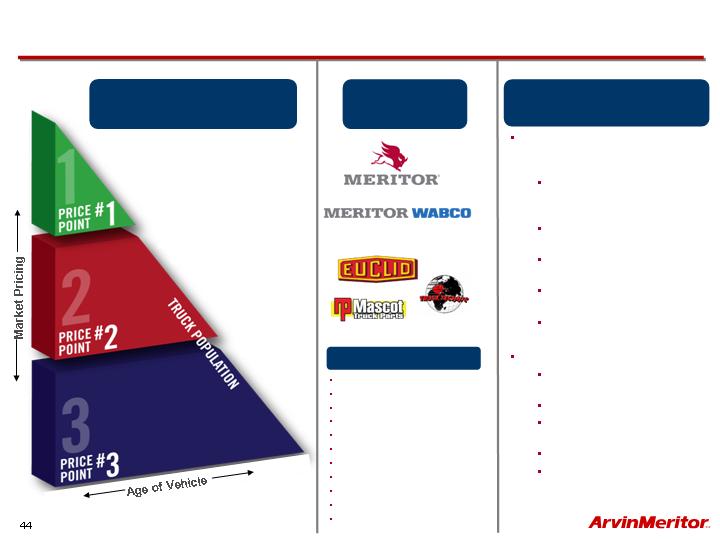

Axles, brakes, suspension and transmissions

to commercial vehicle aftermarket customers

Wide variety of undercarriage products and

systems for trailer applications

Transforming the Business

Drivetrain systems and components

including axles, drivelines, braking and

suspension systems

Medium and heavy duty trucks in NA,

SA and Europe

Drivetrain systems including axles, brakes,

drivelines and suspensions

Off-highway, military, construction, bus and

coach, fire and emergency and other

industrial

On- and off-highway activities in Asia

Pacific

Aftermarket & Trailer

Industrial

Commercial Truck

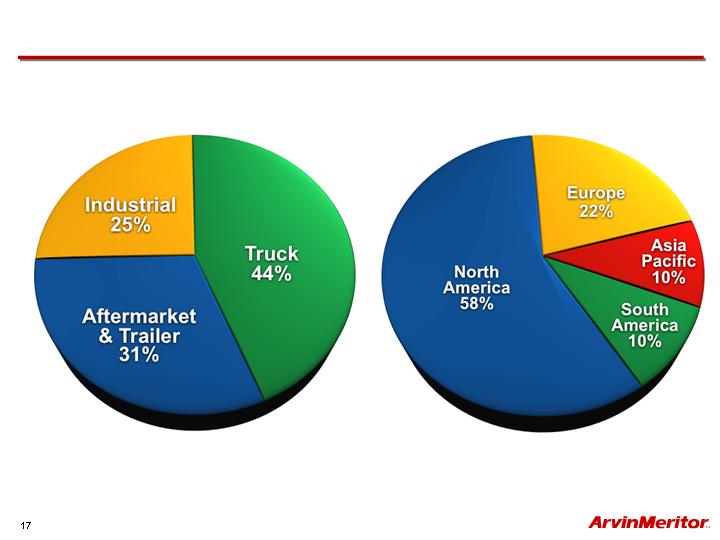

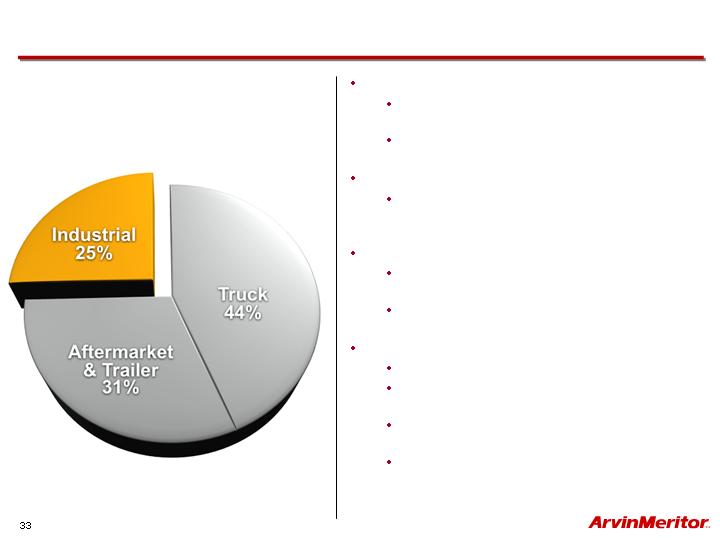

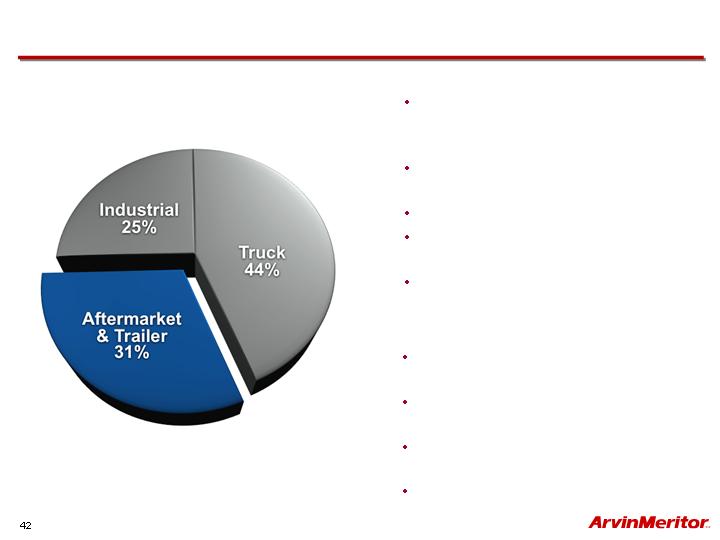

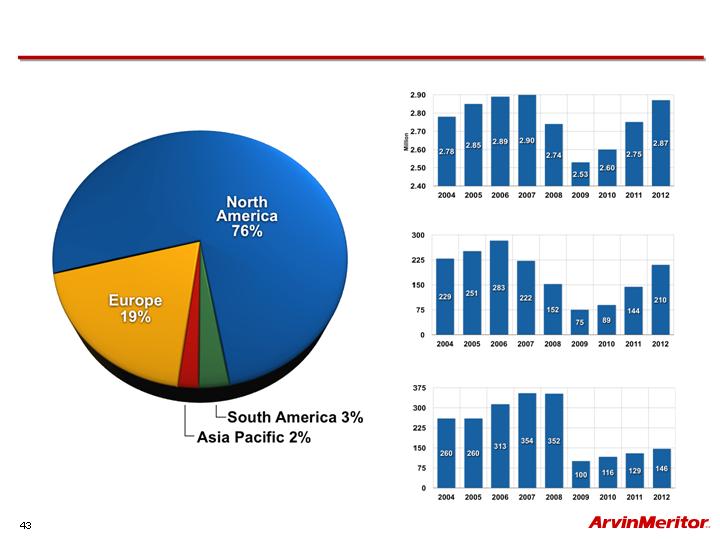

Regional and Segment Mix – Core Business

2009 Sales: $3.1 billion

Commercial Truck, Industrial, Aftermarket & Trailer

Direct Material

Optimization

Manufacturing

Overhead

C

O

S

T

SIX MAIN AREAS DEFINED IN 2006

More than 450 initiatives in the pipeline; more than 1,300

complete

Forty full-time employees

Active business process in NA, EU, SA, India and China

Reduced supply base by 15%

Invested $100 million in rationalization, flexibility and capacity

Exceeded targeted annual labor and burden savings of 3% (net

of economics)

One plant opened, six plants closed and consolidated

APS launched in 100% of our plants globally

Investment initiated in additional capacity in lucrative, emerging

markets in Brazil and China

Substantially exceeded risk-adjusted target of ~$45 million

Including 8% indirect material savings

Additional G&A savings include: temp labor, travel &

entertainment, shared services and outsourcing

Product Strategy

Engineering R&D

Aftermarket

R

E

V

E

N

U

E

SIX MAIN AREAS DEFINED IN 2006

Increased engineering staff by 10%+

Invested $3 million in testing and validation

Forty-seven major program launches since 2007

Presented dual-mode hybrid technology

Grew electronics and controls capabilities

Defined key growth segments such as off-highway,

defense, drivetrain efficiency and brake technology

First products have hit the marketplace

Focused program to improve profitability of products

through pricing and complexity reduction

Increased revenue by approximately $120 million or 17%

Revenue growth of 70% in Remanufacturing

Launched new products including Platinum Shield

Combined trailer axle offering with remanufactured

products to EU fleets for lower cost of operation

Launched CVA product platform in BRIC countries

Commercial Truck

Based on FY09 Sales

Well-positioned to benefit from

rebound in global commercial

truck markets in North America

and Europe

Well-established position in

South America

Strong product portfolio and

customer relationships

Building on strong position to

diversify customer mix

Aggressive product launch

cadence in 2010/2011/2012

Designing products for vehicle

efficiency

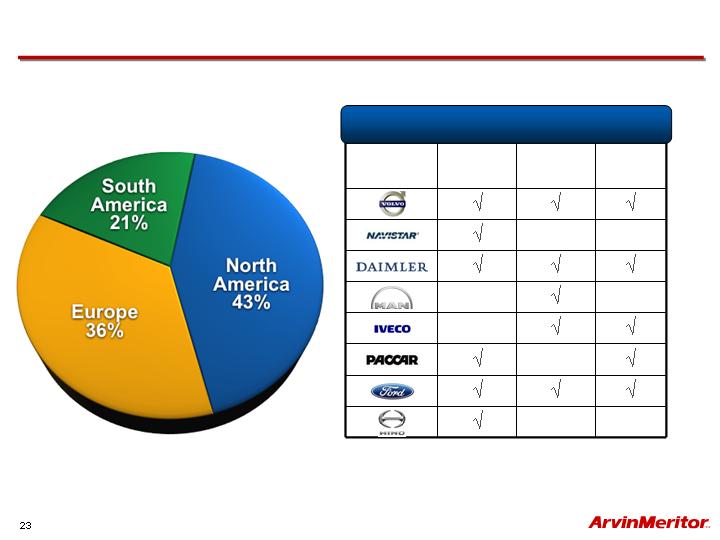

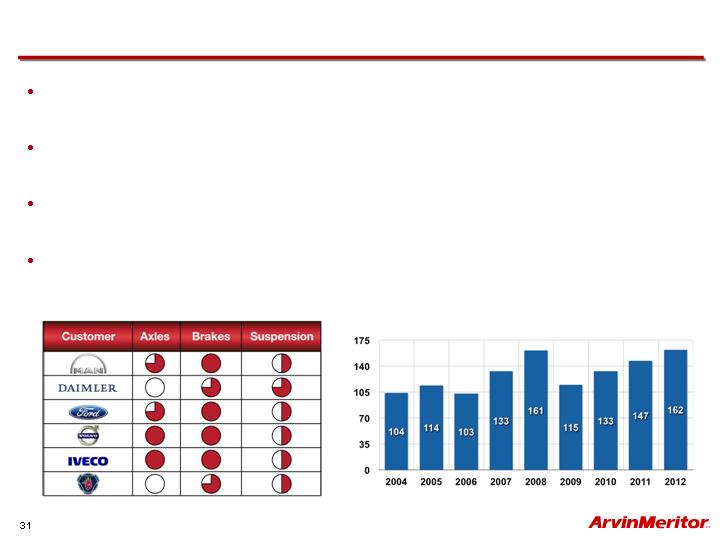

Truck Markets and Customers

Customer

North

America

South

America

Europe

v

v

v

v

v

v

v

v

v

v

v

v

v

v

v

v

Top Truck Customers 2009

Based on FY09 Sales

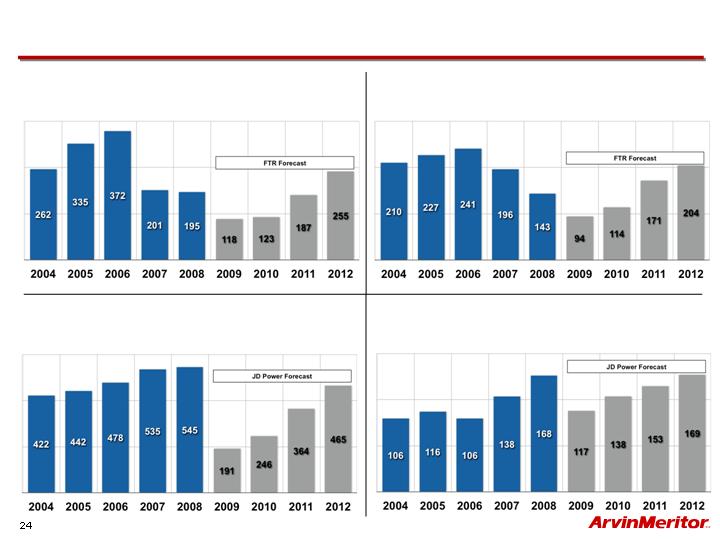

Global Truck Production Trends

North America

Class 8 Production (000)

Calendar Year

Western Europe

Med. & Heavy Truck Production GVW>6t (000)

Calendar Year

North America

Class 4-7 Production (000)

Calendar Year

South America

Med. & Heavy Truck Production GVW>6t (000)

Calendar Year

Growing Business in North America

PACCAR

Meritor front and rear

axles and brakes now

standard on the

KENMEX new T460 for

cement mixer and dump

truck applications

KENMEX is the Mexican

subsidiary of the

Kenworth Truck

Company, a PACCAR

company

Volvo

Meritor will continue to be the

standard drive axle supplier for

the Volvo and Mack truck

brands for the next three years

RPL Meritor drivelines will be

standard on Volvo

RN Meritor drivelines will be

standard on Mack

DTNA

Extends long-term

relationship with DTNA

Agreement through 2011

Continues supply of axles,

brakes and drivelines to

Freightliner and Western

Star at historical penetration

levels

Meritor WABCO awarded

standard position for new

SS1200 plus air dryer

beginning January 2010

Navistar

Signed 7-year axle agreement

in March 2009

Meritor axles now standard

position on International

medium duty trucks and IC Bus

brand school and commercial

buses

Gained additional standard axle

position on International’s

heavy-duty trucks

Gained data book positions for

Meritor WABCO

Next Generation Technology

New design

addresses

customer needs

Improved vehicle

efficiency

Lowest weight in

industry

Optimized

driveline

angularity

Higher torque/HP

capability

Faster axle ratios

MT-14X Tandem Axle

Developing technologies to improve

product cost, performance and vehicle

efficiency to support key customers

Successfully launched 17-X drive axle

for European applications

Plan to begin production of

MS-18X for 60 ton GCW Global

applications in 2Q11

Significant investment planned to

support foundation air disc brake

business

Increasing the scale of our well known,

on-highway hub reduction technology

with the 610 product platform

Growing Business in Western Europe

ELSA Disc Brake

17-X Technology

Hub Reduction Technology

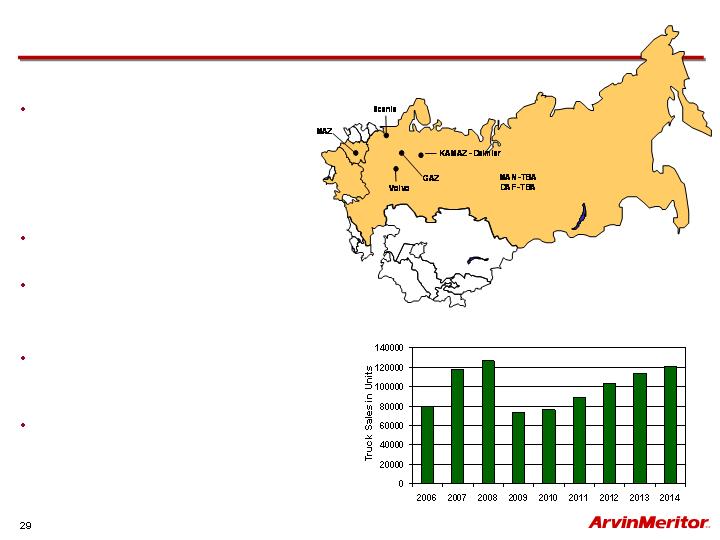

Growing Business in Russia

Background

ARM sales in the Commonwealth of

Independent States (CIS) have

increased to more than $10 million as

100,000 new and used EU and NA

trucks have been imported into the

region

Moscow office opened in 2008 to

support region with aftermarket needs

Further growth in CIS expected as

conditions improve

Next Steps

Signed MOU to study feasibility of a

joint venture for axles, brakes and

trailer components in the region

JV would serve the CIS

and provide low cost manufactured

components for other territories

Market Growth in CIS Significant

Source: Global Insight

Brazil Economy Improving

GDP expanded by 1.9% quarter-over-quarter in 2Q; estimates for

approximately 5% real GDP growth through 2015

Government plans to invest $160 billion from 2009-2013 on recovery and

production of recently discovered deep water oil reserves

Expected government stimulus for 2014 World Cup and 2016 Summer

Olympics

Growth Acceleration Program will invest more than $400 billion over next

five years in infrastructure

Brazil

Truck Production, GVW>6t

Calendar Year

Source: J.D. Power and Associates

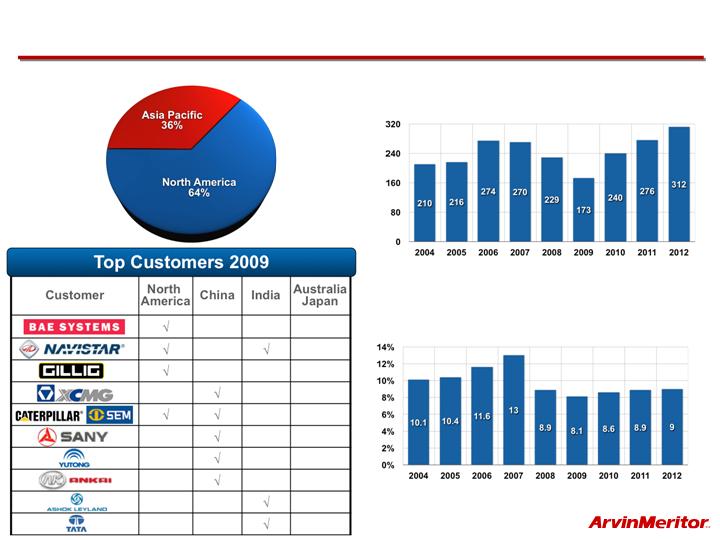

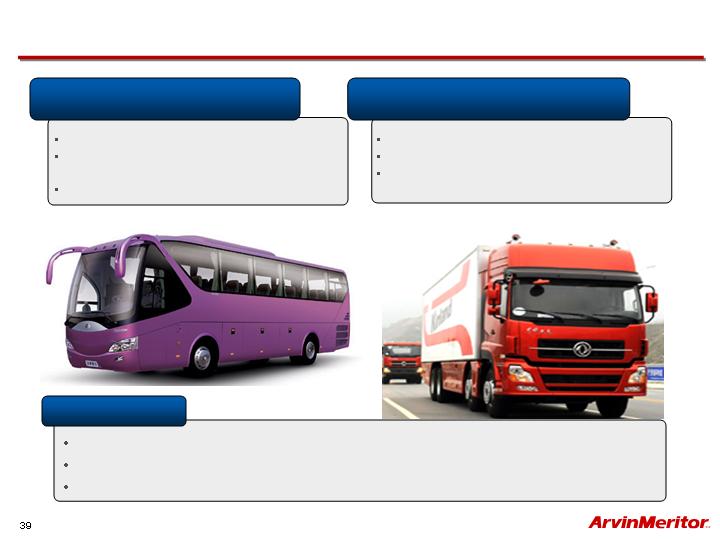

Industrial and Asia Pacific

Off-Highway

Leading independent off-highway axle

supplier in China

Re-entering global off-highway market

leveraging global scale and technology

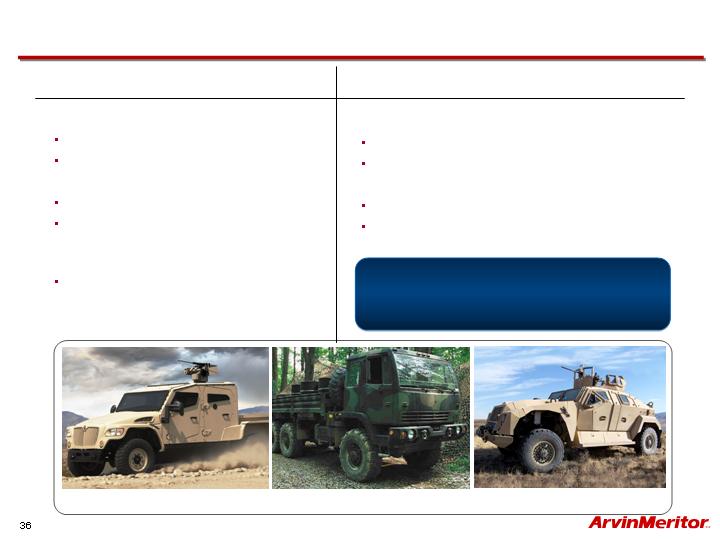

Defense

Largest independent drivetrain producer

for tactical wheeled vehicles globally

Commercial Vehicle

Largest independent supplier of axles

in India and Australia

Leading supplier of drum brakes in

China

Specialty

Leader in Bus & Coach in U.S.

Leader in customized fire truck market

in the U.S.

Leader in Class 5 AWD market in the

U.S.

Expanding in premium bus & coach

market in India and China

Based on FY09 Sales

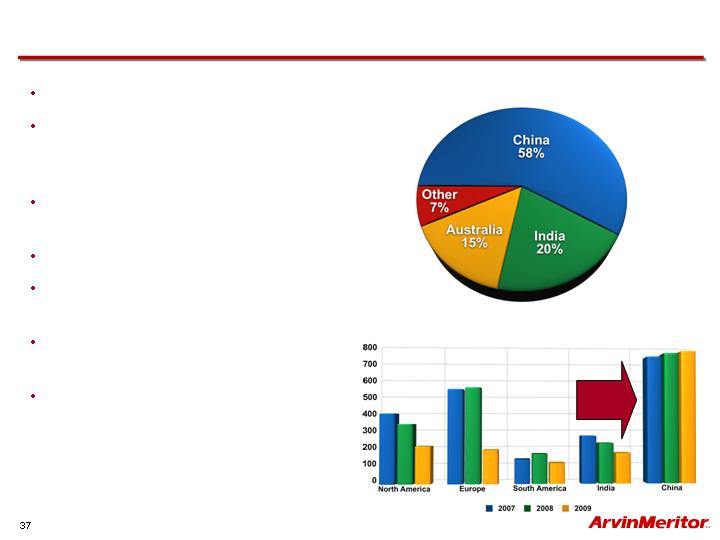

Industrial and Asia Pacific

China

GDP Growth

India

Truck Production GVW>6t

Source: J.D. Power and Associates

Source: J.D. Power and Associates

Based on FY09 Sales

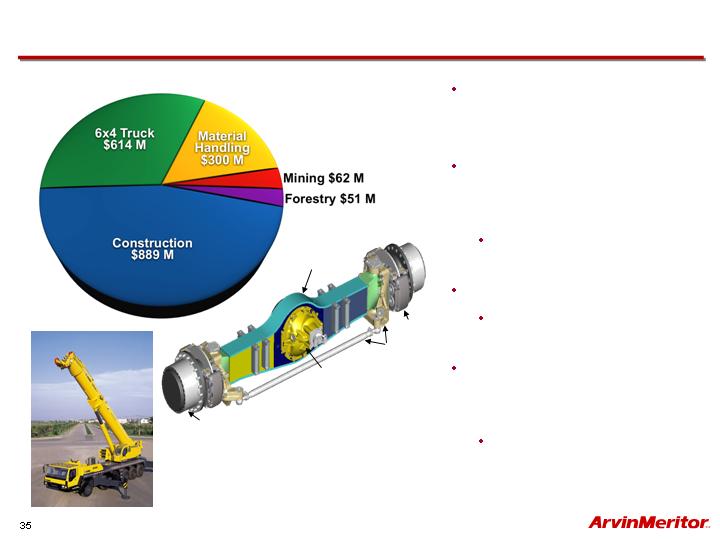

Global Off-Highway Market

Target Launch Market of $1.9B

Demand expected to grow

through 2014; AP major

growth market

Leveraging China installed

base and commercial

vehicle products

More than 50 new axle

models

Robust global product plans

New axle families from

35,000 lb-300,000 lb capacity

Significant investment

planned for Xuzhou Meritor

Axle Co. joint venture

Targeting 20% increase in

capacity

Housing

Brake

Steering

Wheel end

Carrier

AT Crane

MXT

FMTV

JLTV

Defense Programs

Future Programs

Booked Business

FMTV

On-contract through 2010

Re-buy contract starts in 2011

MXT

Production contract with British MoD

Meritor TACTX™ High Mobility

Independent Suspension

Heavy Tactical Trucks

Freightliner on contract through 2010

Aftermarket Service for All Models

Joint Light Tactical Vehicle (JLTV)

HMMWV replacement, production SOP 2013

ArvinMeritor partnered with 2/3 current OEM’s

Marine Personnel Carrier (MPC)

Next Generation LAV

ArvinMeritor on team to build a demonstrator,

production 2014

DEFENSE STRATEGY

Secure North America position

Expand in selective markets

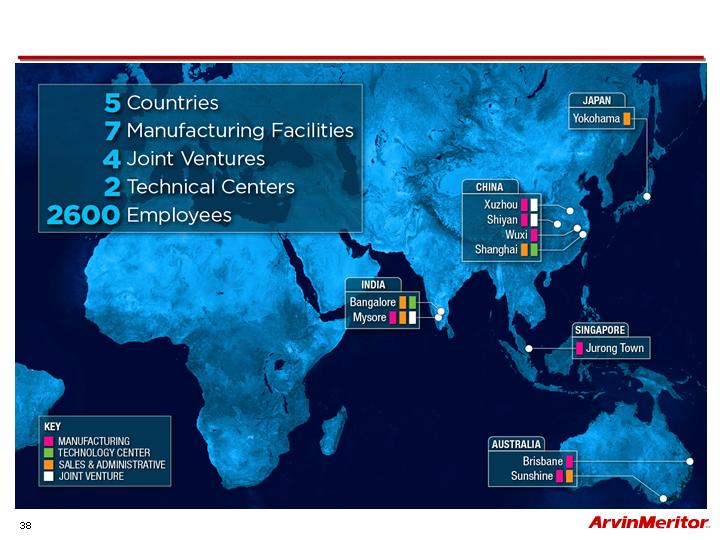

Asia Pacific Strategy

Market presence for nearly 30 years

Strong in-region management with

localized manufacturing and

sourcing

Regional product development

leveraging global capabilities

Strong relationships

Focused on China, India and

ASEAN region

Exploring organic and inorganic

growth opportunities

Increasing engineering capabilities

Regional Market Comparison for Truck Production

FOCUS

Based on FY09 Sales

China Commercial Vehicle and Specialty

ArvinMeritor Vehicle Systems

Co., Ltd.

Location: Wuxi, Jiangsu Province, China

Products: Air disc brake, carrier assembly,

axles, trailer beam and axle

Markets: Bus & Coach

Meritor Huayang Vehicle Braking

Co., Ltd.

Expand axle offering for high and mid-range OE Market (truck and bus)

Increase brake capabilities

Increase local engineering and customer service capability

Growth Strategy

Location: Shiyan, Hubei Province, China

Products: Drum brakes

Markets: Commercial vehicles, Bus

& Coach and Off-Highway

India Growth Strategy

Meritor HVS (India) Ltd. and Automotive Axles Ltd.

Location: Mysore

Main Products: Drive axles, front steer axles, tag axles and brakes; significant engineering

and validation capabilities exist

Established: Partnerships with Kalyani Group established in 1998 and 1981

Sales growth in foundation and air disc brakes

Expand product portfolio to meet increasing needs in the commercial vehicle market

Strategically enter growing Indian off-highway market

Opportunities in military market

Advanced product design and development capabilities in Bangalore technical center

Growth Strategy

Aftermarket & Trailer Segment

Global Aftermarket Business

Well-known brand portfolio and

product life-cycle service and

support

World-class packaging and

distribution

Remanufacturing global enterprise

Extensive product portfolio and “all

makes” competitor product lines

Industry-wide leader in customer

service

Global Trailer Business

Full-line axle, wheel-end and

suspension supplier

Established footprint in North

America and Europe

Leading market position with joint

venture in South America

Distribution in Asia Pacific region

Based on FY09 Sales

Aftermarket & Trailer

North American Trailer Production

U.S. Truck Freight Ton Miles

Seasonally Adjusted

Source: FTR Associates

Source: FTR Associates

Source: 2004-08 CLEAR data; 2009-12 blended data

Europe Trailer Production

Based on FY09 Sales

Aftermarket Success Formula

Genuine Product

Genuine Product –

Price/Reman

Price/Reman

Advanced warehousing

management and distribution

systems

Highly-automated

component packaging

capability

Same day shipment for

vehicle-down emergencies

Lean warehousing and Six

Sigma-driven processes

Highly-efficient order

processing capability

Low transaction cost

Global Reach

11 distribution centers

across 5 continents

7 remanufacturing centers

8 customer assistance call

centers

3,300 distributors

2,600 OE dealers

Servicing the Full

Lifecycle of the Vehicle

Distribution Expertise and

Extensive Global Network

Product

Brands

Products

Transmissions

Axles

Electronic products

Braking components

Drivelines

Trailer axles/components

Steering gears

Air systems/components

Clutches

Hydraulic braking systems

Remanufactured portfolio

Aftermarket Growth Initiatives - Europe

2003

2009

52%

48%

65%

35%

All-makes extensions

Reman offerings

Brand differentiation

Growth driven by:

Infrastructure investments

Price point products for broad

European market

“Meritor Service Point”

OEM service parts

Independent distributor channel

Based on Sales

North

America

Europe

South

America

Asia Pacific

Trailer Growth Initiatives

Significantly reduced breakeven levels at current industry volumes

Well-positioned with new product launches

Prepared to capitalize on market recovery

MTA Air

Suspension

Euroflex

Maintain #1 position in trailer axles and braking

systems

Expand product offerings

Launch new MTA air suspension in 2010

Introduce new advanced technologies (MTIS)

Enhance product lines

Launched Euroflex new air suspension in 2009

Drive growth by leveraging:

Sales and service support

Aftermarket distribution network

Grow with strong joint venture partner

Expand product offerings

Launch next generation air suspension in

2010

Continue to build strong alignment with key

customers

Increase market share in Australia and New

Zealand and expand in other Asian countries

Expand mfg. and dist. footprint in region

CS Suspension

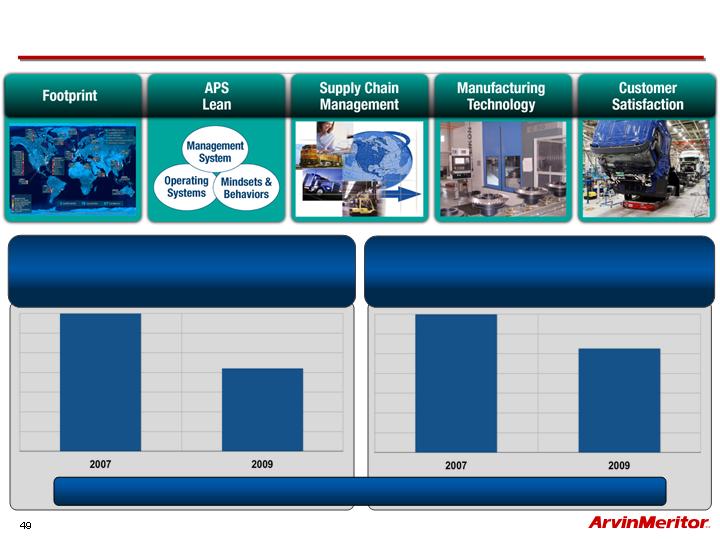

Manufacturing Operations Turnaround

Five focus areas driven by a foundation of talented employees

Labor and Burden

40% reduction in manufacturing

conversion cost

Inventory

25% reduction in inventory

through performance

Preparing North America for the Upturn

Mexico

Increased flexibility and capability

Consolidated footprint

North American Footprint

Industrializing Footprint for Growth in Asia

China

Localizing capability

Positioning footprint for growth

Asia Pacific Footprint

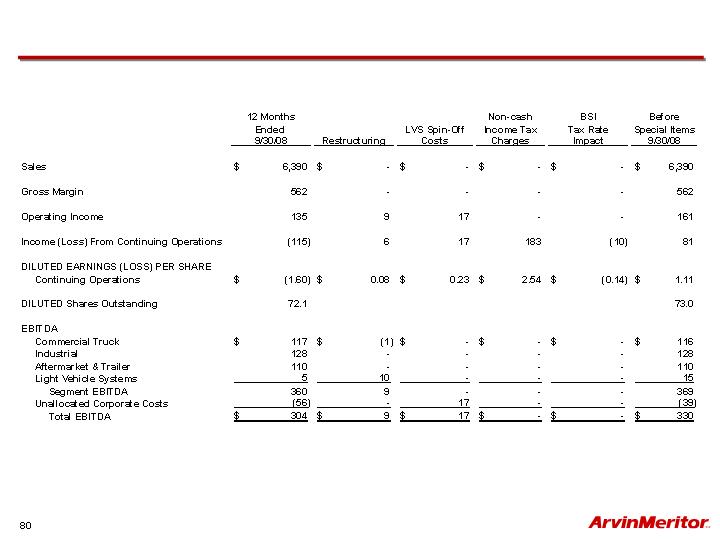

Segment EBITDA Before Special Items(1)

Quarter Ended

September 30,

Year Ended

September 30,

2009

2008

2009

2008

Sales

Commercial Truck

$ 325

$ 690

$ 1,566

$ 2,922

Industrial

220

290

888

1,117

Aftermarket & Trailer

219

307

954

1,183

Light Vehicle Systems

288

340

1,033

1,571

Intersegment Sales

(68)

(96)

(333)

(403)

Total Sales

$ 984

$ 1,531

$ 4,108

$ 6,390

EBITDA

Commercial Truck

$ 1

$ 27

$ (38)

$ 116

Industrial

24

36

126

128

Aftermarket & Trailer

18

34

89

110

Light Vehicle Systems

-

5

(53)

15

Segment EBITDA

$ 43

$ 102

$ 124

$ 369

Unallocated Corporate Costs

(3)

(15)

(8)

(39)

Total EBITDA

$ 40

$ 87

$ 116

$ 330

Total EBITDA Margin

4.1%

5.7%

2.8%

5.2%

(in millions)

(1) Continuing operations before special items. See appendix – “Non-GAAP Financial Information.”

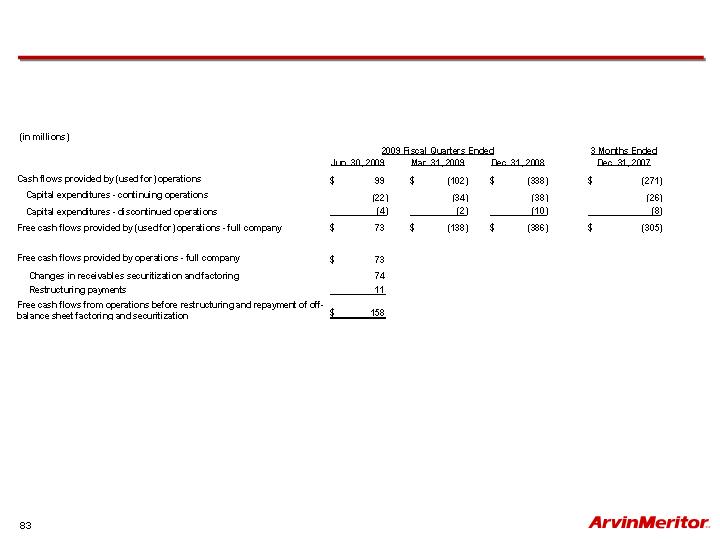

Free Cash Flow (1)

Quarter Ended

September 30,

Year Ended

September 30,

2009

2008

2009

2008

Pretax Income from Continuing Operations

$ (2)

$ 23

$ (361)

$ 93

Impairments

-

-

223

-

Net Spending (D&A less Capital Expenditures)

4

(17)

(30)

(18)

Pension and Retiree Medical Net of Expense

(5)

6

(26)

22

Performance Working Capital (2)

41

234

210

(154)

Off Balance Sheet Securitization and Factoring

(15)

(83)

(275)

120

Other, including Restructuring

(13)

(84)

(131)

(21)

Free Cash Flow from Continuing Ops.

$ 10

79

$ (390)

$ 42

Discontinued Operations

12

24

(39)

(51)

Free Cash Flow

$ 22

$ 103

$ (429)

$ (9)

Memo: Cash Flow Provided by Continuing

Operations

$ 27

$ 127

$ (279)

$ 180

(in millions)

(1) See appendix – “Non-GAAP Financial Information.”

(2) Change in payables less changes in receivables, inventory and customer tooling.

Fourth Quarter 2009 Results Comparisons(1)

FY09 Q3

Actual(2)

FY09 Q4

Actual

Sales

$942 million

$984 million

EBITDA BSI

$28 million

$40 million

EPS BSI

$(0.29)

$(0.28)

FCF before Factoring

and Restructuring

$158 million

$48 million

FCF

$73 million

$22 million

(1)

See appendix – “Non-GAAP Financial Information.”

(2)

Recast for LVS divestitures, including removal of Wheels, as reported in Q4 2009.

EBITDA Margin Before Special Items (1)

EBITDA(1) Margin

Q309 – As previously reported

3.3%

Wheels and Chassis divestitures

(0.3)

Q309 – Excluding Wheels and Chassis

3.0%

Europe medium & heavy truck production volume

(1.0)

North America production volume

0.3

South America production volume

0.3

Performance Plus and other cost savings

1.6

Other

(0.2)

Core Business subtotal

4.0%

LVS

0.1

Q409

4.1%

(1) ArvinMeritor uses EBITDA as the primary basis for the chief operating decision maker to evaluate the performance of each of the

company’s reportable segments. See appendix for consolidation and comparison to GAAP measures. EBITDA margin equals

EBITDA divided by sales.

Margins vs. Prior Quarter

Structural Cost Reductions(1)

Core Business

FY09 Savings(1)

Q4

FY

Run

Rate

Structural Cost

Reductions

$34

$97

$136

Temporary Cost

Reductions

$13

$48

$52

Variable Labor

(Volume related)

$18

$50

$72

Total

$65

$195

$260

(1) Cost reductions represent expected savings based on current information and management’s best estimates.

Pay reductions restored

in November

($12 million annual run rate)

FY10 and beyond

(in millions)

Pension & OPEB Update

FY07

FY08

FY09

FY10E(1)

Pension

Unfunded Status

$181

$115

$517

N/A

Expense(2)

$69

$46

$22

$38

Contributions

$152

$34

$25

$51

Discount Rate

U.S.

6.35%

7.10%

5.70%

N/A

Asset Returns

U.S.

OPEB

Contributions(3)

$50

$48

$75

$46

(1)

Based on management’s current planning assumptions and other factors. Actual results may differ materially from projections as a

result of risks and uncertainties. Please see slide “Forward Looking Statements.”

(2)

Based on continuing operations excluding restructuring expenses.

(3)

Includes $28 million one-time settlement of USW retiree medical in Q1 2009.

(in millions)

Long-term return assumption currently at 8.5%

2010 Planning Assumptions(1)

(in millions)

Capital Expenditures

$90 - $110

Interest Expense

$95 - $110

Income Tax Expense - BSI

$40 - $60

Cash Income Taxes

$25 - $50

(1) Based on management’s current planning assumptions and other factors. Actual results may differ materially from

projections as a result of risks and uncertainties. Please see slide “Forward Looking Statements.”

Fiscal Year Basis

Update on First Quarter Outlook(1)

FY 2009 Q4

Actual(2)

FY 2010 Q1

Outlook(1)

Sales

$984 million

Higher

EBITDA BSI

$40 million

Higher

Income before

Taxes BSI

$2 million

Higher

FCF before

Factoring and

Restructuring

$48 million

Slightly Negative

FCF

$22 million

Around Breakeven

(1)

Based on management’s current planning assumptions and other factors. Actual results may differ materially from projections as a

result of risks and uncertainties. Please see slide “Forward Looking Statements.”

(2)

See appendix – “Non-GAAP Financial Information” for a reconciliation to GAAP.

Q1 FY 2010 Free Cash Flow is expected to be

significantly better than previous years

We expect to achieve positive Free Cash Flow for

three consecutive quarters

Stable Cash Flow Results(1)(2)

(1)

Based on management’s current planning assumptions and other factors. Actual results may differ materially from projections as a

result of risks and uncertainties. Please see slide “Forward Looking Statements.”

(2)

See appendix – “Non-GAAP Financial Information.”

(3) GAAP cash flow provided by (used for) continuing operations was $ (338) million for fiscal year 2009 first quarter, $(271) million for

fiscal year 2008 first quarter, $27 million for fiscal year 2009 fourth quarter, $99 million for fiscal year 2009 third quarter and $(102)

million for fiscal year 2009 second quarter.

(in millions)

FY 2010 Q1

Outlook(1)

FY 2009 Q1

Actual

FY 2008 Q1

Actual

Free Cash Flow

Around

Breakeven

$(386) million

$(305) million

(in millions)

FY 2010 Q1

Outlook(1)

FY 2009 Q4

Actual

FY 2009 Q3

Actual

FY 2009 Q2

Actual

FY 2009 Q1

Actual

Free Cash Flow

Around

Breakeven

$22

$73

$(138)

$(386)

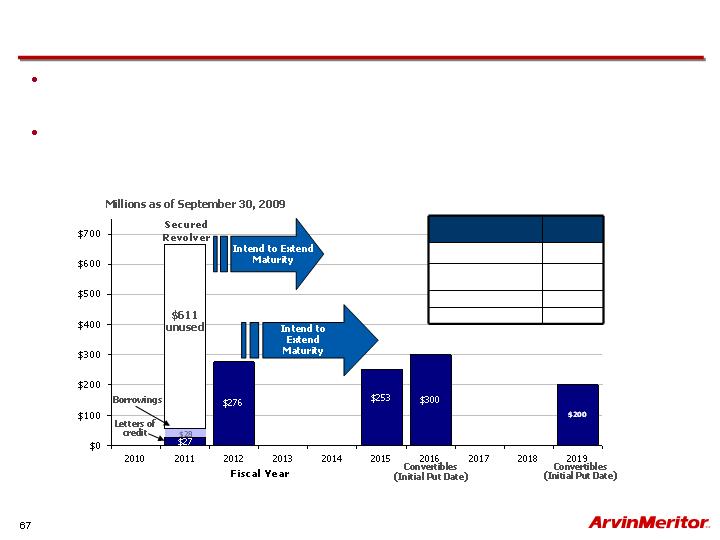

FY10 plan to extend maturities of our revolver and bulk of 2012

notes

Long-term objective of achieving credit statistics near

investment grade

Long-Term Capital Structure(1)

(1)

Based on management’s current planning assumptions and other factors. Actual results may differ materially from projections as a

result of risks and uncertainties. Please see slide “Forward Looking Statements.”

(2)

S&P key industrial financial ratios – Three-year (2005-2007) average medians for BB rated companies.

(Three-year average)

S&P BB

Ratios(2)

EBITDA Interest Coverage

4.8X

Free Operating Cash Flow /

Total Debt

7.1%

Total Debt / EBITDA

3.1X

Total Debt / Capitalization

52.5%

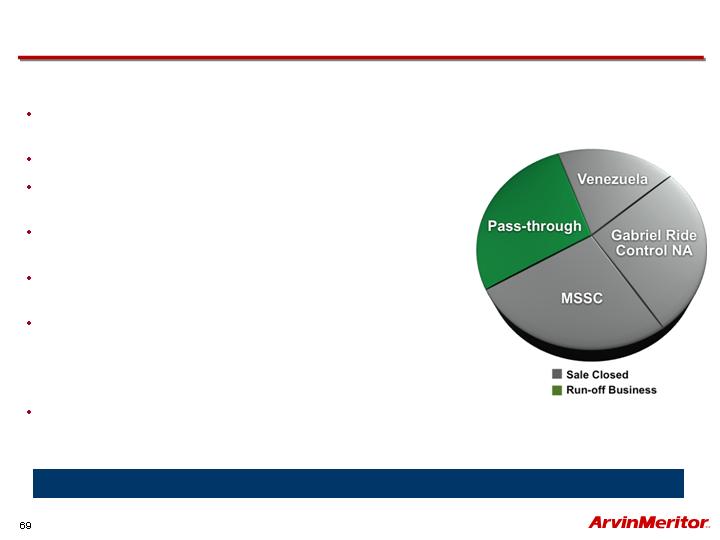

Chassis

Transactions solidified ArvinMeritor’s liquidity

position

Sold stake in Gabriel de Venezuela (June 2009)

Sold Gabriel Ride Control North America U.S.

(July 2009), Mexico (August 2009)

Sold stake in joint venture with Mitsubishi Steel

(MSSC) (October 2009)

Sales from remaining Chassis businesses were

$106 million in FY09

Remaining Chassis businesses have operated

near breakeven; most will run off over the next

two years as vehicle programs end

Chassis Operations

2008 Sales

Wheels

Sold and closed in September 2009;

$166 million net proceeds

Wheels complete; Chassis divestiture essentially complete

LVS Divestiture – Significant Progress to Date

LVS Financial Update

3Q 2009

4Q 2009

Sales

$259

$288

EBITDA – BSI(1)

$(6)

$0

Free Cash Flow

(Before Factoring)

Slightly

Positive

About

Breakeven

Capital

Expenditures(2)

$25 - $30 million in FY 2010

(included in total company FY 2010

assumption of $90 - $110 million)

(1) See appendix – “Non-GAAP Financial Information.”

(2)

Based on management’s current planning assumptions and other factors. Actual results may differ materially from

projections as a result of risks and uncertainties. Please see slide “Forward Looking Statements.”

Based on FY09 Sales

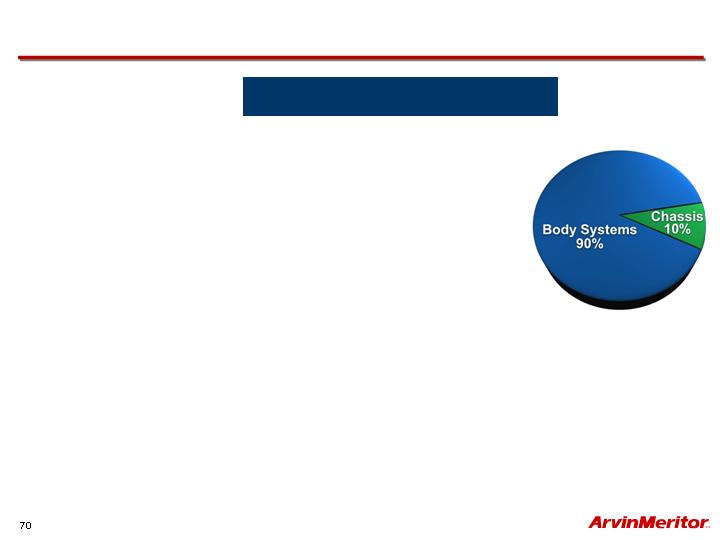

LVS Divestiture – Body Systems

Committed to divest Body Systems and will work to

achieve the best outcome for our shareholders,

customers and employees as we move through 2010

Body Systems is believed to have stabilized at continuing

depressed market volumes

EBITDA near breakeven levels in Q3 and Q4 2009

Improved “cost to carry” should provide time to divest the

business in the most economically advantageous way

possible

Preferred outcome is strategic buyer for the business

External progress updates will be provided

A company prepared to realize its full potential

Strong leadership team

Strong focus

Strong market positions

Strong global foundation

Strong profitable growth strategy

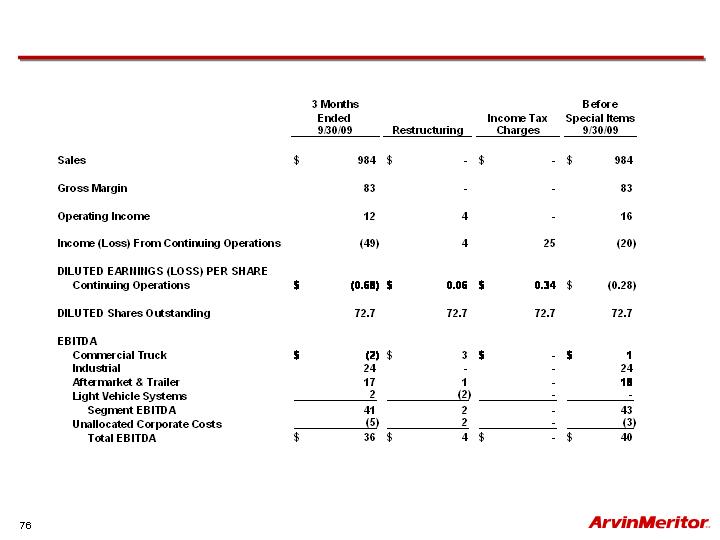

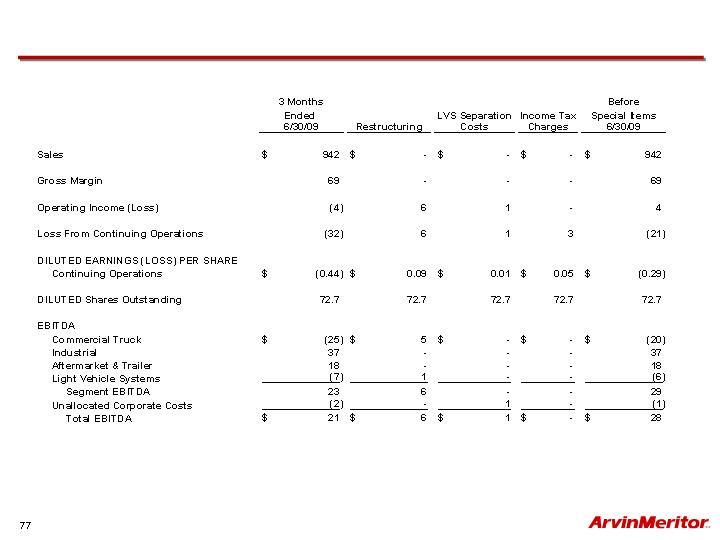

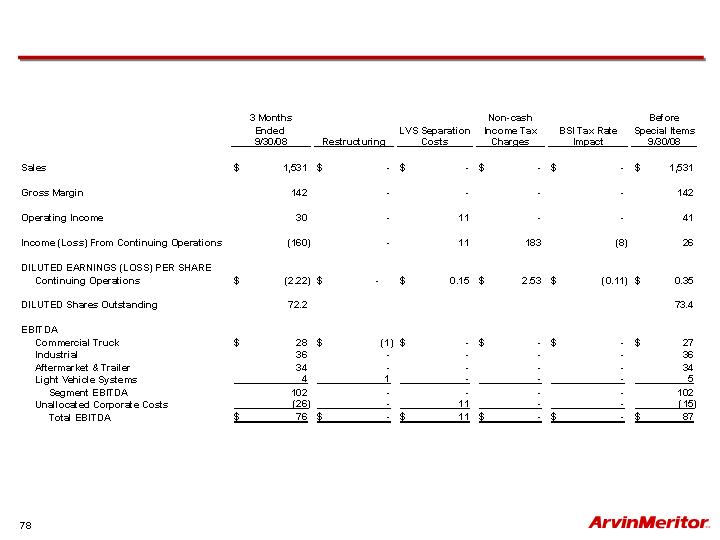

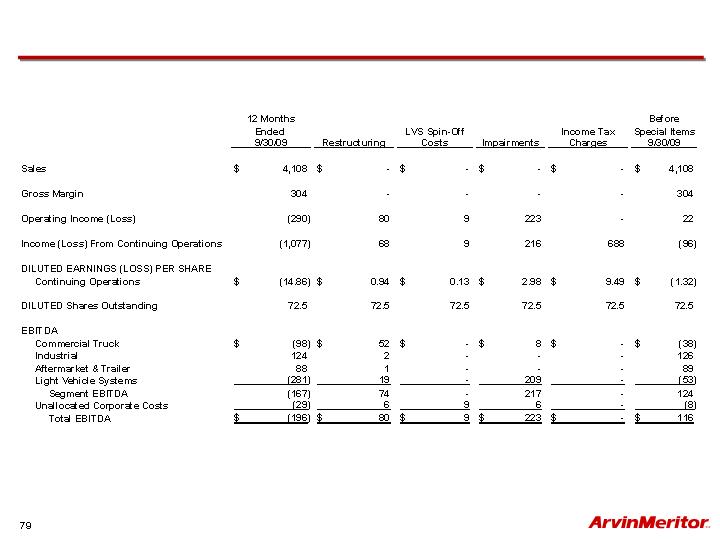

Use of Non-GAAP Financial Information

In addition to the results reported in accordance with accounting principles generally accepted in the United States (“GAAP”)

included throughout this presentation, the Company has provided information regarding income from continuing operations

and diluted earnings per share before special items, which are non-GAAP financial measures. These non-GAAP measures

are defined as reported income or loss from continuing operations and reported diluted earnings or loss per share from

continuing operations plus or minus special items. Other non-GAAP financial measures include “EBITDA” and “free cash

flow”. EBITDA before special items is defined as earnings before interest, taxes, depreciation and amortization, and losses

on sales of receivables, plus or minus special items. Free cash flow represents net cash provided by operating activities less

capital expenditures.

Management believes that the non-GAAP financial measures used in this presentation are useful to both management and

investors in their analysis of the Company’s financial position and results of operations. In particular, management believes

that free cash flow is useful in analyzing the Company’s ability to service and repay its debt. EBITDA is a meaningful

measure of performance commonly used by management, the investment community and banking institutions to analyze

operating performance and entity valuation. Further, management uses these non-GAAP measures for planning and

forecasting in future periods. The company uses EBITDA as the primary basis for the chief operating decision maker to

evaluate the performance of each of the company’s reportable segments.

These non-GAAP measures should not be considered a substitute for the reported results prepared in accordance with

GAAP. Free cash flow should not be considered substitutes for cash provided by operating activities or other balance sheet

or cash flow statement data prepared in accordance with GAAP or as a measure of financial position or liquidity. In addition,

the calculation of free cash flow does not reflect cash used to service debt and thus, does not reflect funds available for

investment or other discretionary uses. EBITDA should not be considered an alternative to operating income as an indicator

of operating performance or to cash flows as a measure of liquidity. These non-GAAP financial measures, as determined and

presented by the Company, may not be comparable to related or similarly titled measures reported by other companies.

Set forth on the following slides are reconciliations of these non-GAAP financial measures, if applicable, to the most directly

comparable financial measures calculated and presented in accordance with GAAP.

In addition, financial data may be provided on a “trailing twelve month basis,” which equates to the sum of the measure in

question for the four most recent quarters.