Exhibit 99.2

Aeterna Zentaris

Management's Discussion and Analysis

of Financial Condition and Results of Operations

Company Overview

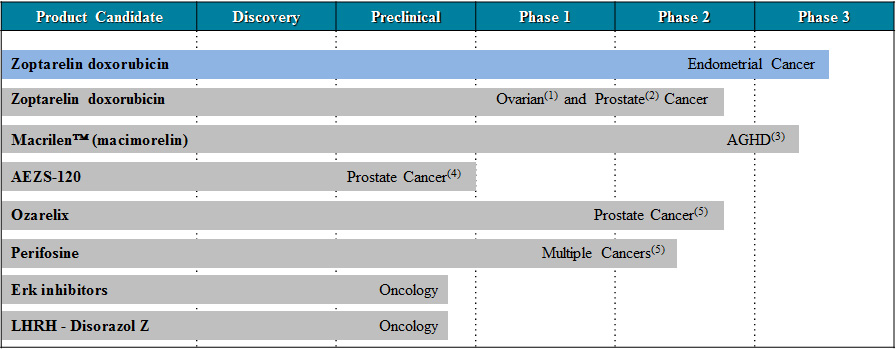

Aeterna Zentaris Inc. is a specialty biopharmaceutical company engaged in developing and commercializing novel treatments in oncology, endocrinology and women's health.

Our drug development efforts are focused currently on two compounds, zoptarelin doxorubicin and Macrilen™, which are in clinical development, and on two oncology compounds (our Erk inhibitors and LHRH-disorazol Z product candidates), which are in pre-clinical development. We also are working concurrently to pursue strategic initiatives in connection with our goal to become a commercially operating specialty biopharmaceutical organization.

The Company's common shares are listed on both the NASDAQ Capital Market ("NASDAQ"), under the symbol "AEZS", and on the Toronto Stock Exchange ("TSX"), under the symbol "AEZ".

Introduction

This Management's Discussion and Analysis ("MD&A") provides a review of the results of operations, financial condition and cash flows of Aeterna Zentaris Inc. for the year ended December 31, 2014. In this MD&A, "Aeterna Zentaris", the "Company", "we", "us", "our" and the "Group" mean Aeterna Zentaris Inc. and its subsidiaries. This discussion should be read in conjunction with the information contained in the Company's consolidated financial statements and the accompanying notes thereto as at December 31, 2014 and December 31, 2013 and for the years ended December 31, 2014, 2013 and 2012. Our consolidated financial statements have been prepared in accordance with International Financial Reporting Standards ("IFRS") as issued by the International Accounting Standards Board ("IASB").

All amounts in this MD&A are presented in United States ("US") dollars, except for share, option and warrant data, per share and per warrant data and as otherwise noted.

All shares, options and share purchase warrants as well as per share, option and share purchase warrant information presented in this MD&A have been adjusted, including proportionate adjustments being made to each stock option and share purchase warrant exercise price, to reflect and give effect to a consolidation, on October 2, 2012, of our issued and outstanding common shares on a six-to-one basis. The share consolidation affected all shareholders, optionholders and warrantholders uniformly and thus did not materially affect any securityholder's percentage of ownership interest.

About Forward-Looking Statements

This document contains forward-looking statements, which reflect our current expectations regarding future events. Forward-looking statements may include words such as "anticipate", "assume", "believe", "could", "expect", "foresee", "goal", "guidance", "intend", "may", "objective", "outlook", "plan", "seek", "should", "strive", "target" and "will".

Forward-looking statements involve risks and uncertainties, many of which are discussed in this MD&A and others of which are discussed under the caption "Key Information – Risk Factors" in our most recent Annual Report on Form 20-F filed with the relevant Canadian securities regulatory authorities in lieu of an annual information form and with the US Securities and Exchange Commission ("SEC"). Such statements include, but are not limited to, statements about the progress of our research, development and clinical trials and the timing of, and prospects for, regulatory approval and commercialization of our product candidates, the timing of expected results of our studies, anticipated results of these studies, statements about the status of our efforts to establish a commercial operation and to obtain the right to promote or sell products that we did not develop and estimates regarding our capital requirements and our needs for, and our ability to obtain, additional financing. Known and unknown risks and uncertainties could cause our actual results to differ materially from those in the forward-looking statements. Such risks and uncertainties include, among others, the availability of funds and resources to pursue our research and development ("R&D") projects, the successful and timely completion of clinical studies, the degree of market acceptance once our products are approved for commercialization, our ability to take advantage of business opportunities in the

Aeterna Zentaris

2014 Annual MD&A

pharmaceutical industry, our ability to protect our intellectual property, uncertainties related to the regulatory process and general changes in economic conditions. See also the section entitled "Risk Factors and Uncertainties", in this MD&A.

Given these uncertainties and risk factors, readers are cautioned not to place undue reliance on any forward-looking statements. We disclaim any obligation to update any such factors or to publicly announce any revisions to any of the forward-looking statements contained herein to reflect future results, events or developments, unless required to do so by a governmental authority or by applicable law.

About Material Information

This MD&A includes information that we believe to be material to investors after considering all circumstances, including potential market sensitivity. We consider information and disclosures to be material if they result in, or would reasonably be expected to result in, a significant change in the market price or value of our securities, or where it is likely that a reasonable investor would consider the information and disclosures to be important in making an investment decision.

The Company is a reporting issuer under the securities legislation of all of the provinces of Canada, and our securities are registered with the SEC. The Company is therefore required to file or furnish continuous disclosure information, such as interim and annual financial statements, MD&As, proxy or information circulars, annual reports on Form 20-F, material change reports and press releases with the appropriate securities regulatory authorities. Copies of these documents may be obtained free of charge upon request from the Company's Investor Relations department or on the Internet at the following addresses: www.aezsinc.com, www.sedar.com and www.sec.gov.

Key Developments

Commercial Developments

| |

| • | During the fourth quarter, our full-time contract sales force of 19 sales representatives started the field selling in the US of EstroGel®, pursuant to the co-promotion services agreement (the "Co-promotion Agreement") entered into with ASCEND Therapeutics US LLC ("ASCEND") in August 2014. The Co-promotion Agreement provides that we or one of our subsidiaries detail and market ASCEND's leading non-patch transdermal hormone replacement therapy product, available under the name EstroGel®, in specific agreed-upon US territories, in exchange for a sales commission, which will be payable to us based upon incremental EstroGel® sales volumes that are generated over certain pre-established thresholds. |

Product Candidate Developments

Zoptarelin Doxorubicin

| |

| • | During the year, we completed site initiation, with over 120 sites currently in operation, for our ZoptEC (Zoptarelin doxorubicin in Endometrial Cancer) Phase 3 trial in women with locally advanced, recurrent or metastatic endometrial cancer. To date, over 400 of the expected 500 patients have been entered into the trial. The ZoptEC Phase 3 trial is an open-label, randomized, multicenter trial conducted in North America, Europe and Israel under a Special Protocol Assessment ("SPA") with the FDA; it compares zoptarelin doxorubicin with doxorubicin as second line therapy. The primary efficacy endpoint is improvement in median Overall Survival. |

| |

| • | On December 1, 2014, we entered into a master collaboration agreement, a Technology Transfer and Technical Assistance Agreement ("TTA") and a License Agreement ("LA") with Sinopharm A-Think Pharmaceuticals Co., Ltd. ("Sinopharm") for the development, manufacture and commercialization of zoptarelin doxorubicin ("the Product") in all human uses, in the People's Republic of China, including Hong Kong and Macau (collectively, "the Territory"). Under the terms of the TTA, Sinopharm made a one-time, non-refundable payment of $1.1 million ("Transfer Fee") to us for the transfer of technical documentation and materials, know-how and technical assistance services. Additionally, per the LA, we will be entitled to receive additional consideration upon achieving certain pre-established milestones, including the occurrence of certain regulatory and commercial events in the Territory. Furthermore, we will be entitled to receive royalties on future net sales of the Product in the Territory. |

Aeterna Zentaris

2014 Annual MD&A

Macrilen™

| |

| • | On November 6, 2014, the FDA issued a Complete Response Letter ("CRL") for our New Drug Application ("NDA") for Macrilen™ in the evaluation of adult growth hormone deficiency ("AGHD"). Based on its review, the FDA determined that our NDA could not be approved in its form as submitted. The CRL stated that the planned analysis of our pivotal trial did not meet its stated primary efficacy objective as agreed to in the SPA agreement between the Company and the FDA, and that we will need to demonstrate the efficacy of macimorelin as a diagnostic test for growth hormone deficiency in a new, confirmatory clinical study. The CRL also stated that a serious event of electrocardiogram QT interval prolongation occurred for which attribution to drug could not be excluded. Therefore, a dedicated thorough QT study to evaluate the effect of macimorelin on the QT interval would be necessary. We intend to make a decision regarding the future development of Macrilen™ in the near term, taking into account various considerations, including our prior and upcoming discussions with the FDA. |

Erk Inhibitors

| |

| • | On April 9, 2014, we announced that we had presented, at the American Association for Cancer Research Annual Meeting in San Diego, a poster, entitled Erk Inhibition as a Therapeutic Option for the Treatment of Raf- and Mek- Inhibitor Resistant Tumors, on AEZS-134, a highly potent and selective adenosine triphosphate competitive Erk inhibitor. The poster provided a rationale for new therapeutic opportunities in oncology with this compound, given that preclinical data suggest that Erk inhibitors such as AEZS-134 may provide a treatment option for patients suffering from tumors that are resistant to currently established therapies such as B-Raf and Mek inhibitors. |

Corporate Developments

Establishment of Global Commercial Operations and Resource Optimization

| |

| • | On May 5, 2014, we announced that we had selected Charleston, South Carolina, as the new location for our North American business and global commercial operations. In conjunction with our plans and commitment to our Charleston office, we expect to be eligible to receive job development investment tax credits pursuant to approval received from the Coordinating Council for Economic Development of South Carolina. |

| |

| • | On August 7, 2014, our Nominating, Governance and Compensation Committee approved our global resources optimization program (the "Resource Optimization Program"), which has been rolled out as part of our strategy to transition into a commercially operating specialty biopharmaceutical organization. The Resource Optimization Program, the goal of which is to streamline R&D activities and to increase commercial operations and flexibility, is expected to result in the termination of 30 employees. Employee departures under this program, which commenced during the first quarter of 2015, will continue through August 31, 2015. We expect that overall annualized savings upon completion of the Resource Optimization Program will amount to approximately $2.3 million. Total restructuring costs associated with the Resource Optimization Program recorded during 2014 were approximately $2.5 million, representing our estimated severance payments, onerous lease provision and other directly related costs. Our estimates of restructuring costs and annualized savings may be revised in future periods as new information becomes available. |

Public Offerings

| |

| • | On January 14, 2014, we completed a public offering of 11.0 million units, generating net proceeds of approximately $12.2 million, with each unit consisting of one common share and 0.80 of a warrant to purchase one common share, at a purchase price of $1.20 per unit (the "January 2014 Offering"). |

| |

| • | On March 11, 2015, we completed a public offering of 59,677,420 units (the "Units"), generating net proceeds of approximately $34.5 million, with each Unit consisting of either one common share or one warrant to purchase one common share ("Series C Warrant"), 0.75 of a warrant to purchase one common share ("Series A Warrant") and 0.50 of a warrant to purchase one common share ("Series B Warrant"), at a purchase price of $0.62 per Unit (the "March 2015 Offering"). The Series A Warrants are exercisable for a period of five years at an exercise price of $0.81 per share, and the Series B Warrants are exercisable for a period of 18 months at an exercise price of $0.81 per share. Both the Series A and Series B warrants are subject to certain anti-dilution provisions. The Series C Warrants are exercisable for a period of five years at an exercise price of $0.62 per share. Total gross proceeds payable to us in connection with the exercise of the Series C Warrants have been pre-paid by investors and therefore are included in the aforementioned proceeds. |

Aeterna Zentaris

2014 Annual MD&A

| |

| • | In connection with the March 2015 Offering, the holders of 21,123,332 of the 21,900,000 outstanding warrants issued by us in connection with a previous public offering of units in November 2013 and with the January 2014 Offering, as defined above, entered into an amendment agreement that caused such previously issued warrants to expire and terminate in exchange of a cash payment made by us in the aggregate amount of approximately $5.7 million. |

"At-the-Market" Issuance Program

| |

| • | Between July 1, 2014 and December 31, 2014, we issued a total of approximately nine million common shares under our At-the-Market ("ATM") sales agreement entered into May 2014 with MLV & Co. LLC (the "May 2014 ATM Program"), at an average price of $1.36 for aggregate gross proceeds of approximately $12.2 million, less cash and non-cash transaction costs of approximately $0.4 million. The May 2014 ATM Program provides that we may, at our discretion, from time to time during the term of the sales agreement, sell up to a maximum of 14.0 million of our common shares through ATM issuances on the NASDAQ, up to an aggregate amount of $15 million. |

NASDAQ Minimum Bid Price Compliance

| |

| • | On December 18, 2014, we received a notice from the NASDAQ regarding our failure to comply with the NASDAQ's $1.00 minimum bid price requirement. The Company has 180 calendar days, or until June 16, 2015, to regain compliance with the minimum bid price requirement. |

Status of Our Drug Pipeline

_________________________

(1) Phase 2 trial in ovarian cancer completed.

(2) Investigator-driven and sponsored.

(3) Currently evaluating options and future plans after issuance of CRL from the FDA.

(4) Potential oral prostate cancer vaccine available for out-licensing.

(5) Sponsored entirely by licensees.

We are focused on advancing our ZoptEC Phase 3 program with zoptarelin doxorubicin in endometrial cancer, as discussed further below, and on evaluating our options for Macrilen™ for the evaluation of AGHD.

As for our compounds in earlier stages of development, as part of the Resource Optimization Program, we have decided to streamline our drug discovery activities and focus on specific projects related to our Erk inhibitors and our LHRH-disorazol Z product candidates. Regarding our Erk inhibitors program, we are looking to select an optimized molecule for development in the first half of 2015.

Our investment in the development of Erk inhibitors and our LHRH-disorazol Z product candidate will depend on the level of liquidity available to fund our R&D activities.

Aeterna Zentaris

2014 Annual MD&A

Consolidated Statements of Comprehensive Income (Loss) Information

|

| | | | | | | | | | | | | | | |

| | | Three-month periods ended December 31, | | Years ended December 31, |

| (in thousands, except share and per share data) | | 2014 | | 2013 | | 2014 | | 2013 | | 2012 |

| | | $ | | $ | | $ | | $ | | $ |

| Revenues | | | | | | | | | | |

| Sales | | — |

| | — |

| | — |

| | 96 |

| | 834 |

|

| License fees | | 11 |

| | — |

| | 11 |

| | 6,079 |

| | 1,219 |

|

| | | 11 |

| | — |

| | 11 |

| | 6,175 |

| | 2,053 |

|

| Operating expenses | | | | | | | | | | |

| Cost of sales | | — |

| | — |

| | — |

| | 51 |

| | 591 |

|

| Research and development costs, net of refundable tax credits and grants | | 6,282 |

| | 5,345 |

| | 23,716 |

| | 21,284 |

| | 20,592 |

|

| Selling, general and administrative expenses | | 4,676 |

| | 2,627 |

| | 13,690 |

| | 12,316 |

| | 10,606 |

|

| | | 10,958 |

| | 7,972 |

| | 37,406 |

| | 33,651 |

| | 31,789 |

|

| Loss from operations | | (10,947 | ) | | (7,972 | ) | | (37,395 | ) | | (27,476 | ) | | (29,736 | ) |

| Finance income | | 15,053 |

| | 65 |

| | 20,319 |

| | 1,748 |

| | 6,974 |

|

| Finance costs | | — |

| | (2,689 | ) | | — |

| | (1,512 | ) | | (382 | ) |

| Net finance income (costs) | | 15,053 |

| | (2,624 | ) | | 20,319 |

| | 236 |

| | 6,592 |

|

| Income (loss) before income taxes | | 4,106 |

| | (10,596 | ) | | (17,076 | ) | | (27,240 | ) | | (23,144 | ) |

| Income tax expense | | (111 | ) | | — |

| | (111 | ) | | — |

| | — |

|

| Net income (loss) from continuing operations | | 3,995 |

| | (10,596 | ) | | (17,187 | ) | | (27,240 | ) | | (23,144 | ) |

| Net income from discontinued operations | | 158 |

| | 2,353 |

| | 623 |

| | 34,055 |

| | 2,732 |

|

| Net income (loss) | | 4,153 |

| | (8,243 | ) | | (16,564 | ) | | 6,815 |

| | (20,412 | ) |

| Other comprehensive income (loss): | | | | | | | | | | |

| Items that may be reclassified subsequently to profit or loss: | | | | | | | | | | |

| Foreign currency translation adjustments | | (677 | ) | | 424 |

| | (1,158 | ) | | 1,073 |

| | (504 | ) |

| Items that will not be reclassified to profit or loss: | | | | | | | | | | |

| Actuarial gain (loss) on defined benefit plans | | 1,336 |

| | 2,346 |

| | (1,833 | ) | | 2,346 |

| | (3,705 | ) |

| Comprehensive income (loss) | | 4,812 |

| | (5,473 | ) | | (19,555 | ) | | 10,234 |

| | (24,621 | ) |

| Net income (loss) per share (basic and diluted) from continuing operations | | 0.06 |

| | (0.28 | ) | | (0.29 | ) | | (0.92 | ) | | (1.17 | ) |

| Net income (basic and diluted) from discontinued operations | | — |

| | 0.06 |

| | 0.01 |

| | 1.16 |

| | 0.14 |

|

| Net income (loss) (basic and diluted) per share | | 0.06 |

| | (0.22 | ) | | (0.28 | ) | | 0.24 |

| | (1.03 | ) |

| Weighted average number of shares outstanding: | | | | | | | | | | |

| Basic | | 65,383,290 |

| | 37,274,129 |

| | 59,024,730 |

| | 29,476,455 |

| | 19,775,073 |

|

| Diluted | | 65,383,290 |

| | 37,274,129 |

| | 59,024,730 |

| | 29,476,455 |

| | 19,806,687 |

|

Aeterna Zentaris

2014 Annual MD&A

2014 compared to 2013

Revenues

Revenues are derived predominantly from license fees, which include the amortization of upfront payments received from our licensees and R&D contract service fees.

Sales revenues are derived from the sale of active pharmaceutical ingredients, or raw materials, to licensees. Periodic variations of sales, and, consequently, of cost of sales, are attributable to the R&D needs of the requesting licensee.

Revenues recorded during the year ended December 31, 2013 resulted predominantly from the non-recurring, accelerated recognition of remaining unamortized deferred revenue associated with an upfront payment received from a licensee following the termination of related R&D activities.

We expect revenues during the year ended December 31, 2015 to be higher than those recorded during the year ended December 31, 2014 due to the initial recognition of the Transfer Fee and due to sales commission revenue that we expect to begin generating in connection with our sales efforts related to EstroGel®, provided that we are able to begin to exceed the pre-established baselines outlined in the Co-promotion Agreement.

Operating Expenses

R&D costs, net of refundable tax credits and grants, were $6.3 million and $23.7 million for the three-month period and the year ended December 31, 2014, respectively, compared to $5.3 million and $21.3 million for the same periods in 2013.

The increase for the year ended December 31, 2014, as compared to the same period in 2013, is attributable to higher comparative employee compensation and benefits costs, which in turn are mainly due to the recording of R&D restructuring costs. Following the approval of the Resource Optimization Program, discussed above, we recorded a provision for restructuring costs, amounting to approximately $2.5 million, for severance payments, onerous lease provision and other directly related costs associated with the Resource Optimization Program. This increase is partly offset by lower comparative salaries and short-term employee benefits and share-based compensation costs.

The following table summarizes our net R&D costs by nature of expense:

|

| | | | | | | | | | | | | | | |

| | | Three-month periods ended December 31, | | Years ended December 31, |

| (in thousands) | | 2014 | | 2013 | | 2014 | | 2013 | | 2012 |

| | | $ | | $ | | $ | | $ | | $ |

| Third-party costs | | 3,967 |

| | 2,828 |

| | 11,356 |

| | 10,049 |

| | 8,679 |

|

| Employee compensation and benefits | | 1,231 |

| | 1,629 |

| | 8,430 |

| | 7,864 |

| | 8,590 |

|

| Facilities rent and maintenance | | 887 |

| | 466 |

| | 2,160 |

| | 1,758 |

| | 1,661 |

|

| Other costs* | | 197 |

| | 540 |

| | 1,901 |

| | 2,130 |

| | 2,530 |

|

| R&D tax credits and grants | | — |

| | (118 | ) | | (131 | ) | | (517 | ) | | (868 | ) |

| | | 6,282 |

| | 5,345 |

| | 23,716 |

| | 21,284 |

| | 20,592 |

|

_________________________

* Includes depreciation, amortization, impairment charges and onerous lease provision recognized.

Aeterna Zentaris

2014 Annual MD&A

The following table summarizes primary third-party R&D costs, by product candidate, incurred by the Company during the three-month periods ended December 31, 2014 and 2013.

|

| | | | | | | | | | | | |

| (in thousands, except percentages) | | Three-month periods ended December 31, |

| Product Candidate | | 2014 | | 2013 |

| | | $ | | % | | $ | | % |

| Zoptarelin doxorubicin | | 3,609 |

| | 91.0 |

| | 1,667 |

| | 58.9 |

|

| Macrilen™, macimorelin | | 192 |

| | 4.8 |

| | 284 |

| | 10.0 |

|

| Erk inhibitors | | 112 |

| | 2.8 |

| | 312 |

| | 11.0 |

|

| LHRH - Disorazol Z | | 54 |

| | 1.4 |

| | 139 |

| | 4.9 |

|

| Other | | — |

| | — |

| | 426 |

| | 15.2 |

|

| | | 3,967 |

| | 100.0 |

| | 2,828 |

| | 100.0 |

|

The following table summarizes primary third-party R&D costs, by product candidate, incurred by the Company during the years ended December 31, 2014, 2013 and 2012.

|

| | | | | | | | | | | | | | | | | | |

| (in thousands, except percentages) | | Years ended December 31, |

| Product Candidate | | 2014 | | 2013 | | 2012 |

| | | $ | | % | | $ | | % | | $ | | % |

| Zoptarelin doxorubicin | | 9,668 |

| | 85.1 |

| | 4,934 |

| | 49.1 |

| | 2,133 |

| | 24.6 |

|

| Erk inhibitors | | 488 |

| | 4.3 |

| | 1,128 |

| | 11.2 |

| | 1,727 |

| | 19.9 |

|

| Macrilen™, macimorelin | | 404 |

| | 3.6 |

| | 1,238 |

| | 12.3 |

| | 112 |

| | 1.3 |

|

| LHRH - Disorazol Z | | 257 |

| | 2.3 |

| | 659 |

| | 6.6 |

| | 331 |

| | 3.8 |

|

| Perifosine | | 196 |

| | 1.7 |

| | 1,134 |

| | 11.3 |

| | 3,801 |

| | 43.8 |

|

| Other | | 343 |

| | 3.0 |

| | 956 |

| | 9.5 |

| | 575 |

| | 6.6 |

|

| | | 11,356 |

| | 100.0 |

| | 10,049 |

| | 100.0 |

| | 8,679 |

| | 100.0 |

|

As shown above, a substantial portion of the increase in 2013-to-2014 quarter-to-date and year-to-date third-party R&D costs relates to development initiatives associated with zoptarelin doxorubicin, and in particular with our Phase 3 ZoptEC trial initiated in 2013 with Ergomed Clinical Research Ltd. ("Ergomed"), the contract clinical development organization with which, in April 2013, we entered into a co-development and profit sharing agreement. This increase is partially offset by the lower comparative development costs associated with most of our other product candidates.

During the year ended December 31, 2014, ongoing services provided by Ergomed included the conducting of initiation and monitoring visits at various clinical sites, screening and enrolment initiatives, investigation-related management and analysis and regulatory support. ZoptEC-related efforts are progressing in accordance with pre-established timelines. As we continue to closely monitor all initiatives supported by Ergomed, we may decide to revise some of the trial's parameters or expand the scope of work performed by Ergomed, and consequently, total estimated costs in connection with the co-development and revenue sharing agreement may be adjusted. To date, our arrangement with Ergomed has been revised following our decision to open additional clinical sites and to perform additional sub-studies, resulting in estimated cost increases of approximately $1.8 million, as compared to our original estimate.

Excluding the impact of foreign exchange rate fluctuations, we expect net R&D costs for 2015 to slightly decrease, as compared to 2014, due to the realization of cost savings in connection with the Resource Optimization Program, offset partially by slightly higher third-party R&D costs in connection with our Phase 3 ZoptEC trial. Based on currently available information and forecasts, we expect that we will incur net R&D costs of between $21 million and $23 million for the year ended December 31, 2015.

Aeterna Zentaris

2014 Annual MD&A

Selling, general and administrative ("SG&A") expenses were $4.7 million and $13.7 million for the three-month period and the year ended December 31, 2014, respectively, compared to $2.6 million and $12.3 million for the same periods in 2013.

For the three-month period ended December 31, 2014, the increase in SG&A expenses, as compared to the same period in 2013, is mainly related to the deployment of our contracted sales force, which is currently detailing EstroGel®, and higher comparative operating foreign exchange losses.

For the year ended December 31, 2014, the increase in SG&A expenses, as compared to the same period in 2013, is mainly related to higher comparative operating foreign exchange losses, the ramping up of our pre-commercialization activities, the deployment of our contracted sales force related to our co-promotion activities and the recording of restructuring costs related to administrative staff redundancies resulting from the Resource Optimization Program.

During 2015, excluding the impact of foreign exchange rate fluctuations and the recording of transaction costs related to potential financing activities (not currently known or estimable), we expect SG&A expenses to remain broadly in line with expenditures incurred during the year ended December 31, 2014, despite the fact that our contracted sales force is expected to detail EstroGel® during the full year 2015, as compared to less than two months in 2014. This year-over-year increase, associated with our co-promotion activities, is expected to be offset by lower marketing and other pre-commercialization expenses related to Macrilen™ and by lower termination benefit expenses.

Net finance income (costs) are comprised predominantly of the change in fair value of warrant liability and of gains and losses recorded due to changes in foreign currency exchange rates, as presented below.

|

| | | | | | | | | | | | | | | |

| | | Three-month periods ended December 31, | | Years ended December 31, |

| | | 2014 | | 2013 | | 2014 | | 2013 | | 2012 |

| | | $ | | $ | | $ | | $ | | $ |

| Finance income | | | | | | | | | | |

| Change in fair value of warrant liability | | 14,079 |

| | — |

| | 18,272 |

| | 1,563 |

| | 6,746 |

|

| Gains due to changes in foreign currency exchange rates | | 924 |

| | — |

| | 1,879 |

| | — |

| | — |

|

| Interest income | | 50 |

| | 65 |

| | 168 |

| | 185 |

| | 228 |

|

| | | 15,053 |

| | 65 |

| | 20,319 |

| | 1,748 |

| | 6,974 |

|

| Finance costs | | | | | | | | | | |

| Change in fair value of warrant liability | | — |

| | (1,884 | ) | | — |

| | — |

| | — |

|

| Losses due to changes in foreign currency exchange rates | | — |

| | (805 | ) | | — |

| | (1,512 | ) | | (382 | ) |

| | | — |

| | (2,689 | ) | | — |

| | (1,512 | ) | | (382 | ) |

| | | 15,053 |

| | (2,624 | ) | | 20,319 |

| | 236 |

| | 6,592 |

|

The change in fair value of our warrant liability results from the periodic "mark-to-market" revaluation, via the application of the Black-Scholes option pricing model, of currently outstanding share purchase warrants. The Black-Scholes "mark-to-market" warrant valuation most notably has been impacted by the issuance of 8.8 million additional share purchase warrants and by the closing price of our common shares, which, on the NASDAQ, has fluctuated from $0.52 to $1.50 during the year ended December 31, 2014 and from $1.03 to $3.23 for the same period in 2013.

With specific reference to 2014, we recorded substantial fair value gains on our warrant liability, resulting from the significant reduction in our share price following our announcement, in November, that the FDA had issued a CRL in connection with our NDA for Macrilen™. The lower closing price of our shares following our announcement of the CRL has resulted in a lower Black-Scholes valuation of our outstanding share purchase warrants during the fourth quarter of 2014.

Aeterna Zentaris

2014 Annual MD&A

Gains or losses due to changes in foreign currency exchange rates are mainly related to the US dollar, which strengthened against the euro ("EUR") by approximately 4.2% and 12.2%, during the three-month and twelve-month periods ended December 31, 2014, respectively. During the three-month and twelve-month periods ended December 31, 2013, however, the US dollar weakened against the EUR by approximately 2.0% and 4.5%, respectively.

Net income (loss) from continuing operations for the three-month period and the year ended December 31, 2014 was $4.0 million and $(17.2) million, or $0.06 and $(0.29) per basic and diluted share, respectively, compared to $(10.6) million and $(27.2) million, or $(0.28) and $(0.92) per basic and diluted share for the same periods in 2013.

The increase in net income from continuing operations for the three-month period ended December 31, 2014, as compared to the same period in 2013, is due to the higher comparative net finance income, partly offset by higher comparative R&D and SG&A expenses, as presented above.

The decrease in net loss from continuing operations for the year ended December 31, 2014, as compared to the same period in 2013, is due largely to higher comparative net finance income, partly offset by lower comparative license fee revenues and by higher comparative net R&D costs and SG&A expenses, as presented above.

Discontinued Operations

Following a strategic review of our risk and prospects with respect to the manufacturing of Cetrotide® and related activities (collectively, the "Cetrotide® Business"), and, in particular, having taken into account, as discussed below, the previous monetization of the corresponding royalty stream, we decided to transfer all manufacturing rights of Cetrotide® and to discontinue our involvement with the Cetrotide® Business. On April 3, 2013 (the "Effective Date"), we entered into a transfer and service agreement ("TSA") and concurrent agreements with various partners and licensees with respect to our manufacturing rights for Cetrotide®, marketed for therapeutic use as part of in vitro fertilization programs. The principal effect of these agreements was to transfer, effective October 1, 2013 (the "Closing Date"), our manufacturing rights for Cetrotide® to Merck Serono in all territories. Also per the TSA, we agreed to provide certain transition services to Merck Serono over a period of 36 months from the Effective Date in order to assist Merck Serono in managing overall responsibility for the Cetrotide® Business.

Under the TSA, during the period commencing on the Effective Date and ending on the Closing Date (the "Interim Period"), we were obligated to continue to conduct the Cetrotide® Business in the ordinary course in a manner consistent with past practices, subject to certain conditions. Per the TSA, we received a non-refundable, one-time payment of €2.5 million (approximately $3.3 million) in consideration for the transfer of our manufacturing rights referred to above, as well as other payments in exchange for the transfer, also on the Closing Date, of certain assets, such as inventory and equipment used solely for the manufacture of Cetrotide®. We recognized the non-refundable, one-time payment on the Closing Date, as we no longer had managerial involvement or effective control over the manufacturing of goods sold through the Cetrotide® Business. We provide the aforementioned transition services to Merck Serono in exchange for a monthly service fee.

As a result of the transfer of substantially all of the risks and rewards associated with the Cetrotide® Business on the Closing Date, the Cetrotide® Business has been classified as a discontinued operation in the consolidated financial statements. As such, relevant amounts in our consolidated statements of comprehensive (loss) income have been retroactively reclassified to reflect the Cetrotide® Business as a discontinued operation.

Aeterna Zentaris

2014 Annual MD&A

|

| | | | | | | | | | | | | | | |

| | | Three-month periods ended December 31, | | Years ended December 31, |

| (in thousands) | | 2014 | | 2013 | | 2014 | | 2013 | | 2012 |

| | | $ | | $ | | $ | | $ | | $ |

| Revenues | | | | | | | | | | |

| Sales and royalties | | — |

| | 3,057 |

| | — |

| | 63,755 |

| | 30,704 |

|

| License fees and other* | | 118 |

| | 3,717 |

| | 1,037 |

| | 4,589 |

| | 908 |

|

| | | 118 |

| | 6,774 |

| | 1,037 |

| | 68,344 |

| | 31,612 |

|

| Operating expenses | | | | | | | | | | |

| Cost of sales | | — |

| | 3,071 |

| | — |

| | 30,002 |

| | 26,229 |

|

| Research and development costs, net of tax credits and grants | | 8 |

| | — |

| | 25 |

| | 8 |

| | 12 |

|

| Selling, general and administrative expenses | | (48 | ) | | 1,350 |

| | 389 |

| | 4,279 |

| | 2,639 |

|

| | | (40 | ) | | 4,421 |

| | 414 |

| | 34,289 |

| | 28,880 |

|

| Net income from discontinued operations | | 158 |

| | 2,353 |

| | 623 |

| | 34,055 |

| | 2,732 |

|

_________________________

| |

| * | Includes the non-refundable, one-time payment made by Merck Serono in exchange for the manufacturing rights for Cetrotide®and revenues from certain transition services provided pursuant to the aforementioned agreement. |

The decrease in sales and royalties from discontinued operations, in cost of sales from discontinued operations and in SG&A expenses from discontinued operations during the three-month period and the year ended December 31, 2014, as compared to the same periods in 2013, reflects the fact that we recorded no sales of Cetrotide® and royalties during the three-month period and the year ended December 31, 2014, as compared to the corresponding period of 2013, given that the transfer of the Cetrotide® Business was effective on October 1, 2013.

Net income (loss)

Net income (loss) for the three-month period and the year ended December 31, 2014 was $4.2 million and $(16.6) million, or $0.06 and $(0.28) per basic and diluted share, respectively, compared to $(8.2) million and $6.8 million, or $(0.22) and $0.24 per basic and diluted share, for the same periods in 2013.

The increase in net income for the three-month period ended December 31, 2014, as compared to the same period in 2013, is due largely to higher comparative net finance income, offset partially by higher comparative operating expenses and by lower net income from discontinued operations.

The decrease in net income for the year ended December 31, 2014, as compared to the same period in 2013, is due largely to higher loss from operations and to lower net income from discontinued operations, partially offset by higher comparative net finance income.

2013 compared to 2012

Revenues

License fees and other revenues were $6.1 million for the year ended December 31, 2013, as compared to $1.2 million for the same period in 2012.

In March 2011, we entered into an agreement with Yakult for the development, manufacture and commercialization of perifosine in all human uses, excluding leishmaniasis, in Japan. Under the terms of this agreement, Yakult had made an initial, non-refundable gross upfront payment to the Company of approximately $8.4 million. We recorded this upfront payment as deferred revenues and commenced amortizing the underlying proceeds on a straight-line basis over the estimated life cycle of perifosine in colorectal cancer ("CRC") and multiple myeloma ("MM").

Aeterna Zentaris

2014 Annual MD&A

On April 1, 2012, following negative results of a Phase 3 study of perifosine in CRC, we discontinued the perifosine program in that indication. Furthermore, in March 2013, following an analysis of interim results of the Phase 3 study of perifosine in MM, we also discontinued the development of perifosine in the MM indication. Given these results and the termination of these studies, we determined that we no longer had significant obligations under the agreement with Yakult to continue with the development of perifosine, and we recognized, in March 2013, the remaining unamortized amount of deferred revenue of $5.9 million related to the above licensing agreement.

On a year-over-year basis, the increase in license fees and other revenues is therefore attributable to the earlier-than-expected recognition of the previously deferred upfront license payment received from Yakult, following the discontinuance of our development of perifosine and given that the earnings process associated with this compound as pertaining to the upfront proceeds received was deemed to be complete.

Operating Expenses

R&D costs, net of refundable tax credits and grants, were $21.3 million for the year ended December 31, 2013, compared to $20.6 million for the same period in 2012.

Third-party R&D costs were $10.0 million for the year ended December 31, 2013, as compared to $8.7 million for the same period in 2012. This increase mainly results from the higher development costs associated with zoptarelin doxorubicin, and in particular with our Phase 3 ZoptEC trial initiated in 2013 with Ergomed, as discussed above. Additionally, we incurred higher development costs in 2013 related to Macrilen™ and macimorelin, primarily consisting of the purchase of active pharmaceutical ingredients. These increases were partly offset by the lower comparative development costs associated with perifosine, given that we have decided not to make any further investment in this product candidate, as discussed above, and by the lower preclinical study-related costs associated with our Erk/PI3K inhibitors program.

Third-party R&D costs also increased during the year ended December 31, 2013 due to higher expenditures associated with our disorazol Z product candidates, pursuant to a variety of collaboration agreements with various universities and institutes, and to the purchase of active pharmaceutical ingredients.

Selling, general and administrative ("SG&A") expenses were $12.3 million for the year ended December 31, 2013, compared to $10.6 million for the same period in 2012. This increase is mainly related to the recognition in the second quarter of 2013 of non-recurring termination benefits (approximately $1.4 million) paid to our former Chief Executive Officer and to the recording of related non-cash share-based compensation costs, amounting to approximately $0.7 million.

Net finance income totaled $0.2 million for the year ended December 31, 2013, as compared to $6.6 million for the same period in 2012. This decrease is mainly due to the decrease in net gain related to the change in fair value of our warrant liability and the increase in losses due to changes in foreign currency exchange rates.

The change in fair value of our warrant liability results from the "mark-to-market" revaluation, via the application of the Black-Scholes option pricing model, of currently outstanding share purchase warrants. The Black-Scholes "mark-to-market" warrant valuation most notably has been impacted by the closing price of our common shares, which, on the NASDAQ, fluctuated between $1.03 and $3.23 during the year ended December 31, 2013.

Gains or losses due to changes in foreign currency exchange rates are mainly related to the US dollar, which weakened against the EUR by approximately 3.3% from 2012 to 2013.

Net loss from continuing operations for the year ended December 31, 2013 was $27.2 million, or $0.92 per basic and diluted share, compared to $23.1 million or $1.17 per basic and diluted share for the same period in 2012.

The increase in net loss from continuing operations for the year ended December 31, 2013, as compared to 2012, is due largely to the recording of non-recurring termination benefits and related non-cash share-based compensation costs, lower comparative net finance income and higher comparative net R&D costs, partially offset by higher comparative license fee revenues, largely associated with the accelerated recognition of remaining net unamortized amount of deferred revenues related to the licensing agreement entered into with Yakult, as discussed above.

Aeterna Zentaris

2014 Annual MD&A

Discontinued Operations

Sales and royalties related to discontinued operations were comprised of both net sales of Cetrotide® and royalties, which represented the amortization, under the units-of-revenue method, of the proceeds received pursuant to a transaction with Healthcare Royalty Partners L.P. (formerly Cowen Healthcare Royalty Partners L.P.) ("HRP"), in which we monetized our royalty stream related to Cetrotide®. In this transaction, we had received a payment of $52.5 million, less certain transaction costs, from HRP in exchange for our rights to royalties on future net sales of Cetrotide® generated by Merck Serono.

We had initially recorded the proceeds received from HRP as deferred revenue due to our then significant continuing involvement with the Cetrotide® Business. However, as of the Closing Date, there was no basis to continue amortizing the deferred revenue associated with HRP, primarily due to the fact that we no longer had significant continuing involvement in the Cetrotide® Business. As such, commencing on the Effective Date, we accelerated the amortization of the remaining deferred revenues of approximately $31.9 million over the Interim Period, by continuing to apply the units-of-revenue method, which is consistent with past practice. The remaining deferred revenues were fully amortized through the end of September 2013.

Sales and royalties from discontinued operations were $63.8 million for the year ended December 31, 2013, as compared to $30.7 million for the same period in 2012. This increase is primarily due to the accelerated amortization of deferred revenues mentioned above.

The substantial license fees and other revenues from discontinued operations recorded during the year ended December 31, 2013, and as compared to the years ended December 31, 2012 and 2014, are primarily attributable to the recognition, on the Closing Date, of the non-refundable, one-time payment made by Merck Serono, as discussed above.

Cost of sales from discontinued operations were $30.0 million for the year ended December 31, 2013, as compared to $26.2 million for the same period in 2012. Cost of sales from discontinued operations increased in 2013, as compared to 2012, as a result of the higher comparative volume of Cetrotide® product sales, including the sale of inventory assets to Merck Serono, as mentioned above.

For the year ended December 31, 2013, cost of sales as a percentage of sales and royalties decreased to approximately 47.1%, as compared to 85.4% for the same period in 2012, predominantly due to the accelerated recognition of royalties as mentioned above.

SG&A expenses from discontinued operations amounted to $4.3 million for the year ended December 31, 2013, as compared to $2.6 million for the same period in 2012. The year-over-year increase is largely attributable to the recording of a provision for certain non-cancellable contracts related to the Cetrotide® Business that were deemed onerous due to the fact that management expected no economic benefits to flow to the Company following the transfer of the Cetrotide® Business on the Closing Date. The provisions for onerous contracts recognized total $1.3 million and represent the present value of estimated unavoidable future royalty and patent costs associated with the intellectual property underlying Cetrotide®.

Net income from discontinued operations was $34.1 million for the year ended December 31, 2013, as compared to $2.7 million for the same period in 2012. The comparative increase reflects the net impact of items discussed above, and in particular, are influenced in large part by the inclusion of the accelerated recognition of previously deferred remaining HRP-related revenues as discontinued operations.

Net income (loss) for the year ended December 31, 2013 was $6.8 million, or $0.24 per basic and diluted share, compared to $(20.4) million, or $(1.03) per basic and diluted share for the same period in 2012.

The comparative year-over-year decrease in net loss is mainly due to higher net income from discontinued operations and higher revenues, partially compensated by higher operating costs and lower finance income.

Aeterna Zentaris

2014 Annual MD&A

Quarterly Consolidated Results of Operations Information

|

| | | | | | | | | | | | |

| (in thousands, except for per share data) | | Three-month periods ended |

| | | December 31, 2014 | | September 30, 2014 | | June 30, 2014 | | March 31, 2014 |

| | | $ | | $ | | $ | | $ |

| Revenues | | 11 |

| | — |

| | — |

| | — |

|

| Loss from operations | | (10,947 | ) | | (9,843 | ) | | (8,410 | ) | | (8,195 | ) |

| Net income (loss) from continuing operations | | 3,995 |

| | (11,629 | ) | | (5,249 | ) | | (4,304 | ) |

| Net income (loss) | | 4,153 |

| | (11,337 | ) | | (5,024 | ) | | (4,356 | ) |

| Net income (loss) per share from continuing operations (basic and diluted)* | | 0.06 |

| | (0.20 | ) | | (0.09 | ) | | (0.08 | ) |

| Net income (loss) per share (basic and diluted)* | | 0.06 |

| | (0.20 | ) | | (0.09 | ) | | (0.08 | ) |

|

| | | | | | | | | | | | |

| (in thousands, except for per share data) | | Three-month periods ended |

| | | December 31, 2013 | | September 30, 2013 | | June 30, 2013 | | March 31, 2013 |

| | | $ | | $ | | $ | | $ |

| Revenues | | — |

| | 17 |

| | 96 |

| | 6,062 |

|

| Loss from operations | | (7,972 | ) | | (8,648 | ) | | (9,693 | ) | | (1,163 | ) |

| Net (loss) income from continuing operations | | (10,596 | ) | | (7,799 | ) | | (9,848 | ) | | 1,003 |

|

| Net (loss) income | | (8,243 | ) | | 3,842 |

| | 9,330 |

| | 1,886 |

|

| Net (loss) income per share from continuing operations (basic and diluted)* | | (0.28 | ) | | (0.26 | ) | | (0.39 | ) | | 0.04 |

|

| Net (loss) income per share (basic and diluted)* | | (0.22 | ) | | 0.13 |

| | 0.37 |

| | 0.07 |

|

_________________________

| |

| * | Net income (loss) per share is based on the weighted average number of shares outstanding during each reporting period, which may differ on a quarter-to-quarter basis. As such, the sum of the quarterly net income (loss) per share amounts may not equal year-to-date net (loss) income per share. |

Historical quarterly results of operations and net income (loss) from continuing operations cannot be taken as reflective of recurring revenue or expenditure patterns or of predictable trends, largely given the non-recurring nature of certain components of our historical revenues due most notably to the accelerated recognition of upfront payments and to unpredictable quarterly variations attributable to our net finance income (costs), which in turn are comprised of the impact of the periodic "mark-to-market" revaluation of our warrant liability and of foreign exchange gains and losses. Additionally, our net R&D costs historically have varied on a quarter-over-quarter basis due to the ramping up or winding down of potential product candidate activities, which in turn are dependent upon a number of factors that often do not occur on a linear or predictable basis.

More recently, our SG&A expenses have increased on a quarter-over-quarter basis due to the ramping up of pre-commercialization activities associated with Macrilen™ (prior to the receipt of the CRL from the FDA) and to the deployment of our contracted sales force related to our co-promotion activities associated with EstroGel®.

In addition to the items referred to above, our net income (loss) also has been impacted by net variations attributable to the Cetrotide® Business, which, as discussed above, has been presented on a retrospective basis within discontinued operations.

Aeterna Zentaris

2014 Annual MD&A

Consolidated Statement of Financial Position Information

|

| | | | | | |

| | | As at December 31, |

| (in thousands) | | 2014 | | 2013 |

| | | $ | | $ |

Cash and cash equivalents1 | | 34,931 |

| | 43,202 |

|

| Trade and other receivables and other current assets | | 1,286 |

| | 2,453 |

|

| Restricted cash equivalents | | 760 |

| | 865 |

|

| Property, plant and equipment | | 797 |

| | 1,351 |

|

| Other non-current assets | | 9,661 |

| | 11,325 |

|

| Total assets | | 47,435 |

| | 59,196 |

|

Payables and other current liabilities2 | | 7,304 |

| | 7,242 |

|

| Current portion of deferred revenues | | 270 |

| | — |

|

| Warrant liability | | 8,225 |

| | 18,010 |

|

Non-financial non-current liabilities3 | | 17,152 |

| | 16,880 |

|

| Total liabilities | | 32,951 |

| | 42,132 |

|

| Shareholders' equity | | 14,484 |

| | 17,064 |

|

| Total liabilities and shareholders' equity | | 47,435 |

| | 59,196 |

|

_________________________

1 Of which approximately $3.6 million was denominated in EUR as at December 31, 2014.

2 Of which approximately $1.5 million is related to a provision for restructuring costs.

3 Comprised mainly of employee future benefits, provisions for onerous contracts and non-current portion of deferred revenues.

The decrease in cash and cash equivalents as at December 31, 2014, as compared to December 31, 2013, is due to variations in components of our working capital and to recurring disbursements, as well as to the effect of exchange rate fluctuations, partially offset by the receipt of net proceeds of $12.2 million in connection with the January 2014 Offering, of $11.9 million pursuant to drawdowns made under the May 2014 ATM Program and of $0.3 million pursuant to drawdowns made under a previous ATM sales agreement program, entered into in May 2013 and discontinued in connection with the implementation of the May 2014 ATM Program.

The decrease in trade and other receivables and other current assets as at December 31, 2014, as compared to December 31, 2013, is mainly due to lower trade accounts receivable related to discontinued operations.

The decrease in other non-current assets as at December 31, 2014, as compared to December 31, 2013, is primarily due to the lower comparative exchange rate of the EUR against the US dollar, which weakened from December 31, 2013 to December 31, 2014. The decrease is also due to the net reduction in the carrying value of our identifiable intangible assets, for which we recognized an impairment loss of approximately $0.2 million, pursuant to the implementation of the Resource Optimization Program, discussed above.

The increase in payables and other current liabilities as at December 31, 2014, as compared to December 31, 2013, is due to the recording of a provision for restructuring costs related to the Resource Optimization Program, discussed above, to the higher comparative trade accounts payable balances due to the increased number of patients that have been entered into our ZoptEC Phase 3 program and to costs incurred in connection with the deployment of our contracted sales force, partially offset by lower comparative trade accounts payable balances related to the Cetrotide® Business as well as by the lower comparative exchange rate of the EUR against the US dollar.

Aeterna Zentaris

2014 Annual MD&A

Our warrant liability decreased from December 31, 2013 to December 31, 2014. The decrease is due to net fair value revaluation gains of $18.3 million, which were recorded pursuant to our periodic "mark-to-market" revaluation of the underlying outstanding share purchase warrants, as discussed above and was partly offset by the issuance of 8.8 million additional share purchase warrants in connection with the January 2014 Offering, which initially had increased our warrant liability by $8.5 million.

The decrease in shareholders' equity as at December 31, 2014, as compared to December 31, 2013, is mainly attributable to the increase in our deficit due to the recording of net loss and actuarial loss on pension-related employee benefit obligation and to the increase in our accumulated other comprehensive loss due to foreign currency translation adjustments, partly offset by the increase in our share capital following the issuance of common shares discussed above.

Financial Liabilities, Obligations and Commitments

We have certain contractual lease obligation commitments as well as other long-term obligations related to unfunded benefit pension plans and unfunded post-employment benefit plans. The following tables summarize future cash requirements with respect to these obligations.

Expected future minimum lease payments and future minimum sublease receipts under non-cancellable operating leases (subleases) as well as future payments in connection with utility service agreements are as follows:

|

| | | | | | |

| | | As at December 31, 2014 |

| (in thousands) | | Minimum lease payments | | Sublease income |

| | | $ | | $ |

| Less than 1 year | | 1,678 |

| | (392 | ) |

| 1 – 3 years | | 1,352 |

| | (493 | ) |

| 4 – 5 years | | 325 |

| | (19 | ) |

| Total | | 3,355 |

| | (904 | ) |

With regard to our lease arrangement in Germany for laboratory, office and storage space, we do not expect to renew the agreement beyond the end of its original term (expiry of March 2016), and we are examining options for alternative space to accommodate remaining German-based staff. As such, the minimum lease payments presented above exclude any lease payments for our German subsidiary beyond March 2016.

In accordance with the assumptions used in our employee future benefits obligation calculation as at December 31, 2014, undiscounted benefits expected to be paid are as follows:

|

| | | |

| (in thousands) | | $ |

| Less than 1 year | | 495 |

|

| 1 – 3 years | | 1,014 |

|

| 4 – 5 years | | 1,084 |

|

| More than 5 years | | 19,867 |

|

| Total | | 22,460 |

|

Outstanding Share Data

As at March 16, 2015, we had 90,557,142 common shares issued and outstanding, as well as 3,885,200 stock options outstanding. Warrants outstanding as at March 16, 2015 represented a total of 116,887,987 equivalent common shares.

Aeterna Zentaris

2014 Annual MD&A

Capital Disclosures

Our objective in managing capital, consisting of shareholders' equity, with cash and cash equivalents and restricted cash equivalents being its primary components, is to ensure sufficient liquidity to fund R&D activities, selling, general and administrative expenses, working capital and capital expenditures.

Over the past several years, we have increasingly raised capital via public equity offerings and drawdowns under various ATM sales programs as our primary source of liquidity.

Our capital management objective remains the same as that in previous periods. The policy on dividends is to retain cash to keep funds available to finance the activities required to advance our product development portfolio and to pursue appropriate commercial opportunities as they may arise.

We are not subject to any capital requirements imposed by any regulators or by any other external source.

Liquidity, Cash Flows and Capital Resources

Our operations and capital expenditures have been financed through certain transactions impacting our cash flows from operating activities, public equity offerings, as well as from the drawdowns under various ATM programs.

Based on our assessment, which took into account current cash levels, as well as our strategic plan and corresponding budgets and forecasts, we believe that we have sufficient liquidity and financial resources to fund planned expenditures and other working capital needs for at least, but not limited to, the 12-month period following the statement of financial position date of December 31, 2014.

We may endeavour to secure additional financing, as required, through strategic alliance arrangements or through other activities, as well as via the issuance of new share capital or other securities.

Aeterna Zentaris

2014 Annual MD&A

The variations in our cash and cash equivalents by activity are explained below.

|

| | | | | | | | | | | | | | | |

| (in thousands) | | Three-month periods ended December 31, | | Years ended December 31, |

| | | 2014 | | 2013 | | 2014 | | 2013 | | 2012 |

| | | $ | | $ | | $ | | $ | | $ |

| Cash and cash equivalents - Beginning of period | | 41,952 |

| | 24,829 |

| | 43,202 |

| | 39,521 |

| | 46,881 |

|

| Cash flows from operating activities: | | | | | | | | | | |

| Cash used in operating activities from continuing operations | | (8,676 | ) | | (6,184 | ) | | (30,787 | ) | | (30,131 | ) | | (25,681 | ) |

| Cash provided by (used in) operating activities from discontinued operations | | 93 |

| | 9,622 |

| | (295 | ) | | 10,147 |

| | (5,134 | ) |

| | | (8,583 | ) | | 3,438 |

| | (31,082 | ) | | (19,984 | ) | | (30,815 | ) |

| Cash flows from financing activities: | | | | | | | | | | |

| Net proceeds from issuance of common shares and warrants | | 2,075 |

| | 14,795 |

| | 24,358 |

| | 23,708 |

| | 23,619 |

|

| Net proceeds from the exercise of share purchase warrants and other | | — |

| | — |

| | — |

| | — |

| | 589 |

|

| | | 2,075 |

| | 14,795 |

| | 24,358 |

| | 23,708 |

| | 24,208 |

|

| | | | | | | | | | | |

| Cash flows from investing activities: | | | | | | | | | | |

| Net cash used in provided by investing activities from continuing operations | | (4 | ) | | (21 | ) | | (61 | ) | | (85 | ) | | (272 | ) |

| Net cash provided by investing activities from discontinued operations | | — |

| | 113 |

| | — |

| | 113 |

| | — |

|

| | | (4 | ) | | 92 |

| | (61 | ) | | 28 |

| | (272 | ) |

| | | | | | | | | | | |

| Effect of exchange rate changes on cash and cash equivalents | | (509 | ) | | 48 |

| | (1,486 | ) | | (71 | ) | | (481 | ) |

| Cash and cash equivalents - End of period | | 34,931 |

| | 43,202 |

| | 34,931 |

| | 43,202 |

| | 39,521 |

|

Operating Activities

2014 compared to 2013

Cash flows (used in) provided by operating activities were $(8.6) million and $(31.1) million for the three-month period and the year ended December 31, 2014, respectively, compared to $3.4 million and $(20.0) million for the same periods in 2013. The significant increase in cash flows used in operating activities for the three-month period ended December 31, 2014 as compared to the same period in 2013 is due to severance payments made in connection with the Resource Optimization Program, the comparative increase in R&D expenditures, mainly related to our ZoptEC trial and in SG&A expenditures, mainly related to the deployment of our contract sales force and other commercial activities. Additionally, the overall increase in cash used in operating activities was due to variations associated with our discontinued operations, following the transfer of the Cetrotide® Business in the fourth quarter of 2013, as discussed above. This increase is partly offset by the receipt of the Transfer Fee in connection with the agreements entered into with Sinopharm, as discussed above.

The significant increase in cash used in operating activities for the year ended December 31, 2014 as compared to the same period in 2013 is mainly due to the variations associated with our discontinued operations, following the transfer of the Cetrotide® Business in the fourth quarter of 2013, as discussed above.

Aeterna Zentaris

2014 Annual MD&A

We expect net cash used in operating activities to range from $33 million to $35 million for the year ended December 31, 2015, mainly as we continue to invest in our ZoptEC Phase 3 program and related substudies, as we carry out initiatives related to the co-promotion of EstroGel® and as we continue making severance payments in connection with the Resource Optimization Program. This guidance may vary significantly in future periods, most notably in light of ongoing business development initiatives, as discussed further below.

2013 compared to 2012

Cash flows used in operating activities were $20.0 million and $30.8 million for the years ended December 31, 2013 and 2012, respectively. The significant decrease in cash flows used in operating activities is mainly due to the cash provided by operating activities from discontinued operations as a result of the change in operating assets and liabilities and to the receipt in 2013, of the non-refundable, one-time payment from Merck Serono pursuant to the transfer of the Cetrotide® Business, as discussed above. This decrease is partly offset by the increase in cash used in operating activities from continuing operations, which is explained by the comparable increase in R&D and SG&A expenditures, mainly related to the zoptarelin doxorubicin and Macrilen™ projects, as well as by lower cash flows provided by license fee revenues.

Financing Activities

2014 compared to 2013

Cash flows provided by financing activities were $2.1 million and $24.4 million for the three-month period and the year ended December 31, 2014, respectively, compared to $14.8 million and $23.7 million for the same periods in 2013. The decrease for the three-month period ended December 31, 2014, as compared to the same period in 2013 is due to lower net proceeds received from the issuance of common shares and warrants.

Critical Accounting Policies, Estimates and Judgments

Our consolidated financial statements as at December 31, 2014 and December 31, 2013 and for the years ended December 31, 2014, 2013 and 2012 have been prepared in accordance with IFRS as issued by the IASB.

The preparation of consolidated financial statements in accordance with IFRS requires management to make judgments, estimates and assumptions that affect the reported amounts of our assets, liabilities, revenues, expenses and related disclosures. Judgments, estimates and assumptions are based on historical experience, expectations, current trends and other factors that management believes to be relevant at the time at which our consolidated financial statements are prepared.

Management reviews, on a regular basis, the Company's accounting policies, assumptions, estimates and judgments in order to ensure that the consolidated financial statements are presented fairly and in accordance with IFRS. Revisions to accounting estimates are recognized in the period in which the estimates are revised and in any future periods affected.

A summary of those critical accounting estimates and assumptions, as well as critical judgments used in applying accounting policies in the preparation of our consolidated financial statements, can be found in note 3 to our consolidated financial statements as at December 31, 2014 and December 31, 2013 and for the years ended December 31, 2014, 2013 and 2012.

Recent Accounting Pronouncements

Adopted in 2014

The following new standards and amendments to standards are effective for the first time for interim periods beginning on or after January 1, 2014 and have been applied in preparing our consolidated financial statements. The accounting policies have been applied consistently by all subsidiaries of the Company.

In May 2013, the IASB made amendments to the disclosure requirements of IAS 36, Impairment of Assets, requiring disclosure, in certain instances, of the recoverable amount of an asset or cash-generating unit, and the basis for the determination of fair value less costs of disposal, when an impairment loss is recognized or when an impairment loss is subsequently reversed.

Aeterna Zentaris

2014 Annual MD&A

In May 2013, the IFRS Interpretations Committee ("IFRIC") issued International Financial Reporting Standard Interpretation 21, Levies ("IFRIC 21"), an interpretation on the accounting for levies imposed by governments. IFRIC 21 is an interpretation of IAS 37, Provisions, Contingent Liabilities and Contingent Assets ("IAS 37"). IAS 37 sets out criteria for the recognition of a liability, one of which is the requirement for the entity to have a present obligation as a result of a past event (known as an obligating event). IFRIC 21 clarifies that the obligating event that gives rise to a liability to pay a levy is the activity described in the relevant legislation that triggers the payment of the levy.

The adoption of these standards and amendments did not have a significant impact on our consolidated financial statements.

Not yet adopted

The final version of IFRS 9, Financial instruments ("IFRS 9"), was issued by the IASB in July 2014 and will replace IAS 39 Financial Instruments: Recognition and Measurement. IFRS 9 introduces a model for classification and measurement, a single, forward-looking expected loss impairment model and a substantially reformed approach to hedge accounting. The new single, principle-based approach for determining the classification of financial assets is driven by cash flow characteristics and the business model in which an asset is held. The new model also results in a single impairment model being applied to all financial instruments, which will require more timely recognition of expected credit losses. It also includes changes in respect of an entity's own credit risk in measuring liabilities elected to be measured at fair value, so that gains caused by the deterioration of an entity's own credit risk on such liabilities are no longer recognized in profit or loss. IFRS 9, which is to be applied retrospectively, is effective for annual periods beginning on or after January 1, 2018 and is available for early adoption. In addition, an entity's own credit risk changes can be applied early in isolation without otherwise changing the accounting for financial instruments. We are currently assessing the impact, if any, that this new standard will have on our consolidated financial statements.

In May 2014, the IASB issued IFRS 15, Revenue from Contracts with Customers. The objective of this new standard is to provide a single, comprehensive revenue recognition framework for all contracts with customers to improve comparability of financial statements of companies globally. This new standard contains principles that an entity will apply to determine the measurement of revenue and timing of when it is recognized. The underlying principle is that an entity will recognize revenue to depict the transfer of goods or services to customers at an amount that the entity expects to be entitled to receive in exchange for those goods or services. This new standard is effective for annual periods beginning on or after January 1, 2017. We are currently assessing the impact that this new standard may have on our consolidated financial statements.

Outlook for 2015

Commercial Development

With our focus to become a growth-oriented, commercially operating specialty biopharmaceutical organization, and in addition to our commitment to developing key product candidates in our existing pipeline, we expect to continue to evaluate potential in-licensing and/or acquisition opportunities, as well as additional co-promotional arrangements related to targeted commercial products.

Zoptarelin doxorubicin

With regard to our ZoptEC Phase 3 study in collaboration with Ergomed, we will continue to monitor patient enrollment in North America, Europe and Israel, such that we are able to secure a first interim analysis during the first half of 2015. We also expect to complete patient recruitment for this trial before year-end 2015.

Macrilen™

We intend to make a decision regarding the future development of Macrilen™ in the near term, taking into account various considerations, including our prior and upcoming discussions with the FDA.

Erk Inhibitors Development Program

For this program, we expect to select an optimized molecule for development in the first half of 2015.

Aeterna Zentaris

2014 Annual MD&A

Summary of key expectations for revenues, operating expenditures and cash flows

Having entered into the Co-promotion Agreement with ASCEND, we expect to generate sales commission revenue in 2015 pursuant to the initiation of sales coverage in the agreed-upon territories and as we begin to exceed certain minimum agreed-upon thresholds. Further, having entered into the master collaboration agreement, TTA and LA with Sinopharm, we will commence recognition of the amortization of deferred revenues related to the Transfer Fee.

For the year ended December 31, 2015, we expect that R&D costs will range between $21 million and $23 million. Our R&D costs are expected to decrease in 2015, as compared to 2014, mainly as a result of the implementation of our Resource Optimization Program, as discussed above.

Our main focus for R&D efforts will continue to be on our later-stage compound, zoptarelin doxorubicin and its Phase 3 ZoptEC study, as discussed above, where we anticipate substantial investment to fund ongoing development initiatives.

Excluding the impact of foreign exchange rate fluctuations, our SG&A expenses are expected to remain consistent in 2015, as compared to 2014.

Excluding any foreign exchange impacts, as well as income from new business development initiatives, we expect that our overall operating burn in 2015 will range from $33 million to $35 million as we continue to fund operating activities and working capital requirements.

Financial Risk Factors and Other Instruments

Fair value risk

As noted above, the change in our warrant liability, which is measured at fair value through profit or loss, results from the periodic "mark-to-market" revaluation, via the application of the Black-Scholes option pricing model, of currently outstanding share purchase warrants. The Black-Scholes valuation is impacted, among other inputs, by the market price of our common shares. As a result, the change in fair value of the warrant liability, which is reported as finance income (cost) in our consolidated statements of comprehensive income (loss), has been and may continue in future periods to be materially affected by changes in our common share closing price, which has ranged from $0.52 to $1.50 on the NASDAQ during the year ended December 31, 2014.

If variations in the market price of our common shares of -10% and +10% were to occur, the impact on our net loss for the warrant liability held at December 31, 2014 would be as follows:

|

| | | | | | | | | |

| (in thousands) | | Carrying

amount | | -10% | | +10% |

| | | $ | | $ | | $ |

| Warrant liability | | 8,225 |

| | 1,117 |

| | (1,147 | ) |

| Total impact on net loss – decrease / (increase) | | | | 1,117 |

| | (1,147 | ) |

Foreign currency risk

Since we operate internationally, we are exposed to currency risks as a result of potential exchange rate fluctuations related to non-intragroup transactions. In particular, fluctuations in the US dollar exchange rates against the EUR could have a significant impact on our results of operations.

Aeterna Zentaris

2014 Annual MD&A

If foreign exchange rate variations of -5% (depreciation of the EUR) and +5% (appreciation of the EUR) against the US$, from period-end rates of EUR1 = US$1.2101 were to occur, the impact on our net loss for each category of financial instruments held at December 31, 2014 would be as follows:

|

| | | | | | | | | |

| | | | | Balances denominated in US$ |

| (in thousands) | | Carrying

amount | | -5% | | +5% |

| | | $ | | $ | | $ |

| Cash and cash equivalents | | 25,184 |

| | 1,259 |

| | (1,259 | ) |

| Warrant liability | | 8,225 |

| | (411 | ) | | 411 |

|

| Total impact on net loss – decrease / (increase) | | | | 848 |

| | (848 | ) |

Liquidity risk

Liquidity risk is the risk that we will not be able to meet our financial obligations as they become due. We manage this risk through the management of our capital structure and by continuously monitoring actual and projected cash flows. Our Board of Directors reviews and approves our operating and capital budgets, as well as any material transactions out of the ordinary course of business. We have adopted an investment policy in respect of the safety and preservation of our capital to ensure our liquidity needs are met. The instruments are selected with regard to the expected timing of expenditures and prevailing interest rates.

We believe that we have sufficient funds to pay our ongoing general and administrative expenses, to pursue our R&D activities and to meet our obligations and existing commitments as they fall due at least through December 31, 2015. In making this assessment, we took into account all available information about the future, which is at least, but not limited to, twelve months from the end of the most recent reporting period. We expect to continue to incur operating losses and may require significant capital to fulfill our future obligations. Our ability to continue future operations beyond December 31, 2015 and to fund our activities is dependent on our ability to secure additional funding, which may be completed in a number of ways, including but not limited to licensing arrangements, partnerships, share and other security issuances and other financing activities. We will pursue such additional sources of financing when required, and while we have been successful in securing financing in the past, there can be no assurance we will be able to do so in the future or that these sources of funding or initiatives will be available for the Company or that they will be available on terms which are acceptable to us.

Credit risk