QuickLinks -- Click here to rapidly navigate through this document

As filed with the Securities and Exchange Commission on March 18, 2008

Registration No. 333-145547

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 7 TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

CardioNet, Inc.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) | 8090 (Primary Standard Industrial Classification Code Number) | 33-0604557 (I.R.S. Employer Identification Number) |

1010 Second Avenue

San Diego, California 92101

(619) 243-7500

(Address, including zip code, and telephone number, including

area code, of registrant's principal executive offices)

Arie Cohen

President and

Chief Executive Officer

CardioNet, Inc.

1010 Second Avenue

San Diego, California 92101

(619) 243-7500

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Frederick T. Muto, Esq. Ethan E. Christensen, Esq. Cooley Godward Kronish LLP 4401 Eastgate Mall San Diego, California 92121 (858) 550-6000 | Donald J. Murray, Esq. Dewey & LeBoeuf LLP 1301 Avenue of the Americas New York, New York 10019 (212) 259-8000 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended (the "Securities Act"), check the following box. o

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. o

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered | Proposed maximum aggregate offering price(1) | Amount of registration fee | ||

|---|---|---|---|---|

| Common Stock, $0.001 par value per share | $78,200,000 | $3,073(2) | ||

- (1)

- Estimated solely for the purpose of calculating the amount of the registration fee in accordance with Rule 457(o) under the Securities Act of 1933, as amended. Includes $10,200,000 of shares that the underwriters have the option to purchase to cover over-allotments, if any.

- (2)

- Previously paid.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment that specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. Neither we nor the selling stockholder may sell or accept an offer to buy these securities under this preliminary prospectus until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities, and neither we nor the selling stockholder are soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to completion, dated March 18, 2008

PROSPECTUS

3,400,000 Shares

Common Stock

CardioNet, Inc. is selling 3,000,000 shares of common stock. The selling stockholder included in this prospectus is selling an additional 400,000 shares of common stock. We will not receive any proceeds from the sale of shares of common stock by the selling stockholder.

This is the initial public offering of our common stock. The estimated initial public offering price is between $18.00 and $20.00 per share.

Prior to this offering, there has been no public market for our common stock. Our common stock has been approved for listing on the Nasdaq Global Market under the symbol "BEAT."

Investing in our common stock involves a high degree of risk. See "Risk Factors" beginning on page 11.

| | Per share | Total | ||||

|---|---|---|---|---|---|---|

| Initial public offering price | $ | $ | ||||

| Underwriting discounts and commissions | $ | $ | ||||

| Proceeds to CardioNet, before expenses | $ | $ | ||||

| Proceeds to selling stockholder, before expenses | $ | $ | ||||

The selling stockholder has granted the underwriters an option for a period of 30 days to purchase up to 510,000 additional shares of common stock on the same terms and conditions set forth above to cover over-allotments, if any.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of common stock to investors on , 2008.

| Citi | ||

Lehman Brothers | ||

Leerink Swann | Thomas Weisel Partners LLC | |

| | Page | |

|---|---|---|

| PROSPECTUS SUMMARY | 1 | |

| RISK FACTORS | 11 | |

| FORWARD-LOOKING STATEMENTS | 28 | |

| USE OF PROCEEDS | 29 | |

| DIVIDEND POLICY | 30 | |

| CAPITALIZATION | 31 | |

| DILUTION | 34 | |

| UNAUDITED PRO FORMA CONSOLIDATED STATEMENTS OF OPERATIONS | 38 | |

| SELECTED CONSOLIDATED FINANCIAL DATA | 42 | |

| MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 43 | |

| BUSINESS | 61 | |

| MANAGEMENT | 85 | |

| EXECUTIVE COMPENSATION | 92 | |

| RELATED PARTY TRANSACTIONS | 116 | |

| PRINCIPAL STOCKHOLDERS AND SELLING STOCKHOLDER | 121 | |

| DESCRIPTION OF CAPITAL STOCK | 124 | |

| MATERIAL U.S. FEDERAL INCOME TAX CONSEQUENCES TO NON-U.S. HOLDERS | 130 | |

| SHARES ELIGIBLE FOR FUTURE SALE | 133 | |

| UNDERWRITING | 136 | |

| LEGAL MATTERS | 141 | |

| EXPERTS | 141 | |

| WHERE YOU CAN FIND ADDITIONAL INFORMATION | 142 | |

| INDEX TO CONSOLIDATED FINANCIAL STATEMENTS | F-1 |

You should rely only on the information contained in this prospectus and any free writing prospectus prepared by or on behalf of us or to which we have referred you. We have not authorized anyone to provide you with different information. We and the selling stockholder are offering to sell, and seeking offers to buy, common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale or our common stock.

No action is being taken in any jurisdiction outside the United States to permit a public offering of the common stock or possession or distribution of this prospectus in that jurisdiction. Persons who come into possession of this prospectus in jurisdictions outside the United States are required to inform themselves about and to observe any restrictions as to this offering and the distribution of this prospectus applicable to that jurisdiction.

Through and including , 2008 (25 days after the commencement of this offering), all dealers that buy, sell or trade in our common stock, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealer's obligation to deliver a prospectus when acting as an underwriter and with respect to their unsold allotments or subscriptions.

i

"CardioNet" and "PDS Heart" are registered trademarks in the United States. This prospectus also includes references to trademarks and service marks of other entities, and those trademarks and service marks are the property of their respective owners.

We are a Delaware company. We reincorporated in Delaware from California on February 22, 2008. Unless the context indicates otherwise, as used in this prospectus, the terms "CardioNet," "we," "us" and "our" refer to CardioNet, Inc., a Delaware corporation, and its subsidiaries taken as a whole.

ii

This summary highlights what we believe is the most important information about us and this offering. Because it is only a summary, it does not contain all of the information that you should consider before investing in shares of our common stock. The information in this summary is qualified in its entirety by, and should be read in conjunction with, the more detailed information appearing elsewhere in this prospectus. Before you decide to invest in our common stock, you should read this entire prospectus carefully, including the "Risk Factors" section and the consolidated financial statements and related notes included in this prospectus.

Overview

We are the leading provider of ambulatory, continuous, real-time outpatient management solutions for monitoring relevant and timely clinical information regarding an individual's health. We have raised over $200 million of capital and spent seven years developing a proprietary integrated patient monitoring platform that incorporates a wireless data transmission network, internally developed software, FDA-cleared algorithms and medical devices, and a 24-hour digital monitoring service center. Our initial efforts are focused on the diagnosis and monitoring of cardiac arrhythmias, or heart rhythm disorders, with a solution that we market as the CardioNet System.

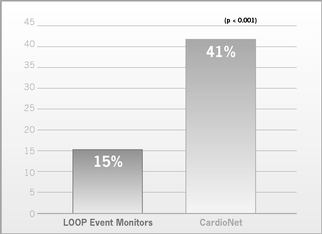

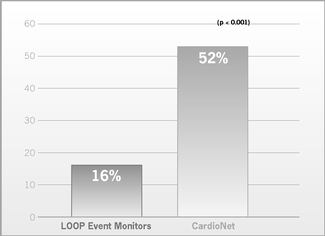

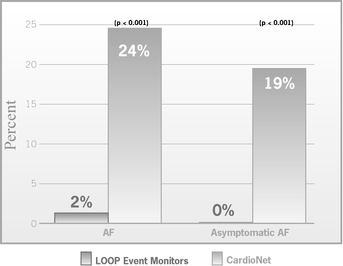

We believe that the CardioNet System's continuous, heartbeat-by-heartbeat monitoring is a fundamental advancement in arrhythmia monitoring, with the potential to transform an industry that has historically relied on memory-constrained, intermittent digital or tape recorders, such as event monitors and Holter monitors. Existing technologies have one or more drawbacks including the inability to detect asymptomatic events, which are defined as clinically significant events that the patient cannot feel, algorithms with limited detection capabilities, failure to provide real-time data, memory constraints, frequent inaccurate diagnoses and an inability to monitor patient compliance and interaction. We believe these drawbacks lead to suboptimal diagnostic yields, adversely impacting clinical outcomes and health care costs. In a randomized clinical trial, the CardioNet System detected clinically significant arrhythmias nearly three times as often as traditional loop event monitors in patients who had previously experienced negative or nondiagnostic Holter monitoring.

The CardioNet System incorporates a lightweight patient-worn sensor attached to electrodes that capture two-lead electrocardiogram, or ECG, data measuring electrical activity of the heart and communicates wirelessly with a compact, handheld monitor. The monitor analyzes incoming heartbeat-by-heartbeat information from the sensor on a real-time basis by applying proprietary algorithms designed to detect arrhythmias. When the monitor detects an arrhythmic event, it automatically transmits the ECG to the CardioNet Monitoring Center, even in the absence of symptoms noticed by the patient and without patient involvement. At the CardioNet Monitoring Center, which operates 24 hours a day and 7 days per week, experienced certified cardiac monitoring specialists analyze the sent data, respond to urgent events and report results in the manner prescribed by the physician. The CardioNet System currently stores at least 96 hours of ECG data, in contrast to 10 minutes for a typical event monitor. We are in the process of upgrading our monitors to provide expanded storage of 21 days of ECG data. The CardioNet System employs two-way wireless communications, enabling continuous transmission of patient data to the CardioNet Monitoring Center and permitting physicians to remotely adjust monitoring parameters and request previous ECG data from the memory stored in the monitor.

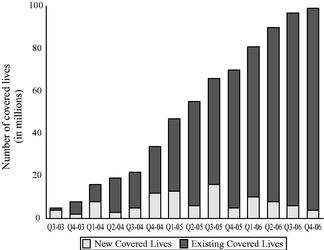

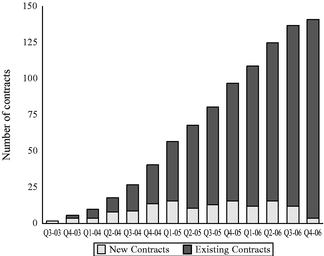

Since our commercial introduction of the CardioNet System in January 2003, physicians have enrolled over 109,000 patients. Through the end of 2007, we marketed our solution in 48 states. In addition, we have achieved reimbursement levels that we believe reflects the clinical efficacy of the CardioNet System relative to existing technologies. We have secured direct contracts with

1

169 commercial payors as of December 31, 2007. We estimate that, combined with Medicare, this represents more than 160 million covered lives.

Recent Developments

- •

- Publication of Randomized Clinical Trial. We completed a 300-patient randomized clinical trial finding that the CardioNet System provided a significantly higher diagnostic yield compared to traditional loop event monitoring, including loop event monitoring incorporating a feature designed to automatically detect certain arrhythmias. We are using the clinical evidence from this trial to both drive continued physician adoption of our solution and to attempt to secure contracts with additional commercial payors. Of the 21 targeted commercial payors, representing approximately 95 million covered lives, who had previously required proof of product superiority evidenced by a published randomized clinical trial, we have secured contracts with three such payors, representing over 26 million covered lives, since publication of our trial results in March 2007. Several of the remaining payors have indicated that they do not believe that the data from the clinical trial is sufficient. We continue to work with these and other payors to secure reimbursement contracts.

- •

- Acquisition of PDSHeart, Inc. In March 2007, we acquired PDSHeart, Inc., a leading cardiac monitoring company that provides event, Holter and pacemaker monitoring services in 48 states. For the year ended December 31, 2006, PDSHeart provided event monitoring services to approximately 76,000 patients, representing approximately 80% of PDSHeart's $20.9 million in revenues for the year ending December 31, 2006. We believe that the acquisition of PDSHeart can have numerous benefits for us, including the opportunity to cross-sell into our respective customer bases and the ability to become a "one stop shop" for arrhythmia monitoring services given our full spectrum of solutions, ranging from our differentiated CardioNet System to event and Holter monitoring. We believe that only approximately 5% of our accounts overlapped with those of PDSHeart at the time of the acquisition, due primarily to our complementary geographic coverage. In 2006, we derived approximately 75% of our revenues from sales of our CardioNet System in the Northeast states, while PDSHeart derived approximately 80% of its revenues in states outside the Northeast. As a result, the acquisition has accelerated our market expansion strategy by providing us with immediate access to a sales force with existing physician relationships capable of marketing our CardioNet System in areas of the country where it had previously not been sold. Our sales force increased from 27 account executives at December 31, 2006 to 76 account executives as of December 31, 2007, largely as a result of the PDSHeart acquisition. On a pro-forma basis, for the year ended December 31, 2007, our revenues were $77.1 million, including $4.1 million of revenues recorded by PDSHeart prior to the acquisition.

Industry Overview

An arrhythmia is categorized as a temporary or sustained abnormal heart rhythm that is caused by a disturbance in the electrical signals in the chambers of the heart. Proper transmission of electrical signals through the heart is necessary to ensure effective heart function. There are two main categories of arrhythmia: tachycardia, meaning too fast a heartbeat, and bradycardia, meaning too slow a heartbeat.

Arrhythmias affect more than 4 million people in the United States. According to the American Heart Association, arrhythmias result in more than 780,000 hospitalizations and contribute to approximately 480,000 deaths per year.

The ability to diagnose or rule out an arrhythmia as a symptom of a cardiac condition is important both to treat those patients with serious cardiovascular diseases as well as to identify those patients that may not require further medical attention. Arrhythmias may be diagnosed either in a physician's office

2

or other health care facility or remotely by monitoring a patient's heart rhythm. Typically, physicians will initially administer a resting ECG that monitors the electrical impulses in a patient's heart. If a physician determines that a patient needs to be monitored for a longer period of time to produce a diagnosis, the physician will typically prescribe an ambulatory cardiac monitoring device, such as a Holter monitor or an event monitor.

- •

- Holter Monitors. A Holter monitor is an ambulatory cardiac monitoring device, first used in 1961, that is generally worn by a patient for a one or, in rare instances, two day period in order to record continuous ECG data. After the one or two day period, the magnetic or digital storage, or other medium containing the data recorded by this device, is delivered by hand, mail or internet for processing and analysis by the physician or a third party service provider. Despite the advent of newer technologies, Holter monitoring continues to be used today for patients whose suspected arrhythmia is believed to occur many times during the course of a day, in which case a Holter is often effective or adequate. However, for a patient that has an unpredictable or intermittent arrhythmia, a Holter may not provide clinically useful information due to the insufficient duration of the monitoring period. In addition, as a result of the typical one to three day reporting delay and the lack of real-time physician notification, patients may not receive timely diagnosis of their condition. Any artifact, or noise, in the data will not be discovered until the test is analyzed. A 2005 Frost & Sullivan study reported that Holters have been found to be effective in diagnosing cardiac arrhythmias only 10% of the time.

- •

- Event Monitors. An event monitor records several minutes of ECG activity at a time and then begins overwriting the memory, a process referred to as memory loop recording. When a patient feels the symptoms of an event, he or she pushes a button to activate the recording, which typically freezes 45 seconds of ECG data before symptom onset and records 15 seconds live following the symptom. Event monitors have limited memory, usually less than 10 minutes, and can generally store data concerning between one and six cardiac events. The patient must transmit event data to the monitoring center, typically by phone, and then erase the memory. To the extent that the patient does not call in and transmit data concerning an event, the device will become unable to store future event data once the device's event storage is full.

Event monitors offer certain advantages over Holters given that they are worn over a period of up to 30 days, instead of the one or two day Holter period. However, event monitors have significant shortcomings. Manual-trigger loop event monitors capture only cardiac events associated with symptoms detectable by the patient and not asymptomatic cardiac events. In our experience, only 15% to 20% of clinically significant cardiac events are symptomatic, meaning that the patient can feel them as they occur. Other drawbacks of manual-trigger loop event monitors include the limited data storage, the lack of trend data, and poor patient compliance relating to the requirement that the patient must both trigger and transmit events.

A newer version of event monitoring devices was introduced in 1999 called auto-detect loop event monitors, which incorporate basic algorithms that look at fast, slow or irregular heart rates and in some cases, pauses, to automatically detect certain asymptomatic arrhythmias. The primary drawback of auto-detect loop event monitors is that they require the patient to call in to transmit data to physicians. The latest development in event monitoring is referred to as auto-detect/auto-send loop event monitors, which have the ability to send captured event data to a monitoring center via cell phone. The drawbacks of auto-detect/auto-send loop event monitors are that they suffer from limited data storage and, to our knowledge, utilize algorithms that were not subject to the same level of FDA scrutiny prior to marketing as the CardioNet System.

Despite major advances in cardiology with new therapeutic drugs, such as beta blockers and statins, and new therapeutic devices and procedures over the last several decades, there have been few advances in ambulatory monitoring. We believe that there is a significant opportunity for new

3

arrhythmia monitoring solutions that exploit the convergence of wireless, low power microelectronic and software technologies to address the shortcomings of traditional Holter and event monitors. We believe these shortcomings often lead to suboptimal diagnostic yields, adversely impacting clinical outcomes and health care costs.

CardioNet Solution

We have developed an ambulatory, continuous and real-time arrhythmia monitoring solution that we believe represents a significant advancement over event and Holter monitoring. The CardioNet System incorporates a patient-worn sensor attached to electrodes that capture two-lead ECG data and communicates wirelessly with a compact monitor that analyzes incoming information by applying proprietary algorithms designed to detect arrhythmias and eliminate data noise. When the monitor detects an arrhythmic event, it automatically transmits the ECG data to the CardioNet Monitoring Center, where experienced certified cardiac monitoring specialists analyze the sent data, respond to urgent events and report results in the manner prescribed by the physician. The CardioNet System, on average, is worn by the patient for a period of approximately 14 days.

The CardioNet System results in a high diagnostic yield of clinically significant arrhythmias, allowing for real-time detection and analysis as well as timely intervention and treatment by the physician. In a randomized 300-patient clinical study, the CardioNet System detected clinically significant arrhythmias nearly three times as often as traditional loop event monitors in patients who have previously experienced negative or nondiagnostic Holter monitoring or 24 hours of telemetry.

We believe that the CardioNet System offers the following advantages to physicians, payors and patients:

- •

- Real-time, continuous data. The CardioNet System initiates real-time analysis and automatic transmission as events occur, which allows physicians to receive urgent notifications in a timely manner. The CardioNet System currently stores at least 96 hours of ECG data, considerably more than the typical 10 minutes of memory of event monitors. We are in the process of upgrading our monitors to store 21 days of ECG data. In addition, the CardioNet System works without patient interaction, automatically detecting and transmitting asymptomatic events.

- •

- Reflects real-life cardiac activity. Patients using the CardioNet System can continue normal activities, including activities that may trigger an arrhythmia, with a minimum of data artifacts or "noise." Patients experiencing a symptom record details of their symptom and activity data on the touch-screen of the CardioNet System monitor, which allows physicians to correlate the information to the underlying ECG data.

- •

- Two-way wireless capabilities for transmission, remote programming and data retrieval. The CardioNet System allows two-way wireless communications, compared to most event monitors which only support one-way transmissions. With the CardioNet System, physicians can adjust device parameters remotely, "check in" on the patient and request ECG data from the previous 96 hours, or 21 days of ECG data from our upgraded monitors as they become available. Our monitors currently in development will also allow for voice capabilities in addition to the text messaging capabilities of our current monitor.

- •

- Potential reduction in health care costs. We have demonstrated increased diagnostic yield as compared to event monitoring, which we believe may reduce "time to diagnosis" and reduce health care costs resulting from repeated emergency room and physician visits, additional diagnostic testing, prolonged hospitalization for the sole purpose of arrhythmia monitoring and unnecessary hospitalizations for drug initiation and titration, as well as expenditures resulting from stroke and other serious cardiovascular complications.

4

- •

- Tailored and customized to physician's needs. The prescribing physician selects patient-specific monitoring thresholds and response parameters. The physician selects the events to be monitored and the level and timing of response by the CardioNet Monitoring Center—from routine daily reporting to urgent "stat" reports. Physicians can review the data by fax or internet, depending on their preferences.

Our Business Strategy

Our goal is to maintain our position as the leading provider of ambulatory, continuous and real-time outpatient monitoring services by establishing our proprietary integrated technology and service offering as the standard of care for multiple health care markets. The key elements of the business strategy by which we intend to achieve these goals include:

- •

- Continue to Educate the Market on the Higher Diagnostic Yield of Our Differentiated Arrhythmia Monitoring Solution. We intend to continue to educate cardiologists and electrophysiologists on the benefits of using the CardioNet System to meet their arrhythmia monitoring needs, stressing the increased diagnostic yield and their ability to use the clinically significant data to make timely interventions and guide more effective treatments.

- •

- Capitalize on Clinical Trial Results to Enhance Payor Relationships. We have achieved reimbursement for our advanced monitoring solution at levels that we believe reflect its clinical efficacy relative to existing technologies. Our efforts have resulted in contracts with 169 commercial payors as of December 31, 2007. We estimate that, combined with Medicare, this represents more than 160 million covered lives. We intend to continue to use the clinical evidence from our 300-patient randomized clinical trial to secure contracts with 18 targeted commercial payors, representing approximately 69 million covered lives, which had previously required proof of product superiority evidenced by a published randomized clinical trial.

- •

- Position CardioNet as "One Stop Shop" for Arrhythmia Monitoring. Through our acquisition of PDSHeart, we are able to offer to physicians both the CardioNet System and event and Holter monitoring services. We believe that certain cardiologists and electrophysiologists prefer to use a single source of arrhythmia monitoring solutions with a full spectrum of those solutions.

- •

- Leverage Expanded Sales Footprint to Enhance Market Penetration. With the acquisition of PDSHeart, we now provide services to patients in 48 states. Our sales force increased from 27 account executives at December 31, 2006 to 76 account executives as of December 31, 2007, largely as a result of the PSDHeart acquisition, and we intend to continue to add sales capacity. The acquisition accelerated our market expansion strategy by providing us with immediate access to a sales force with existing physician relationships capable of marketing our CardioNet System in areas of the country where it had previously not been marketed or sold.

- •

- Leverage Monitoring Platform to New Market Opportunities. We believe that the CardioNet System is a platform that can be leveraged for applications in multiple markets. While our initial focus has been on arrhythmia diagnosis and monitoring, we intend to expand into new market areas such as cardiac monitoring for clinical trials, including QT prolongation and arrhythmia trials, and comprehensive disease management for congestive heart failure, diabetes and other diseases that require outpatient or ambulatory monitoring and management. We believe that our technology could also be used to create "instant telemetry beds" in hospitals, particularly in rural hospitals, step-down units or skilled nursing facilities to help cope with acute nursing shortages by reducing the number of nurses needed to oversee ECG monitoring and reduce capital equipment costs.

5

Risks Affecting Us

We are subject to a number of risks that you should be aware of before you buy our common stock, including:

- •

- risks relating to our ability to obtain physician prescriptions;

- •

- our dependence upon reimbursements associated with our services;

- •

- changes in the Medicare program and government regulations; and

- •

- increased competition.

These and other risks are discussed more fully in the "Risk Factors" section of this prospectus.

Corporate Information

We were originally incorporated in the State of California in March 1994. We reincorporated in the State of Delaware on February 22, 2008. Our principal executive offices are located at 1010 Second Avenue, San Diego, California 92101, and our telephone number is (619) 243-7500. Our website address iswww.cardionet.com. The information contained in, or that can be accessed through, our website is not part of this prospectus.

6

| | | |

|---|---|---|

| Common stock offered by CardioNet | 3,000,000 shares | |

Common stock offered by the selling stockholder | 400,000 shares | |

Over-allotment option | The selling stockholder has granted the underwriters an option for a period of 30 days to purchase up to 510,000 additional shares of common stock. | |

Common stock to be outstanding after this offering | 22,564,607 shares, assuming an initial public offering price of $19.00 per share, the mid-point of the price range set forth on the cover page of this prospectus, and assuming a conversion date of December 31, 2007 with respect to shares of our mandatorily redeemable convertible preferred stock. | |

Use of proceeds. | We intend to use the net proceeds to us from this offering (i) to repay in full a term loan with and to pay a success fee to Silicon Valley Bank, (ii) to make required payments to former stockholders of PDSHeart, (iii) for research and development, to build our inventory of future generations of the CardioNet Systems, increase our sales and marketing capabilities for our CardioNet System, hire additional personnel, invest in infrastructure and pursue new markets and geographies, (iv) to acquire or license products, technologies or businesses, and (v) for working capital and general corporate purposes. | |

We will not receive any of the proceeds from the sale of common stock by the selling stockholder. See "Use of Proceeds." | ||

Proposed symbol on The Nasdaq Global Market | BEAT |

The share amounts listed above are based on 19,564,607 shares outstanding as of December 31, 2007 and includes 103,292 unvested shares held by employees. These amounts exclude:

- •

- 1,641,613 shares of common stock issuable upon the exercise of outstanding options under our 2003 Equity Incentive Plan as of December 31, 2007 having a weighted average exercise price of $6.38 per share;

- •

- a number of shares of common stock reserved for future issuance under our 2008 Equity Incentive Plan equal to the number of shares reserved under the 2003 Equity Incentive Plan that are available for future issuance at the effective date of the 2008 Equity Incentive Plan (617,518 shares as of December 31, 2007), 142,500 shares of common stock reserved for future issuance under our 2008 Non-Employee Directors' Stock Option Plan and 238,000 shares of common stock reserved for future issuance under our 2008 Employee Stock Purchase Plan, each of which will become effective upon the signing of the underwriting agreement for this offering; and

7

- •

- 6,250 shares of common stock issuable upon the exercise of an outstanding warrant having an exercise price of $2.94 per share.

Unless otherwise noted, the information in this prospectus reflects a one-for-two reverse split of our common stock effected in March 2008 and assumes:

- •

- the conversion of all our outstanding shares of preferred stock into 16,026,820 shares of common stock upon the completion of this offering, assuming a conversion date of December 31, 2007 and an initial public offering price of $19.00 per share, the mid-point of the price range set forth on the cover page of this prospectus;

- •

- the automatic cashless exercise of warrants to purchase shares of our Series D-1 preferred stock upon the completion of this offering pursuant to the terms thereof, resulting in the issuance of 304,468 shares of our common stock, assuming an initial public offering price of $19.00 per share, the mid-point of the price range set forth on the cover page of this prospectus;

- •

- the adoption of our amended and restated certificate of incorporation and bylaws upon the completion of this offering; and

- •

- no exercise of the underwriters' over-allotment option.

The number of shares of our common stock issuable upon conversion of our mandatorily redeemable convertible preferred stock and upon exercise of warrants to purchase shares of our Series D-1 preferred stock, which convert into shares of common stock, will vary based on the initial public offering price of our common stock in this offering. The number of shares of common stock into which each share of mandatorily convertible preferred stock is convertible increases daily at the rate of 5% per annum, compounding quarterly. As a result, between December 31, 2007 and March 25, 2008, the shares of mandatorily convertible preferred stock will become convertible into 84,861 additional shares of common stock, assuming an initial public offering price of $19.00 per share, the mid-point of the price range set forth on the cover page of this prospectus. The number of shares of our common stock outstanding after this offering would be 22,954,291 shares if the initial public offering price is $18.00 per share, the low end of the price range set forth on the cover page of this prospectus, and 22,213,907 shares if the initial public offering price is $20.00 per share, the high end of the price range set forth on the cover page of this prospectus, in each case assuming a conversion date of December 31, 2007 with respect to shares of our mandatorily redeemable convertible preferred stock. See "Capitalization" and "Description of Capital Stock."

8

Summary Consolidated Financial Information

The following summary consolidated financial data should be read together with our consolidated financial statements and related notes, "Management's Discussion and Analysis of Financial Condition and Results of Operations" and other more detailed financial information appearing elsewhere in this prospectus. The summary consolidated financial data for the years ended December 31, 2005, 2006 and 2007 are derived from our audited financial statements, which are included elsewhere in this prospectus. The summary consolidated financial data for the quarter ended December 31, 2007 are based on the historical statements of operations of CardioNet, Inc. and PDSHeart.

The summary unaudited pro forma consolidated statements of operations data for the year ended December 31, 2007 are based on the historical statements of operations of CardioNet, Inc. and PDSHeart, Inc., giving effect to our acquisition of PDSHeart as if the acquisition had occurred on January 1, 2007. The summary unaudited pro forma consolidated statement of operations data is based on the estimates and assumptions set forth in the notes to the unaudited pro forma consolidated statements of operations, which are included elsewhere in this prospectus. These estimates and assumptions are preliminary and subject to change, and have been made solely for the purposes of developing such pro forma information. The summary unaudited pro forma consolidated statement of operations data is presented for illustrative purposes only and is not necessarily indicative of the combined results of operations to be expected in any future period or the results that actually would have been realized had the entities been a single entity during these periods.

The pro forma balance sheet data reflects the balance sheet data at December 31, 2007, after giving effect to (i) the conversion of all our outstanding shares of preferred stock into common stock and (ii) the automatic cashless exercise of warrants upon the completion of this offering pursuant to the terms thereof. The pro forma as adjusted balance sheet data reflects the pro forma balance sheet data at December 31, 2007, as further adjusted for the sale by us of 3,000,000 shares of our common stock in this offering at an assumed initial offering price to the public of $19.00 per share, after deducting the estimated underwriting discounts, commissions and offering expenses payable by us.

We have prepared the summary unaudited consolidated financial data set forth below on the same basis as our audited financial statements and have included all adjustments, consisting only of normal recurring adjustments, that we consider necessary for a fair presentation of our financial position and operating results for such periods. The pro forma basic net loss per share data are unaudited and give effect to the conversion into common stock of all outstanding shares of our preferred stock for the periods indicated. The interim results set forth below are not necessarily indicative of results for future periods.

9

| | Year ended December 31, | Quarter ended December 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Actual | Pro Forma | Actual | ||||||||||||||

| | 2005 | 2006 | 2007 | 2007 | 2007 | ||||||||||||

| | | | | (unaudited) | (unaudited) | ||||||||||||

| | (in thousands, except share and per share data) | ||||||||||||||||

| Statement of Operations Data: | |||||||||||||||||

| Revenues: | |||||||||||||||||

| Net patient revenues | $ | 29,467 | $ | 33,019 | $ | 72,357 | $ | 76,412 | $ | 23,775 | |||||||

| Other revenues | 1,471 | 904 | 635 | 649 | 168 | ||||||||||||

| Total revenues | 30,938 | 33,923 | 72,992 | 77,061 | 23,943 | ||||||||||||

| Cost of revenues | 16,963 | 12,701 | 25,526 | 27,172 | 8,683 | ||||||||||||

| Gross profit | 13,975 | 21,222 | 47,466 | 49,889 | 15,260 | ||||||||||||

| Operating expenses: | |||||||||||||||||

| Research and development | 3,361 | 3,631 | 3,782 | 3,782 | 962 | ||||||||||||

| General and administrative | 13,853 | 15,631 | 26,675 | 27,715 | 7,798 | ||||||||||||

| Sales and marketing | 6,456 | 6,448 | 15,968 | 17,030 | 4,336 | ||||||||||||

| Amortization | — | — | 799 | 985 | 246 | ||||||||||||

| Total operating expenses | 23,670 | 25,710 | 47,224 | 49,512 | 13,342 | ||||||||||||

| Income (loss) from operations | (9,695 | ) | (4,488 | ) | 242 | 377 | 1,918 | ||||||||||

| Other income (expense): | |||||||||||||||||

| Interest income | 97 | 114 | 1,622 | 1,627 | 248 | ||||||||||||

| Interest expense | (1,865 | ) | (3,271 | ) | (2,222 | ) | (2,264 | ) | (73 | ) | |||||||

| Total other expense | (1,768 | ) | (3,157 | ) | (600 | ) | (637 | ) | 175 | ||||||||

| Net income (loss) | (11,463 | ) | (7,645 | ) | (358 | ) | (260 | ) | 2,093 | ||||||||

| Dividends on and accretion of mandatorily redeemable convertible preferred stock | — | — | (8,346 | ) | (8,346 | ) | (2,759 | ) | |||||||||

| Net loss applicable to common shares | $ | (11,463 | ) | $ | (7,645 | ) | $ | (8,704 | ) | $ | (8,606 | ) | (666 | ) | |||

| Net loss per common share(1): | |||||||||||||||||

| Basic and diluted | $ | (4.04 | ) | $ | (2.63 | ) | $ | (2.89 | ) | $ | (2.86 | ) | $ | (0.22 | ) | ||

| Pro forma | $ | (0.51 | ) | $ | (0.04 | ) | |||||||||||

| Shares used to compute net loss per share(1): | |||||||||||||||||

| Basic and diluted | 2,837,772 | 2,908,360 | 3,011,699 | 3,011,699 | 3,011,699 | ||||||||||||

| Pro forma | 16,839,493 | 16,839,493 | |||||||||||||||

- (1)

- Please see Note 2 to our consolidated financial statements for an explanation of the method used, the historical and pro forma net (loss) income per share and the number of shares used in computation of the per share amounts.

| | As of December 31, 2007 | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| | Actual | Pro Forma | Pro Forma As Adjusted(2) | ||||||

| | | (unaudited) | (unaudited) | ||||||

| | (in thousands) | ||||||||

| Summary Consolidated Balance Sheet Data: | |||||||||

| Cash and cash equivalents | $ | 18,091 | $ | 18,091 | $ | 69,885 | |||

| Working capital | 29,375 | 29,375 | 81,169 | ||||||

| Total assets | 103,040 | 103,040 | 152,850 | ||||||

| Total debt | 2,744 | 2,744 | 2,744 | ||||||

| Mandatorily redeemable convertible preferred stock | 115,302 | — | — | ||||||

| Total shareholders' equity (deficit) | $ | (26,865 | ) | $ | 88,437 | $ | 138,247 | ||

- (2)

- A $1.00 increase (decrease) in the assumed initial public offering price of $19.00 per share, the mid-point of the price range set forth on the cover page of this prospectus, would increase (decrease) cash and cash equivalents, working capital, total assets and total shareholders' equity (deficit) by approximately $2.8 million, assuming the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting underwriter discounts and commissions and estimated offering expenses payable by us. Depending on market conditions at the time of pricing this offering and other considerations, we may sell a greater or lesser number of shares than the number set forth on the cover page of this prospectus. An increase or decrease of 1,000,000 shares in the number of shares offered by us would increase or decrease cash and cash equivalents, working capital, total assets and total shareholders' deficit by approximately $17.7 million, assuming the offering price per share remains the same.

10

Before you decide to invest in our common stock, you should consider carefully the risks described below, together with the other information contained in this prospectus. We believe the risks described below are the risks that are material to us as of the date of this prospectus. If any of the following risks comes to fruition, our business, financial condition, results of operations and future growth prospects would likely be materially and adversely affected. In these circumstances, the market price of our common stock could decline, and you may lose all or part of your investment.

Risks related to our business and industry

We have a history of net losses and may never become profitable.

We have incurred net losses from our inception through December 31, 2007, including net losses of $11.5 million for the year ended December 31, 2005, $7.6 million for the year ended December 31, 2006 and $0.4 million for the year ended December 31, 2007. Even giving effect to the PDSHeart acquisition, we are operating at a loss, with pro forma losses for the year ended December 31, 2007, giving effect to the acquisition, of $0.3 million. As of December 31, 2007, we had total shareholders' deficit of approximately $26.9 million. We expect our operating expenses to increase as we, among other things:

- •

- expand our sales and marketing activities;

- •

- invest in designing, manufacturing and building our inventory of future generations of the CardioNet System;

- •

- hire additional personnel;

- •

- invest in infrastructure; and

- •

- incur the additional expenses associated with being a public company.

With increasing expenses, we will need to substantially increase our revenues to become profitable. Because of the risks and uncertainties associated with further developing and marketing the CardioNet System, we are unable to predict the extent of any future losses or when we will become profitable, if at all.

Our business is dependent upon physicians prescribing our services; if we fail to obtain those prescriptions, our revenues could fail to grow and could decrease.

The success of our business is dependent upon physicians prescribing our services for patients and cross-selling the respective CardioNet and PDSHeart customer bases. Our success in obtaining prescriptions and cross-selling will be directly influenced by a number of factors, including:

- •

- the ability of the physicians with whom we work to obtain sufficient reimbursement and be paid in a timely manner for the professional services they provide in connection with the use of our arrhythmia monitoring solutions, particularly the CardioNet System;

- •

- our ability to educate physicians regarding, and convince them of, the benefits of the CardioNet System over existing treatment methods such as Holter monitors and event monitors; and

- •

- the perceived clinical efficacy of the CardioNet System.

If we are unable to educate physicians regarding the benefits of the CardioNet System, obtain sufficient prescriptions and cross-sell our respective customer bases, revenues from the provision of our arrhythmia monitoring solutions could fail to grow and could decrease.

11

We and the physicians with whom we work are dependent upon reimbursement for the fees associated with our services; the absence or inadequacy of reimbursement would cause our revenues to fail to grow or decrease.

We receive reimbursement for our services from commercial payors and from Medicare Part B carriers where the services are performed on behalf of the Centers for Medicare and Medicaid Services, or CMS. The Medicare Part B carriers in each state change from time to time, which may result in changes to our reimbursement rates, increased administrative burden and reimbursement delays.

In addition, our prescribing physicians receive reimbursement for professional interpretation of the information provided by our products and services from commercial payors or Medicare carriers within the state where they practice. The efficacy, safety, performance and cost-effectiveness of our products and services, on a stand-alone basis and relative to competing services, will determine the availability and level of reimbursement we and our prescribing physicians receive. Our ability to successfully contract with payors is critical to our business because physicians and their patients will select arrhythmia monitoring solutions other than ours in the event that payors refuse to adequately reimburse our technical fees and physicians' professional fees.

Many commercial payors refuse to enter into contracts to reimburse the fees associated with medical devices or services that such payors determine to be "experimental and investigational." Commercial payors typically label medical devices or services as "experimental and investigational" until such devices or services have demonstrated product superiority evidenced by a randomized clinical trial. We completed a clinical trial in which the CardioNet System provided higher diagnostic yield than traditional loop event monitoring. Prior to our clinical trial, the CardioNet System was labeled "experimental and investigational" by 21 targeted commercial payors, representing approximately 95 million covered lives. Subsequent to our trial, three commercial payors, representing over 26 million covered lives, removed the designation of the CardioNet System as "experimental and investigational." Several of the remaining payors, however, have informed us that they do not believe the data from this trial justifies the removal of this designation. Other commercial payors may also find the data from our clinical trial not compelling. Additional commercial payors may also label the CardioNet System as "experimental and investigational" and, as a result, refuse to reimburse the technical and professional fees associated with the CardioNet System.

Administration of the claims process for the many commercial payors is complex. As a result we sometimes bill payors for services for which we have no reimbursement contract. These payors may require that we return any funds that they pay in respect of these claims.

If commercial payors or Medicare decide not to reimburse our services or the related services provided by physicians, or the rates of such reimbursement change, or if we fail to properly administer claims, our revenues could fail to grow and could decrease.

Reimbursement by Medicare is highly regulated and subject to change; our failure to comply with applicable regulations, could decrease our revenues and may subject us to penalties or have an adverse impact on our business.

We receive approximately 30% of our revenues as reimbursement from Medicare. The Medicare program is administered by Centers for Medicare & Medicaid Services, or CMS, which imposes extensive and detailed requirements on medical services providers, including, but not limited to, rules that govern how we structure our relationships with physicians, how and when we submit reimbursement claims, how we operate our monitoring facilities and how and where we provide our arrhythmia monitoring solutions. Our failure to comply with applicable Medicare rules could result in discontinuing our reimbursement under the Medicare payment program, our being required to return funds already paid to us, civil monetary penalties, criminal penalties and/or exclusion from the Medicare program.

12

In addition, reimbursement from Medicare is subject to statutory and regulatory changes, local and national coverage decisions, rate adjustments and administrative rulings, all of which could materially affect the range of services covered or the reimbursement rates paid by Medicare for use of our arrhythmia monitoring solutions. For example, CMS adopted a new payment policy in January 2007 that reduced the rate of reimbursement for a number of services reimbursed by Medicare. Although this modification to Medicare's reimbursement rates did not affect the amount paid by Medicare for reimbursement of the fees associated with the CardioNet System, it resulted in the reduction of reimbursement rates for event services by 3% to 8%, depending on the type of service, and Holter services by 8% as compared to the corresponding rates in effect in 2006. Based on current proposed Medicare rates for 2008 through 2010, we expect that reimbursement for event and Holter services will continue to decline at an annual rate similar to 2007. In addition, we cannot predict whether future modifications to Medicare's reimbursement policies could reduce or eliminate the amounts we receive from Medicare for the solutions we provide. In addition, Medicare's reimbursement rates can affect the rate that commercial payors are willing to pay for our products and services. Consequently, any future elimination, limitation or reduction in the reimbursement rates provided by Medicare for our arrhythmia monitoring solutions could result in a reduction in the rates we receive from commercial payors.

Reimbursement for the CardioNet System by Medicare and other commercial payors is complicated by the lack of a specific Current Procedural Terminology, or CPT, code, which may result in lower prescription rates or varying reimbursement rates.

When we bill Medicare and certain other commercial payors for the service we provide in connection with the CardioNet System, we submit the bill using the nonspecific billing, or CPT, code "93799." Unlike dedicated CPT codes approved by the American Medical Association, or AMA, and CMS, claims using non-specific codes may require semi-automated or manual processing, as well as additional review by payors. The claims processing requirements associated with a nonspecific code can make our services less attractive to physicians because added time and effort is often required in order to receive payment for their services. Furthermore, the Medicare reimbursement rate for non-specific codes is determined by local Medicare carriers. As a result, the reimbursement rates relating to our CardioNet System are subject to change without notice.

A request to the AMA for a specific CPT code that describes our CardioNet System has been made. The request was discussed and voted upon by the CPT Editorial Panel at its public October 2007 meeting. The results of the vote are confidential. We have been informally advised that the CPT Editorial Panel voted in favor of the request. However, the results of the vote are subject to change until such results are published in the fall of 2008. If the request is officially approved by the AMA CPT Editorial Panel, the specific CPT code would be published in the fall of 2008 and would be available for use in 2009. However, we cannot guarantee that we will receive a specific CPT code for the CardioNet System in that timeframe, or ever. Moreover, if we do receive a CPT code, the reimbursement rate associated with that code, which would be subject to change on an annual basis through a public notice and comment process, may be lower than our current reimbursement rates.

A reduction in sales of our services or a loss of one or more of our key commercial payors would adversely affect our business and operating results.

A small number of commercial payors represent a significant percentage of our revenues. In the year ended December 31, 2007, our top 10 commercial payors by revenues accounted for approximately 29.9% of our total revenues. Our agreements with these commercial payors typically allow either party to the contract to terminate the contract by providing between 60 and 120 days prior written notice to the other party at any time following the end of the initial term of the contract. Our commercial payors may elect to terminate or not to renew their contracts with us for any reason and, in some instances can unilaterally change the reimbursement rates they pay. In the event any of our key commercial

13

payors terminate their agreements with us, elect not to renew their agreements with us or elect not to enter into new agreements with us upon expiration of their agreements with us on terms as favorable as our current agreements, our business, operating results and prospects would be adversely affected.

Consolidation of commercial payors could result in payors eliminating coverage of our CardioNet System or reduced reimbursement rates for our CardioNet System.

The commercial payor industry is undergoing significant consolidation. When payors combine their operations, the combined company may elect to reimburse our CardioNet System at the lowest rate paid by any of the participants in the consolidation. If one of the payors participating in the consolidation does not reimburse for the CardioNet System at all, the combined company may elect not to reimburse for the CardioNet System. Our reimbursement rates tend to be lower for larger payors. As a result, as payors consolidate, our average reimbursement rate may decline.

Our acquisition of PDSHeart, as well as any other companies or technologies we may acquire in the future, could prove difficult to integrate and may disrupt our business and harm our operating results and prospects.

Our acquisition of PDSHeart involves numerous risks, including the risk that we will not take advantage of the cross-selling opportunities brought about by the acquisition. In addition, our acquisition of PDSHeart, as well as acquisitions in which we may engage in the future, involve risks associated with our assumption of the liabilities of an acquired company, which may be liabilities that we were or are unaware of at the time of the acquisition, potential write-offs of acquired assets and potential loss of the acquired company's key employees or customers.

We may encounter difficulties in successfully integrating our operations, technologies, services and personnel with that of the acquired company, and our financial and management resources may be diverted from our existing operations. For example, following our acquisition of PDSHeart we have offices in Pennsylvania, California, Florida, Georgia and Minnesota. Our offices in multiple states creates a strain on our ability to effectively manage our operations and key personnel. If we elect to consolidate our facilities we may lose key personnel unwilling to relocate to the consolidated facility, may have difficulty hiring appropriate personnel at the consolidated facility and may have difficulty providing continuity of service through the consolidation.

Physician and patient satisfaction or performance problems with an acquired business, technology, service or device could also have a material adverse effect on our reputation. Additionally, potential disputes with the seller of an acquired business or its employees, suppliers or customers and amortization expenses related to goodwill and other intangible assets could adversely affect our business, operating results and financial condition.

We may not be able to realize the anticipated benefits of the PDSHeart acquisition or any other acquisition we may pursue or to profitably deploy acquired assets. If we fail to properly evaluate and execute acquisitions, our business may be disrupted and our operating results and prospects may be harmed.

If we are unable to manage our expected growth, our revenues and operating results may be adversely affected.

Our business plans call for rapid expansion of our sales and marketing operations and growth of our research and development, product development and administrative operations. We had a sales force of 27 account executives at December 31, 2006 and 76 account executives at December 31, 2007. We intend to expand our sales force to 89 individuals by December 31, 2008. We expect this expansion will place a significant strain on our management and operational and financial resources. Our current and planned personnel, systems, procedures and controls may not be adequate to support our anticipated growth. To manage our growth we will be required to improve existing and implement new operational and financial systems, procedures and controls and expand, train and manage our growing employee base. If we are unable to manage our growth effectively, revenue growth may not be realized or may not be sustainable, may not result in improved operating results or earnings, and our business, financial condition and results of operations could be harmed.

14

Our business is dependent upon having sufficient monitors and sensors. If we do not have enough monitors or sensors or experience delays in manufacturing, we may be unable to fill prescriptions in a timely manner, physicians may elect not to prescribe the CardioNet System, and our revenues and growth prospects could be harmed.

When a physician prescribes the CardioNet System to a patient, our customer service department begins the patient hook-up process, which includes procuring a monitor and sensors from our distribution department and sending them to the patient. While our goal is to provide each patient with a monitor and sensors in a timely manner, we have experienced and may in the future experience delays due to the availability of monitors, primarily when converting to a new generation of monitor or, more recently, in connection with the increase in prescriptions following our acquisition of PDSHeart.

We may also experience shortages of monitors or sensors due to manufacturing difficulties. Multiple suppliers provide the components used in the CardioNet System, but our facilities in San Diego, California are registered and approved by the United States Food and Drug Administration, or FDA, as the ultimate manufacturer of the CardioNet System. Our manufacturing operations could be disrupted by fire, earthquake or other natural disaster, a work stoppage or other labor-related disruption, failure in supply or other logistical channels, electrical outages or other reasons. If there was a disruption to our facilities in San Diego, we would be unable to manufacture the CardioNet System until we have restored and re-qualified our manufacturing capability or developed alternative manufacturing facilities.

Our success in obtaining future prescriptions from physicians is dependent upon our ability to promptly deliver monitors and sensors to our patients, and a failure in this regard would have an adverse effect on our revenues and growth prospects.

Interruptions or delays in telecommunications systems or in the data services provided to us by QUALCOMM or the loss of our wireless or data services could impair the delivery of our CardioNet System services.

The success of the CardioNet System is dependent upon our ability to store, retrieve, process and manage data and to maintain and upgrade our data processing and communication capabilities. The monitors we use in connection with the CardioNet System rely on a third party wireless carrier to transmit data over its data network during times that the monitor is removed from its base. All data sent by our monitors via this wireless data network or via landline is routed directly to QUALCOMM data centers and subsequently routed to our monitoring center. We are dependent upon these third parties to provide data transmission and data hosting services to us. We do not have an agreement directly with this third party wireless carrier. Although we do have an agreement with QUALCOMM that has an initial termination date in September 2010, QUALCOMM may terminate its agreement with us if certain conditions occur, including if QUALCOMM's agreement with the third party wireless carrier terminates or in the event we fail to maintain an agreed-upon number of active cardiac monitoring devices on the QUALCOMM network. We have no control over the status of the agreement between QUALCOMM and the wireless carrier. If we fail to maintain our relationships with QUALCOMM or if we lose wireless carrier services, we would be forced to seek alternative providers of data transmission and data hosting services, which might not be available on commercially reasonable terms or at all.

As we expand our commercial activities, an increased burden will be placed upon our data processing systems and the equipment upon which they rely. Interruptions of our data networks or the data networks of QUALCOMM for any extended length of time, loss of stored data or other computer problems could have a material adverse effect on our business, financial condition and results of operations. Frequent or persistent interruptions in our arrhythmia monitoring services could cause permanent harm to our reputation and could cause current or potential users of the CardioNet System

15

or prescribing physicians to believe that our systems are unreliable, leading them to switch to our competitors. Such interruptions could result in liability, claims and litigation against us for damages or injuries resulting from the disruption in service.

Our systems are vulnerable to damage or interruption from earthquakes, floods, fires, power loss, telecommunication failures, terrorist attacks, computer viruses, break-ins, sabotage, and acts of vandalism. Despite any precautions that we may take, the occurrence of a natural disaster or other unanticipated problems could result in lengthy interruptions in these services. We do not carry business interruption insurance to protect against losses that may result from interruptions in service as a result of system failures. Moreover, the communications and information technology industries are subject to rapid and significant changes, and our ability to operate and compete is dependent in significant part on our ability to update and enhance the communication technologies used in our systems and services.

The market for arrhythmia monitoring solutions is highly competitive. If our competitors are able to develop or market monitoring solutions that are more effective, or gain greater acceptance in the marketplace, than any solutions we develop, our commercial opportunities will be reduced or eliminated.

The market for arrhythmia monitoring solutions is evolving rapidly and becoming increasingly competitive. Our industry is highly fragmented and characterized by a small number of large providers and a large number of smaller regional service providers. These third parties compete with us in marketing to payors and prescribing physicians, recruiting and retaining qualified personnel, acquiring technology and developing solutions complementary to our programs. In addition, as companies with substantially greater resources than ours enter our market, we will face increased competition. If our competitors are better able to develop and patent arrhythmia monitoring solutions than us, or develop more effective and/or less expensive arrhythmia monitoring solutions that render our solutions obsolete or non-competitive or deploy larger or more effective marketing and sales resources than ours, our business will be harmed and our commercial opportunities will be reduced or eliminated.

If we need to raise additional funding in the future, we may be unable to raise such capital when needed, or at all, and the terms of such capital may be adverse to our stockholders.

We believe that the net proceeds from this offering, together with our existing cash and cash equivalent balances, will be sufficient to meet our anticipated cash requirements for the foreseeable future. However, our future funding requirements will depend on many factors, including:

- •

- the costs associated with manufacturing and building our inventory of our next generation C3 monitor;

- •

- the costs of hiring additional personnel and investing in infrastructure;

- •

- the reimbursement rates associated with our products and services;

- •

- actions taken by the FDA, CMS and other regulatory authorities affecting the CardioNet System and competitive products;

- •

- our ability to secure contracts with additional commercial payors providing for the reimbursement of our services;

- •

- the emergence of competing technologies and products and other adverse market developments;

- •

- the costs of preparing, filing, prosecuting, maintaining and enforcing patent claims and other intellectual property rights or defending against claims of infringement by others; and

- •

- the costs of investing in additional lines of business outside of arrhythmia monitoring solutions.

If we need to, or choose to, raise additional capital in the future, such capital may not be available on reasonable terms, or at all. If we raise additional funds by issuing equity securities, substantial

16

dilution to existing stockholders would likely result. If we raise additional funds by incurring additional debt financing, the terms of the debt may involve significant cash payment obligations as well as covenants and financial ratios that may restrict our ability to operate our business.

Our manufacturing facilities and the manufacturing facilities of our suppliers must comply with applicable regulatory requirements. If we or our suppliers fail to achieve or maintain regulatory approval of these manufacturing facilities, our growth could be limited and our business could be harmed.

We currently manufacture the monitors and sensors for the CardioNet System in San Diego, California. Monitors used in the provision of services by PDSHeart are purchased from several third parties. In order to maintain compliance with FDA and other regulatory requirements, our manufacturing facilities must be periodically re-evaluated and qualified under a quality system to ensure they meet production and quality standards. Suppliers of components of and products used to manufacture the CardioNet System and the manufacturers of the monitors used in the provision of services by PDSHeart must also comply with FDA and foreign regulatory requirements, which often require significant resources and subject us and our suppliers to potential regulatory inspections and stoppages. We or our suppliers may not satisfy these requirements. If we or our suppliers do not maintain regulatory approval for our manufacturing operations, our business would be harmed.

Our dependence on a limited number of suppliers may prevent us from delivering our devices on a timely basis.

We currently rely on a limited number of suppliers of components for the CardioNet System. If these suppliers became unable to provide components in the volumes needed or at an acceptable price, we would have to identify and qualify acceptable replacements from alternative sources of supply. Qualifying suppliers is a lengthy process. Delays or interruptions in the supply of our requirements could limit or stop our ability to provide sufficient quantities of devices on a timely basis, meet demand for our services, which could have a material adverse effect on our business, financial condition and results of operations.

We could be subject to medical liability or product liability claims which may not be covered by insurance and which would adversely affect our business and results of operations.

The design, manufacture and marketing of services of the types we provide entail an inherent risk of product liability claims. Any such claims against us may require us to incur significant defense costs, irrespective of whether such claims have merit. In addition, we provide information to health care providers and payors upon which determinations affecting medical care are made, and claims may be made against us resulting from adverse medical consequences to patients resulting from the information we provide. In addition, we may become subject to liability in the event that the monitors and sensors we use fail to correctly record or transfer patient information or if we provide incorrect information to patients or health care providers using our services. We have also agreed to indemnify QUALCOMM for any claims resulting from the provision of our services. If we incur one or more significant claims against us, if we are required to indemnify QUALCOMM as a result of the provision of our services, or if we are required to undertake remedial actions in response to any such claims, such claims or actions would adversely affect our business and results of operations.

Our liability insurance is subject to deductibles and coverage limitations. In addition, our current insurance may not continue to be available to us on acceptable terms, if at all, and, if available, the coverages may not be adequate to protect us against any future claims. If we are unable to obtain insurance at an acceptable cost or on acceptable terms with adequate coverage or otherwise protect against any claims against us, we will be exposed to significant liabilities, which may harm our business.

17

If we do not obtain and maintain adequate protection for our intellectual property, the value of our technology and devices may be adversely affected.

Our business and competitive positions are dependent in part upon our ability to protect our proprietary technology. To protect our proprietary rights, we rely on a combination of trademark, copyright, patent, trade secret and other intellectual property laws, employment, confidentiality and invention assignment agreements with our employees and contractors, and confidentiality agreements and protective contractual provisions with other third parties. We attempt to protect our intellectual property position by filing trademark applications and U.S., foreign and international patent applications related to our proprietary technology, inventions and improvements that are important to the development of our business.

As of December 31, 2007, we had 14 issued U.S. patents, seven foreign patents and 42 pending U.S., foreign and international patent applications relating to various aspects of the CardioNet System. As of December 31, 2007, we also had 11 trademark registrations and one pending trademark application in the United States for a variety of word marks and slogans. We do not believe that any single patent, trademark or other intellectual property right of ours, or combination of our intellectual property rights, is likely to prevent others from competing with us using a similar business model. There are many issued patents and patent applications held by others in our industry and the electronics field. Our competitors may independently develop technologies that are substantially similar or superior to our technologies, or design around our patents or other intellectual property to avoid infringement. In addition, we may not apply for a patent relating to products or processes that are patentable, we may fail to receive any patent for which we apply or have applied, and any patent owned by us or issued to us could be circumvented, challenged, invalidated, or held to be unenforceable, or rights granted thereunder may not adequately protect our technology or provide a competitive advantage to us. For example, with respect to one of our U.S. patents, we have a corresponding foreign patent, the claims of which were amended substantially more so than in the United States, to overcome art that was of record in the U.S. patent. If a third-party challenges the validity of any patents or proprietary rights of ours, we may become involved in intellectual property disputes and litigation that would be costly and time-consuming.

Although third parties may infringe our patents and other intellectual property rights, we may not be aware of any such infringement, or we may be aware of potential infringement but elect not to seek to prevent such infringement or pursue any claim of infringement, and the third party may continue its potentially infringing activities. We believe that LifeWatch Corp. may be infringing our intellectual property rights and have filed a lawsuit against LifeWatch, as is discussed in greater detail in "Legal Proceedings." Any decision whether or not to take further action in response to the activities of LifeWatch or any other potential infringement of our patent or other intellectual property rights may be based on any one or more of a variety of factors, such as the potential costs and benefits of taking such action, and business and legal issues and circumstances. Litigation of claims of infringement of a patent or other intellectual property rights may be costly and time-consuming and divert the attention of key company personnel, and may not be successful or result in any significant recovery of compensation for any infringement or enjoining of any infringing activity. Litigation or licensing discussions may also involve or lead to counterclaims or proceedings that could be brought by a potential infringer to challenge the validity or enforceability of our patents and other intellectual property.

To protect our trade secrets and other proprietary information, we generally require our employees, consultants, contractors and outside collaborators to enter into written nondisclosure agreements. These agreements, however, may not provide adequate protection to prevent any unauthorized use, misappropriation or disclosure of our trade secrets, know-how or other proprietary information. These agreements may be breached, and we may not become aware of, or have adequate remedies in the event of, any such breach. Also, others may independently develop the same or

18

substantially equivalent proprietary information and techniques or otherwise gain access to our trade secrets.

Our ability to market our services may be impaired by the intellectual property rights of third parties.

Our success is dependent in part upon our ability to avoid infringing the patents or proprietary rights of others. Our industry and the electronics field are characterized by a large number of patents, patent filings and frequent litigation based on allegations of patent infringement. Competitors may have filed applications for or have been issued patents and may obtain additional patents and proprietary rights related to devices, services or processes that we compete with or are similar to ours. We may not be aware of all of the patents or patent applications potentially adverse to our interests that may have been or may later be issued to or filed by others. U.S. patent applications may be kept confidential while pending in the Patent and Trademark Office. If other companies have or obtain patents relating to our products or services, we may be required to obtain licenses to those patents or to develop or obtain alternative technology. We may not be able to obtain any such licenses on acceptable terms, or at all. Any failure to obtain such licenses could impair or foreclose our ability to make, use, market or sell our products and services.