Exhibit 99.3

HYDRO ONE INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the years ended December 31, 2013 and 2012

The following Management’s Discussion and Analysis (MD&A) of the financial condition and results of operations should be read together with the consolidated financial statements and accompanying notes (the Consolidated Financial Statements) of Hydro One Inc. (the Company) for the year ended December 31, 2013. The Consolidated Financial Statements are presented in Canadian dollars and have been prepared in accordance with United States (US) Generally Accepted Accounting Principles (GAAP). All financial information in this MD&A is presented in Canadian dollars, unless otherwise indicated.

The Company has prepared this MD&A with reference to National Instrument 51-102 – Continuous Disclosure Obligations of the Canadian Securities Administrators. Under the US/Canada Multijurisdictional Disclosure System, the Company is permitted to prepare this MD&A in accordance with the disclosure requirements of Canada, which are different from those of the US. This MD&A provides information for the year ended December 31, 2013.

EXECUTIVE SUMMARY

We are wholly owned by the Province of Ontario (Province), and our transmission and distribution businesses are regulated by the Ontario Energy Board (OEB). Our mission and vision reflects the unique role we play in the economy of the Province and as a provider of critical infrastructure to all our customers. We strive to be an innovative and trusted company, delivering electricity safely, reliably and efficiently to create value for our customers. We operate as a commercial enterprise with an independent Board of Directors. Our strategic plan is driven by our values: health and safety; excellence; stewardship; and innovation. Safety is of utmost importance to us because we work in an environment that can be hazardous. We take our responsibility as stewards of critical provincial assets seriously. We demonstrate sound stewardship by managing our assets in a manner that is commercial, transparent and which values our customers. We strive for excellence by being trained, prepared and equipped to deliver high-quality service. We value innovation because it allows us to increase our productivity and develop enhanced methods to meet the needs of our customers. In 2013, we continued to focus on our core businesses and our commitment to our customers, and made important contributions to the rebuilding of Ontario’s core infrastructure while continuing to meet the requirements of the Green Energy Act (GEA).

We manage our business using the following framework:

Core Business and Strategy

Our corporate strategy is based on our mission and vision and our values. Our strategic objectives, which are discussed in the section “Our Strategy,” encompass the core values that drive our business. Our strategy touches every part of our core business: health and safety; our customers; innovation; the reliability and efficiency of our systems; the environment; our workforce; shareholder value; and productivity.

Key Performance Drivers

Performance drivers have been identified that relate to achieving certain of our company’s strategic objectives. We establish specific performance targets for each driver aimed at measuring the achievement of our strategic objectives over time. For example, we track the duration of unplanned customer interruptions per delivery point as an indication of our commitment to provide a reliable transmission system for our customers. We measure transmission and distribution unit costs as an indication of our commitment to increasing productivity. These and other key performance drivers are included in the discussion of our performance measures in the section “Performance Measures and Targets.”

1

HYDRO ONE INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

For the years ended December 31, 2013 and 2012

Capability to Deliver Results

We continue to use a balanced scorecard approach as we strive to manage our performance and deliver results each and every year. In 2013, we set nine stretch targets and we met or exceeded five of them. In 2012, we also met or exceeded five of nine stretch targets. We met our target for minimizing the duration of unplanned customer interruptions within our Distribution Business. We also met our targets of satisfying our transmission and distribution customers with the service they receive from our company. Our targets, and our 2013 performance relating to these targets, are discussed in the section “Performance Measures and Targets.” Our ability to deliver results in each of our strategic areas is limited by risks inherent in our regulatory environment, our business, our workforce, and in the economic environment. These risks, as well as our strategies to mitigate them, are discussed in the section “Risk Management and Risk Factors.”

Results and Outlook

During 2013, our financial fundamentals remained strong with net income of $803 million. In 2013, we issued $1,185 million of long-term debt, the proceeds of which were used to fund the retirement of $600 million of long-term debt, and to fund a portion of our capital expenditures and other corporate requirements. A full discussion of our results of operations and financing activities can be found in the sections “Annual Results of Operations” and “Liquidity and Capital Resources.”

In 2013, we made capital investments totaling $1,394 million to improve our transmission and distribution systems’ reliability and performance, address our aging power system infrastructure, facilitate new generation, and improve service to our customers. Capital investments for the next few years will include expenditures required to build critical infrastructure identified in the Long-Term Energy Plan (LTEP), which is based on recommendations from the Ontario Power Authority (OPA), and expenditures to address our aging power system infrastructure. Our future capital expenditures are more fully described in the section “Future Capital Investments.”

OVERVIEW

Our Businesses

Our company has three reportable segments:

| • | Our Transmission Business, which comprises the core business of providing electricity transportation and connection services, is responsible for transmitting electricity throughout the Ontario electricity grid; |

| • | Our Distribution Business, which comprises the core business of delivering and selling electricity to customers; and |

| • | Other, the operations of which primarily consist of those of our telecommunications business. |

Transmission

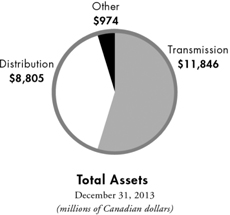

| Our Transmission Business includes the transmission business of our subsidiary Hydro One Networks, which owns and operates substantially all of Ontario’s electricity transmission system. Our transmission system forms an integrated transmission grid that is monitored, controlled and managed centrally from our Ontario Grid Control Centre. Our system operates over relatively long distances and links major sources of generation to transmission stations and larger area load centres. In 2013, we earned total transmission revenues of $1,529 million, primarily by transmitting approximately 140.7 TWh of electricity, directly or indirectly, to substantially all consumers of electricity in Ontario. Our transmission system is one of the largest in North America, and it is linked to five adjoining jurisdictions through 26 interconnections, through which we can accommodate electricity imports of up to 6,510 MW in the summer and 6,390 MW in the winter, and electricity exports of up to 6,070 MW in the summer and 6,270 MW in the winter. In terms of assets, our Transmission Business is our largest business segment, representing approximately 55% of our total assets at December 31, 2013. |  |

2

HYDRO ONE INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

For the years ended December 31, 2013 and 2012

Distribution

| Our consolidated Distribution Business includes the distribution business of our subsidiary Hydro One Networks, as well as our subsidiaries Hydro One Brampton Networks Inc. (Hydro One Brampton Networks) and Hydro One Remote Communities Inc. (Hydro One Remote Communities). Our consolidated distribution system is the largest in Ontario and spans roughly 75% of the province. We serve approximately 1.4 million rural and urban customers. Hydro One Remote Communities operates small, regulated generation and distribution systems in a number of remote communities across northern Ontario that are not connected to Ontario’s electricity grid. In 2013, we earned total distribution revenues of $4,484 million, and over half of our distribution revenues were earned from our residential customers. At December 31, 2013, our Distribution Business assets represented approximately 41% of our total assets. |

Other

Our Other business segment primarily represents the operations of our subsidiary, Hydro One Telecom Inc. (Hydro One Telecom), which markets fibre-optic capacity to telecommunications carriers and commercial customers with broadband network requirements, including a dedicated optical network providing secure, high-capacity connectivity across numerous health care locations in Ontario. In 2013, our Other business segment contributed revenues of $61 million, and had assets of $974 million at December 31, 2013, representing 4% of our total assets.

Our Strategy

Our corporate strategy builds on our strong commitment to the Province and is shaped by our values. It lays out a set of objectives to position our company to achieve our mission and vision, which is to be an innovative and trusted company delivering electricity safely, reliably and efficiently to create value for our customers. Our values represent our core beliefs.

| • | Health and safety: Nothing is more important than the health and safety of our employees, those who work on our property, and the public. |

| • | Excellence: We achieve excellence through continuous training, ensuring we are prepared and equipped to deliver high-quality and affordable service, with integrity. |

| • | Stewardship: We invest in our assets and people to build a safe, environmentally sustainable electricity network in a commercial manner. |

| • | Innovation: We innovate through new processes, people and technology to allow us to find better ways to meet the needs of our customers. |

We have eight strategic objectives that are inextricably linked. They drive the fulfillment of our mission and vision and ensure we remain focused on achieving our corporate goal of providing safe, reliable and affordable service to our customers, today and tomorrow, while increasing enterprise value for our shareholder.

| • | Creating an injury-free workplace and maintaining public safety. Health and safety must be integrated into all that we do as we continue to reinforce that nothing is more important than the health and safety of our employees. We will continue to create a passion for preventing injury, staying safe and keeping each other safe. We will invest in building a culture of accountability to continue our drive to zero injuries in the workplace. In addition, we will continue to strengthen our already strong safety culture through our Journey to Zero initiative and our successful certification to the Occupational Health and Safety Assessment Series (OHSAS) 18001 standard. |

| • | Satisfying our customers. We exist to serve our customers, and serving our customers means reducing costs, improving customer service and meeting their expectations regarding reliable power supply. We will continue to |

3

HYDRO ONE INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

For the years ended December 31, 2013 and 2012

focus our efforts to improve our relationship with customers and to improve our customers’ satisfaction with us. We will meet our commitments, make customers our focus in all planning discussions, communicate effectively, coordinate across our company, and maximize opportunities to improve our corporate image and every customer interaction. We will develop and deliver targeted customer segment strategies, products and delivery channels that will respond to their unique needs. |

| • | Continuous innovation. Innovation represents one of our values and is critical to achieving our mission and vision. We have been using innovation and technology to build the foundation of our company as the utility of the future. Over the next two decades, we will continue to build on that foundation to improve the reliability and efficiency of our transmission and distribution systems and provide our customers with more capability to manage their power costs. The development of the Advanced Distribution System (ADS) is a key element in our investment in innovation, as are the investments we have made, through our Cornerstone project, in next generation business tools to enable us to implement leading industry practices and increase productivity. |

| • | Building and maintaining reliable, affordable transmission and distribution systems. Our transmission strategy is to provide a robust and reliable provincial grid that accommodates Ontario’s emerging generation profile, manages an aging asset base and meets demand requirements through prudent expansion and effective maintenance. Our distribution strategy is focused on continuing to meet the challenge of providing reliable, affordable service to our customers in a wide range of geographical regions and climate zones; incorporating ADS technology to provide greater visibility; and increased control and improved customer service. We will meet customer expectations regarding reliability, in part through our investment planning process, which starts with the identification of asset and customer needs. |

| • | Protecting and sustaining the environment for future generations. Consistent with our value of stewardship, we play a central role in reducing Ontario’s carbon footprint through the delivery of clean and renewable energy and through measures that allow our customers to manage and reduce their energy use. |

| • | Championing people and culture. We believe our primary strength is the capability of our people. In order to sustain this advantage, we will continue to address the issues of corporate culture, labour demographics, diversity, development of critical core competencies, and skill and knowledge retention. We will continue to develop a culture of accountability and trust as a key component to fostering employee engagement. Our labour strategy is to consolidate and clarify our collective agreements, increase flexibility and reduce costs, and maintain a progressive relationship with our unions. |

| • | Maintaining a commercial culture that increases value for our shareholder. For the delivery component of a customer bill, we are committed to maintaining total annual bill impacts for an average residential customer at or below the rate of inflation, and delivering income and dividends to our shareholder. We will pursue growth opportunities through local distribution company (LDC) consolidation to increase the enterprise value of our company by leveraging our existing assets, technologies, capabilities, unparalleled experience in LDC acquisitions and our distribution and transmission footprint. |

| • | Achieving productivity improvements and cost-effectiveness. To achieve our mission and vision, we must constantly strive for productivity through efficiency and effective management of costs. Productivity is key to meeting our other strategic objectives and, in particular, to achieving value for our customers and our shareholder. |

Performance Measures and Targets

We target and measure our performance by using a balanced scorecard approach. Key performance drivers are closely monitored throughout the year to ensure that we maintain a focus on our strategic objectives and take mitigating actions as required. In 2013, we met or exceeded five of nine stretch targets. Overall, we are making progress towards achieving many of our strategic goals.

Achieving productivity improvements and cost-effectiveness

One of our strategic objectives is to increase productivity through efficiency improvements and effective management of costs. The measures for this objective for 2013 were transmission unit cost and distribution unit cost. For transmission unit cost, we measured the capital expenditures and operation, maintenance and administration costs per dollar of gross in-service assets (expressed as a percentage). For distribution unit cost, the measure is capital expenditures and operation, maintenance and administration costs per kilometre of line ($’000/km) due to the

4

HYDRO ONE INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

For the years ended December 31, 2013 and 2012

length of line required to connect our rural customers. Our objective with our ongoing work and investment program is to maintain and improve our assets and monitor our productivity year-over-year. Our transmission unit cost target was set at 9.8%, and we met this target. The distribution unit cost target was set at $9,800 per kilometre of line. We did not meet this target.

Building and maintaining reliable, cost-effective transmission and distribution systems

We continue to build and retain public confidence and trust in our operations, as stewards of Ontario’s electricity grid. In 2013, we continued our focus on this strategic priority by investing in the key assets of the electricity delivery system and by operating the existing system for customers in a safe, reliable and efficient fashion. We are conscious that commercial customers of all sizes require reliable service to allow them to deliver their products and services and that customers’ expectations are for a reasonably limited duration when interruptions occur. Transmission and distribution reliability is measured through the duration of customer interruptions.

For the duration of unplanned customer interruptions within our transmission business, the target for 2013 was 9 minutes per delivery point. We did not meet this target.

For the duration of unplanned customer interruptions within our distribution business, the target for 2013 was set at 6.7 hours per customer. While we did not meet this target, our Board of Directors noted that the impact of storms in January and February of 2013 would require our company to change work practices and alter resource levels to simply meet the target and that the cost to do so would be prohibitive and not in the best interests of the ratepayer. Considering the storm impacts and the positive results over the balance of the year, our Board of Directors, in the exercise of its discretion, determined that this target was met.

Satisfying our customers

Customer satisfaction measures the degree to which our transmission and distribution customers are satisfied with the service they receive from our company. Customer satisfaction is based on the results of customer surveys conducted on our behalf by independent third parties. In 2013, for transmission customers we targeted a customer satisfaction rate of 82%. The survey was given to three major groups of transmission customers. Our Board of Directors determined that there was significant improvement in two of the three groups which comprise the survey members and accordingly, in the exercise of its discretion, considered this target met. For our distribution customers, we targeted a satisfaction rate of 86%, and we met this target.

Employee engagement

We continue to focus efforts on increasing employee engagement throughout the Company. An engaged workforce is one in which employees embrace the corporate values of safety, stewardship, excellence and innovation. The employee engagement survey is administered by an independent third party expert. Our goal is to improve the grand mean score year-over-year. The target of improving the grand mean score to 4.06 (out of 5) in 2013 was not met.

Maintaining a commercial culture that increases value for our shareholder

Achievement of strong financial performance is measured by a performance measure of targeted level of net income after tax. Our 2013 target was $702 million net income after tax, and we exceeded our target.

Creating an injury-free workplace and maintaining public safety

The safety of our employees is paramount. In 2013, we used medical attentions, defined as injuries that require treatment by a medical practitioner (beyond first aid), as the performance measure for this strategic objective. The medical attentions measure reflects incidents that are reported to the Workplace Safety Insurance Board and is calculated as the number of attentions per 200,000 hours worked. In 2013, we set a target of no higher than 1.9 attentions per 200,000 hours worked. We did not meet this target.

5

HYDRO ONE INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

For the years ended December 31, 2013 and 2012

REGULATION

Our electricity transmission and distribution businesses are licensed and regulated by the OEB. Our transmission revenues primarily include our transmission tariff, which is based on the province-wide Uniform Transmission Rates (UTRs) approved by the OEB for all transmitters across Ontario. Our distribution revenues primarily include our distribution tariff, which is also based on OEB-approved rates, and the recovery of the cost of purchased power used by our customers. Transmission and distribution tariff rates are set based on an approved revenue requirement that provides for cost recovery and a return on deemed common equity. In addition, the OEB approves rate riders to allow for the recovery or disposition of specific regulatory accounts over specified timeframes.

The OEB approved the use of US GAAP for rate setting and regulatory accounting and reporting by Hydro One Networks’ Transmission and Distribution Businesses, as well as by Hydro One Remote Communities, beginning with the year 2012. Hydro One Brampton Networks currently uses Canadian GAAP for its distribution rate-setting purposes.

Renewed Regulatory Framework

In December 2010, the OEB initiated a coordinated consultation process for the development of a Renewed Regulatory Framework for Electricity. In October 2012, the OEB issued its reportA Renewed Regulatory Framework for Electricity Distributors: A Performance Based Approach. The report identified three rate-setting models available to provide choices suitable for distributors having varying capital requirements: a fourth generation Incentive Regulation Mechanism (IRM); a custom rate setting; and an Annual Incentive Rate-setting Index method. The report also provided information on performance measurement, continuous improvement and implementation of the new framework.

In late 2013, the OEB issued itsReport of the Board on Rate-Setting Parameters and Benchmarking under the Renewed Regulatory Framework for Ontario’s Electricity Distributors. This report sets out the OEB’s policies and approaches to the rate adjustment parameters for incentive rate setting for electricity distributors and the benchmarking of electricity distributor total cost performance. It also includes the OEB’s determination on rate adjustment parameter values for 2014 incentive rate setting, which were used to adjust Hydro One Networks’ 2014 distribution rates.

Electricity Rates

Under the current market structure, low-volume and designated consumers pay electricity rates established through the Regulated Price Plan (RPP) and wholesale electricity consumers pay a blend of regulated, contract and wholesale spot market prices. The OEB sets prices for RPP customers based on both a two-tiered electricity pricing structure, with seasonal consumption thresholds, and a three-tiered electricity pricing structure with Time of Use (TOU) thresholds. Substantially all of our RPP customers are now on TOU billing. We received an exemption from the OEB, effective until December 31, 2014, from implementing mandatory TOU pricing for approximately 122,000 customers that are currently out of reach of our smart meter telecommunications infrastructure. Unexpected shortfalls or overpayments associated with the RPP are temporarily financed by the OPA. RPP prices are reviewed by the OEB every six months and may change based on an updated OEB forecast and any accumulated differences between the amount that customers paid for electricity and the amount paid to generators in the previous period.

Customers who are not eligible for the RPP and wholesale customers pay the market price for electricity, adjusted for the difference between market prices and prices paid to generators by the Independent Electricity System Operator (IESO) under theElectricity Act, 1998. The IESO is responsible for overseeing and operating the wholesale market, as well as ensuring the reliability of the integrated power system. The following is a summary of the RPP for the reporting and comparative periods:

RPP | Tier Threshold (kWh/month) | Tier Rates (cents/kWh) | ||||||||||||||

Effective Date | Residential | Non-Residential | Lower Tier | Upper Tier | ||||||||||||

November 1, 2011 | 1,000 | 750 | 7.1 | 8.3 | ||||||||||||

May 1, 2012 | 600 | 750 | 7.5 | 8.8 | ||||||||||||

November 1, 2012 | 1,000 | 750 | 7.4 | 8.7 | ||||||||||||

May 1, 2013 | 600 | 750 | 7.8 | 9.1 | ||||||||||||

November 1, 2013 | 1,000 | 750 | 8.3 | 9.7 | ||||||||||||

6

HYDRO ONE INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

For the years ended December 31, 2013 and 2012

RPP TOU | Rates (cents/kWh) | |||||||||||

Effective Date | On Peak | Mid Peak | Off Peak | |||||||||

November 1, 2011 | 10.8 | 9.2 | 6.2 | |||||||||

May 1, 2012 | 11.7 | 10.0 | 6.5 | |||||||||

November 1, 2012 | 11.8 | 9.9 | 6.3 | |||||||||

May 1, 2013 | 12.4 | 10.4 | 6.7 | |||||||||

November 1, 2013 | 12.9 | 10.9 | 7.2 | |||||||||

Transmission Rates

In May 2010, we filed a cost-of-service application with the OEB for 2011 and 2012 transmission rates, seeking the approval of revenue requirements of approximately $1,446 million for 2011 and $1,547 million for 2012. In December 2010, the OEB approved revenue requirements of $1,346 million for 2011 and $1,658 million for 2012. The approved 2012 revenue requirement was higher than that applied for, reflecting OEB direction for our company to adopt a cost capitalization policy based on modified IFRS. This adjustment was subsequently reversed when the OEB approved the use of US GAAP for transmission rate-setting purposes beginning January 1, 2012. Consequently, the OEB approved a revenue requirement of $1,418 million for 2012, along with new 2012 UTRs, with an effective date of January 1, 2012. The new rates resulted in an approximate 8% transmission rate increase, or 0.6% when considering total bill impact, for a typical residential customer consuming 800 kWh per month. The adoption of US GAAP in lieu of modified IFRS as a basis for rate setting decreased the approved rates by approximately 15%.

In May 2012, we filed a cost-of-service application with the OEB for our 2013 and 2014 transmission rates. The application sought OEB approval for revenue requirement increases of approximately 0.6% in 2013 and 9.1% in 2014, or estimated increases of 0% in 2013 and 0.7% in 2014 on an average customer’s total bill. In November 2012, we submitted a draft Rate Order, which included revenue requirements of approximately $1,438 million and $1,528 million for 2013 and 2014, respectively. For the transmission portion of the bill, this represents no change from existing 2012 OEB-approved rate levels in 2013 and a 5.8% increase in 2014. For a typical residential customer consuming 800 kWh per month, this represents increases of nil for 2013 and 0.5% for 2014. In December 2012, the OEB approved the 2013 and 2014 transmission revenue requirements of $1,438 million and $1,528 million, respectively, and the 2013 Ontario UTRs, which remained unchanged at the 2012 levels.

On December 6, 2013, we submitted a draft Rate Order for our 2014 transmission rates. The 2014 revenue requirement has been increased to $1,535 million from the originally-approved revenue requirement of $1,528 million, primarily due to changes in the cost of capital parameters for 2014 released by the OEB in November 2013. On January 9, 2014, the OEB approved the draft Rate Order for 2014 transmission rates as filed. For the transmission portion of a customer’s bill, this represents an increase of 6.3% in 2014, or 0.5% when considering total bill impact, for a typical residential customer consuming 800 kWh per month.

Distribution Rates

As a distributor, we are responsible for delivering electricity and billing our customers for our approved distribution rates, purchased power costs and other approved regulatory charges. Substantially all of our purchased power costs and other approved regulatory charges are settled through the IESO, which facilitates payments to other parties, such as generators, the Ontario Electricity Financial Corporation (OEFC), and itself.

| • | Hydro One Networks |

Hydro One Networks elected to retain the same distribution rates for 2012 as approved by the OEB for 2011, with a revenue requirement of $1,218 million.

In June 2012, Hydro One Networks filed an IRM rate application with the OEB for 2013 distribution rates, to be effective January 1, 2013. In December 2012, the OEB issued a final Rate Order, which resulted in an increase in distribution rates of approximately 1.3% in 2013, or 0.4% when considering total bill impact, for a typical residential customer consuming 800 kWh per month.

On April 26, 2013, Hydro One Networks filed an IRM rate application with the OEB for 2014 distribution rates, to be effective January 1, 2014. On September 26, 2013, the OEB issued a partial decision, approving a rate rider to

7

HYDRO ONE INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

For the years ended December 31, 2013 and 2012

recover a 2014 revenue requirement of $29.3 million for operation, maintenance and administration expenses and in-service capital costs of the ADS Project, which will modernize our distribution system. On December 5, 2013, the OEB issued its final decision, which resulted in an increase of distribution rates of approximately 2.4% in 2014, or 0.85% when considering total bill impact, for a typical residential customer consuming 800 kWh per month.

On December 19, 2013, Hydro One Networks filed a 2015-2019 distribution custom rate application with the OEB, for rates effective January 1 of each test year. This application is a five-year custom rate application which is being submitted under the OEB’s Renewed Regulatory Framework for Electricity Distributors. It has been customized to fit Hydro One Networks’ specific circumstances, which necessitate significant multi-year investments. The submitted evidence includes the overall business plan, revenue requirements, and rate information necessary to support the issuance of a notice by the OEB. We are seeking OEB approvals for revenue requirements of $1,411 million for 2015, $1,515 million for 2016, $1,571 million for 2017, $1,615 million for 2018, and $1,666 million for 2019. If the application is approved as filed, the resulting change to the distribution portion of the average customer bill will be approximately a 1.3% decrease in 2015, 4.2% increase in 2016, 2.6% increase in 2017, 1.9% increase in 2018, and 2.9% increase in 2019, for a typical residential customer consuming 800 kWh per month. When considering total bill impact, the resulting change will be approximately a 1.1% decrease in 2015, 1.5% increase in 2016, 0.9% increase in 2017, 0.7% increase in 2018, and 1.1% increase in 2019.

| • | Hydro One Brampton Networks |

In September 2011, Hydro One Brampton Networks filed an IRM application with the OEB for 2012 distribution rates, with an effective date of January 1, 2012. In January 2012, the OEB released a decision that resulted in a reduction in distribution rates of approximately 13.2% for 2012, or a 1.7% reduction on the average customer’s total bill, for a typical residential customer consuming 800 kWh per month. These rate reductions were primarily due to OEB-approved adjustments to depreciation rates.

In August 2012, Hydro One Brampton Networks filed an IRM application with the OEB for 2013 distribution rates, to be effective January 1, 2013. In December 2012, the OEB released a decision that resulted in an increase in distribution rates of approximately 0.3% for 2013, or less than 0.1% on the average customer’s total bill, for a typical residential customer consuming 800 kWh per month.

In August 2013, Hydro One Brampton Networks filed an IRM application with the OEB for 2014 distribution rates, to be effective January 1, 2014. On December 5, 2013, the OEB released a decision that resulted in a reduction in distribution rates of approximately 2.5% for 2014, or a 0.5% reduction on the average customer’s total bill, for a typical residential customer consuming 800 kWh per month.

| • | Hydro One Remote Communities |

In November 2011, Hydro One Remote Communities filed an IRM application with the OEB for 2012 distribution rates. In March 2012, the OEB approved an increase of approximately 1.08% to basic rates for the distribution and generation of electricity, with an effective date of May 1, 2012, representing an increase of approximately $1 on the average residential customer’s total bill.

In September 2012, Hydro One Remote Communities filed a cost-of-service application with the OEB for 2013 distribution rates, seeking approval for a 2013 revenue requirement of $53 million. In August 2013, the OEB issued a final decision approving a revenue requirement of $51 million and rate increase of approximately 3.45%, with an effective date of May 1, 2013.

In October 2013, Hydro One Remote Communities filed an IRM application with the OEB for 2014 distribution rates, seeking approval for a rate increase of approximately 0.48%, to be effective May 1, 2014.

Recent Industry Developments

Long-Term Energy Plan

In 2010, the Ministry of Energy released Ontario’s LTEP, which set out the province’s expected electricity needs until 2030 and supported the continued procurement of new, cleaner generation. The 2010 LTEP addressed seven key areas: demand, supply, conservation, transmission, Aboriginal communities, capital investments, and electricity prices.

8

HYDRO ONE INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

For the years ended December 31, 2013 and 2012

On December 2, 2013, the Province released its updated LTEP, which sets out the Province’s plan of action for the energy sector, including strategies for mitigating increases in electricity rates; increased renewable energy procurement; nuclear refurbishment; enhanced regional planning with respect to energy infrastructure; transmission enhancements; encouraging Aboriginal participation in energy development, transmission and conservation projects; and the expansion of natural gas infrastructure. The plans are guided by the goal of balancing five core principles: cost-effectiveness, reliability, clean energy, community engagement, and conservation and demand management (CDM). Pursuant to the updated LTEP, the Province “will encourage Ontario Power Generation Inc. (OPG) and Hydro One to explore new business lines and opportunities inside and outside Ontario. These opportunities will help leverage existing areas of expertise and grow revenues for the benefit of Ontarians.” We will continue to work with the Province to develop business plans and efficiency targets that will reduce costs and result in significant ratepayer savings.

In November 2013, the Minister issued a directive to the OEB, which in turn issued a decision and order on January 9, 2014, to amend the transmission licence of Hydro One Networks to develop and seek approval for the Northwest Bulk Transmission Line Project, an expansion or reinforcement of the transmission system in the area west of Thunder Bay. The scope and timing of the Northwest Bulk Transmission Line Project shall be in accordance with the recommendations of the OPA.

Distribution Sector Consolidation

In April 2012, the Province announced it was launching a comprehensive review of Ontario’s electricity sector to explore options to improve efficiencies, including LDC consolidation. As a result, the Province created the Ontario Distribution Sector Review Panel (Panel). In December 2012, the Panel released its report, “Renewing Ontario’s Electricity Distribution Sector: Putting the Consumer First” with recommendations for electricity sector consolidation. This report recommended that the 73 LDCs, comprising the focus of the report, be consolidated into eight to 12 larger regional electricity distributors within a two-year timeframe. Specifically, it recommended there be two regional distributors in northern Ontario and between six and ten regional distributors in southern Ontario with a minimum of 400,000 customers each. Given our company’s position as the largest LDC, the report recommended that Hydro One Networks be given unambiguous direction to lead and engage in the discussion of the merger of distribution assets with the appropriate interested utilities on a commercial basis. The minister of Energy subsequently indicated he was supportive of voluntary consolidation and expects all LDCs to pursue innovative partnerships and transformative initiatives that will result in electricity ratepayer savings.

On April 2, 2013, we reached an agreement with Norfolk County to acquire the outstanding shares of Norfolk Power Inc. (Norfolk Power) for $93 million, subject to final closing adjustments. We will pay Norfolk County approximately $66 million net after assuming Norfolk Power’s existing debt of approximately $27 million. Norfolk Power is a holding company that owns Norfolk Power Distribution Inc., a local distribution company, and Norfolk Energy Inc., a non-rate regulated energy services company. The selection of our company as successful bidder followed a comprehensive competitive sales process initiated by Norfolk Power. The acquisition is pending a regulatory decision from the OEB, which is anticipated in 2014.

We will continue to pursue growth opportunities through LDC consolidation by leveraging our existing assets, technologies, capabilities, unparalleled experience in LDC acquisitions, and our distribution footprint.

Procurement of New Generation

In 2009, the OPA launched its Feed-in Tariff (FIT) Program which is designed to procure energy from a wide range of renewable energy sources, including wind, solar, photovoltaic, bio-energy, and waterpower up to 50 MW. The FIT program is currently divided into three streams: Micro FIT (projects up to 10 kW), Small FIT (projects between 10 kW and 500 kW) and regular FIT (projects greater than 500 kW), all of which may result in connections to our distribution system. Under the FIT program, the OPA has entered into contracts or conditional contracts with generation proponents pursuant to which the OPA will pay a fixed rate for power produced over a specified period of time. We continue to connect projects for which there are firm contracts.

On May 30, 2013, the Province announced that it would make 900 MW of new capacity available between 2013 and 2018 for the Small FIT and Micro FIT programs. The Province has set annual procurement targets, from 2014 onwards, of 150 MW for Small FIT generation and 50 MW for Micro FIT generation. The Province is working with the OPA to develop a competitive process for renewable energy generation projects above 500 kW. The new process will replace the existing large project stream of the FIT program. As at December 31, 2013, our company has connected more than 370 FIT and 11,000 Micro FIT projects.

9

HYDRO ONE INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

For the years ended December 31, 2013 and 2012

Conservation and Demand Management

In April 2012, the OEB issued its CDM guidelines for all electricity distributors. These guidelines provide guidance on certain provisions in the CDM Code and the type of evidence that should be filed by distributors in support of an application for OEB-approved CDM programs. The guidelines also provide details on the Lost Revenue Adjustment Mechanism (LRAM) related to CDM programs implemented under the CDM Code. LRAM is the mechanism by which LDCs are compensated for lost revenues associated with their respective load reductions resulting from CDM programs. In addition, the guidelines state that savings associated with TOU pricing are eligible to be counted towards the 2011-2014 CDM targets.

In December 2012, the Minister of Energy issued a directive to the OPA to extend funding for the OPA-contracted Ontario-wide CDM programs for one additional year, to December 31, 2015. This extension will provide an opportunity for the OPA and LDCs to collaboratively work to strengthen the current framework, and to keep customer programs in place for 2015.

On September 30, 2013, in accordance with the CDM Code, Hydro One Networks and Hydro One Brampton Networks each filed a 2012 Annual CDM Report with the OEB. The reports discussed CDM activities, energy and peak demand savings results achieved in 2012, and plans to reach CDM targets by the end of 2014. Hydro One Networks reported that it expects to reach 100% of its demand target and 80% of its cumulative energy target by 2014. Hydro One Brampton Networks reported that it expects to reach 68% of its demand target and 100% of its cumulative energy target by 2014. The OEB has indicated that there are several LDCs that have a similar issue. The OEB is aware of our situation.

ANNUAL RESULTS OF OPERATIONS

Year ended December 31 (millions of Canadian dollars) | 2013 | 2012 | $ Change | % Change | ||||||||||||

Revenues | 6,074 | 5,728 | 346 | 6 | ||||||||||||

Purchased power | 3,020 | 2,774 | 246 | 9 | ||||||||||||

Operation, maintenance and administration | 1,106 | 1,071 | 35 | 3 | ||||||||||||

Depreciation and amortization | 676 | 659 | 17 | 3 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

| 4,802 | 4,504 | 298 | 7 | |||||||||||||

Income before financing charges and provision for payments in lieu of corporate income taxes | 1,272 | 1,224 | 48 | 4 | ||||||||||||

Financing charges | 360 | 358 | 2 | 1 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Income before provision for payments in lieu of corporate income taxes | 912 | 866 | 46 | 5 | ||||||||||||

Provision for payments in lieu of corporate income taxes | 109 | 121 | (12 | ) | (10 | ) | ||||||||||

|

|

|

|

|

|

|

| |||||||||

Net income | 803 | 745 | 58 | 8 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

10

HYDRO ONE INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

For the years ended December 31, 2013 and 2012

Revenues

Year ended December 31 (millions of Canadian dollars) | 2013 | 2012 | $ Change | % Change | ||||||||||||

Transmission | 1,529 | 1,482 | 47 | 3 | ||||||||||||

Distribution | 4,484 | 4,184 | 300 | 7 | ||||||||||||

Other | 61 | 62 | (1 | ) | (2 | ) | ||||||||||

|

|

|

|

|

|

|

| |||||||||

| 6,074 | 5,728 | 346 | 6 | |||||||||||||

|

|

|

|

|

|

|

| |||||||||

Average annual Ontario 60-minute peak demand (MW)1 | 21,493 | 21,132 | 361 | 2 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Distribution – units distributed to customers (TWh)1 | 29.8 | 29.2 | 0.6 | 2 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

| 1 | System-related statistics are preliminary. |

Transmission

Transmission revenues primarily consist of our transmission tariff, which is based on the monthly peak electricity demand across our high-voltage network. The tariff is designed to recover revenues necessary to support a transmission system with sufficient capacity to accommodate the maximum expected demand. Demand is primarily influenced by weather and economic conditions. Transmission revenues also include export revenues associated with transmitting excess generation to surrounding markets, ancillary revenues primarily attributable to maintenance services provided to generators, and secondary use of our land rights.

Our 2013 transmission revenues were higher by $47 million, or 3%, compared to 2012. The average Ontario 60-minute peak demand was higher in 2013, resulting in an increase in transmission revenues of $26 million, compared to 2012. The higher energy consumption in 2013 mainly resulted from a warmer summer and a colder winter, as compared to 2012. In addition, we experienced higher revenues of $21 million in 2013, associated with the OEB’s approval of export service revenues and ancillary services.

Distribution

Distribution revenues include our distribution tariff and amounts to recover the cost of purchased power used by the customers of our Distribution Business. Accordingly, our distribution revenues are influenced by the amount of electricity we distribute, the cost of purchased power and our distribution tariff rates. Distribution revenues also include minor ancillary distribution service revenues, such as fees related to the joint use of our distribution poles by the telecommunications and cable television industries, as well as miscellaneous charges such as charges for late payments.

Our 2013 distribution revenues were higher by $300 million, or 7%, compared to 2012. The increase was primarily due to the recovery of higher purchased power costs of $246 million, as described below under “Purchased Power.” In addition, energy consumption was higher by $29 million in 2013, mainly resulting from a warmer summer and a colder winter, as compared to 2012. Distribution revenues also increased by $15 million as a result of our placement in service of new smart grid and smart meter investments, which are currently being recovered through separate rate mechanisms.

In December 2012, the OEB approved new tariff rates effective January 1, 2013, based on its third generation IRM process. As part of the IRM decision, the OEB approved our application for an additional rate rider related to an incremental capital module (ICM) adjustment to our rates, reflecting our placement in service of certain specific capital investments. This ICM approval resulted in an increase of $13 million, compared to 2012. In addition, the OEB’s IRM decision resulted in higher distribution revenues of $10 million, which will support the maintenance and investment requirements of our distribution system and enable the safe and reliable delivery of electricity to our customers throughout Ontario. The 2013 distribution revenue increases were partially offset by lower 2013 ancillary distribution revenues of $13 million, primarily associated with OEB-approved regulatory accounts.

11

HYDRO ONE INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

For the years ended December 31, 2013 and 2012

Purchased Power

Purchased power costs are incurred by our Distribution Business and represent the cost of purchased electricity delivered to customers within our distribution service territory. These costs comprise the wholesale commodity cost of energy, the IESO wholesale market service charges, and transmission charges levied by the IESO. The commodity cost of energy is based on the OEB’s RPP, as described above under “Regulation.”

Our 2013 purchased power costs increased by $246 million, or 9%, to $3,020 million, compared to 2012. The increase in our 2013 purchased power costs was mainly due to a $104 million increase resulting from higher purchased power costs for customers who are not eligible for the RPP, an $85 million increase resulting from the impact of changes in the OEB’s RPP rates for residential and other eligible customers, a $44 million increase due to higher electricity demand, a $9 million increase resulting from the IESO’s Smart Metering Entity charge effective May 1, 2013, and a $4 million reduction in wholesale market service charges levied by the IESO.

Operation, Maintenance and Administration

Our operation, maintenance and administration costs consist of labour, materials, equipment and purchased services which support the operation and maintenance of the transmission and distribution systems. Also included in these costs are property taxes and payments in lieu thereof related to our transmission and distribution lines, stations and buildings. Our transmission operation, maintenance and administration costs are incurred to sustain our high-voltage transmission stations, lines and rights-of-way. Our distribution operation, maintenance and administration costs are required to maintain our low-voltage distribution system. Our company continues to focus on managing its costs, while continuing to substantially complete our planned work programs for both our Transmission and Distribution Businesses.

Year ended December 31 (millions of Canadian dollars) | 2013 | 2012 | $ Change | % Change | ||||||||||||

Transmission | 375 | 402 | (27 | ) | (7 | ) | ||||||||||

Distribution | 672 | 608 | 64 | 11 | ||||||||||||

Other | 59 | 61 | (2 | ) | (3 | ) | ||||||||||

|

|

|

|

|

|

|

| |||||||||

| 1,106 | 1,071 | 35 | 3 | |||||||||||||

|

|

|

|

|

|

|

| |||||||||

Transmission

Our 2013 transmission operation, maintenance and administration costs decreased by $27 million, or 7%, to $375 million, compared to 2012. Within our work programs, we continued to invest in the safe and reliable operation of our transmission system.

Expenditures in support of our transmission system decreased by $33 million in 2013, compared to 2012, primarily due to a reduction to our provision for payments in lieu of property taxes related to transmission stations for the years 1999 to 2012, inclusive, following the finalization of the related regulations and receipt of a final assessment of our property tax returns. The decrease in our transmission system support costs was partially offset by an increase of $6 million in our work program costs, compared to 2012. This increase was primarily due to higher expenditures related to our forestry work program on our transmission rights-of-way resulting from heavy tree densities, power equipment preventive and corrective maintenance, and emergency restoration requirements as a result of severe flooding at our Richview and Manby transmission stations caused by a major rainstorm in July 2013. We also experienced increased cyber security and internal compliance program requirements related to the reliability standards and criteria mandated by the North American Electric Reliability Corporation (NERC). These increases in work program costs were partially offset by lower expenditures related to the OPA’s recommendation to increase short circuit and/or transformer capacity at ten of our transmission stations to enable the connection of small renewable projects, as this work was substantially completed by the end of 2012. Expenditures for these station upgrades were recorded within operation, maintenance and administration rather than as capital expenditures, given that recovery was restricted pursuant to a shareholder declaration made in April 2011. No such declarations were issued in 2013. In addition, we experienced lower expenditures within our overhead lines program.

12

HYDRO ONE INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

For the years ended December 31, 2013 and 2012

Distribution

Our 2013 distribution operation, maintenance and administration costs increased by $64 million, or 11%, to $672 million, compared to 2012. Our work program expenditures increased by $63 million compared to 2012, mainly as a result of increased power restoration expenditures following major storms in 2013, increased customer-driven work related to trouble calls and cable locates in support of the new One Call Program, higher requirements within the line patrol program, higher expenditures on our customer care programs, higher Information Technology (IT) improvements and enhancements, and continued work on the ADS Project. These impacts were partially offset by lower station corrective and preventive maintenance expenditures, as well as lower line clearing expenditures, compared to 2012. Our expenditures in support of our distribution system increased marginally by $1 million, compared to 2012.

Depreciation and Amortization

Our 2013 depreciation and amortization costs increased by $17 million, or 3%, compared to 2012. This increase was attributable to higher 2013 depreciation expense, primarily related to our placement of new assets in service consistent with our ongoing capital work program, as well as higher asset removal costs in 2013.

Financing Charges

Financing charges increased by $2 million, or 1%, to $360 million for 2013, compared to 2012. Higher financing costs in 2013 were mainly due to a decrease in interest capitalized, partially offset by a decrease in interest expense on long-term debt due to lower average interest rates.

Provision for Payments in Lieu of Corporate Income Taxes

The provision for payments in lieu of corporate income taxes (PILs) decreased by $12 million, or 10%, to $109 million in 2013, compared to 2012. This decrease primarily resulted from changes in net temporary differences, and a true-up relating to the 2012 research and development tax credits. This reduction was partially offset by the impact of higher levels of pre-tax income in 2013, compared to 2012.

Net Income

Our 2013 net income increased by $58 million, or 8%, to $803 million, compared to 2012. We experienced higher distribution revenues in 2013 mainly reflecting increased purchased power costs, primarily related to the OEB’s RPP rate-setting process and the IESO’s spot market. We also experienced increased transmission revenues in 2013 reflecting a higher peak demand due to intermittent periods of hot weather in the summer of 2013, as well as extreme cold winter weather. Our 2013 net income was also positively impacted by a lower provision for PILs and by a reduction to our provision for payments in lieu of transmission station property taxes, following the finalization of the assessment of certain prior years’ property tax returns. This reduction was partially offset by power restoration expenditures following several major storms in 2013.

QUARTERLY RESULTS OF OPERATIONS

The following table sets forth unaudited quarterly information for each of the eight quarters, from the quarter ended March 31, 2012 through December 31, 2013. This information has been derived from our unaudited interim Consolidated Financial Statements and our audited annual Consolidated Financial Statements which include all adjustments, consisting only of normal recurring adjustments, necessary for fair presentation of our financial position and results of operations for those periods. These operating results are not necessarily indicative of results for any future period and should not be relied upon to predict our future performance.

(millions of Canadian dollars) | 2013 | 2012 | ||||||||||||||||||||||||||||||

Quarter ended | Dec. 31 | Sept. 30 | Jun. 30 | Mar. 31 | Dec. 31 | Sept. 30 | Jun. 30 | Mar. 31 | ||||||||||||||||||||||||

Total revenue | 1,557 | 1,542 | 1,403 | 1,572 | 1,435 | 1,466 | 1,359 | 1,468 | ||||||||||||||||||||||||

Net income | 160 | 218 | 168 | 257 | 165 | 201 | 169 | 210 | ||||||||||||||||||||||||

Net income to common shareholder | 155 | 214 | 163 | 253 | 160 | 197 | 164 | 206 | ||||||||||||||||||||||||

13

HYDRO ONE INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

For the years ended December 31, 2013 and 2012

Electricity demand generally follows normal weather-related variations, and consequently, our electricity-related revenues and profit, all other things being equal, would tend to be higher in the first and third quarters than in the second and fourth quarters.

LIQUIDITY AND CAPITAL RESOURCES

Our primary sources of liquidity and capital resources are funds generated from our operations, debt capital market borrowings and bank financing. These resources will be used to satisfy our capital resource requirements, which continue to include our capital expenditures, servicing and repayment of our debt, and dividends.

Summary of Sources and Uses of Cash

Year ended December 31(millions of Canadian dollars) | 2013 | 2012 | ||||||

Operating activities | 1,404 | 1,294 | ||||||

Financing activities | ||||||||

Long-term debt issued | 1,185 | 1,085 | ||||||

Long-term debt retired | (600 | ) | (600 | ) | ||||

Dividends paid | (218 | ) | (370 | ) | ||||

Investing activities | ||||||||

Capital expenditures | (1,412 | ) | (1,463 | ) | ||||

Other financing and investing activities | 11 | 21 | ||||||

|

|

|

| |||||

Net change in cash and cash equivalents | 370 | (33 | ) | |||||

|

|

|

| |||||

Operating Activities

Net cash from operating activities increased by $110 million to $1,404 million in 2013, compared to 2012. The increase was primarily due to higher 2013 net income, compared to 2012, as well as changes in accrual balances, mainly related to timing of tax payments and to capital projects. The increase was partially offset by growth in accounts receivable balances, resulting from higher revenues and lower collections in the period.

Financing Activities

Short-term liquidity is provided through funds from operations, our Commercial Paper Program, under which we are authorized to issue up to $1,000 million in short-term notes with a term to maturity of less than 365 days, our revolving credit facility, and our holding of Province of Ontario Floating-Rate Notes.

Our Commercial Paper Program is supported by our $1,500 million committed revolving credit facility with a syndicate of banks, which matures in June 2018. In addition, our investment in Province of Ontario Floating-Rate Notes of $250 million (with a fair value of $251 million at December 31, 2013) maturing on November 19, 2014 also provides temporary liquidity. The short-term liquidity under this program and anticipated levels of funds from operations should be sufficient to fund our normal operating requirements.

At December 31, 2013, we had $9,045 million in long-term debt outstanding, including the current portion. Our notes and debentures mature between 2014 and 2062. Long-term financing is provided by our access to the debt markets, primarily through our Medium-Term Note (MTN) Program. The maximum authorized principal amount of medium-term notes issuable under this program is $3,000 million. At December 31, 2013, $1,815 million remained available until October 2015.

Cash generated from operations, after payment of expected dividends, will not be sufficient to fund capital expenditures, fund the repayment of our existing indebtedness, and meet other liquidity requirements. We rely on debt financing through our MTN Program and our Commercial Paper Program to repay our existing indebtedness and fund a portion of our capital expenditures.

14

HYDRO ONE INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

For the years ended December 31, 2013 and 2012

The credit ratings assigned to our debt securities by external rating agencies are important to our ability to raise capital and funding to support our business operations. Maintaining strong credit ratings allows us to access capital markets on competitive terms. A material downgrade of our credit ratings would likely increase our cost of funding significantly, and our ability to access funding and capital through the capital markets could be reduced. Our corporate credit ratings from approved rating organizations are as follows:

Rating | ||||

Rating Agency | Short-term Debt | Long-term Debt | ||

| DBRS Limited | R-1 (middle) | A (high) | ||

| Moody’s Investors Service Inc. | Prime-1 | A1 | ||

| Standard & Poor’s Rating Services Inc. (S&P)1 | A-1 | A+ | ||

| 1 | On April 25, 2012, S&P revised their outlook on our company to negative from stable. |

We have the customary covenants normally associated with long-term debt. Among other things, our long-term debt covenants limit our permissible debt as a percentage of our total capitalization, limit our ability to sell assets, and impose a negative pledge provision, subject to customary exceptions. The credit agreements related to our credit facilities have no material adverse change clauses that could trigger default. However, the credit agreements require that we provide notice to the lenders of any material adverse change within three business days of the occurrence. The agreements also provide limitations that debt cannot exceed 75% of total capitalization and that third party debt issued by our subsidiaries cannot exceed 10% of the total book value of our assets. We were in compliance with all these covenants and limitations as at December 31, 2013.

In 2013, we issued $1,185 million of long-term debt under our MTN Program, compared to $1,085 million of long-term debt issued in 2012. In 2013, we also repaid $600 million in maturing long-term debt, compared to $600 million of long-term debt called and redeemed in 2012, prior to its maturity date of November 15, 2012. We had no short-term notes outstanding at December 31, 2013 or 2012.

Common dividends are declared at the sole discretion of our Board of Directors, and are recommended by management based on results of operations, maintenance of the deemed regulatory capital structure, financial condition, cash requirements, and other relevant factors, such as industry practice and shareholder expectations. Common dividends pertaining to our quarterly financial results are generally declared and paid in the following quarter.

In 2013, we paid dividends to the Province in the amount of $218 million, consisting of $200 million in common dividends and $18 million in preferred dividends. In 2012, we paid dividends to the Province in the amount of $370 million, consisting of $352 million in common dividends and $18 million in preferred dividends. In 2013, cash dividends per common share were $2,000, compared to $3,523 per common share in 2012. Cash dividends per preferred share were $1.375 in each of 2013 and 2012.

Our objectives with respect to our capital structure are to maintain effective access to capital on a long-term basis at reasonable rates and to deliver appropriate financial returns to our shareholder.

Investing Activities

Capital investments consist of cash capital expenditures and related accruals. Capital investments primarily relate to enhancing and reinforcing of our transmission and distribution infrastructure.

Year ended December 31(millions of Canadian dollars) | 2013 | 2012 | $ Change | % Change | ||||||||||||

Transmission | 714 | 776 | (62 | ) | (8 | ) | ||||||||||

Distribution | 673 | 671 | 2 | — | ||||||||||||

Other | 7 | 7 | — | — | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total capital investments | 1,394 | 1,454 | (60 | ) | (4 | ) | ||||||||||

|

|

|

|

|

|

|

| |||||||||

Transmission

Our 2013 transmission capital investments decreased by $62 million, or 8%, to $714 million, compared to 2012. Investments to expand and reinforce our transmission system were $170 million in 2013, representing a decrease of $143 million, compared to 2012. The decrease was mainly due to the completion of our Bruce to Milton Transmission Reinforcement Project to connect refurbished nuclear and new wind generation sources in the Huron-Grey-Bruce area. This project was

15

HYDRO ONE INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

For the years ended December 31, 2013 and 2012

placed in-service in May 2012. In addition, we experienced lower expenditures as a result of completing our Commerce Way Transmission Station, a new load supply station in the City of Woodstock to address load growth issues in the Woodstock area, and the Switchyard Reconstruction Project at our Burlington Transmission Station, where two new 115 kV switchyards were constructed to increase the load supply capacity and to ensure reliability of supply to customers in the area. These projects were placed in-service in February 2013 and December 2012, respectively.

During 2013, we continued to invest in inter-area network projects to support the Province’s supply mix objectives for generation, and in load customer connections and local area supply projects to address growing loads. Our local area supply project expenditures include investments in our Midtown Transmission Reinforcement Project, which will provide additional supply capability to meet future load growth in midtown Toronto as well as areas to the west. Work at our Hearn Switching Station was partially completed in December 2013, where we rebuilt an existing switchyard that had reached its end-of-life. This project will also increase short circuit capability to accommodate future connection of renewable generation in central and downtown Toronto. We are also constructing our Lambton to Longwood Transmission Upgrade to increase transmission capability between our Lambton (Sarnia) and Longwood (London) transmission stations. This project is needed to satisfy government policy relating to the incorporation of 10,700 MW of non-hydroelectric renewable generation resources by 2021.

Investments to sustain our existing transmission system were $481 million in 2013, representing an increase of $89 million, compared to 2012. In 2013, we made significant investments in the refurbishment and replacement of end-of-life equipment for overhead lines and system re-investments in order to improve reliability, as well as replacement of circuit breakers. In addition, we have experienced higher expenditures associated with the timing of work related to the replacement of end-of-life power transformers. We continued work on replacing end-of-life underground transmission cables between our Strachan Transmission Station and Riverside Junction. These new underground cables will maintain a reliable supply of electricity to downtown Toronto. These increases were partially offset by lower expenditures related to the replacement of protection and control equipment.

Our other transmission capital investments were $63 million in 2013, representing a decrease of $8 million, compared to 2012. The decrease was mainly due to lower requirements associated with IT initiatives, including our entity-wide SAP information system replacement and improvement project, and timing of field facilities improvements. These reductions were partially offset by increased fleet acquisitions and emergency flood restoration work at our Richview transmission station caused by a major rainstorm in July 2013.

Distribution

Our 2013 distribution capital investments increased by $2 million, or less than 1%, to $673 million, compared to 2012. Investments to expand and reinforce our distribution network were $235 million in 2013, representing a decrease of $49 million, compared to 2012. We experienced reduced expenditures related to some of our major projects, including the ADS Project, as we completed the deployment of our Distribution Management System within our Owen Sound pilot area in 2012, and the Smart Metering Project, as most of the network expansion work was completed in 2012. In 2013, we also experienced a lower demand for new customer connections and upgrades. These decreases were partially offset by increased work on upgrading and adding capacity to our system to enable new customer connections and timing of generation connection projects. Given that the OEB has assessed the prudency of the ADS Project, the next phase of this project is anticipated in 2014.

Investments to sustain our distribution system were $324 million in 2013, representing an increase of $79 million, compared to 2012. The increase was primarily due to increased expenditures for replacements related to storm restoration work caused by major storms in 2013. We also experienced increased work within our wood pole replacement program and station refurbishment projects. Investments were also impacted by the timing of customer contribution payments received in 2012 relating to work for joint use and relocation of our lines. These increases were partially offset by lower work within our lines programs.

Our other distribution capital investments were $114 million in 2013, representing a decrease of $28 million, compared to 2012. The majority of these expenditures were related to the Customer Information System (CIS) phase of our entity-wide information system replacement and improvement project, which was placed into service in May 2013. In addition to replacing end-of-life systems, this implementation will result in process improvements that are expected to provide many benefits including enhancements to customer satisfaction through reduced call times and first call resolution of issues given faster availability of information. Productivity savings are also anticipated to result from performance improvements,

16

HYDRO ONE INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

For the years ended December 31, 2013 and 2012

consolidation and/or decommissioning of legacy IT systems. In addition, we experienced decreased expenditures associated with IT initiatives, including our entity-wide SAP information system replacement and improvement project, and the timing of field facilities improvements, partially offset by an increase in fleet acquisitions and emergency flood restoration work at our Richview Transmission Station.

Future Capital Investments

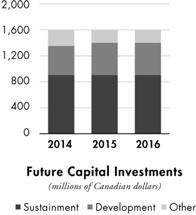

| Our capital investments for 2014 are budgeted at approximately $1,600 million. Our 2014 capital budgets for our Transmission and Distribution Businesses are approximately $950 million and $650 million, respectively. Consolidated capital investments are expected to be approximately $1,600 million in each of 2015 and 2016. These investment levels reflect the sustainment requirements of our aging infrastructure. Our sustainment program capital investments are expected to be approximately $900 million in each of 2014, 2015, and 2016. Our development capital investments are expected to be approximately $450 million in 2014, $500 million in 2015, and $500 million in 2016. Our development projects include the inter-area network upgrades that reflect supply mix policies, local area supply improvements, the ADS, new load and generation connections and requirements to enable Distributed Generation (DG), and customer demand work. Other capital investments are expected to be $250 million in 2014, $200 million in 2015, and $200 million in 2016. This includes investments in operating infrastructure integration, IT, fleet services and facilities, and real estate. Our future capital investments amounts do not include future LDC acquisitions. |  |

Transmission

Transmission capital investments are incurred to manage the replacement and refurbishment of our aging transmission infrastructure in order to ensure a continued reliable supply of energy to customers throughout the province. Our sustainment program future capital investments include the replacement of air blast circuit breakers and switchgear, high-voltage underground cables, and power transformers. These investments are necessary to ensure that we maintain our current levels of supply to our customers and continue to meet all regulatory, compliance, safety and environmental objectives.

Our development future capital investments include the Clarington Transmission Station Project to install additional auto-transformer capacity in east Greater Toronto Area; the Guelph Area Transmission Refurbishment Project, an upgrade of a transmission line and transmission stations in south-central Guelph; investments in ADS; requirements to enable DG; and up to four other transmission station upgrades, which when combined with the new Hearn Switching Station, will collectively enable up to 600 MW of new generation capacity in the Niagara, Toronto and Ottawa areas.

In 2011, the OPA provided the scope and timing to increase short circuit and/or transformer capacity at ten of 15 transmission stations. Seven of these station upgrades have now been completed, and alternate solutions have been determined for the remaining three projects. The Lambton to Longwood Transmission Upgrade has a required in-service date of December 2014, and is included in our budgeted future capital investments. This project is needed to satisfy government policy relating to the incorporation of 10,700 MW of non-hydroelectric renewable generation resources by 2021. In August 2013, the OPA requested us to terminate work related to the Southwestern Ontario Reactive Compensation Priority Project, and an OPA recommendation regarding the third priority specified transmission project, which was not included in the most recent LTEP, is not expected in the foreseeable future. Therefore, these two projects are not included in our budgeted future capital investments.

Based on the OEB’s framework for competitive designation for the development of eligible transmission projects, we did not include in our budgeted future capital investments any projects that could meet the definition of expansions. We do not plan to undertake large capital investments without a reasonable expectation of recovering them through our rates.

The actual timing and investments of many development projects are uncertain as they are dependent upon various regulatory approvals, negotiations with customers, neighbouring utilities and other stakeholders, and consultations with First Nations and Métis communities. Projects are also dependent upon the timing and level of generator contributions for enabling facilities.

17

HYDRO ONE INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

For the years ended December 31, 2013 and 2012

Distribution

Distribution capital investments include the sustainment of our infrastructure. Our core work will continue to focus on maintaining the performance of our aging distribution asset base through renewal and refurbishment activities. Planned capital investments include the continued replacements of equipment and components that are beyond their expected service life, as well as increased wood pole replacements and distribution station refurbishments. Sustainment capital investments in the Smart Metering project will decrease through 2016.

Distribution development capital investments are expected to be relatively stable through 2016, with the exception of capital contributions for capacity improvements at the Orleans Transmission Station in 2015 and the Hanmer Transmission Station in 2016. We will continue to make investments required to connect new load and DG customers, as well as investments to ensure the system is capable of supplying customer needs. During 2014 to 2016, a number of our projects will address local load growth issues. Generation connections investments will decrease as the volume of connections is expected to decrease. The budgeted capital expenditures only reflect projects with FIT and Micro FIT Program contracts from the OPA that are expected to connect to our distribution system.

In 2014 and 2015, the ADS Project will continue to pilot various technologies and related capital investments will begin to decrease in 2016. Pilot technologies include improvements to outage response management through more effective resource dispatch, automation to isolate faults where needed, and the dynamic regulation of voltage to reduce losses.

Off-Balance Sheet Arrangements

There are no off-balance sheet arrangements that have, or are reasonably likely to have, a material current or future effect on our financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources.

Summary of Contractual Obligations and Other Commercial Commitments

The following table presents a summary of our debt and other major contractual obligations, as well as other major commercial commitments:

December 31, 2013(millions of Canadian dollars) | Total | 2014 | 2015/2016 | 2017/2018 | After 2018 | |||||||||||||||

Contractual obligations(due by year) | ||||||||||||||||||||

Long-term debt – principal repayments1 | 9,045 | 750 | 1,050 | 1,350 | 5,895 | |||||||||||||||

Long-term debt – interest payments1 | 7,634 | 422 | 770 | 691 | 5,751 | |||||||||||||||

Pension2 | 172 | 160 | 12 | — | — | |||||||||||||||

Environmental and asset retirement obligations3 | 329 | 32 | 63 | 46 | 188 | |||||||||||||||

Inergi LP (Inergi) outsourcing agreement4 | 152 | 130 | 22 | — | — | |||||||||||||||

Operating lease commitments | 48 | 11 | 14 | 14 | 9 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total contractual obligations | 17,380 | 1,505 | 1,931 | 2,101 | 11,843 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Other commercial commitments(by year of expiry) | ||||||||||||||||||||

Bank line5 | 1,500 | — | — | 1,500 | — | |||||||||||||||

Letters of credit6 | 149 | 149 | — | — | — | |||||||||||||||

Guarantees6 | 326 | 326 | — | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total other commercial commitments | 1,975 | 475 | — | 1,500 | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||