SECURITIES AND EXCHANGE COMMISSION

FORM 6-K

REPORT OF FOREIGN ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16 OF

THE SECURITIES EXCHANGE ACT OF 1934

Date: May 14, 2003

Commission file number:

1-15060

UBS AG

Bahnhofstrasse 45, Zurich, Switzerland, and

Aeschenvorstadt 1, Basel, Switzerland

(Registrant’s Address)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

| Form 20-F x | Form 40-F o |

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

| Yes o | No x |

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): 82-

This Form 6-K consists of the the First Quarter 2003 Report, which appears immediately following this page.

Financial Reporting

First Quarter 2003 Report

13 May 2003

UBS Group Financial Highlights

| Quarter ended | % change from | |||||||||||||||||||

| CHF million, except where indicated | 31.3.03 | 31.12.02 | 31.3.02 | 4Q02 | 1Q02 | |||||||||||||||

Income statement key figures | ||||||||||||||||||||

| Operating income | 7,773 | 7,524 | 9,589 | 3 | (19 | ) | ||||||||||||||

| Operating expenses | 6,177 | 7,776 | 7,750 | (21 | ) | (20 | ) | |||||||||||||

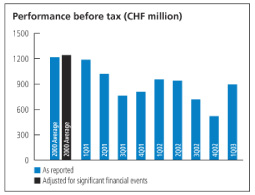

| Operating profit/(loss) before tax | 1,596 | (252 | ) | 1,839 | (13 | ) | ||||||||||||||

| Net profit/(loss) | 1,214 | (101 | ) | 1,363 | (11 | ) | ||||||||||||||

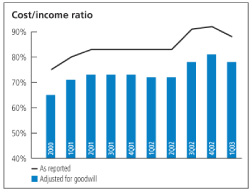

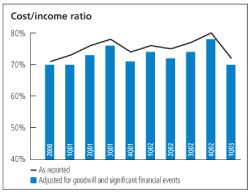

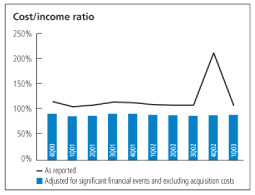

Cost/income ratio (%)1 | 78.4 | 103.5 | 80.1 | |||||||||||||||||

Per share data (CHF) | ||||||||||||||||||||

Basic earnings per share2 | 1.05 | (0.09 | ) | 1.10 | (5 | ) | ||||||||||||||

Diluted earnings per share2 | 1.02 | (0.09 | ) | 1.06 | (4 | ) | ||||||||||||||

Return on shareholders’ equity (%)3 | 13.2 | 8.9 | 12.3 | |||||||||||||||||

| % change from | ||||||||||||||||||||

| CHF million, except where indicated | ||||||||||||||||||||

| As at | 31.3.03 | 31.12.02 | 31.3.02 | 31.12.02 | 31.3.02 | |||||||||||||||

Balance sheet key figures | ||||||||||||||||||||

| Total assets | 1,232,318 | 1,181,118 | 1,229,625 | 4 | 0 | |||||||||||||||

| Shareholders’ equity | 39,764 | 38,991 | 44,769 | 2 | (11 | ) | ||||||||||||||

Market capitalization | 67,808 | 79,448 | 103,216 | (15 | ) | (34 | ) | |||||||||||||

BIS capital ratios | ||||||||||||||||||||

Tier 1 (%)4 | 11.5 | 11.3 | 11.8 | |||||||||||||||||

| Total BIS (%) | 13.6 | 13.8 | 14.7 | |||||||||||||||||

| Risk-weighted assets | 238,746 | 238,790 | 255,157 | 0 | (6 | ) | ||||||||||||||

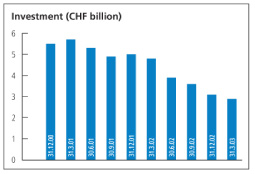

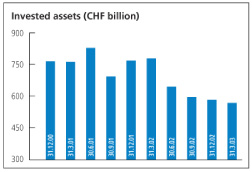

Invested assets (CHF billion) | 1,994 | 2,037 | 2,468 | (2 | ) | (19 | ) | |||||||||||||

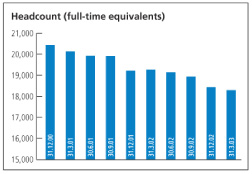

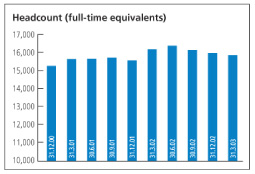

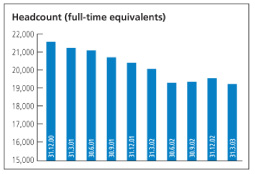

Headcount (full-time equivalents) | 68,395 | 69,061 | 70,221 | 5 | (1 | ) | (3 | ) | ||||||||||||

Long-term ratings | ||||||||||||||||||||

| Fitch, London | AAA | AAA | AAA | |||||||||||||||||

| Moody’s, New York | Aa2 | Aa2 | Aa2 | |||||||||||||||||

| Standard & Poor’s, New York | AA+ | AA+ | AA+ | |||||||||||||||||

Earnings adjusted for significant financial events and pre-goodwill6, 7

| Quarter ended | % change from | |||||||||||||||||||

CHF million, except where indicated | 31.3.03 | 31.12.02 | 31.3.02 | 4Q02 | 1Q02 | |||||||||||||||

| Operating income | 7,773 | 7,452 | 9,434 | 4 | (18 | ) | ||||||||||||||

| Operating expenses | 5,935 | 6,259 | 7,414 | (5 | ) | (20 | ) | |||||||||||||

| Operating profit before tax | 1,838 | 1,193 | 2,020 | 54 | (9 | ) | ||||||||||||||

| Net profit | 1,456 | 1,075 | 1,574 | 35 | (7 | ) | ||||||||||||||

Cost/income ratio (%)8 | 75.3 | 84.1 | 77.9 | |||||||||||||||||

Basic earnings per share (CHF)9 | 1.26 | 0.92 | 1.27 | 37 | (1 | ) | ||||||||||||||

Diluted earnings per share (CHF)10 | 1.23 | 0.92 | 1.23 | 34 | 0 | |||||||||||||||

Return on shareholders’ equity (%)11 | 15.8 | 13.9 | 15.2 | |||||||||||||||||

| 1 | Operating expenses/operating income less credit loss expense. | |

| 2 | For the EPS calculation, see Note 8 to the Financial Statements. | |

| 3 | Year to date annualized net profit/average shareholders’ equity less dividends. | |

| 4 | Includes hybrid Tier 1 capital, please refer to the BIS capital and ratios table in the Group Review. | |

| 5 | Klinik Hirslanden was sold on 5 December 2002. The Group headcount does not include the Klinik Hirslanden headcount of 2,687 at 31 March 2002. | |

| 6 | Excludes the amortization of goodwill and other intangible assets. | |

| 7 | Details of significant financial events can be found in the Group Review section on page 7. | |

| 8 | Operating expenses less the amortization of goodwill and other intangible assets and significant financial events/operating income less credit loss expense and significant financial events. | |

| 9 | Net profit less the amortization of goodwill and other intangible assets and significant financial events (after tax)/weighted average shares outstanding. | |

| 10 | Net profit for diluted EPS less the amortization of goodwill and other intangible assets and significant financial events (after tax) / weighted average shares outstanding for diluted EPS. | |

| 11 | Year to date annualized net profit less the amortization of goodwill and other intangible assets and significant financial events (after tax)/average shareholders’ equity less dividends. |

Throughout this report, 2002 segment results have been restated to reflect the transfer of the Private Banks & GAM to Corporate Center.

All financial information included in this report is unaudited, except for balance sheet information as at 31 December 2002, which is audited.

First Quarter 2003 Report

13 May 2003

Contents

Shareholders’ Letter | 2 | |||

Group Review | 4 | |||

UBS Wealth Management & Business Banking | 16 | |||

UBS Global Asset Management | 26 | |||

UBS Warburg | 30 | |||

UBS PaineWebber | 39 | |||

Corporate Center | 44 | |||

Financial Statements | ||||

| UBS Group Income Statement | 46 | |||

| UBS Group Balance Sheet | 47 | |||

| UBS Group Statement of Changes in Equity | 48 | |||

| UBS Group Statement of Cash Flows | 49 | |||

| Notes to the Financial Statements | 50 | |||

UBS Registered Shares | 56 |

| Financial Calendar | ||

| Publication of Second Quarter 2003 results | Wednesday, 13 August 2003 | |

| Publication of Third Quarter 2003 results | Tuesday, 11 November 2003 |

| UBS Investor Relations | ||||

| Hotline: +41 1 234 4100 | E-mail: sh-investorrelations@ubs.com | Web: www.ubs.com/investors |

| Zurich | New York | |||||

| Christian Gruetter | +41 1 234 4360 | Richard Feder | +1 212 713 6142 | |||

| Mark Hengel | +41 1 234 8439 | Christopher McNamee | +1 212 713 3091 | |||

| Oliver Lee | +41 1 234 2733 | |||||

| Catherine Lybrook | +41 1 234 2281 | |||||

| Fax | +41 1 234 3415 | Fax | +1 212 713 1381 |

| UBS AG | UBS Americas Inc. | |||

| Investor Relations G41B | Investor Relations | |||

| P.O. Box | 135 West 50th Street, 9th Floor | |||

| CH-8098 Zurich | New York, NY 10020 | |||

| Switzerland | United States of America | |||

| UBS Shareholder Services | US Transfer Agent | |||

| UBS AG | Mellon Investor Services. | |||

| Shareholder Services GUMV | Overpeck Centre | |||

| P.O. Box | 85 Challenger Road | |||

| CH-8098 Zurich | Ridgefield Park, NJ 07660 | |||

| Switzerland | United States of America | |||

| Phone: +41 1 235 62 02 | ||||

| Fax: +41 1 235 31 54 | calls from the US | +1 866 541 9689 | ||

| E-Mail: sh-shareholder-services@ubs.com | calls outside the US | +1 201 329 8451 |

Interactive First Quarter 2003 Report

An interactive version of this report can be viewed online in the First Quarter 2003 Results section of the UBS Investors & Analysts website: www.ubs.com/investors.

Other reports

All UBS’s published financial reports (including SEC filings) are available on the internet at: www.ubs.com/investors. Alternatively, printed copies of our reports can be obtained from: UBS AG, Economic Information Center, GHDE CA50-AUL, P.O. Box, CH-8098 Zurich, Switzerland. E-mail: sh-iz-ubs-publikationen@ubs.com.

1

Shareholders’ Letter

13 May 2003

Shareholders’ Letter

Dear Shareholders,

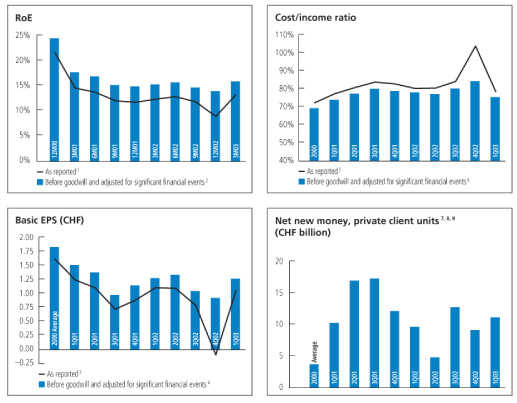

We started 2003 with a cautious outlook, and the events of this past quarter have again made revenue growth hard to find. However, UBS has once more delivered robust results in turbulent times. Indeed, through the past three years, a period of uncommon difficulty for our industry, we have never been disappointed with our overall performance. We have had no need for restructuring, for deep cuts, for changes of course — all things that can sap the confidence of clients and employees alike. Again this quarter, we have proved that we can protect and even enhance shareholder returns, despite tough markets. We kept a strong grip on costs, pushing our cost/income ratio to its lowest since mid-2001. And by managing our capital resources tightly, we have again improved the return on shareholders’ equity.

Taking a look at some business highlights for this quarter, Private Banking reported very strong net new money inflows with flows into its European wealth management initiative at record levels. UBS PaineWebber again attracted strong, positive inflows of net new money. In total, private clients placed CHF 11.1 billion in new assets with us, showing the value they place on our financial strength and individualized advisory services. Business Banking Switzerland generated higher volumes in its Swiss mortgage business, reinforcing its market leadership. UBS Global Asset Management funds continued to report strong relative investment performance while its institutional business experienced strong inflows into equity mandates. And UBS Warburg’s Fixed Income, Rates and Currencies business reported its best quarterly performance since 1999.

The new holding company comprising our five fully owned private banks and GAM, our specialist asset manager, is now set up and has begun to make changes. The three Swiss-German private banks — Armand von Ernst, Bank Ehinger and Cantrade — are now merging under the name Ehinger & Armand von Ernst.

Turning to our financial performance, net profit in first quarter 2003 was CHF 1,214 million, down 11% from the same quarter a year earlier. Before goodwill and adjusted for the gain from the sale of Hyposwiss in first quarter 2002, net profit fell just 7%.

Compared to the same period a year earlier, income and expenses in first quarter 2003 were both significantly impacted by the US dollar’s 20% weakening against the Swiss franc, with about half of the overall change in both measures driven by currency moves. In fact, this effect accounts for almost the entire 7% year-on-year drop in adjusted profit.

Operating income was down 19% from a year earlier, and, adjusted for the sale of Hyposwiss, it was 18% lower. Apart from the currency effects, the decrease was mainly due to poor equities trading conditions and low equity

2

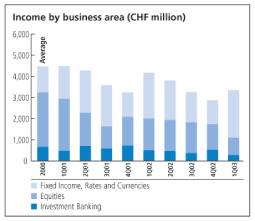

market levels, which affected asset-based revenues. Encouragingly, private equity writedowns at UBS Capital returned to more moderate levels, decreasing to CHF 123 million in first quarter 2003 from CHF 383 million in the same quarter a year earlier. Our fixed income business contributed significantly in near-perfect trading conditions. Revenues in the Fixed Income, Rates and Currencies business rose 4% from a year earlier and doubled compared to fourth quarter 2002, despite the negative currency effect.

Our credit businesses, despite another quarter of generally weak economic conditions, have again proved resilient. Aggregate net credit loss expense during the quarter amounted to CHF 104 million, compared to CHF 85 million in the same quarter in 2002 and the net recovery of CHF 11 million we recorded in fourth quarter 2002.

Costs remained under tight control. Operating expenses fell 20% when compared to first quarter 2002, reaching their lowest level since the merger with PaineWebber. General and administrative expenses were cut in practically all business areas and sectors. Performance-related compensation also fell.

9 June 2003 — one firm, one brand

All our businesses will operate under the single brand UBS from 9 June. Preparations are well on track and at UBS we are proud of this significant milestone in our corporate history. A single brand mirrors our integrated business model, the way we deliver ‘one firm’ to our clients, allowing them to access all of our services wherever and whenever they are required.

Our new brand strategy is also an important cornerstone in our organic growth drive. In the financial services industry, a strong brand is one of the major factors influencing new client acquisition and retention. It can be the deciding factor behind clients’ choice of financial provider. For any company, however, a brand is not only a name or a logo. It should represent how a company defines itself. For our clients, UBS stands for the relentless pursuit of their success, giving them access to proactive advice and all the resources of a global powerhouse. With UBS they should always feel confident they have made the right financial decision.

Outlook

Markets and trading conditions are tough and will likely remain so. But while some further degree of volatility cannot be excluded, we do feel that the downward pressure on our industry from the business and market environment could be beginning to ease and that the worst earnings declines may be behind us.

Our businesses are proving highly competitive and we remain convinced that our strategy is the right one. Although the timing of a return to sustained revenue growth is hard to predict, we are still in a position to protect and enhance shareholder returns by flexing costs and tightly managing capital. At the same time, because of our successful strategic initiatives, we continue to be well placed to profit from growth opportunities as they arise.

13 May 2003

UBS AG

|  | |

| Marcel Ospel Chairman | Peter Wuffli President |

3

Group Review

13 May 2003

Group Review

Cantrade, Bank Ehinger and Armand von Ernst merge

On 18 February 2003, UBS announced the creation of a holding company for its five fully owned independent private banking subsidiaries (Armand von Ernst, Banco di Lugano, Bank Ehinger, Cantrade and Ferrier Lullin) and GAM, its specialist asset manager.

Three of the five subsidiaries (Armand von Ernst, Bank Ehinger and Cantrade) will now merge to form Ehinger & Armand von Ernst with the new legal structure retroactively effective to 1 January 2003. Full operational integration of the three banks is expected to be complete by 1 January 2004. The new bank, headquartered in Zurich, with branches in Basel and Berne, will be one of the most important providers of private banking services located in the Swiss-German part of Switzerland. The merger is designed to capture the potential for cost synergies among the three banks.

GAM, Ferrier Lullin and Banco di Lugano are not affected by the merger and will continue to service their clients under their present brands.

Transfer of the Private Banks & GAM to the Corporate Center

On 25 April 2003 we published results for 2002, 2001 and 2000 that reflect the revised structure for GAM and the private banks. Moving these businesses affects the income statement and key performance indicators (KPIs) of Private Banking, UBS Global Asset Management and the Corporate Center. From now on, separate information will be provided on the holding company’s performance before tax, net new money, invested assets, and headcount.

None of the above-mentioned changes have an impact on the UBS Group Financial Statements.

4

UBS Group Performance Against Targets

| Year to date, annualized | 31.3.03 | 31.12.02 | 31.3.02 | |||||||||

RoE (%) | ||||||||||||

as reported1 | 13.2 | 8.9 | 12.3 | |||||||||

before goodwill and adjusted for significant financial events2 | 15.8 | 13.9 | 15.2 | |||||||||

For the quarter ended | 31.3.03 | 31.12.02 | 31.3.02 | |||||||||

Basic EPS (CHF) | ||||||||||||

as reported3 | 1.05 | (0.09 | ) | 1.10 | ||||||||

before goodwill and adjusted for significant financial events4 | 1.26 | 0.92 | 1.27 | |||||||||

| Cost/income ratio (%) | ||||||||||||

as reported5 | 78.4 | 103.5 | 80.1 | |||||||||

before goodwill and adjusted for significant financial events6 | 75.3 | 84.1 | 77.9 | |||||||||

Net new money, private client units (CHF billion)7, 8 | ||||||||||||

| Private Banking | 7.4 | 2.8 | 2.2 | |||||||||

| UBS PaineWebber | 3.7 | 6.3 | 7.4 | |||||||||

Total | 11.1 | 9.1 | 9.6 | |||||||||

| 1 | Year to date annualized net profit/average shareholders’ equity less dividends. | |

| 2 | Year to date annualized net profit less the amortization of goodwill and other intangible assets and significant financial events (after tax)/average shareholders’ equity less dividends. | |

| 3 | For the EPS calculation, see Note 8 to the Financial Statements. | |

| 4 | Net profit less the amortization of goodwill and other intangible assets and significant financial events (after tax)/ weighted average shares outstanding. | |

| 5 | Operating expenses/operating income less credit loss expense. | |

| 6 | Operating expenses less the amortization of goodwill and other intangible assets and significant financial events/operating income less credit loss expense and significant financial events. | |

| 7 | Excludes interest and dividend income. | |

| 8 | Restated to reflect the transfer of Private Banks & GAM to Corporate Center. | |

| 9 | Private Banking and UBS PaineWebber. |

5

Group Review

13 May 2003

Results

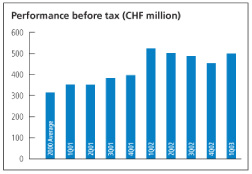

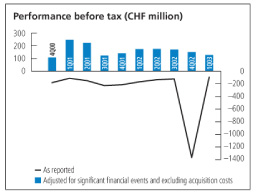

In first quarter 2003, UBS reported a net profit of CHF 1,214 million, compared to a net profit of CHF 1,363 million in first quarter 2002. Before goodwill and adjusted for the first quarter 2002 after-tax gain of CHF 125 million due to the sale of Hyposwiss, net profit declined 7% from first quarter 2002. Our continued success at cutting costs across our businesses offset much of the negative impact of falling markets on asset-based fees, and falling equities-related income.

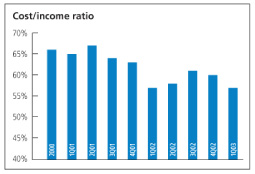

Annualized return on equity for first quarter 2003 was 13.2%, compared to 12.3% a year earlier. Basic earnings per share were CHF 1.05 in first quarter, against CHF 1.10 in the same quarter a year earlier. The cost/income ratio was 78.4% in first quarter 2003, down from 80.1% a year earlier.

Group targets

UBS’s performance is reported in accordance with International Financial Reporting Standards (IFRS — formerly known as International Accounting Standards (IAS)). Additionally, we provide comments and analysis on an adjusted basis which excludes from the reported amounts certain items we term significant financial events (SFEs). An additional adjustment we use in our results discussion is the exclusion of the amortization of goodwill and other acquired intangible assets.

These adjustments reflect our internal analysis approach where SFE-adjusted figures before the amortization of goodwill and intangibles are used to assess past performance against peers and to estimate future growth potential. In particular, our financial targets have been set in terms of adjusted results, excluding SFEs and the amortization of goodwill and intangibles. All the analysis provided in our internal management accounting is based on operational SFE-adjusted performance. This helps us to illustrate the underlying operational performance of our business, insulated from the impact of individual gain or loss items that are not relevant to our management’s business planning decisions. A policy approved by the Group Executive Board defines which items may be classified as SFEs.

We focus on four key performance targets, designed to deliver continually improving returns to our shareholders. These targets are evaluated on this adjusted basis.

Accordingly, before goodwill and adjusted for the sale of Hyposwiss in first quarter 2002:

| • | Our annualized return on equity for first quarter 2003 was 15.8%, up from 15.2% in the same quarter a year ago and back within our target range of 15-20%. Our ongoing commitment to reducing equity through share buyback programs more than offset the market-related decline in earnings. | |

| • | Basic earnings per share in first quarter 2003 were CHF 1.26, just below CHF 1.27 in the same quarter last year. The 7% decline in profit was again offset by the reduced average number of shares outstanding, driven by our ongoing share buyback programs. |

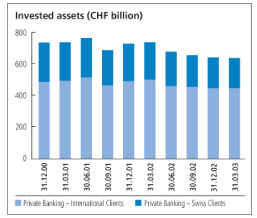

Invested Assets

| Quarter ended | % change | |||||||||||||||||||

| CHF billion | 31.3.03 | 31.12.02 | 31.3.02 | 31.12.02 | 31.3.02 | |||||||||||||||

UBS Group | 1,994 | 2,037 | 2,468 | (2 | ) | (19 | ) | |||||||||||||

UBS Wealth Management & Business Banking | ||||||||||||||||||||

| Private Banking | 638 | 642 | 737 | (1 | ) | (13 | ) | |||||||||||||

| Business Banking Switzerland | 197 | 205 | 219 | (4 | ) | (10 | ) | |||||||||||||

UBS Global Asset Management | ||||||||||||||||||||

| Institutional | 264 | 274 | 324 | (4 | ) | (19 | ) | |||||||||||||

| Wholesale Intermediary | 255 | 259 | 327 | (2 | ) | (22 | ) | |||||||||||||

UBS Warburg | 3 | 3 | 1 | 0 | 200 | |||||||||||||||

UBS PaineWebber | 569 | 584 | 779 | (3 | ) | (27 | ) | |||||||||||||

Corporate Center | ||||||||||||||||||||

| Private Banks & GAM | 68 | 70 | 81 | (3 | ) | (16 | ) | |||||||||||||

6

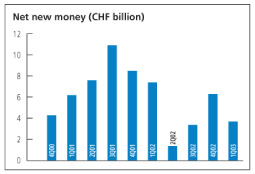

Net New Money1

| Quarter ended | ||||||||||||

| CHF billion | 31.3.03 | 31.12.02 | 31.3.02 | |||||||||

UBS Group | 17.1 | 9.0 | 11.8 | |||||||||

UBS Wealth Management & Business Banking | ||||||||||||

| Private Banking | 7.4 | 2.8 | 2.2 | |||||||||

| Business Banking Switzerland | (1.9 | ) | (2.7 | ) | 2.3 | |||||||

UBS Global Asset Management | ||||||||||||

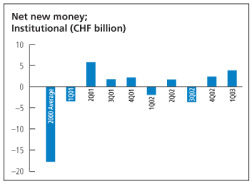

| Institutional | 3.9 | 2.4 | (1.9 | ) | ||||||||

| Wholesale Intermediary | 3.4 | (0.8 | ) | 0.5 | ||||||||

UBS Warburg | 0.0 | 0.1 | 0.1 | |||||||||

UBS PaineWebber | 3.7 | 6.3 | 7.4 | |||||||||

Corporate Center | ||||||||||||

| Private Banks & GAM | 0.6 | 0.9 | 1.2 | |||||||||

1 Excludes interest and dividend income.

| • | The cost/income ratio this quarter was 75.3%, a decrease from 77.9% in first quarter last year and at the lowest since second quarter 2001. Our ongoing cost initiatives, particularly in UBS PaineWebber, UBS Warburg’s Corporate and Institutional Clients unit as well as in the Business Banking Switzerland unit, as well as the return of private equity writedowns to more moderate levels, more than offset the effects on revenues of declining market valuations and poor equity trading conditions. |

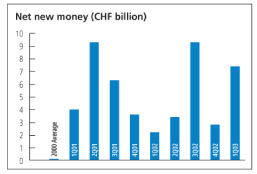

Net new money in the private client units (Private Banking and UBS PaineWebber) was again strong, with inflows of CHF 11.1 billion this quarter, up CHF 2.0 billion from the strong fourth quarter result. In particular, our European wealth management initiative continues to report strong inflows with a record result of CHF 3.0 billion in first quarter 2003. In the US, UBS PaineWebber’s net new money inflow was CHF 3.7 billion, down from CHF 6.3 billion in fourth quarter 2002, but still highly satisfactory given the market environment, and the difficulty competitors are experiencing in attracting new funds.

Significant financial events

There were no significant financial events in first quarter 2003, but there were two significant financial events in fourth quarter 2002 and one in first quarter 2002.

| • | In fourth quarter 2002, UBS recorded a non-cash net writedown of CHF 953 million (pre-tax CHF 1,234 million) for the PaineWebber brand that was held as an intangible asset on our balance sheet. The writedown was due to our decision, announced in November 2002, to move to the single UBS brand. The new brand structure will be implemented in June 2003. | |

| • | We realized a net gain of CHF 60 million (pre-tax CHF 72 million) in fourth quarter 2002 from the sale of Klinik Hirslanden, a private hospital group. | |

| • | In first quarter 2002, we realized a net gain of CHF 125 million (pre-tax CHF 155 million) from the sale of Hyposwiss. |

Details of significant financial events and a reconciliation between the IFRS numbers and the adjusted IFRS numbers for these quarters are shown in the table on page 8.

Group results

Operating income

Total operating income was CHF 7,773 million in first quarter 2003, a decrease of 19% compared to a year earlier. Adjusted for the gain from the sale of Hyposwiss, operating income dropped by 18% compared to the same quarter a year earlier. The remaining drop was mainly due to low equity market levels, which continue to affect asset-based revenues. Revenues were influenced by the significant drop of major currencies against the Swiss franc, accounting for half of the decline. Income was also negatively influenced

7

Group Review

13 May 2003

Significant Financial Events (SFE)

| UBS | ||||||||||||||||||||||||||||

| UBS Group | PaineWebber | Corporate Center | ||||||||||||||||||||||||||

| CHF million | ||||||||||||||||||||||||||||

| For the quarter ended | Line affected in Income Statement | 31.3.03 | 31.12.02 | 31.3.02 | 31.12.02 | 31.12.02 | 31.3.02 | |||||||||||||||||||||

Operating income | ||||||||||||||||||||||||||||

As reported | 7,773 | 7,524 | 9,589 | 1,213 | 591 | 721 | ||||||||||||||||||||||

| Less: Gain on disposal of Hyposwiss | Other income | 155 | 155 | |||||||||||||||||||||||||

| Less: Gain on disposal of Klinik Hirslanden | Other income | 72 | 72 | |||||||||||||||||||||||||

Adjusted operating income | 7,773 | 7,452 | 9,434 | 1,213 | 519 | 566 | ||||||||||||||||||||||

Operating expenses | ||||||||||||||||||||||||||||

As reported | 6,177 | 7,776 | 7,750 | 2,581 | 621 | 528 | ||||||||||||||||||||||

| Less: Writedown of PaineWebber brand name | Amortization of goodwill | |||||||||||||||||||||||||||

| and other intangible assets | 1,234 | 1,234 | ||||||||||||||||||||||||||

Adjusted operating expenses | 6,177 | 6,542 | 7,750 | 1,347 | 621 | �� | 528 | |||||||||||||||||||||

Operating profit/(loss) | ||||||||||||||||||||||||||||

Operating profit/(loss) before tax and minority interests | 1,596 | (252 | ) | 1,839 | (1,368 | ) | (30 | ) | 193 | |||||||||||||||||||

| SFE adjustments, net | 1,162 | (155 | ) | 1,234 | (72 | ) | (155 | ) | ||||||||||||||||||||

Adjusted operating profit before tax and minority interests | 1,596 | 910 | 1,684 | (134 | ) | (102 | ) | 38 | ||||||||||||||||||||

Net profit/(loss) | ||||||||||||||||||||||||||||

As reported | 1,214 | (101 | ) | 1,363 | ||||||||||||||||||||||||

| SFE adjustments, net | 1,162 | (155 | ) | |||||||||||||||||||||||||

| Tax effect of significant financial events, net | Tax expense/(benefit) | (269 | ) | 30 | ||||||||||||||||||||||||

Adjusted net profit | 1,214 | 792 | 1,238 | |||||||||||||||||||||||||

| Amortization of goodwill and other intangible assets | 242 | 283 | 1 | 336 | ||||||||||||||||||||||||

Adjusted net profit before goodwill | 1,456 | 1,075 | 1,574 | |||||||||||||||||||||||||

1 Excludes significant financial event: Writedown of PaineWebber brand name of CHF 1,234 million (net of taxes: CHF 953 million).

by continued poor trading conditions in equity markets, as well as weak investor sentiment, particularly in the US. Private equity writedowns, however, returned to more moderate levels.

Net interest income and net trading income. Net interest income of CHF 2,909 million in first quarter 2003 was 5% higher than the same quarter a year ago. Net trading income declined 36% from CHF 1,983 million in first quarter 2002 to CHF 1,261 million in first quarter 2003.

As well as income from interest margin based activities (loans and deposits), net interest income includes income earned as a result of trading activities (for example, coupon and dividend income). This component is volatile from period to period, depending on the composition of the trading portfolio. In order to provide a better explanation of the movements in net interest income and net trading income, we analyze the total according to the business activities that give rise to the income, rather than by the type of income generated.

Net income from interest margin products dropped by 10% to CHF 1,285 million in first quarter 2003 from CHF 1,423 million in the same quarter a year earlier, mainly reflecting lower interest margins on cash accounts due to the particularly low interest rate environment as well as a decline in the Swiss franc equivalent of US dollar interest rate revenues. This was partially offset by increased volumes of mortgages and savings accounts.

Net income from trading activities was CHF 2,761 million in first quarter 2003, a drop of 16% compared to the same quarter a year ago. Equity trading revenues, at CHF 315 million, dropped by 57% compared to the same quarter a year earlier. Conditions were dictated by low market volumes and a lack of corporate

8

Net Interest and Trading Income

| Quarter ended | % change from | ||||||||||||||||||||

| CHF million | 31.3.03 | 31.12.02 | 31.3.02 | 4Q02 | 1Q02 | ||||||||||||||||

| Net interest income | 2,909 | 2,697 | 2,763 | 8 | 5 | ||||||||||||||||

| Net trading income | 1,261 | 666 | 1,983 | 89 | (36 | ) | |||||||||||||||

Total net interest and trading income | 4,170 | 3,363 | 4,746 | 24 | (12 | ) | |||||||||||||||

| Breakdown by business activity: | |||||||||||||||||||||

| Net income from interest margin products | 1,285 | 1,296 | 1,423 | (1 | ) | (10 | ) | ||||||||||||||

| Equities | 315 | 522 | 731 | (40 | ) | (57 | ) | ||||||||||||||

| Fixed income | 2,000 | 1,050 | 2,155 | 90 | (7 | ) | |||||||||||||||

| Foreign exchange | 370 | 328 | 342 | 13 | 8 | ||||||||||||||||

| Other | 76 | 71 | 54 | 7 | 41 | ||||||||||||||||

| Net income from trading activities | 2,761 | 1,971 | 3,282 | 40 | (16 | ) | |||||||||||||||

| Net income from treasury activities | 384 | 435 | 419 | (12 | ) | (8 | ) | ||||||||||||||

Other1 | (260 | ) | (339 | ) | (378 | ) | 23 | 31 | |||||||||||||

Total net interest and trading income | 4,170 | 3,363 | 4,746 | 24 | (12 | ) | |||||||||||||||

1 Principally external funding costs of the Paine Webber Group, Inc. acquisition.

activity, and revenues from proprietary trading dropped significantly. Fixed income trading revenues dropped from CHF 2,155 million in first quarter 2002 to CHF 2,000 million in this quarter. The drop was due to the US dollar’s decline against the Swiss franc. Excluding the effect of the weakening US dollar, fixed income had a much stronger quarter than a year ago, reflecting a buoyant trading environment benefiting from low rates and a steep yield curve. Particularly strong results were posted in Principal Finance, Cash and Collateral Trading, and Mortgage Trading. Negative revenues of CHF 38 million relating to Credit Default Swaps (CDS) hedging existing credit exposures in the loan book reflected the general narrowing of credit spreads. Foreign exchange trading revenues showed another strong quarter, with revenues increasing from CHF 342 million in first quarter 2002 to CHF 370 million in first quarter 2003, due to higher client volumes.

Net income from treasury activities dropped from CHF 419 million in first quarter 2002 to CHF 384 million this quarter. The decline was driven by a drop in unrealized gains from derivatives used to economically hedge interest rate risk related to structured notes issued.

Other net trading and interest income showed negative revenue of CHF 260 million in first quarter 2003 compared to negative CHF 378 million in the same quarter last year. Lower goodwill funding costs, reflecting the weakening of the US dollar against the Swiss franc, were responsible for the decline.

Net fee and commission income was CHF 3,826 million in first quarter 2003, a decrease of 21% from first quarter 2002’s CHF 4,870 million, mainly due to market-driven declines in asset-based fees, as well as low levels of investor activity, pushing down brokerage income and investment fund sales fees. Underwriting fees, at CHF 437 million in first quarter 2003, were down 12% from the same period a year earlier, reflecting the dormant equity underwriting market, partially offset by strong fixed income underwriting revenues, which rose 68%. Corporate finance fees, at CHF 114 million, dropped by 36% from first quarter 2002, reflecting a global fee pool at its second lowest quarterly level in six years. Net brokerage fees fell 31% to CHF 895 million in first quarter 2003 due to very low individual and institutional client activity in common with global market experience. At CHF 882 million, investment fund fees dropped 20% compared to first quarter 2002. Both sales fees as well as asset-based commissions were lower. Portfolio and other management and advisory fees decreased 22% to CHF 901 million in first quarter 2003, resulting from both lower performance fees, and from management fees, pushed down by market levels.

9

Group Review

13 May 2003

Other income decreased by CHF 177 million from a gain of CHF 58 million in first quarter 2002 to a loss of CHF 119 million in first quarter 2003. This drop is mainly due to the fall-off of revenues from the Klinik Hirslanden business sold in fourth quarter 2002, a significant writedown of our stake in Swiss International Airlines Ltd, and the absence of divestment gains. Impairment charges in our private equity portfolio were, however, much reduced.

Operating expenses

We continue to cut into our cost base, with stringent cost control measures in place across the firm. Total operating expenses, at CHF 6,177 million in first quarter 2003, were 20% lower than the CHF 7,750 million in first quarter 2002. This very significant drop brought our total operating expenses to their lowest level since the merger with PaineWebber, and reflected a sharp decline in both personnel and general and administrative expenses, down 21% and 18% respectively from the same quarter a year earlier. The drop was accentuated by the fall of major currencies against the Swiss franc as well as the 2002 sale of Klinik Hirslanden.

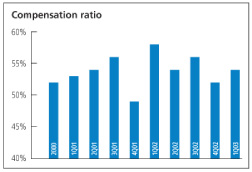

Personnel expenses dropped from CHF 5,317 million in first quarter 2002 to CHF 4,202 million this quarter, reflecting a drop in UBS Warburg’s compensation ratio and declining salaries due to headcount reductions, mainly in the Business Banking Switzerland and UBS PaineWebber units. Accruals for performance-related compensation fell in line with revenues. Personnel expenses are managed on a full year basis with final fixing of annual performance-related payments in the fourth quarter.

First quarter 2003 general and administrative expenses, at CHF 1,397 million, were the lowest since the merger with PaineWebber, and 18% less than in first quarter a year ago, with declines reported in almost all categories of costs. Professional fees, administration costs, travel and entertainment and IT expenses were at their lowest levels since 2000. Marketing and public relations expenses also showed significant drops. Both the Corporate and Institutional Clients and Business Banking Switzerland units posted record low general and administrative expenses.

Depreciation dropped 15% from CHF 397 million in first quarter 2002 to CHF 336 million in

Allowances and provisions for credit risk

| UBS Wealth Management & | ||||||||

| Business Banking | ||||||||

| CHF million | ||||||||

| As at | 31.3.03 | 31.12.02 | ||||||

| Loans to banks (gross) | 3,433 | 3,292 | ||||||

| Loans to customers (gross) | 168,550 | 165,814 | ||||||

| Gross loans | 171,983 | 169,106 | ||||||

| Non-performing loans | 4,952 | 5,032 | ||||||

| Other impaired loans | 3,146 | 3,332 | ||||||

Total impaired loans | 8,098 | 8,364 | ||||||

| Allowances for non-performing loans | 2,927 | 2,749 | ||||||

| Allowances for other impaired loans | 565 | 824 | ||||||

Total allowances for impaired loans | 3,492 | 3,573 | ||||||

Other allowances and provisions | 381 | 452 | ||||||

Total allowances and provisions | 3,873 | 4,025 | ||||||

of which country allowances and provisions | 527 | 515 | ||||||

Ratios | ||||||||

| Impaired loans as a % of gross loans | 4.7 | 4.9 | ||||||

| Non-performing loans as a % of gross loans | 2.9 | 3.0 | ||||||

| Allowances and provisions for credit loss as a % of gross loans | 2.3 | 2.4 | ||||||

| Allocated allowances as a % of impaired loans | 43.1 | 42.7 | ||||||

| Allocated allowances as a % of non-performing loans | 59.1 | 54.6 | ||||||

10

the same quarter this year, mainly reflecting lower IT and property-related charges.

Amortization of goodwill and other intangible assets decreased from CHF 336 million in first quarter 2002 to CHF 242 million this quarter, reflecting the writedown of the PaineWebber brand name in fourth quarter 2002, as well the drop of the US dollar against the Swiss franc.

Tax

The Group tax expense of CHF 310 million in first quarter 2003 reflects an effective tax rate of 19.4%, compared to last year’s rate of 16.5% (before significant financial events), which was driven by particularly low progressive tax rates in Switzerland, the ability to benefit from tax losses in the US and UK and a high proportion of earnings generated in lower tax jurisdictions. We believe that an underlying tax rate of around 20% (before significant financial events) is a reasonable indicator for the remainder of the year, driven by a change in regional profit mix resulting in higher progressive Swiss tax rates.

Credit risk

Our credit portfolios have again been very resilient despite continued economic weakness worldwide. Aggregate net credit loss expense during the quarter was CHF 104 million compared to CHF 85 million in first quarter 2002 and a net writeback of CHF 11 million in fourth quarter 2002.

This continued strong performance is the result of ongoing low requirements for new provisions. The small increase in net credit loss expenses was due to less releases of provisions compared to fourth quarter 2002 which was affected by significant recoveries of country provisions due to the successful exposure reductions in Indonesia and Brazil.

UBS Wealth Management & Business Banking reported a credit loss expense of CHF 64 million in first quarter, roughly on par with the CHF 60 million last quarter and CHF 61 million in first quarter a year earlier. The continued relatively low level of credit losses in Switzerland in face of a deteriorating economic climate reflects the result of our efforts to upgrade our domestic credit portfolio in recent years and to reduce our portfolio of impaired loans.

| UBS Global | ||||||||||||||||||||||||||||||||||||||||

| Asset Management | UBS Warburg | UBS PaineWebber | Corporate Center | UBS Group | ||||||||||||||||||||||||||||||||||||

| 31.3.03 | 31.12.02 | 31.3.03 | 31.12.02 | 31.3.03 | 31.12.02 | 31.3.03 | 31.12.02 | 31.3.03 | 31.12.02 | |||||||||||||||||||||||||||||||

| 147 | 285 | 25,259 | 24,495 | 1,301 | 1,327 | 3,948 | 3,512 | 34,088 | 32,911 | |||||||||||||||||||||||||||||||

| 41 | 28 | 33,857 | 37,223 | 11,409 | 11,530 | 1,967 | 1,864 | 215,824 | 216,459 | |||||||||||||||||||||||||||||||

| 188 | 313 | 59,116 | 61,718 | 12,710 | 12,857 | 5,915 | 5,376 | 249,912 | 249,370 | |||||||||||||||||||||||||||||||

| 0 | 0 | 1,008 | 967 | 29 | 29 | 1 | 1 | 5,990 | 6,029 | |||||||||||||||||||||||||||||||

| 0 | 0 | 927 | 996 | 0 | 0 | 4 | 8 | 4,077 | 4,336 | |||||||||||||||||||||||||||||||

| 0 | 0 | 1,935 | 1,963 | 29 | 29 | 5 | 9 | 10,067 | 10,365 | |||||||||||||||||||||||||||||||

| 0 | 0 | 785 | 706 | 29 | 29 | 1 | 1 | 3,742 | 3,485 | |||||||||||||||||||||||||||||||

| 0 | 0 | 513 | 575 | 0 | 0 | 8 | 8 | 1,086 | 1,407 | |||||||||||||||||||||||||||||||

| 0 | 0 | 1,298 | 1,281 | 29 | 29 | 9 | 9 | 4,828 | 4,892 | |||||||||||||||||||||||||||||||

| 0 | 0 | 249 | 264 | 12 | 13 | 0 | 0 | 642 | 729 | |||||||||||||||||||||||||||||||

| 0 | 0 | 1,547 | 1,545 | 41 | 42 | 9 | 9 | 5,470 | 5,621 | |||||||||||||||||||||||||||||||

| 0 | 0 | 212 | 221 | 0 | 0 | 0 | 0 | 739 | 736 | |||||||||||||||||||||||||||||||

| 3.3 | 3.2 | 0.2 | 0.2 | 0.1 | 0.2 | 4.0 | 4.2 | |||||||||||||||||||||||||||||||||

| 1.7 | 1.6 | 0.2 | 0.2 | 0.0 | 0.0 | 2.4 | 2.4 | |||||||||||||||||||||||||||||||||

| 2.6 | 2.5 | 0.3 | 0.3 | 0.2 | 0.2 | 2.2 | 2.3 | |||||||||||||||||||||||||||||||||

| 67.1 | 65.3 | 100.0 | 100.0 | 180.0 | 100.0 | 48.0 | 47.2 | |||||||||||||||||||||||||||||||||

| 77.9 | 73.0 | 100.0 | 100.0 | 100.0 | 100.0 | 62.5 | 57.8 | |||||||||||||||||||||||||||||||||

11

Group Review

13 May 2003

Actual credit loss expense/(recovery)

| Quarter ended | % change from | |||||||||||||||||||

| CHF million | 31.3.03 | 31.12.02 | 31.3.02 | 4Q02 | 1Q02 | |||||||||||||||

| UBS Wealth Management & Business Banking | 64 | 60 | 61 | 7 | 5 | |||||||||||||||

| UBS Warburg | 40 | (72 | ) | 31 | 29 | |||||||||||||||

| UBS PaineWebber | 0 | 1 | 3 | (100 | ) | (100 | ) | |||||||||||||

| Corporate Center | 0 | 0 | (10 | ) | 100 | |||||||||||||||

UBS Group | 104 | (11 | ) | 85 | 22 | |||||||||||||||

Credit loss expense at UBS Warburg was CHF 40 million, after a net recovery of CHF 72 million in fourth quarter and a credit loss expense of CHF 31 million in first quarter 2002. In light of the continued high level of corporate defaults being experienced on a global scale, the performance of UBS Warburg’s credit portfolio has been very strong, and there were very few new impairments in the quarter.

UBS’s loan portfolio amounted to CHF 249.9 billion on 31 March 2003, almost unchanged from CHF 249.4 billion on 31 December 2002. As announced previously and reported elsewhere, the five independent Swiss private banks and GAM have been moved to Corporate Center. Although of minor importance in the credit business, the corresponding effects have been factored into the comparative December 2002 loan and related figures shown in the table on page 10 and 11.

Helped by growth in our Swiss residential mortgage lending business, the loan book of UBS Wealth Management & Business Banking increased by CHF 2.9 billion or 1.7% in the three months between 31 December 2002 and 31 March 2003. On the other hand, the volume of UBS Warburg’s gross loans decreased by CHF 2.6 billion, while unutilized committed credit facilities increased by CHF 2.5 billion. UBS PaineWebber’s loan portfolio was CHF 12.7 billion on 31 March 2003, down 1.1% from CHF 12.9 billion on 31 December 2002, mainly a reflection of the weaker US dollar.

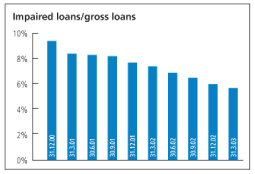

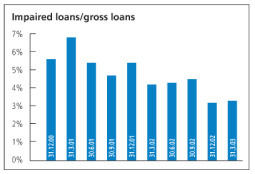

Total impaired loans decreased to CHF 10,067 million on 31 March 2003 from CHF 10,365 million on 31 December 2002 as the continued high level of workouts of recovery positions more than compensated for new impairments. As a result, the impaired loans to total loans ratio again improved, falling to 4.0% in first quarter from 4.2% in the previous quarter.

Market risk

Market risk is incurred primarily through UBS’s trading activities, which are centered in the UBS Warburg Business Group.

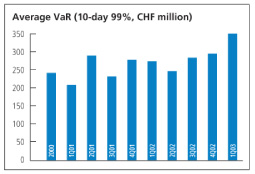

Market risk for UBS Warburg, as measured by average 10-day 99% confidence level Value at Risk (VaR) increased to CHF 350 million from CHF 295 million in fourth quarter 2002. The overall increase in average VaR came mainly from interest rate products which, together with equity products, remained the predominant risk drivers.

12

UBS Group: Value at Risk (10-day 99% confidence)

| Quarter ended 31.3.03 | Quarter ended 31.12.02 | |||||||||||||||||||||||||||||||||||

| CHF million | Limits | Min. | Max. | Average | 31.3.03 | Min. | Max. | Average | 31.12.02 | |||||||||||||||||||||||||||

Business Groups | ||||||||||||||||||||||||||||||||||||

| UBS Warburg | 450 | 290.4 | 447.0 | 350.0 | 300.0 | 243.7 | 389.6 | 295.0 | 310.0 | |||||||||||||||||||||||||||

| UBS PaineWebber | 50 | 11.4 | 18.4 | 15.3 | 11.7 | 12.2 | 22.9 | 16.9 | 14.2 | |||||||||||||||||||||||||||

| UBS Global Asset Management | 30 | 8.2 | 15.6 | 10.5 | 10.3 | 7.0 | 13.1 | 10.2 | 8.6 | |||||||||||||||||||||||||||

| UBS Wealth Management & Business Banking | 50 | 3.5 | 4.7 | 4.1 | 3.6 | 4.1 | 6.2 | 4.7 | 4.1 | |||||||||||||||||||||||||||

Corporate Center1, 2 | 150 | 59.6 | 82.7 | 70.5 | 65.1 | 37.5 | 63.7 | 44.7 | 62.1 | |||||||||||||||||||||||||||

| Reserve | 150 | |||||||||||||||||||||||||||||||||||

| Diversification effect | 3 | 3 | (89.2 | ) | (73.2 | ) | 3 | 3 | (75.0 | ) | (86.6 | ) | ||||||||||||||||||||||||

Total | 600 | 297.5 | 461.7 | 361.1 | 317.5 | 247.9 | 373.9 | 296.5 | 312.4 | |||||||||||||||||||||||||||

1 Includes interest rate exposures in the banking books of the Private Banks.2 Includes interest rate exposures in the banking book of Group Treasury.3 As the minimum and maximum occur on different days for different Business Groups, it is not meaningful to calculate a portfolio diversification effect.

UBS Warburg — Corporate and Institutional Clients: Value at Risk (10-day 99% confidence)

| Quarter ended 31.3.03 | Quarter ended 31.12.02 | |||||||||||||||||||||||||||||||

| CHF million | Min. | Max. | Average | 31.3.03 | Min. | Max. | Average | 31.12.02 | ||||||||||||||||||||||||

Risk type | ||||||||||||||||||||||||||||||||

| Equities | 160.6 | 186.3 | 172.5 | 160.8 | 165.2 | 293.0 | 195.4 | 178.3 | ||||||||||||||||||||||||

| Interest rates | 251.1 | 428.1 | 319.6 | 280.4 | 168.7 | 303.4 | 234.9 | 280.9 | ||||||||||||||||||||||||

| Foreign exchange | 6.6 | 28.8 | 14.3 | 21.8 | 6.2 | 62.2 | 25.3 | 9.6 | ||||||||||||||||||||||||

Other (incl. energy)1 | 10.5 | 51.3 | 17.4 | 16.8 | 10.3 | 31.5 | 15.9 | 12.6 | ||||||||||||||||||||||||

| Diversification effect | 2 | 2 | (173.9 | ) | (179.8 | ) | 2 | 2 | (176.5 | ) | (171.4 | ) | ||||||||||||||||||||

Total | 290.4 | 447.0 | 350.0 | 300.0 | 243.7 | 389.6 | 295.0 | 310.0 | ||||||||||||||||||||||||

1 Includes energy risk from UBS Warburg Energy and precious metals risk.2 As the minimum and maximum occur on different days for different risk types, it is not meaningful to calculate a portfolio diversification effect.

Equity markets have been particularly volatile and trading conditions unattractive, but we have taken advantage of excellent opportunities in the fixed income markets. We continue to avoid risk concentrations of any kind and to hedge tail risk. Overall, there was no change in strategy and risk appetite and we continue to operate within our VaR limits.

The quality of the VaR model is continuously monitored by backtesting - comparing actual revenues arising from closing positions (i. e. excluding intraday revenues, fees and commissions) with the 1-day VaR calculated on these positions. The graph on page 12 shows these daily revenues and the corresponding 1-day VaR over the last 12 months. The 10-day VaR, which is the basis of the limits and exposures in the tables above, is also shown in this graph for information. Revenues over this period were within the range predicted by the VaR model.

UBS also routinely assesses potential stress loss against a standard set of forward-looking scenarios. Stress events modeled in our standard scenarios include crises in equity, corporate bond and emerging markets, and severe currency and interest rate movements. These scenarios are kept under constant review and fine-tuned as necessary. We also monitor our positions against more specific scenarios that target individual sectors or are based on current concerns. Stress loss utilization development broadly followed VaR during the quarter, with the average utilization marginally higher than fourth quarter 2002. Utilization remained well within limits.

Capital management

We remain committed to being one of the best-capitalized financial services firms in the world and will therefore continue to manage our balance sheet prudently. This clear focus and our ongoing strong cash flow generation mean that we have been able to keep our BIS Tier 1 ratio high while continuing our share buyback programs.

13

Group Review

13 May 2003

BIS Capital and Ratios

| % change from | ||||||||||||||||||||

| CHF million, except where indicated | ||||||||||||||||||||

| As at | 31.3.03 | 31.12.02 | 31.3.02 | 31.12.02 | 31.3.02 | |||||||||||||||

| Risk-weighted assets | 238,746 | 238,790 | 255,157 | 0 | (6 | ) | ||||||||||||||

| BIS Tier 1 capital | 27,562 | 27,047 | 30,221 | 2 | (9 | ) | ||||||||||||||

of which hybrid Tier 1 capital1 | 3,113 | 3,182 | 3,859 | (2 | ) | (19 | ) | |||||||||||||

| BIS total capital | 32,490 | 33,009 | 37,567 | (2 | ) | (14 | ) | |||||||||||||

| BIS Tier 1 capital ratio (%) | 11.5 | 11.3 | 11.8 | |||||||||||||||||

of which hybrid Tier 1 capital (%)1 | 1.3 | 1.3 | 1.5 | |||||||||||||||||

| BIS total capital ratio (%) | 13.6 | 13.8 | 14.7 | |||||||||||||||||

1 Trust preferred securities.

Risk-weighted assets remained virtually unchanged at CHF 239 billion on 31 March 2003. Slightly higher VaR capital requirements were offset by slightly lower capital requirements from our loan and derivative businesses. However, our BIS Tier 1 capital increased from CHF 27.0 billion to CHF 27.6 billion in the period despite our ongoing share buyback program. The increase, reflecting higher retained earnings, pushed our Tier 1 capital ratio up to 11.5% on 31 March 2003 from 11.3% on 31 December 2002.

Buyback program

We terminated our second 2002 share buyback program on 5 March 2003 after repurchasing a total of 8,270,080 shares for an average price of CHF 64.07. Following the approval at the Annual General Meeting on 16 April 2003, these shares, along with the shares bought back under the first 2002 buyback program (67,700,000 shares), will be canceled in July 2003.

In light of our continued strong capitalization, we started a new program on 6 March 2003, which will again lead to a cancelation of the repurchased shares. The program will allow the repurchase of shares for a maximum value of CHF 5 billion, corresponding to about 6.8% of total share capital and will run for one year. The cancelation of shares bought back under this program will have to be approved at the Annual General Meeting in April 2004.

At 31 March 2003, a total of 1,470,000 shares had been repurchased under the new program at an average price of CHF 53.68.

Treasury shares

IFRS requires a company that holds its own shares for trading or non-trading purposes to record those shares as treasury shares and deduct them from shareholders’ equity.

UBS Shares and Market Capitalization

| % change from | |||||||||||||||||||||

| Number of shares, except where indicated | |||||||||||||||||||||

| As at | 31.3.03 | 31.12.02 | 31.3.02 | 31.12.02 | 31.3.02 | ||||||||||||||||

Total ordinary shares issued | 1,256,702,037 | 1,256,297,678 | 1,282,251,732 | 0 | (2 | ) | |||||||||||||||

| Second trading line treasury shares | |||||||||||||||||||||

| 2001 program | (28,818,690 | ) | |||||||||||||||||||

| 2002 first program | (67,700,000 | ) | (67,700,000 | ) | (6,860,123 | ) | |||||||||||||||

| 2002 second program | (8,270,080 | ) | (6,335,080 | ) | |||||||||||||||||

| 2003 program | (1,470,000 | ) | |||||||||||||||||||

Shares outstanding for market capitalization | 1,179,261,957 | 1,182,262,598 | 1,246,572,919 | 0 | (5 | ) | |||||||||||||||

Share price (CHF) | 57.50 | 67.20 | 82.80 | (14 | ) | (31 | ) | ||||||||||||||

Market capitalization (CHF million) | 67,808 | 79,448 | 103,216 | (15 | ) | (34 | ) | ||||||||||||||

Total treasury shares | 106,106,685 | 97,181,094 | 46,229,822 | 9 | 130 | ||||||||||||||||

14

Our holding of own shares increased from 97,181,094, or 7.7% of shares issued, on 31 December 2002, to 106,106,685 shares, or 8.4% of shares issued, on 31 March 2003, reflecting the additional shares we bought under our second trading line program and shares purchased to fund our employee share and option programs.

Of these treasury shares, 77,440,080 shares were purchased under the two 2002 and the new 2003 buyback programs. The remaining 28,666,605 shares were held for general treasury purposes, including coverage of employee share and option programs, and for market making activities by UBS Warburg. UBS Warburg acts as a market maker in UBS shares as well as derivatives related to those shares and may hold a significant amount of UBS shares as a hedge for derivatives issued to retail and institutional investors. Changes in the trading approach can lead to fluctuations in the size of our direct holding of UBS shares.

15

UBS Wealth Management & Business Banking

13 May 2003

UBS Wealth Management & Business Banking

In first quarter 2003, Private Banking’s profit before tax was CHF 534 million, up 7% from fourth quarter 2002. Net new money, at CHF 7.4 billion, included strong inflows to our European wealth management initiative. Business Banking Switzerland’s profit before tax was CHF 499 million in first quarter 2003, a 10% increase from fourth quarter 2002.

Business Group reporting

| Quarter ended | % change from | |||||||||||||||||||

| CHF million, except where indicated | 31.3.03 | 31.12.02 | 31.3.02 | 4Q02 | 1Q02 | |||||||||||||||

| Income | 2,866 | 2,857 | 3,184 | 0 | (10 | ) | ||||||||||||||

Credit loss expense1 | (57 | ) | (64 | ) | (93 | ) | (11 | ) | (39 | ) | ||||||||||

Total operating income | 2,809 | 2,793 | 3,091 | 1 | (9 | ) | ||||||||||||||

| Personnel expenses | 1,146 | 1,148 | 1,166 | 0 | (2 | ) | ||||||||||||||

| General and administrative expenses | 517 | 547 | 540 | (5 | ) | (4 | ) | |||||||||||||

| Depreciation | 94 | 118 | 116 | (20 | ) | (19 | ) | |||||||||||||

| Amortization of goodwill and other intangible assets | 19 | 26 | 24 | (27 | ) | (21 | ) | |||||||||||||

Total operating expenses | 1,776 | 1,839 | 1,846 | (3 | ) | (4 | ) | |||||||||||||

Business Group performance before tax | 1,033 | 954 | 1,245 | 8 | (17 | ) | ||||||||||||||

| Business Group performance before tax and amortization of goodwill and other intangible assets | 1,052 | 980 | 1,269 | 7 | (17 | ) | ||||||||||||||

Additional information | ||||||||||||||||||||

| Regulatory equity allocated (average) | 8,500 | 8,450 | 8,600 | 1 | (1 | ) | ||||||||||||||

Cost/income ratio (%)2 | 62 | 64 | 58 | |||||||||||||||||

Cost/income ratio before goodwill (%)3 | 61 | 63 | 57 | �� | ||||||||||||||||

1In management accounts, statistically derived actuarial expected loss adjusted by deferred releases rather than the net IFRS actual credit loss is reported in the Business Groups (see Note 2 to the Financial Statements).2Operating expenses/operating income less credit loss expense.3Operating expenses less the amortization of goodwill and other intangible assets/operating income less credit loss expense.

Georges Gagnebin

Chairman UBS Wealth Management

& Business Banking

Marcel Rohner

CEO UBS Wealth Management

& Business Banking

16

Private Banking

Business Unit reporting

| Quarter ended | % change from | |||||||||||||||||||

| CHF million, except where indicated | 31.3.03 | 31.12.02 | 31.3.02 | 4Q02 | 1Q02 | |||||||||||||||

| Income | 1,575 | 1,576 | 1,756 | 0 | (10 | ) | ||||||||||||||

Credit loss expense1 | (2 | ) | (10 | ) | (7 | ) | (80 | ) | (71 | ) | ||||||||||

Total operating income | 1,573 | 1,566 | 1,749 | 0 | (10 | ) | ||||||||||||||

| Personnel expenses | 474 | 465 | 464 | 2 | 2 | |||||||||||||||

| General and administrative expenses | 525 | 545 | 521 | (4 | ) | 1 | ||||||||||||||

| Depreciation | 21 | 30 | 19 | (30 | ) | 11 | ||||||||||||||

| Amortization of goodwill and other intangible assets | 19 | 26 | 24 | (27 | ) | (21 | ) | |||||||||||||

Total operating expenses | 1,039 | 1,066 | 1,028 | (3 | ) | 1 | ||||||||||||||

Business unit performance before tax | 534 | 500 | 721 | 7 | (26 | ) | ||||||||||||||

| Business unit performance before tax and amortization of goodwill and other intangible assets | 553 | 526 | 745 | 5 | (26 | ) | ||||||||||||||

KPI’s | ||||||||||||||||||||

| Invested assets (CHF billion) | 638 | 642 | 737 | (1 | ) | (13 | ) | |||||||||||||

Net new money (CHF billion) 2 | 7.4 | 2.8 | 2.2 | |||||||||||||||||

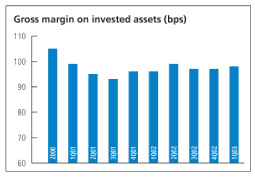

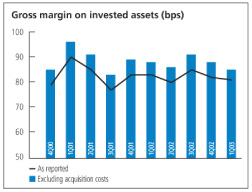

Gross margin on invested assets (bps) 3 | 98 | 97 | 96 | 1 | 2 | |||||||||||||||

Cost/income ratio (%) 4 | 66 | 68 | 59 | |||||||||||||||||

Cost/income ratio before goodwill (%) 5 | 65 | 66 | 57 | |||||||||||||||||

Cost/income ratio before goodwill and excluding the European wealth management initiative (%) 6 | 57 | 57 | 51 | |||||||||||||||||

| Client advisors (full-time equivalents) | 3,065 | 3,001 | 2,806 | 2 | 9 | |||||||||||||||

Private Banking — International Clients | ||||||||||||||||||||

| Income | 1,088 | 1,090 | 1,214 | 0 | (10 | ) | ||||||||||||||

| Invested assets (CHF billion) | 447 | 447 | 501 | 0 | (11 | ) | ||||||||||||||

Net new money (CHF billion)2 | 7.0 | 2.4 | 3.9 | |||||||||||||||||

Gross margin on invested assets (bps) 3 | 97 | 97 | 98 | 0 | (1 | ) | ||||||||||||||

European wealth management initiative (part of Private Banking — International Clients) | ||||||||||||||||||||

| Income | 52 | 47 | 43 | 11 | 21 | |||||||||||||||

| Invested assets (CHF billion) | 31 | 28 | 23 | 11 | 35 | |||||||||||||||

Net new money (CHF billion)2 | 3.0 | 2.0 | 1.3 | |||||||||||||||||

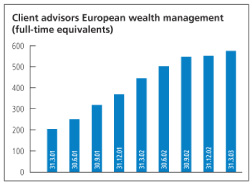

| Client advisors (full-time equivalents) | 575 | 551 | 445 | 4 | 29 | |||||||||||||||

Private Banking — Swiss Clients | ||||||||||||||||||||

| Income | 487 | 486 | 542 | 0 | (10 | ) | ||||||||||||||

| Invested assets (CHF billion) | 191 | 195 | 236 | (2 | ) | (19 | ) | |||||||||||||

Net new money (CHF billion) 2 | 0.4 | 0.4 | (1.7 | ) | ||||||||||||||||

Gross margin on invested assets (bps) 3 | 101 | 99 | 92 | 2 | 10 | |||||||||||||||

| % change from | ||||||||||||||||||||

| Additional information | ||||||||||||||||||||

| As at | 31.3.03 | 31.12.02 | 31.3.02 | 4Q02 | 1Q02 | |||||||||||||||

| Client assets (CHF billion) | 777 | 788 | 898 | (1 | ) | (13 | ) | |||||||||||||

| Regulatory equity allocated (average) | 2,550 | 2,650 | 3,000 | (4 | ) | (15 | ) | |||||||||||||

| Headcount (full-time equivalents) | 9,316 | 9,399 | 8,912 | (1 | ) | 5 | ||||||||||||||

1 In management accounts, statistically derived actuarial expected loss adjusted by deferred releases rather than the net IFRS actual credit loss is reported in the Business Groups (see Note 2 to the Financial Statements).

2 Excludes interest and dividend income.

3 Annualized income/average invested assets.

4 Operating expenses/operating income less credit loss expense.

5 Operating expenses less the amortization of goodwill and other intangible assets/operating income less credit loss expense.

6 Operating expenses less the amortization of goodwill and other intangible assets and expenses for the European wealth management initiative/operating income less credit loss expense and income for the European wealth management initiative.

17

UBS Wealth Management & Business Banking

13 May 2003

Key performance indicators

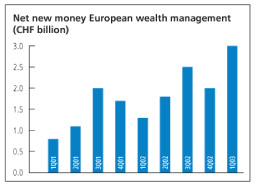

Net new money in first quarter 2003 was CHF 7.4 billion, up from CHF 2.8 billion in the previous quarter. This strong inflow — our third best quarter since 2000 - - came despite a very discouraging environment for clients’ investment decisions. The Private Banking — International Clients area recorded CHF 7.0 billion in net new money, with a positive inflow in all markets and a record inflow into our European wealth management initiative, while the Private Banking - - Swiss Clients area showed a modest inflow of CHF 0.4 billion.

Despite the strong inflow of net new money, invested assets on 31 March 2003 were CHF 638 billion, down 1% from CHF 642 billion on 31 December 2002. The decline was due to the further falls in global equity markets as well as the 2% drop in the US dollar against the Swiss franc during the quarter.

Gross margin on invested assets increased slightly by one basis point to 98 basis points in first quarter 2003.

The pre-goodwill cost/income ratio, at 65% in first quarter 2003, was down one percentage point from fourth quarter 2002. The slight drop in income was more than offset by our cost control measures. We will continue to cut running costs while at the same time investing in the long-term success of our European wealth management initiative. Excluding the European wealth management initiative, the pre-goodwill cost/income ratio was 57% in first quarter 2003, unchanged from fourth quarter 2002.

European wealth management

Net new money in first quarter 2003 stood at CHF 3.0 billion — the best quarterly result since the initiative’s launch at the beginning of 2001. Excellent inflows were recorded in Germany and the UK. Despite falling equity markets, the level of invested assets also rose to a new high of CHF 31 billion.

Income for the European wealth management initiative in first quarter 2003 was a record CHF 52 million, up from CHF 47 million in fourth quarter 2002 due to higher revenues from the growing asset base.

18

The number of client advisors rose to 575 at the end of March 2003, up from 551 at the end of December 2002, reflecting our continued investment in qualified advisory staff.

Initiatives and achievements

Corporate Employee Financial Services launched

In January 2003, we launched a business in Europe to administer stock and option plans for European executives and corporations. The business is known as Corporate Employee Financial Services (CEFS).

The CEFS Europe team draws on the experience of the UBS PaineWebber team of the same name, which runs a similar and successful service in the US. In Europe, CEFS is expected to meet the growing demand from companies for stock and option plan services. A 2002 survey by Mercer Consulting showed that up to 75% of European companies list administrative issues as their primary concern when offering such plans to their employees. Thus the potential demand for this service in the European market is significant.

The goal of our CEFS Europe service is to present an integrated solution that combines plan administration with other related financial services for corporate and private clients. Such services can include equity risk management, corporate finance, training and financial planning advice to corporations and their executives.

Warsaw representative office opened

At the end of March 2003, UBS opened a new representative office in Warsaw, Poland. The office will promote the firm’s range of products and services in wealth management, investment banking, and asset management.

New software for client advisors

During the first quarter, we also introduced a software application in Switzerland called the “Front End Tool” that supports our systematic advisory process. By using it, client advisors and their clients can pinpoint individual investment objectives and conduct a thorough risk analysis. This, in turn, assists client advisors in developing a personalized investment strategy tailored to each client, derived from our strategic asset allocations recommended for different risk profiles. After that, the software helps client advisors choose a suitable portfolio from a selection of carefully screened mutual funds. If the client accepts an advisor’s recommendations, contract documents can be automatically generated during the meeting, with client advisors also able to place the initial investment directly afterwards through the new tool. The application also tracks a client’s portfolio performance and helps both the clients and client advisors assess overall performance when meeting to review progress.

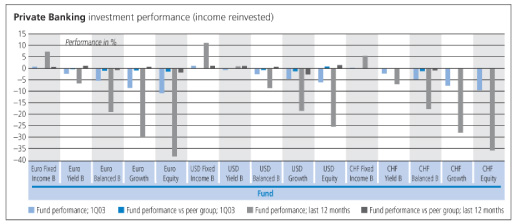

Investment performance

Financial market sentiment suffered further in the first quarter because of the deteriorating outlook for a global economic recovery, and the crisis in the Middle East — which culminated in the war in Iraq. Although equity markets showed short periods of recovery, overall they continued to lose ground over the quarter.

The performance of UBS Strategy Funds was strongly influenced by these global financial

19

UBS Wealth Management & Business Banking

13 May 2003

market developments. In first quarter 2003, UBS Strategy Funds performed below those of our peers, due to their slightly higher-than-average weighting of equities. This contrasts with our performance in the previous quarter and over the last 12 months.

The graph above illustrates how pure equity funds saw, in absolute terms, a clearly negative performance in first quarter 2003, in line with global share market developments. In contrast, bond-only funds still produced positive absolute returns. US dollar-denominated funds, also in absolute terms, again reported the best performance because of their weighting towards US shares, which outperformed their European and Swiss counterparts. Additionally, the euro and Swiss franc gained further ground against the US dollar in the first quarter, supporting the absolute returns of funds denominated in US dollars.

Relative to benchmark, our overall performance was negatively affected by stock selection. In contrast, our market selection on the fixed income side added positively to relative performance.

Results

In first quarter 2003, Private Banking’s profit before tax was CHF 534 million, up 7% from the fourth quarter 2002, as performance benefited from lower running costs. The cost/income ratio dropped from 68% in fourth quarter 2002 to 66% in first quarter 2003.

Operating income

Total operating income, at CHF 1,573 million in first quarter 2003, increased by CHF 7 million from fourth quarter 2002, mainly due to lower credit loss expenses. While transaction income rose on higher sales commissions for UBS investment funds, recurring income declined slightly because of lower asset-based revenues reflecting falling invested assets. The share of recurring fees to total income remained unchanged at 73%.

Operating expenses

Total operating expenses were CHF 1,039 million, down 3% from the previous quarter, as costs remained under tight control despite continued investment in our European wealth management initiative. While personnel expenses increased in first quarter 2003 by 2% from the previous quarter, mainly because of higher expenses for our early retirement program, general and administrative expenses fell 4% from

20

the previous quarter due to lower professional fees as well as reduced travel and entertainment expenses. Depreciation fell CHF 9 million from CHF 30 million in the previous quarter to CHF 21 million in first quarter 2003, due to lower charges for information technology equipment, which is increasingly being leased instead of bought.

Headcount

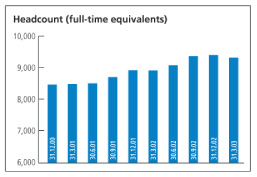

Headcount, at 9,316 on 31 March 2003, decreased by 83 from 31 December 2002. While we continued to hire client advisors for our European wealth management initiative, non-client advisor headcount was reduced, mainly reflecting our currently restrictive hiring policy.

Outlook

The uncertain political and economic environment will continue to weigh on investor sentiment and limit our ability to grow revenues. However, we believe that the most severe pressure from market-related declines on asset levels could be behind us.

It is clear from our ability to attract new money that clients value our financial strength and individualized advisory services. Indeed, in difficult markets, clients seem increasingly to turn to us. We are confident that this strong asset-gathering performance and the corresponding market share gains provide a good basis for future growth. As long as revenue prospects remain uninspiring however, we will be able to rely on our proven cost control discipline to underpin earnings.

21

UBS Wealth Management & Business Banking

13 May 2003

Business Banking Switzerland

Business Unit reporting

| Quarter ended | % change from | |||||||||||||||||||

| CHF million, except where indicated | 31.3.03 | 31.12.02 | 31.3.02 | 4Q02 | 1Q02 | |||||||||||||||

| Income | 1,291 | 1,281 | 1,428 | 1 | (10 | ) | ||||||||||||||

Credit loss expense1 | (55 | ) | (54 | ) | (86 | ) | 2 | (36 | ) | |||||||||||

Total operating income | 1,236 | 1,227 | 1,342 | 1 | (8 | ) | ||||||||||||||

| Personnel expenses | 672 | 683 | 702 | (2 | ) | (4 | ) | |||||||||||||

| General and administrative expenses | (8 | ) | 2 | 19 | ||||||||||||||||

| Depreciation | 73 | 88 | 97 | (17 | ) | (25 | ) | |||||||||||||

| Amortization of goodwill and other intangible assets | 0 | 0 | 0 | |||||||||||||||||

Total operating expenses | 737 | 773 | 818 | (5 | ) | (10 | ) | |||||||||||||

Business unit performance before tax | 499 | 454 | 524 | 10 | (5 | ) | ||||||||||||||

| Business unit performance before tax and amortization of goodwill and other intangible assets | 499 | 454 | 524 | 10 | (5 | ) | ||||||||||||||

KPI’s | ||||||||||||||||||||

| Invested assets (CHF billion) | 197 | 205 | 219 | (4 | ) | (10 | ) | |||||||||||||

Net new money (CHF billion)2 | (1.9 | ) | (2.7 | ) | 2.3 | |||||||||||||||

Cost/income ratio (%)3 | 57 | 60 | 57 | |||||||||||||||||

Cost/income ratio before goodwill (%)4 | 57 | 60 | 57 | |||||||||||||||||

| Non-performing loans/gross loans outstanding (%) | 3.5 | 3.6 | 4.4 | |||||||||||||||||

| Impaired loans/gross loans outstanding (%) | 5.7 | 6.0 | 7.4 | |||||||||||||||||

| % change from | ||||||||||||||||||||

| Additional information | ||||||||||||||||||||

| As at or for the period ended | 31.3.03 | 31.12.02 | 31.3.02 | 4Q02 | 1Q02 | |||||||||||||||

Deferred releases included in credit loss expense1 | 77 | 70 | 53 | 10 | 45 | |||||||||||||||

| Client assets (CHF billion) | 481 | 494 | 559 | (3 | ) | (14 | ) | |||||||||||||

| Regulatory equity allocated (average) | 5,950 | 5,800 | 5,600 | 3 | 6 | |||||||||||||||

| Headcount (full-time equivalents) | 18,302 | 18,442 | 19,262 | (1 | ) | (5 | ) | |||||||||||||

1 In management accounts, statistically derived actuarial expected loss adjusted by deferred releases rather than the net IFRS actual credit loss is reported in the Business Groups (see Note 2 to the Financial Statements). Deferred releases represent amortization of historical differences between actual credit losses and actuarial expected loss (for more information, please refer to pages 39-40 of the UBS Financial Report 2002).2Excludes interest and dividend income.3 Operating expenses/operating income less credit loss expense.4Operating expenses less the amortization of goodwill and other intangible assets/operating income less credit loss expense.

Key performance indicators

Net new money was a negative CHF 1.9 billion in first quarter 2003, mainly due to CHF 3.6 billion in transfers by corporate clients from their short-term deposits to their current accounts, which are not classified as invested assets. Although this is the second consecutive quarterly outflow we have reported, the corporate clients business is traditionally subject to relatively large swings in net new money. In first quarter, the main reason for the transfers was the extremely low interest rates for short-term investments.

Invested assets were CHF 197 billion on 31 March 2003, down 4% from 31 December 2002, due to the impact of declining global equity markets, the fall in value of the US dollar against the Swiss franc, as well as the outflow of net new money from corporations.

Our cost/income ratio improved significantly, falling to 57% in first quarter 2003 from 60% in

22

fourth quarter 2002, proving our ability to control costs in a difficult environment.

At the end of first quarter 2003, Business Banking Switzerland’s loan portfolio increased to CHF 141.4 billion from CHF 139.5 billion at the end of 2002. Inflows in the mortgage area, which benefited from interest rates at historic lows and a national advertising campaign (see article on the next page) more than offset the ongoing workout of the recovery portfolio, which fell to CHF 8.2 billion this quarter from CHF 8.6 billion in the previous quarter. The non-performing loans ratio declined to 3.5% on 31 March 2003 from 3.6% on 31 December 2002, and the impaired loan ratio fell to 5.7% on 31 March 2003, down from 6.0% on 31 December 2002.

In first quarter 2003, Business Banking Switzerland’s net interest income rose slightly in comparison to fourth quarter 2002. This was mainly due to an increase in the interest margin on savings accounts and higher savings account volumes. Also, our mortgage business saw an increase in volume, in particular for fixed-rate and money market mortgages, contributing positively to net interest income. Lower investment interest margins on current accounts, however, offset some of the positive impact.

Initiatives and achievements

UBS launches another transaction securitizing loans to Swiss SMEs

In March 2003, UBS securitized part of the credit risks related to a CHF 2.5 billion portfolio of loans to Swiss small and medium-sized enterprises. This deal, a collateralized loan obligation called HAT (Helvetic Asset Trust) II, involves transferring not the loans themselves, but rather the default risks to the capital market. In order to achieve this transfer, a special purpose vehicle entered into a credit default swap with UBS, and issued four classes of euro-denominated credit-linked notes that were placed on the euro capital market and listed on the Irish Stock Exchange.

UBS’s first HAT transaction, launched in June 2000, had a similar structure, but involved Swiss franc-denominated instruments. For HAT II, the euro capital market was chosen due to its higher liquidity and receptivity for such structured debt instruments. For investors, HAT II offers an opportunity to diversify their portfolios by gaining exposure to Swiss small-business credit risks.

Strategic Project Portfolio

Our Strategic Project Portfolio, which groups our most important initiatives, is aimed at enhancing revenues and controlling costs by improving processes, products and distribution methods.

In 2000, as part of this portfolio, we launched the “Site Optimization Program” in Switzerland. Its aim was to improve computer system availability while containing IT costs. Other objectives were to enhance our ability to cope with operational crises and allow growth in IT capacity for entry into new markets. In order to achieve this, we are building a new computer center near Zurich that is scheduled to start operating in 2004. It will be linked by fiber-optic cable to our existing major IT center which is located roughly 10 kilometers away. In the event that one center fails, the other would immediately take over its tasks. The new center is being built on the assumption of 99.999

23

UBS Wealth Management & Business Banking

13 May 2003

percent system availability, meaning that it would be down for around five minutes a year, planned or unplanned. When the Program is fully in place, it will allow us to close a number of smaller back-up IT sites located around Switzerland.

Results

In first quarter 2003, Business Banking Switzerland reported its third-highest quarterly pre-tax profit ever of CHF 499 million — a 10% increase from fourth quarter 2002. Revenues rose slightly due to higher interest income, while costs fell to a record low, mainly due to lower personnel expenses. The cost/income ratio dropped to a record low of 57% in first quarter 2003 from 60% in fourth quarter 2002.

Operating income

Total operating income in first quarter 2003 was CHF 1,236 million, up 1% or CHF 9 million from fourth quarter 2002 despite the adverse market environment. Interest income increased due to higher mortgage and savings volumes, while fee income remained stable and trading income fell in the difficult financial market environment.

Operating expenses

Operating expenses fell to CHF 737 million in first quarter 2003, down 5% from fourth quarter 2002. Personnel expenses, at CHF 672 million, decreased 2%, showing the impact of a restrictive hiring policy and the ongoing streamlining of processes and structures, which held headcount down.

General and administrative expenses dropped again in first quarter to a negative CHF 8 million, against a positive CHF 2 million in fourth quarter 2002. The decline was due to lower professional fees, and falling travel and

Low rates, high season for Swiss mortgage business

The message is clear. “We are the right address for competitive mortgages.” As the advertising campaign along Switzerland’s high streets shows, the country’s historically low interest rates have provided UBS mortgage loan marketers with their latest opportunity.

The street advertising placards are the more visible manifestations of a concerted campaign to consolidate and even extend the firm’s strong position in the domestic home loans business. Already the market leader, UBS Wealth Management & Business Banking sees falling interest rates as a unique opportunity to re-invigorate consumer interest in its products.

The current campaign started in the autumn of 2002 with nationwide TV spots for UBS home loan products. From early 2003, client advisors followed up with coordinated marketing activities, including personalized mailings and approaches to potential new clients.