1

MERGER BETWEEN UBS AG AND CREDIT SUISSE AG

On December 7, 2023, UBS AG (“UBS Parent Bank”) and Credit Suisse AG (“Credit Suisse Parent Bank”) entered into a merger

agreement that provides for the merger of Credit Suisse Parent Bank into UBS Parent Bank. On the terms and subject to the

conditions set forth in the merger agreement and in accordance with applicable provisions of the Swiss law, Credit Suisse Parent

Bank will merge with and into UBS Parent Bank. UBS Parent Bank being the absorbing company will continue to operate and

Credit Suisse Parent Bank being the absorbed company will cease to exist (the “Transaction”). Under the terms of the merger

agreement, at the effective time of the Transaction all of the outstanding ordinary shares of Credit Suisse Parent Bank will be

cancelled; no consideration will be paid as all of the outstanding shares of each of UBS Parent Bank and Credit Suisse Parent

Bank are owned by UBS Group AG. Completion of the Transaction is subject to certain conditions, including obtaining of all

regulatory approvals and licenses or other regulatory action required for the completion of the Transaction or the subsequent

continuation of the business by UBS Parent Bank.

2

UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION

All amounts in this section are in US dollars (USD) unless otherwise specified. The abbreviation “bn” is used to represent

“billion”. The abbreviation “CHF” is used to represent “Swiss francs”. Numbers presented throughout this section may not add up

precisely to the totals provided in the tables and text due to rounding.

The following unaudited pro forma condensed combined financial information is intended to illustrate the effect of the transaction

(as previously defined) and comprises the following:

•

the unaudited pro forma condensed combined income statement of UBS AG for the year ended 31 December

2022, prepared as if the transaction occurred on 1 January 2022 (and the merger between UBS Group AG and

Credit Suisse Group AG (Group merger) occurred just before the transaction);

•

the unaudited pro forma condensed combined income statement of UBS AG for the six-month period ended 30

June 2023, prepared as if the transaction occurred on 1 January 2022 (and the Group merger occurred just before

the transaction); and

•

the unaudited pro forma condensed combined balance sheet as of 30 June 2023 for UBS AG, prepared as if the

transaction had occurred at that date (and the Group merger occurred as of 12 June 2023).

The transaction is a business combination of entities under common control (a “common control transaction”) as defined under

IFRS 3

Business Combinations

when the Group merger occurred, and it controls the two businesses merged before and after the business combination. IFRS 3

Business Combinations

required. Instead, in the absence of a specific IFRS requirement, UBS Parent Bank applied the

carry over basis

the predecessor accounting method) consistent with previous UBS group-internal legal entity transactions and as commonly

applied under Swiss regulations.

Under the carry over basis, the estimated IFRS-equivalent balance sheet amounts of Credit Suisse Parent Bank are added across

each line item with the UBS Parent Bank balance sheet amounts, as at the merger date. No adjustments have been made to reflect,

for example, the fair value of amortized cost assets and the fair value of non-financial assets and liabilities that were recorded in

the UBS Group AG consolidated financial statements as a result of applying the acquisition method as required under IFRS 3 on

31 May 2023 for the acquisition of Credit Suisse Group AG (note that with the acquisition date of 12 June 2023, for convenience

the Credit Suisse Group was consolidated with effect from 31 May 2023, as the effect of transactions and activities in the period

from 31 May 2023 to 12 June 2023 on the consolidated financial statements was not material).

The unaudited pro forma condensed combined financial information is presented for illustrative purposes only and reflects

estimates and assumptions made by UBS Parent Bank’s management that it considers reasonable. Such estimates and assumptions

are subject to change as additional analyses are completed in advance of the transaction. The unaudited pro forma condensed

combined financial information does not purport to represent what UBS Parent Bank’s actual results of operations or financial

condition would have been had the transaction occurred on the dates indicated, nor is it necessarily indicative of future results of

operations or financial condition.

At the UBS Group AG level, IFRS 3 Business Combinations provides a twelve-month measurement period from the date of the

Credit Suisse acquisition (12 June 2023). The finalization of the respective valuations may result in further knock-on impacts for

the accompanying unaudited pro forma condensed combined financial information (and the future combined results of operations

or combined financial condition of the merged entity) and such impacts could be material. Other than those disclosed in the notes,

the unaudited pro forma condensed combined financial information does not reflect expense efficiencies, asset dispositions or

business reorganizations that are or may be contemplated, or any cost or revenue synergies, including any potential restructuring

actions.

The unaudited pro forma condensed combined financial information should be read in conjunction with the consolidated financial

statements of UBS Parent Bank and Credit Suisse Parent Bank and the accompanying notes included in UBS Parent Bank’s and

Credit Suisse Parent Bank’s Annual Reports on Form 20-F and interim financial reports on Form 6-K, as well as the additional

disclosures contained therein. These documents are available on UBS’s website at www.ubs.com/investors and at the SEC’s

website at www.sec.gov.

3

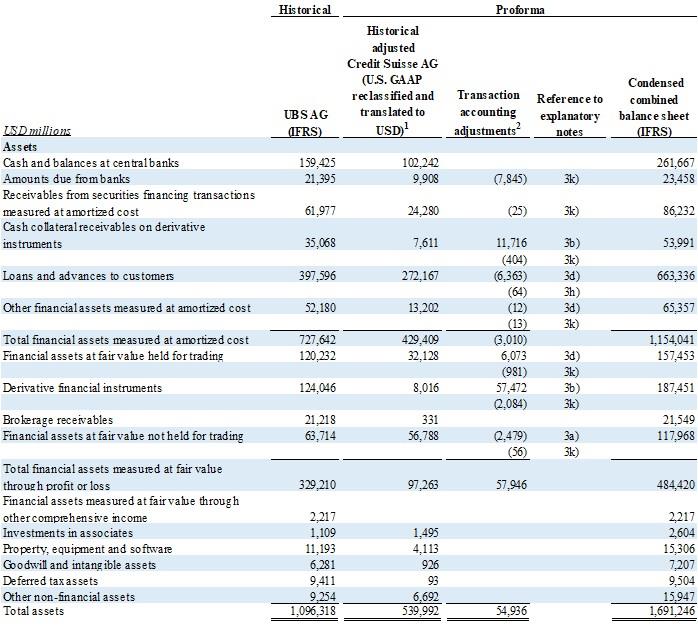

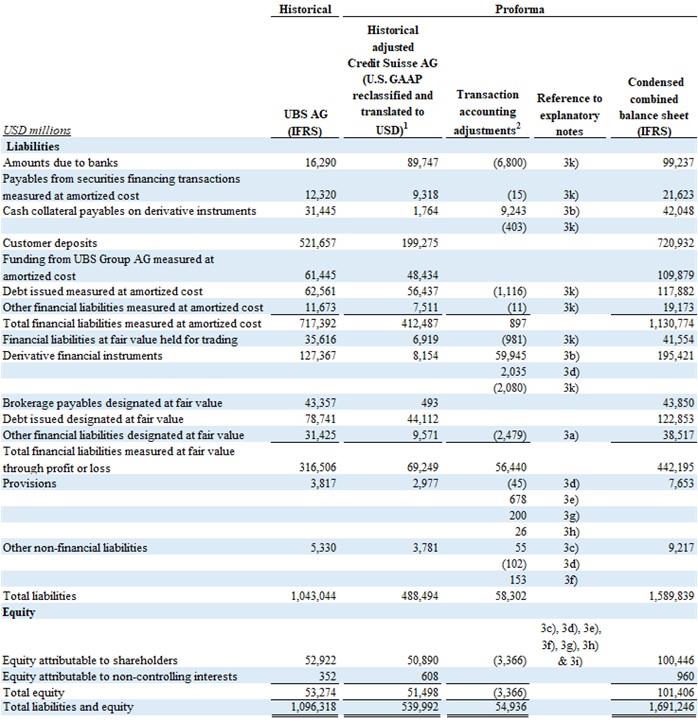

Unaudited Pro Forma Condensed Combined Balance Sheet

as of 30 June 2023

4

Unaudited Pro Forma Condensed Combined Balance Sheet

as of 30 June 2023

1

Reflects the U.S. GAAP balance sheet for Credit Suisse Parent Bank as of 30 June 2023, translated to US dollars at a rate of

1.12 (CHF/USD) and reflecting asset and liability presentation reclassification adjustments applied to conform with UBS

Parent Bank’s consolidated financial statement presentation. Refer to Note 2 in the explanatory notes for further

information.

2

Refer to Note 3 in the explanatory notes for further information.

See accompanying notes.

5

Unaudited Pro Forma Condensed Combined Income Statement

for the six-month period ended 30 June 2023

1

Reflects the U.S. GAAP income statement of Credit Suisse Parent Bank for the six-month period ended 30 June 2023,

translated to US dollars at a rate of 1.10 (CHF/USD) and reflecting presentation reclassification adjustments applied to

conform with UBS Parent Bank’s consolidated financial statement presentation. Refer to Note 2 in the explanatory notes for

further information.

2

Refer to Note 3 in the explanatory notes for further information.

3

Includes 15,483m relating to the cancellation of additional tier 1 capital obligations of Credit Suisse Parent Bank to Credit

Suisse Group AG that were written down concurrently with the FINMA ordered write-down of the additional tier 1 capital

instruments of Credit Suisse Group AG.

See accompanying notes.

6

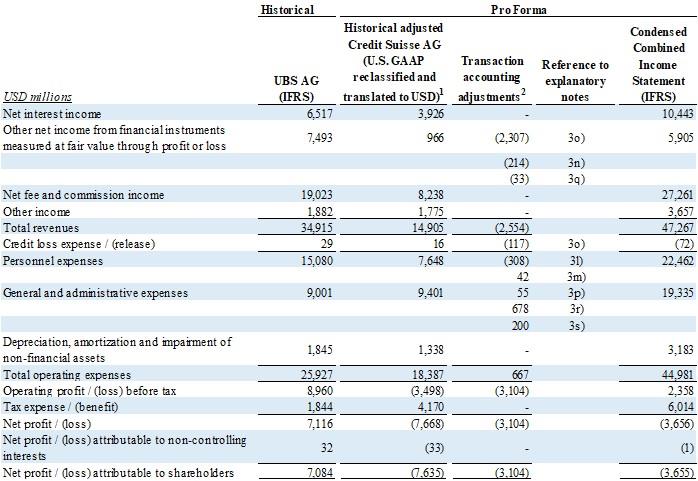

Unaudited Pro Forma Condensed Combined Income Statement

for the year ended 31 December 2022

1

Reflects the U.S. GAAP income statement of Credit Suisse Parent Bank for the year ended 31 December 2022, translated to

US dollars at a rate of 1.05 (CHF/USD) and reflecting presentation reclassification adjustments applied to conform with

UBS Parent Bank’s consolidated financial statement presentation. Refer to Note 2 in the explanatory notes for further

information.

2

Refer to Note 3 in the explanatory notes for further information.

See accompanying notes.

7

Notes to unaudited pro forma condensed combined financial information

(in USDbn except where otherwise indicated)

Basis of preparation

The unaudited pro forma condensed combined financial information gives effect to the merger of Credit Suisse Parent Bank into

UBS Parent Bank. The unaudited pro forma condensed combined balance sheet gives effect to the transaction as if it had closed

on 30 June 2023.

The unaudited pro forma condensed combined income statements for the year ended 31 December 2022 and for the six-month

period ended 30 June 2023 give effect to the transaction as if it had closed on 1 January 2022. The unaudited pro forma condensed

combined income statement for the twelve months ended 31 December 2022 does not include certain transaction accounting

adjustments associated with the Group merger, as they are already reflected in the historical income statement of the Credit Suisse

Parent Bank for the six-month period ended 30 June 2023. The acquisition of Credit Suisse AG by UBS Group AG is also

assumed to have occurred as of 1 January 2022 for the purpose of the income statements.

No adjustments have been reflected in the unaudited pro forma condensed combined financial information for the effects of items

that have been considered to be immaterial.

Explanatory notes on pro forma condensed combined financial information

Note 1: Basis of preparation

The unaudited pro forma condensed combined financial information was prepared based on the audited and unaudited

consolidated financial statements of UBS Parent Bank and Credit Suisse Parent Bank respectively as of and for the year ended

31 December 2022 and for the six-month period ended 30 June 2023, respectively, as well as other information . The unaudited

pro forma condensed combined financial information should therefore be read in conjunction with the following consolidated

financial statements, including the notes thereto:

•

the audited consolidated financial statements of UBS AG as of and for the year ended 31 December 2022, which

have been prepared in accordance with IFRS and are included in the UBS Group AG Annual Report;

•

the unaudited consolidated financial statements of UBS AG as of and for the six-month period ended 30 June

2023, which have been prepared in accordance with IFRS and are included in the UBS AG second quarter 2023

Report;

•

the audited consolidated financial statements of Credit Suisse AG as of and for the year ended 31 December

2022, which have been prepared in accordance with U.S. GAAP and are included in the Credit Suisse Group AG

Annual Report; and

•

the unaudited consolidated financial statements of Credit Suisse AG as of and for the six-month period ended 30

June 2023, which have been prepared in accordance with U.S. GAAP and are included in the Credit Suisse AG

half-year 2023 Report.

The Credit Suisse Parent Bank historical consolidated financial statements were prepared in accordance with U.S. GAAP and

presented in Swiss francs (CHF). For purposes of the unaudited pro forma condensed combined financial information, those

financial statements have been adjusted to conform to the recognition, measurement and presentation requirements of IFRS and

presented in US dollars (USD), which is the presentation currency of UBS Parent Bank. Balance sheet information available for

Credit Suisse Parent Bank in CHF has been translated to USD using a spot rate of 1.12 (CHF/USD) as of 30 June 2023. Income

statement information available for Credit Suisse Parent Bank in CHF has been translated to USD using an average rate of 1.05

(CHF/USD) for the year ended 31 December 2022 and 1.10 (CHF/USD) for the six-month period ended 30 June 2023.

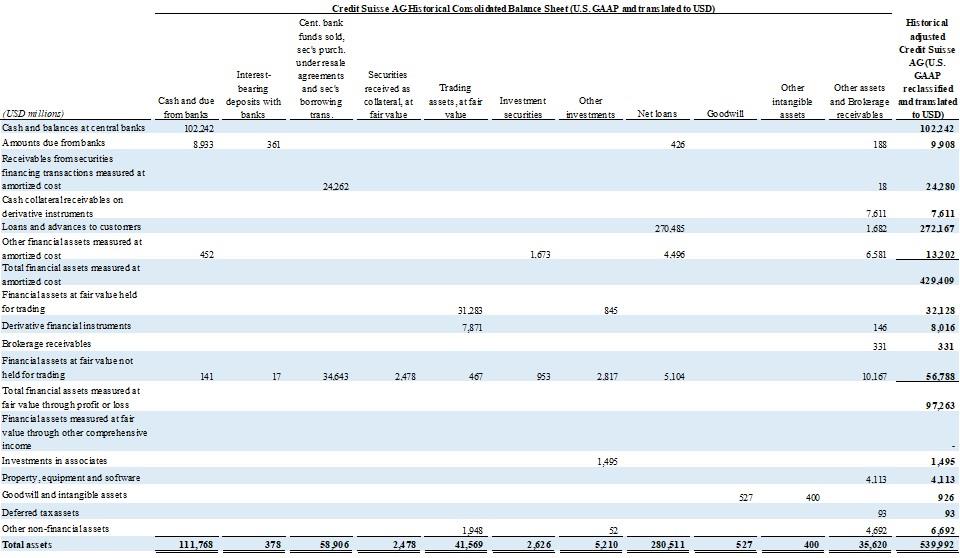

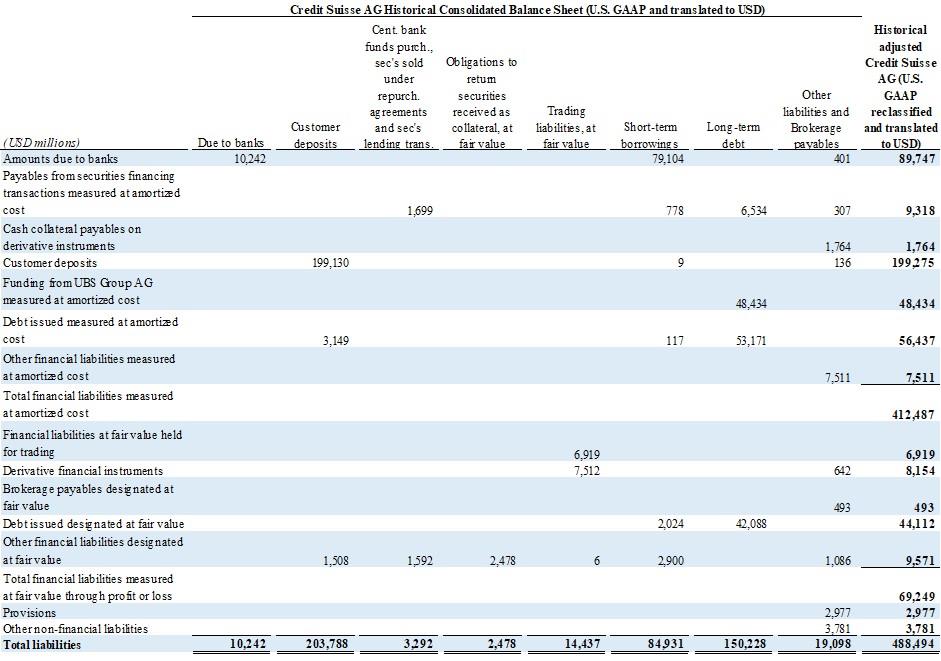

Note 2: Presentation reclassification adjustments

Presentation reclassification adjustments have been applied to Credit Suisse Parent Bank’s balance sheet and income statement

information in order to conform with UBS Parent Bank’s consolidated financial statement presentation.

The tables below show the reclassification of historical Credit Suisse Parent Bank consolidated assets and liabilities as of 30 June

2023 and income statement lines for the six-month period ended 30 June 2023 and for the year ended 31 December 2022 from the

U.S. GAAP presentation (horizontal captions and amounts) to the respective UBS Parent Bank asset and liability and income

statement structure (U.S. GAAP reclassified) (vertical captions and amounts). The Credit Suisse Parent Bank financial statement

amounts are presented in USD and have been translated from CHF as indicated in Note 1 above.

8

Credit Suisse AG consolidated balance sheet as of 30 June 2023

9

Credit Suisse AG consolidated balance sheet as of 30 June 2023

10

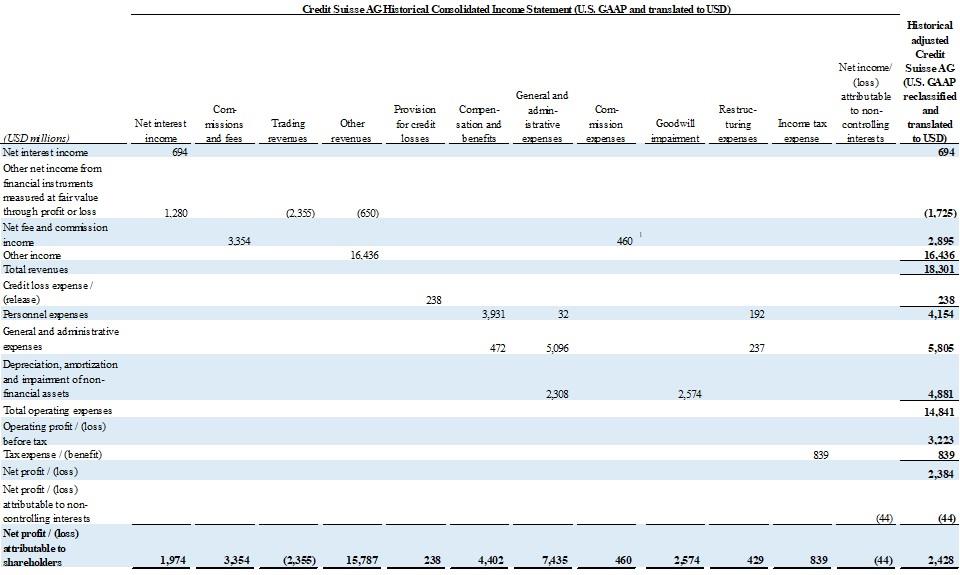

Credit Suisse AG consolidated income statement for the six-month period ended 30 June 2023

1 Commission expenses are presented for UBS as a contra-revenue item and are therefore a deduction from net fee and commission income. For the purpose of this table however they are

presented as a positive number, consistent with the presentation of expenses.

11

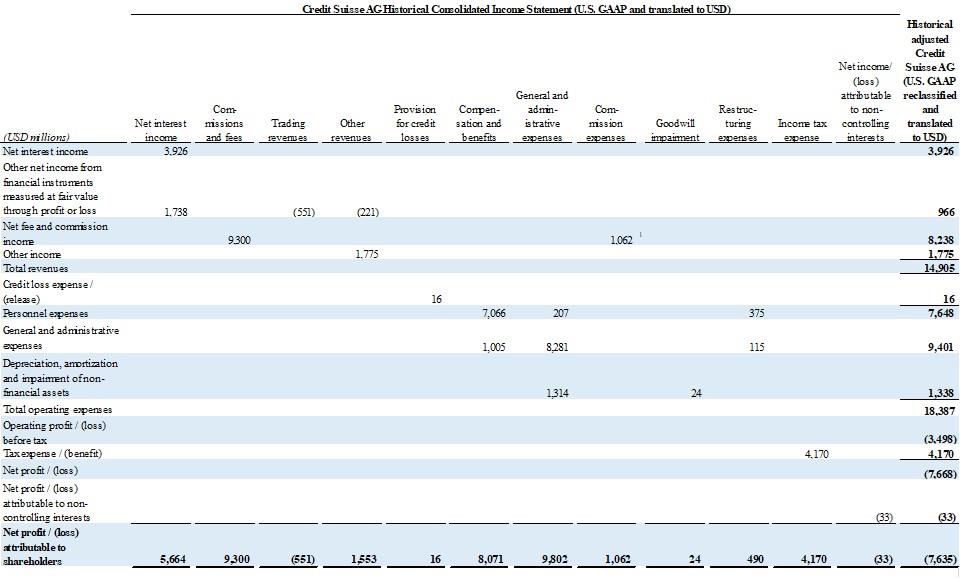

Credit Suisse AG consolidated income statement for the year ended 31 December 2022

1 Commission expenses are presented for UBS as a contra-revenue item and are therefore a deduction from net fee and commission income. For the purpose of this table however they are

presented as a positive number, consistent with the presentation of expenses.

12

Note 3: Transaction accounting adjustments

Transaction accounting adjustments include certain pro forma preliminary adjustments to conform Credit Suisse Parent Bank’s

balance sheet and income statements to UBS Parent Bank’s IFRS accounting policies and certain combination adjustments.

All pro forma adjustments have been considered on a pre- and post-tax basis. UBS Parent Bank’s internal tax assessment

concluded that there are no material estimated tax impacts arising from the pre-tax adjustments set out in this section. Refer to

Note 3j) for further detail. This assessment included certain assumptions and represents UBS Parent Bank’s best estimate as to the

likely tax impacts. The assessment could change as further information becomes available, including how the entities and

businesses in each location will be reorganized, receipt of revised profit forecasts for those entities, and discussions with the

relevant tax authorities. No deferred tax assets have been recognized in connection with the pre-tax adjustments as it is assumed

that the pre-tax adjustments will either not be recognized for tax purposes, or they will generally relate to entities with tax losses

carried forward that are not recognized as deferred tax assets.

The following notes reference the unaudited pro forma condensed combined balance sheet as of 30 June 2023 and the unaudited

pro forma condensed combined income statements for the year ended 31 December 2022 and the six-month period ended 30 June

2023.

Balance sheet

a) Reflects an adjustment to derecognize certain positions that were recognized under U.S. GAAP. Under U.S. GAAP,

lenders of securities are required to gross up their balance sheet if they receive securities as collateral (recognizing a

respective asset and liability for the securities received that need to be redelivered). These transactions are not

reflected in the balance sheet under IFRS. Securities received as collateral and the associated obligation to return

securities received as collateral of 2.5bn recognized by Credit Suisse Parent Bank under U.S. GAAP have been

derecognized under IFRS.

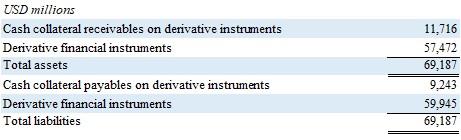

b) Reflects an adjustment to reverse certain netting impacts allowable under U.S. GAAP but not under IFRS. Under

U.S. GAAP, derivative financial instruments may be presented on a net basis where an enforceable master netting

agreement is in place. IFRS offsetting rules are more restrictive, requiring, in addition to having an enforceable right

to offset upon the counterparty’s default, the right to offset if the reporting entity itself defaults and the right and

intent to offset in the normal course of business.

UBS Parent Bank has reviewed Credit Suisse Parent Bank’s offsetting under U.S. GAAP and the estimated impact

of this accounting difference as of 30 June 2023 results in an increase in Credit Suisse Parent Bank’s total assets and

liabilities by approximately 69.2bn. The table below summarizes the impact of this adjustment on the relevant

balance sheet line items.

c) An adjustment has been reflected to include an accrual for estimated costs to effect the merger of 55m, based on the

estimate of costs to be incurred up to closing of the Transaction for both UBS Parent Bank and Credit Suisse Parent

Bank, consisting primarily of external legal, accounting and consulting fees. An increase to liabilities of 55m for

estimated costs for Credit Suisse Parent Bank and UBS Parent Bank is reflected in the unaudited pro forma

condensed combined balance sheet line under “Other non-financial liabilities”. As these accruals have not yet been

reflected in UBS Parent Bank’s and Credit Suisse Parent Bank’s individual balance sheets as of 30 June 2023, the

respective income statement charge to “General and administrative expenses” has been reflected in the earliest pro

forma condensed combined income statement presented, being the year ended 31 December 2022. Refer to Note 3p)

for the associated impact on the pro forma condensed combined income statement for the year ended 31 December

2022.

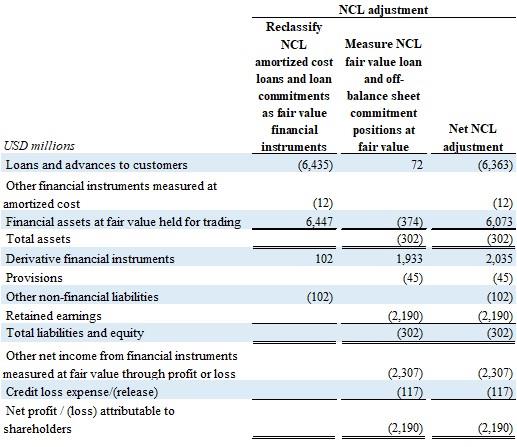

d) In the third quarter of 2023, the management of UBS determined that it intended to sell certain loans and off-balance

sheet loan commitments held by the newly created Non-core and Legacy business division (“NCL”), which affects

the IFRS 9 classification of these loans and loan commitments. Accordingly, 6,435m of “Loans and advances to

customers” and 12m of accrued interest on those loans (recorded in “Other financial instruments measured at

amortized cost”), previously measured at amortized cost, were reclassified to “Financial assets at fair value held for

trading”. Further, off-balance sheet loan commitments with a notional value of 27.5bn not measured at fair value

were reclassified to derivative loan commitments. The reclassification impact on the liability side resulted in 98m of

deferred loan commitment fees and 4m of other liabilities (both recorded in “Other non-financial liabilities”) being

13

reclassified to “Derivative financial instruments”. The carrying values of the reclassified assets and loan

commitments were then remeasured at fair value.

The fair value measurement adjustments arising from the reclassification were primarily (i) a fair value reduction

in ”Financial assets at fair value held for trading” by 374m and a fair value increase in Derivative financial liabilities

of 1,933m, resulting in a 2,307m charge against “Other net income from financial instruments measured at fair value

through profit or loss” and (ii) an estimated 117m release of credit provisions no longer required on the amortized

cost loans (72m) and the loan commitments (45m) which was credited to “Credit loss expense/(release)”.

The fair value reclassification and measurement adjustments are summarized in the table below. As this event arose

subsequent to 30 June 2023 and is significant, it has been reflected in the balance sheet as of 30 June 2023 and in the

earliest pro forma condensed combined income statement presented, being the year ended 31 December 2022. Refer

to Note 3o) for the associated impact on the pro forma condensed combined income statement for the year ended

31 December 2022.

e) Reflects an adjustment to recognize an estimated 0.7bn provision for onerous contracts, reflecting UBS management

decisions taken in connection with the Group merger for a service arrangement. Under U.S. GAAP, onerous contract

provisions cannot be recognized while the respective contract is still in use; under IFRS, such provisions are

recognized on the basis of a management decision to reduce usage. An associated income statement charge to

“General and administrative expenses” has been reflected in the earliest pro forma condensed combined income

statement presented (the year ended 31 December 2022). Refer to Note 3r) for the associated impact on the pro

forma condensed combined income statement for the year ended 31 December 2022.

f) As mentioned in Note 3l)ii., share based payments under which Credit Suisse Parent Bank delivered shares of its

parent are considered to be cash settled under IFRS, as opposed to equity settled under U.S. GAAP, requiring a

liability of 153m to be recognized within “Other non-financial liabilities”.

g) In the third quarter ended 30 September 2023, management of UBS recorded real estate onerous contract provisions

in connection with decisions to vacate certain premises post the acquisition of Credit Suisse Group AG. For the

purpose of the unaudited condensed combined pro forma information, an additional expense of 0.2bn has been

reflected in the pro forma income statement for the year ended 31 December 2022 and a provision of 0.2bn has been

recognized in the pro forma balance sheet as of 30 June 2023 in connection with this event. Refer to Note 3s) for the

associated impact on the pro forma condensed combined income statement for the year ended 31 December 2022.

14

h) For the purpose of the condensed combined pro forma financial information, differences between accounting for

credit losses between U.S. GAAP and IFRS have been considered. An estimated additional allowance of 64m has

been recorded against the carrying value of non-impaired Loans and advances to customers and an estimated

additional provision for credit losses of 26m has been recognized for qualifying off-balance sheet commitments and

guarantees that are not impaired. The increase in comparison with the Credit Suisse Parent Bank U.S. GAAP credit

loss provision reflects the estimated impact of applying UBS’s scenarios and scenario weights, calibration of model

outputs with UBS’s model outputs and scope differences. This is partly offset by ECL reductions related to

performing loans and loan commitments which are not subject to a significant increase of credit risk (SICR) since

their inception (stage 1 positions), and hence are valued on the basis of a one-year horizon rather than on a lifetime

approach, which was applied under U.S. GAAP. The estimated impact on the condensed combined pro forma

income statement for the year ended 31 December 2022 and the six-month period ended 30 June 2023 is not

material.

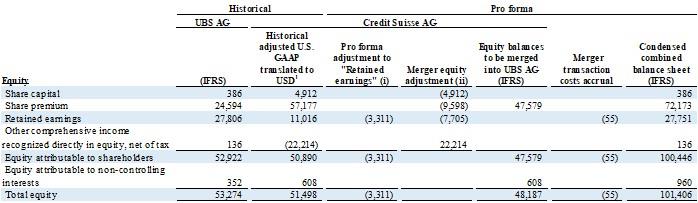

i) The transaction is considered to be a contribution by UBS Group AG of Credit Suisse AG’s business into UBS AG

and, upon the merger, UBS AG recorded an entry in “Share Premium” to reflect the net carrying amount of the

contributed Credit Suisse AG assets and liabilities. The table below summarizes the impact of the pro forma

adjustments on the combined equity of UBS Parent Bank as of 30 June 2023, which include:

i.

Credit Suisse Parent Bank’s historical shareholders’ equity components are adjusted for the pro forma

adjustments made relating to the reclassification and measurement of NCL assets and liabilities (Note 3d)),

recognition of provisions for onerous contracts (Note 3e)), recognition of an additional share award

compensation liability (Note 3f)), recognition of real estate onerous contract provisions (Note 3g)) and

additional credit allowance and credit loss provision (Note 3h)).

ii.

Under the carry over basis, at the time of the Group merger on 31 May 2023, Credit Suisse Parent Bank

balances under “Retained earnings” and “Other comprehensive income recognized directly in equity, net of

tax” are reset to zero and the “Share capital” balance is eliminated, with an offsetting adjustment in “Share

premium” (in line with the accounting applied at the UBS Group AG level for the Group merger).

1.

Reflects the U.S. GAAP balance sheet for Credit Suisse Parent Bank as of 30 June 2023 translated to US dollars at a rate of 1.12 (CHF/USD) and

reflecting UBS Parent Bank’s equity component presentation.

j) All pro forma pre-tax adjustments have been considered and no tax expense or benefit has been recognized in

connection with the pre-tax adjustments in the pro forma condensed combined income statement as it is assumed

that the pre-tax adjustments will either not be recognized for tax purposes, or they will generally relate to entities

with tax losses carried forward that are not recognized as deferred tax assets. Any changes to the pro forma

condensed combined income statement for the year ended 31 December 2022 and for the six-month period ended 30

June 2023 in respect of these entities would, therefore, only affect the amount of their unrecognized tax losses

carried forward and would have no impact on their tax expenses or benefits for the year ended 31 December 2022

and for the six-month period ended 30 June 2023. This assessment includes assumptions and represents UBS Parent

Bank’s best estimate as to the likely tax impacts. The assessment could change as further information becomes

available, including how the entities and businesses in each location will be reorganized, receipt of revised profit

forecasts for those entities, and discussions with the relevant tax authorities.

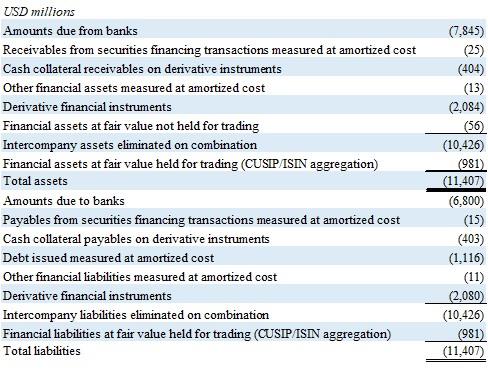

k) UBS Parent Bank has reviewed exposures and transactions with Credit Suisse Parent Bank as of 30 June 2023 and

applied intercompany asset and liability elimination adjustments of 10.4bn as summarized in the table below. UBS

Parent Bank also aggregated the estimated long/short positions in trading securities in both UBS Parent Bank and

Credit Suisse Parent Bank by security (CUSIP/ISIN) and aggregated the positions into a single net asset/liability

amount by individual security. This resulted in a balance sheet asset and liability reduction of 981m as set out in the

table below. Estimated intercompany effects on the income statement are not considered to be material and thus

have not been adjusted.

15

Income statements

l) The pro forma adjustment to personnel expenses is a net decrease of 308m for the year ended 31 December 2022

and a decrease of 418m for the six-month period ended 30 June 2023. These adjustments reflect the following:

i. Aligning Credit Suisse Parent Bank’s annual variable incentive framework and deferral structure with UBS

Parent Bank’s resulted in higher variable compensation expense of 476m in the year ended 31 December

2022. For the six-month period ended 30 June 2023, the actual impact was already reflected under U.S.

GAAP.

ii. Credit Suisse Parent Bank consolidated accounts under U.S. GAAP applied equity settled accounting for

share based payments it settled using shares of its parent rather than its own. Under IFRS, a subsidiary

delivering its parent’s shares is required to treat such schemes as cash settled. In addition, compensation

expense has been retrospectively recalibrated to reflect the estimated impact of a conversion from Credit

Suisse Group AG shares to UBS Group AG shares (leveraging the conversion rate taken for the transaction

in June 2023), with a consequential decrease in share-based compensation expense of 784m for the year

ended 31 December 2022 and 418m for the six-month period ended 30 June 2023. See Note 3f) for the

respective balance sheet impact.

m) The Credit Suisse Parent Bank Swiss pension plan has been accounted for as a defined contribution plan under U.S.

GAAP, and under IFRS will be accounted for as a defined benefit plan. Personnel expenses include an estimated pro

forma adjustment of 42m for the year ended 31 December 2022 to reflect additional expenses recognized under

IFRS with the application of defined benefit plan accounting for the Swiss pension plan. The difference for the six-

month period ended 30 June 2023 is not material. Please note that no corresponding balance sheet adjustment was

required to recognize the pension scheme asset due to the application of the IFRIC 14 “asset ceiling”.

n) Under IFRS, Day 1 gains on financial instruments, after taking account of any valuation adjustments, are recognized

in the income statement only when their fair value is evidenced by an observable market source. A similar restriction

does not exist under U.S. GAAP. On this basis, a debit adjustment of 214m has been recognized in the pro forma

condensed combined income statement for the year ended December 2022 and a debit adjustment of 28m has been

recognized in the six-month period ended 30 June 2023.

16

o) In the third quarter ended 30 September 2023, the management of UBS determined that it intended to sell certain

loans and off-balance sheet loan commitments in its NCL division which resulted in those positions being

remeasured to fair value. This remeasurement gave rise to a reduction in “Other net income from financial

instruments measured at fair value through profit or loss” of 2,307m and an estimated release in credit loss

provisions of 117m, together resulting in an estimated net profit reduction of 2,190m. Refer to Note 3d) for a full

description of this adjustment.

p) General and administrative expenses for the year ended 31 December 2022 contains an accrual for estimated costs

not yet reflected the balance sheet as of 30 June 2023 of 55m to effect the legal merger. Refer to Note 3c) for the

respective balance sheet impact and further detail on this adjustment.

q) Under U.S. GAAP, recycling of own credit gains and losses to the income statement is recognized upon

derecognition of the related financial instrument. Under IFRS there is no recycling to the income statement and the

balances are recognized and remain in retained earnings within equity. An estimated adjustment of 33m for the year

ended December 2022 and 135m for the six-month period ended 30 June 2023 has been made to reverse the gains

recognized in the income statement under U.S. GAAP for the Credit Suisse Parent Bank by charging “Other net

income from financial instruments measured at fair value through profit or loss”.

r) As noted under Note 3e), an expense of 0.7bn has been recognized in “General and administrative expenses” in

connection with the recognition of an onerous contract provision under IFRS.

s) As noted under Note 3g), an expense of 0.2bn has been recognized in “General and administrative expenses” in

connection with the recognition of real estate onerous contract provisions.