Table of Contents

Filed Pursuant to Rule 424(b)(3)

Registration Statement No. 333-156695

| Amendment No. 2 dated August 5, 2010* to PROSPECTUS SUPPLEMENT dated July 6, 2010 (To Prospectus dated January 13, 2009) |

UBS AG 2×Monthly Leveraged Long Exchange Traded Access Securities (E-TRACS) Linked to the Alerian MLP Infrastructure Index due July 9, 2040

UBS AG $100,000,000 E-TRACS

The UBS AG 2×Monthly Leveraged Long Exchange Traded Access Securities (E-TRACS) linked to the Alerian MLP Infrastructure Index (the “Securities”) are senior unsecured debt securities issued by UBS AG (“UBS”) that provide two times leveraged long exposure to the compounded monthly performance of the Alerian MLP Infrastructure Index (the “Index”), reduced by (i) an Accrued Tracking Fee (as described below) based on an Annual Tracking Fee of 0.85% per annum and (ii) the Accrued Financing Charges (as described below). Investing in the Securities involves significant risks.You may lose some or all of your principal at maturity, early redemption, acceleration or upon exercise by UBS of its call right if the compounded leveraged monthly return of the Index (calculated as described herein) is not sufficient to offset the combined negative effect of the Accrued Tracking Fee and the Accrued Financing Charges, and the Redemption Fee Amount, if applicable. In addition, the Securities are two times leveraged with respect to the Index and, as a result, will benefit from two times any beneficial, but will be exposed to two times any adverse, compounded monthly performance of the Index. The Securities may pay a quarterly coupon during their term. You will receive a cash payment at maturity, acceleration or upon exercise by UBS of its call right, based on the compounded leveraged monthly performance of the Index less the Accrued Tracking Fee and the Accrued Financing Charges, as described herein. You will receive a cash payment upon early redemption based on the compounded leveraged monthly performance of the Index less the Accrued Tracking Fee, the Accrued Financing Charges and the Redemption Fee amount. Payment at maturity, upon early redemption, call or acceleration is subject to the creditworthiness of UBS. In addition, the actual and perceived creditworthiness of UBS will affect the market value, if any, of the Securities prior to maturity, call, acceleration or early redemption. The principal terms of the Securities are as follows:

Issuer: | UBS AG (Jersey Branch) |

Initial Trade Date: | July 6, 2010 |

Initial Settlement Date: | July 9, 2010 |

Term: | 30 years, subject to your right to require UBS to redeem your Securities on any Redemption Date, the UBS Call Right or acceleration upon minimum indicative value or intraday index value, each as described below. |

Maturity Date: | July 9, 2040, subject to adjustments |

Denomination/Face Amount: | $25.00 per Security |

Coupon Amount: | For each Security you hold on the applicable Coupon Record Date you will receive on each Coupon Payment Date an amount in cash equal to the Coupon Amount, if any. As further described in “Specific Terms of the Securities — Coupon Payment” beginning on page S-47, the Coupon Amount will equal the sum of the cash distributions that a hypothetical holder of Index constituents would have been entitled to receive in respect of the Index constituents during the relevant period, reduced by the Accrued Tracking Fee. The final Coupon Amount will be included in the Cash Settlement Amount. |

Coupon Payment Date: | The 15th Index Business Day following each Coupon Valuation Date, commencing on October 21, 2010, provided that the final Coupon Payment Date will be the Maturity Date. |

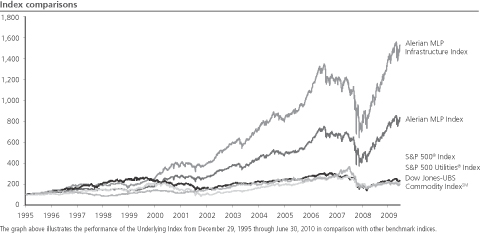

Underlying Index: | The return on the Securities is linked to the performance of the Alerian MLP Infrastructure Index. The Alerian MLP Infrastructure Index provides an enhanced liquid subset of master limited partnerships that includes only midstream energy transportation and storage assets, and selects those companies that are infrastructure hard-asset focused. The Index provides diversified exposure specifically to infrastructure investment. For a detailed description of the Index, see “Alerian MLP Infrastructure Index” beginning on page S-34. |

Payment at Maturity: | For each Security, unless earlier redeemed or called, you will receive at maturity a cash payment equal to (a) the product of (i) the Current Principal Amount and (ii) the Index Factor as of the last Index Business Day in the Final Measurement Period plus (b) the final Coupon Amount, minus (c) the Accrued Tracking Fee as of the last Index Business Day in the Final Measurement Period minus (d) the Accrued Financing Charges as of the last Index Business Day in the Final Measurement Period plus (e) the Stub Reference Distribution Amount as of the last Index Business Day in the Final Measurement Period, if any. We refer to this cash payment as the “Cash Settlement Amount.” If the amount so calculated is less than zero, the payment at maturity will be zero. |

UBS Call Right: | On any Business Day on or after July 11, 2011 through and including the Maturity Date (the “Call Settlement Date”), UBS may at its option redeem all, but not less than all, issued and outstanding Securities. To exercise its Call Right, UBS must provide notice to the holders of the Securities not less than eighteen calendar days prior to the Call Settlement Date. Upon early redemption in the event UBS exercises this right, you will receive a cash payment equal to the Call Settlement Amount, which will be calculated as described herein and paid on the Call Settlement Date. If the amount so calculated is less than zero, the payment upon exercise of the Call Right will be zero. |

| UBS Investment Bank | (cover continued on next page) |

Prospectus Supplement dated August 5, 2010

Table of Contents

Redemption Amount: | Subject to your compliance with the procedures described under “Specific Terms of the Securities — Weekly Early Redemption at the Option of the Holders,” upon early redemption, you will receive per Security a cash payment on the relevant Redemption Date equal to (a) the product of (i) the Current Principal Amount and (ii) the Index Factor as of the Redemption Valuation Date plus (b) the Coupon Amount with respect to the Coupon Valuation Date immediately preceding the Redemption Valuation Date if on the Redemption Valuation Date the Coupon Ex-Date with respect to such Coupon Amount has not yet occurred, plus (c) the Adjusted Coupon Amount, if any, minus (d) the Adjusted Tracking Fee Shortfall, if any, as of the Redemption Valuation Date, minus (e) the Accrued Financing Charges as of the Redemption Valuation Date minus (f) the Redemption Fee Amount. We refer to this cash payment as the “Redemption Amount.” For purposes of calculating the Redemption Amount, either the Adjusted Coupon Amount will be included or the Adjusted Tracking Fee Shortfall will be subtracted, but not both. |

Redemption Fee Amount: | The product of (a) 0.125%, (b) the Current Principal Amount and (c) the Index Factor as of the Redemption Valuation Date. |

Call Settlement Amount: | In the event UBS exercises its Call Right, you will receive per Security a cash payment on the relevant Call Settlement Date equal to (a) the product of (i) the Current Principal Amount and (ii) the Index Factor as of the last Index Business Day in the Call Measurement Period plus (b) the Coupon Amount with respect to the Coupon Valuation Date immediately preceding the Call Valuation Date if on the last Index Business Day in the Call Measurement Period the Coupon Ex-Date with respect to such Coupon Amount has not yet occurred, plus (c) the Adjusted Coupon Amount, if any, minus (d) the Accrued Tracking Fee as of the last Index Business Day in the Call Measurement Period, minus (e) the Accrued Financing Charges as of the last Index Business Day in the Call Measurement Period plus (f) the Stub Reference Distribution Amount as of the last Index Business Day in the Call Measurement Period, if any. We refer to this cash payment as the “Call Settlement Amount.” |

Acceleration upon Minimum Indicative Value or Intraday Index Value: | If, at any time, (1) the indicative value on any Index Business Day equals $5.00 or less or (2) the intraday index value on any Index Business Day decreases 30% from the most recent Monthly Initial Closing Level (each such day, an “Acceleration Date”), all issued and outstanding Securities will be automatically accelerated and mandatorily redeemed by UBS (even if the indicative value would later exceed $5.00 or the intraday index value would increase from the -30% level on such Acceleration Date or any subsequent Index Business Day) for a cash payment equal to the Acceleration Amount. The “Acceleration Amount” will equal (a) the product of (i) the Current Principal Amount and (ii) the Index Factor as of the last Index Business Day in the Acceleration Valuation Period plus (b) the Coupon Amount with respect to the Coupon Valuation Date immediately preceding the Acceleration Date if on the last Index Business Day in the Acceleration Valuation Period the Coupon Ex-Date with respect to such Coupon Amount has not yet occurred, plus (c) the Adjusted Coupon Amount, if any, minus (d) the Accrued Tracking Fee as of the last Index Business Day in the Acceleration Valuation Period, minus (e) the Accrued Financing Charges as of the last Index Business Day in the Acceleration Valuation Period plus (f) the Stub Reference Distribution Amount as of the last Index Business Day in the Acceleration Valuation Period, if any. If the minimum indicative value or intraday index value threshold has been breached, you will receive on the Acceleration Settlement Date only the Acceleration Amount in respect of your investment in the Securities. The “Acceleration Settlement Date” will be the third Business Day following the last Index Business Day of the Acceleration Valuation Period. |

Index Factor: | 1 + (2 × Index Performance Ratio) |

Index Performance Ratio: | On any Index Business Day during the Final Measurement Period, the Acceleration Valuation Period or the Call Measurement Period, or on any Redemption Valuation Date, as applicable: |

Final VWAP Level – Monthly Initial Closing Level

Monthly Initial Closing Level

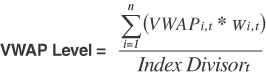

VWAP: | With respect to each Index constituent, as of any date of determination, the volume-weighted average price of one unit of such Index constituent as determined by the VWAP Calculation Agent based on the Primary Exchange for each Index constituent. |

Final VWAP Level: | As determined by the VWAP Calculation Agent, the arithmetic mean of the VWAP Levels measured on each Index Business Day during the Final Measurement Period, the Acceleration Valuation Period or the Call Measurement Period, or the VWAP Level on any Redemption Valuation Date, as applicable. |

VWAP Level: | On any Index Business Day, as calculated by the VWAP Calculation Agent, (1) the sum of the products of (i) the VWAP of each Index constituent as of such date and (ii) the published share weighting of that Index constituent as of such date, divided by (2) the Index Divisor as of such date. |

Current Principal Amount: | For the period from the Initial Settlement Date to July 30, 2010 (such period, the “initial calendar month”), the Current Principal Amount will equal $25.00 per Security. For each subsequent calendar month, the Current Principal Amount for each Security will be reset as follows on the Monthly Reset Date: |

New Current Principal Amount =previous Current Principal Amount × Monthly Reset Factor on the applicable Monthly Valuation Date – Accrued Financing Charges on the applicable Monthly Valuation Date

Monthly Reset Factor: | 1 + (2 × Monthly Performance Ratio) |

(cover continued on next page)

Table of Contents

Monthly Performance Ratio: | On any Monthly Valuation Date: |

Index Closing Level – Monthly Initial Closing Level

Monthly Initial Closing Level

Monthly Initial Closing Level: | For the initial calendar month, 497.89, the Index Closing Level on July 6, 2010 as reported on the NYSE and Bloomberg L.P. For each subsequent calendar month, the Monthly Initial Closing Level on the Monthly Reset Date equals the Index Closing Level on the Monthly Valuation Date for the previous calendar month. |

Index Closing Level: | The closing level of Index as reported on the NYSE and Bloomberg L.P. |

Security Calculation Agent: | UBS Securities LLC |

VWAP Calculation Agent: | NYSE |

Calculation Date: | June 28, 2040, unless such day is not an Index Business Day, in which case the Calculation Date will be the next Index Business Day, subject to adjustments. |

Listing: | The Securities have been approved for listing on NYSE Arca under the symbol “MLPL.” If an active secondary market develops, we expect that investors will purchase and sell the Securities primarily in this secondary market. |

CUSIP Number: | 902664200 |

ISIN Number: | US9026642002 |

Additional Key Terms: | See “Prospectus Supplement Summary – Additional Key Terms” on page S-7. |

See “Risk Factors” beginning on page S-21 for additional risks related to an investment in the Securities.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus supplement or the accompanying prospectus. Any representation to the contrary is a criminal offense.

On the Initial Trade Date, we sold $10,000,000 face amount of Securities to UBS Securities LLC at 100% of their aggregate face amount. From time to time after the Initial Trade Date, either UBS Securities LLC or UBS Financial Services Inc. may sell a portion of those Securities at market prices prevailing at the time of sale, at prices related to market prices or at negotiated prices. Additionally, after the Initial Trade Date, UBS Securities LLC, UBS Financial Services Inc. and dealers purchasing as principal may sell the Securities for a price equal to their current Issuance Amount, as calculated by UBS Securities LLC as of the date of such sale. “Issuance Amount” means a value at a given date equal to (i) the Current Principal Amount multiplied by the Index Factor, assuming such date is the Redemption Valuation Date, less (ii) the Adjusted Tracking Fee Shortfall, if any, as of such date, assuming such date is the Redemption Valuation Date, minus (iii) the Accrued Financing Charges as of such date, assuming such date is the Redemption Valuation Date, plus (iv) assuming such date is the Redemption Valuation Date, the Coupon Amount with respect to the Coupon Valuation Date if on such Redemption Valuation Date the Coupon Ex-Date with respect to such Coupon Amount has not yet occurred plus (v) the Adjusted Coupon Amount, if any, as of such date. We will receive proceeds in each such sale equal to the Issuance Amount multiplied by the number of Securities sold. Neither UBS Securities LLC nor UBS Financial Services Inc. will receive any commission in connection with any of the sales described above. Please see “Supplemental Plan of Distribution” on page S-75 for more information.

We may use this prospectus supplement in the initial sale of the Securities. In addition, UBS Securities LLC or another of our affiliates may use this prospectus supplement in market-making transactions in any Securities after their initial sale.Unless we or our agent informs you otherwise in the confirmation of sale or in a notice delivered at the same time as the confirmation of sale, this prospectus supplement is being used in a market-making transaction.

The Securities are not deposit liabilities of UBS AG and are not FDIC insured.

| * | This Amendment No. 2, dated August 5, 2010 to the prospectus supplement dated July 6, 2010 (as amended, the ‘‘prospectus supplement’’) is being filed for the purpose of updating (i) the Index historical data presented under “Alerian MLP Infrastructure Index – Historical and Estimated Historical Performance” and (ii) the definition of “Financing Level” on pages S-2 and S-50. Otherwise, all terms of the Securities remain as stated in the prospectus supplement. |

Table of Contents

The UBS AG 2×Monthly Leveraged Long Exchange Traded Access Securities (E-TRACS) being offered as described in this prospectus supplement and the accompanying prospectus constitute one offering in a series of offerings of UBS AG E-TRACS exchange-traded notes. We are offering and may continue to offer from time to time E-TRACS linked to different underlying indices and with the same or different terms and conditions, relative to those set forth in this prospectus supplement. You should be sure to refer to the prospectus supplement for the particular offering of E-TRACS in which you are considering an investment.

This prospectus supplement contains the specific financial and other terms that apply to the securities being offered herein. Terms that apply generally to all our Medium-Term Notes, Series A, are described under “Description of Debt Securities We May Offer” in the accompanying prospectus. The terms described here (i.e., in this prospectus supplement) modify or supplement those described in the accompanying prospectus and, if the terms described here are inconsistent with those described there, the terms described here are controlling. The contents of any website referred to in this prospectus supplement are not incorporated by reference in this prospectus supplement or the accompanying prospectus.

You should rely only on the information incorporated by reference or provided in this prospectus supplement or the accompanying prospectus. We have not authorized anyone to provide you with different information. We are not making an offer of these Securities in any state where the offer is not permitted. You should not assume that the information in this prospectus supplement is accurate as of any date other than the date on the front of the document.

Prospectus Supplement

| Prospectus Supplement Summary | S-1 | |

| Hypothetical Examples | S-15 | |

| Risk Factors | S-21 | |

| Alerian MLP Infrastructure Index | S-34 | |

| Valuation of the Index and the Securities | S-43 | |

| Specific Terms of the Securities | S-46 | |

| Use of Proceeds and Hedging | S-66 | |

| Certain U.S. Federal Income Tax Consequences | S-67 | |

| Benefit Plan Investor Considerations | S-73 | |

| Supplemental Plan of Distribution | S-75 | |

| S-75 | ||

| Prospectus | ||

| Introduction | 1 | |

| Cautionary Note Regarding Forward-Looking Information | 3 | |

| Incorporation of Information About UBS AG | 4 | |

| Where You Can Find More Information | 5 | |

| Presentation of Financial Information | 6 | |

| Ratio of Earnings to Fixed Charges | 6 | |

| Limitations on Enforcement of U.S. Laws Against UBS AG, Its Management and Others | 7 | |

| Capitalization of UBS | 7 | |

| UBS | 8 | |

| Use of Proceeds | 10 | |

| Description of Debt Securities We May Offer | 11 | |

| Description of Warrants We May Offer. | 33 | |

| Legal Ownership and Book-Entry Issuance | 49 | |

| Considerations Relating to Indexed Securities | 54 | |

| Considerations Relating to Securities Denominated or Payable in or Linked to a Non-U.S. Dollar Currency | 57 | |

| U.S. Tax Considerations | 60 | |

| Tax Considerations Under the Laws of Switzerland | 71 | |

| Benefit Plan Investor Considerations | 73 | |

| Plan of Distribution | 75 | |

| Validity of the Securities | 78 | |

| Experts | 78 |

i

Table of Contents

The following is a summary of terms of the Securities, as well as a discussion of factors you should consider before purchasing the Securities. The information in this section is qualified in its entirety by the more detailed explanations set forth elsewhere in this prospectus supplement and in the accompanying prospectus. Please note that references to “UBS,” “we,” “our” and “us” refer only to UBS AG and not to its consolidated subsidiaries.

What are the Securities?

The Securities are senior unsecured medium-term notes issued by UBS with a two times leveraged return linked to the compounded monthly performance of the Alerian MLP Infrastructure Index. If the Indexincreases over any calendar month (a “beneficial monthly performance”), the return on the Index for the Securities willincrease by two times the movement of the Index. If the Indexdecreases over any calendar month (an “adverse monthly performance”), the return on the Index for the Securities willdecrease by two times the movement of the Index.

The Alerian MLP Infrastructure Index provides an enhanced liquid subset of master limited partnerships that includes only midstream energy transportation and storage assets, and selects those companies that are infrastructure hard-asset focused. The Index provides diversified exposure specifically to infrastructure investment. The Index is a proprietary index. For a detailed description of the Index, see “Alerian MLP Infrastructure Index” beginning on page S-34.

We refer to the master limited partnerships (MLPs) included in the Alerian MLP Infrastructure Index as the “Index constituents.”

The Securities seek to approximate the monthly returns that might be available to investors through a leveraged “long” investment in the equity securities of the Index constituents. A leveraged “long” investment strategy involves the practice of borrowing money from a third party lender at an agreed-upon rate of interest and using the borrowed money together with investor capital to purchase assets (e.g., equity securities). A leveraged long investment strategy terminates with the sale of the underlying assets and repayment of the third party lender, provided that the proceeds of the sale of underlying assets are sufficient to repay the loan. By implementing a leveraged strategy, the leveraged investor seeks to benefit from an anticipated increase in the value of the assets between the purchase and sale of such assets, and assumes that the increase in value of the underlying assets will exceed the cumulative interest due to the third party lender over the term of the loan. A leveraged investor will incur a loss if the value of the assets does not increase sufficiently to cover payment of the interest. In order to seek to replicate a leveraged “long” investment strategy in the equity securities of the Index constituents, the Securities provide that each $25 invested by investors on the Initial Trade Date is leveraged through a notional loan of $25 on the Initial Trade Date. Investors are thus considered to have notionally borrowed $25, which, together with the $25 invested, represents a notional investment of $50 in the equity securities of the Index constituents on the Initial Trade Date. During the term of your Securities, the leveraged portion of the notional investment, which will be equal to the Current Principal Amount, accrues financing charges for the benefit of UBS referred to as “accrued financing charges,” which seek to represent the monthly amount of interest that leveraged investors might incur if they sought to borrow funds at a similar rate from a third-party lender. Upon maturity, call, acceleration or redemption, the investment in the equity securities of the Index constituents is notionally sold at the then-current values of the equity securities, and the investor then notionally repays UBS an amount equal to the principal of the notional loan plus accrued interest. The payment at maturity, call, acceleration or redemption under the Securities, therefore, generally represents the profit or loss that the investor would receive by applying a leveraged “long” investment strategy, after taking into account, and making assumptions for, the accrued financing charges that are commonly present in such leveraged “long” investment strategies. In order to mitigate the risk to UBS that the value of the equity securities of the Index constituents is not sufficient to repay

S-1

Table of Contents

the principal and accrued financing charges of the notional loan, an automatic early termination of the Securities is provided for under the “Acceleration upon Minimum Indicative Value or Intraday Index Value” provisions hereunder.

Financing Level: On the Initial Trade Date, the Financing Level for each Security will equal $25. On any subsequent Monthly Valuation Date after the first Monthly Valuation Date, the Financing Level for each Security will equal the Current Principal Amount on the immediately following Monthly Reset Date.

Accrued Financing Charges: On the Initial Trade Date, the Accrued Financing Charges for each Security will equal $0. On any subsequent Monthly Valuation Date, the Accrued Financing Charges for each Security will equal the product of (i) the Financing Level on the immediately preceding Monthly Valuation Datetimes(ii) the Financing Ratetimes(iii) the number of calendar days from, but excluding, the immediately preceding Monthly Valuation Date to, and including, the then current Monthly Valuation Datedivided by (iv) 360. The Accrued Financing Charges as of the last Index Business Day in the Final Measurement Period, the Call Measurement Period or the Acceleration Valuation Period, or as of the Redemption Valuation Date, as applicable, is an amount equal to the product of (i) the Financing Level on the immediately preceding Monthly Valuation Date times (ii) the Financing Rate times (iii) the number of calendar days from, but excluding, the immediately preceding Monthly Valuation Date to, and including, such last Index Business Day in the Final Measurement Period, the Call Measurement Period or the Acceleration Valuation Period, or the Redemption Valuation Date, as applicable, divided by (iv) 360.

The accrued financing charges seek to compensate UBS for providing investors with the potential to receive a leveraged participation in movements in the Index Closing Level of the Index and are intended to approximate the financing costs that investors may have otherwise incurred had they sought to borrow funds at a similar rate from a third party to invest in the Securities. These charges accrue and compound on a daily basis during the applicable period.

Financing Rate:The Financing Rate will equal the London interbank offered rate (British Banker’s Association) for three-month deposits in U.S. Dollars, which is displayed on Reuters page LIBOR01 (or any successor service or page for the purpose of displaying the London interbank offered rates of major banks, as determined by the Security Calculation Agent), as of 11:00 a.m., London time, on the day that is two London business days prior to the immediately preceding Monthly Valuation Date. “London business day” means each Monday, Tuesday, Wednesday, Thursday and Friday that is not a day on which banking institutions in London generally are authorized or obligated by law, regulation or executive order to close and is also a day on which dealings in U.S. dollars are transacted in the London interbank market.

The Securities do not guarantee any return of principal at, or prior to, maturity or call, or upon early redemption or acceleration. Instead, at maturity, you will receive a cash payment equal to (a) the product of (i) the Current Principal Amount and (ii) the Index Factor as of the last Index Business Day in the Final Measurement Period plus (b) the final Coupon Amount minus (c) the Accrued Tracking Fee as of the last Index Business Day in the Final Measurement Period, minus (d) the Accrued Financing Charges as of the last Index Business Day in the Final Measurement Period plus (e) the Stub Reference Distribution Amount as of the last Index Business Day in the Final Measurement Period, if any. We refer to this cash payment as the “Cash Settlement Amount.” If the amount calculated above is less than zero, the payment at maturity will be zero.You may lose some or all of your investment at maturity. Because the Accrued Tracking Fee (including any Tracking Fee Shortfall (as defined below)) and the Accrued Financing Charges reduce your final payment, the compounded leveraged monthly return of the Index will need to be sufficient to offset the combined negative effect of the Accrued Tracking Fee and the Accrued Financing Charges over the relevant period, less any Coupon Amounts, any Stub Reference Distribution Amount and/or Adjusted Coupon Amount, as applicable, in order for you to receive an

S-2

Table of Contents

aggregate amount over the term of the Securities equal to your initial investment in the Securities. If thecompounded leveraged monthly return of the Index is insufficient to offset such a negative effect, or if the compounded leveraged monthly return of the Index is negative, you will lose some or all of your investment at maturity. See “Specific Terms of the Securities — Cash Settlement Amount at Maturity” beginning on page S-49.

As a result of compounding, the performance of the Securities for periods greater than one month is likely to be either greater than or less than two times the performance of the Index, before accounting for the Accrued Tracking Fee and the Accrued Financing Charges.

In addition, because the Current Principal Amount is reset each month and is subject to the Accrued Tracking Fee and the Accrued Financing Charges, the Securities do not offer a return based on the simpleperformance of the Index from the Initial Settlement Date to the Maturity Date.Instead, the amount you receive at maturity or call, or upon early redemption or acceleration, will be contingent upon the compounded monthly performance of the Index during the term of the Securities, subject to the combined negative effect of the Accrued Tracking Fee and the Accrued Financing Charges. Accordingly, even if over the term of the Securities, the Index has demonstrated an overall beneficial performance (i.e., the Index increases), there is no guarantee that you will receive at maturity or call, or upon early redemption or acceleration, your initial investment back or any return on that investment. This is because the amount you receive at maturity or call, or upon an early redemption or acceleration, depends on how the Index has performed in each month on a compounded, leveraged basis prior to maturity or call, or upon an early redemption or acceleration, and consequently, how the Current Principal Amount has been reset in each month. In particular, significant adverse monthly performances for your Securities may not be offset by any beneficial monthly performances of the same magnitude.

The amount of your payment upon maturity, redemption, call or acceleration will depend, in part, upon the level of the Index. However, positive or negative monthly changes in the Index Closing Level, or the Final VWAP Level, will not solely determine the return on your Securities due to the combined effects of leverage, monthly compounding and any applicable fees and financing charges.

For the period from the Initial Settlement Date to July 30, 2010 (such period, the “initial calendar month”), the Current Principal Amount will equal $25.00 per Security. For each subsequent calendar month, the Current Principal Amount for each Security will be reset as follows on the Monthly Reset Date:

New Current Principal Amount =previous Current Principal Amount × Monthly Reset Factor on the applicable Monthly Valuation Date – Accrued Financing Charges on the applicable Monthly Valuation Date

The Monthly Reset Factor will be calculated as follows:

1 + (2 × Monthly Performance Ratio)

The Monthly Performance Ratio will be calculated as follows:

| Index Closing Level – Monthly Initial Closing Level |

Monthly Initial Closing Level |

where the “Monthly Initial Closing Level” for the initial calendar month is 497.89, the Index Closing Level on July 6, 2010. For each subsequent calendar month, the Monthly Initial Closing Level will equal the Index Closing Level on the Monthly Valuation Date for the previous calendar month.

S-3

Table of Contents

The Index Factor will be calculated as follows:

1 + (2 × Index Performance Ratio)

The Index Performance Ratio on any Index Business Day during the Final Measurement Period, the Acceleration Valuation Period or the Call Measurement Period, or any Redemption Valuation Date, as applicable, will be calculated as follows:

| Final VWAP Level – Monthly Initial Closing Level |

Monthly Initial Closing Level |

The “Final Measurement Period” is the five Index Business Days from and including the Calculation Date, subject to adjustment as described under “Specific Terms of the Securities — Market Disruption Event” beginning on page S-58.

How and why is the Current Principal Amount reset?

Initially, the Current Principal Amount is equal to $25 per Security. At the start of each subsequent calendar month, the Current Principal Amount is reset by applying the Monthly Reset Factor to, and subtracting the Accrued Financing Charges for the immediately preceding month from, the previous Current Principal Amount.

For example, if for August the Current Principal Amount is $20 and the Monthly Reset Factor is equal to 0.90, the Current Principal Amount for September will equal $20 times 0.90 minus the Accrued Financing Charges for August. Subsequently, the Monthly Reset Factor and Accrued Financing Charges for September will be applied to the Current Principal Amount for September to derive the Current Principal Amount for October.

The Current Principal Amount is reset each calendar month to ensure that a consistent degree of leverage is applied to any performance of the Index. If the Current Principal Amount is reduced by an adverse monthly performance, the Monthly Reset Factor of any further adverse monthly performance will lead to a smaller dollar loss when applied to that reduced Current Principal Amount than if the Current Principal Amount were not reduced. Equally, however, if the Current Principal Amount increases, the dollar amount lost for a certain level of adverse monthly performance will increase correspondingly.

Resetting the Current Principal Amount also means that the dollar amount which may be gained from any beneficial monthly performance will be contingent upon the Current Principal Amount. If the Current Principal Amount is above $25, then any beneficial monthly performance will result in a gain of a larger dollar amount than would be the case if the Current Principal amount were reduced below $25. Conversely, as the Current Principal Amount is reduced towards zero, the dollar amount to be gained from any beneficial monthly performance will decrease correspondingly.

See “Specific Terms of the Securities — Cash Settlement Amount at Maturity” beginning on page S-49.

Coupon Amounts

For each Security you hold on the applicable Coupon Record Date, you will receive on each Coupon Payment Date an amount in cash equal to the difference between the Reference Distribution Amount, calculated as of the corresponding Coupon Valuation Date, and the Accrued Tracking Fee, calculated as of the corresponding Coupon Valuation Date (the “Coupon Amount”). To the extent the Reference Distribution Amount on a Coupon Valuation Date is less than the Accrued Tracking Fee on the corresponding Coupon Valuation Date, there will be no Coupon Amount payment made on the corresponding Coupon Payment Date, and an amount equal to the difference between the Accrued

S-4

Table of Contents

Tracking Fee and the Reference Distribution Amount (the “Tracking Fee Shortfall”) will be included in the Accrued Tracking Fee for the next Coupon Valuation Date. This process will be repeated to the extent necessary until the Reference Distribution Amount for a Coupon Valuation Date is greater than the Accrued Tracking Fee for the corresponding Coupon Valuation Date. If there is a Tracking Fee Shortfall as of the last Coupon Valuation Date, that amount will be taken into account in determining the Cash Settlement Amount. See “Specific Terms of the Securities — Coupon Payment” beginning on page S-47.

Unlike ordinary debt securities, the Securities do not guarantee any return of principal at maturity or call, or upon early redemption or acceleration. You may lose some or all of your initial investment. In addition, you are not guaranteed any coupon payment.

For a further description of how your payment at maturity or call, or upon early redemption or acceleration, will be calculated, see “Specific Terms of the Securities — Cash Settlement Amount at Maturity,” “—UBS’s Call Right,” “— Weekly Early Redemption at the Option of the Holders” and “—Acceleration upon Minimum Indicative Value” beginning on page S-55.

Weekly Early Redemption

You may elect to require UBS to redeem your Securities, in whole or in part, once a week prior to the Maturity Date commencing on July 19, 2010 through and including the final Redemption Date, subject to a minimum redemption amount of at least 50,000 Securities. If you redeem your Securities, you will receive a cash payment equal to the Redemption Amount, as defined below. You must comply with the redemption procedures described below in order to redeem your Securities. To satisfy the minimum redemption amount, your broker or other financial intermediary may bundle your Securities for redemption with those of other investors to reach this minimum amount of 50,000 Securities. We may from time to time in our sole discretion reduce this minimum requirement in whole or in part. Any such reduction will be applied on a consistent basis for all holders of the Securities at the time the reduction becomes effective.

Upon early redemption, you will receive per Security a cash payment on the relevant Redemption Date equal to (a) the product of (i) the Current Principal Amount and (ii) the Index Factor as of the Redemption Valuation Date plus (b) the Coupon Amount with respect to the Coupon Valuation Date immediately preceding the Redemption Valuation Date if on the Redemption Valuation Date the Coupon Ex-Date with respect to such Coupon Amount has not yet occurred, plus (c) the Adjusted Coupon Amount, if any, minus (d) the Adjusted Tracking Fee Shortfall, if any, as of the Redemption Valuation Date, minus (e) the Accrued Financing Charges as of the Redemption Valuation Date minus (f) the Redemption Fee Amount. We refer to this cash payment as the “Redemption Amount.” For purposes of calculating the Redemption Amount, either the Adjusted Coupon Amount will be included or the Adjusted Tracking Fee Shortfall will be subtracted, but not both. If the amount calculated above is less than zero, the payment upon early redemption will be zero.You may lose some or all of your investment upon early redemption. Because the Accrued Tracking Fee, Adjusted Tracking Fee Shortfall, if any, the Accrued Financing Charges and the Redemption Fee Amount reduce your final payment, the compounded leveraged monthly return of the Index will need to be sufficient to offset the combined negative effect of the Accrued Tracking fee, Adjusted Tracking Fee Shortfall, if any, the Accrued Financing Charges and the Redemption Fee Amount, less any Coupon Amounts, any Stub Reference Distribution Amount, as applicable, and/or any Adjusted Coupon Amount, in order for you to receive an aggregate amount over the term of the Securities equal to your initial investment in the Securities. If the compounded leveraged monthly return of the Index is insufficient to offset such a negative effect or if the compounded leveraged monthly return of the Index is negative, you will lose some or all of your investment upon early redemption. See “Specific Terms of the Securities —Weekly Early Redemption at the Option of the Holders” beginning on page S-51 and “— Redemption Procedures” beginning on page S-53.

S-5

Table of Contents

Redemption Valuation Date: The last Business Day of each week, generally Friday. This day is also the first Index Business Day following the date that a Redemption Notice and Redemption Confirmation, each as described under “Specific Terms of the Securities — Weekly Early Redemption at the Option of the Holders — Redemption Requirements,” are delivered. Any applicable Redemption Valuation Date is subject to adjustment as described under “Specific Terms of the Securities — Market Disruption Event.”

Adjusted Coupon Amount: With respect to any applicable Redemption Valuation Date or Call Valuation Date, as applicable, a coupon payment, if any, in an amount in cash equal to the difference between the Adjusted Reference Distribution Amount, calculated as of the applicable Redemption Valuation Date or Call Valuation Date, as applicable, and the Adjusted Tracking Fee, calculated as of such Redemption Valuation Date or Call Valuation Date, to the extent that the Adjusted Reference Distribution Amount, calculated as of such Redemption Valuation Date or Call Valuation Date, is greater than or equal to the Adjusted Tracking Fee, calculated as of such Redemption Valuation Date or Call Valuation Date.

Redemption Procedures

To redeem your Securities prior to the Maturity Date, you must instruct your broker to deliver a Redemption Notice to UBS by email no later than 12:00 noon (New York City time) on the Business Day immediately preceding the applicable Redemption Valuation Date and you and your broker must follow the procedures described herein. If you fail to comply with these procedures, your notice will be deemed ineffective. See also “Description of the Debt Securities We May Offer — Redemption and Payment” in the accompanying prospectus.

UBS’s Call Right

On any Business Day on or after July 11, 2011 through and including the Maturity Date (the “Call Settlement Date”), UBS may at its option redeem all, but not less than all, issued and outstanding Securities. To exercise its Call Right, UBS must provide notice to the holders of the Securities not less than eighteen calendar days prior to the Call Settlement Date specified by UBS. In the event UBS exercises this right, you will receive a cash payment equal to (a) the product of (i) the Current Principal Amount and (ii) the Index Factor as of the last Index Business Day in the Call Measurement Period plus (b) the Coupon Amount with respect to the Coupon Valuation Date immediately preceding the Call Valuation Date if on the last Index Business Day in the Call Measurement Period the Coupon Ex-Date with respect to such Coupon Amount has not yet occurred, plus (c) the Adjusted Coupon Amount, if any, minus (d) the Accrued Tracking Fee as of the last Index Business Day in the Call Measurement Period, minus (e) the Accrued Financing Charges as of the last Index Business Day in the Call Measurement Period plus (f) the Stub Reference Distribution Amount as of the last Index Business Day in the Call Measurement Period, if any. We refer to this cash payment as the “Call Settlement Amount.” If UBS issues a call notice on any calendar day, the “Call Valuation Date” will be the last Business Day of the week following the week in which the call notice is issued, generally Friday, subject to a minimum five calendar day period commencing on the date of the issuance of the call notice and ending on the related Call Valuation Date. If UBS issues a call notice on a Friday, the related Call Valuation Date will fall on the following Friday. The Call Settlement Date will be the third Business Day following the last Index Business Day in the Call Measurement Period.

Call Measurement Period: The five Index Business Days from and including the Call Valuation Date, subject to adjustment as described under “Specific Terms of the Securities — Market Disruption Event.”

S-6

Table of Contents

Acceleration Upon Minimum Indicative Value or Intraday Index Value

If, at any time, (1) the indicative value on any Index Business Day equals $5.00 or less or (2) the intraday index value on any Index Business Day decreases 30% from the most recent Monthly Initial Closing Level (each such day, an “Acceleration Date”), all issued and outstanding Securities will be automatically accelerated and mandatorily redeemed by UBS (even if the indicative value would later exceed $5.00 or the intraday index value would increase from the -30% level on such Acceleration Date or any subsequent Index Business Day) for a cash payment equal to the Acceleration Amount. The “Acceleration Amount” will equal (a) the product of (i) the Current Principal Amount and (ii) the Index Factor as of the last Index Business Day in the Acceleration Valuation Period plus (b) the Coupon Amount with respect to the Coupon Valuation Date immediately preceding the Acceleration Date if on the last Index Business Day in the Acceleration Valuation Period the Coupon Ex-Date with respect to such Coupon Amount has not yet occurred, plus (c) the Adjusted Coupon Amount, if any, minus (d) the Accrued Tracking Fee as of the last Index Business Day in the Acceleration Valuation Period, minus (e) the Accrued Financing Charges as of the last Index Business Day in the Acceleration Valuation Period plus (f) the Stub Reference Distribution Amount as of the last Index Business Day in the Acceleration Valuation Period, if any. If the minimum indicative value or intraday index value threshold has been breached, you will receive on the Acceleration Settlement Date only the Acceleration Amount in respect of your investment in the Securities. The “Acceleration Settlement Date” will be the third Business Day following the last Index Business Day of the Acceleration Valuation Period. The “Acceleration Valuation Period” will be the five Index Business Days from but excluding the Acceleration Date, subject to adjustment as described under “Specific Terms of the Securities — Market Disruption Event.” UBS must provide notice to the holders of the Securities that the minimum indicative value or intraday index value threshold has been breached not less than five calendar days prior to the Acceleration Settlement Date. For a detailed description of how the intraday indicative value of the Securities is calculated see “Valuation of the Index and the Securities – Intraday Security Values.”

Additional Key Terms

Annual Tracking Fee: | As of any date of determination, an amount per Security equal to the product of (i) 0.85% per annum and (ii) the Current Indicative Value as of the immediately preceding Index Business Day. |

Accrued Tracking Fee: | (1) | The Accrued Tracking Fee with respect to the first Coupon Valuation Date is an amount equal to the product of |

| (a) | the Annual Tracking Fee as of the first Coupon Valuation Date and |

| (b) | a fraction, the numerator of which is the total number of calendar days from and excluding the Initial Trade Date to and including the first Coupon Valuation Date, and the denominator of which is 365. |

| (2) | The Accrued Tracking Fee with respect to any Coupon Valuation Date other than the first Coupon Valuation Date is an amount equal to |

| (a) | the product of (i) the Annual Tracking Fee as of such Coupon Valuation Date and (ii) a fraction, the numerator of which is the total number of calendar days from and excluding the immediately preceding Coupon Valuation Date to and including such Coupon Valuation Date, and the denominator of which is 365, plus |

| (b) | the Tracking Fee Shortfall as of the immediately preceding Coupon Valuation Date, if any. |

See “Specific Terms of the Securities — Coupon Payment” beginning on page S-47.

S-7

Table of Contents

| (3) | The Accrued Tracking Fee as of the last Index Business Day in the Final Measurement Period is an amount equal to |

| (a) | the product of (i) the Annual Tracking Fee calculated as of the last Index Business Day in the Final Measurement Period and (ii) a fraction, the numerator of which is the total number of calendar days from and excluding the Calculation Date to and including the last Index Business Day in the Final Measurement Period, and the denominator of which is 365, plus |

| (b) | the Tracking Fee Shortfall as of the last Coupon Valuation Date, if any. |

See “Specific Terms of the Securities — Cash Settlement Amount at Maturity” beginning on page S-49.

| (4) | The Accrued Tracking Fee as of the last Index Business Day in the Call Measurement Period is an amount equal to |

| (a) | the product of (i) the Annual Tracking Fee calculated as of the last Index Business Day in the Call Measurement Period and (ii) a fraction, the numerator of which is the total number of calendar days from and excluding the Call Valuation Date to and including the last Index Business Day in the Call Measurement Period, and the denominator of which is 365, plus |

| (b) | the Adjusted Tracking Fee Shortfall, if any. |

See “Specific Terms of the Securities — UBS’s Call Right” beginning on page S-54.

| (5) | The Accrued Tracking Fee as of the last Index Business Day in the Acceleration Valuation Period is an amount equal to |

| (a) | the product of (i) the Annual Tracking Fee calculated as of the last Index Business Day in the Acceleration Valuation Period and (ii) a fraction, the numerator of which is the total number of calendar days from and excluding the Acceleration Date to and including the last Index Business Day in the Acceleration Measurement Period, and the denominator of which is 365, plus |

| (b) | the Adjusted Tracking Fee Shortfall, if any. |

See “Specific Terms of the Securities — Acceleration upon Minimum Indicative Value or Intraday Index Value” beginning on page S-55.

Adjusted Reference Distribution Amount: | As of any Redemption Valuation Date, the Call Valuation Date or the Acceleration Date, as applicable, an amount equal to the gross cash distributions that a Reference Holder would have been entitled to receive in respect of the Index constituents held by such Reference Holder on the “record date” with respect to any Index constituent for those cash distributions whose “ex-dividend date” occurs during the period from and excluding the immediately preceding Coupon Valuation Date (or if the Redemption Valuation Date occurs prior to the first Coupon Valuation Date, the period from and excluding the Initial Trade Date) to and including such Redemption Valuation Date, the Call Valuation Date or the Acceleration Date. |

Adjusted Tracking Fee: | As of any Redemption Valuation Date, the Call Valuation Date, or the Acceleration Date, as applicable, an amount equal to (a) the Tracking Fee Shortfall as of the immediately preceding Coupon Valuation Date plus (b) the |

S-8

Table of Contents

product of (i) the Annual Tracking Fee as of such Redemption Valuation Date, or the Call Valuation Date or the Acceleration Date, and (ii) a fraction, the numerator of which is the total number of calendar days from and excluding the immediately preceding Coupon Valuation Date (or if the Redemption Valuation Date occurs prior to the first Coupon Valuation Date, the period from and excluding the Initial Trade Date) to and including such Redemption Valuation Date, or the Call Valuation Date or the Acceleration Date, and the denominator of which is 365. |

Adjusted Tracking Fee Shortfall: | To the extent that the Adjusted Reference Distribution Amount, calculated on any Redemption Valuation Date, or the Call Valuation Date or the Acceleration Date, as applicable, is less than the Adjusted Tracking Fee, calculated on such Redemption Valuation Date, or the Call Valuation Date or the Acceleration Date, the difference between the Adjusted Tracking Fee and the Adjusted Reference Distribution Amount. |

Reference Distribution Amount: | (i) As of the first Coupon Valuation Date, an amount equal to the gross cash distributions that a Reference Holder would have been entitled to receive in respect of the Index constituents held by such Reference Holder on the “record date” with respect to any Index constituent for those cash distributions whose “ex-dividend date” occurs during the period from and excluding the Initial Trade Date to and including the first Coupon Valuation Date; and (ii) as of any other Coupon Valuation Date, an amount equal to the gross cash distributions that a Reference Holder would have been entitled to receive in respect of the Index constituents held by such Reference Holder on the “record date” with respect to any Index constituent for those cash distributions whose “ex-dividend date” occurs during the period from and excluding the immediately preceding Coupon Valuation Date to and including such Coupon Valuation Date. Notwithstanding the foregoing, with respect to cash distributions for an Index constituent which is scheduled to be paid prior to the applicable Coupon Ex-Date, if, and only if, the issuer of such Index constituent fails to pay the distribution to holders of such Index constituent by the scheduled payment date for such distribution, such distribution will be assumed to be zero for the purposes of calculating the applicable Reference Distribution Amount. |

See “Specific Terms of the Securities — Weekly Early Redemption at the Option of the Holders” beginning on page S-51 and “— UBS’s Call Right” beginning on page S-54.

Coupon Valuation Date: | The 30thof March, June, September and December of each calendar year during the term of the Securities or if such date is not an Index Business Day, then the first Index Business Day following such date, provided that the final Coupon Valuation Date will be the Calculation Date. The first Coupon Valuation Date will be September 30, 2010. |

Current Indicative Value: | As determined by the Security Calculation Agent as of any date of determination, an amount per Security, equal to |

| Current Principal Amount × | ( | 1+2 × | Index Closing Level–Monthly Initial Closing Level | ) | ||||||

| Monthly Initial Closing Level |

Index Divisor: | As of any date of determination, the divisor used by the Index Calculation Agent to calculate the level of the Index, as further described under “Alerian MLP Infrastructure Index — Index Equations.” |

Index Calculation Agent: | Standard & Poor’s |

S-9

Table of Contents

Selected Risk Considerations

An investment in the Securities involves risks. Selected risks are summarized here, but we urge you to read the more detailed explanation of risks described under “Risk Factors” beginning on page S-21.

| Ø | You may lose some or all of your principal — The Securities are exposed to two times any monthly decline in the level of the Index. Because the combined negative effect of the Accrued Tracking Fee and the Accrued Financing Charges reduce your final payment, the compounded leveraged monthly return of the Index will need to be sufficient to offset the combined negative effect of the Accrued Tracking Fee, Accrued Financing Charges and Redemption Fee Amount, if applicable, less any Coupon Amounts, any Stub Reference Distribution Amount and/or Adjusted Coupon Amount, as applicable, in order for you to receive an aggregate amount over the term of the Securities equal to your initial investment in the Securities. If the compounded leveraged monthly return of the Index is insufficient to offset the negative effect of the Accrued Tracking Fee and the Accrued Financing Charges over the relevant period, and Redemption Fee Amount, if applicable, less any Coupon Amounts, any Stub Reference Distribution Amount and/or Adjusted Coupon Amount, as applicable, or if the compounded leveraged monthly return of the Index is negative, you will lose some or all of your investment at maturity, call, acceleration or upon early redemption. |

| Ø | Correlation and compounding Risk — A number of factors may affect the Security’s ability to achieve a high degree of correlation with the performance of the Index, and there can be no guarantee that the Security will achieve a high degree of correlation. Because the Current Principal Amount is reset monthly, you will be exposed to compounding of monthly returns. As a result, the performance of the Securities for periods greater than one month is likely to be either greater than or less than the Index performance times the leverage factor of two, before accounting for Accrued Tracking Fees and Accrued Financial Charges, and the Redemption Fee Amount, if any. In particular, significant adverse monthly performances of your Securities may not be offset by subsequent beneficial monthly performances of equal magnitude. |

| Ø | Leverage risk— The Securities are two times leveraged long with respect to the Index, which means that you will benefit two times from any beneficial, but will be exposed to two times any adverse, monthly performance of the Index, before the combined negative effect of the Accrued Tracking Fee, the Accrued Financing Charges and Redemption Fee Amount, if any. |

| Ø | Market risk — The return on the Securities, which may be positive or negative, is linked to the compounded leveraged monthly return on the Index. The monthly return on the Index is measured by the Monthly Performance Ratio, which, in turn, is affected by a variety of market and economic factors, interest rates in the markets and economic, financial, political, regulatory, judicial or other events that affect the markets generally. |

| Ø | Credit of issuer — The Securities are senior unsecured debt obligations of the issuer, UBS, and are not, either directly or indirectly, an obligation of any third party. Any payment to be made on the Securities, including any payment at maturity, upon early redemption, call or acceleration, depends on the ability of UBS to satisfy its obligations as they come due. As a result, the actual and perceived creditworthiness of UBS will affect the market value, if any, of the Securities prior to maturity, call, acceleration or early redemption. In addition, in the event UBS were to default on its obligations, you may not receive any amounts owed to you under the terms of the Securities. |

| Ø | Potential over-concentration in a particular industry — There is only one industry — energy — related to the MLPs included in the Index. An investment in the Securities will increase your portfolio’s exposure to fluctuations in the energy industry. |

| Ø | A trading market for the Securities may not develop — Although we have been approved for listing the Securities on NYSE Arca, a trading market for the Securities may not develop. Certain affiliates of UBS may engage in limited purchase and resale transactions in the Securities, although they are not |

S-10

Table of Contents

required to and may stop at any time. We are not required to maintain any listing of the Securities on NYSE Arca or any other exchange. In addition, we are not obliged to, and may not, sell the full aggregate principal amount of the Securities. We may suspend or cease sales of the Securities at any time, at our discretion. |

| Ø | No redemption prior to July 19, 2010 — You may elect to redeem your Securities on or after July 19, 2010. Accordingly, your ability to liquidate the Securities may be limited prior to this date. |

| Ø | Minimum redemption amount — You must elect to redeem at least 50,000 Securities for UBS to repurchase your Securities, unless we determine otherwise or your broker or other financial intermediary bundles your Securities for redemption with those of other investors to reach this minimum requirement. |

| Ø | Your redemption election is irrevocable — You will not be able to rescind your election to redeem your Securities after your redemption notice is received by UBS. Accordingly, you will be exposed to market risk in the event market conditions change after UBS receives your offer and the Redemption Amount is determined on the Redemption Valuation Date. |

| Ø | Potential automatic acceleration — In the event the indicative value of the Securities is equal to $5.00 or less on any Index Business Day or the intraday index value on any Index Business Day decreases 30% from the most recent Monthly Initial Closing Level, the Securities will be automatically accelerated and mandatorily redeemed by UBS and you will receive a cash payment equal to the Acceleration Amount as determined during the Acceleration Valuation Period. The Acceleration Amount you receive on the Acceleration Settlement Date may be significantly less than $5.00 per Security and may be zero if the level of the Index continues to decrease during trading on one or more Index Business Days during the Acceleration Valuation Period as measured by the Index Performance Ratio on one or more Index Business Days during the Acceleration Valuation Period. |

| Ø | You are not guaranteed a coupon payment — You will not receive a coupon payment on a Coupon Payment Date if the Reference Distribution Amount is less than the Accrued Tracking Fee. Similarly, you will not receive a coupon payment on a Redemption Date, the Call Settlement Date or the Acceleration Settlement Date if the Adjusted Reference Distribution Amount is less than the Adjusted Tracking Fee, and in the case of a redemption, the Redemption Fee Amount. |

| Ø | Uncertain tax treatment — Significant aspects of the tax treatment of the Securities are uncertain. You should consult your own tax advisor about your own tax situation. |

| Ø | UBS’s Call Right — UBS may elect to redeem all outstanding Securities at any time on or after July 11, 2011, as described under “Specific Terms of the Securities — UBS’s Call Right” beginning on page S-54. If UBS exercises its Call Right, the Call Settlement Amount may be less than your initial investment in the Securities. |

The Securities may be a suitable investment for you if:

| Ø | You seek an investment with a return linked to two times the monthly performance of the Index, which will provide exposure to energy infrastructure-oriented MLPs. |

| Ø | You understand (i) leverage risk, including the risks inherent in maintaining a constant two times leverage on a monthly basis, and (ii) the consequences of seeking monthly leveraged investment results generally, and you intend to actively monitor and manage your investment. |

| Ø | You believe the compounded leveraged monthly return of the Index will be sufficient to offset the combined negative effect of the Accrued Tracking Fee and the Accrued Financing Charges, and any Redemption Fee Amount, less any Coupon Amounts, any Stub Reference Distribution Amount and/or any Adjusted Coupon Amount. |

| Ø | You are willing to accept the risk that you may lose some or all of your investment. |

S-11

Table of Contents

| Ø | You are willing to hold securities that may be redeemed early by UBS, pursuant to the UBS Call Right, on or after July 11, 2011. |

| Ø | You are willing to hold securities that have a long-term maturity (30 years). |

| Ø | You are willing to receive a lower amount of distributions than you would if you owned interests in the Index constituents directly. |

| Ø | You are willing to accept the risk of fluctuations in the energy industry, in general, and the risks inherent in a concentrated investment in energy infrastructure-oriented MLPs, in particular. |

| Ø | You are willing to accept the risk that the price at which you are able to sell the Securities may be significantly less than the amount you invested. |

| Ø | You seek current income from your investment. |

| Ø | You are not seeking an investment for which there will be an active secondary market. |

| Ø | You are comfortable with the creditworthiness of UBS, as issuer of the Securities. |

The Securities maynot be a suitable investment for you if:

| Ø | You do not seek an investment with a return linked to two times the monthly performance of the Index, which will provide exposure to energy infrastructure-oriented MLPs. |

| Ø | You do not understand (i) leverage risk, including the risks inherent in maintaining a constant two times leverage on a monthly basis, and (ii) the consequences of seeking monthly leveraged investment results generally, and you do not intend to actively monitor and manage your investment. |

| Ø | You believe that the compounded leveraged monthly return of the Index will be negative during the term of the Securities or the compounded leveraged monthly return will not be sufficient to offset the combined negative effect of the Accrued Tracking Fee and the Accrued Financing Charges, and any Redemption Fee Amount, less any Coupon Amounts, any Stub Reference Distribution Amount and/or any Adjusted Coupon Amount. |

| Ø | You are not willing to accept the risk that you may lose some or all of your investment. |

| Ø | You are not willing to hold securities that may be redeemed early by UBS, pursuant to the UBS Call Right, on or after July 11, 2011. |

| Ø | You are not willing to hold securities that have a long-term maturity (30 years). |

| Ø | You are not willing to be exposed to the risk of fluctuations in the energy prices, in general, and the risks inherent in a concentrated investment in energy infrastructure-oriented MLPs, in particular. |

| Ø | You are not willing to accept the risk that the price at which you are able to sell the Securities may be significantly less than the amount you invested. |

| Ø | You prefer the lower risk and therefore accept the potentially lower returns of fixed-income investments with comparable maturities and credit ratings. |

| Ø | You seek an investment for which there will be an active secondary market. |

| Ø | You are not comfortable with the creditworthiness of UBS, as issuer of the Securities. |

Who calculates and publishes the Index?

The level of the Index is calculated by Standard and Poor’s and disseminated by the NYSE approximately every fifteen seconds (assuming the level of the Index has changed within such fifteen-second interval) from 4:00 a.m. to 4:15 p.m., New York City time, and a daily Index level is published at approximately 4:00 p.m., New York City time, on each Exchange Business Day. Index information, including the Index

S-12

Table of Contents

level, is available from the NYSE and Bloomberg L.P. (“Bloomberg”) under the symbol “AMZI”. Index levels can also be obtained from the official website of Alerian, www.alerian.com. The historical performance of the Index is not indicative of the future performance of the Index or the level of the Index on the Final Valuation Date or applicable Redemption Valuation Date or Call Valuation Date, as the case may be.

Who calculates and publishes the VWAP Level?

The VWAP Level, which is calculated based on the information published by Standard and Poor’s as described in the paragraph above, is published and disseminated by the NYSE.

What are the tax consequences of the Securities?

The United States federal income tax consequences of your investment in the Securities are uncertain. Some of these tax consequences are summarized below, but we urge you to read the more detailed discussion in “Certain U.S. Federal Income Tax Consequences” on page S-67.

Pursuant to the terms of the Securities, you and we agree, in the absence of a statutory, regulatory, administrative or judicial ruling to the contrary, to characterize the Securities as a pre-paid forward contract with respect to the Index. In addition, you and we agree, in the absence of a statutory, regulatory, administrative or judicial ruling to the contrary, to treat the Coupon Amount (including amounts received upon the sale or maturity of the Securities in respect of accrued but unpaid Coupon Amounts) as an amount that should be included in ordinary income for tax purposes at the time such amounts accrue or are received, in accordance with the your regular method of tax accounting for tax purposes. If your Securities are so treated (and subject to the discussion below regarding the application of Section 1260 of the Internal Revenue Code), you should generally recognize capital gain or loss upon the sale or maturity of your Securities in an amount equal to the difference between the amount realized (other than any amount attributable to the Coupon Amount, which will be treated as ordinary income) and the amount you paid for your Securities. Such gain or loss should generally be long-term capital gain or loss if you held your Securities for more than one year.

In the opinion of our counsel, Sullivan & Cromwell LLP, the Securities should be treated in the manner described above. However, because there is no authority that specifically addresses the tax treatment of the Securities, it is possible that the Securities could be treated for tax purposes in an alternative manner as described under “Certain U.S. Federal Income Tax Consequences” on page S-67.

The Internal Revenue Service may assert that your Securities should be treated as a “constructive ownership transaction” which would be subject to the constructive ownership rules of Section 1260 of the Internal Revenue Code. Under Section 1260 of the Internal Revenue Code, special tax rules apply to an investor that enters into a “constructive ownership transaction” with respect to an equity interest in a “pass-thru entity.” For this purpose, a constructive ownership transaction includes entering into a forward contract with respect to a pass-thru entity and a partnership is considered to be a pass-thru entity. It is, however, not entirely clear how Section 1260 of the Internal Revenue Code applies in the case of an index of pass-thru entities like the Index. Although the matter is not free from doubt, it is likely that Section 1260 should also apply to an index of pass-thru entities, in which case Section 1260 would apply to the Securities. If your Securities are subject to Section 1260, then any long-term capital gain that you realize upon the sale, exchange or maturity of your Securities would be recharacterized as ordinary income (and you would be subject to an interest charge on the deferred tax liability with respect to such capital gain) to the extent that such capital gain exceeds the amount of long-term capital gain that you would have realized had you purchased an actual interest in any of the Index constituents (in an amount equal to the leveraged notional amount of the Index that is represented by the Securities) on the date that you purchased your Securities and sold your interest in the Index constituents on the date of the

S-13

Table of Contents

sale or maturity of the Securities (the “excess gain amount”). If your Securities are subject to these rules, the excess gain amount will be presumed to be equal to all of the gain that you recognized in respect of the Securities (in which case all of such gain would be recharacterized as ordinary income that is subject to an interest charge) unless you provide clear and convincing evidence to the contrary. You should review the discussion of Section 1260 on page S-68 and are urged consult your own tax advisor regarding the potential application of these rules.

The Internal Revenue Service has released a notice that may affect the taxation of holders of the Securities. According to the notice, the Internal Revenue Service and the Treasury Department are actively considering whether the holder of an instrument such as the Securities should be required to accrue ordinary income on a current basis. It is not possible to determine what guidance they will ultimately issue, if any. It is possible, however, that under such guidance, holders of the Securities will ultimately be required to accrue income currently over the term of the Securities and this could be applied on a retroactive basis. The Internal Revenue Service and the Treasury Department are also considering other relevant issues, including whether additional gain or loss from such instruments should be treated as ordinary or capital, whether foreign holders of such instruments should be subject to withholding tax on any deemed income accruals, and whether the special “constructive ownership rules” of Section 1260 of the Internal Revenue Code should be applied to such instruments. Holders are urged to consult their tax advisors concerning the significance, and the potential impact of the above considerations. Except to the extent otherwise required by law, UBS intends to treat your Securities for United States federal income tax purposes in accordance with the treatment described above and under “Certain U.S. Federal Income Tax Consequences” on page S-67 unless and until such time as the Treasury Department and Internal Revenue Service determine that some other treatment is more appropriate.

Furthermore, in 2007, legislation was introduced in Congress that, if enacted, would have required holders of Securities purchased after the bill was enacted to accrue interest income over the term of the Securities despite the fact that there will be no interest payments over the term of the Securities. It is not possible to predict whether a similar or identical bill will be enacted in the future, or whether any such bill would affect the tax treatment of your Securities.

S-14

Table of Contents

Hypothetical Coupon Amount Calculation

The following table illustrates the hypothetical Coupon Amount payable on each Annual Coupon Payment Date over a hypothetical period of five quarters. Each of the hypothetical Coupon Amounts set forth below is for illustrative purposes only and may not be the actual Coupon Amount payable to a purchaser of the Securities on any Coupon Payment Date. The actual Coupon Amount payable on any Coupon Payment Date will be determined by reference to the Reference Distribution Amount calculated as of the corresponding Coupon Valuation Date and the Accrued Tracking Fee (including any Tracking Fee Shortfall) calculated as of the corresponding Coupon Valuation Date and may be substantially different from any amounts set forth below. The numbers appearing in the following table and examples have been rounded for ease of analysis. You may not be paid, and are not guaranteed, a Coupon Amount during the term of the Securities.

Quarter | Current Indicative Value | Reference Distribution Amount as of the applicable Coupon Valuation Date | Accrued Tracking Fee (excluding Tracking Fee Shortfall accrued from Previous Quarter) as of the applicable Coupon Valuation Date* | Accrued Tracking Fee (including Tracking Fee Shortfall accrued from Previous Quarter) as of the applicable Coupon Valuation Date* | Coupon Amount | Tracking Fee Shortfall for the Following Quarter | ||||||

| Quarter 1 | 25.15 | 0.9528 | 0.0527 | 0.0527 | 0.9001 | 0 | ||||||

| Quarter 2 | 24.50 | 0.6512 | 0.0513 | 0.0513 | 0.5999 | 0 | ||||||

| Quarter 3 | 25.75 | 0.0000 | 0.0540 | 0.0540 | 0.0000 | 0.0540 | ||||||

| Quarter 4 | 25.00 | 0.0330 | 0.0524 | 0.1064 | 0.0000 | 0.0734 | ||||||

| Quarter 5 | 26.05 | 1.0152 | 0.0546 | 0.1280 | 0.8872 | 0 |

| * | Assuming that the total number of calendar days in each quarter is 90. |

For additional information and key terms related to the Coupon Amount, please see “Specific Terms of the Securities — Coupon Payment.”

Hypothetical Payment at Maturity Call or Acceleration, or upon Early Redemption

The following examples illustrate how the Securities would perform at maturity or call, or upon early redemption, in hypothetical circumstances. We have included examples in which the Index Closing Level increases at a constant rate of 1.25% per month for twelve months (Example 1), as well as examples in which the Index Closing Level decreases at a constant rate of 1.25% per month for twelve months (Example 2). In addition, Example 3 shows the Index Closing Level increasing by 1.25% per month for the first six months and then decreasing by 1.25% per month for the next 6 months, whereas Example 4 shows the reverse scenario of the Index Closing Level decreasing by 1.25% per month for the first six months, and then increasing by 1.25% per month for the next six months. For ease of analysis and presentation,the following examples assume that the term of the Securities is twelve months, no Coupon Amount was paid during the term of the Securities, the Reference Distribution Amount for each applicable period is zero, no Stub Reference Distribution Amount will be paid at maturity or call and no Adjusted Coupon Amount will be paid upon call or early redemption, and that no acceleration upon minimum indicative value or intraday index value has occurred. The Financing Rate is assumed to be 0.533%. These examples highlight the effect of the two times leverage and monthly compounding, and the impact of the Accrued Tracking Fee and Accrued Financing Charges on the payment at maturity or call, or upon early redemption, under different circumstances. Because the Accrued Tracking Fee and Accrued Financing Charges take into account the performance of the Index, as measured by the Index Closing Level, the absolute level of the Accrued Tracking Fee and Accrued Financing Charges are dependent on the path taken by the Index Closing Level to arrive at its ending level. The figures in these examples have been rounded for convenience. The Cash Settlement Amount figures for month twelve are as of the hypothetical Calculation Date, and given the indicated assumptions, a holder will receive payment at maturity or call, or upon early redemption, in the indicated amount, according to the indicated formula.

S-15

Table of Contents

Hypothetical Examples

Example 1

Assumptions:

| Annual Tracking Fee: * | 0.85% per annum | |

| Financing Rate: | 0.533% | |

| Denomination/Face Amount: | $25.00 | |

| Initial Index Level: | 490.00 | |

| Redemption Fee Amount: | 0.125% |

Month End | Index Closing Level** | Monthly Performance Ratio | Monthly Reset Factor | Accrued Financing Charges* | Current Principal Amount | Annual Tracking Fee for the Applicable Year | Accrued Tracking Fee | Cash Settlement Amount/ Call Settlement Amount | Redemption Amount | ||||||||||||||

A | B | C | D | E | F | G | H | I | J | ||||||||||||||

| ( ( Index Closing Level - Monthly Initial Closing Level ) / Monthly Initial Closing Level ) | 1 + (2 x C) | (Current Principal Amount x Financing Rate x Act/360) | (previous Current Principal Amount x D - E) | ( C x Annual Tracking Fee ) | ( Cumulative Total of G ) | ( F - H ) | ( I-Redemption Fee Amount ) | ||||||||||||||||

| 1 | 496.13 | 0.0125 | 1.03 | 0.0111 | $ | 25.61 | $ | 0.0179 | $ | 0.0179 | $ | 25.60 | $ | 25.56 | |||||||||

| 2 | 502.33 | 0.0125 | 1.03 | 0.0114 | $ | 26.24 | $ | 0.0183 | $ | 0.0362 | $ | 26.21 | $ | 26.17 | |||||||||