Filed Pursuant to Rule 424(b)(3)

Registration Statement No. 333-200212

CALCULATION OF REGISTRATION FEE

| ||||

Title of Each Class of Securities Offered | Maximum Offering Price | Amount of Registration Fee(1) | ||

Contingent Absolute Return Autocallable Optimization Securities Linked to the relevant nearby NYMEX-traded natural gas futures contracts due August 19, 2015 | $1,986,000.00 | $230.77 | ||

| ||||

| ||||

| (1) | Calculated in accordance with Rule 457(r) of the Securities Act of 1933. |

| PRICING SUPPLEMENT (To Prospectus dated November 14, 2014) |  |

UBS AG $1,986,000 Contingent Absolute Return Autocallable Optimization Securities

Linked to the relevant nearby NYMEX-traded natural gas futures contracts due August 19, 2015

Investment Description

UBS AG Contingent Absolute Return Autocallable Optimization Securities (the ‘‘Securities’’) are unsubordinated, unsecured debt securities issued by UBS AG (‘‘UBS’’ or the ‘‘issuer’’) linked to the performance of the relevant nearby natural gas futures contract (the ‘‘underlying asset”) as traded on the New York Mercantile Exchange (the “NYMEX”). The Securities are designed for investors who believe that the official settlement price of the underlying asset will remain flat or increase during the term of the Securities, or believe that the official settlement price will be equal to or greater than the trigger price on the final valuation date. If the official settlement price of the underlying asset is equal to or greater than the initial price on any quarterly observation date (including the final valuation date), UBS will automatically call the Securities and pay you an amount in cash equal to the principal amount per Security plus the applicable call return for the relevant observation date (the “call price”). The call return, and therefore the call price, increases the longer the Securities are outstanding. If by maturity the Securities have not been called and the official settlement price of the underlying asset is equal to or greater than the trigger price on the final valuation date, UBS will repay your principal amount per Security plus an amount equal to the product of (i) your principal amount multiplied by (ii) the absolute value of the percentage decline of the official settlement price of the underlying asset from the trade date to the final valuation date (the “contingent absolute return”). If by maturity the Securities have not been called and the official settlement price of the underlying asset is less than the trigger price on the final valuation date, the contingent absolute return will not apply and UBS will repay less than the principal amount, if anything, resulting in a loss on your investment that is proportionate to the decline in the official settlement price of the underlying asset from the trade date to the final valuation date (the “underlying return”).Investing in the Securities involves significant risks. The Securities do not pay interest. You may lose some or all of your principal amount. The contingent absolute return, and any contingent repayment of your principal, apply only if you hold the Securities to maturity. Any payment on the Securities, including any repayment of principal, is subject to the creditworthiness of the issuer. If UBS were to default on its payment obligations you may not receive any amounts owed to you under the Securities and you could lose all of your initial investment.

Features

| q | Call Return — If the official settlement price of the underlying asset is equal to or greater than the initial price on any observation date (including the final valuation date), UBS will automatically call the Securities and pay you a cash payment per Security equal to the call price for the applicable observation date. The call return, and therefore the call price, increases the longer the Securities are outstanding. If the Securities are not called, investors will have the potential for downside market risk at maturity. |

| q | Contingent Absolute Return with Contingent Repayment of Principal at Maturity — If by maturity the Securities have not been called and the official settlement price of the underlying asset is equal to or greater than the trigger price on the final valuation date, UBS will repay your principal amount per Security plus an amount equal to the product of (i) your principal amount multiplied by (ii) the contingent absolute return. If, however, the official settlement price of the underlying asset is less than the trigger price on the final valuation date, the contingent absolute return will not apply and UBS will repay less than the principal amount, if anything, at maturity, resulting in a loss on your investment that is proportionate to the underlying return. The contingent absolute return, and any contingent repayment of your principal, apply only if you hold the Securities until maturity. Any payment on the Securities, including any repayment of principal, is subject to the creditworthiness of UBS. |

Key Dates

| Trade Date | November 14, 2014 | |

| Settlement Date | November 19, 2014 | |

| Observation Dates* | Quarterly (see page 2) | |

| Final Valuation Date* | August 14, 2015 | |

| Maturity Date* | August 19, 2015 |

| * | Subject to postponement in the event of a market disruption event as described under “Market Disruption Events” on page 15 of this pricing supplement. |

Notice to investors: the Securities are significantly riskier than conventional debt instruments. The issuer is not necessarily obligated to repay the full principal amount of the Securities at maturity, and the Securities can have downside market risk similar to the underlying asset. This market risk is in addition to the credit risk inherent in purchasing a debt obligation of UBS. You should not purchase the Securities if you do not understand or are not comfortable with the significant risks involved in investing in the Securities.

You should carefully consider the risks described under ‘‘Key Risks’’ beginning on page 5 before purchasing any Securities. Events relating to any of those risks, or other risks and uncertainties, could adversely affect the market value of, and the return on, your Securities. You may lose some or all of your initial investment in the Securities. The Securities will not be listed or displayed on any Securities exchange or any electronic communications network.

Security Offering

These terms relate to Securities linked to the performance of the relevant nearby natural gas futures contract as traded on the NYMEX. The Securities are offered at a minimum investment of 100 Securities at $10 per Security (representing a $1,000 investment) and integral multiples of $10 in excess thereof.

| Underlying Asset | Call Return Rate | Initial Price | Trigger Price | CUSIP | ISIN | |||||

| Relevant nearby NYMEX-traded natural gas futures contract | 23.50% per annum* | $4.020 | $3.216, which is 80% of the Initial Price | 90274F163 | US90274F1637 |

| * | If the Securities are called, your call return will vary depending on the observation date on which the Securities are called. The call return increases the longer the Securities are outstanding. Because the term of the Securities is at most 9 months, the maximum potential call return will be 17.625%. |

The estimated initial value of the Securities as of the trade date is $9.81 for Securities linked to the relevant nearby natural gas futures contract as traded on the NYMEX. The estimated initial value of the Securities was determined as of the close of the relevant markets on the date of this pricing supplement by reference to UBS’ internal pricing models, inclusive of the internal funding rate. For more information about secondary market offers and the estimated initial value of the Securities, see “Key Risks — Fair value considerations” and “— Limited or no secondary market and secondary market price considerations” beginning on page 6 of this pricing supplement.

See ‘‘Additional Information about UBS and the Securities’’ on page ii. The Securities will have the terms set forth in the accompanying prospectus, dated November 14, 2014 and this pricing supplement.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these Securities or passed upon the adequacy or accuracy of this pricing supplement or the accompanying prospectus. Any representation to the contrary is a criminal offense.

The Securities are not bank deposits and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency.

| Offering of Securities | Issue Price to Public | Underwriting Discount | Proceeds to UBS | |||||||||

| Total | Per Security | Total | Per Security | Total | Per Security | |||||||

| Securities linked to the relevant nearby NYMEX-traded natural gas futures contract | $1,986,000.00 | $10.00 | $19,860.00 | $0.10 | $1,966,140.00 | $9.90 | ||||||

UBS Financial Services Inc. Pricing Supplement dated November 14, 2014 | UBS Investment Bank |

Additional Information about UBS and the Securities

UBS has filed a registration statement (including a prospectus for the Securities we may offer, including the Securities) with the Securities and Exchange Commission, or SEC, for the offering to which this pricing supplement relates. Before you invest, you should read these documents and any other documents relating to the Securities that UBS has filed with the SEC for more complete information about UBS and this offering. You may obtain these documents for free from the SEC website at www.sec.gov. Our Central Index Key, or CIK, on the SEC website is 0001114446. Alternatively, UBS will arrange to send you these documents if you so request by calling toll-free 1-877-387-2275.

You may access these documents on the SEC website at www.sec.gov as follows:

| ¨ | Prospectus dated November 14, 2014: |

http://www.sec.gov/Archives/edgar/data/1114446/000119312514413375/d816529d424b3.htm

References to “UBS,” “we,” “our” and “us” refer only to UBS AG and not to its consolidated subsidiaries. In this document, the “Securities” refer to the Contingent Absolute Return Autocallable Optimization Securities that are offered hereby. Also, references to “accompanying prospectus” mean the UBS prospectus titled “Debt Securities and Warrants,” dated November 14, 2014.

This pricing supplement, together with the accompanying prospectus, contains the terms of the Securities and supersedes all other prior or contemporaneous oral statements as well as any other written materials including pricing terms, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among other things, the matters set forth in “Key Risks” on page 5, as the Securities involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisors before deciding to invest in the Securities.

UBS reserves the right to change the terms of, or reject any offer to purchase, the Securities prior to their issuance. In the event of any changes to the terms of the Securities, UBS will notify you and you will be asked to accept such changes in connection with your purchase. You may also choose to reject such changes in which case UBS may reject your offer to purchase.

ii

Investor Suitability

The Securities may be suitable for you if:

| ¨ | You fully understand the risks inherent in an investment in the Securities, including the risk of loss of some or all of your initial investment. |

| ¨ | You can tolerate a loss of all or a substantial portion of your initial investment and are willing to make an investment that could have the same downside market risk as an investment in the underlying asset. |

| ¨ | You believe the official settlement price of the underlying asset will be equal to or greater than the initial price on one of the specified observation dates, including the final valuation date, or will be greater than the trigger price on the final valuation date. |

| ¨ | You understand and accept that you will not participate in any appreciation in the price of the underlying asset and that your potential return is limited to the applicable call return if the Securities are called, and to the contingent absolute return (as limited by the trigger price) if the Securities have not been called. |

| ¨ | You can tolerate fluctuations in the price of the Securities prior to maturity that may be similar to or exceed the downside price fluctuations of the underlying asset. |

| ¨ | You are willing to invest in the Securities based on the call return rate and trigger price indicated on the cover hereof. |

| ¨ | You do not seek current income from this investment. |

| ¨ | You fully understand the risks associated with an investment in commodity futures contracts generally, and natural gas futures contracts specifically. |

| ¨ | You are willing to invest in securities that may be called early and you are otherwise willing to hold such securities to maturity, a term of approximately 9 months, and accept that there may be little or no secondary market for the Securities. |

| ¨ | You are willing to assume the credit risk of UBS for all payments under the Securities, and understand that if UBS defaults on its obligations you may not receive any amounts due to you, including any repayment of principal. |

| ¨ | You understand that the estimated initial value of the Securities determined by our internal pricing models is lower than the issue price and that should UBS Securities LLC or any affiliate make secondary markets for the Securities, the price (not including their customary bid-ask spreads) will temporarily exceed the internal pricing model price. |

The Securities may not be suitable for you if:

| ¨ | You do not fully understand the risks inherent in an investment in the Securities, including the risk of loss of some or all of your initial investment. |

| ¨ | You cannot tolerate a loss of all or a substantial portion of your investment and are unwilling to make an investment that could have the same downside market risk as an investment in the underlying asset. |

| ¨ | You require an investment designed to provide a full return of your initial investment at maturity. |

| ¨ | You believe that the price of the underlying asset will decline during the term of the Securities and is likely to be less than the trigger price on the final valuation date exposing you to the underlying return at maturity. |

| ¨ | You seek an investment that participates in the full appreciation, or benefits fully from any depreciation, in the price of the underlying asset or that has unlimited return potential. |

| ¨ | You are unwilling to invest in the Securities based on the call return rate and trigger price indicated on the cover hereof. |

| ¨ | You cannot tolerate fluctuations in the price of the Securities prior to maturity that may be similar to or exceed the downside price fluctuations of the underlying asset. |

| ¨ | You seek current income from this investment. |

| ¨ | You do not fully understand the risks associated with an investment in commodity futures contracts generally, and natural gas futures contracts specifically. |

| ¨ | You are unable or unwilling to hold securities that may be called early, or you are otherwise unable or unwilling to hold such securities to maturity, a term of approximately 9 months, or you seek an investment for which there will be an active secondary market. |

| ¨ | You are not willing to assume the credit risk of UBS for all payments under the Securities, including any repayment of principal. |

The suitability considerations identified above are not exhaustive. Whether or not the Securities are a suitable investment for you will depend on your individual circumstances and you should reach an investment decision only after you and your investment, legal, tax, accounting and other advisors have carefully considered the suitability of an investment in the Securities in light of your particular circumstances. You should also review carefully the ‘‘Key Risks’’ beginning on page 5 of this pricing supplement for risks related to an investment in the Securities.

1

Final Terms

| Issuer | UBS AG, London Branch | |

| Principal Amount | $10 per Security (subject to a minimum investment of 100 Securities) | |

| Term(1) | Approximately 9 months, unless called earlier. | |

| Underlying Asset | The Securities are linked to the official settlement price per million British thermal units (“mmBtu”) of natural gas of the first nearby month futures contract stated in U.S. dollars, as traded on the NYMEX (Bloomberg Ticker: “NG1” <Comdty>); provided that if the trade date or the relevant observation date falls within the notice period for delivery of NYMEX-traded natural gas under such futures contract or on the last trading day of such futures contract, then the second nearby month futures contract (Bloomberg Ticker: “NG2” <Comdty>) will be used with respect to such date. | |

| Observation Dates(1)(2) | February 17, 2015, May 14, 2015 and August 14, 2015 (the “final valuation date”). As scheduled, the relevant futures contract related to each observation date will be the first nearby month futures contract. If the observation date falls within the notice period for delivery of natural gas under such futures contract or on the last trading day of such futures contract, then the second nearby month futures contract will be used. | |

| Call Feature | The Securities will be called if the official settlement price of the underlying asset on any observation date (including the final valuation date) is equal to or greater than the initial price. If the Securities are called, UBS will pay you on the applicable call settlement date a cash payment per Security equal to the applicable call price for the relevant observation date. | |

| Call Settlement Dates | Three business days following the relevant observation date; provided however, if the Securities are called on the final valuation date, the related call settlement date will be the maturity date. | |

| Call Return and Call Return Rate | The call return increases the longer the Securities are outstanding and is based upon a call return rate of 23.500% per annum. Because the term of the Securities is at most 9 months, the maximum potential call return is 17.625%. | |

| Call Price | The call price equals the principal amount per Security plus the applicable call return. |

The table below reflects the call return rate of 23.50% per annum.

| Observation Dates(1) | Relevant Nearby Futures Contract | Call Return | Call Price (per Security) | |||

| February 17, 2015 | March 2015 | 5.8750% | $10.5875 | |||

| May 14, 2015 | June 2015 | 11.7500% | $11.1750 | |||

| August 14, 2015 (final valuation date) | September 2015 | 17.6250% | $11.7625 |

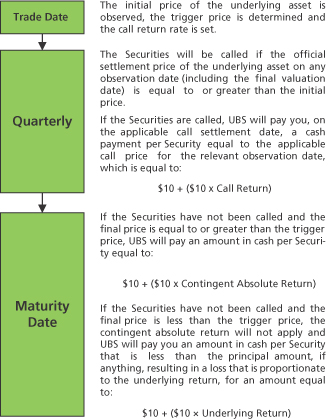

| Payment at Maturity (per Security) | If the Securities have not been called and the final price is equal to or greater than the trigger price, at maturity we will pay you an amount in cash equal to: $10 + ($10 x Contingent Absolute Return).

If the Securities have not been called and the final price is less than the trigger price, the contingent absolute return will not apply and at maturity we will pay you an amount in cash that is less than the principal amount, if anything, resulting in a loss that is proportionate to the underlying return, for an amount equal to: $10 + ($10 × Underlying Return).

Accordingly, you may lose all or a substantial portion of your principal amount at maturity, depending on how much the underlying asset declines. | |

| Underlying Return | Final Price - Initial Price

Initial Price | |

| Contingent Absolute Return | The absolute value of the underlying return. For example, if the underlying return is -5%, the contingent absolute return will equal 5%.

Because the contingent absolute return will only apply if the Securities have not been called and the final price is equal to or greater than the trigger price, the maximum possible contingent absolute return will be 20%, which would result from an underlying return of -20% if the final price were equal to the trigger price. You will not receive a contingent absolute return in the case of any further depreciation of the final price in excess of the trigger price and will lose of some or all of your investment. | |

| Trigger Price | $3.216, which is 80% of the initial price. | |

| Initial Price | $4.020, which is the official settlement price of the underlying asset on the trade date, as determined by the calculation agent by reference to the December 2014 natural gas futures contract, which is set to expire in November 2014. | |

| Final Price | The official settlement price of the underlying asset on the final valuation date, as determined by the calculation agent. The expected final valuation date would result in the final price being determined by reference to the September 2015 natural gas futures contract, which is set to expire in August 2015. | |

| Final Valuation Date | August 14, 2015, unless the calculation agent determines that a market disruption event (as set forth under “Market Disruption Events” on page 15 of this pricing supplement) has occurred or is continuing with respect to the underlying asset on any such day. In the case of a market disruption event, or if the final valuation date is not a business day for such underlying asset, the final valuation date for the underlying asset will be the first following business day on which the calculation agent determines that a market disruption event does not occur and/or is not continuing with respect to such underlying asset. In no event however, will the final valuation date for the underlying asset be postponed by more than 10 business days. See “Market Disruption Events” on page 15 of this pricing supplement. |

Investing in the Securities involves significant risks. The Securities do not pay interest. You may lose some or all of your principal amount. Any payment on the Securities, including any repayment of principal, is subject to the creditworthiness of the issuer. If UBS were to default on its payment obligations, you may not receive any amounts owed to you under the Securities and you could lose all your initial investment.

| (1) | Subject to the market disruption event provisions set forth under “Market Disruption Events” on page 15 of this pricing supplement. |

2

Investment Timeline

Investing in the Securities involves significant risks. You may lose some or all of your initial investment. Any payment on the Securities, including any repayment of principal, is subject to the creditworthiness of UBS. If UBS were to default on its payment obligations, you may not receive any amounts owed to you under the Securities and you could lose all of your initial investment.

3

Hypothetical Examples

The examples below illustrate the payment upon an automatic call or at maturity for a $10.00 Security on a hypothetical offering of the Securities, with the following assumptions (the actual terms are specified on the first page of this pricing supplement; amounts may have been rounded for ease of reference):

| Principal Amount: | $10.00 | |

| Term: | Approximately 9 months | |

| Initial Price: | $5.00 | |

| Call Return Rate:* | 23.00% per annum (increasing at a rate of 5.75% per quarter) | |

| Observation Dates: | Quarterly | |

| Trigger Price: | $4.00 (which is 80.00% of the Initial Price) |

| * | The call return rate for your Securities may be greater or less than than the amount shown above in which case, if your Securities are called, the call price may be greater or less than the amounts shown below. |

Example 1 — Securities are Called on the First Potential Call Settlement Date

| Official Settlement Price at first Observation Date: | $5.10 (at or above Initial Price, Securities are called) | |

| Call Price (per Security): | $10.575 |

Because the official settlement price is equal to or greater than the initial price on the first observation date, UBS will pay you on the first call settlement date a total call price of $10.575 per $10.00 principal amount (5.75% return on the Securities).

Example 2 — Securities are Called on the Maturity Date

| Official Settlement Price at first Observation Date: | $4.85 (below Initial Price, Securities NOT called) | |

| Official Settlement Price at second Observation Date: | $3.90 (below Initial Price, Securities NOT called) | |

| Official Settlement Price at Final Valuation Date: | $5.20 (at or above Initial Price, Securities are called) | |

| Call Price (per Security): | $11.725 | |

Because the official settlement price is equal to or greater than the initial price on the final valuation date, UBS will pay you on the maturity date a total call price of $11.725 per $10.00 principal amount (17.25% return on the Securities).

Example 3 — Securities are NOT Called and the Final Price is equal to or greater than the Trigger Price

| Official Settlement Price at first Observation Date: | $4.90 (below Initial Price, Securities NOT called) | |

| Official Settlement Price at second Observation Date: | $4.10 (below Initial Price, Securities NOT called) | |

| Official Settlement Price at Final Valuation Date: | $4.50 (below Initial Price, but above Trigger Price, Securities NOT called) | |

| Settlement Amount (per Security): | $10.00 + ($10 x Contingent Absolute Return) $10.00 + ($10 x 10%) $10.00 + $1.00 $11.00 | |

Because the Securities are not called and the final price is equal to or greater than the trigger price, at maturity UBS will pay you a total of $11.00 per $10.00 principal amount (10.00% return on the Securities).

Example 4 — Securities are NOT Called and the Final Price is less than the Trigger Price

| Official Settlement Price at first Observation Date: | $4.80 (below Initial Price, Securities NOT called) | |

| Official Settlement Price at second Observation Date: | $3.15 (below Initial Price, Securities NOT called) | |

| Official Settlement Price at Final Valuation Date: | $2.50, (below Initial Priceand Trigger Price, Securities NOT called) | |

| Settlement Amount (per Security): | $10.00 + ($10 × Underlying Return) $10.00 + ($10 × -50%) $10.00 - $5.00 $5.00 | |

Because the Securities are not called and the final price is less than the trigger price, at maturity UBS will pay you a total of $5.00 per $10.00 principal amount (a 50%loss on the Securities).

4

Key Risks

An investment in the Securities involves significant risks. Investing in the Securities is not equivalent to investing in the underlying asset. We also urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the Securities.

| ¨ | Risk of loss at maturity— The Securities differ from ordinary debt securities in that the issuer will not necessarily pay the full principal amount of the Securities. If the Securities are not called, UBS will pay you an amount in cash equal to the principal amount plus an amount equal to the product of the principal amount multiplied by the contingent absolute return only if the final price of the underlying asset is equal to or greater than the trigger price and will only make such payment at maturity. If the Securities are not called and the final price is less than the trigger price, the contingent absolute return will not apply and you will lose some or all of your initial investment in an amount proportionate to the underlying return. |

| ¨ | The contingent absolute return, and any contingent repayment of your principal, apply only at maturity — You should be willing to hold your Securities to maturity. If you are able to sell your Securities prior to maturity in the secondary market, you may have to sell them at a loss relative to your initial investment even if the price of the underlying asset is equal to or greater than the trigger price. |

| ¨ | Your potential return on the Securities is limited — The return potential of the Securities resulting from an automatic call is limited to the applicable call return regardless of the appreciation of the underlying asset. In addition, because the call return increases the longer the Securities have been outstanding, the call price payable on earlier observation dates is less than the call price payable on later observation dates. The earlier a Security is called, the lower your return will be. If the Securities are not called, your potential gain on the Securities from the contingent absolute return will be limited by the trigger price. Because your ability to receive a positive return on the Securities equal to the contingent absolute return is available only if the Securities are not called and if the final price is equal to or greater than the trigger price, your return on the Securities in this scenario is limited to 20%. You will not benefit from any further depreciation of the final price below the trigger price, and in that case will not receive a contingent absolute return and will participate in the full downside performance of the underlying asset, resulting in a loss of some or all of your investment. |

| ¨ | Higher call return rates are generally associated with a greater risk of loss — Greater expected volatility with respect to the underlying asset reflects a higher expectation as of the trade date that the official settlement price of such asset could be less than its trigger price on the final valuation date of the Securities. This greater expected risk will generally be reflected in a higher call return rate for that Security. However, while the call return rate is set on the trade date, an asset’s volatility can change significantly over the term of the Securities. The price of the underlying asset for your Securities could fall sharply, which could result in a significant loss of your initial investment. |

| ¨ | No interest payments— UBS will not pay any interest with respect to the Securities. |

| ¨ | Reinvestment risk— If your Securities are called early, the term of the Securities will be reduced and you will not receive any payment on the Securities after the applicable call settlement date. There is no guarantee that you would be able to reinvest the proceeds from an automatic call of the Securities at a comparable rate of return for a similar level of risk. To the extent you are able to reinvest such proceeds in an investment comparable to the Securities, you may incur transaction costs such as dealer discounts and hedging costs built into the price of the new securities. Because the Securities may be called as early as three months after issuance, you should be prepared in the event the Securities are called early. |

| ¨ | Credit risk of UBS — The Securities are unsubordinated, unsecured debt obligations of the issuer, UBS, and are not, either directly or indirectly, an obligation of any third party. Any payment to be made on the Securities, including payments in respect of an automatic call or any repayment of principal, depends on the ability of UBS to satisfy its obligations as they come due. As a result, UBS’s actual and perceived creditworthiness may affect the market value of the Securities. If UBS were to default on its obligations you may not receive any amounts owed to you under the terms of the Securities and you could lose all of your initial investment. |

| ¨ | Market risk— The official settlement price for the underlying asset is the result of the supply of, and the demand for, the underlying asset and for exchange-traded futures contracts for the purchase or delivery of natural gas. Changes in the official settlement price result over time from the interaction of many factors directly or indirectly affecting economic and political conditions such as the expected volatility of the price of natural gas, and of the prices of exchange-traded futures contracts for the purchase or delivery of natural gas and a variety of economic, financial, political, regulatory or judicial events. You, as an investor in the Securities, should make your own investigation into the respective underlying asset and the merits of an investment linked to it. |

| ¨ | The Securities are not regulated by the Commodity Futures Trading Commission (the “CFTC”)— An investment in the Securities does not constitute either an investment in futures contracts, options on futures contracts, or commodity options and therefore you will not benefit from the regulatory protections attendant to CFTC regulated products. This means that the Securities are not traded on a regulated exchange and issued by a clearinghouse. See “There may be little or no secondary market for the Securities” below. In addition, the proceeds to be received by UBS from the sale of the Securities will not be used to purchase or sell any commodity futures contracts, options on futures contracts or options on commodities for your benefit. Therefore an investment in the Securities does not constitute a collective investment vehicle that trades in these instruments. An investment in a collective investment vehicle that invests in these instruments often is subject to regulation as a commodity pool and its operator may be required to be registered with and regulated by the CFTC as a commodity pool operator. |

| ¨ | Trading in futures contracts is subject to legal and regulatory regimes that may change in ways that could adversely affect the return on the Securities—The regulation of commodity transactions in the U.S. is subject toongoing modification. It is not possible to predict the effect of any future legal or regulatory action relating to futurescontracts, but any such action could cause unexpected volatility and instability in commodity markets with a substantial andadverse effect on the performance of any underlying asset and, consequently, on the value of the Securities. |

5

| ¨ | Fair value considerations. |

| ¨ | The issue price you pay for the Securities exceeds their estimated initial value— The issue price you pay for the Securities exceeds their estimated initial value as of the trade date due to the inclusion in the issue price of the underwriting discount, hedging costs, issuance costs and projected profits. As of the close of the relevant markets on the trade date, we have determined the estimated initial value of the Securities by reference to our internal pricing models and it is set forth in this pricing supplement. The pricing models used to determine the estimated initial value of the Securities incorporate certain variables, including the official settlement price of the underlying asset; the volatility and global supply and demand of the underlying asset; the prices of exchange-traded futures contracts for purchase and delivery of natural gas; prevailing interest rates; the term of the Securities and our internal funding rate. Our internal funding rate is typically lower than the rate we would pay to issue conventional fixed or floating rate debt securities of a similar term. The underwriting discount, hedging costs, issuance costs, projected profits and the difference in rates will reduce the economic value of the Securities to you. Due to these factors, the estimated initial value of the Securities as of the trade date is less than the issue price you pay for the Securities. |

| ¨ | The estimated initial value is a theoretical price; the actual price that you may be able to sell your Securities in any secondary market (if any) at any time after the trade date may differ from the estimated initial value — The value of your Securities at any time will vary based on many factors, including the factors described above and in “— Market risk” above and is impossible to predict. Furthermore, the pricing models that we use are proprietary and rely in part on certain assumptions about future events, which may prove to be incorrect. As a result, after the trade date, if you attempt to sell the Securities in the secondary market, the actual value you would receive may differ, perhaps materially, from the estimated initial value of the Securities determined by reference to our internal pricing models. The estimated initial value of the Securities does not represent a minimum or maximum price at which we or any of our affiliates would be willing to purchase your Securities in any secondary market at any time. |

| ¨ | Our actual profits may be greater or less than the differential between the estimated initial value and the issue price of the Securities as of the trade date — We may determine the economic terms of the Securities, as well as hedge our obligations, at least in part, prior to the trade date. In addition, there may be ongoing costs to us to maintain and/or adjust any hedges and such hedges are often imperfect. Therefore, our actual profits (or potentially, losses) in issuing the Securities cannot be determined as of the trade date and any such differential between the estimated initial value and the issue price of the Securities as of the trade date does not reflect our actual profits. Ultimately, our actual profits will be known only at the maturity of the Securities. |

| ¨ | Limited or no secondary market and secondary market price considerations. |

| ¨ | There may be little or no secondary market for the Securities — The Securities will not be listed or displayed on any securities exchange or any electronic communications network. There can be no assurance that a secondary market for the Securities will develop. UBS Securities LLC and its affiliates may make a market in the Securities, although they are not required to do so and may stop making a market at any time. If you are able to sell your Securities prior to maturity, you may have to sell them at a substantial loss. The estimated initial value of the Securities does not represent a minimum or maximum price at which we or any of our affiliates would be willing to purchase your Securities in any secondary market at any time. |

| ¨ | The price at which UBS Securities LLC and its affiliates may offer to buy the Securities in the secondary market (if any) may be greater than UBS’ valuation of the Securities at that time, greater than any other secondary market prices provided by unaffiliated dealers (if any) and, depending on your broker, greater than the valuation provided on your customer account statements— For a limited period of time following the issuance of the Securities, UBS Securities LLC or its affiliates may offer to buy or sell such Securities at a price that exceeds (i) our valuation of the Securities at that time based on our internal pricing models, (ii) any secondary market prices provided by unaffiliated dealers (if any) and (iii) depending on your broker, the valuation provided on customer account statements. The price that UBS Securities LLC may initially offer to buy such Securities following issuance will exceed the valuations indicated by our internal pricing models due to the inclusion for a limited period of time of the aggregate value of the underwriting discount, hedging costs, issuance costs and theoretical projected trading profit. The portion of such amounts included in our price will decline to zero on a straight line basis over a period ending no later than the date specified under “Supplemental Plan of Distribution (Conflicts of Interest); Secondary Markets (if any).” Thereafter, if UBS Securities LLC or an affiliate makes secondary markets in the Securities, it will do so at prices that reflect our estimated value determined by reference to our internal pricing models at that time. The temporary positive differential relative to our internal pricing models arises from requests from and arrangements made by UBS Securities LLC with the selling agents of structured debt securities such as the Securities. As described above, UBS Securities LLC and its affiliates are not required to make a market for the Securities and may stop making a market at any time. The price at which UBS Securities LLC or an affiliate may make secondary markets at any time (if at all) will also reflect its then current bid-ask spread for similar sized trades of structured debt securities. UBS Financial Services Inc. and UBS Securities LLC reflect this temporary positive differential on their customer statements. Investors should inquire as to the valuation provided on customer account statements provided by unaffiliated dealers. |

| ¨ | Price of Securities prior to maturity — The market price of the Securities will be influenced by many unpredictable and interrelated factors, including the official settlement price of the underlying asset; the volatility and global supply and demand of the underlying asset; the prices of exchange-traded futures contracts for purchase and delivery of natural gas; the time remaining to the maturity of the Securities; interest rates in the markets; geopolitical conditions and economic, financial, political, force majeure and regulatory or judicial events; the creditworthiness of UBS and the then current bid-ask spread for the Securities. |

| ¨ | Impact of fees and the use of internal funding rates rather than secondary market credit spreads on secondary market prices — All other things being equal, the use of the internal funding rates described above under “— Fair value considerations” as well as the inclusion in the issue price of the underwriting discount, hedging costs, issuance costs and any projected profits are, subject to the temporary mitigating effect of UBS Securities LLC’s and its affiliates’ market making premium, expected to reduce the price at which you may be able to sell the Securities in any secondary market. |

6

| ¨ | Owning the Securities is not the same as purchasing, or taking short positions in, natural gas or certain other related contracts directly — The return on your Securities will not reflect the return you would realize if you had actually purchased or took a short position in natural gas directly, or any exchange-traded or over-the-counter instruments based on natural gas. You will not have any rights that holders of such assets or instruments have. Even if the official settlement price of the underlying asset moves favorably during the term of the Securities, the market value of the Securities may not increase by the same amount. It is also possible for the price of the underlying asset to move favorably while the market value of the Securities declines. |

| ¨ | No assurance that the investment view implicit in the Securities will be successful— It is impossible to predict whether the price of the underlying asset will rise or fall. The official settlement price of the underlying asset will be influenced by complex and interrelated political, economic, financial and other factors that affect the underlying asset. You should be willing to accept the downside risks of owning commodities futures contracts in general and the underlying asset in particular, and to assume the risk that, if the Securities are not automatically called and the final price is less than the trigger price, you will lose some or all of your initial investment. |

| ¨ | The determination as to whether the Securities are subject to an automatic call, or the formula for calculating the payment at maturity of the Securities do not take into account all developments in the official settlement price of the underlying asset— Changes in the official settlement price of the underlying asset during the periods betweeneach observation date will not be reflected in the determination as to whether the Securities are subject to an automatic call,or the calculation of the amount payable at maturity of the Securities. The calculation agent will determine whether theSecurities are subject to an automatic call, by observing only the official settlement price of the underlying asset on theapplicable observation date. The calculation agent will calculate the payment at maturity by comparing only the final price tothe initial price. No other prices will be taken into account. As a result, you may lose some or all of your principal amount evenif the price of the underlying asset has risen at certain times during the term of the Securities before falling to an officialsettlement price that is less than the trigger price on the final valuation date. |

| ¨ | The Securities offer exposure to futures contracts and not direct exposure to physical commodities — The Securities will reflect a return based on the performance of the relevant nearby NYMEX-traded natural gas futures contract and do not provide exposure to natural gas spot prices. The price of a commodity futures contract reflects the expected value of the commodity upon delivery in the future, whereas the spot price of a commodity reflects the immediate delivery value of the commodity. A variety of factors can lead to a disparity between the expected future price of a commodity and the spot price at a given point in time, such as the cost of storing the commodity for the term of the futures contract, interest charges incurred to finance the purchase of the commodity and expectations concerning supply and demand for the commodity. The price movement of a futures contract is typically correlated with the movements of the spot price of the reference commodity, but the correlation is generally imperfect and price moves in the spot market may not be reflected in the futures market (and vice versa). Accordingly, the Securities may underperform a similar investment that reflects the return on the physical commodity. |

| ¨ | Prices of commodities and commodity futures contracts are highly volatile and may change unpredictably — Commodity prices are highly volatile and, in many sectors, have experienced unprecedented historical volatility. Commodity prices are affected by numerous factors including: changes in supply and demand relationships (whether actual, perceived, anticipated, unanticipated or unrealized); weather; agriculture; trade; fiscal, monetary and exchange control programs; domestic and foreign political and economic events and policies; disease; pestilence; technological developments; changes in interest rates, whether through governmental action or market movements; monetary and other governmental policies, action and inaction; macroeconomic or geopolitical and military events, including political instability; and natural or nuclear disasters. Those events tend to affect prices worldwide, regardless of the location of the event. Market expectations about these events and speculative activity also cause prices to fluctuate. These factors may adversely affect the performance of the underlying asset and, as a result, the market value of the Securities, and any payments you may receive in respect of the Securities. |

| ¨ | Changes in supply and demand in the market for natural gas futures contracts may adversely affect the value of the Securities — The Securities are linked to the performance of futures contracts on the underlying physical commodity natural gas. Futures contracts are legally binding agreements for the buying or selling of a certain commodity at a fixed price for physical settlement on a future date. Commodity futures contract prices are subject to similar types of pricing volatility patterns as may affect the specific commodities underlying the futures contracts, as well as additional trading volatility factors that may impact futures markets generally. Moreover, changes in the supply and demand for commodities, and futures contracts for the purchase and delivery of particular commodities, may lead to differentiated pricing patterns in the market for futures contracts over time. For example, a futures contract scheduled to expire in the first nearby month may experience more severe pricing pressure or greater price volatility than the corresponding futures contract scheduled to expire in a later month. Because the official settlement price of the underlying asset is generally scheduled to be determined by reference to the first nearby expiring natural gas futures contract for each observation date, the value of the Securities may be less than would otherwise be the case if the official settlement price of the underlying asset had been determined by reference to the corresponding futures contract scheduled to expire in a more favorable month for pricing purposes. |

| ¨ | Suspension or disruptions of market trading in commodities and related futures may adversely affect the value of the Securities — The commodity futures markets are subject to temporary distortions or other disruptions due to various factors, including the lack of liquidity in the markets, the participation of speculators and government regulation and intervention. In addition, U.S. futures exchanges and some foreign exchanges have regulations that limit the amount of fluctuation in some futures contract prices that may occur during a single business day. These limits are generally referred to as “daily price fluctuation limits” and the maximum or minimum price of a contract on any given day as a result of these limits is referred to as a “limit price”. Once the limit price has been reached in a particular contract, no trades may be made at a price beyond the limit, or trading may be limited for a set period of time. Limit prices have the effect of precluding trading in a particular contract or forcing the liquidation of contracts at potentially disadvantageous times or prices. These circumstances could adversely affect the price of the underlying asset and, therefore, the value of the Securities. |

7

| ¨ | The Securities may be subject to certain risks specific to natural gas as a commodity — Natural gas is an energy-related commodity. Consequently, in addition to factors affecting commodities generally that are described above and in the prospectus supplement, the Securities may be subject to a number of additional factors specific to energy-related commodities that might cause price volatility. These may include, among others: |

| ¨ | changes in the level of industrial and commercial activity with high levels of energy demand; |

| ¨ | disruptions in the supply chain or in the production or supply of other energy sources; |

| ¨ | price changes in alternative sources of energy; |

| ¨ | adjustments to inventory; |

| ¨ | variations in production and shipping costs; |

| ¨ | costs associated with regulatory compliance, including environmental regulations; and |

| ¨ | changes in industrial, government and consumer demand, both in individual consuming nations and internationally. |

These factors interrelate in complex ways, and the effect of one factor on the official settlement price of the underlying asset, and the market value of the Securities linked to the underlying asset, may offset or enhance the effect of another factor.

| ¨ | Changes in law or regulations relating to commodity futures contracts could adversely affect the market value of, and the amounts payable on, the Securities — Futures contracts and options on futures contracts are subject to extensive regulations and the regulation of commodity transactions in the U.S. is subject to ongoing modification by government and judicial action. The effect on the value of the Securities of any future regulatory changes, including but not limited to changes resulting from the Dodd-Frank Wall Street Reform and Consumer Protection Act, is impossible to predict, but may have the effect of making the markets for commodities, commodity futures contracts, options on futures contracts and other related derivatives more volatile and over time potentially less liquid. Such effects could be substantial and adverse to the interests of holders of the Securities and may affect the amounts payable on and the value of the Securities. |

| ¨ | The calculation agent can postpone the determination of the official settlement price or the final price and a call settlement date or the maturity date, if a market disruption event occurs on an observation date or the final valuation date — If the calculation agent determines that a market disruption event has occurred or is continuing on the trade date, an observation date or the final valuation date, then the trade date, such observation date or the final valuation date will be postponed until the first business day on which no market disruption event occurs or is continuing. If such a postponement occurs, then the calculation agent will instead use the relevant official settlement price of the underlying asset on the first business day after that day on which no market disruption event occurs or is continuing. In no event, however, will the trade date, an observation date or the final valuation date for the Securities be postponed by more than ten business days. As a result, the settlement date, applicable call settlement date or maturity date for the Securities could also be postponed. |

If the trade date, an observation date or the final valuation date is postponed to the last possible day, but a market disruption event occurs or is continuing on that day, that day will nevertheless be the trade date, observation date or the final valuation date, as applicable. If the official settlement price of the underlying asset is not available on the last possible day that qualifies as the trade date, observation date or final valuation date, either because of a market disruption event or for any other reason, the calculation agent will make an estimate of the official settlement price of the underlying asset that would have prevailed in the absence of the market disruption event or such other reason. See “Market Disruption Event” on page 15 of this pricing supplement.

| ¨ | Discontinuation of trading of the underlying asset — If the relevant exchange of the underlying asset discontinues trading in such underlying asset then, the calculation agent may replace the underlying asset with another commodity futures contract, the price of which is quoted on such relevant exchange or any other exchange, that the calculation agent determines to be comparable to the discontinued underlying asset (a “successor commodity”). The calculation agent will thereafter determine the official settlement price on each observation date and the final price by reference to the official settlement price of such successor commodity on the relevant date. See “Discontinuation of Trading of the Underlying Asset on Its Relevant Exchange; Alternative Method of Calculation” on page 17 of this pricing supplement. |

| ¨ | Potential UBS impact on price — Trading or transactions by UBS or its affiliates in the underlying asset, listed and/or over-the-counter options, futures or other instruments with returns linked to the performance of the underlying asset may adversely affect the performance and, therefore, the market value of the Securities. |

| ¨ | Potential conflict of interest— There are potential conflicts of interest between you and the calculation agent, which will be an affiliate of UBS. The calculation agent will determine whether the Securities are subject to an automatic call and the payment at maturity of the Securities based on observed official settlement prices of the underlying asset. The calculation agent can postpone the determination of the initial price and the final price of the underlying asset on the trade date or final valuation date, respectively, or the determination of the official settlement price on any observation date, if a market disruption event occurs and is continuing on that date. As UBS determines the economic terms of the Securities, including the call return rate and the trigger price, and such terms include hedging costs, issuance costs and projected profits, the Securities represent a package of economic terms. There are other potential conflicts of interest insofar as an investor could potentially get better economic terms if that investor entered into exchange-traded and/or OTC derivatives or other instruments with third parties, assuming that such instruments were available and the investor had the ability to assemble and enter into such instruments. |

8

| ¨ | Potentially inconsistent research, opinions or recommendations by UBS — UBS and its affiliates publish research from time to time on financial markets and other matters that may influence the value of the Securities, or express opinions or provide recommendations that are inconsistent with purchasing or holding the Securities. Any research, opinions or recommendations expressed by UBS or its affiliates may not be consistent with each other and may be modified from time to time without notice. Investors should make their own independent investigation of the merits of investing in the Securities and the underlying asset to which the Securities are linked. |

| ¨ | Under certain circumstances, the Swiss Financial Market Supervisory Authority (“FINMA”) has the power to take actions that may adversely affect the Securities — Pursuant to article 25 et seq. of the Swiss Banking Act, FINMA has broad statutory powers to take measures and actions in relation to UBS if it (i) is overindebted, (ii) has serious liquidity problems or (iii) fails to fulfill the applicable capital adequacy provisions after expiration of a deadline set by FINMA. If one of these prerequisites is met, the Swiss Banking Act grants significant discretion to FINMA to open restructuring proceedings or liquidation (bankruptcy) proceedings in respect of, and/or impose protective measures in relation to, UBS. In particular, a broad variety of protective measures may be imposed by FINMA, including a bank moratorium or a maturity postponement, which measures may be ordered by FINMA either on a stand-alone basis or in connection with restructuring or liquidation proceedings. In a restructuring proceeding, the resolution plan may, among other things, (a) provide for the transfer of UBS’s assets or a portion thereof, together with debts and other liabilities, and contracts of UBS, to another entity, (b) provide for the conversion of UBS’s debt and/or other obligations, including its obligations under the Securities, into equity and/or (c) potentially provide for haircuts on obligations of UBS, including its obligations under the Securities. Although no precedent exists, if one or more measures under the revised regime were imposed, such measures may have a material adverse effect on the terms and market value of the Securities and/or the ability of UBS to make payments thereunder. |

| ¨ | Dealer incentives— UBS and its affiliates act in various capacities with respect to the Securities. We and our affiliates may act as a principal, agent or dealer in connection with the sale of the Securities. Such affiliates, including the sales representatives, will derive compensation from the distribution of the Securities and such compensation may serve as an incentive to sell these Securities instead of other investments. We will pay total underwriting compensation in an amount equal to the underwriting discount listed on the cover hereof per Security to any of our affiliates acting as agents or dealers in connection with the distribution of the Securities. Given that UBS Securities LLC and its affiliates temporarily maintain a market making premium, it may have the effect of discouraging UBS Securities LLC and its affiliates from recommending sale of your Securities in the secondary market. |

| ¨ | Uncertain tax treatment — Significant aspects of the tax treatment of the Securities are uncertain. You should consult your own tax advisor about your tax situation. See “What Are the Tax Consequences of the Securities” beginning on page 12. |

9

Description of the Underlying Asset

In this pricing supplement, when we refer to the official settlement price of the underlying asset, we mean the official U.S. dollar settlement price of natural gas (expressed in dollars and cents per mmBtu) for the relevant first nearby natural gas futures contract, as traded on the NYMEX and displayed on Bloomberg under the symbol “NG1” <Comdty>. If the trade date or relevant observation date falls within the notice period for delivery of natural gas under such futures contract or on the last trading day of such futures contract, then the second nearby month futures contract will be used.

Natural gas is a mixture of hydrocarbons, or hydrocarbons and noncombustible gases, in a gaseous state, consisting essentially of methane. The natural gas futures contract is used as a principal national pricing benchmark. The contract trades in units of 10,000 million British thermal units, and the delivery point is the Henry Hub, which refers to piping and related facilities owned and/or leased by Sabine Pipe Line LLC near Erath, Louisiana. The Henry Hub is the nexus of 16 intra- and interstate natural gas pipeline systems that draw supplies from the region’s gas deposits. The exchange lists 118 continuous monthly contracts.

The natural gas futures contracts are traded on the NYMEX. Additional information about the natural gas futures contracts is available at the following website: http://www.cmegroup.com/trading/energy/natural-gas/natural-gas_contract_specifications.html.

Information from outside sources is not incorporated by reference in, and should not be considered part of, this pricing supplement or the accompanying prospectus. We have not conducted any independent review or due diligence of information contained in outside sources.

10

Historical Information

The following graph shows the performance of the underlying asset based on the daily official settlement prices from October 28, 2004 through November 14, 2014. On November 14, 2014, the underlying asset official settlement price was obtained, as described in “Underlying Asset” on page 2, without independent verification; the official settlement price of the underlying asset was $4.020/per mmBtu. The dotted line represents the trigger price of $3.216, which is equal to 80% of the official settlement price on November14, 2014. The historical performance of the underlying asset should not be taken as an indication of future performance, and no assurance can be given as to the official settlement price of the underlying asset on any given day.

Historical Performance of Natural Gas Futures Contracts

11

What are the Tax Consequences of the Securities?

The United States federal income tax consequences of your investment in the Securities are uncertain. Some of these tax consequences are summarized below, but we urge you to discuss the tax consequences of your particular situation with your tax advisor. This discussion only applies to you if you are a “U.S. holder” (as defined below) that holds the Securities as capital assets for tax purposes and you purchased your Securities in the initial issuance of such Securities.

This discussion is based on the Internal Revenue Code of 1986, as amended (the “Code”), administrative pronouncements, judicial decisions and final, temporary and proposed Treasury regulations as of the date of this pricing supplement, changes to any of which subsequent to the date of this pricing supplement may affect the U.S. federal income tax consequences described herein. If you are considering the purchase of a Security, you should consult your own tax advisor concerning the application of the United States federal income tax laws to your particular situation, as well as any tax consequences arising under the laws of any state, local or non-U.S. jurisdictions.

You are a U.S. holder if you are a beneficial owner of a Security and you are: (i) a citizen or resident of the United States, (ii) a domestic corporation, (iii) an estate whose income is subject to United States federal income tax regardless of its source, or (iv) a trust if a United States court can exercise primary supervision over the trust’s administration and one or more United States persons are authorized to control all substantial decisions of the trust. This section does not apply to you if you are a member of a class of holders subject to special rules, such as a dealer in securities or non-U.S. currencies, a trader in securities that elects to use a mark-to-market method of accounting for your securities holdings, a financial institution or a bank, a regulated investment company or a real estate investment company, a life insurance company, a tax-exempt organization including an “Individual Retirement Account” or “Roth IRA”, a person that owns Securities as part of a hedging transaction, straddle, synthetic security, conversion transaction, or other integrated transaction, or enters into a “constructive sale” with respect to the Securities or a “wash sale” with respect to the Securities or the underlying assets, or a U.S. holder (as defined below) whose functional currency for tax purposes is not the U.S. dollar.

An individual may, subject to certain exceptions, be deemed to be a resident of the United States by reason of being present in the United States for at least 31 days in the calendar year and for an aggregate of at least 183 days during a three-year period ending in the current calendar year (counting for such purposes all of the days present in the current year, one-third of the days present in the immediately preceding year, and one-sixth of the days present in the second preceding year).

If a partnership, or any entity treated as partnership for U.S. federal income tax purposes, holds the Securities, the United States federal income tax treatment of a partner will generally depend on the status of the partner and the tax treatment of the partnership. A partner in a partnership holding the Securities should consult its tax advisor with regard to the United States federal income tax treatment of an investment in the Securities.

There are no statutory provisions, regulations, published rulings or judicial decisions addressing the characterization for U.S. federal income tax purposes of securities with terms that are substantially the same as the Securities. Pursuant to the terms of the Securities, UBS and you agree, in the absence of a statutory, regulatory, administrative or judicial ruling to the contrary, to characterize your Securities as a pre-paid cash-settled derivative contract with respect to the underlying asset. If your Securities are so treated, you should generally recognize gain or loss upon the sale, maturity or automatic call of your Securities. Such gain or loss should be short-term capital gain or loss, in an amount equal to the difference between the amount you receive at such time and the amount you paid for your Securities. The deductibility of capital losses is subject to limitations.

In the opinion of our counsel, Cadwalader, Wickersham & Taft LLP, it would be reasonable to treat your Securities in the manner described above. However, because there is no authority that specifically addresses the tax treatment of the Securities, it is possible that your Securities could alternatively be treated for tax purposes as a single contingent debt instrument, or pursuant to some other characterization, such that the timing and character of your income from the Securities could differ materially from the treatment described above, as described below. The risk that the Securities may be recharacterized for United States federal income tax purposes as instruments giving rise to current ordinary income (even before receipt of any cash) and short-term capital gain or loss (even if held for more than one year) is higher than with other securities that do not guarantee full repayment of principal.

Alternative Treatments

Because of the absence of authority regarding the appropriate tax characterization of your Securities, it is possible that the IRS could seek to characterize your Securities in a manner that results in tax consequences to you that are different from those described above.

Short-Term Debt Instruments. Because the Securities have a term of one year or less, the IRS may assert that your Securities should be treated as short-term debt instruments. Although there is no authority that specifically addresses the tax treatment of short-term notes that provide for contingent payments, it is likely that if your Securities are so treated you would not recognize any income prior to the automatic call or maturity of the Securities. If your Securities are so treated and you are an initial purchaser of the Securities whose taxable year does not end on a day that is between the final valuation date and the maturity date (or between an observation date and the call settlement date), you should recognize ordinary income or short-term capital loss upon the maturity of your Securities in an amount equal to the difference between the amount you receive with respect to your Securities at such time and the amount you paid for your Securities. Upon a

12

sale or exchange of your Securities, it would be reasonable for you to recognize short-term capital gain or loss in an amount equal to the difference between the amount you paid for your Securities and the amount received by you upon such sale or exchange, unless you sell or exchange your Securities between the final valuation date and the maturity date (or between an observation date and the call settlement date), in which case it would be reasonable for you to generally treat any gain that you recognize as ordinary income and any loss that you recognize as a short-term capital loss. There is no statutory, judicial or administrative authority that governs how short-term contingent debt should be treated for U.S. federal income tax purposes. Accordingly, you should consult your tax advisor as to the tax consequences of such characterization.

Section 1256. Furthermore, the Internal Revenue Service (“IRS”), for example, might assert that Section 1256 of the Code should apply to your Securities. If Section 1256 were to apply to your Securities, gain or loss recognized with respect to your Securities (or a portion of your Securities) would be treated as 60% long-term capital gain or loss and 40% short-term capital gain or loss, without regard to your holding period in the Securities. You would also be required to mark your Securities (or a portion of your Securities) to market at the end of each year (i.e., recognize income as if the Securities or the relevant portion of the Securities had been sold for fair market value). The IRS might also assert that the Securities should be recharacterized for United States federal income tax purposes as instruments giving rise to current ordinary income (even before receipt of any cash) or that you should be required to recognize taxable gain on any rebalancing or rollover of the underlying asset. There may be also a risk that the IRS could additionally assert that the Securities should only give rise to short-term capital gain or loss because the Securities offer, at least in part, short exposure to the underlying asset.

IRS Notice 2008-2. Additionally, in 2007, the IRS released a notice that may affect the taxation of holders of the Securities. According to the notice, the IRS and the Treasury Department are actively considering whether the holder of an instrument similar to the Securities should be required to accrue ordinary income on a current basis, and they are seeking taxpayer comments on the subject. It is not possible to determine what guidance they will ultimately issue, if any. It is possible, however, that under such guidance, holders of the Securities will ultimately be required to accrue income currently and this could be applied on a retroactive basis. The IRS and the Treasury Department are also considering other relevant issues, including whether additional gain or loss from such instruments should be treated as ordinary or capital, whether foreign holders of such instruments should be subject to withholding tax on any deemed income accruals, and whether the special “constructive ownership rules” of Section 1260 of the Code should be applied to such instruments. Holders are urged to consult their tax advisors concerning the significance, and the potential impact, of the above considerations. Except to the extent otherwise required by law, UBS intends to treat your Securities for United States federal income tax purposes in accordance with the treatment described above unless and until such time as the Treasury Department and IRS determine that some other treatment is more appropriate.

Proposed Legislation. Moreover, in 2007, legislation was introduced in Congress that, if enacted, would have required holders of Securities purchased after the bill was enacted to accrue interest income over the term of the Securities despite the fact that there will be no interest payments over the term of the Securities. It is not possible to predict whether a similar or identical bill will be enacted in the future, or whether any such bill would affect the tax treatment of your Securities.

Also, in 2013, the House Ways and Means Committee released in draft form certain proposed legislation relating to financial instruments. If enacted, the effect of this legislation generally would be to require instruments such as the Securities to be marked to market on an annual basis with all gains and losses to be treated as ordinary, subject to certain exceptions. You are urged to consult your tax advisor regarding the draft legislation and its possible impact on you.

Medicare Tax on Net Investment Income

U.S. holders that are individuals, estates, and certain trusts will be subject to an additional 3.8% tax on all or a portion of their “net investment income,” which may include any income or gain realized with respect to the Securities, to the extent of their net investment income that when added to their other modified adjusted gross income, exceeds $200,000 for an unmarried individual, $250,000 for a married taxpayer filing a joint return (or a surviving spouse), or $125,000 for a married individual filing a separate return. The 3.8% Medicare tax is determined in a different manner than the income tax. U.S. holders should consult their tax advisors with respect to their consequences with respect to the 3.8% Medicare tax.

Information Reporting with respect to Foreign Financial Assets

U.S. holders that are individuals (and to the extent provided in future regulations, entities) that own “specified foreign financial assets” may be required to file information with respect to such assets with their U.S. federal income tax returns, especially if such assets are held outside the custody of a U.S. financial institution. “Specified foreign financial assets” include stock or other securities issued by foreign persons and any other financial instrument or contract that has an issuer or counterparty that is not a United States person. Individuals that fail to provide such information are subject to a penalty of $10,000 for the taxable year. You are urged to consult your tax advisor as to the application of this legislation to your ownership of the Securities.

Treasury Regulations Requiring Disclosure of Reportable Transactions

Treasury regulations require United States taxpayers to report certain transactions (“Reportable Transactions”) on IRS Form 8886. An investment in the Securities or a sale of the Securities should generally not be treated as a Reportable Transaction under current law, but it is possible that future legislation, regulations or administrative rulings could cause your investment in the Securities or a sale of the Securities to be treated as a Reportable Transaction. You should consult with your tax advisor regarding any tax filing and reporting obligations that may apply in connection with acquiring, owning and disposing of Securities.

13

Backup Withholding and Information Reporting

The proceeds received from a sale, exchange, automatic call or maturity of the Securities will be subject to information reporting unless you are an “exempt recipient” and may also be subject to backup withholding at the rate specified in the Code if you fail to provide certain identifying information (such as an accurate taxpayer number, if you are a U.S. holder) or meet certain other conditions. If you are a non-U.S. holder and you provide a properly executed and fully completed applicable IRS Form W-8, you will generally establish an exemption from backup withholding.

Amounts withheld under the backup withholding rules are not additional taxes and may be refunded or credited against your U.S. federal income tax liability, provided the required information is furnished to the IRS.

Non-U.S. Holders.

Subject to FATCA (as discussed below), if you are not a U.S. holder, you should generally not be subject to United States withholding tax with respect to payments on your Securities or to generally applicable information reporting and backup withholding requirements with respect to payments on your Securities if you comply with certain certification and identification requirements as to your foreign status (by providing us (and/or the applicable withholding agent) with a fully completed and duly executed appropriate IRS FormW-8). Gain from the sale, maturity or automatic call of a Security or settlement at maturity generally will not be subject to U.S. tax unless such gain is effectively connected with a trade or business conducted by the non-U.S. holder in the United States or unless the non-U.S. holder is a non-resident alien individual and is present in the U.S. for 183 days or more during the taxable year of such sale, maturity or automatic call and certain other conditions are satisfied, or has certain other present or former connections with the United States.