Table of Contents

Filed Pursuant to Rule 424(b)(3)

Registration Statement No. 333-204908

Table of Contents

| Amendment No. 1 dated December 15, 2015† to PRICING SUPPLEMENT dated October 8, 2015 (To Product Supplement dated October 8, 2015 and Prospectus dated June 12, 2015) |

$100,000,000 ETRACS Monthly Pay 2xLeveraged Mortgage REIT ETN Series B* due October 16, 2042

The ETRACS Monthly Pay 2xLeveraged Mortgage REIT ETN Series B due October 16, 2042 (the “Securities”) is a series of Monthly Pay 2xLeveraged ETRACS linked to the Market Vectors® Global Mortgage REITs Index (the “Index”). The Index tracks the overall performance of publicly-traded mortgage REITs that derive at least 50% of their revenues from mortgage-related activities. The Securities are senior unsecured debt securities issued by UBS AG (UBS). The Securities provide a monthly compounded two times leveraged long exposure to the performance of the Index, reduced by the Accrued Fees (as described below). Investing in the Securities involves significant risks. The Securities are two times leveraged with respect to the Index, and, as a result, will benefit from two times any positive, but will be exposed to two times any negative, compounded monthly performance of the Index. You will receive a cash payment at maturity, upon acceleration or upon exercise by UBS of its Call Right based on the compounded leveraged monthly performance of the Index less the Accrued Fees, calculated as described in the accompanying product supplement. You will receive a cash payment upon early redemption based on the monthly compounded leveraged performance of the Index less the Accrued Fees and the Redemption Fee, calculated as described in the accompanying product supplement. The Securities may pay a monthly coupon during their term linked to two times the cash distributions, if any, on the Index Constituent Securities.

The Securities do not guarantee any return of your initial investment and may not pay any coupon. You may lose some or all of your principal if you invest in the Securities. If the compounded leveraged monthly return of the Index (calculated as described herein) is not sufficient to offset the negative effect of the Accrued Fees and the Redemption Fee, if applicable, (each as calculated as described in the accompanying product supplement, you may lose some or all of your investment. Any payment at maturity or call, upon early redemption or upon acceleration is subject to the creditworthiness of UBS and is not guaranteed by any third party. In addition, the actual and perceived creditworthiness of UBS will affect the market value, if any, of the Securities.

See “Risk Factors” beginning on page PS-1 of this pricing supplement and on page S-17 of the accompanying product supplement for a description of risks related to an investment in the Securities.

The general terms of the Monthly Pay 2xLeveraged ETRACS are described in the accompanying product supplement under the heading “General Terms of the Securities”, beginning on page S-34 in the product supplement. These general terms include, among others, the manner in which any payments on the Securities will be calculated, such as the Cash Settlement Amount at Maturity, the Redemption Amount, the Call Settlement Amount or the Acceleration Amount, as applicable, and the Coupon Amount, if any. These general terms are supplemented and modified by the specific terms of the Securities listed below and in “Additional Terms of the Securities” on page PS-27 of this pricing supplement. Capitalized terms used herein but not otherwise defined have the meanings specified in the accompanying product supplement. To the extent there are differences between the terms of the Securities described in this pricing supplement and the terms described in the product supplement, the terms of the Securities described in this pricing supplement control.

Issuer: | UBS AG (London Branch) |

Series: | Medium-Term Notes, Series B* |

Initial Trade Date: | October 8, 2015 |

Initial Settlement Date: | October 14, 2015 |

Term: | Approximately 27 years, subject to your right to receive payment for your Securities upon redemption, acceleration upon minimum indicative value or exercise of the UBS Call Right, each as described in the accompanying product supplement. |

Maturity Date: | October 16, 2042, subject to adjustment. |

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this pricing supplement, the accompanying product supplement or the accompanying prospectus. Any representation to the contrary is a criminal offense.

The Securities are not deposit liabilities of UBS AG and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency in the United States, Switzerland or any other jurisdiction.

| UBS Investment Bank | (cover continued on next page) |

Pricing Supplement dated December 15, 2015

| * | UBS AG Exchange Traded Access Securities (ETRACS) issued prior to June 14, 2015 are part of a series of debt securities entitled “Medium-Term Notes, Series A,” and UBS Switzerland AG is a co-obligor of such debt securities. The Securities are part of a series of debt securities entitled “Medium Term Notes, Series B,” which do not benefit from the co-obligation of UBS Switzerland AG. The Securities are intended to have the same economic terms as the Series A debt securities entitled “ETRACS Monthly Pay 2xLeveraged Mortgage REIT ETN due October 16, 2042” (the “Series A REIT ETRACS”), except for (i) the date of issuance of the Securities, (ii) the lack of the co-obligation of UBS Switzerland AG, (iii) the first day on which UBS may exercise its Call Right and (iv) certain other changes relating to the calculation of the Current Principal Amount, Coupon Amounts and Accrued Fees with respect to the initial calendar month of the Securities, intended to conform the terms of the Securities to the Series A REIT ETRACS. |

Table of Contents

Stated Principal Amount: | $25.00 per Security |

Underlying Index: | The return on the Securities is linked to the performance of the Market Vectors® Global Mortgage REITs Index. The Index tracks the overall performance of publicly-traded U.S. and non-U.S. mortgage REITs that derive at least 50% of their revenues from mortgage-related activity. As of the date of this pricing supplement, however, the Index contained only U.S. mortgage REITs. See “The Market Vectors® Global Mortgage REITs Index”. |

Coupon Payment Dates: | The 15th Trading Day following each Coupon Valuation Date, commencing on November 20, 2015 (subject to adjustment). The final Coupon Payment Date will be the Maturity Date. |

Initial Coupon Valuation Date: | October 30, 2015 |

Annual Tracking Fee: | 0.40% per annum |

Financing Spread (component

of the Financing Rate): | 0.40% per annum |

First Redemption Date: | October 15, 2015 |

Final Redemption Date: | October 9, 2042 |

First Call Settlement Date: | The first date that UBS may exercise its Call Right is October 17, 2016. |

Current Principal Amount: | For the period from the Initial Trade Date to the initial Monthly Valuation Date (such period, the “Initial Calendar Month”), the Current Principal Amount will equal $13.6835 per Security of any series. For each subsequent calendar month, the Current Principal Amount will be reset as follows on the Monthly Reset Date: |

| New Current Principal Amount = previous Current Principal Amount × Index Factor on the applicable Monthly Valuation Date - Accrued Fees on the applicable Monthly Valuation Date |

| If the Securities undergo a split or reverse split, the Current Principal Amount will be adjusted accordingly. |

Current Indicative Value: | The Current Indicative Value will be calculated as described in the accompanying product supplement. As of October 7, 2015, the Current Indicative Value was 14.8663. |

Monthly Initial Closing

Level for the Initial Calendar

Month: | 283.2, the Index Closing Level on September 30, 2015. |

Monthly Reset Dates: | For each calendar month, the Monthly Reset Date is the first Trading Day of that month beginning on November 1, 2015 and ending on October 1, 2042, subject to adjustment. |

Monthly Valuation Dates: | For each Monthly Reset Date, the Monthly Valuation Date is the last Trading Day of the previous calendar month, beginning on October 30, 2015 and ending on September 30, 2042, subject to adjustment. |

Index Calculation Agent: | Solactive AG |

Index Divisor: | As of any date of determination, the divisor used by the Index Calculation Agent to calculate the level of the Index, as further described under “The Market Vectors® Global Mortgage REITs Index — Calculation and Adjustments” beginning on page PS-21.” |

Calculation Date: | October 7, 2042, unless that day is not a Trading Day, in which case the Calculation Date will be the next Trading Day, subject to adjustment. |

Listing: | The Securities have been approved for listing, subject to official notice of issuance, on NYSE Arca under the symbol “MRRL”. There can be no assurance that an active secondary market will develop; if it does, we expect that investors will purchase and sell the Securities primarily in this secondary market. |

Indicative Value: | The term “indicative value” refers to the value at a given time and date equal to (i) Current Principal Amount multiplied by the Index Factor calculated using the intraday indicative value of the relevant Index as of such time as the Index Valuation Level, plus (ii) assuming such time and date is the Redemption Valuation Date, the Coupon Amount with respect to the Coupon Valuation Date if on such Redemption Valuation Date the Coupon Ex-Date with respect to such Coupon Amount has not yet occurred; plus (iii) the Stub Reference Distribution Amount, if any, as of such time and date, assuming such time and date is the Redemption Valuation Date, minus (iv) the Accrued Fees as of such time and date, assuming such time and date is the Redemption Valuation Date. The actual trading price of the Securities in the secondary market may vary significantly from the indicative value. |

Indicative Value Symbol of

the Securities: | The closing indicative value and of the Securities and the intraday indicative value of the Securities will be published on each Index Business Day under the ticker symbols: |

| MRRLIV <INDEX> (Bloomberg); ^MRRL-IV (Yahoo! Finance) |

Intraday Index Value: | The “Intraday Index Value” means the value, as calculated by the Index Calculation Agent, of the Index, as published by Bloomberg under the symbol “MVMORT” and by Reuters under the symbol “MVMORT”. |

Table of Contents

Accrued Tracking Fee: | The Accrued Tracking Fee with respect to the initial Monthly Valuation Date is an amount equal to the product of: (a) the Annual Tracking Fee as of the initial Monthly Valuation Date and (b) a fraction, the numerator of which is the total number of calendar days from, but excluding, September 30, 2015, to, and including, the initial Monthly Valuation Date, and the denominator of which is 365. |

| The Accrued Tracking Fee with respect to any Monthly Valuation Date other than the first Monthly Valuation Date is an amount equal to the product of: (a) the Annual Tracking Fee as of such Monthly Valuation Date and (b) a fraction, the numerator of which is the total number of calendar days from, but excluding, the immediately preceding Monthly Valuation Date to, and including, such Monthly Valuation Date, and the denominator of which is 365. |

| The Accrued Tracking Fee as of the last Trading Day of the applicable Measurement Period, or as of the Redemption Valuation Date, as applicable, is an amount equal to the product of: (a) the Annual Tracking Fee calculated as of the last Trading Day of such Measurement Period, or as of such Redemption Valuation Date, as applicable, and (b) a fraction, the numerator of which is the total number of calendar days from, but excluding, the immediately preceding Monthly Valuation Date to, and including, (i) such last Trading Day of such Measurement Period, or (ii) such Redemption Valuation Date (or if the Acceleration Date or Redemption Valuation Date occurs prior to the initial Monthly Valuation Date, the period from, and excluding, September 30, 2015), as applicable, and the denominator of which is 365. |

Accrued Financing Charge: | On the initial Monthly Valuation Date, the Accrued Financing Charge for each Security will equal (a) the aggregate sum of (i) the Financing Level as of each date starting from, but excluding, September 30, 2015 to, and including, the initial Monthly Valuation Date times (ii) the Financing Rate as of such date, divided by (b) 360. |

| On any subsequent Monthly Valuation Date, the Accrued Financing Charge for each Security will equal (a) the aggregate sum of (i) the Financing Level as of each date starting from, but excluding, the immediately preceding Monthly Valuation Date to, and including, the then current Monthly Valuation Date times (ii) the Financing Rate as of such date, divided by (b) 360. |

| The Accrued Financing Charge as of the last Trading Day of the applicable Measurement Period, or as of any Redemption Valuation Date, as applicable, is an amount equal to (a) the aggregate sum of (i) the Financing Level as of each date starting from, but excluding, the immediately preceding Monthly Valuation Date (or, if the Redemption Valuation Date falls in the Initial Calendar Month, starting from, but excluding, September 30, 2015) to, and including, such last Trading Day in such Measurement Period, or such Redemption Valuation Date, as applicable, times (ii) the Financing Rate as of such date, divided by (b) 360. |

| The Accrued Financing Charge seeks to compensate UBS for providing investors with the potential to receive a leveraged participation in movements in the Index Closing Level and is intended to approximate the financing costs that investors may have otherwise incurred had they sought to borrow funds at a similar rate from a third party to invest in the Securities. These charges accrue on a daily basis during the applicable period. |

Reference Distribution Amount: | (i) As of the first Coupon Valuation Date, an amount equal to the cash distributions that a Reference Holder would have been entitled to receive in respect of the Index Constituent Securities held by such Reference Holder on the “record date” with respect to any such securities for those cash distributions whose “ex-dividend date” occurs during the period from and excluding September 30, 2015 to and including the first Coupon Valuation Date; and (ii) as of any other Coupon Valuation Date, an amount equal to the cash distributions that a Reference Holder would have been entitled to receive in respect of such securities held by such Reference Holder on the “record date” with respect to any such securities for those cash distributions whose “ex-dividend date” occurs during the period from and excluding the immediately preceding Coupon Valuation Date to and including such Coupon Valuation Date. |

Stub Reference Distribution Amount: | The “Stub Reference Distribution Amount” as of the last Trading Day in the applicable Measurement Period or as of the Redemption Valuation Date, as applicable, is an amount equal to the cash distributions that a Reference Holder would have been entitled to receive in respect of the Index Constituent Securities held by such Reference Holder on the “record date” with respect to any such securities for those cash distributions whose “ex-dividend date” occurs during the period from, but excluding, the immediately preceding Coupon Valuation Date (or if such Redemption Valuation Date or the Acceleration Date occurs prior to the first Coupon Valuation Date, the period from but excluding, September 30, 2015) to, and including, such last Trading Day of such Measurement Period or such Redemption Valuation Date, as applicable; provided that, for the purpose of calculating the Stub Reference Distribution Amount as of such last Trading Day of such Measurement Period, the Reference Holder will be deemed to hold on each Trading Day in such Measurement Period ((t-d)/t) of the shares of such securities it would otherwise hold on each of the Trading Days in such Measurement Period beginning on the second Trading Day in such Measurement Period until and including the final Trading Day in such Measurement Period. For purposes of this definition, d = the number of Trading Days that have occurred in the applicable Measurement Period. For purposes of this definition, “t” equals the number of Trading Days in the applicable Measurement Period. Such cash distributions may be adjusted to account for withholding taxes imposed by the taxing authority of the applicable Index Constituent and for any fees related to such cash distributions. In the event of such an adjustment, UBS would not be |

Table of Contents

required to pay any of the additional amounts described in the accompanying prospectus under “Description of Debt Securities We May Offer – Payment of Additional Amounts”. Notwithstanding the foregoing, with respect to the cash distributions for any such securities that are scheduled to be paid prior to the applicable Coupon Ex-Date, if, and only if, the issuer of such security fails to pay the distribution to holders of such securities by the scheduled payment date for such distribution, such distribution will be assumed to be zero for the purposes of calculating the applicable Stub Reference Distribution Amount. Any cash distributions on the Index Constituent Securities that are paid in a non-U.S. dollar currency will be converted into U.S. dollars for purposes of calculating the Stub Reference Distribution Amount. |

Related Definitions: | See “Additional Terms of the Securities” beginning on page PS-27 for the definitions of “Trading Day,” “Primary Exchange” and “cash distributions.” |

CUSIP No.: | 90274D432 |

ISIN No.: | US90274D4328 |

On the Initial Trade Date, we sold $37,500,000 aggregate principal amount of Securities (1,500,000 Securities) to UBS Securities LLC at the closing indicative value of the Series A REIT ETRACS on October 8, 2015, as calculated by the NYSE and published by Bloomberg. After the Initial Trade Date, from time to time we may sell a portion of these Securities and issue and sell additional Securities at market prices prevailing at the time of sale, at prices related to market prices or at negotiated prices. We expect to receive proceeds equal to 100% of the offering price at which the Securities are sold, less any commissions paid to UBS Securities LLC and UBS Financial Services Inc. The Securities may be sold at a price that is higher or lower than the Stated Principal Amount. UBS Securities LLC and UBS Financial Services Inc. may charge normal commissions for the sale of the Securities and may also receive a portion of the Annual Tracking Fee in connection with future distributions.

Please see “Supplemental Plan of Distribution” on page PS-32 for more information.

We may use this prospectus supplement in the initial sale of the Securities. In addition, UBS Securities LLC, UBS Financial Services Inc. or another of our affiliates may use this prospectus supplement in market-making transactions in any Securities after their initial sale.Unless we or our agent informs you otherwise in the confirmation of sale or in a notice delivered at the same time as the confirmation of sale, this prospectus supplement is being used in a market-making transaction.

| † | This Amendment No. 1 to the pricing supplement dated October 8, 2015 (as amended, the “pricing supplement”) is being filed for the purposes of updating (i) “Risk Factors,” (ii) “The Market Vectors® Global Mortgage REITs Index” and (iii) “Material U.S. Federal Income Tax Consequences.” Otherwise, all terms of the Securities remain as stated in the pricing supplement. |

Table of Contents

UBS has filed a registration statement (including a prospectus as supplemented by a product supplement) with the Securities and Exchange Commission, or SEC, for the offering to which this pricing supplement relates. Before you invest, you should read these documents and any other documents relating to this offering that UBS has filed with the SEC for more complete information about UBS and this offering. You may obtain these documents for free from the SEC website at www.sec.gov. Our Central Index Key, or CIK, on the SEC website is 0001114446. Alternatively, UBS will arrange to send you these documents if you so request by calling toll-free 800-722-7370.

You may access these documents on the SEC website at www.sec.gov as follows:

Prospectus dated June 12, 2015:

http://www.sec.gov/Archives/edgar/data/1114446/000119312515222010/d935416d424b3.htm

Product Supplement dated October 8, 2015:

http://www.sec.gov/Archives/edgar/data/1114446/000119312515340228/d79385d424b2.htm

References to “UBS” “we” “our” and “us” refer only to UBS AG and not to its consolidated subsidiaries. Also, references to the “accompanying prospectus” mean the UBS prospectus titled “Debt Securities and Warrants,” dated June 12, 2015, and references to the “accompanying product supplement” mean the UBS product supplement “UBS AG Monthly Pay 2xLeveraged Exchange Traded Access Securities (ETRACS)” dated October 8, 2015.

You should rely only on the information incorporated by reference or provided in this pricing supplement, the accompanying product supplement or the accompanying prospectus. We have not authorized anyone to provide you with different information. We are not making an offer of the Securities in any state where the offer is not permitted. You should not assume that the information in this pricing supplement, the accompanying product supplement or the accompanying prospectus is accurate as of any date other than the date on the front of the document.

UBS reserves the right to change the terms of, or reject any offer to purchase, the Securities prior to their issuance. In the event of any changes to the terms of the Securities, UBS will notify you and you will be asked to accept such changes in connection with your purchase. You may also choose to reject such changes in which case UBS may reject your offer to purchase.

i

Table of Contents

The Securities, are part of a single series of senior debt securities issued under our indenture, dated as of June 12, 2015 between us and U.S. Bank Trust National Association, as trustee.

Your investment in the Securities involves significant risks. The Securities are not secured debt and are significantly riskier than ordinary unsecured debt securities. Unlike ordinary debt securities, the return on the Securities is linked to the performance of the Index. The Securities are two times leveraged with respect to the Index and, as a result, may benefit from two times any positive, but will be exposed to two times any negative, monthly performance of the Index. As described in more detail below, the trading price of the Securities may vary considerably before the Maturity Date, due to events that are difficult to predict and beyond our control. Investing in the Securities is not equivalent to investing directly in the Index Constituent Securities (as defined in the accompanying product supplement) or the Index itself.

As more fully described in the accompanying product supplement, investing in the Securities, a series of Monthly Pay 2xLeveraged Exchange Traded Access Securities (ETRACS), involves significant risks. In addition to the risks relating to the Index and mortgage REITs, the structure of the Securities involves the risk of loss of your entire investment, leverage risk, correlation and compounding risk and market risk, among other complex risks. In addition, you may not receive monthly coupons during the term of the Securities. As a result, the Securities may not be a suitable investment for some investors. We urge you to read the more detailed explanation of these risks described under “Risk Factors” in the accompanying product supplement, together with “Considerations Relating to Indexed Securities” in the accompanying prospectus and the other information in this pricing supplement, the accompanying product supplement and the accompanying prospectus, before investing in the Securities.

Risk of Investing in Mortgage REITs.

Mortgage real estate investment trusts (“REITs”) are exposed to the risks specific to the real estate market as well as the risks that relate specifically to the way in which mortgage REITs are organized and operated. Mortgage REITs receive principal and interest payments from the owners of the mortgaged properties. Accordingly, mortgage REITs are subject to the credit risk of the borrowers to whom they extend credit. Credit risk refers to the possibility that the borrower will be unable and/or unwilling to make timely interest payments and/or repay the principal on the loan to a mortgage REIT when due. To the extent that a mortgage REIT invests in mortgage-backed securities offered by private issuers, such as commercial banks, savings and loan institutions, private mortgage insurance companies, mortgage bankers and other secondary market issuers, the mortgage REIT may be subject to additional risks. Timely payment of interest and principal of non-governmental issuers may be supported by various forms of private insurance or guarantees, including individual loan, title, pool and hazard insurance purchased by the issuer. There can be no assurance that the private insurers can meet their obligations under the applicable insurance policies or guarantees. Unexpected high rates of default on the mortgages held by a mortgage pool may adversely affect the value of a mortgage-backed security and could result in losses to a mortgage REIT. The risk of such defaults is generally higher in the case of mortgage pools that include subprime mortgages. To the extent that a mortgage REIT’s portfolio is exposed to lower-rated, unsecured or subordinated instruments, the risk of loss may increase, which may have a negative impact on the Securities.

Mortgage REITs are subject to significant interest rate risk. Interest rate risk refers to fluctuations in the value of a mortgage REIT’s investment in fixed rate obligations resulting from changes in the general level of interest rates. When the general level of interest rates goes up, the value of a mortgage REIT’s investment in fixed rate obligations goes down. When the general level of interest rates goes down, the value of a mortgage REIT’s investment in fixed rate obligations goes up.

PS-1

Table of Contents

Risk Factors

Mortgage REITs typically use leverage and many are highly leveraged, which exposes them to leverage risk. Leverage risk refers to the risk that leverage created from borrowing may impair a mortgage REIT’s liquidity, cause it to liquidate positions at an unfavorable time and increase the volatility of the values of securities issued by the mortgage REIT. The use of leverage may not be advantageous to a mortgage REIT. The success of using leverage is dependent on whether the investments made using the proceeds of leverage exceed the cost of using leverage. To the extent that a mortgage REIT incurs significant leverage, it may incur substantial losses if its borrowing costs increase. Borrowing costs may increase for any of the following reasons: short term interest rates increase; the market value of a mortgage REIT’s assets decrease; interest rate volatility increases; or the availability of financing in the market decreases. During periods of adverse market conditions the use of leverage may cause a mortgage REIT to lose more money than would have been the case if leverage was not used.

Mortgage REITs are subject to prepayment risk, which is the risk that borrowers may prepay their mortgage loans at faster than expected rates. Prepayment rates generally increase when interest rates fall and decrease when interest rates rise. These faster than expected payments may adversely affect a mortgage REIT’s profitability because the mortgage REIT may be forced to replace investments that have been redeemed or repaid early with other investments having a lower yield. Additionally, rising interest rates may cause the duration of a mortgage REIT’s investments to be longer than anticipated and increase such investments’ interest rate sensitivity.

REITs are subject to special U.S. federal tax requirements. A REIT’s failure to comply with these requirements may negatively affect its performance.

Mortgage REITs may be dependent upon their management skills and may have limited financial resources. Mortgage REITs are generally not diversified and may be subject to heavy cash flow dependency, default by borrowers and self-liquidation. In addition, transactions between mortgage REITs and their affiliates may be subject to conflicts of interest which may adversely affect a mortgage REIT’s shareholders.

The Index value is subject to foreign currency exchange rate risk.

As of December 11, 2015, the Index contained only U.S. mortgage REITs. However, as a global mortgage REIT index, the Index may, at a future time, also contain non-U.S. mortgage REITs. As necessary, the Index Calculation Agent will convert each Index Constituent Security to U.S. Dollars. The real-time Index values are calculated with the midpoint between the latest available real-time bid- and ask-prices. The closing Index values are calculated at 22:40:00 CET with fixed 17:00 CET exchange rates from WM company (please see Reuters page WMRSPOT01 or Bloomberg pages WMCO). A Security holder’s net exposure will depend on the extent to which the currencies represented in the Index strengthen or weaken against the U.S. Dollar and the relative weighting of each relevant currency represented in the Index. If, taking into account such weighting, the U.S. Dollar strengthens against the component currencies of the various Index Constituent Securities, the value of the Index (as measured by the Index Valuation Level) will be adversely affected and the amount payable at maturity or call, upon acceleration or upon early redemption may be reduced.

Foreign currency exchange rates vary over time, and may vary considerably during the term of the Securities. Changes in a particular exchange rate result from the interaction of many factors directly or indirectly affecting economic and political conditions. Of particular importance are:

| Ø | rates of inflation; |

| Ø | interest rate levels; |

PS-2

Table of Contents

Risk Factors

| Ø | the balance of payments among countries; |

| Ø | the extent of government surpluses or deficits in the relevant foreign country and the United States; |

| Ø | government or central bank intervention, or intervention by supranational entities, in each case in the foreign exchange or other financial markets; and |

| Ø | other financial, economic, military and political factors. |

All of these factors are, in turn, sensitive to the monetary, fiscal and trade policies pursued by the governments of the relevant foreign countries and the United States and other countries important to international trade and finance.

The intraday indicative value of the Securities and payment at maturity or call, upon acceleration or upon early redemption could also be adversely affected by delays in, or refusals to grant, any required governmental approval for conversions of a local currency and remittances abroad with respect to the relevant Index Constituent Securities or other de facto restrictions on the repatriation of U.S. Dollars.

The Coupon Amount, Reference Distribution Amount and Stub Reference Distribution Amount are subject to exchange rate risk.

The Reference Distribution Amount and the Stub Reference Distribution Amount (each as defined in the accompanying product supplement) are calculated based on the cash distributions, if any, of the Index Constituent Securities. Coupon Amounts (as defined in the accompanying product supplement), if any, are based on the Reference Distribution Amount and will be paid in U.S. Dollars. Because some of the cash distributions on the Index Constituent Securities may, at a future time, be paid in non-U.S. Dollar currencies, they will, as necessary, be converted into U.S. Dollars by the Calculation Agent as described in this pricing supplement under “Additional Terms of the Securities” and, consequently, will be subject to exchange rate risk.

Potential exposure to exchange rate risk will depend on the extent to which the non-U.S. Dollar currency strengthens or weakens against the U.S. Dollar. If the U.S. Dollar strengthens against the relevant non-U.S. Dollar currency, the U.S. Dollar value of the Index Constituent Security’s cash distributions will be adversely affected and the Coupon Amount, Reference Distribution Amount and Stub Reference Distribution Amount will be reduced.

Foreign currency exchange rates vary over time, and may vary considerably during the term of any series of the Securities. Changes in a particular exchange rate result from the interaction of many factors directly or indirectly affecting economic and political conditions. Of particular importance are:

| Ø | rates of inflation; |

| Ø | interest rate levels; |

| Ø | the balance of payments among countries; |

| Ø | the extent of government surpluses or deficits in the relevant foreign country and the United States; |

| Ø | government or central bank intervention, or intervention by supranational entities, in each case in the foreign exchange or other financial markets; and |

| Ø | other financial, economic, military and political factors. |

PS-3

Table of Contents

Risk Factors

All of these factors are, in turn, sensitive to the monetary, fiscal and trade policies pursued by the governments of the relevant foreign countries and the United States and other countries important to international trade and finance. See “Additional Terms of the Securities” for more information about cash distributions.

Risk of Investing in the Financial Services Sector.

The financial services sector includes companies engaged in banking, commercial and consumer finance (such as mortgage REITs), investment banking, brokerage, asset management, custody or insurance. Because as currently constituted the Index is concentrated in mortgage REITs, which operate in the financial services sector, the Securities are sensitive to changes in, and its performance may depend on, the overall condition of the financial services sector. Companies in the financial services sector may be subject to extensive government regulation that affects the scope of their activities, the prices they can charge and the amount of capital they must maintain. The profitability of companies in the financial services sector may be adversely affected by increases in interest rates. The profitability of companies in the financial services sector may be adversely affected by loan losses, which usually increase in economic downturns. In addition, the financial services sector is undergoing numerous changes, including continuing consolidations, development of new products and structures and changes to its regulatory framework. Furthermore, increased government involvement in the financial services sector, including measures such as taking ownership positions in financial institutions, could result in a dilution of the Index’s concentration in financial institutions. Developments in the credit markets since the 2008 financial crisis have caused companies operating in the financial services sector to incur large losses, experience declines in the value of their assets and even cease operations.

Risk of Investing in the Real Estate Industry.

The Index is comprised of companies that invest in real estate, such as mortgage REITs, which subjects the value of the Index to many of the risks of owning real estate directly. Therefore, adverse economic, business or political developments affecting the value of real estate could have a major effect on the value of the Securities.

Risk of Investing in Small- and Medium-Capitalization Companies.

The Index is comprised of small- and medium-capitalization companies. Such companies may be more volatile and more likely than large-capitalization companies to have narrower product lines, fewer financial resources, less management depth and experience and less competitive strength. Returns on investments in securities of these companies could trail the returns on investments in securities of larger companies.

The calculation of the Reference Distribution Amount and Stub Reference Distribution Amount may have to take into account withholding taxes, consequently reducing the Coupon Amount.

As discussed above, the Reference Distribution Amount and the Stub Reference Distribution Amount are calculated based on the cash distributions, if any, on the Index Constituent Securities. Such cash distributions may be adjusted to account for withholding taxes imposed by the taxing authority of the applicable Index Constituent Security. Such taxes could reduce any potential Coupon Amount. In the event that the calculation of the Reference Distribution Amount or the Stub Reference Distribution Amount is affected by any applicable withholding taxes, UBS will not compensate for those withholding taxes by paying the additional amounts described in the accompanying prospectus under “Description of Debt Securities We May Offer — Payment of Additional Amounts”.

PS-4

Table of Contents

Risk Factors

Even though currencies trade around-the-clock, the Securities will not.

As discussed above, the closing levels for the Index Constituent Securities on their primary markets are adjusted by the Index Calculation Agent to reflect their U.S. Dollar value in calculating the Index Closing Level. Similarly, any non-U.S. Dollar currencies in which the cash distributions on the Index Constituent Securities are paid will be converted into U.S. Dollars in calculating the Coupon Amount. The interbank market in foreign currencies is a global, around-the-clock market. Therefore, the hours of trading for the Securities, if any trading market develops, will not conform to the hours during which the currencies in which the Index Constituent Securities or the cash distributions thereon are denominated or in which the Index Constituent Securities. Significant price and rate movements may take place in the underlying foreign currency exchange markets that will not be reflected immediately in the price of your Securities. The possibility of these movements should be taken into account in relating the value of your Securities to those in the underlying foreign currency exchange markets. There is no systematic reporting of last-sale information for foreign currencies. Reasonably current bid and offer information is available in certain brokers’ offices, in bank foreign currency trading offices and to others who wish to subscribe for this information, but this information will not necessarily be reflected in the Index Closing Level, Index Valuation Level or the Coupon Amount. There is no regulatory requirement that those quotations be firm or revised on a timely basis. The absence of last-sale information and the limited availability of quotations to individual investors may make it difficult for many investors to obtain timely, accurate data about the state of the underlying foreign currency exchange markets.

Intervention in the foreign currency exchange markets by the countries issuing any currency of an Index Constituent Security could materially and adversely affect the value of the Securities and the Coupon Amount.

Specific foreign currencies’ exchange rates are volatile and are affected by numerous factors specific to each foreign country. Foreign currency exchange rates can be fixed by the sovereign government, allowed to float within a range of exchange rates set by the government, or left to float freely. Governments, including those issuing the currencies in which the Index Constituent Securities trade, use a variety of techniques, such as intervention by their central bank or imposition of regulatory controls or taxes, to affect the exchange rates of their respective currencies. Currency developments may occur in any of the countries issuing the currencies in which the Index Constituent Securities trade and in which the cash distributions on the Index Constituent Securities are made. Often, these currency developments impact foreign currency exchange rates in ways that cannot be predicted.

Governments may also issue a new currency to replace an existing currency, fix the exchange rate or alter the exchange rate or relative exchange characteristics by devaluation or revaluation of a currency. Thus, a special risk in purchasing the Securities is that their liquidity, trading value and payment amount could be affected by the actions of sovereign governments that could change or interfere with previously freely determined currency valuations, fluctuations in response to other market forces and the movement of currencies across borders.

The Calculation Agent is not obligated to make any offsetting adjustment or change in the event of any other devaluation or revaluation or imposition of exchange or other regulatory controls or taxes or in the event of other developments affecting Index Constituent Securities whose closing prices on their primary markets are converted into U.S. Dollars by the Index Calculation Agent. The Calculation Agent is also not obligated to make any such offsetting adjustment or change with respect to cash distributions on the Index Constituent Securities, if such cash distributions are made in non-U.S. Dollar currencies, when calculating the Reference Distribution Amount, Stub Reference Distribution Amount or Coupon Amount.

PS-5

Table of Contents

Risk Factors

Suspensions or disruptions in market trading in one or more foreign currencies may adversely affect the value of the Securities and the Coupon Amount.

The foreign currency exchange markets are subject to temporary distortions or other disruptions due to various factors, including government regulation and intervention, the lack of liquidity in the markets and the participation of speculators. Because the closing levels for the Index Constituent Securities on their primary markets are adjusted by the Index Calculation Agent to reflect their U.S. Dollar value in calculating the Index Closing Level, these circumstances could adversely affect the relevant foreign currency exchange rates and, therefore, the amount payable at maturity or call, upon acceleration or upon early redemption may be reduced. Those same circumstances could also cause an adverse effect on the Coupon Amount, if any.

The Securities are exposed to risks associated with foreign securities markets.

The Index may include stocks issued by foreign companies. You should be aware that investments in securities linked to the value of foreign equity securities involve particular risks. The foreign securities markets in which the Index Constituent Securities trade may have less liquidity and may be more volatile than U.S. or other securities markets and market developments may affect foreign markets differently from U.S. or other securities markets. Direct or indirect government intervention to stabilize these foreign securities markets, as well as cross-shareholdings in foreign companies, may affect trading prices and volumes in these markets. Also, there is generally less publicly available information about foreign companies than about those U.S. companies that are subject to the reporting requirements of the U.S. Securities and Exchange Commission, and foreign companies are subject to accounting, auditing and financial reporting standards and requirements that differ from those applicable to U.S. reporting companies.

Securities prices in foreign countries are subject to political, economic, financial and social factors that apply in those geographical regions. These factors, which could negatively affect those securities markets, include the possibility of recent or future changes in a foreign government’s economic and fiscal policies, the possible imposition of, or changes in, currency exchange laws or other laws or restrictions applicable to foreign companies or investments in foreign equity securities and the possibility of fluctuations in the rate of exchange between currencies, the possibility of outbreaks of hostility and political instability and the possibility of natural disaster or adverse public health development in the region. Moreover, foreign economies may differ favorably or unfavorably from the U.S. economy in important respects such as growth of gross national product, rate of inflation, capital reinvestment, resources and self-sufficiency.

Certain of the countries in which the primary market for any Index Constituent Security is located may be considered to be countries with emerging market economies. Countries with emerging market economies may have relatively less stable governments, may present the risks of nationalization of businesses, restrictions on foreign ownership and prohibitions on the repatriation of assets, and may have less protection of property rights than more developed countries. Emerging market economies may be based on only a few industries, may be highly vulnerable to changes in local or global trade conditions, and may suffer from extreme and volatile debt burdens or inflation rates. Local securities markets may trade a small number of securities and may be unable to respond effectively to increases in trading volume, potentially making prompt liquidation of holdings difficult or impossible at times.

UBS and its affiliates have no affiliation with the Index Sponsor and are not responsible for its public disclosure of information.

We and our affiliates are not affiliated with the Index Sponsor (except for the licensing arrangements discussed under “Market Vectors® Global REITs Index — Licensing Agreement”) and have no ability to control or predict its actions, including any errors in or discontinuation of public disclosure regarding

PS-6

Table of Contents

Risk Factors

methods or policies relating to the calculation of the Index. If the Index Sponsor discontinues or suspends the calculation of the Index, it may become difficult to determine the market value of the Securities and the payment at maturity or call, upon acceleration or upon early redemption. The Calculation Agent may designate a successor index in its sole discretion. If the Calculation Agent determines in its sole discretion that no successor index comparable to the Index exists, the payment you receive at maturity or call, upon acceleration or upon early redemption will be determined by the Calculation Agent in its sole discretion. See “General Terms of the Securities — Market Disruption Event” and “— Calculation Agent” in the accompanying product supplement. The Index Sponsor is not involved in the offer of the Securities in any way and has no obligation to consider your interest as an owner of the Securities in taking any actions that might affect the market value of your Securities.

We have derived the information about the Index Sponsor and the Index from publicly available information, without independent verification. Neither we nor any of our affiliates assume any responsibility for the adequacy or accuracy of the information about the Index Sponsor or the Index contained in this pricing supplement.You, as an investor in the Securities, should make your own independent investigation into the Index Sponsor and the Index.

There are uncertainties regarding the Index because of its limited performance history.

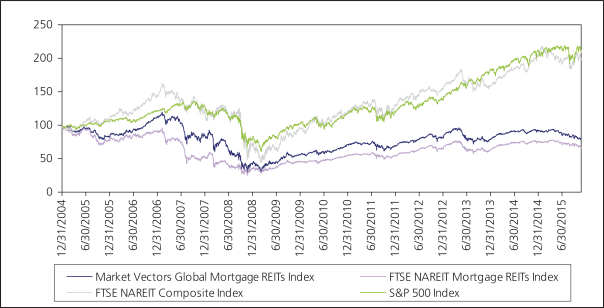

The Index was first calculated on August 4, 2011, and therefore has no performance history prior to that date. As a result, little or no historical information is available for you to consider in making an independent investigation of the Index performance, which may make it difficult for you to make an informed decision with respect to an investment in the Securities. The base value of the Index was set at 1000 on December 30, 2004, and, therefore, we are able to provide hypothetical, or “backtested,” Index returns. This data may be considered when making an investment decision concerning the Securities and evaluating the potential performance of the Index, but it is solely hypothetical and does not guarantee future performance.

The Securities may trade at a substantial premium to or discount from the intraday indicative value.

The market value of the Securities is influenced by many unpredictable factors, some of which may cause the price at which the Securities can be sold in the secondary market to vary substantially from the intraday indicative value that is calculated and disseminated throughout trading hours. For example, if UBS were to suspend sales of the Securities for any reason, the liquidity of the market for the Securities could be affected, potentially leading to insufficient supply, causing the market price of the Securities to increase. Such an increase could represent a premium over the intraday indicative value of the Securities. Before trading in the secondary market, you should compare the intraday indicative value of the Securities with the then-prevailing trading price of the Securities.

Conversely, suspension of additional issuances of the Securities can also result in a significant reduction in the number of outstanding Securities if investors subsequently exercise their early redemption right. If the total number of outstanding Securities has fallen to a level that is close to or below the minimum redemption amount, you may not be able to purchase enough Securities to meet the minimum size requirement in order to exercise your early redemption right. The unavailability of the redemption right could result in the Securities trading in the secondary market at discounted prices below the intraday indicative value. Having to sell your Securities at a discounted market price below the intraday indicative value of the Securities could lead to significant losses or the loss of your entire investment. Prior to making an investment in the Securities, you should take into account whether or not the market price is tracking the intraday indicative value of the Securities.

PS-7

Table of Contents

Risk Factors

The Securities are part of a series of UBS AG debt securities entitled “Medium-Term Notes, Series B” and do not benefit from a co-obligation of UBS Switzerland AG.

UBS AG Exchange Traded Access Securities (ETRACS) issued prior to June 14, 2015 are part of a series of UBS AG debt securities entitled “Medium-Term Notes, Series A”. UBS Switzerland AG is a co-obligor of such debt securities. However, the Securities are part of a separate series of UBS AG debt securities entitled “Medium-Term Notes, Series B”, and were issued after June 14, 2015. As a result, UBS Switzerland AG is not a co-obligor of the Securities and has no liability with respect to the Securities. If UBS AG fails to perform and observe every covenant of the indenture to be performed or observed by UBS AG with respect to the Securities, holders of the Securities will have recourse only against UBS AG, and not against UBS Switzerland AG.

If UBS were to be subject to restructuring proceedings, the market value of the Securities may be adversely affected.

Under certain circumstances, the Swiss Financial Market Supervisory Authority (FINMA) has the power to open restructuring or liquidation proceedings in respect of, and/or impose protective measures in relation to, UBS, which proceedings or measures may have a material adverse effect on the terms and market value of the Securities and/or the ability of UBS to make payments thereunder. Pursuant to article 25 et seq. of the Swiss Banking Act, FINMA has broad statutory powers to take measures and actions in relation to UBS if it (i) is overindebted, (ii) has serious liquidity problems or (iii) fails to fulfill the applicable capital adequacy provisions after expiration of a deadline set by FINMA. If one of these prerequisites is met, FINMA is authorized to open restructuring proceedings (Sanierungsverfahren) or liquidation (bankruptcy) proceedings (Bankenkonkurs) in respect of, and/or impose protective measures (Schutzmassnahmen) in relation to, UBS. The Swiss Banking Act, as last amended as of January 1, 2013, grants significant discretion to FINMA in connection with the aforementioned proceedings and measures. In particular, a broad variety of protective measures may be imposed by FINMA, including a bank moratorium (Stundung) or a maturity postponement (Fälligkeitsaufschub), which measures may be ordered by FINMA either on a stand-alone basis or in connection with restructuring or liquidation proceedings. In a restructuring proceeding, the resolution plan may, among other things, (a) provide for the transfer of UBS’s assets or a portion thereof, together with debts and other liabilities, and contracts of UBS, to another entity, (b) provide for the conversion of UBS’s debt and/or other obligations, including its obligations under the Securities, into equity, and/or (c) potentially provide for haircuts on obligations of UBS, including its obligations under the Securities. As of the date of this pricing supplement, there are no precedents as to what impact the revised regime would have on the rights of holders of the Securities or the ability of UBS to make payments thereunder if one or several of the measures under the revised insolvency regime were imposed in connection with a resolution of UBS.

Significant aspects of the tax treatment of the Securities are uncertain.

Significant aspects of the tax treatment of the Securities are uncertain. We do not plan to request a ruling from the Internal Revenue Service (“IRS”) regarding the tax treatment of the Securities, and the IRS or a court may not agree with the tax treatment described in this pricing supplement. Please read carefully the section entitled “Material U.S. Federal Income Tax Consequences” on page PS-28. You should consult your tax advisor about your own tax situation.

Pursuant to the terms of the Securities, you and we agree (in the absence of a statutory, regulatory, administrative or judicial ruling to the contrary) to characterize the Securities as a coupon-bearing pre-paid derivative contract with respect to the Index. In addition, you and we agree (in the absence of a statutory, regulatory, administrative or judicial ruling to the contrary) to treat the Coupon Amounts (including amounts received upon the sale, exchange, redemption or maturity of the Securities in respect of accrued but unpaid Coupon Amounts) and the Stub Reference Distribution Amount, if any, as

PS-8

Table of Contents

Risk Factors

amounts that are included in ordinary income for tax purposes at the time such amounts accrue or are received, in accordance with your regular method of tax accounting. You will be required to treat such amounts in such a manner despite the fact that (i) a portion of such amounts may be attributable to distributions on the Index Constituent Securities that give rise to long-term capital gain which, in the case of non-corporate taxpayers, is currently subject to tax at rates more favorable than the rates applicable to ordinary income and (ii) there may be other possible treatments of such amounts that would be more advantageous to holders of the Securities. Under that treatment (subject to the discussion below regarding the application of Section 1260 of the Internal Revenue Code of 1986, as amended (the “Code”)), you should generally recognize capital gain or loss upon the sale, exchange, redemption or maturity of your Securities in an amount equal to the difference between the amount realized (other than any amount attributable to accrued but unpaid Coupon Amounts, which will likely be treated as ordinary income) and the amount you paid for your Securities. Such gain or loss should generally be long-term capital gain or loss if you held your Securities for more than one year.

It is possible that your Securities could be treated as a “constructive ownership transaction” which would be subject to the constructive ownership rules of Section 1260 of the Code. Under Section 1260 of the Code, special tax rules apply to an investor that enters into a “constructive ownership transaction” with respect to an equity interest in a “pass-thru entity.” For this purpose, a constructive ownership transaction includes entering into a forward contract with respect to a pass-thru entity, and a derivative contract of the type represented by the Securities should be treated as a forward contract for this purpose. In addition, a pass-thru entity includes any United States REIT, and therefore each of the current Index Constituents is treated as a pass-thru entity for this purpose. It is, however, not entirely clear how Section 1260 of the Code applies in the case of an index that is comprised in whole or in part of pass-thru entities, like the Index. Although the matter is not free from doubt, it is likely that Section 1260 should apply to an index of pass-thru entities, in which case Section 1260 would apply to the Securities. If your Securities are subject to Section 1260 of the Code, then any long-term capital gain that you realize upon the sale, exchange, redemption or maturity of your Securities will be recharacterized as ordinary income (and you will be subject to an interest charge on the deferred tax liability with respect to such capital gain) to the extent that such capital gain exceeds the amount of long-term capital gain that you would have realized had you purchased an actual interest in the Index Constituents (in an amount equal to the notional amount of the Index that is represented by the Securities) on the date that you purchased your Securities and sold your interest in the Index Constituents on the date of the sale, exchange, redemption or maturity of the Securities (the “Excess Gain Amount”). If your Securities are subject to Section 1260 of the Code rules, the Excess Gain Amount will be presumed to be equal to all of the gain that you recognized in respect of the Securities (in which case all of such gain would be recharacterized as ordinary income that is subject to an interest charge) unless you provide clear and convincing evidence to the contrary. You should review the discussion of Section 1260 in the section entitled “Material U.S. Federal Income Tax Consequences — Section 1260 of the Code” on page PS-28 and are urged to consult your own tax advisor regarding the potential application of these rules.

The IRS released a notice in 2007 that may affect the taxation of holders of the Securities. According to the notice, the IRS and the Treasury Department are actively considering, among other things, whether holders of instruments such as the Securities should be required to accrue ordinary income on a current basis (possibly in excess of the Coupon Amounts), whether gain or loss upon the sale, exchange, redemption or maturity of such instruments should be treated as ordinary or capital, whether foreign holders of such instruments should be subject to withholding tax, and whether the special “constructive ownership rules” of Section 1260 of the Code, should be applied to such instruments.

Similarly, the IRS and the Treasury Department have current projects open with regard to the tax treatment of pre-paid forward contracts and contingent notional principal contracts. While it is

PS-9

Table of Contents

Risk Factors

impossible to anticipate how any ultimate guidance would affect the tax treatment of instruments such as the Securities (and while any such guidance may be issued on a prospective basis only), such guidance could be applied retroactively and could in any case increase the likelihood that you will be required to accrue income (possibly in excess of the Coupon Amounts) over the term of an instrument such as the Securities. The outcome of this process is uncertain.

Furthermore, in 2007, legislation was introduced in Congress that, if enacted, would have required holders of the Securities purchased after the bill was enacted to accrue interest income over the term of the Securities in an amount that could exceed the Coupon Amounts that are paid on the Securities. It is not possible to predict whether a similar or identical bill will be enacted in the future and whether any such bill would affect the tax treatment of your Securities.

Holders are urged to consult their tax advisors concerning the significance and the potential impact of the above considerations. We intend to treat your Securities for United States federal income tax purposes in accordance with the treatment described above and under “Material U.S. Federal Income Tax Consequences” on page PS-28 unless and until such time as there is a change in law or the Treasury Department or IRS determines that some other treatment is more appropriate.

Non-United States Holders of the Securities may become subject to withholding tax.

Non-United States Holders of the Securities may become subject to withholding with respect to the Coupon Amount under Section 871(m) of the Code. Non-United States Holders are urged to consult their tax advisors and to review the discussion below under “Material U.S. Federal Income Tax Consequences — Non-United States Holders” on page PS-30 of this pricing supplement.

PS-10

Table of Contents

The following four examples illustrate how the Securities would perform at maturity or call, or upon early redemption, in hypothetical circumstances. We have included an example in which the Index Closing Level increases at a constant rate of 3.00% per month for twelve months (Example 1), as well as an example in which the Index Closing Level decreases at a constant rate of 3.00% per month for twelve months (Example 2). In addition, Example 3 shows the Index Closing Level increasing by 3.00% per month for the first six months and then decreasing by 3.00% per month for the next six months, whereas Example 4 shows the reverse scenario of the Index Closing Level decreasing by 3.00% per month for the first six months, and then increasing by 3.00% per month for the next six months. For ease of analysis and presentation,the following four examples assume that the term of the Securities is twelve months, the last Trading Day of the Call Measurement Period, or the Redemption Valuation Date, occurs on the month end, no acceleration upon minimum indicative value has occurred, no Coupon Amount has been paid during the term of the Securities and no Stub Reference Distribution Amount was paid at maturity, call or upon early redemption.

The following assumptions are used in each of the four examples:

| Ø | the initial level for the Index is 400; |

| Ø | the Redemption Fee Rate is 0.125%; |

| Ø | the Financing Rate (the Financing Spread plus three-month LIBOR, as defined in the accompanying product supplement) is 0.80%; |

| Ø | the Current Principal Amount (as defined in the accompanying product supplement) on the first day is $25.00; and |

| Ø | the Annual Tracking Fee (a component of the Annual Tracking Fee, each as defined in the accompanying product supplement) is 0.40%. |

The examples highlight the effect of two times leverage and monthly compounding, and the impact of the Accrued Fees (as defined in the accompanying product supplement) on the payment at maturity or call, or upon early redemption, under different circumstances. The assumed Financing Rate is not an indication of the Financing Rate throughout the term of the Securities. The Financing Rate will change during the term of the Securities, which will affect the performance of the Securities.

Because the Accrued Fees take into account the monthly performance of the Index, as measured by the Index Closing Level, the absolute level of the Accrued Fees are dependent on the path taken by the Index Closing Level to arrive at its ending level. The figures in these examples have been rounded for convenience. The Cash Settlement Amount figures for month twelve are as of the hypothetical Calculation Date, and given the indicated assumptions, a holder will receive payment at maturity in the indicated amount, according to the indicated formula.

PS-11

Table of Contents

Hypothetical Examples

Example 1: The Index Closing Level increases at a constant rate of 3.00% per month for twelve months.

Month End | Index Closing Level* | Index Performance Ratio | Index Factor | Accrued Financing Charge for the Applicable Month** | Current Indicative Value | Accrued Tracking Fee for the Applicable Month*** | Accrued Fees for the Applicable Month | Current Principal Amount #^**** | Redemption Amount | |||||||||||||||||||||||||||

A | B | C | D | E | F | G | H | I | J | |||||||||||||||||||||||||||

|

| ((Index Closing Level – Monthly Initial Closing Level) / Monthly Initial Closing Level) | (1 + (2 x C)) | (Previous Current Principal Amount x Financing Rate x Financing Rate x Act/360) | (Previous Current Principal Amount x D)* | (Annual Tracking Fee x F x Act/365) | (E + G) | ((Previous Current Principal Amount x D) – H) | (I – Redemption Fee) | |||||||||||||||||||||||||||

| 1 | 412.00 | 0.0300 | 1.060 | 0.0167 | $ | 26.50 | $ | 0.0087 | $ | 0.0254 | $ | 26.47 | $ | 26.4434 | ||||||||||||||||||||||

| 2 | 424.36 | 0.0300 | 1.060 | 0.0176 | $ | 28.06 | $ | 0.0092 | $ | 0.0269 | $ | 28.04 | $ | 28.0031 | ||||||||||||||||||||||

| 3 | 437.09 | 0.0300 | 1.060 | 0.0187 | $ | 29.72 | $ | 0.0098 | $ | 0.0285 | $ | 29.69 | $ | 29.6549 | ||||||||||||||||||||||

| 4 | 450.20 | 0.0300 | 1.060 | 0.0198 | $ | 31.47 | $ | 0.0103 | $ | 0.0301 | $ | 31.44 | $ | 31.4041 | ||||||||||||||||||||||

| 5 | 463.71 | 0.0300 | 1.060 | 0.0210 | $ | 33.33 | $ | 0.0110 | $ | 0.0319 | $ | 33.30 | $ | 33.2564 | ||||||||||||||||||||||

| 6 | 477.62 | 0.0300 | 1.060 | 0.0222 | $ | 35.29 | $ | 0.0116 | $ | 0.0338 | $ | 35.26 | $ | 35.2181 | ||||||||||||||||||||||

| 7 | 491.95 | 0.0300 | 1.060 | 0.0235 | $ | 37.38 | $ | 0.0123 | $ | 0.0358 | $ | 37.34 | $ | 37.2954 | ||||||||||||||||||||||

| 8 | 506.71 | 0.0300 | 1.060 | 0.0249 | $ | 39.58 | $ | 0.0130 | $ | 0.0379 | $ | 39.54 | $ | 39.4953 | ||||||||||||||||||||||

| 9 | 521.91 | 0.0300 | 1.060 | 0.0264 | $ | 41.91 | $ | 0.0138 | $ | 0.0401 | $ | 41.87 | $ | 41.8249 | ||||||||||||||||||||||

| 10 | 537.57 | 0.0300 | 1.060 | 0.0279 | $ | 44.39 | $ | 0.0146 | $ | 0.0425 | $ | 44.34 | $ | 44.2919 | ||||||||||||||||||||||

| 11 | 553.69 | 0.0300 | 1.060 | 0.0296 | $ | 47.00 | $ | 0.0155 | $ | 0.0450 | $ | 46.96 | $ | 46.9045 | ||||||||||||||||||||||

| 12 | 570.30 | 0.0300 | 1.060 | 0.0313 | $ | 49.78 | $ | 0.0164 | $ | 0.0477 | $ | 49.73 | $ | 49.6711 | ||||||||||||||||||||||

Cumulative Index Return: |

| 42.58% | ||||||||||||||||||||||||||||||||||

| Return on Securities (assumes no early redemption): | 98.92% | |||||||||||||||||||||||||||||||||||

| * | The Index Closing Level is also: (i) the Monthly Initial Closing Level for the following month; and (ii) the Index Valuation Level for calculating the Call Settlement Amount, the Redemption Amount and the Cash Settlement Amount |

| ** | Accrued Financing Charge is calculated on an act/360 basis (30-day months are assumed for the above calculations) |

| *** | Accrued Tracking Fee is calculated on an act/365 basis (30-day months are assumed for the above calculations) |

| **** | Previous Current Principal Amount is also the Financing Level |

| # | This is also the Call Settlement Amount |

| ^ | For month twelve, this is also the Cash Settlement Amount |

PS-12

Table of Contents

Hypothetical Examples

Example 2: The Index Closing Level decreases at a constant rate of 3.00% per month for twelve months.

Month End | Index Closing Level* | Index Performance Ratio | Index Factor | Accrued Financing Charge for the Applicable Month** | Current Indicative Value | Accrued Tracking Fee for the Applicable Month*** | Accrued Fees for the Applicable Month | Current Principal Amount #^**** | Redemption Amount | |||||||||||||||||||||||||||

A | B | C | D | E | F | G | H | I | J | |||||||||||||||||||||||||||

|

| ((Index Closing Level – Monthly Initial Closing Level) / Monthly Initial Closing Level) | (1 + (2 x C)) | (Previous Current Principal Amount x Financing Rate x Financing Rate x Act/360) | (Previous Current Principal Amount x D)* | (Annual Tracking Fee x F x Act/365) | (E + G) | ((Previous Current Principal Amount x D) – H) | (I –Redemption Fee) | |||||||||||||||||||||||||||

| 1 | 388.00 | -0.0300 | 0.940 | 0.0167 | $ | 23.50 | $ | 0.0077 | $ | 0.0244 | $ | 23.48 | $ | 23.4444 | ||||||||||||||||||||||

| 2 | 376.36 | -0.0300 | 0.940 | 0.0157 | $ | 22.07 | $ | 0.0073 | $ | 0.0229 | $ | 22.04 | $ | 22.0148 | ||||||||||||||||||||||

| 3 | 365.07 | -0.0300 | 0.940 | 0.0147 | $ | 20.72 | $ | 0.0068 | $ | 0.0215 | $ | 20.70 | $ | 20.6725 | ||||||||||||||||||||||

| 4 | 354.12 | -0.0300 | 0.940 | 0.0138 | $ | 19.46 | $ | 0.0064 | $ | 0.0202 | $ | 19.44 | $ | 19.4119 | ||||||||||||||||||||||

| 5 | 343.49 | -0.0300 | 0.940 | 0.0130 | $ | 18.27 | $ | 0.0060 | $ | 0.0190 | $ | 18.25 | $ | 18.2283 | ||||||||||||||||||||||

| 6 | 333.19 | -0.0300 | 0.940 | 0.0122 | $ | 17.16 | $ | 0.0056 | $ | 0.0178 | $ | 17.14 | $ | 17.1168 | ||||||||||||||||||||||

| 7 | 323.19 | -0.0300 | 0.940 | 0.0114 | $ | 16.11 | $ | 0.0053 | $ | 0.0167 | $ | 16.09 | $ | 16.0731 | ||||||||||||||||||||||

| 8 | 313.50 | -0.0300 | 0.940 | 0.0107 | $ | 15.13 | $ | 0.0050 | $ | 0.0157 | $ | 15.11 | $ | 15.0930 | ||||||||||||||||||||||

| 9 | 304.09 | -0.0300 | 0.940 | 0.0101 | $ | 14.21 | $ | 0.0047 | $ | 0.0147 | $ | 14.19 | $ | 14.1727 | ||||||||||||||||||||||

| 10 | 294.97 | -0.0300 | 0.940 | 0.0095 | $ | 13.34 | $ | 0.0044 | $ | 0.0138 | $ | 13.33 | $ | 13.3085 | ||||||||||||||||||||||

| 11 | 286.12 | -0.0300 | 0.940 | 0.0089 | $ | 12.53 | $ | 0.0041 | $ | 0.0130 | $ | 12.51 | $ | 12.4970 | ||||||||||||||||||||||

| 12 | 277.54 | -0.0300 | 0.940 | 0.0083 | $ | 11.76 | $ | 0.0039 | $ | 0.0122 | $ | 11.75 | $ | 11.7350 | ||||||||||||||||||||||

Cumulative Index Return: |

| -30.62% | ||||||||||||||||||||||||||||||||||

| Return on Securities (assumes no early redemption): | -53.00% | |||||||||||||||||||||||||||||||||||

| * | The Index Closing Level is also: (i) the Monthly Initial Closing Level for the following month; and (ii) the Index Valuation Level for calculating the Call Settlement Amount, the Redemption Amount and the Cash Settlement Amount |

| ** | Accrued Financing Charge is calculated on an act/360 basis (30-day months are assumed for the above calculations) |

| *** | Accrued Tracking Fee is calculated on an act/365 basis (30-day months are assumed for the above calculations) |

| **** | Previous Current Principal Amount is also the Financing Level |

| # | This is also the Call Settlement Amount |

| ^ | For month twelve, this is also the Cash Settlement Amount |

PS-13

Table of Contents

Hypothetical Examples

Example 3: The Index Closing Level increases by 3.00% per month for the first six months and then decreases by 3.00% per month for the next 6 months.

Month End | Index Closing Level* | Index Performance Ratio | Index Factor | Accrued Financing Charge for the Applicable Month** | Current Indicative Value | Accrued Tracking Fee for the Applicable Month*** | Accrued Fees for the Applicable Month | Current Principal Amount #^**** | Redemption Amount | |||||||||||||||||||||||||||

A | B | C | D | E | F | G | H | I | J | |||||||||||||||||||||||||||

|

| ((Index Closing Level – Monthly Initial Closing Level) / Monthly Initial Closing Level) | (1 + (2 x C)) | (Previous Current Principal Amount x Financing Rate x Financing Rate x Act/360) | (Previous Current Principal Amount x D)* | (Annual Tracking Fee x F x Act/365) | (E + G) | ((Previous Current Principal Amount x D) – H) | (I –Redemption Fee) | |||||||||||||||||||||||||||

| 1 | 412.00 | 0.0300 | 1.060 | 0.0167 | $ | 26.50 | $ | 0.0087 | $ | 0.0254 | $ | 26.47 | $ | 26.4434 | ||||||||||||||||||||||

| 2 | 424.36 | 0.0300 | 1.060 | 0.0176 | $ | 28.06 | $ | 0.0092 | $ | 0.0269 | $ | 28.04 | $ | 28.0031 | ||||||||||||||||||||||

| 3 | 437.09 | 0.0300 | 1.060 | 0.0187 | $ | 29.72 | $ | 0.0098 | $ | 0.0285 | $ | 29.69 | $ | 29.6549 | ||||||||||||||||||||||

| 4 | 450.20 | 0.0300 | 1.060 | 0.0198 | $ | 31.47 | $ | 0.0103 | $ | 0.0301 | $ | 31.44 | $ | 31.4041 | ||||||||||||||||||||||

| 5 | 463.71 | 0.0300 | 1.060 | 0.0210 | $ | 33.33 | $ | 0.0110 | $ | 0.0319 | $ | 33.30 | $ | 33.2564 | ||||||||||||||||||||||

| 6 | 477.62 | 0.0300 | 1.060 | 0.0222 | $ | 35.29 | $ | 0.0116 | $ | 0.0338 | $ | 35.26 | $ | 35.2181 | ||||||||||||||||||||||

| 7 | 463.29 | -0.0300 | 0.940 | 0.0235 | $ | 33.14 | $ | 0.0109 | $ | 0.0344 | $ | 33.11 | $ | 33.0656 | ||||||||||||||||||||||

| 8 | 449.39 | -0.0300 | 0.940 | 0.0221 | $ | 31.12 | $ | 0.0102 | $ | 0.0323 | $ | 31.09 | $ | 31.0494 | ||||||||||||||||||||||

| 9 | 435.91 | -0.0300 | 0.940 | 0.0207 | $ | 29.23 | $ | 0.0096 | $ | 0.0303 | $ | 29.20 | $ | 29.1562 | ||||||||||||||||||||||

| 10 | 422.83 | -0.0300 | 0.940 | 0.0195 | $ | 27.44 | $ | 0.0090 | $ | 0.0285 | $ | 27.41 | $ | 27.3784 | ||||||||||||||||||||||

| 11 | 410.15 | -0.0300 | 0.940 | 0.0183 | $ | 25.77 | $ | 0.0085 | $ | 0.0267 | $ | 25.74 | $ | 25.7089 | ||||||||||||||||||||||

| 12 | 397.84 | -0.0300 | 0.940 | 0.0172 | $ | 24.20 | $ | 0.0080 | $ | 0.0251 | $ | 24.17 | $ | 24.1413 | ||||||||||||||||||||||

Cumulative Index Return: |

| -0.54% | ||||||||||||||||||||||||||||||||||

| Return on Securities (assumes no early redemption): | -3.31% | |||||||||||||||||||||||||||||||||||

| * | The Index Closing Level is also: (i) the Monthly Initial Closing Level for the following month; and (ii) the Index Valuation Level for calculating the Call Settlement Amount, the Redemption Amount and the Cash Settlement Amount |

| ** | Accrued Financing Charge is calculated on an act/360 basis (30-day months are assumed for the above calculations) |

| *** | Accrued Tracking Fee is calculated on an act/365 basis (30-day months are assumed for the above calculations) |

| **** | Previous Current Principal Amount is also the Financing Level |

| # | This is also the Call Settlement Amount |

| ^ | For month twelve, this is also the Cash Settlement Amount |

PS-14

Table of Contents

Hypothetical Examples

Example 4: The Index Closing Level decreases by 3.00% per month for the first six months, and then increases by 3.00% per month for the next six months.

Month End | Index Closing Level* | Index Performance Ratio | Index Factor | Accrued Financing Charge for the Applicable Month** | Current Indicative Value | Accrued Tracking Fee for the Applicable Month*** | Accrued Fees for the Applicable Month | Current Principal Amount #^**** | Redemption Amount | |||||||||||||||||||||||||||

A | B | C | D | E | F | G | H | I | J | |||||||||||||||||||||||||||

|

| ((Index Closing Level – Monthly Initial Closing Level) / Monthly Initial Closing Level) | (1 + (2 x C)) | (Previous Current Principal Amount x Financing Rate x Financing Rate x Act/360) | (Previous Current Principal Amount x D)* | (Annual Tracking Fee x F x Act/365) | (E + G) | ((Previous Current Principal Amount x D) – H) | (I –Redemption Fee) | |||||||||||||||||||||||||||

| 1 | 388.00 | -0.0300 | 0.940 | 0.0167 | $ | 23.50 | $ | 0.0077 | $ | 0.0244 | $ | 23.48 | $ | 23.4444 | ||||||||||||||||||||||

| 2 | 376.36 | -0.0300 | 0.940 | 0.0157 | $ | 22.07 | $ | 0.0073 | $ | 0.0229 | $ | 22.04 | $ | 22.0148 | ||||||||||||||||||||||

| 3 | 365.07 | -0.0300 | 0.940 | 0.0147 | $ | 20.72 | $ | 0.0068 | $ | 0.0215 | $ | 20.70 | $ | 20.6725 | ||||||||||||||||||||||

| 4 | 354.12 | -0.0300 | 0.940 | 0.0138 | $ | 19.46 | $ | 0.0064 | $ | 0.0202 | $ | 19.44 | $ | 19.4119 | ||||||||||||||||||||||

| 5 | 343.49 | -0.0300 | 0.940 | 0.0130 | $ | 18.27 | $ | 0.0060 | $ | 0.0190 | $ | 18.25 | $ | 18.2283 | ||||||||||||||||||||||

| 6 | 333.19 | -0.0300 | 0.940 | 0.0122 | $ | 17.16 | $ | 0.0056 | $ | 0.0178 | $ | 17.14 | $ | 17.1168 | ||||||||||||||||||||||

| 7 | 343.18 | 0.0300 | 1.060 | 0.0114 | $ | 18.17 | $ | 0.0060 | $ | 0.0174 | $ | 18.15 | $ | 18.1292 | ||||||||||||||||||||||

| 8 | 353.48 | 0.0300 | 1.060 | 0.0121 | $ | 19.24 | $ | 0.0063 | $ | 0.0184 | $ | 19.22 | $ | 19.1985 | ||||||||||||||||||||||

| 9 | 364.08 | 0.0300 | 1.060 | 0.0128 | $ | 20.37 | $ | 0.0067 | $ | 0.0195 | $ | 20.35 | $ | 20.3309 | ||||||||||||||||||||||

| 10 | 375.01 | 0.0300 | 1.060 | 0.0136 | $ | 21.58 | $ | 0.0071 | $ | 0.0207 | $ | 21.56 | $ | 21.5301 | ||||||||||||||||||||||

| 11 | 386.26 | 0.0300 | 1.060 | 0.0144 | $ | 22.85 | $ | 0.0075 | $ | 0.0219 | $ | 22.83 | $ | 22.8001 | ||||||||||||||||||||||

| 12 | 397.84 | 0.0300 | 1.060 | 0.0152 | $ | 24.20 | $ | 0.0080 | $ | 0.0232 | $ | 24.17 | $ | 24.1450 | ||||||||||||||||||||||

Cumulative Index Return: |

| -0.54% | ||||||||||||||||||||||||||||||||||

| Return on Securities (assumes no early redemption): | -3.31% | |||||||||||||||||||||||||||||||||||

| * | The Index Closing Level is also: (i) the Monthly Initial Closing Level for the following month; and (ii) the Index Valuation Level for calculating the Call Settlement Amount, the Redemption Amount and the Cash Settlement Amount |

| ** | Accrued Financing Charge is calculated on an act/360 basis (30-day months are assumed for the above calculations) |

| *** | Accrued Tracking Fee is calculated on an act/365 basis (30-day months are assumed for the above calculations) |

| **** | Previous Current Principal Amount is also the Financing Level |

| # | This is also the Call Settlement Amount |

| ^ | For month twelve, this is also the Cash Settlement Amount |