Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

o | Registration Statement pursuant to Section 12(b) or 12(g) of the Securities Exchange Act of 1934 |

or | |

ý | Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the fiscal year ended February 29, 2004 |

or | |

o | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the transition period from to |

Commission file number: 333-11948

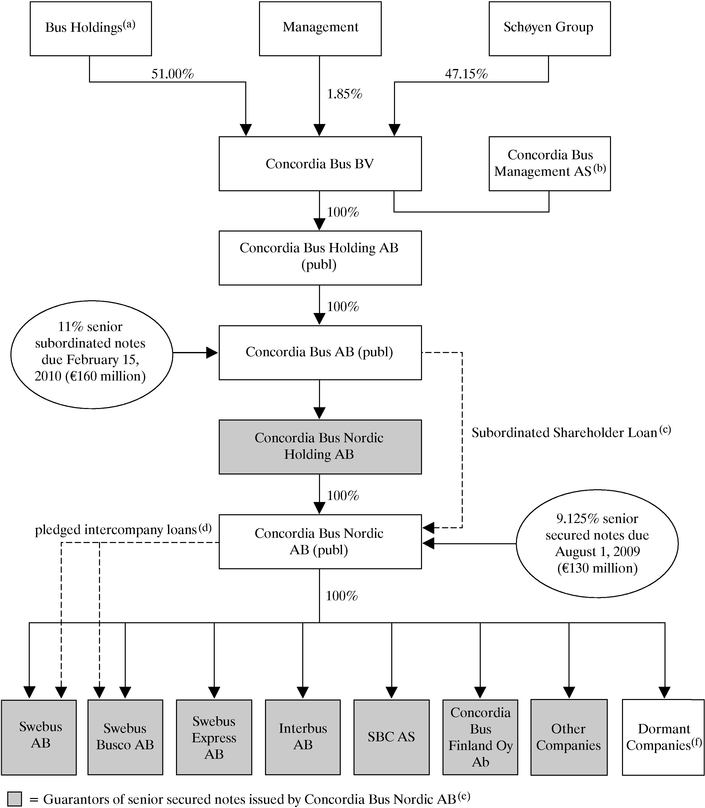

CONCORDIA BUS AB (publ)

(Exact Name of Registrant as Specified in its Charter)

SWEDEN

(Jurisdiction of Incorporation or Organization)

Solna Strandväg 78, 171-54 Solna, Sweden

(Address of Principal Executive Offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

NONE

Securities registered or to be registered pursuant to Section 12(g) of the Act:

NONE

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

Euro 160,000,000 11% Senior Subordinated Notes due February 2010

(Title of Class)

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

| ý Yes | o No |

Indicate by check mark which financial statement item the registrant has elected to follow:

| ý Item 17 | o Item 18 |

CAUTIONARY NOTICE REGARDING FORWARD LOOKING STATEMENTS

This annual report includes forward looking statements. We have based these forward looking statements on our current expectations and projections about future events. These forward looking statements can be identified by the use of forward looking terminology, including the terms "believe," "estimate," "anticipate," "expect," "intend," "continue," "may," "will" or "should" or, in each case, their negative, or other variations or comparable terminology. These forward looking statements include all matters that are not historical facts. They appear under subheading "D. Risk Factors" of "Item 3. Key Information" and "Item 5. Operating and Financial Review and Prospects" and elsewhere in this annual report and include statements regarding our intentions, beliefs or current expectations concerning, among other things, our results of operations, financial condition, liquidity, prospects, growth, strategies and the industry in which we operate.

By their nature, forward looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. We caution you that forward looking statements are not guarantees of future performance and that our actual results of operations, financial condition and liquidity, and the development of the industry in which we operate may differ materially from those made in or suggested by the forward looking statements contained in this annual report. In addition, even if our results of operations, financial condition and liquidity, and the development of the industry in which we operate are consistent with the forward looking statements contained in this annual report, those results or developments may not be indicative of results or developments in subsequent periods. Important factors that could cause those differences include, but are not limited to:

- •

- our substantial leverage and our ability to meet our debt service obligations;

- •

- our ability to win and/or renew public contracts;

- •

- downward pressure on prices resulting from competition in our industry;

- •

- our exposure to cost increases that may not be sufficiently accounted for by the indexation terms in our contracts;

- •

- potential changes in the funding provided to transportation authorities by governments;

- •

- our ability to win contracts with a margin and return on capital commensurate with our cost structure;

- •

- our ability to forecast the costs associated with contracts successfully;

- •

- our ability to take advantage of terms in our lease agreements;

- •

- our relations with our employees;

- •

- our exposure to fluctuations in fuel prices;

- •

- possible financial losses pursuant to our hedging strategies; and

- •

- our exposure to currency exchange rate fluctuations.

We undertake no obligation to update publicly or to revise any forward looking statements, whether as a result of new information, future events or otherwise. Furthermore, these forward looking statements may be materially impacted by the factors listed under subheading "D. Risk Factors" of "Item 3. Key Information". In light of these risks, uncertainties and assumptions, the forward looking events discussed in this annual report might not occur. You should not interpret statements regarding past trends or activities as representations that those trends or activities will continue in the future.

i

ENFORCEMENT OF CERTAIN CIVIL LIABILITIES

Concordia Bus AB (publ) ("Concordia") is organized under the laws of Sweden. All of our directors, executive officers and our subsidiaries and the independent auditors named in this prospectus are non-residents of the United States. As a result, it may not be possible for investors to effect service of process within the United States upon us or such persons or to enforce against any of them judgments of US courts predicated upon civil liabilities under US federal securities laws. Although we agree under the terms of the indenture relating to the senior subordinated notes to accept service of process in the United States by an agent designated for such purpose, it may not be possible for investors to (i) effect service of process within the United States upon our officers and directors and the independent auditors named herein and to (ii) realize in the United States upon judgments against such persons obtained in such courts predicated upon civil liabilities of such persons, including any judgments predicated upon US federal securities laws to the extent such judgments exceed such person's US assets. There is also doubt as to the enforceability in Sweden, in original actions or in actions for enforcement, of judgments of US courts predicted upon the civil liability provisions of the federal securities laws of the United States.

CURRENCY AND FINANCIAL STATEMENT PRESENTATION

Unless otherwise indicated, references in this prospectus to "SEK," "Swedish Krona" or "Swedish Kronor" are to the lawful currency of Sweden; references to "euro" or "€" are to the single currency of the participating Member States in the Third Stage of European Economic and Monetary Union of the Treaty Establishing the European Community, as amended from time to time; references to "Norwegian Kroner" or "NOK" are to the lawful currency of Norway; and references to "US dollars" or "$" are to the lawful currency of the United States of America.

The consolidated financial statements of Concordia and Concordia Bus Nordic AB (publ) ("Concordia Bus Nordic") are prepared in accordance with accounting principles generally accepted in Sweden ("Swedish GAAP"), which differ in certain respects from generally accepted accounting principles in certain other countries. The significant differences between Swedish GAAP and accounting principles generally accepted in the United States of America ("US GAAP") are discussed in Note 33 to the consolidated financial statements of Concordia included elsewhere in this annual report.

ii

Item 1. Identity of Directors, Senior Management and Advisors

Not Applicable.

Item 2. Offer Statistics and Expected Timetable

Not Applicable

A. Selected Financial Data

Concordia, which was incorporated on September 17, 1999, acquired 100% of the share capital of Concordia Bus Nordic on January 14, 2000. From its inception until its acquisition of Concordia Bus Nordic, Concordia was inactive and had insignificant net losses, assets, liabilities and shareholders' equity. As a result of this acquisition, the carrying value of Concordia Bus Nordic's net assets was increased to Concordia's purchase price and Concordia Bus Nordic's fiscal year-end was changed from April 30 to the last day of February.

Accordingly, the following tables set forth selected consolidated financial data for Concordia Bus Nordic derived from audited financial statements as of and for the ten month period ended February 29, 2000 and (ii) selected consolidated financial data for Concordia derived from audited financial statements as of and for the years ended February 28, 2001, February 28, 2002, February 28, 2003 and February 29, 2004.

This information should be read in conjunction with "Item 5. Operating and Financial Review and Prospects" and the consolidated financial statements and the notes thereto included elsewhere in this annual report.

1

The consolidated financial statements of both Concordia and Concordia Bus Nordic have been prepared in accordance with Swedish GAAP, which differ in certain significant respects from US GAAP. The significant differences between Swedish GAAP and US GAAP are discussed in Note 33 to the consolidated financial statements of Concordia included elsewhere in this annual report.

| | Concordia Bus Nordic | Concordia | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | As of and for the 8.5 months ended January 14, 2000 | As of and for the 1.5 months ended February 29, 2000 | As of and for the year ended February 28, 2001(1)(2)(6) | As of and for the year ended February 28, 2002(5)(6) | As of and for the year ended February 28, 2003 | As of and for the year ended February 29, 2004 | |||||||

| | (SEK in millions, except share and per share amount and operating data) | ||||||||||||

| SWEDISH GAAP | |||||||||||||

| Income Statement Data | |||||||||||||

| Net revenue | 2,209 | 426 | 3,576 | 4,226 | 4,758 | 4,761 | |||||||

| Operating expenses | (1,918 | ) | (395 | ) | (3,299 | ) | (3,999 | ) | (4,522 | ) | (4,559 | ) | |

| Gain on sale of fixed assets | 9 | 2 | 65 | 20 | (4 | ) | 6 | ||||||

| Depreciation and amortization | (231 | ) | (44 | ) | (364 | ) | (383 | ) | (404 | ) | (363 | ) | |

| Write-down of fixed assets | — | — | — | (11 | ) | — | |||||||

| Operating income (loss) | 69 | (11 | ) | (22 | ) | (147 | ) | (172 | ) | (155 | ) | ||

| Financial income (expenses), net | (40 | ) | (35 | ) | (286 | ) | (217 | ) | (255 | ) | (308 | ) | |

| Income tax benefit (expense) | 1 | 12 | 83 | 78 | 83 | 54 | |||||||

| Net income (loss) | 30 | (34 | ) | (225 | ) | (286 | ) | (344 | ) | (409 | ) | ||

| Basic and diluted net income (loss) per share | 188 | (6,730 | ) | (45,035 | ) | (57,171 | ) | (68,780 | ) | (81,721 | ) | ||

Balance Sheet Data | |||||||||||||

| Total fixed assets | 3,459 | 3,572 | 2,965 | 2,720 | 2,386 | ||||||||

| Total current assets | 602 | 855 | 979 | 783 | 1,024 | ||||||||

| Total assets | 4,061 | 4,427 | 3,944 | 3,503 | 3,410 | ||||||||

| Share capital | 1 | 1 | 1 | 1 | 1 | ||||||||

| Total shareholder's equity (deficit) | 615 | 723 | 422 | 78 | (330 | ) | |||||||

| Total provisions | 337 | 299 | 236 | 171 | 146 | ||||||||

| Total noncurrent liabilities | 2,381 | 2,504 | 2,480 | 2,318 | 2,689 | ||||||||

| Total current liabilities | 728 | 901 | 806 | 936 | 905 | ||||||||

Other Financial Data | |||||||||||||

| Total capital expenditures | 525 | 59 | 336 | 43 | 216 | 32 | |||||||

| Capital expenditures on buses | 279 | 60 | 322 | 21 | 198 | 15 | |||||||

| Cash flow from operations(3) | 349 | (63 | ) | (72 | ) | 95 | 11 | 7 | |||||

| Cash flow from investing activities(3) | (494 | ) | (1,371 | ) | 103 | 275 | (136 | ) | (11 | ) | |||

| Cash flow from financing activities(3) | 84 | 1,585 | 53 | (194 | ) | (99 | ) | 153 | |||||

| Number of shares | 160,000 | 5,000 | 5,000 | 5,000 | 5,000 | 5,000 | |||||||

2

| | Concordia Bus Nordic | Concordia | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | As of and for the 8.5 months ended January 14, 2000 | As of and for the 1.5 months ended February 29, 2000 | As of and for the year ended February 28, 2001(1)(2)(6) | As of and for the year ended February 28, 2002(5)(6) | As of and for the year ended February 28, 2003 | As of and for the year ended February 29, 2004 | |||||||

| | (SEK in millions, except share and per share amounts, ratios and operating data) | ||||||||||||

| U.S. GAAP | |||||||||||||

| Income Statement Data | |||||||||||||

| Operating income (loss) | 25 | (5 | ) | (69 | ) | (108 | ) | (111 | ) | (80 | ) | ||

| Net loss | (5 | ) | (29 | ) | (260 | ) | (269 | ) | (301 | ) | (334 | ) | |

| Basic and diluted net loss per share | (33 | ) | (5,828 | ) | (51,920 | ) | (53,728 | ) | (60,180 | ) | (66,895 | ) | |

| Balance Sheet Data | |||||||||||||

| Total fixed assets | 3,459 | 3,505 | 3,086 | 2,882 | 2,588 | ||||||||

| Total current assets | 602 | 827 | 979 | 783 | 1,024 | ||||||||

| Total assets | 4,061 | 4,332 | 4,065 | 3,665 | 3,612 | ||||||||

| Share capital | 1 | 1 | 1 | 1 | 1 | ||||||||

| Total shareholder's equity (deficit) | 577 | 664 | 399 | 86 | (247 | ) | |||||||

| Total noncurrent liabilities | 2,756 | 2,779 | 2,876 | 2,644 | 2,945 | ||||||||

| Total current liabilities | 728 | 889 | 790 | 935 | 914 | ||||||||

OPERATING DATA | |||||||||||||

| Number of buses(4) | 3,455 | 3,289 | 4,137 | 4,021 | 3,949 | 3,908 | |||||||

| Average number of employees | 5,044 | 5,206 | 6,696 | 6,924 | 7,484 | 6,924 | |||||||

| Number of kilometers of service provided (in thousands) | 148,439 | 186,134 | 223,876 | 251,959 | 269,198 | 257,672 | |||||||

- (1)

- In March/April 2000, Concordia Finland experienced a 3-day strike among its employees. This strike resulted in losses of SEK 1.2 million.

- (2)

- Following the acquisition of SBC by Concordia, which was effective from February 1, 2001, the carrying value of the bus fleet used in the local public bus transportation business was increased by SEK 63 million to reflect its estimated fair value. The depreciation period was also extended prospectively from 8.33 years to 10 years. As a result of this acquisition, SBC's fiscal year-end was changed from December 31 to the last day of February.

- (3)

- For additional information about cash flow data for the years ended February 28, 2002, 2003 and February 29, 2004, see the Consolidated Cash Flow Statements included in this annual report.

- (4)

- Number of buses includes operating and surplus buses in Sweden, Norway, and Finland.

- (5)

- In early 2002, Concordia launched a plan to close its regional offices. As a result, termination costs for 80 employees are included as a provision which totaled SEK 17 million for the year ended February 28, 2002. These costs are included as a component of our operating loss.

3

- (6)

- Certain amounts as of and for the years ended February 28, 2002 and 2001 have been restated to give retroactive effect of a change in accounting policy under Swedish GAAP. See Note 1 to the consolidated financial statements included elsewhere in this annual report for a description of the change in accounting policy and the related effects. The change in accounting policy for Swedish GAAP had no impact on the results of operations or financial position of Concordia under U.S. GAAP.

The table below sets forth, for the periods and dates indicated, certain information concerning the exchange rate for the Swedish Krona against the US dollar based upon the noon buying rate in the City of New York for cable transfers in Swedish Krona as announced by the Federal Reserve Bank of New York for customs purposes (the "SEK Noon Buying Rate").

| | Period End | Average | High | Low | ||||

|---|---|---|---|---|---|---|---|---|

| Fiscal Year | ||||||||

| Ended February 29, 2000 | 8.7500 | 8.4329 | (a) | 8.8200 | 8.0940 | |||

| Ended February 28, 2001 | 9.8150 | 9.3723 | (a) | 10.3600 | 8.5330 | |||

| Ended February 28, 2002 | 10.4700 | 10.5832 | (a) | 11.0270 | 9.6730 | |||

| Ended February 28, 2003 | 8.5050 | 9.3218 | (a) | 10.500 | 8.4100 | |||

| Ended February 29, 2004 | 7.4330 | 7.8456 | (a) | 8.7030 | 7.0850 | |||

Month | ||||||||

| November 2003 | 7.5510 | 7.6799 | 7.9150 | 7.5200 | ||||

| December 2003 | 7.1950 | 7.3395 | 7.5420 | 7.1903 | ||||

| January 2004 | 7.4120 | 7.2334 | 7.4120 | 7.0850 | ||||

| February 2004 | 7.4330 | 7.2630 | 7.4330 | 7.1295 | ||||

| March 2004 | 7.5500 | 7.5322 | 7.6620 | 7.3660 | ||||

| April 2004 | 7.6425 | 7.6496 | 7.7510 | 7.4650 | ||||

| May 2004 | 7.4579 | 7.6097 | 7.7725 | 7.4170 | ||||

| June 2004 (through June 25, 2004) | 7.5460 | 7.5344 | 7.6280 | 7.4123 |

- (a)

- The average of the SEK Noon Buying Rate on the last day of each month during the applicable period.

B. Capitalization and Indebtedness

Not applicable.

C. Reasons For the Offer and Use of Proceeds

Not applicable.

4

D. Risk Factors

Concordia and Concordia Bus Nordic are holding companies with no revenue generating operations of their own.

Concordia and Concordia Bus Nordic are holding companies whose principal assets are their investments in their subsidiaries. They conduct no business or operations except through direct and indirect subsidiaries. Their ability to service indebtedness, including the €160,000,000 11.0% Senior Subordinated Notes due 2010 issued by Concordia (the "Senior Subordinated Notes") and the €130,000,000 9.125% Senior Secured Notes due August 1, 2009 issued by Concordia Bus Nordic and guaranteed by the guarantors as defined in footnote (e) under subheading "C. Organisational Structure" under "Item 4. Information on the Company" (the "Senior Secured Notes"), is entirely dependent upon the receipt of funds from subsidiaries by means of dividends, interest, intercompany loans or otherwise. The ability of subsidiaries to make those funds available to them is subject to, among other things, applicable corporate and other laws and restrictions contained in agreements to which such subsidiaries may be subject. We cannot assure you that those subsidiaries will be in a position to make funds available. Although the indentures related to the Senior Subordinated Notes and the Senior Secured Notes limit the ability of such subsidiaries to enter into consensual restrictions on their ability to pay dividends and make other payments to us, such limitations are subject to a number of significant qualifications. This could have a material adverse effect on our financial condition.

Ability to Service Debt—to service our debt, we will require a significant amount of cash. Our ability to generate cash depends on many factors beyond our control.

Our ability to make payments on and to refinance our debt, including the Senior Subordinated Notes and the Senior Secured Notes, will depend on our subsidiaries' ability to generate cash in the future and our subsidiaries' ability to generate distributable earnings or other funds available for that purpose. This, to a certain extent, is subject to general economic, financial, competitive and other factors that are beyond our control.

Based on our current level of operations and anticipated cost savings and operating improvements, we believe our cash flow from operations and available cash will be adequate to meet our future liquidity and debt service needs. However, we cannot assure you that (1) our business will generate sufficient cash flow from operations, particularly if our bus fleet grows more rapidly than anticipated, with the associated increase in operating lease costs, (2) currently anticipated cost savings, fleet management strategies and operating improvements will be realized on schedule, or at all or (3) future borrowings will be available to us in an amount sufficient to enable us to make required payments on, and redemptions of, our debt, including these Notes, or to fund our other liquidity needs.

We sustained operating losses of SEK 155 million for the year ended February 29, 2004, SEK 172 million for the year ended February 28, 2003 and SEK 147 million for the year ended February 28, 2002.

We may need to refinance all or a portion of our and our subsidiaries' debt, the Senior Subordinated Notes or the Senior Secured Notes, on or before maturity. We may not be able to refinance any of such debt, the Senior Subordinated Notes or the Senior Secured Notes, on commercially reasonable terms or at all, which could have a material adverse effect on our business.

5

Our substantial leverage could adversely affect our ability to run our business.

We have now and will continue to have a significant amount of debt. As of February 29, 2004, our total consolidated debt was approximately SEK 2,689 million, of which total consolidated senior debt was approximately SEK 2,673 million and our shareholder's deficit was SEK 330 million. We also have substantial commitments in the form of our operating lease payments.

Our and our subsidiaries' substantial debt could have important consequences for you. For example, it could among other things:

- •

- make it more difficult for us to satisfy our obligations under the Senior Subordinated Notes or the Senior Secured Notes;

- •

- limit our ability to fund our working capital, capital expenditures and general corporate requirements;

- •

- limit our ability to borrow additional funds;

- •

- limit our ability to enter into operating leases for buses;

- •

- require us to dedicate a substantial portion of our cash flow from operations to payments on our debt, thereby reducing the funds available to us for other purposes;

- •

- make us more vulnerable to economic downturns; and

- •

- reduce our flexibility to respond to changing business and economic conditions.

In addition, we and our subsidiaries may be able to incur substantial additional debt in the future. The terms of the indentures governing the Senior Subordinated Notes and the Senior Secured Notes restrict but do not fully prohibit us and our subsidiaries from borrowing after completion of this offering, and some of those borrowings may be secured. Further, if new debt is added to our and our subsidiaries' current debt levels, the related risks that we and they now face could intensify.

Any of the foregoing could have a material adverse effect on our business, our ability to make payments under the Senior Subordinated Notes and the Senior Secured Notes and our ability to continue presenting our financial statements under the assumption that we are a going concern.

The terms of our indebtedness restrict our corporate activities.

The indenture under which the Senior Subordinated Notes and the Senior Secured Notes were issued restrict, and in some cases prohibit, among other things, our and our subsidiaries' ability to:

- •

- incur additional debt;

- •

- make prepayments of certain debt;

- •

- pay dividends;

- •

- make investments;

- •

- engage in transactions with affiliates;

- •

- issue capital stock;

- •

- create liens;

- •

- sell assets; and

- •

- engage in mergers and consolidations.

6

A failure to comply with these covenants could result in a default under the Senior Subordinated Notes or the Senior Secured Notes, which in turn could result in an event of default under our other indebtedness.

If we or our Swedish, Norwegian or Finnish operating subsidiaries incur substantial operating losses, we or they may be subject to liquidation under our respective national regimes.

The respective companies acts and insolvency and reorganization laws of Sweden, Norway and Finland apply to Concordia and its operating subsidiaries. Under these regimes, if losses reduce the equity of these entities or any of their subsidiaries (including Concordia itself on a stand alone rather than a consolidated basis) to an amount less than 50% of its registered share capital, or (in Norway only) if the equity becomes inadequate compared to the risks and the size of its business, the directors of such entity would be obligated by law to convene a general shareholders meeting to resolve to liquidate such entity unless the directors were able to balance the amount of such equity and the registered share capital (in Sweden, within eight months of such meeting, and in Finland, within twelve months of such meeting) by (1) increasing the equity in an amount sufficient to achieve such balance and, in the Norwegian scheme, to ensure that its equity becomes adequate compared to the risks and the size of its business, or (2) reducing the share capital to pay off losses in an amount sufficient to achieve such balance. Due to these requirements, Concordia Finland Oy Ab ("Concordia Finland") converted portions of its shareholder loan from Concordia into a subordinated loan in July 2001 and in February 2003. In addition, if we are not successful in our cost-cutting initiatives and our losses continue, this may cause our equity to decrease sufficiently to require an equity increase or share capital reduction as described above. If we are unable to procure such an equity increase or share capital reduction, it would have an adverse effect on our ability to continue presenting our financial statements under the assumption that we are a going concern. See Subheading "A. Operating Results—Critical Accounting Policies—Going concern matters" under "Item 5. Operating and Financial Review and Prospects."

If we lose many local public transportation authorities' contracts as they are renewed or we are unable to win new contracts, our business will be adversely affected. Further, if we experience difficulties in operating under our existing contracts, our business may be adversely affected.

In the year ended February 29, 2004, our contracts with local public transportation authorities comprise approximately 89.1% of our revenue. In Sweden, Norway and Finland, we operate under 154, 33 and 13 contracts, respectively, with the largest contract accounting for 5.2% of our net revenue and the top 25 contracts accounting for approximately 51.2% of total revenue in the year ended February 29, 2004. These contracts usually have a five to eight year term. Local public transport authorities conduct a competitive bidding process for each contract shortly before it terminates and the most important criteria for determining the success of the bid is usually price. See subheading "B. Business Overview—Sweden—Regulation—Tendering Procedures" in "Item 4. Information on the Company" for a discussion of the competitive bidding process in Sweden. If we fail to continue to renew our local public transportation authorities contracts, our revenues will be adversely affected as our older local public transportation authorities contracts expire. This may affect our ability to satisfy obligations under the Senior Subordinated Notes and the Senior Secured Notes.

7

During the year ended February 28, 2003, Swebus faced significant operating difficulty in the Stockholm and Uppsala region, due largely to poor operational planning of summer and winter traffic schedules, together with an exceptionally severe winter. Restrictions on our ability to manage inherited bus drivers under the new contracts due to a grace period of one year from March 4, 2002, and a shortage of drivers caused significant problems. This situation resulted in additional overtime, training costs, substantial payments due to the inconvenience of working hours, increased subcontracting costs, loss of revenues and contractual penalties. If similar difficulties were to be experienced under other contracts, our business would be adversely affected.

If we do not retain or gain local public transportation authority contracts, we may not benefit from the option to renew existing operating lease agreements at a lower cost.

As of February 29, 2004, we have entered into operating leasing arrangements for 1,317 of our 3,908 buses and an additional 15 buses not yet delivered. The contracts under which these buses are leased are classified as operating leases which means that no asset values are recorded on our balance sheet. The term of any given lease is established to match as far as possible with the duration of the underlying contract with the local public transportation authority, generally five to eight years.

The structure of the lease contract is such that at the inception of a new lease contract, the leasing fee is established based on the purchase price paid by the lessor and residual value agreed with the manufacturer for the period of the lease. At the end of each leasing contract period each leasing contract can be renewed or terminated (and we have an obligation to renew the lease contracts for a certain aggregate number of buses). The lease payments for the second leasing period, which are based on the agreed residual value at the date of the extension, are lower than the payments during the initial term. If we are not successful in renewing or extending the local public transportation authority contracts, or in efficiently redeploying our buses elsewhere, we may not gain the benefit of such lower costs.

Further, in the event of an acceleration under the Senior Subordinated Notes or the Senior Secured Notes following a default, all or part of the leasing contracts covering a significant portion of our leases may be terminated at the option of the lessor. This could have a material adverse effect on our business.

Competition on price or other factors could adversely affect our business.

It is our policy to focus on increasing our return on capital and cash generation. We believe that our change in focus toward more appropriate tendering levels has been adopted by other major operators, particularly since 1998. Consolidation in the industry and this change in focus among the larger competitors from a tendering strategy based on increasing market share to a strategy of seeking to maintain adequate margins have recently resulted in more favorable pricing dynamics. We believe that this trend will continue. For example, in fiscal 2002, fiscal 2003 and fiscal 2004, CPTAs awarded contracts to us on renewal with prices between 10% and 54% above the prices in the previous contracts. However, no assurance can be given that the more favorable pricing trends will continue in the future for new tenders. For more information, see subheading "B. Business—Sweden—Competition in the Swedish Bus Transportation Market" under "Item 4. Information on the Company".

8

If indices in our contracts do not reflect our cost increases, our business could be adversely affected.

Local public transportation authorities contracts provide for a fee to be paid to us in return for providing bus operations for the routes and schedules described in the contracts. The amount of the fee to be paid each year is adjusted annually based on an index, or on several indices, that is intended to account for changes in our costs. Historically, contracts with local public transportation authorities, which produce a substantial portion of Swebus' revenues in Sweden, have contained cost indices primarily based on consumer price indices.

While, as tendered contracts expire and new contracts are tendered, it is now becoming increasingly common to include either (i) a price adjustment index which reflects bus industry costs, or (ii) a combination of a consumer price index, a labor cost index and a diesel fuel price index, there can be no assurance this trend will continue. Should price adjustment indices contained in our future local public transportation authorities contracts fail to reflect our actual cost structure, changes in our costs that are not reflected in the indices included in these contracts could adversely affect our operating margins.

The local public transport authorities rely on government subsidies. Removal of these subsidies could drive down local public transportation authorities' contract fees.

In Sweden and Norway, management believes that approximately 50% and 40%, respectively, of fees to bus operating companies paid by local public transportation authorities under local public transportation authorities contracts in 2003 were funded by government subsidies (as opposed to bus ticket revenues). Many European countries have sought to reduce subsidies in recent years. Should Sweden more aggressively seek to reduce subsidies, fees from local public transportation authorities contracts may decrease, and local public transportation authorities could seek to renegotiate the scope of existing contracts. A decision to reduce subsidies could have an adverse effect on potential fees under local public transportation authorities contracts.

Our employees are heavily unionized. Bargaining power and strikes can hurt our business.

Our bus drivers and most of our other employees are unionized. The collective bargaining agreement generally applicable to our blue collar employees expires on January 31, 2005. See subheading "B. Business Overview—Drivers and Other Personnel" under "Item 4. Information on the Company." Personnel costs constituted approximately 57% of our total operating expenses (excluding depreciation and amortization) in the year ended February 29, 2004.

Fluctuation in price and availability of diesel fuel could hurt our business.

Significant changes in fuel availability or costs would materially impact our business. Diesel fuel availability and prices are affected by a number of factors, including environmental legislation and global economic and political developments, over which we have little to no control. In addition, our costs are affected by annual increases in fuel taxes, which are largely offset by compensation from indexation. In the event of a shortage in diesel fuel supply resulting from a disruption of oil imports, reduction in production or otherwise, we could face higher diesel fuel prices or the curtailment of scheduled diesel fuel deliveries. We enter into hedging arrangements to fix the cost of diesel fuel before taxes, supplier and transportation costs. As a result of hedging, in the year ended February 29, 2004, our total cost of diesel fuel averaged SEK 5.49 per liter. For a further discussion of our response to fluctuations in prices or a decrease in fuel availability, including our hedging policies, see subheading "B. Liquidity and Capital Resources—Market Risk" under "Item 5. Operating and Financial Review and Prospects".

9

Variations in exchange rates may affect our performance.

Ingeniør Schøyens Bilcentraler A.S. ("SBC"), which comprised approximately 8% of our revenue in the year ended February 29, 2004, prepares its financial statements in, and its functional currency is, Norwegian Kroner. In preparing our consolidated financial statements, we translate SBC's financial statements into Swedish Kronor at each fiscal year end. Consequently, our results from operations are affected by fluctuations in the rate of exchange between Swedish Kronor and Norwegian Kroner.

Concordia Finland, which comprised approximately 8% of our revenue in the year ended February 29, 2004, prepares its financial statements in, and its functional currency is, the euro. In preparing our consolidated financial statements, we translate Concordia Finland's financial statements into Swedish Kronor at each reporting period. Consequently, our results from operations are affected by fluctuations in the rate of exchange between the Swedish Krona and the euro.

Further, we are also exposed to currency fluctuations on loans, primarily as a result of having to make interest and principal payments in euro on the Senior Subordinated Notes and Senior Secured Notes. We have entered into collar arrangements through the sale of puts and the purchase of calls with the same settlement dates, while this arrangement caps the amount of benefits we can obtain from an appreciation of the Swedish Kronor against the euro, it also caps our potential increased interest costs through a depreciation of the Swedish Kronor against the euro. Our policy is to hedge 50% of our future interest payments on the Senior Subordinated Notes against adverse movements in the Swedish Kronor/euro exchange rate and to hedge 50% of our future payments on the Senior Subordinated Notes through a cap in positive movements for us in the Swedish Kronor/euro exchange rate. See subheading "B. Liquidity and Capital Resources," under "Item 5. Operating and Financial Review and Prospects." We estimate that, a 10% depreciation in the value of the Swedish Krona against the euro would increase our interest costs relating to the Senior Subordinated Notes and Senior Secured Notes by approximately SEK 27.2 million per annum (assuming a SEK 9.2175/€ 1.00 exchange rate and assuming that we successfully hedge 50% of our exposure). Any such depreciation could have a material adverse effect on our financial condition.

Item 4. Information on the Company

A. History and Development of the Company

Our legal name is Concordia Bus AB (publ) and our commercial name is Concordia. We were incorporated on September 17, 1999. Concordia is domiciled in Sweden and is a public limited liability company. We are incorporated in Sweden and our registered address is Solna Strandväg 78, SE 171 54, Solna, Sweden. Our financial year ends on the last day of February. Our authorized and issued share capital is SEK 500,000 divided into 5,000 shares of one class with a nominal value of SEK 100 each. The share capital is fully paid. Our telephone number is +46 8 546 300 00. Our agent for service of process is CT Corporation System, 111 Eighth Avenue, New York, New York 10011.

In January 2000, Concordia, backed by SG (the then parent company of SBC) and certain private equity funds affiliated with Goldman Sachs International, acquired Concordia Bus Nordic. In February 2001, we acquired SBC.

10

B. Business Overview

We provide public bus transportation services in Sweden, Norway and Finland, operating through our three main operating subsidiaries: Swebus, SBC and Concordia Finland, respectively. We also provide express bus and coach hire services. In Sweden, we currently operate 3,156 buses, and are the largest operator through Swebus, with an estimated market share of approximately 31.3% of the public bus transportation market (measured by the number of buses in operation). In Norway, SBC currently operates approximately 405 buses and has an estimated 20% market share of the public bus transportation market in southeastern Norway, which includes Oslo and neighboring cities. In Finland, Concordia Finland currently operates 347 buses and is the second largest operator in the greater Helsinki area with a market share of 26%.

For the year ended February 29, 2004, we had net revenue of SEK 4,761 million.

Our core business is providing bus services to local public transportation authorities in Sweden (our most important market), Norway and Finland. In our markets, the substantial majority of bus transportation services are provided under long-term contracts (generally five to eight year terms) with local public transportation authorities, according to which the bus operator provides services for a specific set of bus routes for fixed annual fees (subject to periodic adjustments based on price indices) which we refer to as "gross agreements." These contracts provide us with steady revenue streams because we receive a fixed annual amount from the respective public transportation authorities rather than relying on passenger ticket receipts. Certain contracts, called "net agreements," include passenger numbers as part of their pricing. Public transportation authorities have shown an excellent record of payment and have in the past rarely faced bankruptcy or insolvency. In the year ended February 29, 2004, we derived approximately 89.1% of our revenue from a combination of gross agreements and net agreements in Sweden, Norway and Finland. We operate under approximately 200 contracts with local public transportation authorities, the largest of which accounted for only 5.2% of our net revenue in the year ended February 29, 2004. The top 25 contracts accounted for approximately 51.2% of net revenue in the year ended February 29, 2004.

We also provide express bus services (scheduled intercity or long distance bus services) and coach hire services.

Following deregulation in 1989, there was a wave of consolidation in the Swedish bus market. This has resulted in three large operators who have a combined market share in the contractual public bus transportation market in Sweden of approximately 64% (measured by the number of buses in operation). Swebus is the largest operator with a 31% market share. (Source: Svenska Lokaltrafikföreningen, the Swedish local traffic organization, or "SLTF".) Recent tenders for bus transportation contracts provide evidence that consolidation in the industry in Sweden has produced a more favorable pricing environment. We expect this trend to continue in the near term. We also believe that a similar pattern of pricing dynamics is now beginning to occur in Norway and Finland.

11

Over the last two years, we have rolled out the initial phase of the Hastus planning system at all our locations. In its initial phase of use, the Hastus system captures traffic planning data and uses it to produce unoptimized bus and driver schedules. The subsequent phase of Hastus use involves the entry of additional data, in particular data relating to the relationships among different bus routes, to produce optimized schedules. We augment our use of Hastus with Sintopt, our proprietary logistics system. Sintopt uses higher level algorithms to enable us to achieve increased levels of optimization with our bus and driver schedules. We have also strengthened our traffic planning department in order to better utilize our driver and bus fleet resources. Currently approximately 34% of our driver hours have been subject to some level of optimization. We believe we will achieve 100% optimization of all traffic plans within the next 18 months. We expect to fully realize further cost savings from the implementation of these systems of SEK 30 million to SEK 40 million during this period, in addition to the cost savings of approximately SEK 18 million already realized. In addition, we have also identified other sources of cost savings, including fuel consumption optimization, purchasing cost savings, and reductions of employee sickness and absences.

The improved planning and scheduling described above, combined with an integrated plan for bus fleet utilization and maintenance, enable us to determine with a higher degree of certainty the optimal number of buses needed for our existing operations. We are currently in the process of developing a capital optimization system, which we expect will be functional in the second quarter of fiscal 2005. The system will help us minimize bus investments by allowing us to align the characteristics of our bus fleet to the average and maximum age specified in our contracts. In addition, we are focusing our efforts on utilizing our existing fleet to provide new revenues through alternative uses, such as local coach and school bus hire.

We have improved our bus maintenance procedures by implementing a new fleet maintenance planning system, known as ASW. ASW improves our ability to schedule bus maintenance and capture costs and analyze data for cost reduction. Going forward, we will improve our ability to schedule maintenance staffing requirements through implementation of an updated version of ASW. We have also reduced the number of different types of buses in our fleet by reducing the number of manufacturers and models we use. In line with our operating lease strategy we have entered into framework agreements for the supply of buses with Volvo and Evobus. We have re-negotiated our agreement with Volvo, securing our requirements for the next four years. We believe that further bus standardization will continue to reduce maintenance costs and downtime and increase bus utilization.

We have developed and are in the process of implementing a web-based system for our personnel (such as tracking absence for medical reasons) and a new Operational Management System (OMS). This system is the last phase of our IT strategy and brings together operational data residing in our centralized database and provides several new ways for us to track our business operations, such as kilometer/fuel tracking, driver activity capture and daily production statistics. The system is now operational in a majority of our locations.

As the largest operator of buses in the Nordic region, we have achieved significant savings by centralizing more of our bulk/commodity purchasing. We obtain the majority of our diesel fuel requirements in bulk from the major Nordic petroleum companies. We rent our tires from Michelin on a per-kilometer basis. We have succeeded in increasing the percentage of purchases that we make under centralized purchase agreements (excluding fuel and tires) from 10% in 1999 to approximately 91% today and expect to increase the utilization of central purchasing agreements further.

12

We have reduced the impact of cost volatility within our business by negotiating for contract adjustment provisions that better reflect operating costs. The level of the fee paid to us by local public transportation authorities is adjusted periodically based on an index. Historically, a substantial portion of contracts have contained cost indices based on a consumer price index, which did not appropriately reflect key elements of our cost base such as wages and diesel fuel. We now increasingly seek to include a combination of a consumer price index and a labor cost index as well as a diesel fuel price index in proportion to our underlying cost base. We have also sought to reduce the impact of cost volatility within our business through fuel price and foreign exchange risk hedging.

Our ultimate goal is to move towards becoming an "asset free" bus operator that acquires transportation capacity by the kilometer and focuses on providing the most efficient bus service possible. We have initiated a program designed to reduce our residual asset value risk and significantly reduce operating risks, financing costs and capital employed. This program is based on a combination of residual value guarantees and operating leases. In the year ended February 29, 2004, we had 1,317 buses under operating leases with a present value of future minimum lease payments of SEK 905 million. The key elements of this strategy for us are (i) to match operating lease terms with the duration of the underlying public transportation contracts and (ii) to obtain residual value guarantees from bus manufacturers. If we are successful in implementing this strategy more broadly, we will substantially eliminate our capital expenditures on buses, thereby freeing up considerable capital.

Sweden

General

As of February 29, 2004, we operated 3,156 buses in three bus transportation markets in Sweden:

- •

- contractual public bus transportation;

- •

- express bus services (scheduled intercity or long distance bus services); and

- •

- coach hire services.

Contractual public bus transportation services operated 2,989 buses, express bus services 99 buses and coach hire services in Sweden operated 68 buses. Our Swedish operations generated revenue of SEK 3,986 million for the year ended February 29, 2004.

Contractual Public Bus Transportation Service

As of February 29, 2004, we were operating 2,989 buses under 154 public bus transportation contracts with local public transport authorities.

As of February 29, 2004, we had a market share of approximately 31.3% (in terms of number of buses) of the Swedish contractual public bus transportation market. We have a relatively even distribution of our contract portfolio in terms of revenue among the southern, eastern and western regions of Sweden. Due to the economics of the bus industry in the northern region of Sweden, we have a smaller presence in this region. We intend to focus on areas of high urban concentration and to review our contract portfolio critically with regard to smaller, less profitable contracts, particularly those relating to areas of relatively low population density.

The greater city area of Stockholm, together with Gävleborg, Halland, Malmö and Uppsala, are our most important markets, and collectively account for approximately 62% of our total revenue in Sweden.

Bus services are provided in the Swedish public bus transportation market according to publicly tendered contracts entered into by bus operators with local public transport authorities. See the heading "Regulation—Tendering Procedures" in this section.

13

Most Swedish bus operators have similar cost bases, as most bus drivers are in the same unions and most buses meet similar specifications. We believe the difference in competitive power comes from a bus operator's ability to optimize its depot structure, its skill in planning and scheduling, and its ability to solve the complex logistical issues involved in meeting the requirements of the contracts. Having access to a large fleet and being able to shift resources significantly benefit the larger operators.

Regulation

In Sweden, the administration of public transportation for a particular region is delegated to the relevant local public transport authorities, which plan, price and coordinate public transport within their geographical area and which enter into contracts with both public and private operators. There are 24 independent local public transport authorities in Sweden, which cover the 21 provinces of Sweden and its five largest cities.

Prior to 1989, public transportation contracts were not subject to competitive tendering procedures and operators typically monopolized a particular public authority's geographical area of responsibility. In 1989, Sweden began requiring, subject to specific exceptions, local public transport authorities purchasing bus services to conduct competitive tender procedures. This deregulation and the resulting price competition led to a reduction in contract prices by an estimated 20% to 30% in real terms in the decade after competitive tendering requirements were introduced in 1989. During this period, the underlying costs for bus operators increased significantly due to increases in vehicle and diesel fuel taxes and diesel fuel costs. Although operators are compensated based on a consumer price index which takes fuel costs into account, overall, in recent years, this index has not risen sufficiently despite the increase in the component based on fuel costs to reflect the increase in our costs. Therefore, operators have not been compensated in a manner allowing them to cover their increased costs fully. This trend led to consolidation in the industry and begun to produce a more favorable pricing environment. As a result, commencing in 1998 and to a greater extent in 2000 through 2003, we have renewed contracts at higher prices.

Tendering Procedures

Under Swedish law implementing European Union directives concerning public procurement, public bus transportation contracts must be awarded on a commercial basis and, subject to limited exceptions, must involve a competitive bidding process.

Typically, following a study of the community's transportation needs and input from transportation providers, the local public transportation authorities determine the required bus routes, schedules, fares and other requirements. Invitations to tender contain bid information packages which state the specific routes and timetables to be covered by the operator and usually contain requirements regarding bus types, technical standards (seats, age, design, etc.), exterior appearance requirements, the environmental standards (such as types of fuel, emissions standards and requirements for exhaust filters) and quality requirements.

The local public transport authorities are required to follow established criteria for awarding contracts, of which the single most important is typically price. Other factors may be considered, including the cost of adapting to a new operator and the level of service quality. In many cases, local public transport authorities choose to subdivide procurement into a series of contracts, each with a specified portion of a community's routes to avoid having a single operator dominating a large area.

14

Contracts

While each public transportation contract is different, there are many terms common to virtually all of them. These contracts, other than contracts for school bus transportation, are generally for five to eight year terms, although many have recently provided for the extension of the term. In some cases, there are options which may be exercised by either Swebus or the local transportation authority, but other options are exercisable only by the local transportation authority. Extension options exercisable only by the local transportation authorities generally provide for one or two year extensions.

The various criteria set forth in the bid information package, as described in the heading "Tendering Procedures" in this section, become part of the contracts. Bus operators must then seek to comply with these requirements as efficiently as possible. In isolated cases, there are provisions that an incoming operator must purchase used buses from the outgoing operator.

Public transportation contracts in Sweden usually provide for fixed fees to be paid to the operator in return for the contracted bus services, which fees are subject to monthly, quarterly, semi-annual or annual fee adjustments intended to account for changes in costs incurred. At present, contracts with local public transportation authorities that produce a substantial portion of Swebus' revenues in Sweden contain cost indices based on a consumer price index, although it is becoming increasingly common to negotiate indices which reflect bus industry costs or an index which contains a labor or fuel cost component. Although management believes that Swebus' indices will match bus operation industry costs more closely than in the past, there can be no assurance this will be the case. See the subheading "D. Risk Factors—If indices in our contracts do not reflect our cost increases, our business could be adversely affected" under "Item 3".

Over 90% of the public transport contracts subject to competitive bidding are gross agreements, which means the operator receives a fixed amount (usually per vehicle kilometer) for operating the routes and there is no direct financial benefit to the operator for increasing passenger volumes. The local public transportation authorities retain all ticketing revenues and set the fares.

Express Bus Services

We operate an extensive network of express bus services under the trade name "Swebus Express" which operates under a separate legal entity called "Swebus Express AB" and provides public long distance transportation. In the year ended February 29, 2004, we employed approximately 99 buses on a full time basis for express bus services in Sweden. We operate daily and weekend services throughout Sweden, as well as international routes between Oslo and Stockholm and Oslo, Gothenburg and Copenhagen. Our express buses covered in aggregate approximately 354,000 kilometers per week during the year ending February 29, 2004, and transported more than 3.0 million passengers.

For the year ended February 29, 2004, express bus services in Sweden had total revenue of SEK 327 million. Providing an extensive national network and a seamless mode of transport between a large number of destinations has become Swebus' main competitive advantage. Swebus Express sells tickets on the buses as well as in advance through ticket agencies. Swebus' policy is to provide coaches for any passengers who want to travel and who arrive at the applicable embarkation points at scheduled departure times. We do not allocate particular seats for passengers. We offer discounts for children, students and pensioners as well as for all passengers traveling on Mondays to Thursdays inclusive (subject to some exceptions). Management believes that the increase in the amount of pensioner travel on Swebus Express reflects pensioners' growing demand for inexpensive flexibly scheduled travel.

15

Express bus services in Sweden are generally deregulated so that an express bus service operator has full responsibility for all aspects of the service, including route planning, schedules and fares. In some regions, express bus services are combined with regional or local public bus services. In these circumstances the local public transportation authorities compensates the express bus operators for making a number of stops in proximity to a regular local public bus service within a region.

We believe that the express bus service industry will enjoy continued growth as more routes are developed and more passengers appreciate the price competitive service as compared to rail and airline services and, more importantly, the high costs of driving private cars. Based on current demographic trends, we expect that the potential passenger base for express bus services will expand as the number of people engaged in long-distance employment or studies increases.

Coach Hire Services

We also operate a coach hire service under the name "Interbus," which operates under a separate legal entity called "Interbus AB." The coach hire market involves providing chartered bus services, as well as daily and weekend excursions, sightseeing tours and special events. Interbus operates a coach hire service business in the Stockholm and Gothenburg areas. As of February 29, 2004, Interbus operated approximately 68 full-time coaches and additional express buses as needed. Our coach hire bus fleet consists of a range of buses from small 10-seat buses to large luxurious sleeper coaches.

For the year ended February 29, 2004, we had total third party revenue of SEK 137 million from coach hire services in Sweden. The Swedish coach hire market is concentrated primarily in densely populated areas, such as Stockholm, Gothenburg and Malmö. The customer base for the coach hire market is diverse, ranging from small groups organizing private outings to organizers of major sporting events.

Interbus' typical customers include major event planners, corporations and travel agencies. Swebus' coach fleet size enables it to meet the requirements of a wide range of customers and to manage bus transportation for both small and large events. We are one of a few major operators in Sweden which has the capacity to satisfy larger customers. A significant and growing portion of the coach hire service is related to cruise line operations. Our fleet size improves our competitiveness in this market because cruise ships require operators with significant carrying capacity to ferry people between the ship and the relevant city, or to provide sightseeing tours.

Competition in the Swedish Bus Transportation Market

Contractual Public Bus Transportation

Deregulation has changed the nature of competition in the Swedish bus industry. Over the past several years, the Swedish contractual public bus transportation market has experienced intense price competition. In this competitive pricing environment, large companies with advantages of economies of scale, such as Swebus and Connex, have enjoyed expansion at the expense of relatively inefficient larger carriers (including operators owned by the local public transport authorities) and smaller bus operators. As a result of this competition there are currently three large private bus operators.

The Swedish contractual public bus transportation market features a few operators that hold large shares of the market and many small local operators. Management believes that the relative market shares of the three largest Swedish bus operators are Swebus (with approximately 31.3% of the market), Busslink (with approximately 16% of the market) and Connex (with approximately 17% of the market). (Source: SLTF). Swebus, Busslink and Connex are the only national competitors.

16

In rural markets, and, in particular, in the northern region of Sweden, large bus companies face stiff competition from small, privately owned local operators, who have formed into loose cooperative ventures in which bus fleets are pooled and who can operate very flexible schedules and are not heavily unionized. These factors, combined with the lower levels of operations in northern areas that do not benefit large scale operators, allow these smaller operators to bid for services at prices that are often not economically viable for larger operators such as Swebus.

In general, we believe that we face more competition on tenders that require less than 50 buses, as there are more operators capable of servicing such requirements. In the tenders for larger contracts, such as in the major cities, there is generally a maximum of four operators tendering.

Express Bus Services

The express bus market in Sweden is fully open to competition and is highly fragmented. In the year ending February 29, 2004, we had more than 50% market share of the Swedish express bus service market, as measured by kilometers served. (Source: SLTF). We operate 99 buses in this market. The next largest operator is Säfflebussen, which operates primarily between Gothenburg and Stockholm and to Oslo. Säfflebussen has a market share exceeding 20%.

The third largest operator is Svenska Buss, which is a joint venture among seven privately owned bus companies and operates primarily in the south of Sweden. Svenska Buss has a market share of about 10% and operates primarily between Stockholm and several northern cities.

Coach Hire Services

The coach hire market is fully open to competition, and is more fragmented than the contractual public bus transportation market. While we dedicate approximately 68 buses to coach hire services, the market is characterized primarily by small to medium sized operators. The medium sized operators typically have between 10 and 20 buses. The small operators are usually private companies operating up to four buses, where the owners of the buses both drive and maintain the buses themselves. The small operators are cost efficient and highly competitive, but cannot bid for larger contracts due to their limited resources. Within the bus industry, the coach hire market is the segment that is most sensitive to general economic conditions, as tourism and attendance of special events are more directly affected by economic conditions than the basic transportation requirements provided by public contractual bus operators. Nevertheless, we have been able to adjust the scale of our coach hire operations, so that our operating margins in this segment have been less volatile than revenues in times of downturns.

Insurance

Swebus carries the following types of insurance: general legal and product liability, property and business travel insurance. We generally self-insure with respect to ordinary course damage to our bus fleet. Swebus believes that it carries types and levels of insurance that are consistent with the types and levels carried by other major bus operating companies in Europe. Swebus does not carry business interruption insurance, but this is common for many European businesses, particularly those (like Swebus) in which the risk of major interruption of business is small.

Environmental Matters and Other Regulations

We are required to comply with a series of Swedish and EU environmental, health, and safety regulations. These regulations include requirements regarding emission standards, safe storage of diesel fuel, and proper maintenance for the buses. In addition, public transportation contracts stipulate additional environmental standards relating to emission standards and the maintenance of the bus fleet. We believe that Swebus materially complies with these regulations and contract requirements.

17

Intellectual Property

Swebus has six registered trademarks in Sweden: "Swebus Express," "Nepal Resor," "Resecentrum," "Fjällexpressen," "Helsingborgstrafiken," "Swebus" and our company logo. In addition, "Swebus" is a registered trademark in the European Union.

Drivers and Other Personnel

For the year ended February 29, 2004, we had an average of 6,182 full-time employees in Sweden. Should a company lose a public transportation authorities contract, it is often the case that drivers will move to the company that wins the contract. The incoming operator generally does not need to employ any of these drivers. However, under some circumstances, such as if the new operator hires additional drivers to service the routes on the contract, it must offer to hire from the pool of drivers previously employed by the outgoing operator before hiring elsewhere. We believe that of the new drivers we hired in the year ended February 29, 2004, approximately 100 can be attributed to our implementation of a Swedish law requiring a greater frequency of breaks for drivers.

Collective bargaining agreements

The majority of our drivers and maintenance personnel in Sweden are members of trade unions. The principal union to which the drivers and maintenance personnel belong is Svenska Kommunalarbetareförbundet (the Swedish Municipal Workers Union). A small minority of drivers belong to Svenska Transportarbetareförbundet (the Swedish Transportation Workers Union).

In Sweden, wages and general working conditions are generally the subject of nationally negotiated collective bargaining agreements. The collective bargaining agreement generally applicable to our blue collar employees expires on October 30, 2005. A separate collective bargaining agreement normally applies to operations under public tenders.

We believe that our relationships with our employees and unions are good. Swebus has only experienced one industrial disruption in the last five years, in February 1999. This strike was industry-wide in Sweden and lasted for 13 days. See subheading "D. Risk Factors—Risks Related to the Company—Our employees are heavily unionized. Bargaining power and strikes can hurt our business" under "Item 3."

Pensions

In addition to the state sponsored pension scheme, we provide pension benefits, under the terms of our collective bargaining agreements, through two plans: a defined benefit plan with Alecta covers the majority of our white collar employees; our blue collar employees are covered under a defined contribution plan with Fora.

Legal Proceedings

Swebus is not currently involved in any material legal proceedings.

Norway

Contractual Public Bus Transportation

SBC is the sixth largest bus operator in Norway, with 405 buses and a market share in the greater Oslo area of approximately 16.5% and a market share in southeastern Norway of 20%, based on results of competitive tenders. SBC's operations generated revenue of SEK 365 million for the year ended February 29, 2004.

18

SBC operates principally in the contractual public bus transportation sector in the city of Oslo and the greater Oslo area of Akershus. SBC also operates in the counties of Vestfold, Oppland and østfold in Southern Norway, SBC primarily operates under four traffic agreements, of which two have been renewed and amended on several occasions since their inception. In 1976, SBC entered into an agreement with Stor-Oslo Lokaltrafikk AS for public transportation outside the city of Oslo. Stor-Oslo Lokaltrafikk AS is controlled by the local public transportation authorities in the county of Akershus. In the last two years we have won two contracts and have increased our geographic presence in southern Norway. In addition, we have lost a number of contracts, including one in Slemmestad and one in Romerike.

In 2004, management estimates that the Norwegian market for contractual public bus transportation employed approximately 7,000 buses and amounted to NOK 8.9 billion (SEK 9.9 billion). There are 19 local public transport authorities in Norway each of which is responsible for public bus transportation in one of Norway's 19 counties.

Regulation

The administration of public transportation in Norway for a particular region is delegated to the relevant local public transportation authorities, which are responsible for planning, pricing and coordinating public transport within their geographical area. Local public transport authorities in Norway may subject bus service procurement to a competitive bidding process, but are not required by law to do so. As of February 29, 2004, only ten of the 19 local public transport authorities in Norway had opted to use competitive bidding methods as their means of distributing public transportation contracts. SBC expects, however, that further local public transport authorities will follow suit because of the significant cost savings associated with putting a contract up for competitive tender. If competitive bidding is not used, bus operators negotiate with local public transport authorities to provide exclusive service for specific routes for specified periods (up to ten years). Bus operators are aware that if they do not offer competitive prices, the authorities will open bidding either in a formal tendering process or by simply requesting competitors to approach them with offers. The threat of competitive bidding has also increased the bargaining power of the public authorities and caused prices to decrease. The level of public subsidies varies largely from province to province in Norway, and management estimates that the average level of subsidies in Norway is approximately 40%. SBC believes that the general trend is that the level of subsidies is generally decreasing. For further information relating to subsidies, see the subheading "D. Risk Factors—Risks Related to the Company—The local public transport authorities rely on government subsidies. Removal of these subsidies could drive down local public transportation authorities' contract fees" under "Item 3. Key Information."

Competition

In Norway, the public transportation market has begun to experience developments similar to those that have occurred in Sweden. These developments include price competition and consolidation. Nevertheless, the Norwegian bus industry remains fragmented with approximately 240 bus companies operating a total of approximately 8,700 buses in 2003. Almost 60% of Norwegian bus operators had fleets averaging under ten buses. In contrast to Sweden, competitive bidding is not prevalent and has instead been used for smaller contracts to obtain a "signal price," which is then used as a target for renegotiating the entire contract portfolio.

SBC is a major operator in greater Oslo. On a national level, both Norgesbuss AS and Nettbuss AS (owned by Norges Statsbaner BA, the state railway operator) have significantly larger fleets than SBC, but neither of them are dominant in any single region.

19

Since 1989, contracts with public transport authorities in Norway to provide bus services have been potentially subject to competitive bidding procedures. The ability to compel competitive bidding has increased the bargaining power of the public authorities, particularly in recent periods, and they have been able to obtain price reductions in their contracts with SBC and increased the risk that SBC will lose its contracts for bus routes. For further information about risks relating to our current contracts see the subheading "D. Risk Factors—Risks Related to the Company—If we lose many local public transportation authorities' contracts as they are renewed or we are unable to win new contracts, our business will be adversely affected. Further, if we experience difficulties in operating under our existing contracts, our business may be adversely affected" under Item 3.

Operating leases

In order to meet SBC's requirements for new buses, SBC intends to continue to enter into operating leases. In addition, SBC benefits from a residual value guarantee arrangement for buses purchased from the Schøyen Group on July 1, 1999. Schøyen Group entered into an agreement with Evobus permitting the Schøyen Group to return buses to Evobus according to stipulated residual value schedules (which are subject to adjustments). Evobus has made available all the benefits under this agreement to SBC. The arrangement provides for limitations in specific circumstances on the number of buses that may be returned in any year and on the aggregate number of buses that may be returned in a multi-year period.

Drivers and Other Personnel

For the year ended February 29, 2004, SBC had an average of 580 full-time employees.

Nearly all of SBC's employees are represented by unions under the terms of industry-wide collective bargaining agreements. All union agreements are renegotiated every two years. The largest collective bargaining agreement, which covers drivers and maintenance personnel, expires on January 31, 2005.

SBC considers its relations with its employees and the unions to be good.

Legal Proceedings

SBC is not currently involved in any material legal proceedings.

Finland

Contractual Public Bus Transportation

We operate a Finnish public bus transportation business through our principal subsidiary in Finland, Concordia Finland. Concordia Finland is a major bus operator in Finland with approximately 347 buses in operation as of February 29, 2004, and approximately 30 public bus transportation contracts with local public transport authorities. Our Finnish operations generated revenue of SEK 396 million for the year ended February 29, 2004. Concordia Finland operates only in the Finnish contractual public bus transportation sector in the greater Helsinki area in the cities of Helsinki, Vantaa and Espoo, and does not offer either express bus or coach hire services.

Management estimates that in 2004, the Finnish bus market employed approximately 8,800 buses and included approximately 400 operators. The Finnish bus market is well developed in both rural and urban areas. Finland's geography and low population density make bus transportation very competitively priced as compared to railway services. Additionally, the passenger railway network is centered on Helsinki and is being reduced in rural areas. This situation provides an advantage to bus operators because they can offer bus passengers the possibility to make more convenient cross country trips than on the railways.

20

The greater Helsinki area, with a total population of approximately one million, is Finland's largest market for contractual public bus transportation. The greater Helsinki area and Turku are the only markets currently subject to competitive bidding. Significant price pressure has led to consolidation in these areas. Except for the greater Helsinki and Turku areas, local traffic in most cities is largely provided by local operators.

Regulation

As in Sweden, the administration of public transportation in Finland for a particular region is the responsibility of the local transportation authority. In greater Helsinki and Turku, public transportation authorities have opened their local public transportation contracts to competitive bidding. In 1994, the Helsinki Metropolitan Area Council (commonly known as the YTV), which is the authority that regulates inter region public transport traffic between the three cities of Helsinki, Espoo, and Vantaa, was the first to initiate competitive bidding in Finland. Although the YTV and the public transport authorities regulating public transport traffic within the cities of Helsinki, Espoo, Vantaa and Turku represent the only regions currently open to competition, the EU directives concerning public procurement, along with the prospect of cost savings for local authorities, is expected to increase the number of regions open to competitive bidding. Concordia Finland expects an increase in the number of regions subject to competitive tendering in the near future.

Currently, in areas other than those referenced above, the local public transport authorities have granted independent operators licenses to run bus services, which essentially gives each operator a monopoly position. Licenses are normally granted for a three to ten year period and are usually renewed with the same operator. We do not have any contractual public bus services agreements in areas not subject to competitive bidding.

Contracts and Contract Tendering

In the YTV region, and other areas in which competitive bidding has been instituted, the contract structure and bidding and procurement procedures closely resembles that of the local public transportation authorities contracts in Sweden described in the subheading "Sweden—Tendering Procedures" and "Sweden—Contracts" in this section. Typically, the public transportation contracts have four to five year terms and under these contracts all ticket revenues are forwarded to the local public transportation authorities and the operator receives fixed fees. The compensation is adjusted periodically by reference to an index intended to cover cost items that relate to the bus transportation industry such as drivers' wages, cost of buses and fuel.

Drivers and Other Personnel

For the year ended February 29, 2004, Concordia Finland had an average of 750 employees.

All of Concordia Finland's employees are represented by unions under the terms of industry-wide collective bargaining agreements. The largest collective bargaining agreement, which covers drivers and maintenance personnel, expires on February 1, 2006.

Concordia Finland considers its relations with its employees and the unions to be good. See subheading "D. Risk Factors—Risks Related to the Company—Our employees are heavily unionized. Bargaining power and strikes can hurt our business" under "Item 3. Key Information."

21