Exhibit 99

| Orient-Express Hotels Analyst & Investor Day November 13, 2007 |

| Forward-Looking Statement This presentation and the accompanying remarks by management contain, in addition to historical information, forward-looking statements that involve risks and uncertainties. These include statements regarding earnings outlook, investment plans and similar matters that are not historical facts. These statements are based on management’s current expectations and are subject to a number of uncertainties and risks that could cause actual results to differ materially from those described in the forward-looking statements. Factors that may cause a difference include, but are not limited to, those mentioned in the presentation and remarks, unknown effects on the travel and leisure markets of terrorist activity and any police or military response, varying customer demand and competitive considerations, realization of hotel bookings and reservations and planned property development sales as actual revenue, inability to sustain price increases or to reduce costs, fluctuations in interest rates and currency values, uncertainty of negotiating and completing proposed capital expenditures and acquisitions, adequate sources of capital and acceptability of finance terms, possible loss or amendment of planning permits and delays in construction schedules for expansion or development projects, delays in reopening properties closed for repair or refurbishment and possible cost overruns, shifting patterns of tourism and business travel and seasonality of demand, adverse local weather conditions, uncertainty of recovering on insurance claims for property damage and lost earnings, changing global and regional economic conditions, and legislative, regulatory and political developments. Further information regarding these and other factors is included in the filings by the company with the U.S. Securities and Exchange Commission. Management believes that EBITDA (net earnings adjusted for interest expense, foreign currency, tax, depreciation and amortization) is a useful measure of operating performance, for example to help determine the ability to incur capital expenditure or service indebtedness, because it is not affected by non-operating factors such as leverage and the historic cost of assets. EBITDA is also a financial performance measure commonly used in the hotel and leisure industry, although the company’s EBITDA may not be comparable in all instances to that disclosed by other companies. EBITDA does not represent net cash provided by operating, investing and financing activities under U.S. generally accepted accounting principles, is not necessarily indicative of cash available to fund all cash flow needs, and should not be considered as an alternative to earnings from operations or net earnings under U.S. generally accepted accounting principles for purposes of evaluating operating performance. |

| Corporate Overview Orient-Express owns or part-owns and operates 50 luxury hotels, restaurants, tourist trains and river cruise businesses operating in 25 countries. NYSE: OEH Market Cap: $2.5 billion Registered Office: Hamilton, Bermuda Number of employees: 7,100 worldwide |

| Industry Landscape Luxury market becoming increasingly crowded Differentiation is key US market is softening Global expansion, outreach and footprint will be increasingly important Industry experience expanding out of regional comfort zones has proven difficult for big brands Regional relevance and identity are keys to success Leisure travelers’ monies becoming more powerful |

| Key Differentiators Global hospitality and leisure company with exclusive focus on deluxe luxury market 40 hotels, two restaurants, six trains, two river cruise operations Client base More resilient but more demanding; good mix of leisure and business travelers Distinguished luxury brand names Orient-Express, Hotel Cipriani, Copacabana Palace, ‘21’ Club, Mount Nelson, Hotel Ritz Madrid Benefits of ownership Irreplaceable assets, high barriers to entry |

| Core Strategies Portfolio Management Expansion Real Estate Development Brand Opportunities |

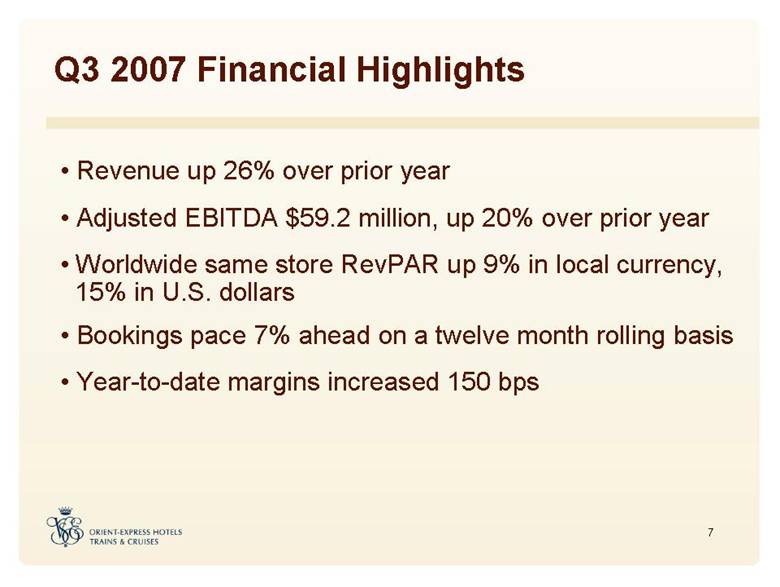

| Q3 2007 Financial Highlights Revenue up 26% over prior year Adjusted EBITDA $59.2 million, up 20% over prior year Worldwide same store RevPAR up 9% in local currency, 15% in U.S. dollars Bookings pace 7% ahead on a twelve month rolling basis Year-to-date margins increased 150 bps |

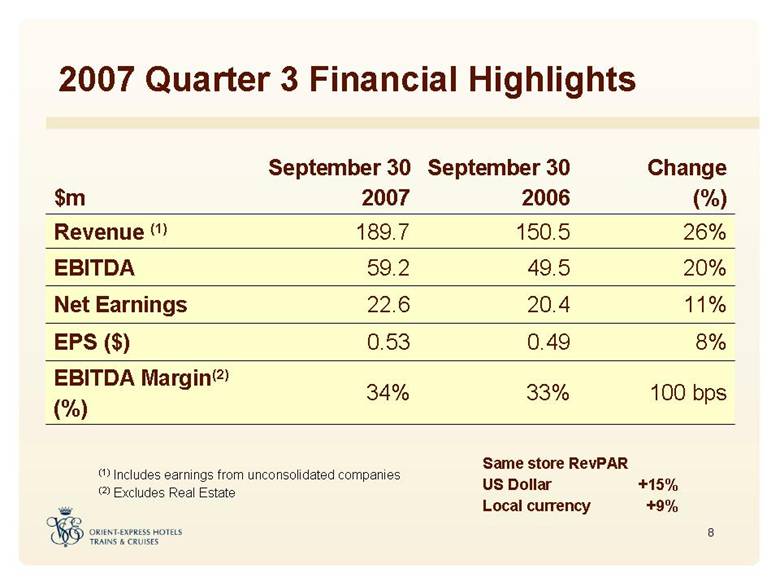

| 2007 Quarter 3 Financial Highlights 100 bps 33% 34% EBITDA Margin(2) (%) 8% 0.49 0.53 EPS ($) 11% 20% 26% Change (%) 20.4 49.5 150.5 September 30 2006 22.6 59.2 189.7 September 30 2007 Net Earnings EBITDA Revenue (1) $m Same store RevPAR US Dollar +15% Local currency +9% (1) Includes earnings from unconsolidated companies (2) Excludes Real Estate |

| 2007 9 Month Results 150 bps 28% 29% EBITDA Margin (%) (2) 11% 0.82 0.91 EPS ($) 17% 17% 23% Change (%) 33.1 105.7 372.0 September 30 2006 38.6 123.2 457.1 September 30 2007 Net Earnings EBITDA Revenue (1) $m Same store RevPAR US Dollar +13% Local currency +9% (1) Includes earnings from unconsolidated companies (2) Excludes Real Estate |

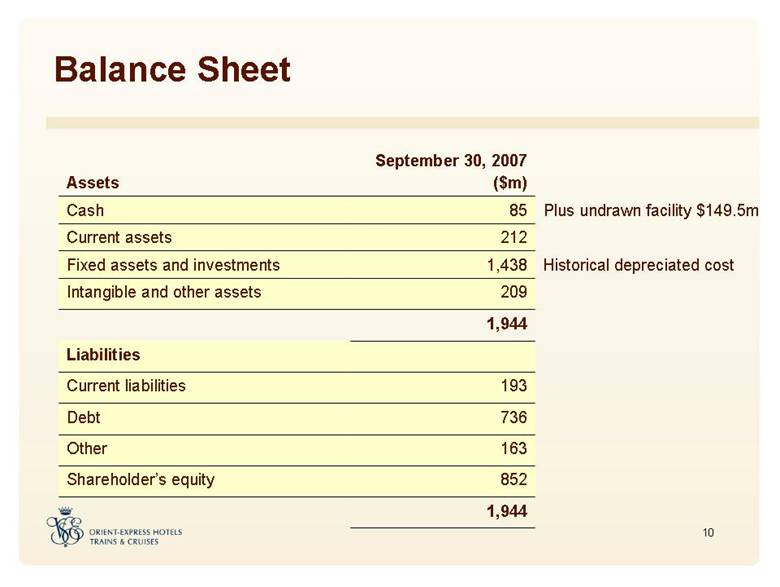

| Balance Sheet 1,944 1,944 852 Shareholder’s equity 163 Other 736 Debt 193 Current liabilities Historical depreciated cost Plus undrawn facility $149.5m 209 1,438 212 85 September 30, 2007 ($m) Liabilities Intangible and other assets Fixed assets and investments Current assets Cash Assets |

| Global and Expanding Existing Operations New Projects |

| Competitive Advantages of OEH Loyal, High-end Customer Base Combination of Luxury and Experience Global Geographic Reach Superior Asset Base Brand Strengths with Regional Resonance Solid Supply Pipeline Experienced and Focused Management Team Hired CFO Strong Balance Sheet Well-positioned for Growth |

| Core Strategies Portfolio Management Expansion Real Estate Development Brand Opportunities |

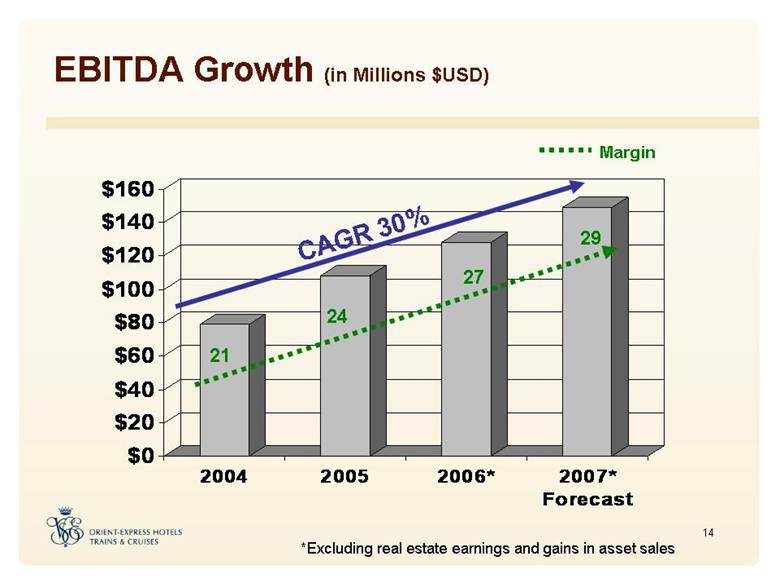

| EBITDA Growth (in Millions $USD) *Excluding real estate earnings and gains in asset sales 21 24 27 29 Margin CAGR 30% $0 $20 $40 $60 $80 $100 $120 $140 $160 2004 2005 2006* 2007* Forecast |

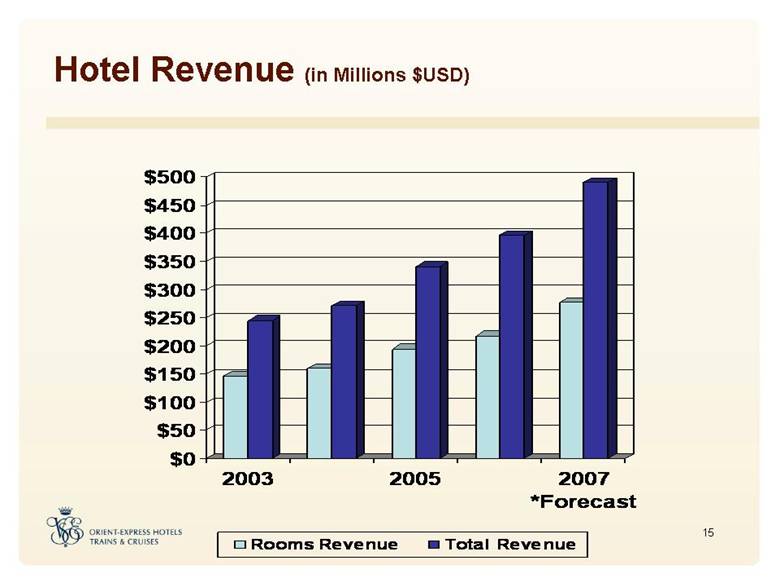

| Hotel Revenue (in Millions $USD) $0 $50 $100 $150 $200 $250 $300 $350 $400 $450 $500 2003 2005 2007 *Forecast Rooms Revenue Total Revenue |

| Increasing Total Revenue Grow food and beverage revenues Develop spa offering Grow retail opportunities |

| Portfolio Management - Key Priorities Give managers room and time to operate Maintain ownership culture Deliver quality experiences Manage asset portfolio Maximize profitability |

| Core Strategies Portfolio Management Expansion Real Estate Development Brand Opportunities |

| Acquisition Strategy Sharpening of Focus Looking at strategic and opportunistic acquisitions Building on legacy brands Regional resonance drives brand expansion More targeted throughout portfolio Strengthening of Structure Appointed CDO to lead efforts Looking at financial structures that will provide additional flexibility Seeking solid financial returns for new properties |

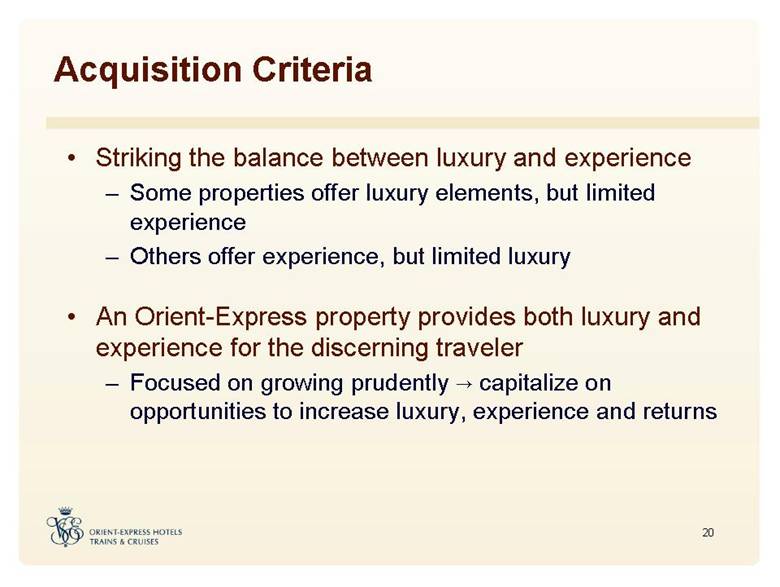

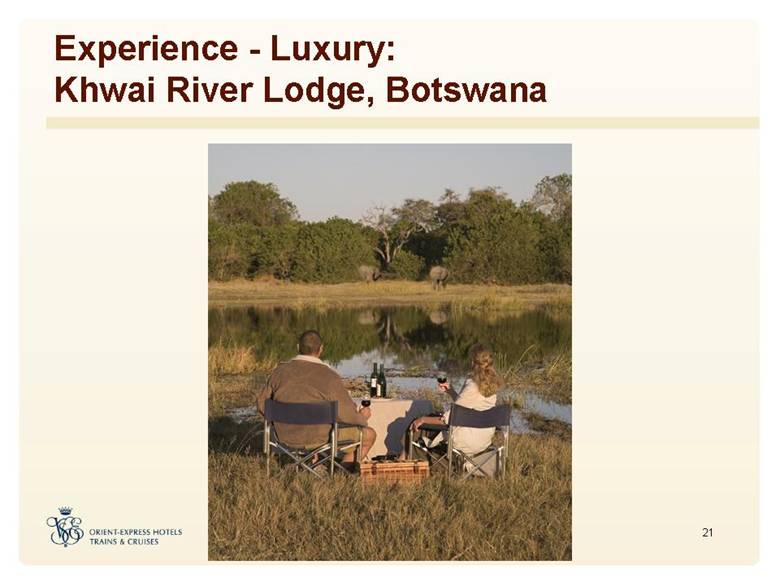

| Acquisition Criteria Striking the balance between luxury and experience Some properties offer luxury elements, but limited experience Others offer experience, but limited luxury An Orient-Express property provides both luxury and experience for the discerning traveler Focused on growing prudently —> capitalize on opportunities to increase luxury, experience and returns |

| Experience - Luxury: Khwai River Lodge, Botswana |

| Luxury - Experience: Hiram Bingham, Peru |

| Financial Return Plus Luxury and Experience: Grand Hotel Europe |

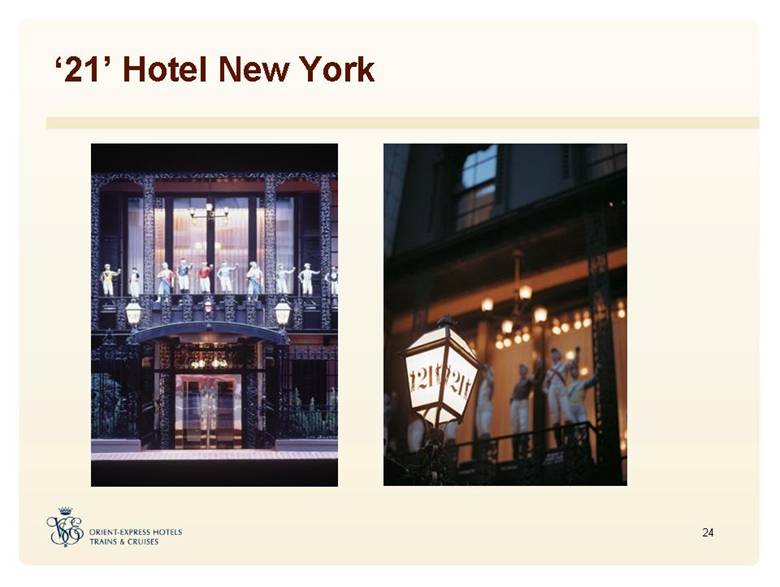

| ‘21’ Hotel New York |

| ‘21’ Hotel New York Great example of building out iconic legacy brand Circa 150 room property, personalized butler service Targeting 50/50 business and leisure traveler Leverage both the existing food and beverage facilities Other offerings will include retail, spa and wellness facilities Timing of Project: Construction 2009 – 2010 Opening early 2011 |

| Core Strategies Portfolio Management Expansion Real Estate Development Brand Opportunities |

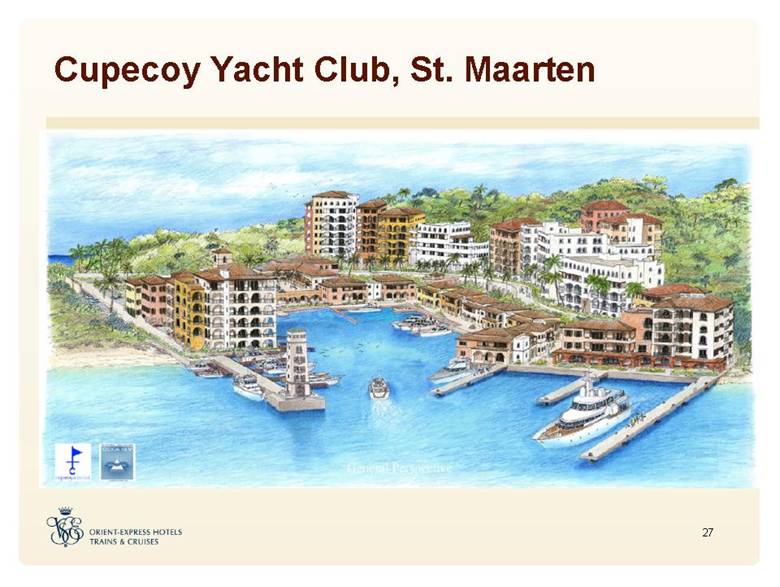

| Cupecoy Yacht Club, St. Maarten |

| Cupecoy Yacht Club, St. Maarten Mediterranean style 180-unit condominium, marina and village 40% pre-sold Condominium pricing – mid-upper scale $500 per sq feet average Marketing and sales resources to target European repeat island visitors including La Samanna regular guests OEH has knowledge, experience to increase sales figures Possible slowdown risks may affect earnings, limited pricing downside Total EBITDA USD$40M plus ongoing earnings $10-12M 2008, $10-$12M 2009, $8-$12M 2010 |

| Villas at La Samanna, St. Martin |

| Villas at La Samanna, St. Martin Eight luxury villas – four bedroom, 600 sq metres Private horizon edge pools Three master bedroom design French fiscal structure EBITDA Total US$11–$13M One villa retained in hotel inventory $4-$5M 2008, $7-$8M 2009 Phase II |

| Maroma Haciendas, Riviera Maya, Mexico |

| Maroma Haciendas, Riviera Maya, Mexico Limited to 25 homes of three to four bedrooms Timing: design and construction 2008 – 2009 EBITDA: $20 - $25 million Ongoing earnings: $4 - $6 million rentals and resort spend |

| Keswick Estate, Virginia, USA |

| Keswick Estate, Virginia, USA Charlottesville, Virginia’s leader in high-end real estate Destination country lifestyle living, featuring golf club, equestrian center, shooting and fishing EBITDA Total value of unsold lot sales: US$22M $2.5M 2007, $3M 2008, $18.5M 2009-10 Ongoing earnings will be generated by Keswick Club fees and spend |

| ‘21’ Hotel and Residences Potential destinations Chicago, Washington, Las Vegas, San Francisco, Miami and Boston Joint ventures with institutional partners and developers Branding and development fees Standard hotel management fees Balancing our ownership with fee income sources of earnings |

| ‘21’ Hotel and Residences Example: 225 key hotel - RevPAR $400 75 condominiums Condo pre-tax profit $70 – $80 million Ongoing operations EBITDA of $20 - $25 million Expected IRR: 20% |

| Longer Term Projects Napasai Villas Reid’s Palace Lapa Palace – conversion of the new wing into condominiums La Residencia Villas on adjoining land Buzios developments Inn at Perry Cabin – residential home sites on owned land Grand Hotel St. Petersburg residential building Cape Town winery and villas Jimbaran Bay villas Hotel Cipriani acquisition of nearby Palazzi |

| Core Strategies Portfolio Management Expansion Real Estate Development Brand Opportunities |

| Brand Strategy Build on existing strong brands Capitalize on regional brand power Strong brand in Europe Opportunity to grow standalone brand elsewhere Use umbrella brand where has greatest impact Growth of brands works best where attributes are part of societal fabric Copacabana Palace, Brazil —> grow throughout the rest of South America; similar strategy with ‘21’ Club brand throughout Americas Identify key brands which are best suited for expansion Including Cipriani, ‘21’, Copacabana Palace |

| Orient-Express Brands |

| Summary New Era for Orient-Express Hotels Portfolio Management Not just a RevPAR game Total Revenue per room available/occupied Increase margins Acquisitions Strategic focus Management attention Broader approach to structure of deals Continued quest for well priced deals |

| Summary Real Estate Existing opportunities Future tie-in to acquisitions Brand Opportunities Undervalued asset Time to leverage |

| Investment Highlights Brand Opportunities Geographic Reach & Expansion Superior Asset Base Loyal, High-end Customer Base Solid Supply Pipeline Favorable Demographics Experienced Management Team Strong Balance Sheet Strong Luxury Market |

| Orient-Express Hotels November 13, 2007 |