Exhibit 99.1

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 | |

| |

| PRUDENTIAL PLC’S STRONG MIX OF BUSINESSES AROUND THE WORLD POSITIONS US WELL TO BENEFIT FROM THE GROWTH IN CUSTOMER DEMAND FOR ASSET ACCUMULATION AND INCOME IN RETIREMENT. OUR INTERNATIONAL REACH AND DIVERSITY OF EARNINGS BY GEOGRAPHIC REGION AND PRODUCT WILL CONTINUE TO GIVE US A SIGNIFICANT ADVANTAGE. | |||||||

| OUR COMMITMENT TO THE SHAREHOLDERS WHO OWN PRUDENTIAL IS TO MAXIMISE THE VALUE OVER TIME OF THEIR INVESTMENT. WE DO THIS BY INVESTING FOR THE LONG TERM TO DEVELOP AND BRING OUT THE BEST IN OUR PEOPLE AND OUR BUSINESSES TO PRODUCE SUPERIOR PRODUCTS AND SERVICES, AND HENCE SUPERIOR FINANCIAL RETURNS. OUR AIM IS TO DELIVER TOP QUARTILE PERFORMANCE AMONG OUR INTERNATIONAL PEER GROUP IN TERMS OF TOTAL SHAREHOLDER RETURNS. | |||||||

| AT PRUDENTIAL OUR AIM IS LASTING RELATIONSHIPS WITH OUR CUSTOMERS AND POLICYHOLDERS, THROUGH PRODUCTS AND SERVICES THAT OFFER VALUE FOR MONEY AND SECURITY. WE ALSO SEEK TO ENHANCE OUR COMPANY’S REPUTATION, BUILT OVER 150 YEARS, FOR INTEGRITY AND FOR ACTING RESPONSIBLY WITHIN SOCIETY. | |||||||

| CONTENTS | |||||||

| 1 | Group Financial Highlights | 27 | Achieved Profits Basis – | ||||

| 2 | Chairman’s Statement | Operating Profit Before Amortisation of Goodwill | |||||

| 4 | Group Chief Executive’s Review | and Exceptional Items | |||||

| 6 | Our Brands | 28 | Insurance and Investment Products | ||||

| 8 | Business Review | New Business | |||||

| 12 | Financial Review | 29 | Statutory Basis – Summary Consolidated | ||||

| 16 | Corporate Responsibility Review | Profit and Loss Account | |||||

| 20 | Board of Directors | 30 | Statutory Basis – | ||||

| 21 | Summary Corporate Governance Report | Operating Profit Before Amortisation | |||||

| 22 | Summary Remuneration Report | of Goodwill and Exceptional Items | |||||

| 24 | Summary Directors’ Report | 30 | Analysis of Borrowings | ||||

| 24 | Summary Financial Statement | 31 | Statutory Basis – | ||||

| 25 | Independent Auditors’ Statements | Summary Consolidated Balance Sheet | |||||

| 26 | Achieved Profits Basis – | 32 | Basis of Financial Reporting | ||||

| Summary Results and Balance Sheet | 32 | How to Contact Us | |||||

| IBC | Shareholder Information | ||||||

| This Annual Review and Summary Financial Statement is only a summary of the Group’s 2003 Annual Report. | |||||||

| Any shareholder can obtain a copy of the Annual Report by contacting Lloyds TSB Registrars. The Annual Report can also be viewed in full on our Group website at www.prudential.co.uk | |||||||

GROUP FINANCIAL HIGHLIGHTS

†Operating profit and operating earnings per share exclude amortisation of goodwill and exceptional items. This basis of presentation has been adopted consistently throughout this Annual Review and Summary Financial Statement.

| PRUDENTIAL PLCANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 | 01 |

CHAIRMAN’S STATEMENT

2003 was not an easy year for the life insurance industry but I believe Prudential ended the year in a strong position and is well placed to take advantage of the upturn in world markets. Many people still think of us as a UK business, but the reality is that we are a major international financial services group with strong businesses also in Asia and the United States. This geographic diversification has grown significantly over recent years and is reflected in the percentage of total sales generated by our overseas operations, which increased from 40 per cent in 1998 to over 70 per cent in 2003.

The challenging market conditions of 2003, particularly in the first half, affected the financial results we announced in February. While total insurance and investment sales of £31.5 billion increased by 11 per cent at constant exchange rates, our new business achieved profits of £605 million decreased by 18 per cent and our modified statutory basis operating profits decreased 17 per cent to £357 million.

At our interim results last year in July, we said that we had reviewed our dividend policy to ensure that this reflected both our operating cash flows as well as our strategy of investing in the business for long-term growth. Accordingly, the Board has decided to pay a total dividend for the year of 16 pence per share. We recognise that the dividend payment is very important to many shareholders, large and small alike, and the reduction from last year will be unwelcome. But we believe that the new level is one from which it will be possible to grow the dividend in the future. The level of growth will be determined after considering the opportunities to invest in those areas of our business offering attractive growth prospects, our financial flexibility and the development of our statutory profits over the medium to long-term.

As markets around the world recover, a key issue to be addressed is the need to restore consumer confidence in financial services at a time when saving for long-term security has never been more important. At Prudential, we are very aware of our responsibility to our customers: they have placed their trust in us and we believe that more can be done to help prospective and existing customers understand the nature of the financial decisions they are taking. Our interest in informed and satisfied customers

goes beyond our immediate commercial interest. In many of the countries in which we operate, there is a recognition that the financial services industry should work in partnership with government, regulators and consumer groups to raise the basic level of financial skills.

Prudential regards financial education as an important objective in each of the geographic regions in which we operate, as well as forming a core part of our wider Group Corporate Responsibility programme. We run several initiatives to raise the financial literacy of consumers, our customers and our employees. Within the UK, our ‘Plan for Life Learning’ programme has been established in partnership with charities, research bodies and international organisations to deliver local programmes and encourage responsible policy development. This work runs alongside Prudential UK’s ‘Plan from the Pru’ which was launched in 2002 to encourage people to take more control of their financial health by providing them with a free, simple, step-by-step guide to finances focusing on key life stages. Education is also a part of the core philosophy of our businesses in Asia and the United States. PRUuniversity, for example, has been run by Prudential Corporation Asia since 2001, with the objective of providing high-quality training for its staff, sales agents and business partners. Related to these issues, I was pleased at the end of last year to be asked by the Chief Executive of the Financial Services Authority to serve on a group which is looking at ways to improve financial services capability. Further details of these and other initiatives in which Prudential is involved can be found in the Corporate Responsibility section of this Review.

During 2003, I visited a number of our operations around the world and continue to be struck by the enthusiasm and energy of our staff. I would like to thank them for their professionalism and commitment.

Over the last 12 months, there have been a number of changes to our Board. Mark Tucker resigned as Chief Executive of Prudential Corporation Asia (PCA) with effect from the end of June. Under his leadership, PCA has become the leading European life insurer in the region, and I would like to thank him for his significant contribution to Prudential and to wish him well for the future. In January 2004, Mark Norbom joined us as Chief Executive of PCA.

MAKING

INFORMED CHOICES

| 02 | PRUDENTIAL PLCANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 |

| ||||

| AT PRUDENTIAL, WE ARE VERY AWARE OF OUR RESPONSIBILITY TO OUR CUSTOMERS: THEY HAVE PLACED THEIR TRUST IN US AND WE BELIEVE THAT MORE CAN BE DONE TO HELP PROSPECTIVE AND EXISTING CUSTOMERS UNDERSTAND THE NATURE OF THE FINANCIAL DECISIONS THEY ARE TAKING. | ||||

Mark was previously with General Electric where he was President and Chief Executive Officer for GE Japan. He brings a wealth of experience to the role, as well as considerable knowledge of the region having worked in Asia for over 10 years, and I know that he will make a valuable contribution to the future prosperity of the Group.

Sir David Barnes stood down as a non-executive director at our Annual General Meeting in May, having served on the Board for over four years. Ann Burdus retired as a non-executive director at the end of the year, having served on the Board for seven years. I would like to thank them both for their invaluable contribution and to wish them well for the future. Two new non-executive directors were appointed during the year: Kathleen O’Donovan joined us in May; and Bridget Macaskill rejoined us in September having previously been a non-executive director at Prudential for almost two years until March 2001. We were delighted to welcome both of them to the Board.

Since this time last year, the Combined Code for listed companies has been amended to take account of proposals arising from the Report by Sir Derek Higgs on the role and

effectiveness of non-executive directors. We support the changes and believe that they represent a fair attempt to capture good governance practice. It is important to remember that the Code is a Code of Good Practice, subject to the principle of ‘comply or explain’; and that ‘best practice’ must depend on the specific circumstances of individual companies. Shareholders still need to look at individual cases and exercise judgement. M&G, our investment management business, is one of the largest investors in UK-listed companies and will continue to exercise such judgement.

Looking ahead, our Asian and US businesses are particularly well positioned for growth in their respective markets. And in the UK, although we are cautious about the operating environment in the short term, we believe that there are significant opportunities in the longer-term. The balance and diversity of the Group puts us in a strong position to generate attractive returns for shareholders.

SIR DAVID CLEMENTI

CHAIRMAN

| PRUDENTIAL PLCANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 | 03 |

| GROUP CHIEF EXECUTIVE’S REVIEW | ||||

In my review in last year’s Annual Review, I talked about the importance of our international reach and diversity of earnings and the need to manage the business prudently in challenging market conditions to preserve our strong competitive position and growth prospects in each of the markets we operate in around the world. This was particularly important during 2003 when instability in international markets, volatile bond and equity markets and an uncertain economic outlook all had a negative impact on consumer confidence for much of the year. Against this background, we maintained our clear focus on investing for value and allocated capital to those areas of our business generating higher returns. Specifically, we continued to grow our Asian operations; increased Jackson National Life’s market share in core product areas on a self-financing basis; and grew our shareholder-backed businesses in the UK. There were some increasingly positive trends in the third and fourth quarters as markets began to stabilise and sales started to recover, and we ended the year in good shape. We have one of the strongest UK life funds in the industry, our capital position is strong and we are well placed to manage the business for growth. GROUP RESULTS New business achieved profits of £605 million decreased by 18 per cent at CER, reflecting lower sales volumes in the UK and the US, and total achieved basis operating profits of £794 million were down 27 per cent at CER. Modified statutory basis (MSB) operating profits decreased 17 per cent to £357 million at CER, principally due to lower annual and terminal bonus rates in the UK in 2003 which affected the shareholder transfer from the long-term fund. | In these difficult markets, our continued focus on value and in particular higher margin business enabled us to report a Group new business margin of 38 per cent, a level that we have broadly maintained over the last five years. POSITIONING THE BUSINESS FOR GROWTH With approximately 70 per cent of the world’s retirement assets, the US is a key market for us. In Jackson National Life (JNL), we have one of the few life insurers to have a significant market position across the range of fixed, variable and equity-linked products and when combined with its broad distribution mix, this allows JNL to operate successfully across the economic cycle. Despite equity market volatility and the low interest rate environment during the year, JNL delivered strong results in 2003 with MSB operating profits up 15 per cent at CER. It remained focused on delivering value from retail markets while actively managing capital. Retail sales of £3.6 billion represented JNL’s second best year and over 90 per cent of JNL’s sales during the year came from products launched since the beginning of 2002, demonstrating its strength in product design and execution. Over recent years, JNL has developed into one of the leading life insurance companies in the fragmented US market and with its low cost base, |

|

| ||||

| 04 | PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 |

| UNDERSTANDING | ||||

| OUR MARKETS | ||||

flexible and innovative product range and broad distribution mix, JNL is well positioned to benefit from the upturn in the US savings market. The UK remains the toughest market in which we operate. Uncertain equity markets, low interest rates and the continuing government and regulatory reviews on the future of the industry have caused consumer appetite for long-term savings to remain weak. Against this background, Prudential UK has maintained its financial strength and focused on higher margin products where it has competitive advantage. It has also grown market share in key product areas, developed innovative new products, strengthened and diversified its distribution capabilities and maintained its focus on cost management. In 2003, the long-term fund earned a return of 16.5 per cent and over the last 10 years it has generated a compound annual return of 8.6 per cent, reflecting the benefits of our diversified investment policy. The fund remains well capitalised and is one of the strongest in the UK. The free asset ratio at the end of 2003 was approximately 10.5 per cent without taking account of future profits or implicit items. Although we remain relatively cautious for the UK in the first half of 2004, we believe that the long-term demographics are attractive and that as consumers increasingly look to financially strong and trusted brands when making their investment decisions, Prudential UK is well placed for growth. M&G maintained its good track record of profitable growth and investment performance, increasing its underlying profit by 43 per cent and total funds under management by 12 per cent. This strong result reflects M&G’s focus on effective cost control and the strength of its diversified product range in retail fund management, institutional fixed income, pooled life and pension funds, property and private finance. Egg continued to make excellent progress in the UK. It more than doubled its operating profit to £73 million, increased its customer base to almost 3.2 million and it now has a market share of almost six per cent of UK credit card balances. In France, Egg has 130,000 customers with 66,000 credit cards in issue. Egg France reported an operating loss for the year of £89 million and Group pre-tax losses were £34 million compared with £20 million in 2002. | MAXIMISING OUR STRENGTHS As a major international financial services group, one of our key strengths is our ability to maximise the synergies that exist across the Group for the benefit of our customers. Each of our business units around the world is focused increasingly on sharing ideas and expertise in areas such as customer service, product innovation, distribution and sales, and systems development. For example, the opening of our customer service centre in Mumbai was an initiative on which Prudential UK worked closely with PCA who already had considerable experience of the Indian market; PCA used JNL’s product and systems expertise to help launch a new variable annuity product in Japan and Korea; and the launch of the Flexible Investment Plan in the UK was based on the concept behind JNL’s Perspective II variable annuity which allows customers to tailor individual product features and benefits to their specific investment needs. As we continue to grow internationally, this ability to maximise the synergies that exist across our businesses is essential as we look to gain competitive advantage in our markets and grow the value of the Group. OUTLOOK

| |||

| JONATHAN BLOOMER | ||||

| GROUP CHIEF EXECUTIVE | ||||

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 | 05 |

|  | ||||||

| WHAT WE DO | Prudential is a leading life and pensions provider to | M&G is Prudential’s UK and European fund manager, | |||||

| around seven million customers in the United | with £111 billion of funds under management and | ||||||

| Kingdom | over 850,000 unit holder accounts | ||||||

| OPERATIONS | Products | M&G offers a range of over 40 funds and invests in | |||||

| AND PRODUCTS | • | Annuities | a wide range of assets including UK and international | ||||

| • | Corporate Pensions | equities, fixed interest, property and private equity | |||||

| • | With-profits Bonds | ||||||

| • | Savings and Investment | Retail products | |||||

| • | Protection | • | Open Ended Investment Companies (OEICs) | ||||

| • | Unit Trusts | ||||||

| Distribution Channels | • | Investment Trusts | |||||

| • | Direct to customers (telephone, internet and mail) | • | Individual Savings Accounts (ISAs) | ||||

| • | Independent Financial Advisers | • | Personal Equity Plans (PEPs) | ||||

| • | Business to Business (consulting actuaries and | ||||||

| benefit advisers) | Institutional Business | ||||||

| • | Partnerships (affinities and banks) | • | Segregated fixed interest, pooled pension funds, | ||||

| structured and private finance | |||||||

| ACHIEVEMENTS | IN 2003, THE LONG-TERM WITH-PROFITS FUND | UNDERLYING PROFIT INCREASED BY | |||||

| EARNED A RETURN OF | 43 PER CENT | ||||||

| 16.5 PER CENT | IN 2003 TO £70 MILLION | ||||||

| 06 | PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 |

![]()

| Egg plc is an innovative financial services company, providing a range of banking and financial services products through its internet site, www.egg.com | Jackson National Life (JNL) is a leading lifeinsurance company in the United States andhas more than 1.5 million policies and contractsin force | Prudential Corporation Asia (PCA) is the leading European life insurer in Asia with 23 life and fund management operations across 12 countries. Across the region, PCA has 11 operations with a top-five market share | |||||

| Products | • | Offers fixed, equity-indexed and variable | • | A comprehensive range of savings, protection | |||

| • Banking | annuities, term and permanent life insurance | and investment products tailored to the needs | |||||

| • Insurance | and institutional products | of each local market | |||||

| • Investments | |||||||

| • | Markets products in 50 states and the District | • | Pioneered a unit-linked product in Malaysia, | ||||

| Customers | of Columbia (in the State of New York through | Indonesia, the Philippines, Singapore and Taiwan | |||||

| • Over three million customers and a market | Jackson National Life Insurance Company | ||||||

| share of nearly six per cent of UK credit | of New York) through independent broker- | • | A network of over 110,000 agents serving more | ||||

| card balances | dealers, independent agents, banks, regional | than five million customers around the region | |||||

| broker-dealers and the registered investment | |||||||

| advisor channel | • | A total of 29 bancassurance agreements in | |||||

| 11 countries | |||||||

| • | JNL’s investment portfolio manager, PPM | ||||||

| America Inc., manages around US$68 billion | |||||||

| of assets | |||||||

| IN 2003, UK PROFITS MORE THAN | IN 2003, RECORD VARIABLE ANNUITY | ANNUAL PREMIUM EQUIVALENT | |||||

| DOUBLED TO | SALES OF | SALES OF | |||||

| £73 MILLION | £1.9 BILLION | £555 MILLION | |||||

| UP 16 PER CENT ON 2002 (AT CONSTANT | |||||||

| EXCHANGE RATES) | |||||||

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 | 07 |

BUSINESS REVIEW

KNOWING WHERE THE GROWTH

MARKETS ARE

ASIA

Prudential Corporation Asia (PCA) is the leading European life insurer in Asia with 23 life and fund management operations across 12 countries. PCA continued to strengthen its position as a leader in both the life insurance and mutual fund markets across the region. Based on preliminary estimates, PCA believes that it ended 2003 with top-five market shares in eight Asian life insurance markets, two mutual fund markets and Hong Kong’s Mandatory Provident Fund market.

In 2003, PCA delivered a strong set of results with annual premium equivalent (APE) sales of £555 million, up 16 per cent at constant exchange rates (CER) compared with 2002 and new business achieved profit (NBAP) up one per cent to £291 million at CER. PCA’s modified statutory basis (MSB) profits (before development costs and PCA head office costs) were £98 million, compared with £88 million in 2002.

PCA’s primary business is the manufacture and distribution of life insurance and medium to long-term savings products through agency and third party distribution channels. While agency continues to be the principal distribution channel, PCA has also successfully diversified distribution to include a number of alternative channels including brokers, banks

ASIA

HAS MANY OF THE

FASTEST-GROWING

ECONOMIES IN THE WORLD

and direct marketing. Bancassurance has continued to provide a material source of new business. Across the region, PCA now has a total of 29 bancassurance agreements in 11 countries and these generated 13 per cent of APE sales in 2003. APE from all alternative distribution channels grew by 14 per cent in 2003 and represented 22 per cent of regional APE sales.

PCA’s retail fund management operations continue to build scale with year-end funds under management of £6.6 billion up 26 per cent compared with 2002, driven principally by strong fund inflows in its existing market-leading operations in India and Taiwan and also by good results in its newer operations in Malaysia.

PCA launched its new Beijing life insurance joint venture with its partner CITIC in August. This will enable it to build on its already successful business in Guangzhou, where it has a 14 per cent market share of new business.

Prudential remains exceptionally well positioned to benefit from Asia’s outstanding long-term growth prospects. PCA has a strong track record of successful delivery and a robust business model firmly focused on building businesses in markets and sectors that combine scale opportunities with secure long-term profitability and very attractive returns on capital.

SIGNIFICANT OPPORTUNITIES

IN ASIA DUE TO STRONG

SAVINGS

CULTURE

| 08 | PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 |

UNITED STATES

Over recent years, Jackson National Life (JNL) has successfully grown from a narrow-product, single-channel life insurance company to a multi-product, multi-channel financial services company. Today, JNL offers fixed, equity-indexed and variable annuities, term and permanent life insurance and institutional products, through a number of channels. These include independent broker-dealers, independent agents, banks, regional broker-dealers and the registered investment advisor channel.

During 2003, JNL continued to focus on retail markets consistent with its stated goal of operating on a self-financing basis. Retail sales of £3.6 billion represented its second best year, only 10 per cent lower at CER than the record sales JNL delivered in 2002. This was driven by record sales of variable annuities, which at £1.9 billion were up 55 per cent on 2002 at CER. Total sales for the year were down 23 per cent on 2002 at CER to £4.1 billion due to the lower retail sales together with a reduction in sales of institutional products. Lower institutional sales reflected JNL’s focus on retail markets, and the active management of its capital position during the year. In 2003, 93 per cent of JNL’s sales came from products launched since the beginning of 2002, demonstrating its strength in product design and execution.

NBAP fell 31 per cent at CER reflecting lower APE sales (down 24 per cent) and a lower margin (from 39 per cent in 2002 to 35 per cent in 2003). The MSB operating result of £162 million for US operations was 15 per cent ahead of 2002 at CER.

Distribution in the US is highly fragmented, and JNL’s strategy is to focus on the most profitable channels. JNL has positioned itself with a large base of intermediaries who provide comprehensive financial advice. JNL provides a valuable service offering to its intermediaries to help them increase their productivity in meeting increasingly complex customer needs.

In March 2003, JNL entered the registered investment advisor channel with the launch of Curian Capital LLC, which provides innovative fee-based separately managed accounts and investment products to advisors through a state-of-the-art technology platform. At the year-end, retail funds under management had grown to £148 million (US$266 million), more than five times the funds under management at the half-year.

In the testing market conditions of recent years, JNL has focused on its core strengths: strong administrative capabilities; a low cost base; flexible and innovative product range; and its broad relationship-driven distribution model. In addition, it has actively and successfully managed its capital position and is well placed as markets in the US continue to recover.

70%

OF THE WORLD’S

RETIREMENT ASSETS

ARE IN THE UNITED STATES

40

MILLION

BABY BOOMER HOUSEHOLDS IN AMERICA WILL MOVE INTORETIREMENT IN THE NEXT 20 YEARS

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 | 09 |

BUSINESS REVIEWCONTINUED

30%

OF THE UK POPULATION

IS FORECAST TO BE AGED

60 AND OVER BY 2030

UNITED KINGDOM AND EUROPE

UK and Europe Insurance Operations

In 2003, Prudential UK continued to focus on long-term value creation for shareholders rather than short-term sales growth. It remains focused on high margin products where it has competitive advantage as a result of its scale, brand recognition, financial strength, diversified distribution and low cost base.

Total APE sales in 2003 were £616 million, 21 per cent lower than 2002. This was largely due to the contraction of the with-profits bond market, which according to the Association of British Insurers (ABI) recorded 65 per cent lower sales in 2003 compared with 2002. Prudential leads IFA distribution of with-profit bonds and grew its market share of the independent financial adviser (IFA) market from 25 per cent in the fourth quarter of 2002 to 51 per cent in the fourth quarter of 2003 (source: ABI). NBAP of £166 million was 29 per cent lower than 2002, reflecting lower new business sales and reduced new business margins.

Prudential UK continues to be a market leader in its other chosen product segments including corporate pensions and bulk and individual annuities. In 2003, it had a 48 per cent market share of the group additional voluntary contribution market and a 23 per cent share of the individual annuity market (source: ABI, annuity market share excluding income drawdown and purchased life annuities). It also continues to develop and launch innovative new products, with products launched since the beginning of 2000 accounting for 37 per cent of APE sales in 2003 (excluding DWP rebates). This included developments across all product ranges including the Flexible Lifetime Annuity, the International With-Profit Bond, the Prospect Bond and the Flexible Investment Plan.

‘The Plan from the Pru’ campaign was launched in September 2002, and provides customers with a financial plan to guide them through key financial stages of their lives. It was actively promoted in the press and on television and radio throughout 2003 and contributed to an increased awareness of the Prudential brand during the year.

In 2003, Prudential’s long-term with-profits fund earned an investment return of 16.5 per cent compared with a return of negative 8.1 per cent in 2002. Over the last 10 years, the long-term fund has consistently generated positive returns for investors, demonstrating the benefits of Prudential’s diversified investment policy.

In November 2001, Prudential UK announced a review of operations with a target of reducing annual costs by £175 million to be achieved by the end of 2004. Following the first phase of this work in July 2002 the target was increased to £200 million. This has been achieved in full, 12 months ahead of schedule.

Prudential UK opened a customer service centre in India in May 2003. The centre, which at the end of December employed over 800 people and has handled over 500,000 calls since launch, will be fully operational later this year and is part of Prudential UK’s commitment to improving customer service.

M&G

M&G is Prudential’s UK and European fund management business. It has over £111 billion of funds under management, of which £87 billion relates to Prudential’s long-term business funds. M&G operates in markets where it has a leading position and competitive advantage, including retail fund management, institutional fixed income, pooled life and pension funds, property and private finance. As at 31 December 2003,

| 10 | PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 |

M&G was the third largest retail fund manager in the UK in terms of funds under management (source: IMA) and is one of the largest fund managers in the UK.

M&G’s operating profit including performance-related fees was £83 million in 2003, an increase of £12 million on the previous year, and its underlying profit increased 43 per cent to £70 million. This reflects the strengths of M&G’s diversified revenue streams and disciplined cost management. In 2003, M&G continued to develop new external business lines with attractive margins and over 20 per cent of its underlying profits during the year came from businesses that did not exist five years ago.

M&G recorded gross fund inflows of £3.8 billion in 2003, a slight increase on the previous year. External funds under management, which represent nearly a quarter of M&G’s total funds under management, increased significantly during the year, rising 19 per cent to £24.2 billion due to a combination of net fund inflows from both retail and institutional clients and market gains on existing funds.

Gross fund inflows into M&G’s retail products were £1.2 billion in 2003, a six per cent fall on 2002. Net fund inflows for 2003 were £184 million. M&G continued to benefit from its leading position as a fixed income provider and its revised equity investment process has delivered good performance. M&G also maintained its focused expansion into Germany, Austria and Italy in 2003 with €101 million of assets at the end of 2003.

In its institutional business, M&G continued to build on its position as a leading innovator in fixed income and private finance. Gross fund inflows were £2.6 billion during the year, a six per cent increase on 2002. Net institutional fund inflows were £1.2 billion.

M&G’s property division, which primarily invests on behalf of the Prudential Assurance Company, also enjoyed a successful year. With over £12.5 billion invested in the property market, Prudential Property Investment Managers is the largest institutional property manager in the UK.

Egg

Egg is an innovative financial services company, providing a range of banking and financial services products through its internet site.

In 2003, operating income increased by 30 per cent to £424 million (2002: £327 million). In the UK, Egg more than doubled its operating profit to £73 million and grew its customer base during 2003 by 635,000 to almost 3.2 million. It continues to grow revenues and unsecured lending balances, while at the same time reducing both unit operating costs and marketing acquisition costs.

In France, Egg ended the year with 130,000 customers and 66,000 credit cards in issue and grew unsecured lending balances to £120 million. Egg France recorded a loss of £89 million in 2003. Egg Group’s pre-tax losses increased to £34 million from £20 million in 2002.

| HALF THE UK | WORKFORCE ARE ESTIMATED TO BE UNDER-SAVING FOR THEIR RETIREMENT |

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 | 11 |

FINANCIAL REVIEW

SALES AND FUNDS UNDER MANAGEMENT

Prudential continued to benefit from the strength of its international operations with total new insurance business and investment product sales reaching £31.5 billion, an increase of 11 per cent on 2002 at constant exchange rates (CER). At reported exchange rates, total new business inflows were up five per cent.

Total sales of new insurance and investment products from outside the UK represented 74 per cent of the Group total of £31.5 billion, reflecting the international diversification of the Group.

Total insurance sales were down 21 per cent at CER to £9.5 billion, while sales on the annual premium equivalent (APE) basis were down 12 per cent at CER to £1,589 million compared with last year. At reported exchange rates, total insurance sales were down 24 per cent and APE insurance sales were down 16 per cent.

Insurance and investment funds under management at31 December 2003 totalled £168 billion, compared with £155 billion at the end of 2002 at reported exchange rates (£150 billion at CER).

TOTAL ACHIEVED OPERATING PROFIT

Total achieved operating profit was £794 million, down 27 per cent from 2002 at CER. At reported exchange rates the result was 30 per cent lower.

This result comprised an 18 per cent reduction in new business achieved profit (NBAP) to £605 million at CER and a reduction in the in-force profit, which was down 29 per cent to £351 million at CER. At reported exchange rates, NBAP was down 22 per cent and the in-force profit was down 34 per cent.

NEW BUSINESS ACHIEVED PROFIT

Group NBAP from insurance business of £605 million was 18 per cent below 2002 at CER reflecting lower sales and margins in the UK and the US, partially offset by increased sales in Asia. The average Group NBAP margin fell from 41 per cent in 2002 to 38 per cent. At reported exchange rates, NBAP was down 22 per cent.

![]()

UK and Europe Insurance Operations’ NBAP of £166 million was 29 per cent lower than 2002. This reflected a 21 per cent fall in APE sales, revised economic assumptions and an adverse movement in sales mix resulting from reduced levels of higher-margin with-profit bonds being sold. The new business margin moved from 30 per cent in 2002 to 27 per cent in 2003 and reflects the revised economic assumptions and adverse sales mix relative to 2002.

The 31 per cent fall in Jackson National Life’s (JNL) NBAP to £148 million at CER was due to a 24 per cent reduction in APE sales and a reduction in the new business margin from 39 per cent to 35 per cent. The margin reduction reflects the net change in economic assumptions offset by certain targeted revisions to annuity commissions. At reported exchange rates, JNL’s NBAP was down 37 per cent.

In Asia, NBAP of £291 million was up one per cent at CER reflecting a 16 per cent increase in APE sales at CER offset by a reduction in the new business margin from 60 per cent to 52 per cent in 2003. This fall in margin reflects the net impact of changes in product and country mix combined with a revision to a number of operating and economic assumptions.

![]()

IN-FORCE ACHIEVED PROFIT

The unwind of the discount (including return on surplus assets over target surplus for JNL) in 2003 was £636 million compared with £659 million in 2002, reflecting reductions in the UK and the US offset by an increase in Asia. In the UK, the decline reflects lower shareholders’ funds at the start of the year, partially offset by the increase in the discount rate. In the US, the fall in the unwind of the discount was primarily due to foreign exchange movements. In Asia, the unwind has increased principally due to the higher opening shareholders’ funds.

UK and European Insurance Operations’ in-force profit of £193 million was down 32 per cent on 2002 (after development and re-engineering charges), principally reflecting lower expected returns from business in-force due to the lower opening embedded value and an increase in negative assumption changes and experience variances. Negative assumption changes of £67 million included the £50 million personal pensions persistency assumption

| 12 | PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 |

charge disclosed at the half-year for poor persistency experience on business sold through the closed direct salesforce channel. In addition, a charge for persistency experience variance of £35 million was recorded.

The US in-force profit increased significantly from £17 million in 2002 to £71 million in 2003. This reflects a £55 million reduction in the negative spread variance to negative £17 million and a lower negative charge for changes in assumptions of £21 million in 2003 compared with negative £54 million in 2002. The change in assumptions in 2003 reflects a revision to unit expense factors. Net losses on bonds, including defaults and impairments, are included within the operating result on a five-year averaged basis with a charge in 2003 of £137 million compared with £133 million in 2002. Actual losses in 2003 of £39 million were a significant improvement over the £289 million recorded in 2002.

PCA’s in-force profit (before development expenses) decreased significantly from £209 million in 2002 to £87 million in 2003 largely due to the positive £101 million of assumption changes included in the 2002 result. This assumption change in 2002 primarily related to Singapore and included £59 million relating to sub-divisions of long-term funds and £42 million due to a revision in the death claims rate assumptions. This compares to assumption changes in 2003 of negative £27 million, primarily reflecting expense assumption changes in Japan following the impact of the strategic review conducted during the year.

NON-INSURANCE OPERATIONS

M&G’s profit including performance-related fees (PRF) was £83 million in 2003, an increase of £12 million on the previous year. This reflected a 43 per cent increase in underlying profit to £70 million and was partly offset by a reduction in the PRF from the £22 million achieved in 2002 to £13 million in 2003.

Egg’s UK banking operations continued their profit growth, generating a £73 million operating profit. Egg’s French business recorded an £89 million loss in 2003. Egg’s pre-tax losses increased to £34 million from £20 million in 2003.

National Planning Holdings and PPM America earned profits of £19 million. Curian Capital LLC (Curian) delivered a loss of £22 million, which reflects losses in its investment phase as funds under management continue to grow. JNL anticipates a similar loss for Curian in 2004. Together these businesses delivered a loss of £3 million.

Other net expenditure decreased by £8 million to £181 million.

ACHIEVED PROFITS – RESULT BEFORE TAX

The result before tax and minority interests was a profit of £838 million compared with a loss of £483 million in 2002. The significant increase in profit principally reflects the movement in short-term fluctuations in investment returns. Total short-term fluctuations in investment return were £682 million, with £531 million relating to the UK and £132 million in the US.

Adverse economic assumption changes of £540 million reflect changes in assumptions for future investment returns, discount rate and related items and included £122 million for the UK, £263 million for the US and £155 million for Asia.

MODIFIED STATUTORY BASIS RESULTS – OPERATING PROFIT

Group operating profit on the modified statutory basis (MSB) of £357 million was £72 million lower than 2002 at CER. At reported exchange rates, operating profit was £92 million lower than 2002.

UK and Europe Insurance Operations’ operating profit in 2003 was £256 million, £116 million below the restated 2002 figure. This included a reduction of £90 million from the PAC with-profit fund due to lower annual and terminal bonus rates announced earlier in the year partially offset by higher funds under management and increased claims. The 2002 result has been restated for a £17 million positive adjustment (2003: £10 million) in respect of the financing element of certain reinsurance contracts.

The US Operations’ result of £162 million was 15 per cent ahead of 2002 at CER. At reported exchange rates, the 2003 result was six per cent ahead of 2002. The increase primarily reflects lower amortisation of deferred acquisition costs (DAC) for variable annuity products, and higher fee and other income, offset by higher market value adjustment payments, higher average bond losses and the loss on Curian.

PCA’s operating profit before development expenses of £27 million was £98 million compared with £88 million in 2002. At CER, operating profit was £17 million up on the prior year. PCA’s three longest established operations in Singapore, Hong Kong and Malaysia saw their combined MSB profit increase by 16 per cent to £91 million. This was offset by expected losses at a number of PCA’s newer operations such as Japan and South Korea as they continued to build scale and fund new business strain.

MODIFIED STATUTORY BASIS RESULTS – PROFIT BEFORE TAX

MSB profit before tax and minority interests was £350 million in 2003, compared with £501 million in 2002. The 2002 result included £355 million relating to the disposal of the UK General Insurance operations. The 2003 result was offset by an improvement in the adjustment for short-term fluctuations in investment returns from a negative adjustment of £205 million in 2002 to a positive adjustment of £91 million in 2003.

Within the improvement in the adjustment for short-term fluctuations, the US result has improved from a loss of £258 million in 2002 to a gain of £93 million in 2003. The short-term fluctuations in Asia principally reflect the five-year averaging impact of an appreciation in bond values.

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 | 13 |

FINANCIAL REVIEWCONTINUED

EARNINGS PER SHARE

Earnings per share based on achieved basis operating profit after tax and related minority interests but before amortisation of goodwill, were down 16.4 pence to 26.4 pence. Earnings per share based on MSB operating profit after tax and related minority interests but before amortisation of goodwill, were down 3.8 pence to 12.9 pence.

Basic earnings per share, based on achieved basis profit for the year after minority interests were 24.3 pence compared with a loss of 7.3 pence in 2002. Basic earnings per share, based on MSB profit for the year after minority interests were down 13.1 pence to 10.4 pence.

DIVIDEND PER SHARE

The final dividend per share is 10.7 pence, resulting in a full-year dividend of 16.0 pence, compared with a full-year dividend for 2002 of 26.0 pence.

CASH FLOW

The Group received £586 million in cash remittances from business units in 2003 (2002: £536 million) comprising the shareholders’ statutory life fund transfer of £286 million relating to earlier bonus declarations, together with dividends and interest from subsidiaries of £300 million. The shareholder transfer in 2004 representing 2003’s profits from the PAC with-profits fund, is expected to be approximately £80 million lower than in 2003. Dividends and interest received include £84 million from M&G, £48 million from each of PCA and JNL and £120 million from UK Insurance Operations, including £100 million of special dividends from the PAC shareholders’ funds in respect of profits arising from earlier business disposals. A similar amount will also be distributed from PAC shareholders’ funds in 2004 and 2005. After dividends and interest paid, there was a net inflow of £12 million (2002: £97 million net outflow).

| CASH FLOW | ||||

| 2003 | 2002 | |||

| £m | £m | |||

| UK life fund transfer* | 286 | 324 | ||

| Cash remitted by business units | 300 | 212 | ||

| Total cash remitted to group | 586 | 536 | ||

| Interest | (127 | ) | (124 | ) |

| Dividends | (447 | ) | (509 | ) |

| Cash remittances after interest and dividends | 12 | (97 | ) | |

| Tax received | 77 | 59 | ||

| Equity (scrip dividends and share options) | 30 | 40 | ||

| Corporate activities | 58 | 543 | ||

| Cash flow before investment in businesses | 177 | 545 | ||

| Capital invested in business units: | ||||

| Asia | (145 | ) | (158 | ) |

| JNL | – | (321 | ) | |

| Other | (28 | ) | (196 | ) |

| Increase (decrease) in cash | 4 | (130 | ) | |

| * In respect of prior year bonus declarations |

The Group also received £58 million from corporate activities (2002: £543 million). In 2002, this included cash proceeds arising from the sale of the General Insurance business and exceptional tax receipts. Together with the proceeds of equity issuance and Group relief, this gave rise to a total net surplus of £177 million (2002: £545 million).

During 2003, the Group invested £173 million (2002: £675 million) in its business units, including £145 million in Asia. Prudential expects to invest approximately the same amount in each of 2004 and 2005. Based on current business plans, Prudential expects PCA to be a net capital provider to the Group in 2006. In 2002, JNL received £321 million (2003: nil) to support high volumes of fixed annuity business, additional guaranteed minimum death benefits (GMDB) reserves and to replace capital consumed by bond losses and impairments. However, in 2003 due to significant improvements in the credit cycle, JNL returned to its normal self-funding operating model.

In aggregate this gave rise to an increase in cash of £4 million (2002: reduction of £130 million).

BORROWING

Prudential plc enjoys strong debt ratings from both Standard & Poor’s and Moody’s. Prudential long-term senior debt is rated AA- (negative outlook) and A2 (stable outlook) from Standard & Poor’s and Moody’s respectively, while short-term ratings are A1+ and P-1.

During 2003, Prudential issued US$1 billion of perpetual subordinated capital with a coupon of 6.5 per cent to optimise its balance sheet structure and financial flexibility. The proceeds of the issue were used to refinance existing senior debt, primarily commercial paper.

FINANCIAL STRENGTH OF INSURANCE OPERATIONS

United Kingdom

A common measure of financial strength in the UK for long-term insurance business is the free asset ratio. The free asset ratio is the ratio of assets less liabilities to liabilities, and is expressed as a percentage of liabilities. On a comparable basis with 2002, the free asset (or Form 9) ratio of the Prudential Assurance Company (PAC) long-term fund was approximately 10.5 per cent at the end of 2003, compared with 8.4 per cent at 31 December 2002. The valuation has been prepared on a conservative basis in accordance with the current Financial Services Authority (FSA) valuation rules, and without the use of implicit items.

The fund is very strong with an inherited estate measured on an essentially deterministic valuation basis of more than £6 billion compared with approximately £5 billion at the end of 2002. On a realistic basis, with liabilities recorded on a market consistent basis calculated using the approach set out in the Association of British Insurers (ABI) guidance for reporting at the 2003 year-end the free assets are valued at around £5 billion before a deduction for the risk capital margin. The approach to realistic reporting adopted may change pending confirmation of the FSA regulations and guidelines.

| 14 | PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 |

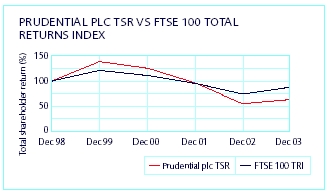

The investment return on the Prudential main with-profits fund was 16.5 per cent in the year to 31 December 2003 compared with the rise in the FTSE 100 (Total Return) Index of 17.9 per cent over the same period. Over the last 10 years, the with-profits fund has consistently generated positive fund returns with three, five and 10 year compound returns of 1.1 per cent per annum, 4.9 per cent per annum and 8.6 per cent per annum respectively. These returns demonstrate the benefits of the fund’s strategic asset allocation and long-term out-performance.

United States

The capital adequacy position of Jackson National Life remains strong, with a strong risk-based capital ratio more than 3.5 times the NAIC Company Action Level Risk Based Capital. As a core business to the Group, JNL’s financial strength is rated AA by Standard & Poor’s.

Asia

Solvency margins have been maintained at levels at or above local regulatory requirements by the insurance operations in Asia.

INHERITED ESTATE

The long-term fund contains the amount that the Company expects to pay out to meet its obligations to existing policyholders and an additional amount used as working capital. The amount payable over time to policyholders from the With-Profits Sub-Fund is equal to the policyholders’ accumulated asset shares plus any additional payments that may be required by way of smoothing or to meet guarantees. The balance of the assets of the With-Profits Sub-Fund is called the ‘inherited estate’ and represents the major part of the working capital of Prudential’s long-term fund which enables the Company to support with-profits business by:

| • | providing the benefits associated with smoothing and guarantees; |

| • | providing investment flexibility for the fund’s assets; |

| • | meeting the regulatory capital requirements, which demonstrate solvency; |

| • | absorbing the costs of significant events or fundamental changes in its long-term business without affecting bonus and investment policies. |

The Company believes that it would be beneficial if there were greater clarity as to the status of the inherited estate and therefore it has discussed with the Financial Services Authority (FSA) the principles that would apply to any re-attribution of the inherited estate. No conclusions have been reached. Furthermore, the Company expects that the entire inherited estate will need to be retained within the long-term fund for the foreseeable future to provide working capital and so it has not considered any distribution of the inherited estate to policyholders and shareholders.

SHAREHOLDERS’ FUNDS

On the achieved profits basis, which recognises the shareholders’ interest in long-term businesses, shareholders’ funds at 31 December 2003 were £7.0 billion, a decrease of £153 million from 31 December 2002.

GOING CONCERN

After making appropriate enquiries, the directors consider that the Group has adequate resources to continue its operations for the foreseeable future. They therefore continue to use the going concern basis in preparing the financial statements.

![]()

PHILIP BROADLEY

GROUP FINANCE DIRECTOR

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 | 15 |

| CORPORATE RESPONSIBILITY REVIEW | ||||

KEY CHALLENGES • Changing Demographics and Consumer Choice. Around the world, populations are ageing as people are living longer and birth rates decline. While living longer is good news for many, it creates a fresh set of challenges for societies. Financial service providers have a key role in providing solutions. The challenge is to develop products and services that respond to our customers’ needs today and tomorrow; • Consumer Confidence. Consumer confidence in savings has been affected by poorly performing equity markets and expectations of lower nominal investment returns, as well as a range of issues concerning the performance and capital of a number of insurance companies in the UK. Building trust among consumers and giving them the confidence to buy the products they will increasingly need | means developing a sustainable business through responsible marketing, quality customer service, education, providing realistic returns and clearing away jargon; • Globalisation. As a leading international financial services provider we recognise the complex issues that result from corporations extending their facilities overseas. No international business can ignore the opportunities for growth and efficiencies that a global market presents, but our choices instantly affect people around the world. Socially acceptable business growth, based on internationally accepted standards of conduct, is key to how we operate; • Sustainable Development. Our natural resources are not limitless and it is essential that firms manage their environmental impacts efficiently. But sustainable development is about more than reducing the consumption of raw materials and limiting waste emissions. It also means ensuring human rights, treating staff and suppliers fairly and educating consumers. CORPORATE RESPONSIBILITY MEANS INTEGRITY |

INITIATIVES COMMITTED STAFF ARE THE BEST INVESTMENT In 2003 we were accredited as an Investor In People (IIP) for our operations in the UK and in India. IIP is the UK national standard that sets out levels of good practice for the training and development of staff to achieve business goals. We are one of the first companies to receive accreditation for multiple work sites which also includes our offshore office in Mumbai, India. DIVERSITY All employees and applicants for roles across the Group are given equal opportunity in all aspects of employment. This principle is embedded in policies and management practices. PCA Life Japan sponsored the first Women in Japan Forum under the theme Balancing Work and Lifestyle. The three hour event attracted over 100 working women with very positive feedback. PRESERVING NATURAL HABITATS The grounds surrounding Jackson National Life’s headquarters in Lansing, Michigan, have been designed to simulate the natural environment. When the building was constructed in 2000, all wetlands around the building were protected and still remain intact. These areas provide habitat for geese, cranes, deer, and other types of wildlife. Although the original site lacked trees and foliage, Jackson National Life has planted approximately 400 new trees around the site to enhance the environment. | ||||

| 16 | PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 | |||

standards of responsible business conduct. Our policies, programmes and management systems support this approach and ensure that we understand and respond to material social, ethical and environmental risks and opportunities. A detailed report on our performance is given in our on-line corporate responsibility report at www.prudential.co.uk/cr and a summary of this is also available in hard copy from our corporate responsibility unit. The standards we strive to achieve rightly go beyond our legal and regulatory obligations. We see responsible corporate behaviour as essential to maintaining successful relationships with, among others: our customers, who make our business viable; our employees, upon whose talent and commitment we depend; and local communities, from whom we recruit and to whom we market our products and services. We believe this approach is central to maintaining and building trust in our brand and business over the long term. ACTING RESPONSIBLY IS GOOD FOR BUSINESS | business and to demonstrate how they are responding to these. We believe that economic factors will remain the fundamental basis of consumer choice in future years. However, we also recognise the growing body of research pointing to the fact that a company's intangible assets – its corporate standards and its social and environmental performance – are becoming increasingly significant differentiators. Consumers will increasingly support those organisations that exhibit and define values around trust, ethics and environmental responsibility. WHY FOCUS ON FINANCIAL LITERACY? | |||

| ACTING RESPONSIBLY BUILDS TRUST | CLEARING AWAY THE JARGON | |||

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 | 157 | |

CORPORATE RESPONSIBILITY REVIEWCONTINUED

INFORMED

DECISIONS

| BENEFIT | ||

| EVERYONE | MANAGING OUR RESPONSIBILITIES MANAGEMENT AND POLICY MARKETPLACE/CUSTOMERS M&G is also concerned with simplifying terminology and has produced a series of ‘spin free guides’ designed to explain financial products in a straightforward manner. MeetPRU is an opportunity for our customers in the UK to meet Prudential face to face. Members of the UK Executive host regular regional seminars where customers can ask questions and get direct feedback. Senior technical advisers | |

| 18 | PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 |

are also on hand to answer individual product-related queries. Events have already been held in Belfast, Cardiff, Edinburgh, Newcastle, Norwich and Reading.

Since 2002, Prudential Property Investment Managers Limited (PruPIM) have been involved with Kingston University in a major industry research project to:

| • | establish the sustainable characteristics of individual properties; |

| • | identify how these should be evaluated in investment appraisals; |

| • | ascertain how to measure the performance of a wide range of properties and portfolios with varying levels of sustainable characteristics. |

PruPIM is the leading private sector sponsor in this sustainable property investment project. Through this relationship we are also supporting the Kingston University team and others in bidding for further UK Government funding for socially responsible investment related projects. These include an initiative to educate property investors about environmental issues and an initiative to develop methods of measuring the environmental performance of buildings.

WORKPLACE/EMPLOYEES

Ensuring that our employees enjoy a safe and healthy working environment is of great importance to Prudential. Our key objectives are to maintain a framework which allows us to meet all our legal obligations and to prevent incidents of work-related accidents and ill health. Our safety management system sets out our policies, assigns key responsibilities and performance standards to ensure the health and safety of our people, visitors and contractors.

Jackson National Life (JNL) provides a subsidised child development centre for the young children of JNL employees. The centre provides more than just childcare. JNL places a high priority on education for both its associates and their children at all age levels and the emphasis is on education and structured development programmes. Another unique aspect is that the subsidy available for parents is based on family income, with a greater discount for those on lower income.

Employee education is provided across our Asian markets through PRUuniversity, which is available to all staff and is offered in 12 languages. Programmes are centrally credited and many are endorsed by external learning institutions. The courses cover management and leadership, technical and business skills as well as a comprehensive range of self-improvement material including language courses.

COMMUNITY/SOCIETY

Our ‘Plan for Life Learning' consumer education programme is testing a variety of financial education approaches in partnership with major charities and is also informing good practice and public policy development via research and seminar activity. We have established a three-year partnership

programme with Citizens Advice called ‘Financial Skills for Life’. This funds nine bureaux to test new models of delivering face to face financial education, as well as supports and co-ordinates existing work in this area undertaken by 65 other bureaux.

In Poland we have established the Przezornosc Charitable Foundation, in recognition of former Prudential policyholders and their heirs, who lost contact with the Company as a consequence of World War II and have been unable to claim on their life policies. The charities selected to receive funding via the Foundation cover welfare, cultural, historical and educational issues. The Foundation, established in 2003, will run for five years.

ENVIRONMENT/SUSTAINABLE DEVELOPMENT

The Belfry Shopping Centre at Redhill in the UK – part of PruPIM’s property portfolio – in 2003 became one of the first shopping centres in the UK to switch to receiving all its electricity from renewable sources, saving 600 tonnes of CO2 every year. The Belfry was also the first shopping centre in the UK to achieve ISO 14001, the internationally recognised standard for environmental management, in 2000.

In India, one of our most rapidly expanding markets and where we have had a long-standing presence, approximately 60 million children aged 6 to 14 are not in school. We are helping to tackle this issue through our support of the Commonwealth Education Fund (CEF), which acts as a catalyst to emphasise the importance of universal primary education. We are specifically supporting work to build national coalitions on education, deliver training for parents on education spending and increase access for marginalised children who are excluded from school. The CEF operates in 17 Commonwealth countries in Asia and Africa. This programme is managed through Action Aid, Save the Children and Oxfam.

WORKING WITH STAKEHOLDERS

We consult regularly with our key stakeholders – such as our customers, our employees and local communities. We are also involved in a growing number of partnerships with national and international bodies in order to contribute to debate on key policy issues:

| • | we are sponsoring a major international research study being undertaken by the Organisation for Economic Co-operation and Development (OECD) to identify levels of financial literacy and education in OECD and selected non-OECD Asian markets and to develop guidelines on effective financial literacy strategies; |

| • | in the UK we have partnered with the Scottish Council Foundation to identify a way forward for improved financial education in Scotland; |

| • | during 2003 PruPIM joined the Institutional Investors Group on Climate Change; and |

| • | we are members of the United Nations Environment Programme. |

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 | 19 |

BOARD OF DIRECTORS

1. SIR DAVID CLEMENTI Chairman (Age 55)

Chairman since 1 December 2002. In July 2003 he was appointed by the Secretary of State for Constitutional Affairs to carry out a review of the regulation of legal services in England and Wales. In February 2003 he joined the Financial Reporting Council. He is also a non-executive director of Rio Tinto plc which he joined in February 2003. From September 1997 to August 2002 he was Deputy Governor of the Bank of England. During this time he served as a member of the Monetary Policy Committee and as a non-executive director of the Financial Services Authority. From 1975 to 1997 he worked for the Kleinwort Benson Group, latterly as Chief Executive.

2. JONATHAN BLOOMER FCA (Age 49)

Group Chief Executive. Appointed as a director in January 1995 and as Group Chief Executive in March 2000. He was previously Deputy Group Chief Executive and Group Finance Director. He is a non-executive director of Egg plc. He is also Chairman of the Practitioner Panel of the Financial Services Authority and a Board Member of the Association of British Insurers.

3. PHILIP BROADLEY FCA (Age 43)

Group Finance Director. Appointed in May 2000. Previously he was with the UK firm of Arthur Andersen where he became a partner in 1993. He specialised in providing services to clients in the financial services industry, including regulators and government agencies in the UK and the US.

4. CLARK MANNING (Age 45)

Executive director. Appointed in January 2002. He is also President and Chief Executive Officer of Jackson National Life. He was previously Chief Operating Officer, Senior Vice President and Chief Actuary of Jackson National Life, which he joined in 1995. Prior to that he was Senior Vice President and Chief Actuary for SunAmerica Inc, and prior to that Consulting Actuary at Milliman & Robertson Inc. He is a Fellow of the Society of Actuaries and a Member of the American Academy of Actuaries.

5. MICHAEL McLINTOCK (Age 42)

Executive director. Appointed in September 2000. He is also Chief Executive of M&G, a position he held at the time of M&G’s acquisition by Prudential in March 1999. He joined M&G in October 1992. He is also a non-executive director of Close Brothers Group plc and CoFunds Holdings Limited.

6. MARK NORBOM (Age 46)

Executive director. Appointed in January 2004. He is also Chief Executive, Prudential Corporation Asia. He was previously President and Chief Executive Officer of General Electric Japan, and a Company Officer of General Electric Company. He has spent the last 10 years with General Electric in Taiwan, Indonesia, Thailand and Japan. Prior to that, his career was with General Electric in various posts in the US.

7. MARK WOOD (Age 50)

Executive director. Appointed in June 2001. He is also Chief Executive of Prudential Assurance, UK and Europe. In May 2002 he became a member of the Life Insurance Committee of the Association of British Insurers. He was previously Chief Executive of Axa UK plc (formerly Sun Life & Provincial Holdings plc) and Axa Equity and Law plc, and Managing Director of AA Insurance.

8. BART BECHT (Age 47)

Independent non-executive director. Appointed in May 2002. He is Chief Executive of Reckitt Benckiser plc. He joined Benckiser N.V. in 1988 and was appointed Chief Executive in 1995. Benckiser N.V. and Reckitt & Colman plc merged in December 1999. Previously he served in various functions in Procter & Gamble.

9. BRIDGET MACASKILL (Age 55)

Independent non-executive director. Appointed in September 2003. She rejoined the Board of Prudential plc having previously resigned due to a potential conflict of interest in March 2001. She is a non-executive director of J Sainsbury plc. She was previously Chairman and Chief Executive Officer of OppenheimerFunds Inc, a major New York based investment management company.

10. ROBERTO MENDOZA (Age 58)

Independent non-executive director and Chairman of the Remuneration Committee. Appointed in May 2000. He is the non-executive Chairman of Egg plc. He is also a non-executive director of Reuters Group PLC and The BOC Group plc. He is a founder member of Integrated Finance Limited and a member of the World Bank-IFC Bank Advisory Group. He was previously Vice Chairman and director of JP Morgan & Co, Inc., and a managing director of Goldman Sachs.

11. KATHLEEN O'DONOVAN (Age 46)

Independent non-executive director. Appointed in May 2003. She is a non-executive director of EMI Group plc and Great Portland Estates PLC. She is also a non-executive director of the Court of the Bank of England. She was previously Finance Director at BTR and Invensys. Prior to that she was a partner at Ernst & Young.

12. ROB ROWLEY (Age 54)

Senior independent non-executive director and Chairman of the Audit Committee. Appointed in July 1999. He is executive Deputy Chairman of Cable & Wireless Public Limited Company, and a non-executive director of Taylor Nelson Sofres plc. He retired as a director of Reuters Group PLC in December 2001, where he was Finance Director from 1990 to 2000.

13. SANDY STEWART (Age 70)

Independent non-executive director. Appointed in October 1997. He is Chairman of Murray Extra Return Investment Trust plc. He is also Chairman of the Scottish Amicable (supervisory) Board, which is a special committee of the Board of The Prudential Assurance Company Limited. He was previously a practising solicitor and Chairman of Scottish Amicable Life Assurance Society.

Ages as at 19 March 2004.

| 20 | PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 |

SUMMARY CORPORATE GOVERNANCE REPORT

The directors are committed to high standards of corporate governance and support the Combined Code on Corporate Governance issued in 1998 and appended to the Listing Rules of the Financial Services Authority (the Code). The Company has complied throughout the financial year ended 31 December 2003 with all the Code provisions set out in Section 1 of the Code save for the appointment of a senior independent director for the whole of the year under review. As set out below, an appointment to this role was made on 4 December 2003. The 2003 Annual Report contains our full corporate governance statement.

THE BOARD

As at 31 December 2003, the Board comprised the Chairman, five executive directors and seven independent non-executive directors. Following recent changes, there are currently six executive directors and six non-executive directors. These non-executive directors bring a wide range of business, financial and global experience to the Board. Biographical details of the current Board members appear on page 20. The roles of Chairman and Group Chief Executive are separate and clearly defined, so that no individual has unfettered powers of decision. The Chairman is responsible for the leadership and governance of the Board as a whole and the Group Chief Executive for the management of the Group, the implementation of Board strategy and policy on the Board’s behalf. In discharging his responsibility, the Group Chief Executive is advised and assisted by the Group Executive Committee, comprising all the business unit heads and a Group head office team of functional specialists. On 4 December 2003 Rob Rowley was appointed as the Company’s Senior Independent Director.

During 2003 the Board met 10 times and held a separate strategy day. In addition there were a further 12 Board Committee meetings. The Board’s terms of reference set out those matters specifically reserved to it for decision, in order to ensure that it exercises control over the Group’s affairs.

A corporate governance framework has been approved by the Board which maps out the internal approvals processes and those matters which are delegated to business units.

Non-executive directors are appointed initially for a three-year term. The appointment is then reviewed towards the end of this period.

BOARD COMMITTEES

The Board has established the following standing committees:

Audit Committee

Rob Rowley (Chairman)

Bart Becht (until 8 May 2003)

Ann Burdus (until 31 December 2003)

Kathleen O’Donovan (from 8 May 2003)

Sandy Stewart

The Audit Committee normally meets six times a year and assists the Board in meeting its responsibilities under the Code for an effective system of financial reporting, internal control and risk management. It provides a direct channel of communication between the external and internal auditors and the Board, and assists the Board in assessing that the external audit is conducted in a thorough, objective and cost-effective manner. It also reviews the Internal Audit annual work plan.

The terms of reference of the Audit Committee include reviewing with the management of the Company and the external auditors the performance of the external auditors and the extent of non-audit services; and the value for money obtained from auditors’ fees for both statutory audit work and non-audit work. The terms of reference were amended in February 2003 to ensure they comply with the provisions of the US Sarbanes-Oxley Act of 2002, which affect UK companies with a dual listing in the US, and the proposed guidance in Sir Robert Smith’s report ‘Audit Committees – Combined Code Guidance’, published in January 2003 and incorporated into the revised Combined Code issued in July 2003.

Remuneration Committee

Roberto Mendoza (Chairman)

Sir David Barnes (until 8 May 2003)

Bart Becht

Ann Burdus (until 31 December 2003)

Bridget Macaskill (from 1 September 2003)

Kathleen O’Donovan (from 8 May 2003)

Rob Rowley

Sandy Stewart

The Remuneration Committee normally has scheduled meetings at least twice a year and a number of ad hoc meetings, as required, to review remuneration policy and determine the remuneration packages of the Chairman and executive directors. In framing its remuneration policy, the Committee has given full consideration to the provisions of Section 1B of and Schedules A and B to the Code. The Summary Remuneration Report prepared by the Board is set out on pages 22 and 23. In preparing the Report, the Board has followed the provisions of Schedule B to the Code and The Directors’ Remuneration Report Regulations 2002.

Nomination Committee

Sir David Clementi (Chairman)

Sir David Barnes (until 8 May 2003)

Jonathan Bloomer (from 6 November 2003)

Ann Burdus (until 31 December 2003)

Bridget Macaskill (from 18 March 2004)

Rob Rowley

Sandy Stewart

The Nomination Committee, which is comprised of a majority of independent non-executive directors, meets as required to consider candidates for appointment to the Board and to make recommendations to the Board in respect of those candidates. In doing so, it evaluates the balance of skills, knowledge and experience on the Board and makes recommendations regarding appointments based on merit and against objective criteria, and the requirements of the Company’s business. In appropriate cases, search consultants are used to identify suitable candidates.

Board Committees – Terms of Reference

The full terms of reference of the Audit, Remuneration and Nomination Committees are available on the Company’s website at www.prudential.co.uk under the section headed ‘About Prudential’.

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2003 | 21 |

SUMMARY REMUNERATION REPORT

FOR YEAR ENDED 31 DECEMBER 2003

This report summarises information about the remuneration of the Company’s directors. The full Directors’ Remuneration Report contains further explanations about our policies and arrangements and is available in our Annual Report and on our website. It has been approved by the Board and complies with The Directors’ Remuneration Report Regulations 2002.

THE REMUNERATION COMMITTEE

The terms of reference of the Remuneration Committee are available on the Company’s website. A copy can also be obtained by contacting the Secretary to the Remuneration Committee, Group Secretarial Department. Members of the Remuneration Committee during 2003 are listed in the Summary Corporate Governance Report.

REMUNERATION POLICY

The aim of the Company’s remuneration policy is to be able to recruit and retain the highest calibre executives. To achieve this objective, Prudential must continue to use remuneration practices relevant to the different markets in which the Company does business around the world. The Remuneration Committee considers remuneration within the context of the UK’s regulatory framework and shareholder views, and is guided by UK corporate governance standards.

Remuneration policy for executive directors

The Remuneration Committee recognises that a successful remuneration policy needs to be sufficiently flexible to take account of changes in the Company’s business environment. The Committee will keep the policy under review, consulting with major shareholders over any proposed changes. Any changes to the policy will be described in future Remuneration Reports.

Key principles of the remuneration policy

The principles developed by the Remuneration Committee reflect the relative importance of those elements that are performance-related and those which are fixed and are as follows:

| • | a high proportion of total remuneration will be delivered through performance-related reward; |

| • | a significant element of performance-related reward will be provided in the form of shares; |

| • | the total remuneration package for each director will be set against the relevant employment market; |

| • | performance measures will include both absolute financial measures and comparative measures as appropriate to provide a clear alignment between the creation of shareholder value and reward; |

| • | performance will be rewarded at both a regional and Group level. |

Elements of the remuneration package

Executive directors are provided with basic salary, annual bonuses and long-term incentive arrangements that are tailored to their respective roles and employment markets. These elements are normally reviewed each year. Salary reviews take account of business results, individual accountabilities and performance, as well as market conditions. Annual bonus arrangements depend on Company and individual performance, while the long-term arrangements depend on Group and, where relevant, business unit performance, with a portion being share-based. All current executive directors have contracts that require the Company to provide one-year’s notice. Non-executive directors do not have service contracts; they receive fees, are not eligible for any incentive plans and are not members of any company pension scheme.

| Directors’ Remuneration for 2003 | Total | Total | ||||||||

| Salary/Fees | Bonus | Benefits | 2003 | 2002 | ||||||

| £000 | £000 | £000 | £000 | £000 | ||||||

| Chairman | ||||||||||

| Sir David Clementi (appointed 1 December 2002) | 420 | – | 24 | 444 | 37 | |||||

| Executive directors* | ||||||||||