Exhibit 99.2

| A world of opportunity | ||

| Annual Review and Summary Financial Statement 2004 | ||

![]()

| A WORLD OF OPPORTUNITY | ||

| Prudential plc is an international financial services company, which aims to help people enhance and protect their own and their dependants’ financial well-being by providing them with appropriate savings and protection products. | ||

| We have strong positions in three of the largest and most attractive markets in the world, where rising global wealth and changing demographics are fuelling demand for long-term savings. | ||

| Our strategy is to build sustainable, profitable businesses in each of these markets, and thereby maximise returns to our shareholders over time. | ||

| Contents | ||

| 1 Group Financial Highlights 2 Chairman’s Statement 4 Group Chief Executive’s Review 6 Our Brands 8 Strategic Review 14 Financial Review 22 Corporate Responsibility Review 24 Board of Directors 26 Summary Corporate Governance Report 28 Summary Remuneration Report 30 Summary Directors’ Report 30 Summary Financial Statement 31 Independent Auditor’s Statements 32 Achieved Profits Basis – Summary Results and Balance Sheet 33 Achieved Profits Basis – Operating Profit Before Amortisation of Goodwill 34 Insurance and Investment Products New Business 36 Statutory Basis – Summary Consolidated Profit and Loss Account 38 Statutory Basis – Operating Profit Before Amortisation of Goodwill 38 Analysis of Borrowings 39 Statutory Basis – Summary Consolidated Balance Sheet 40 Basis of Financial Reporting 40 How to Contact Us IBC Shareholder Information | ||

| This summary financial statement is only a summary of the information contained in the Group’s 2004 full Annual Report and does not contain sufficient information to allow as full an understanding of the results of the Group and state of affairs of the Company or of the Group as is provided by the Group’s 2004 full Annual Report. Any shareholder or debenture holder has the right to obtain, free of charge, a copy of the Group’s 2004 full Annual Report and/or future Annual Reports by contacting Lloyds TSB Registrars or the Company Secretary in writing. Copies can also be obtained via the Company’s website at www.prudential.co.uk | ||

GROUP FINANCIAL

HIGHLIGHTS

It’s about... our results

|  | |

|  | |

|  |

*Annual premium equivalent (insurance sales only).

†Operating profit and operating earnings per share exclude amortisation of goodwill and exceptional items. This basis of presentation has been adopted consistently throughout this Annual Review and Summary Financial Statement.

^Comparative figures have been restated to take account of the Rights Issue in 2004.

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 | 01 |

| CHAIRMAN’S STATEMENT | A WORLD OF OPPORTUNITY | |

It’s about…

capitalising on our

After several years of difficult market conditions in the UK and the US, 2004 was a year in which we began to see signs of recovery. In Asia, the economies in which we operate continued to grow, and rising wealth and market liberalisation fuelled interest in savings and investment products.

Across the world we saw a continuation of the growing awareness of the impact that shifting demographics will have on people’s lives, and the central role that insurers can play in helping to address the global savings gap and secure the financial well-being of those who are living longer. Against this backdrop, we continued to pursue opportunities for sustainable, profitable growth in each of our chosen markets, and we ended the year in a stronger position than we have enjoyed for some time.

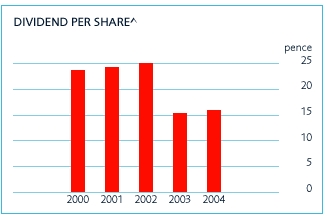

For the year to 31 December 2004, total insurance sales rose 26 per cent to £1,846 million*; operating profit on an achieved profits basis increased 39 per cent to £1,124 million; operating profit under the modified statutory basis increased 49 per cent to £603 million; and the full year dividend per share has been increased by three per cent to 15.84 pence per share**.

Shareholders’ funds on an achieved profits basis rose by 27 per cent to £8.6 billion, an increase which reflects the proceeds of our

Rights Issue announced in October and the growth in the value of our long-term business.

In the UK we have transformed our insurance business over the last three years, and now have a robust, multi-channel operation, which is increasingly writing shareholder-backed business. Growth in this business over the medium term will be funded from the proceeds of the Rights Issue. Jackson National Life and M&G are already delivering strong profits and funding their own growth from internal revenues. Our Asian business continues to grow and is on track to become cash positive from 2006.

Egg closed its loss-making French arm during 2004 and is now focused on delivering value from its profitable UK operations. We were disappointed that we were unable to sell Egg during the year but, although we do not see it as a long-term core business, we are determined to ensure that it is managed to protect and build the value of our investment.

Looking to the future, we see many opportunities for growth in each of our core markets. As governments and individuals seek to address the combined challenge of rising life expectancy and inadequate retirement funding, we believe they will look increasingly to the private sector to fulfil their needs. By sharing

| We see many opportunities for growth in each of our core markets | ||||

| 02 | PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 |

| ||

| ||

| SIR DAVID CLEMENTI CHAIRMAN | ||

opportunities

around the world

knowledge between Prudential’s businesses we can adapt and export products across borders, meeting emerging needs often more quickly and efficiently than competitors. Our operational plans, in areas such as product design and IT product processing, are increasingly developed on an international, rather than a local, basis.

A sustainable business also requires commitment to the communities in which it operates; and Prudential believes that financial education must be a fundamental part of any forward-looking financial services company’s approach. This is the thinking behind the financial education programme that we have developed over the past four years, more details of which are given in the Corporate Responsibility section of this Review. This programme is an integral part of our strategy to build trusting, long-term relationships with consumers.

During the year it was my pleasure to welcome to the Board two new non-executives: James Ross who joined us in May and Michael Garrett who joined in September. In December we announced that Keki Dadiseth would be joining us from 1 April 2005. All three have substantial experience of operating in overseas markets and will significantly increase the international strength of the Board.

Two directors left the Board in 2004: Sandy Stewart in May and Bart Becht in August; and I would like to thank them both for their contribution.

Shortly before publication of this Review, we also announced that Jonathan Bloomer will step down at the close of the Annual General Meeting. He will be replaced as Group Chief Executive by Mark Tucker. I would like to thank Jonathan for his significant contribution over the last 10 years, first as Group Finance Director and then as Group Chief Executive. He has brought Prudential through one of the severest markets the insurance sector has experienced and has overseen significant changes in our operations which have contributed to the very good results delivered in 2004. We wish him well for the future.

Mark Tucker previously worked for Prudential from 1986 to 2003. He was an Executive Director of Prudential from 1999 to 2003 and Chief Executive of Prudential Corporation Asia from 1993 to 2003. His background and experience mean that he is well suited to lead Prudential to the next stage in the Group’s development.

While the prospects for the future are encouraging, we will continue to rely on our experienced and talented people around the world to capitalise on them; and I would like to thank our staff for their hard work and commitment to the Group over the past year.

*All year-on-year comparisons of financial performance are at constant exchange rates (CER), unless otherwise stated.

**Adjusted for the Rights Issue in 2004.

| +3% | ||

| FULL YEAR DIVIDEND PER SHARE UP BY THREE PER CENT TO 15.84 PENCE** | ||

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 | 03 |

| GROUP CHIEF EXECUTIVE’S REVIEW | A WORLD OF OPPORTUNITY | |

It’s about…

profitable growth

In 2004, each of our regional businesses delivered double-digit growth in sales and profits. As a result, we achieved record Group insurance annual premium equivalent (APE) sales, and a 23 per cent increase in new business achieved profit compared with 2003*.

We achieved these results by adopting a disciplined approach to investment and growth, allocating capital to those businesses that deliver sustainable high returns. At the same time, we managed our risks by maintaining a diversified portfolio of businesses across our chosen markets, principally in the UK, the US and Asia, including several mature cash generators, as well as attractive newer businesses which require investment.

Going forward, we see excellent growth opportunities across the Group.

UNITED KINGDOM

The UK insurance market is starting to recover from three years of decline. During this period, we transformed our UK insurance business from a direct-sales operation, selling with-profits products, into a company that sells mainly shareholder-backed products through a range of channels, including independent financial advisers, business to business and partnership agreements with other companies. We also improved our efficiency and broadened our product range. These changes enabled us to take advantage of the upturn in the market in 2004, and resulted in a 40 per cent rise in new business achieved profit year-on-year.

Over the next few years, we see new opportunities arising from the creation of multi-ties, and we have won places on many of the multi-tie panels announced to date. We expect these agreements to begin to have an effect on our performance in 2005, and to make an increasing contribution thereafter.

The Rights Issue, announced in October 2004, will allow us to take advantage of these developments in both our business and the marketplace.

In 2005, we expect sales to grow by about 10 per cent from our 2004 base, against an industry expectation of around five per cent market growth. We are aiming for a blended internal rate of return on this business of 14 per cent.

UNITED STATES

The US is the largest long-term savings market in the world, with considerable opportunities for growth.

Jackson National Life is an industry leader in distributing products and is able to react quickly to market changes, establishing strong positions in new products and channels. In 2004 it increased new business achieved profit by 18 per cent, to £156 million, with nearly 90 per cent of new sales coming from products developed in the last two years.

The business continues to fund its own growth, including small acquisitions, such as that of Life Insurance Company of Georgia, announced in November. It also contributed US$120 million to the Group in 2004, and this is expected to increase to US$150 million in 2005.

In 2005, we expect the US market to grow at about four per cent and Jackson National Life to grow sales at around twice this rate, while keeping its costs down and delivering above market returns.

ASIA

The Asian economies’ consistently high growth rates and favourable demographics, together with the trend towards allowing greater access and ownership to foreign financial services players, make these markets very attractive for Prudential, and we have a strong record of success in the region.

In the past decade we have expanded across 12 countries and delivered APE compound growth of 26 per cent per year, while

| Prudential has built strong positions in three of the most attractive savings markets in the world | £688m RECORD NEW BUSINESS ACHIEVED | ||||

| *All figures at constant exchange rates | |||||

| 04 | PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 |

| ||

| ||

| JONATHAN BLOOMER GROUP CHIEF EXECUTIVE | ||

in our chosen markets

maintaining margins above 50 per cent. In 2004, new business achieved profit rose 19 per cent.

We are now Europe’s leading life insurer in Asia in terms of market coverage and number of top five market positions. We have also established a complementary regional funds management business in seven markets and are setting up a fund management operation in Vietnam.

We see very good growth prospects in the region, particularly in India and China, and we are well placed to take advantage of these.

In India, our joint venture with ICICI delivered APE sales growth of 127 per cent and continues to be the leading private sector player. In 2004, the Indian government announced its intention to allow increased foreign ownership in Indian companies, and we remain interested in increasing our stake in the joint venture. However, the relevant legislation has not yet been put before the Indian Parliament.

In China, our joint venture with CITIC is one of the country’s leading foreign players, and it achieved new business APE growth of 70 per cent last year. We already operate in three cities, and will launch our fourth operation, in Shanghai, in the second quarter of 2005. We have recently received licences for two further cities, and a licence to write Group Life insurance business. We expect to continue to develop rapidly in China as geographic licensing restrictions ease further.

We are confident of our ability to grow strongly and profitably in the region, and our Asian business remains on track to become cash positive from 2006.

M&G

M&G provides high quality investment management services for Prudential’s customers, and is also a leading UK manager of retail investment funds and institutional fixed income and pooled life and pensions funds. At the end of 2004, it had total funds under management of £126 billion.

External funds under management rose by 19 per cent during the year to £28.7 billion, due to a combination of net fund inflows from both retail and institutional clients and market gains on existing funds.

In recent years, M&G has developed profitable new income streams while keeping a tight control over costs. This powerful combination has resulted in underlying profit of £110 million, up 57 per cent on 2003.

We expect M&G to continue to perform strongly in 2005.

EGG

Egg has closed its loss-making French operation and has recently put its Funds Direct business on the market. It is now firmly focused on its profitable core UK business, where it achieved underlying profit of £74 million in 2004. This was a good performance from Egg’s UK business, especially given the increased competition and rising interest rates that have affected the credit card and personal loan markets. Egg’s effective cost management and good credit quality also contributed to the solid results from its UK operation.

Looking ahead, Egg will continue to develop its UK operation, building its unsecured lending business, while expanding its product range to increase cross-sales to existing customers.

We expect Egg to finance its own growth without requiring capital support from the Group.

OUTLOOK

Prudential has built strong positions in three of the most attractive savings markets in the world. Each of the businesses is performing well, and is positioned to take advantage of the opportunities in its respective market. We are on track to deliver sustainable, profitable growth and to achieve our target returns on capital in 2005 and beyond.

*All year-on-year comparisons of financial performance are at constant exchange rates (CER), unless otherwise stated.

| +26% | £187bn | ||

| RECORD INSURANCE APE SALES OF £1.85 BILLION, UP 26 PER CENT* | RECORD FUNDS UNDER MANAGEMENT OF £187 BILLION, UP 11 PER CENT* | ||

| *All figures at constant exchange rates | *All figures at constant exchange rates | ||

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 | 05 |

| THE WORLD OF PRUDENTIAL | A WORLD OF OPPORTUNITY | |

It’s about... having the right

businesses in the right places

| STIRLING | |||||

| BELFAST | |||||

| DUBLIN | BERLIN | ||||

| NEW YORK | DERBY | ||||

| LANSING | |||||

| CHICAGO | NEW JERSEY | DUDLEY | |||

| LONDON | |||||

| SANTA MONICA | READING | ||||

| MILAN | |||||

| ATLANTA | |||||

|  | ||||||

| OUR BRANDS | Prudential is a leading life and pensions provider to more than seven million customers in the United Kingdom. | M&G is Prudential's UK and European fund manager with £126 billion of funds under management and over 830,000 unit holder accounts. | |||||

| OPERATIONS | Products | M&G offers a range of over 40 funds and | |||||

| AND PRODUCTS | • | Annuities | invests in a wide range of assets including | ||||

| • | Corporate Pensions | UK and international equities, fixed interest, | |||||

| • | With-profits Bonds and Unit-linked Bonds | property and private equity. | |||||

| • | Savings and Investment | ||||||

| • | Protection | Retail Products | |||||

| • | Equity Release | • | Open Ended Investment Companies | ||||

| • | Health Insurance | (OEICs) | |||||

| • | Unit Trusts | ||||||

| Product Distribution Channels | • | Investment Trusts | |||||

| • | Independent Financial Advisers | • | Individual Savings Accounts (ISAs) | ||||

| • | Business to Business (consulting actuaries and benefit advisers) | • | Personal Equity Plans (PEPs) | ||||

| • | Partnerships (affinities and banks) | ||||||

| • | Multi-tie Panels | Institutional Business | |||||

| • | Direct to customers (telephone, internet and mail) | • | Segregated fixed interest, pooled pension funds, | ||||

| structured and private finance | |||||||

| HIGHLIGHTS | In 2004, APE sales grew 40 per cent and | Underlying profit increased by 57 per cent | |||||

| Comparisons are quoted at | gross premiums grew 58 per cent. | in 2004 to £110 million. | |||||

| constant exchange rates | |||||||

| 06 | PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 |

| INSURANCE BUSINESS | INSURANCE BUSINESS | |

| OPERATING PROFIT BY REGION – | OPERATING PROFIT BY REGION – | |

| ACHIEVED PROFITS BASIS | MODIFIED STATUTORY BASIS | |

|  |

| BEIJING | ||||

| SEOUL | TOKYO | |||

| TAIPEI | ||||

| HONG KONG | ||||

| MUMBAI | ||||

| BANGKOK | MANILA | |||

| HO CHI MINH | ||||

| KUALA LUMPUR | ||||

| SINGAPORE | ||||

| JAKARTA | ||||

|  |  | |||||

| Egg plc is an innovative financial services company, providing a range of banking and financial services products through its internet site, www.egg.com | Jackson National Life (JNL) is a leading life insurance company in the United States and has more than 1.5 million policies and contracts in force. | Prudential has life insurance and fund management operations across 12 countries in Asia and is Europe’s leading life insurer in Asia in terms of market coverage and number of top five market positions. | |||||

| • Banking | • | Offers fixed, equity-indexed and variable annuities, term and permanent life insurance and institutional products | • | A comprehensive range of savings, protection and investment products tailored to the needs of each local market | |||

| • Insurance | |||||||

| • Investments | |||||||

Egg has a market share of nearly six per cent of UK credit card balances. | • | Markets products in 50 states and the District of Columbia (in the State of New York through Jackson National Life Insurance Company of New York) through independent broker-dealers, independent agents, banks, regional broker-dealers and the registered investment adviser channel | • | Pioneered a unit-linked product in Malaysia, Indonesia, the Philippines, Singapore and Taiwan | |||

| • | A network of over 130,000 agents serving more than 5.7 million customers around the region | ||||||

| • | JNL's investment portfolio manager, PPM America Inc., manages around US$71 billion of assets | ||||||

| Egg's core UK business made an operating profit of £74 million (2003: £73 million). | Record variable annuity sales of £2 billion in 2004. | In 2004, new business achieved profit rose 19 per cent. | |||||

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 | 07 |

| STRATEGIC REVIEW | A WORLD OF OPPORTUNITY |

![]()

CASE STUDY

Prudential Corporation Asia prides itself on developing customer-centric products, but in the complex world of insurance, explaining these products to consumers can be difficult.

In China, our joint venture CITIC Prudential has risen to this challenge by becoming the first life insurer to

develop plain language contracts, using simple words to help customers to understand and feel more confident about the products that they are buying.

Customers who purchase CITIC Prudential products now encounter policy documents that use familiar, everyday language such as ‘we’ instead of the full legal company name, ‘you’ as opposed to ‘the policyholder’, and replacement of complex phrases and

instructions such as ‘Please refer to Clause...’.

The Chinese Insurance Regulator has backed this approach, which will reduce the risk of misunderstandings about policy details or claims. It will also make it easier to train insurance agents, at a time when increasingly sophisticated products are being launched in China, including unit-linked and universal life plans.

| 08 | PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 |

Prudential has built its reputation over more than 150 years, and has a portfolio of well-known and respected brands around the world.

In 2004, we sought to enhance this reputation further by leveraging our strengths in brand, distribution, service, product innovation and investment management to create value for our customers and our shareholders.

In the UK, Prudential is the largest life insurer in terms of insured funds under management, and its brand awareness is among the highest in the UK insurance industry.

It has leading positions in several product areas, including annuities, where it has secured a significant proportion of both bulk and individual pension annuities, and with-profits bonds. In corporate pensions, Prudential is a provider to 20 per cent of the FSTE 350 companies, and manages more than 4,000 schemes.

In 2004, Prudential UK launched two mould-breaking products: PruFund, a transparent smoothed investment product, which leverages the financial strength and consistently strong investment track record of the with-profits fund; and PruHealth, a private medical insurance plan which links premiums to customers’ efforts to improve their health.

In the US, Jackson National Life (JNL) has become a significant national player, largely on the strength of its relationship-based distribution model, which aims to attract top distributors by offering a superior service proposition. In 2004,

JNL was one of only eight companies to earn a world-class satisfaction award from North America’s Service Quality Measurement Group. It also received the ‘highest customer satisfaction by industry’ award for the financial services industry.

JNL has built a reputation for product innovation, particularly for its Perspective II variable annuity, which was the best-selling variable annuity in the US in terms of net flow (premiums minus surrenders and annuitisations) in 2004.

In Asia, Prudential is the leading European insurer in terms of market coverage and number of top five market positions. It is also one of the region’s largest international fund managers in terms of assets under management.

Over the last decade we have built a solid reputation for launching new businesses in the region, often in partnership with leading local institutions, and developing innovative, customer-centric products. We were, for example, a pioneer of unit-linked products in the region, and now offer these products in 10 of our 12 insurance markets.

The face of Prudence is well known throughout the region and has similar recognition levels to other leading international financial services companies.

As a long-term business, a key part of Prudential’s reputation rests on its financial strength, which we maintained during the year. Our UK long-term fund remains well capitalised with an AA+ rating from Standard & Poor’s and an Aa1 rating from Moody’s, and is among the strongest long-term funds in the UK. At the end of 2004,

the free asset ratio of the fund was approximately 14.8 per cent on a statutory basis without taking account of future profits or implicit items (compared with 10.7 per cent at the half year and 10.5 per cent at the end of 2003).

In 2004, the with-profits fund delivered a pre-tax return of 13.4 per cent compared with a FTSE All Share total return of 12.8 per cent.

The majority of this fund is managed by M&G, which, as well as providing in-house fund management services, also manages and distributes investment funds to retail and institutional customers. The Investment Management Association ranks M&G as the third largest asset manager in the UK and the third largest retail fund manager in the UK.

In 2004, M&G was one of only three fund management companies in the UK to receive a Gold Standard Award. The award reflects a number of criteria such as financial strength, service, capability, fair value and trustworthiness.

Egg is an innovative, internet-based company, which sells a range of banking and financial services. Since its launch in 1998 it has built a strong brand based on helping people to understand and manage their money more effectively. Research suggests that Egg customers have a strong inclination to buy additional services from the company.

| Captain Chia, CEO of CITIC Prudential, said: “We believe that it is important to make sure our customers understand the terms and benefits of their policies. We will continue to champion simplicity and clarity in all our policy documents.” | We have a portfolio of well-known and respected brands around the world | |||

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 | 09 |

STRATEGIC REVIEW CONTINUED | A WORLD OF OPPORTUNITY |

![]()

CASE STUDY

As one of the largest institutional

property investors in the UK, Prudential Property Investment Managers (PruPIM) manages over £14 billion of property assets on behalf of Prudential. John Cartwright, Head of Retail Funds at PruPIM, believed that they had the skills to manage a retail property fund that is fully invested in commercial property.

At the same time, M&G, one of the largest fund managers in the UK, had a range of successful bond and equity products, but was on the look out for profitable new income streams. Together they decided to launch an innovative property fund that combined PruPIM’s extensive property experience with M&G’s sales and marketing expertise.

In March 2004, the M&G Property Fund, managed by John Cartwright,

was launched with a well-diversified portfolio of £95 million, offering scale and diversity from day one, and comprising over 20 UK commercial properties spread across all key sectors.

Chris Jackson, Market Development Director at M&G, said: “This was a highly fruitful collaboration between M&G and PruPIM and has certainly been a most effective intra-group project. Working with PruPIM, we have been able to

| 10 | PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 |

In 2004, we continued to focus on building profitable long-term savings and investment businesses in our chosen markets around the world. We broadened our product range, and improved our mix of income, with the aim of meeting customer needs and achieving growth throughout the economic cycle, as well as reducing overall risks.

In the UK, Prudential UK strengthened and extended its product range, while maintaining leading positions in core products such as annuities, corporate pensions and with-profits bonds. Total annual premium equivalent (APE) sales were up by 40 per cent on 2003, driven by increased sales of unit-linked bonds, credit life protection products and individual and bulk annuities, including the acquisition of the existing annuity portfolio of another insurer.

In 2004, we also significantly increased the proportion of business we wrote in our shareholder-backed annuity business, Prudential Retirement Income Limited (PRIL), reducing the proportion backed by the with-profits life fund. Almost all annuity business is now written in PRIL, and this was a key factor in the significant increase in PRIL’s modified statutory basis (MSB) operating profit.

Several new products were introduced during the year, increasing Prudential’s appeal to the independent financial adviser (IFA) market and other distributors. These products included a transparent smoothed investment plan and an innovative private medical insurance policy.

Our US business, Jackson National Life (JNL) has also pursued a successful strategy of diversification, evolving from a company that traditionally focused on fixed annuities, to one that now also has a top 10 position in variable annuities, and a growing life business.

In 2004, this change of business mix enabled JNL to offset falling fixed annuity sales (as a result of low interest rates) against record sales of more profitable variable annuities, up 15 per cent on 2003, compared with market growth of 2.9 per cent.

JNL also continued to develop its life business, and launched its first variable universal life product in March. In November, it announced the purchase of Life Insurance Company of Georgia for £137 million, which will double its life insurance and annuity policies to just over three million.

In Asia, Prudential Corporation Asia continued to expand by product and distribution channel. The company’s consistently superior new business achieved profit (NBAP) margins and returns illustrate both the overall attractiveness of the Asian markets, and the company’s increasing success in managing its participation and product mix in each of its markets to maximise long-term value and manage risk.

In Taiwan, for example, the business has improved profitability by shifting its product mix away from traditional products and towards its higher margin unit-linked range, which has already been successful in markets such as Singapore and Malaysia.

Across the region, the company has a compelling mix of more mature businesses, such as in Hong Kong, Singapore and Malaysia, and newer, high growth potential businesses, such as in India and China.

In the fund management business, Japan achieved strong funds growth by leveraging PPM America’s expertise to market US funds. This, combined with good results from the Korean asset management business, offset a marked decline in funds under management of Taiwanese bond funds as a result of changing local market conditions.

M&G, our UK-based fund management arm, has successfully developed a diverse business, which now comprises retail fund management, institutional fixed income, pooled life and pension funds, property and private finance. M&G’s ability to develop new and varied revenue sources, combined with disciplined cost management, enabled it to increase underlying profit by 57 per cent year-on-year.

M&G also continued its expansion into selected countries in continental Europe, where gross fund inflows grew fourfold to €611 million compared with 2003.

Egg has closed its loss-making French operation and is now focused on its core UK business, where it achieved profits of £74 million in 2004. Income rose by 18 per cent, through a combination of net interest income and other income, particularly from loans, credit cards and associated insurances.

|

| ||||

establish a whole new asset class, and this has really opened doors for us with private clients through financial intermediaries.” The fund has been well received and took in £136 million in its first nine months. | We have broadened our product range and improved our mix of income | ||||

|

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 | 11 |

| STRATEGIC REVIEW CONTINUED | A WORLD OF OPPORTUNITY |

![]()

CASE STUDY

As a company that works closely with third party distributors to sell its products, Prudential is constantly looking at ways to deepen its relationships with these key individuals and help them to be more effective.

This is the thinking behind training schemes run by both Jackson National

Life (JNL) and Prudential UK. In the US, several courses have been devised to meet different advisers’ needs. In Pennsylvania, for example, JNL runs an accredited two-day course for insurance representatives of one of its major banking clients, which helps them towards the continuing education credits that they are required to obtain. JNL provides books and lectures and runs the tests. “Offering services like training and education helps us to stand

out from other wholesalers,” says Robert McGrorty, at JNL. “And the more educated they are, the better they will be able to serve their customers.”

Taking the best and making them better is the theme behind a training scheme launched in the UK at the end of 2004. Based on research that suggests that 20 per cent of advisers produce 80 per cent of the business, Prudential’s ‘Top Gun’ academy offers

| 12 | PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 |

Across the world, Prudential’s success depends on our ability to build effective, long-lasting relationships with customers and distribution partners.

In the UK, Prudential draws its business from relationships with independent financial advisers (IFAs), banks, insurers and other companies, as well as directly from customers.

The IFA channel is undergoing significant change, following the introduction of new rules allowing IFAs to move to a multi-tie approach where they offer the products of a small ‘panel’ of insurers, rather than the whole market.

We expect large numbers of IFAs to choose this route over the coming years, and in 2004 we worked hard to build relationships with the emerging multi-tie panels of the major networks, and to increase our appeal to them through a range of service and product enhancements.

We have already won places on many of the panels announced to date, including Millfield and Sesame, two of the UK’s largest IFA networks.

In our partnerships channel we achieved significant increases in credit life protection sales through Lloyds TSB and Alliance & Leicester, and in annuity sales through agreements with Zurich and Pearl. A further partnership was agreed with St James’ Place in January regarding sales of annuities. Barclays has also announced its intention to appoint Prudential UK as one of its product providers.

Prudential UK’s strong relationships with consulting actuaries and employee

benefits consultants also drove fee-based group pension business APE sales up by 14 per cent year-on-year.

In the US, Jackson National Life’s (JNL) success depends on the strength of its relationships with third party distributors. The company uses its IT expertise and low cost base to offer these partners award-winning service and market-leading sales support, combined with an attractive product range.

In 2004, JNL’s service was further improved following a reorganisation of its customer support centres to standardise procedures and improve efficiency. It also introduced Fifth Third Perspective, a variable annuity (VA) product designed exclusively for customers of one of its largest banking clients, Fifth Third Securities. Fifth Third Perspective generated over US$50 million in sales in only eight months, more than 65 per cent of JNL’s total 2004 VA sales through Fifth Third Securities.

In its broker-dealer network, National Planning Holdings (NPH), JNL has introduced on-line systems that reduce compliance paperwork for representatives so they can spend more time on revenue generation. This helped to drive NPH’s strong revenue growth in 2004 of 20 per cent, and generate record net income of US$3.5 million.

In Asia, Prudential’s impressive multi-channel distribution network includes over 130,000 tied agents and several leading international and local financial institutions, such as Standard Chartered in Hong Kong, Malaysia, Singapore, Thailand and Taiwan.

In India, Prudential’s life insurance expertise combined with ICICI’s local presence and reputation has been particularly powerful, and this joint venture is the leading private sector player in India.

In 2004, Prudential formed new partnerships with E. Sun Bank in Taiwan and Maybank in Singapore. In China, CITIC Prudential was awarded life licences for Shanghai and Suzhou. Earlier this year, it added two further life licences for Dongguan and Foshan, and a licence to write Group Life business.

M&G’s retail businesses’ diversified distribution network covers all major channels, including discretionary brokers, IFAs, charities, third party distributors and direct to investors. In the UK, M&G has strong relationships with intermediaries and is a major player in equities and fixed income across all channels.

M&G’s institutional business continues to develop new external business lines using the expertise developed for internal funds, in areas such as leveraged loans and project finance. Its long-standing relationships with investment banks and consulting actuaries places it in a strong position to develop new fixed income and private finance products for external clients.

A key part of Egg’s strategy is to use its strong relationships with existing customers, to encourage them to buy other Egg products. In 2004, it was successful in cross-selling personal loans to credit card customers, and also achieved significant general insurance sales in the fourth quarter. In 2005, Egg will increase its range of products to drive further cross-sales.

|

| |||||

high-flying independent financial advisers the chance to spend three and a half days working on their sales, presentation and business development skills, as well as networking with other high-performers. Pam Aurbach of Prudential UK says: “The participants to date have valued particularly the opportunity to get feedback both from trainers and their peer group; something which is not normally available to them.” | Across the world, our | |||||

|

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 | 13 |

| FINANCIAL REVIEW | A WORLD OF OPPORTUNITY | |

RESULTS HIGHLIGHTS

The Group has delivered a good set of results for 2004, as illustrated by the double-digit growth of all the key performance measures shown in the table below. This is the result of strong contributions across all regions.

As a result of healthy sales in the UK, the US and Asia, the Group achieved record insurance sales and new business achieved profit (NBAP) in 2004. This, together with the significant increase in contributions from the in-force insurance business and fund management operations, drove achieved profits basis operating profit up 39 per cent on 2003.

On the modified statutory basis (MSB), operating profit was up 49 per cent on last year. This reflects a combination of solid year-on-year growth in profit in both the insurance and fund management businesses of 40 per cent and 55 per cent respectively.

IMPACT OF CURRENCY MOVEMENTS

Prudential has a diverse international mix of businesses with a significant proportion of its profit generated outside the UK. In preparing the Group’s consolidated accounts, results of overseas operations are converted at rates of exchange based on the year average, while shareholders’ funds are converted at year end rates of exchange.

Changes in exchange rates from year to year have an impact on the Group’s results when these are converted into pounds sterling for reporting purposes. In some cases, these exchange rate fluctuations can mask underlying business performance. For example, growth in Asia’s total MSB operating profit was 83 per cent at reported rates, compared to 103 per cent at Constant Exchange Rates (CER). This reflects the close relationship between most Asian currencies and the US dollar and its depreciation against sterling during the year.

Consequently, the Board has for a number of years reviewed the Group’s international performance at CER. This basis

eliminates the impact from conversion, the effects of which do not alter the long-term value of shareholders’ interests in our non UK businesses.

In the Financial Review, year-on-year comparisons of financial performance are at CER, unless otherwise stated.

SALES AND FUNDS UNDER MANAGEMENT

![]()

Prudential delivered strong growth in sales during 2004 with total new insurance sales up 40 per cent to £12.1 billion at CER. This resulted in record insurance sales of £1.85 billion on the annual premium equivalent (APE) basis, an increase of 26 per cent on 2003. At reported exchange rates, APE was up 19 per cent on 2003.

In 2004, gross written premiums, including insurance renewal premiums, increased 19 per cent to £16.4 billion, reflecting the growth of new insurance sales in 2004 and the significant contribution from regular premium business written in previous years.

| 2003 (at 2004 exchange rate) | ||||||||||||

| RESULTS HIGHLIGHTS | 2004 (as reported) | Percentage change | 2004 (as reported) | 2003 (as reported) | Percentage change | |||||||

| £m unless otherwise stated | ||||||||||||

| Annual premium equivalent (APE) sales | 1,846 | 1,464 | 26 | % | 1,846 | 1,557 | 19 | % | ||||

| Net investment flows | 3,589 | 2,908 | 23 | % | 3,589 | 3,031 | 18 | % | ||||

| New business achieved profit (NBAP) | 688 | 561 | 23 | % | 688 | 605 | 14 | % | ||||

| NBAP margin | 37 | % | 38 | % | – | 37 | % | 38 | % | – | ||

| Total achieved profits basis operating profit* | 1,124 | 807 | 39 | % | 1,124 | 861 | 31 | % | ||||

| Total modified statutory basis (MSB) operating profit* | 603 | 405 | 49 | % | 603 | 424 | 42 | % | ||||

| Achieved profits basis shareholders’ funds | 8,596 | 6,762 | 27 | % | 8,596 | 7,005 | 23 | % | ||||

| MSB shareholders’ funds | 4,281 | 3,060 | 40 | % | 4,281 | 3,240 | 32 | % | ||||

| *Continuing operations – excluding Jackson Federal Bank (JFB) and Egg’s France business. In the Financial Review, year-on-year comparisons of financial performance are at constant exchange rates (CER), unless otherwise stated. | ||||||||||||

| 14 | PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 |

Total gross investment sales for 2004 were £25.1 billion, up 21 per cent on 2003 at CER. Net investment sales of £3.6 billion were up 23 per cent on last year at CER. Total investment funds under management in 2004 increased by 19 per cent from £30.9 billion to £37.1 billion, reflecting net investment flows of £3.6 billion and net market and other movements of £2.6 billion.

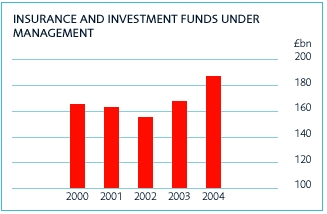

At 31 December 2004, total insurance and investment funds under management were £187 billion, an increase of 11 per cent from 2003. This marked a record level of funds under management and the increase was primarily due to the combination of changes in the market value of investments and the impact of net insurance and investment sales achieved during the year.

BASIS OF PREPARATION OF RESULTS

Prudential is required to account for its long-term insurance business on the modified statutory basis (MSB) of reporting under UK accounting standards. The Group's primary financial statements are therefore prepared on this basis and broadly reflect the UK solvency-based reporting regime and, for overseas territories, adjusted local or US GAAP. In broad terms, MSB profit for long-term business reflects the aggregate of statutory transfers from with-profits funds and profit on a traditional deferral and matching approach for other long-term business. Although the statutory transfers from with-profits funds are closely aligned with cash flow generation, the pattern of MSB profit over time from shareholder-backed long-term businesses will generally differ from the cash flow pattern. Over time however, aggregate MSB profit will be the same as aggregate cash flow.

Life insurance products are, by their nature, long-term and the profit on this business is generated over a significant number of years. MSB profit does not, in Prudential’s opinion, properly reflect the inherent value of these future profit streams.

Accordingly, in common with other listed UK life assurers, Prudential also reports supplementary results for its long-term

operations on the achieved profits basis. These results are combined with the statutory basis results of the Group’s other operations, including fund management and banking businesses. Reference to operating profit relates to profit including investment returns at the expected long-term rate of return, but excludes amortisation of goodwill, exceptional items, short-term fluctuations in investment returns and the effect of changes in economic assumptions.

In the directors' opinion, the achieved profits basis provides a more realistic reflection of the current performance of the Group's long-term insurance operations than results on the MSB basis, as it reflects the business performance during the accounting period under review, although both bases should be considered in forming a view of the Group’s performance.

ACHIEVED PROFITS BASIS RESULTS

Achieved Profits Basis Operating Profit

Total achieved profits basis operating profit from continuing operations was £1,124 million, up 39 per cent from 2003 at CER. At reported exchange rates, the result was up 31 per cent. This result reflects a combination of strong growth in the insurance and fund management businesses.

Prudential’s insurance business achieved significant growth, both in terms of new business achieved profit (NBAP) and in-force profit, resulting in a 35 per cent increase in operating profit over 2003 at CER. NBAP of £688 million was up 23 per cent on the prior year at CER and up 14 per cent at reported exchange rates. In-force profit increased 51 per cent on 2003 at CER to £460 million. At reported exchange rates, in-force profit was up 46 per cent.

Results from fund management and banking business were £184 million, an increase of 26 per cent at CER on 2003. This was mainly driven by the significant contribution from M&G.

| ACHIEVED PROFITS BASIS OPERATING PROFIT | ||||||||||||

| 2004 (as reported) £m | 2003 (at 2004 exchange rate) £m | Percentage change | 2004 (as reported) £m | 2003 (as reported) £m | Percentage change | |||||||

| Insurance business: | ||||||||||||

| UK and Europe | 450 | 359 | 25 | % | 450 | 359 | 25 | % | ||||

| US | 317 | 176 | 80 | % | 317 | 197 | 61 | % | ||||

| Asia | 381 | 328 | 16 | % | 381 | 365 | 4 | % | ||||

| Development expenses | (15 | ) | (24 | ) | 38 | % | (15 | ) | (27 | ) | 44 | % |

| 1,133 | 839 | 35 | % | 1,133 | 894 | 27 | % | |||||

| Fund management business: | ||||||||||||

| M&G | 136 | 83 | 64 | % | 136 | 83 | 64 | % | ||||

| US broker-dealer and fund management | (14 | ) | (3 | ) | (367 | )% | (14 | ) | (3 | ) | (367 | )% |

| Asia fund management | 19 | 11 | 73 | % | 19 | 13 | 46 | % | ||||

| 141 | 91 | 55 | % | 141 | 93 | 52 | % | |||||

| Banking: | ||||||||||||

| Egg (UK) | 43 | 55 | (22 | )% | 43 | 55 | (22 | )% | ||||

| Other income and expenditure | (193 | ) | (178 | ) | (8 | )% | (193 | ) | (181 | ) | (7 | )% |

| Operating profit from continuing operations | 1,124 | 807 | 39 | % | 1,124 | 861 | 31 | % | ||||

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 | 15 |

| FINANCIAL REVIEW CONTINUED | A WORLD OF OPPORTUNITY | |

New Business Achieved Profit (NBAP)

![]()

In 2004, the Group has generated record new business achieved profit (NBAP) from insurance business of £688 million which was 23 per cent above 2003 at CER, driven by strong sales momentum across all markets. At reported exchange rates, NBAP was up 14 per cent. The average Group NBAP margin of 37 per cent was slightly down from 38 per cent in 2003. The overall margin has been broadly maintained over the last two years, reflecting careful management of product mix within each business and across the three regions.

NBAP from the UK and Europe Insurance Operations was £220 million, an increase of 40 per cent on 2003. This reflected increased APE sales and a balanced shift in sales mix. This positive movement arose due to increased sales of more profitable bulk annuities partially offset by reduced sales of high margin with-profits bonds and increased sales of less profitable executive pensions. The NBAP margin has been maintained at 27 per cent, the same as 2003.

In the US, JNL’s NBAP of £156 million was up 18 per cent on 2003 at CER and up five per cent at reported rates. This increase was principally volume driven as a result of high sales levels recorded during the year. The NBAP margin was 34 per cent in 2004, a slight reduction from 35 per cent in 2003 due to a shift in product mix and a small impact from economic assumption changes.

In Asia, NBAP of £312 million was up 19 per cent at CER on 2003, reflecting a combination of increased sales and higher NBAP margin. During 2004, APE sales were up 14 per cent on 2003 and the NBAP margin was 54 per cent, compared with 52 per cent in 2003 at CER. The increase in margin was principally due to a combination of changes in country mix and product mix being offset by the impact of assumption changes.

In-Force Achieved Profit

Total in-force profit in 2004 was £460 million, an increase of 51 per cent on 2003 at CER. This was driven by the significant increase in the in-force profit in the US.

UK and European in-force profit of £230 million was up 19 per cent on 2003. The profit arising from the unwind of discount from the in-force book was partially offset by adverse operating assumption changes and other experience charges. A charge of £66 million was made reflecting a 40 per cent strengthening of the persistency assumptions on the closed-book of personal pensions business sold through the closed direct sales force channel. This assumption change reflects Prudential UK’s experience over the last three years and, post-tax, represents about one per cent of the overall embedded value of the UK business. Measures to manage and improve the conservation of in-force business have had a beneficial effect on persistency that Prudential UK expects to maintain or improve. Consequently, Prudential UK has not changed persistency assumptions for all other products. Other charges of £34 million include £21 million of costs associated with complying with new regulatory requirements and restructuring.

In the US, the in-force profit of £161 million was more than three times higher than in 2003. This growth reflects improvements from 2003 in net experience variances to positive £33 million (an increase of £46 million at CER), changes in operating assumptions to negative £3 million (an increase of £16 million at CER) and changes in other items to positive £12 million (an increase of £37 million at CER). Included in other items is a £28 million favourable legal settlement. The £33 million positive total experience variance includes a £43 million positive spread variance (net of risk margin reserve) primarily reflecting a favourable variance in the fixed annuity portfolio. The assumed spread on new fixed annuity business is 155 basis points grading to 175 basis points over five years.

Asia’s in-force profit (before development expenses and the Asia fund management business) increased to £69 million in 2004 from £67 million in 2003 at CER. This reflects a higher unwind of the discount rate as the in-force business builds scale and lower experience variances, offset by assumption changes of £56 million. The assumption changes made in 2004 principally reflect a worsening persistency in Singapore and a revision to expense assumptions in Vietnam.

Non-Insurance Operations

M&G

M&G’s operating profit was £136 million, an increase of 64 per cent on last year. This included £26 million in performance-related fees (PRF), of which £20 million was generated by PPM Ventures on the exceptionally profitable realisation of several investments during the year.

| 16 | PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 |

Underlying profit of £110 million was 57 per cent higher than 2003, achieved as a result of a strong performance across all of M&G’s business lines. Significant growth was delivered in the areas of fixed income, retail and property; attributable to the continued development of new business streams and the recovery in stock markets during 2004. In addition, underlying profit was also boosted by £7 million of one-off provision releases in 2004 that will not recur in future years. Effective cost control also contributed to the significant growth in profit where the tight management of overhead across the entire business has resulted in costs remaining flat for the last four years.

US broker-dealer and fund management businesses

The broker-dealer and fund management operations, which include Curian Capital, reported a total loss of £14 million, compared with a £3 million loss in 2003. This primarily reflects increased losses at Curian Capital as the business continues to build scale.

Asian fund management business

Profit from Asian fund management operations was £19 million, up 73 per cent from 2003, reflecting a combination of increasing scale and profitability in the retail business, particularly from the joint venture with ICICI in India, and higher management fees from the UK and Asian life businesses.

Egg

Egg’s total continuing operating profit in 2004 was £43 million, compared with £55 million in 2003. Egg’s UK business achieved a profit of £74 million, compared with £73 million in 2003. This represents a solid result considering the increased competition and rising interest rates that have impacted the credit card and personal loan markets. Following the decision to dispose of its investment in Funds Direct, its investment wrap platform business, Egg provided for a £17 million impairment charge against the full carrying value of the underlying assets of Funds Direct.

Others

Asia’s development expenses (excluding the regional head office expenses) reduced by 38 per cent at CER to £15 million, compared with £24 million in 2003. Other net expenditure increased by £15 million to £193 million.

Total Achieved Profits Basis – Result Before Tax

(Year-on-year comparisons below are based on reported exchange rates.)

The result before tax and minority interests was a profit of £1,521 million, up 82 per cent on 2003. This primarily reflects the strong operating profit from continuing operations of £1,124 million and the lower negative effect of changes in economic assumption of £100 million, compared with negative £540 million in 2003. The result also benefited from strong investment performance which was ahead of the long-term investment assumptions.

The short-term investment fluctuations were £679 million (2003: £682 million), with £402 million relating to the UK and £207 million arising from the US.

Total economic assumption changes of negative £100 million (2003: £540 million) reflect changes in assumptions for future investment returns, discount rate and related items and included £19 million for the UK, £53 million for the US and £28 million for Asia.

Amortisation of goodwill was £97 million in 2004 compared to £98 million in 2003. Profit on the disposals of Jackson Federal Bank and the Group’s 15 per cent interest in Life Assurance Holding Corporation Limited was £41 million and £7 million respectively.

In France, an exit cost provision of £113 million was established in July 2004 following Egg’s announcement of its intention to withdraw from the French market. £96 million of the provision had been used by 31 December 2004 and it is expected that the withdrawal can be completed within the provision established.

![]()

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 | 17 |

| FINANCIAL REVIEW CONTINUED | A WORLD OF OPPORTUNITY | |

MODIFIED STATUTORY BASIS (MSB) RESULTS

MSB Operating Profit

Group operating profit from continuing operations on the modified statutory basis (MSB) was £603 million, an increase of 49 per cent from 2003 at CER. At reported exchange rates, operating profit was up 42 per cent on last year. This reflects strong growth in insurance and fund management businesses.

In the UK, MSB operating profit was £305 million in 2004, an increase of 19 per cent on 2003. This included a fourfold increase in Prudential Retirement Income Limited’s (PRIL) profit from £31 million to £124 million. This more than offset the £17 million reduction in the profit from the with-profits fund, which fell due to lower annual and terminal bonus rates announced in February 2004.

In the US, Jackson National Life’s (JNL) operating profit from continuing operations of £182 million was up 46 per cent on 2003. Total MSB operating profit for long-term business from continuing operations was £196 million, up 53 per cent from £128 million in 2003.

Growth in the long-term business operating profit reflects JNL’s clear focus on profitability and its ability to deliver improved investment returns. In 2004, spread income was £169 million higher than in 2003 and variable annuity fee income was at a record level due to the significant growth (47 per cent) in separate account assets. In addition, there were two one-off items, a favourable legal settlement of £28 million and a positive £8 million adjustment arising from the adoption of a new US accounting pronouncement.

Prudential Corporation Asia’s operating profit for long-term business before development expenses of £15 million was £126 million, an increase of 64 per cent on 2003 at CER. At reported rates, operating profit was 48 per cent up on last year. The majority of this profit currently still comes from the larger and more established operations of Singapore, Hong Kong and Malaysia, which represented £110 million of the total in 2004, compared to £86 million last year. Five life operations made MSB losses; China, India and Korea reflecting their rapid building of scale while Thailand is marginally loss making and Japan’s loss

reduced significantly over 2003 due to lower new business strain, reduced management expenses and mark to market gains on investments.

Total MSB Profit – Result Before Tax

(Year-on-year comparisons below are based on reported exchange rates.)

MSB profit before tax and minority interests was £650 million in 2004, compared with £350 million in 2003. This mainly reflects growth in operating profit of £226 million and improvement in short-term fluctuations in investment return, up £138 million from last year to positive £229 million.

Amortisation of goodwill was £97 million in 2004 compared with £98 million in 2003. Profit on the disposals of Jackson Federal Bank and the Group’s 15 per cent interest in Life Assurance Holding Corporation Limited was £41 million and £7 million respectively. In France, an exit cost provision of £113 million was established in July 2004 following Egg’s announcement of its intention to withdraw from the French market. £96 million of the provision had been used by 31 December 2004 and it is expected that the withdrawal can be completed within the provision established.

EARNINGS PER SHARE

Earnings per share, based on achieved profits basis operating profit after tax and related minority interests, but before amortisation of goodwill, were up 11.8 pence to 37.2 pence. The 2003 figure has been restated from 26.4 pence to 25.4 pence to adjust for the bonus element of the Rights Issue. Earnings per share, based on MSB operating profit after tax and related minority interests, but before amortisation of goodwill, were 19.2 pence, compared with a restated 2003 figure of 12.4 pence.

Basic earnings per share, based on total achieved profits basis profit for the year after minority interests, were 49.1 pence, compared with a restated figure of 23.4 pence in 2003. Basic earnings per share, based on MSB profit for the year after minority interests, were 20.1 pence, 10.1 pence up from a restated 2003 figure of 10.0 pence.

| MODIFIED STATUTORY BASIS OPERATING PROFIT | ||||||||||||

| 2003 | ||||||||||||

| 2004 | (at 2004 | 2004 | 2003 | |||||||||

| (as reported) | exchange rate) | Percentage | (as reported) | (as reported) | Percentage | |||||||

| £m | £m | change | £m | £m | change | |||||||

| Insurance business: | ||||||||||||

| UK and Europe | 305 | 256 | 19 | % | 305 | 256 | 19 | % | ||||

| US | 196 | 128 | 53 | % | 196 | 143 | 37 | % | ||||

| Asia | 126 | 77 | 64 | % | 126 | 85 | 48 | % | ||||

| Development expenses | (15 | ) | (24 | ) | 38 | % | (15 | ) | (27 | ) | 44 | % |

| 612 | 437 | 40 | % | 612 | 457 | 34 | % | |||||

| Fund management business: | ||||||||||||

| M&G | 136 | 83 | 64 | % | 136 | 83 | 64 | % | ||||

| US broker dealer and fund management | (14 | ) | (3 | ) | (367 | )% | (14 | ) | (3 | ) | (367 | )% |

| Asia fund management | 19 | 11 | 73 | % | 19 | 13 | 46 | % | ||||

| 141 | 91 | 55 | % | 141 | 93 | 52 | % | |||||

| Banking: | ||||||||||||

| Egg (UK) | 43 | 55 | (22 | )% | 43 | 55 | (22 | )% | ||||

| Other income and expenditure | (193 | ) | (178 | ) | 8 | % | (193 | ) | (181 | ) | 7 | % |

| Operating profit from continuing operations | 603 | 405 | 49 | % | 603 | 424 | 42 | % | ||||

| 18 | PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 |

DIVIDEND PER SHARE

As outlined in the Rights Issue prospectus, Prudential has maintained its current dividend policy, with the proposed 2004 final dividend payment per share taking account of the bonus element of the Rights Issue.

The shares issued as part of the Rights Issue were issued at a discount to market price (308 pence per share versus a closing share price of 458 pence per share on the day immediately preceding the announcement of the Rights Issue). It is therefore necessary to restate the Company’s previously reported earnings and previously declared dividends per share for this bonus element.

The bonus adjustment is equal to the closing share price on the final day Prudential’s shares traded cum-rights (19 October 2004) divided by the theoretical ex-rights price (TERP) as outlined in the table below.

The resulting bonus adjustment factor used for restating earnings and dividends per share using the methodology outlined above is 0.9614.

The final dividend per share for 2003 was 10.29 pence after adjusting for the bonus element of the Rights Issue (10.70 pence before the adjustment). The interim dividend for 2004 was 5.40 pence (5.19 pence after adjustment for the Rights Issue).

The directors recommend that the shareholders declare a final dividend for 2004 of 10.65 pence per share. The total dividend for the year, comprising the adjusted interim dividend and the recommended final dividend, amounts to 15.84 pence per share, an increase of 3.0 per cent over the full year 2003 dividend of 15.38 pence per share after adjustment for the bonus element of the Rights Issue.

The 2004 dividend is covered 1.2 times by post-tax modified statutory basis profit for the financial year after minority interests.

RIGHTS ISSUE

The strength of Prudential’s businesses and positive developments in a number of its markets represent an opportunity to enhance its

market position and generate improved returns for its shareholders. A strong financial position at a Group level will provide increased financial flexibility and allow Prudential to capitalise on these opportunities as they arise.

In response to these developments the Board took the decision in October 2004 to launch a 1 for 6 Rights Issue.

The majority of the net proceeds of the Rights Issue (£1,021 million) will be used to provide capital to support Prudential’s growth plans for the UK and to fund a potential opportunity to increase its ownership from 26 per cent to 49 per cent of its joint venture life insurance business with ICICI in India. The remainder of the proceeds will be used to ensure that Prudential meets the parent company solvency test under the EU Financial Groups Directive (FGD) that became effective from 1 January 2005. The proceeds of the Rights Issue have initially been invested centrally within the Group in fixed interest securities.

SHAREHOLDERS’ FUNDS

On the achieved profits basis, which recognises the shareholders’ interest in long-term businesses, shareholders’ funds at 31 December 2004 were £8.6 billion, up £1.6 billion from 31 December 2003.

Modified statutory basis (MSB) shareholders’ funds, which are not affected by fluctuations in the value of investments in the Group’s with-profits funds, were £4.3 billion, an increase of £1.1 billion from 31 December 2003.

INTERNAL RATE OF RETURN (IRR) OF INSURANCE OPERATIONS

United Kingdom and Europe

Prudential allocates shareholder capital to support new business growth across a wide range of products in the UK. The weighted average post-tax Internal Rate of Return (IRR) on the capital allocated to new business growth in the UK in 2004 was 12 per cent. By the financial year ending 2007, Prudential is targeting an IRR of 14 per cent on the capital required to support new business sold in that year in the UK.

| RIGHTS ISSUE BONUS ADJUSTMENT | ||||

| Market price cum-rights (Tuesday 19 October 2004) (pence) | A | 422.00 | ||

| Rights Issue price (pence) | B | 308.00 | ||

| Number of shares pre Rights Issue (million) | C | 2,023.29 | ||

| Number of shares issued through Rights Issue (million) | D | 337.22 | ||

| (A x C) + (B x D) | ||||

| Theoretical ex-rights price (pence) | TERP = | 405.71 | ||

| C + D | ||||

| Bonus adjustment | TERP/A | 0.96 | 14 | |

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 | 19 |

| FINANCIAL REVIEW CONTINUED | A WORLD OF OPPORTUNITY |

United States

For Jackson National Life (JNL), the average IRR on new business was 13 per cent which we believe to be above the returns being earned currently in the US life insurance industry.

Asia

In Asia we have target IRRs on new business at a country level of 10 per cent over the country risk discount rate. Risk discount rates vary from five per cent to 19 per cent depending upon the maturity of the market. These target rates of return are average rates and the marginal return on capital on a particular product could be above or below the target.

CASH FLOW

The table below shows the Group holding company cash flow. Prudential believes that this format gives a clearer presentation of the use of the Group’s resources than the FRS 1 statement required by UK GAAP.

The Group received £521 million in cash remittances from business units in 2004 (2003: £586 million) comprising the shareholders’ statutory life fund transfer of £208 million relating to earlier bonus declarations, together with dividends and interest from subsidiaries of £313 million. The shareholder transfer in 2005 representing 2004’s profits from the PAC with-profits fund, is expected to be approximately £198 million.

Prudential UK paid a £100 million special dividend from the PAC shareholders’ funds in respect of profits arising from earlier business disposals. A similar amount will also be distributed from

PAC shareholders’ funds in 2005. The level of scrip dividend take-up in 2004 (for both the 2003 final and 2004 interim dividend) was greater than the corresponding take-up in 2003, in part due to the change in basis of the election offered to shareholders. After dividends and interest paid, there was a net inflow of £173 million (2003: £42 million).

During 2004, the Group invested £31 million in corporate activities (2003: £58 million receipt, arising from disposal proceeds and exceptional tax receipts).

The Group invested £347 million during 2004 in its business units (2003: £173 million). Investment in the UK amounted to £189 million. This amount is expected to increase to around £250 million in 2005. Investment in Asia in 2004 of £158 million is expected to remain broadly the same in 2005. In 2006, based on current plans and expectations, Prudential expects Asia to be a net capital provider to the Group.

Together with the proceeds from the Rights Issue of £1,021 million, there was a total increase in cash of £850 million (2003: £4 million).

SHAREHOLDERS’ BORROWINGS AND FINANCIAL FLEXIBILITY

As a result of the holding company’s net funds inflow of £850 million and exchange conversion gains of £49 million, net core borrowings at 31 December 2004 were £1,236 million, compared with £2,135 million at 31 December 2003. After adjusting for holding company cash and short-term investments of £1,561 million, core structural borrowings of shareholder-financed

| GROUP HOLDING COMPANY CASH FLOW | 2004 | 2003 | ||

| £m | £m | |||

| Cash remitted by business units: | ||||

| UK life fund transfer* | 208 | 286 | ||

| UK other dividends (including special dividend) | 100 | 120 | ||

| JNL | 62 | 48 | ||

| Asia | 67 | 48 | ||

| M&G | 84 | 84 | ||

| Total cash remitted to Group | 521 | 586 | ||

| Net interest paid | (144 | ) | (127 | ) |

| Dividends paid | (323 | ) | (447 | ) |

| Scrip dividends and share options | 119 | 30 | ||

| Cash remittances after interest and dividends | 173 | 42 | ||

| Tax received | 34 | 77 | ||

| Corporate activities | (31 | ) | 58 | |

| Cash flow before investment in businesses | 176 | 177 | ||

| Capital invested in business units: | ||||

| UK and Europe | (189 | ) | (23 | ) |

| JNL | 0 | 0 | ||

| Asia | (158 | ) | (145 | ) |

| Other | 0 | (5 | ) | |

| (Decrease) increase in cash before Rights Issue proceeds | (171 | ) | 4 | |

| Rights Issue proceeds | 1,021 | 0 | ||

| Increase in cash | 850 | 4 | ||

| *In respect of prior year bonus declarations. |

| 20 | PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 |

| | |

operations at the end of 2004 totalled £2,797 million, compared with £2,567 million at the end of 2003. This increase reflected the issue of US$250 million (£137 million at transaction rate) Perpetual Subordinated Capital Securities and additional short-term borrowings of £150 million, partially offset by exchange conversion gains of £57 million.

Prudential plc enjoys strong debt ratings from both Standard & Poor’s and Moody’s. Prudential long-term senior debt is rated AA– (negative outlook) and A2 (stable outlook) from Standard & Poor’s and Moody’s respectively, while short-term ratings are A1+ and P-1.

FINANCIAL STRENGTH OF INSURANCE OPERATIONS

United Kingdom

A common measure of financial strength in the United Kingdom for long-term insurance business is the free asset ratio. The free asset ratio is the ratio of assets less liabilities to liabilities, and is expressed as a percentage of liabilities. On a comparable basis with 2003, the free asset (or previous regulatory Form 9) ratio of the Prudential Assurance Company (PAC) long-term fund was approximately 14.8 per cent at the end of 2004, compared with 10.5 per cent at 31 December 2003. The valuation has been prepared, in our opinion, on a conservative basis in accordance with the current FSA valuation rules, and without the use of implicit items.

The fund is very strong with an inherited estate measured on an essentially deterministic valuation basis of more than £6.5 billion compared with approximately £6 billion at the end of 2003. On a realistic basis, with liabilities recorded on a market consistent basis, the free assets are valued at around £5 billion before a deduction for the risk capital margin.

The PAC long-term fund is rated AA+ (stable outlook) by Standard & Poor’s and Aa1 (stable outlook) by Moody’s.

United States

The capital adequacy position of Jackson National Life (JNL) remains strong, with a strong risk-based capital ratio of 4.3 times the NAIC Company Action Level Risk Based Capital. JNL’s financial strength is rated AA by Standard & Poor’s (negative outlook) and A1 by Moody’s.

Asia

Prudential Corporation Asia maintains solvency margins in each of its operations so that these are at or above the local regulatory requirements. Across the region, approximately 30 per cent of non-linked funds are invested in equities.

INHERITED ESTATE

The long-term fund contains the amount that the Company expects to pay out to meet its obligations to existing policyholders and an additional amount used as working capital. The amount payable over time to policyholders from the With-Profits Sub-Fund is equal to the policyholders' accumulated asset shares plus any additional payments that may be required for smoothing or to meet guarantees. The balance of the assets of the With-Profits Sub-Fund is called the ‘inherited estate’ and represents the major part of the working capital of Prudential’s long-term fund which enables the Company to support with-profits business by:

| providing the benefits associated with smoothing and guarantees; | |

| providing investment flexibility for the fund’s assets; | |

| meeting the regulatory capital requirements, which demonstrate solvency; |

| absorbing the costs of significant events, or fundamental changes in its long-term business without affecting bonus and investment policies. |

The size of the inherited estate fluctuates from year to year depending on the investment return and the extent to which it has been required to meet smoothing costs, guarantees and other events.

The Company believes that it would be beneficial if there were greater clarity as to the status of the inherited estate and therefore it has discussed with the Financial Services Authority (FSA) the principles that would apply to any re-attribution of the inherited estate. No conclusions have been reached. Furthermore, the Company expects that the entire inherited estate will need to be retained within the long-term fund for the foreseeable future to provide working capital and so it has not considered any distribution of the inherited estate to policyholders and shareholders.

GOING CONCERN

The directors consider that the Group has adequate resources to continue its operations for the foreseeable future. They therefore continue to use the going concern basis in preparing the financial statements.

PHILIP BROADLEY

GROUP FINANCE DIRECTOR

| PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 | 21 |

CORPORATE | A WORLD OF OPPORTUNITY |

| It’s about… being responsible | ACTING RESPONSIBLY BUILDS TRUST Our focus on acting responsibly and with integrity is not new. It is a philosophy that we have striven to incorporate within the way we work throughout our history. Responsible corporate behaviour is essential in maintaining successful relationships with, among others, our customers, our people and the communities around our business. Understanding our stakeholders’ needs today can also help us innovate in a way that creates both commercial and social future value. | |||

| INITIATIVES | |||||

| PROMOTING HEALTHY LIFESTYLES PruHealth, our private medical insurance joint venture that provides financial incentives for people to lead healthier lifestyles, was launched in 2004 in the UK. The more effort people make to improve their general levels of fitness, control their weight, stop smoking and maintain sensible levels of alcohol intake, the lower their premiums will be. The PruHealth model is based on similar schemes which have been established in South Africa and, more recently, in the US. In all these markets, there have been significant changes in people’s attitude and behaviour. For example, in Illinois, 79 per cent of policyholders took up a new fitness programme or changed their eating plan within 12 months of becoming a policyholder; this compares with a 32 per cent average among all policyholders. | |||||

| IMPROVING FINANCIAL CAPABILITY Given the increasing variety and complexity of financial products, there is an urgent need to provide financial education and we play an active role around the world in addressing this issue. Four years into our financial education programme, we are seeing significant progress. In the UK, via partnerships with charities such as Citizens Advice, thousands of adults and children are now benefiting. Last year, we extended our work to China. Already, about 1,000 women in 211 State Owned Enterprises in Beijing have graduated from Prudential Corporation Asia’s new Invest In Your Future programme. This draws on the skills of our female colleagues who understand the issues currently facing women in China. The programme has proved both popular and successful and we now intend to extend the initiative to elsewhere in China and into Vietnam. | |||||

INVESTING IN OUR COMMUNITIES | |||||

| 22 | PRUDENTIAL PLC ANNUAL REVIEW AND SUMMARY FINANCIAL STATEMENT 2004 |