UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-09995

| T. Rowe Price Global Technology Fund, Inc. |

| (Exact name of registrant as specified in charter) |

| 100 East Pratt Street, Baltimore, MD 21202 |

| (Address of principal executive offices) |

| David Oestreicher |

| 100 East Pratt Street, Baltimore, MD 21202 |

| (Name and address of agent for service) |

Registrant’s telephone number, including area code: (410) 345-2000

Date of fiscal year end: December 31

Date of reporting period: December 31, 2017

|

| Global Technology Fund | December 31, 2017 |

The views and opinions in this report were current as of December 31, 2017. They are not guarantees of performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the managers reserve the right to change their views about individual stocks, sectors, and the markets at any time. As a result, the views expressed should not be relied upon as a forecast of the fund’s future investment intent. The report is certified under the Sarbanes-Oxley Act, which requires mutual funds and other public companies to affirm that, to the best of their knowledge, the information in their financial reports is fairly and accurately stated in all material respects.

REPORTS ON THE WEB

Sign up for our Email Program, and you can begin to receive updated fund reports and prospectuses online rather than through the mail. Log in to your account at troweprice.com for more information.

Manager’s Letter

Fellow Shareholders

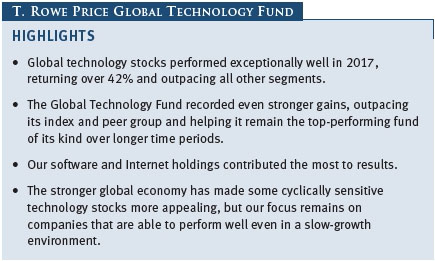

Global technology stocks led the market higher in a year of very strong global stock performance. Many leading global Internet platforms and other major tech firms continued to record robust earnings and revenue gains as they benefited from the heathy global economy while also seizing market share from slower-footed competitors. I am pleased to report that our concentrated investments in these firms, paired with our nimble and valuation-sensitive approach, helped us build on our strong record of relative and absolute performance. I should caution that investors should not expect such returns to be the norm, however, particularly given elevated valuations throughout much of the sector.

PERFORMANCE COMPARISON

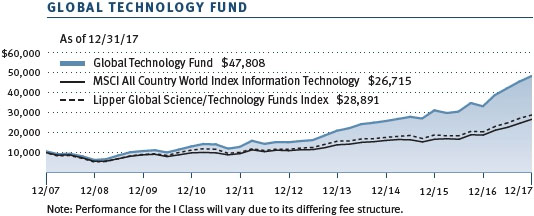

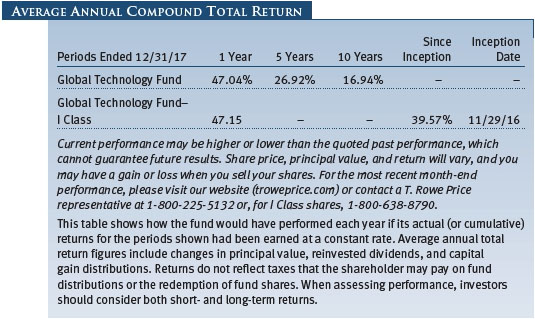

The Global Technology Fund returned 47.04% in the 12 months ended December 31, 2017. The fund outpaced the MSCI All Country World Index Information Technology and the Lipper Global Science/Technology Funds Index. (Performance for the I Class will vary due to its differing fee structure.) The fund continued to rank first among its peers over the longer-term time periods ended December 31, 2017. (Based on cumulative total return, Lipper ranked the Global Technology Fund 12 of 40, 1 of 37, 1 of 35, and 1 of 15 global science/technology funds for the 1-, 3-, 5-, and 10-year periods ended December 31, 2017, respectively. Past performance cannot guarantee future results.)

MARKET ENVIRONMENT

Markets in general benefited from a pickup in global growth, with all of the major developed economies expanding together for the first time since the initial recovery from the financial crisis nearly a decade ago. Investors were also encouraged by a more stable political situation in Europe, where pro-European Union parties prevailed in several closely watched elections. U.S. markets received a boost at the end of the year from the passage of tax reform, which included a steep reduction in corporate tax rates. Finally, monetary policy around the globe remained broadly supportive. The Federal Reserve raised rates three times but signaled it would continue to move slowly, while the European Central Bank and the Bank of Japan continued with massive asset purchases designed to keep longer-term interest rates very low or even near 0%, in Japan’s case.

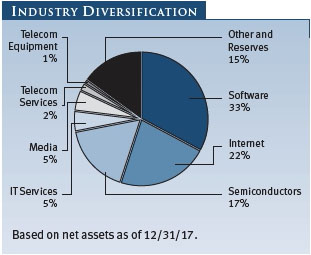

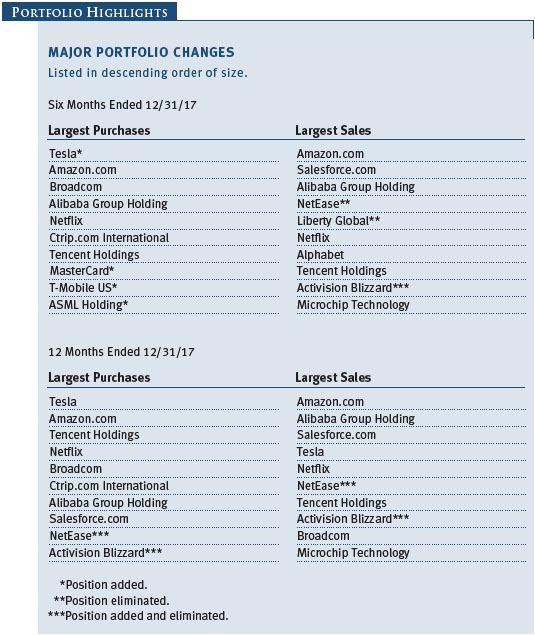

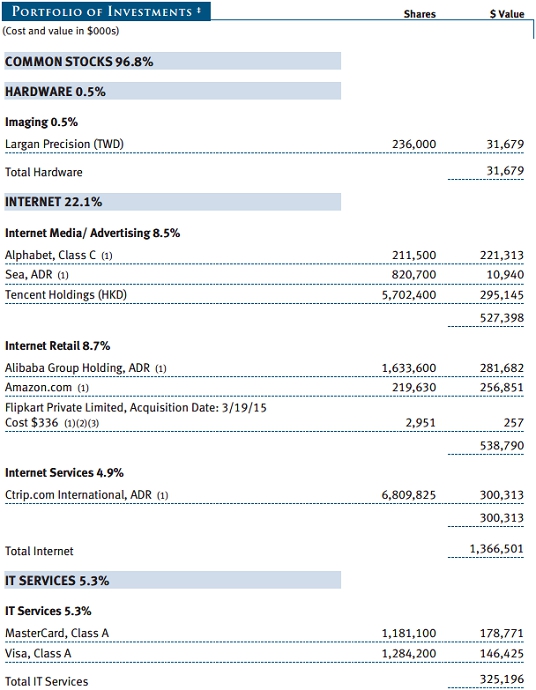

Global technology stocks performed exceptionally well in 2017, outpacing all other sectors in the broad MSCI index. Within the fund’s Lipper benchmark, Internet- and media-related shares performed especially well in 2017, rising roughly 74% and 55%, respectively. The heavily weighted software, semiconductor, and hardware segments performed generally in line with the benchmark, while the smaller services and telecom-related segments lagged. A notable phenomenon over the past year was the continued strong performance of the most highly valued technology firms, with a small group of companies adding over $1 trillion in market value during the year, according to some estimates. Moreover, at some point during 2017, as many as seven of the top 10 companies in terms of global market capitalization were technology firms. Finally, the year was notable for semiconductor maker Broadcom’s hostile bid for rival Qualcomm in November for $103 billion—if consummated, the acquisition would be the largest ever in the technology sector. (Please refer to the fund’s portfolio of investments for a complete list of holdings and the amount each represents in the portfolio.)

PORTFOLIO REVIEW

The fund saw strong gains from a wide range of its holdings over its fiscal year, with only a very small position in the hardware segment detracting from returns on an overall basis. Our significant holdings in the software industry contributed the most to returns, thanks in large part to our emphasis on so-called cloud-based providers, or those that provide services through the Internet rather than on systems installed on customers’ servers. Salesforce.com continued to benefit from its high-quality product portfolio, highly recurring subscription business model, and strong ecosystem. The stock performed well as the company released earnings showing growth that exceeded expectations. Human resources software maker Workday also performed well, making strides especially in its financials business.

We also benefited from holdings in traditional software firms that are making the transition to the cloud. Intuit is pursuing a software-as-a-service model, which we believe will lead to higher margins and revenues. Third-quarter earnings suggested encouraging progress, and we believe the company will benefit especially from tax reform. Microsoft also continues to transition to the cloud with Office 365 and its cloud services business, Azure. The stock performed well for us after Microsoft reported double-digit growth in the Office suite, as well as in server products and services. Gaming is also moving to the cloud, in a sense, in the form of digital downloads and in-game purchases. Electronic Arts performed well on the back of its sport franchises, although the company had a setback in November with the release of its new Star Wars game, which sparked a social media backlash because of the cost of its add-on content.

Our sole real disappointment in the software segment was a new investment in Twilio, which facilitates real-time communications between businesses and their customers. The stock plunged nearly 30% in early May after one of its leading customers, Uber, announced that it was going to both develop technology in-house and look at other vendors. Our willingness to move out of a stock quickly when our thesis is broken served us well, however, and we limited our losses by exiting our position by August.

The Internet remained a dominant and lucrative theme in the portfolio. We recorded strong gains from the two leading Internet retailers in the world, Amazon.com and China’s Alibaba Group Holding. Amazon continued to beat revenue expectations in its retail business while also seeing stellar growth in its cloud computing operation, Amazon Web Services. Alibaba surprised investors by continuing to grow revenues by roughly 60% while maintaining profit margins of nearly 40%—a remarkable achievement for a company of its size. Tencent Holdings, the dominant social platform in China, with over 900 million users, reported its strongest revenue growth in seven years, thanks primarily to impressive results in mobile gaming. We see significant opportunity for Tencent in other areas, including online payments, Internet finance, and subscription-based content. Alphabet, Google’s parent company, beat analyst expectations for advertising growth while also doing a better job of controlling expenses.

Our underweight in semiconductors detracted a bit from our relative performance, but we more than made up for this from stock selection in the segment. Our leading contributor was a new position in Taiwan Semiconductor Manufacturing. We believe the company will be the biggest beneficiary of booming demand for non-memory chips deployed for use in artificial intelligence and machine learning. ASML Holding, which provides equipment for the industry, performed well as it beat revenue estimates. We are optimistic that the company will achieve commercialization of extreme ultraviolet lithography (EUV) and become the foremost provider of leading-edge lithography tools. Broadcom rose after reporting strong quarterly results and guidance, and we are encouraged by its bid for Qualcomm, which could drive meaningful growth of the company. Conversely, Microsemi wavered as speculation that the company might be taken over faded and as quarterly results failed to surprise on the upside. We sold the last of our position in September. Analog semiconductor firm Analog Devices also detracted a bit, as did rival NXP Semiconductors, which we eliminated from the portfolio.

Within the media segment, Netflix rose sharply in July after reporting exceptionally strong subscriber gains in the previous quarter, overcoming historical seasonality with a content slate heavy on returning original hit shows. In the following quarter, the company reported particularly strong growth in international subscriptions, which have been rising at roughly a 40% annual pace. As viewership increases, we expect that Netflix’s content algorithms will further improve the customer experience, increasing Netflix’s negotiation leverage with content suppliers globally and helping it stave off the threat from regional competitors. We had less luck with our sole position in the mature cable and satellite industry, and we exited a poorly performing position in European cable operator Liberty Global.

The credit card industry has also been around for many years, but we are interested how established players are embracing technology and the transition to electronic payments. Visa performed well for us after reporting strong results in Europe, where it is enjoying higher revenues due to improved cross-border volume growth, increasing share of processed transactions, and improved pricing. MasterCard also sustained its recent strong performance in cross-border growth and reported steady market share gains.

OUTLOOK

I entered 2017 somewhat skeptical that the global economy would accelerate meaningfully in the coming year, which has left me pleasantly surprised by the pickup in global demand in recent months. Stronger growth in Europe and Japan has helped many of our holdings, and the massive Chinese market has remained stable even as policymakers have taken steps to rein in financial excesses. While growth in the U.S. has only picked up moderately to date, business confidence has improved sharply, likely thanks to deregulation and tax changes. A related acceleration in capital spending in late 2017 may pay off in faster growth in 2018.

The prospect of a better growth in the months ahead, fed in part by recent tax reform, has led our team to take a deeper look at some cyclical stocks. The opportunity for companies to repatriate cash could benefit large-cap legacy technology names that may deploy it in strategic mergers and acquisitions. The lower corporate tax rate is unlikely to have a substantial direct impact on technology companies, however, because most are global businesses that pay a mixture of foreign and U.S. taxes, resulting in relatively low effective rates. A secondary impact is possible, however, as companies that do see substantially lower rates increase investment in technology and other forms of capital spending. Indeed, many of tax reform’s biggest beneficiaries are the companies that are arguably most in need of investment in next-generation technologies.

Overall, valuations for technology companies are higher than their historical levels were in the last three to five years, and our sense is that the recent “melt-up” in the stock market has seen investors be less discriminating in bidding up stock prices. However, we do not believe that technology stocks are overvalued compared with the broader market, especially given their growth prospects relative to other industries that are facing disruptive headwinds. Within the sector, companies with durable growth records still properly trade at higher valuations versus slower-growing, legacy technology companies.

The heightened valuations have made it harder to find compelling new investment opportunities in recent months, especially as we have not experienced a significant pullback that presents a broad buying opportunity—as last happened in early 2016. Nonetheless, I am optimistic that we will see chances in the coming year to add to holdings or renew positions where temporary missteps or factors cause valuations to overshoot on the downside. I am pleased to work with a talented team of industry-specific analysts in Baltimore, San Francisco, London, Hong Kong, and elsewhere in pursuit of such opportunities, and I look forward to reporting to you again on our efforts in six months.

Respectfully submitted,

Joshua K. Spencer

President of the fund and chairman of its Investment Advisory Committee

January 22, 2018

The committee chairman has day-to-day responsibility for managing the portfolio and works with committee members in developing and executing the fund’s investment program.

RISKS OF INVESTING IN THE FUND

Funds that invest only in specific industries will experience greater volatility than funds investing in a broad range of industries. Technology stocks have historically experienced unusually wide price swings, both up and down. The potential for wide variation in performance reflects the special risks common to companies in the rapidly changing field of technology. For example, products or services that at first appear promising may not prove commercially successful and may become obsolete quickly. Earnings disappointments and intense competition for market share can result in sharp price declines.

GLOSSARY

Lipper Global Science/Technology Funds Index: An index of returns for specified periods of funds that invest in technology companies around the world as tracked by Lipper Inc.

MSCI All Country World Index Information Technology: An index that tracks information technology stocks in developed and emerging markets.

Note: MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed, or produced by MSCI.

Performance and Expenses

| Growth of $10,000 |

This chart shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds lacking 10-year records). The result is compared with benchmarks, which may include a broad-based market index and a peer group average or index. Market indexes do not include expenses, which are deducted from fund returns as well as mutual fund averages and indexes.

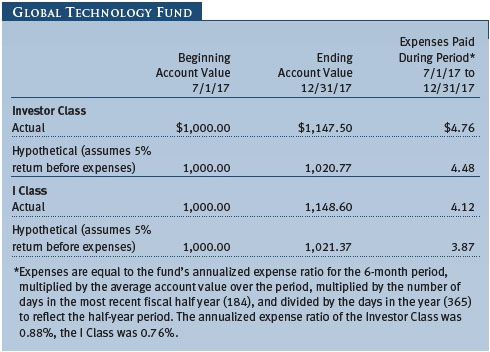

| Fund Expense Example |

As a mutual fund shareholder, you may incur two types of costs: (1) transaction costs, such as redemption fees or sales loads, and (2) ongoing costs, including management fees, distribution and service (12b-1) fees, and other fund expenses. The following example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the most recent six-month period and held for the entire period.

Please note that the fund has two share classes: The original share class (Investor Class) charges no distribution and service (12b-1) fee, and the I Class shares are also available to institutionally oriented clients and impose no 12b-1 or administrative fee payment. Each share class is presented separately in the table.

Actual Expenses

The first line of the following table (Actual) provides information about actual account values and expenses based on the fund’s actual returns. You may use the information on this line, together with your account balance, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number on the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The information on the second line of the table (Hypothetical) is based on hypothetical account values and expenses derived from the fund’s actual expense ratio and an assumed 5% per year rate of return before expenses (not the fund’s actual return). You may compare the ongoing costs of investing in the fund with other funds by contrasting this 5% hypothetical example and the 5% hypothetical examples that appear in the shareholder reports of the other funds. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

Note: T. Rowe Price charges an annual account service fee of $20, generally for accounts with less than $10,000. The fee is waived for any investor whose T. Rowe Price mutual fund accounts total $50,000 or more; accounts electing to receive electronic delivery of account statements, transaction confirmations, prospectuses, and shareholder reports; or accounts of an investor who is a T. Rowe Price Personal Services or Enhanced Personal Services client (enrollment in these programs generally requires T. Rowe Price assets of at least $250,000). This fee is not included in the accompanying table. If you are subject to the fee, keep it in mind when you are estimating the ongoing expenses of investing in the fund and when comparing the expenses of this fund with other funds.

You should also be aware that the expenses shown in the table highlight only your ongoing costs and do not reflect any transaction costs, such as redemption fees or sales loads. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. To the extent a fund charges transaction costs, however, the total cost of owning that fund is higher.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

| Notes to Financial Statements |

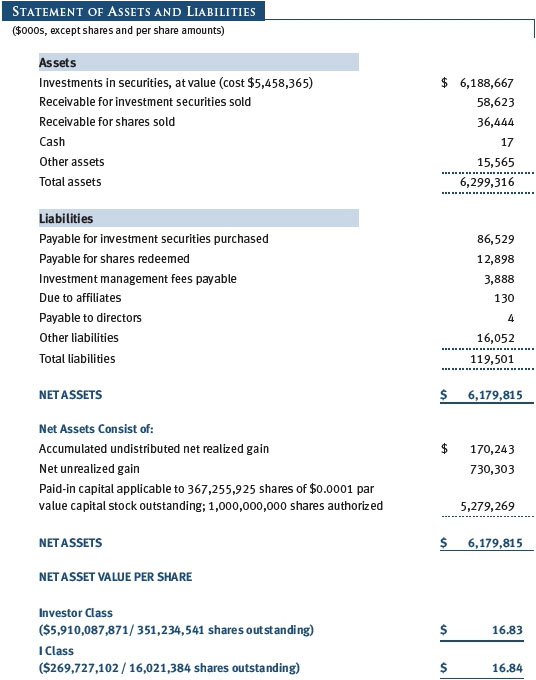

T. Rowe Price Global Technology Fund, Inc. (the fund) is registered under the Investment Company Act of 1940 (the 1940 Act) as a diversified, open-end management investment company. The fund seeks to provide long-term capital growth. The fund has two classes of shares: the Global Technology Fund (Investor Class) and the Global Technology Fund–I Class (I Class). I Class shares generally are available only to investors meeting a $1,000,000 minimum investment or certain other criteria. Each class has exclusive voting rights on matters related solely to that class; separate voting rights on matters that relate to both classes; and, in all other respects, the same rights and obligations as the other class.

NOTE 1 - SIGNIFICANT ACCOUNTING POLICIES

Basis of Preparation The fund is an investment company and follows accounting and reporting guidance in the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946 (ASC 946). The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America (GAAP), including, but not limited to, ASC 946. GAAP requires the use of estimates made by management. Management believes that estimates and valuations are appropriate; however, actual results may differ from those estimates, and the valuations reflected in the accompanying financial statements may differ from the value ultimately realized upon sale or maturity.

Investment Transactions, Investment Income, and Distributions Investment transactions are accounted for on the trade date basis. Income and expenses are recorded on the accrual basis. Realized gains and losses are reported on the identified cost basis. Dividends received from mutual fund investments are reflected as dividend income; capital gain distributions are reflected as realized gain/loss. Dividend income and capital gain distributions are recorded on the ex-dividend date. Income tax-related interest and penalties, if incurred, are recorded as income tax expense. Income distributions are declared and paid by each class annually. Distributions to shareholders are recorded on the ex-dividend date. A capital gain distribution may also be declared and paid by the fund annually.

Currency Translation Assets, including investments, and liabilities denominated in foreign currencies are translated into U.S. dollar values each day at the prevailing exchange rate, using the mean of the bid and asked prices of such currencies against U.S. dollars as quoted by a major bank. Purchases and sales of securities, income, and expenses are translated into U.S. dollars at the prevailing exchange rate on the respective date of such transaction. The portion of the results of operations attributable to changes in foreign exchange rates on investments is not bifurcated from the portion attributable to changes in market prices. The effect of changes in foreign currency exchange rates on realized and unrealized security gains and losses is reflected as a component of security gains and losses.

Class Accounting Shareholder servicing, prospectus, and shareholder report expenses incurred by each class are charged directly to the class to which they relate. Expenses common to both classes, investment income, and realized and unrealized gains and losses are allocated to the classes based upon the relative daily net assets of each class. To the extent any expenses are waived or reimbursed in accordance with an expense limitation (see Note 6), the waiver or reimbursement is charged to the applicable class or allocated across the classes in the same manner as the related expense.

Rebates Subject to best execution, the fund may direct certain security trades to brokers who have agreed to rebate a portion of the related brokerage commission to the fund in cash. Commission rebates are reflected as realized gain on securities in the accompanying financial statements and totaled $186,000 for the year ended December 31, 2017.

New Accounting Guidance In March 2017, the FASB issued amended guidance to shorten the amortization period for certain callable debt securities, held at a premium. The guidance is effective for fiscal years and interim periods beginning after December 15, 2018. Adoption will have no effect on the fund’s net assets or results of operations.

On August 1, 2017, the fund implemented amendments to Regulation S-X, issued by the Securities and Exchange Commission, which require standardized, enhanced disclosures, particularly related to derivatives, in investment company financial statements. Adoption had no effect on the fund’s net assets or results of operations.

Indemnification In the normal course of business, the fund may provide indemnification in connection with its officers and directors, service providers, and/or private company investments. The fund’s maximum exposure under these arrangements is unknown; however, the risk of material loss is currently considered to be remote.

NOTE 2 - VALUATION

The fund’s financial instruments are valued and each class’s net asset value (NAV) per share is computed at the close of the New York Stock Exchange (NYSE), normally 4 p.m. ET, each day the NYSE is open for business. However, the NAV per share may be calculated at a time other than the normal close of the NYSE if trading on the NYSE is restricted, if the NYSE closes earlier, or as may be permitted by the SEC.

Fair Value The fund’s financial instruments are reported at fair value, which GAAP defines as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The T. Rowe Price Valuation Committee (the Valuation Committee) is an internal committee that has been delegated certain responsibilities by the fund’s Board of Directors (the Board) to ensure that financial instruments are appropriately priced at fair value in accordance with GAAP and the 1940 Act. Subject to oversight by the Board, the Valuation Committee develops and oversees pricing-related policies and procedures and approves all fair value determinations. Specifically, the Valuation Committee establishes procedures to value securities; determines pricing techniques, sources, and persons eligible to effect fair value pricing actions; oversees the selection, services, and performance of pricing vendors; oversees valuation-related business continuity practices; and provides guidance on internal controls and valuation-related matters. The Valuation Committee reports to the Board and has representation from legal, portfolio management and trading, operations, risk management, and the fund’s treasurer.

Various valuation techniques and inputs are used to determine the fair value of financial instruments. GAAP establishes the following fair value hierarchy that categorizes the inputs used to measure fair value:

Level 1 – quoted prices (unadjusted) in active markets for identical financial instruments that the fund can access at the reporting date

Level 2 – inputs other than Level 1 quoted prices that are observable, either directly or indirectly (including, but not limited to, quoted prices for similar financial instruments in active markets, quoted prices for identical or similar financial instruments in inactive markets, interest rates and yield curves, implied volatilities, and credit spreads)

Level 3 – unobservable inputs

Observable inputs are developed using market data, such as publicly available information about actual events or transactions, and reflect the assumptions that market participants would use to price the financial instrument. Unobservable inputs are those for which market data are not available and are developed using the best information available about the assumptions that market participants would use to price the financial instrument. GAAP requires valuation techniques to maximize the use of relevant observable inputs and minimize the use of unobservable inputs. When multiple inputs are used to derive fair value, the financial instrument is assigned to the level within the fair value hierarchy based on the lowest-level input that is significant to the fair value of the financial instrument. Input levels are not necessarily an indication of the risk or liquidity associated with financial instruments at that level but rather the degree of judgment used in determining those values.

Valuation Techniques Equity securities listed or regularly traded on a securities exchange or in the over-the-counter (OTC) market are valued at the last quoted sale price or, for certain markets, the official closing price at the time the valuations are made. OTC Bulletin Board securities are valued at the mean of the closing bid and asked prices. A security that is listed or traded on more than one exchange is valued at the quotation on the exchange determined to be the primary market for such security. Listed securities not traded on a particular day are valued at the mean of the closing bid and asked prices for domestic securities and the last quoted sale or closing price for international securities.

For valuation purposes, the last quoted prices of non-U.S. equity securities may be adjusted to reflect the fair value of such securities at the close of the NYSE. If the fund determines that developments between the close of a foreign market and the close of the NYSE will affect the value of some or all of its portfolio securities, the fund will adjust the previous quoted prices to reflect what it believes to be the fair value of the securities as of the close of the NYSE. In deciding whether it is necessary to adjust quoted prices to reflect fair value, the fund reviews a variety of factors, including developments in foreign markets, the performance of U.S. securities markets, and the performance of instruments trading in U.S. markets that represent foreign securities and baskets of foreign securities. The fund may also fair value securities in other situations, such as when a particular foreign market is closed but the fund is open. The fund uses outside pricing services to provide it with quoted prices and information to evaluate or adjust those prices. The fund cannot predict how often it will use quoted prices and how often it will determine it necessary to adjust those prices to reflect fair value. As a means of evaluating its security valuation process, the fund routinely compares quoted prices, the next day’s opening prices in the same markets, and adjusted prices.

Actively traded equity securities listed on a domestic exchange generally are categorized in Level 1 of the fair value hierarchy. Non-U.S. equity securities generally are categorized in Level 2 of the fair value hierarchy despite the availability of quoted prices because, as described above, the fund evaluates and determines whether those quoted prices reflect fair value at the close of the NYSE or require adjustment. OTC Bulletin Board securities, certain preferred securities, and equity securities traded in inactive markets generally are categorized in Level 2 of the fair value hierarchy.

Investments in mutual funds are valued at the mutual fund’s closing NAV per share on the day of valuation and are categorized in Level 1 of the fair value hierarchy. Assets and liabilities other than financial instruments, including short-term receivables and payables, are carried at cost, or estimated realizable value, if less, which approximates fair value.

Thinly traded financial instruments and those for which the above valuation procedures are inappropriate or are deemed not to reflect fair value are stated at fair value as determined in good faith by the Valuation Committee. The objective of any fair value pricing determination is to arrive at a price that could reasonably be expected from a current sale. Financial instruments fair valued by the Valuation Committee are primarily private placements, restricted securities, warrants, rights, and other securities that are not publicly traded.

Subject to oversight by the Board, the Valuation Committee regularly makes good faith judgments to establish and adjust the fair valuations of certain securities as events occur and circumstances warrant. For instance, in determining the fair value of an equity investment with limited market activity, such as a private placement or a thinly traded public company stock, the Valuation Committee considers a variety of factors, which may include, but are not limited to, the issuer’s business prospects, its financial standing and performance, recent investment transactions in the issuer, new rounds of financing, negotiated transactions of significant size between other investors in the company, relevant market valuations of peer companies, strategic events affecting the company, market liquidity for the issuer, and general economic conditions and events. In consultation with the investment and pricing teams, the Valuation Committee will determine an appropriate valuation technique based on available information, which may include both observable and unobservable inputs. The Valuation Committee typically will afford greatest weight to actual prices in arm’s length transactions, to the extent they represent orderly transactions between market participants, transaction information can be reliably obtained, and prices are deemed representative of fair value. However, the Valuation Committee may also consider other valuation methods such as market-based valuation multiples; a discount or premium from market value of a similar, freely traded security of the same issuer; or some combination. Fair value determinations are reviewed on a regular basis and updated as information becomes available, including actual purchase and sale transactions of the issue. Because any fair value determination involves a significant amount of judgment, there is a degree of subjectivity inherent in such pricing decisions, and fair value prices determined by the Valuation Committee could differ from those of other market participants. Depending on the relative significance of unobservable inputs, including the valuation technique(s) used, fair valued securities may be categorized in Level 2 or 3 of the fair value hierarchy.

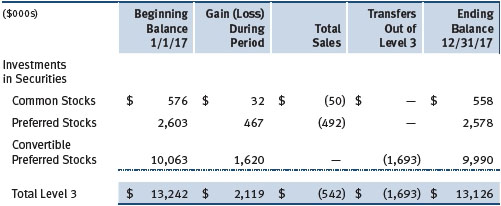

Valuation Inputs The following table summarizes the fund’s financial instruments, based on the inputs used to determine their fair values on December 31, 2017:

There were no material transfers between Levels 1 and 2 during the year ended December 31, 2017.

Following is a reconciliation of the fund’s Level 3 holdings for the year ended December 31, 2017. Gain (loss) reflects both realized and change in unrealized gain/loss on Level 3 holdings during the period, if any, and is included on the accompanying Statement of Operations. The change in unrealized gain/loss on Level 3 instruments held at December 31, 2017, totaled $2,183,000 for the year ended December 31, 2017. Transfers into and out of Level 3 are reflected at the value of the financial instrument at the beginning of the period. During the year, transfers out of Level 3 were because observable market data became available for the security.

NOTE 3 - OTHER INVESTMENT TRANSACTIONS

Consistent with its investment objective, the fund engages in the following practices to manage exposure to certain risks and/or to enhance performance. The investment objective, policies, program, and risk factors of the fund are described more fully in the fund’s prospectus and Statement of Additional Information.

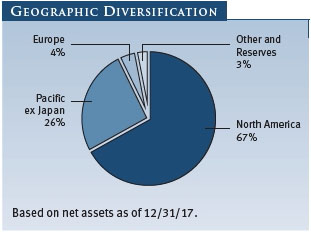

Emerging Markets The fund may invest, either directly or through investments in T. Rowe Price institutional funds, in securities of companies located in, issued by governments of, or denominated in or linked to the currencies of emerging market countries; at period-end, approximately 19% of the fund’s net assets were invested in emerging markets. Emerging markets generally have economic structures that are less diverse and mature, and political systems that are less stable, than developed countries. These markets may be subject to greater political, economic, and social uncertainty and differing regulatory environments that may potentially impact the fund’s ability to buy or sell certain securities or repatriate proceeds to U.S. dollars. Such securities are often subject to greater price volatility, less liquidity, and higher rates of inflation than U.S. securities.

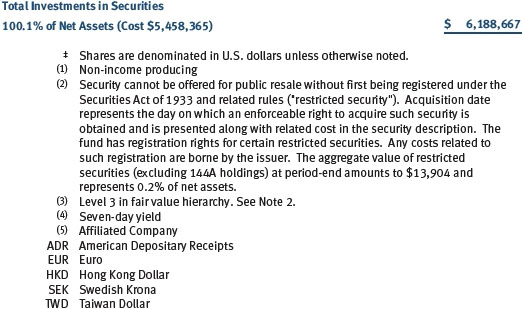

Restricted Securities The fund may invest in securities that are subject to legal or contractual restrictions on resale. Prompt sale of such securities at an acceptable price may be difficult and may involve substantial delays and additional costs.

Other Purchases and sales of portfolio securities other than short-term securities aggregated $10,563,484,000 and $9,447,575,000, respectively, for the year ended December 31, 2017.

NOTE 4 - FEDERAL INCOME TAXES

No provision for federal income taxes is required since the fund intends to continue to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and distribute to shareholders all of its taxable income and gains. Distributions determined in accordance with federal income tax regulations may differ in amount or character from net investment income and realized gains for financial reporting purposes. Financial reporting records are adjusted for permanent book/tax differences to reflect tax character but are not adjusted for temporary differences.

The fund files U.S. federal, state, and local tax returns as required. The fund’s tax returns are subject to examination by the relevant tax authorities until expiration of the applicable statute of limitations, which is generally three years after the filing of the tax return but which can be extended to six years in certain circumstances. Tax returns for open years have incorporated no uncertain tax positions that require a provision for income taxes.

Reclassifications to paid-in capital relate primarily to a tax practice that treats a portion of the proceeds from each redemption of capital shares as a distribution of taxable net investment income or realized capital gain. Reclassifications between income and gain relate primarily to the offset of the current net operating loss against realized gains. For the year ended December 31. 2017, the following reclassifications were recorded to reflect tax character (there was no impact on results of operations or net assets):

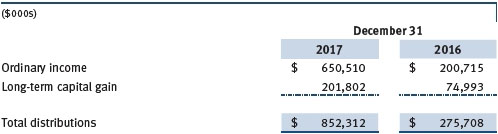

Distributions during the years ended December 31, 2017 and December 31, 2016, were characterized for tax purposes as follows:

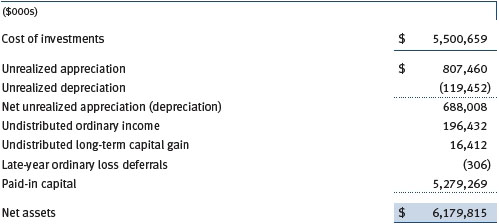

At December 31, 2017, the tax-basis cost of investments, including derivatives, and components of net assets were as follows:

The difference between book-basis and tax-basis net unrealized appreciation (depreciation) is attributable to the deferral of losses from wash sales for tax purposes. During the year ended December 31, 2017, the fund utilized $18,379,000 of capital loss carryforwards. In accordance with federal tax laws applicable to investment companies, net specified losses realized between November 1 and December 31 are not recognized for tax purposes until the subsequent year (late-year ordinary loss deferrals); however, such losses are recognized for financial reporting purposes in the year realized.

NOTE 5 - FOREIGN TAXES

The fund is subject to foreign income taxes imposed by certain countries in which it invests. Additionally, certain foreign currency transactions are subject to tax, and capital gains realized upon disposition of securities issued in or by certain foreign countries are subject to capital gains tax imposed by those countries. All taxes are computed in accordance with the applicable foreign tax law, and, to the extent permitted, capital losses are used to offset capital gains. Taxes attributable to income are accrued by the fund as a reduction of income. Taxes incurred on the purchase of foreign currencies are recorded as realized loss on foreign currency transactions. Current and deferred tax expense attributable to capital gains is reflected as a component of realized or change in unrealized gain/loss on securities in the accompanying financial statements. At December 31, 2017, the fund had no deferred tax liability attributable to foreign securities and $2,381,000 of foreign capital loss carryforwards, including $28,000 that expire in 2020 and $2,353,000 that expire in 2023.

NOTE 6 - RELATED PARTY TRANSACTIONS

The fund is managed by T. Rowe Price Associates, Inc. (Price Associates), a wholly owned subsidiary of T. Rowe Price Group, Inc. (Price Group). The investment management agreement between the fund and Price Associates provides for an annual investment management fee, which is computed daily and paid monthly. The fee consists of an individual fund fee, equal to 0.45% of the fund’s average daily net assets, and a group fee. The group fee rate is calculated based on the combined net assets of certain mutual funds sponsored by Price Associates (the group) applied to a graduated fee schedule, with rates ranging from 0.48% for the first $1 billion of assets to 0.265% for assets in excess of $650 billion. The fund’s group fee is determined by applying the group fee rate to the fund’s average daily net assets. At December 31, 2017, the effective annual group fee rate was 0.29%.

The I Class is subject to an operating expense limitation (I Class limit) pursuant to which Price Associates is contractually required to pay all operating expenses of the I Class, excluding management fees, interest, expenses related to borrowings, taxes, brokerage, and other non-recurring expenses permitted by the investment management agreement, to the extent such operating expenses, on an annualized basis, exceed 0.05% of average net assets. This agreement will continue until April 30, 2019, and may be renewed, revised, or revoked only with approval of the fund’s Board. The I Class is required to repay Price Associates for expenses previously paid to the extent the class’s net assets grow or expenses decline sufficiently to allow repayment without causing the class’s operating expenses (after the repayment is taken into account) to exceed both: (1) the expense limitation in place at the time such amounts were paid; and (2) the class’s current expense limitation. However, no repayment will be made more than three years after the date of a payment or waiver. For the year ended December 31, 2017, the I Class operated below its expense limitation.

In addition, the fund has entered into service agreements with Price Associates and two wholly owned subsidiaries of Price Associates (collectively, Price). Price Associates provides certain accounting and administrative services to the fund. T. Rowe Price Services, Inc. provides shareholder and administrative services in its capacity as the fund’s transfer and dividend-disbursing agent. T. Rowe Price Retirement Plan Services, Inc. provides subaccounting and recordkeeping services for certain retirement accounts invested in the Investor Class and I Class. For the year ended December 31, 2017, expenses incurred pursuant to these service agreements were $86,000 for Price Associates; $1,593,000 for T. Rowe Price Services, Inc.; and $163,000 for T. Rowe Price Retirement Plan Services, Inc. The total amount payable at period-end pursuant to these service agreements is reflected as Due to Affiliates in the accompanying financial statements.

The fund may invest its cash reserves in certain open-end management investment companies managed by Price Associates and considered affiliates of the fund: the T. Rowe Price Government Reserve Fund or the T. Rowe Price Treasury Reserve Fund, organized as money market funds, or the T. Rowe Price Short-Term Fund, a short-term bond fund (collectively, the Price Reserve Funds). The Price Reserve Funds are offered as short-term investment options to mutual funds, trusts, and other accounts managed by Price Associates or its affiliates and are not available for direct purchase by members of the public. Cash collateral from securities lending is invested in the T. Rowe Price Short-Term Fund. The Price Reserve Funds pay no investment management fees.

The fund may participate in securities purchase and sale transactions with other funds or accounts advised by Price Associates (cross trades), in accordance with procedures adopted by the fund’s Board and Securities and Exchange Commission rules, which require, among other things, that such purchase and sale cross trades be effected at the independent current market price of the security. Purchases and sales cross trades aggregated $44,552,000 and $20,495,000, respectively, with net realized loss of $1,483,000 for the year ended December 31, 2017.

| Report of Independent Registered Public Accounting Firm |

To the Board of Directors and Shareholders of

T. Rowe Price Global Technology Fund, Inc.

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities, including the portfolio of investments, of T. Rowe Price Global Technology Fund, Inc. (the “Fund”) as of December 31, 2017, the related statement of operations for the year ended December 31, 2017, the statement of changes in net assets for each of the two years in the period ended December 31, 2017, including the related notes, and the financial highlights for each of the periods indicated therein (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of December 31, 2017, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period ended December 31, 2017 and the financial highlights for each of the periods indicated therein, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits of these financial statements in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. Our procedures included confirmation of securities owned as of December 31, 2017 by correspondence with the custodians, transfer agent and brokers; when replies were not received from brokers, we performed other auditing procedures. We believe that our audits provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Baltimore, Maryland

February 15, 2018

We have served as the auditor of one or more investment companies in the T. Rowe Price group of investment companies since 1973.

| Tax Information for the Tax Year Ended 12/31/17 |

We are providing this information as required by the Internal Revenue Code. The amounts shown may differ from those elsewhere in this report because of differences between tax and financial reporting requirements.

The fund’s distributions to shareholders included:

| ● | $719,094,000 from short-term capital gains, |

| ● | $227,813,000 from long-term capital gains, subject to a long-term capital gains tax rate of not greater than 20%. |

For taxable non-corporate shareholders, $12,912,000 of the fund’s income represents qualified dividend income subject to a long-term capital gains tax rate of not greater than 20%.

For corporate shareholders, $6,441,000 of the fund’s income qualifies for the dividends-received deduction.

| Information on Proxy Voting Policies, Procedures, and Records |

A description of the policies and procedures used by T. Rowe Price funds and portfolios to determine how to vote proxies relating to portfolio securities is available in each fund’s Statement of Additional Information. You may request this document by calling 1-800-225-5132 or by accessing the SEC’s website, sec.gov.

The description of our proxy voting policies and procedures is also available on our corporate website. To access it, please visit the following Web page:

https://www3.troweprice.com/usis/corporate/en/utility/policies.html

Scroll down to the section near the bottom of the page that says, “Proxy Voting Policies.” Click on the Proxy Voting Policies link in the shaded box.

Each fund’s most recent annual proxy voting record is available on our website and through the SEC’s website. To access it through T. Rowe Price, visit the website location shown above, and scroll down to the section near the bottom of the page that says, “Proxy Voting Records.” Click on the Proxy Voting Records link in the shaded box.

| How to Obtain Quarterly Portfolio Holdings |

The fund files a complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year on Form N-Q. The fund’s Form N-Q is available electronically on the SEC’s website (sec.gov); hard copies may be reviewed and copied at the SEC’s Public Reference Room, 100 F St. N.E., Washington, DC 20549. For more information on the Public Reference Room, call 1-800-SEC-0330.

| About the Fund’s Directors and Officers |

Your fund is overseen by a Board of Directors (Board) that meets regularly to review a wide variety of matters affecting or potentially affecting the fund, including performance, investment programs, compliance matters, advisory fees and expenses, service providers, and business and regulatory affairs. The Board elects the fund’s officers, who are listed in the final table. At least 75% of the Board’s members are independent of T. Rowe Price Associates, Inc. (T. Rowe Price), and its affiliates; “inside” or “interested” directors are employees or officers of T. Rowe Price. The business address of each director and officer is 100 East Pratt Street, Baltimore, Maryland 21202. The Statement of Additional Information includes additional information about the fund directors and is available without charge by calling a T. Rowe Price representative at 1-800-638-5660.

| Independent Directors | ||

| Name | ||

| (Year of Birth) | ||

| Year Elected* | ||

| [Number of T. Rowe Price | Principal Occupation(s) and Directorships of Public Companies and | |

| Portfolios Overseen] | Other Investment Companies During the Past Five Years | |

| Bruce W. Duncan | Chief Executive Officer and Director (2009 to December 2016), | |

| (1951) | Chairman of the Board (January 2016 to present), and President | |

| 2013 | (2009 to September 2016), First Industrial Realty Trust, an owner | |

| [191] | and operator of industrial properties; Chairman of the Board | |

| (2005 to September 2016) and Director (1999 to September | ||

| 2016), Starwood Hotels & Resorts, a hotel and leisure company; | ||

| Director, Boston Properties (May 2016 to present); Director, Marriott | ||

| International, Inc. (September 2016 to present) | ||

| Robert J. Gerrard, Jr. | Advisory Board Member, Pipeline Crisis/Winning Strategies, a | |

| (1952) | collaborative working to improve opportunities for young African | |

| 2012 | Americans (1997 to present) | |

| [191] | ||

| Paul F. McBride | Advisory Board Member, Vizzia Technologies (2015 to present) | |

| (1956) | ||

| 2013 | ||

| [191] | ||

| Cecilia E. Rouse, Ph.D. | Dean, Woodrow Wilson School (2012 to present); Professor and | |

| (1963) | Researcher, Princeton University (1992 to present); Member of | |

| 2012 | National Academy of Education (2010 to present); Director, MDRC, | |

| [191] | a nonprofit education and social policy research organization (2011 | |

| to present); Research Associate of Labor Studies Program (2011 | ||

| to 2015) and Board Member (2015 to present), National Bureau | ||

| of Economic Research (2011 to present); Chair of Committee | ||

| on the Status of Minority Groups in the Economic Profession | ||

| (2012 to present); Vice President (2015 to present), American | ||

| Economic Association | ||

| John G. Schreiber | Owner/President, Centaur Capital Partners, Inc., a real estate | |

| (1946) | investment company (1991 to present); Cofounder, Partner, and | |

| 2001 | Cochairman of the Investment Committee, Blackstone Real Estate | |

| [191] | Advisors, L.P. (1992 to 2015); Director, General Growth Properties, | |

| Inc. (2010 to 2013); Director, Blackstone Mortgage Trust, a real | ||

| estate finance company (2012 to 2016); Director and Chairman of | ||

| the Board, Brixmor Property Group, Inc. (2013 to present); Director, | ||

| Hilton Worldwide (2013 to present); Director, Hudson Pacific | ||

| Properties (2014 to 2016) | ||

| Mark R. Tercek | President and Chief Executive Officer, The Nature Conservancy | |

| (1957) | (2008 to present) | |

| 2009 | ||

| [191] | ||

| *Each independent director serves until retirement, resignation, or election of a successor. | ||

| Inside Directors | ||

| Name | ||

| (Year of Birth) | ||

| Year Elected* | ||

| [Number of T. Rowe Price | Principal Occupation(s) and Directorships of Public Companies and | |

| Portfolios Overseen] | Other Investment Companies During the Past Five Years | |

| Edward C. Bernard | Director and Vice President, T. Rowe Price; Vice Chairman of the | |

| (1956) | Board, Director, and Vice President, T. Rowe Price Group, Inc.; | |

| 2006 | Chairman of the Board, Director, and Vice President, T. Rowe Price | |

| [191] | Investment Services, Inc., and T. Rowe Price Services, Inc.; Chairman | |

| of the Board and Director, T. Rowe Price Retirement Plan Services, | ||

| Inc.; Chairman of the Board, Chief Executive Officer, Director, and | ||

| President, T. Rowe Price International and T. Rowe Price Trust | ||

| Company; Chairman of the Board, all funds | ||

| Robert W. Sharps, CFA, CPA** | Vice President, T. Rowe Price, T. Rowe Price Group, Inc., and T. Rowe | |

| (1971) | Price Trust Company | |

| 2017 | ||

| [135] | ||

| *Each inside director serves until retirement, resignation, or election of a successor. | ||

| **Effective April 1, 2017, Brian C. Rogers was replaced by Robert W. Sharps as an inside director of certain Price Funds. | ||

| Officers | ||

| Name (Year of Birth) | ||

| Position Held With Global Technology Fund | Principal Occupation(s) | |

| Kennard W. Allen (1977) | Vice President, T. Rowe Price and T. Rowe Price | |

| Vice President | Group, Inc. | |

| Darrell N. Braman (1963) | Vice President, Price Hong Kong, Price | |

| Vice President and Secretary | Singapore, T. Rowe Price, T. Rowe Price Group, | |

| Inc., T. Rowe Price International, T. Rowe Price | ||

| Investment Services, Inc., and T. Rowe Price | ||

| Services, Inc. | ||

| Christopher W. Carlson (1967) | Vice President, T. Rowe Price and T. Rowe Price | |

| Vice President | Group, Inc. | |

| Gregory Dunham, CFA (1974) | Vice President, T. Rowe Price and T. Rowe | |

| Vice President | Price Group; formerly, Analyst, Goldman Sachs | |

| (to 2015) | ||

| David J. Eiswert, CFA (1972) | Vice President, T. Rowe Price, T. Rowe Price | |

| Vice President | Group, Inc., and T. Rowe Price International | |

| Henry M. Ellenbogen (1973) | Vice President, T. Rowe Price, T. Rowe Price | |

| Vice President | Group, Inc., and T. Rowe Price Trust Company | |

| John R. Gilner (1961) | Chief Compliance Officer and Vice President, | |

| Chief Compliance Officer | T. Rowe Price; Vice President, T. Rowe Price | |

| Group, Inc., and T. Rowe Price Investment | ||

| Services, Inc. | ||

| Paul D. Greene II (1978) | Vice President, T. Rowe Price and T. Rowe Price | |

| Vice President | Group, Inc. | |

| Paul J. Krug, CPA (1964) | Vice President, T. Rowe Price, T. Rowe Price | |

| Vice President | Group, Inc., and T. Rowe Price Trust Company | |

| Jacqueline L. Liu (1979) | Vice President, Price Hong Kong and T. Rowe | |

| Vice President | Price Group, Inc.; formerly, Investment Analyst, | |

| Fidelity International Hong Kong Limited | ||

| (to 2014) | ||

| Jennifer Martin (1972) | Vice President, T. Rowe Price and T. Rowe Price | |

| Vice President | Group, Inc. | |

| Catherine D. Mathews (1963) | Vice President, T. Rowe Price, T. Rowe Price | |

| Treasurer and Vice President | Group, Inc., and T. Rowe Price Trust Company | |

| Heather K. McPherson, CPA (1967) | Vice President, T. Rowe Price and T. Rowe Price | |

| Vice President | Group, Inc. | |

| Tobias F. Mueller (1980) | Vice President, T. Rowe Price Group, Inc., and | |

| Vice President | T. Rowe Price International | |

| David Oestreicher (1967) | Director, Vice President, and Secretary, T. Rowe | |

| Vice President | Price Investment Services, Inc., T. Rowe Price | |

| Retirement Plan Services, Inc., T. Rowe | ||

| Price Services, Inc., and T. Rowe Price Trust | ||

| Company; Chief Legal Officer, Vice President, | ||

| and Secretary, T. Rowe Price Group, Inc.; Vice | ||

| President and Secretary, T. Rowe Price and | ||

| T. Rowe Price International; Vice President, | ||

| Price Hong Kong and Price Singapore | ||

| John W. Ratzesberger (1975) | Vice President, T. Rowe Price, T. Rowe Price | |

| Vice President | Group, Inc., and T. Rowe Price Trust Company; | |

| formerly, North American Head of Listed | ||

| Derivatives Operation, Morgan Stanley | ||

| (to 2013) | ||

| Shannon H. Rauser (1987) | Employee, T. Rowe Price | |

| Assistant Secretary | ||

| Corey D. Shull, CFA (1983) | Vice President, T. Rowe Price and T. Rowe Price | |

| Vice President | Group, Inc. | |

| Joshua K. Spencer, CFA (1973) | Vice President, T. Rowe Price and T. Rowe Price | |

| President | Group, Inc. | |

| Alan Tu (1985) | Vice President, T. Rowe Price and T. Rowe Price | |

| Vice President | Group, Inc.; formerly, student, University of | |

| Chicago Booth School of Business (to 2014); | ||

| intern, T. Rowe Price (to 2013) | ||

| Megan Warren (1968) | Vice President, T. Rowe Price, T. Rowe Price | |

| Vice President | Group, Inc., T. Rowe Price Retirement Plan | |

| Services, Inc., T. Rowe Price Services, Inc., | ||

| and T. Rowe Price Trust Company; formerly, | ||

| Executive Director, JP Morgan Chase (to 2017) | ||

| Thomas H. Watson (1977) | Director and Vice President, T. Rowe Price Trust | |

| Vice President | Company; Vice President, T. Rowe Price and | |

| T. Rowe Price Group, Inc. | ||

| Alison Mei Ling Yip (1966) | Vice President, Price Hong Kong and T. Rowe | |

| Vice President | Price Group, Inc. | |

| Unless otherwise noted, officers have been employees of T. Rowe Price or T. Rowe Price International for at least 5 years. | ||

Item 2. Code of Ethics.

The registrant has adopted a code of ethics, as defined in Item 2 of Form N-CSR, applicable to its principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions. A copy of this code of ethics is filed as an exhibit to this Form N-CSR. No substantive amendments were approved or waivers were granted to this code of ethics during the period covered by this report.

Item 3. Audit Committee Financial Expert.

The registrant’s Board of Directors/Trustees has determined that Mr. Bruce W. Duncan qualifies as an audit committee financial expert, as defined in Item 3 of Form N-CSR. Mr. Duncan is considered independent for purposes of Item 3 of Form N-CSR.

Item 4. Principal Accountant Fees and Services.

(a) – (d) Aggregate fees billed for the last two fiscal years for professional services rendered to, or on behalf of, the registrant by the registrant’s principal accountant were as follows:

Audit fees include amounts related to the audit of the registrant’s annual financial statements and services normally provided by the accountant in connection with statutory and regulatory filings. Audit-related fees include amounts reasonably related to the performance of the audit of the registrant’s financial statements and specifically include the issuance of a report on internal controls and, if applicable, agreed-upon procedures related to fund acquisitions. Tax fees include amounts related to services for tax compliance, tax planning, and tax advice. The nature of these services specifically includes the review of distribution calculations and the preparation of Federal, state, and excise tax returns. All other fees include the registrant’s pro-rata share of amounts for agreed-upon procedures in conjunction with service contract approvals by the registrant’s Board of Directors/Trustees.

(e)(1) The registrant’s audit committee has adopted a policy whereby audit and non-audit services performed by the registrant’s principal accountant for the registrant, its investment adviser, and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant require pre-approval in advance at regularly scheduled audit committee meetings. If such a service is required between regularly scheduled audit committee meetings, pre-approval may be authorized by one audit committee member with ratification at the next scheduled audit committee meeting. Waiver of pre-approval for audit or non-audit services requiring fees of a de minimis amount is not permitted.

(2) No services included in (b) – (d) above were approved pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

(f) Less than 50 percent of the hours expended on the principal accountant’s engagement to audit the registrant’s financial statements for the most recent fiscal year were attributed to work performed by persons other than the principal accountant’s full-time, permanent employees.

(g) The aggregate fees billed for the most recent fiscal year and the preceding fiscal year by the registrant’s principal accountant for non-audit services rendered to the registrant, its investment adviser, and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant were $2,169,000 and $2,146,000, respectively.

(h) All non-audit services rendered in (g) above were pre-approved by the registrant’s audit committee. Accordingly, these services were considered by the registrant’s audit committee in maintaining the principal accountant’s independence.

Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. Investments.

(a) Not applicable. The complete schedule of investments is included in Item 1 of this Form N-CSR.

(b) Not applicable.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

Not applicable.

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

Not applicable.

Item 10. Submission of Matters to a Vote of Security Holders.

Not applicable.

Item 11. Controls and Procedures.

(a) The registrant’s principal executive officer and principal financial officer have evaluated the registrant’s disclosure controls and procedures within 90 days of this filing and have concluded that the registrant’s disclosure controls and procedures were effective, as of that date, in ensuring that information required to be disclosed by the registrant in this Form N-CSR was recorded, processed, summarized, and reported timely.

(b) The registrant’s principal executive officer and principal financial officer are aware of no change in the registrant’s internal control over financial reporting that occurred during the registrant’s second fiscal quarter covered by this report that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting.

Item 12. Exhibits.

(a)(1) The registrant’s code of ethics pursuant to Item 2 of Form N-CSR is attached.

(2) Separate certifications by the registrant's principal executive officer and principal financial officer, pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(a) under the Investment Company Act of 1940, are attached.

(3) Written solicitation to repurchase securities issued by closed-end companies: not applicable.

(b) A certification by the registrant's principal executive officer and principal financial officer, pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(b) under the Investment Company Act of 1940, is attached.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

T. Rowe Price Global Technology Fund, Inc.

| By | /s/ Edward C. Bernard | |||||

| Edward C. Bernard | ||||||

| Principal Executive Officer | ||||||

| Date | February 15, 2018 | |||||

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

| By | /s/ Edward C. Bernard | |||||

| Edward C. Bernard | ||||||

| Principal Executive Officer | ||||||

| Date | February 15, 2018 | |||||

| By | /s/ Catherine D. Mathews | |||||

| Catherine D. Mathews | ||||||

| Principal Financial Officer | ||||||

| Date | February 15, 2018 | |||||