|

Exhibit 99.2

|

TTM 2016 Investor Day

[Location]

[Date]

Global Presence Local Knowledge

Agenda

[Specific Agenda to be included for each conference.]

Disclaimer

Forward-Looking Statements

Certain statements in this communication may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, including statements related to TTM’s future business outlook. Actual results may differ materially from these forward-looking statements. Such statements relate to a variety of matters, including but not limited to: the operations of the businesses of TTM Technologies, Inc. (“TTM” or the “Company”). These statements are made on the basis of the current beliefs, expectations and assumptions of the management of TTM regarding future events and are subject to significant risks and uncertainty. Statements regarding our expected performance in the future are forward-looking statements.

It is uncertain whether any of the events anticipated by the forward-looking statements will transpire or occur, or if any of them do, what impact they will have on the results of operations and financial condition of the Company. These forward-looking statements involve certain risks and uncertainties that could cause actual results to differ materially from those indicated in such forward-looking statements and are set forth in the Company’s most recent Annual Report on Form 10-K and Quarterly Report on Form 10-Q and in the

Company’s other filings filed with the Securities and Exchange Commission (the “SEC”) under the heading “Risk Factors” and which are available at the SEC’s website at www.sec.gov.

TTM does not undertake any obligation to update any of theses statements to reflect any new information, subsequent events or circumstances, or otherwise, except as may be required by law.

Use of Non-GAAP Financial Measures

In addition to the financial statements presented in accordance with U.S. GAAP, TTM uses certain non-GAAP financial measures, including “adjusted EBITDA.” The companies present non-GAAP financial information to enable investors to see each company through the eyes of management and to provide better insight into its ongoing financial performance.

Adjusted EBITDA is defined as earnings before interest expense, income taxes, depreciation, amortization of intangibles, stock-based compensation expense, gain on sale of assets, asset impairments, restructuring, costs related to acquisitions, and other charges. For a reconciliation of adjusted EBITDA to net income, please see the appendix at the end of this presentation. Adjusted EBITDA is not a recognized financial measure under U.S. GAAP and does not purport to be an alternative to operating income or an indicator of operating performance. Adjusted EBITDA is presented to enhance an understanding of operating results and is not intended to represent cash flows or results of operations. The use of this non-GAAP measure provides an indication of each company’s ability to service debt, and management considers it an appropriate measure to use because of the Company’s leveraged positions.

Adjusted EBITDA has certain material limitations, primarily due to the exclusion of certain amounts that are material to each Company’s consolidated results of operations, such as interest expense, income tax expense, and depreciation and amortization. In addition, adjusted EBITDA may differ from the adjusted EBITDA calculations reported by other companies in the industry, limiting its usefulness as a comparative measure.

Data Used in This Presentation

Due to rounding, numbers presented throughout this and other documents may not add up precisely to the totals provided and percentages may not precisely reflect the absolute figures.

Third Party Information

This presentation has been prepared by the Company and includes information from other sources believed by the Company to be reliable. No representation or warranty, express or implied, is made as to the fairness, accuracy or completeness of any of the opinions and conclusions set forth herein based on such information. This presentation may contain descriptions or summaries of certain documents and agreements, but such descriptions or summaries are qualified in their entirety by reference to the actual documents or agreements. Unless otherwise indicated, the information contained herein speaks only as of the date hereof and is subject to change, completion or amendment without notice.

Diversified, Differentiated and Disciplined

Tom Edman

Key Messages

Diversification Differentiation Discipline

Diversified Near term—Auto, Aerospace & Defense

Technology breadth One stop solutions

Disciplined integration Cash flow generation

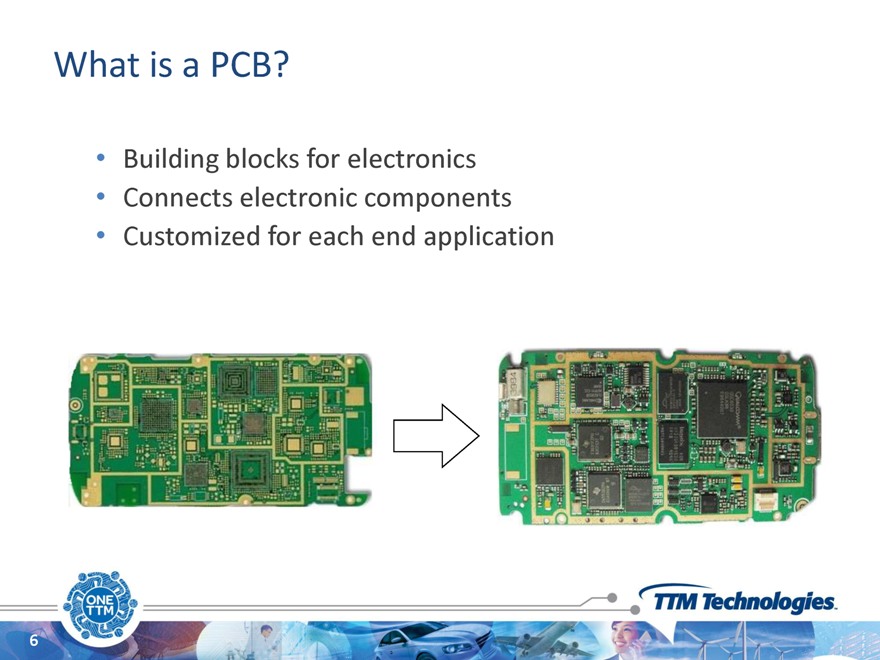

What is a PCB?

Building blocks for electronics Connects electronic components

Customized for each end application

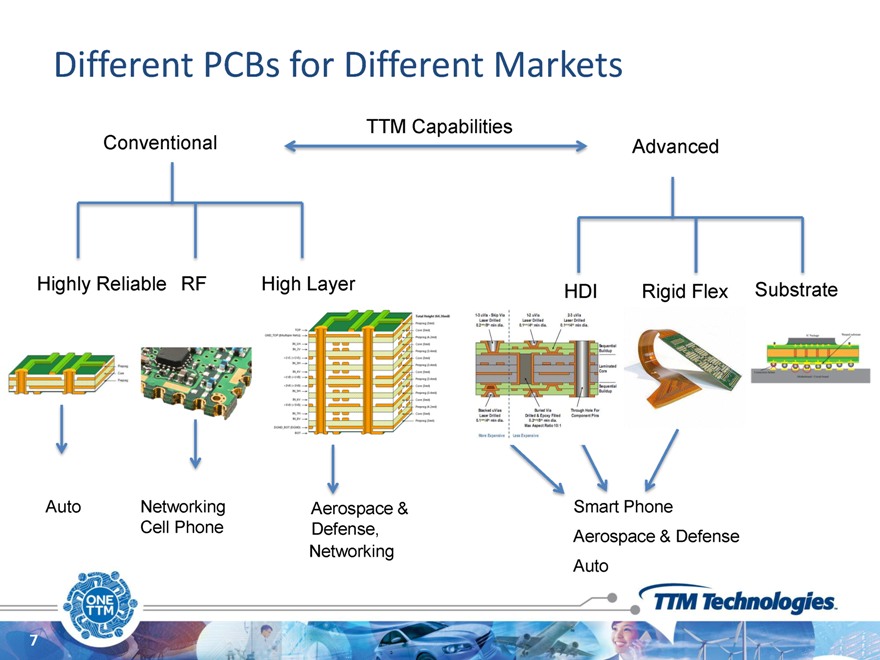

Different PCBs for Different Markets

TTM Capabilities

Conventional Advanced

Highly Reliable RF High Layer HDI Rigid Flex Substrate

Auto Networking pace & Cell Phone Defense,

Networking Aerospace & Defense Auto

PCBs: Foundation of all Electronics

Automotive

Mobile Station

Storage Data Center

Smar

Commercial Aircraft

Network Router

Message #1 – Diversification and

Growth

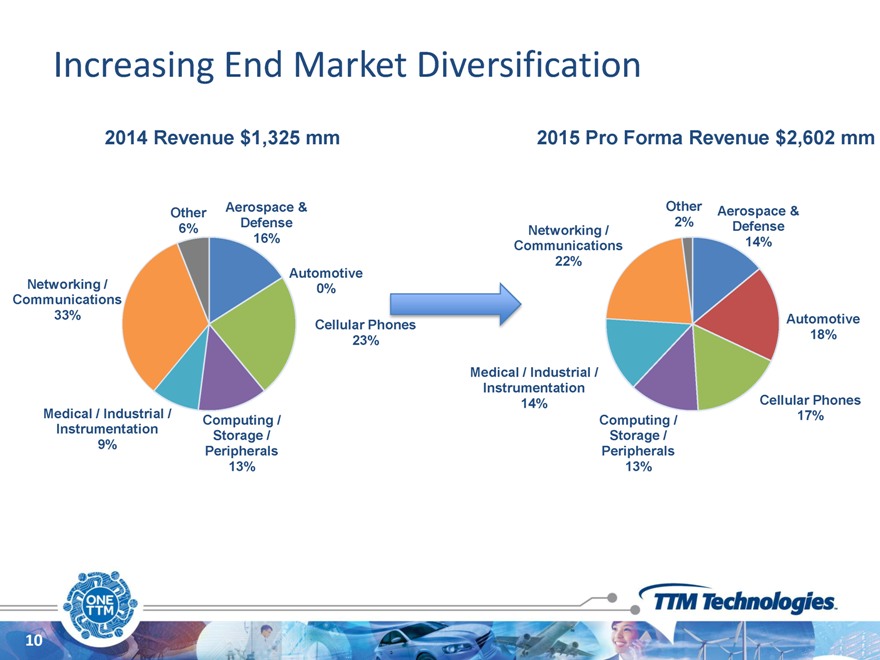

Increasing End Market Diversification

2014 Revenue $1,325 mm 2015 Pro Forma Revenue $2,602 mm

Aerospace & Other Aerospace & Other Defense 2% Defense

6% Networking /

16% 14% Communications Automotive 22% Networking / 0% Communications

33% Automotive Cellular Pho 18% 23%

Medical / Industrial /

Instrumentation Cellular Phones 14% Medical / Industrial / 17% Computing / Computing / Instrumentation Storage / Storage / 9% Peripherals Peripherals 13% 13%

10

Top Tier Customers

11

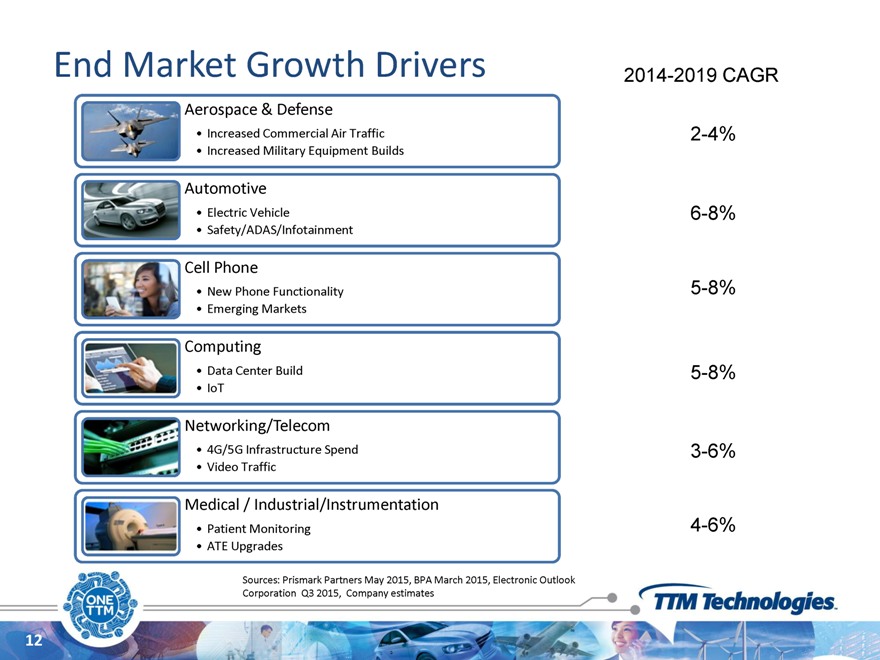

End Market Growth Drivers 2014-2019 CAGR

Aerospace & Defense

Increased Commercial Air Traffic 2-4%

Increased Military Equipment Builds

Automotive

Electric Vehicle 6-8%

Safety/ADAS/Infotainment

Cell Phone

New Phone Functionality 5-8%

Emerging Markets

Computing

Data Center Build 5-8%

IoT

Networking/Telecom

4G/5G Infrastructure Spend 3-6%

Video Traffic

Medical / Industrial/Instrumentation

Patient Monitoring 4-6%

ATE Upgrades

Sources: Prismark Partners May 2015, BPA March 2015, Electronic Outlook Corporation Q3 2015, Company estimates

12

Automotive Opportunities

Safety – Advanced Driver Assist (ADAS) driving adoption of new technologies like Radar, IR, Ultrasound

Electric – Tighter emission standards driving EV/hybrid adoption

Infotainment – Video/Audio entertainment, internet access, connectivity

Key growth driver – Increasing electronic content

13

Aerospace & Defense Opportunities

Aerospace seeing strong traffic growth

Continued rollout of Boeing 737 and 787 programs

2016 Defense budget up 5.8%

Missile Defense Agency awards New Long Range Discrimination Radar contract to Lockheed ($784 M)

Navy awards Air and Missile Defense Radar to Raytheon

Joint Strike Fighter (JSF F35) DoD’s largest planned procurement

Key growth drivers – Increasing traffic and procurements

14

Message #2 – Differentiated through “One Stop Shop”

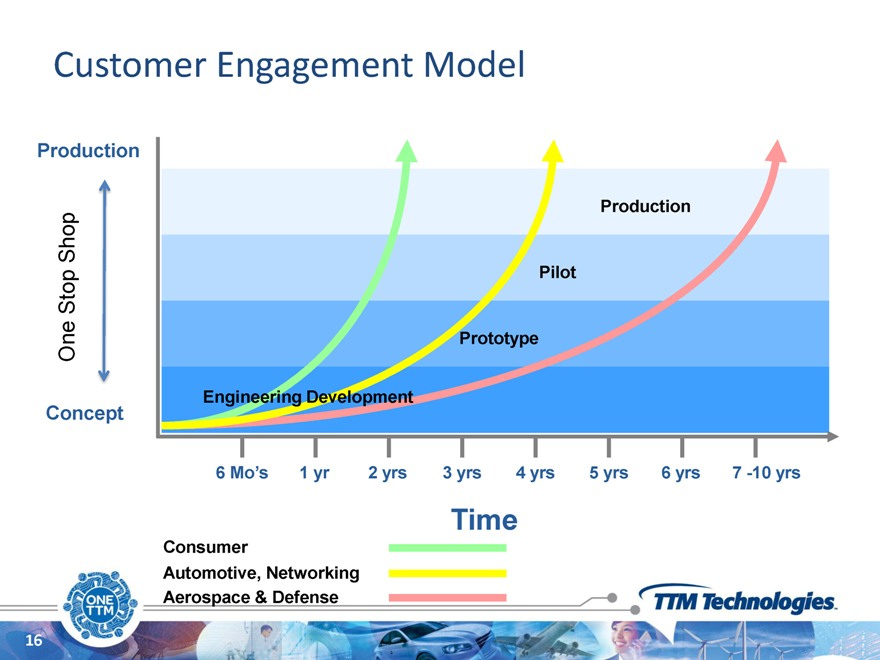

Customer Engagement Model

Production

Shop Production

Stop Pilot

One Prototype Concept Engineering Development

6 | | Mo’s 1 yr 2 yrs 3 yrs 4 yrs 5 yrs 6 yrs 7 -10 yrs |

Time

Consumer

Automotive, Networking Aerospace & Defense

16

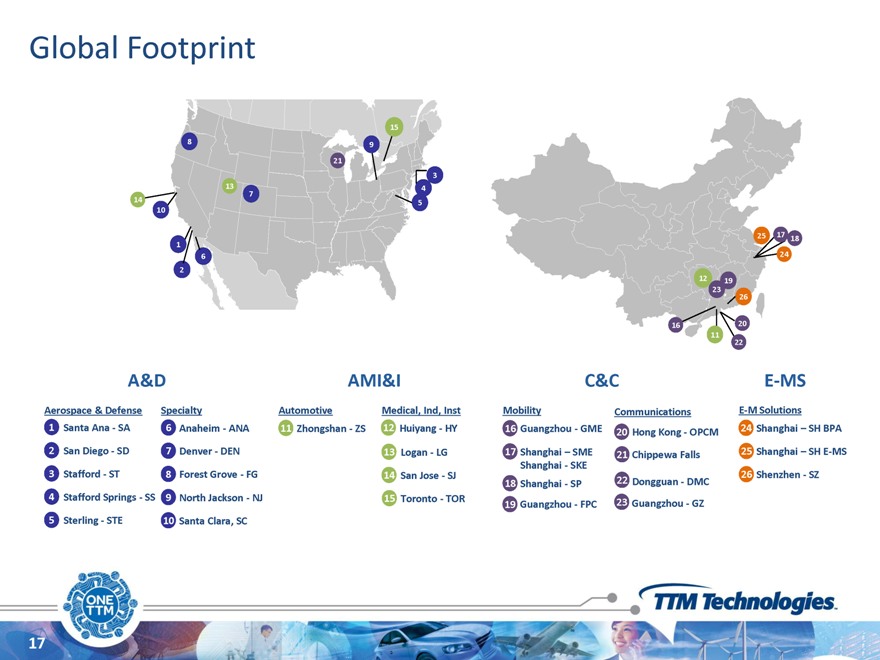

Global Footprint

15

8 9 21

3

13 4

14 7

5 10

25 17

1 18

6 24 2

12 19 23 26

16 20 11 22

A&D AMI&I C&C E-MS

Aerospace & Defense Specialty Automotive Medical, Ind, Inst Mobility Communications E-M Solutions

1 Santa Ana—SA 6 Anaheim—ANA 11 Zhongshan—ZS 12 Huiyang—HY 16 Guangzhou—GME 24 Shanghai – SH BPA

20 Hong Kong—OPCM

2 San Diego—SD 7 Denver—DEN 13 Logan—LG 17 Shanghai – SME 21 25 Shanghai – SH E-MS

Chippewa Falls

3 Shanghai—SKE

Stafford—ST 8 Forest Grove—FG 14 San Jose—SJ 26 Shenzhen—SZ

18 Shanghai—SP 22 Dongguan—DMC

4 Stafford Springs—SS 9 North Jackson—NJ 15 Toronto—TOR

19 Guangzhou—FPC 23 Guangzhou—GZ

5 Sterling—STE 10 Santa Clara, SC

17

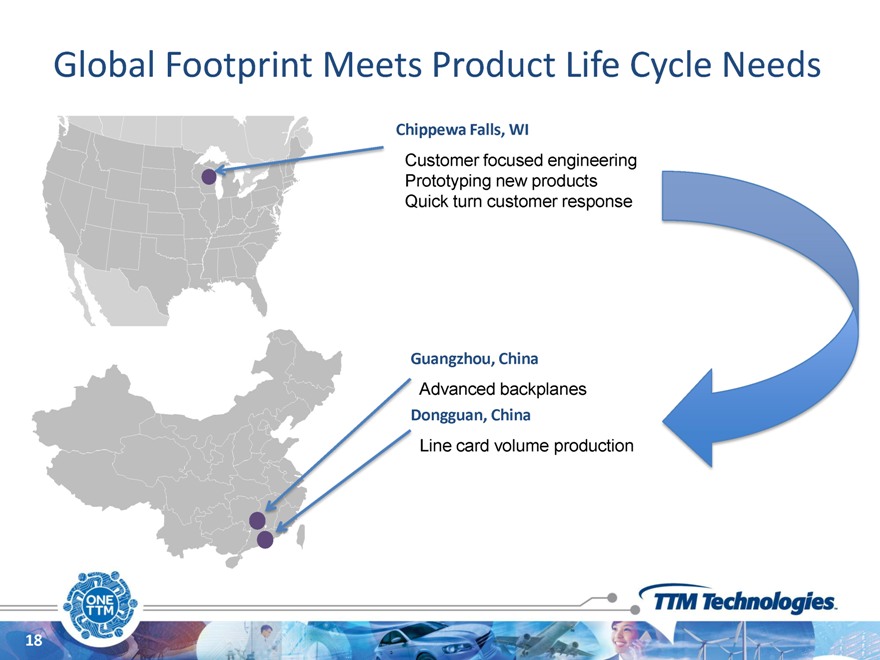

Global Footprint Meets Product Life Cycle Needs

Chippewa Falls, WI

Customer focused engineering Prototyping new products Quick turn customer response

Guangzhou, China

Advanced backplanes

Dongguan, China

Line card volume production

18

Aligned with Technology Trends

End Device Trends PCB Features TTM Capabilities

Increasing complexity Decreasing size Increasing signal speed Increasing performance

Higher layer count Microvias Thin cores Material/Laminate innovations

HDI Rigid Flex RF Radar

Increasingly Crowded PCBs Microvias

Laser Drills

19

Leveraging New Technology in Smart Phones

Adoption of HDI and Rigid Flex

Smartphones New Auto Features Medical Patient

Aerospace & Defense ADAS, Infotainment Monitoring

20

Message #3 – Disciplined

Integration & Deleveraging

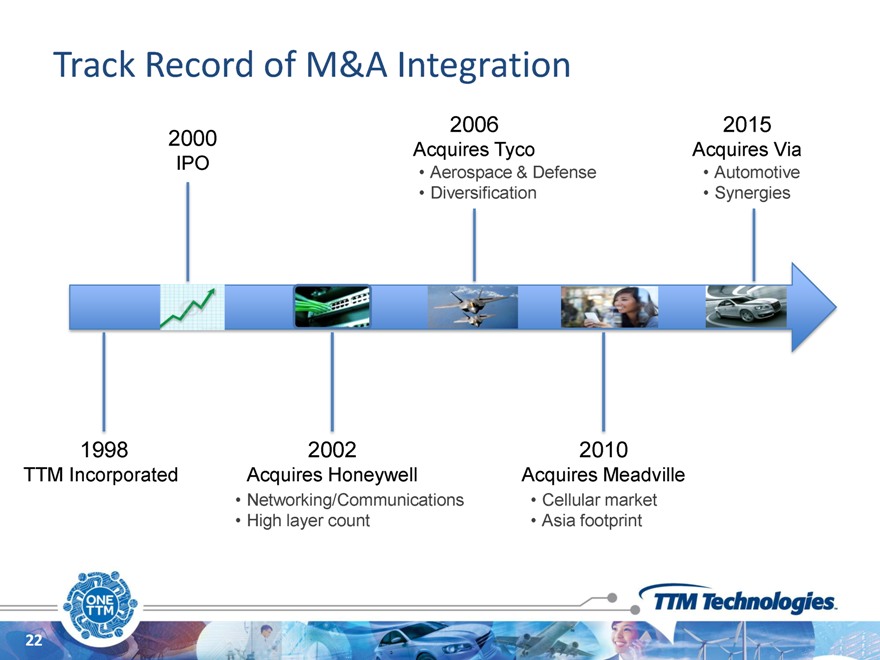

Track Record of M&A Integration

2006 2015 2000

Acquires Tyco Acquires Via IPO

Aerospace & Defense Automotive

Diversification Synergies

1998 2002 2010

TTM Incorporated Acquires Honeywell Acquires Meadville

Networking/Communications Cellular market

High layer count Asia footprint

22

Business Units and Leadership

Phil Jon Doug Tony Titterton Pereira Soder Princiotta

23

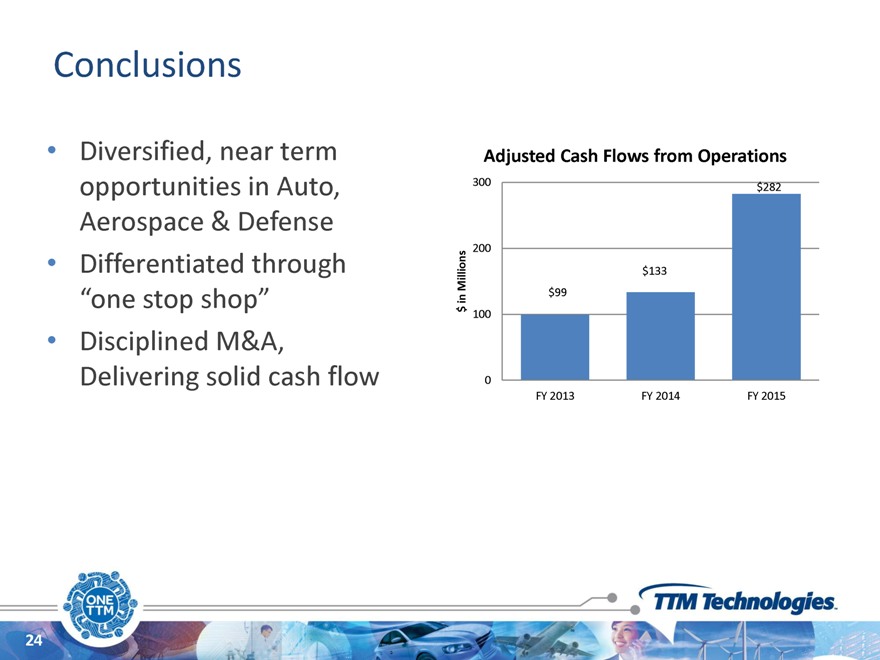

Conclusions

Diversified, near term opportunities in Auto,

Aerospace & Defense Differentiated through

“one stop shop”

Disciplined M&A,

Delivering solid cash flow

Adjusted Cash Flows from Operations

300 $282

200

Millions $133 in $99 $

100

0

FY 2013 FY 2014 FY 2015

24

Communications and Computing

Doug Soder

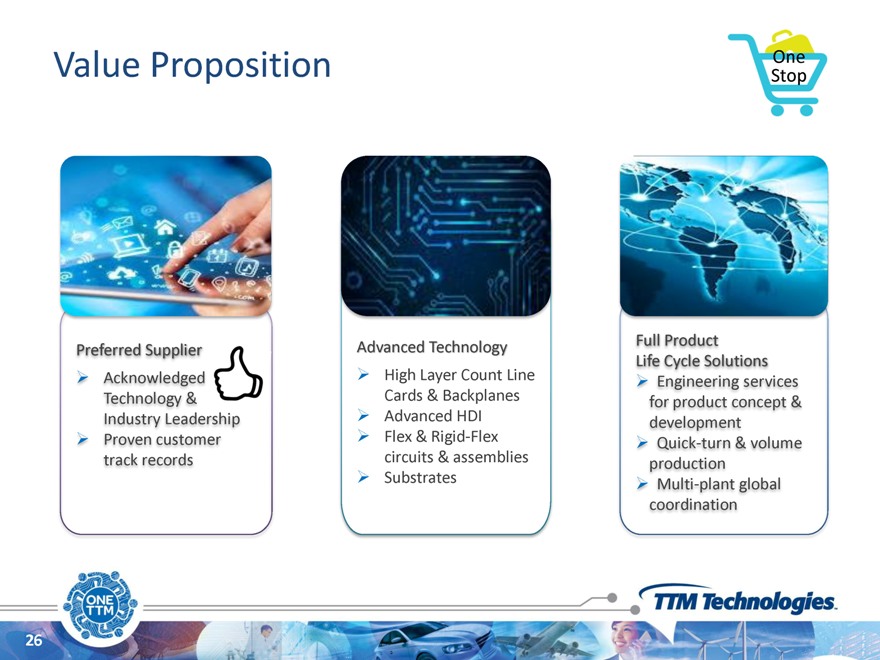

Value Proposition

Full Product Preferred Supplier Advanced Technology Life Cycle Solutions Acknowledged High Layer Count Line Engineering services Technology & Cards & Backplanes for product concept & Industry Leadership Advanced HDI development Proven customer Flex & Rigid-Flex Quick-turn & volume track records circuits & assemblies production Substrates Multi-plant global coordination

26

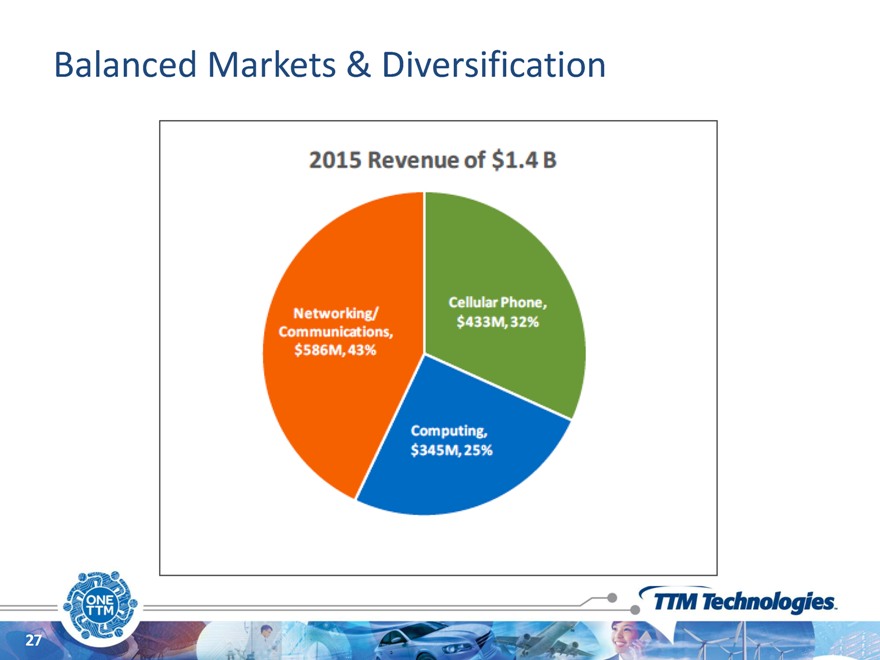

Balanced Markets & Diversification

27

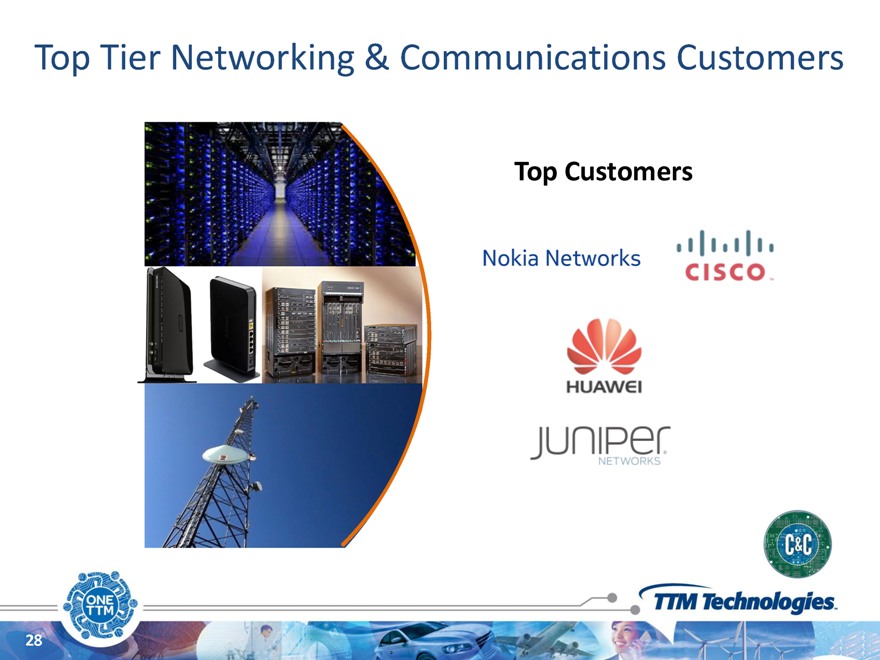

Top Tier Networking & Communications Customers

Top Customers

28

Top Tier Cellular Phone Customers

Top Customers

Chengrui

29

Top Tier Computing Customers

Top Customers

30

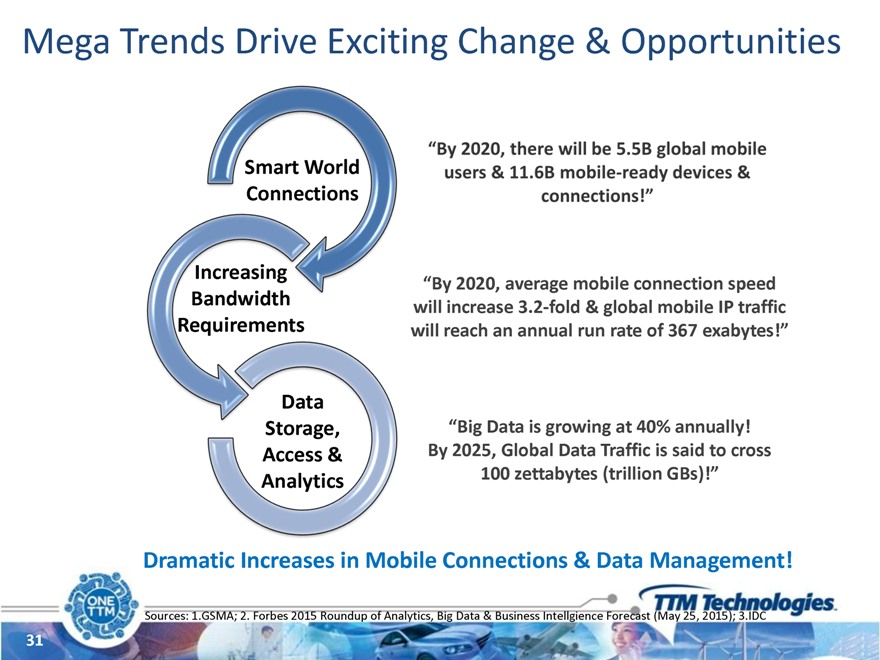

Mega Trends Drive Exciting Change & Opportunities

Smart World Connections

“By 2020, average mobile connection speed will increase 3.2-fold & global mobile IP traffic will reach an annual run rate of 367 exabytes!”

Data

Storage, “Big Data is growing at 40% annually! Access & By 2025, Global Data Traffic is said to cross Analytics 100 zettabytes (trillion GBs)!”

Dramatic Increases in Mobile Connections & Data Management!

Sources: 1.GSMA; 2. Forbes 2015 Roundup of Analytics, Big Data & Business Intellgience Forecast (May 25, 2015); 3.IDC

31

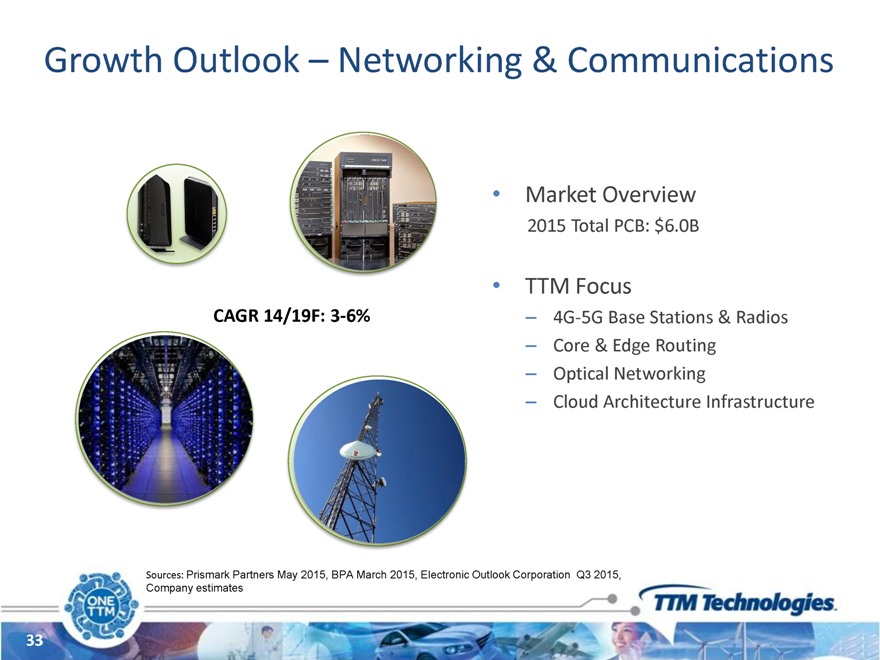

Networking & Communications

Growth Outlook – Networking & Communications

Market Overview

2015 Total PCB: $6.0B

TTM Focus

4G-5G Base Stations & Radios Core & Edge Routing Optical Networking Cloud Architecture Infrastructure

CAGR 14/19F: 3-6%

Sources: Prismark Partners May 2015, BPA March 2015, Electronic Outlook Corporation Q3 2015, Company estimates

33

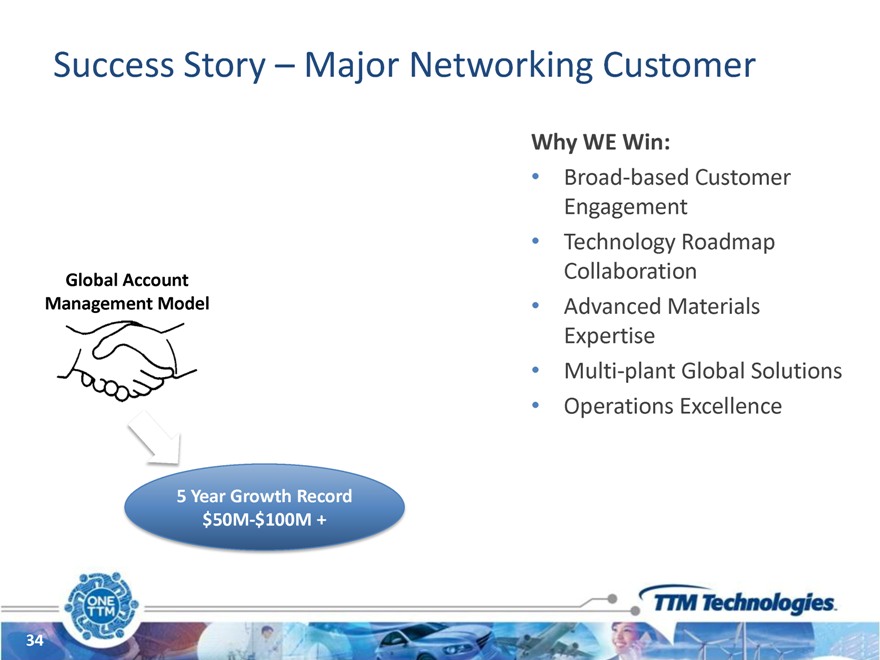

Success Story – Major Networking Customer

Why WE Win:

Broad-based Customer Engagement Technology Roadmap Collaboration Advanced Materials Expertise Multi-plant Global Solutions Operations Excellence

Product Portfolio Global Account Management Model Line Cards Backplanes Flex Rigid Flex HDI

5 | | Year Growth Record $50M-$100M + |

34

Cellular Phones

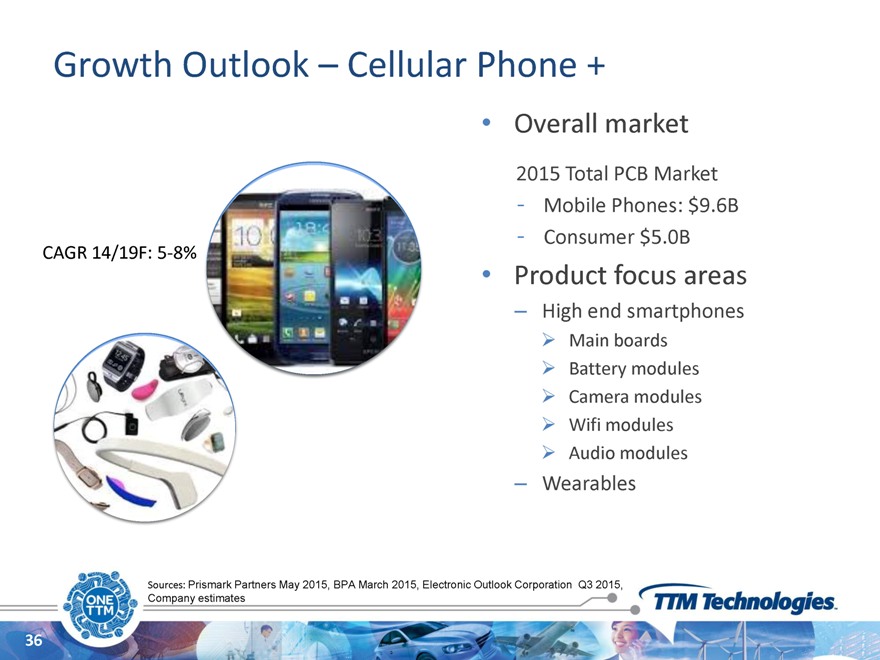

Growth Outlook – Cellular Phone +

Overall market

2015 Total PCB Market

Mobile Phones: $9.6B

Consumer $5.0B

Product focus areas

High end smartphones

Main boards Battery modules Camera modules Wifi modules Audio modules

Wearables

CAGR 14/19F: 5-8%

Sources: Prismark Partners May 2015, BPA March 2015, Electronic Outlook Corporation Q3 2015, Company estimates

36

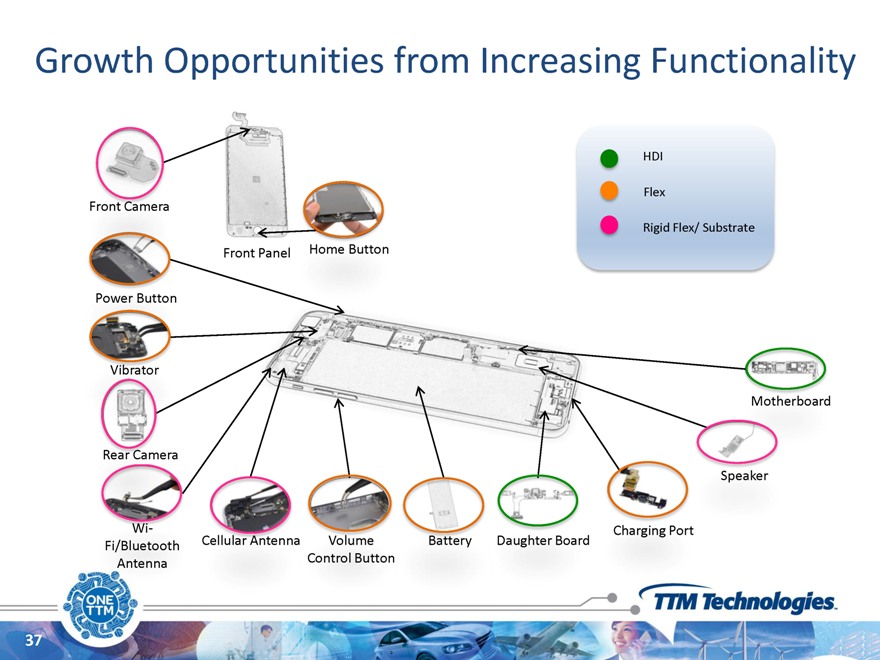

Growth Opportunities from Increasing Functionality

HDI

Flex

Rigid Flex/ Substrate

Front Panel Home Button

Power Button

Vibrator

Motherboard

Charging Battery Daughter Board

37

Success Story – Top Tier Smartphone OEM

Why WE Win

Industry Reputation

Close Engineering Engagement for New Product Development Multiple Product Line Solutions Integrated Rigid & Flex factory

speed & flexibility

NPI through Mass Production Capability

Record 2M—$25M & Growing

IoT Module

Camera Module

WiFi Module

38

Communications & Computing Business Unit

Growth Opportunities

Increasing Smartphone Functionality

IoT / Wearables

Cloud Infrastructure

Service Provider Infrastructure

Why WE Win?

Industry Leadership Reputation Technology Leadership Global Scale & Flexibility

39

Electro-Mechanical Solutions

Tony Princiotta

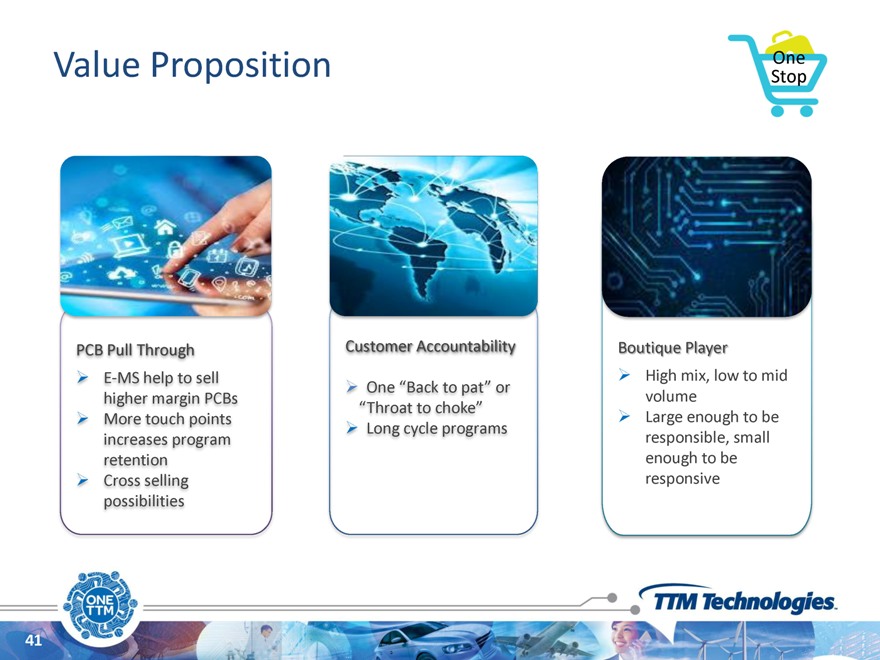

Value Proposition

PCB Pull Through Customer Accountability Boutique Player E-MS help to sell High mix, low to mid

One “Back to pat” or higher margin PCBs volume

“Throat to choke”

More touch points Large enough to be Long cycle programs increases program responsible, small retention enough to be Cross selling responsive possibilities

41

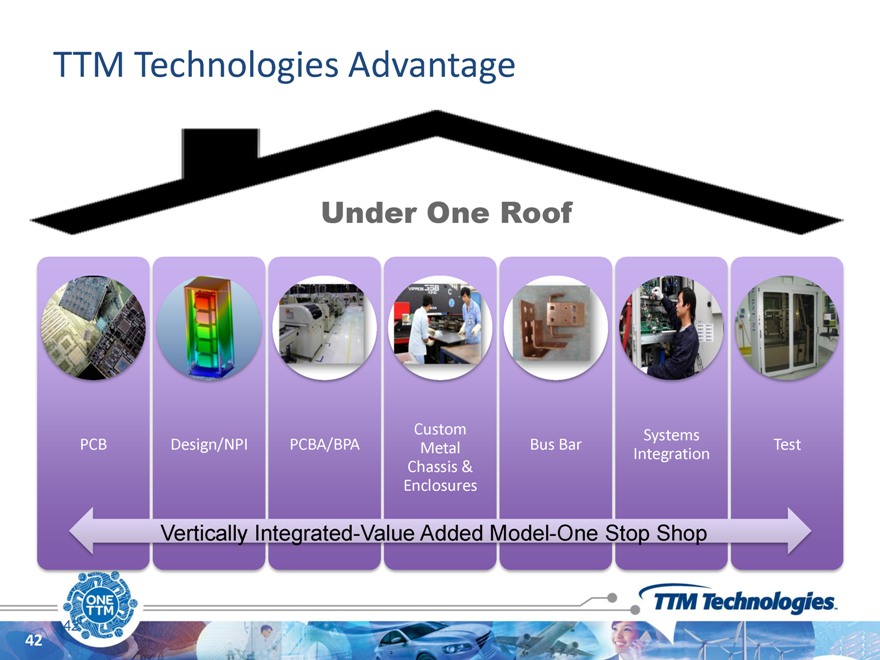

TTM Technologies Advantage

Under One Roof

Custom Systems

PCB Design/NPI PCBA/BPA Metal Bus Bar Test Chassis & Integration Enclosures

Vertically Integrated-Value Added Model-One Stop Shop

42

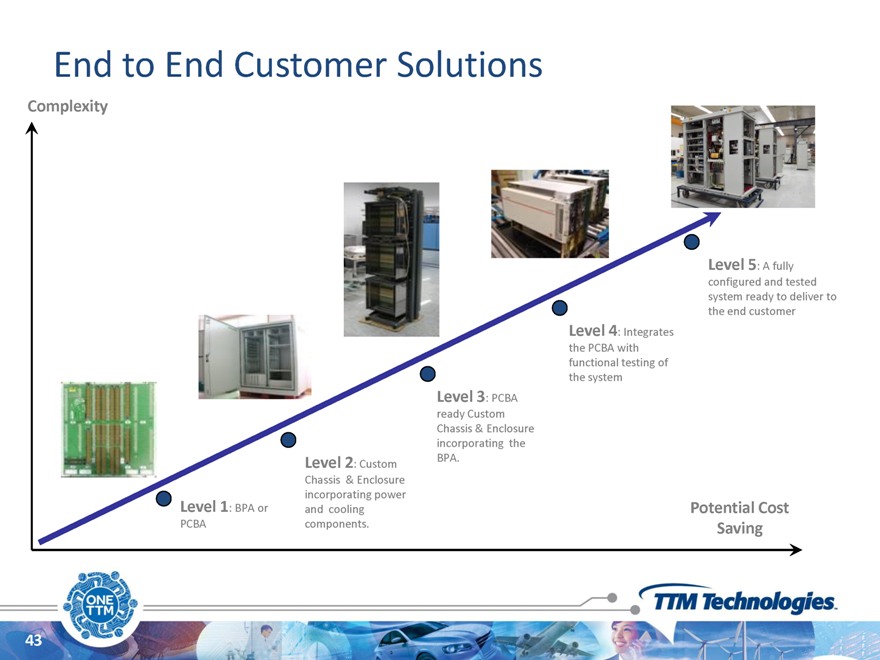

End to End Customer Solutions

Complexity

Level 5: A fully configured and tested system ready to deliver to the end customer Level 4: Integrates the PCBA with functional testing of the system Level 3: PCBA ready Custom Chassis & Enclosure incorporating the BPA.

Level 2: Custom

Chassis & Enclosure incorporating power

Level 1: BPA or and cooling Potential Cost PCBA components. Saving

43

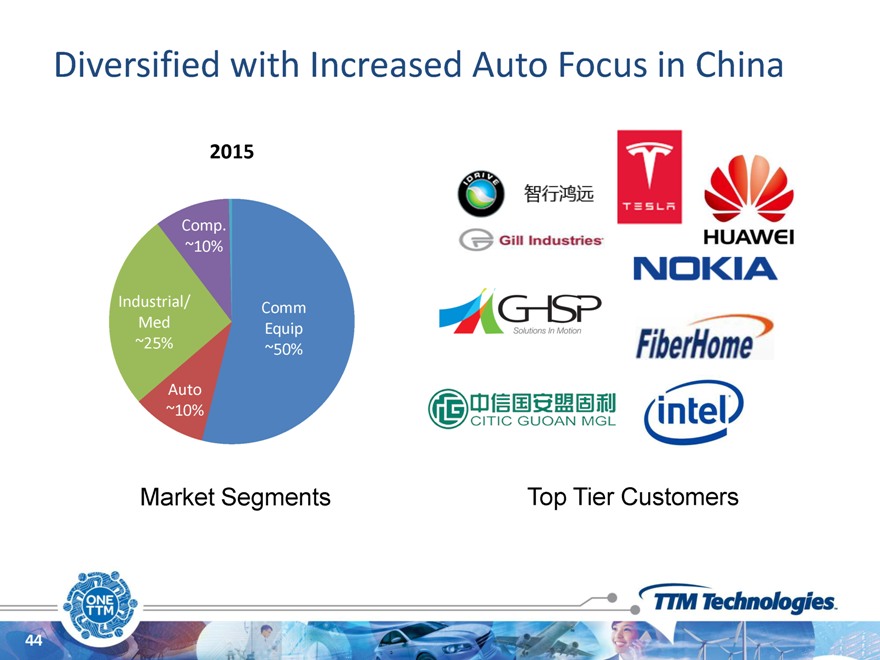

Diversified with Increased Auto Focus in China

2015

Comp. ~10%

Industrial/ Comm Med Equip ~25% ~50%

Auto ~10%

Market Segments Top Tier Customers

44

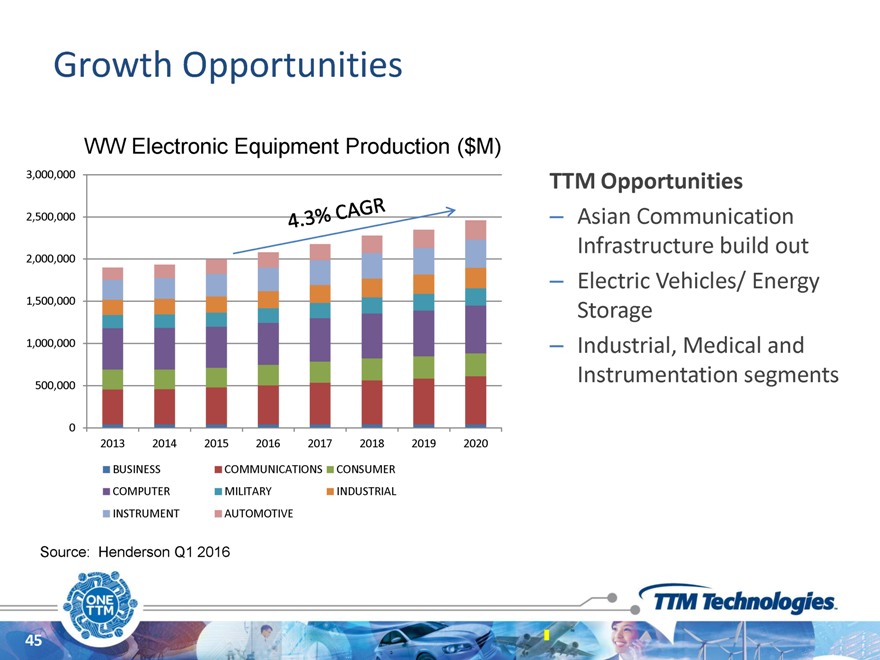

Growth Opportunities

WW Electronic Equipment Production ($M)

3,000,000 2,500,000 2,000,000 1,500,000 1,000,000 500,000

0

2013 2014 2015 2016 2017 2018 2019 2020

BUSINESS COMMUNICATIONS CONSUMER

COMPUTER MILITARY INDUSTRIAL

INSTRUMENT AUTOMOTIVE

Source: Henderson Q1 2016

TTM Opportunities

Asian Communication Infrastructure build out Electric Vehicles/ Energy Storage Industrial, Medical and Instrumentation segments

45

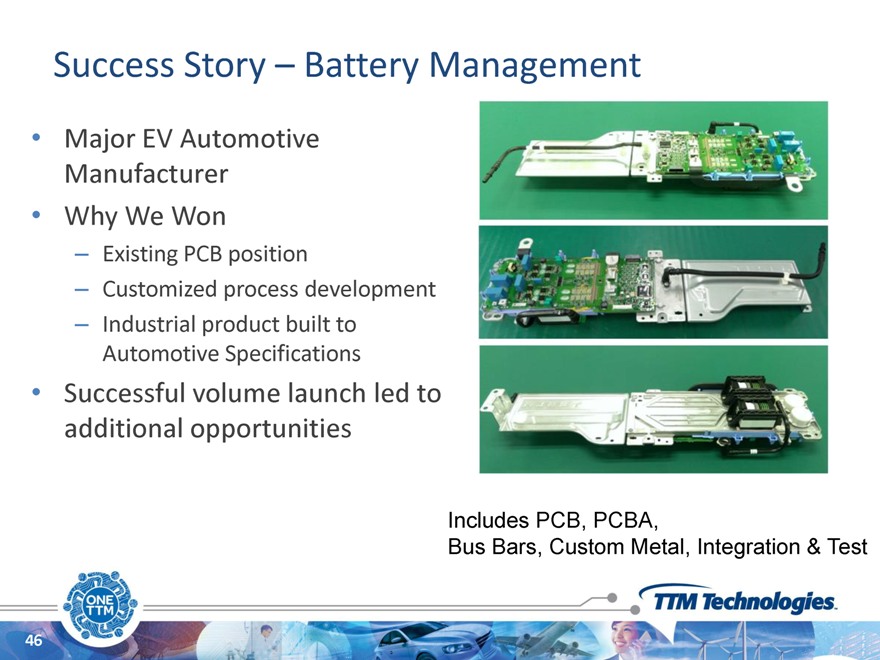

Success Story – Battery Management

Major EV Automotive

Manufacturer

Why We Won

Existing PCB position

Customized process development Industrial product built to Automotive Specifications

Successful volume launch led to additional opportunities

Includes PCB, PCBA,

Bus Bars, Custom Metal, Integration & Test

46

Success Story—Industrial

1.6 Megawatt Converter Why we won

Crisp manufacturing transition to China Effective localization of the supply chain Redesigned three separate enclosures to a single unit

Success:

Delivered in excess of 10,000 units

47

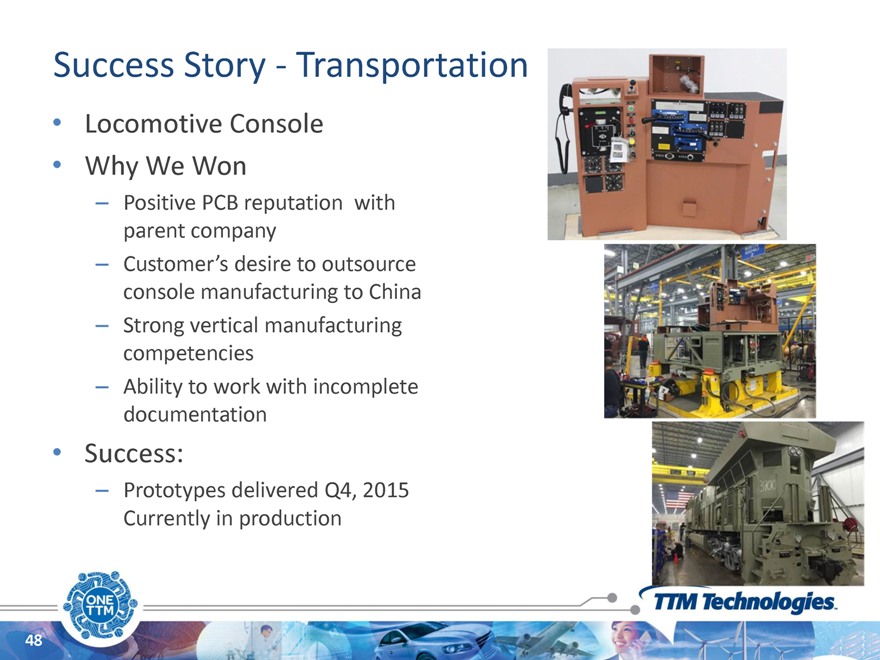

Success Story—Transportation

Locomotive Console Why We Won

Positive PCB reputation with parent company Customer’s desire to outsource console manufacturing to China Strong vertical manufacturing competencies Ability to work with incomplete documentation

Success:

Prototypes delivered Q4, 2015 Currently in production

48

Conclusions

E-M Solutions helps drive customer adoption of PCB products

One stop shop that provides complete solutions increases

“stickiness” to the customer and helps the PCB business retain core programs

Growth opportunities in electric vehicles, optical transmission networks, industrial products

49

Aerospace & Defense / Specialty

Phil Titterton

Value Proposition

Superior reliability for mission critical applications

Multi-site solution to the military/aerospace community All necessary certifications

One stop shop offering technology breadth and depth

51

Leading Player Alignment with Top Tier Customers

Leading

#1 A&D PCB Manufacturer with 2015 Revenue ~$350 million

Player

52

Strategic Partnerships Strengthen Position

Customer Years Partnered Industry Sector(s)

25 Comm Aero & Defense

17 Defense & Space

18 Defense & Space

29 Comm Aero, Defense & Space

16 Comm Aero, Defense & Space

31 Defense & Space

34 Defense & Space

28 Defense & Space

20 Comm Aero, Defense & Space

33 Comm Aero, Defense & Space

53

Aerospace & Defense – Diverse Applications

Flight Critical Electronics Missile & Munitions Communication Products Sensing & Surveillance Engine Control Systems Satellite Communications Foreign Military Sales Nuclear Deterrence Infrared Acquisition Targets Power Distribution Systems Ballistic Defense Jamming Countermeasures Internal Research & Development

54

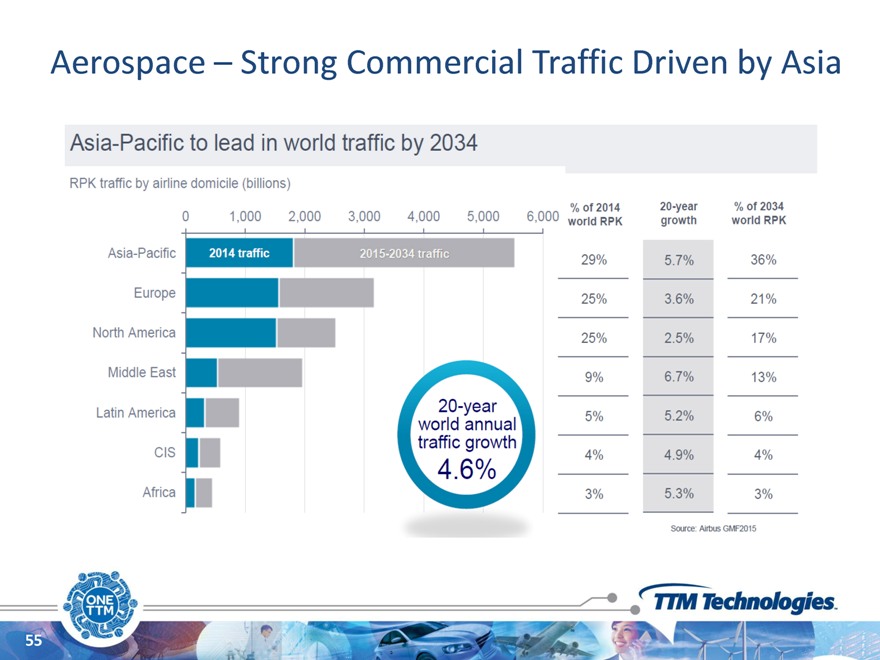

Aerospace – Strong Commercial Traffic Driven by Asia

55

cial Aerospace

TTM supports flight critical electronics on 737, 777, 787, A319, A320, A321, A350, A380 Fly by wire electrical content replacing traditional hydraulic systems

Opportunity

56

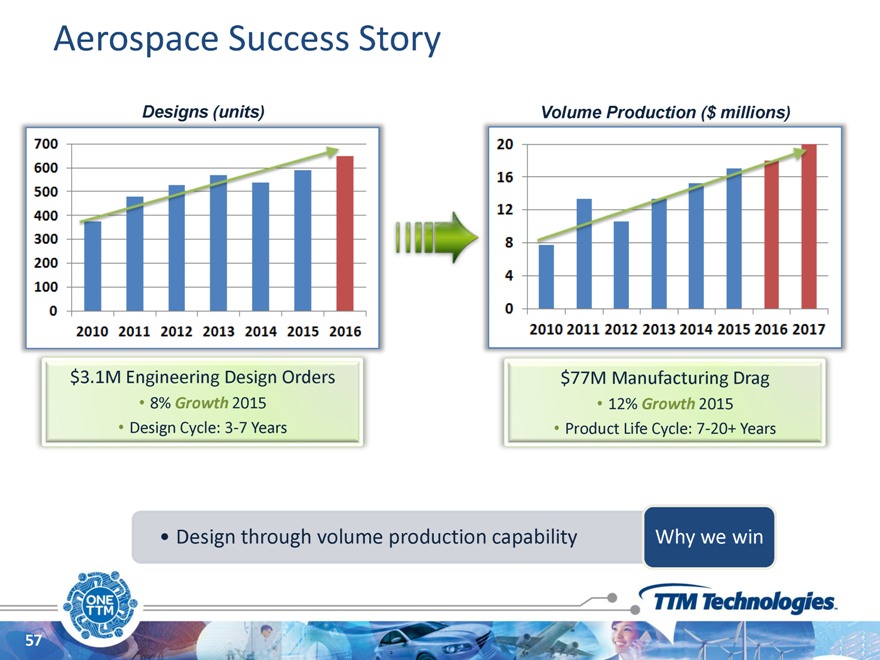

Aerospace Success Story

Designs (units) Volume Production ($ millions)

$3.1M Engineering Design Orders $77M Manufacturing Drag

8% Growth 2015 12% Growth 2015

Design Cycle: 3-7 Years Product Life Cycle: 7-20+ Years

Design through volume production capability

Why we win

57

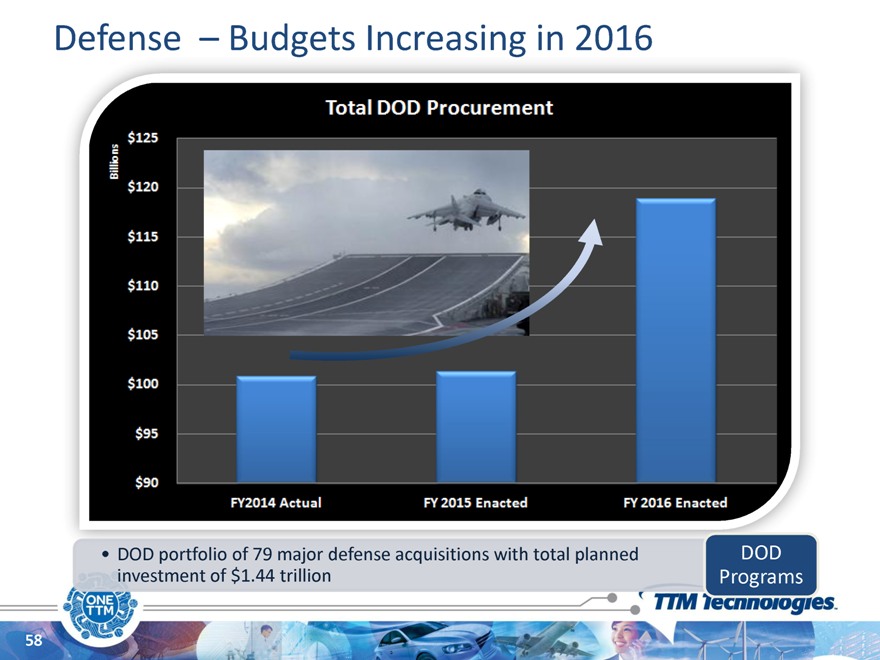

Defense – Budgets Increasing in 2016

DOD portfolio of 79 major defense acquisitions with total planned investment of $1.44 trillion

DOD Programs

58

Key Opportunities in Defense

TTM supports mission critical electronics for a majority of DOD Programs including JSF, THADD, Patriot, F16, JDAM & Hellfire

Opportunity

59

Defense Success Story 1 – “One Stop Shop”

Space Fence

SUPPORTING FACILITIES CAPABILITY

DESIGN ENGINEERING Digital, RF, Flex • Space Fence 100,000 debris

tracking system down to size of

STAFFORD, CT RF Structure

baseball

STAFFORD SPRINGS, CT Flex Assembly

Radar installation is equivalent to

CHIPPEWA FALLS, WI Digital PCB the size of a football field and is

SANTA CLARA, CA Flex PCB located on a South Pacific island

ANAHEIM, CA HDI Interposer

Ability to meet all of customer’s needs with multiple factory engagement

Why we win

capability vs. option of procuring from six different suppliers

60

Defense Success Story 2 – “Mission Critical”

Proven mission critical technology provider Why we win

61

Conclusion

Aerospace & Defense BU offers mission critical, reliable product to industry leaders

One stop solution that provides enabling technologies and capabilities

Strategic partnerships with our customers strengthens our leading market position

Growth opportunities in commercial aerospace and increased defense procurement

62

Automotive, Medical, Industrial and Instrumentation

Jon Pereira

Value Proposition

ONE-STOP SOLUTION TRUSTED HIGH SEAMLESS GLOBAL RELIABILITY SUPPLIER TRANSFER

WIDE-RANGE OF PROVEN TRACK FULL PRODUCT CAPABILITIES RECORD LIFE-CYCLE

64

Diverse Markets and Top Tier Customers

MI&I ~40%

US $326m US $448m

Automotive ~60%

2015

65

Automotive

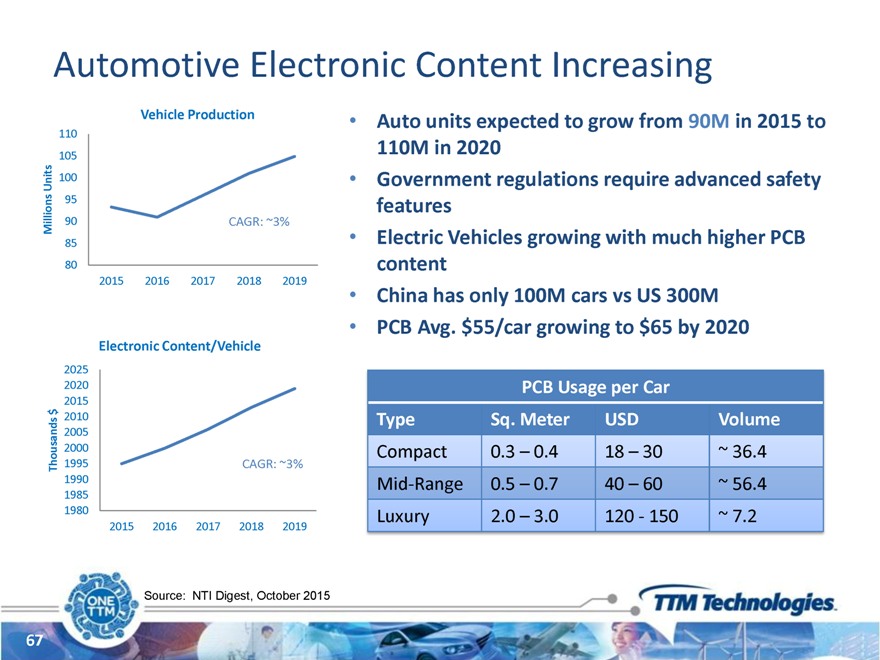

Automotive Electronic Content Increasing

Vehicle Production • Auto units expected to grow from 90M in 2015 to

110 110M in 2020

105

Units 100 • Government regulations require advanced safety

95

features

Millions 90 CAGR: ~3%

85 • Electric Vehicles growing with much higher PCB

80 content

2015 2016 2017 2018 2019

China has only 100M cars vs US 300M

PCB Avg. $55/car growing to $65 by 2020

Electronic Content/Vehicle

2025

2020 PCB Usage per Car

2015 $

2010 Type Sq. Meter USD Volume

2005

2000 Compact 0.3 – 0.4 18 – 30 ~ 36.4

Thousands 1995 CAGR: ~3%

1990 Mid-Range 0.5 – 0.7 40 – 60 ~ 56.4

1985

1980 Luxury 2.0 – 3.0 120—150 ~ 7.2

2015 2016 2017 2018 2019

Source: NTI Digest, October 2015

67

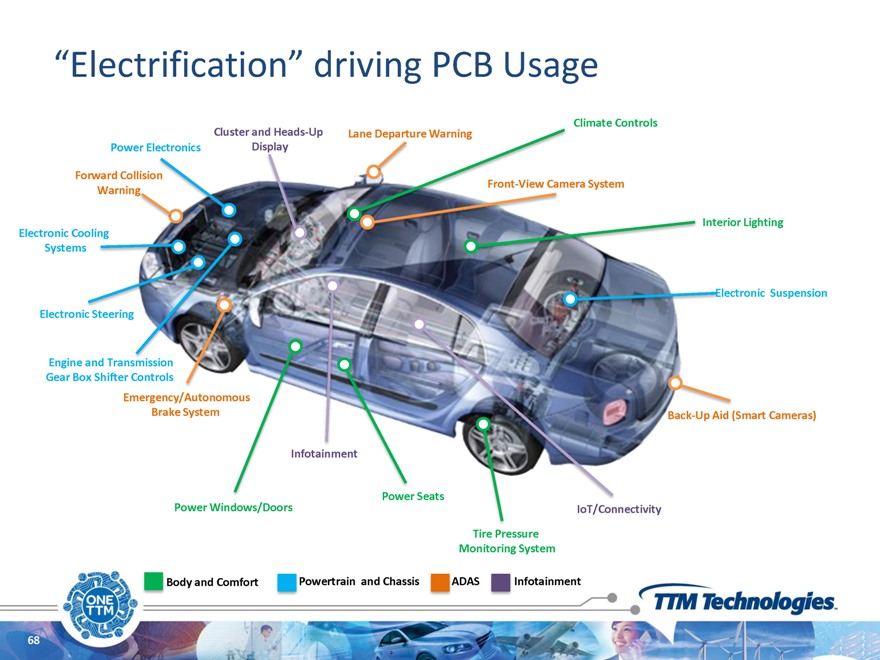

“Electrification” driving PCB Usage

Cluster and Heads-Up Climate Controls Lane Departure Warning Power Electronics Display

Forward Collision

Front-View Camera System Warning

Interior Lighting Electronic Cooling Systems

Electronic Suspension

Electronic Steering

Engine and Transmission Gear Box Shifter Controls

Emergency/Autonomous

Brake System Back-Up Aid (Smart Cameras)

Infotainment

Power Seats

Power Windows/Doors IoT/Connectivity

Tire Pressure Monitoring System

Body and Comfort Powertrain and Chassis ADAS Infotainment

68

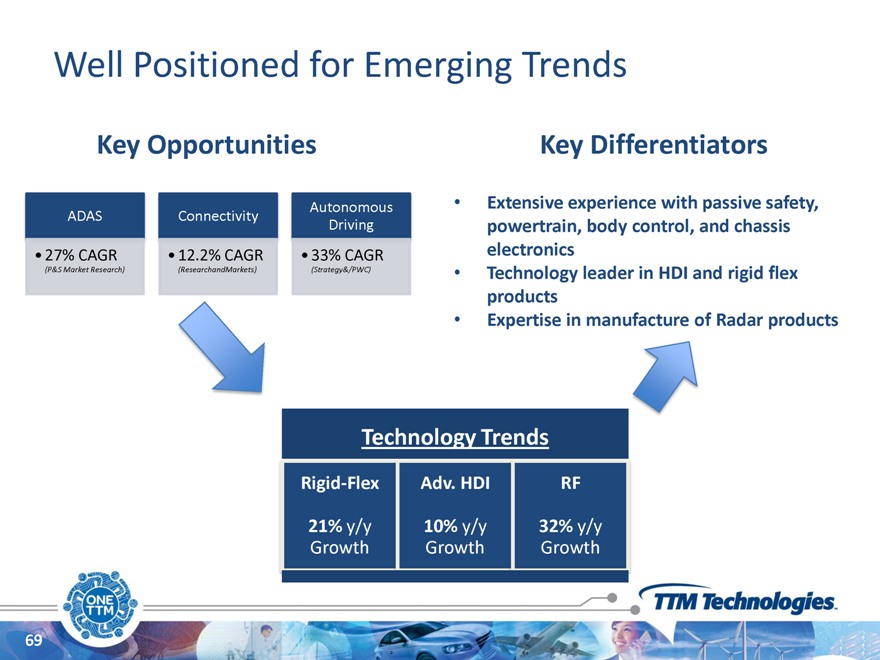

Well Positioned for Emerging Trends

Key Opportunities Key Differentiators

ADAS Connectivity Autonomous Extensive experience with passive safety, Driving powertrain, body control, and chassis

27% CAGR 12.2% CAGR 33% CAGR electronics

(P&S Market Research) (ResearchandMarkets) (Strategy&/PWC) Technology leader in HDI and rigid flex

products

Expertise in manufacture of Radar products

Technology Trends

Rigid-Flex Adv. HDI RF

21% y/y 10% y/y 32% y/y Growth Growth Growth

69

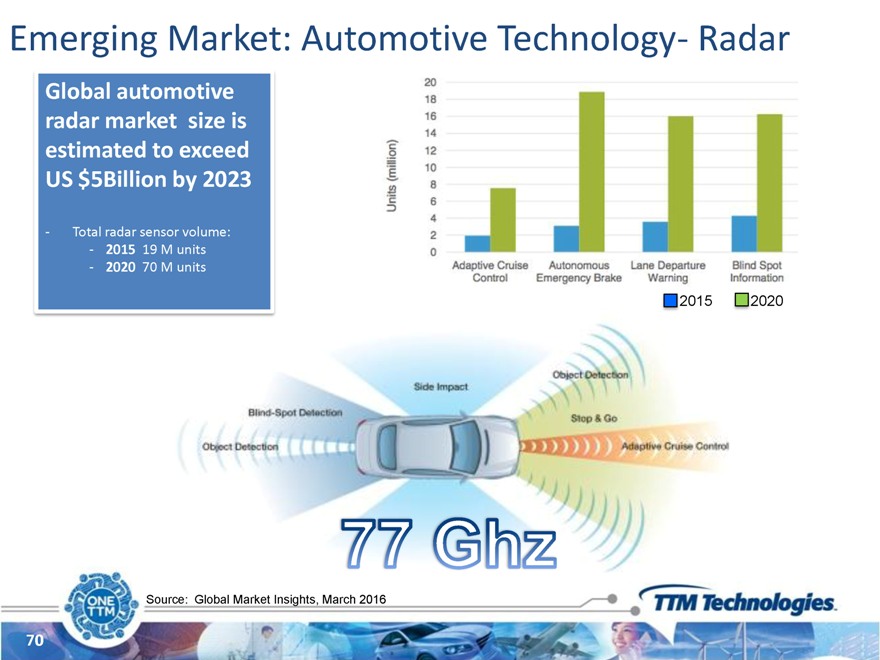

Emerging Market: Automotive Technology- Radar

Global automotive radar market size is estimated to exceed US $5Billion by 2023

- Total radar sensor volume:

- 2015 19 M units

- 2020 70 M units

2015 2020

Source: Global Market Insights, March 2016

70

Success Story: Autoliv

Multiple products including: Airbag, braking, Radar & camera

New product launch 2016: 77Ghz (advanced radar detection)

Major Customers: GM, Hyundai, Honda, VW, Mercedes, & Chrysler Designed in North America

pre-production in North America; seamless transfer to Asia Pacific for production

We won because TTM was able to offer a full-service solution, from concept to completion.

71

Medical, Industrial and Instrumentation

Growth Opportunities: Medical, Industrial & Instrumentation

Surgical Robotics $17.9B by 2020

12.7% CAGR through 2020

(Grand View Research, Inc.)

Home Automation (IoT) $12.8B by 2020

11.4% CAGR through 2020

(MarketsandMarkets)

Automated Test Equipment $4.4B by 2020

2.5% CAGR through 2020

(Radiant Insights)

73

MII PCB Market Growth 4-5%

CAGR 2015-2020

Strength of product offering and technical expertise

Growth for high reliability medical systems correlates to higher procedure rates and aging populations

73

Seamless Transition Wins MI&I Business

Medical Device Company specializing in ``continuous” glucose monitoring systems

Small wearable device — smart device compatible Development initiated in Sterling and seamlessly migrated to Toronto; FDA approval required Patient monitoring systems are expected to grow at a CAGR of 5.6% from 2015 – 2020

(markets and markets)

TTM won because we can support the entire product life cycle— in North America.

74

AMI&I Growth Opportunities

Increasing Auto PCB content with focus on faster growing Electric

Vehicles, ADAS, and Infotainment.

In Medical, focus on surgical robotics and patient monitoring.

In industrial, focus on automation, robotics, and home connectivity.

Why AMI&I Wins

One Stop, Highly Customized, Global Solutions

Trusted High-Reliability

Supplier

Proven Track Record with Top Automotive and Medical OEMs

75

Diversified, Disciplined and Deleveraging

Todd Schull

Agenda

Via Integration/Cost Improvement P&L Operating Model Cash Flow/Deleveraging Model

77

Via Integration Review

What we said last year

Increased scale

Increased auto exposure New BU operating model

Expect $55 million synergies by Q2 16 Pay down debt

78

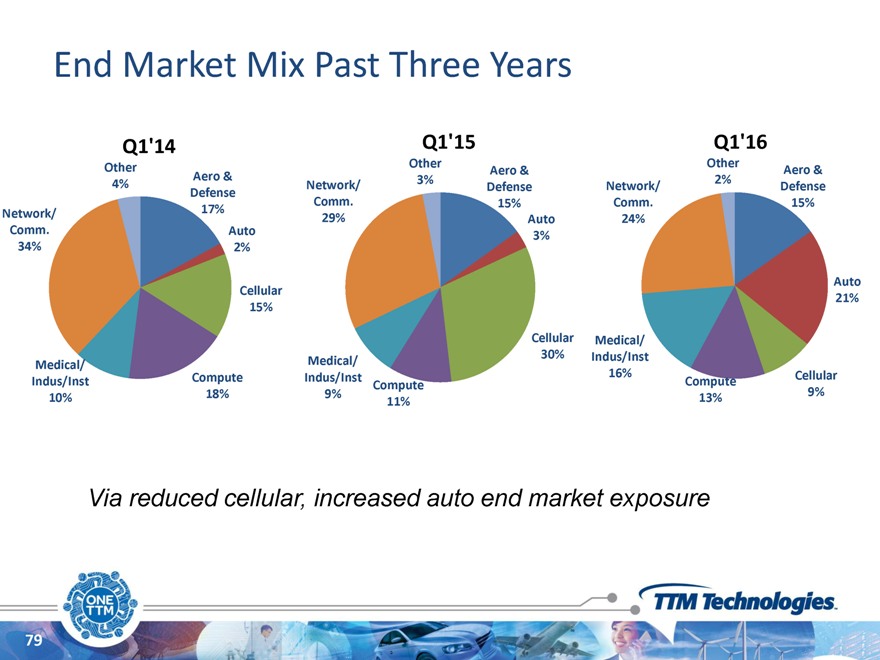

End Market Mix Past Three Years

Q1’14 Q1’15 Q1’16

Other Other Other

Aero & Aero & Aero & 3% 2%

4% Network/ Defense Network/ Defense Defense Comm. 15% Comm. 15% Network/ 17% 29% Auto 24% Comm. Auto 3% 34% 2%

Auto Cellular 21% 15%

Cellular Medical/ 30% Indus/Inst Medical/ Medical/

Compute Indus/Inst 16% Cellular Indus/Inst Compute Compute 9% 10% 18% 9% 13% 11%

Via reduced cellular, increased auto end market exposure

79

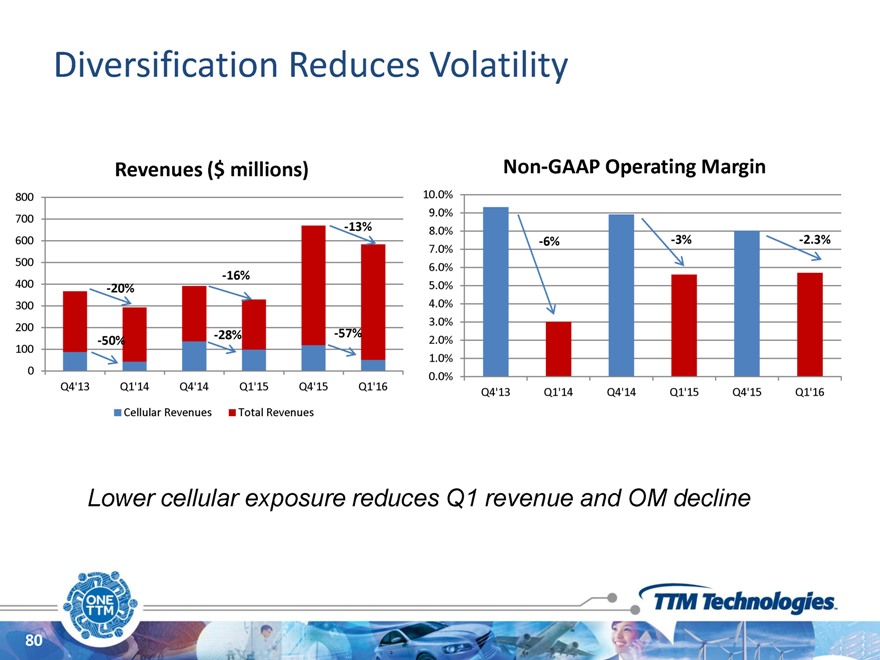

Diversification Reduces Volatility

Revenues ($ millions) Non-GAAP Operating Margin

800 10.0%

9.0% 700

-13% 8.0%

600 7.0% -6% -3% -2.3%

500

6.0%

-16%

400 -20% 5.0% 300 4.0%

3.0% 200

-28% -57%

100 -50% 2.0%

1.0% 0

0.0% Q4’13 Q1’14 Q4’14 Q1’15 Q4’15 Q1’16

Q4’13 Q1’14 Q4’14 Q1’15 Q4’15 Q1’16 Cellular Revenues Total Revenues

Lower cellular exposure reduces Q1 revenue and OM decline

80

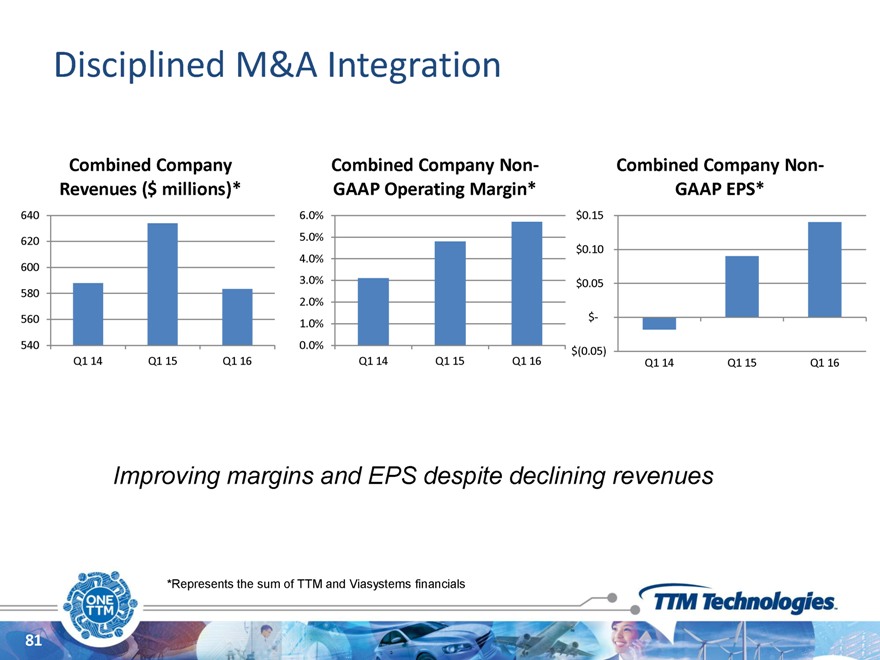

Disciplined M&A Integration

Combined Company Combined Company Non- Combined Company Non-Revenues ($ millions)* GAAP Operating Margin* GAAP EPS*

640 6.0% $0.15

620 5.0%

4.0% $0.10 600

3.0% $0.05 580 2.0%

560 $-

1.0%

540 0.0% $(0.05)

Q1 14 Q1 15 Q1 16 Q1 14 Q1 15 Q1 16 Q1 14 Q1 15 Q1 16

Improving margins and EPS despite declining revenues

*Represents the sum of TTM and Viasystems financials

81

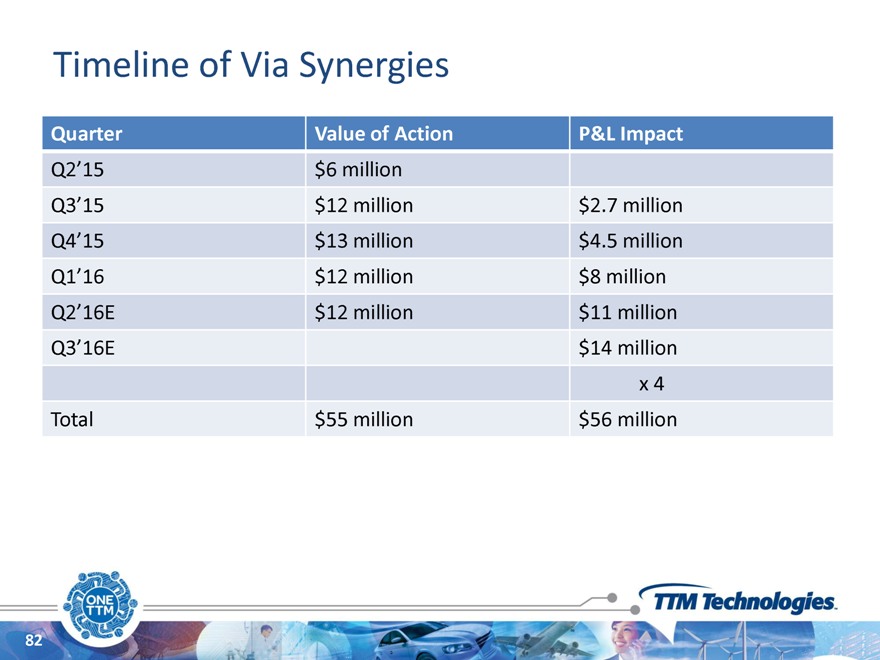

Timeline of Via Synergies

Quarter Value of Action P&L Impact

Q2’15 $6 million

Q3’15 $12 million $2.7 million Q4’15 $13 million $4.5 million Q1’16 $12 million $8 million Q2’16E $12 million $11 million Q3’16E $14 million x 4

Total $55 million $56 million

82

Post Via—Continuous Cost Improvement

Supply chain management

Alternate suppliers Price reductions

Best practice sharing

Materials usage reduction Process improvement

Margin improvement

Yield/Scrap improvement Productivity improvement

G&A efficiencies

Shared services ERP

83

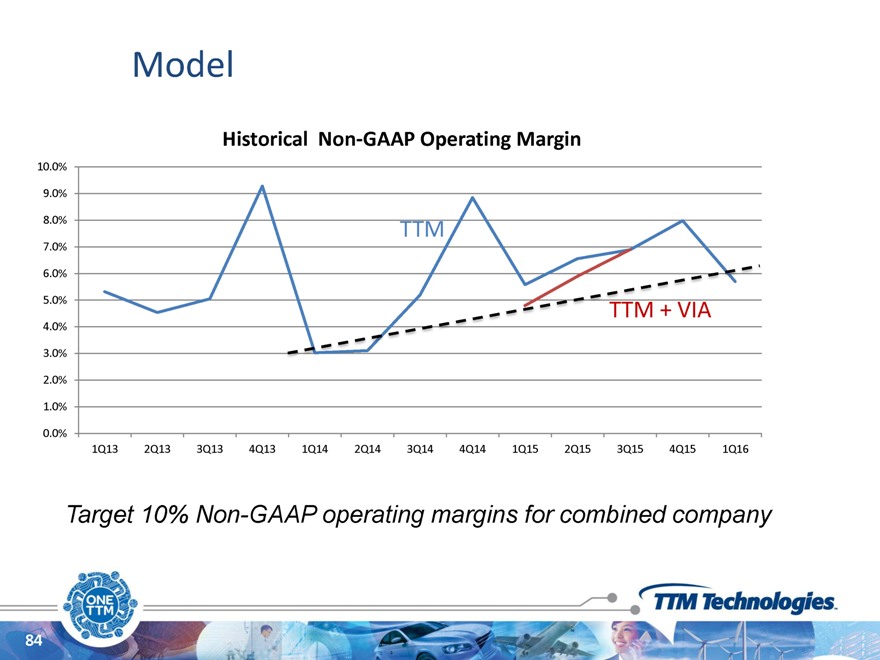

Operating Model

Historical Non-GAAP Operating Margin

10.0% 9.0%

8.0% TTM 7.0%

6.0% 5.0% 4.0% 3.0% 2.0% 1.0%

0.0%

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16

Target 10% Non-GAAP operating margins for combined company

84

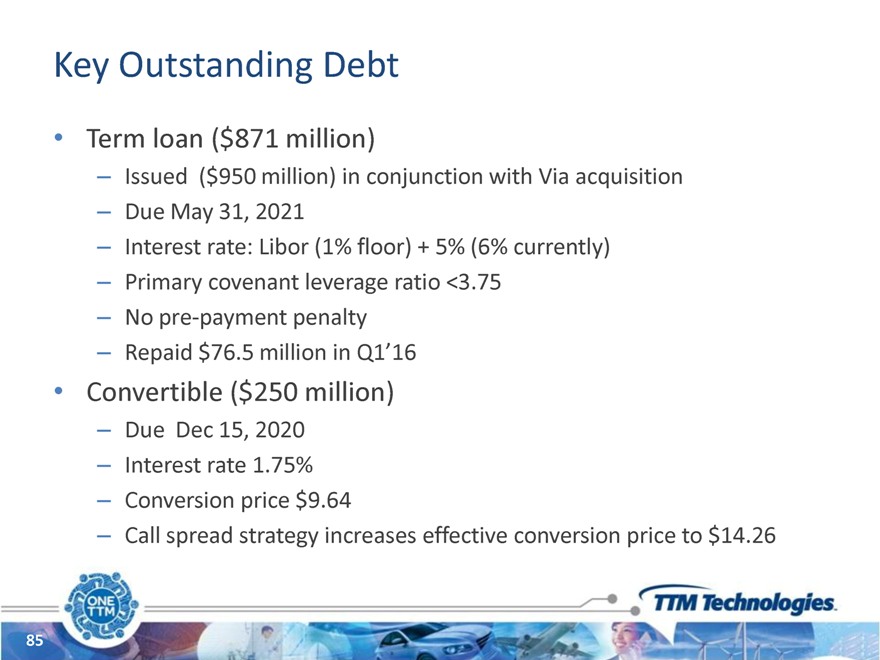

Key Outstanding Debt

Term loan ($871 million)

Issued ($950 million) in conjunction with Via acquisition Due May 31, 2021 Interest rate: Libor (1% floor) + 5% (6% currently) Primary covenant leverage ratio <3.75 No pre-payment penalty

Repaid $76.5 million in Q1’16

Convertible ($250 million)

Due Dec 15, 2020 Interest rate 1.75% Conversion price $9.64

Call spread strategy increases effective conversion price to $14.26

85

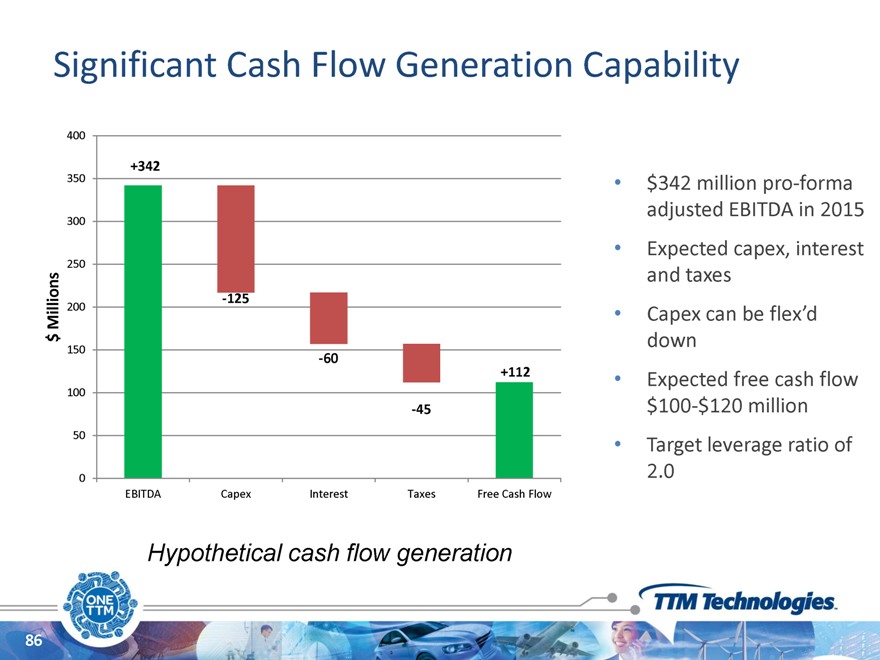

Significant Cash Flow Generation Capability

400

+342

350 • $342 million pro-forma

300 adjusted EBITDA in 2015

Expected capex, interest

250

and taxes

-125

Millions 200 • Capex can be flex’d $ down

150

-60

+112 • Expected free cash flow 100 $100-$120 million

-45

50 •

Target leverage ratio of

0 2.0

EBITDA Capex Interest Taxes Free Cash Flow

Hypothetical cash flow generation

86

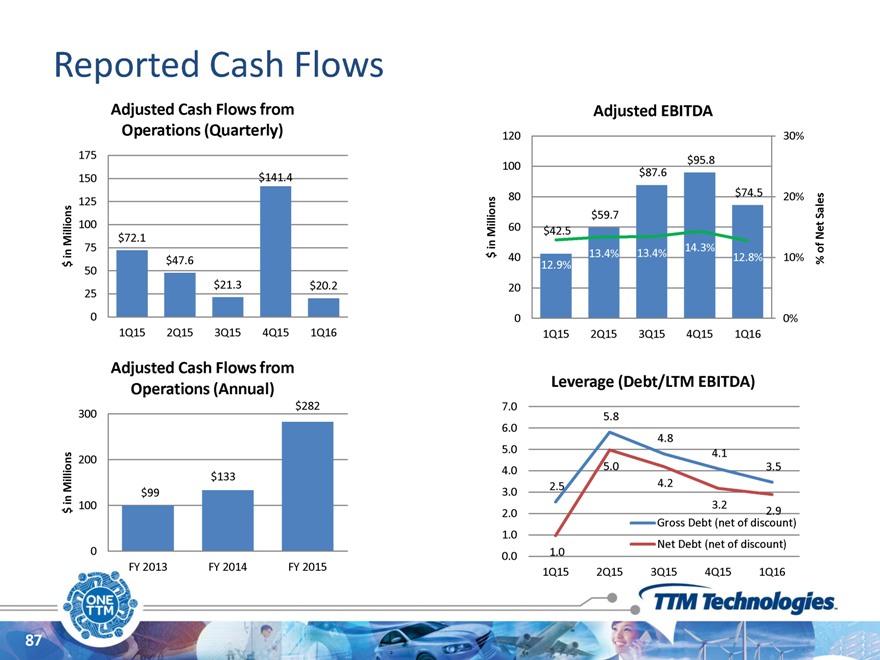

Reported Cash Flows

Adjusted Cash Flows from Adjusted EBITDA

Operations (Quarterly) 120 30%

175

$95.8 100

$87.6 150 $141.4

$74.5 125 80 20%

Sales

100 $59.7 Millions 60 $42.5 Net Millions $72.1 75 in 14.3% of in $ 13.4% 13.4%

$ $47.6 40 12.9% 12.8% 10% % 50

25 $21.3 $20.2 20

0 0 0% 1Q15 2Q15 3Q15 4Q15 1Q16 1Q15 2Q15 3Q15 4Q15 1Q16

Adjusted Cash Flows from

Leverage (Debt/LTM EBITDA) Operations (Annual)

$282 7.0

300 5.8 6.0

4.8

5.0 4.1 200

4.0 5.0 3.5 $133

Millions 2.5 4.2 in $99 3.0 $ 100 3.2 2.9 2.0 Gross Debt (net of discount) 1.0 Net Debt (net of discount)

0 1.0 0.0 FY 2013 FY 2014 FY 2015

1Q15 2Q15 3Q15 4Q15 1Q16

87

Future Priorities for Cash Flow Generation

Generate Cash from Operations – Grow Earnings

Execution

Synergies

Generate Cash through Asset Efficiency

Deleverage our Balance Sheet – More Cash for Shareholders

88

Conclusions

Successful Via integration – Improved cost structure

Continuous focus on cost reduction and cash flow generation

Solid cash flow capability for deleveraging

89

Thank You

Reconciliations

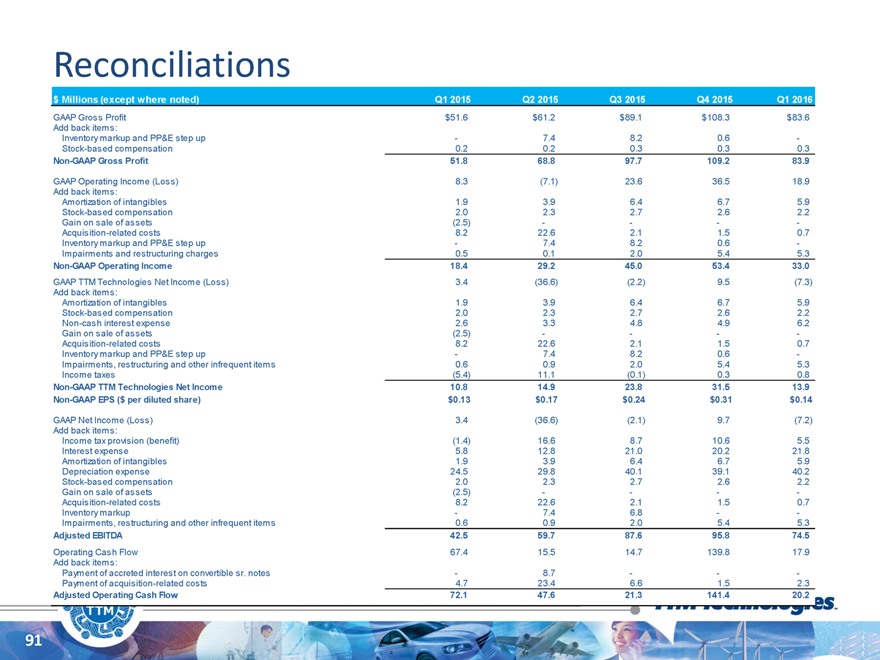

$ Millions (except where noted) Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016

GAAP Gross Profit $51.6 $61.2 $89.1 $108.3 $83.6

Add back items:

Inventory markup and PP&E step up — 7.4 8.2 0.6 -

Stock-based compensation 0.2 0.2 0.3 0.3 0.3

Non-GAAP Gross Profit 51.8 68.8 97.7 109.2 83.9

GAAP Operating Income (Loss) 8.3 (7.1) 23.6 36.5 18.9

Add back items:

Amortization of intangibles 1.9 3.9 6.4 6.7 5.9

Stock-based compensation 2.0 2.3 2.7 2.6 2.2

Gain on sale of assets (2.5) ——— -

Acquisition-related costs 8.2 22.6 2.1 1.5 0.7

Inventory markup and PP&E step up — 7.4 8.2 0.6 -

Impairments and restructuring charges 0.5 0.1 2.0 5.4 5.3

Non-GAAP Operating Income 18.4 29.2 45.0 53.4 33.0

GAAP TTM Technologies Net Income (Loss) 3.4 (36.6) (2.2) 9.5 (7.3)

Add back items:

Amortization of intangibles 1.9 3.9 6.4 6.7 5.9

Stock-based compensation 2.0 2.3 2.7 2.6 2.2

Non-cash interest expense 2.6 3.3 4.8 4.9 6.2

Gain on sale of assets (2.5) ——— -

Acquisition-related costs 8.2 22.6 2.1 1.5 0.7

Inventory markup and PP&E step up — 7.4 8.2 0.6 -

Impairments, restructuring and other infrequent items 0.6 0.9 2.0 5.4 5.3

Income taxes (5.4) 11.1 (0.1) 0.3 0.8

Non-GAAP TTM Technologies Net Income 10.8 14.9 23.8 31.5 13.9

Non-GAAP EPS ($ per diluted share) $0.13 $0.17 $0.24 $0.31 $0.14

GAAP Net Income (Loss) 3.4 (36.6) (2.1) 9.7 (7.2)

Add back items:

Income tax provision (benefit) (1.4) 16.6 8.7 10.6 5.5

Interest expense 5.8 12.8 21.0 20.2 21.8

Amortization of intangibles 1.9 3.9 6.4 6.7 5.9

Depreciation expense 24.5 29.8 40.1 39.1 40.2

Stock-based compensation 2.0 2.3 2.7 2.6 2.2

Gain on sale of assets (2.5) ——— -

Acquisition-related costs 8.2 22.6 2.1 1.5 0.7

Inventory markup — 7.4 6.8 — -

Impairments, restructuring and other infrequent items 0.6 0.9 2.0 5.4 5.3

Adjusted EBITDA 42.5 59.7 87.6 95.8 74.5

Operating Cash Flow 67.4 15.5 14.7 139.8 17.9

Add back items:

Payment of accreted interest on convertible sr. notes — 8.7 —— -

Payment of acquisition-related costs 4.7 23.4 6.6 1.5 2.3

Adjusted Operating Cash Flow 72.1 47.6 21.3 141.4 20.2

91

Reconciliations

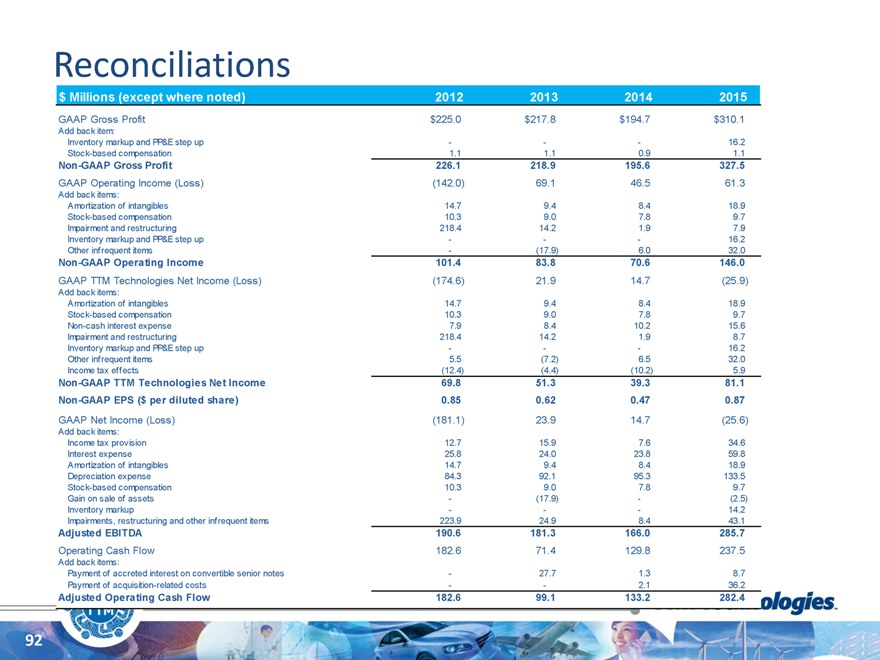

$ Millions (except where noted) 2012 2013 2014 2015

GAAP Gross Profit $225.0 $217.8 $194.7 $310.1

Add back item:

Inventory markup and PP&E step up ——— 16.2

Stock-based compensation 1.1 1.1 0.9 1.1

Non-GAAP Gross Profit 226.1 218.9 195.6 327.5

GAAP Operating Income (Loss) (142.0) 69.1 46.5 61.3

Add back items:

Amortization of intangibles 14.7 9.4 8.4 18.9

Stock-based compensation 10.3 9.0 7.8 9.7

Impairment and restructuring 218.4 14.2 1.9 7.9

Inventory markup and PP&E step up ——— 16.2

Other infrequent items — (17.9) 6.0 32.0

Non-GAAP Operating Income 101.4 83.8 70.6 146.0

GAAP TTM Technologies Net Income (Loss) (174.6) 21.9 14.7 (25.9)

Add back items:

Amortization of intangibles 14.7 9.4 8.4 18.9

Stock-based compensation 10.3 9.0 7.8 9.7

Non-cash interest expense 7.9 8.4 10.2 15.6

Impairment and restructuring 218.4 14.2 1.9 8.7

Inventory markup and PP&E step up ——— 16.2

Other infrequent items 5.5 (7.2) 6.5 32.0

Income tax effects (12.4) (4.4) (10.2) 5.9

Non-GAAP TTM Technologies Net Income 69.8 51.3 39.3 81.1

Non-GAAP EPS ($ per diluted share) 0.85 0.62 0.47 0.87

GAAP Net Income (Loss) (181.1) 23.9 14.7 (25.6)

Add back items:

Income tax provision 12.7 15.9 7.6 34.6

Interest expense 25.8 24.0 23.8 59.8

Amortization of intangibles 14.7 9.4 8.4 18.9

Depreciation expense 84.3 92.1 95.3 133.5

Stock-based compensation 10.3 9.0 7.8 9.7

Gain on sale of assets — (17.9) — (2.5)

Inventory markup ——— 14.2

Impairments, restructuring and other infrequent items 223.9 24.9 8.4 43.1

Adjusted EBITDA 190.6 181.3 166.0 285.7

Operating Cash Flow 182.6 71.4 129.8 237.5

Add back items:

Payment of accreted interest on convertible senior notes — 27.7 1.3 8.7

Payment of acquisition-related costs —— 2.1 36.2

Adjusted Operating Cash Flow 182.6 99.1 133.2 282.4

92