| Filed by Embraer-Empresa Brasileira de Aeronáutica S.A. |

| Pursuant to Rule 425 under the Securities Act of 1933 |

|

|

| Subject Company: Embraer-Empresa Brasileira de Aeronáutica S.A. |

| Commission File No. 1-15102 |

In connection with the proposed restructuring (the “Restructuring”), Embraer and Rio Han will file important documents with the SEC. Investors and security holders are urged to carefully read these documents when they become available, because they will contain important information. Investors and security holders may obtain copies of these documents for free, when available, at the SEC’s web site at www.sec.gov, as well as from Embraer’s web site at www.embraer.com, or by requesting such documents from Embraer at Av. Brigadeiro Faria Lima, 2,170, 12227-901 São José dos Campos, SP, Brazil, Attention: Anna Cecilia Bettencourt (telephone 55-12-3927-4404; fax 55-12-3922-6070; email: investor.relations@embraer.com.br).

The documents attached hereto may include forward-looking statements or statements about events or circumstances which have not occurred. These forward-looking statements include, but are not limited to, statements regarding the (i) timing of the meeting of Embraer shareholders and the approval of the Restructuring by such shareholders, (ii) expected changes that may be necessary if the Restructuring is effected, and (iii) benefits of the implementation of the Restructuring to Embraer and Embraer shareholders, including statements regarding enhanced access to capital markets and financing resources for future new program developments, and statements regarding the dispersed ownership and increased liquidity of Rio Han common shares, as well as the possible effects thereof on the market capitalization of Rio Han. The company has based these forward-looking statements largely on its current expectations about the Restructuring, its implementation and the consequences arising therefrom. These forward-looking statements are subject to risks, uncertainties and assumptions, including, among other things: the non-approval of the Restructuring by Embraer shareholders; political and business conditions, both in Brazil and in Embraer’s markets; and existing and future government regulations in Brazil and abroad.

The words “believes,” “may,” “will,” “estimates,” “continues,” “anticipates,” “intends,” “expects” and similar words are intended to identify forward-looking statements. Embraer and Rio Han undertake no obligation to update publicly or revise any forward-looking statements because of new information, future events or other factors. In light of these risks and uncertainties, the forward-looking events and circumstances discussed in this communication might not occur. Actual results could differ substantially from those anticipated in the forward-looking statements.

TABLE OF CONTENTS

1. | Notice to the Market (of material fact) dated January 19, 2006. |

|

|

2. | Descriptive Memorandum of the Transaction and exhibits thereto. |

|

|

3. | Merger Agreement and exhibits thereto. |

|

|

4. | Minutes of the Meeting of the Board of Directors held on January 19, 2006. |

|

|

5. | Minutes of the Meeting of the Conselho Fiscal (Fiscal Council) held on January 19, 2006. |

|

|

6. | Call Notice regarding Shareholders’ Meeting to be held on March 31, 2006. |

Free Translation

from the Portuguese

Embraer – Empresa Brasileira de Aeronáutica S.A. |

|

CNPJ/MF no. 60.208.493/0001-81 |

|

NIRE no. 35.300.026.420 |

|

Public Company |

NOTICE TO THE MARKET

(of material fact)

Embraer – Empresa Brasileira de Aeronáutica S.A. (“Embraer”, “Company” or “Merged Company”), pursuant to paragraph 4 of article 157 of Law 6,404/76 and CVM Instructions 319/99 and 358/02, and in addition to the Notice to the Market published on January 16, hereby informs to the shareholders and the market that the Company’s management will submit for the approval of all its shareholders, regardless of the type of shares held, the proposal for its corporate restructuring, as presented below (the “Restructuring”).

In addition to the information herein, Embraer recommends the reading of the Descriptive Memorandum of the Transaction and further ancillary documents that present the Restructuring, which include detailed information on the matters addressed hereunder. Such documents are available for the shareholders at the Company’s head offices and on the website www.embraer.com.br. The administration of the Company has requested legal opinions from the most renowned Brazilian scholars, in order to provide legal support to the proposed Restructuring. At the time such legal opinions are delivered to the Company, they will be disclosed and available to all shareholders at the head offices of Embraer or on the website www.embraer.com.br.

1. OBJECTIVE OF THE PROPOSAL

As detailed in Item 2 below, the proposed Restructuring to be submitted to the shareholders of the Company aims to create a basis for the sustainability, growth and continuity of the Company’s businesses and activities, as its implementation will assure the Company’s improved access to the capital markets and the increase of its financing capacity and development of expansion programs.

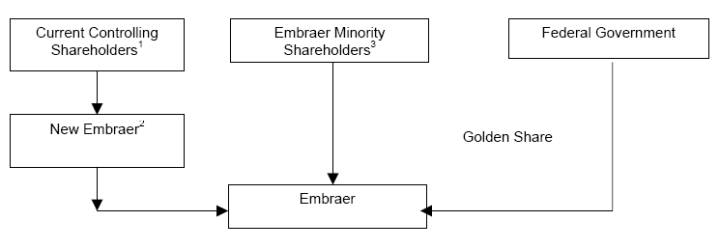

The Restructuring includes the merger of Embraer with and into Rio Han Empreendimentos e Participações S.A. (the “Merger”), a corporation with head offices in the City of São José dos Campos, State of São Paulo, Avenida Brigadeiro Faria Lima, n.º 2170, Prédio F56, ground floor, room 2565, enrolled in the CNPJ/MF under no. 07.689.002/0001-89, with its acts of incorporation registered with the Commercial Registry of the State of São Paulo – JUCESP under NIRE 35.300.325.761 (“Rio Han”, “Mergor Company” or “New Embraer”), organized with the specific purpose to act as a vehicle in the Restructuring process. As a result of the Merger, Embraer will cease to exist and, consequently, all shares issued by it will cease to be outstanding, and the Company’s shareholders will receive common shares issued by Rio Han. The golden share issued by Embraer to, and held by, the Federal Government (the “Golden Share”) will be replaced by another golden share to be issued by Rio Han.

The Restructuring will result in higher liquidity to all shareholders of Embraer, who will benefit from the potential increase of the market value of their shares and improvement of the current corporate governance standards to be adopted by the Company, which include, among others, the extension of voting rights to all shareholders of New Embraer.

Upon conclusion of the Restructuring, New Embraer, as successor of the Company, will request its registration as a public company with the Comissão de Valores Mobiliários – CVM, its listing on the Novo Mercado segment of the São Paulo Stock Exchange (“BOVESPA”), as well as the listing of its American Depositary Shares (“ADS”) on the New York Stock Exchange - NYSE. New Embraer will become the largest Brazilian public company with dispersed corporate control and majority of voting rights necessarily held by Brazilian shareholders. As holder of the Golden Share, the Federal Government will be assured maintenance of its special rights, which were granted in order to preserve Brazil’s strategic interests inherent in the Company’s business activities.

Reference to shares issued by the Company and shares not subject to the Embraer Shareholders’ Agreement shall be deemed to include American Depositary Shares (“ADS”) issued under Embraer’s American Depositary Receipt (“ADR”) program. References to Embraer shareholders shall be deemed to also include holders of Embraer ADS.

2

2. THE RESTRUCTURING AND ITS STAGES

2.1. RIO HAN’S INCORPORATION AND CAPITALIZATION

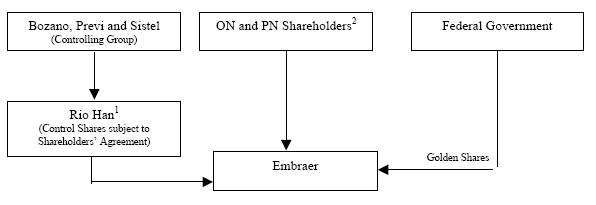

Rio Han is a companhia fechada (a “closed” company), whose only shareholders are Cia. Bozano, Caixa de Previdência dos Funcionários do Banco do Brasil – PREVI and Fundação Sistel de Seguridade Social, the current controlling shareholders of Embraer (the “Current Controlling Shareholders”). Rio Han holds 60% of Embraer’s voting capital and 20.16% of its total capital, in accordance with the chart below.

1. | Shares of the Current Controlling Shareholders subject to the Shareholders’ Agreement. |

|

|

2. | Embraer’s shares transferred to Rio Han as a result of the capital increase. |

|

|

3. | All other common and preferred shares, including those of Bozano, Previ and Sistel, not subject to the Shareholders’ Agreement and those subject to the Embraer ADR program. |

Rio Han has the specific purpose to serve as a vehicle for the transaction and (i) hold the 145,527,000 common shares issued by Embraer and transferred by its Current Controlling Shareholders, all subject to the Shareholders’ Agreement dated July 24, 1997, as amended (the “Control Shares” and the “Shareholders’ Agreement”, respectively) and, (ii) in the event the Restructuring proposal is approved, Rio Han will merge with, and become the successor of, Embraer.

On January 18, 2005, the Control Shares were contributed to the capital of Rio Han, and each one of the Current Controlling Shareholders received 1.1153 common shares issued by Rio Han for each Control Share contributed into Rio Han’s capital, for a total of 162,306,263 new common shares issued by Rio Han. On the date hereof, the capital stock of Rio Han is comprised as follows:

Shareholder |

| Number of common |

| Percentage |

| ||

|

|

| |||||

Bozano |

|

| 54,102,501 |

|

| 33.33 | % |

Previ |

|

| 54,102,131 |

|

| 33.33 | % |

Sistel |

|

| 54,102,131 |

|

| 33.33 | % |

Total |

|

| 162,306,763 |

|

| 100 | % |

*. Includes 168 shares of Rio Han held by Bozano, 166 held by Sistel and 166 held by Previ. |

3

2.2. THE MERGER PROPOSAL:

On January 19, 2006, the Board of Directors of Embraer approved the proposal presented by the Executive Committee regarding the Merger of the Company with and into Rio Han, in accordance with the Protocol of Justification and Merger (“Merger Agreement”), as executed by the managements of Rio Han and Embraer on that same date.

On the same occasion, the Board of Directors of Embraer approved the calling of the Company’s General Shareholders’ Meeting, to be held on March 31, 2006, in accordance with the call notice to be published on a future date. Nonetheless, the Board of Directors of the Company may decide, until March 24, 2006, to postpone such General Shareholders’ Meeting, since the effective holding of the Meeting is conditioned upon registration with the U.S. Securities and Exchange Commission (“SEC”), as described in item 8 below.

When deciding on the proposal for the Merger of the Company with and into Rio Han, the shareholders will discuss and analyze the terms of the Merger Agreement and all exhibits thereto, which include the proposal for amendment to the By-Laws of New Embraer, which will become effective immediately after approval of the Restructuring. Additionally, Embraer’s shareholders will also analyze the proposals to: (i) include a temporary provision in the By-Laws of the Company, entitling all shareholders the right to vote in such General Shareholders’ Meeting, as detailed in item 2.3 below; (ii) ratify the appointment of the specialized companies that are responsible for the preparation of the valuations of the Company under different criteria; and (iii) approve the valuations prepared by the specialized companies mentioned in item (ii) above.

The Merger proposal and the terms of the Merger Agreement, including all exhibits thereto, were approved by all members of the Conselho Fiscal (Fiscal Council) of Embraer, at the meeting held on January 19, 2006.

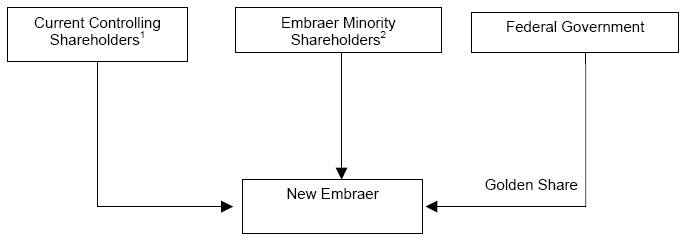

Upon approval of the Merger, both the Shareholders’ Agreement and Embraer will automatically cease to exist and Embraer’s shareholders and ADS holders, regardless of the type of shares held, will receive, respectively, common shares and ADS issued by New Embraer, in accordance with the exchange ratio indicated in item 5.2 below. The Golden Share held by the Federal Government will be replaced by another golden share issued by New Embraer. The chart below sets forth the capital composition of New Embraer after approval of the Restructuring:

4

1. | New Embraer’s shares, received by the Current Controlling Shareholders in exchange for the transfer to Rio Han of the shares issued by Embraer subject to the Shareholders’ Agreement. |

|

|

2. | New Embraer’s shares received by the other preferred and common shareholders of Embraer, including Bozano, Previ and Sistel, not bound to the Shareholders’ Agreement and subject to the Embraer ADR program. |

2.3. PROCEDURES FOR VOTING ON THE RESTRUCTURING PROPOSAL AT THE GENERAL SHAREHOLDERS’ MEETING OF EMBRAER:

In accordance with the recommendations of CVM relating to corporate governance practices and in order to allow greater transparency to the voting process, the Restructuring proposal will be submitted to all shareholders of the Company for approval, regardless of the type of shares held by them, in two different stages, subject to the veto right granted to the Federal Government, as holder of the Golden Share.

First, the Restructuring proposal will be submitted for approval by all shareholders of the Company – including the ADR Program depositary bank, which will vote as instructed by ADS holders but excluding Rio Han and the Current Controlling Shareholders, which will not vote in this first voting stage.

5

In the event that the Restructuring proposal is rejected in this first voting stage, by the shareholders (including ADS holders) representing the majority of the outstanding shares (i.e., all common and preferred shares issued by the Company outstanding in the market, excluding those held by the management of Embraer, by Rio Han and by the Current Controlling Shareholders whether or not subject to the Shareholders’ Agreement), the Current Controlling Shareholders will vote against the approval of the Restructuring. In case the Restructuring proposal is not rejected in the first voting stage by the majority of the Company’s outstanding shares, Rio Han and the Controlling Shareholders will vote on the Restructuring proposal at their discretion.

In order to allow the implementation of the voting procedure described above, an amendment to Embraer’s By-Laws will be submitted to the Company’s General Shareholders’ Meeting called to consider and vote on the Restructuring proposal, in order to provide for the inclusion of a temporary provision with limited validity.

3. RATIONALE, PURPOSES AND BENEFITs ARISING FROM THE RESTRUCTURING:

The main goal of the Restructuring is to create a basis for the sustainability, growth and continuity of Embraer’s businesses and activities, through its successor, New Embraer. These goals will be reached through improved access by New Embraer to the capital markets, upon expansion of its capacity to raise funds for the development of products and business or market expansion programs. Furthermore, the Restructuring will result in the strengthening and independence of New Embraer’s management, thus benefiting all shareholders through the adoption of more comprehensive corporate governance practices. The Restructuring will specifically result in several advantages to all parties involved, as follows:

3.1. BENEFITS TO THE COMPANY AFTER THE RESTRUCTURING, UNDER THE LEGAL STRUCTURE OF THE SUCCEEDING COMPANY, NEW EMBRAER:

|

|

|

| • | Enhancement of the capacity to fund the expansion of New Embraer’s programs due to improved access to the capital markets, currently limited because of: (i) the share control structure of the Company; and (ii) the maximum proportion allowed by the Brazilian Corporation Law between common and preferred shares; and |

|

|

|

| • | Possibility to use New Embraer’s shares as an acquisition currency for assets, which shall enable its potential international expansion. |

6

3.2. BENEFITS TO EMBRAER’S CURRENT SHAREHOLDERS:

| • | Extension of voting rights to all shareholders – including to the ADR program depositary, which will vote as instructed by ADS holders – since the shares of New Embraer will be common shares, thus allowing New Embraer’s admission to BOVESPA’s Novo Mercado segment; |

|

|

|

| • | Potential liquidity increase of the shares, thus impacting their quotation in the stock exchanges; |

|

|

|

| • | Improvement of the corporate governance practices and higher transparency in the management of New Embraer; and |

|

|

|

| • | For the Current Controlling Shareholders, establishment of a premium for the termination of the Shareholders’ Agreement and relinquishment of control of the Company. Based on the Restructuring proposal, the premium will be granted to the Control Shares upon the attribution of a differentiated exchange ratio for purposes of the transfer thereof to Rio Han on the capital increase when compared to that attributed to the other shares issued by Embraer at the time of the Merger. |

3.3.BENEFITS TO THE BRAZILIAN CAPITAL MARKETS:

| • | The first major Brazilian company with dispersed corporate control and adequate structure to adhere to BOVESPA’s Novo Mercado, creating a standard that may be used as a model for similar transactions; and |

|

|

|

| • | Creation of a new corporate governance benchmark. |

3.4. BENEFITS TO THE FEDERAL GOVERNMENT:

| • | Maintenance of the Golden Share with the previously attributed rights and improvement of their exercise; |

|

|

|

| • | Assurance of the majority of voting rights held by Brazilian shareholders, through the limitation of foreign shareholders’ voting rights set forth in the By-Laws of New Embraer, in order to maintain the principle established in the Privatization Notice; |

|

|

|

| • | Control over the concentration of an equity interest in the capital stock of New Embraer equal to or greater than 35%; |

7

| • | Statutory assurance of maintenance of a capital dispersion structure, due to the adoption of mechanisms restricting the number of votes to be cast by each shareholder or group of shareholders; and |

|

|

|

| • | Assurance of New Embraer’s continuance as the technological and industrial support of the Brazilian Army strategic actions, taking into consideration the maintenance of the control of New Embraer with Brazilian shareholders and the strengthening of the rights of the Golden Share. |

4. BY-LAWS OF NEW EMBRAER

The proposed Amendment to the By-Laws of New Embraer, attached to the Merger Agreement, to be submitted to the Company’s General Shareholders’ Meeting that will decide on the Restructuring, will include the provisions necessary to ensure, among other measures described herein: (i) the adoption of the best practices of corporate governance; (ii) the maintenance of the shareholding control dispersion among its shareholders; and (iii) the limitation to the participation of foreign shareholders in the shareholder deliberations, thus ensuring that the Brazilian shareholders will maintain the majority of the voting rights therein, in accordance with the restrictions created as part of the Company’s privatization.

Some of the main provisions included in the proposed Amendment to the By-Laws of New Embraer, which were created to allow the Restructuring, are listed herein.

For a more detailed description, the Descriptive Memorandum of the Transaction and the Proposal for Amendment of New Embraer’s By-Laws, attached to the Merger Agreement as Exhibit V and available at the Company’s head office and on the website www.embraer.com.br, should be analized.

4.1. GENERAL LIMITATION ON THE EXERCISE OF VOTING RIGHTS AT GENERAL MEETINGS:

The maximum number of votes allowed to any shareholder (or group of shareholders) at any General Shareholders’ Meeting of New Embraer will correspond to 5% of the capital stock, regardless of the number of shares or ADS held by such shareholder. This measure, based on article 110, paragraph 1 of Law 6,404/76, intends to avoid the excessive concentration of shares in the hands of a shareholder or group of shareholders.

In conformity with the privileges granted to the Golden Share, which aims to avoid the excessive concentration of shares in the hands of one shareholder or group of shareholders, as set forth in Item 4.3 hereunder, this restriction does not impose any limitation on the ownership of shares or on the economic rights of the shares, including in relation to the distribution of dividends.

8

4.2. LIMITATION ON THE EXERCISE OF THE VOTING RIGHTS OF FOREIGN SHAREHOLDERS AT THE GENERAL SHAREHOLDERS’ MEETINGS:

In addition to the limitation imposed on all shareholders of New Embraer described above, the total votes that may be cast by foreign shareholders, individually or collectively, in any General Shareholders’ Meeting, will be limited to 40% of the total votes present at such meeting.

The inclusion of such limitation in the By-Laws of New Embraer takes into consideration the principles established in the Embraer Privatization Notice, as published in the Official Gazette dated April 4, 1994. Such orientation was ratified by the Attorney General’s Office in the Opinion GQ-215, of January 6, 2000 and approved by the Presidency of the Federative Republic of Brazil on January 17, 2000, according to the order published in the Official Gazette dated January 20, 2000, which limits the participation of foreign shareholders to 40% of Embraer’s voting capital.

Therefore, the limitation on the exercise of the political rights by foreign shareholders of New Embraer will be maintained, but without any prejudice to, or limitation on, the free float of these shares, or the economic and equity rights inherent to them.

4.3. APPROVAL OF THE FEDERAL GOVERNMENT FOR ACQUISITION OF INTEREST EQUAL TO OR HIGHER THAN 35% OF THE CAPITAL STOCK AND REQUIREMENT OF A PUBLIC TENDER OFFER FOR ACQUISITION OF SHARES

The acquisition of amounts equal to or higher than 35% of the capital stock of New Embraer, whether in shares or ADS, by any shareholder or group of shareholders, will be subject to the approval of the Federal Government. In the event an authorization by the Federal Government is obtained, such increased in participation must also be subject to a public tender offer for acquisition of shares (Oferta Pública de Aquisição de Ações - OPA) of the total shares and ADS of New Embraer, at the price calculated based on the criteria established in the By-Laws.

This mechanism ensures at the same time that: (i) the Federal Government will have the control over the acquisition of interests equal to or higher than 35% of the capital stock of New Embraer; and (ii) in case such authorization is granted, the other shareholders of New Embraer may sell their shares through a public tender offer to the offering shareholder.

9

4.4. RIGHTS OF THE GOLDEN SHARE:

Besides the provisions set forth in Item 4.3 above, the By-Laws of New Embraer keep all prerogatives currently granted to the Federal Government, as holder of the Golden Share, and as established in the Privatization Notice, and, furthermore, assure to the Federal Government, the veto right in any decision related to: (i) changes in the vote restrictions described in items 4.1 and 4.2 above; (ii) statutory amendments involving changes to the rights granted to the Golden Share; and (iii) statutory changes to the provisions related to the acquisition of interests equal to or higher than 35% of the capital stock.

4.5. MONITORING OF EQUITY SHAREHOLDINGS:

Without prejudice to the other legal duties, the Officer of Investor Relations of New Embraer will be responsible to coordinate a task force in charge of monitoring alterations in New Embraer’s shareholding composition, whether in relation to the equity interest held by each shareholder or group of shareholders (including ADS holders) of New Embraer, or in relation to the shareholders’ nationality, denouncing to the proper authorities possible breaches of the By-Laws.

4.6. BOARD OF DIRECTORS OF NEW EMBRAER – GENERAL RULE AND TRANSITION PERIOD:

The Board of Directors of New Embraer will be comprised of 11 members and their respective alternates. The Federal Government, as holder of the Golden Share, will have the right to appoint one member and an alternate, and the employees of New Embraer will have the right to appoint two (2) members and their respective alternates. The eight (8) remaining members and their respective alternates will be elected by the other shareholders, gathered at the General Shareholders’ Meeting, in due observance to the vote limitations mentioned in items 4.1 and 4.2 above.

In according with the rules of the Novo Mercado, the members of the Board of Directors will have a unified two-year term. However, in order to ensure the stability of the corporate actions and the continuity of management guidelines during the period immediately subsequent to the approval of our Restructuring, the first term of the Board of Directors will be of three (3) years, terminating at the Annual General Shareholders’ Meeting to approve the financial statements for the fiscal year ended in 2008, after which the maximum two-year term of the members of the Board must be observed. This measure intends to avoid any break in the short and medium-term strategies already planned by the current management, and also provides for the Company’s transition to the new structure without prejudice to its businesses.

10

Additionally, in order to ensure the stability and continuity of the management during the transition period mentioned above, the members of the Board of Directors of New Embraer will be elected at the General Shareholders’ Meeting of Rio Han immediately before the decision on the approval of the Merger.

The first term of office of the Board of Directors will comprise the transition period following the Merger. According to information received from Rio Han, its shareholders intend to elect the following individuals to manage New Embraer during this transition period, Mr. Maurício Novis Botelho (Brazilian, married, engineer, resident and domiciled in the city of São Paulo, State of São Paulo, bearer of the identity card RG no. 01.641.893-1 IFP/RJ, enrolled with the CPF/MF under no. 044.967.107-06 and the current Chief Executive Officer of the Company) as the Chairman of the Board of Directors of Rio Han, who will then also be elected Chief Executive Officer of Rio Han, in accordance with the rules mentioned above. The other positions on the Board of Directors will be filled by: one member appointed by the Federal Government; two members appointed by the Company’s employees; and one member will be appointed by each one of the Current Controlling Shareholders. Four members will be independent, and not related to Rio Han, the Company or the Current Controlling Shareholders, based on the criteria set forth in the Novo Mercado Regulation.

After the approval of the Merger by the General Shareholders’ Meeting of Rio Han, a meeting of the Board of Directors of Rio Han will be held for the election of the Officers. The Officers’ term will follow the same criteria applicable to the Board of Directors, including as concerns the initial period of three years after the Restructuring. After the transition period, the terms of the members of the Board of Directors and Executive Board will be of two years and necessarily concurring.

As part of the procedures to ensure the coordinated and stable transition of New Embraer to the dispersed control environment, the Chairman of the Board of Directors of New Embraer, Mr. Maurício Novis Botelho, qualified above, will also be its Chief Executive Officer until the Ordinary General Meeting that will approve the financial statements for the fiscal year ended on December 31, 2008. After the mentioned Shareholders’ Meeting, the Board of Directors of New Embraer will appoint a new Chief Executive Officer, and a same person will be expressly prohibited from holding simultaneously seats in New Embraer’s Board of Directors and Executive Committee.

11

4.6. BREACH TO LEGAL AND STATUTORY PROVISIONS:

Pursuant to article 120 of Law 6,404/76, violations of law or of the By-Laws of New Embraer will subject the violating shareholder to the suspension of its political rights (i.e., the temporary loss of its voting rights), upon decision of the General Shareholders’ Meeting to this effect, such suspension to be lifted as soon as compliance is restored.

The provision mentioned above is also included in the proposed By-Laws of New Embraer, attached to the Merger Agreement as Exhibit V, in order to emphasize that such measure may also be adopted upon proposal of the management of New Embraer, in case of a breach of the statutory provisions, especially those mentioned in Items 4.1 to 4.4 above.

5. VALUATIONS, EXCHANGE RATIO AND CHANGES IN POLITICAL AND EQUITY RIGHTS:

As result of the Merger, Embraer will cease to exist and its current shareholders will receive common shares or ADS issued by New Embraer, as the case may be, based on the exchange ratio described below. The shares of the capital stock of Embraer held by New Embraer will be cancelled.

5.1. VALUATION REPORT - BOOK VALUE:

The calculation of the amount of the capital increase of New Embraer resulting from the Merger will be based on the Shareholders’ Equity Valuation Report of Embraer, prepared on January 18, 2006 by Acal Consultoria e Auditoria S/S, with head office in the City of São Paulo, State of São Paulo, at Av. Paulista no. 2300, Pilotis, Cj. 60, enrolled with CNPJ/MF under no. 28.005.734/0003-44.

The valuation conducted by Acal Consultoria e Auditoria S/S was based on the Company’s book value calculation criterion, in accordance with the Company’s balance sheet as of September 30, 2005, duly audited. According to the valuation report of Embraer’s book value, the book value of the Company as of September 30, 2005 amounted to R$ 4,771,725,554.66. Consequently, the increase in the capital stock of New Embraer arising from the Merger will be of R$ 3,809,708,284.77.

The net worth variations verified in New Embraer between September 30, 2005 – base date of the valuation of its accounting net worth – and the General Shareholders’ Meeting that approves the Merger, shall be absorbed by New Embraer.

The appointment of Acal Consultoria e Auditoria S/S, as well as the valuation report assessing the book value of Embraer, will be submitted for the approval of the General Shareholders’ Meeting of Embraer and Rio Han called to decide on the Merger, in which occasion the proposal for ratification of the acts practiced up to that moment by their respective administrators within the Restructuring process will also be analyzed.

12

5.2. EXCHANGE RATIO OF EMBRAER’S SHARES AND ADS FOR NEW EMBRAER’S SHARES AND ADS AND PREMIUM ATTRIBUTED TO THE SHARES SUBJECT TO THE SHAREHOLDERS’ AGREEMENT:

In order to support the process for determination of the exchange ratio for the Company’s shares and New Embraer’s shares and ADS, Goldman Sachs & Companhia, with head offices in the city of São Paulo, State of São Paulo, at Av. Presidente Juscelino Kubitschek no. 510, 6th floor, enrolled with the CNPJ/MF under no. 30.892.178/0001-55, was appointed to conduct the corresponding economic and financial analyses (the “Financial Analyses”). Such studies were conducted taking into consideration the base date of September 30, 2005.

The Management of Embraer understands that there is a legitimate and justified expectation of the Current Controlling Shareholders that the Control Shares receive an amount higher than that applied to the other shares that are not subject to the Shareholders’ Agreement. This understanding is based on the Financial Analysis, specifically retained to support the exchange ratio of Embraer’s shares for shares of New Embraer. The Merger will result in the dilution of New Embraer shareholding composition and, therefore, will equalize the amount of all New Embraer shares, granting to its shareholders, indistinctly, higher chances of influencing its management.

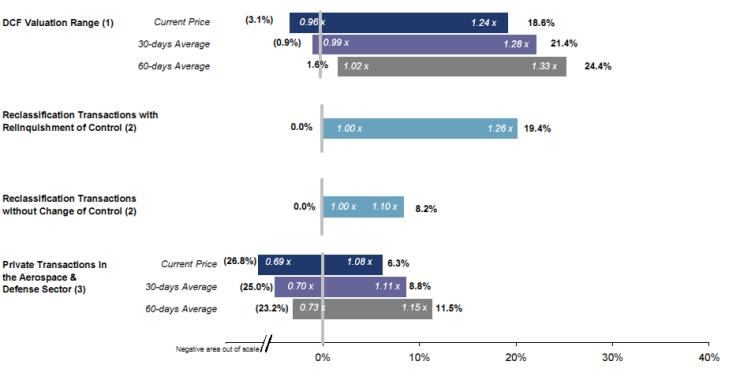

The Financial Analysis assesses the existence of elements that would justify the payment of a premium of up to 24.4% to the holders of the Control Shares, on the valuation value of the shares – and ADS – of Embraer not subject to the Shareholders’ Agreement, regardless of their type. The management of the Company and Rio Han understand that the approval of the Restructuring proposal by the Current Controlling Shareholders imposes the concession of incentives that justify the waiver of rights currently set forth in the Shareholders’ Agreement and the power to control the Company.

On the other hand, the management of Embraer must consider the best interests of the Company and of the group represented by all its shareholders, without favoring any group, whether controlling or minority. Due to the assumptions above, and based on the opinions of the most renowned Brazilian scholars, the management of the Company and Rio Han proposed the implementation of the Restructuring, based on the exchange ratio mentioned above.

13

The management of Embraer and New Embraer understand that, among the several criteria addressed in the Financial Analyses, the discounted cash flow method is the one which best reflects the value of Embraer and, consequently, of New Embraer, since the assets of Rio Han are exclusively comprised of the shares of Embraer previously held by the Current Controlling Shareholders.

Taking into consideration the Financial Analyses and in observance with the exchange ratio bands included therein, the management of Embraer and New Embraer will propose that as result of the Merger the exchange ratio of the Company’s shares not subject to the Shareholders’ Agreement is made at the ratio of 1 new common share of New Embraer for each common or preferred share of the Company. The Company’s shares held by New Embraer will be cancelled.

Considering that due to the Restructuring: (i) the transfer of the Control Shares to the capital stock of New Embraer will be made at the ratio of 1.1153 shares of New Embraer for each Control Share; and (ii) the Proposal of the Executive Committee and the Merger Agreement determine that, upon the Merger, each share of the Company not subject to the Shareholders’ Agreement, regardless of the type, will be replaced by one common share of New Embraer, the proposal to be submitted to the shareholders of Embraer includes the concession of a premium of 9.0%, exclusively to the Control Shares.

The implementation of the Restructuring will result in the increase in the interest participation of the Control Shares, from 20.16% of the Company’s capital stock to 21.97% of New Embraer’s capital stock. On the other hand, the interest of the shares not subject to the Shareholders’ Agreement, including those held by the Current Controlling Shareholders, will be reduced from 79.84% of the Company’s capital stock to 78.03% of New Embraer’s capital stock, resulting in a dilution of 2.3%.

Embraer’s common and preferred shares held by the Current Controlling Shareholders but not subject to the Shareholders’ Agreement will not be entitled to a control premium, and will receive the same treatment given to the shares held by the non-controlling shareholders.

Embraer’s common and preferred shares, as well as ADS, will be replaced for shares with voting rights, or ADS, as the case may be, of Rio Han. The By-Laws of New Embraer will prohibit the issuance of preferred shares. Accordingly, due to the Merger, the holders of Embraer’s preferred shares – and, consequently, ADS – will lose the following equity rights, currently prescribed by article 8 of its By-laws: (i) priority in the reimbursement of capital, without bonus; and (ii) dividends per share at least ten (10) times higher than those attributed to each common share.

The management of Embraer considers equitable the application of the same exchange ratio between the Company’s common and preferred shares (ADS included) and New Embraer’s shares and ADS, since the equity losses suffered by the preferred shares (including those in form of ADS) of Embraer will be offset against the acquisition of the voting rights granted to the shareholders of Rio Han.

14

5.3. NEW EMBRAER’S CAPITAL STOCK AFTER THE MERGER:

Upon implementation of the Merger, the capital stock of New Embraer will be increased by R$3,809,708,284.77, equivalent to the book value of Embraer, discounting the portion corresponding to the interest currently held by Rio Han in the Company’s capital stock.

The mentioned capital increase will be represented by the issuance of 576,305,057 common book-entry shares, with no par value of New Embraer, as follows:

New Embraer’s Capital Stock |

| R$ |

| Number of |

| ||

|

|

| |||||

Pre Merger |

|

| 962,017,769.89 |

|

| 162,306,763 |

|

Post Merger |

|

| 4,771,726,054.66 |

|

| 738,611,820 |

|

5.4. VALUATION REPORT - MARKET VALUE

In compliance with article 264 of Law 6,404/76, the market value of Embraer and New Embraer for purposes of the calculation of the amount to be paid as reimbursement in case of withdrawal of dissenting shareholders, was also assessed by Acal Consultoria e Auditoria S/S, above qualified. Such valuations were made using the same criteria and on the same date (January 18, 2006), based on the duly audited financial statements of Embraer and of Rio Han, as of September 30, 2005.

For preparation of the valuation reports in compliance with article 264 of Law 6,404/76, Acal Consultoria e Auditoria S/S made the necessary adjustments to the financial statements of Rio Han, in order to account the transfer of 145,527,000 Control Shares to its corporate capital that occurred on January 18, 2006.

For preparation of the valuation reports, Acal Consultoria e Auditoria S/S assumed that Rio Han: (i) owns the Control Shares as its sole asset; and (ii) does not have any debts or obligations that could negatively impact its net worth.

15

The result of such valuation is presented below:

Before the Merger |

| EMBRAER |

|

| NEW |

| |

|

|

| |||||

Amounts per share valued at market value |

| R$ | 2,756,720 |

| R$ | 555,727 |

|

Number of shares comprising the total capital |

|

| 721,831,057 |

|

| 162,306,763 |

|

Book value per share |

| R$ | 3.82 |

| R$ | 3.42 |

|

Exchange ratio valued at market value (or ADS) |

|

| 1.1154 shares of New Embraer |

| |||

5.5. DISSENTERS’ OR APPRAISAL RIGHTS:

The Merger will grant dissenters’ or appraisal rights to the shareholders of the Merged Company who expressly disagree with the proposal within 30 days from the publication of the minutes of the General Shareholders’ Meeting which approves the Merger Agreement, and the payment of the respective reimbursement will depend on the performance of the transaction, as set forth in article 230 of Law 6,404/76.

In accordance with article 137, item II of Law 6.404/76, the appraisal right is not granted to holders of shares of any type that cumulatively presents: (i) liquidity, typified by the listing of such shares in a trading index; and (ii) dispersed ownership, when the controlling shareholder, the controlling company or other companies under its control, hold less than half of the shares of such type or class.

Both Embraer’s common shares and preferred shares are listed in the Bovespa Index, but only preferred shares are liquid. Accordingly, appraisal rights will be assured to the holders of Embraer’s common shares who timely and formally express their disagreement with the Merger, being these shareholders entitled to claim the auditing of the special balance sheet of Embraer, as set forth in paragraph 2 of article 45 of Law 6,404/76, for purposes of calculation of the reimbursement price.

The express disagreement will be considered to be timely if received within 30 days from the publication of the minutes of the General Shareholders’ Meeting of the Company that approves the Merger, and the payment of the reimbursement price will depend on the effective performance of the transaction, as set forth in article 230 of Law 6,404/76. In the cases in which auditing of the special balance sheet is requested, according to paragraph 2 of article 45 of Law 6,404/76, the shareholder will receive 80% of the reimbursement price, and the balance, if any, will be paid within 120 days from the date of approval of the Meeting, as set forth in paragraph 3 of article 137.

16

The appraisal rights of Embraer’s shareholders dissenting from the Merger will be limited to the shares held by these shareholders until the day of the first publication of the call notice to the General Shareholders’ Meeting, and cannot be exercised in relation to the shares purchased afterwards, as set forth in paragraph 1 of article 137 of Law 6,404/76.

As set forth in the main section and paragraph 3 of article 264 of Law 6,404/76 and considering that the exchange ratio of Embraer’s shares for New Embraer’s shares proposed based on the valuation of the Company at economic value – of 1 share of New Embraer for each share of the Company – is less beneficial to New Embraer’s shareholders in relation to the price set forth based on the valuation of the Companies at market value – of 1.1153 shares of New Embraer for each Company’s share – the reimbursement to the shareholders of Embraer that timely and formally express their disagreement in relation to the Merger will be guaranteed and made based on Embraer’s shareholders’ equity, calculated on September 30, 2005, corresponding to R$ 6.61 per share, as follows:

EMBRAER – BEFORE THE MERGER | ||||

Book value at 09.30.2005 |

| R$ | 4,771,725,554.66 |

|

Number of shares comprising the capital stock |

|

| 721,832,057 |

|

Book value per share at 09.30.2005 |

| R$ | 6.61 |

|

6. CHANGE TO RIO HAN’S CORPORATE NAME:

Upon approval of the Merger, Rio Han will be renamed “Embraer – Empresa Brasileira de Aeronáutica S.A.”, thus assuming the name of the Merged Company.

7. RESTRICTIONS FOR TRADING OF THE SHARES HELD BY THE CURRENT CONTROLLING SHAREHOLDERS

During the six month period as from the date of the approval of the Merger, the Current Controlling Shareholders and the management of New Embraer cannot trade the shares held by them in the capital stock of the Company. Besides showing to the market that the Current Controlling Shareholders and the management remain committed to New Embraer and believe in its future, this measure intends to prevent the sale of a volume of shares of New Embraer immediately after approval of the transaction, which may adversely affect the quotation of its shares in the market.

17

8. REGISTRATION OF THE TRANSACTION WITH THE U.S. SECURITIES AND EXCHANGE COMMISSION (“SEC”):

The effective holding of the General Shareholders’ Meetings of Embraer and New Embraer to decide on the approval of the corporate transactions described herein is conditioned upon registration with the SEC, as set forth in SEC regulations.

9. GENERAL PROVISIONS:

The costs to be incurred with the implementation of the merger amounts to approximately R$12 million, including expenses related to the fees of auditors, valuation companies, legal counselors and publications.

The specialized companies Goldman Sachs & Companhia, and ACAL Consultoria e Auditoria S/S declared the inexistence of any conflict of interests regarding the transaction or any shareholder of Embraer or New Embraer, or any other company involved in the transaction and its related partners.

With due regard for item 8 above, the corporate transaction described herein is not subject to the approval of the local or foreign regulatory agencies or antitrust authorities.

Upon implementation of the Merger described herein New Embraer will request to the Brazilian Securities Commission (CVM) its listing as public company, pursuant to paragraph 3 of article 223 of Law 6,404/76 and, reinforcing the Company’s commitment with management transparency and promoting the interests of its shareholders, will request to adhere to Bovespa’s Novo Mercado. Moreover, the necessary changes will be made in the ADR Program launched by Embraer as of July 21, 2000.

All information and documents related to the Restructuring process, including the Merger Agreement and its exhibits, including valuation reports, opinions, economic and financial analyses, financial statements and proposed amendments to the New Embraer’s By-Laws, are, as from the date hereof, available to the shareholders at the head offices of Embraer, located in the City of São José dos Campos, State of São Paulo, at Av. Brigadeiro Faria Lima no. 2170, at the Company’s website www.embraer.com.br and at the head offices of New Embraer, located in the City of São José dos Campos, State of São Paulo, at Av. Brigadeiro Faria Lima no. 2170, Prédio F56, térreo, Sala 2656. This documentation was also submitted to CVM and Bovespa, and will also be furnished to the SEC.

18

Embraer and the New Corporation will file important documents with the SEC. If the Proposal is approved, or by requesting such documents from Embraer at Av. Brigadeiro Faria Lima, 2,170, 12227-901 São José dos Campos, SP, Brazil, Attention: Anna Cecilia Bettencourt (telephone 55-12-3927-4404; fax 55-12-3922-6070; email: investor.relations@embraer.com.br).

The Restructuring and respective supporting documents will be submitted by Embraer and New Embraer to SEC. Investors and security holders are urged to carefully read these documents when they become available, because they will contain important information. Investors and security holders may obtain copies of these documents for free, when available, at the SEC’s web site at www.sec.gov, as well as at the Company’s head offices and on its web site at www.embraer.com.br.

The shareholders of Embraer interested in accessing the information or clarifying any doubts regarding the Restructuring proposal should contact the Company’s Investor Relations Department via phone (55-12-3927 4404) or e-mail: investor.relations@embraer.com.br.

São José dos Campos, January 19, 2006

| /s/ ANTONIO LUIZ PIZARRO MANSO |

|

|

| |

| Antonio Luiz Pizarro Manso |

|

| Vice President Executive and Investor Relations |

|

This communication may include forward-looking statements or statements about events or circumstances which have not occurred. These forward-looking statements include, but are not limited to, statements regarding the (i) timing of the meeting of Embraer shareholders and the approval of the restructuring (the “Restructuring”) by such shareholders, (ii) expected changes that may be necessary if the Restructuring is effected, and (iii) benefits of the implementation of the Restructuring to Embraer and Embraer shareholders, including statements regarding improved access to capital markets and financing resources for future new program developments, and statements regarding the dispersed ownership and increased liquidity of Rio Han common shares, as well as the possible effects thereof on the market capitalization of Rio Han. The company has based these forward-looking statements largely on its current expectations about the Restructuring, its implementation and the consequences arising therefrom. These forward-looking statements are subject to risks, uncertainties and assumptions, including, among other things: the non-approval of the Restructuring by Embraer’s shareholders; political and business conditions, both in Brazil and in Embraer’s markets; and existing and future government regulations in Brazil and abroad.

The words “believes,” “may,” “will,” “estimates,” “continues,” “anticipates,” “intends,” “expects” and similar words are intended to identify forward-looking statements. Embraer and Rio Han undertake no obligation to update publicly or revise any forward-looking statements because of new information, future events or other factors. In light of these risks and uncertainties, the forward-looking events and circumstances discussed in this communication might not occur. Actual results could differ substantially from those anticipated in the forward-looking statements

19

Free Translation

from the Portuguese

NM Project

Descriptive Memorandum of the Transaction

January 13, 2006

This Memorandum was prepared solely for information purposes, aiming to present the proposed structure for the restructuring of Embraer and submitting it for the analysis and considerations of the parties involved. Therefore, it should not be considered as any form of commitment to carry out the transaction described, collectively or partially, nor as a recommendation to any person, shareholder or not, to adopt any measure in relation to the Company’s investments.

The restructuring of Embraer and the documents that support it, shall be submitted to the U.S. Securities and Exchange Commission. The investors of American Depositary Shares (ADS) of Embraer and the American holders of common and preferred shares issued by Embraer are hereby advised to carefully analyze the supporting documents of the restructuring, regarding the prominence of its terms. As of their disclosure, such documents can be freely obtained from the website of SEC, www.sec.gov, or in the head offices of Embraer or in its official website – www.embraer.com.br.

Definitions

The terms used in this Memorandum will have the meaning attributed to them in this section:

ACAL | ACAL Consultoria e Auditoria S/S. |

|

|

ADR | American Depositary Receipts. |

|

|

ADS | American Depositary Shares. |

|

|

AGU’s Opinion | Opinion GQ-215 of the General Attorney of the Government, dated as of January 6, 2000, and approved by the President through resolution of January 19, 2000. |

|

|

ANBID | National Association of Investment Banks. |

|

|

BNDESPAR | BNDES Participações S.A. – BNDESPAR. |

|

|

Control Shares | Shares issued by Embraer held by the Controlling Group, bound to the Shareholders’ Agreement. |

|

|

BOVESPA | São Paulo Stock Exchange. |

|

|

Bozano | Cia. Bozano, company part of the Controlling Group. |

|

|

Brazilian Corporate Law | Law No. 6,404 of December 15, 1976, and subsequent amendments. |

|

|

CMN | National Monetary Council. |

|

|

Company or Embraer | EMBRAER – Empresa Brasileira de Aeronáutica S.A. |

|

|

Controlling Group | Bozano, Previ and Sistel, jointly, as Embraer’s controlling shareholders. |

|

|

CVM | Brazilian Securities Commission. |

|

|

Embraer’s Accounting Report | Embraer’s Accounting Appraisal Report, prepared by ACAL based on the net assets, according to Section IX.4. |

|

|

European Shareholders | Dassault Aviation, ThalesTM , EADS – Eutopean Aeronautic Defence and Space Company N.V. and Safran (ancient SNECMA – Société Nationale d’Étude et Construction de Moteurs d’Aviation), jointly, as the Embraer’s current shareholders. |

|

|

Financial Appraisal | Financial and economic analysis of Embraer, to be prepared by Goldman Sachs, which will determine the exchange ratio between the shares issued by Embraer and the new shares to be issued by Rio Han, as set forth in Section IX.4. |

|

|

Golden Share | Special common share, held by the Federal Government, which grants veto powers in resolutions involving certain matters. |

|

|

Goldman Sachs | Goldman Sachs & Cia., Embraer’s financial advisors. |

|

|

Market Price Report | Embraer’s and Rio Han’s Market Appraisal Report, to be prepared by ACAL based on the net assets at Market prices, according to Section IX.4. |

|

|

Mattos Filho | Mattos Filho, Veiga Filho, Marrey Jr. e Quiroga Advogados, Embraer’s legal advisors. |

|

|

New Embraer or Rio Han | Rio Han Empreendimentos e Participações S.A. |

2

Novo Mercado | Novo Mercado, BOVESPA’s trading segment for companies with differentiated corporate governance practices. |

|

|

NYSE | New York Stock Exchange |

|

|

OPA | Public offering for acquisition of shares, pursuant to Brazilian Corporate Law and the CVM’s regulations. |

|

|

Previ | Caixa de Previdência dos Funcionários do Banco do Brasil - PREVI, comprising the Controlling Group. |

|

|

Privatization Notice | Notice n.º PND-A-05/94-Embraer, published in the Official Gazette dated of April 4, 1994, relating to Embraer’s privatization process. |

|

|

SEC | U.S. Securities and Exchange Commission. |

|

|

Securities Act | Law No. 6,385 of December 7, 1976, and subsequent amendments. |

|

|

Shareholders’ Agreement | Shareholders’ Agreement entered into between Bozano, Previ and Sistel on July 24, 1997, relating to Embraer’s control. |

|

|

Sistel | Fundação Sistel de Seguridade Social, comprising the Controlling group. |

3

Table of Contents

I. | Introduction |

| 5 | |

II. | Executive Summary |

| 7 | |

III. | History |

| 10 | |

IV. | The Proposed Transaction |

| 12 | |

| 1. | Implementation Mechanism |

| 12 |

| 2. | Lock-Up Period for Negotiation of the Shares Held by the Controlling Group (“Lock-Up”).. |

| 14 |

V. | Protection Mechanisms |

| 15 | |

| 1. | Limitation of Voting Rights |

| 16 |

| 2. | Foreign Shareholders' Voting Limitation |

| 17 |

| 3. | Federal Government's Approval for the Acquisition of Interest Equal to or Above 35% of the Capital and the Mandatory Tender offer |

| 19 |

| 4. | Disclosure of Information regarding to Significant Interests |

| 20 |

| 5. | Follow-up of Corporate Interests |

| 20 |

| 6. | Violation of Statutory and Legal Provisions |

| 20 |

| 7. | Voting System for Decisions taken in the New Embraer General Shareholders' Meeting |

| 21 |

VI. | Maintenance of the Golden Share Rights |

| 24 | |

VII. | Procedures for Election of the Management |

| 26 | |

| 1. | Transition Period |

| 26 |

| 2. | Election of the Board of Directors in a Dispersed Control Environment |

| 26 |

VIII. | Benefits of the Transaction |

| 28 | |

IX. | Summary of the Legal Aspects |

| 30 | |

| 1. | Incorporation of Rio Han by the Controlling Group |

| 30 |

| 2. | Contribution of Embraer Shares to the Capital Stock of Rio Han |

| 30 |

| 3. | Merger of Embraer into Rio Han |

| 30 |

| 4. | Valuation Reports |

| 32 |

| 5. | Dissenters’ or Appraisal Rights |

| 34 |

| 6. | Definition of the Exchange ratio of the Shares Held by Minority Shareholders |

| 35 |

| 7. | Approval by Shareholders Representing the Majority of Capital Stock as a Condition for the Transaction |

| 36 |

| 8. | Disclosure of Information on the Transaction |

| 36 |

X. | Company By-laws and the Corporate Governance Model of the Company |

| 40 | |

APPENDIX I – Bovespa's “Novo Mercado” |

| 41 | ||

APPENDIX II – Shareholders' Agreement of Embraer |

| 44 | ||

APPENDIX III – Current By-laws of Embraer |

| 46 | ||

APPENDIX IV – Project of By-laws of New Embraer |

| 62 | ||

4

This Memorandum was prepared by the management of Embraer, with the support of the Company’s advisors, Goldman Sachs and Mattos Filho, to present a proposal of the Company’s restructuring which will entail its listing in the Novo Mercado upon a corporate structure with dispersed ownership among its shareholders (the “NM Project”).

Initially, it should be pointed out that the development of new products by Embraer, as well as its future growth, depends on the expansion of the Company’s capacity to access the capital markets, which would allow the raising of funds through the issuance of new shares and/or securities convertible into shares for public subscription.

The Company’s current capital structure not only limits its access to resources through the capital markets but also precludes the obtaining of higher share liquidity since it limits the adoption of the highest corporate governance standards currently existing, including, for example, the granting of voting right to all shareholders.

Once the transaction is carried out, the Company will be merged into Rio Han, which capital will be exclusively represented by common shares and one Golden Share (Golden Share). Embraer’s shareholders will receive shares issued by New Embraer to replace the shares held by them at the date of the merger.

As part of the restructuring process, Rio Han will have its name altered to “EMBRAER – Empresa Brasileira de Aeronáutica S.A.”. However, for purposes of this Memorandum, “Embraer” or “Company” will always be referred to as the merged company, and “Rio Han” or “New Embraer” as the company into which Embraer will be merged.

Once the restructuring is concluded, New Embraer’s by-laws will include mechanisms mainly aimed to: (i) preclude the formation of a new permanent controlling group through the limitation of the number of votes granted to individual shareholders or to a group of bound shareholders; (ii) limit the foreign shareholders’ aggregate voting right to 40% of the total votes at each General Meeting of Shareholders, thus ensuring that the principle established at the Privatization Bid and confirmed on the AGU’s Opinion as regards to the limitation of foreign interest in the Company’s voting capital; and (iii) maintain the current rights of the Golden Share.

As a result of the transaction, New Embraer will become the biggest public company with fully dispersed ownership and with the majority of the vote rights held by Brazilians, providing higher liquidity for all its shareholders, who will then benefit from the potential share valuation increase, and improvement of current corporate governance standards resulting from the extension of voting rights to all shareholders and holders of ADS of New Embraer.

5

In addition, the transaction will be inNewtive in the Brazilian capital markets as a result of not only the restriction mechanisms for acquisition of the control and hostile take overs, but also due to the high levels of corporate governance which the Company intends to implement, both initiatives without precedents in Brazilian companies.

6

1. | This Memorandum contemplates the Company’s corporate restructuring, through its merger into Rio Han, and its subsequent dissolution. The proposal aims at promoting the dispersion of New Embraer’s control amongst its shareholders, as well as its listing on the BOVESPA’s Novo Mercado segment and its ADS listed on NYSE. The implementation of the transaction, as it was structured, will have two stages, to be submitted for the approval of the shareholders of the two companies, as follows: | |

|

|

|

| (a) | Embraer will be merged into a new company, Rio Han; |

|

|

|

| (b) | Due to the merger, Embraer will cease to exist, and New Embraer will be the full successor of Embraer; |

|

|

|

| (c) | All Embraer’s shareholders will have the Company’s shares and ADS replaced by New Embraer’s common shares and ADS, respectively, with voting rights, and the By-laws of New Embraer will prohibit the issuance of preferred shares. |

|

|

|

| As explained in the specific chapters of this Memorandum, the Brazilian shareholders will be assured to represent the majority of the votes at the General Shareholders’ Meetings of New Embraer, thus ensuring that the Brazilian shareholders will have decision-making powers at the General Shareholders’ Meetings. | |

|

| |

| As a direct result of the implementation of the phases described above, New Embraer will become the biggest Brazilian company with dispersed capital and with the majority of its voting rights held by Brazilian shareholders. The Federal Government will be assured with the maintenance of its special rights, as holder of the Golden Share, which were created in order to maintain the Brazilian strategic interests, inherent to the business activities of the Company. | |

|

| |

2. | Amongst the main benefits of the transaction, analyzed in further details in Chapter VIII below, are: | |

|

| |

| (a) | The growth of the capacity of attraction of resources to support New Embraer’s expansion programs, arising from the easier access to the capital markets, which is currently limited due to the: (i) Embraer’s shareholding control structure; and (ii) maximum proportion allowed by Brazilian Corporate Law between common and preferred shares1. |

1 Brazilian Corporate Law allows the Company to issue up to 66.66% of the capital stock in preferred shares. Currently, the percentage of prefered shares issued by the Company represents 66.22%. |

7

| (b) | The improvement of corporate governance and increased transparency of the administration’s acts. |

|

|

|

| (c) | The possibility to use New Embraer’ shares as currency for acquisition of assets and potential international expansion. |

|

|

|

| (d) | Extension of voting right granted to all shareholders, including holders of ADS, since all shares issued by New Embraer shall be common, allowing the admission of Embraer to the Novo Mercado; and |

|

|

|

| (e) | The potential liquidity increase of shares, thus impacting its quotation on the stock exchange and its the market value. |

|

|

|

3. | Under New Embraer’s project by-laws, attached hereto as Appendix IV, protective mechanisms were created to ensure not only the dilution of the shareholding control, but also the holding by Brazilian shareholders of the majority of the votes at the general shareholders meetings of New Embraer, ensuring that the decision-making power is held by Brazilian individuals. Among these mechanisms we highlight the following: | |

|

| |

| (a) | No shareholder or group of shareholders, national or foreign, may vote at each General Shareholders’ Meetings with a number higher than 5% of the number of shares in which the capital stock is divided. This limitation intends to prevent the excessive concentration of shares or ADS in only one shareholder or group of shareholders; |

|

|

|

| (b) | The total votes granted to foreign shareholders at any General Shareholders’ Meeting, solely or in a group, will be limited to 40% of the total votes to be cast at the Meeting; |

|

|

|

| (c) | Any shareholder or group of shareholders will be prohibited from acquiring participation equal or higher than 35% of New Embraer’s stock capital, except if expressly authorized by the Federal Government, as the holder of the Golden Share, and upon implementation of an OPA, as further detailed; |

|

|

|

| (d) | The shares exceeding 35% of New Embraer’s capital stock must be mandatorily sold, in case the Federal Government does not authorize the implementation of the OPA to acquire the shares above this limit, under the penalty of suspension of the voting rights inherent to these shares through the approval at the General Meeting of Shareholder that is specifically called by New Embraer’s management to discuss that matter; and |

|

|

|

| (e) | The shareholding composition must be disclosed whenever: (i) a shareholder’s interest reaches or exceeds 5% of the company’s capital stock; and (ii) any shareholder’s interest exceeds at least 5% of New Embraer’s capital. This provision will be included in its by-laws, which reinforces the legal obligation of carrying out this disclosure. |

8

4. | The rights of the Golden Share to be held by the Federal Government, as currently set forth in the Embraer’s by-laws, will be fully maintained in New Embraer’s by-laws, namely: | |

|

| |

| (a) | Maintenance of the Federal Government’s right, as the holder of the Golden Share, to appoint one director, pursuant to paragraph 1, of article 18 of the Embraer’s current by-laws; |

|

|

|

| (b) | Submission for previous approval by the Federal Government, as holder of the Golden Share, for the acquisition, by any shareholder or group of related shareholders, of an interest equal or greater than 35% of New Embraer’s capital, as described in item 3(c) above; |

|

|

|

| (c) | Veto rights in resolutions that may change the rights of the Golden Share, or change the protection mechanisms described in item 3 above; |

|

|

|

| (d) | Maintenance of all other rights of the Golden Share currently set forth in Embraer’s by-laws; and |

|

|

|

| (e) | Requirement of Federal Government’s approval, as the holder of the Golden Share, to change certain matters in New Embraer’s by-laws. |

|

|

|

5. | The transaction will be implemented through the Company’s merger into Rio Han. The transaction will be carried out in two stages: (i) contribution of the Control Shares to pay-in capital increase of Rio Han; and (ii) merger of Embraer into Rio Han. The Controlling Group will have a different exchange ratio for the Control Shares, so as to assure proper compensation for the assignment of the controlling ownership of the Company in favor of the Company’s shareholders. | |

|

| |

6. | As described in Section IX.7 below, the transaction will be submitted for the approval of the Company’s shareholders and holders of ADS of the Company, at a Special General Meeting in which each share, common or preferred, including ADS, will have voting rights, in express compliance with the corporate governance practices recommended by the CVM2. | |

2 According to the book “CVM Recommendations on Corporate Governance”, dated as of June 2002: “Significant decisions should be approved by the majority of the stockholders, having each share the right to one vote, regardless of the class or type. Amongst the most significant decisions are: (1) approval of the appraisal report of the assets which will be merged into the capital; (2) changes in the Company’s objectives; (3) reduction of the mandatory dividend; (4) merger, split-up or incorporation; and (5) significant transactions with related parties. In certain issues, including those mentioned above, the restricted voting rights of the preferred shares shall not persist, taking into consideration the materiality of the decisions, which will affect all shareholders. |

9

On December 20, 1994, Embraer was privatized within the National Privatization Program. As the Company is a strategic company, the Golden Share3 was created within the privatization process. The Golden Share, while held by the Federal Government, grants veto rights in the approval of certain matters, as well as the prerogative of appointing a member and an alternate to the Board of Directors.

Embraer’s current controlling shareholders – Bozano, Previ and Sistel – entered into the Shareholders’ Agreement on July 24, 1997. The Shareholders’ Agreement is valid until July 24, 2007, provided that the controlling shareholders have, each, at least, 20% of the voting shares, being renewable for successive periods of five years (for further information on the Shareholders Agreement, see Appendix II –Shareholders Agreement of Embraer).

Aiming to continuously expand its technological capacity, increase its access to markets and develop new products and activities, the Embraer’s Shareholders’ Agreement provided for the selection of one or more strategic partners. In 1999, the European Shareholders acquired, jointly, 20% of the Company’s voting capital, but they were not included in the Controlling Group.

The following chart presents the Company’s shareholding composition as of December 30, 2005:

|

| December 30, 2005 |

| ||||||||||||||||

|

|

| |||||||||||||||||

|

| Common |

| Preferred |

| Total interest |

| ||||||||||||

|

|

|

|

| |||||||||||||||

Shareholders |

| Quantity |

| % |

| Quantity |

| % |

| Quantity |

| % |

| ||||||

|

|

|

|

|

|

| |||||||||||||

Caixa de Previdência dos Funcionários do Banco do Brasil – PREVI |

|

| 56,643,580 |

|

| 23.35 |

|

| 59,037,178 |

|

| 12.32 |

|

| 115,680,758 |

|

| 16.03 |

|

Fundação Sistel de Seguridade Social |

|

| 48,508,890 |

|

| 20.00 |

|

| 155,726 |

|

| 0.03 |

|

| 48,664,616 |

|

| 6.74 |

|

Cia Bozano |

|

| 48,509,220 |

|

| 20.00 |

|

| 18,786,588 |

|

| 3.92 |

|

| 67,295,808 |

|

| 9.32 |

|

Bozano Holdings, Ltd. |

|

| — |

|

| — |

|

| 8,896,920 |

|

| 1.86 |

|

| 8,896,920 |

|

| 1.23 |

|

BNDES Participações S.A. – BNDESPAR |

|

| 3,488,893 |

|

| 1.44 |

|

| 43,223,686 |

|

| 9.02 |

|

| 46,712,579 |

|

| 6.47 |

|

Dassault Aviation (1) |

|

| 13,744,186 |

|

| 5.67 |

|

| 1,953,132 |

|

| 0.41 |

|

| 15,697,318 |

|

| 2.17 |

|

Thomson CSF/Thales (1) |

|

| 13,744,186 |

|

| 5.67 |

|

| 1,953,132 |

|

| 0.41 |

|

| 15,697,318 |

|

| 2.17 |

|

EADS (1) |

|

| 13,744,186 |

|

| 5.67 |

|

| 1,953,132 |

|

| 0.41 |

|

| 15,697,318 |

|

| 2.17 |

|

Safran (1) |

|

| 7,276,332 |

|

| 3.00 |

|

| 1,034,010 |

|

| 0.22 |

|

| 8,310,342 |

|

| 1.15 |

|

Federal Government |

|

| 1,850,495 |

|

| 0.75 |

|

| 499,416 |

|

| 0.10 |

|

| 2,349,911 |

|

| 0.33 |

|

Other |

|

| 35,034,480 |

|

| 14.45 |

|

| 341,794,689 |

|

| 71.30 |

|

| 376,829,169 |

|

| 52.22 |

|

|

|

|

|

|

|

|

| ||||||||||||

|

|

| 242,544,448 |

|

| 100 | % |

| 479,287,609 |

|

| 100 | % |

| 721,832,057 |

|

| 100 | % |

|

|

|

|

|

|

|

| ||||||||||||

(1) European shareholders |

3 The Federal Government also holds 0.75% of Embraer’s voting capital. However, only the Golden Share was considered for purposes of this Memorandum, and the remaining shares held by the Federal Government were considered as outstanding shares. |

10

In the terms of the Shareholders Agreement, the European Shareholders are treated as strategic partners, and have the right to appoint two effective members and the respective alternates to the Board of Directors, provided that the equity interest of the European Shareholders is maintained at exactly 20% of the Company’s voting capital. Upon implementation of the restructuring, the Shareholders Agreement will be terminated, and the formation of the Board of Directors will comply with the provisions of the Brazilian Corporate Law and New Embraer’s by-laws.

Due to a provision included in Embraer’s by-Laws, which will be reflected in New Embraer by-laws, the Federal Government has the right to appoint 1 (one) member to the Board of Directors and its respective alternate, as long as it holds the Golden Share.

Similarly, Embraer’s employees have the right to elect two members to the Board of Directors and their respective alternates, being one appointed by the CIEMB – Embraer Employees’ Investment Club, and the other appointed by the employees who are not shareholders of the Company.

11

According to the proposed structure of the transaction, Embraer’s restructuring process will be divided into two stages:

(i) Organization of Rio Han and increase of its capital with the Control Shares.

Rio Han, is a close corporation, specially destined for purposes of the implementation of the restructuring described herein, which only has as shareholders the members of the Controlling Group, each one with equal interest in the Company’s corporate capital.

Immediately before submitting the transaction to Embraer’s Board of Directors, the Controlling Group will pay-in a capital increase of Rio Han with the transfer of all its Control Shares. For each Embraer’s share, the subscriber will receive a quantity of Rio Han’s shares to be defined by the management of the two companies based on the Financial Appraisal (see Section IX.6, below – Definition of the Exchange Ratio for the Shares Held by Minority Shareholders).

The following chart outlines Embraer’s capital structure after the conclusion of the first stage, after the Control Shares bound to the Shareholders Agreement had been transferred to Rio Han’s capital stock:

1. | Control Shares. |

2. | All other preferred and common shares, including Bozano, Sistel and Previ shares not bound to the Shareholders’ Agreement, European Shareholders and shares bound to Embraer’s ADR program. |

12

(ii) Merger of Embraer with and into Rio Han

After Rio Han’s capital increase through the transfer of the Control Shares, the process which will result in the Company’s merger will be started.

In accordance with CVM’s recommendations of corporate governance practices, and in order to provide increased transparency to the voting process, the restructuring proposal will be submitted to all shareholders of the Company, regardless of the type of shares held by them, in two different stages. At first, the restructuring proposal will the submitted to all shareholders of the Company, including the depositary Bank of the ADR Program of Embraer, which shall vote as instructed by ADS holders but excluding the shareholders of the Controlling Group, which shall not, direct or indirectly, cast a vote in this first stage of the voting process.

In case the restructuring proposal is rejected by shareholders or ADS holders representing more than 50% of the outstanding shares (considered as such all the common and preferred shares issued by the Company and traded in the market, including ADS, with exclusion of the shares held by the management of Embraer, by Rio Han and by the shareholders of the Control Group), the shareholders of the Control Group shall vote against the approval of the restructuring. In the event that the restructuring proposal is not rejected by the majority of the outstanding shares of Embraer, Rio Han and the shareholders of the Control Group will be free to cast their votes at their discretion.

In order to allow the implementation of the voting system described above, an amendment to Embraer’s by-laws, through the insertion of a transitory resolution with limited validity, will be proposed to the General Shareholders’ Meeting of Embraer that is called to resolve on the restructuring proposal.

As a result of the merger, Embraer shall automatically cease to exist and its shareholders, regardless of the type or class of their shares, will receive New Embraer’s common shares (including ADS), according to the exchange ratio proposed by the management of the Company and of Rio Han, provided that:

| (a) | all shares will be of the common type; |

|

|

|

| (b) | there will be no controlling group ; and |

|

|

|

| (c) | in exchange for the distribution of the control of the Company among all shareholders, Previ, Bozano and Sistel will be entitled to a differentiated exchange ratio, only in what concerns the Control Shares, in comparison to the exchange ratio applied to the other shareholders of Embraer as a result of the merger. |

As a result of the merger above described, the Shareholders’ Agreement will be terminated, and the mergor company will then be called “EMBRAER – Empresa Brasileira de Aeronáutica S.A.”, by taking over the acquired company’s name.

13

The following chart outlines New Embraer’s structure after the merger:

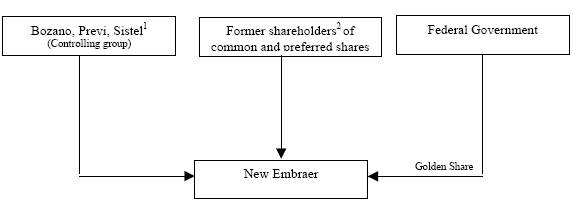

1. | New Embraer’s shares received by the Control Group in exchange for replace the Control Shares. |

2. | New Embraer’s shares received by the other holders of Embraer’s common and preferred shares not bound to the Shareholders Agreement and bound to Embraer ADR program. |

2. Lock-Up Period for Negotiation of the Shares Held by the Controlling Group

A six month lock-up period will be proposed, during which after the merger the members of the Controlling Group and the member of the Management will not be able to trade their New Embraer’s shares on the stock market.

Such lock-up will be established in the Merger Agreement and the Minutes of the Extraordinary General Meetings of the Company and New Embraer, and will be included in the respective Material Fact that will disclose the conditions of the transaction.

The lock-up period not only will demonstrate to the market that the Controlling Group and the Management of New Embraer remain committed with the company and believe in its future, but also such provision will prevent the sale of a considerable amount of shares of New Embraer immediately after the approval of the transaction, which could adversely affect its valuation in the market.