UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 14A

PROXY STATEMENT PURSUANT TO SECTION 14(A) OF

THE SECURITIES EXCHANGE ACT OF 1934

Filed by the Registrant [X]

Filed by a Party other than the Registrant [ ]

Check the appropriate box:

[X] Preliminary Proxy Statement

[ ] Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2))

[ ] Definitive Proxy Statement

[ ] Definitive Additional Materials

[ ] Soliciting Material Pursuant to Rule 14a-12

DICON FIBEROPTICS, INC.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| [ | ] | No fee required. |

| [ | ] | Fee computed on table below per Exchange Act Rules 14a-6(i)(4) and 0-11. |

[X] Fee paid previously with preliminary materials.

| [ | ] | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| 1. | Amount Previously Paid: |

| 2. | Form, Schedule or Registration Statement No.: |

| 3. | Filing Party: |

| 4. | Date Filed: |

Preliminary Copy

September , 2006

Dear Fellow Shareholder:

The Board of Directors of DiCon Fiberoptics, Inc. (the "Company"), after much deliberation, has decided it is in the Company’s best interest to deregister the Company’s shares of common stock with the Securities and Exchange Commission (the "SEC"). The purpose of the transaction is to eliminate the substantial time and expense required to comply with reporting and related requirements under the Securities Exchange Act of 1934, as amended, including the Sarbanes-Oxley Act of 2002, and to increase our operational flexibility.

Deregistering the shares will allow the Company to cease filing reports with the SEC and will substantially reduce or eliminate other compliance costs, which primarily include legal and auditing fees, as well as internal costs associated with document preparation and review. The Company has estimated that by taking this step, it can realize recurring annual cost savings of up to approximately $125,000, not including time and resources of the management team and Company personnel. Additionally, it would help the Company avoid the additional cost of complying with Section 404 of the Sarbanes-Oxley Act, which currently is expected to become effective for the Company commencing with the fiscal year ending March 31, 2008.

The Board has concluded that the costs associated with remaining registered with the SEC outweigh the benefits, particularly in light of the fact that many of the new compliance measures created by the Sarbanes-Oxley Act are designed for companies much larger than the Company and are unnecessarily burdensome to small companies like ours, and provide modest additional benefit to the Company’s shareholders.

There is no established public trading market for the Company’s common stock. Consequently, the deregistration of the Company’s stock will not affect the liquidity of the Company’s common stock.

To successfully complete the transaction, the Company will need to reduce the number of its shareholders of record below 300. The Company currently has 305 shareholders of record. The Board has proposed a two-step transaction (the "Transaction"): (1) a 5-for-1 reverse stock split (the "Stock Split") to increase the number of shareholders holding less than 100 shares of the Company’s stock ("Odd-lot Shareholders") which would be (2) followed by an issuer tender offer (the "Tender Offer") at a price of $5.00 per post-Stock Split share. Provided a sufficient number of Odd-lot Shareholders tender their shares, the Tender Offer may have the result of reducing our number of record holders below 300. In the Transaction, shareholders will be affected as follows:

Preliminary Copy

| · | All shareholders of the Company before the Stock Split will remain shareholders of the Company after the Stock Split. The Stock Split will affect all of DiCon’s shareholders uniformly and will not affect any shareholder’s percentage ownership interest in DiCon, except to the extent that the Stock Split results in any of DiCon’s shareholders owning a fractional share (which will be cashed out by DiCon). All shareholders will have the number of their shares reduced and will retain the same proportionate interest in the Company. Common stock issued pursuant to the Stock Split will remain fully paid and non-assessable. |

| · | All shareholders will have an opportunity to participate in the Tender Offer; and |

| · | After the Stock Split, the number of Odd-lot Shareholders will increase from 6 to 78 and the total number of shares held by Odd-lot Shareholders will increase from 371 to 20,708 on a pre-stock split basis (or from 74 to 4,141 shares on a post-stock split basis). |

The Board of Directors established the purchase prices of the shares following a valuation of the Company’s common stock by Howard Frazier Barker Elliot, Inc., an independent financial consultant.

The notice of annual meeting of shareholders, proxy statement and proxy card are included with this letter along with copies of the Company’s most recent Form 10-KSB. We encourage you to review the materials carefully. On pages 9-12 of the proxy statement you will find a section entitled "Summary Term Sheet" that summarizes the terms of the proposed Stock Split and "Questions and Answers" that are intended to address some of the questions you may have. After reviewing the proxy statement and other materials, please complete the proxy card and return it in the enclosed envelope at your earliest convenience.

On behalf of the Board of Directors, I would like to express our great appreciation of your loyalty and commitment to DiCon Fiberoptics, Inc. Should you have any questions regarding this matter, please feel free to contact me at (510) 620-5000. We will be happy to address any questions or concerns that you may have on this matter.

Sincerely,

/s/ Ho-Shang Lee

_______________________________

Ho-Shang Lee

President, Chief Executive Officer and Director

DiCon Fiberoptics, Inc.

Preliminary Copy

September , 2006

NOTICE OF ANNUAL MEETING OF

SHAREHOLDERS OF

DICON FIBEROPTICS, INC.

To the Shareholders of DiCon Fiberoptics, Inc. ("DiCon"):

NOTICE IS HEREBY GIVEN that the annual meeting of the shareholders of DiCon will be held at the DiCon executive offices, 1689 Regatta Blvd., Richmond, CA 94804, on , October 15, 2006, commencing at 10:00 a.m. local time, for the following purposes:

| 1. | To elect the directors of DiCon. The nominees presented by the Board of Directors for election are Ho-Shang Lee, Gilles M. Corcos, C.L. Lin, Andrew F. Mathieson, and Dunson Cheng. |

| 2. | To ratify the appointment of Burr, Pilger & Mayer LLP as the Independent Registered Public Accounting Firm of DiCon Fiberoptics, Inc. for the fiscal year ending March 31, 2007. |

| 3. | To approve an amendment to the Company’s Articles of Incorporation to effect a 5-for-1 reverse stock split. |

| 4. | To transact such other business as may properly come before the meeting. |

/s/ Anthony T. Miller

_______________________________

Anthony T. Miller

General Counsel and Secretary

Enclosures

TO ASSURE THAT A QUORUM IS PRESENT AT THE ANNUAL MEETING, PLEASE DATE, SIGN AND PROMPTLY RETURN THE ENCLOSED PROXY WHETHER OR NOT YOU EXPECT TO ATTEND THE ANNUAL MEETING. A SELF-ADDRESSED, POSTAGE-PAID RETURN ENVELOPE IS ENCLOSED FOR YOUR CONVENIENCE.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THE STOCK SPLIT, PASSED UPON THE MERITS OR FAIRNESS OF THE STOCK SPLIT, OR PASSED UPON THE ADEQUACY OR ACCURACY OF THE DISCLOSURE IN THIS DOCUMENT. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

Preliminary Copy

TABLE OF CONTENTS

& #160; Page

SUMMARY TERM SHEET; QUESTIONS AND ANSWERS .....................................................................................................................................................................................2

IMPORTANT NOTICES ...................................................................................................................................................................................................................................................7

PROPOSAL NO. 1ELECTION OF DIRECTORS .............................................................................................................................................................................................................8

Nominees .............................................................................................................................................................................................................................................................................8

Information Concerning the Board of Directors ............................................................................................................................................................................................................9

Meetings of the Board of Directors ................................................................................................................................................................................................................................9

Shareholder Communications with the Board of Directors .........................................................................................................................................................................................9

Compensation of Directors ............................................................................................................................................................................................................................................10

REQUIRED VOTE ............................................................................................................................................................................................................................................................10

RECOMMENDATION OF THE BOARD .....................................................................................................................................................................................................................10

PROPOSAL NO. 2 APPOINTMENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM ........................................................................................................10

Audit Fees .........................................................................................................................................................................................................................................................11

Audit-Related Fees ..........................................................................................................................................................................................................................................11

All Other Fees ...................................................................................................................................................................................................................................................11

Policy on Board Approval of Accountant Services ....................................................................................................................................................................................11

REQUIRED VOTE ..............................................................................................................................................................................................................................................................11

RECOMMENDATION OF THE BOARD .......................................................................................................................................................................................................................11

PROPOSAL NO. 3 AMENDMENT TO THE COMPANY’S ARTICLES OF INCORPORATION TO EFFECT A 5-FOR-1 REVERSE STOCK SPLIT .................................11

CAUTIONARY NOTICE REGARDING FORWARD-LOOKING STATEMENTS ....................................................................................................................................................12

SPECIAL FACTORS ..........................................................................................................................................................................................................................................................12

Background of the Transaction ........................................................................................................................................................................................................................12

Structure and Effects of the Transaction ........................................................................................................................................................................................................17

Alternatives to the Transaction .......................................................................................................................................................................................................................22

FINANCING, SOURCE OF FUNDS AND EXPENSES ..................................................................................................................................................................................................22

FAIRNESS OF THE TRANSACTION .............................................................................................................................................................................................................................23

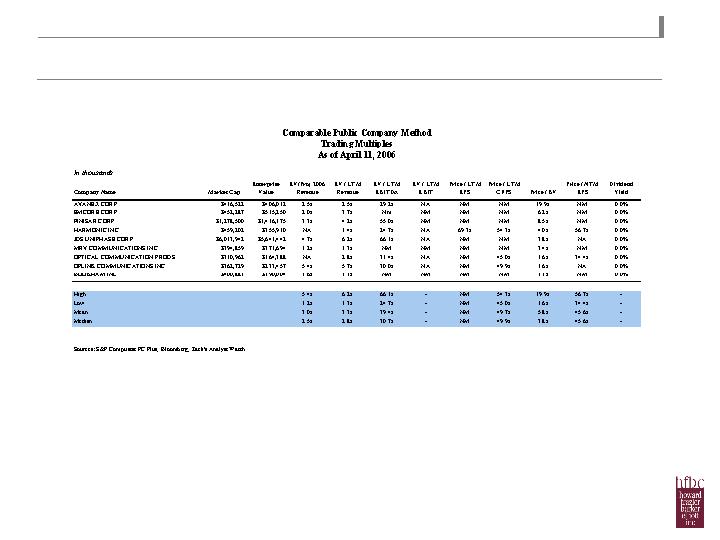

Fairness Opinions of Financial Advisor .........................................................................................................................................................................................................29

Valuation Analysis .............................................................................................................................................................................................................................................31

- i -

TABLE OF CONTENTS

(continued)

& #160; Page

Disadvantages of the Stock Split .....................................................................................................................................................................................................................35

Conclusion ..........................................................................................................................................................................................................................................................36

MATERIAL FEDERAL INCOME TAX CONSEQUENCES .........................................................................................................................................................................................36

ADDITIONAL INFORMATION REGARDING THE TRANSACTION .....................................................................................................................................................................38

Unavailability of Dissenters’ Rights ...............................................................................................................................................................................................................38

Structure and Effects of the Transaction .......................................................................................................................................................................................................38

Escheat Laws .....................................................................................................................................................................................................................................................38

Termination of Stock Split ...............................................................................................................................................................................................................................39

Price Range Of Shares; Dividends .................................................................................................................................................................................................................39

Recent Stock Repurchases ..............................................................................................................................................................................................................................39

.

Financial Information ........................................................................................................................................................................................................................................40

INTEREST OF DIRECTORS AND OFFICERS; TRANSACTIONS AND ARRANGEMENTS CONCERNING SHARES ..................................................................................41

REGULATORY APPROVALS .........................................................................................................................................................................................................................................42

REQUIRED VOTE ..............................................................................................................................................................................................................................................................42

RECOMMENDATION OF THE BOARD .......................................................................................................................................................................................................................43

EXECUTIVE COMPENSATION ......................................................................................................................................................................................................................................43

Management And Affiliates ............................................................................................................................................................................................................................43

Summary Compensation Table ........................................................................................................................................................................................................................44

Options Grants in Last Fiscal Year ..................................................................................................................................................................................................................44

Aggregated Option Exercises in Last Fiscal Year and Fiscal Year - End Option Values ........................................................................................................................44

Board Report on Executive Compensation ....................................................................................................................................................................................................45

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS,

MANAGEMENT AND DIRECTORS .............................................................................................................................................................................................................46

Security Ownership of Certain Beneficial Owners .......................................................................................................................................................................................46

Security Ownership of Management and Directors ....................................................................................................................................................................................47

Changes in Control ...........................................................................................................................................................................................................................................47

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS ...........................................................................................................................................................................48

Compliance with Section 16(a) of the Exchange Act ...................................................................................................................................................................................48

OTHER BUSINESS ...........................................................................................................................................................................................................................................................48

SHAREHOLDER PROPOSALS - 2007 ANNUAL MEETING ....................................................................................................................................................................................49

- ii -

TABLE OF CONTENTS

(continued)

0; Page

PROXY ...........................................................................................................................................................................................................................................................................50

APPENDIX A - PROPOSED FORM OF CERTIFICATE OF AMENDMENT TO

ARTICLES OF INCORPORATION OF DICON FIBEROPTICS, INC.

TO EFFECT REVERSE STOCK SPLIT .........................................................................................................................................................................................A-1

APPENDIX B - FAIRNESS OPINION PRESENTATION OF HOWARD FRAZIER BARKER ELLIOTT, INC DATED APRIL 19, 2006 ..................................................B-1

APPENDIX C - FAIRNESS OPINION PRESENTATION OF HOWARD FRAZIER BARKER ELLIOTT, INC DATED JULY 6, 2006 ......................................................C-1

APPENDIX D - FAIRNESS OPINION OF HOWARD FRAZIER BARKER ELLIOTT, INC. DATED APRIL 19, 2006 ................................................................................D-1

APPENDIX E - FAIRNESS OPINION OF HOWARD FRAZIER BARKER ELLIOTT, INC. DATED JULY 6, 2006 .....................................................................................E-1

- iii -

PROXY STATEMENT

DiCon Fiberoptics, Inc. ("DiCon," the "Company", "we" or "us") is providing this Proxy Statement in connection with the solicitation by the Board of Directors of DiCon of proxies to be voted at DiCon’s annual shareholders meeting (the "Annual Meeting") to be held on , October 15, 2006, at 10:00 a.m., local time, in the auditorium of our executive offices, 1689 Regatta Blvd., Richmond, CA 94804.

We are asking shareholders to complete and return to us before the meeting the enclosed proxy.

We are asking shareholders to vote for the election of directors. Biographical information about the directors is set forth in the Section titled "Nominees" in Proposal No. 1.

We are asking shareholders to ratify the appointment of Burr, Pilger & Mayer LLP as the Independent Registered Public Accounting Firm for DiCon for the fiscal year ending March 31, 2007.

We are asking the shareholders to approve a proposal to amend (the "Amendment") the Articles of Incorporation, as amended, of the Company to effect a 5-for-1 reverse stock split (the "Stock Split") of the shares of common stock of the Company, no par value (the "common stock"). The Stock Split is part of a two-step transaction (the "Transaction") intended to reduce the number of shareholders of record below 300 and subsequently suspend the Company's obligation to file reports, statements and other information with the Securities and Exchange Commission (the "SEC" or the "Commission"). The two steps consist of (1) a 5-for-1 reverse stock split to increase the number of shareholders holding less than 100 shares of the common stock ("Odd-lot Shareholders") followed by (2) an issuer tender offer (the "Tender Offer").

DiCon will not issue any fractional shares of common stock in connection with the Stock Split. In lieu of issuing any fractional shares resulting from the Stock Split, the Company will pay in cash an amount equal to $5.00 multiplied by each fractional share resulting from the Stock Split (determined after aggregating all of the common stock held by each holder).

DiCon shareholders should not return stock certificates with the enclosed proxy.

The solicitation of proxies in connection with the Stock Split proposal does not constitute a tender offer or an offer to purchase the shares of any shareholder. Any such offer will be made pursuant to separate tender offer materials complying with the requirements of Section 13(e) of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), and Rule 13e-4 thereunder.

Lastly, we are asking the shareholders to indicate whether or not they authorize the proxy holder to vote on other business that may come before the meeting. At the present time, we know of no other business to be presented at the Annual Meeting.

The Proxy Statement and form of proxy are first being sent or delivered to shareholders on September , 2006, to shareholders of record on September 12,, 2006 (the "record date"). There were 111,907,283 shares of DiCon common stock outstanding as of the close of business on September 12, 2006. The presence, in person or by proxy, of shareholders representing a majority of such outstanding shares constitutes a quorum for the transaction of business at the Annual Meeting.

A shareholder is entitled to one vote for each share held. In the election for directors, if one or more shareholders has given notice at the Annual Meeting prior to the voting of the shareholder’s intent to cumulate votes, then every shareholder entitled to vote may cumulate votes and give one candidate a number of votes equal to the number of directors to be elected multiplied by the number of shares which the shareholder is entitled to vote, or distribute the votes on the same principle among as many candidates as the shareholder chooses. The candidates receiving the highest number of votes up to the number of directors to be elected shall be elected. For the proposal to ratify the appointment of Burr, Pilger & Mayer LLP as the Independent Registered Public Accounting Firm for DiCon for the fiscal year ending March 31, 2007, the affirmative vote of a majority of the shares represented and voting with respect to such matter is required. For the proposal to approve the Stock Split, the affirmative vote of a majority of the shares outstanding as of the record date is required.

1

If not revoked and if no instructions are indicated on the proxy card with respect to one or more items, the proxy will be voted (1) "FOR" the election of directors in the manner described in the Proxy Statement, (2) "FOR" the ratification of the appointment of Burr, Pilger & Mayer LLP as Independent Registered Public Accounting Firm of DiCon for the fiscal year ending March 31, 2007, and (3) "FOR" the Amendment of the Articles of the Company to effect the Stock Split, and in the discretion of the proxies as to other matters that may properly come before the Annual Meeting.

Abstentions on any matter will be treated as present and entitled to vote for purposes of determining the presence or absence of a quorum, and as voting on the proposal in determining the total number of votes cast with respect to a proposal submitted to shareholders for a vote. Since none of the shares are held in street name, there will be no "Broker Non-Votes." On any matter which requires the affirmative vote of a majority of the outstanding shares, abstentions have the same effect as a negative vote. Accordingly, abstentions can have the effect of preventing approval of the Amendment of the Articles of Incorporation of the Company to effect the Stock Split. While there is no definitive specific statutory or case law authority in California concerning the proper treatment of abstentions, we believe that the tabulation procedures to be followed as discussed above are consistent with the general statutory requirements in California concerning determination of a quorum and voting of shares.

You may revoke your proxy prior to the vote pursuant thereto by a written notice delivered to DiCon stating that the proxy is revoked, by submitting a later dated proxy or by voting in person at the Annual Meeting.

Whether or not you plan to attend the Annual Meeting in person, please complete and return the enclosed proxy as promptly as possible in the enclosed postage prepaid envelope.

We urge you to read this Proxy Statement carefully and in its entirety, including the attached appendices.

SUMMARY TERM SHEET; QUESTIONS AND ANSWERS

This Summary Term Sheet highlights selected information about the proposed Stock Split included elsewhere in this Proxy Statement. This summary is qualified in its entirety by reference to the more detailed information appearing or incorporated by reference elsewhere in this Proxy Statement. We encourage you to read the entire Proxy Statement before you vote at the Annual Meeting.

2

| · | To successfully complete the Transaction, the Company will need to reduce the number of its shareholders of record below 300. The Company currently has 305 shareholders of record. The Board has proposed a two-step Transaction: (1) the Stock Split to increase the number of shareholders of record holding less than 100 shares of the common stock which would be (2) followed by an issuer tender offer. See "Special Factors- Structure and Effects of the Transaction." |

| · | The purpose of the Transaction is to reduce the number of the Company’s shareholders of record so that we may deregister our common stock under the Exchange Act to suspend our SEC reporting obligations. The Board’s primary reason for engaging in the Transaction is to reduce the cost to the Company of filing reports, statements and other information with the SEC and otherwise comply with the reporting and related requirements of the Exchange Act. If we so deregister, we will not be subject to certain extra burdens imposed on public companies by the Sarbanes-Oxley Act of 2002 (the "Sarbanes-Oxley Act"). We will no longer file periodic reports with the SEC, including annual and quarterly reports on Form 10-KSB and Form 10-QSB, nor will we be subject to the SEC’s proxy rules. We also will no longer have to furnish to our shareholders financial statements audited by an independent registered public accounting firm. Other reasons for, and anticipated consequences of, the Stock Split are discussed in this Proxy Statement. See "Special Factors-Background of the Transaction." |

| · | The Stock Split is subject to shareholder approval at the Annual Meeting. However, the Tender Offer is not subject to shareholder approval. If the Stock Split is approved, the Stock Split will be effected simultaneously for all outstanding shares of DiCon Common stock. A 5-for-1 reverse stock split of the shares will occur on the date (the "Effective Date") that the California Secretary of State accepts for filing the certificate of amendment to our Articles reflecting the Amendment (the "Certificate of Amendment"). The Stock Split will affect all of DiCon’s shareholders uniformly and will not materially change any shareholder’s percentage ownership interest in DiCon, except to the extent that the Stock Split results in any of DiCon’s shareholders owning a fractional share. Fractions of shares resulting from the Stock Split will be immediately cancelled and exchanged for cash in the amount of $5.00 multiplied by the fraction (the "Fractional Share Price"). The Stock Split will have no material effect on the relative voting power of the shareholders. Common stock issued pursuant to the Stock Split will remain fully paid and non-assessable. See "Special Factors- Structure and Effects of the Transaction." |

| · | All stock certificates representing issued and outstanding shares of common stock immediately prior to the Stock Split will be cancelled. After the Certificate of Amendment has been filed with the California Secretary of State, the Company will send shareholders transmittal materials that will inform shareholders how to collect cash to be paid for fractional shares and receive copies of new stock certificates. See "Additional Information Regarding The Transaction - Structure and Effects of the Transaction." |

| · | Termination of our obligations to file reports, statements and other information with the SEC will not have an effect on the liquidity of the Company’s common stock since our stock is not publicly traded. See "Special Factors-Background of the Transaction." |

| · | For a discussion of the material federal income tax consequences of the Stock Split, see "Material Federal Income Tax Consequences." |

3

| · | Howard Frazier Barker Elliott, Inc. (“HFBE”), an independent financial advisor to the Special Committee of the Board of Directors, has delivered its Opinion Update dated July 6, 2006 to the Special Committee. The Opinion Update states that, as of its date, the Fractional Share Price to be paid to our shareholders in the Stock Split and the Tender Offer Price to be paid to our shareholders in the Tender Offer were fair, from a financial point of view, to the shareholders, including the unaffiliated shareholders. This Opinion Update was one of the factors considered by the Special Committee and the Board in determining the price to be paid in the Transaction. A copy of this Opinion Update is attached as Appendix E to this Proxy Statement. The opinion is based upon and subject to the various assumptions and limitations described in the opinion. Please read the opinion in its entirety. See "Fairness of the Transaction- Fairness Opinions of Financial Advisor." |

| · | The Stock Split will not be effective unless and until DiCon’s shareholders approve the proposed Amendment. We anticipate that the Certificate of Amendment will be filed with the Secretary of State, and the Stock Split will take place, shortly after the Annual Meeting. See "Special Factors-Summary Term Sheet" and "Special Factors-Structure and Effects of the Transaction." |

| · | No dissenters’ rights for the fractional shares are available to shareholders who vote against the Stock Split under California law or under the Company’s Articles of Incorporation or Bylaws. See "Additional Information Regarding The Transaction-Unavailability of Dissenters’ Rights." |

| · | We estimate that approximately $533 will be required for the Company to pay for the fractional shares cashed out as a result of the Stock Split and the Tender Offer for up to 30,900 post-Stock Split shares of common stock (or 154,500 shares on a pre-Stock Split basis) at a purchase price of $5.00 per share would require payment by the Company of approximately $154,500. In addition, we estimate that we will incur approximately $160,000 in transaction expenses related to the Transaction. We intend to pay for the shares to be cashed out and the expenses of the Transaction from the working capital of the Company. At March 31, 2006, DiCon (including its subsidiary) had approximately $21.2 million in cash and cash equivalents and marketable securities. See " Financing, Source Of Funds And Expenses." |

| · | The Board established a Special Committee for this Transaction. The Board considered the Company’s prior associations with each member of the Special Committee and concluded that such prior associations did not compromise each member’s independence. See "Special Factors - Background of the Transaction." |

| · | DiCon’s Special Committee chose not to adopt any of the protective structures typical of transactions of this kind, such as a Special Committee with separate representatives, conditioning the Stock Split on the approval by a majority of the unaffiliated shareholders, conditioning the Tender Offer on tenders by a majority of the unaffiliated shareholders, and the like. See "Special Factors-Background of the Transaction" and "Fairness of the Transaction." |

| · | The Special Committee and the Board of Directors each believes that the Stock Split is in the best interests of the Company and its shareholders and has unanimously approved the Stock Split. The Board recommends that shareholders vote "FOR" approval of the Amendment to effect the Stock Split. See "Special Factors-Background of the Transaction." |

| · | The Special Committee and the Board of Directors have each determined that the Stock Split, including the Fractional Share Price to be paid in connection with the Stock Split, is fair to the Company’s shareholders, including its unaffiliated shareholders. See "Special Factors- Background of the Transaction" and "Fairness of the Transaction." |

4

| · | The Board may, in its discretion, withdraw the Stock Split from the agenda of the Annual Meeting prior to any shareholder vote if it believes that such withdrawal is in the Company’s best interests. Although the Board presently believes that the Transaction, including the Stock Split, is in the Company’s best interests and has recommended a vote for the Stock Split, circumstances could change prior to the Effective Date that may render the Transaction inadvisable. Among other things, the Board may withdraw the Stock Split from the agenda if there is: (1) any change in the nature of the Company’s shareholdings that would prevent us from reducing the number of record holders below 300 as a result of the Transaction; (2) any change in the number of our record holders that would allow the Company to deregister its shares without effecting the Transaction; (3) any change in the number of the shares to be exchanged for cash in the Transaction that would substantially increase the cost and expense of the Transaction (as compared to what is currently anticipated); or (4) any adverse change in the condition of the Company that would render the Transaction inadvisable. See "Additional Information Regarding The Transaction - Termination of Stock Split." |

The following questions and answers are intended to briefly address commonly asked questions regarding the Annual Meeting and the Stock Split. These questions and answers may not address all questions that may be important to you as a shareholder. Please refer to the more detailed information contained elsewhere in this Proxy Statement, the appendices to this Proxy Statement, and the information and documents referred to or incorporated by reference in this Proxy Statement.

When and where is the Annual Meeting?

The Annual Meeting will be held at the DiCon executive offices, 1689 Regatta Blvd., Richmond, California 94804, on , October 15, 2006, at 10:00 a.m., local time.

How many votes do I have?

You will have one vote for each share that you own on the record date, which is September 12, 2006.

How many votes can be cast by all shareholders?

As of the record date, 111,907,283 shares were issued and outstanding and held of record by 305 shareholders.

Can I change my vote?

Yes, you may revoke your proxy by either (i) submitting a new proxy with a later date or a written revocation so long as the new proxy or written revocation is received by the Company before the proxy is exercised or (ii) by attending the Annual Meeting and voting in person or giving notice of revocation in open meeting before the proxy is exercised.

What happens if the meeting is postponed or adjourned?

Your proxy will be valid and may be voted at the postponed or adjourned meeting. You will still be able to change or revoke your proxy until it is voted.

5

Why should I vote to approve the Stock Split set forth in Proposal No. 3?

The Board believes that the Stock Split is in the best interests of all of the Company’s shareholders. The Stock Split will increase the number of Odd-lot Shareholders, which will allow us to conduct a Tender Offer seeking to reduce the number of record holders of our shares below 300 persons. If that reduction is achieved, we will be able to deregister our shares under the Exchange Act and suspend our SEC reporting obligations. We also will no longer have to furnish our shareholders financial statements audited by an independent registered public accounting firm. The Board believes that the monetary expense and the burden on management incident to continued compliance with the Exchange Act outweigh any material benefits derived from continued registration of the shares.

As you are aware, in April 2006 the Company commenced an issuer tender offer for 154,500 shares at the price of $1.00 per share for the purpose of reducing the number of shareholders below 300 (the "April Tender Offer"). The Company withdrew the April Tender Offer because the limited number of Odd-Lot Shareholders at the time, coupled with the pro ration purchase requirement triggered by the oversubscription, meant that to continue with the April Tender Offer would not achieve the Company’s stated purpose of reducing the Company’s holders of record below 300. As stated in the announcement to withdraw the April Tender Offer, the Board of Directors has remained committed to reducing the number of holders of record below 300 so that the Company may deregister under the Exchange Act and suspend its SEC reporting obligations.

How will the Transaction affect the day-to-day operations?

The Transaction will have limited effect on the Company’s business and operations. After the Transaction is completed, the officers and directors of the Company will continue to hold the positions they currently hold. However, provided that the number of shareholders of record is reduced below 300 and the Company deregisters its common stock under the Exchange Act, after the Transaction the Company will no longer be an SEC reporting Company and it may be detrimental DiCon shareholders in that as a result of deregistration, public information regarding DiCon will be reduced substantially following deregistration. Additionally the remaining shareholders would not be subject to the protections of the Sarbanes-Oxley Act.

How were the Fractional Share Price and Tender Offer Price determined?

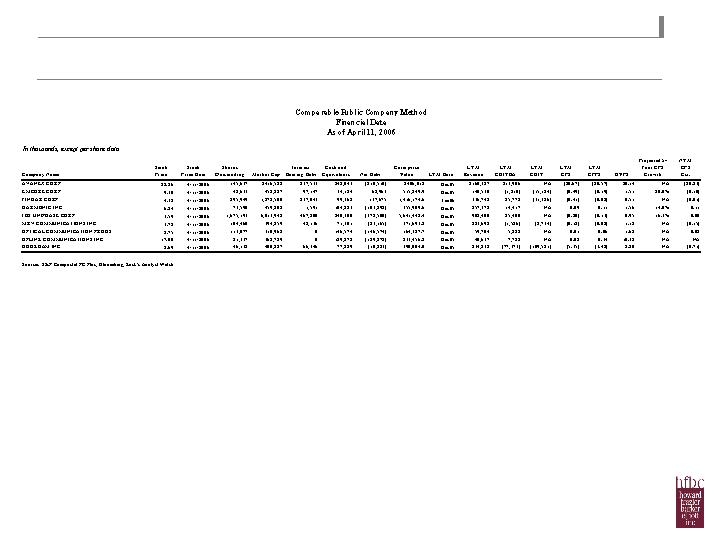

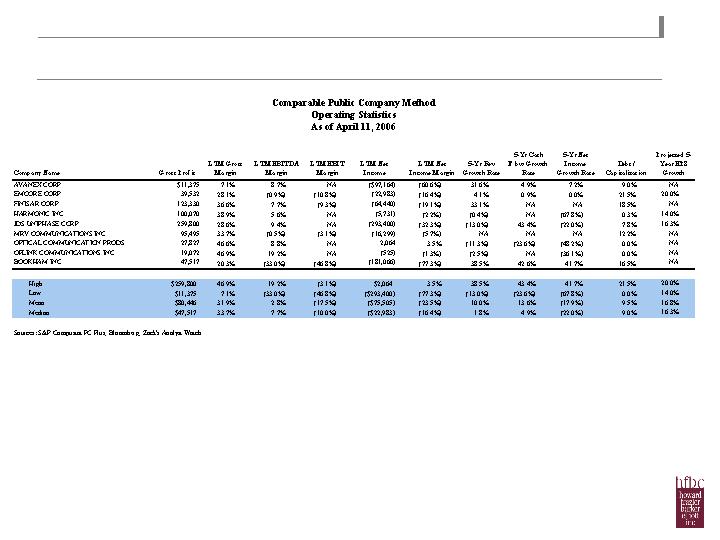

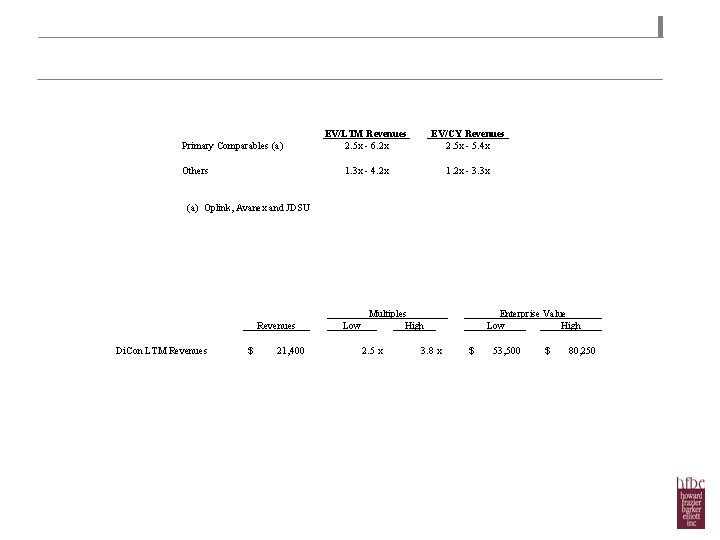

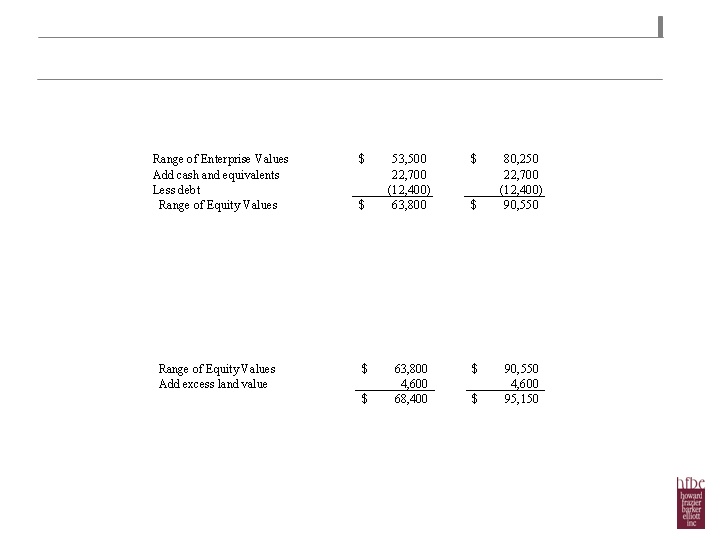

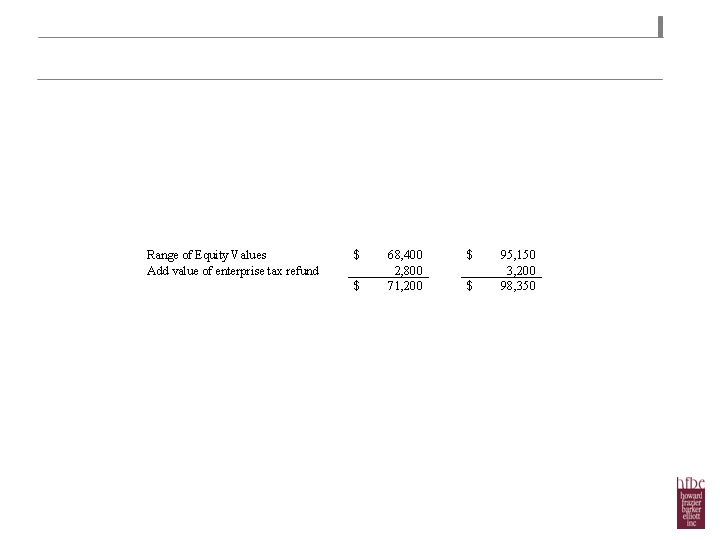

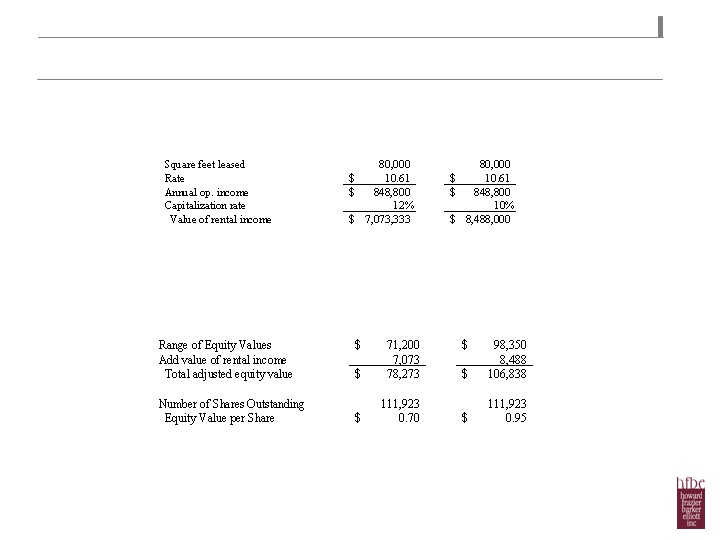

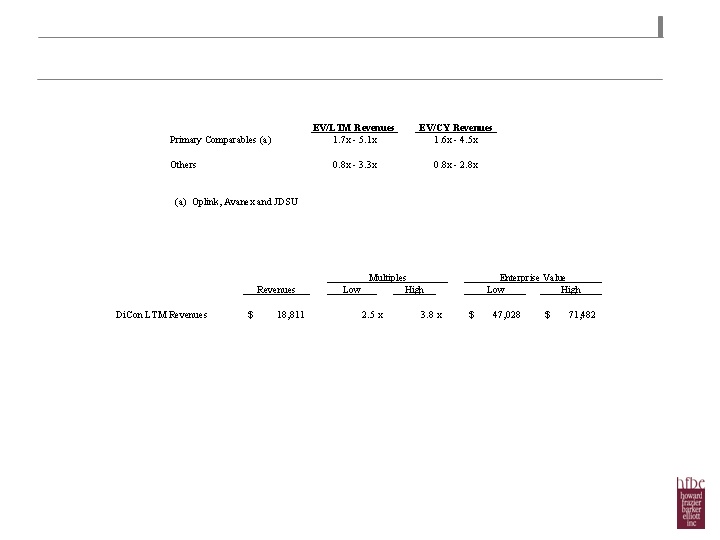

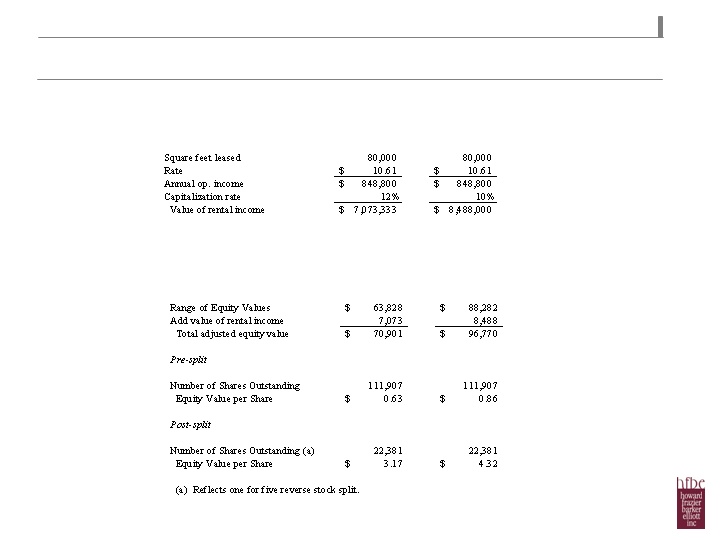

The Board retained HFBE, an independent financial advisor experienced in the financial analysis and valuation of companies, to assist the Board in determining the Fractional Share Price and the Tender Offer Price. On April 19, 2006, HFBE delivered a valuation report (the "April Valuation Report") to the Special Committee of the Board of Directors, which had been established for the purpose of evaluating the various methods of reducing the number of holders of record below 300, approving the Transaction and determining the fairness of the Transaction (the "Special Committee"), valuing the shares at $0.70-0.95 per share and issued a fairness opinion (the "April Fairness Opinion") to the Special Committee that the $1.00 tender offer price for the April Tender Offer was fair, from a financial point of view, to the unaffiliated shareholders. On July 6, 2006, HFBE delivered an updated valuation report (the "Valuation Update," together with the April Valuation Report, the "Valuation Reports") to the Special Committee valuing the Company's shares at $0.63 to $0.86 per pre-Stock Split share (or $3.17 to $4.32 per post-Stock Split share) and issued a fairness opinion update (the "Opinion Update," together with the April Fairness Opinion, the "Fairness Opinions") to the Special Committee that the Fractional Share Price of $5.00 per post-Stock Split share and the Tender Offer Price of $5.00 per post-Stock Split share were fair, from a financial point of view, to the unaffiliated shareholders. The Special Committee considered the independent valuation and other factors and determined that the Fractional Share Price of $5.00 for each post-Stock Split share and Tender Offer Price of $5.00 for each post-Stock Split share are fair. On July 17, 2006, the Special Committee reported its determination to the Board and the Board ratified this determination that the Fractional Share Price of $5.00 for each post-Stock Split share and Tender Offer Price of $5.00 for each post-Stock Split share are fair. See "Fairness of the Transaction." A copy of the April Fairness Opinion and the Opinion Update is attached for your review as Appendices D and E, respectively, to this Proxy Statement.

6

May I obtain a copy of Howard Frazier Barker Elliott, Inc.’s valuation report?

In connection with the Fairness Opinions, HFBE has prepared and delivered to the Company the Valuation Reports that detail the valuation principles and methodologies used to determine the fairness of the proposed transaction. A copy of the April Valuation Report and the Valuation Update are attached as Appendices B and C, respectively, to this Proxy Statement.

When will the Stock Split be completed?

We plan to complete the Stock Split as soon as practicable after we obtain the necessary shareholder approval in October of 2006.

When will the Transaction be completed?

We plan to commence the Tender Offer immediately after the Stock Split in October of 2006 and conclude the Tender Offer in November of 2006.

Will I receive any declared dividends for shares that are cashed out or tendered?

So long as the shareholder held the shares on the record date for the declared dividend, he or she will be entitled to receive declared dividends on his or her shares, even if the declared dividend is not paid until after the Stock Split has been completed or after the shares have been sold into the Tender Offer.

What do I need to do now?

Mail your signed proxy card in the enclosed return envelope as soon as possible so that your shares may be represented at the Annual Meeting. If you sign and return your proxy but do not include instructions on how to vote, your shares will be voted "FOR" the proposal to amend the Company’s Articles to effect the Stock Split.

IMPORTANT NOTICES

We have not authorized any person to give any information or to make any representations other than the information and statements included in this Proxy Statement. You should not rely on any other information. The information contained in this Proxy Statement is correct only as of the date of this Proxy Statement, regardless of the date it is delivered or when shares are converted.

You should not construe the contents of this Proxy Statement or any communication from the Company, whether written or oral, as legal, tax, accounting or other expert advice. You should consult with your own counsel, accountant or other professional advisor, as appropriate.

7

PROPOSAL NO. 1

ELECTION OF DIRECTORS

The Board has nominated the five persons named below to serve as directors to hold office until the next annual meeting of shareholders, until their respective successors have been elected and qualified or until such directors’ earlier resignation or removal. The five nominees receiving the highest number of votes of the shares present in person or represented by proxy at the Annual Meeting and voting on the election of directors will be elected. All of the nominees have served as directors of the Company since the last annual meeting of shareholders. If any nominee for any reason is unable to serve, or for good cause, will not serve as a director, the proxies may be voted for such substitute nominee as the proxy holder may determine. The Company is not aware of any nominee who will be unable to or, for good cause, will not serve as a director.

Nominees

DiCon’s directors and executive officers as of June 30, 2006, are as follows:

| Name | Age | Position | ||

| Ho-Shang Lee, Ph.D. | 47 | President, Chief Executive Officer and Director | ||

| Gilles M. Corcos, Ph.D. | 79 | Chairman of the Board and Director | ||

| Chun-Lung Lin | 47 | President of Global Fiberoptics Inc. and Director | ||

| Andrew F. Mathieson | 49 | Director | ||

| Dunson Cheng, Ph.D. | 61 | Director |

Ho-Shang Lee, Ph.D., President, Chief Executive Officer and Director. Dr. Ho-Shang Lee has served as DiCon’s President, Chief Executive Officer and a member of the Board of Directors since the inception of DiCon in June 1986. Dr. Lee earned his B.S. in Engineering from National Cheng-Kung University, Taiwan, in 1979 and his M.S. and Ph.D. in Mechanical Engineering from the University of California, Berkeley in 1984 and in 1986, respectively.

Gilles M. Corcos, Ph.D., Chairman of the Board and Director. Dr. Gilles M. Corcos has served as Chairman of the Board and Director since 1986. Dr. Corcos has also served as Chief Financial Officer. From 1958 to 1990, Dr. Corcos was a professor in the University of California, Berkeley’s Mechanical Engineering Department. Dr. Corcos holds a Ph.D. from the University of Michigan and a Doctorat d’Etat (Physics) from the University of Grenoble, France. Dr. Corcos also serves as a director of Agua Para La Vida, a non-government organization incorporated in the State of California.

Chun-Lung Lin, President of Global Fiberoptics Inc. ("Global") and Director. Chun-Lung Lin is the President of Global, DiCon’s subsidiary in Taiwan. Before joining Global in January 2000, Mr. Lin owned and managed Guo Bao Construction Co. Ltd. in Taiwan for ten years. Mr. Lin joined DiCon’s Board of Directors in June 2000. Mr. Lin earned a B.S. and an M.S. in Engineering from National Cheng-Kung University, Taiwan, in 1979 and 1981, respectively. He is the brother-in-law of Dr. Ho-Shang Lee.

Andrew F. Mathieson, Director. Andrew F. Mathieson has served as a member of the Board of Directors since June 2000. Mr. Mathieson is the President of Fairview Capital Investment Management LLC ("Fairview"), a registered investment advisor located in Greenbrae, California. Fairview, which was founded by Mr. Mathieson in 1995, manages separate portfolios and is the General Partner of a private investment partnership. Mr. Mathieson earned a B.A. from Yale University in 1978, and an M.B.A. from Stanford University in 1984.

8

Dunson Cheng, Ph.D., Director. Dr. Dunson Cheng joined the Board of Directors in February 2002. Dr. Cheng is Chairman of the Board, Director, and President and Chief Executive Officer of Cathay Bank and Cathay General Bancorp. Dr. Cheng earned his B.S. in Applied Math and Physics from the University of Wisconsin at Madison, Wisconsin and his Ph.D. in Physics from the State University of New York at Stony Brook, and did post-doctorate research at the University of Oregon. Dr. Cheng worked for Xerox before joining Cathay Bank. Dr. Cheng was appointed President of Cathay Bank in 1985, President of Cathay Bancorp (predecessor of Cathay General Bancorp) in 1990 and Chairman of both institutions in 1994.

Information Concerning the Board of Directors

The Board of Directors has five directors.

The Board of Directors does not have standing audit, nominating or compensation committees or committees performing similar functions.

The Board of Directors believes it is appropriate for DiCon not to have a nominating committee or committee performing similar functions because members of the Board either beneficially own or represent shareholders who beneficially own approximately 90% of the outstanding shares of DiCon. These shareholders determine who shall be nominated for and elected to membership on the Board.

The entire Board of Directors participates in the identification and consideration of director nominees. The Board of Directors does not have a charter concerning the director nomination process. Andrew F. Mathieson and Dunson Cheng are the only members of the Board of Directors who qualify as independent under the NASD standard for NASDAQ traded issuers, which is the independence standard the Company has adopted for its Board.

The Board of Directors will consider director candidates recommended by shareholders. Shareholders may submit recommendations for candidates at the annual meeting of shareholders in accordance with DiCon’s bylaws and California law. The Board has not established any specific qualifications for nominees.

Meetings of the Board of Directors

The Board of Directors held three meetings during the fiscal year ended March 31, 2006.

Shareholder Communications with the Board of Directors

Shareholders may communicate with the Board of Directors by calling or emailing Dr. Ho-Shang Lee at 510-620-5000 or hslee@diconfiber.com, respectively, or by contacting individual members of the Board.

DiCon encourages members of the Board to attend the annual shareholder meetings. Two members of the Board attended the 2005 annual meeting.

9

Compensation of Directors

Dr. Gilles M. Corcos received compensation of $55,200 during the fiscal year ended March 31, 2006. None of the other Directors received compensation from the Company other than the stock options described below.

All Directors are reimbursed for out-of-pocket expenses incurred in connection with attending Board meetings.

Non-employee Directors receive stock options under the Employee Stock Option Plan as follows:

| · | Upon first joining the Board, each Director is granted 20,000 stock options. These options vest in twelve equal quarterly installments, commencing on the last day of the calendar quarter in which the option was granted. |

| · | Immediately after each annual shareholders meeting, each Director elected to the Board is granted 10,000 stock options. These options vest in four equal quarterly installments, commencing on the last day of the calendar quarter in which the option was granted. |

| · | The exercise price for the options is the fair market value of the shares on the date of the grant. |

| · | The term of the options is ten years from the date of the grant. |

In January 2004, Dunson Cheng voluntarily surrendered past and future stock option awards under the Employee Stock Option Plan.

REQUIRED VOTE

If a quorum is present, the five nominees receiving the highest number of affirmative votes of shares present and voting at the Annual Meeting in person or by proxy and voting on the election of directors shall be elected as directors.

RECOMMENDATION OF THE BOARD

THE BOARD RECOMMENDS A VOTE FOR THE ELECTION OF EACH

OF THE NOMINATED DIRECTORS.

PROPOSAL NO. 2

APPOINTMENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The Board of Directors is recommending that shareholders ratify the appointment of Burr, Pilger & Mayer LLP ("BPM") as the Independent Registered Public Accounting Firm of DiCon for the fiscal year ending March 31, 2007.

The audit report of BPM on the consolidated financial statements of DiCon and subsidiaries as of and for the year ended March 31, 2006 did not contain any adverse opinion or disclaimer of opinion, nor was it qualified or modified as to uncertainty, audit scope, or accounting principles.

10

Representatives from BPM are not expected to be present at the Annual Meeting.

Audit Fees

The aggregate fees billed for each of the last two fiscal years for professional services rendered by BPM for the audit of DiCon’s annual financial statements and review of financial statements included in DiCon’s Form 10-QSB quarterly reports and services normally provided by the accountant in connection with statutory and regulatory filings or engagements were $120,000 for the fiscal year ended March 31, 2006 and $124,000 for the fiscal year ended March 31, 2005.

Audit-Related Fees

There were no other fees for audit related services by BPM for the fiscal year ended March 31, 2006 or for the fiscal year ended March 31, 2005.

All Other Fees

There were no other fees billed in either of the fiscal years ended March 31, 2006 and 2005 for products and services provided by BPM, other than reported above.

Policy on Board Approval of Accountant Services

The Board of Directors does not have an audit committee.

It is policy of the Board of Directors that before an accountant is engaged by DiCon to render audit or non-audit services, the engagement will be approved by the Board of Directors.

REQUIRED VOTE

The ratification of the appointment of Burr, Pilger & Mayer LLP as the Company’s independent registered public accounting firm requires the affirmative vote of the holders of a majority of the shares present and voting at the Annual Meeting in person or by proxy and constituting a majority of the required quorum.

RECOMMENDATION OF THE BOARD

THE BOARD RECOMMENDS A VOTE "FOR" THE APPOINTMENT OF BURR, PILGER & MAYER LLP AS THE COMPANY’S INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

FOR FISCAL YEAR ENDED MARCH 31, 2007.

PROPOSAL NO. 3

AMENDMENT TO THE COMPANY’S ARTICLES OF INCORPORATION TO EFFECT A 5-FOR-1 REVERSE STOCK SPLIT

For the reasons set forth below, the Board of Directors believes that the best interests of the Company and its shareholders will be served by amending (the "Amendment") the Company’s Articles of Incorporation, as amended (the "Articles"), to effect a 5-for-1 reverse stock split (the "Stock Split") in furtherance of the Company's plan to reduce the number of holders of record of shares below 300 and, subsequently, suspend the Company's obligation to file reports, statements and other information with the SEC. A copy of the proposal Amendment is attached hereto as Appendix A.

11

CAUTIONARY NOTICE REGARDING FORWARD-LOOKING STATEMENTS

When used in this Proxy Statement, the words or phrases "believe," "anticipate," "expect," "intend," "estimate," "project," "targeted," "will likely result," "are expected to," "will continue" or similar expressions are intended to identify "forward-looking statements." Such statements are subject to certain risks and uncertainties that could cause actual results to differ materially from results presently anticipated or projected. The Company cautions you not to place undue reliance on any such forward-looking statements, which speak only as of the date made. The Company advises readers that the Company’s actual results may differ materially from any opinions or statements expressed with respect to future periods contained in this Proxy Statement or in our other filings with the SEC. To the extent that there is any material change in the information contained in this Proxy Statement, the Company will promptly disclose the change as required by applicable SEC rules and regulations.

SPECIAL FACTORS

Background of the Transaction

DiCon Fiberoptics, Inc. was incorporated in California in 1986. The Company designs and manufactures passive components, modules, Micro Electro-Mechanical Systems ("MEMS") products, and test instruments for the fiberoptic communications industry. The Company conducts research, development, manufacturing, and marketing at its headquarters in Richmond, California 94804. The Company, through Global Fiberoptics Inc. ("Global"), its wholly owned Taiwanese subsidiary formed in 1999, also operates a manufacturing and sales facility in Kaohsiung, Taiwan. While the Company registered its shares of common stock under Section 12(g) of the Exchange Act in 2002, the common stock is not listed and there is no established public trading market for the common stock.

The purpose of this Transaction is to reduce the number of holders of record of the common stock. As of the record date for the Annual Meeting, there were 305 holders of record of the common stock. If, after completion of this Transaction, we have fewer than 300 shareholders of record, as calculated under the rules and regulations of the Commission under the Exchange Act, the Board of Directors intends to deregister the common stock with the Commission. One result of our exiting the SEC reporting system would be that we would no longer have to file periodic reports with the Commission, as required under the Exchange Act, including, among other reports, annual reports on Form 10-KSB and quarterly reports on Form 10-QSB, and we would no longer have to furnish to our shareholders financial statements audited by an independent registered public accounting firm. In addition, we would not be subject to the SEC’s proxy rules. The Board of Directors estimates that this could result in a significant cost savings to DiCon and allow management to spend more time focused on its regular business activities. DiCon made the decision to proceed with the Transaction at this time in light of the costs associated with complying with the Exchange Act, including Section 404 of the Sarbanes-Oxley Act. To comply with Section 404, we would need to retain the services of additional auditors and consultants and we would experience an increase in expenses from our current outside auditor. These costs would continue to increase throughout next year as we prepare for Section 404 compliance. Under current SEC rules, the Section 404 compliance requirement will become effective for non-accelerated filers like DiCon beginning with the first fiscal year ending after July 15, 2007, which is the fiscal year ending March 31, 2008 for DiCon. After Section 404 requirements become effective for the Company, in addition to its annual audit cost, it would incur additional costs of at least $170,000 for Section 404 related audits for the first year and a lesser, but still substantial amount, each year thereafter. Please see "Special Factors-Structure and Effects of the Transaction" below for a breakdown of the costs the Company incurred in 2006 associated with being a reporting company.

12

If this Transaction does not result in DiCon qualifying to deregister with the Commission, the Board of Directors will likely consider other alternatives to achieve that result. Specifically, after the Transaction is completed, the Board of Directors currently anticipates that consistent with its prior practice it will continue to repurchase shares from employees departing through natural attrition under the Company’s standard Buy-Sell Agreement with its employee shareholders. While the Company cannot anticipate the timing of its employee departures through attrition, since the Company currently has 305 shareholders of record, it expects that the Tender Offer will reduce the number of shareholders of record to below 305 and that over the course of the next several months, the Company may be able to repurchase shares from enough departing employees to reduce the number of its holders of record below 300 and be qualified to file a Form 15 for deregistration.

Since the Company registered its shares of common stock under Section 12(g) of the Exchange Act in 2002, DiCon has been subject to the reporting and proxy requirements under the rules of the Commission.

In response to the industry-wide down turn since 2001, the Company down-sized from approximately 1,195 employees in April 2001 to approximately 273 employees as of June 30, 2006. During this period, the Company repurchased shares from its departing employees pursuant to the terms of the Buy-Sell Agreement between the Company and each of the employees. In late 2002 and early 2003, the Company sought no-action relief from the SEC in order to deregister its shares, but this relief was denied and the request was withdrawn. At Dr. Ho-Shang Lee’s suggestion, and with the concurrence of the other Board members, in mid-2003 the Company explored the possibility of soliciting the repurchase of its common stock from certain employees for the purpose of reducing the Company’s holders of record below 300, but the effort was dropped after discussions with the SEC staff.

In June 2005, in connection with the Board’s review of the Company’s Annual Report on Form 10-KSB for the fiscal year ended March 31, 2005, a member of the Board noted the expenses related to the annual report and inquired about the status of deregistration and additional Board members echoed support for deregistration. Dr. Lee and the other Board members exchanged several electronic mail messages discussing the costs of being a reporting company, the future costs increases due to Section 404 of the Sarbanes-Oxley Act and deregistration, and Dr. Lee proposed preparing a plan to achieve deregistration. Several Board members requested that Dr. Lee prepare such a plan. In response to the Board’s inquiry and subsequent electronic mail messages exchanged by Dr. Lee with the directors, Dr. Lee met with representatives from Orrick, Herrington & Sutcliffe LLP (the "special counsel") to discuss deregistration in January of 2006 and requested counsel to prepare a presentation to the Board on considerations related to a transaction to deregister the Company’s common stock.

Present at the February 14, 2006 meeting by conference call were representatives of special counsel and a majority of the Board of Directors. Dr. Lee explained how the costs associated with being an SEC reporting company could be reduced following deregistration of the common stock. Special counsel presented for the Board’s review considerations related to deregistering the Company’s shares from the SEC and compared and contrasted four possible methods to reduce the number of record shareholders below 300, which is required to deregister the common stock: an issuer tender offer, an odd-lot tender offer, a reverse stock split, and a stock repurchase program. Prior to the meeting, management was informed of the legal mechanics and implications of the four methods by counsel.

13

The Board observed the following with respect to of each of the methods discussed for reducing the number of shareholders of record below 300:

| o | An issuer tender offer could be costly and may not reduce the number of shareholders due to proration requirements; |

| o | the Company did not have a sufficient number of Odd-Lot Shareholders to allow an odd-lot tender offer to reduce the number of shareholders of record below 300; |

| o | a reverse stock split that cashes out resulting fractional shareholders would not be voluntary and could be subject to regulatory approval, which may not be readily obtained; and |

| o | a repurchase program to buy back shares held by departing employees under the Company's Buy-Sell Agreements with its shareholders may be a lengthy and uncertain process. |

The Board reviewed a reverse stock split structured to cash out all, rather than a portion, of certain shareholders' shares, such as one at the ratio of 500-for-1 designed to cash-out holders of less than 500 shares of the Company's stock, but determined against it due to the uncertainties related to the requirements under the California Corporate Securities Law that a permit be obtained from the California Department of Corporations to effectuate such a split. The Board then explored a two-step transaction involving a modest reverse stock split designed to increase the number of Odd-Lot Shareholders followed by an odd-lot tender offer and ultimately determined to make the tender offer available to all shareholders and not just the Odd-lot Shareholders. The Board did not consider a sale of the company to a third party buyer at any point in its consideration because the Board intends to continue to operate the Company and the purpose of the transaction is for the Company to exit the SEC reporting system and not to sell the Company. The Board relied on a third-party valuation provider’s report and fairness opinion to conclude that the transaction was fair absent an outside "market check."

At the February 14, 2006 meeting, the Board discussed the advantages and disadvantages of deregistering and possible methods to reduce the number of record shareholders below 300. They also discussed the impairment of a liquid market for a company's stock due to the deregistration of such stock as a common concern of boards of companies considering deregistration. The Board observed that since the Company’s shares were never listed and no trading market for the Company’s shares exists, such concern is not applicable to the Company. Lastly, the Board also discussed a fair process for conducting a transaction for deregistration and the role of a Special Committee as part of the process.

A subsequent special meeting of the Board was conducted on March 13, 2006. At the March 13, 2006 meeting, special counsel further reviewed with the Board the purpose of a Special Committee and the qualifications required of Board members serving on the Special Committee. The Board determined that it was in the best interest of the Company and the shareholders to establish a Special Committee comprised of independent directors to evaluate and approve the transaction for deregistration. The Board empowered the Special Committee with full authorization to 1) determine the best method for reducing the number of shareholders of record below 300 to enable the Company to exit the SEC reporting system and 2) determine the offer price for the transaction, with the assistance of a third-party financial advisor, as necessary.

In considering the composition of the Special Committee, the Board reviewed each director’s independence 1) in light of the director’s possible interest in the transaction, 2) based on the independence standards that the Company has elected to adopt, which is the NASD standard for NASDAQ traded issuers, and 3) in light of any related party transactions between the Company and such director. The Board determined that only two of the outside directors, Andrew Mathieson and Dunson Cheng, could potentially meet the independence standards.

14

The Board closely considered the relationships between the Company and Mr. Andrew Mathieson, including his beneficial ownership of approximately 6.5% of the Company’s outstanding shares due to his role as a co-Trustee for the Charlotte Bliss Taylor Trust and as a managing member of Fairview Capital Investment Management. The Board considered that 1) Mr. Mathieson personally does not hold any outstanding shares in the Company and consequently will not participate in the transaction as a shareholder, 2) pursuant to NASD's independence criteria for directors of NASDAQ traded issuers, size of ownership of Company stock by itself would not preclude a Board finding of independence; and 3) Mr. Mathieson has not engaged in any related party transaction with the Company. The Board ultimately concluded that Mr. Mathieson would qualify as an independent member to serve on the Special Committee.

The Board separately considered relationships between the Company and Dr. Dunson Cheng, including his status as the Chairman of Cathay Bank, the largest creditor of the Company. The Board considered that 1) Dr. Cheng personally does not hold any outstanding shares in the Company and consequently will not participate in the transaction as a shareholder, 2) pursuant to NASD’s independence criteria for directors of NASDAQ traded issuers, the interest payments Cathay Bank has received from DiCon under its loan to DiCon is not significant enough to Cathay Bank to preclude a finding of independence by the Board and 3) Dr. Cheng individually has not engaged in any related party transaction with the Company. The Board ultimately concluded that Dr. Cheng would qualify as an independent member to serve on the Special Committee. Accordingly, the Board designated Mr. Mathieson and Dr. Cheng to serve on the Special Committee.

In March 2006, the Special Committee met on two occasions to review possible transaction structures and financial advisor candidates. After soliciting proposals by several financial advisors, in light of its experiences with this type of project and its familiarity with the Company’s industry, the Special Committee engaged HFBE to perform a valuation study and render a fairness opinion related to a possible deregistration related transaction. During the meetings, the Special Committee further explored a two-step transaction involving an odd-lot tender offer following a modest reverse stock split designed to increase the number of Odd-lot Shareholders necessary to reduce the number of shareholders of record below 300. The Special Committee reviewed and studied the Company’s shareholder list and ultimately decided against an odd-lot tender offer as it would not be available to all shareholders. Instead, the Special Committee decided that an issuer tender offer open to all shareholders was the most favorable way to reduce the record shareholder base below 300. Based on a list of shareholders arranged by their holdings of the Company’s common stock provided by Dr. Lee, the Special Committee noted that more than 80 of the holders held 500 shares or less. Consequently, the Special Committee determined the maximum share amount for the issuer tender offer based on 500 shares multiplied by the number of shareholders.

On April 14, 2006, the Special Committee met with a representative from HFBE to receive a report on the preliminary results of HFBE's work. On April 19, 2006, HFBE presented its valuation report, a copy of which is included in this Proxy Statement as Appendix B, to the Special Committee that, based on its analysis, the range of implied equity values per share was $0.70 to $0.95 per share. After considering this information and the financial data supportive of the valuation range, the Special Committee determined, in the interest of offering a premium to the tendering shareholders and in light of the price the Company had paid to buy back shares from departing employees in the past two years, $0.96 per share to be the offer price for an issuer tender offer.

15

On April 19, 2006, the Special Committee reported its decisions regarding the transaction method and the offer price to the Board. Present at the meeting were all members of the Special Committee, all members of the Board of Directors, a representative from HFBE and special counsel. The Board ratified the issuer tender offer transaction. The Board of Directors reviewed the same valuation report presented by HFBE to the Special Committee and discussed the $0.70 to $0.95 per share range that HFBE concluded were the implied equity values per share, the price that the Company had paid to repurchase shares in the past two years, and the premium over the high end of the implied equity value necessary to induce shareholders to tender their shares in the issuer tender offer. Dr. Lee suggested that an offer price of $1.00 per share would represent an appropriate premium over the fair value of the shares. The Board then considered and concluded that an offer price of $1.00 would be a fair price. After reviewing the potential financial impact an additional premium to the price may have on the Company and concluding such to be immaterial, the Board, including members of the Special Committee, voted unanimously to set the issuer tender offer price at $1.00 per share.

On April 25, 2006, DiCon filed with the SEC tender offer materials and commenced an issuer tender offer to repurchase up to 154,500 shares of its common stock at a price of $1.00 per share (the "April Tender Offer"). Prior to the expiration of the tender offer period, the Company received SEC comments to the filed tender offer materials. On May 22, 2006, DiCon extended the April Tender Offer to respond to comments from the SEC in connection with the tender offer materials. On May 23, 2006, the Special Committee met to review the shareholders' response to the April Tender Offer to date, noting that the tender offer had been oversubscribed, thus triggering the legal requirement that the Company purchase the tendered shares on a pro rata basis. The Special Committee then determined that the April Tender Offer would not reduce the Company’s holders of record below 300. The Special Committee then instructed special counsel to explore additional alternatives to achieve the goal of so reducing the number of record of shareholders.

On May 25, 2006, the Special Committee met with the special counsel to review and discuss three possible alternatives:

| o | Alternative I - Continue with the April Tender Offer and, after completion of the April Tender Offer, reduce additional record shareholders gradually through natural attrition and deregister when the Company’s holders of record fall below 300. |

| o | Alternative II - Withdraw the April Tender Offer and execute a new two-step transaction, consisting of (1) a proposal for a reverse stock split to increase the number of Odd-lot Shareholders and (2) a new issuer tender offer for a portion of the post-stock split shares followed by deregistration when the Company’s holders of record fall below 300 after completion of the new issuer tender offer. |

| o | Alternative III - Conduct a substantial reverse stock split at a ratio designed to reduce the Company’s holders of record below 300 and thereafter deregister. |

On May 30, 2006, the Special Committee held a special meeting and discussed with management its expectations for the rate of employee attrition and confirmed that the rate of attrition was outside of management’s control. Based on input from management, the Special Committee concluded that the timing for Alternative I would be too uncertain to pursue. As to Alternative III, the Special Committee considered the uncertainties related to the requirement under the California Corporate Securities Law that a permit be obtained from the California Department of Corporations to effectuate such a split.