UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16 of the

Securities Exchange Act of 1934

For the month of February, 2025

Commission File Number 1-15106

PETRÓLEO BRASILEIRO S.A. – PETROBRAS

(Exact name of registrant as specified in its charter)

Brazilian Petroleum Corporation – PETROBRAS

(Translation of Registrant's name into English)

Avenida Henrique Valadares, 28 – 9th floor

20231-030 – Rio de Janeiro, RJ

Federative Republic of Brazil

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F ___X___ Form 40-F _______

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes _______ No___X____

INDEX

PETROBRAS

| 2 |

STATEMENT OF FINANCIAL POSITION

PETROBRAS

December 31, 2024 and 2023 (In millions of reais, unless otherwise indicated)

| Consolidated | Parent Company | ||||

| Assets | Notes | 2024 | 2023 | 2024 | 2023 |

| Cash and cash equivalents | 8 | 20,254 | 61,613 | 3,134 | 2,562 |

| Marketable securities | 8 | 26,397 | 13,650 | 13,941 | 13,644 |

| Trade and other receivables | 14 | 22,080 | 29,702 | 129,592 | 77,757 |

| Inventories | 15 | 41,550 | 37,184 | 36,774 | 31,612 |

| Recoverable income taxes | 17 | 2,545 | 1,055 | 2,321 | 731 |

| Other recoverable taxes | 17 | 9,630 | 4,648 | 9,328 | 4,392 |

| Others | 21 | 9,599 | 7,603 | 10,817 | 10,253 |

| 132,055 | 155,455 | 205,907 | 140,951 | ||

| Assets classified as held for sale | 29 | 3,157 | 1,624 | 3,455 | 2,053 |

| Current assets | 135,212 | 157,079 | 209,362 | 143,004 | |

| Trade and other receivables | 14 | 7,777 | 8,942 | 6,964 | 8,099 |

| Marketable securities | 8 | 3,605 | 11,661 | 3,605 | 11,661 |

| Judicial deposits | 19 | 72,745 | 71,390 | 72,282 | 70,968 |

| Deferred income taxes | 17 | 5,710 | 4,672 | − | − |

| Other recoverable taxes | 17 | 22,301 | 21,861 | 21,742 | 21,516 |

| Others | 21 | 15,488 | 11,209 | 16,424 | 12,230 |

| Long-term receivables | 127,626 | 129,735 | 121,017 | 124,474 | |

| Investments | 28 | 4,081 | 6,574 | 366,398 | 268,220 |

| Property, plant and equipment | 23 | 843,917 | 742,774 | 858,561 | 759,569 |

| Intangible assets | 24 | 13,961 | 14,726 | 13,772 | 14,563 |

| Non-current assets | 989,585 | 893,809 | 1,359,748 | 1,166,826 | |

| Total assets | 1,124,797 | 1,050,888 | 1,569,110 | 1,309,830 | |

| Consolidated | Parent Company | ||||

| Liabilities | Notes | 2024 | 2023 | 2024 | 2023 |

| Trade payables | 16 | 37,659 | 23,302 | 39,741 | 26,649 |

| Finance debt | 30 | 15,887 | 20,923 | 106,522 | 46,736 |

| Lease liability | 31 | 52,896 | 34,858 | 54,953 | 36,364 |

| Income taxes payable | 17 | 8,671 | 6,295 | 4,121 | 4,445 |

| Other taxes payable | 17 | 20,336 | 20,168 | 19,895 | 19,669 |

| Dividends payable | 32 | 16,452 | 17,134 | 16,334 | 16,947 |

| Provision for decommissioning costs | 20 | 10,500 | 9,837 | 10,426 | 9,661 |

| Employee benefits | 18 | 14,337 | 14,194 | 13,222 | 13,274 |

| Others | 21 | 13,652 | 14,596 | 12,045 | 12,252 |

| 190,390 | 161,307 | 277,259 | 185,997 | ||

| Liabilities related to assets classified as held for sale | 29 | 4,418 | 2,621 | 4,418 | 2,621 |

| Current liabilities | 194,808 | 163,928 | 281,677 | 188,618 | |

| Finance debt | 30 | 127,539 | 118,508 | 478,198 | 346,419 |

| Lease liability | 31 | 177,145 | 128,773 | 182,625 | 133,240 |

| Income taxes payable | 17 | 3,284 | 1,446 | 3,256 | 1,409 |

| Deferred income taxes | 17 | 9,100 | 52,820 | 14,254 | 59,000 |

| Employee benefits | 18 | 66,082 | 75,421 | 64,716 | 74,009 |

| Provisions for legal proceedings | 19 | 17,543 | 16,000 | 16,451 | 14,855 |

| Provision for decommissioning costs | 20 | 151,753 | 102,493 | 151,221 | 102,167 |

| Others | 21 | 10,029 | 9,159 | 10,706 | 9,672 |

| Non-current liabilities | 562,475 | 504,620 | 921,427 | 740,771 | |

| Current and non-current liabilities | 757,283 | 668,548 | 1,203,104 | 929,389 | |

| Share capital (net of share issuance costs) | 32 | 205,432 | 205,432 | 205,432 | 205,432 |

| Capital reserve, capital transactions and treasury shares | (2,457) | (538) | (2,241) | (322) | |

| Profit reserves | 32 | 95,193 | 159,171 | 94,977 | 158,955 |

| Accumulated other comprehensive | 67,838 | 16,376 | 67,838 | 16,376 | |

| Attributable to the shareholders of Petrobras | 366,006 | 380,441 | 366,006 | 380,441 | |

| Non-controlling interests | 28 | 1,508 | 1,899 | − | − |

| Equity | 367,514 | 382,340 | 366,006 | 380,441 | |

| Total liabilities and equity | 1,124,797 | 1,050,888 | 1,569,110 | 1,309,830 | |

The notes form an integral part of these financial statements.

| 3 |

PETROBRAS

December 31, 2024 and 2023 (In millions of reais, unless otherwise indicated)

| Consolidated | Parent Company | ||||

| Notes | 2024 | 2023 | 2024 | 2023 | |

| Sales revenues | 9 | 490,829 | 511,994 | 473,547 | 494,372 |

| Cost of sales | 10 | (244,367) | (242,061) | (237,497) | (241,098) |

| Gross profit | 246,462 | 269,933 | 236,050 | 253,274 | |

| Income (expenses) | |||||

| Selling expenses | 10 | (26,134) | (25,163) | (27,980) | (25,114) |

| General and administrative expenses | 10 | (9,931) | (7,952) | (8,509) | (6,688) |

| Exploration costs | 26 | (4,997) | (4,892) | (4,901) | (4,887) |

| Research and development expenses | (4,281) | (3,619) | (4,281) | (3,619) | |

| Other taxes | (6,708) | (4,444) | (5,215) | (3,391) | |

| Impairment losses, net | 25 | (9,371) | (13,111) | (9,567) | (12,950) |

| Other income and expenses, net | 11 | (44,372) | (19,930) | (43,050) | (18,791) |

| (105,794) | (79,111) | (103,503) | (75,440) | ||

| Income before finance income (expenses), results in equity-accounted investments and income taxes | 140,668 | 190,822 | 132,547 | 177,834 | |

| Net finance income (expense): | 12 | (82,471) | (11,861) | (101,999) | (24,679) |

| Finance income | 10,488 | 10,821 | 12,326 | 10,790 | |

| Finance expense | (32,093) | (19,542) | (51,867) | (33,884) | |

| Foreign exchange gains (losses) and inflation indexation | (60,866) | (3,140) | (62,458) | (1,585) | |

| Results in equity-accounted investments | 28 | (3,467) | (1,480) | 19,110 | 19,814 |

| Net income before income taxes | 54,730 | 177,481 | 49,658 | 172,969 | |

| Income taxes | 17 | (17,721) | (52,315) | (13,052) | (48,363) |

| Net income of the year | 37,009 | 125,166 | 36,606 | 124,606 | |

| Attributable to: | |||||

| Shareholders of Petrobras | 36,606 | 124,606 | 36,606 | 124,606 | |

| Non-controlling interests | 403 | 560 | − | − | |

| Net income of the year | 37,009 | 125,166 | 36,606 | 124,606 | |

| Basic and diluted earnings per weighted-average of common and preferred share (in R$) | 32 | 2.84 | 9.57 | 2.84 | 9.57 |

| The Notes form an integral part of these Financial Statements. | |||||

| 4 |

STATEMENT OF COMPREHENSIVE INCOME

PETROBRAS

December 31, 2024 and 2023 (In millions of reais, unless otherwise indicated)

| Consolidated | Parent Company | ||||

| Notes | 2024 | 2023 | 2024 | 2023 | |

| Net income for the year | 37,009 | 125,166 | 36,606 | 124,606 | |

| Items that will not be reclassified to the statement of income: | |||||

| Actuarial gains (losses) on post-employment defined benefit plans | 18 | 19,111 | (17,552) | 18,653 | (17,260) |

| Deferred income tax | (2,286) | 1,341 | (2,280) | 1,341 | |

| 16,825 | (16,211) | 16,373 | (15,919) | ||

| Share of other comprehensive income in equity-accounted investments | − | − | 438 | (278) | |

| Items that may be reclassified subsequently to the statement of income: | |||||

| Unrealized gains (losses) on cash flow hedge - highly probable future exports | |||||

| Recognized in equity | (85,507) | 22,410 | (85,507) | 22,410 | |

| Reclassified to the statement of income | 16,246 | 18,846 | 16,191 | 18,371 | |

| Deferred income tax | 23,549 | (14,027) | 23,567 | (13,866) | |

| 33 | (45,712) | 27,229 | (45,749) | 26,915 | |

| Translation adjustments in investees (1) | |||||

| Recognized in equity | 81,818 | (21,461) | 81,813 | (21,460) | |

| 81,818 | (21,461) | 81,813 | (21,460) | ||

| Share of other comprehensive income (loss) in equity-accounted investments | |||||

| Recognized in equity | 28 | (1,450) | 1,306 | (1,413) | 1,620 |

| (1,450) | 1,306 | (1,413) | 1,620 | ||

| Other comprehensive income (loss) | 51,481 | (9,137) | 51,462 | (9,122) | |

| Total comprehensive income | 88,490 | 116,029 | 88,068 | 115,484 | |

| Comprehensive income attributable to: | |||||

| Shareholders of Petrobras | 88,068 | 115,484 | 88,068 | 115,484 | |

| Non-controlling interests | 422 | 545 | − | − | |

| Total comprehensive income | 88,490 | 116,029 | 88,068 | 115,484 | |

| (1) In the Consolidated, it includes credit effect of R$3,125 (debit effect of R$1,154, as of December 31, 2023), referring to associates and joint ventures. | |||||

| The notes form an integral part of these financial statements. | |||||

| 5 |

PETROBRAS

December 31, 2024 and 2023 (In millions of reais, unless otherwise indicated)

| Consolidated | Parent Company | ||||

| Notes | 2024 | 2023 | 2024 | 2023 | |

| Cash flows from operating activities | |||||

| Net income for the year | 37,009 | 125,166 | 36,606 | 124,606 | |

| Adjustments for: | |||||

| Pension and medical benefits | 18 | 15,788 | 7,695 | 15,350 | 7,494 |

| Results of equity-accounted investments | 28 | 3,467 | 1,480 | (19,110) | (19,814) |

| Depreciation, depletion and amortization | 35 | 67,033 | 66,204 | 69,532 | 69,609 |

| Impairment of assets, net | 25 | 9,371 | 13,111 | 9,567 | 12,950 |

| Inventory write-down (write-back) to net realizable value | 15 | (214) | (40) | − | − |

| Allowance for credit loss on trade and other receivables, net | 1,536 | 205 | 1,507 | 202 | |

| Exploratory expenditure write-offs | 26 | 2,654 | 2,087 | 2,653 | 2,087 |

| Gain on disposal/write-offs of assets | 11 | (1,171) | (6,511) | (795) | (5,776) |

| Foreign exchange, indexation and finance charges | 84,138 | 12,707 | 99,933 | 21,176 | |

| Income taxes | 17 | 17,721 | 52,315 | 13,052 | 48,363 |

| Revision and unwinding of discount on the provision for decommissioning costs | 21,107 | 10,132 | 21,062 | 10,106 | |

| Results from co-participation agreements in bid areas | 11 | (1,482) | (1,399) | (1,482) | (1,399) |

| Early termination and cash outflows revision of lease agreements | 11 | (1,938) | (2,086) | (1,954) | (2,174) |

| Losses with legal, administrative and arbitration proceedings, net | 11 | 5,395 | 3,982 | 5,118 | 3,467 |

| Decrease (Increase) in assets | |||||

| Trade and other receivables | 9,207 | 672 | 1,118 | (73,648) | |

| Inventories | (1,560) | 7,926 | (5,277) | 7,245 | |

| Judicial deposits | 1,295 | (8,663) | 1,560 | (8,623) | |

| Other assets | (1,020) | 1,619 | 612 | 1,713 | |

| Increase (Decrease) in liabilities | |||||

| Trade payables | 5,517 | (4,741) | 4,545 | (7,182) | |

| Other taxes payable | (15,803) | (2,363) | (16,552) | (799) | |

| Pension and medical benefits | (5,408) | (4,617) | (5,380) | (4,596) | |

| Provisions for legal proceedings | (2,554) | (2,927) | (2,389) | (2,559) | |

| Other employee benefits | (480) | 1,726 | (663) | 1,468 | |

| Provision for decommissioning costs | (5,275) | (4,491) | (5,181) | (4,457) | |

| Other liabilities | (3,896) | (2,781) | (2,758) | (2,854) | |

| Income taxes paid | (36,400) | (50,712) | (35,128) | (49,494) | |

| Net cash provided by operating activities | 204,037 | 215,696 | 185,546 | 127,111 | |

| Cash flows from investing activities | |||||

| Acquisition of PP&E and intangible assets | (79,856) | (60,315) | (78,547) | (60,002) | |

| Acquisition of equity interests | (127) | (120) | 83 | 463 | |

| Proceeds from disposal of assets – Divestment | 4,381 | 18,232 | 4,374 | 18,215 | |

| Financial compensation from co-participation agreements | 1,951 | 2,032 | 1,951 | 2,032 | |

| Divestment (Investment) in marketable securities (1) | 501 | 237 | (37,470) | 11,175 | |

| Dividends received (2) | 787 | 439 | 2,037 | 2,007 | |

| Net cash (used in) provided by investing activities | (72,363) | (39,495) | (107,572) | (26,110) | |

| Cash flows from financing activities | |||||

| Changes in non-controlling interest | (509) | (14) | − | − | |

| Financings and loans operations, net: | |||||

| Proceeds from finance debt | 30 | 12,027 | 10,716 | 230,827 | 124,844 |

| Repayment of principal - finance debt | 30 | (35,933) | (21,080) | (136,354) | (71,686) |

| Repayment of interest - finance debt (2) | 30 | (10,276) | (9,900) | (25,473) | (21,118) |

| Repayment of lease liability | 31 | (42,672) | (31,335) | (44,178) | (32,537) |

| Dividends paid to Shareholders of Petrobras | 32 | (100,305) | (97,925) | (100,305) | (97,925) |

| Share repurchase program | 32 | (1,919) | (3,644) | (1,919) | (3,644) |

| Dividends paid to non-controlling interests | (387) | (253) | − | − | |

| Net cash used in financing activities | (179,974) | (153,435) | (77,402) | (102,066) | |

| Effect of exchange rate changes on cash and cash equivalents | 6,941 | (2,876) | − | − | |

| Net change in cash and cash equivalents | (41,359) | 19,890 | 572 | (1,065) | |

| Cash and cash equivalents at the beginning of the period | 61,613 | 41,723 | 2,562 | 3,627 | |

| Cash and cash equivalents at the end of the period | 20,254 | 61,613 | 3,134 | 2,562 | |

| (1) In the parent company, it includes values referring to changes in investments in FIDC-NP receivables. | |||||

| (2) The company classifies dividends/interest received and interest paid as cash flow from investing activities and cash flow from financing activities, respectively. | |||||

| The notes form an integral part of these financial statements. | |||||

| 6 |

STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY

PETROBRAS

December 31, 2024 and 2023 (In millions of reais, unless otherwise indicated)

| Accumulated other comprehensive income | |||||||||||

| Share capital (net of share issuance costs) | Capital reserve, capital transactions and treasury shares | Cumulative translation adjustment | Actuarial losses on defined benefit pension plans | Cash flow hedge – highly probable future exports | Other comprehensive income and deemed cost | Legal reserves | Retained earnings | Equity attributable to the shareholders of Petrobras | Non-controlling interests | Consolidated Shareholders’ Equity | |

| 205,432 | 3,318 | 101,306 | (27,245) | (46,258) | (2,305) | 128,346 | − | 362,594 | 1,791 | 364,385 | |

| Balance at January 1st, 2023 | 205,432 | 3,318 | 25,498 | 128,346 | − | 362,594 | 1,791 | 364,385 | |||

| Treasury shares | − | (3,644) | − | − | − | − | − | − | (3,644) | − | (3,644) |

| Capital transactions | − | 4 | − | − | − | − | − | − | 4 | (16) | (12) |

| Net income of the year | − | − | − | − | − | − | − | 124,606 | 124,606 | 560 | 125,166 |

| Other comprehensive income | − | − | (21,460) | (16,197) | 27,229 | 1,306 | − | − | (9,122) | (15) | (9,137) |

| Additional dividends approved at General Shareholders’ Meeting of 2023 | − | − | − | − | − | − | (35,815) | − | (35,815) | − | (35,815) |

| Expired unclaimed dividends | − | − | − | − | − | − | − | 33 | 33 | − | 33 |

| Appropriations: | |||||||||||

| Appropriations of net income in reserves | − | − | − | − | − | − | 52,220 | (52,220) | − | − | − |

| Dividends | − | − | − | − | − | − | 14,204 | (72,419) | (58,215) | (421) | (58,636) |

| Balance at December 31, 2023 | 205,432 | (322) | 79,846 | (43,442) | (19,029) | (999) | 158,955 | − | 380,441 | 1,899 | 382,340 |

| 205,432 | (322) | 16,376 | 158,955 | − | 380,441 | 1,899 | 382,340 | ||||

| Balance at January 1st, 2024 | 205,432 | (322) | 79,846 | (43,442) | (19,029) | (999) | 158,955 | − | 380,441 | 1,899 | 382,340 |

| Treasury shares | − | (1,919) | − | − | − | − | − | − | (1,919) | − | (1,919) |

| Capital transactions | − | − | − | − | − | − | − | − | − | (511) | (511) |

| Net income of the year | − | − | − | − | − | − | − | 36,606 | 36,606 | 403 | 37,009 |

| Other comprehensive income | − | − | 81,813 | 16,811 | (45,712) | (1,450) | − | − | 51,462 | 19 | 51,481 |

| Additional dividends approved at General Shareholders’ Meeting of 2024 | − | − | − | − | − | − | (36,139) | − | (36,139) | − | (36,139) |

| Expired unclaimed dividends | − | − | − | − | − | − | − | 316 | 316 | − | 316 |

| Appropriations: | |||||||||||

| Appropriations of net income in reserves | − | − | − | − | − | − | 790 | (790) | − | − | − |

| Dividends | − | − | − | − | − | − | (28,629) | (36,132) | (64,761) | (302) | (65,063) |

| Balance at December 31, 2024 | 205,432 | (2,241) | 161,659 | (26,631) | (64,741) | (2,449) | 94,977 | − | 366,006 | 1,508 | 367,514 |

| 205,432 | (2,241) | 67,838 | 94,977 | − | 366,006 | 1,508 | 367,514 | ||||

The notes form an integral part of these financial statements.

| 7 |

PETROBRAS

December 31, 2024 and 2023 (In millions of reais, unless otherwise indicated)

| Consolidated | Parent Company | |||

| 2024 | 2023 - Reclassified | 2024 |

2023 - Reclassified | |

| Income | ||||

| Sales of products, services provided and other revenues | 644,511 | 633,932 | 623,573 | 612,956 |

| Allowance for credit loss on trade and other receivables, net | (1,536) | (205) | (1,507) | (202) |

| Revenues related to construction of assets for own use | 77,616 | 52,798 | 76,999 | 52,108 |

| 720,591 | 686,525 | 699,065 | 664,862 | |

| Inputs acquired from third parties | ||||

| Materials consumed and products for resale | (99,730) | (96,049) | (88,886) | (83,773) |

| Materials, power, third-party services and other operating expenses | (135,397) | (108,019) | (138,744) | (115,888) |

| Tax credits on inputs acquired from third parties | (39,761) | (36,760) | (41,590) | (38,792) |

| Impairment of assets, net | (9,371) | (13,111) | (9,567) | (12,950) |

| (284,259) | (253,939) | (278,787) | (251,403) | |

| Gross added value | 436,332 | 432,586 | 420,278 | 413,459 |

| Depreciation, depletion and amortization | (67,033) | (66,204) | (69,532) | (69,609) |

| Net added value produced by the Company | 369,299 | 366,382 | 350,746 | 343,850 |

| Transferred added value | ||||

| Share of profit of equity-accounted investments | (3,467) | (1,480) | 19,110 | 19,814 |

| Finance income | 10,488 | 10,821 | 12,326 | 10,790 |

| Rental, royalties and others | 3,102 | 3,024 | 5,596 | 5,550 |

| 10,123 | 12,365 | 37,032 | 36,154 | |

| Total added value to be distributed | 379,422 | 378,747 | 387,778 | 380,004 |

| Distribution of added value | ||||

| Personnel and officers | ||||

| Direct compensation | ||||

| Salaries | 19,676 | 17,382 | 17,485 | 15,501 |

| Variable compensation | 4,954 | 5,043 | 4,313 | 4,572 |

| 24,630 | 22,425 | 21,798 | 20,073 | |

| Benefits | ||||

| Short-term benefits | 1,111 | 2,045 | 872 | 1,714 |

| Pension plan | 4,331 | 4,609 | 4,199 | 4,485 |

| Medical plan | 13,205 | 4,594 | 12,696 | 4,342 |

| 18,647 | 11,248 | 17,767 | 10,541 | |

| FGTS | 1,369 | 1,222 | 1,255 | 1,123 |

| 44,646 | 34,895 | 40,820 | 31,737 | |

| Taxes | ||||

| Federal (1) (2) | 121,988 | 132,688 | 118,516 | 128,503 |

| State | 63,097 | 47,649 | 62,430 | 47,008 |

| Municipal | 715 | 698 | 255 | 187 |

| Abroad (1) | 4,459 | 2,665 | − | − |

| 190,259 | 183,700 | 181,201 | 175,698 | |

| Financial institutions and suppliers | ||||

| Interest, and exchange and indexation charges | 101,428 | 29,106 | 122,791 | 41,893 |

| Rental and leases | 6,080 | 5,880 | 6,360 | 6,070 |

| 107,508 | 34,986 | 129,151 | 47,963 | |

| Shareholders | ||||

| Dividends | 14,091 | 52,918 | 14,091 | 52,918 |

| Interest on capital | 22,041 | 19,501 | 22,041 | 19,501 |

| Non-controlling interests | 403 | 560 | − | − |

| Profit retention | 474 | 52,187 | 474 | 52,187 |

| 37,009 | 125,166 | 36,606 | 124,606 | |

| Added value distributed | 379,422 | 378,747 | 387,778 | 380,004 |

(1) Includes production taxes. (2) As of December 31, 2024 and 2023, includes amounts referring to deferred income tax and social contribution as per Note 17.1. | ||||

| The notes form an integral part of these financial statements | ||||

| 8 |

| NOTES TO THE FINANCIAL STATEMENTS PETROBRAS (In millions of reais, unless otherwise indicated) |

| 1. | The Company and its operations |

Petróleo Brasileiro SA – Petrobras, hereinafter referred to as “Petrobras” or “company”, is a mixed capital company, under the control of the Federal Government, with an indefinite term, governed by the rules of private law - in general - and, specifically, by the Law No. 6,404, of December 15, 1976 (Brazilian Corporation Law), by Law No. 13,303, of June 30, 2016 (State-owned Companies' Legal Statute), by Decree No. 8,945, of December 27, 2016, and by its Bylaws.

Petrobras’ shares are listed on the Brazilian stock exchange (B3) in the Level 2 Corporate Governance special listing segment and, therefore, the Company, its shareholders, its managers and fiscal council members are subject to provisions under its regulation (Level 2 Regulation - Regulamento de Listagem do Nível 2 de Governança Corporativa da Brasil Bolsa Balcão – B3). These Regulations shall prevail over the statutory provisions, in the event of prejudice to the rights of the recipients of public offerings provided for in the Company's Bylaws, except in certain cases, due to a specific rule.

The Company is dedicated to prospecting, drilling, refining, processing, trading and transporting crude oil from producing onshore and offshore oil fields and from shale or other rocks, as well as oil products, natural gas and other liquid hydrocarbons. In addition, Petrobras carries out energy related activities, such as research, development, production, transport, distribution and trading of all forms of energy, as well as other related or similar activities.

Petrobras may perform any of the activities related to its corporate purpose, directly, through its wholly-owned subsidiaries, controlled companies, alone or through joint ventures with third parties, in Brazil or abroad.

The economic activities linked to its corporate purpose will be developed by the company, in a free competition with other companies, according to market conditions, observing the other legal principles and guidelines, such as the Petroleum Law (Law No. 9,478/97) and the Gas Law (Law nº 14.134/21). However, Petrobras may have its activities, as long as they are in line with its corporate purpose, guided by the Union, in order to contribute to the public interest that justified its creation, aiming at meeting the objective of the national energy policy, when:

I – established by law or regulation, as well as under agreements provisions with a public entity that is competent to establish such obligation, abiding with the broad publicly stated of such instruments; and

II – the cost and revenues thereof have been broken down and disseminated in a transparent manner.

In this case, the Company’s Investment Committee and Minority Shareholders Committee will evaluate and measure the difference between market conditions and the operating result or economic return of the obligation assumed by the company, in such a way that the Union compensates, for each fiscal year, the difference between market conditions and the operating result or economic return of the assumed obligation.

1.1. Highlights of the year

Petrobras presented positive operational results in 2024, generating value for society and its shareholders. The debt was within the gross debt level established in the Strategic Plan 2024-2028 (SP 24-28), reaching US$ 60 billion.

Total oil and gas production in 2024 was 2.7 million barrels of oil equivalent per day (boed), within the target established in SP 24-28. The main factors that resulted in this operational performance were: i) entry into operation of two new platforms in the pre-salt layer - FPSO Maria Quitéria in the Jubarte field and the FPSO Marechal Duque de Caxias in the Mero field; ii) reaching the maximum oil production capacity of the FPSO Sepetiba platform, in the Mero field; and (iii) start of commercial operation of the Natural Gas Processing Unit (UPGN), located at the Boaventura Energy Complex in Itaboraí, Rio de Janeiro. These factors offset the reduction in production due to maintenance stoppages, the decline of mature fields.

| 9 |

| NOTES TO THE FINANCIAL STATEMENTS PETROBRAS (In millions of reais, unless otherwise indicated) |

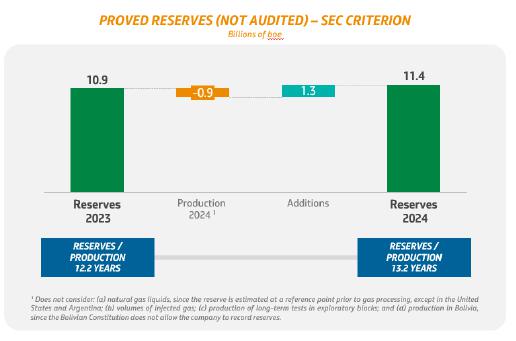

In 2024, according to SEC - Securities and Exchange Commission criteria, the company maintained the trajectory of significant addition of reserves, focusing on profitable assets and aligned with the search for a fair energy transition. The incorporation occurred mainly due to the continued development of the Atapu and Sépia Fields and of the performance of the assets, with emphasis on the Búzios, Itapu, Tupi and Sépia fields, in the Santos Basin. There were no relevant changes in reserves resulting from changes in the price of oil (more details in Additional information on oil and natural gas exploration and production activities – unaudited).

Petrobras also estimates reserves according to the ANP/SPE criteria (National Agency for Petroleum, Natural Gas and Biofuels / Society of Petroleum Engineers). As of December 31, 2024, proven reserves according to this criterion reached 11.7 billion barrels of oil equivalent. The main differences between the two criteria are detailed in note 4.1.

The cash provided by operational activities, besides the proceeds from finance debt and the other sources of funds were used for Property, Plant and Equipment (note 23), debt service fulfillment (that includes the prepayment of securities in the international capital market and the amortization of leases (notes 30 and 31), and used for payment of dividends (note 32).

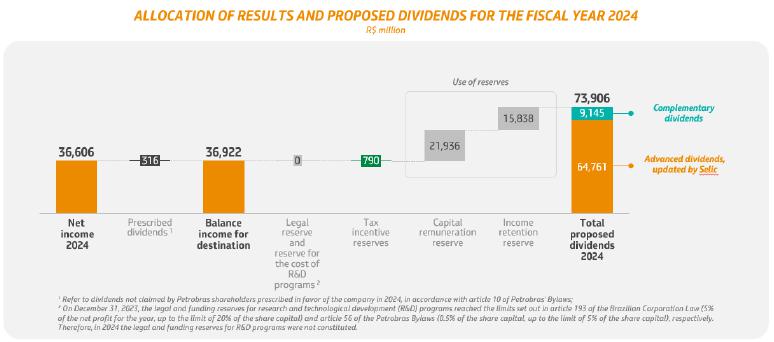

The proposed allocation of the result to be submitted for deliberation at the 2025 Ordinary General Meeting, which considers the distribution of dividends for the 2024 financial year, is in line with the shareholder remuneration policy (note 32).

| 10 |

| NOTES TO THE FINANCIAL STATEMENTS PETROBRAS (In millions of reais, unless otherwise indicated) |

Gross debt in reais was impacted mainly by the 27.9% devaluation of the real against the dollar in 2024 (note 7).

The financial result in 2024 was mainly influenced by the loss with exchange rate variation of the real against the dollar and by the financial expenses from the enrollment to the tax settlement program, reflecting the charges and financial updates (notes 12 and 33).

In litigation, the highlight of the year was the reduction of non-accrued tax contingencies, due to the enrollment to the tax settlement program involving CIDE and PIS/COFINS on Imports (notes 19 and 23).

| 11 |

| NOTES TO THE FINANCIAL STATEMENTS PETROBRAS (In millions of reais, unless otherwise indicated) |

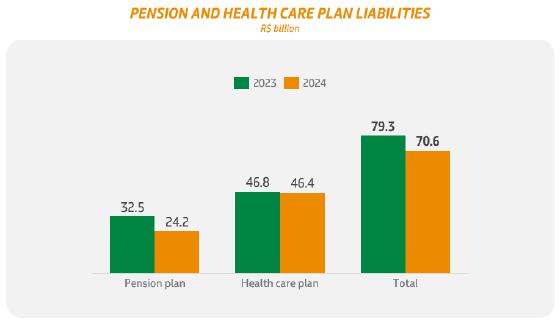

The annual review of actuarial liabilities with post-employment benefit plans reflected a decrease in liabilities, recognized as a counterpart in shareholders’ equity, resulting from the increase in the discount rate applied to actuarial obligations, offset, in part, by the return on guaranteeing assets marked to market and the variation of the hospital medical costs, in addition to recognition in the result of the past service cost due to the change in the health plan's funding relationship (note 18).

The review of the economic, financial and operational assumptions of Business Plan 25-29, which includes the project portfolio and reserve estimates, supported the review of the provision for decommissioning areas for the year 2024 (note 20), in addition to the devaluation of Real against the U.S. dollar. Such assumptions also impact recoverability tests (note 25). The review of the provision for decommissioning areas generated an increase in liabilities as a counterpart to property, plant and equipment (note 23) to the crude oil fields in operation and other operating expenses, mainly referring to fields in the process of being returned (note 11).

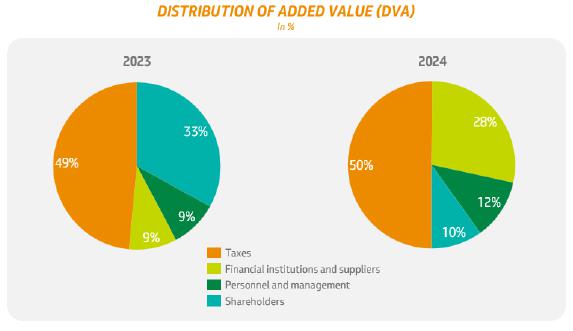

The wealth generated by the company in 2024, in the amount of R$380 billion (R$378 billion in 2023), was distributed as follows:

| 12 |

| NOTES TO THE FINANCIAL STATEMENTS PETROBRAS (In millions of reais, unless otherwise indicated) |

In addition, Petrobras' financial statements in US dollars, converted based on Technical Pronouncement CPC 02 – “Effects of Changes in Exchange Rates and Conversion of Financial Statements” (IAS 21), are also disclosed and filed. The table below presents the main information in millions of dollars:

| Consolidated | ||

| 2024 | 2023 | |

| Sales revenues | 91,416 | 102,409 |

| Gross profit | 45,972 | 53,974 |

| Income before finance income (expenses), results in equity-accounted investments and income taxes | 26,876 | 38,033 |

| Net income for the year – Petrobras’ shareholders | 7,528 | 24,884 |

| Cash and cash equivalents | 3,271 | 12,727 |

| Property, plant and equipment | 136,285 | 153,424 |

| Finance debt and leases – current and non-current | 60,311 | 62,600 |

| Shareholders’ equity | 59,349 | 78,975 |

| Cash flow from operating activities | 37,984 | 43,212 |

| Cash flow from investing activities | (13,369) | (7,955) |

| Cash flow from financing activities | (33,088) | (30,700) |

| 2. | Basis of preparation and presentation of financial statements |

The consolidated and individual (Parent Company) financial statements have been prepared in accordance with the IFRS Accounting Standards as issued by the International Accounting Standards Board (IASB), and with the pronouncements issued by the Brazilian Accounting Pronouncements Committee (Comitê de Pronunciamentos Contábeis - CPC) that were approved by the Brazilian Securities and Exchange Commission (Comissão de Valores Mobiliários – CVM).

All relevant information related to financial statements, and only them, are presented and corresponds to the information used by the Company’s Management.

The financial statements have been prepared under the historical cost convention, except when otherwise indicated.

In preparing these financial statements, Management used judgments, estimates and assumptions that affect the application of accounting practices and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates. The relevant estimates and judgments that require a higher level of complexity are disclosed in note 4.

The Company's Board of Directors, at a meeting held on February 26, 2025, authorized the disclosure of these financial statements.

| 2.1. | Statement of added value |

Brazilian corporate law requires publicly-held companies to prepare a Statement of Added Value and disclose it as an integral part of the set of financial statements.

| 13 |

| NOTES TO THE FINANCIAL STATEMENTS PETROBRAS (In millions of reais, unless otherwise indicated) |

This statement aims to present information relating to the wealth created by the company and the way in which such wealth was distributed and is presented as supplementary information for IFRS purposes.

This statement was prepared in accordance with Technical Pronouncement CPC 09 (R1) - Statement of Added Value, reviewed in February 2024 and approved by CVM Resolution 199/24.

The review generated a restatement of the Statement of Added Value between components of the wealth created (revenue, inputs acquired from third parties and depreciation, depletion and amortization) without affecting the net added value produced by the company, as follows:

| Consolidated | Parent Company | |||||

| Disclosed on 12.31.2023 |

CPC 09 (R1) Effect | Restated 12.31.2023 | Disclosed 12.31.2023 | CPC 09 (R1) Effect | Restated 12.31.2023 | |

| Revenues | 694,684 | (8,159) | 686,525 | 673,061 | (8,199) | 664,862 |

| Inputs acquired from third parties | (252,282) | (1,657) | (253,939) | (249,786) | (1,617) | (251,403) |

| Gross added value | 442,402 | (9,816) | 432,586 | 423,275 | (9,816) | 413,459 |

| Depreciation, depletion and amortization | (76,020) | 9,816 | (66,204) | (79,425) | 9,816 | (69,609) |

| Net added value produced by the company | 366,382 | − | 366,382 | 343,850 | − | 343,850 |

The main changes introduced by CPC 09 (R1) that impacted the company's Statement of Added Value were:

| · | Adjustments to the net realizable value of inventories – they are no longer presented as inputs acquired from third parties and are now disclosed as other revenues; |

| · | Depreciation, depletion and amortization – the portion capitalized in the company's assets is no longer presented as revenue related to the construction of assets for use and the portion used in liabilities for decommissioning areas is no longer presented as inputs acquired from third parties. Thus, depreciation, depletion and amortization now represent the amounts recognized in the statement of income for the period and normally used to reconcile the cash flow from operating activities and the net income. |

| 2.2. | Functional currency |

The functional currency of Petrobras and all of its Brazilian subsidiaries is the Brazilian Real, which is the currency of its primary economic environment of operation. The functional currency of the direct controlled entities that operate in the international economic environment is the U.S. dollar.

The statements of income and cash flow of investees, with a functional currency other than the Parent Company, are converted into reais at the average monthly exchange rate, assets and liabilities are translated at the final rate and other items of shareholders' equity are converted at the historical rate.

Exchange variations on investments in subsidiaries and affiliates, with a functional currency different from the Parent Company, are recorded in shareholders' equity, as a cumulative translation adjustment, and are transferred to the statement of income when investments are sold.

| 3. | Material accounting policies |

For a better understanding of the recognition and measurement basis applied in the preparation of the financial statements, the accounting practices are presented in the respective notes that deal with the topics of their applications.

| 4. | Key estimates and judgements |

The preparation of the consolidated financial information requires the use of estimates and judgments for certain transactions. Next is presented: (i) key judgments; and (ii) the main sources of uncertainty with a significant risk of causing material adjustments to the company's accounting estimates over the next fiscal year.

| 14 |

| NOTES TO THE FINANCIAL STATEMENTS PETROBRAS (In millions of reais, unless otherwise indicated) |

| 4.1. | Recognition of exploration costs and oil and natural gas reserves estimates |

After obtaining the legal rights to explore a specific area, the Company uses the successful efforts method to recognize costs incurred in connection with the exploration and evaluation of mineral resources, before demonstrating technical and commercial feasibility of extracting those resources. This method requires a direct relationship between costs incurred and mineral resources for these costs to be characterized as assets. The types of exploration costs and their respective recognition are presented in note 26.

The moment in which the technical and commercial feasibility of extracting a mineral resource is determined requires management judgments. An internal commission of technical executives of the Company periodically reviews the conditions of each well, by analysis of geological, geophysical and engineering data, as well as economic conditions, operating methods and government regulations.

The Company considers that the technical and commercial feasibility of a mineral resource can be demonstrated when the project has all the necessary information to characterize the reservoir as a proved reserve. Costs associated with non-commercial mineral resources are recognized as expenses in the period when identified.

According to the definitions prescribed by the SEC, proved oil and natural gas reserves are those quantities of oil and gas which, by analysis of geoscience and engineering data, can be estimated with reasonable certainty to be economically feasible from a given date, from known reservoirs and under existing economic conditions, operating methods and government regulation.

The Company also determines reserves according to the criteria of the National Agency for Petroleum, Natural Gas and Biofuels / Society of Petroleum Engineers (ANP/SPE). The main differences between these criteria and the SEC criterion are related to the use of different economic assumptions and the possibility of considering as reserves, in the ANP/SPE criteria, the volumes expected to be produced beyond the concession contract expiration date in fields in Brazil, according to the ANP technical reserves regulations.

| 4.2. | Impairment testing |

| 4.2.1. | Main sources of estimation uncertainty related to impairment testing |

Impairment testing involves uncertainties mainly related to: (a) the average Brent prices and to the Brazilian real/U.S. dollar average exchange rate, whose estimates are relevant to virtually all of the Company's operating segments; (b) discount rates; and (c) estimated proved and probable reserves (according to the criteria established by the ANP/SPE). A significant number of interdependent variables are derived from these key assumptions and there is a high degree of complexity in their application in determining value in use for impairment testing. Value in use is the present value of expected future cash flows expected to arise from an asset or cash-generating unit.

A sensitivity analysis for assets or CGUs most sensitive to future impairment losses or reversals in the next year is presented in note 25.

Average Brent prices and average exchange rate

The markets for crude oil and natural gas have a history of significant price volatility and, although prices can drop or increase precipitously, industry prices over the long term tends to continue being driven by market supply and demand fundamentals.

Brent prices and exchange rate projections are derived from the Strategic Plan and are consistent with market evidence, such as independent macro-economic forecasts, industry analysts and experts. Backtesting analysis and feedback processes in order to continually improve forecast techniques are also performed.

The Company’s oil price forecast model is based on a nonlinear relationship between variables reflecting market supply and demand fundamentals. This model also takes into account other relevant factors, such as the effects of the Organization of the Petroleum Exporting Countries (OPEC) decisions on the oil market, industry costs, idle capacity, oil and gas production forecasted by specialized firms, and the relationship between the oil price and the Brazilian Real/U.S. dollar exchange rate.

The process of projecting Brazilian Real/U.S. dollar exchange rate is based on econometric models that consider long-term assumptions involving observable inputs, such as commodity prices, country risk, interest rates in the United States and the value of the U.S. dollar relative to a basket of foreign currencies (U.S. Dollar Index – USDX).

Changes in the economic environment may result in changing assumptions and, consequently, the recognition of impairment losses or reversals on certain assets or CGUs. For example, the Company’s sales revenues and refining margins are directly impacted by Brent price variations, as well as Brazilian Real/U.S. dollar exchange rate variations, which also impacts our capital and operating expenditures.

Note 25 presents Brent prices and exchange rate estimates adopted by the Company.

| 15 |

| NOTES TO THE FINANCIAL STATEMENTS PETROBRAS (In millions of reais, unless otherwise indicated) |

Discount rates

The discount rates used in impairment tests reflect specific risks associated with the estimated cash flows of the assets or CGUs. For example, changes in the economic and political environment may result in higher country risk projections, causing increases in the discount rates used in impairment tests, as well as investment decisions that result in the postponement or interruption of projects considering specific risks related to non-completion or delayed start of operations.

Note 25 presents the main discount rates applied in impairment tests.

Estimated proved and probable reserves

Reserves estimates, according to the criteria established by the ANP/SPE (as set out in note 4.1) are revised at least annually, carried out based on the re-evaluation of pre-existing data and/or new information available related to the production and geology of the reservoirs, as well as changes in prices and costs used in the estimates. Revisions may also result from significant changes in the Company’s strategy for development projects or in the production capacity.

Although the Company is reasonably certain that proved reserves will be produced, the timing and amount recovered can be affected by a sort of factors including completion of development projects, reservoir performance, regulatory aspects and significant changes in long-term oil and gas price levels.

| 4.2.2. | Identifying cash-generating units for impairment testing |

A cash-generating unit (CGU) represents the smaller identifiable group of assets that generate cash inflows, which are largely independent of the cash inflows of other assets or groups of assets. Identifying CGUs requires management assumptions and judgment, based on the Company’s business and management model. The level of asset disaggregation in CGUs can reach the limit of assets being tested individually.

Changes in CGUs resulting from the review of investment, strategic or operational factors, may result in changes in the interdependencies of assets and, consequently, alter the aggregation or breakdown of assets that were part of certain CGUs, which may influence their ability to generate cash and cause additional losses or reversals in the recovery of such assets. If the approval for the sale of a CGU’s component occurs between the reporting date and the date of the issuance of the consolidated financial statements, the Company reassesses whether the value in use of this component, estimated with the information existing at the reporting date, reasonably represents its fair value, net of sales expenses. Such information must include evidence of the stage at which management was committed to the sale of the CGU’s component.

The primary considerations in identifying the CGUs are set out as follows:

| a) | Exploration and Production CGUs: |

| i) | Crude oil and natural gas producing properties: comprise assets related to exploration and production development of a field or a cluster (group of two or more fields) in Brazil and abroad. At December 31, 2024, there are 30 fields and 15 clusters representing different Exploration and Production CGUs in Brazil. |

| ii) | Equipment not related to crude oil and natural gas producing properties: comprise assets that ceased to operate, such as platforms, drilling rigs and other assets which are not part of any CGU and are assessed for impairment separately. |

| b) | Refining, transportation and marketing CGUs: |

i) CGU Set of refining and logistics assets: comprises refineries, terminals and pipelines, as well as logistics assets operated by Transpetro. The combined and centralized operation of such assets aims at serving the market at the lowest overall costs and preserving the strategic value of the whole set of assets in the long term. The operational planning is made in a centralized manner and these assets are not managed, measured or evaluated by their individual results. Refineries do not have autonomy to choose the oil to be processed, the mix of oil products to produce, the markets in which these products will be traded, which amounts will be exported, which intermediaries will be received and to decide the sale prices of oil products. Operational decisions are analyzed through an integrated model of operational planning for market supply, considering all the options for production, imports, exports, logistics and inventories, seeking to maximize the Company’s global performance. The decision on new investments is not based on the individual assessment of the asset where the project will be installed, but on the additional result for the CGU as a whole. The model that supports the entire planning, used in technical and economic feasibility studies of new investments in refining and logistics, seeks to allocate a certain type of oil, or a mix of oil products, define market supply (area of influence), aiming at achieving the best integrated results. Pipelines and terminals are a complementary and interdependent portion of the refining assets, required to supply the market.

| 16 |

| NOTES TO THE FINANCIAL STATEMENTS PETROBRAS (In millions of reais, unless otherwise indicated) |

ii) CGU Boaventura Energy Complex - Utilities: composed of assets that supports the natural gas processing plant (UPGN) of the route 3 integrated project;

iii) CGU Boaventura Energy Complex - Refining: set of assets that remain in hibernation and are being evaluated for use in other projects.

iv) CGU Second Refining Unit of RNEST: comprises assets of the second refining unit of Abreu e Lima refinery and associated infrastructure;

v) CGU Transportation: comprises assets relating to Transpetro’s fleet of vessels;

vi) CGU Hidrovia: comprises the fleet of vessels under construction of the Hidrovia project (transportation of ethanol along the Tietê River);

vii) Nitrogen fertilizer plants: each plant represents individual CGUs, wheter it is hibernated or in operation; and

viii) Other RT&M CGUs: valued at the smallest identifiable group of assets that generate cash inflows independent of cash inflows from other assets or other groups of assets.

| c) | Gas and Low Carbon Energies CGUs: |

i) CGU Integrated Systems: set of assets formed by natural gas processing plants in Itaboraí, Cabiúnas and Caraguatatuba, grouped together due to the contractual characteristics of the Integrated Processing System and the Integrated Transportation System;

ii) CGUs of Natural Gas Processing Plants: each remaining natural gas processing plant represents a separate CGU;

iii) CGU Set of thermoelectric power generation plants (UTEs): the operation and trade of energy of this CGU are carried out and coordinated in an integrated manner. The economic results of each of these plants in the integrated portfolio are highly dependent on each other, due to operational optimization aimed at maximizing the overall result;

iv) CGU Biodiesel: set of assets comprising the biodiesel plants, reflecting the production planning and operation process, that takes into consideration domestic market conditions, the production capacity of each plant, as well as the results of biofuels auctions and raw materials supply;

v) CGU Quixadá: comprises the assets of biofuel plant located in the city of Quixadá, state of Ceará;

vi) Other G&LCE CGUs: valued at the smallest identifiable group of assets that generate cash inflows independent of cash inflows from other assets or other groups of assets.

Further information on impairment testing is set out in note 25.

| 4.3. | Sources of estimation uncertainty related to depreciation, depletion and amortization |

As presented in note 23, assets directly related to the oil and gas production are depleted using the units of production method, calculated by monthly production over the respective developed proved reserves, except for the signature bonuses, which are calculated over total proved reserves.

Proved developed reserves are those for which recovery can be expected: (i) through existing wells, equipment and operating methods, or in which the cost of the required equipment is relatively minor compared to the cost of a new well; and (ii) through extraction equipment and operational infrastructure installed at the time of the reserves estimate, if the extraction is carried out by means that do not involve a well.

Estimates of proved reserves volumes used in the units of production method are prepared by Company’s technicians according to the SEC definitions (as described in note 4.1). Revisions to the Company’s proved developed and undeveloped reserves impact prospectively the amounts of depreciation, depletion and amortization recognized in the statement of income and the carrying amounts of oil and gas properties assets. Information on uncertainties related to reserve volume estimates are presented in note 4.1.

Therefore, assuming all other variables remain constant, a decrease in estimated proved reserves would increase, prospectively, depreciation, depletion and amortization expense, while an increase in reserves would reduce depreciation, depletion and amortization.

| 17 |

| NOTES TO THE FINANCIAL STATEMENTS PETROBRAS (In millions of reais, unless otherwise indicated) |

| 4.4. | Sources of estimation uncertainty related to pension plan and other post-employment benefits |

The net actuarial liability represents the Company's actuarial obligations, net of fair value of plan assets (when applicable), at present value, as described in note 18.3.2.

The actuarial obligations and net expenses related to defined benefit pension and health care post-employment plans are computed based on several financial and demographic assumptions, of which the most significant are:

a) Discount rate: comprises the projected future inflation in addition to an equivalent discounted interest rate that matches the duration of the pension and health care obligations with the future yield curve of long-term Brazilian Government Bonds; and

b) Medical costs: comprise the projected growth rates based on per capita health care benefits paid over the last five years, which are used as a basis for projections, converged to the general price inflation index within 30 years.

In conjunction with other actuarial assumptions, the discount rate and rate of variation of medical and hospital costs are reviewed annually and may differ from actual results due to changes in market and economic conditions.

The measurement uncertainties associated with the defined benefit obligation and a sensitivity analysis of discount rates and changes in medical costs are disclosed in notes 18.3.6 and 18.3.7, respectively.

| 4.5. | Sources of estimation uncertainty related to provisions for legal proceedings and contingencies |

The Company is part in arbitrations and in legal and administrative proceedings involving civil, tax, labor and environmental issues arising from the normal course of its business and makes use of estimates to recognize the amounts and the probability of outflow of resources, based on reports and technical assessments from legal advisors and on management’s assessment.

These estimates are performed individually, or aggregated if there are cases with similar characteristics, primarily considering factors such as assessment of the plaintiff’s demands, consistency of the existing evidence, jurisprudence on similar cases and doctrine on the subject. Specifically for lawsuits by outsourced employees, the Company estimates the expected loss based on a statistical procedure, due to the number of actions with similar characteristics.

Arbitral, legal and administrative decisions against the Company, new jurisprudence and changes of existing evidence can result in changes on the probability of outflow of resources and on the estimated amounts, according to the assessment of the legal basis.

Note 19 provides further detailed information about contingencies and legal proceedings.

| 4.6. | Sources of estimation uncertainty related to decommissioning costs |

The Company has legal obligations to remove equipment and restore onshore and offshore areas at the end of operations. Its most significant asset removal obligations relate to offshore areas. Estimates of costs for future environmental cleanup and remediation activities are based on current information about costs and expected plans for remediation. The timing of abandonment and dismantling of areas is based on the length of reserves depletion, in accordance with the ANP/SPE definitions. Therefore, revisions to reserves estimates that result in changes in the timing of reserves depletion may impact the provision for decommissioning cost. For additional information about revisions to the Company’s reserves estimates, see note 4.1.

These obligations are recognized at present value, using a risk-free discount rate, adjusted to the Company's credit risk. Changes in the discount rate can cause significant variations in the recognized amount, due to the long-term nature until abandonment.

The calculation to determine the amounts to be provisioned are complex, since: i) the obligations are long-term; ii) the contracts and regulations contain subjective definitions of the removal and remediation practices and criteria involved when the events occur; and iii) asset removal technologies and costs are constantly changing, along with regulations, environmental, safety and public relations considerations. Additionally, abandonment costs are mostly denominated in foreign currency, which may result in significant changes in the estimates due to changes in the exchange rates overtime.

The Company constantly conducts studies to incorporate technologies and procedures to optimize the process of abandonment, considering industry best practices. However, the timing and amounts of future cash flows are subject to significant uncertainty.

In the event of a total or partial sale of an interest in Exploration and Production agreements, the company remains jointly and severally liable for decommissioning costs of areas after production has ceased, if the purchaser fails to comply with this obligation, as determined by the ANP.

| 18 |

| NOTES TO THE FINANCIAL STATEMENTS PETROBRAS (In millions of reais, unless otherwise indicated) |

The sensitivity analysis of discount rates and other information on provision for decommissioning costs are presented in note 20.

| 4.7. | Sources of estimation uncertainty related to leases |

The Company uses incremental borrowing rates to determine the present value of the lease payments, when the interest rate implicit in the lease cannot be readily determined.

The determination of incremental rates requires estimates based on corporate funding rates (obtained from the yields on bonds issued by Petrobras), which take into account the risk-free rate and the Company's credit risk premium, adjusted to reflect the specific conditions and characteristics of the lease, such as the risk of the country's economic environment, guarantees, currency and duration of the payment flow.

The present value of lease liabilities is determined based on the incremental rates estimated at the start date of each lease. Therefore, even in cases where lease agreements have similar characteristics, their cash flows may be discounted at significantly different incremental rates depending on the Company's corporate funding rates on the start date of each lease.

Note 31 presents information on lease arrangements by class of underlying assets.

| 4.8. | Sources of estimation uncertainty related to cash flow hedge accounting involving the Company’s future exports |

The Company determines its “highly probable future exports” based on its current Business Plan and on short-term estimates on a monthly basis. The highly probable future exports are determined by a percentage of projected exports revenues.

The estimate of the amount of highly probable future exports considers future uncertainty regarding the Brent oil prices, oil production and demand for products in a model which optimizes the Company's operations and investments, in addition to considering the historical profile of exported volume in relation to total oil production.

As described in note 33.4.1, foreign exchange gains and losses relating to the effective portion of hedging instruments are recognized in other comprehensive income and reclassified to the statement of income within finance income (expense) in the periods when the hedged item affects the statement of income. However, if future exports for which foreign exchange gains and losses hedging relationship has been designated is no longer expected to occur, any related cumulative foreign exchange gains or losses that have been recognized in other comprehensive income from the date the hedging relationship was designated to the date the Company revoked the designation is immediately recycled from other comprehensive income to the statement of income.

For the long-term, future exports forecasts are reviewed whenever the Company reviews its Strategic Plan assumptions, while for the short-term future exports are reviewed monthly. The approach for determining highly probable future exports is reviewed annually, at least.

See note 33.4.1 for more detailed information about cash flow hedge accounting and a sensitivity analysis of the cash flow hedge involving future exports.

| 4.9. | Sources of estimation uncertainty related to income taxes |

Income taxes rules and regulations may be interpreted differently by tax authorities, and situations may arise in which these interpretations differ from the Company's understanding.

Uncertainties over income taxes treatments represent the risks that the tax authority does not accept a certain tax treatment applied by the Company, mainly related to different interpretations of deductions and additions to the income taxes (Imposto de Renda sobre Pessoa Jurídica - IRPJ and Contribuição Social sobre Lucro Líquido – CSLL) calculation basis. The Company evaluates each uncertain tax treatment separately or in a group where there is interdependence in relation to the expected result.

The Company estimates the probability of acceptance of an uncertain tax treatment by the tax authority based on technical assessments by its legal advisors, considering precedent jurisprudence applicable to current tax legislation, which may be impacted mainly by changes in tax rules or court decisions which may affect the analysis of the fundamentals of uncertainty. The tax risks identified are evaluated, treated and, when applicable, follows a pre-determined tax risk management methodology.

If it is probable that the tax authorities will accept an uncertain tax treatment, the amounts recorded in the financial statements are consistent with the tax records and, therefore, no uncertainty is reflected in the measurement of current or deferred income taxes. If it is not probable that the tax authorities will accept an uncertain tax treatment, the uncertainty is reflected in the measurement of current or deferred income taxes in the financial statements.

| 19 |

| NOTES TO THE FINANCIAL STATEMENTS PETROBRAS (In millions of reais, unless otherwise indicated) |

To the extent that the Company concludes that it is unlikely that the tax authorities will accept an uncertain tax treatment, the amounts recorded in the financial statements must reflect this uncertainty in the measurement of current or deferred income taxes.

The effect of uncertainty for each uncertain tax treatment is estimated by using the method that provides the best prediction of the resolution of the uncertainty. The most probable amount method provides as an estimate the single most probable amount in a set of possible outcomes, while the expected amount method represents the sum of the amounts weighted by the probability in relation to a range of possible outcomes.

Additional information on uncertainty over income taxes treatments is disclosed in Note 17.1.

| 4.10. | Sources of estimation uncertainty related to expected credit losses |

Credit losses correspond to the difference between all contractual cash flows owed to the Company and all cash flows that the entity expects to receive, discounted at the original effective interest rate. The expected credit loss of a financial asset corresponds to the average of expected credit losses weighted by the respective default risks.

Expected credit losses on financial assets are based on assumptions relating to risk of default, the determination of whether or not there has been a significant increase in credit risk, expectation of recovery, among others. The Company uses judgment for such assumptions in addition to information from credit rating agencies and inputs based on collection delays.

Notes 14.2 and 14.3 provide details on the expected credit losses recognized by the Company.

| 4.11. | Sources of estimation uncertainty related to the compensation for the surplus volume for the Transfer of Rights Agreement |

As a result of the Second Bidding Round for the Surplus Volume of the Transfer of Rights Agreement under the Production Sharing regime, the Company signed amendments and new agreements in 2022 with partners in the Atapu and Sépia fields. These agreements provide, in addition to the compensation already received upon signature, possible additional amounts receivable that may be owed to the Company, according to the conditions described in note 29.3.

Additionally, over the last few years the Company has sold assets considered non-strategic and established partnerships in E&P assets aiming, among other objectives, at sharing risks and developing new technologies. Such transactions were carried out through partnerships (note 27) and divestments, with procedures aligned with current legislation and regulatory bodies. In some of these transactions, contingent receipts are also provided for, subject to contractual clauses (note 29.3).

| 5. | Climate Change |

Climate change may result in both negative and positive effects for the Company. Potential negative effects of climate change for the Company are referred to as climate-related risks (climate risks). Conversely, potential positive effects arising from climate change for the Company are referred to as climate-related opportunities.

Climate risks are categorized as: (i) climate-related transition risks (transition risks); and (ii) climate-related physical risks (physical risks).

| 5.1. | Potential effects of climate risks on accounting estimates |

Accounting estimates are monetary amounts in financial statements that are subject to measurement uncertainty.

The following information used in relevant accounting estimates of the Company is largely determined based on the assumptions and projections of the Petrobras Business Plan (PN):

| · | value in use for impairment of assets testing purposes (note 4.2.1); |

| · | timing and costs used in measuring the provision for decommissioning costs (note 4.6); |

| · | highly probable future exports used in cash flow hedge accounting involving the Company’s future exports (note 4.8); and |

| · | useful life of PP&E and intangible assets used in measuring depreciation, depletion and amortization expenses (notes 23 and 24). |

| 20 |

| NOTES TO THE FINANCIAL STATEMENTS PETROBRAS (In millions of reais, unless otherwise indicated) |

As specified in the following topic, the company considered the impacts related to climate risks in its Business Planning approved by the Board of Directors, updated each year, which includes actions to achieve its climate commitments and its ambition to neutralize its net operational emissions of Greenhouse Gases (GHG) (scopes 1[1] and 2[2]) by 2050.

The ambition and commitments above do not constitute guarantees of future performance by the company and are subject to assumptions that may not materialize and to risks and uncertainties that are difficult to predict.

| a) | Transition risk to low carbon economy |

Transition risks arise from efforts to the transition to a low-carbon economy. In this category, the Company has identified the following risks that can reasonably be expected to affect its cash flows, access to financing or cost of capital:

| Risk | Description | Time length (2) |

| Market | Increased demand for low-carbon energy and products and preference for fossil fuels with lower greenhouse gas (GHG) intensity in production processes, leading to reduced demand for oil and a consequent drop in the prices of fossil fuels. In Brazil, demand for our products may be affected, for example, by increased demand for alternative fuels, also stimulated by Public Policies integrated into the Fuel of the Future Law (1), among others. | Medium and long-term |

| Technological | Loss of competitiveness due to the non-implementation or implementation of ineffective or ineffective technologies to reduce emissions from our operations and products. | Medium and long-term |

| Regulatory | Establishment of stricter regulatory requirements regarding the control of GHG emissions and other requirements related to climate change, which may cause operational restrictions and financial penalties for our activities. In Brazil, an example is the regulation for the adoption of a carbon pricing instrument, considering the provisions of Law 15.042/2024, which institutes the Brazilian Greenhouse Gas Emissions Trading System (SBCE), resulting in additional costs for our operations. | Medium and long-term |

| Legal and Reputational | Litigation and/or reputational damage due to non-compliance with climate commitments. | Medium-term |

(1) Legislation that aligns a series of initiatives to stimulate and guide the production of biofuels and reduce greenhouse gas emissions – GHG, including the National Sustainable Aviation Fuel Program (ProBioQAV), the National Green Diesel Program (PNDV) and the National Program for Decarbonization of Natural Gas Producers and Importers and for Incentive to Biomethane. Furthermore, it changes the maximum and minimum limits for the anhydrous ethanol blend content in gasoline and the biodiesel blend content in diesel oil and provides for the regulation and inspection of carbon dioxide capture and geological storage activities and the regulation of the production and sale of synthetic fuels. It also promotes the integration of initiatives and measures adopted within the scope of the National Biofuels Policy (RenovaBio), the Green Mobility and Innovation Program (Mover Program), the Brazilian Vehicle Labeling Program (PBEV) and the Vehicle Emissions Control Program (Proconve). (2) Criteria adopted for the time horizon: short term (1 year), medium term (between 1 and 5 years) and long term (after 5 years). | ||

The risks above were considered in the development of the Company's Business Plan 2025-2029 (PN 25-29). Such consideration was based on the following external environment assumptions that reflect the dynamics of the energy sector:

| • | Moderate economic growth compared to the recent past; |

| • | Shifts in consumption habits and behaviors; |

| • | Public policies focusing on mobility, air quality and adaptation of urban infrastructure to climate change; |

| • | International coordination in efforts to reduce GHG emissions; |

| • | Regulations in favor of energy transition and decarbonization, which will drive the reduction of fossil fuel consumption; and |

| • | Diffusion of end-use technologies that reduce the need for fossil fuel consumption. |

[1] Direct GHG emissions that occur from sources that are owned or controlled by the company.

[2] GHG emissions from the generation of purchased electricity and steam consumed by the company, which occur at the facilities where the electricity and steam are generated.

| 21 |

| NOTES TO THE FINANCIAL STATEMENTS PETROBRAS (In millions of reais, unless otherwise indicated) |

As a result of this, demand and prices, both domestic and international, of the main products considered in the Strategic Plan 25-29 are negatively affected.

In 2024, the Company adopted three distinct scenarios that are used for different purposes in its planning activities. These scenarios are called Adaptation, Negotiation, and Commitment. In all of them, there is a slowdown and subsequent contraction of fossil fuel sources. The Negotiation scenario, which is used as a reference scenario for quantifying the Company's Business Plan, considers that fossil fuels, which currently represent approximately 80% of primary energy sources of the world matrix, will represent around 48% by 2050. The share of oil will decrease from the current 30% to around 20% of the world's primary energy sources.

The Brent price considered in the reference scenario of the Business Plan decreases from US$80 per barrel in 2024 to US$65 per barrel in 2050. For additional information about the behavior of the Brent price, considered in the Company's Business Plan reference scenario, please see note 25. The following table compares the oil price used in the reference scenario of the Strategic Plan for the years 2030 and 2050 with those projected in the Announced Pledges Scenario (APS) and Net Zero Emission (NZE) scenarios by the International Energy Agency (IEA), even if they are not used corporately by the company:

| Brent price US$/Barrel | 2030 | 2050 |

| PN | 65 | 65 |

| APS | 72 | 58 |

| NZE | 42 | 25 |

According to the IEA, the APS scenario considers that all climate commitments made by governments around the world, including Nationally Determined Contributions (NDCs), as well as long-term net-zero targets, will be met in full and on time, with an increase of approximately 1.7oC in temperature by 2100 (with a 50% probability of occurrence). As for the NZE scenario, according to the IEA, it presents a pathway for the global energy sector to achieve net-zero CO2 emissions by 2050, consistent with limiting the temperature increase to 1.5 °C (with at least a 50% probability of occurrence).

The Business Plan also includes Company's actions to achieve the carbon sustainability commitments, such as low-carbon Research and Development (R&D) projects and decarbonization projects for operations. These actions aim to address transition risks as well as reflect climate opportunities.

The Company's accounting estimates did not incorporate the effect of carbon pricing. Currently, due to uncertainties regarding the implementation and dynamics of the carbon market in Brazil, the Company considers it necessary to await the regulation of Law No. 15,042 of 2024, which establishes the Brazilian Greenhouse Gas Emissions Trading System (SBCE). This regulation will provide the necessary and sufficient details to reliably and reasonably assess the impact on the cash flows of Petrobras's assets and its CGUs.

a.1) Potential effects on the value in use in impairment tests

When measuring the value in use of its assets, the Company bases its cash flow projections on reasonable and supportable assumptions that represent management's best estimate of the range of economic conditions.

A faster transition to a low-carbon economy than projected in the Business Plan could result in Brent prices and demand for the Company’s products that are lower than the ones considered to estimate the value in use of the Company’s assets for impairment testing purposes.

The reduction in the value in use of the Company's assets may result in the recognition of losses due to the non-recoverability of the carrying amounts of these assets.

Given that the oil price is a variable that decisively influences the recoverable amount of assets, the Company carried out a sensitivity analysis of the effect of using the Brent prices considered in the APS and NZE scenarios, for the impairment test of the Company's E&P assets in Brazil.

Using the prices in the APS and NZE scenarios to perform a sensitivity analysis on projected gross revenues deducted of production taxes, net of income taxes, and keeping unchanged all other components, variables, assumptions and data for calculating the recoverable amount, the Company's E&P segment, regarding the impairment loss recognized by the Company, as disclosed in note 25, would have additional impairment reversal of R$ 2,710 in the APS scenario and additional impairment losses of R$ 69,505 in the NZE scenario, concentrated in the Campos basin fields.

The Company does not consider this sensitivity analysis, based on APS and NZE Brent price scenarios, to be the best estimates to determine expected effects on the recoverable amount of assets, sales revenues or net income.

| 22 |

| NOTES TO THE FINANCIAL STATEMENTS PETROBRAS (In millions of reais, unless otherwise indicated) |

Considering that the Company did not incorporate in its accounting estimates the carbon price effects, the Company carried out a sensitivity analysis of the effect of GHG emissions pricing costs on the impairment test of assets in the E&P segment in Brazil, considering a monetary charge per ton of CO2 emission starting from 2030, and the existence of free emission allowances.

In this context, using a base price of US$ 10/CO2 in 2030, US$ 49.7/CO2 in 2035, US$ 68/CO2 in 2040, US$ 84.8/CO2 in 2045, and US$ 100.3/CO2 in 2050, including gradual emission exemptions, to simulate additional cash outflows (net of income taxes), and keeping all other components, variables, assumptions and data for the calculation of recoverable amount unchanged, the E&P segment of the Parent Company would have an additional R$ 1,439 impairment loss.

The Company does not consider this sensitivity analysis of the effect of greenhouse gas emissions pricing costs on the impairment test of assets to be the best estimate to determine expected effects on the recoverable amount, neither the estimated effects on expenses nor net income.

a.2) Potential effects on decommissioning costs

Due to its operations, the Company has legal obligations to remove equipment and restore onshore and offshore areas. On December 31, 2024, the provision for decommissioning costs recognized by the Parent Company totaled R$ 161,647, as set out in Note 20. On an undiscounted basis the nominal amount would be R$ 321,709.

The estimated timing used by the Company to account for decommissioning costs are consistent with the useful lives of the related assets. The average decommissioning period of oil and gas assets weighted by the carrying amounts of such assets is 14 years.

During 2024, there were no issuances of government regulations related to climate matters that changed or had potential to change the period for decommissioning the Parent Company's assets, as well as no identification any triggers that would accelerate the expected dates for decommissioning the Company's assets due to the Company’s climate goals and ambition to neutralize GHG emissions in activities under its control (scopes 1 and 2) by 2050.

A transition to a low-carbon economy that is faster than anticipated by the Company may accelerate the timing to remove equipment and restore onshore or offshore areas. Such acceleration would increase the present value of the decommissioning obligations recognized by the Company.

To illustrate the effect of a possible acceleration of the transition to a low-carbon economy, the Company estimates that the provision for decommissioning costs would increase by R$ 6,786, R$ 22,001 and R$ 36,612 if the timing currently used were brought forward by one, three and five years, respectively. This sensitivity analysis assumed that all other components, variables, assumptions and data for calculating the provision remained unchanged. The year ranges used are not intended to be predictions of likely future events or outcomes.

a.3) Potential effects on “highly probable future exports” used in cash flow hedge accounting involving the Company's future exports

A transition to a low-carbon economy that is faster than it was anticipated by the Company may negatively effect the Company's future exports. Such effect may result in certain exports, whose foreign exchange gains or losses were designated for hedge accounting, no longer be considered highly probable, but remain forecasted, or, depending on the magnitude of the transition and its speed, cease to be considered forecasted. The consequences of such effects are described in the accounting policy of note 33.4.1 (a) involving the Company's future exports.

The calculation of “highly probable future exports” is based on the projected exports in the Business Plan, as set out in note 4.8. The Company considers only a portion of its projected exports as “highly probable future exports”. When determining future exports as highly probable, and therefore eligible as a hedged item for application of cash flow hedge accounting, the Company considers the effects related to the transition to a low-carbon economy. Carbon prices were not incorporated in such estimates.