Exhibit A

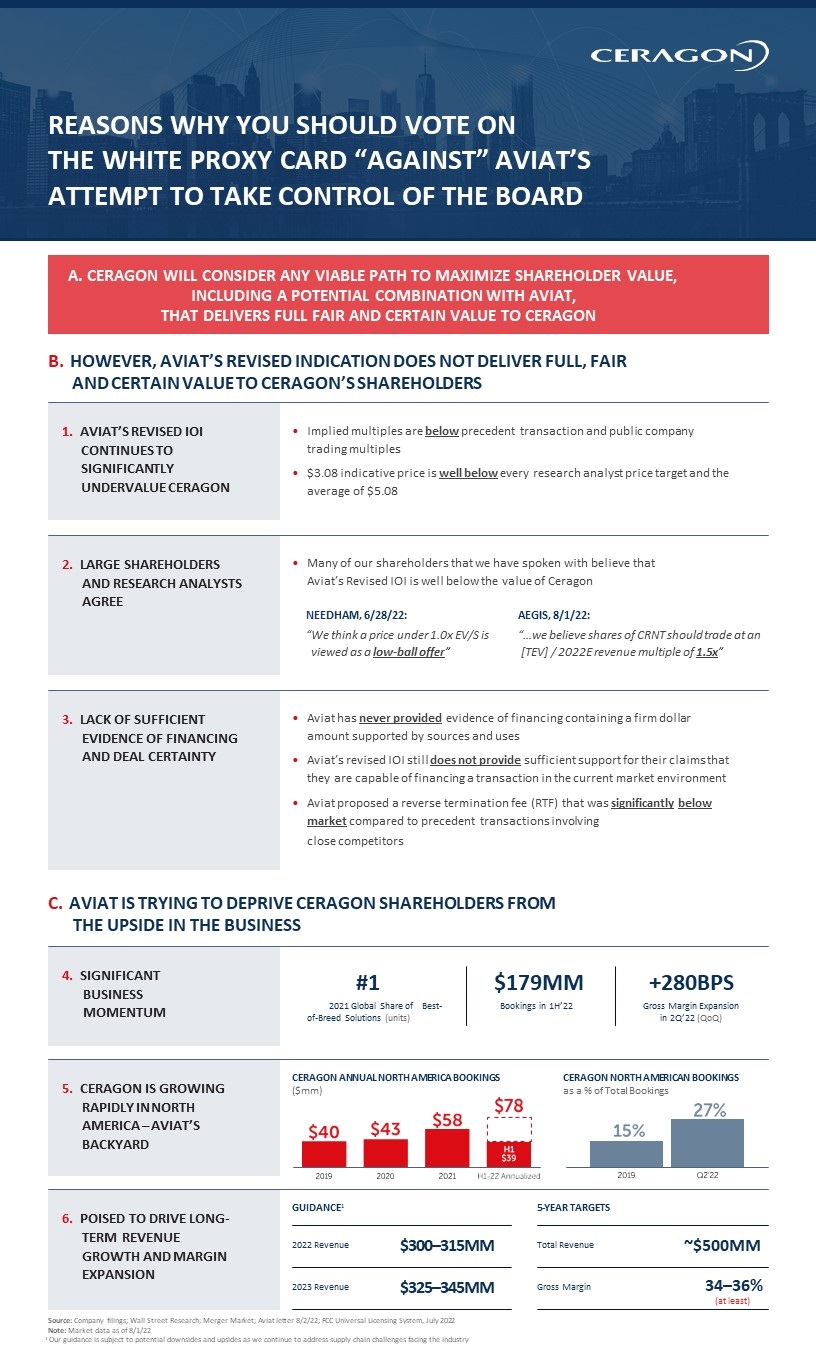

B. HOWEVER, AVIAT’S REVISED INDICATION DOES NOT DELIVER FULL, FAIR AND CERTAIN VALUE TO CERAGON’S SHAREHOLDERS 1. AVIAT’S REVISED IOI CONTINUES TO SIGNIFICANTLY UNDERVALUE CERAGON Source: Company filings; Wall Street Research; Merger Market; Aviat letter 8/2/22; FCC Universal Licensing System, July 2022 Note: Market data as of 8/1/22 1 Our guidance is subject to potential downsides and upsides as we continue to address supply chain challenges facing the industry Many of our shareholders that we have spoken with believe that Aviat’s Revised IOI is well below the value of Ceragon 3. LACK OF SUFFICIENT EVIDENCE OF FINANCING AND DEAL CERTAINTY Aviat has never provided evidence of financing containing a firm dollar amount supported by sources and uses Aviat’s revised IOI still does not provide sufficient support for their claims that they are capable of financing a transaction in the current market environment Aviat proposed a reverse termination fee (RTF) that was significantly below market compared to precedent transactions involving close competitors C. AVIAT IS TRYING TO DEPRIVE CERAGON SHAREHOLDERS FROM THE UPSIDE IN THE BUSINESS #1 2021 Global Share of Best-of-Breed Solutions (units) $179MM Bookings in 1H’22 +280BPS Gross Margin Expansion in 2Q’22 (QoQ) CERAGON NORTH AMERICAN BOOKINGS as a % of Total Bookings CERAGON ANNUAL NORTH AMERICA BOOKINGS ($mm) Implied multiples are below precedent transaction and public company trading multiples $3.08 indicative price is well below every research analyst price target and the average of $5.08 2. LARGE SHAREHOLDERS AND RESEARCH ANALYSTS AGREE NEEDHAM, 6/28/22: “We think a price under 1.0x EV/S is viewed as a low-ball offer” AEGIS, 8/1/22: “…we believe shares of CRNT should trade at an [TEV] / 2022E revenue multiple of 1.5x” 6. POISED TO DRIVE LONG-TERM REVENUE GROWTH AND MARGIN EXPANSION GUIDANCE1 5. CERAGON IS GROWING RAPIDLY IN NORTH AMERICA – AVIAT’S BACKYARD 5-YEAR TARGETS $300–315MM $325–345MM ~$500MM 34–36% (at least) 4. SIGNIFICANT BUSINESS MOMENTUM 2022 Revenue 2023 Revenue Total Revenue Gross Margin A. CERAGON WILL CONSIDER ANY VIABLE PATH TO MAXIMIZE SHAREHOLDER VALUE, INCLUDING A POTENTIAL COMBINATION WITH AVIAT, THAT DELIVERS FULL FAIR AND CERTAIN VALUE TO CERAGON REASONS WHY YOU SHOULD VOTE ON THE WHITE PROXY CARD “AGAINST” AVIAT’S ATTEMPT TO TAKE CONTROL OF THE BOARD

D. CERAGON’S BOARD IS FAR SUPERIOR THAN AVIAT’S HAND-PICKED NOMINEES TO PROTECT THE INTERESTS OF CERAGON’S SHAREHOLDERS 7. AVIAT HAS LAUNCHED THIS PROXY FIGHT TO OUST THE CERAGON DIRECTORS TO FORCE ITS HIGHLY CONDITIONAL, LOW- BALL BID 9. CERAGON’S DIRECTORS ARE PROVEN VALUE CREATORS WITH DECADES OF EXPERIENCE SUPPORTING M&A TRANSACTIONS Zohar Zisapel: One of the prominent leaders of Israeli telecom with substantial experience in creating value for shareholders (>100% TSRs at Amdocs and Silicom) Ira Palti: Former President and CEO of Ceragon and has successfully helped transition CEO role to Doron Yael Langer: Oversaw sales of companies on 5 separate occasions (Radlan, RND, Sanrad, RiT, Radvision) and achieved 481% TSR while on the board of Radware David Ripstein: current CEO of SatixFy and former CEO of Radcom where he achieved 311% TSR Ilan Rosen: extensive private equity background and 39% during his tenure at VocalTec, culminating in the merger with Tdsoft Shlomo Liran: 118% TSR at Maytronics, 68% TSR at Minrav Rami Hadar: Extensive M&A experience as the co-founder, CEO and/or C-level exec of three different Telecom companies Our Board has been open to exploring a potential transaction with Aviat, having met with its representatives many times since 2017 Aviat, however, is attempting to replace our highly qualified directors with their unqualified, hand-picked nominees to take control of the Board, which we can only infer is an attempt to force a low-ball sale to Aviat — they should not be entrusted with leading negotiations on your behalf Aviat has a history of abandoning negotiations after the parties have exchanged confidential information; Given that track record, we communicated in our last meeting in June 2022 the need for appropriate deal protections to ensure the Ceragon shareholders would be protected in the event Aviat were to try to walk away — rather than continuing negotiations, Aviat responded with their hostile campaign six days later Aviat began stealthily accumulating shares as early as February 2022 in the midst of our negotiations — it is now clear that Aviat’s disingenuous positioning at the June 2022 meeting was merely a ruse for their hostile campaign Aviat has already dropped their low-ball price once, and they can reduce their price again Aviat has launched their proxy fight in violation of our shareholder-approved Articles, which allow the appointment of only up to three directors at the upcoming Extraordinary General Meeting (“EGM”), in the event all three Ceragon directors they propose to remove are indeed removed, and issued a proxy statement and a gold proxy card for the EGM, which have no legal basis. Aviat designed its offer to give almost all upside to Aviat shareholders, not to Ceragon’s shareholders. 8. AVIAT’S NOMINEES HAVE NO TELECOM OR ADEQUATE PUBLIC COMPANY BOARD EXPERIENCE WE URGE SHAREHOLDERS TO PROTECT THEIR INVESTMENT BY VOTING ONLY ON THE WHITE PROXY CARD AGAINST AVIAT’S ATTEMPT TO TAKE CONTROL OF THE BOARD AND IGNORING AVIAT’S GOLD PROXY CARD Source: FactSet; BoardEx; Company filings 2 TSR relative to S&P 500 over the period between May 2016 and July 2020, including reinvestment of dividends CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS This document contains statements that constitute “forward-looking statements” within the meaning of the Securities Act of 1933, as amended and the Securities Exchange Act of 1934, as amended, and the safe-harbor provisions of the Private Securities Litigation Reform Act of 1995. Ceragon intends forward-looking terminology, such as believes, expects, may, will, should, anticipates, plans or similar expressions to identify forward-looking statements, or other comparable terminology, although not all forward-looking statements contain these identifying words. Such statements are subject to certain risks and uncertainties, which could cause Ceragon’s actual results to differ materially from those projected in such forward-looking statements. Such risks and uncertainties include, but are not limited to, those that are described in Ceragon’s most recent Annual Report on Form 20-F and as may be supplemented from time to time in Ceragon’s other filings with the SEC, all of which are expressly incorporated herein by reference. Forward-looking statements relate to the date initially made, and Ceragon undertakes no obligation to update them. Ceragon’s public filings are available on the Securities and Exchange Commission’s website at www.sec.gov, and may also be obtained from Ceragon’s website at www.ceragon.com AVIAT’S DISSIDENT NOMINEES VS Michelle Clayman Paul Delson Jonathan Foster Overboarded (80)% TSR2 Dennis Sadlowski 0% 0/5 40% 2/5 60% 3/5 Combined Craig Weinstock M&A / Strategic Alternatives Public Company Board Telecom Experience CERAGON’S BOARD 100% 7/7 100% 7/7 100% 7/7 AVIAT’S HOSTILE TAKEOVER ATTEMPT IS NOT IN THE BEST INTEREST OF CERAGON SHAREHOLDERS