UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the Securities

Exchange Act of 1934

Filed by the registrant ☐

Filed by a party other than the registrant ☒

Check the appropriate box:

| ☐ | Preliminary proxy statement |

| ☐ | Confidential, for use of the Commission only (as permitted by Rule 14a-6(e)(2)) |

| ☐ | Definitive proxy statement |

| ☒ | Definitive additional materials |

| ☐ | Soliciting material pursuant to Section 240.14a-12 |

| BROADWIND, INC. |

| (Name of Registrant as Specified in Its Charter) |

WM ARGYLE FUND, LLC JAY DOUGLAS ARMBURGER RYAN BOGENSCHNEIDER CHRISTINE M. CANDELA JAMES M. ROBINSON IV |

| (Name of Person(s) Filing Proxy Statement, if Other Than the Registrant) |

Payment of filing fee (Check the appropriate box):

| ☒ | No fee required. |

| ☐ | Fee paid previously with preliminary materials. |

| ☐ | Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a-6(i)(1) and 0-11. |

Disclaimers

Important Information

WM Argyle Fund, LLC (“Argyle” or the “Fund”), Jay Douglas Armburger, Ryan Bogenschneider, Christine M. Candela and James M. Robinson IV(collectively and together with the Fund, the "Participants") have filed with the Securities and Exchange Commission (the "SEC") a definitive proxy statement and accompanying form of GREEN proxy to be used in connection with the solicitation of proxies from the shareholders of Broadwind, Inc. (the "Company"). All shareholders of the Company are advised to read the definitive proxy statement and other documents related to the solicitation of proxies by the Participants, as they contain important information, including additional information related to the Participants. The definitive proxy statement and an accompanying GREEN proxy card will be furnished to some or all of the Company's shareholders and is, along with other relevant documents, available at no charge at the Fund's website at www.bwen2023.com.

Information about the Participants and a description of their direct or indirect interests by security holdings is contained in the definitive proxy statement filed by the Participants with the SEC on April 11, 2023. This document is available free of charge from the sources described above.

General Considerations

This presentation is for general informational purposes only, is not complete and does not constitute an agreement, offer, a solicitation of an offer, or any advice or recommendation to enter into or conclude any transaction or confirmation thereof (whether on the terms shown herein or otherwise). This presentation should not be construed as legal, tax, investment, financial or other advice. The views expressed in this presentation represent the opinions of the Fund and are based on publicly available information with respect to the Company and the other companies referred to herein. The Fund recognizes that there may be confidential information in the possession of the companies discussed in this presentation that could lead such companies to disagree with the Fund's conclusions. Certain financial information and data used herein have been derived or obtained from filings made with the SEC or other regulatory authorities and from other third party reports. The Fund has not sought or obtained consent from any third party (other than the individuals who have provided the testimonials in this presentation) to use any statements or information indicated herein as having been obtained or derived from statements made or published by third parties, nor has it paid for any such statements. Any such statements or information should not be viewed as indicating the support of such third party for the views expressed herein. The Fund does not endorse third-party estimates or research which are used in this presentation solely for illustrative purposes. No representation or warranty, express or implied, is made that data or information, whether derived or obtained from filings made with the SEC or any other regulatory agency or from any third party, are accurate. Past performance is not an indication of future results. Neither the Participants nor any of their affiliates shall be responsible or have any liability for any misinformation contained in any statement by any third party or in any SEC or other regulatory filing or third party report. Unless otherwise indicated, the figures presented in this presentation have not been calculated using generally accepted account principles ("GAAP") and have not been audited by independent accountants. Such figures may vary from GAAP accounting in material respects and there can be no assurance that the unrealized values reflected in this presentation will be realized. There is no assurance or guarantee with respect to the prices at which any securities of the Company will trade, and such securities may not trade at prices that may be implied herein. The estimates, projections, pro forma information and potential impact of the opportunities identified by the Fund herein are based on assumptions that the Fund believes to be reasonable as of the date of this presentation, but there can be no assurance or guarantee that actual results or performance of the Company will not differ, and such differences may be material. This presentation does not recommend the purchase or sale of any security. The Fund reserves the right to change any of its opinions expressed herein at any time as it deems appropriate. The Fund disclaims any obligation to update the data, information or opinions contained in this presentation.

Forward Looking Statements

This presentation contains forward-looking statements. All statements contained in this presentation that are not clearly historical in nature or that necessarily depend on future events are forward-looking, and the words “anticipate,” “believe,” “expect,” “potential,” “could,” “opportunity,” “estimate,” “plan,” and similar expressions are generally intended to identify forward-looking statements. The projected results and statements contained in this presentation that are not historical facts are based on current expectations, speak only as of the date of this presentation and involve risks, uncertainties and other factors that may cause actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such projected results and statements. Assumptions relating to the foregoing involve judgments with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond the control of Argyle. Although Argyle believes that the assumptions underlying the projected results or forward-looking statements are reasonable as of the date of this presentation, any of the assumptions could be inaccurate and therefore, there can be no assurance that the projected results or forward-looking statements included in this presentation will prove to be accurate and therefore actual results could differ materially from those set forth in, contemplated by, or underlying those forward-looking statements. In light of the significant uncertainties inherent in the projected results and forward-looking statements included in this presentation, the inclusion of such information should not be regarded as a representation as to future results or that the objectives and strategic initiatives expressed or implied by such projected results and forward-looking statements will be achieved. Except to the extent required by applicable law, Argyle will not undertake and specifically declines any obligation to disclose the results of any revisions that may be made to any projected results or forward-looking statements in this presentation to reflect events or circumstances after the date of such projected results or statements or to reflect the occurrence of anticipated or unanticipated events.

1

Not an Offer to Sell or a Solicitation of an Offer to Buy

Under no circumstances is this presentation intended to be, nor should it be construed as, an offer to sell or a solicitation of any offer to buy any security. Funds and investment vehicles managed by the Fund currently beneficially own shares of the Company. These funds and investment vehicles are in the business of trading—buying and selling—securities and intend to continue trading securities of the Company. You should assume such funds and investment vehicles will from time to time sell all or a portion of their holdings of the Company in open market transactions or otherwise, buy additional shares (in open market or privately negotiated transactions or otherwise), or trade in options, puts, calls, swaps or other derivative instruments relating to such shares. Consequently, the Fund's beneficial ownership of shares of, and/or economic interest in, the Company's common stock may vary over time depending on various factors, with or without regard to the Fund's views of the Company's business, prospects or valuation (including the market price of the Company's common stock), including without limitation, other investment opportunities available to the Fund, concentration of positions in the portfolios managed by the Fund, conditions in the securities markets and general economic and industry conditions. The Fund also reserves the right to change its intentions with respect to its investments in the Company and take any actions with respect to investments in the Company as it may deem appropriate, and disclaims any obligation to notify the market or any other party of anu such changes or actions. However, neither the Fund nor any other Participant or any of the respective affiliates has any intention, either alone or in concert with another person, to acquire or exercise control of the Company of any of its subsidiaries.

Concerning Intellectual Property

All registered or unregistered service marks, trademarks and trade names referred to in this presentation are the property of their respective owners, and the Fund's use herein does not imply an affiliation with, or endorsement by, the owners of these service marks, trademarks or trade names or the goods and services sold or offered by such owners.

2

Refreshing Broadwind, Inc.(NASDAQ: BWEN) Replacing three entrenched directors to bring fresh thinking and greater accountability WM Argyle Fund | May 2023

The Need For Shareholder-Driven ChangeTABLE OF 1 2 A Reactive, Defensive and Scared BoardCONTENTS 3 The Three Opposed & Entrenched Directors Poor Track Records 4 Broadwind’s Misleading Claims 5 Broadwind’s Lack of Strategy 6 Our Plan & Nominees

About WM Argyle Fund• Owns 207,200, approximately 1%, of the outstanding common shares of Broadwind• Single purpose investment fund specifically created to invest in Broadwind• Looking to ensure the long-term performance of the Company by reconstituting the Broadwind Board with new members• We are spending our own capital on this proxy campaign to reform the Board to unlock value for all shareholders• WM Argyle Fund is seeking minority representation on Broadwind's board

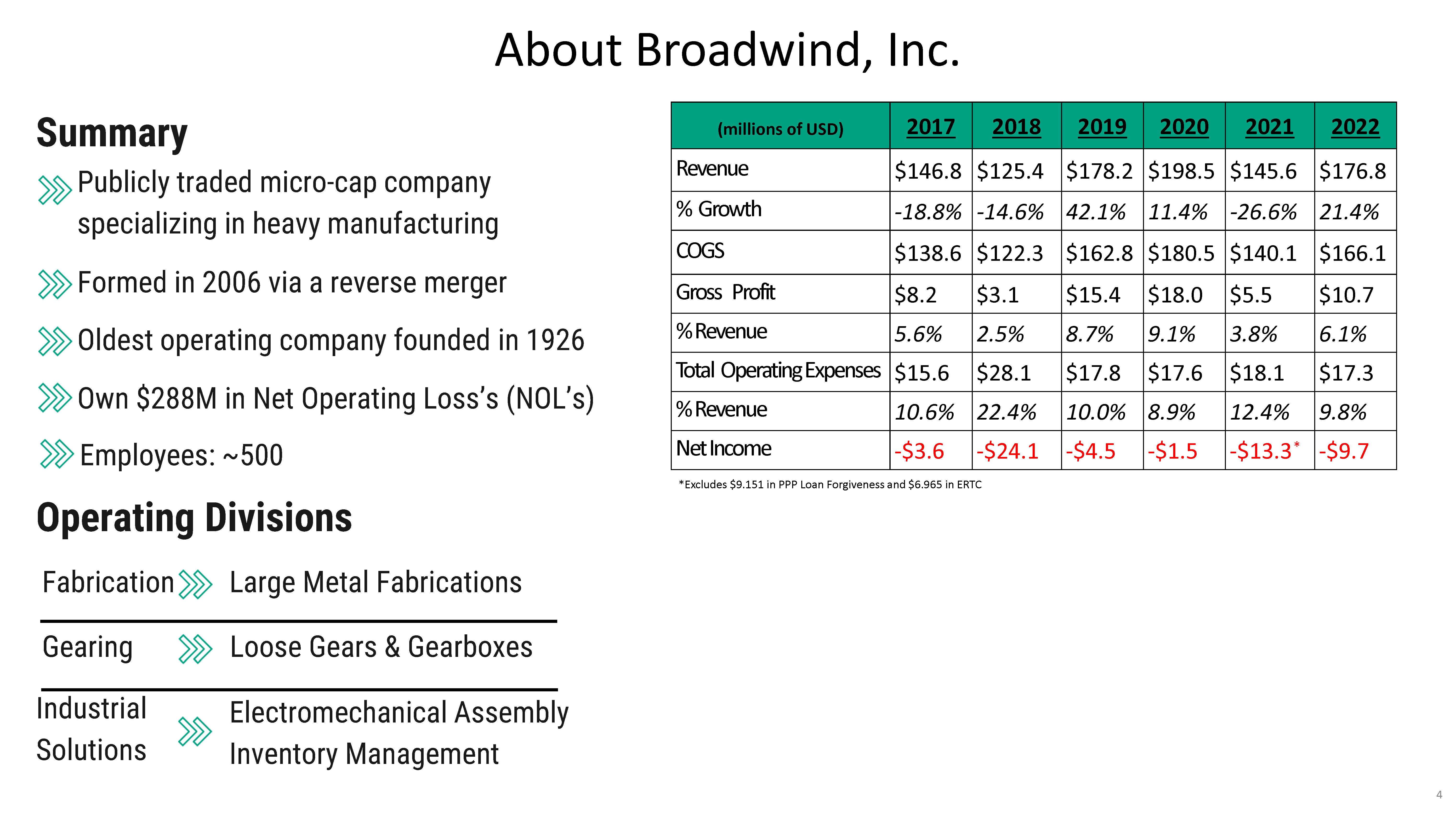

About Broadwind, Inc.SummaryPublicly traded micro-cap company specializing in heavy manufacturing Formed in 2006 via a reverse merger Oldest operating company founded in 1926 Own $288M in Net Operating Loss’s (NOL’s) Employees: ~500 (millions of USD) 2017 2018 2019 2020 2021 2022 Revenue $146.8 $125.4 $178.2 $198.5 $145.6 $176.8 % Growth -18.8% -14.6% 42.1% 11.4% -26.6% 21.4% COGS $138.6 $122.3 $162.8 $180.5 $140.1 $166.1 Gross Profit $8.2 $3.1 $15.4 $18.0 $5.5 $10.7 % Revenue 5.6% 2.5% 8.7% 9.1% 3.8% 6.1% Total Operating Expenses $15.6 $28.1 $17.8 $17.6 $18.1 $17.3 % Revenue 10.6% 22.4% 10.0% 8.9% 12.4% 9.8% Net Income -$3.6 -$24.1 -$4.5 -$1.5 *-$13.3 -$9.7*Excludes $9.151 in PPP Loan Forgiveness and $6.965 in ERTCOperating Divisions Fabrication Large Metal Fabrications Gearing Loose Gears & Gearboxes Industrial Electromechanical Assembly Solutions Inventory Management

1. The Need for Shareholder-Driven Change

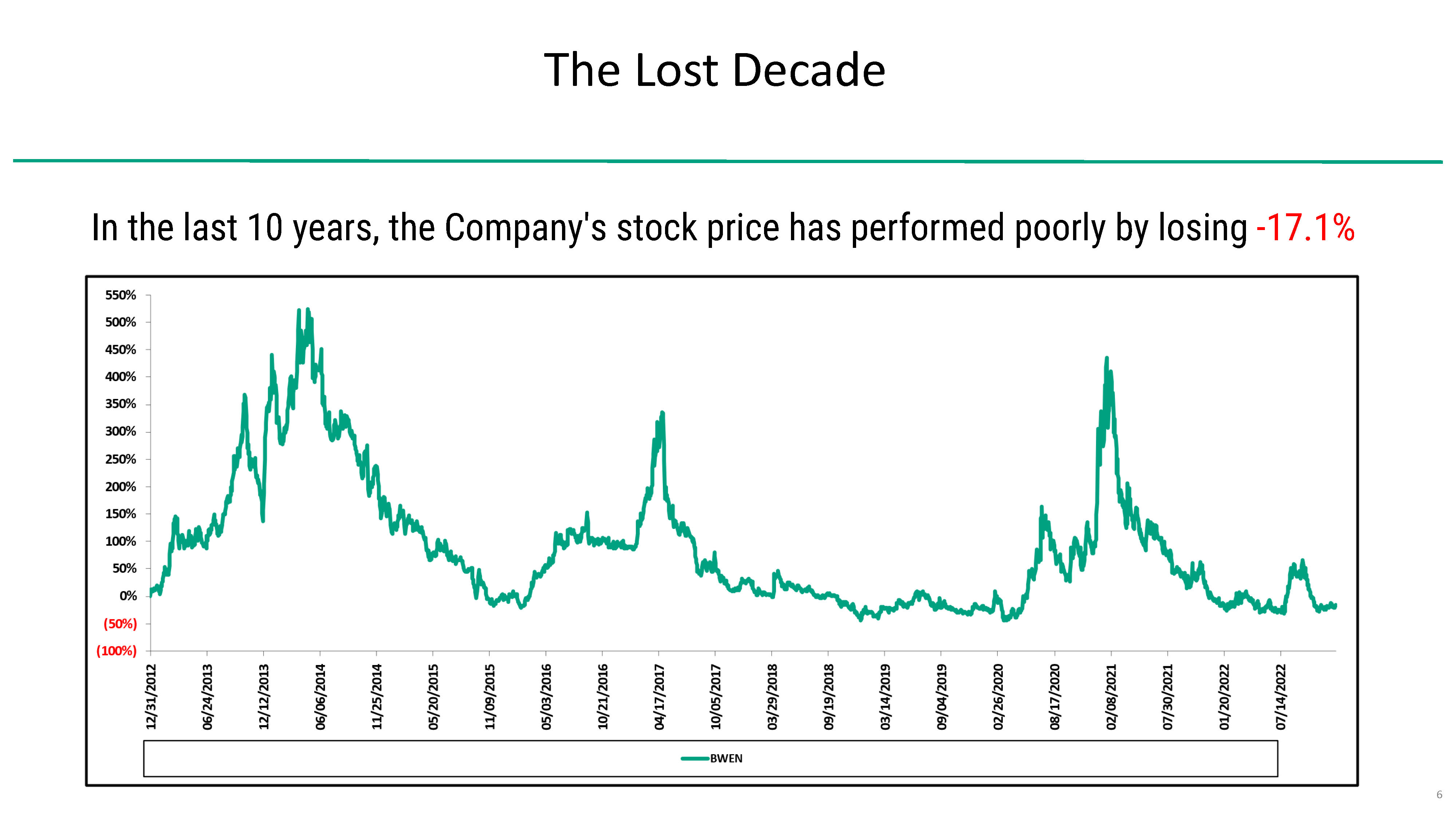

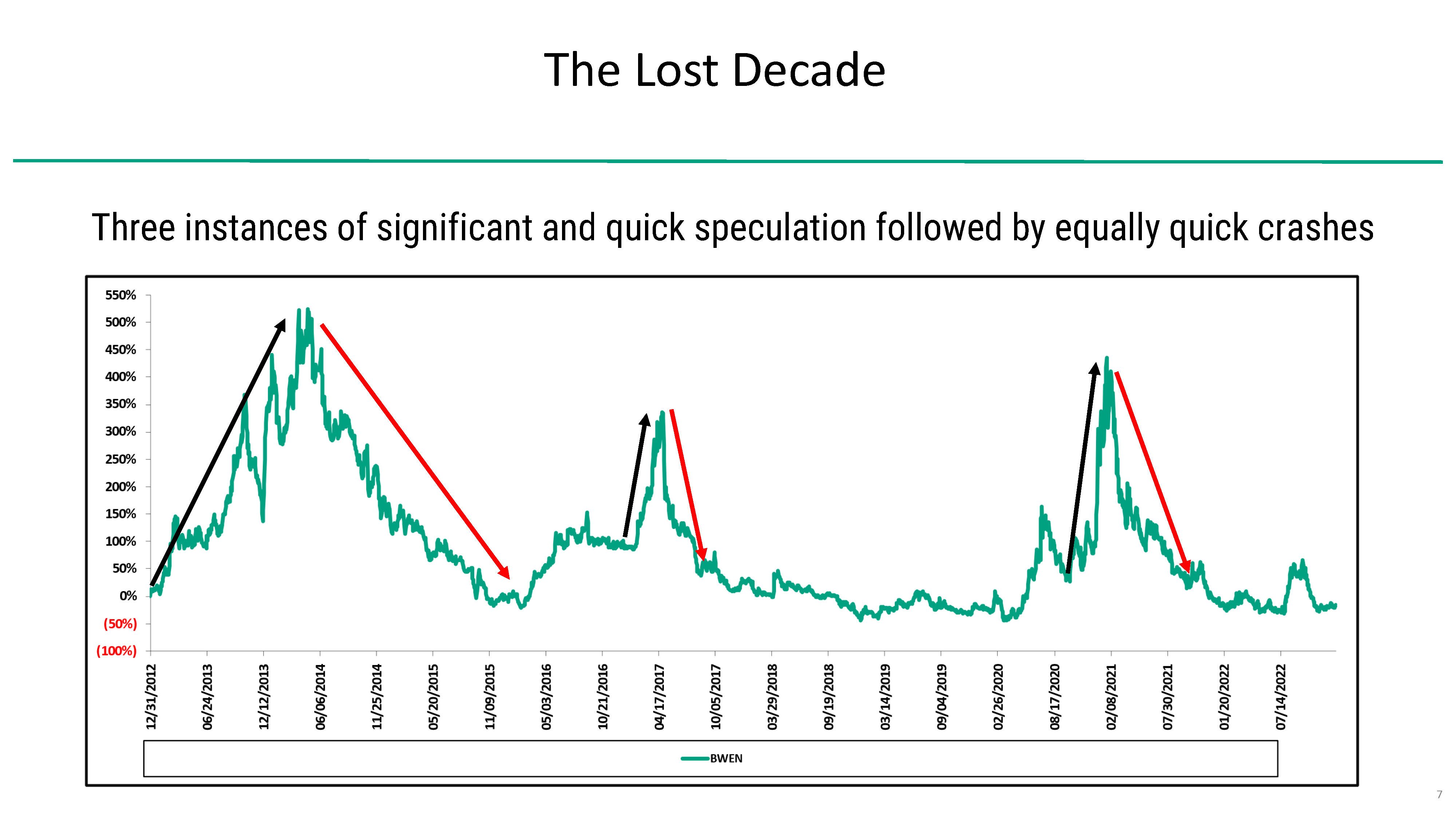

The Lost DecadeIn the last 10 years, the Company's stock price has performed poorly by losing -17.1%

The Lost DecadeThree instances of significant and quick speculation followed by equally quick crashes

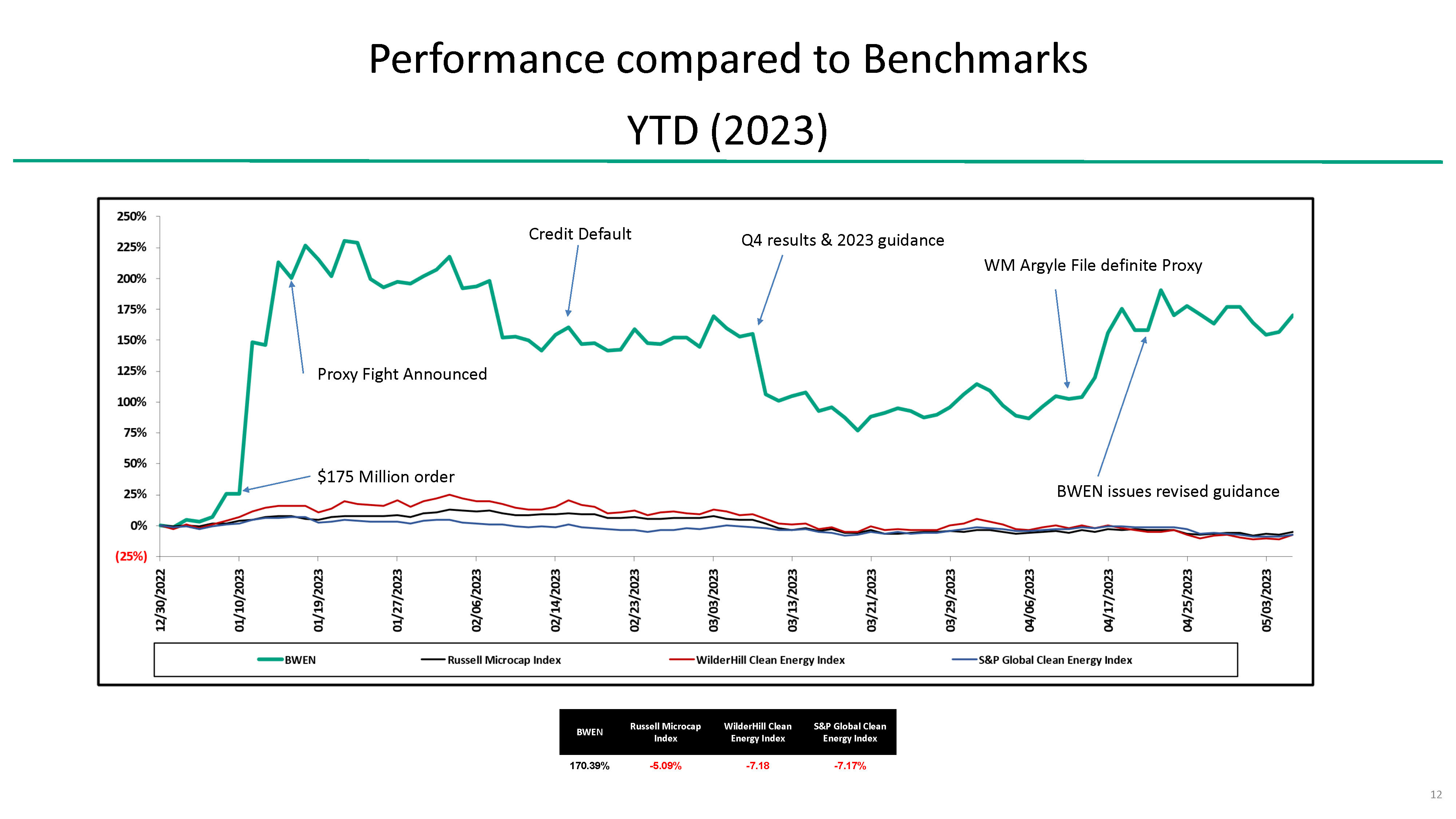

Performance compared to Benchmarks-17.13% 108.54% 89.61% 178.43% Performance compared Benchmarks

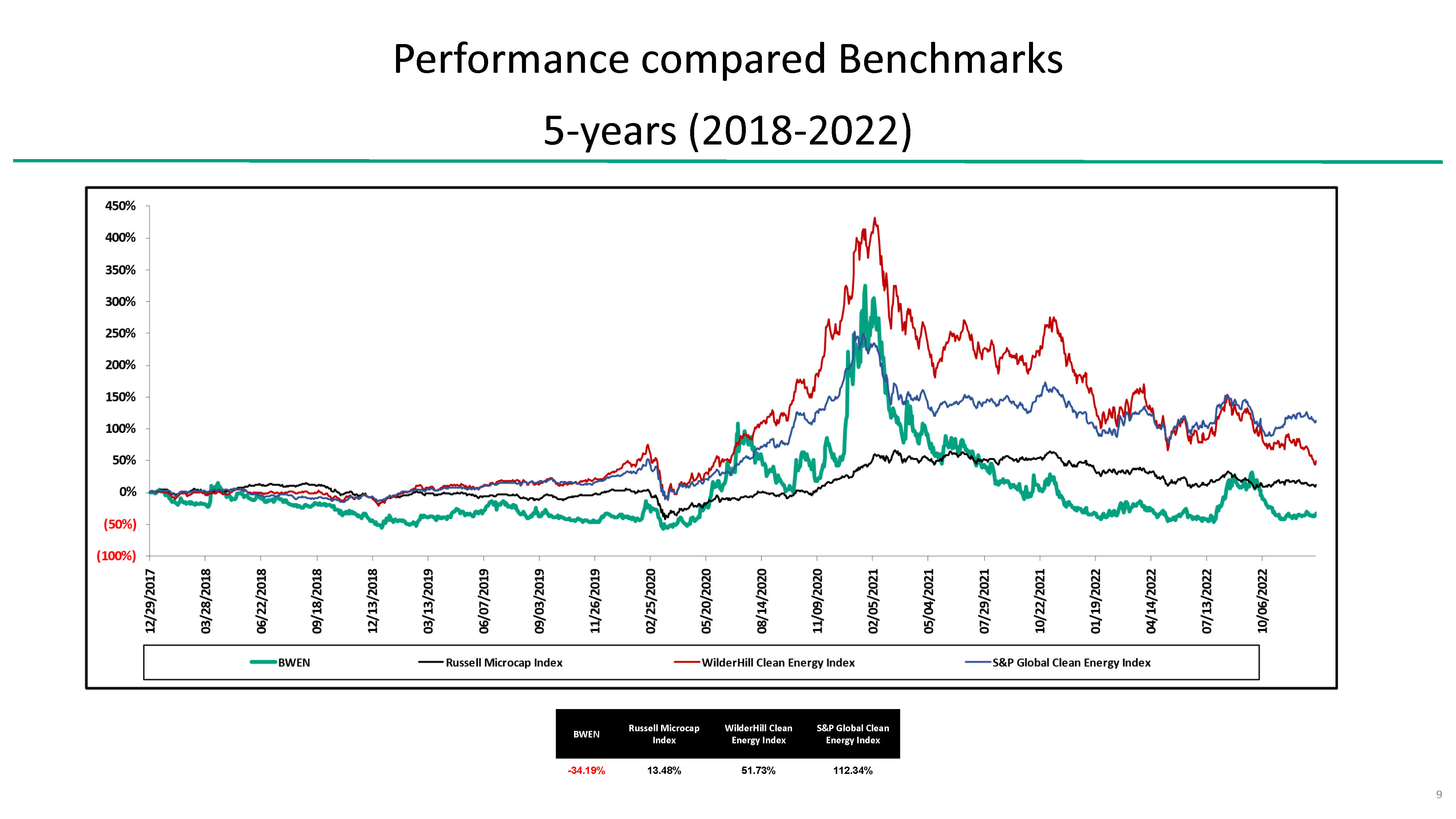

Performance compared Benchmarks-34.19% 13.48% 51.73% 112.34%

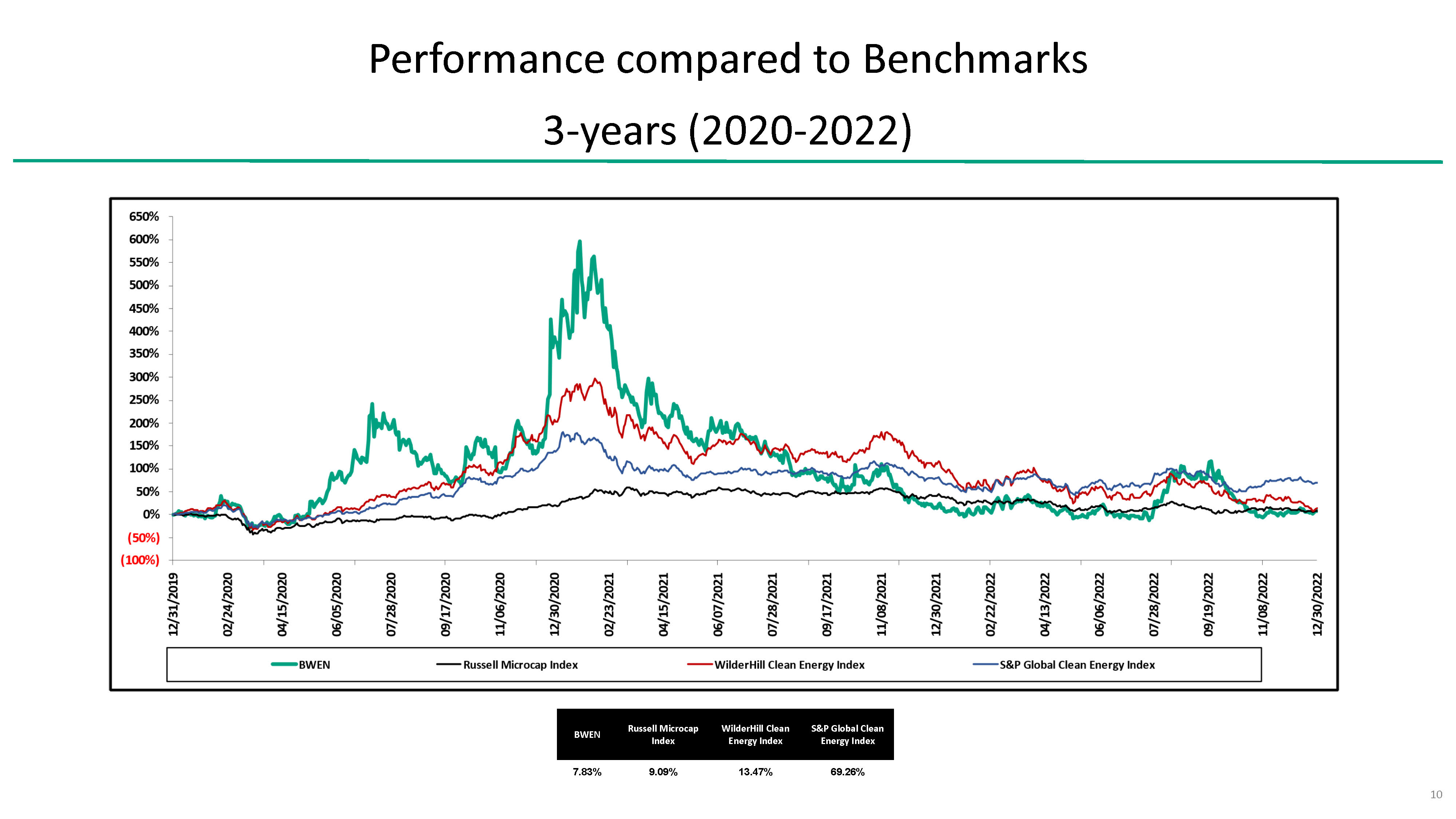

Performance compared to Benchmarks7.83% 9.09% 13.47% 69.26%

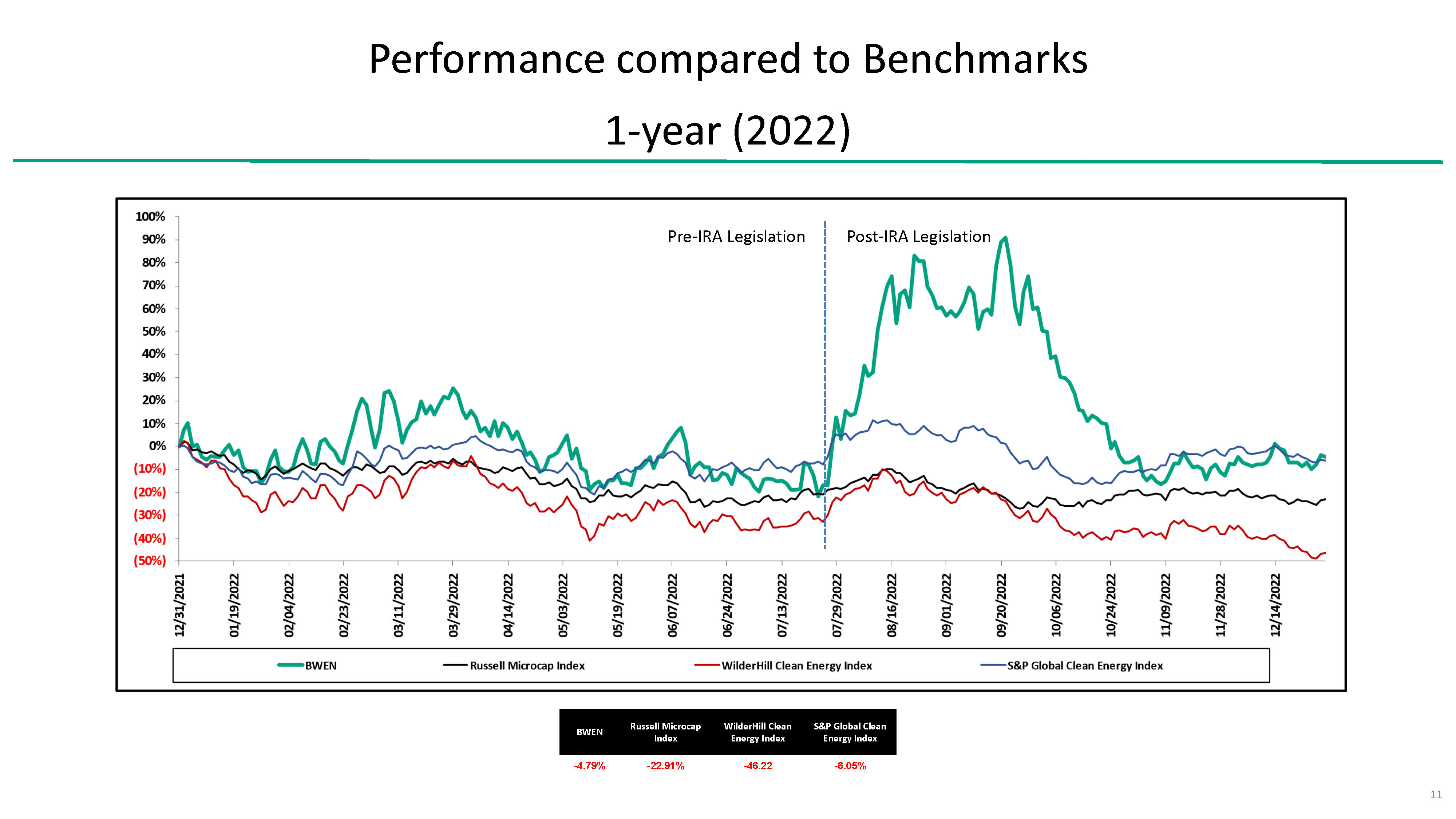

Performance compared to Benchmarks-4.79% -22.91% -46.22 -6.05%

Performance compared to Benchmarks

The Board shouldn’t be rewarded for Inflation Reduction Act (IRA)IRA benefits • Extension of the Production Tax Credit (PTC) for developers of wind power • Manufacturer tax credit for manufacturers of clean technology The stock price is independent of benchmarks and the market• Low correlation between benchmarks and Broadwind stock price movements• Pure market speculation on Broadwind stock• Trading volume on the Jan 11, 2023 was +300% of float and +800 times the 30-day average volume This campaign started well before the IRA was public• The Company still needs to manufacture profitably and for the most part it never has• Tax credits will be sold if the Company doesn’t become profitable The execution risk presented by the Board is too high

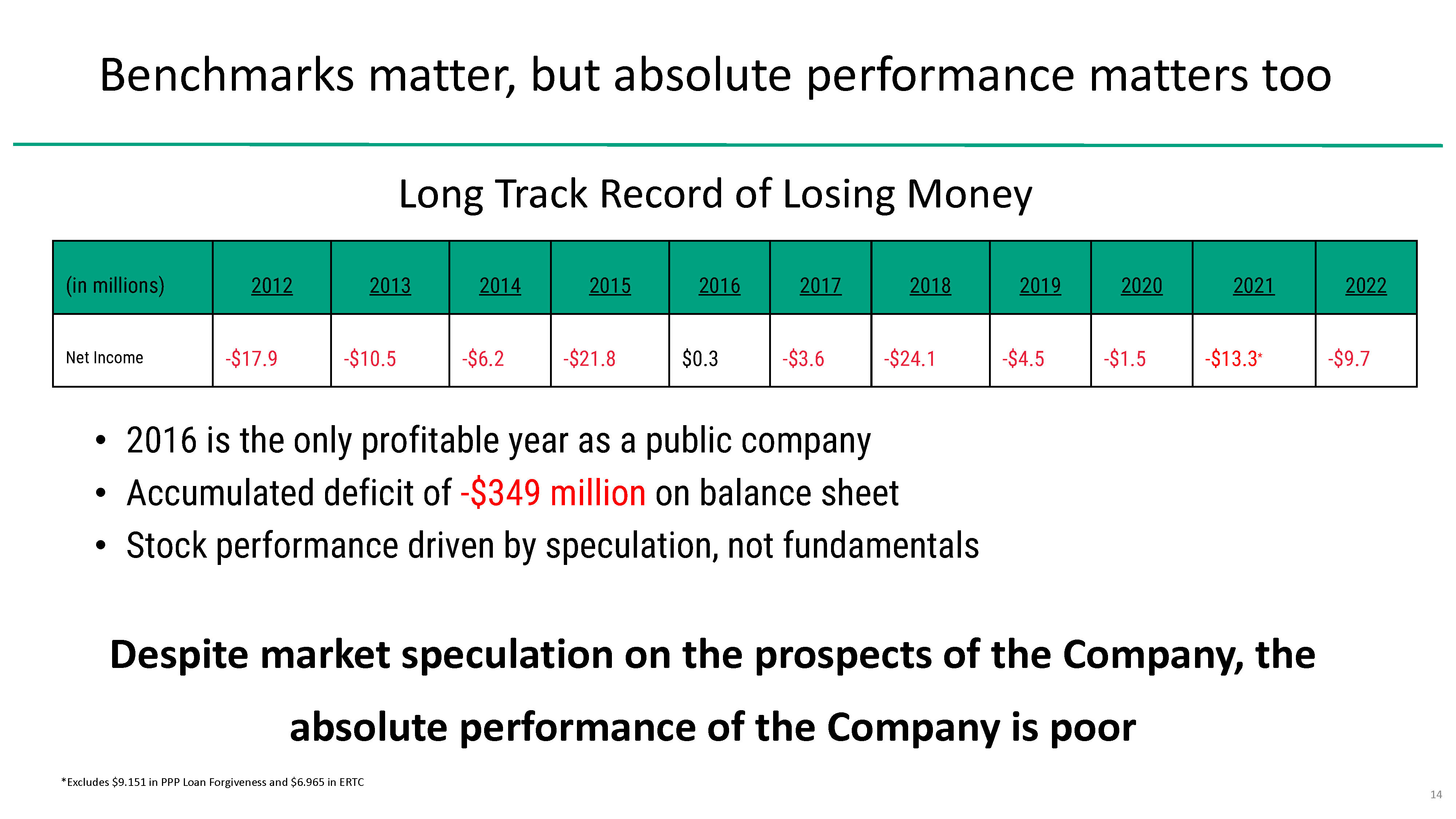

Benchmarks matter, but absolute performance matters tooLong Track Record of Losing Money (in millions) 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 Net Income -$17.9 -$10.5 -$6.2 -$21.8 $0.3 -$3.6 -$24.1 -$4.5 -$1.5 -$13.3* -$9.7• 2016 is the only profitable year as a public company• Accumulated deficit of -$349 million on balance sheet• Stock performance driven by speculation, not fundamentalsDespite market speculation on the prospects of the Company, the absolute performance of the Company is poor *Excludes $9.151 in PPP Loan Forgiveness and $6.965 in ERTC

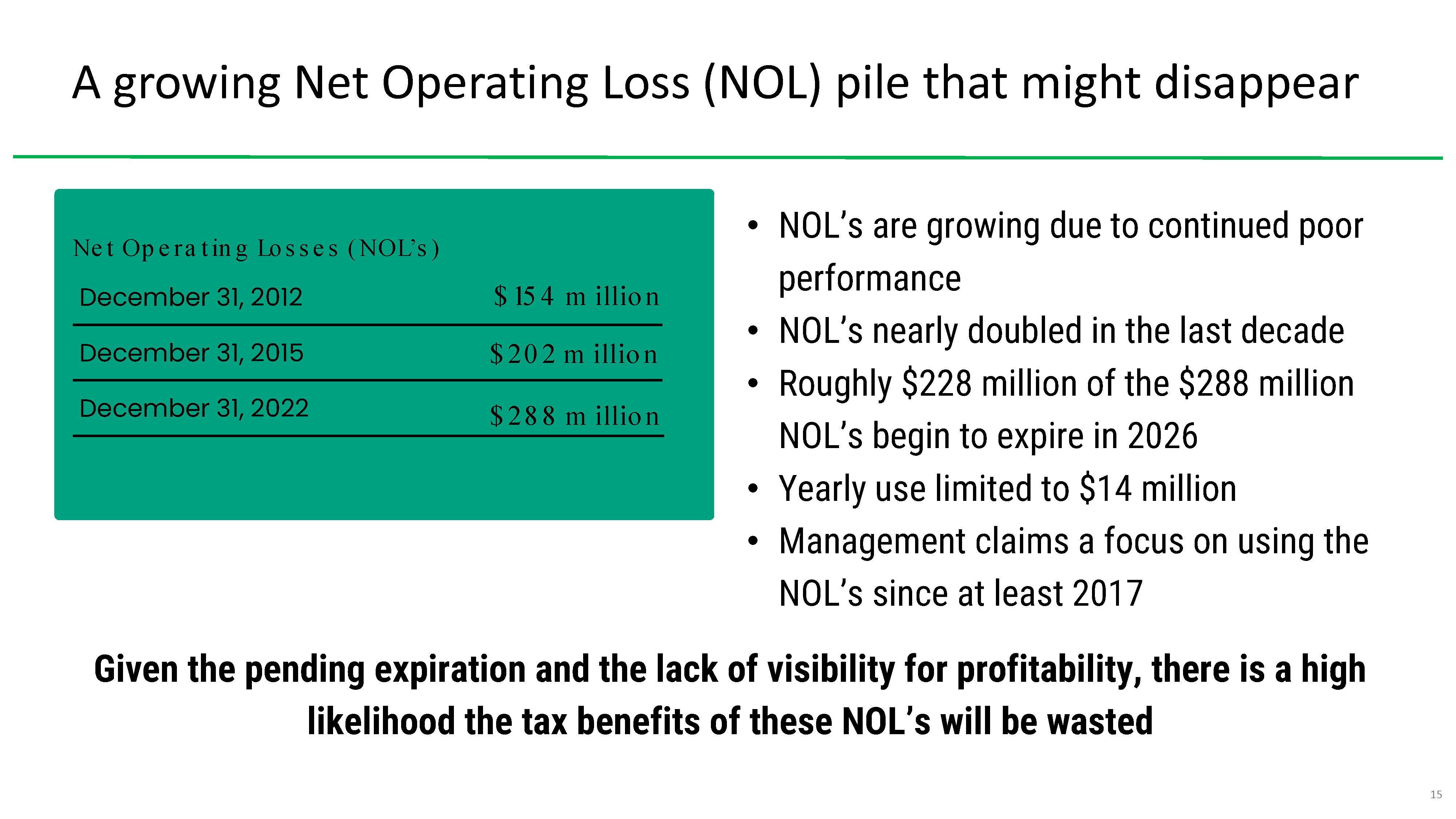

A growing Net Operating Loss (NOL) pile that might disappear• NOL’s are growing due to continued poor performance• NOL’s nearly doubled in the last decade• Roughly $228 million of the $288 million NOL’s begin to expire in 2026• Yearly use limited to $14 million• Management claims a focus on using the NOL’s since at least 2017Given the pending expiration and the lack of visibility for profitability, there is a high likelihood the tax benefits of these NOL’s will be wasted

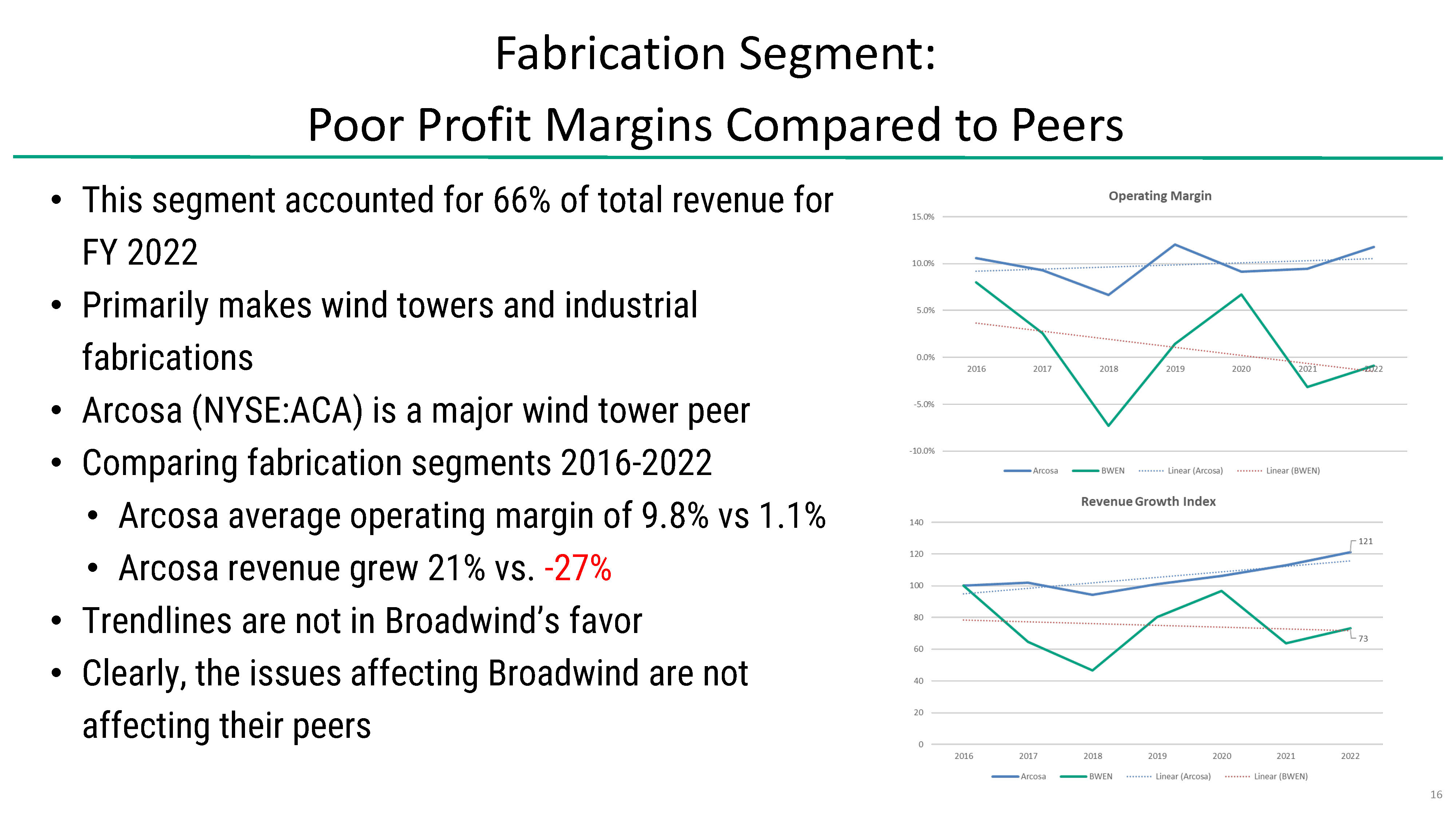

Fabrication Segment: Poor Profit Margins Compared to Peers• This segment accounted for 66% of total revenue for FY 2022• Primarily makes wind towers and industrial fabrications• Arcosa (NYSE:ACA) is a major wind tower peer• Comparing fabrication segments 2016-2022• Arcosa average operating margin of 9.8% vs 1.1%• Arcosa revenue grew 21% vs. -27%• Trendlines are not in Broadwind’s favor• Clearly, the issues affecting Broadwind are not affecting their peers

• This segment accounted for 24% of total revenue for FY 2022• Produces gears and gearboxes for industrial and wind power applications • Between 2016-2022• Revenue between $20 and $43 million.• Materially profitable only once• Sales increased 49% in FY 2022, still wasn’t materially profitable

• This segment accounted for 10% of total revenue for FY 2022• Segment manages supply chain, inventory and kitting/assembly for primarily natural gas turbine market• Segment was created through the 2017 Red Wolf acquisition and by organically investing into natural gas compression products• Goal was to grow the business and to diversify customers• Red Wolf was impaired after 5 quarters, due to impact of one customer• CNG business was exited after a few quarters, after large losses• The business is basically a labor arbitrage businessGearing Segment: Stagnant and Losing Money$, mm 2016 2017 2018 2019 2020 2021 2022 Revenue $20.7 $26 $38.4 $34.9 $25.1 $28.6 $42.6 Operating Income -$3.2 -$2.6 $0.05 $3.2 -$3.9 -$2.6 $0.04Industrial Solutions: Strategy & Execution FailureSince its creation, not one single stated goal has been achieved by the Industrial Solutions segment

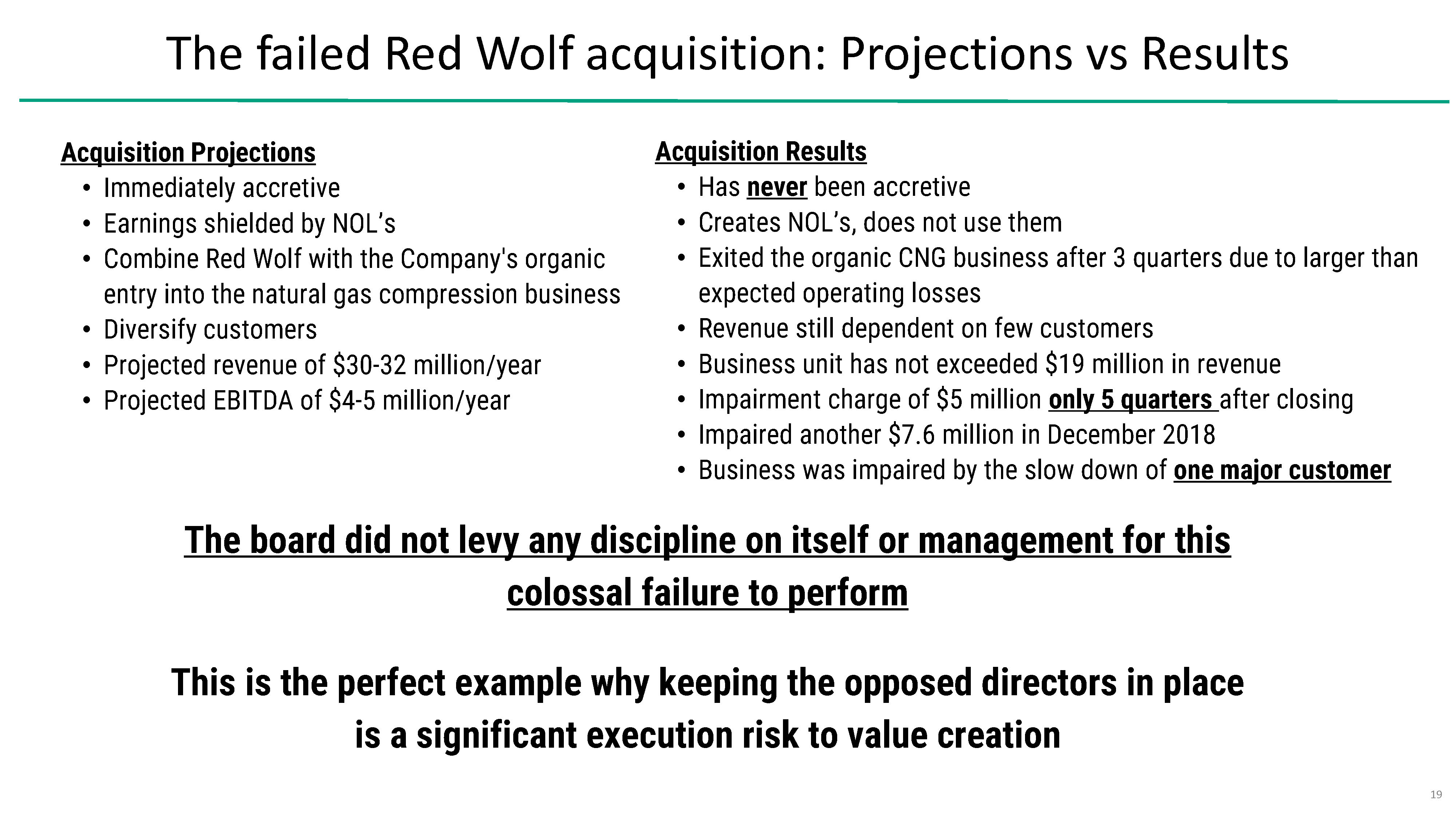

The failed Red Wolf acquisition: Projections vs ResultsAcquisition Projections Acquisition Results • Immediately accretive • Has never been accretive • Earnings shielded by NOL’s • Creates NOL’s, does not use them • Combine Red Wolf with the Company's organic • Exited the organic CNG business after 3 quarters due to larger than entry into the natural gas compression business expected operating losses • Diversify customers • Revenue still dependent on few customers • Projected revenue of $30-32 million/year • Business unit has not exceeded $19 million in revenue • Projected EBITDA of $4-5 million/year • Impairment charge of $5 million only 5 quarters after closing • Impaired another $7.6 million in December 2018 • Business was impaired by the slow down of one major customerThe board did not levy any discipline on itself or management for this colossal failure to perform This is the perfect example why keeping the opposed directors in place is a significant execution risk to value creation

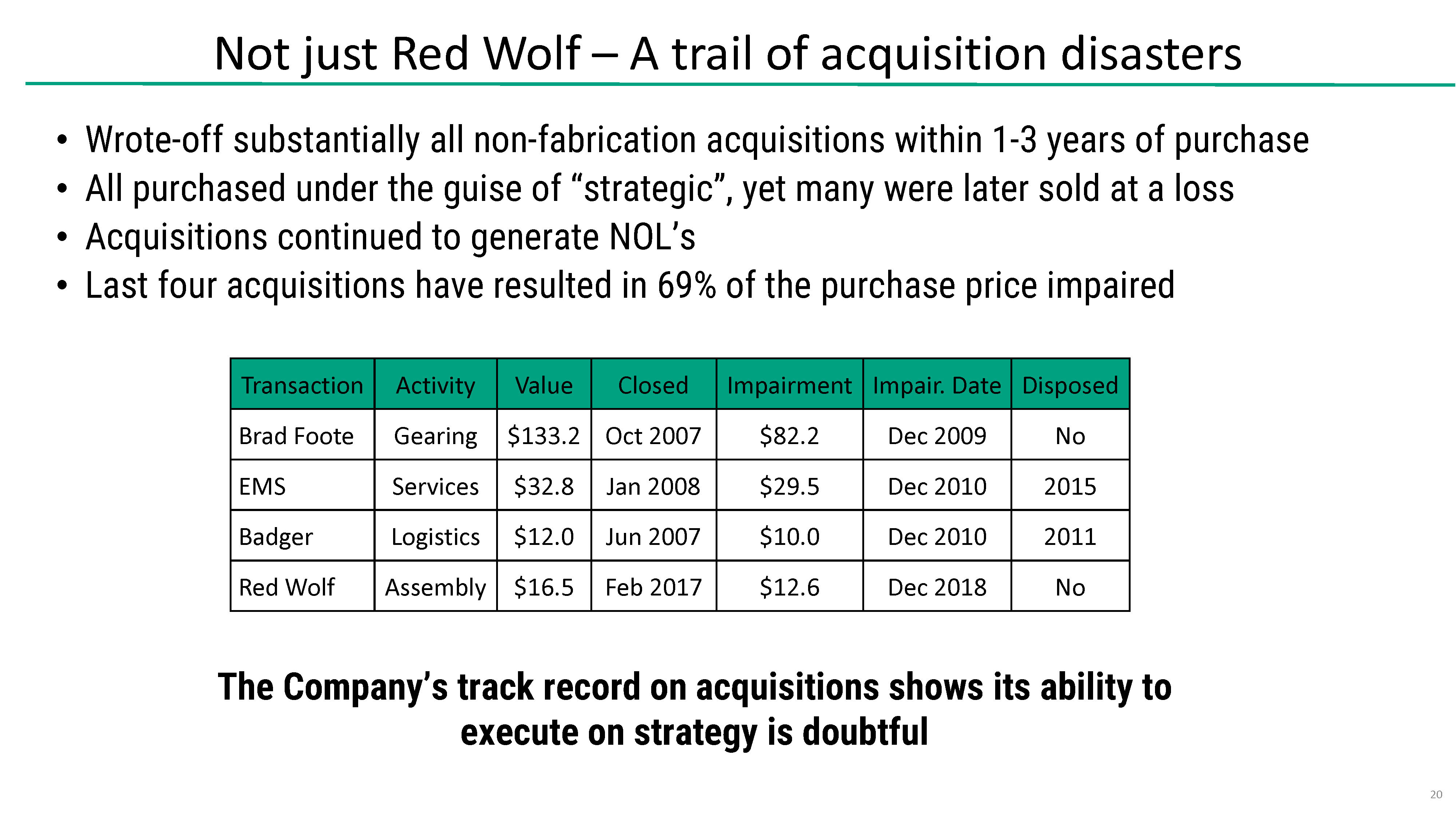

Not just Red Wolf – A trail of acquisition disasters • Wrote-off substantially all non-fabrication acquisitions within 1-3 years of purchase• All purchased under the guise of “strategic”, yet many were later sold at a loss• Acquisitions continued to generate NOL’s• Last four acquisitions have resulted in 69% of the purchase price impairedTransaction Activity Value Closed Impairment Impair. Date Disposed Brad Foote Gearing $133.2 Oct 2007 $82.2 Dec 2009 No EMS Services $32.8 Jan 2008 $29.5 Dec 2010 2015 Badger Logistics $12.0 Jun 2007 $10.0 Dec 2010 2011 Red Wolf Assembly $16.5 Feb 2017 $12.6 Dec 2018 NoThe Company’s track record on acquisitions shows its ability to execute on strategy is doubtful

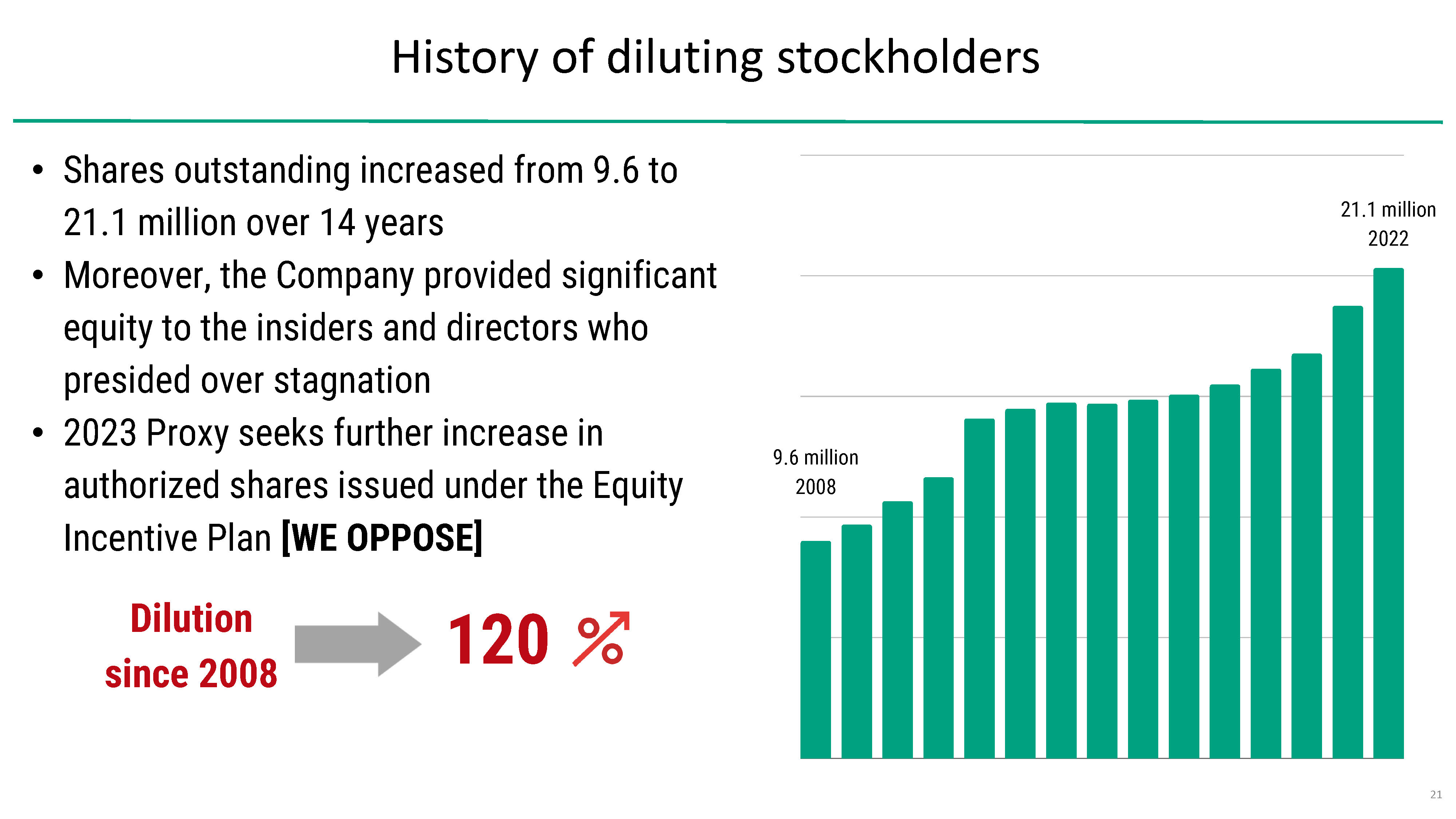

History of diluting stockholders• Shares outstanding increased from 9.6 to 21.1million 21.1 million over 14 years 2022 • Moreover, the Company provided significant equity to the insiders and directors who presided over stagnation• 2023 Proxy seeks further increase in9.6 million authorized shares issued under the Equity 2008 Incentive Plan [WE OPPOSE]

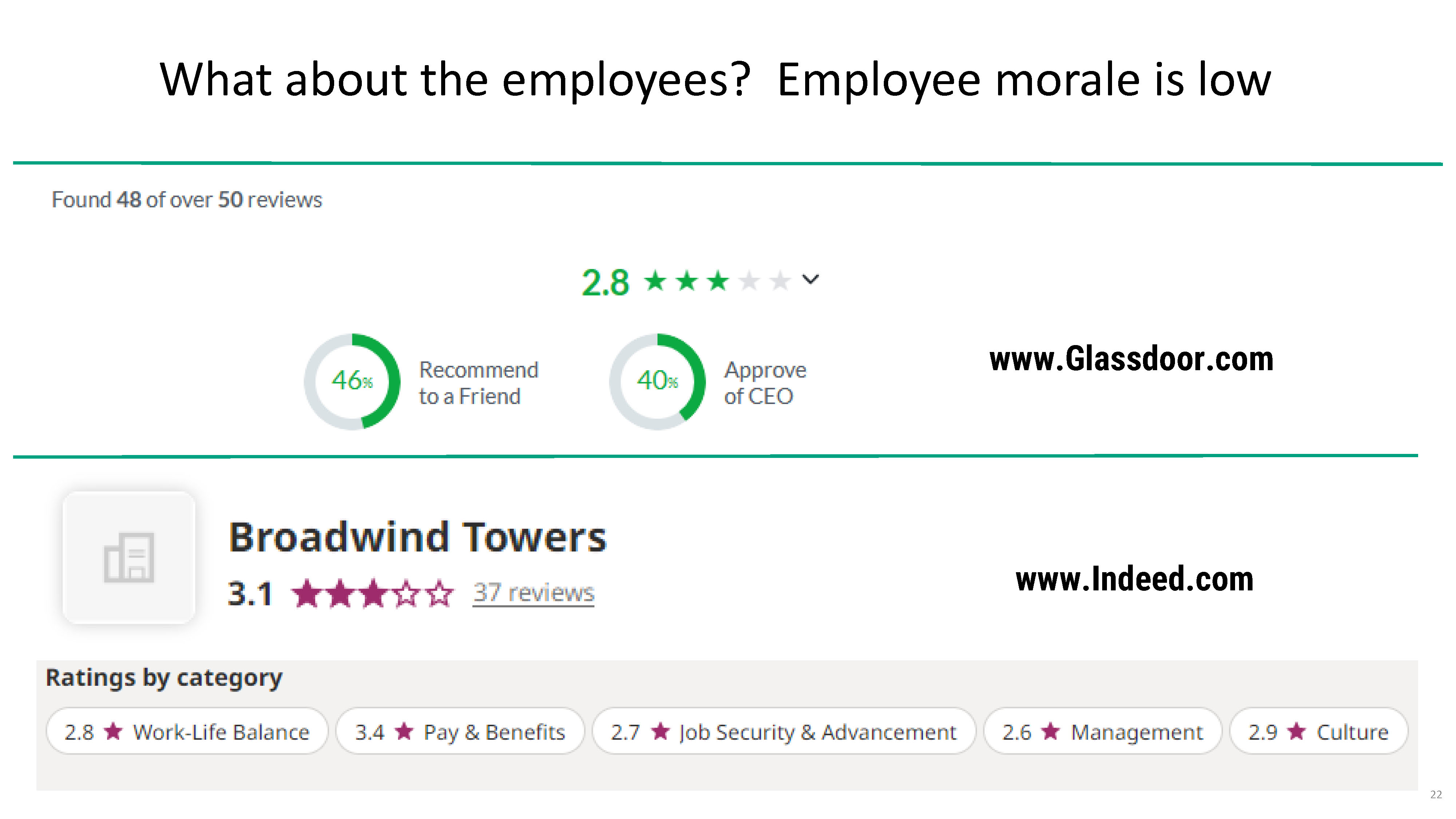

What about the employees? Employee morale is low www.Glassdoor.com www.Indeed.com

Failure to appoint a full-time CFO for over 11 months• On September 2, 2021, Jason Bonfigt delivered his resignation as CFO, effective October 1, 2021• On October 1, 2021, the Company appointed its CEO, Eric Blashford, as interim CFO• After 11 months, on August 10, 2022, the Company appointed Thomas Ciccone as CFO• During this period,• David Reiland served as chairman of the Audit Committee• Cary Wood served as chairman of the Board.• Why did it take more than 11 months to hire a full-time CFO?What purpose do the CFO and CEO serve if they can be the same person for 11 months?

Failure to communicate the incapacitation of the then Chairman• On March 1, 2020, Ms. Kushner was appointed Chairman of the Board• Tragically, Ms. Kushner was involved in a serious accident on November 7, 2021, which rendered her incapacitated and unable to serve in her role• However, the only notice found was March 4, 2022 , when the preliminary proxy for the annual meeting was filed• This is a gap of almost 4 months• Ms. Kushner was the company’s former CFO, CEO and current chair of the BoardWe believe the Board failed to properly notify shareholders about this materially important situation

Violated credit agreement after 5 months• The Company entered into a new credit facility with a new lender on August 4, 2022• On February 14, 2023 the Company disclosed they defaulted on the credit agreement due to failure to meet a December 31, 2022 TTM EBITDA covenant• This is not even 5 months after signing the credit agreement• The lender agreed to a waiver and reduced future EBITDA covenants• Any impact on the credit facility could imperil the entire Company• This is a serious failure by management and the BoardThis shows management failed to execute on its plan and the Board failed to provide effective oversight

Execution risk is too great with the current Board• The stock has underperformed for years• The financial performance of the Company has been stagnant for a decade• The Company has essentially been exclusively unprofitable• No urgency to become profitable• No urgency to benefit from the NOL’s• No successful acquisitions• Significantly diluted shareholders• Unhappy employees• Failure to appoint key employees in timely fashion• Failure to notify shareholders of Chairman’s incapacitation in timely fashion• Violated covenants on the credit agreement We believe the track record of the Board is indefensible and that is why it is time for a refresh of the Board with our nominees

2. A Reactive,Defensive,and Scared Board

The Board is reactive, defensive, and scared• When we reached out to the Board in July 2022, we wanted to discuss several issues• Poor performance• Long-tenure of several directors• The lack of diversity• Vacant Board seats from previous directors leaving• After multiple requests to meet with the Board, they notified us in October 2022 they would not engage in discussions with us• Approximately two weeks later, the Company appointed Sachin Shivaram as a director• A few weeks after we launched our campaign in January 2023, the company added Jeanette Press to its Board

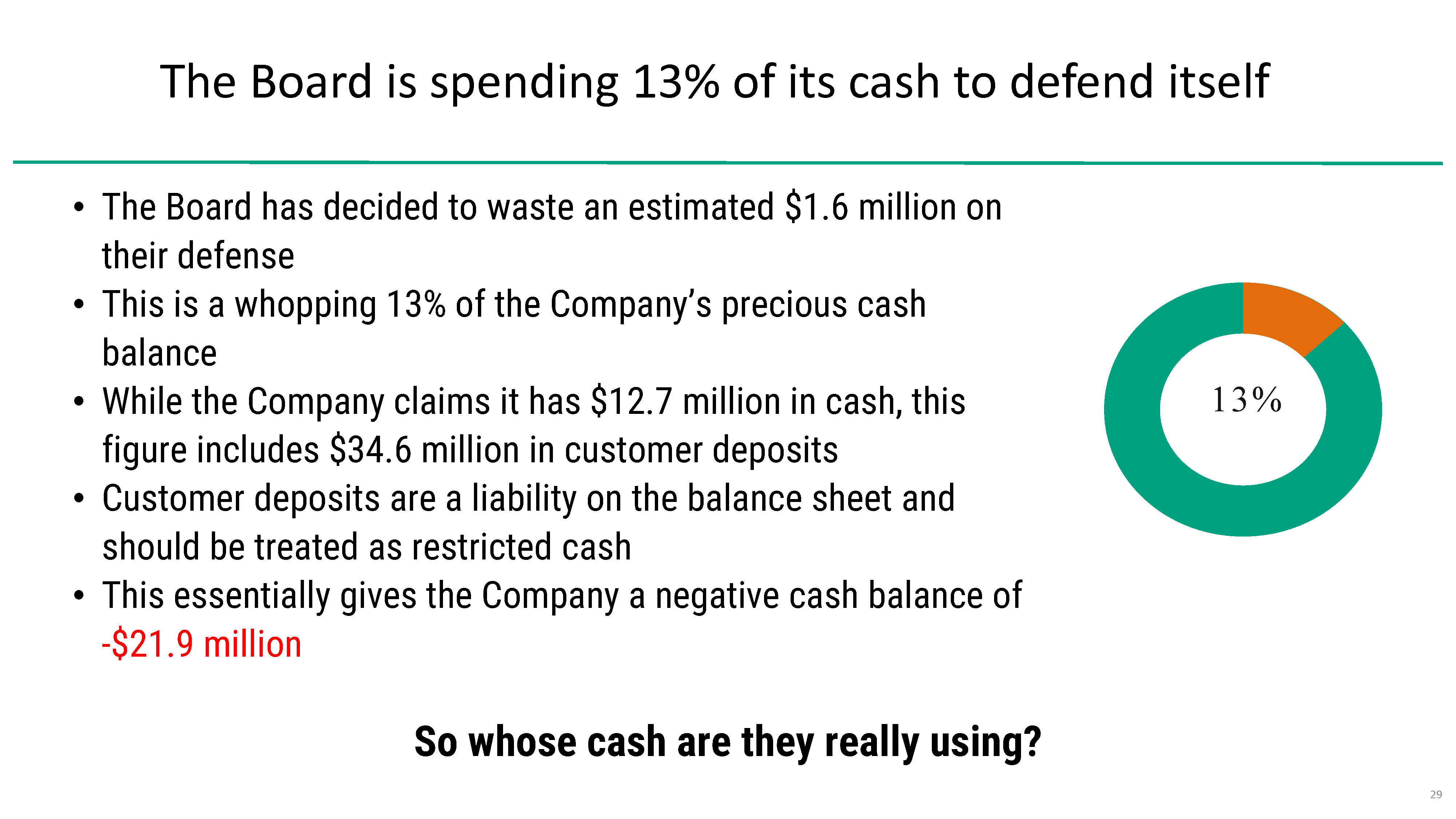

• The Board has decided to waste an estimated $1.6 million on their defense• This is a whopping 13% of the Company’s precious cash balance• While the Company claims it has $12.7 million in cash, this figure includes $34.6 million in customer deposits• Customer deposits are a liability on the balance sheet and should be treated as restricted cash• This essentially gives the Company a negative cash balance ofThe Board is spending 13% of its cash to defend itself-$21.9 millionSo whose cash are they really using?

The Board is scared, and its actions prove it• They have hired some of the best advisors money can buy to defend them• They make personal attacks on our nominees’ character and careers• Because they can’t defend their own track record of poor performance• They think only C-suite officers contribute to the success of a company• They have insulted “mid-level” employees as unimportant• They insist we aren’t qualified because we have not served on public boards• Somehow, that wasn’t a requirement for the two directors they just appointed• They imply we are only after “lucrative” Board fees• We would like to see Board compensation reduced until the Company is profitable Clearly, they think they are entitled to Board positions despite their performance

3. The Three Opposed & Entrenched Directors Poor Track Records

REMOVE THREE ENTRENCHED DIRECTORS Until these three directors are removed, we believe the culture of the Company’s boardroom will not meaningfully change.Cary B. Wood • Director since May 2016• Chairman since April 2022David P. Reiland • Director since April 2008 • Chairman, 2010-2020 Thomas A. Wagner • Director since May 2011

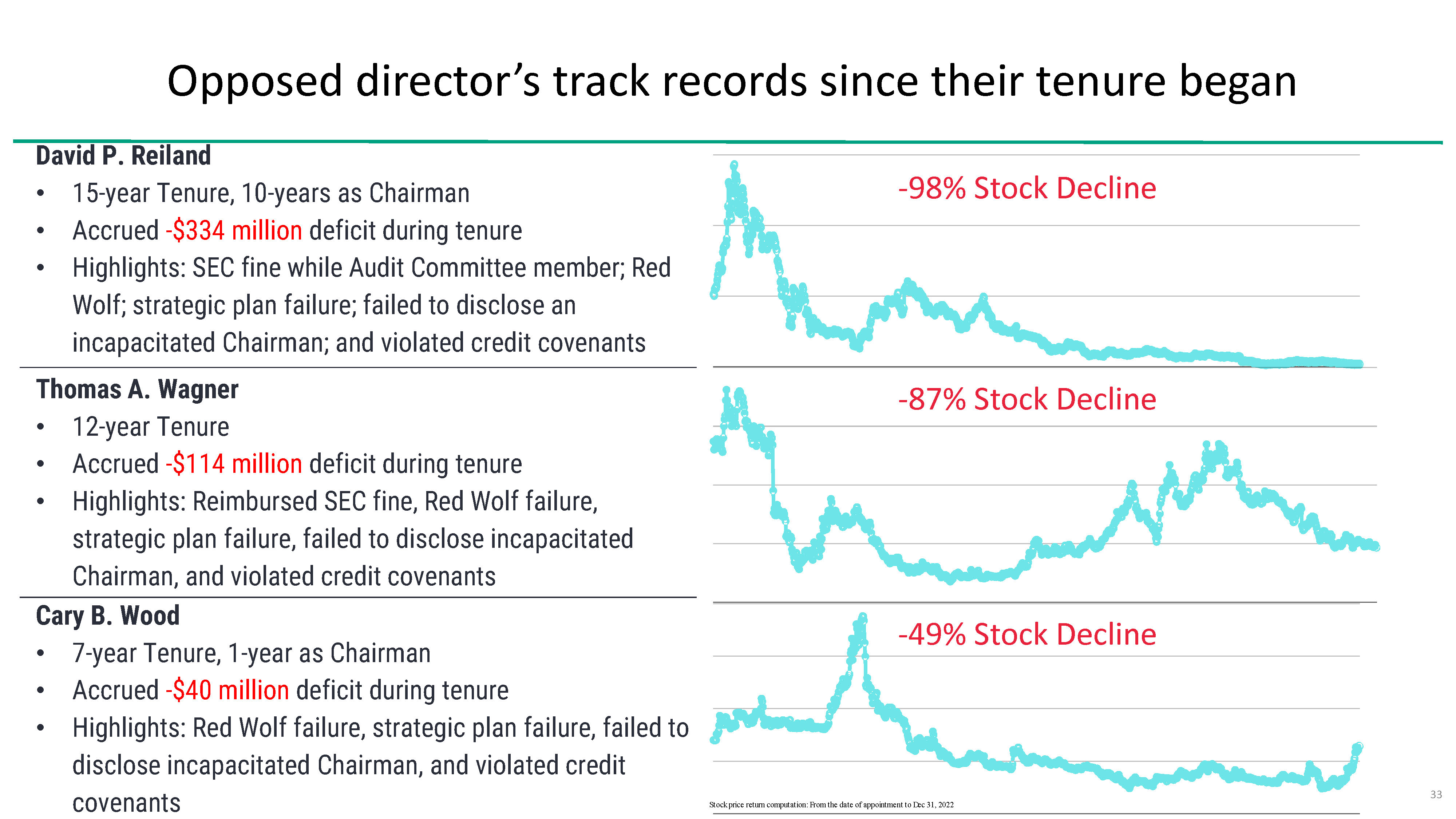

Opposed director’s track records since their tenure began David P. Reiland • 15-year Tenure, 10-years as Chairman• Accrued -$334 million deficit during tenure• Highlights: SEC fine while Audit Committee member; Red Wolf; strategic plan failure; failed to disclose an incapacitated Chairman; and violated credit covenantsThomas A. Wagner • 12-year Tenure • Accrued -$114 million deficit during tenure• Highlights: Reimbursed SEC fine, Red Wolf failure, strategic plan failure, failed to disclose incapacitated Chairman, and violated credit covenantsCary B. Wood • 7-year Tenure, 1-year as Chairman• Accrued -$40 million deficit during tenure• Highlights: Red Wolf failure, strategic plan failure, failed to disclose incapacitated Chairman, and violated credit covenants-98% Stock Decline -87% Stock Decline -49% Stock Decline Stock price return computation: From the date of appointment to Dec 31, 2022

Mr. Wood was pushed out as CEO by angry shareholders• Mr. Wood served as CEO and director of Sparton Corporation from November 2008 until February 2016• After activist shareholders complained about poor performance and failure to reach goals set out in a strategic plan, the Sparton Board terminated Mr. Wood as CEO on February 5, 2016Sparton CEO departs after activist shareholder complaints On a Sparton earnings call last week, CEO Cary Wood got “…you laid out last year a 2020 vision. You’ve had a 2015 vision that doesn’t appear that you’re going to hit until an earful from shareholders of the defense supplier and 2017. And you continue to talk about 2020 vision. How medical industry manufacturer. realistic is it that you can achieve anywhere close to Source: www.chicagobusiness.com those numbers by 2020? Or is that 2020 vision going to become 2022?”Source: SEC Filings

Mr. Wagner led product development of a product that failed• Mr. Wagner was the Chief Product Officer at Ogin, Inc. from July 2012 until October 2015• He led the product development and deployment of a shrouded wind turbine• Ogin raised $150 million in capital• The company shuttered after the product proved to be commercially unviable“But one of the things that is different with Ogin is the sheer scale of the money wasted on this ven• Windmill supplied by Ogin on Deer Island is no longer operational• It hadn’t been producing electricity since February 2015• Its energy production was significantly less than traditional products“Ogin Inc. is the kind of startup story that makes investors regret their foray into the world of clean energy, raising $150 million before running into manufacturing problems and shutting down earlier this year.” www.bizjournals.com “While the company made all kinds of revolutionary claims about its technology, when it came to actual proof, they were pretty light on what they would actually publish in the open literature,” -The Boston Globeture and the names associated with it.” -Paul Gipe, renewable energy analyst Source: bostonglobe.com/business/2017/05/05/deer-island-odd-looking-turbine-testament-failure/GJAe7yEYz1or8QGO07M95O/story.html

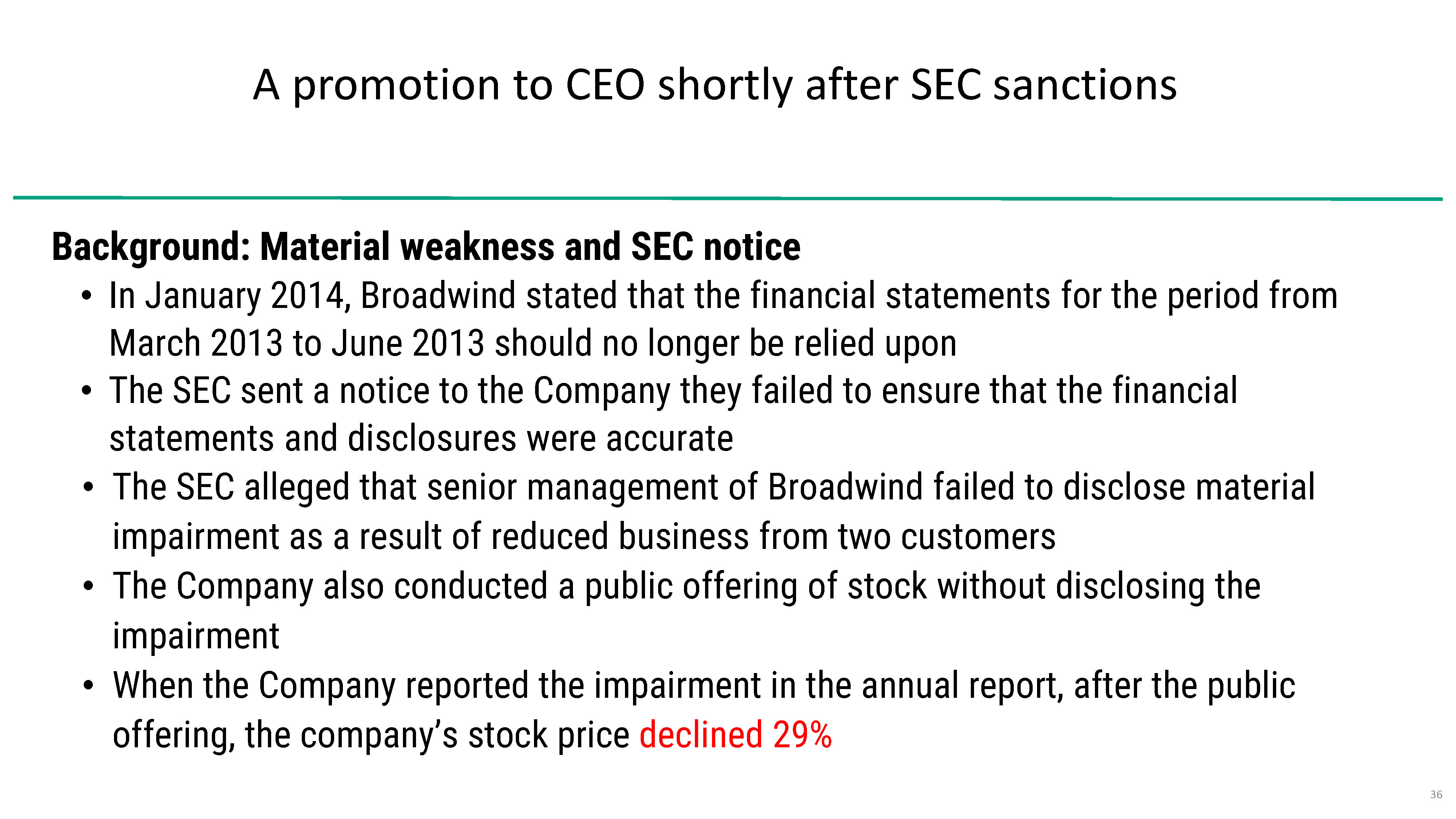

A promotion to CEO shortly after SEC sanctionsBackground: Material weakness and SEC notice • In January 2014, Broadwind stated that the financial statements for the period from March 2013 to June 2013 should no longer be relied upon• The SEC sent a notice to the Company they failed to ensure that the financial statements and disclosures were accurate• The SEC alleged that senior management of Broadwind failed to disclose material impairment as a result of reduced business from two customers• The Company also conducted a public offering of stock without disclosing the impairment• When the Company reported the impairment in the annual report, after the public offering, the company’s stock price declined 29%

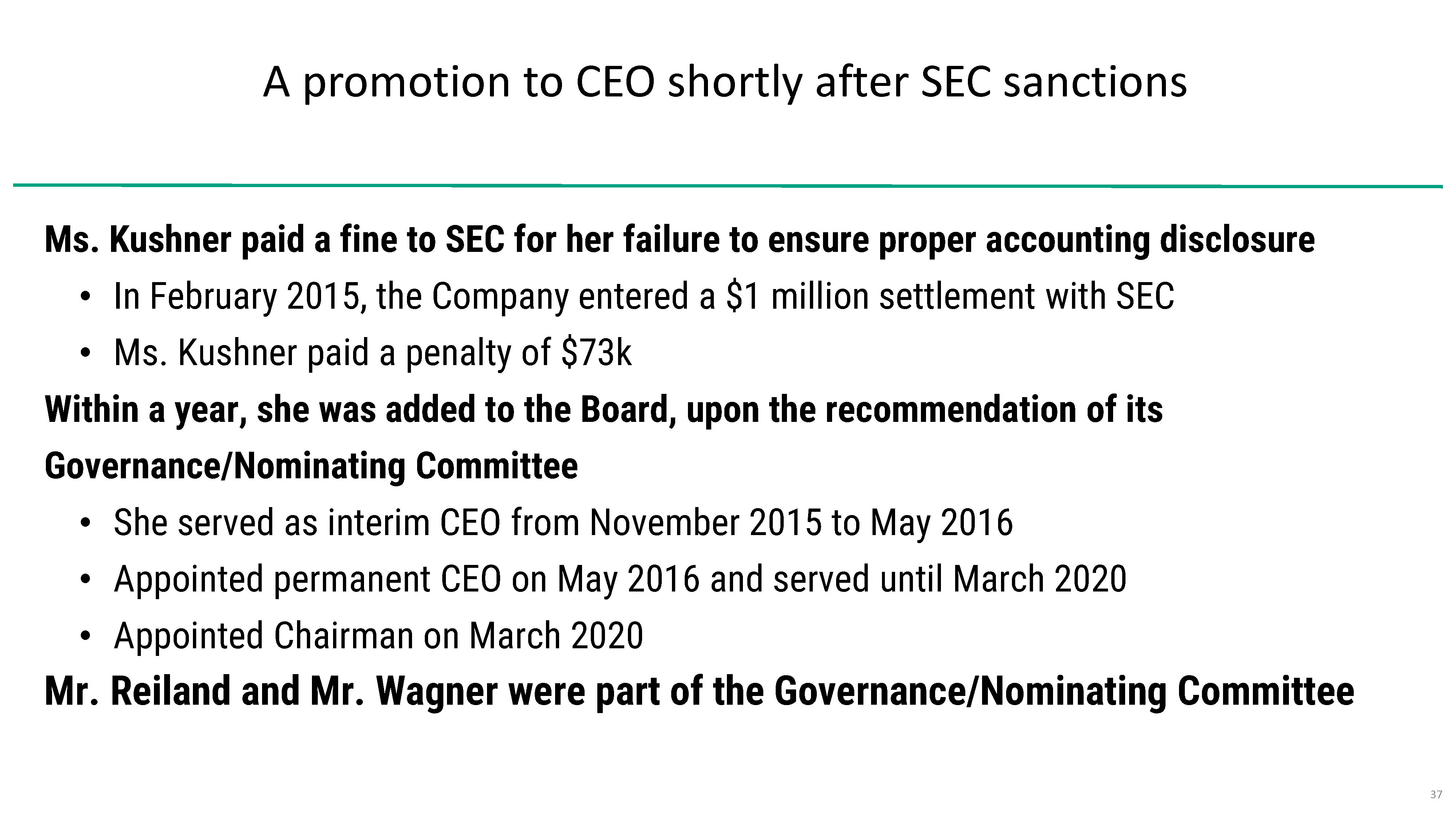

A promotion to CEO shortly after SEC sanctionsMs. Kushner paid a fine to SEC for her failure to ensure proper accounting disclosure • In February 2015, the Company entered a $1 million settlement with SEC • Ms. Kushner paid a penalty of $73k Within a year, she was added to the Board, upon the recommendation of its Governance/Nominating Committee • She served as interim CEO from November 2015 to May 2016• Appointed permanent CEO on May 2016 and served until March 2020• Appointed Chairman on March 2020Mr. Reiland and Mr. Wagner were part of the Governance/Nominating Committee

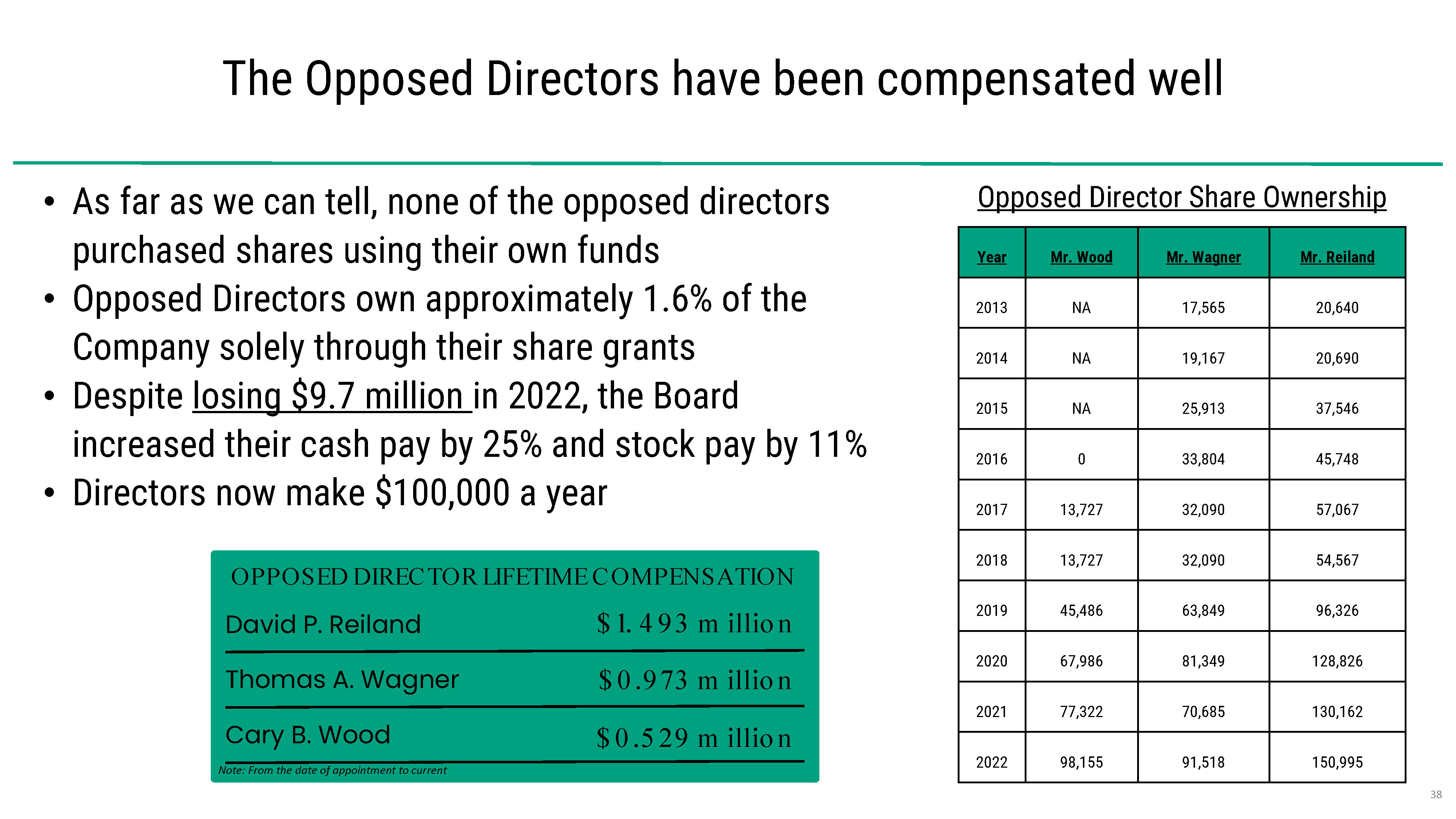

The Opposed Directors have been compensated well• As far as we can tell, none of the opposed directors Opposed Director Share Ownershippurchased shares using their own funds• Opposed Directors own approximately 1.6% of the Company solely through their share grants• Despite losing $9.7 million in 2022, the Board increased their cash pay by 25% and stock pay by 11%• Directors now make $100,000 a yearYear Mr. Wood Mr. Wagner Mr. Reiland 2013 NA 17,565 20,640 2014 NA 19,167 20,690 2015 NA 25,913 37,546 2016 0 33,804 45,748 2017 13,727 32,090 57,067 2018 13,727 32,090 54,567 2019 45,486 63,849 96,326 2020 67,986 81,349 128,826 2021 77,322 70,685 130,162 2022 98,155 91,518 150,995

4. Broadwind’s Misleading Claims

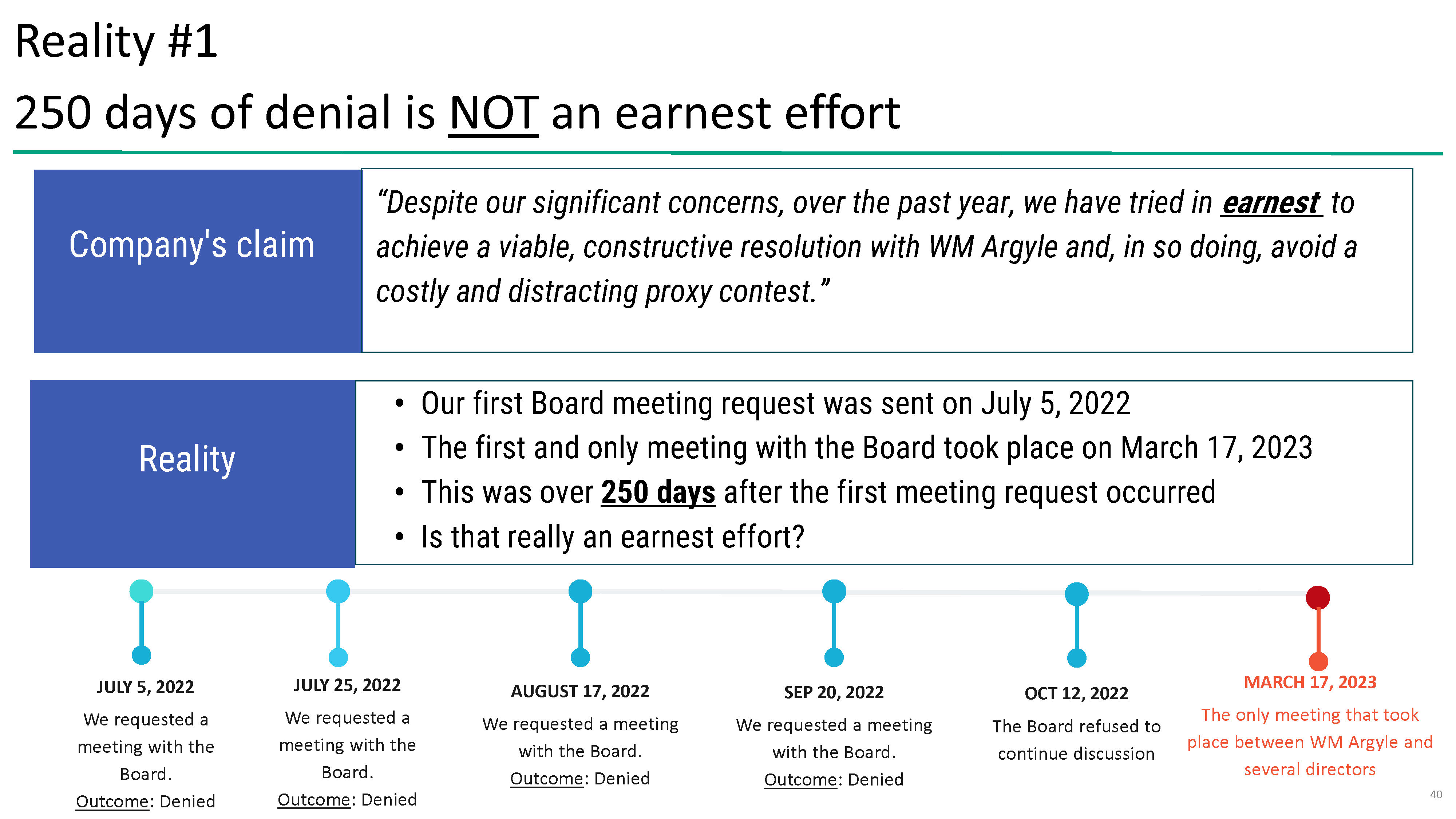

“Lies aren't answers. "But they sound so much better than the truth.” -Alexander Christo, To Kill a KingdomReality #1 250 days of denial is NOT an earnest effort Reality #2 Seeking three Board seats is NOT equal to taking controlJULY 5, 2022 JULY 25, 2022 AUGUST 17, 2022 SEP 20, 2022 OCT 12, 2022 MARCH 17, 2023 We requested a We requested a We requested a meeting We requested a meeting The Board refused to The only meeting that took meeting with the meeting with the with the Board. with the Board. continue discussion place between WM Argyle and Board. Board. Outcome: Denied Outcome: Denied several directors Outcome: Denied Outcome: Denied 40

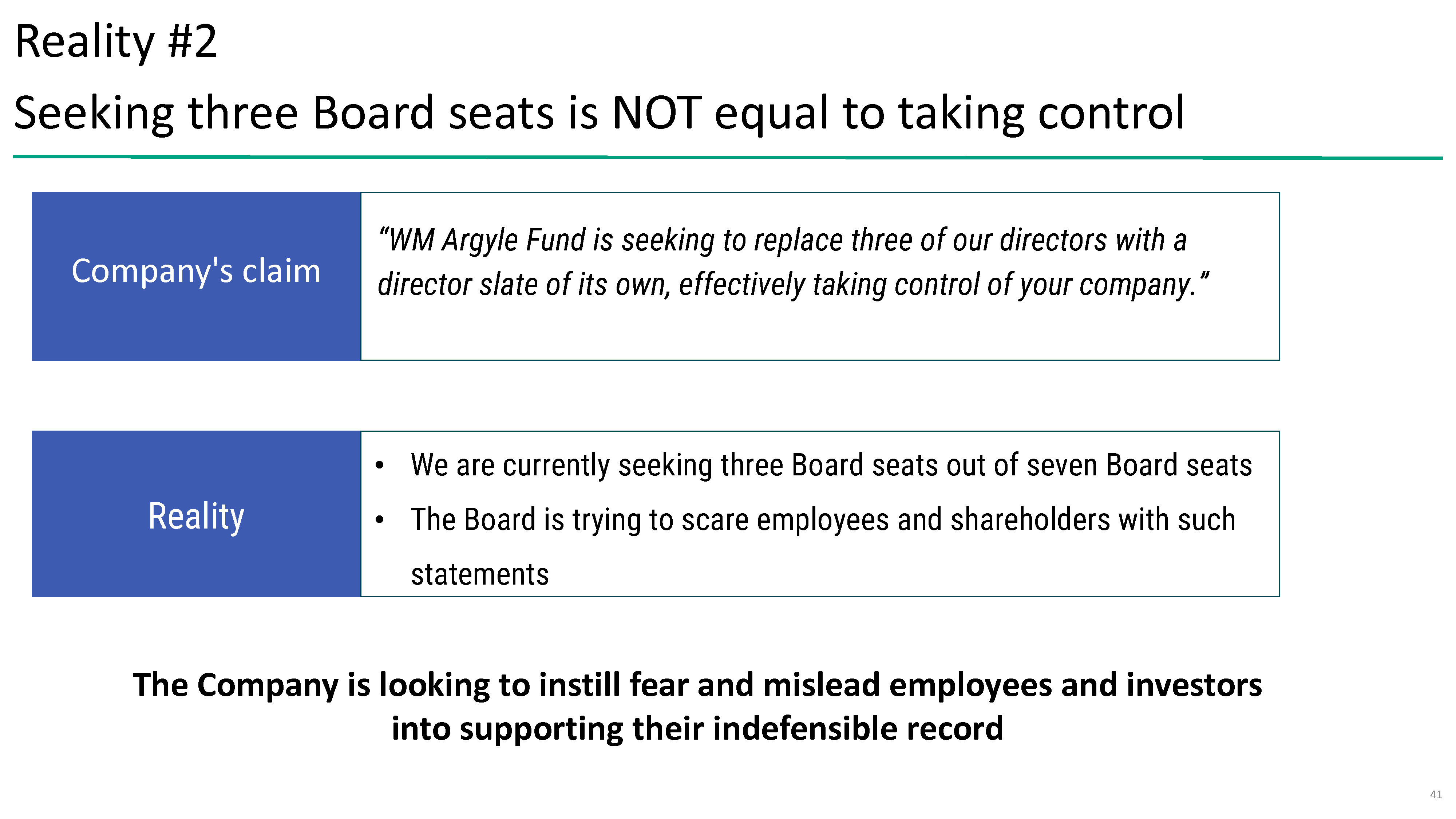

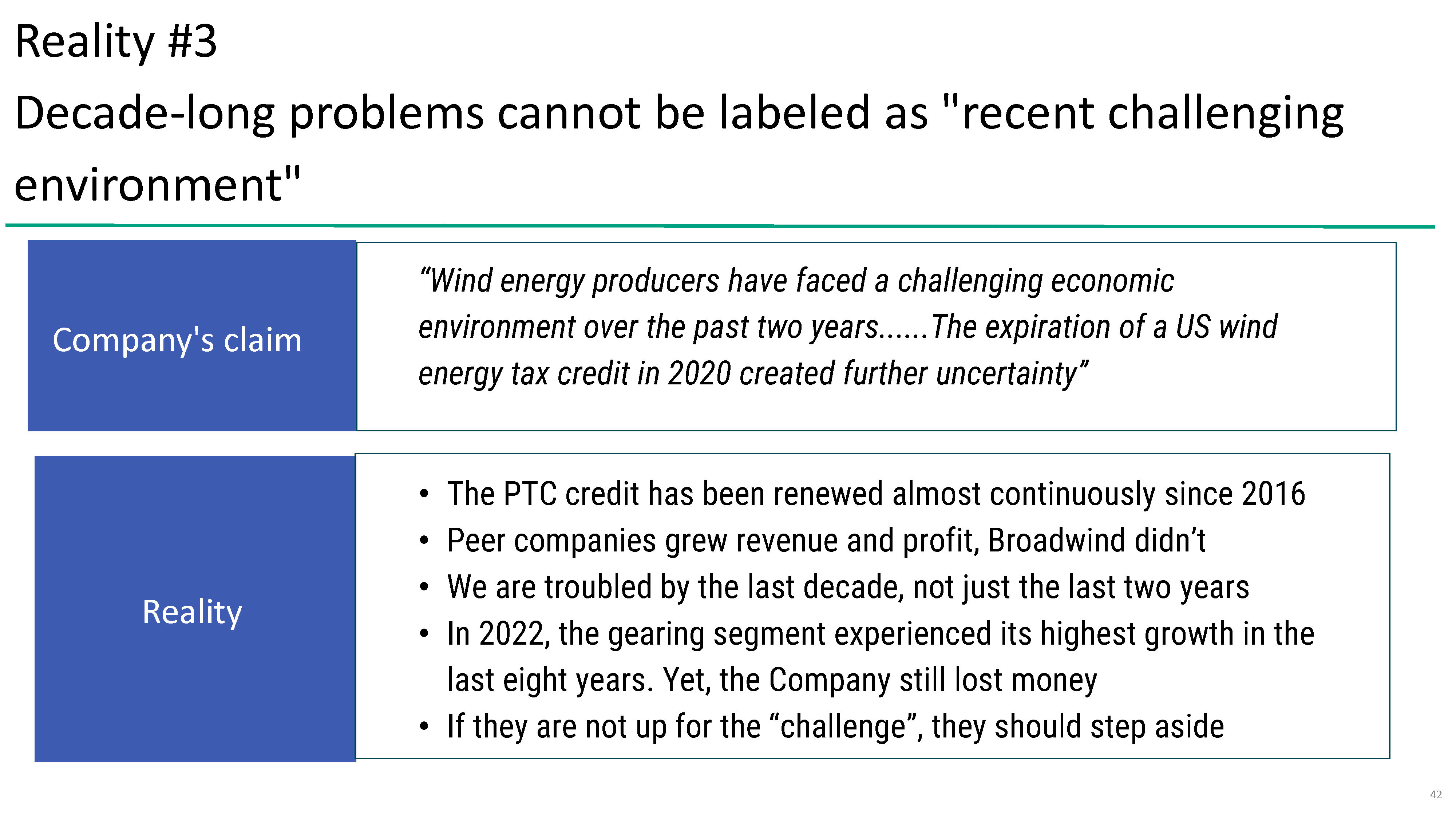

Company's claim “WM Argyle Fund is seeking to replace three of our directors with a director slate of its own, effectively taking control of your company.”• We are currently seeking three Board seats out of seven Board seats Reality • The Board is trying to scare employees and shareholders with such statementsThe Company is looking to instill fear and mislead employees and investors into supporting their indefensible record Reality #3 Decade-long problems cannot be labeled as "recent challenging environment" Reality #4 Chasing profitability is more important Reality #5 Destroying shareholder value does not qualify as effective capitalCompany's claim “Wind energy producers have faced a challenging economic environment over the past two years......The expiration of a US wind energy tax credit in 2020 created further uncertainty”

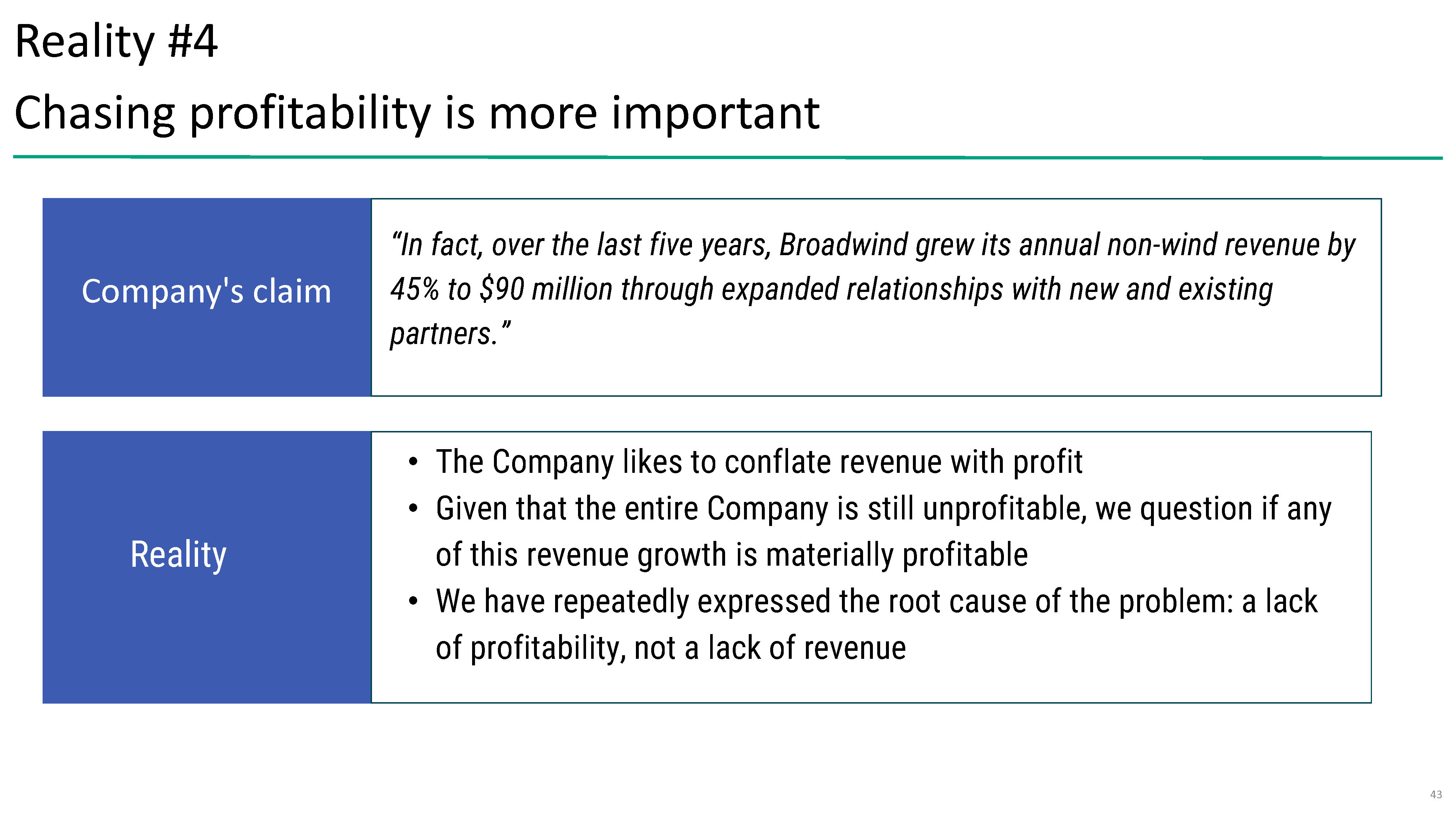

“In fact, over the last five years, Broadwind grew its annual non-wind revenue by Company's claim 45% to $90 million through expanded relationships with new and existing partners.”• The Company likes to conflate revenue with profit Reality • Given that the entire Company is still unprofitable, we question if any of this revenue growth is materially profitable • We have repeatedly expressed the root cause of the problem: a lack of profitability, not a lack of revenue

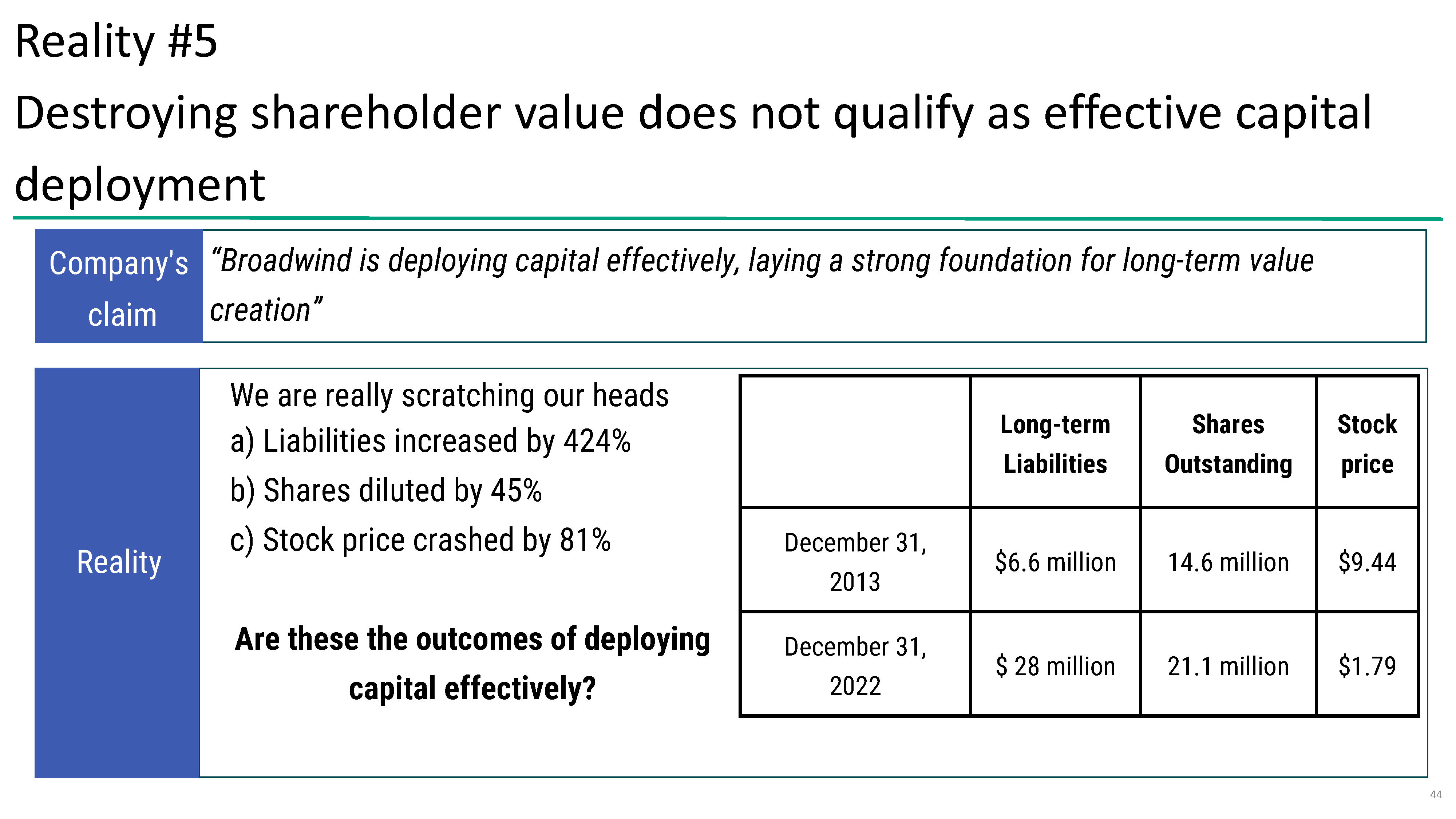

Company's claim “Broadwind is deploying capital effectively, laying a strong foundation for long-term value creation”Reality We are really scratching our heads a) Liabilities increased by 424% b) Shares diluted by 45% c) Stock price crashed by 81% Are these the outcomes of deploying capital effectively? December 31, 2013 December 31, 2022 Long-term Liabilities $6.6 million $ 28 million Shares Outstanding 14.6 million 21.1 million Stock price $9.44 $1.79

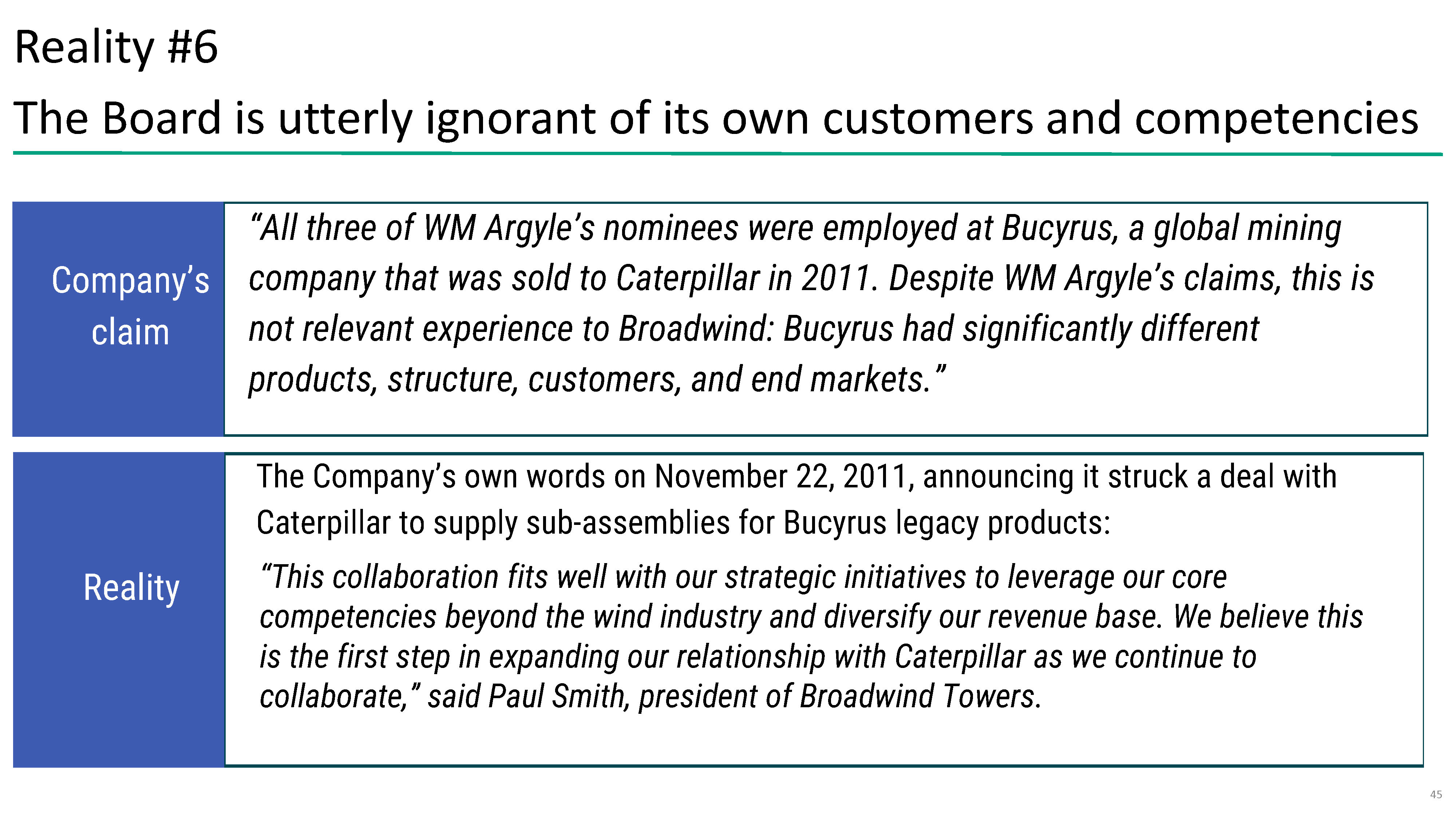

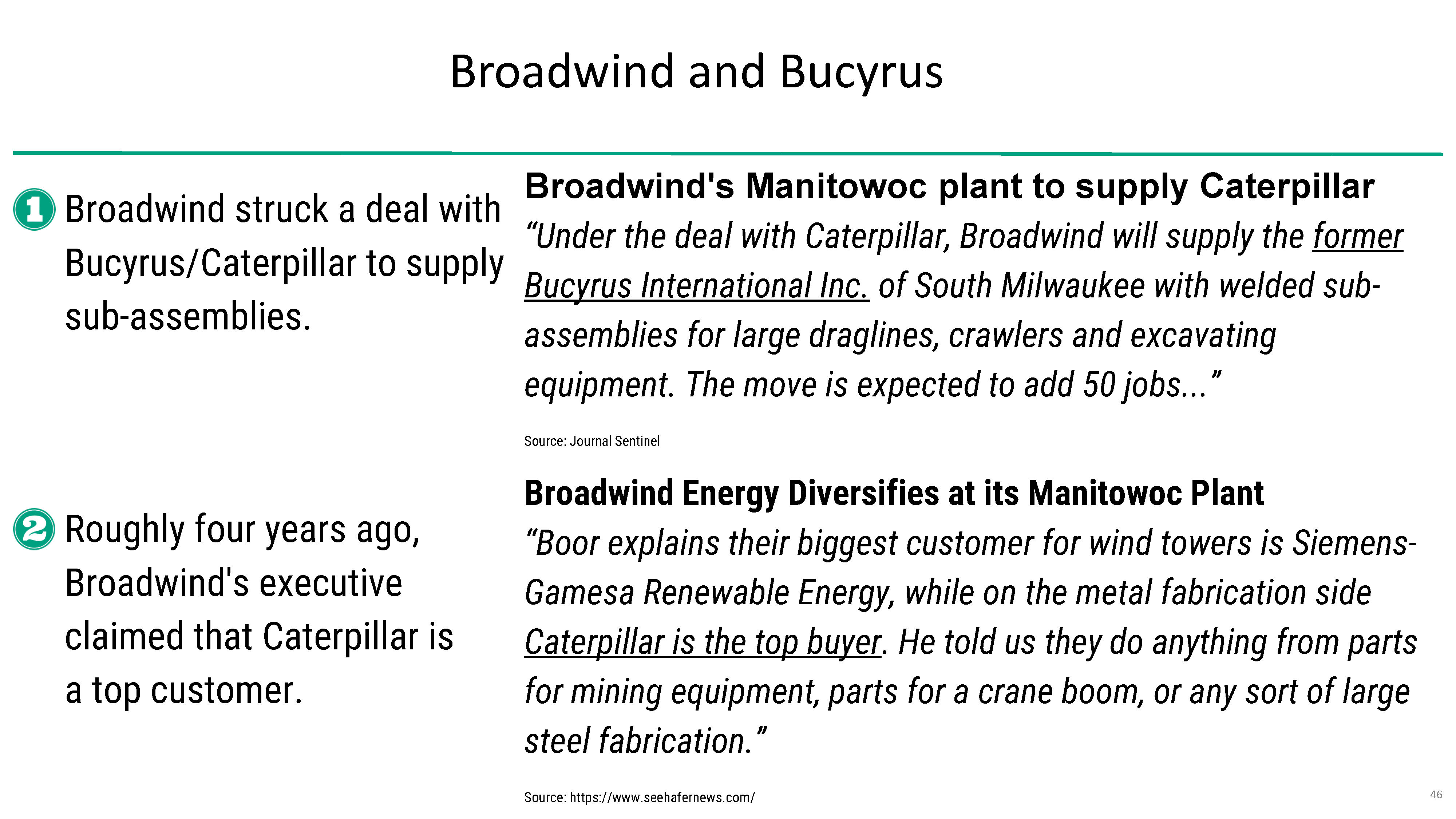

Reality #6Company’s claim “All three of WM Argyle’s nominees were employed at Bucyrus, a global mining company that was sold to Caterpillar in 2011. Despite WM Argyle’s claims, this is not relevant experience to Broadwind: Bucyrus had significantly different products, structure, customers, and end markets.”Reality The Company’s own words on November 22, 2011, announcing it struck a deal with Caterpillar to supply sub-assemblies for Bucyrus legacy products: “This collaboration fits well with our strategic initiatives to leverage our core competencies beyond the wind industry and diversify our revenue base. We believe this is the first step in expanding our relationship with Caterpillar as we continue to collaborate,” said Paul Smith, president of Broadwind Towers.

Broadwind and BucyrusBroadwind struck a deal with Bucyrus/Caterpillar to supply sub-assemblies. Roughly four years ago, Broadwind's executive claimed that Caterpillar is a top customer. Broadwind's Manitowoc plant to supply Caterpillar “Under the deal with Caterpillar, Broadwind will supply the former Bucyrus International Inc. of South Milwaukee with welded sub-assemblies for large draglines, crawlers and excavating equipment. The move is expected to add 50 jobs...” Source: Journal Sentinel Broadwind Energy Diversifies at its Manitowoc Plant “Boor explains their biggest customer for wind towers is Siemens-Gamesa Renewable Energy, while on the metal fabrication side Caterpillar is the top buyer. He told us they do anything from parts for mining equipment, parts for a crane boom, or any sort of large steel fabrication.” Source: https://www.seehafernews.com/

Broadwind and BucyrusMining is an important industry for Broadwind. Its exposure affects the Company's topline significantly. “The pace of order growth from industrial, mining and steel processing is significantly outpacing that from our oil and gas customers…” -Eric Blashford, Current CEO, Broadwind, Q4 2022“The mining sector drove about 9% of TTM revenue” -Eric Blashford, Current CEO, Broadwind, Q3 2020 “Mining remains strong, we are broadening our gear and heavy fabrication customer and product base in this market” -Ms. Kushner, Former CEO, Broadwind Conference call, Q2 2019

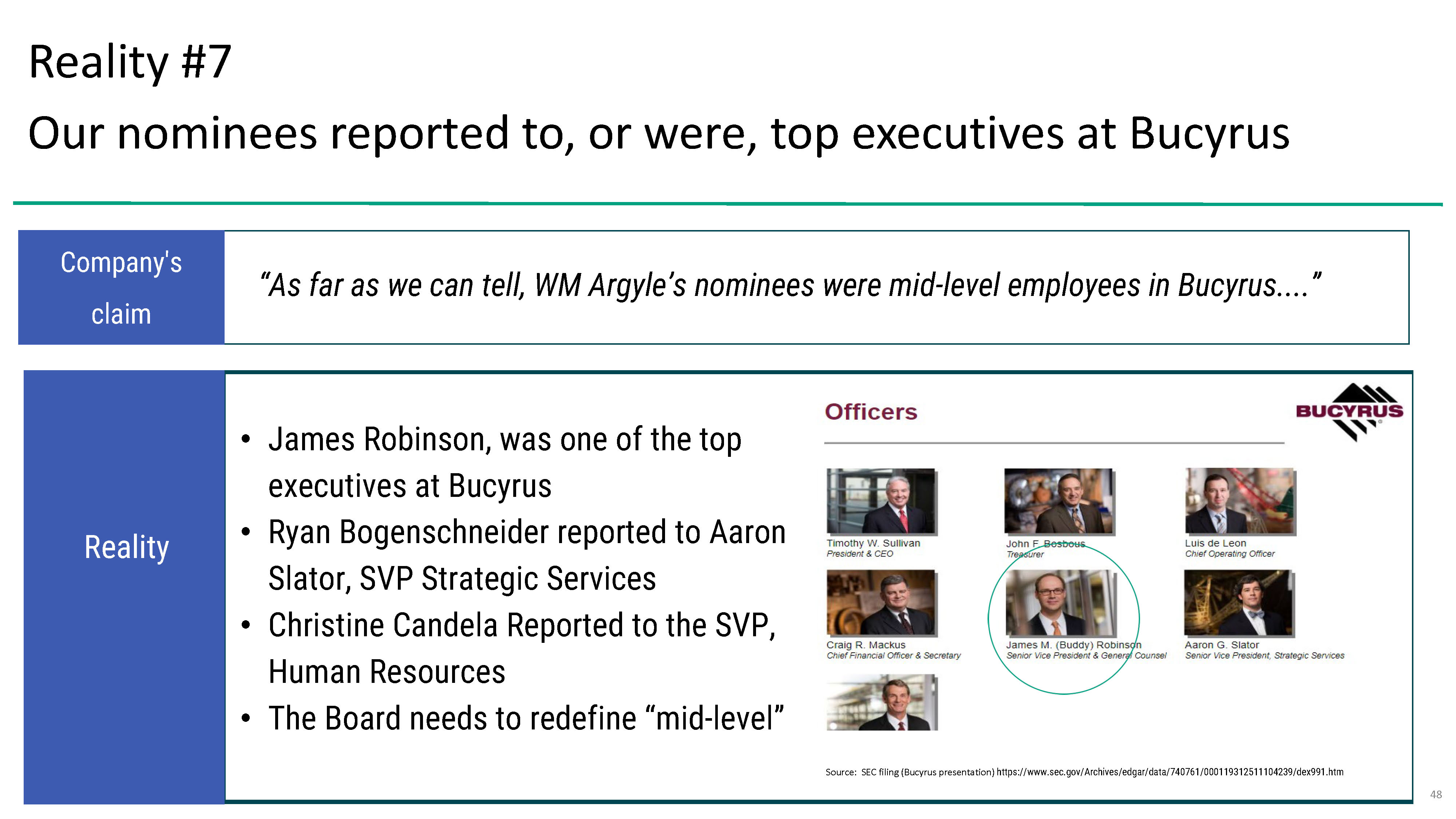

Reality #7 Our nominees reported to, or were, top executives at Bucyrus Reality #8 A company is not a dictatorship, leaders need good adviceCompany's claim “As far as we can tell, WM Argyle’s nominees were mid-level employees in Bucyrus....”

5. Broadwind ’s Lack of Strategy

The Board is banking on tax credits for profitabilityCompany's argument: “Broadwind is a key beneficiary of the Inflation Reduction Act (“IRA”) of 2022, which positions us to deliver significant margin expansion and improved profitability” • The incumbent directors are asking the shareholders to vote for them because the Company's profitability is expected to improve due to the tax credit• The Company's profitability is tied to the mercy of tax credits?• 2023 guidance does not mention profitability• This demonstrates that the Company has no roadmap for profitability other than tax incentives from the U.S. government

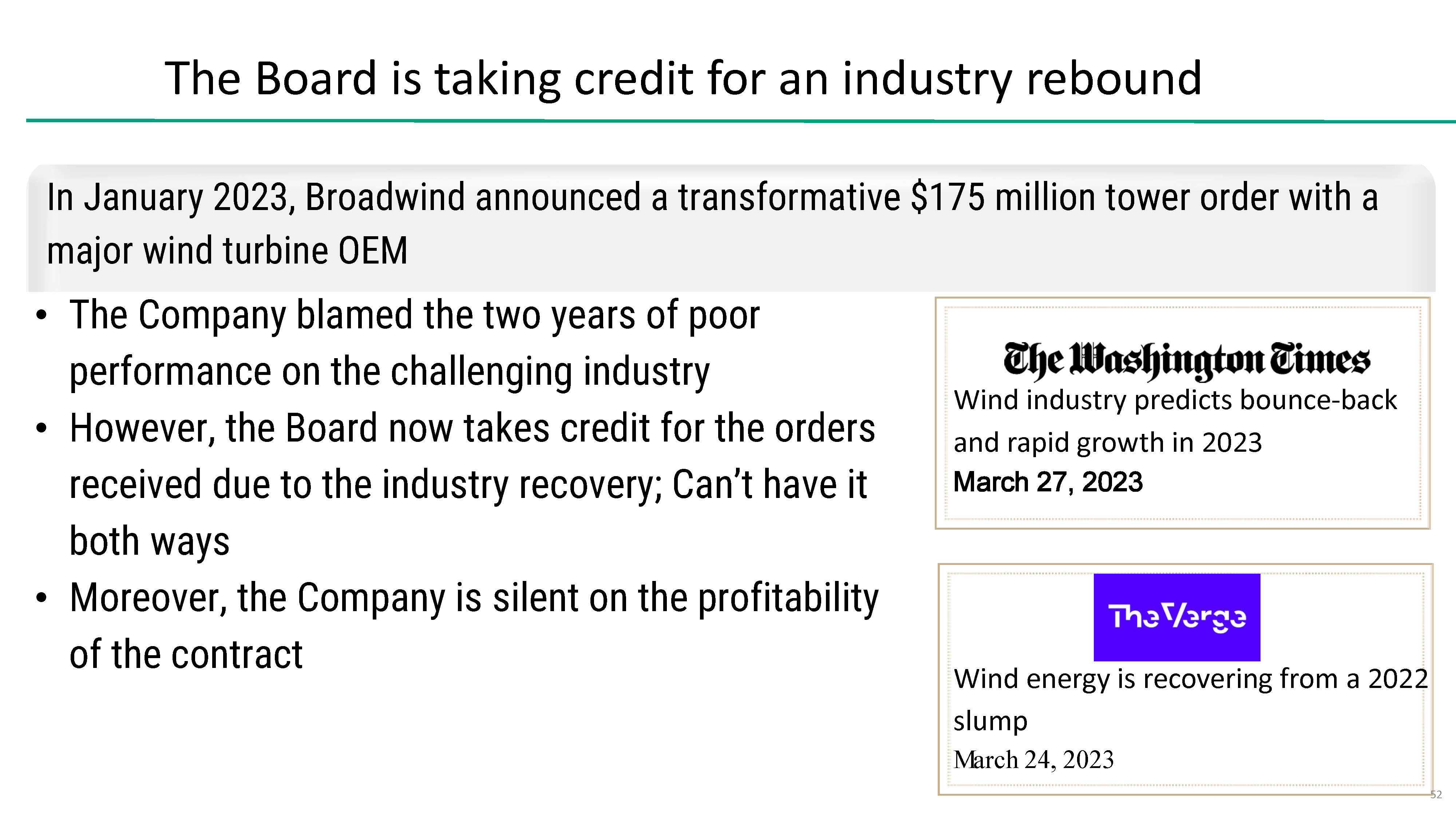

The Board is taking credit for an industry reboundIn January 2023, Broadwind announced a transformative $175 million tower order with a major wind turbine OEM • The Company blamed the two years of poor performance on the challenging industry• However, the Board now takes credit for the orders received due to the industry recovery; Can’t have it both ways• Moreover, the Company is silent on the profitability of the contract

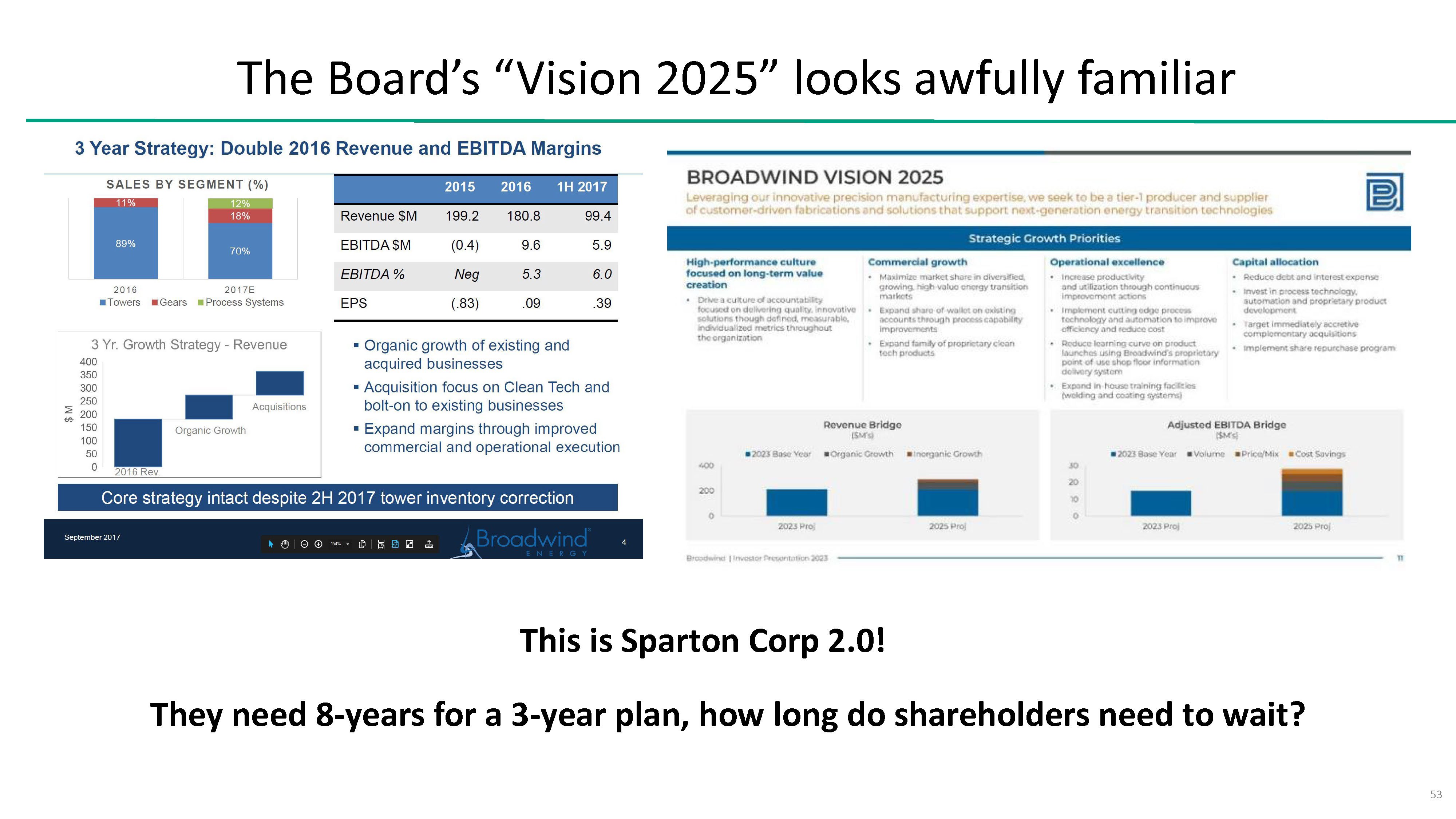

The Board’s “Vision 2025” looks awfully familiarThis is Sparton Corp 2.0! They need 8-years for a 3-year plan, how long do shareholders need to wait?

6. Our Plan & Nominees

Our Plan• Enhance Corporate Governance – Director compensation should be reduced until the Company reaches sustained profitability. Align executive pay with rigorous performance metrics. Address the shareholder dilution in the proposed equity plan. Increase communication with shareholders, employees, and key customers throughout the year.• Optimize the Balance Sheet and Use of the NOL’s – We need to prioritize profitability, use the NOL’s, and maximize the creation of the IRA tax credits. We do NOT want to sell the IRA tax credits unless they are sold at face value. Anything less is unacceptable. Improve our overall balance sheet so customers have faith in our ability to deliver products.

• Assess Management and Improve Human Capital – We need an assessment of management’s capabilities to ensure the Company has a leadership team that is capable of accomplishing the strategic plan. The ideal team will include individuals with deep experience across engineering, manufacturing, sales, strategy, and other growth areas. “Yes Men” need to be removed and replaced with competent managers that can give honest and direct feedback to superiors and subordinates.• Increase the Creation of Intellectual Property – We need to invest in the engineering function to enable the creation of Broadwind-owned Intellectual Property (IP). Controlling the IP of the Company’s products will enable better control over their production, service, and performance.

Our Plan• Prioritize Transparent Investor Relations – The Company needs to host a public investor day open to all investors not just investors management prefers. We need to regularly publish KPI’s such as backlog, install base, new product revenue, and profitability metrics• Explore Accretive M&A to Supplement Organic Growth – We would support management in seeking to secure additional sales contracts, as well as invest in smart, strategic acquisitions that accelerate the Company’s growth.• Strengthen Existing Business Segments – We would focus management to accelerate cost containment and organic investment across all segments. We believe that deploying more capital to customer acquisition, category expansion, and sustaining a frictionless customer service franchise would yield higher returns for stockholders.

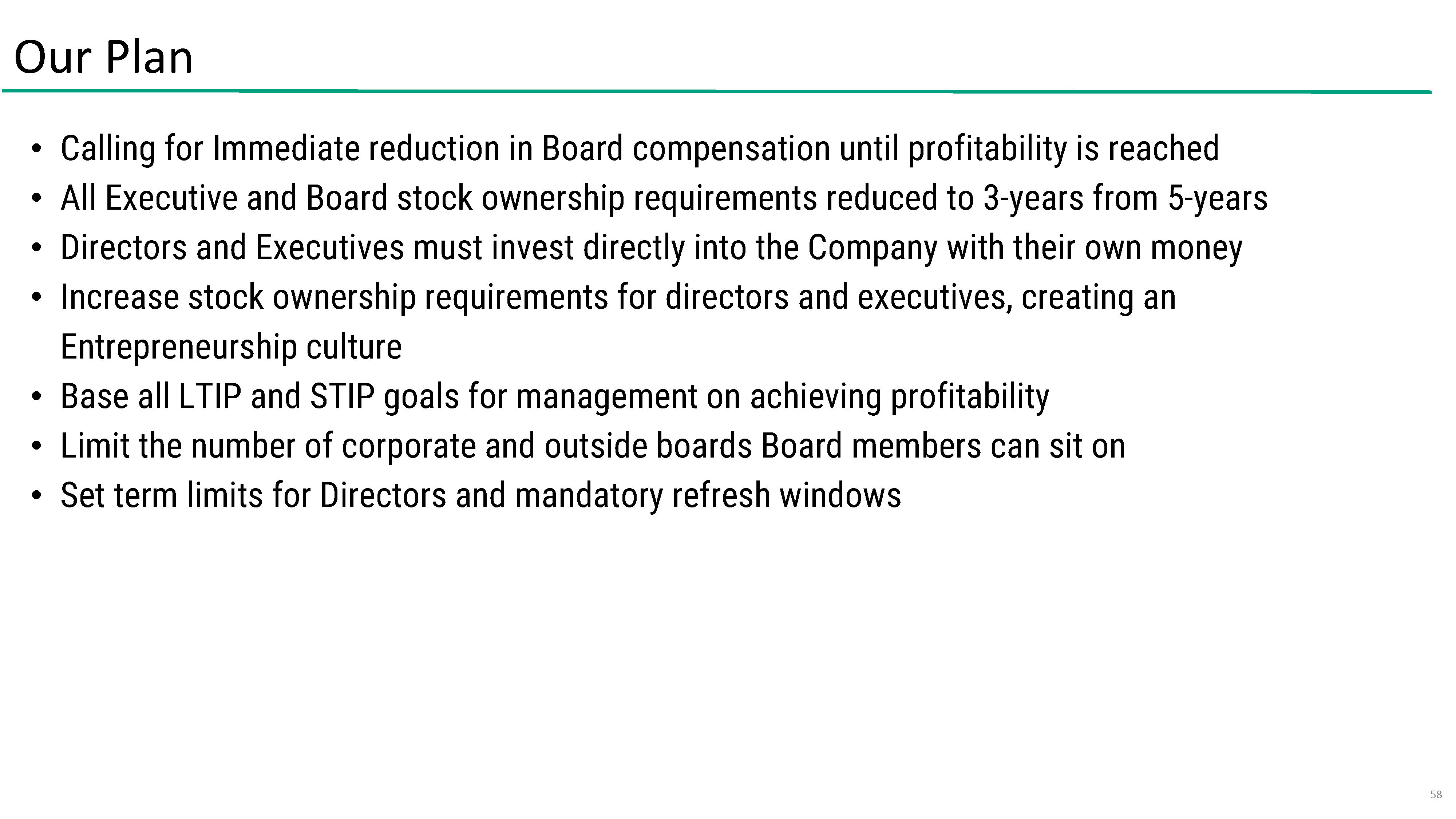

Our Plan• Calling for Immediate reduction in Board compensation until profitability is reached• All Executive and Board stock ownership requirements reduced to 3-years from 5-years• Directors and Executives must invest directly into the Company with their own money• Increase stock ownership requirements for directors and executives, creating an Entrepreneurship culture• Base all LTIP and STIP goals for management on achieving profitability• Limit the number of corporate and outside boards Board members can sit on• Set term limits for Directors and mandatory refresh windows

RYANMEET BOGENSCHNEIDER OURNOMINEESJAMES M. ROBINSON IV

Ryan Bogenschneider is the founder and has served as Principal of The Western Metropolis Company, a management and consulting company, since January 2013. Western Metropolis focuses on corporate development activities such as mergers & acquisitions, growth strategies, and recapitalizations. Mr. Bogenschneider has also served as Chief Executive Officer of WM Argyle Fund LLC, a private fund formed for the purpose of being an investor in Broadwind, Inc., since April 2022. Prior to Western Metropolis, Mr. Bogenschneider worked in corporate development and strategy positions at Mining Technologies International Inc. and Bucyrus International.

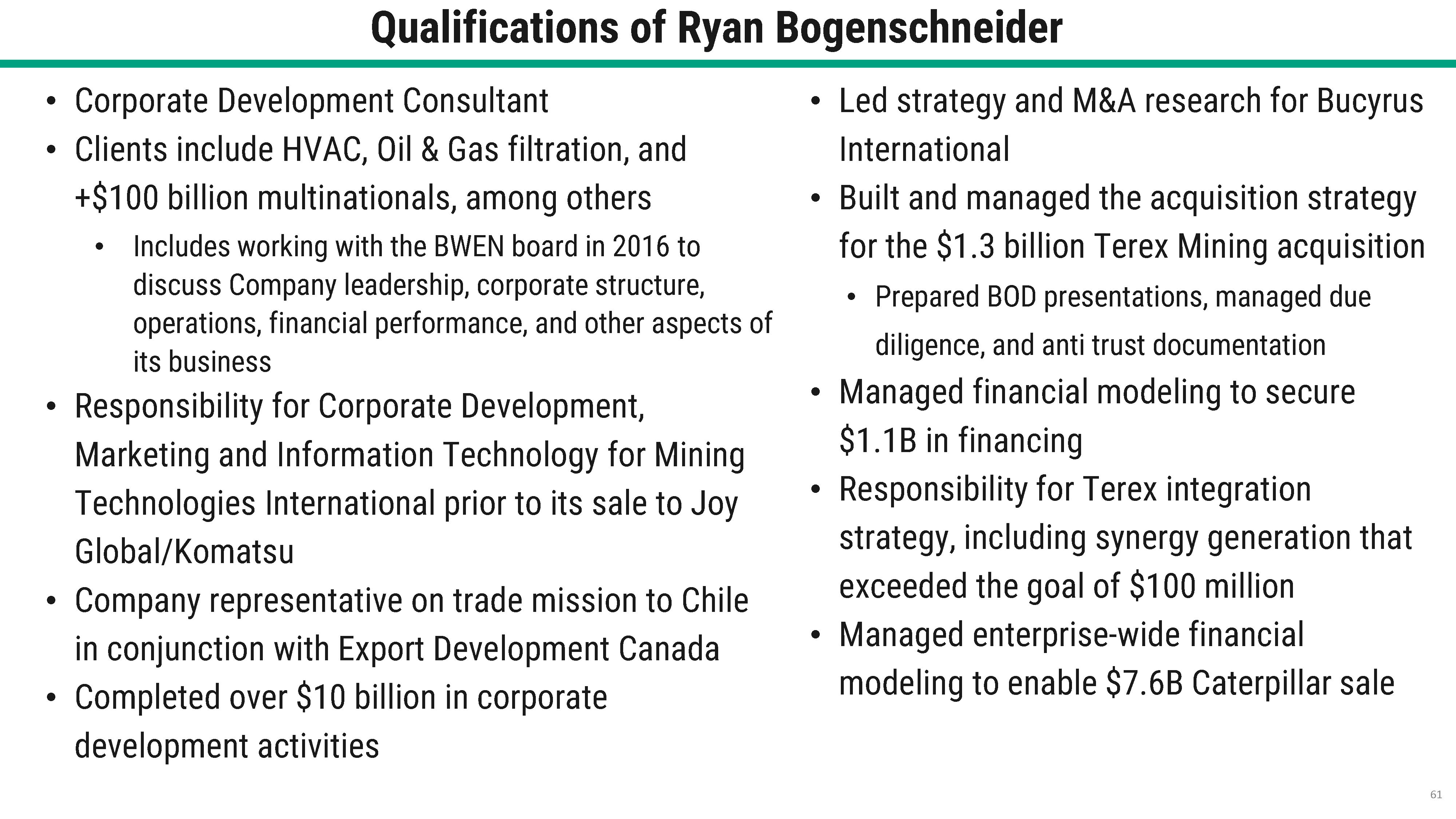

Qualifications of Ryan Bogenschneider • Corporate Development Consultant• Clients include HVAC, Oil & Gas filtration, and +$100 billion multinationals, among others• Includes working with the BWEN board in 2016 to discuss Company leadership, corporate structure, operations, financial performance, and other aspects of its business• Responsibility for Corporate Development, Marketing and Information Technology for Mining Technologies International prior to its sale to Joy Global/Komatsu• Company representative on trade mission to Chile in conjunction with Export Development Canada• Completed over $10 billion in corporate development activities• Led strategy and M&A research for Bucyrus International• Built and managed the acquisition strategy for the $1.3 billion Terex Mining acquisition• Prepared BOD presentations, managed due diligence, and anti trust documentation• Managed financial modeling to secure $1.1B in financing• Responsibility for Terex integration strategy, including synergy generation that exceeded the goal of $100 million• Managed enterprise-wide financial modeling to enable $7.6B Caterpillar sale

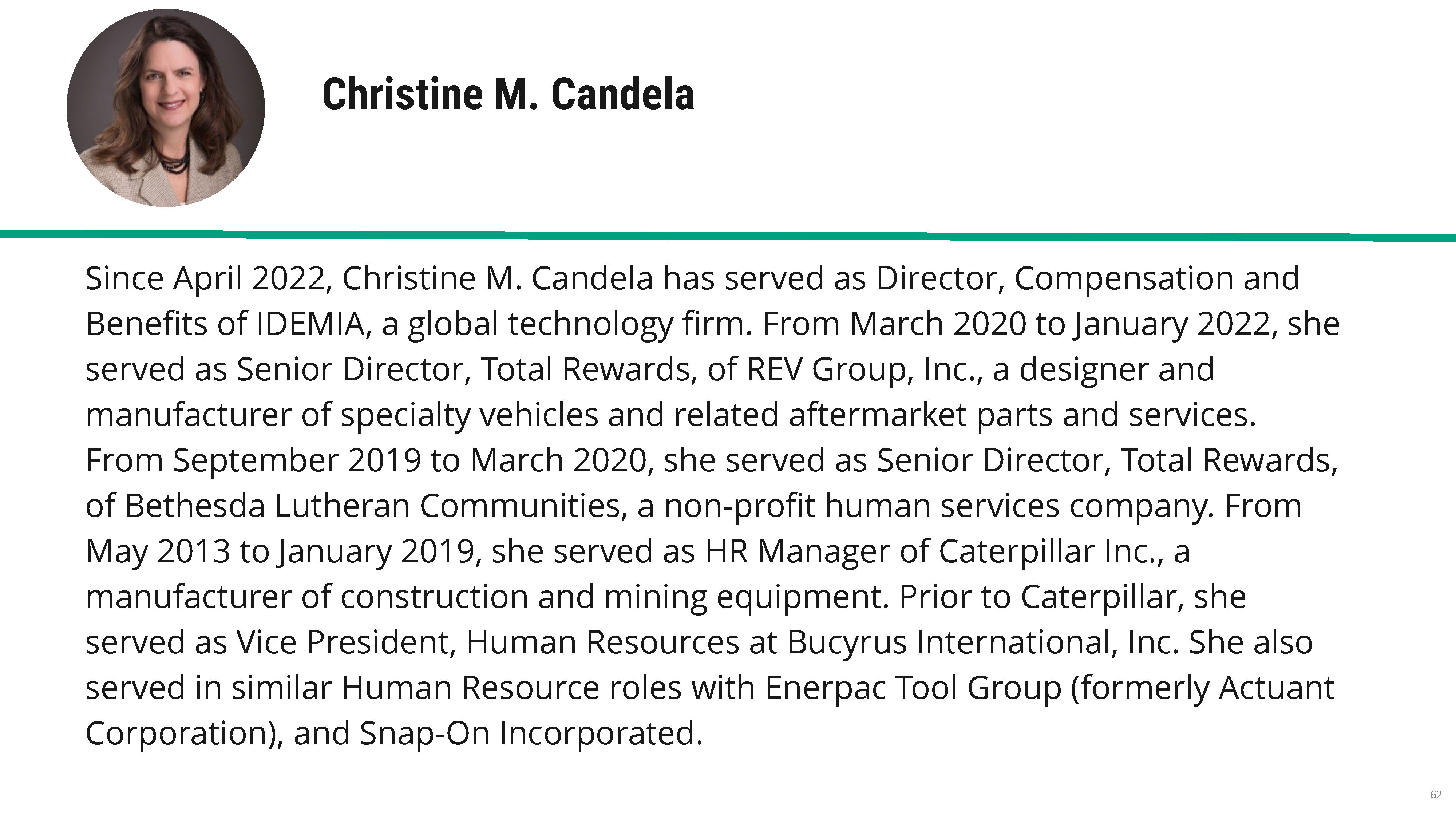

Christine M. CandelaSince April 2022, Christine M. Candela has served as Director, Compensation and Benefits of IDEMIA, a global technology firm. From March 2020 to January 2022, she served as Senior Director, Total Rewards, of REV Group, Inc., a designer and manufacturer of specialty vehicles and related aftermarket parts and services. From September 2019 to March 2020, she served as Senior Director, Total Rewards, of Bethesda Lutheran Communities, a non-profit human services company. From May 2013 to January 2019, she served as HR Manager of Caterpillar Inc., a manufacturer of construction and mining equipment. Prior to Caterpillar, she served as Vice President, Human Resources at Bucyrus International, Inc. She also served in similar Human Resource roles with Enerpac Tool Group (formerly Actuant Corporation), and Snap-On Incorporated.

Qualifications of Christine M. Candela• Selected to oversee a full-scale, two-year global HR integration due to Caterpillar’s acquisition of Bucyrus International, which involved integrating 10,000 employees in 30 countries into new benefits and compensation programs in three distinct phases.• Executed complex golden parachute agreements for outgoing executives as a result of the Bucyrus acquisition• Extensive experience with various types of short-term, long-term, and sales incentive plans in multiple industries to drive pay for performance and align the interests of shareholders with employees.• Prepared CD&As for Proxy and SEC filings• Regularly prepared quarterly presentation materials for Boards of publicly traded companies• Expertise in executive compensation, variable incentive plans, acquisition due diligence, and integration work. Complimentary broad functional HR experience as an HR Director, managing a global mining division with 7,000 employees and $20B in annual sales during periods of extreme market volatility.

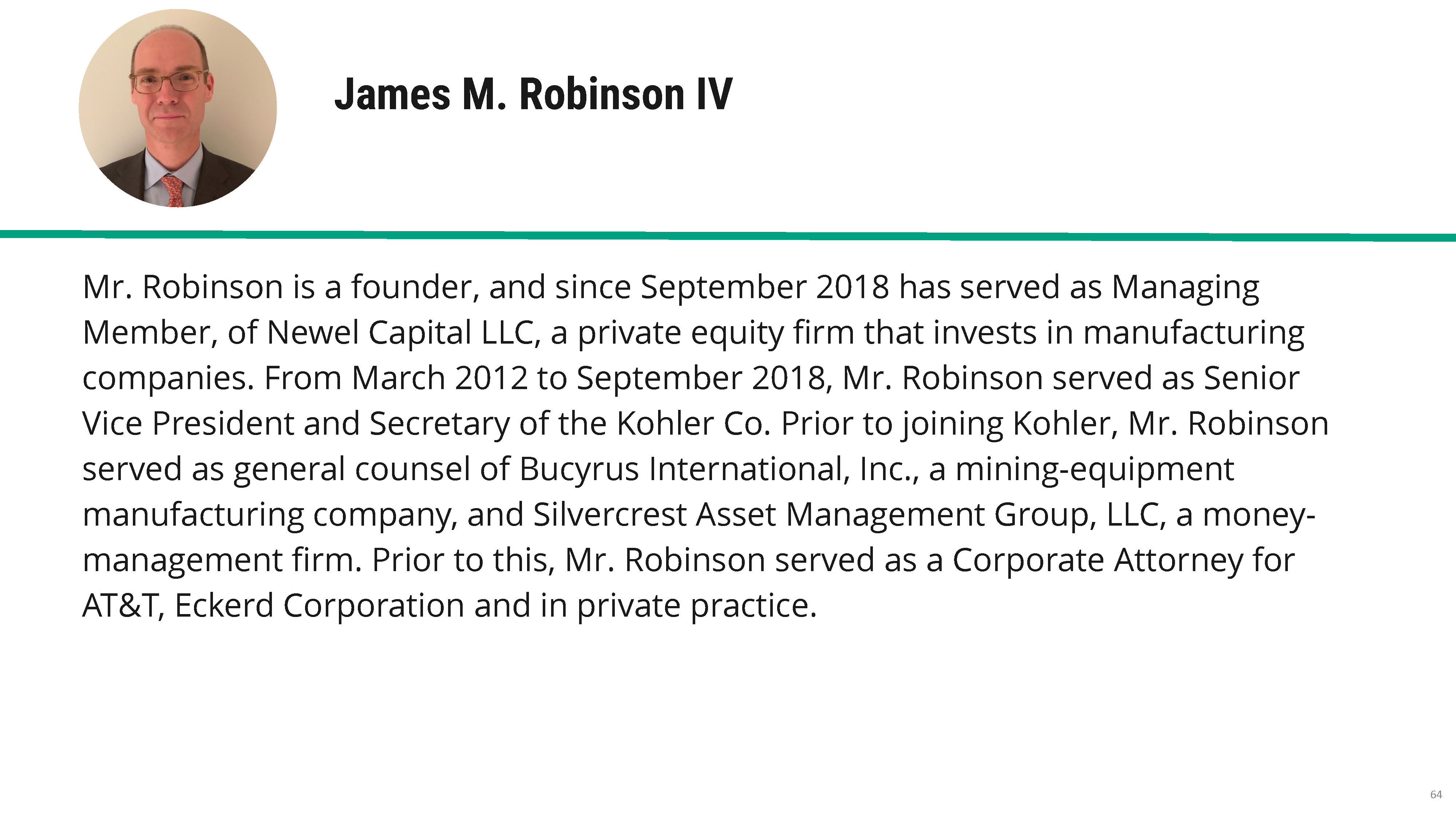

James M. Robinson IVMr. Robinson is a founder, and since September 2018 has served as Managing Member, of Newel Capital LLC, a private equity firm that invests in manufacturing companies. From March 2012 to September 2018, Mr. Robinson served as Senior Vice President and Secretary of the Kohler Co. Prior to joining Kohler, Mr. Robinson served as general counsel of Bucyrus International, Inc., a mining-equipment manufacturing company, and Silvercrest Asset Management Group, LLC, a money-management firm. Prior to this, Mr. Robinson served as a Corporate Attorney for AT&T, Eckerd Corporation and in private practice.

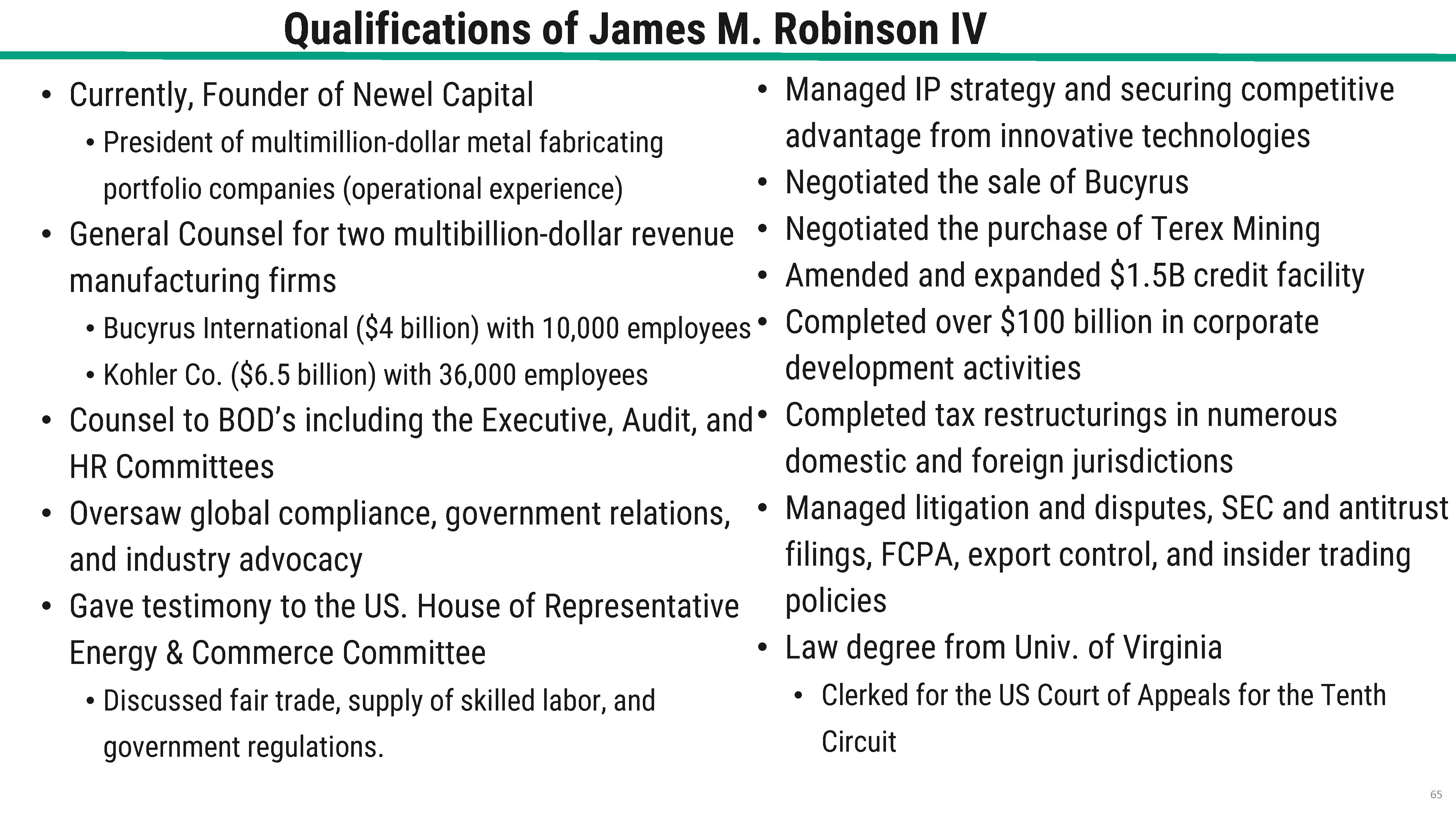

Qualifications of James M. Robinson IV• Currently, Founder of Newel Capital• President of multimillion-dollar metal fabricating portfolio companies (operational experience)• General Counsel for two multibillion-dollar revenue manufacturing firms• Bucyrus International ($4 billion) with 10,000 employees• Kohler Co. ($6.5 billion) with 36,000 employees• Counsel to BOD’s including the Executive, Audit, and HR Committees• Oversaw global compliance, government relations, and industry advocacy• Gave testimony to the US. House of Representative Energy & Commerce Committee• Discussed fair trade, supply of skilled labor, and government regulations. • Managed IP strategy and securing competitive advantage from innovative technologies• Negotiated the sale of Bucyrus• Negotiated the purchase of Terex Mining• Amended and expanded $1.5B credit facility• Completed over $100 billion in corporate development activities• Completed tax restructurings in numerous domestic and foreign jurisdictions• Managed litigation and disputes, SEC and antitrust filings, FCPA, export control, and insider trading policies• Law degree from Univ. of Virginia• Clerked for the US Court of Appeals for the Tenth Circuit

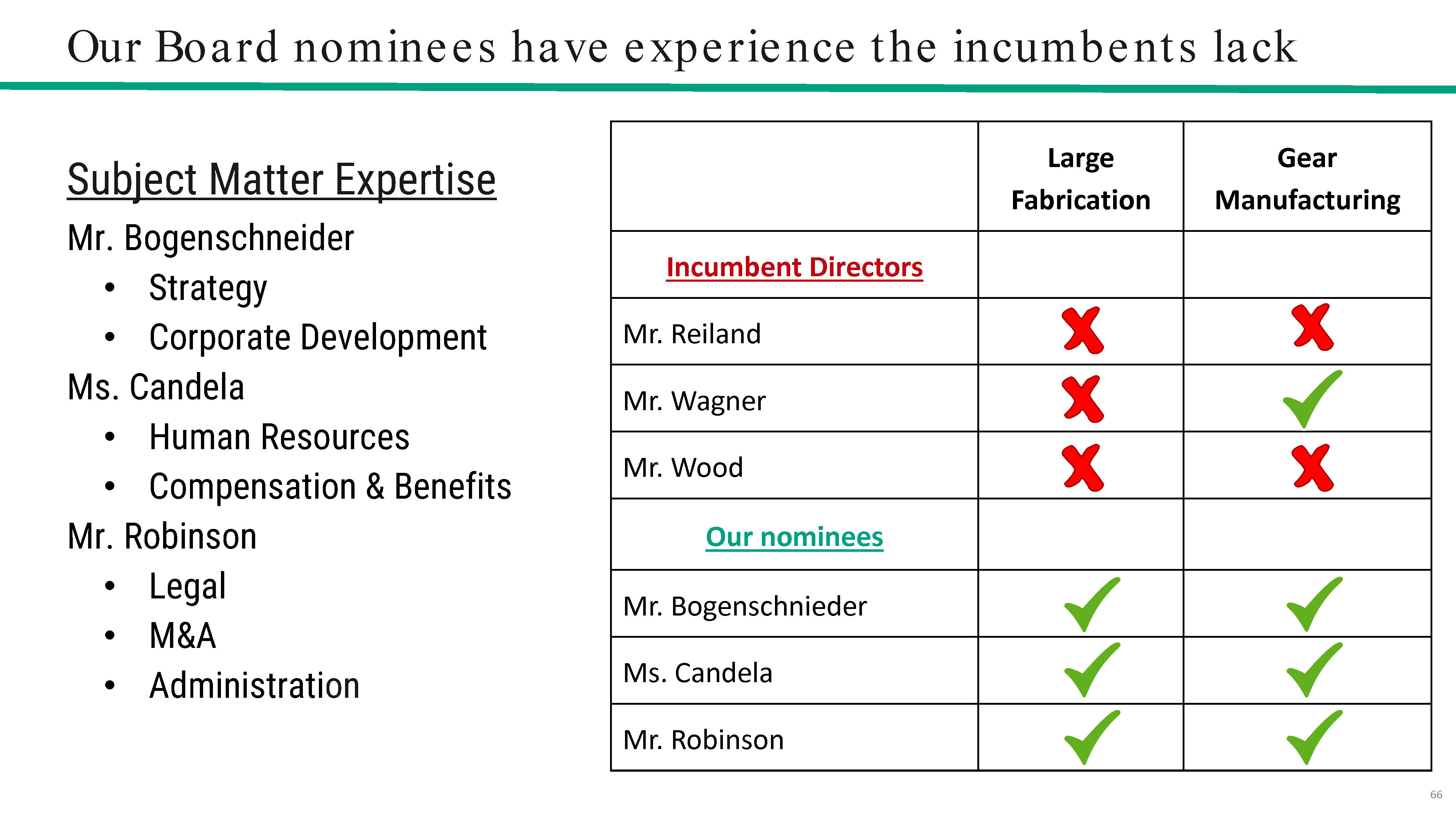

Our Board nominees have experience the incumbents lackSubject Matter Expertise Mr. Bogenschneider • Strategy • Corporate Development Ms. Candela• Human Resources• Compensation & Benefits Mr. Robinson• Legal• M&A• AdministrationLarge Fabrication Gear Manufacturing Incumbent Directors Mr. ReilandMr. WagnerMr. WoodOur nominees Mr. BogenschniederMs. CandelaMr. Robinson

We assembled a slate with the experience, expertise and track record required to deliver long-term shareholder value OUR SLATE IS THE RIGHT SOLUTION FOR STOCKHOLDERS

SUPPORT OUR NOMINEES AND REMOVE THETHREE ENTRENCHED DIRECTORS TO UNLOCK VALUE