AMERICAN SPECTRUM

February 25, 2011

Ms. Cicely LaMothe

Branch Chief

Securities and Exchange Commission

Washington, D.C. 20549

| Re: | American Spectrum Realty, Inc. |

Form 10-K for Year Ended December 31, 2009

File No. 001-16785

Dear Ms. LaMothe:

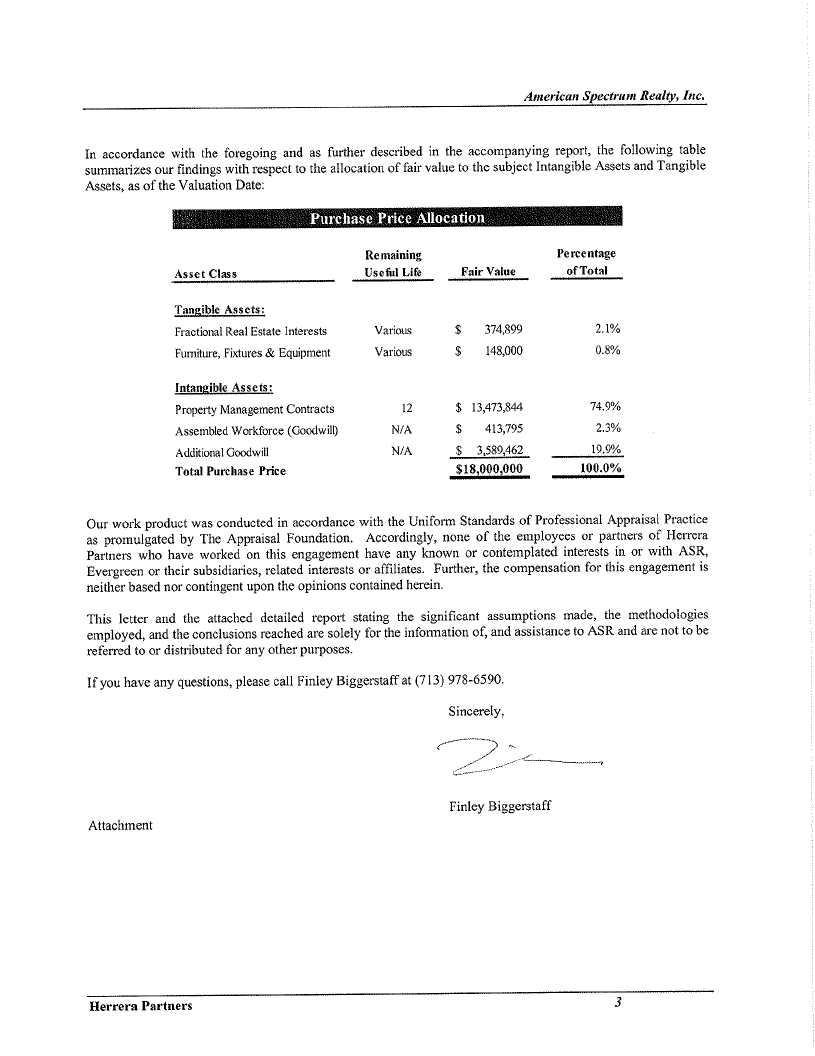

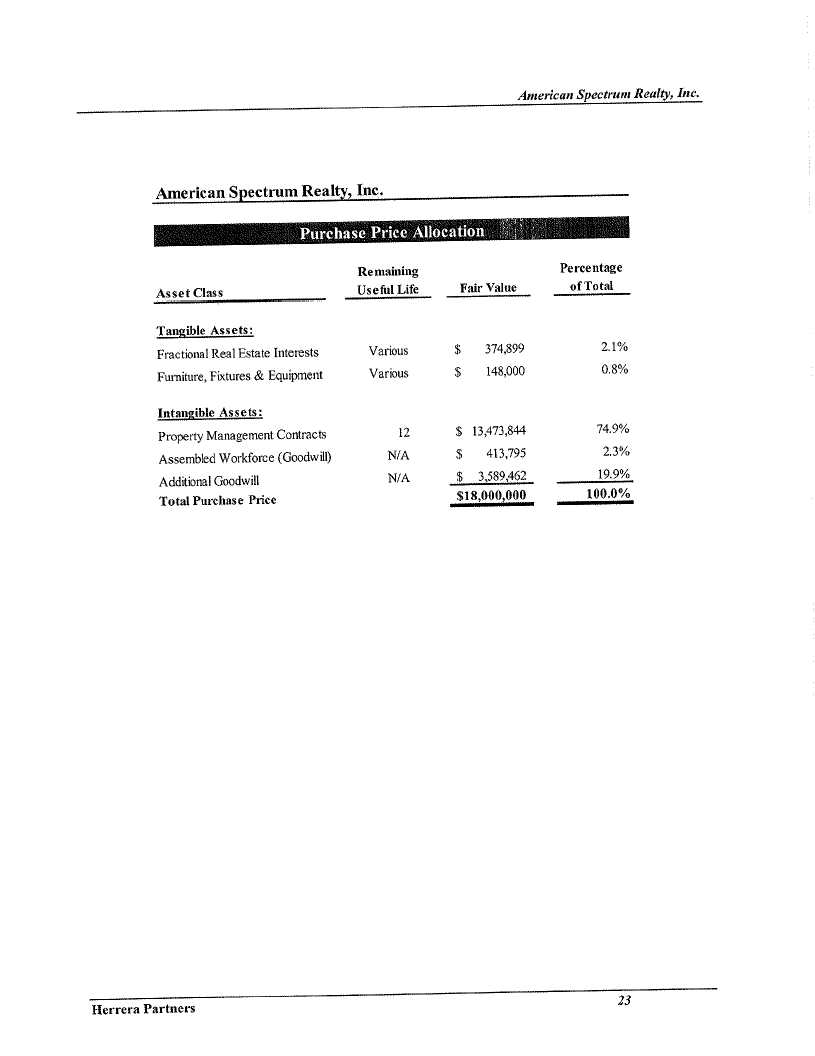

We have the responses set forth below to the comments set forth in your letter of January 7, 2011. Before answering the specific comments, however, we would like to inform you that, based on your prior letters and our telephone discussion, we have agreed to account for our acquisition of assets from Evergreen as a business combination. Accordingly, we have commissioned from Herrera Partners, an independent banking and consulting firm, a valuation allocation and analysis (the "Herrera Report"), which is attached as Exhibit A. We have adopted the findings of the Herrera Report, which concludes that the Evergreen purchase price of $18,000,000 should be allocated as follows:

| Fractional real estate interests | $ | 374,899 | ||

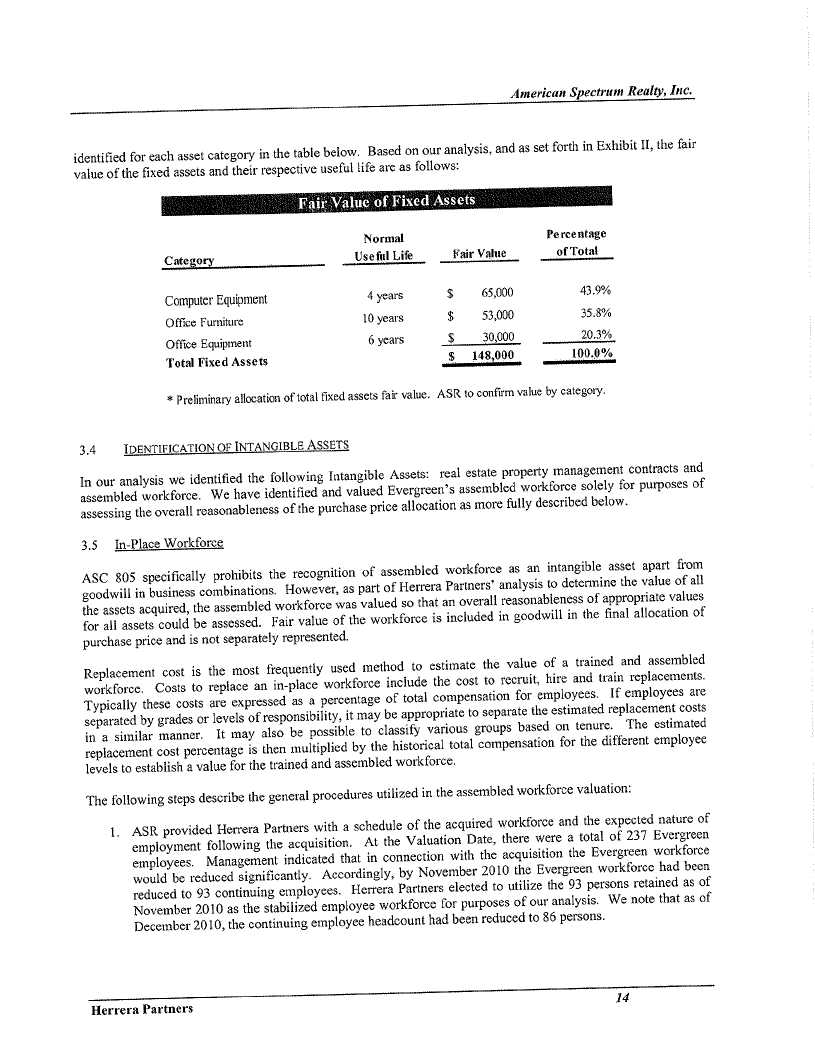

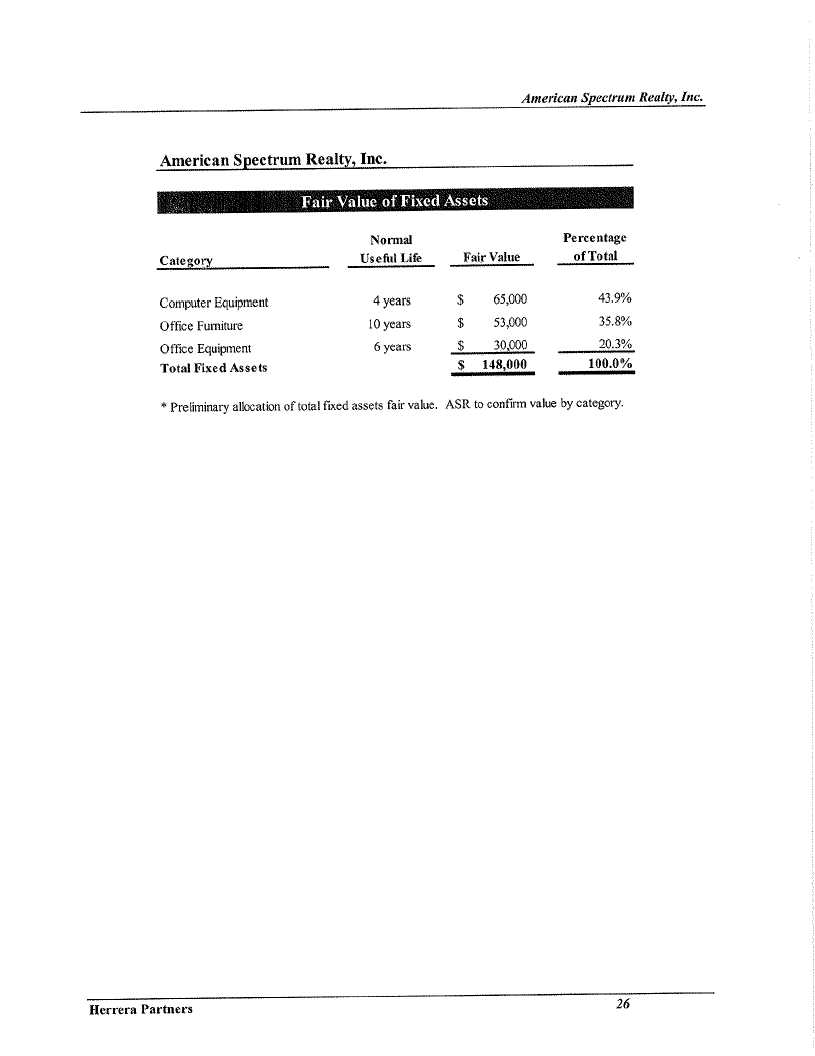

| Furniture, fixtures and equipment | 148,000 | |||

| Property management contracts | 13,473,844 | |||

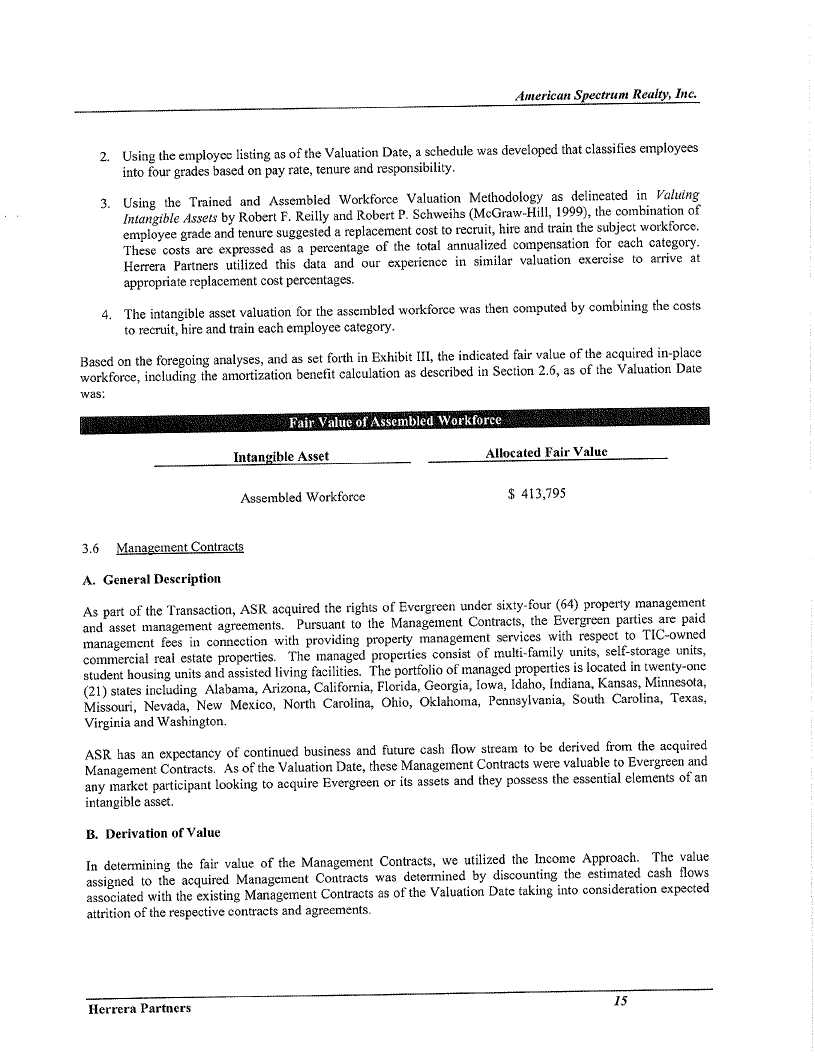

| Assembled workforce | 413,795 | |||

| Additional goodwill | 3,589,462 | |||

| TOTAL | $ | 18,000,000 | ||

Our specific responses to your January 7 comments are as follows:

Comment 1 – Evergreen LLCs:

Subcomment (a). In each of the eight LLCs in which American Spectrum owns membership interests, American Spectrum is named as a Member. In six of these eight LLCs, it has obtained the requisite consent of the Members to become the Manager; in the other two LLCs, it has not yet received the requisite consents to be appointed successor to the Evergreen entity as the Manager.

AMERICAN SPECTRUM REALTY, INC.

2401 Fountain View, Suite 510, Houston, Texas 77057

PH/ 713-706-6200 FX/713-706-6201

www.americanspectrum.com

Ms. Cicely LaMothe

February 25, 2011

Page 2

Subcomment (b). In our earlier letter to you, we indicated that we had received an agreement to be appointed the Manager of a total of 31 LLCs; in fact, upon review of all of the relevant documents, we now know that we received an agreement to be appointed the Manager of a total of 27 LLCs and to be appointed the General Partner of four limited partnerships ("LPs"). In each case, the Manager of the LLC, as such, has no equity interest or other share of profits or distinctions in the LLC,1 and the General Partner of the LP has no equity interest or other share of profits or distinctions of the LLP.

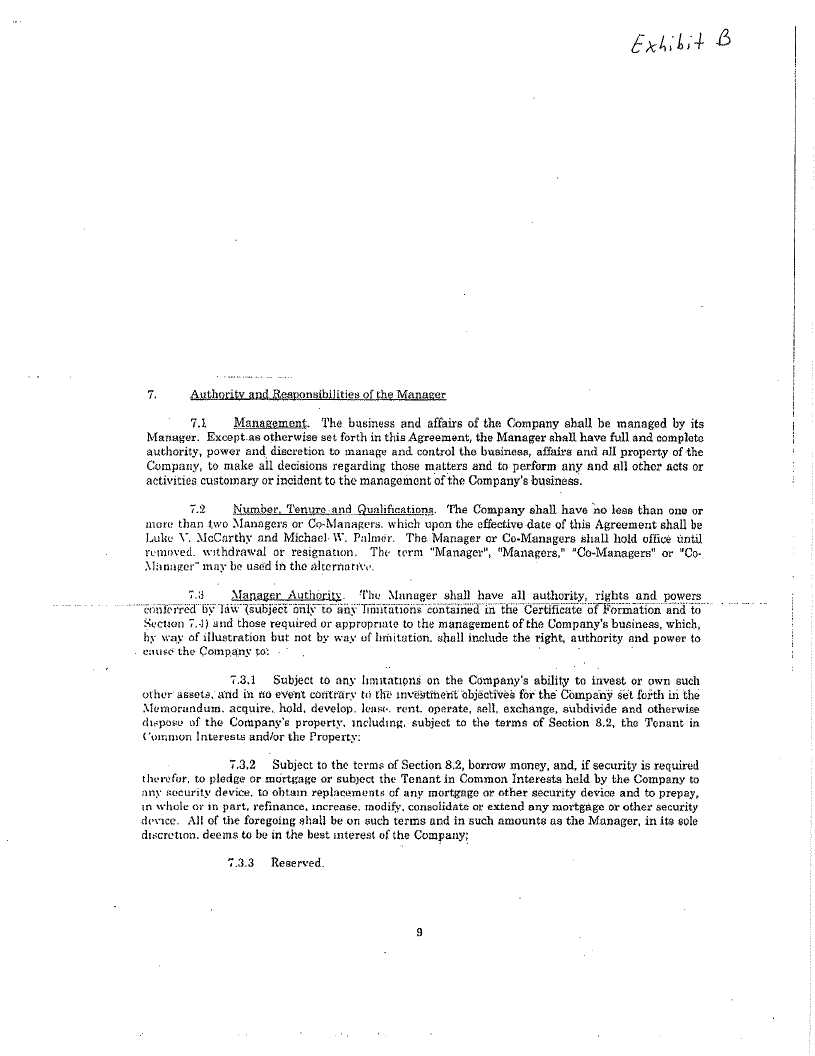

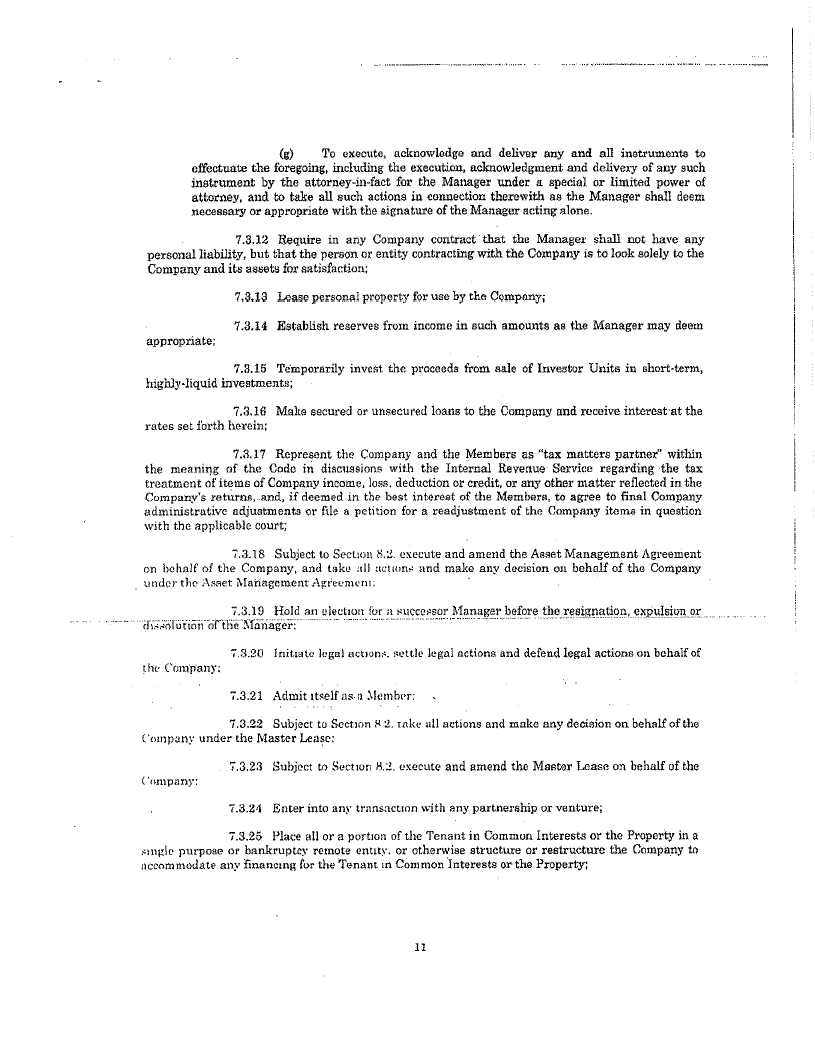

The operating agreements of the 27 LLCs are substantially identical. They provide that the Manager has, with certain enumerated exceptions, "full and complete authority, power and discretion to manage and control the business, affairs and all property of the Company, to make all decisions regarding these matters and to perform any and all other acts or activities customary or incidental to the management of the Company's business." Attached here as Exhibit B is a copy of the Article entitled "Authority and Responsibility of the Manager" excerpted from one of the operating agreements. The corresponding Article in each of the other operating agreements is substantially identical. In addition, the corresponding Article dealing with the authority and responsibility of the General Partner in each of the four limited partnership agreements of the LPs is also substantially identical to Exhibit B.

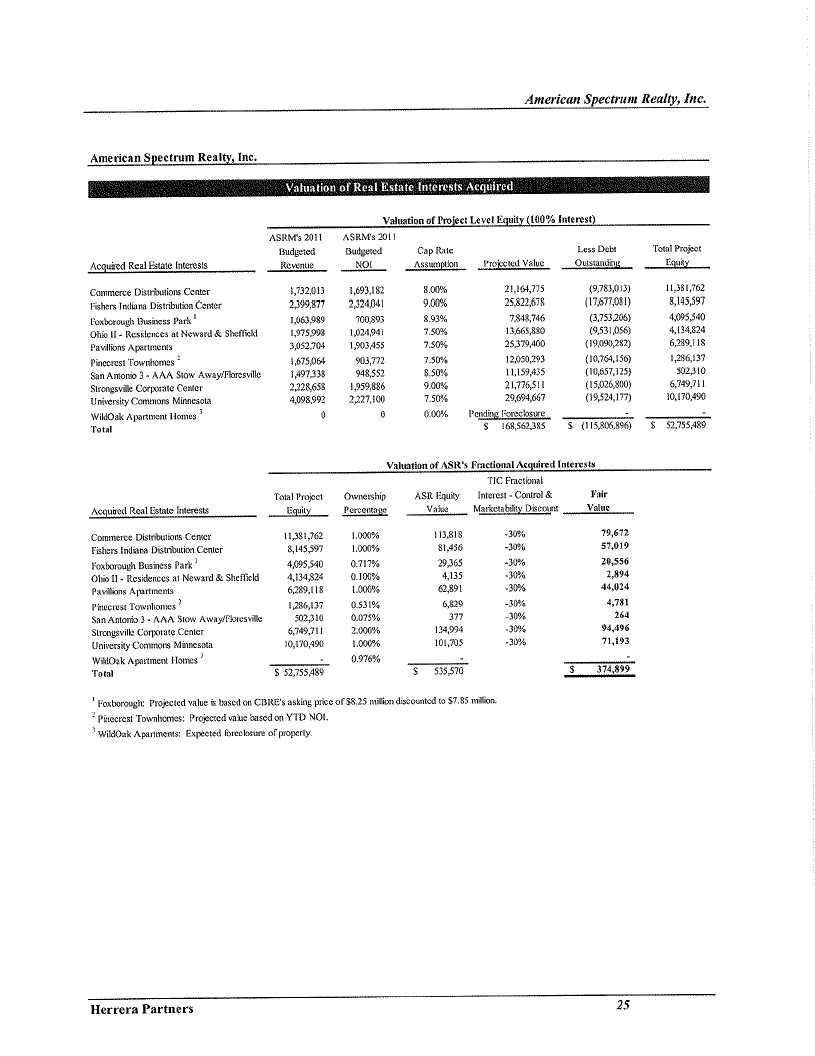

Subcomment (c). We confirm that we hold membership interests in only eight of the LLCs. We have the following percentage interests as equity investments:

| Property | Percentage Interest in Investor LLC | LLC's Percentage Interest in Property | Resulting Net Indirect Interest in Property | |||

| Commerce Distribution Center | 11.2% | 8.9% | 1.0% | |||

| Fishers Indiana Distribution Center | 38.2% | 2.6% | 1.0% | |||

| Ohio II Residences | 4.7% | 2.2% | 0.1% | |||

| Pavilions Apartments | 46.8% | 2.1% | 1.0% | |||

| Pinecrest Townhomes | 40.8% | 1.3% | 0.5% | |||

| Strongsville Corporate Center | 80.3% | 2.8% | 2.2% | |||

| University Commons Minnesota | 21.4% | 4.7% | 1.0% | |||

| Wildoak Apartments | 47.6% | 2.0% | 1.0% | |||

American Spectrum did not reflect its equity investments in these particular entities during the relevant dates in 2010 because it had regarded its equity interests as immaterial. The Company will account for its investment in these LLCs using the equity method. The total value of these interests is $354,079, as indicated in our response to Comment 4 below. Although one LLC is 80.3% owned, the Company intends to use the equity method for all of the LLC interests because the interests are so small as to be immaterial.

Ms. Cicely LaMothe

February 25, 2011

Page 3

American Spectrum does not have any plans to acquire membership interests in other LLCs, but it may do so in the future on a case-by-case basis if it determines that it makes economic sense to do so.

Subcomment (d). The property management agreements for the tenant-in-common properties provide that a successor property manager can be appointed only by all of the tenants-in-common, unanimously. Therefore, possessing control over one tenant-in-common will, as a practical matter, generally enable American Spectrum to block an attempt to appoint a successor property manager for the property owned by a tenant-in-common group. American Spectrum did not assign a value to this ability independent of its valuation of the underlying property management agreements, as this ability was taken into account and included in our valuation of the property management agreements.

Subcomment (e). The Manager (or the General Partner in the case of the LPs) may be removed for cause by a majority in interest of the Members or the Limited Partners), and without cause by 75%-in-interest of the Members (or the Limited Partners). For this purpose, "cause" is generally defined as gross negligence, fraud, malfeasance, misconduct or willful breach.

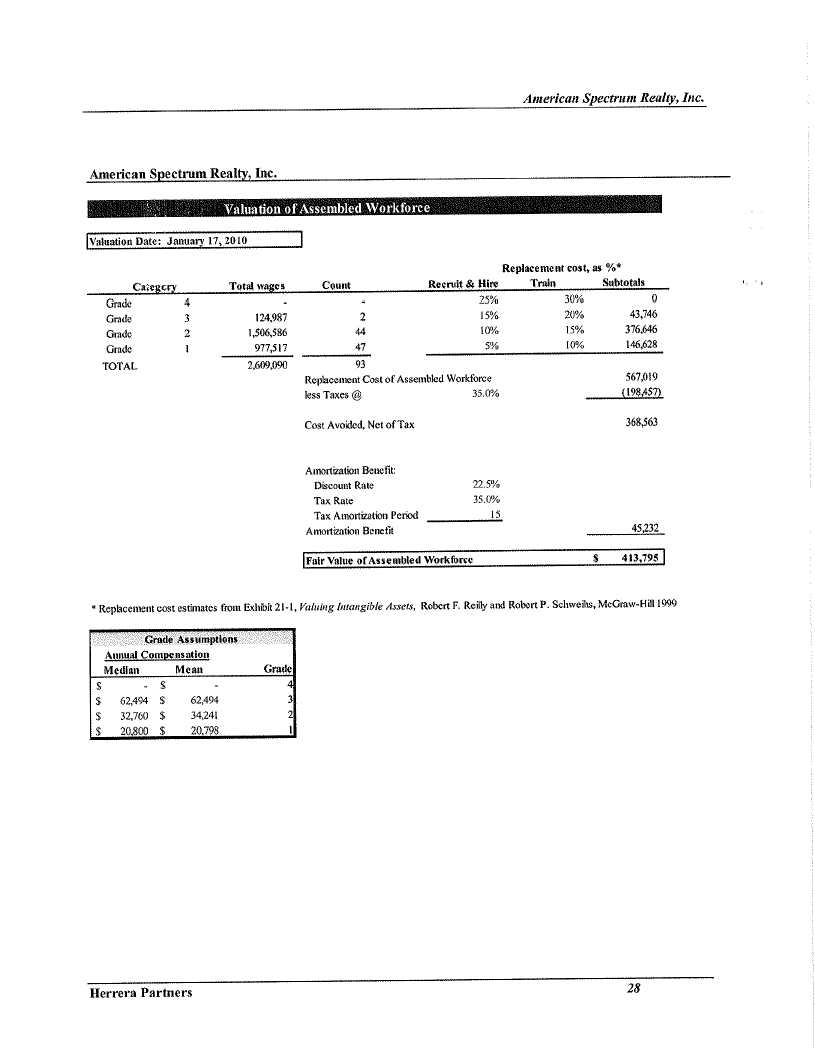

Comment 2 – Valuation of Workforce:

American Spectrum has adopted the valuation of the assembled workforce set forth in the Herrera Report, which found the value of the workforce to be $413,795.

Comment 3 – Consents from Tenants-in-Common:

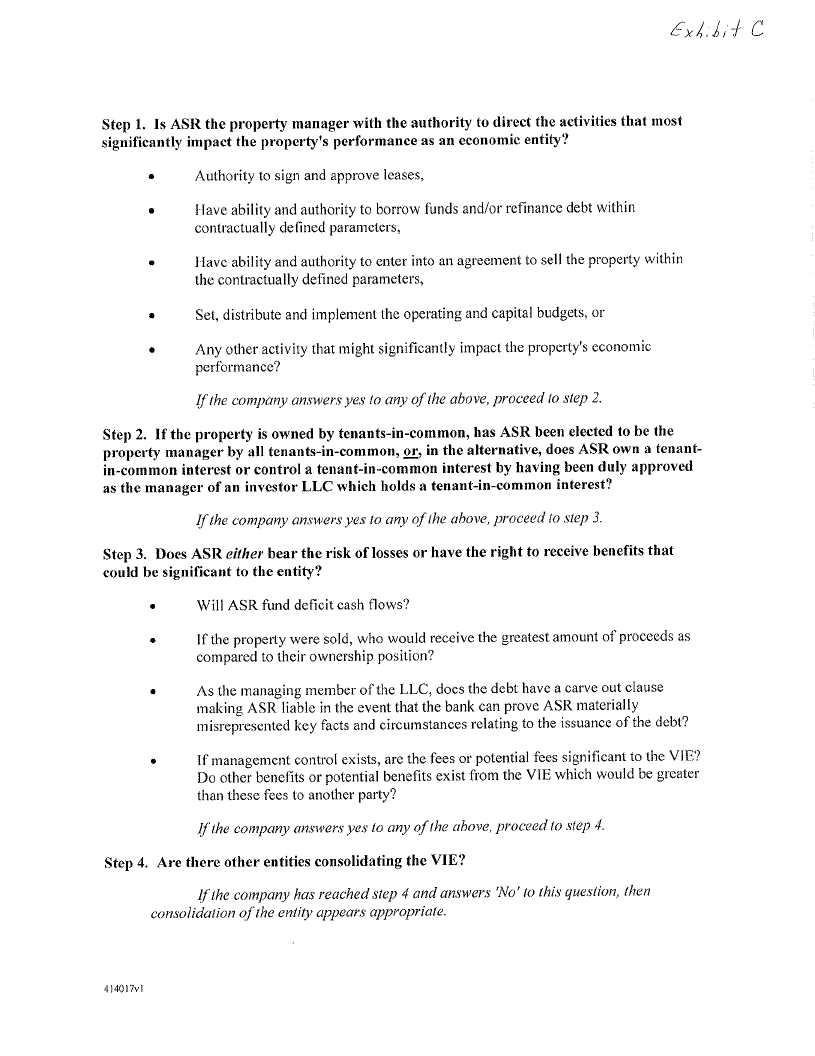

A change from subcontractor to direct property manager as the required consents are obtained will not necessarily have accounting consequences other than potentially affecting our consideration of variable interests. Our criteria for determining consolidation of variable interest entities is attached hereto as Exhibit C.

Comment 4 – Valuation of Property Interests:

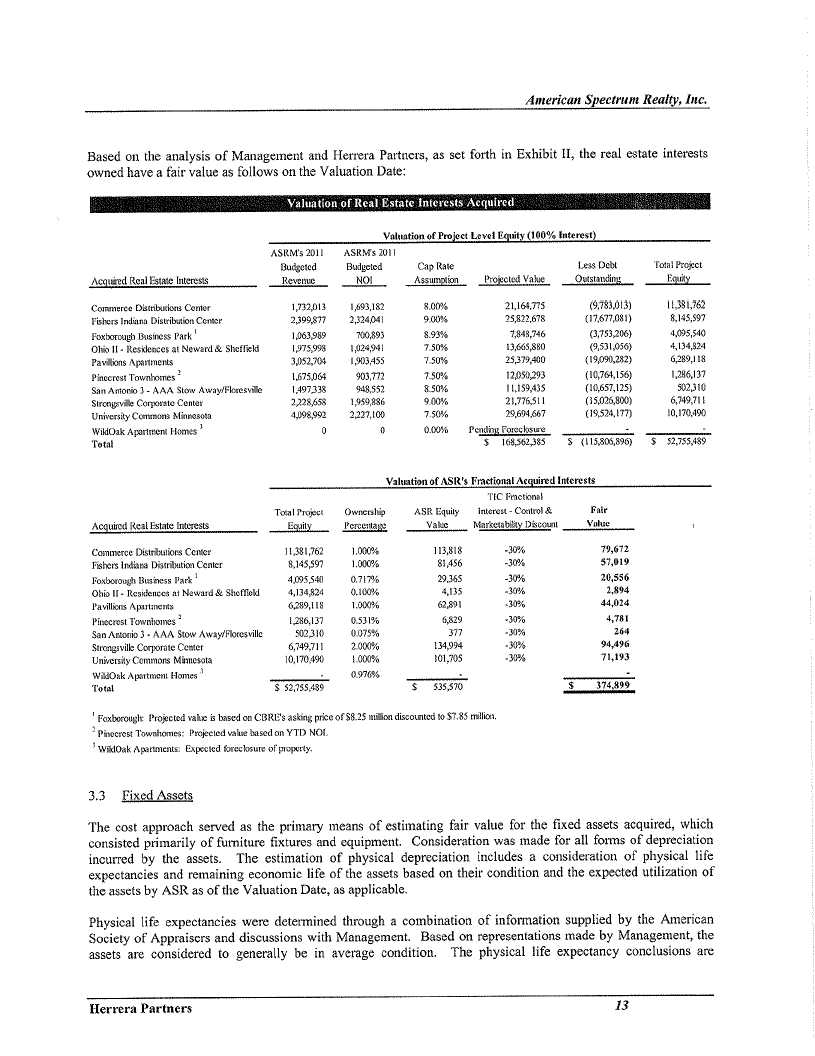

We have adopted the findings of the Herrera Report with respect to the valuation of the eight LLC interests, which the Herrera Report values as if they were indirect real property interests. In accordance with the Herrera Report, they are valued at a total of $354,079, as indicated as the table set forth on page 13 of the Herrera Report.2

Ms. Cicely LaMothe

February 25, 2011

Page 4

Comment 5 – Consents from LLC Members; Consolidation:

The Company acquired the right to manage 31 LLCs, subject to approval by a majority in interest of the members of the LLCs. As of March 31, 2010, we had received approval from a majority in interest of the investors of one LLC to become the manager; as of June 30, 2010, we had acquired approvals for an additional 16 LLCs; as of September 30, 2010, we had acquired approvals for an additional four LLCs, for a total of 21.

As of the dates of these approvals, the Company deemed the properties in which those LLCs had an ownership interest to meet the criteria set forth through Step 2 of its criteria for consolidation of VIEs set forth in Exhibit C. It did not have all relevant facts at these dates, however, to determine whether the properties met the criteria set forth in Step 3. It has subsequently obtained and analyzed those facts and made a determination in the fourth quarter of 2010 as to which properties it would consolidate. That determination will be reflected in the Company's audited financial statements for the year ended December 31, 2010.

Comment 6 – Revised Disclosure:

Our proposed disclosure is as follows:

"In January 2010, the Company acquired the property management and asset management contracts held by Evergreen Realty Group, LLC and affiliates ("Evergreen") for a total of 80 separate properties, pending receipt of all required approvals for the acquisition; until such approvals are received, the Company is managing the properties and assets under subcontract from Evergreen. The Company also acquired from Evergreen (i) Evergreen's interest as the manager of limited liability companies which have invested in 27 of the managed properties (in eight of which it has also acquired an equity interest); (ii) Evergreen's interest as the general partner of limited partnerships which have invested in four of the managed properties (in none of which it acquired an equity interest), and (iii) direct tenant-in-common interests in two properties."

Comment 7 – Useful Life of Management Agreements:

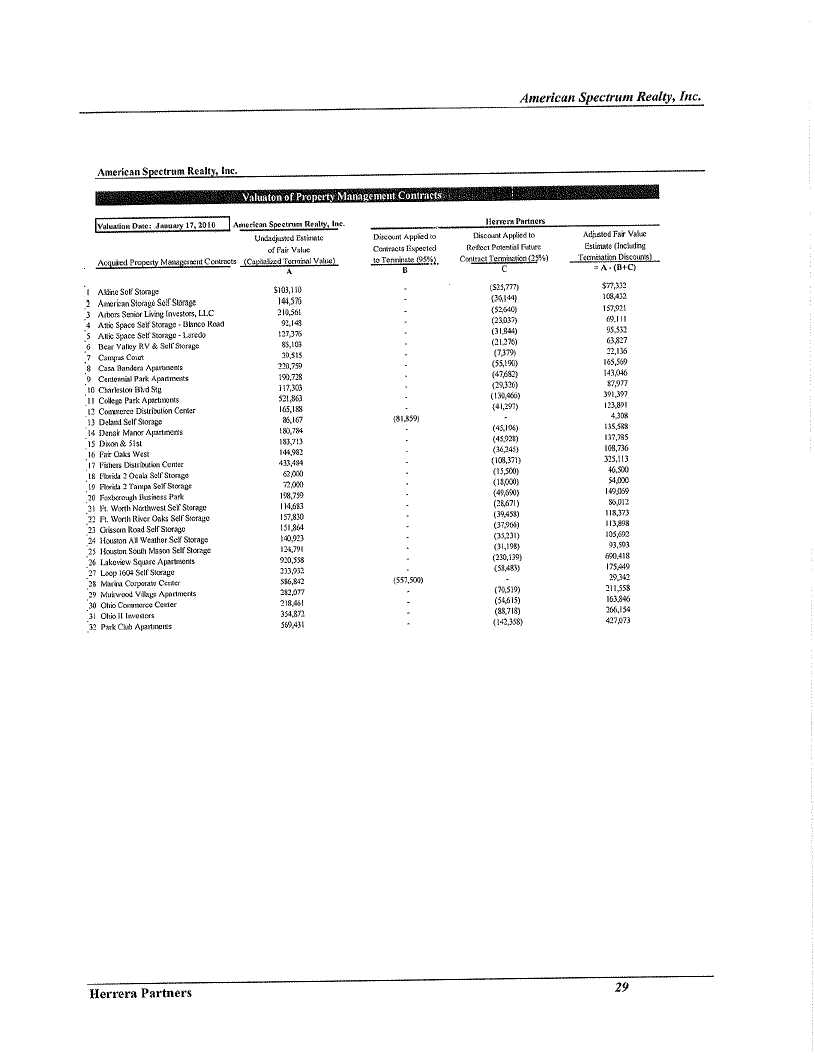

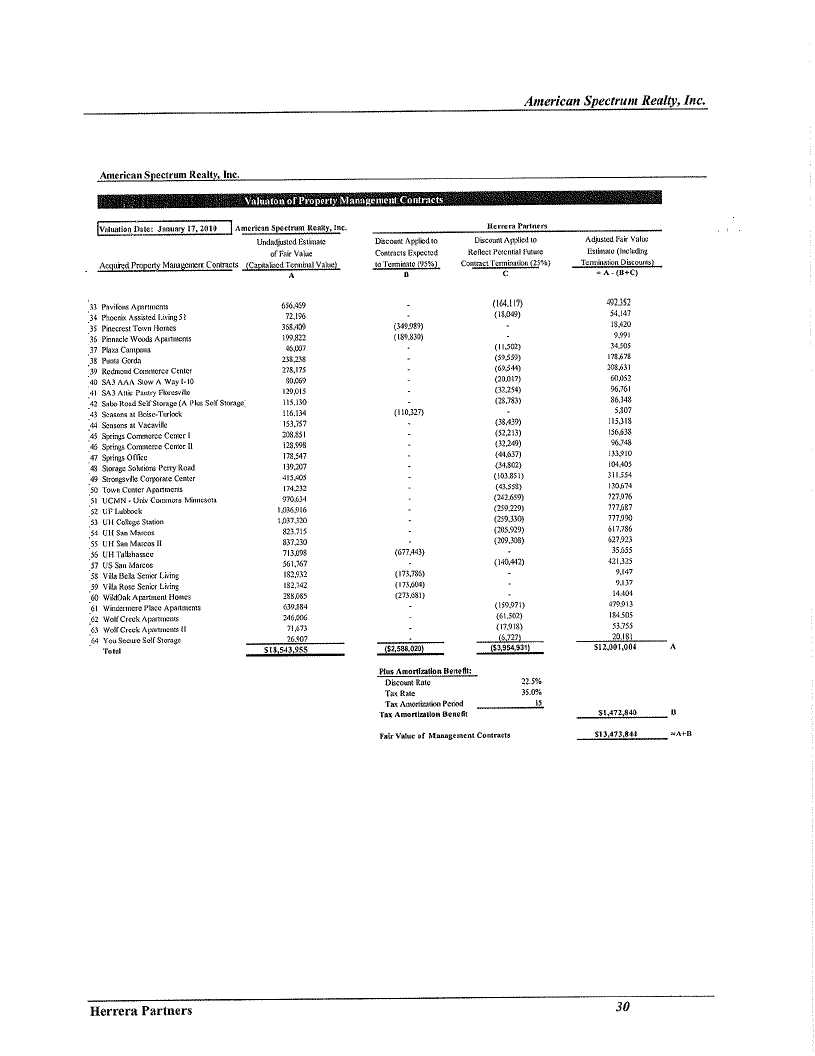

American Spectrum has adopted the findings of the Herrera Report as to the valuation of the management agreements ($13,473,844) and their useful life (12 years). We have also adopted its findings as to the allocation of the $18,000,000 Evergreen purchase price generally.

Comment 8 – Impact of Revised Amortization Schedule:

The adoption of the Herrera Report's findings as to valuations and useful lifes would have the impact on the June 30 and September 30 financial statements shown on Exhibit D hereto. With one exception, the Company's income statement line items, including losses from continuing operations, would have changed less than 10% for all such periods if the Company had recorded the applicable depreciation and amortization expense in each of the periods presented in its prior filings. In regards to the exception, net income attributable to the Company would have changed more than 10% for the three months ended March 31, 2010 and for the six months ended June 30, 2010, due to a gain from discontinued operations recorded the first quarter of 2010. The income generated from the discontinued operations caused the Company to have net income for the first quarter of 2010. Since the change in all of the Company's other income statement line items, including losses from continuing operations, would have been less than 10% for all prior periods presented and due to the fact that depreciation and amortization is considered a non-fund expense, we believe that the Company's financial statements, when taken as a whole, would not have been materially misstated for any prior periods previously presented, and as such we propose to catch up the depreciation and amortization that would have been recorded in the prior quarters in the Company's upcoming Form 10-K for the year ended December 31, 2010.

______________

Ms. Cicely LaMothe

February 25, 2011

Page 5

Thank you for your consideration of these responses. If you have any further questions or believe that further discussion is appropriate, we would be happy to meet with you at your earliest convenience in order to facilitate a prompt resolution of your comments. As you are aware, we must file our 10-K by March 31 and look forward to prompt resolution of your comments so that we may do so.

Sincerely yours, /s/ Anthony Eppolito Anthony Eppolito Chief Financial Officer |

| cc: | Yolanda Crittendon |

William J. Carden

Chip Werlein

Howard F. Hart