Exhibit 99.2VALCENT PRODUCTS INC.

THE ATTACHED UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS DATED DECEMBER 31, 2008 FORM AN INTEGRAL PART OF THIS MANAGEMENT DISCUSSION AND ANALYSIS AND ARE HEREBY INCLUDED BY REFERENCE

Management Discussion and Analysis as of March 2, 2009

By certificate of amendment dated April 15, 2005, we changed our name from Nettron.com, Inc. to Valcent Products Inc. to reflect a newly adopted business plan. On May 3, 2005 we delisted from the TSX Venture Exchange, maintaining only our OTC Bulletin Board listing as a foreign issuer and changed our symbol to “VCTPF”. Effective May 3, 2005, and in order to render our capital structure more amenable to contemplated financing, we effected a consolidation of our common shares on a one-for-three-basis. Unless otherwise noted, all references to the number of common shares are stated on a post-consolidation basis. Our common share authorized share capital remains unlimited. All amounts are stated in Canadian dollars unless otherwise noted.

Fundamental Transaction

On August 5, 2005, we completed a licensing agreement with Pagic LLP, formerly MK Enterprises LLC, (“Pagic”) for the exclusive worldwide marketing rights to certain potential products and a right of first offer on future potential products.

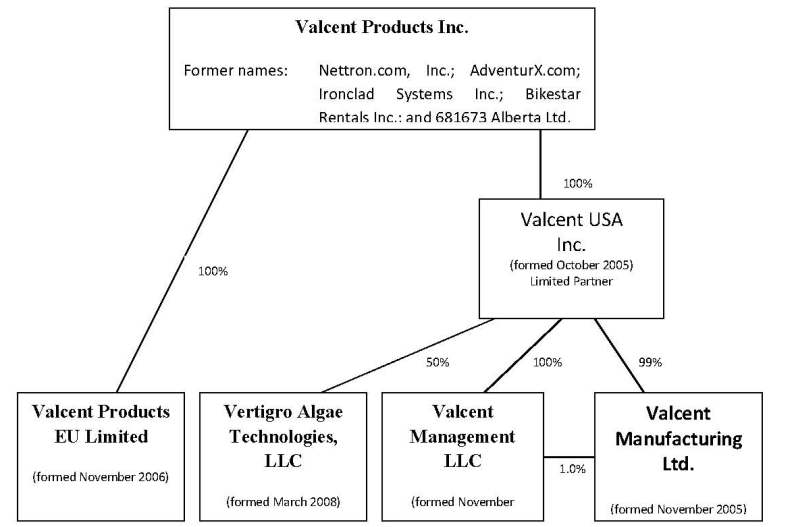

On October 19, 2005, we incorporated Valcent USA, Inc., as a wholly-owned subsidiary under the laws of the State of Nevada. In turn, Valcent USA, Inc. incorporated Valcent Management, LLC, a wholly-owned limited liability company under the laws of the State of Nevada, to serve as the general partner in Valcent Manufacturing Ltd., a limited partnership also formed by Valcent USA, Inc., under the laws of the State of Texas, wherein Valcent USA, Inc. serves as limited partner, in order to conduct operations in Texas.

During the year ended March 31, 2007, the Company incorporated Valcent Products EU Limited in England to conduct operations and development initiatives in Europe.

We are, at present, a development stage company focused primarily on:

| (i) | the development of a commercial bio-diesel feed stock technology via a formalized corporate joint venture with Global Green Solutions, Inc. (“Global Green”), |

| (ii) | the development of our “High Density Vertical Growth System” designed to produce vegetables and other plant crops, and |

| (iii) | the development and marketing of the Tomorrow GardenTM consumer retail product in our UK based subsidiary. |

From inception, we have generated minimal revenues and experienced negative cash flows from operating activities and our history of losses has resulted in our continued dependence on external financing. Any inability to achieve or sustain profitability or otherwise secure additional external financing, will negatively impact our financial condition and raises substantial doubts as to our ability to continue as a going concern.

Organizational Structure

The following organizational chart sets forth our current corporate structure and reflects subsidiary interests relating to our various entities.

Corporate History

We were incorporated in accordance with the provisions of the Business Corporations Act (Alberta) on January 19, 1996, as 681673 Alberta Ltd., later changed to Ironclad Systems Inc. Beginning in 1996, following the completion of a public offering, our common shares began trading as a junior capital pool company on the Alberta Stock Exchange (later becoming part of the Canadian Venture Exchange, which was thereafter acquired and renamed the TSX Venture Exchange).

On May 8, 1999, while still operating our bicycle rental and eco-tour businesses through Bikestar Rentals Inc., we incorporated Nettron Media Group Inc., a wholly-owned subsidiary under the laws of the State of Texas, as a marketing enterprise focusing on products and services that could be effectively marketed through internet as well as more traditional business channels. Nettron Media Group Inc.’s primary focus was Cupid’s Web, an interactive online dating and marketing service. We also changed our name from Bikestar Rentals Inc. to AdventurX.com, Inc., and later to Nettron.com, Inc.

In 2000, and in connection with Cupid’s Web, we signed an agreement in principle to acquire all of the outstanding capital stock of a group of companies operating a worldwide dating service franchise, as well as a collection of dating magazines and websites.

On January 1, 2001, in order to fully focus on our interactive dating and marketing services, we disposed of all of the outstanding capital stock of Arizona Outback Adventures LLC and Bikestar Rentals Inc.

On February 18, 2002, due to general weakness in the equity markets, we terminated the agreement in principle to acquire the dating service franchise and related businesses originally entered into in 2000. On March 24, 2004, we disposed of our interest in Nettron Media Group Inc. and began exploring business opportunities that might allow us to restart commercial operations.

By certificate of amendment dated April 15, 2005, we changed our name from Nettron.com, Inc. to Valcent Products Inc. to reflect a newly adopted business plan. On May 3, 2005 we delisted from the TSX Venture Exchange, maintaining only our OTC Bulletin Board listing and changing our symbol to “VCTPF”. Effective May 3, 2005, and in order to render our capital structure more amenable to contemplated financing, we effected a consolidation of our common shares on a one-for-three-basis. Unless otherwise noted, all references to the number of common shares are stated on a post-consolidation basis.

On August 5, 2005, we completed a licensing agreement with Pagic LLP for the exclusive worldwide marketing rights to certain potential products and a right of first offer on future potential products.

In order to facilitate the business plan, the company formed a wholly-owned Nevada corporation, Valcent USA, Inc. to conduct operations in the United States in November 2006. In turn, Valcent USA, Inc. incorporated Valcent Management, LLC, and a wholly-owned limited liability corporation under the laws of Nevada, to serve as the general partner in Valcent Manufacturing Ltd., a limited partnership also formed by Valcent USA, Inc., under the laws of Texas, wherein Valcent USA, Inc. serves as its limited partner. Valcent Products EU Limited was incorporated by Valcent Products Inc. in the domicile of England to conduct future anticipated operations in Europe. Valcent Vertigro Algae Technologies, LLC, a Delaware limited liability corporation was formed as a 50% owned subsidiary to each of Valcent, USA Inc. and Global Green Solutions Inc. to develop algae related technologies.

Current License Agreements

On July 29, 2005, we entered into five related definitive agreements (the “Pagic Agreements”) with Pagic LP (formerly MK Enterprises LLC), an entity controlled by Malcolm Glen Kertz, our current Chief Executive Officer, acting President, Chairman and a member of our board of directors, including:

| | (i) | a master license agreement for a term continuing so long as royalty payments continue to be made as required for the exclusive worldwide marketing and distribution rights to three unrelated and proprietary potential consumer retail products that had previously been developed (the “Pagic Master License”), certain of which are patent pending by Pagic, including the Nova Skin Care System, the Dust WolfTM, and the Tomorrow GardenTM Kit (collectively, and together with any improvements thereon, the “Initial Products”); |

| (ii) | the Pagic Master License also includes a license for a term continuing so long as royalty payments continue to be made as required for the exclusive worldwide marketing and distribution rights to any ancillary products developed and sold for use by consumers in connection with the Initial Products (the “Initial Ancillaries”); |

| (iii) | a product development agreement pursuant to which we were granted a right for an initial period of five years to acquire a license for a term continuing so long as royalty payments continue to be made as required for the exclusive worldwide marketing and distribution rights to any new products developed by Pagic (any such products, collectively, the “Additional Products”, and, the agreement itself, the “Pagic Product Development Agreement”); |

| (iv) | the Pagic Product Development Agreement also includes a license for a term continuing so long as royalty payments continue to be made as required for the exclusive worldwide marketing and distribution rights to any ancillary products developed and sold for use by consumers in connection with the Additional Products (the “Additional Ancillaries”); and |

| (v) | a related services agreement pursuant to which Pagic shall provide consulting support in connection with the Initial Products, the Initial Ancillaries, the Additional Products and the Additional Ancillaries (the “Pagic Consulting Agreement”), in exchange for the following: |

| 1) | 20,000,000 shares of our common stock which have been issued; |

| 2) | a one-time US$125,000 license fee (paid); |

| 3) | reimbursement for US$125,000 in development costs associated with each of the Initial Products since March 17, 2005 (paid); |

| 4) | consulting fees of US$156,000 per year, payable monthly in advance, which the Company has paid to date; and |

| 5) | the greater of the following, payable annually beginning in the second license year (beginning April 1, 2007): |

(i) US$400,000 inclusive of all consulting fees, royalty and other fees; or

(ii) the aggregate of the following:

subject to a minimum amount of US$37,500 per Initial Product during the second year of the Pagic Master License, and $50,000 US$ each year thereafter, continuing royalties payable quarterly at a rate of:

| Ø | US$10.00 US per Nova Skin Care System unit sold; |

| Ø | US$2.00 per Dust WolfTM unit sold; |

| Ø | 4.5% of annual net sales of the Tomorrow GardenTM Kit; and |

| Ø | 3% of annual net sales of Initial Ancillaries. |

| 6) | a one-time $50,000 US license fee for each Additional Product licensed (except for one pre-identified product); and |

| 7) | subject to a minimum amount of US$50,000 per year commencing with the second year of each corresponding license, continuing royalties of 4.5% of annual net sales and 3% on annual net sales of any Additional Ancillaries. |

Beginning on October 2, 2006, we granted certain rights to Global Green relating to our joint venture of our high density vertical bio-reactor technology named “Vertigro”, an algae based bio-diesel feedstock initiative. Refer to “PLAN OF OPERATIONS, “High Density Vertical Bio-Reactor and Global Green Joint Venture”, and “Technology License Agreement” between Pagic LP, West Peak Ventures of Canada Ltd., and Valcent Products, Inc.

On May 5, 2008, Vertigro Algae executed a Technology License Agreement (“Technology License”) together with Pagic, West Peak, and the Company’s subsidiary, Valcent, USA Inc. The Technology License licenses certain algae biomass technology and intellectual property to Vertigro Algae for purposes of commercialization and exploitation for all industrial, commercial, and retail applications worldwide “Algae Biomass Technology”.

On September 26, 2008, the Company and Global Green entered in to an agreement for the Company to purchase Global Green’s entire interest in Vertigro Algae for US$5,000,000 and 5,000,000 restricted shares in the capital of the Company (“Vertigro Algae Purchase Agreement”). The agreement is subject to finance and under further negotiation for extension. The agreement is subject to finance and its completion has been extended to March 25, 2009 or as further agreed by the parties. Although the parties to the Vertigro Algae Purchase Agreement have extended the closing of this agreement, the unavailability of financing may prevent completion. As a result, the Company continues to accrue amounts due from Global Green according to pro rata ownership per that required under the New Operating Agreement.

PLAN OF OPERATIONS

From inception we have generated minimal revenues from our business operations and have traditionally met our ongoing obligations by raising capital through external sources of financing.

At present, we do not believe that our current financial resources are sufficient to meet our working capital needs in the near term or over the next twelve months and, accordingly, we will need to secure additional external financing to continue our operations. We anticipate raising additional capital though further private equity or debt financings and shareholder loans. If we are unable to secure such additional external financing, we may not be able to meet our obligations as they come due or to fully implement our intended plan of operations, as set forth below, raising substantial doubts as to our ability to continue as a going concern.

In addition, we have recently reduced staffing at our El Paso offices and research facility, transferring our primary development directives previously located there to our UK offices.

Our plan of operations over the course of the next twelve months, subject to adequate financing, is to focus primarily on the continued development, marketing and distribution of our lines of potential consumer retail products, our high density vertical vegetable growing systems (“HDVG System”), and the development via joint venture of our high density vertical bioreactor technology named “Vertigro”, an algae based bio-diesel feedstock initiative. In connection therewith and for each of our potential product lines:

• Glen Kertz, our President and CEO is responsible for overseeing all company department development initiatives while heading Vertigro and HDVG System research, design, and development as well as new product research and development initiatives including tissue culture and plant growth stimulator technologies. Mr. Glen Kertz also manages intellectual property, trademarks, and patents relating to out various technologies and products;

• Chris Bradford, our Managing Director, Valcent Products EU Limited, is responsible for UK business operations and the Company’s “Tomorrow GardenTM” retail plant sales initiative, as well as development of European based HDVG System market development and sales rollout; and

More specifically, our plan of operations with respect to each of our lines of potential consumer retail products and commercial bio-diesel feed stock initiative is provided as follows:

High Density Vertical Bio-Reactor and Global Green Joint Venture

We are in the development stages of creating technology for a High Density Vertical Bio-Reactor (“Vertigro Project”). The objective of this technology is to produce a renewable source of bio-diesel by utilizing the waste gas of carbon dioxide capable of growing micro-algae. Our High Density Vertical Bio-Reactor is configured in a manner intended to promote the rapid growth of various forms of micro-algae which is later processed to remove volatile oils suitable for the production of bio diesel or other fuels. The design of our technology allows the reactors to be stacked on a smaller foot print of land than traditional growing methods require. We believe a secondary potential markets for this technology include industrial, commercial and manufacturing businesses that produce carbon dioxide emissions. We hope to launch this technology in 2009, however, this date may be delayed for several reasons, including but not limited to the availability of financing and delays in the successful or economically viable development of the technology.

On October 2, 2006, the Company entered into a letter agreement replaced on July 9, 2007 by the Vertigro Algae Stakeholders Letter of Agreement, (together “LOA”) with Pagic, West Peak Ventures of Canada Limited (“West Peak”) and Global Green, whereby Global Green agreed to fund the next phase of the development of a high density vertical bio-reactor technology. Pursuant to the LOA, the Company and Global Green established a commercial joint venture named “Vertigro” in which Global Green agreed to provide up to US$3,000,000 in initial funding to continue the research and development of the bio-reactor technology, construct a working prototype of the bio-reactor and develop the technology for commercial uses. The Company is obligated to provide product support, research and development, and the non-exclusive use of the Company’s properties and lands for which Global Green has agreed to reimburse the Company as part of its US$3,000,000 initial funding commitment. Until such time as the joint venture has fully repaid to Global Green the US$3,000,000, Global Green shall receive 70% of the net cash flow generated by anticipated future operations after which each of Global Green and the Company will hold a 50% interest in the Vertigro, subject to an aggregate 4.5% royalty to Pagic and West Peak. Vertigro covers the bio-reactor technology and any subsequent related technologies for the commercial scale products of algae based biomass for all industrial commercial and retail applications including, but not limited to bio-fuel, food, health, pharmaceutical, and animal and agricultural feeds.

Global Green and the Company have completed negotiations and documentation of a formal business arrangements to streamline and enhance Vertigro operating and commercial development systems via a Limited Liability Company Operating Agreement discussed more fully below, and has incorporated a business entity to advance further project development. As a result, the Company incorporated Vertigro Algae Technologies, LLC under the Texas Business Organizations with Global Green Solutions, and other related parties to the Vertigro joint venture. The members of the new Texas LLC are Global Green Solutions, Inc. and the Company, each holding 3 million units. It is anticipated that the Vertigro Algae Technologies, LLC will continue to conduct research and development of the Vertigro growing systems, the development of a commercial scale build out of an operating unit in conjunction with increasing the yield per acre of the algae oil produced by the system.

Limited Liability Company Operating Agreement for Vertigro Algae Technologies, LLC

On May 5, 2008, Valcent USA and Global Green signed a Limited Liability Company Operating Agreement (“New Operating Agreement”) replacing the LOA to form Vertigro Algae Technologies, LLC (“Vertigro Algae”), a Texas LLC, which is the formalized operating entity for the previous unincorporated operations of Vertigro. The business activities of Vertigro Algae will be the same as when the operations were under Vertigro. Under the New Operating Agreement, Global Green and Valcent will each hold a 50% stake in Vertigro Algae, and have committed to fund project development according to ownership allocation. Further, Valcent will acquire assets of Vertigro, including buildings, laboratory, and equipment. To allow for prior capital contributions, Global Green has incurred in excess of the Company’s prior aggregate capital contribution, Global Green will receive 70% of the net cash flow generated by Vertigro Algae until it has received US$3,000,000 in excess of its 50% interest in such cash flow.

On September 26, 2008, the Company and Global Green entered in to an agreement for the Company to purchase Global Green’s entire interest in Vertigro Algae for US$5,000,000 and 5,000,000 restricted shares in the capital of the Company (“Vertigro Algae Purchase Agreement”). The agreement is subject to finance and its completion has been extended to March 25, 2009 or as further agreed by the parties. Although the parties to the Vertigro Algae Purchase Agreement have extended the closing of this agreement, the unavailability of financing may prevent completion. As a result, the Company continues to accrue amounts due from Global Green according to pro rata ownership per that required under the New Operating Agreement.

In addition, due to the recent reduction of staffing at our El Paso research facility, the Company is negotiating for the continued development of the Company’s algae program in Europe.

Technology License Agreement

On May 5, 2008, Vertigro Algae executed a Technology License Agreement (“Technology License”) together with Pagic, West Peak and the Company. The Technology License licenses certain algae biomass technology and intellectual property to Vertigro Algae for purposes of commercialization and exploitation for all industrial, commercial, and retail applications worldwide (“Algae Biomass Technology”). In return for the Algae Biomass Technology, both the Company and Global Green will each issue 300,000 common shares to Pagic, and also pay a one-time commercialization fee of US$50,000 upon the Algae Biomass Technology achieving commercial viability. The Technology License is subject to royalty of 4.5% of gross customer sales receipts for use of the Algae Biomass Technology; and aggregate annual royalty minimum amounts of US$50,000 in 2009, US$100,000 in 2010, and US$250,000 in 2011 and each year thereafter in which the Technology License is in place. The Company issued the 300,000 common shares due to Pagic on August 18, 2008 at a value of $190,746.

All prior agreements between the Company and Pagic that relate to the Algae Biomass Technology will be replaced by the new Operating Agreement and the Technology License.

High Density Vertical Growth System

Valcent Products Inc. has also introduced the HDVG System intended to grow a wide variety of crop products. The Company is experimenting with vegetable crops utilizing the growing system within its greenhouse production plant in El Paso, Texas.

HDVG System Technology – Concept and Advantages: The HDVG System technology provides a solution to rapidly increasing food costs caused by transportation/fuel costs spiraling upwards with the cost of oil. Together with higher cost comes a reduction in availability and nutritional values in the food we consume. The HDVG system is designed to grow vegetables and other foods much more efficiently and with greater food value than in agricultural field conditions. The HDVG System demonstrates the following characteristics:

| | · | Produces substantially more production volume for field crops |

| | · | Requires substantially less than normal water requirements for field crops |

| | · | Can be built on non arable lands and close to major city markets |

| | · | Can work in a variety of environments: urban, suburban, countryside, desert etc. |

| | · | Can be designed not use herbicides or pesticides |

| | · | It is expected to drastically reduce transportation costs to market resulting in further savings; higher quality and fresher foods on delivery, and less transportation pollution |

| | · | Will be easily scalable from small to very large food production situations |

The HDVG System grows plants in closely spaced pockets on clear, vertical panels that are moving on an overhead conveyor system. The system is designed to provide maximum sunlight and precisely correct nutrients to each plant. Ultraviolet light and filter systems may exclude the need for herbicides and pesticides. Sophisticated control systems gain optimum growth performance through the correct misting of nutrients, the accurate balancing of PH and the delivery of the correct amount of heat, light and water.

System Advantages

| | | Reduced global transport and associated carbon emissions |

| | | Food and fuel safety, security and sovereignty |

| | | Local food is better for public health |

| | | Building local economies |

| | | Control of externalities and true costs |

In a rapidly urbanizing world where the majority of people now live in cities, localization requires that food and fuel be produced in an urban context. At present, there are no examples of a locally sustained urban community anywhere in the world. Urban sustainability is yet to be realized primarily because urban agriculture presents a number of technological challenges. The main challenge is a lack of growing space.

Vertical growing is a new idea currently emerging in the sustainability discourse which offers great promise for increasing urban production. Vertical growing systems have been proposed as possible solutions for increasing urban food supplies while decreasing the ecological impact of farming. The primary advantage of vertical growing is the high density production it allows using a much reduced physical footprint and fewer resources relative to conventional agriculture. Vertical growing systems can be applied in combination with existing hydroponics, and greenhouse technologies which already address many aspects of the sustainable urban production challenge (i.e., soil-free, organic production, closed loop systems that maximize water and nutrient efficiencies, etc.). Vertical growing, hydroponics and greenhouse production have yet to be combined into an integrated commercial production system, but, such a system would have major potential for the realization of environmentally sustainable urban food and fuel production.

1/8th Acre HDVG System Commercial Production Model: The Company had been recently developing an HDVG System and specification of a 1/8th acre commercial scale plant capable of defining final operating and capital costs to maximize sales return on cost. Due to lack of financing, the Company has discontinued development of this facility pending the availability of financing to see its completion. All current development relating to the Company’s vertical growing systems are continuing in the Company’s UK offices.

Nova Skin Care System

Our Nova Skin Care System product sales and potential product lines under assessment by management have been suspended pending the availability of financing. Due to limited management and financial resources in combination with the Company’s focus and commitment to Vertigro and HDVG System initiatives, Nova Skin Care Systems development has been formally suspended.

Tomorrow GardenTM

Our Tomorrow GardenTM Kit is an indoor herb garden kit, designed to offer, direct to the consumer, an easy to use kit featuring herbs and plants not otherwise readily available in the marketplace. Glen Kertz, our President, has conducted extensive research in the development, processes and techniques underlying the technology in the Tomorrow GardenTM and based on his research believes that the Tomorrow GardenTM Kit offers an improved plant lifespan of three to six months, as opposed to the traditional shelf life of approximately seven to ten days for fresh herbs, and requires only ambient light, with no watering or other maintenance, to survive. Our Tomorrow GardenTM Plant Kit will be capable of supplying all of the standard herbs traditionally offered in grocery shops today, such as basil, mint, thyme, rosemary, parsley and cilantro, but may, in addition, supply more exotic herbs or pharmaceutical grade plants. Our Tomorrow GardenTM Kit is currently in the design, development, and test sales phase operating out of our offices located in Cornwall, England.

Fluctuations in Results

During the period from March 24, 2004 through the year ended March 31, 2005, we had no meaningful operations and focused exclusively on identifying and adopting a suitable business plan and securing appropriate financing for its execution. As a result of the Company completing a licensing agreement with Pagic for the exclusive worldwide marketing rights to certain potential products and a right of first offer on future potential products during the fiscal year ended March 31, 2006 operating results have fluctuated significantly and past performance should not be used as an indication of future performance.

Valcent Products Inc. [formerly Nettron.Com, Inc.] |

| Selected Financial Data [Annual] |

| (Expressed in Canadian Dollars) |

| | 12 months ended |

| | | 2008 | 2007 | 2006 | 2005 |

| Net Operating Revenues | $ | 0 | 0 | 0 | 0 |

| Loss from operations | $ | 11,605,281 | 7,545,331 | 3,734,600 | 45,694 |

| Loss from prior operations | $ | 0 | 0 | 0 | 45,694 |

Loss from development stage | $ | 3,237,370 | 3,237,370 | 3,734,600 | 0 |

| Net loss per Canadian GAAP | $ | 12,712,358 | 8,138,393 | 3,734,600 | 45,694 |

| Loss per share | $ | 0.36 | 0.42 | 0.35 | 0.01 |

| | | | | | |

| Share capital | $ | 16,691,282 | 8,196,982 | 4,099,870 | 2,999,420 |

| Common shares issued | | 44,276,321 | 30,666,068 | 15,787,835 | 6,435,374 |

| Weighted average shares outstanding | | 35,545,740 | 19,261,192 | 10,548,042 | 6,435,374 |

| Total Assets | $ | 4,605,914 | 4,142,485 | 1,392,801 | 936 |

| Net (liabilities) | $ | (7,674,849) | (4,166,861) | (1,833,900) | (237,950) |

| | | | | | |

Cash Dividends Declared per Common Shares | $ | 0 | 0 | 0 | 0 |

| | | | | | |

Exchange Rates (CDN $ to US $) period average | $ | 1.03304 | 0.8661 | 0.8385 | 0.7824 |

Exchange Rates (CDN $ to British Pound £) period average | $ | 2.07314 | n/a | n/a | n/a |

Selected Quarterly Financial Data

Valcent Products Inc. Selected Financial data [Unaudited] (Expressed in Canadian Dollars) Quarter | Quarter | Quarter | Year | Quarter | Quarter | Quarter | Year |

| | | Ended 12/31/2008 | Ended 09/30/2008 | Ended 06/30/2008 | Ended 03/31/2008 | Ended 12/31/07 | Ended 09/30/07 | Ended 06/30/07 | Ended 03/31/2007 |

| | | | | | | | | | |

| Net Operating Revenues | $ | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Loss from operations | $ | 4,547,838 | 4,077,677 | 3,007,068 | 12,028,222 | 3,482,692 | 2,121,037 | 1,283,819 | 8,171,090 |

| Net loss per Canadian GAAP | $ | 5,566,158 | 4,075,475 | 2,916,081 | 12,028,222 | 3,495,735 | 1,921,261 | 930,968 | 8,171,090 |

| Loss per share from continued operations | $ | 0.109 | 0.09 | 0.06 | 0.36 | 0.10 | 0.06 | 0.03 | 0.42 |

| Share Capital | $ | 20,543,236 | 19,482,091 | 8,620,606 | 16,691,282 | 13,322,958 | 9,333,316 | 9,263,342 | 8,196,982 |

| Common Shares issued | $ | 52,788,932 | 50,274,302 | 48,233,036 | 44,276,321 | 40,228,835 | 33,067,870 | 32,928,193 | 30,666,068 |

| Weighted average shares outstanding | $ | 50,991,403 | 49,056,041 | 46,625,466 | 35,545,740 | 33,437,726 | 33,037,977 | 32,134,177 | 19,261,192 |

| Total assets | $ | 4,001,862 | 4,230,595 | 4,330,428 | 4,605,914 | 4,434,893 | 3,585,751 | 4,520,482 | 4,142,485 |

| Net assets (Liabilities) | $ | (9,776,299) | (5,044,195) | (3,693,115) | (3,068,935) | (2,329,107) | (3,259,327) | (2,019,941) | (24,376) |

| | | | | | | | | | |

| Cash Dividends Declared Per common Shares | $ | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| | | | | | | | | | |

| | | | | | | | | | |

NINE MONTHS ENDED DECEMBER 31, 2008

COMPARED WITH THE NINE MONTHS ENDED DECEMBER 31, 2007

OVERVIEW OF THE NINE MONTHS’S ACTIVITIES:

During the nine months ended December 31, 2008, the Company has focused on (i) the development of a commercial bio-diesel feed stock technology via a joint venture with Global Green (the “Vertigro Project”), (ii) the development of our High Density Vertical Growth System (“HDVG System”) designed to more efficiently produce vegetables and other plant crops, (iii) the development and test marketing of the Tomorrow GardenTM consumer retail product in our UK based subsidiary, (iv) the development of product development initiatives relating to our Nova Skin Care System, and (v) ongoing research and development with tissue culture technologies, and other product and technology development initiatives.

Operating Results

We incurred losses of $12,557,714 ($0.257/share) for the nine months ended December 31, 2008, as compared to $6,347,964 ($0.19/share) for the nine months ended December 31, 2007.

Revenues

As the Company is in the development stage, test sales, bad debts and write-down of inventory related to the Nova Skincare System are included in product development costs. During the nine months ended December 31, 2008, the Company had net sales receipts of approximately $192,142 relating to sales of the Nova Skincare System. As active sales have ceased, accounts receivable relating to the Nova Skin Care System is approximately $16,147. The Company previously wrote down accounts receivable by $138,901 owing to uncertainty of collection. Inventories of raw materials and finished goods have been written down to estimated salvage value in the aggregate value of $116,743.

The foreign exchange loss for the nine months ended December 31, 2008 was $925,131 as opposed to a $539,584 gain for the nine months ended December 31, 2007 due primarily to US currency fluctuations.

Operating Expenses

Product development expenses increased by $3,614,868 to $6,057,847 for the nine months ended December 31, 2008 as compared with the nine months ended December 31, 2007. The increase is due to the larger scale and scope of a) increased Vertigro research and development costs, b) new development initiatives relating to tissue culture research and HDVG System product development, and c) the advent of Valcent EU costs relating to the Tomorrow GardenTM and UK based HDVG System development initiatives. Product development expenses were $2,443,161 during the nine months ended December 31, 2007.

In conjunction with convertible debenture financings during the fiscal year ended March 31, 2008 and in the current fiscal year, the Company incurred $2,897,432 in interest, accretion and financing on convertible notes in the nine month period ended December 31, 2008. This represents a $2,466,308 increase from the $431,124 that had been incurred during the nine months ended December 31, 2007 stemming primarily from accretion and amortization of convertible debenture funding activity during the nine months ended December 31, 2008, as well as increasing interest burden pursuant to large and growing corporate debt instruments both secured and unsecured.

Advertising and media development was $448,418 during the nine months ended December 31, 2008 (2007 $1,372,286) that reflects decreasing stages of marketing development that include infomercial media purchases in connection with test sales initiatives of our Nova Skin Care System. Marketing activity of all kinds has ended, and sales initiatives relating to the Nova Skin Care System have been discontinued to conserve funding for the Company’s core green based technologies.

Professional fees increased by $168,618 to $404,450 for the nine months ended December 31, 2008 from $235,832 for the nine months ended December 31, 2007. The increase is primarily attributable to costs associated with increased business activity relating to intellectual property legal services, executive search services between the respective years, and increasing complexity in accounting and audit services.

Travel expenses increased by $10,160 to $222,066 (2007 - $211,906) for the nine months ended December 31, 2008 as a result of continued activity in all of the Company’s operations, increased number of active development projects, as well as costs relating to an additional subsidiary interest located in the United Kingdom.

Rent expenses increased $60,028 to $103,129 for the nine months ended December 31, 2008 from $43,101 for the nine months ended December 31, 2007. The increase in rent costs incurred relates to our new offices and operations located in the United Kingdom.

Office and miscellaneous expenses increased $187,078 to $373,791 for the nine months ended December 31, 2008 from $186,719 for the nine months ended December 31, 2007. The increase is due to new offices and activity relating to our UK offices and emphasis on multiple project development initiatives in our research facility in El Paso, Texas.

Filing and transfer agent expenses decreased $9,226 to $20,056 for the nine months ended December 31, 2008, from $29,282 for the nine months ended December 31, 2007. The decrease is primarily attributable to lower regulatory filing costs associated with proportionate activity during the nine months ended December 31, 2008 when compared to the same interval in 2007.

Investor relations fees increased $1,020 to $791,950 (2007 - $790,930) for the nine months ended December 31, 2008 as a result of the Company’s continued use of services of third party consultants in advisory, business consulting services, and investor relations activities with the bulk costs paid utilizing non-cash stock based compensation.

As a result of increasing operating capacity and existing and project build out at our El Paso, Texas operation, as well as the development of our new Cornwall, UK offices, the Company’s fixed assets and land had a net book value of $1,683,859 (2007 - $1,135,108) at December 31, 2008, and correspondingly, the Company incurred a higher depreciation and amortization charge of $132,186 (2007 - $34,386) during the nine months ended December 31, 2008 over the same nine month period in 2007.

Net Loss

Our reported loss increased by $6,209,750 to $12,557,714 ($0.257 basic loss per share) for the nine months ended December 31, 2008 as compared to $6,347,964 ($0.190 basic loss per share) for the same period ending December 31, 2007. The increase during the nine months ended December 31, 2008 over the nine months ended December 31, 2007 is largely a result of increasing aggregate expenses associated with increasing scale and scope of product development and marketing initiatives relating to all our projects under development, increasing Company consulting arrangements, as well as expenses our new UK operating offices.

Liquidity and Capital Resources

Because we are organized in Canada, our December 31, 2008 financial statements have been prepared by our management in accordance with Canadian GAAP applicable to a going concern. Our working capital deficit increased to $11,460,159 from $4,153,903, during the nine months ended December 31, 2008 representing a $7,306,256 increase over the year ended March 31, 2008. These interim consolidated financial statements have been prepared in accordance with Canadian generally accepted accounting principles (“GAAP”) applicable to a going-concern, which assumes the realization of assets and the satisfaction of liabilities and commitments in the normal course of business. As at December 31, 2008, the Company had an accumulated deficit of $36,875,353. The Company’s ability to continue as a going-concern is dependent upon the economic development of its products, the attainment of profitable operations, but moreover, the Company’s ability to obtain financing.

These interim consolidated financial statements do not include any adjustments that would be necessary to the carrying values and classification of assets and liabilities should the Company be unable to continue as a going-concern.

During the nine months ended December 31, 2008, the Company,

| · | raised $1,976,564 in net cash proceeds from private placements of units whereby a total of 3,252,666 units were issued at US$0.60. Each unit consists of one common share and one-half common share purchase warrant with each whole warrant exercisable at US$0.75 to purchase an additional common share of the Company; |

| · | issued 4,022,614 common shares upon conversion of US$2,168,438 of convertible notes and interest during the nine months ended December 31, 2008. We raised gross proceeds of US$2,168,000 from the issuance of convertible debentures during the nine months ended December 31, 2008; |

| · | issued 100,000 common shares as part of interest and debt settlement arrangements valued at $65,432; |

| · | issued 754,000 common shares for consulting services valued at $489,602; |

| · | issued 383,331 common shares from the exercise of 383,331 warrants for gross proceeds of $193,331. |

In addition, 1,393,982 warrants exercisable at US$0.40 to US$0.90 per share expiring in July and August 2008 were extended to April 9, 2009, and 2,872,224 warrants expiring in July and August 2009 were extended to December 31, 2008. The warrants with extended terms resulted in a fair value of $632,244 reclassified from share capital to contributed surplus warrants. The 2,872,224 warrants expiring on December 31, 2008 have expired according to their terms.

Our net advances from related parties increased by $1,413,493 during the nine months ended December 31, 2008. Also our advances from third parties increased by $1,622,596.

We purchased $680,937 in fixed assets during the nine months ended December 31, 2008.

Our cash resources increased by $83,944 to $247,381 at December 31, 2008 over the year ended March 31, 2008; we currently have approximately $5,000 in cash as at March 1, 2009.

Accounts receivable as at December 31, 2008 consists of $1,507,024, of which $625,198 (2007 $167,945) is due from the Global Green Solutions Inc. (“Global Green”), the Company’s joint venture partner in the development of the Company’s High Density Vertical Bio-Reactor technology (“Vertigro”); and $787,524 in amounts due pertaining to advances provided on the potential sale of Global Green’s 50% interest in Vertigro Algae, the joint venture company developing Vertigro; $16,147 net of allowance for doubtful accounts of $25,196 from test sales relating to the Company’s Nova Skin Care System; and $78,155 (2007 $38,568) in value added tax is owed to a subsidiary, Valcent Products EU Limited and goods and for services tax receivable by Valcent Products, Inc.

As a result of the cessation of Nova Skin Care System sales and prior and current period impairment of obsolete inventory, our inventories were written down to an aggregate of $116,743 as at December 31, 2008. As previously stated, with the Company’s focus and commitment to Vertigro and HDVG System initiatives, budget for Nova Skin Care System developments has been limited in the current fiscal year, and the Company has proceeded to shut down the product line.

Prepaid expenses as at December 31, 2008 consists of $446,854 (2007 - $2,119,546), $376,995 of which is the deferred portion of investor relations and business consulting services agreements, $60,501 of prepaid rent and equipment deposits relating to the operations of Valcent UK operations, with the balance consisting of $9,358 in prepaid insurance deposits.

All long term debt was repaid in the 6 month period ended December 31, 2008, and cash previously recorded as restricted cash that secured long term debt accounts was returned to general corporate use.

Convertible note continuity: | US $ | CDN $ |

| | Balance | Q1-3 2009 | Q1-3 2009 | Q1-3 2009 | Q1-3 2009 | Balance | Balance |

| | March 31, | Issued | Equity/Warrant | Interest/Accret/ | | Dec. 31, | Dec. 31, |

| Date of Issue | 2008 | Principal | Portions | Penalty | Conversions | 2008 | 2008 |

| | | | | | | | |

| July/August 2005 (Note 10(a)) | $259,825 | - | - | $12,702 | ($101,524) | $171,003 | $209,102 |

| April 2006 (Note 10(b)) | 534,442 | - | - | 18,885 | (441,874) | 111,453 | 136,285 |

| April 2006 (Note 10(c)) | 85,542 | - | - | 3,771 | (64,410) | 24,902 | 30,451 |

| December 2006 (Note 10(e)) | 1,659,782 | - | - | 195,699 | - | 1,855,481 | 2,268,882 |

| January 2007 (Note 10(f)) | 1,569,183 | - | - | 911,722 | (709,995) | 1,770,910 | 2,165,469 |

| August 2007 (Note 10(g)) | 678,567 | - | - | 80,831 | - | 759,398 | 928,592 |

| September 2007 (Note 10(h)) | 297,433 | - | - | 160,616 | - | 458,049 | 560,102 |

| July 2008 (Note 10(i))* | - | 2,168,000 | (1,351,003) | 777,343 | - | 1,594,340 | 1,949,559 |

| | $5,084,774 | $2,168,000 | ($1,351,003) | $2,161,569 | ($1,155,644) | $6,745,537 | $8,248,559 |

| | US $ | CDN $ |

| | Balance | 2008 | 2008 | 2008 | 2008 | Balance | Balance |

| | March 31, | Issued | Equity | Interest / | | March 31, | March 31, |

| Date of Issue | 2007 | Principal | Portion | Penalty | Conversions | 2008 | 2008 |

| | | | | | | | |

| July/August 2005 (Note 10(a)) | $316,957 | - | - | $22,389 | ($79,521) | $259,825 | $265,583 |

| April 2006 (Note 10(b)) | 495,607 | - | - | 38,835 | - | 534,442 | 546,841 |

| April 2006 (Note 10(c)) | 79,115 | - | - | 6,427 | - | 85,542 | 87,527 |

| December 2006 (Note 10(e)) | 670,486 | - | - | 989,296 | - | 1,659,782 | 1,698,289 |

| January 2007 (Note 10(f)) | 813,084 | - | - | 967,767 | (211,668) | 1,569,183 | 1,605,558 |

| August 2007 (Note 10(g)) | - | 650,000 | (230,007) | 258,574 | - | 678,567 | 694,310 |

| September 2007 (Note 10(h)) | - | 391,000 | (213,249) | 119,682 | - | 297,433 | 304,633 |

| | $2,375,249 | $1,041,000 | ($443,256) | $2,402,970 | ($291,189) | $5,084,774 | $5,202,741 |

To provide working capital for product development, during July and August 2005, the Company issued one-year, unsecured US$1,277,200 8% per annum convertible notes and three-year Class A and B warrants to acquire: (i) up to 913,332 common shares of the Company at a price per share of US$0.50; and (ii) up to an additional 913,332 common shares of the Company at a price per share of US$1.00. The holders of the convertible notes may elect to convert the notes into common shares of the Company at the lesser of: (i) 70% of the average of the five lowest closing bid prices for the common stock for the ten trading days prior to conversion; and (ii) US$0.55. Accrued and unpaid interest may be converted into common shares of the Company at US$0.50 per share. The Company may, subject to notice provisions and the common shares trading above US$1.50 per share for more than twenty consecutive trading days, elect to payout the notes and interest due by paying 130% of the amount due under the notes plus interest. The common stock purchase warrants carry a “net cashless” exercise feature (“Cashless Conversion Feature”) allowing the holder thereof, under certain limited circumstances, to exercise the warrants without payment of the stated exercise price, but rather solely in exchange for the cancellation of that number of common shares into which such warrants are exercisable. As a result of the issuance of the warrants in conjunction with the convertible notes, the Company recorded a non-cash financing expense of $1,328,337. These convertible notes are unsecured, and due on demand.

In conjunction with this financing, the Company paid consultants an amount equal to 10% of the gross proceeds, which was included in investor relations during the year ended March 31, 2006 and issued 425,735 common shares at a deemed value of $285,242. There are 255,440 finders’ A warrants outstanding whereby the holders have the right to purchase 255,440 common shares at US$0.50 per share until August 5, 2008 and 425,733 finders’ B warrants whereby the holders shall have the right to purchase 425,733 common shares at US$0.75 per share until August 5, 2008. A total of US$82,200 in registration penalties incurred in the year ended March 31, 2007 were converted to a new convertible debenture in the same amount on April 6, 2007.

During the nine months ended December 31, 2008, interest of US$12,702 (2007 – US$12,499) was accrued on the principal balance of these convertible notes and interest and accrued principal and interest due in the amount of US$101,524 was converted to 267,221 common shares.

On April 6, 2006, the Company consummated a private offering transaction with and among a syndicated group of investors, pursuant to which the Company issued, in the aggregate, US$551,666 in 8% per annum convertible notes and three-year Class A and B warrants to acquire: (i) up to 735,544 shares of the Company’s common stock at a price per share of US$0.50; and (ii) up to an additional 735,544 shares of the Company’s common stock at a price per share of US$1.00. Subject to certain limitations, the principal amount of the notes, together with any accrued interest may be converted into shares of the Company’s common stock at the lesser of: (i) 70% of the average of the five lowest closing bid prices for the common stock for the ten trading days prior to conversion; or (ii) US$0.55. The convertible notes carry a redemption feature, which allows the Company to retire them, in whole or in part, for an amount equal to 130% of that portion of the face amount being redeemed, but only in the event that the common shares have a closing price of US$1.50 per share for at least twenty consecutive trading days and there has otherwise been no default. The common stock purchase warrants carry a Cashless Conversion Feature. These convertible notes are unsecured, and due on demand.

In conjunction with these private offering transactions, the Company paid consultants: (i) US$55,166 cash, representing 10% of the gross proceeds realized; (ii) 183,886 shares of common stock; (iii) three-year warrants to purchase up to 110,320 shares of common stock at a price per share of US$0.50; and (iv) three-year warrants to purchase up to 183,867 shares of common stock at a price per share of US$0.75.

During the nine months ended December 31, 2008, convertible note principal and accrued interest in the aggregate amount of US$441,874 was converted into 2,011,410 common shares, and interest of US$18,885 (2007 – US$21,816) was accrued on the outstanding principal balance of these convertible notes.

On April 6, 2006, and in conjunction with certain private placements, the Company reached a verbal agreement with the group of institutional and other investors, wherein the Company agreed to convert US$82,200 in accrued penalties associated with the July 25, 2005 through August 5, 2005 convertible notes into US$82,200 convertible penalty notes (note 10(a)) carrying terms similar to the July 25, 2005 through August 5, 2005 convertible notes and an aggregate of 109,600 warrants. These warrants carry a Cashless Conversion Feature and each of these warrants entitles the holder to purchase additional common shares for three years at a price of US$0.75 per share. These convertible notes are unsecured, and due on demand.

During the nine months ended December 31, 2008, interest of US$3,771 (2007 – US$3,435) was accrued on the principal balance of these convertible notes. During the nine months ended December 31, 2008, convertible note principal and accrued interest in the aggregate amount of US$64,410 was converted into 323,899 common shares.

Certain of the July and August 2005 and the April 6, 2006 convertible notes contained registration rights whereby the Company agreed to pay a penalty of 2% for every thirty days after a required filing and registration effective date plus a reduction in the warrant price of certain of the warrants issued of US$0.10. As a result of the Company not filing its registration statement until April 27, 2006, the Company incurred penalties, which have been included in interest expense. An aggregate of 3,407,372 previously issued share purchase warrants relating to certain of the July and August 2005 and the April 6, 2006 convertible notes have reduced exercise prices from US$0.50, US$0.75, and US$1.00 to US$0.40, US$0.65, and US$0.90, respectively. In 2007, the Company recognized $80,102 in interest expense with the corresponding amount to contributed surplus as a result of re-valuation of the warrants upon the change in the pricing. The registration statement was subsequently been declared effective.

On December 1, 2006, the Company accepted subscriptions of US$1,500,000 towards a private placement of 8% per annum, unsecured, convertible notes and three-year warrants to acquire: (i) up to an aggregate of 2,000,000 shares of the Company’s common stock at a price per share of US$0.50; and (ii) up to an additional 2,000,000 shares of the Company’s common stock at a price per share of US$1.00. Subject to certain limitations, the principal amount of the notes, together with any accrued interest may be converted into shares of the Company’s common stock at the lesser of: (i) 70% of the average of the five lowest closing bid prices for the Company’s common stock for the ten trading days prior to conversion; or (ii) US$0.55. The convertible notes carry a redemption feature, which allows the Company to retire them, in whole or in part, for an amount equal to 130% of that portion of the face amount being redeemed, but only in the event that the common shares have a closing price of US$1.50 per share for at least twenty consecutive trading days and there has otherwise been no default. These convertible notes are unsecured and due on demand. The common stock purchase warrants may be exercised on a cashless basis.

During the nine months ended December 31, 2008, interest of US$195,699 (2007 – US$64,316) was accrued on the principal balance of these convertible notes.

The right of the note holders to convert into the Company’s common stock is subject to the contractual agreement between the parties that any conversion by the note holders may not lead at the date of such conversion to an aggregate equity interest in the common stock of the Company greater than 9.99% inclusive of any derivative securities including options, warrants, convertible debt, any other convertible debt securities, or any other financial instruments convertible into common equity.

On January 29, 2007, the Company completed a private placement comprised of $2,000,000 convertible notes. The convertible notes will mature on December 11, 2008, carry interest at 6% per annum and are unsecured. The notes are convertible into “Units” at the note holders’ discretion at a conversion price of US$0.50 per Unit. Each “Unit” consists of one common share and one purchase warrant to purchase an additional common share at US$0.70 per share until December 11, 2008. The notes and any accrued interest are callable by the Company at any time after December 11, 2007 by providing thirty days’ written notice to the note holders. Interest on the notes will be compounded annually and be cumulative until the earlier of either the date the Company achieves pre-tax earnings or the end of the term. At the discretion of the note holders, interest on the notes is payable in either cash or units at US$0.50 per unit. In connection with this financing, the Company has paid consultants US$108,000 in cash and issued 135,000 warrants exercisable at US$0.50 per unit, with each unit consisting of one common share and one share purchase warrant to purchase a further common share at US$0.70 per share until December 11, 2008. The Company is obligated to file a resale registration statement on the underlying securities within four months of closing, which it has failed to do.

As a result of the failure to file the registration statement, the Company recorded penalties of US$120,000 as of March 31, 2007 and a further US$289,973 during the year ended March 31, 2008. During the nine months ended December 31, 2008, interest of US$47,342 (2007 – US$46,627) and accretion of the convertible debenture of US$585,237 (2007 – US$180,953) was accrued on the principal balance of these convertible notes; the principal portion of the notes was increased owing to the accretion of interest expense in the same amount relating to convertible debenture equity conversion component.

During the nine months ended December 31, 2008, interest and accretion of the convertible debenture in the aggregate of US$911,722 (2007 – US$294,301) was accrued on the principal balance of these convertible notes; the principal portion of the notes was increased owing to the accretion of interest expense in the same amount relating to convertible debenture equity conversion component. During the nine months ended December 31, 2008, convertible note principal and accrued interest in the aggregate amount of US$625,000 was converted into 1,417,984 common shares.

The Company has acted to change certain terms and conditions of US$1,150,000 in these convertible notes effecting a) the change of conversion price from US$0.50 per unit to US$0.30 per unit, b) the change of the term of the debt from December 11, 2008 to December 11, 2009, c) the change to the conversion unit’s warrant exercise price issuable from US$0.70 to US$0.50, and d) the extension of the unit’s embedded warrant exercise term from December 11, 2008 to December 11, 2010. These changes, retroactive to November, 2008, are subject to board of director’s approval.

On August 10, 2007, the Company issued an unsecured convertible term promissory note in the amount of US$650,000 to a third party. The convertible note is due on demand and bears interest at 6% with both interest and principal convertible at the option of the lender into units at US$0.60 per unit, with each unit consisting of one common share and one-half share purchase warrant with each whole share purchase warrant exercisable at US$0.75 to purchase an additional common share. After November 25, 2008, this convertible note accrues interest at the rate of 15% per annum.

The Company is required to register for trading the securities underlying the conversion features of this convertible note on a best efforts basis, but has failed to do so within terms agreed. A one-time financial penalty of US$28,567 for failure to register the securities underlying this convertible note within 180 days from the date of issuance has been incurred in the year ended March 31, 2008.

During the nine months ended December 31, 2008, interest and accretion of the convertible debenture in the aggregate of US$11,762 (2007 – US$373) was accrued on the principal balance of these convertible notes; the principal portion of the notes was increased owing to the accretion of interest expense in the same amount relating to convertible debenture equity conversion component.

The right of the note holder to convert into the Company’s common stock is subject to the contractual agreement between parties that any conversion by the note holder may not lead, at the date of such conversion, to an aggregate equity interest in the common stock of the Company greater than 9.99% inclusive of any derivative securities including options, warrants, convertible debt, any other convertible debt securities, or any other financial instruments convertible into common equity.

On September 27, 2007, the Company issued unsecured one-year term convertible notes bearing interest at 6% per annum in the amount of US$391,000 to third parties. Both interest and principal may be converted at the option of the lender at any time at US$0.60 per unit, with each unit consisting of one common share and one-half share purchase warrant, with each whole share purchase warrant exercisable at US$0.75 to purchase an additional common share for a two-year term from the date of conversion.

The Company was required to register for trading the securities underlying the conversion features of this convertible note on a best efforts basis, but has failed to do so within terms agreed. A one-time financial penalty of US$23,460 for failure to register the securities underlying this convertible note within 90 days from the date of issuance has been incurred during the nine months ended March 31, 2008.

During the nine months ended December 31, 2008, interest of US$11,762 (2007 – US$373) and accretion of the convertible debenture of US$143,173 (2007 – US$0) was accrued on the principal balance of these convertible notes; the principal portion of the notes was increased owing to the accretion of interest expense in the same amount relating to convertible debenture equity conversion component.

On July 21, 2008, the Company closed a financing of zero coupon, 12% interest, senior secured convertible promissory notes in the amount of US$2,428,160 with an aggregate purchase price of US$2,168,000 with four investors, one of which was the Company’s Chief Financial Officer as to US$168,000. The debt is convertible into shares of common stock at the lesser of US$0.51 per share (unless the conversion price has been adjusted pursuant to further contract covenants) and 70% of the average of the five lowest closing bid prices for the ten preceding trading days. The Company issued each purchaser in the private placement two warrants, one warrant being redeemable by the Company and the other being non-redeemable. The non-redeemable warrants are exercisable at US$0.55 and permit the holder to purchase shares of common stock equal to 100% of the number of shares issuable upon the conversion of the notes calculated on July 21, 2008. The redeemable warrants are exercisable at US$0.75 and permit the holder to purchase common stock equal to 50% of the number of shares issuable upon the conversion of the notes issued calculated on the closing date. The Company issued a total of redeemable warrants to purchase an aggregate of 4,761,098 shares of common stock and a total of redeemable warrants to purchase an aggregate of 2,380,550 shares of common stock. Further, the Company issued 439,216 non-redeemable warrants and 219,608 redeemable warrants and $160,000 in cash fees to close the transaction. Each non-redeemable warrant is exercisable at US$0.55, and each redeemable warrant is exercisable at US$0.75; warrants carry a term of five years from the date of closing of the financing. The redeemable warrants may be redeemed by the Company only if certain conditions have been satisfied including the Company’s common stock having closed at $1.50 per share for a period of 20 consecutive trading days and the warrant holder being able to resell the shares acquired upon exercise through a resale registration statement or under Rule 144 of the Securities Act.

During the nine months ended December 31, 2008, interest and accretion of the convertible debenture in the aggregate of US$777,343 (2007 – US$0) was accrued on the principal balance of these convertible notes; the principal portion of the notes was increased owing to the accretion of interest expense in the same amount relating to convertible debenture equity conversion component. The above warrants in this convertible note become exercisable at $0.30 per warrant share according to contractual provisions, subject to Board of Directors approval.

SUBSEQUENT EVENTS TO DECEMBER 31, 2008

Unless otherwise noted in Management’s Discussion and Analysis, the following events occurred after December 31, 2008:

| (a) | On January 27, 2009, the Company issued 1,062,840 shares from conversions of an aggregate of US $185,000 of convertible notes and US$ 11,515 in interest. |

| (b) | On February 2, 2009, issued 100,000 restricted shares for public relations services. |

| (c) | On February 5, 2009, the Company issued 90,000 restricted shares at $0.40 per share relating to a debt setoff agreement for internet related services rendered. |

| (d) | On February 12, 2009, the Company agreed to trade US$1,500,000 in convertible notes yielding 15% per annum (Notes 9 (e),(g)), and US$235,000 in convertible notes yielding 6% per annum (Note 9 (f)), to demand notes aggregating US$2,240,000 yielding simple interest at the rate of 10% per annum. Accrued interest of US$221,488 was agreed to be settled for an aggregate of 2,500,000 restricted shares. The arrangement is subject to Board of Directors approval. |

INTERNAL CONTROLS

The Company's Chief Executive Officer and Chief Financial Officer have evaluated the effectiveness of the Company's disclosure controls and procedures as of December 31, 2008, and have concluded that the Company's disclosure controls and procedures were not effective.

Due to the size of the Company, there is a lack of segregation of duties which is an internal control weakness. Management mitigates this risk through direct involvement of senior management in day to day operations.

The Company relies on the part time involvement of its Chief Financial Officer and consultants for period end financial disclosure and the reporting process. This risk is mitigated by the active involvement of the audit committee and the board of directors in reviewing the financial statements. However, the lack of full time personnel who have technical experience and knowledge is an internal control weakness and may result in the failure to timely report financial results.

It is unlikely that the above noted internal control weakness can be properly addressed until the Company grows to a significant size to warrant the expense, such as the hiring of additional personnel, associated with implementing additional segregation of duties. We are committed to improving our financial organization and internal controls. As part of this commitment, we intend to hire an additional person on a full time basis, when sufficient funds are available to us, with technical experience and knowledge in accounting to better segregate duties consistent with control objectives and will increase our personnel resources and technical accounting expertise within the accounting function.

During the period ended December 31, 2008 there were no changes in the Company’s internal control over financial reporting that occurred that has materially affected, or is reasonably likely to materially affect, the Company’s internal controls over financial reporting.

RISKS

The business of the Company entails significant risks, and an investment in the securities of the Company should be considered highly speculative. An investment in the securities of the Company should only be undertaken by persons who have sufficient financial resources to enable them to assume such risks. The following is a general description some of the material risks, which can adversely affect the business and in turn the financial results, ultimately affecting the value of an investment the Company. For a more complete description of risks related to the Company, please refer to Form 20-F filed on October 10, 2008 for the fiscal year ended March 31, 2008 at http://sec.gov/

We Have A History Of Operating Losses And We Have Operating Losses And A Negative Cash Flow.

We Have High Levels Of Debt That We May Not Be Able To Repay Without Significant Additional Financing, And Financing Options To The Company Are Extremely Limited With The United States In Recession.

Much Of Our Debt Is Convertible Into Equity At A Discount To Equity Trading In The Market That Could Lead To Unlimited Dilution. Some Of Our Debt Is Secured Against All Our Assets.

Given Our Current Financial Condition, We Need Additional Financing To Meet Our Current And Future Capital Needs And We May Not Be Able To Secure That Financing. The Company May Have To Settle Its Existing Debt On Some Basis, And Seek To Reorganize Its Common Share Equity In Order To Attract Necessary Financing.

We Have Only Limited Experience As A Public Reporting Company Which May Place Significant Demands On Our Operations.

The Company’s Inability To Attract And Retain New Personnel Could Inhibit Our Ability To Grow Or Maintain Our Operations.

There Is Only A Limited Market For Our Common Shares, And Our Common Share Price Is Depressed Making Further Investment Difficult Or Impossible.

The Price Of Our Common Shares May Be Volatile Which Could Result In Substantial Losses For Individual Shareholders

OFF-BALANCE SHEET ARRANGEMENTS

We do not have any off-balance sheet arrangements that have or are reasonably likely to have a material adverse affect on our financial condition or results of operations.

CONTRACTUAL OBLIGATIONS

On November 16, 2007, Valcent EU leased office and development space in Launceston, Cornwall, UK, under a ten-year lease beginning November 15, 2007 and ending on November 15, 2017 at a quarterly cost of $26,017 (GB£12,550). There were 8 years and 10.5 months remaining on the lease as at December 31, 2008.

RELATED PARTY TRANSACTIONS DURING THE NINE MONTHS ENDED DECEMBER 31, 2008

Related party transactions are in the ordinary course of business and are measured at the exchange amount at the time the agreement is entered into or services are provided. Related party transactions not disclosed elsewhere in these interim financial statements are as follows:

| Nine Months ended December 31, 2008 | |

(a) Payments to Pagic, a company related by a common officer and director, for product development expenses including royalties Value of shares issued pursuant to Technology License | $ 216,142 $ 190,746 |

(b) Charges from CFO and director for professional fees | $ 27,000 |

| Interest on advance from CFO, at 10% interest per annum | $ 2,055 |

| Unsecured advances at 10% per annum | $ 275,000 |

| Conversions of advances and fees to convertible debt (Note 9 (i)) | US$ 168,000 |

| Charges from private companies with this director in common for: | |

(i) Office rent | $ 22,500 |

(ii) Consulting fee | $ 112,500 |

(iii) Repayment of advance received | $ 10,000 |

(c) West Peak and its principal shareholder, a beneficial owner of more than 5% of the Company’s common shares: | |

(i) Unsecured loan advances/interest 8% per annum (ii) Consulting fees | $ 1,288,493 $ 47,500 |

(d) Advertising and consulting services of a private company with an ex-director in common | $ 173,916 |

(e) Operational management consulting services of a director | $ 26,250 |

(f) Operational management consulting services of a director and a related company | $ 81,000 |

(g) Unsecured loan advances, at 8% interest per annum received from a director of the Company and repaid during the period | $ 105,242 |

| | |

Due to related parties includes the following amounts at December 31, 2008 in respect to certain of the above and previous transactions:

| | December 31, 2008 |

(a) Pagic royalties, etc. | $ 195,479 |

(b) CFO charges, interest and advances | 142,475* |

(c) Consulting services, unsecured loan advances and related interest | 2,328,220 |

| (d) and (e) Operational management consulting | 39,175 |

Unsecured loan advances from a company with a director in common | 57,364 |

| | $ 2,762,713 |

* In addition, the CFO participated in the July 21, 2008 Convertible debenture as to $168,000 USD.