INDEX

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 2 |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 3 |

STATEMENTS OF FINANCIAL POSITION

| Parent company | Consolidated | Parent company | Consolidated | |||||||||||||||||

| ASSETS | Note | 12.31.21 | 12.31.20 | 12.31.21 | 12.31.20 | LIABILITIES | Note | 12.31.21 | 12.31.20 | 12.31.21 | 12.31.20 | |||||||||

| CURRENT ASSETS | CURRENT LIABILITIES | |||||||||||||||||||

| Cash and cash equivalents | 4 | 4,633,816 | 3,876,139 | 7,528,820 | 7,576,625 | Loans and borrowings | 15 | 2,790,926 | 811,919 | 3,203,068 | 1,059,984 | |||||||||

| Marketable securities | 5 | 324,771 | 312,515 | 346,855 | 314,158 | Trade accounts payable | 16 | 10,440,754 | 8,156,231 | 11,701,996 | 8,996,206 | |||||||||

| Trade and other receivables | 6 | 7,270,531 | 5,254,064 | 4,107,156 | 4,136,421 | Supply chain finance | 17 | 2,237,975 | 1,452,637 | 2,237,975 | 1,452,637 | |||||||||

| Inventories | 7 | 7,403,503 | 5,161,261 | 9,654,870 | 6,802,759 | Lease liability | 18 | 364,470 | 302,946 | 471,956 | 383,162 | |||||||||

| Biological assets | 8 | 2,786,692 | 2,044,288 | 2,899,921 | 2,129,010 | Payroll, related charges and employee profit sharing | 810,960 | 860,836 | 900,394 | 940,816 | ||||||||||

| Recoverable taxes | 9 | 881,927 | 812,338 | 976,133 | 899,120 | Taxes payable | 246,744 | 268,347 | 454,038 | 395,630 | ||||||||||

| Recoverable income taxes | 9 | 29,784 | 28,888 | 71,762 | 43,840 | Derivative financial instruments | 24 | 325,430 | 378,543 | 327,443 | 384,969 | |||||||||

| Derivative financial instruments | 24 | 132,498 | 361,315 | 134,551 | 377,756 | Provision for tax, civil and labor risks | 21 | 956,193 | 860,889 | 959,132 | 865,338 | |||||||||

| Restricted cash | 24,963 | 1 | 24,963 | 1 | Employee benefits | 20 | 42,097 | 114,938 | 54,354 | 125,230 | ||||||||||

| Assets held for sale | 5,000 | 15,637 | 16,628 | 186,025 | Advances from related parties | 30 | 12,393,604 | 8,960,394 | - | - | ||||||||||

| Other current assets | 324,680 | 348,722 | 481,464 | 446,269 | Liabilities directly associated with assets held for sale | - | - | - | 21,718 | |||||||||||

| Other current liabilities | 357,887 | 335,137 | 914,933 | 814,638 | ||||||||||||||||

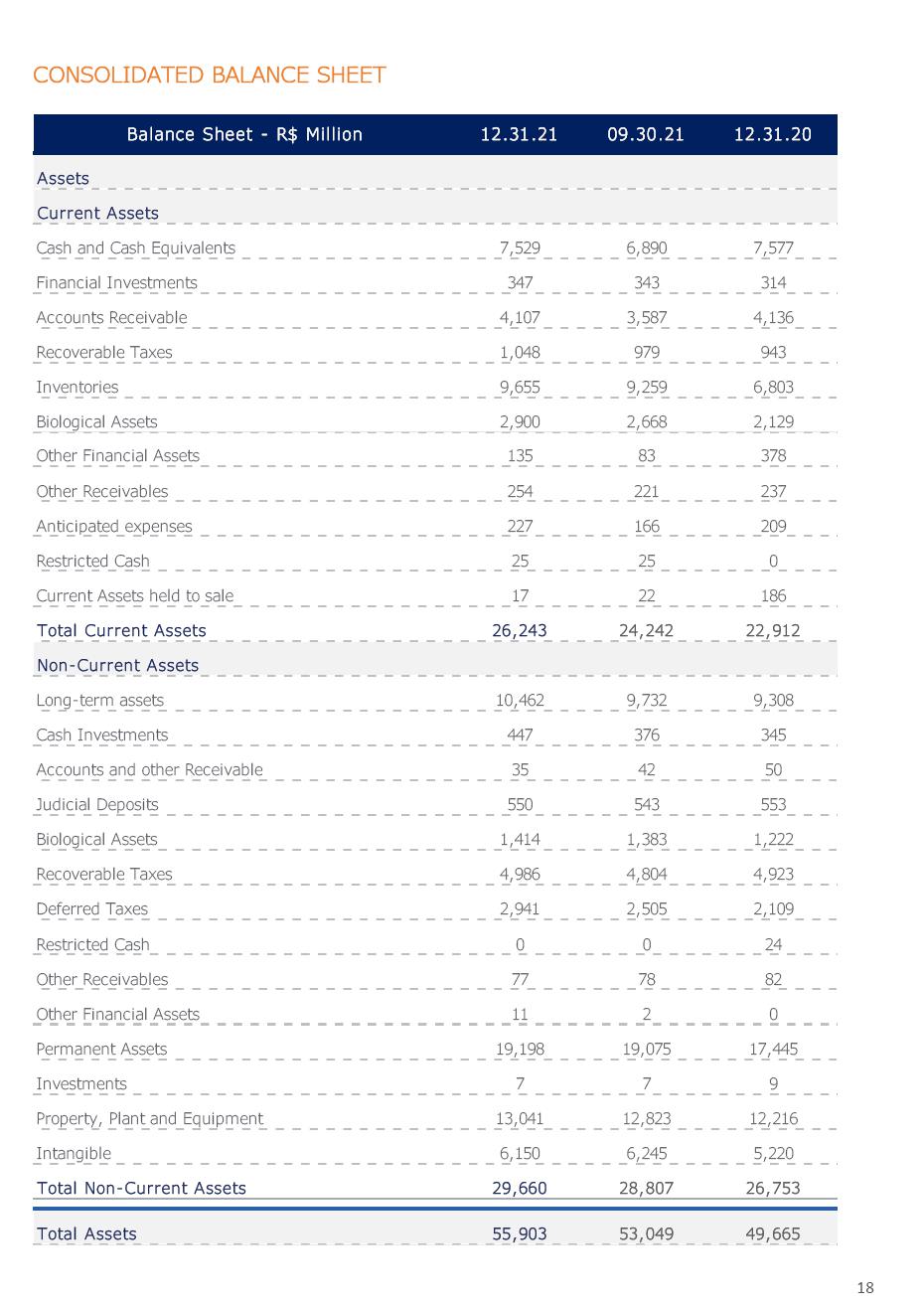

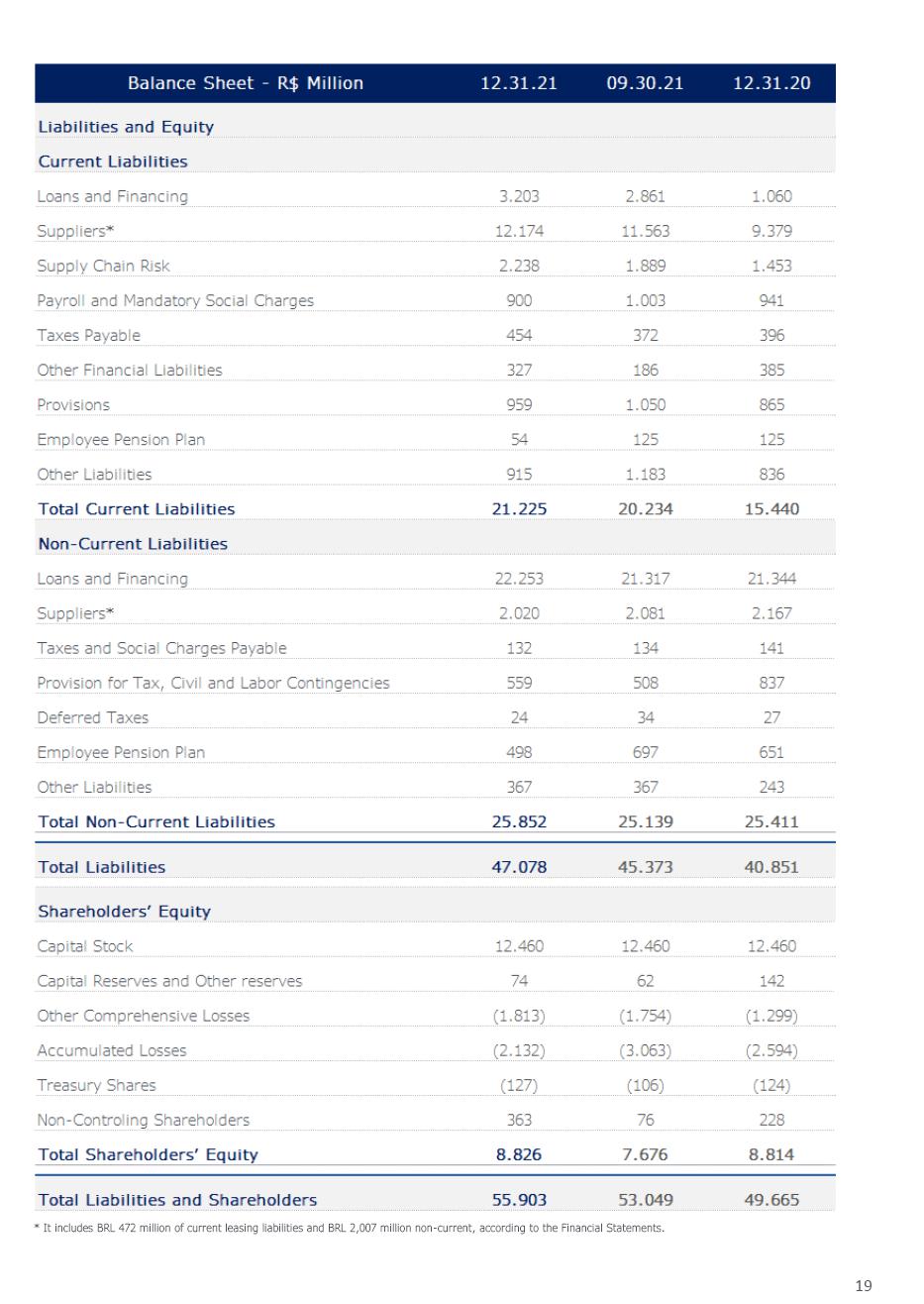

| Total current assets | 23,818,165 | 18,215,168 | 26,243,123 | 22,911,984 | Total current liabilities | 30,967,040 | 22,502,817 | 21,225,289 | 15,440,328 | |||||||||||

| NON-CURRENT ASSETS | NON-CURRENT LIABILITIES | |||||||||||||||||||

| LONG-TERM RECEIVALBLES | Loans and borrowings | 15 | 19,320,254 | 18,498,335 | 22,252,962 | 21,344,442 | ||||||||||||||

| Marketable securities | 5 | 15,438 | 15,044 | 447,413 | 344,577 | Trade accounts payable | 16 | 8,718 | 13,781 | 12,628 | 13,781 | |||||||||

| Trade and other receivables | 6 | 34,540 | 49,569 | 34,978 | 49,864 | Lease liability | 18 | 1,803,853 | 1,965,748 | 2,007,290 | 2,153,519 | |||||||||

| Recoverable taxes | 9 | 4,765,453 | 4,868,219 | 4,780,096 | 4,868,198 | Taxes payable | 130,565 | 141,252 | 132,195 | 141,252 | ||||||||||

| Recoverable income taxes | 9 | 194,979 | 54,123 | 206,355 | 54,859 | Provision for tax, civil and labor risks | 21 | 517,522 | 837,106 | 558,500 | 837,382 | |||||||||

| Deferred income taxes | 10 | 2,885,387 | 2,068,769 | 2,941,270 | 2,109,064 | Deferred income taxes | 10 | - | - | 23,710 | 26,527 | |||||||||

| Judicial deposits | 11 | 545,631 | 553,276 | 550,319 | 553,341 | Liabilities with related parties | 30 | 45,921 | 41,892 | - | - | |||||||||

| Biological assets | 8 | 1,367,013 | 1,154,726 | 1,414,482 | 1,221,749 | Employee benefits | 20 | 361,356 | 521,855 | 498,231 | 651,325 | |||||||||

| Receivables from related parties | 30 | - | 315 | - | - | Derivative financial instruments | 24 | 41,861 | 727 | 41,861 | 727 | |||||||||

| Derivative financial instruments | 24 | 10,804 | 234 | 10,804 | 234 | Other non-current liabilities | 251,512 | 249,691 | 325,098 | 242,089 | ||||||||||

| Restricted cash | 1 | 24,357 | 1 | 24,357 | ||||||||||||||||

| Other non-current assets | 70,228 | 77,829 | 76,757 | 82,123 | ||||||||||||||||

| Total long-term receivables | 9,889,474 | 8,866,461 | 10,462,475 | 9,308,366 | Total non-current liabilities | 22,481,562 | 22,270,387 | 25,852,475 | 25,411,044 | |||||||||||

| EQUITY | 22 | |||||||||||||||||||

| Capital | 12,460,471 | 12,460,471 | 12,460,471 | 12,460,471 | ||||||||||||||||

| Capital reserves | 141,834 | 141,834 | 141,834 | 141,834 | ||||||||||||||||

| Other equity transactions | (67,531) | 246 | (67,531) | 246 | ||||||||||||||||

| Investments | 12 | 13,269,948 | 11,922,325 | 7,113 | 8,874 | Accumulated losses | (2,132,230) | (2,594,028) | (2,132,230) | (2,594,028) | ||||||||||

| Property, plant and equipment | 13 | 11,723,211 | 11,168,558 | 13,040,862 | 12,215,580 | Treasury shares | (127,286) | (123,938) | (127,286) | (123,938) | ||||||||||

| Intangible assets | 14 | 3,210,336 | 3,186,476 | 6,149,814 | 5,220,102 | Other comprehensive loss | (1,812,726) | (1,298,801) | (1,812,726) | (1,298,801) | ||||||||||

| Attributable to controlling shareholders | 8,462,532 | 8,585,784 | 8,462,532 | 8,585,784 | ||||||||||||||||

| Non-controlling interests | - | - | 363,091 | 227,750 | ||||||||||||||||

| Total non-current assets | 38,092,969 | 35,143,820 | 29,660,264 | 26,752,922 | Total equity | 8,462,532 | 8,585,784 | 8,825,623 | 8,813,534 | |||||||||||

| TOTAL ASSETS | 61,911,134 | 53,358,988 | 55,903,387 | 49,664,906 | TOTAL LIABILITIES AND EQUITY | 61,911,134 | 53,358,988 | 55,903,387 | 49,664,906 | |||||||||||

The accompanying notes are an integral part of the financial statements.

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 4 |

| Parent company | Consolidated | ||||||||

| Note | 12.31.21 | 12.31.20 (1) | 12.31.21 | 12.31.20 (1) | |||||

| CONTINUING OPERATIONS | |||||||||

| NET SALES | 26 | 42,118,478 | 32,583,136 | 48,343,305 | 39,469,700 | ||||

| Cost of sales | 29 | (33,810,019) | (26,347,624) | (38,177,609) | (30,133,769) | ||||

| GROSS PROFIT | 8,308,459 | 6,235,512 | 10,165,696 | 9,335,931 | |||||

| OPERATING INCOME (EXPENSES) | |||||||||

| Selling expenses | 29 | (5,162,751) | (4,471,964) | (6,531,413) | (5,673,030) | ||||

| General and administrative expenses | 29 | (542,602) | (555,988) | (822,960) | (832,858) | ||||

| Impairment loss on trade receivables | 6 | (9,347) | (4,822) | (12,799) | (12,137) | ||||

| Other operating income (expenses), net | 27 | 129,211 | 50,009 | 211,263 | 28,887 | ||||

| Income from associates and joint ventures | 12 | 867,505 | 6,320,756 | - | - | ||||

| INCOME BEFORE FINANCIAL RESULTS AND INCOME TAXES | 3,590,475 | 7,573,503 | 3,009,787 | 2,846,793 | |||||

| Financial income | 462,847 | 371,496 | 537,736 | 420,757 | |||||

| Financial expenses | (3,069,588) | (2,568,149) | (3,331,615) | (1,889,454) | |||||

| Foreign exchange and monetary variations | (1,108,816) | (4,221,192) | (250,696) | (230,298) | |||||

| FINANCIAL INCOME (EXPENSES), NET | 28 | (3,715,557) | (6,417,845) | (3,044,575) | (1,698,995) | ||||

| INCOME (LOSS) BEFORE TAXES | (125,082) | 1,155,658 | (34,788) | 1,147,798 | |||||

| Income taxes | 10 | 624,467 | 227,906 | 552,102 | 242,271 | ||||

| INCOME FROM CONTINUING OPERATIONS | 499,385 | 1,383,564 | 517,314 | 1,390,069 | |||||

| LOSS FROM DISCONTINUED OPERATIONS | 1.3 | (79,930) | - | (79,930) | - | ||||

| INCOME FOR THE YEAR | 419,455 | 1,383,564 | 437,384 | 1,390,069 | |||||

| Net Income from Continuing Operation Attributable to | |||||||||

| Controlling shareholders | 499,385 | 1,383,564 | 499,385 | 1,383,564 | |||||

| Non-controlling interest | - | - | 17,929 | 6,505 | |||||

| 499,385 | 1,383,564 | 517,314 | 1,390,069 | ||||||

| Net Loss From Discontinued Operations Attributable to | |||||||||

| Controlling shareholders | (79,930) | - | (79,930) | - | |||||

| Non-controlling interest | - | - | - | - | |||||

| (79,930) | - | (79,930) | - | ||||||

| INCOME PER SHARE FROM CONTINUED OPERATIONS | |||||||||

| Weighted average shares outstanding - basic | 807,929,481 | 809,110,872 | |||||||

| Income per share - basic | 23 | 0.62 | 1.71 | ||||||

| Weighted average shares outstanding - diluted | 808,678,648 | 811,348,808 | |||||||

| Income per share - diluted | 23 | 0.62 | 1.71 | ||||||

| LOSSES PER SHARE FROM DISCONTINUED OPERATIONS | |||||||||

| Weighted average shares outstanding - basic | 807,929,481 | - | |||||||

| Losses per share - basic | 23 | (0.10) | - | ||||||

| Weighted average shares outstanding - diluted | 807,929,481 | - | |||||||

| Losses per share - diluted | 23 | (0.10) | - | ||||||

| (1) | The amounts of employee participation and bonuses were subject to an immaterial classification error correction (note 3.1.). |

The accompanying notes are an integral part of the financial statements.

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 5 |

STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

| Parent company | Consolidated | ||||||||

| Note | 12.31.21 | 12.31.20 | 12.31.21 | 12.31.20 | |||||

| Income for the year | 419,455 | 1,383,564 | 437,384 | 1,390,069 | |||||

| Other comprehensive income (loss), net of taxes | |||||||||

| Loss on foreign currency translation of foreign operations | (386,542) | (207,734) | (403,475) | (179,426) | |||||

| Loss on net investment hedge | (96,555) | (277,856) | (96,555) | (277,856) | |||||

| Cash flow hedges – effective portion of changes in fair value | 24 | (119,482) | 1,294,639 | (121,303) | 1,294,639 | ||||

| Cash flow hedges – reclassified to profit or loss | 24 | (26,201) | (1,376,139) | (26,201) | (1,376,139) | ||||

| Debt investments measured at FVTOCI (1) - changes in fair value | 5 | - | 178 | - | 178 | ||||

| Items that are or may be reclassified subsequently to profit or loss | (628,780) | (566,912) | (647,534) | (538,604) | |||||

| Equity investments measured at FVTOCI (1) - changes in fair value | 5 | 26,030 | 2,384 | 26,030 | 2,384 | ||||

| Actuarial gains on pension and post-employment plans | 20 | 131,168 | 7,589 | 130,671 | 7,121 | ||||

| Items that will not be reclassified to profit or loss | 157,198 | 9,973 | 156,701 | 9,505 | |||||

| Comprehensive income (loss) for the year | (52,127) | 826,625 | (53,449) | 860,970 | |||||

| Attributable to | |||||||||

| Controlling shareholders | (52,127) | 826,625 | (52,127) | 826,625 | |||||

| Non-controlling interest | - | - | (1,322) | 34,345 | |||||

| (52,127) | 826,625 | (53,449) | 860,970 | ||||||

| (1) | FVTOCI: Fair Value Through Other Comprehensive Income. |

Items above are stated net of income taxes and the related taxes are disclosed in note 10.

The accompanying notes are an integral part of the financial statements.

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 6 |

STATEMENTS OF CHANGES IN EQUITY

| Attributed to controlling shareholders | |||||||||||||||||||||||||||||||

| Other comprehensive income (loss) | |||||||||||||||||||||||||||||||

| Capital | Capital reserves | Other equity transactions (5) | Treasury shares | Accumulated foreign currency translation adjustments | Gains (losses) on marketable securities at FVTOCI (2) | Gains (losses) on cash flow hedge | Actuarial gains (losses) | Retained losses | Total equity | Non-controlling interest | Total shareholders' equity (consolidated) | ||||||||||||||||||||

| BALANCES AT DECEMBER 31, 2019 | 12,460,471 | 141,834 | 51,011 | (38,239) | (193,379) | 4,454 | (356,721) | (176,823) | (3,996,985) | 7,895,623 | 252,726 | 8,148,349 | |||||||||||||||||||

| Comprehensive income (loss) (1) | |||||||||||||||||||||||||||||||

| Gains (losses) on foreign currency translation of foreign operations | - | - | - | - | (207,734) | - | - | - | - | (207,734) | 28,308 | (179,426) | |||||||||||||||||||

| Loss on net investment hedge | - | - | - | - | (277,856) | - | - | - | - | (277,856) | - | (277,856) | |||||||||||||||||||

| Marketable securities at FVTOCI (2) - changes in fair value | - | - | - | - | - | 2,562 | - | - | - | 2,562 | - | 2,562 | |||||||||||||||||||

| Unrealized losses in cash flow hedge | - | - | - | - | - | - | (81,500) | - | - | (81,500) | - | (81,500) | |||||||||||||||||||

| Actuarial losses on pension and post-employment plans | - | - | - | - | - | - | - | 7,589 | - | 7,589 | (468) | 7,121 | |||||||||||||||||||

| Income for the year | - | - | - | - | - | - | - | - | 1,383,564 | 1,383,564 | 6,505 | 1,390,069 | |||||||||||||||||||

| SUB-TOTAL COMPREHENSIVE INCOME (LOSS) | - | - | - | - | (485,590) | 2,562 | (81,500) | 7,589 | 1,383,564 | 826,625 | 34,345 | 860,970 | |||||||||||||||||||

| Employee benefits remeasurement - defined benefit | - | - | - | - | - | - | (19,393) | 19,393 | - | - | - | ||||||||||||||||||||

| Appropriation of income (loss) | |||||||||||||||||||||||||||||||

| Dividends | - | - | - | - | - | - | - | - | - | - | (4,458) | (4,458) | |||||||||||||||||||

| Share-based payments | - | - | 180 | 20,371 | - | - | - | - | - | 20,551 | - | 20,551 | |||||||||||||||||||

| Acquisition of non-controlling interests | - | - | (50,945) | - | - | - | - | - | - | (50,945) | (54,863) | (105,808) | |||||||||||||||||||

| Acquisition of treasury shares | - | - | - | (106,070) | - | - | - | - | - | (106,070) | - | (106,070) | |||||||||||||||||||

| BALANCES AT DECEMBER 31, 2020 | 12,460,471 | 141,834 | 246 | (123,938) | (678,969) | 7,016 | (438,221) | (188,627) | (2,594,028) | 8,585,784 | 227,750 | 8,813,534 | |||||||||||||||||||

| Comprehensive income (loss) (1) | |||||||||||||||||||||||||||||||

| Losses on foreign currency translation of foreign operations | - | - | - | - | (386,542) | - | - | - | - | (386,542) | (16,933) | (403,475) | |||||||||||||||||||

| Losses on net investment hedge | - | - | - | - | (96,555) | - | - | - | - | (96,555) | - | (96,555) | |||||||||||||||||||

| Marketable securities at FVTOCI (2) - changes in fair value | - | - | - | - | - | 26,030 | - | - | - | 26,030 | - | 26,030 | |||||||||||||||||||

| Unrealized losses in cash flow hedge | - | - | - | - | - | - | (145,683) | - | - | (145,683) | (1,821) | (147,504) | |||||||||||||||||||

| Actuarial gains (losses) on pension and post-employment plans | - | - | - | - | - | - | - | 131,168 | - | 131,168 | (497) | 130,671 | |||||||||||||||||||

| Income for the year | - | - | - | - | - | - | - | - | 419,455 | 419,455 | 17,929 | 437,384 | |||||||||||||||||||

| SUB-TOTAL COMPREHENSIVE INCOME (LOSS) | - | - | - | - | (483,097) | 26,030 | (145,683) | 131,168 | 419,455 | (52,127) | (1,322) | (53,449) | |||||||||||||||||||

| Marketable securities at FVTOCI (2) - realized gain | - | - | - | - | (33,046) | - | - | 33,046 | - | - | - | ||||||||||||||||||||

| Employee benefits remeasurement - defined benefit | - | - | - | - | - | - | (9,297) | 9,297 | - | - | - | ||||||||||||||||||||

| Dividends | - | - | - | - | - | - | - | - | - | (80) | (80) | ||||||||||||||||||||

| Share-based payments | - | - | (8,762) | (3,348) | - | - | - | - | - | (12,110) | - | (12,110) | |||||||||||||||||||

| Acquisition of minority shareholders (3) | - | - | (79,673) | - | - | - | - | - | - | (79,673) | (157,918) | (237,591) | |||||||||||||||||||

| Write-off of put option held by minority shareholders (4) | - | - | 20,658 | - | - | - | - | - | - | 20,658 | 294,661 | 315,319 | |||||||||||||||||||

| BALANCES AT DECEMBER 31, 2021 | 12,460,471 | 141,834 | (67,531) | (127,286) | (1,162,066) | - | (583,904) | (66,756) | (2,132,230) | 8,462,532 | 363,091 | 8,825,623 | |||||||||||||||||||

| (1) | All changes in other comprehensive income are presented net of taxes. |

| (2) | FVTOCI: Fair Value Through Other Comprehensive Income. |

| (3) | Acquisition of remaining participation in the subsidiary BRF Kuwait WLL (note 1.1.1). |

| (4) | Recognition in Other Equity Transactions of the difference between the amount of the put option liability held by non-controlling interests and the book value of the non-controlling interest in TBQ Foods GmbH in the amount of R$20,658, and recognition of the Non-controlling Interest on the net assets of TBQ Foods GmbH in the amount of R$294,661, as detailed in note 1.1.3. |

| (5) | Balance in the comparative was further breakdown into separate accounts as described in note 22.2. |

The accompanying notes are an integral part of the financial statements.

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 7 |

| Parent company | Consolidated | |||||||

| Restated (4) | Restated (4) | |||||||

| 12.31.21 | 12.31.20 | 12.31.21 | 12.31.20 | |||||

| OPERATING ACTIVITIES | ||||||||

| Income from continuing operations | 499,385 | 1,383,564 | 517,314 | 1,390,069 | ||||

| Adjustments for: | ||||||||

| Depreciation and amortization | 1,343,713 | 1,267,169 | 1,715,863 | 1,517,402 | ||||

| Depreciation and depletion of biological assets | 943,789 | 789,496 | 1,030,491 | 876,976 | ||||

| Result on disposal of property, plant and equipments and investment | (66,600) | 29,287 | (141,211) | 40,220 | ||||

| Write-down of inventories to net realizable value | 100,993 | 93,592 | 128,680 | 122,082 | ||||

| Provision for tax, civil and labor risks | 116,215 | 318,041 | 116,144 | 319,237 | ||||

| Impairment | - | - | - | 10,160 | ||||

| Income from investments under the equity method | (867,505) | (6,320,756) | - | - | ||||

| Financial results, net | 3,715,557 | 6,417,845 | 3,044,575 | 1,698,995 | ||||

| Tax recoveries and gains in tax lawsuits | (107,380) | (379,087) | (108,785) | (379,087) | ||||

| Deferred income tax | (779,862) | (227,906) | (807,744) | (319,644) | ||||

| Employee profit sharing | 117,177 | 235,195 | 170,425 | 283,065 | ||||

| Other provisions | (923) | 253,512 | 2,793 | 265,621 | ||||

| 5,014,559 | 3,859,952 | 5,668,545 | 5,825,096 | |||||

| Trade accounts receivable | (1,916,087) | 976,661 | 386,889 | (481,192) | ||||

| Inventories | (2,343,241) | (2,468,706) | (2,878,507) | (2,622,702) | ||||

| Biological assets - current | (742,404) | (499,161) | (815,699) | (524,414) | ||||

| Trade accounts payable | 1,236,229 | 2,028,927 | 1,420,014 | 2,154,693 | ||||

| Supply chain finance | 790,946 | 620,232 | 790,946 | 620,232 | ||||

| Cash generated by operating activities | 2,040,002 | 4,517,905 | 4,572,188 | 4,971,713 | ||||

| Investments in securities at FVTPL (1) | (23,894) | - | (115,041) | - | ||||

| Redemptions of securities at FVTPL (1) | 44,768 | 102,064 | 145,053 | 102,172 | ||||

| Interest received | 89,696 | 78,070 | 106,388 | 87,334 | ||||

| Dividends and interest on shareholders' equity received | 10 | 304,357 | - | - | ||||

| Payment of tax, civil and labor provisions | (399,646) | (269,819) | (399,252) | (269,820) | ||||

| Derivative financial instruments | 237,043 | 916,503 | 266,491 | 923,709 | ||||

| Payment of income taxes | - | - | - | (155) | ||||

| Other operating assets and liabilities (2) | 2,628,834 | (78,553) | (652,191) | 24,216 | ||||

| Net cash provided by operating activities | 4,616,813 | 5,570,527 | 3,923,636 | 5,839,169 | ||||

| INVESTING ACTIVITIES | ||||||||

| Investments in securities at amortized cost | - | - | (4,060) | - | ||||

| Redemptions of securities at amortized cost | - | - | 166,112 | - | ||||

| Investments in securities at FVTOCI (3) | - | - | (12,866) | - | ||||

| Redemptions of securities at FVTOCI (3) | - | - | 86,059 | 26,352 | ||||

| Redemption of restricted cash | 400 | 285,672 | 400 | 285,672 | ||||

| Additions to property, plant and equipment | (1,407,885) | (758,954) | (1,555,426) | (804,609) | ||||

| Additions to biological assets - non-current | (1,142,533) | (907,497) | (1,239,746) | (1,006,222) | ||||

| Proceeds from disposals of property, plant, equipments and investment | 58,836 | 126,540 | 58,836 | 126,540 | ||||

| Additions to intangible assets | (174,971) | (95,164) | (179,632) | (96,181) | ||||

| Business combination, net of cash | (581) | - | (985,639) | - | ||||

| Sale of participation in subsidiaries with loss of control | - | - | 132,951 | 38,546 | ||||

| Acquisition of participation in joint ventures and subsidiaries | 1,770 | (1,087) | 1,770 | (1,087) | ||||

| Capital increase in associates | (1,006,073) | (10,065) | - | - | ||||

| Net cash used in investing activities | (3,671,037) | (1,360,555) | (3,531,241) | (1,430,989) | ||||

| Net cash used in investing activities from discontinued operations | - | - | (17,550) | - | ||||

| Net cash used in investing activities | (3,671,037) | (1,360,555) | (3,548,791) | (1,430,989) | ||||

| FINANCING ACTIVITIES | ||||||||

| Proceeds from debt issuance | 2,633,863 | 9,701,377 | 2,990,782 | 10,420,333 | ||||

| Repayment of debt | (1,209,864) | (9,861,770) | (1,395,347) | (10,247,359) | ||||

| Payment of interest | (1,060,244) | (1,260,768) | (1,193,367) | (1,421,539) | ||||

| Payment of interest derivatives - fair value hedge | (2,975) | - | (2,975) | - | ||||

| Treasury shares acquisition | (27,721) | (106,070) | (27,721) | (106,070) | ||||

| Acquisition of non-controlling interests | - | - | (238,421) | (100,390) | ||||

| Payment of lease liabilities | (533,885) | (473,984) | (705,427) | (553,556) | ||||

| Net cash used in financing activities | (200,826) | (2,001,215) | (572,476) | (2,008,581) | ||||

| EFFECT OF EXCHANGE RATE VARIATION ON CASH AND CASH EQUIVALENTS | 12,727 | 298,402 | 149,826 | 939,241 | ||||

| Net increase (decrease) in cash and cash equivalents | 757,677 | 2,507,159 | (47,805) | 3,338,840 | ||||

| Balance at the beginning of the year | 3,876,139 | 1,368,980 | 7,576,625 | 4,237,785 | ||||

| Balance at the end of the year | 4,633,816 | 3,876,139 | 7,528,820 | 7,576,625 | ||||

| (1) | FVTPL: Fair Value Through Profit and Loss. |

| (2) | In the Parent company, contemplates mainly the effects of prepayments of exports with subsidiaries in the amount of R$2,850,793 for the year ended December 31, 2021 (R$2,685,566 for the year ended December 31, 2020). In the Consolidated, contemplates the payment of employee profit sharing in the amount of R$290,332 for the year ended December 31, 2021 (R$217,794 for the year ended December 31, 2020). |

| (3) | FVTOCI: Fair Value Through Other Comprehensive Income. |

| (4) | Restated due to the change of accounting policy for the presentation of interest paid as described in note 3.1. |

The accompanying notes are an integral part of the financial statements.

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 8 |

| Parent company | Consolidated | |||||||

| 12.31.21 | 12.31.20 | 12.31.21 | 12.31.20 | |||||

| 1 - REVENUES | 48,221,304 | 37,414,179 | 54,744,458 | 44,299,525 | ||||

| Sales of goods and products | 46,703,553 | 36,613,811 | 53,046,159 | 43,503,289 | ||||

| Other income | 132,868 | 52,241 | 217,011 | 30,222 | ||||

| Revenue related to construction of own assets | 1,394,230 | 752,949 | 1,494,087 | 778,151 | ||||

| Expected credit losses | (9,347) | (4,822) | (12,799) | (12,137) | ||||

| 2 - SUPPLIES ACQUIRED FROM THIRD PARTIES | (32,826,060) | (24,284,767) | (37,820,537) | (28,544,203) | ||||

| Costs of goods sold | (27,522,141) | (20,383,346) | (31,556,767) | (23,866,153) | ||||

| Materials, energy, third parties services and other | (5,289,193) | (3,901,390) | (6,242,780) | (4,670,502) | ||||

| Reversal for inventories losses | (14,726) | (31) | (20,990) | (7,548) | ||||

| 3 - GROSS ADDED VALUE (1-2) | 15,395,244 | 13,129,412 | 16,923,921 | 15,755,322 | ||||

| 4 - DEPRECIATION AND AMORTIZATION | (2,287,502) | (2,056,665) | (2,746,354) | (2,394,378) | ||||

| 5 - NET ADDED VALUE (3-4) | 13,107,742 | 11,072,747 | 14,177,567 | 13,360,944 | ||||

| 6 - RECEIVED FROM THIRD PARTIES | 1,326,695 | 6,690,019 | 534,079 | 419,506 | ||||

| Income from associates and joint ventures | 867,505 | 6,320,756 | - | - | ||||

| Financial income | 462,847 | 371,496 | 537,736 | 420,757 | ||||

| Others | (3,657) | (2,233) | (3,657) | (1,251) | ||||

| 7 - ADDED VALUE TO BE DISTRIBUTED (5+6) | 14,434,437 | 17,762,766 | 14,711,646 | 13,780,450 | ||||

| 8 - DISTRIBUTION OF ADDED VALUE | 14,434,437 | 17,762,766 | 14,711,646 | 13,780,450 | ||||

| Payroll | 5,152,065 | 5,219,387 | 5,771,862 | 5,784,055 | ||||

| Salaries | 3,666,797 | 3,736,854 | 4,163,183 | 4,195,249 | ||||

| Benefits | 1,215,761 | 1,231,371 | 1,319,454 | 1,321,332 | ||||

| Government severance indemnity fund for employees | 269,507 | 251,162 | 289,225 | 267,474 | ||||

| Taxes, Fees and Contributions | 4,426,596 | 4,218,820 | 4,657,361 | 4,236,084 | ||||

| Federal | 1,388,767 | 1,534,926 | 1,528,480 | 1,543,491 | ||||

| State | 2,993,915 | 2,643,539 | 3,077,820 | 2,643,201 | ||||

| Municipal | 43,914 | 40,355 | 51,061 | 49,392 | ||||

| Capital Remuneration from Third Parties | 4,356,391 | 6,940,995 | 3,765,109 | 2,370,242 | ||||

| Interests, including exchange variation | 4,234,740 | 6,811,017 | 3,639,311 | 2,141,428 | ||||

| Rents | 121,651 | 129,978 | 125,798 | 228,814 | ||||

| Interest on Own-Capital | 499,385 | 1,383,564 | 517,314 | 1,390,069 | ||||

| Income for the year from continuing operations | 499,385 | 1,383,564 | 499,385 | 1,383,564 | ||||

| Non-controlling interest | - | - | 17,929 | 6,505 | ||||

The accompanying notes are an integral part of the financial statements.

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 9 |

MANAGEMENT REPORT

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 10 |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 11 |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 12 |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 13 |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 14 |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 15 |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 16 |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 17 |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 18 |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 19 |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 20 |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 21 |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 22 |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 23 |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 24 |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 25 |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 26 |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 27 |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 28 |

| 1. | COMPANY’S OPERATIONS |

BRF S.A. (“BRF”) and its subsidiaries (collectively the “Company”) is a publicly traded company, listed on the segment Novo Mercado of Brasil, Bolsa, Balcão (“B3”), under the ticker BRFS3, and listed on the New York Stock Exchange (“NYSE”), under the ticker BRFS. The Company’s registered office is at Rua Jorge Tzachel, nº 475, Bairro Fazenda, Itajaí - Santa Catarina and the main business office is in the city of São Paulo.

BRF is a Brazilian multinational company, with global presence, which owns a comprehensive portfolio of products, and it is one of the world’s largest companies of food products. The Company operates by raising, producing and slaughtering poultry and pork for processing, production and sale of fresh meat, processed products, pasta, margarine, pet food and others.

The Company holds as main brands Sadia, Perdigão, Qualy, Chester®, Kidelli, Perdix, Banvit, Biofresh and Gran Plus, present mainly in Brazil, Turkey and Middle Eastern countries.

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 29 |

1.1. Equity interest

| % equity interest | |||||||||

| Entity | Main activity | Country (1) | 12.31.21 | 12.31.20 | |||||

| BRF GmbH | (n) | Holding | Austria | 100.00 | 100.00 | ||||

| BRF Foods LLC | (g) | Import, industrialization and commercialization of products | Russia | 99.99 | 99.90 | ||||

| BRF Global Company Nigeria Ltd. | Marketing and logistics services | Nigeria | 99.00 | 99.00 | |||||

| BRF Global Company South Africa Proprietary Ltd. | Administrative, marketing and logistics services | South Africa | 100.00 | 100.00 | |||||

| BRF Global Company Nigeria Ltd. | Marketing and logistics services | Nigeria | 1.00 | 1.00 | |||||

| BRF Global GmbH | Holding and trading | Austria | 100.00 | 100.00 | |||||

| BRF Foods LLC | (h) | Import, industrialization and commercialization of products | Russia | 0.01 | 0.10 | ||||

| BRF Japan KK | Marketing and logistics services, import, export, industrialization and commercialization of products | Japan | 100.00 | 100.00 | |||||

| BRF Korea LLC | Marketing and logistics services | Korea | 100.00 | 100.00 | |||||

| BRF Shanghai Management Consulting Co. Ltd. | Provision of consultancy and marketing services | China | 100.00 | 100.00 | |||||

| BRF Shanghai Trading Co. Ltd. | Import, export and commercialization of products | China | 100.00 | 100.00 | |||||

| BRF Singapore Foods PTE Ltd. | Administrative, marketing and logistics services | Singapore | 100.00 | 100.00 | |||||

| Eclipse Holding Cöoperatief U.A. | Holding | The Netherlands | 99.99 | 99.99 | |||||

| Buenos Aires Fortune S.A. | Holding | Argentina | 4.36 | 4.36 | |||||

| Eclipse Latam Holdings | Holding | Spain | 100.00 | 100.00 | |||||

| Buenos Aires Fortune S.A. | Holding | Argentina | 95.64 | 95.64 | |||||

| Perdigão Europe Lda. | Import, export of products and administrative services | Portugal | 100.00 | 100.00 | |||||

| Perdigão International Ltd. | (d) | Import and export of products | Cayman Island | - | 100.00 | ||||

| ProudFood Lda. | Import and commercialization of products | Angola | 90.00 | 90.00 | |||||

| Sadia Chile S.A. | Import, export and commercialization of products | Chile | 40.00 | 40.00 | |||||

| Wellax Food Logistics C.P.A.S.U. Lda. | Import, commercialization of products and administrative services | Portugal | 100.00 | 100.00 | |||||

| One Foods Holdings Ltd. | Holding | UAE | 100.00 | 100.00 | |||||

| Al-Wafi Food Products Factory LLC | (p) | Import, export, industrialization and commercialization of products | UAE | 49.00 | 49.00 | ||||

| Badi Ltd. | Holding | UAE | 100.00 | 100.00 | |||||

| Al-Wafi Al-Takamol International for Foods Products | Import and commercialization of products | Saudi Arabia | 100.00 | 100.00 | |||||

| Joody Al Sharqiya Food Production Factory LLC | (b) | Import and commercialization of products | Saudi Arabia | 100.00 | - | ||||

| BRF Kuwait WLL | (c) | Import, commercialization and distribution of products | Kuwait | 49.00 | 75.00 | ||||

| BRF Foods GmbH | Industrialization, import and commercialization of products | Austria | 100.00 | 100.00 | |||||

| Al Khan Foodstuff LLC ("AKF") | (p) | Import, commercialization and distribution of products | Oman | 70.00 | 70.00 | ||||

| FFQ GmbH | (e) | Industrialization, import and commercialization of products | Austria | - | 100.00 | ||||

| TBQ Foods GmbH | (o) | Holding | Austria | 60.00 | 60.00 | ||||

| Banvit Bandirma Vitaminli | Import, industrialization and commercialization of products | Turkey | 91.71 | 91.71 | |||||

| Banvit Enerji ve Elektrik Üretim Ltd. Sti. | (a) | Generation and commercialization of electric energy | Turkey | 100.00 | 100.00 | ||||

| Banvit Foods SRL | (f) | Industrialization of grains and animal feed | Romania | - | 0.01 | ||||

| Nutrinvestments BV | Holding | The Netherlands | 100.00 | 100.00 | |||||

| Banvit ME FZE | Marketing and logistics services | UAE | 100.00 | 100.00 | |||||

| Banvit Foods SRL | (f) | Industrialization of grains and animal feed | Romania | - | 99.99 | ||||

| One Foods Malaysia SDN. BHD. | Marketing and logistics services | Malaysia | 100.00 | 100.00 | |||||

| Federal Foods LLC | (p) | Import, commercialization and distribution of products | UAE | 49.00 | 49.00 | ||||

| Federal Foods Qatar | (p) | Import, commercialization and distribution of products | Qatar | 49.00 | 49.00 | ||||

| BRF Hong Kong LLC | (a) | Import, commercialization and distribution of products | Hong Kong | 100.00 | 100.00 | ||||

| Eclipse Holding Cöoperatief U.A. | Holding | The Netherlands | 0.01 | 0.01 | |||||

| Establecimiento Levino Zaccardi y Cia. S.A. | (a) | Industrialization and commercialization of dairy products | Argentina | 99.99 | 99.99 | ||||

| BRF Energia S.A. | Commercialization of eletric energy | Brazil | 100.00 | 100.00 | |||||

| BRF Pet S.A. | Industrialization, commercialization and distribution of feed and nutrients for animals | Brazil | 100.00 | 100.00 | |||||

| Affinity Petcare Brasil Participações Ltda. | (m) | Holding | Brazil | 100.00 | - | ||||

| Mogiana Alimentos S.A. | Manufacturing, distribution and sale of Pet Food products | Brazil | 50.00 | - | |||||

| Gewinner Participações Ltda. | (j) | Industrialization, distribution and sale of feed and nutrients for animals | Brazil | 100.00 | - | ||||

| Hecosul Alimentos Ltda. | Manufacturing and sale of animal feed | Brazil | 100.00 | - | |||||

| Hercosul Distribuição Ltda. | Import, export, wholesale and retail sale of food products for animals | Brazil | 100.00 | - | |||||

| Hercosul Soluções em Transportes Ltda. | Road freight | Brazil | 100.00 | - | |||||

| Hercosul International S.R.L. | (k) | Manufacturing, export, import and sale of feed and nutrients for animals | Paraguay | 99.00 | - | ||||

| Paraguassu Participações S.A. | (m) | Holding | Brazil | 100.00 | - | ||||

| Mogiana Alimentos S.A. | Manufacturing, distribution and sale of Pet Food products | Brazil | 50.00 | - | |||||

| Hercosul International S.R.L. | (k) | Manufacturing, export, import and sale of feed and nutrients for animals | Paraguay | 1.00 | - | ||||

| PP-BIO Administração de bem próprio S.A. | (i) | Management of assets | Brazil | - | 33.33 | ||||

| PR-SAD Administração de bem próprio S.A. | Management of assets | Brazil | 33.33 | 33.33 | |||||

| ProudFood Lda. | Import and commercialization of products | Angola | 10.00 | 10.00 | |||||

| PSA Laboratório Veterinário Ltda. | Veterinary activities | Brazil | 99.99 | 99.99 | |||||

| Sino dos Alpes Alimentos Ltda. | (a) | Industrialization and commercialization of products | Brazil | 99.99 | 99.99 | ||||

| Sadia Alimentos S.A. | Holding | Argentina | 43.10 | 43.10 | |||||

| Sadia Chile S.A. | Import, export and commercialization of products | Chile | 60.00 | 60.00 | |||||

| Sadia International Ltd. | (l) | Import and commercialization of products | Cayman Island | - | 100.00 | ||||

| Sadia Uruguay S.A. | Import and commercialization of products | Uruguay | 100.00 | 100.00 | |||||

| Sadia Alimentos S.A. | Holding | Argentina | 56.90 | 56.90 | |||||

| Vip S.A. Empreendimentos e Participações Imobiliárias | Commercialization of owned real state | Brazil | 100.00 | 100.00 | |||||

| Establecimiento Levino Zaccardi y Cia. S.A. | (a) | Industrialization and commercialization of dairy products | Argentina | 0.01 | 0.01 | ||||

| PSA Laboratório Veterinário Ltda. | Veterinary activities | Brazil | 0.01 | 0.01 | |||||

| Sino dos Alpes Alimentos Ltda. | (a) | Industrialization and commercialization of products | Brazil | 0.01 | 0.01 | ||||

| (1) | UAE – United Arab Emirates. |

| (a) | Dormant subsidiaries. The Company is evaluating the liquidation of these subsidiaries. |

| (b) | On January 18, 2021, 100% of the capital stock of Joody Al Sharqiya Food Production Factory LLC was acquired (note 1.2.1). |

| (c) | On March 9, 2021, the minority stake on BRF AFC was acquired (note 1.1.1) and on December 27, 2021 its name was changed to BRF Kuwait WLL and the participation reduced to 49%. The Company has a shareholders’ agreement that ensures full economic rights on this entity. |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 30 |

| (d) | On March 24, 2021, the subsidiary Perdigão International Ltd. was dissolved. |

| (e) | On March 30, 2021, the subsidiary FFQ GmbH was dissolved. |

| (f) | On May 4, 2021 the sale of shares held in Banvit Foods SRL was concluded (note 1.1.2). |

| (g) | On May 31, 2021, BRF GmbH purchased additional 0.09% interest in BRF Food LLC from BRF Global GmbH. |

| (h) | On May 31, 2021, BRF Global GmbH sold 0.09% interest in BRF Food LLC to BRF GmbH. |

| (i) | On July 30, 2021, BRF S.A. sold all the shares held in PP-BIO Administração de bem próprio S.A. |

| (j) | On August 02, 2021, BRF Pet S.A. acquired 100% of the capital stock of Gewinner Participações Ltda. (note 1.2.2). |

| (k) | On August 02, 2021, BRF S.A. and BRF Pet S.A. acquired interest in Hercosul International S.R.L. (note 1.2.2). |

| (l) | On August 19, 2021, the subsidiary Sadia International Ltd. was dissolved. |

| (m) | On September 01, 2021, BRF Pet S.A. acquired 100% of the capital stock of Affinity Petcare Brasil Participações Ltda. and Paraguassu Participações S.A. (note 1.2.3). |

| (n) | On October 21, 2021 the merger of BRF Austria GmbH into BRF GmbH was approved retroactively to January 01, 2021, as permitted by the Austrian law. The entities previously presented as investees of BRF Austria GmbH are currently presented as BRF GmbH’s investees. |

| (o) | On December 13, 2021, the put option held by minority shareholders was terminated (note 1.1.3). |

| (p) | For these entities, the Company has agreements that ensure full economic rights, except for AKF, in which the economic rights are of 99%. |

Except for the associate PR-SAD, in which the Company recognizes the investments by the equity method, all other entities presented in the table above were consolidated.

| 1.1.1. | Acquisition of minority shareholding in BRF Kuwait WLL |

On March 9, 2021 the Company, through its wholly-owned subsidiary One Foods Holdings Ltd. (“One Foods”) acquired from Al Yasra Food Company W.L.L their minority stake of 25% of BRF Kuwait WLL (previously named BRF Al Yasra Food K.S.C.C. or BRF AFC), entity located in Kuwait, responsible for the distribution of BRF products in the country.

The transaction was concluded for the amount equivalent to R$238,421 (USD40,828) and from this date, BRF Kuwait WLL became a wholly-owned subsidiary of One Foods. The amount paid is presented in the financing activities on the statement of cash flows and the difference between the amount paid and the book value of the participation acquired was recorded in Equity as Other Equity Transactions, in the amount of R$79,673.

| 1.1.2. | Sale of the shares held in Banvit Foods SRL |

On May 4, 2021, Nutrinvestment BV and Banvit Bandirma Vitaminli, indirectly controlled subsidiaries of the Company, concluded the sale to Aaylex System Group S.A. of 100% of the shares held in Banvit Foods SRL, engaged in the activities of manufacture of animal feed and egg hatchery in Romania. The sale amount, received on that date, was equivalent to R$132,425 (EUR 20,300). In June, the parties established a price adjustment due to net debt and working capital, in the amount equivalent to R$13,059 (EUR2,157). In the year ended December 31, 2021, the Company recognized in the statement of income (loss) a gain with the sale of R$76,148, recorded under Other operating income (loss), net.

| 1.1.3. | Amendment to the shareholders’ agreement of TBQ Foods GmbH |

On December 13, 2021, the Company, through its wholly-owned indirect subsidiaries BRF Foods GmbH and One Foods Holdings Ltd. has executed an amendment to the shareholders’ agreement with Qatar Holding LLC, a wholly-owned subsidiary of the Qatar Investment Authority (“QIA”). The amendment provides for new terms and conditions to the partnership between BRF and QIA in TBQ Foods GmbH (“TBQ”), a holding company held 60% by BRF and 40% by QIA, which holds 91.71% of the shares issued by Banvit Bandırma Vitaminli Yem Sanayi Anonim Şirketi (“Banvit”).

In the Amendment, BRF and QIA have agreed on the termination of the put option available to QIA under the original shareholders’ agreement. From 2023, QIA will have further alternatives to liquidate its investment in Banvit and BRF’s financial liability towards QIA has been terminated.

On this date, the financial liability related to the put option held by QIA, in the amount of R$315,319, was derecognized with the corresponding increase in the non-controlling interests in consolidated Equity, in the amount of R$294,661. The difference between the liability and the book value of the non-controlling interest on December 13, 2021, in the amount of R$20,658, was recognized under Other Equity Transactions, increasing the Equity attributable to controlling shareholders.

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 31 |

1.2. Business combinations

| 1.2.1. | Joody Al Sharqiya Food Production Factory |

On January 18, 2021, through its wholly-owned subsidiary Badi Limited ("Badi"), the Company concluded the acquisition of 100% of the capital stock of Joody Al Sharqiya Food Production Factory ("Joody Al"), a food processing company in Saudi Arabia. The fair value of the consideration transferred was equivalent to R$40,720 (SAR29,195) paid in cash and, from this date, Joody Al has become a wholly-owned subsidiary of Badi.

The goodwill of R$11,476 arising from the business combination consists mainly of the synergies expected with the combination of the operations of BRF and Joody Al, strengthening the Company’s presence in the Saudi Arabian market. The results and the goodwill from this business combination are presented in the International segment (note 25).

The fair value of the acquired assets and assumed liabilities in the business combination is presented below:

| Fair value at the acquisition date | ||

| Assets | ||

| Cash and cash equivalents | 408 | |

| Inventories | 832 | |

| Property, plant and equipment | 30,128 | |

| Other current and non-current assets | 232 | |

| 31,600 | ||

| Liabilities | ||

| Trade accounts payable | 1,420 | |

| Taxes payable | 550 | |

| Employee benefits | 286 | |

| Other current and non-current liabilities | 100 | |

| 2,356 | ||

| Net assets acquired | 29,244 | |

| Fair value of consideration transferred | 40,720 | |

| Goodwill | 11,476 |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 32 |

| 1.2.2. | Hercosul Group |

On August 2, 2021 the Company concluded the acquisition of 100% of the capital stock of the companies that compose the Hercosul Group, after with the fulfillment of the conditions precedent. From this date, BRF Pet S.A. (“BRF Pet”) became owner of 100% of Gewinner Participações Ltda. and 99% of Hercosul International S.R.L. (“Hercosul International”) and BRF S.A. became owner of 1% of Hercosul International.

The fair value of the assets acquired and liabilities assumed in the business combination with Hercosul Group is presented below:

| Fair value at the acquisition date | ||||

| Gewinner Participações Consolidated | Hercosul International | |||

| Assets | ||||

| Cash and cash equivalents | 17,743 | 4,402 | ||

| Trade and other receivables | 40,767 | 8,413 | ||

| Inventories | 36,826 | 10,049 | ||

| Recoverable taxes | 15,385 | 3,643 | ||

| Property, plant and equipment | 70,796 | 72,035 | ||

| Intangible assets | 393,308 | 3,656 | ||

| Other current and non-current assets | 28,794 | 2,805 | ||

| 603,619 | 105,003 | |||

| Liabilities | ||||

| Social and Labor Obligations | 6,445 | 200 | ||

| Trade accounts payable | 66,597 | 8,582 | ||

| Taxes payable | 14,879 | 200 | ||

| Loans and borrowings | 65,892 | 30,268 | ||

| Provision for tax, civil and labor risks (1) | 5,949 | - | ||

| Lease liability | 3,961 | 614 | ||

| Deferred income taxes | 1,703 | - | ||

| Other current and non-current liabilities | 8,130 | 20,478 | ||

| 173,556 | 60,342 | |||

| Net assets acquired | 430,063 | 44,661 | ||

| Fair value of consideration transferred | 743,156 | 69,765 | ||

| Goodwill | 313,093 | 25,104 | ||

| (1) | Includes R$5,038 related to contingent liabilities recognized in the business combination. |

The fair value of the consideration transferred was of R$812,921, of which R$675,355 was paid in cash, R$119,180 will be paid in the next 4 years and R$18,386 refers to contingent consideration. The amount payable is subject to interest and was recorded as Other liabilities, with subsequent changes recorded as Financial expenses.

According to conditions established in the acquisition contract, which are common to transactions of this nature, the amount of the consideration may be adjusted based on the net debt and working capital of the Hercosul Group, for which the Company has used its best estimate at the disclosure date of these financial statements. There is no maximum amount defined for the price adjustment.

The recognized contingent consideration is linked to the gain, by the acquired entities, in administrative and legal proceedings existing on the acquisition date. In order to determine the fair value, the prognosis of the attorneys representing each case was considered, in addition to the business aspects determined in the acquisition contract. The payment of the contingent consideration will be made as the legal proceedings are terminated favorably to the Hercosul Group and it uses its economic benefits.

It is worth noting that these processes will be registered within the Hercosul Group when they meet the criteria for asset recognition.

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 33 |

The measurement of assets acquired and liabilities assumed was completed up to the date of disclosure of these financial statements and the main assets and liabilities identified that received fair value allocations in the business combination were: property, plant and equipment, inventories, customer relationship, trademarks and contingent liabilities.

The contingent liability recognized at the amount of R$5,038, is related to legal proceedings classified as present obligations and for which the fair value was measured reliably, based on premises that include the metrics agreed in the share purchase agreement.

The goodwill consists mainly of the value of the synergies expected from the combination of the operations of BRF Pet, Mogiana Group (defined in the note 1.2.3) and Hercosul Group, reinforcing BRF's presence in the pet food sector. The results, intangible assets with indefinite useful life and goodwill arising from this business combination are presented in Other segments (note 25). The Company expects that the goodwill recorded will be deductible for tax purposes.

The Company incurred in expenses with advisors, lawyers and other related to the acquisition and integration of Hercosul Group in the amount of R$19,861 for the year ended December 31, 2021, which were recognized under Administrative expenses.

This business combination contributed net revenue of R$133,280 and net income of R$2,465 from the acquisition date to December 31, 2021 in the consolidated statement of income. If the business combination had taken place at the beginning of the year ended December 31, 2021, the consolidated net revenues for this year would have increased by R$198,168 and the consolidated income for the year would have increased by R$36,258.

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 34 |

| 1.2.3. | Mogiana Group |

On September 1, 2021, the Company, through its wholly-owned subsidiary BRF Pet concluded the acquisition of Paraguassu Participações S.A. ("Paraguassu") and Affinity Petcare Brasil Participações Ltda. ("Affinity"), both owner of 100% of the capital stock of Mogiana Alimentos S.A. (together form the “Mogiana Group”), after fulfillment of all conditions precedent. Therefore, from this date, Paraguassu and Affinity became wholly-owned subsidiaries of BRF Pet.

The fair value of the assets acquired and liabilities assumed in the business combination with Hercosul Group is presented below:

| Mogiana Group Combined | Fair value at the acquisition date | |

| Assets | ||

| Cash and cash equivalents | 938 | |

| Marketable securities | 29,824 | |

| Trade and other receivables | 59,758 | |

| Inventories | 54,517 | |

| Recoverable taxes | 27,748 | |

| Property, plant and equipment | 139,042 | |

| Intangible assets | 206,553 | |

| Other current and non-current assets | 5,486 | |

| 523,866 | ||

| Liabilities | ||

| Trade accounts payable | 55,919 | |

| Loans and borrowings | 22,688 | |

| Lease liability | 10,168 | |

| Taxes payable | 11,487 | |

| Payroll, related charges and employee profit sharing | 6,296 | |

| Provision for tax, civil and labor risks (1) | 34,976 | |

| Employee benefits | 2,081 | |

| Deferred income taxes | 815 | |

| Other current and non-current liabilities | 16,932 | |

| 161,362 | ||

| Net assets acquired | 362,504 | |

| Fair value of consideration transferred | 481,435 | |

| Goodwill | 118,931 |

| (1) | Includes R$28,853 related to contingent liabilities recognized in the business combination. |

The fair value of the consideration transferred was of R$481,435 of which R$290,225 was paid in cash, R$145,548 will be paid in the next 6 years and R$45,662 refers to contingent consideration. The amount payable is subject to interest and was recorded as Other liabilities, with subsequent changes recorded as Financial expenses. In addition, from the term value, R$60,000 will be deposited in an escrow account (restricted cash) after the first anniversary of the acquisition, as a guarantee for BRF Pet in case of eventual indemnities provided for in the acquisition contract.

According to conditions established in the acquisition contract, which are common to transactions of this nature, the amount of the consideration may be adjusted based on the net debt and working capital of Mogiana Alimentos S.A. and for which the Company has used its best estimate at the disclosure date of these financial statements. There is no maximum amount defined for the price adjustment.

The recognized contingent consideration is linked to the gain, by the acquired entities, in administrative and legal proceedings existing on the acquisition date. In order to determine the fair value, the prognosis of the

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 35 |

attorneys representing each case was considered, in addition to the business aspects determined in the purchase and sale agreement. The payment of the contingent consideration will be made as the legal proceedings are won by the Mogiana Group and it uses its economic benefits. In the year ended December 31, 2021, R$2,830 were paid in relation to the contingent consideration.

It is worth noting that these processes will be registered within the Mogiana Group when they meet the criteria for asset recognition.

The measurement of assets acquired and liabilities assumed was completed up to the date of disclosure of these financial statements and the main assets and liabilities identified that received fair value allocation in the business combination were: property, plant and equipment, inventories, customer relationship, trademarks, contingent liabilities and taxes payable (recognized under Other Non-current Liabilities).

The contingent liability recognized at the amount of R$28,853, is related to legal proceedings classified as present obligations and for which the fair value was measured reliably, based on premises that include the metrics agreed in the share purchase agreement.

The goodwill consists mainly of the value of the synergies expected from the combination of the operations of BRF Pet, Mogiana Group and Hercosul Group, reinforcing BRF's presence in the pet food sector. The results, intangible assets with indefinite useful life and goodwill arising from this business combination are presented in Other segments (note 25). The Company expects that the goodwill recorded will be deductible for tax purposes.

The Company incurred in expenses with advisors, lawyers and other related to the acquisition and integration of Mogiana in the amount of R$9,526 for the year ended December 31, 2021, which were recognized under Administrative expenses.

This business combination contributed net revenue of R$173,909 and net income of R$12,873 from the acquisition date to December 31, 2021 in the consolidated statement of income. If the business combination had taken place at the beginning of year ended December 31, 2021, the consolidated net revenues for this period would have increased by R$329,418 and the consolidated net income for the year would be increased by R$27,955.

| 1.2.4. | Effects of the business combinations as though the acquisition date had been as of the beginning of the year |

If the business combinations had occurred at the beginning of the year ended December 31, 2021, the consolidated net sales for the year would be R$48,870,891 and the consolidated net profit for the year would be R$429,081.

1.3. Discontinued Operations

In the year ended December 31, 2021, the Company completed the price adjustment processes related to sale of Campo Austral S.A. and Avex S.A. The referred price adjustments totaled an expense of R$59,270 (R$47,802 net of taxes) and are presented in Net Loss from Discontinued Operations, consistently with the practice adopted in the sale of the operations in 2019.

On December 21, 2021, the Company entered into an agreement with Marfrig Global Foods S.A. (“Marfrig”) and MFG Holding S.A.U. in order to settle indemnities related to the sale of the previously controlled entity Quickfood S.A. to Marfrig, concluded on January 2, 2019. This transaction resulted in an expense of R$48,768 (R$32,128 net of income taxes), which is presented under Net Loss from Discontinued Operations, consistently with the practice adopted in the sale of operations in 2019.

1.4. Partnership – self-generation of energy

| 1.4.1. | Partnership with AES |

On August 16, 2021, the Company executed an investment agreement with a subsidiary of AES Brasil Energia S.A. to incorporate a joint venture for the construction of a wind energy park for self-generation in the wind farm complex of Cajuína, Rio Grande do Norte, with an installed capacity of 160MWm (average Megawatt), generating 80MWm to be supplied to the Company by means of a 15-year power purchase agreement.

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 36 |

The closing of this partnership is subject to approval of the competent authorities and the verification of other usual conditions in operations of this nature. The operation of the park is scheduled to begin by 2024.

| 1.4.2. | Partnership with PontoOn |

On September 16, 2021, the Company together with Intrepid Participações S.A. (“Intrepid”) entered into a 15-year renewable energy power purchase agreement together with a call option agreement, which provides for the entry of BRF, through a holding company jointly held with Intrepid, aiming the construction of a sun energy self-generation plant in Mauriti and Milagres, Ceará, with an installed capacity of 320MWp (Megawatt-peak) generating, on average, 80MWm.

The call option agreement provides BRF with the right to acquire participation in Intrepid for a fixed price. Should BRF exercise the option, the Company will directly invest the approximate amount of R$50 million, to be disbursed during the Project’s development. The operation of the complex is scheduled to begin by 2024.

1.5. Investigations involving BRF

| 1.5.1. | Carne Fraca and Trapaça operations |

The Company has been subject to two investigations conducted by Brazilian governmental entities, denominated “Carne Fraca Operation” in 2017 and “Trapaça Operation” in 2018. The Company’s Audit and Integrity Committee conducted independent investigations, along with the Independent Investigation Committee, composed of external members and with external legal advisors in Brazil and abroad with respect to the allegations involving BRF employees and former employees.

The main impacts observed as result of the referred investigations were recorded in Other Operating Expenses in the amount of R$9,003 for the year ended December 31, 2021 (R$28,004 for the year ended December 31, 2020) mostly related to expenditures with lawyers, legal advisors and consultants.

In addition to the impacts already recorded, there are uncertainties about the outcome of these investigations which may result in penalties, fines and normative sanctions, right restrictions and other forms of liabilities, for which the Company is not able to make a reliable estimate of the potential losses. The outcomes may result in payments of substantial amounts, which may cause a material adverse effect on the Company’s financial position, results and cash flows in the future.

Regarding the investigations conducted by regulators offices and governmental entities in the United States of America about these operations, on February 25, 2021, the Division of Enforcement of the U.S. Securities and Exchange Commission (“SEC”) issued a letter to the Company stating that it has concluded its investigation and, based on information to date, does not intend to recommend an enforcement action by the SEC against the Company. On May 5, 2021, the U.S. Department of Justice (“DOJ”) issued a letter stating that it has closed its investigation against BRF, based on information to date. No sanctions or penalties were imposed against the Company.

| 1.5.2. | Governance enhancement |

The Company has taken actions to strengthen the compliance with its policies, procedures and internal controls.

Among the actions implemented, are: (i) strengthening in the risk management, specially compliance, (ii) continuous improvement of the Compliance, Internal Audit and Internal Controls departments, (iii) review and issuance of new policies and procedures specifically related to applicable anticorruption laws, (iv) review and enhancement of the procedures for reputational verification of business partners, (v) review and enhancement of the processes of internal investigation, (vi) expansion of the independent reporting channel, (vii) review of transactional controls, and (viii) review and issuance of new consequence policy for misconduct.

1.6. Coronavirus (COVID-19)

On January 31, 2020 the World Health Organization announced that the COVID-19 is a global health emergency and on March 11, 2020 declared it a global pandemic. The outbreak has triggered significant decisions from governments and private sector entities, which in addition to the potential impact, increased the uncertainty level for the economic agents and may cause effects in the amounts recognized in the financial statements.

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 37 |

BRF continues to operate its industrial complexes, distribution centers, logistics, supply chain and administrative offices, even if temporarily and partially under remote work regime in some of the corporate offices. Therefore, until the date of approval of these financial statements, there has been no relevant change in its production plan, operation and/or commercialization. Additionally, management has developed and implemented contingency plans to maintain the operations and monitors the effects of the pandemic through a permanent multidisciplinary monitoring committee, formed by executives, specialists in the public health area and consultants.

Due to the pandemic, the Company has incurred in direct expenditures, such as transportation, personnel, prevention, control and donations, which are presented in the statement of income (loss) within the following line items:

| Consolidated | ||||

| 12.31.21 | 12.31.20 | |||

| Cost of sales (1) | (185,994) | (356,960) | ||

| Selling expenses | (18,234) | (56,307) | ||

| General and administrative expenses | (84,623) | (86,032) | ||

| (288,851) | (499,299) |

| (1) | In the year ended December 31, 2020, includes non-incremental expenditures related do idleness in the amount of R$55,926. |

As described in note 14.1 no impairment was recognized to the cash generating units. Due to the high volatility and uncertainty around the length and the impact of the pandemic, the Company will continue to monitor the situation and evaluate the impacts on assumptions and estimates used in preparing our financial reporting.

| 2. | BASIS OF PREPARATION AND PRESENTATION OF FINANCIAL STATEMENTS |

The parent company’s and consolidated financial statements were prepared in accordance with the accounting practices adopted in Brazil and with international financial reporting standards (“IFRS”), issued by International Accounting Standards Board (“IASB”). All the relevant information applicable to the financial statements, and only them, are being evidenced and correspond to those used by administration in its management.

The parent company’s and consolidated financial statements are expressed in thousands of Brazilian Reais (“R$”), unless otherwise stated. For disclosures of amounts in other currencies, the values were also expressed in thousands, unless otherwise stated.

The preparation of the parent company’s and consolidated financial statements require Management to make judgments, use estimates and adopt assumptions that affect the reported amounts of revenues, expenses, assets and liabilities, as well as the disclosures of contingent liabilities. The uncertainty inherent to these judgments, assumptions and estimates could result in material adjustments to the carrying amount of certain assets and liabilities in future periods.

Any judgments, estimates and assumptions are reviewed at each reporting period.

The parent company’s and consolidated financial statements were prepared based on the recoverable historical cost, except for the following material items recognized in the statements of financial position:

(i) derivative financial instruments and non-derivative financial instruments measured at fair value;

(ii) share-based payments and employee benefits measured at fair value;

(iii) biological assets measured at fair value; and

(iv) assets held for sale in instances where the fair value is lower than historical cost.

The Company prepared parent company’s and consolidated financial statements under the going concern assumption and disclosed all relevant information in its explanatory notes, in order to clarify and complement the accounting basis adopted.

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 38 |

| 3. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

3.1. Changes in accounting practices

In the year ended December 31, 2021, the Company changed the classification of payment of interest in the statement of cash flows, reclassifying this item from Operating Activities to Financing Activities. This change was made for better presentation of the Company’s cash flows and convergence with the reports used by the Administration in its management.

To ensure comparability between the years presented, the Company performed the following reclassifications for the year ended December 31, 2020:

| 12.31.20 | ||||||||||||

| Parent company | Consolidated | |||||||||||

| Previously presented | Reclassification | Restated | Previously presented | Reclassification | Restated | |||||||

| Net cash provided by operating activities | 4,309,759 | 1,260,768 | 5,570,527 | 4,417,630 | 1,421,539 | 5,839,169 | ||||||

| Net cash used in investing activities | (1,360,555) | - | (1,360,555) | (1,430,989) | - | (1,430,989) | ||||||

| Net cash provided by (used in) financing activities | (740,447) | (1,260,768) | (2,001,215) | (587,042) | (1,421,539) | (2,008,581) | ||||||

| Effect of exchange rate variation on cash and cash equivalents | 298,402 | - | 298,402 | 939,241 | - | 939,241 | ||||||

| Net increase in cash and cash equivalents | 2,507,159 | - | 2,507,159 | 3,338,840 | - | 3,338,840 | ||||||

In order to improve the level of detail in the presentation of information in the financial statements, in the year ended December 31, 2021, the Company began to classify the expenses with employee participation and bonuses by function in the statement of income (loss). To ensure comparability between the years presented, the comparative balances were restated as below:

| 12.31.20 | ||||||||||||||

| Parent company | Consolidated | |||||||||||||

| Previously presented | Reclassification | Restated | Previously presented | Reclassification | Restated | Corresponding Notes | ||||||||

| Cost of sales | (26,227,283) | (120,341) | (26,347,624) | (29,998,822) | (134,947) | (30,133,769) | 29 | |||||||

| Operating Income (Expenses) | ||||||||||||||

| Selling expenses | (4,405,558) | (66,406) | (4,471,964) | (5,587,488) | (85,542) | (5,673,030) | 29 | |||||||

| General and administrative expenses | (507,540) | (48,448) | (555,988) | (770,282) | (62,576) | (832,858) | 29 | |||||||

| Other operating income (expenses), net | (185,186) | 235,195 | 50,009 | (254,178) | 283,065 | 28,887 | 27 | |||||||

3.2. Consolidation

The consolidated financial statements include BRF and the subsidiaries (note 1.1) of which BRF has direct or indirect control, obtained when the Company is exposed to or has right to variable returns of such subsidiaries and has the power to influence these returns.

The financial information of the subsidiaries was prepared using the same accounting policies of the Parent Company.

All transactions and balances between BRF and its subsidiaries have been eliminated upon consolidation, as well as the unrealized profits or losses arising from these transactions, net of taxes. Non-controlling interests are presented separately.

3.3. Accounting judgments, estimates and assumptions

The Management made the following judgments which have a material impact on the amounts recognized in the financial statements:

Main judgments:

| » | control, significant influence and consolidation (note 1.1); |

| » | share-based payment transactions (note 19); |

| » | transfer of control for revenue recognition (note 26); |

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 39 |

| » | probability of exercise of a renewal option or anticipated termination of the lease agreements (note 18). |

Main estimates:

| » | fair value of financial instruments (note 24); |

| » | annual assessment of impairment of non-financial assets (note 14); |

| » | expected credit losses (note 6); |

| » | write-down of inventories to net realizable value (note 7); |

| » | fair value of biological assets (note 8); |

| » | assessment of recoverability of taxes (note 9 and 10); |

| » | useful lives of property, plant, equipment and intangible assets with definite useful life (note 13 and 14); |

| » | employee benefits (note 20); |

| » | provision for tax, civil and labor risks (note 21); |

| » | Fair value of assets acquired and liabilities assumed in business combinations (note 1.2). |

The Company reviews the estimates and underlying assumptions used in its accounting estimates in each reporting period. Revisions to accounting estimates are recognized in the period in which the estimates are revised.

3.4. Functional currency and foreign currency transactions

The financial statements of each subsidiary included in consolidation are prepared using the currency of the main economic environment where it operates.

The financial statements of foreign subsidiaries with functional currency different from Reais are translated into Brazilian Reais, under the following criteria:

| » | assets and liabilities are translated at the closing exchange rate; |

| » | income and expenses are translated at the monthly average rate; |

| » | the cumulative effects of gains or losses upon translation are recognized in Other Comprehensive Income, within equity. |

Goodwill arising from business combinations with foreign entities is expressed in the functional currency of that entity and translated by the closing exchange rate for the reporting currency of the acquirer, with the exchange variation effects recognized in Other Comprehensive Income.

The transactions in foreign currency follow the criteria below:

| » | non-monetary assets and liabilities, as well as incomes and expenses, are translated at the historical rate of the transaction; |

| » | monetary assets and liabilities are translated at the closing exchange rate; |

| » | the cumulative effects of gains or losses upon translation of monetary assets and liabilities are recognized in the statements of income (loss). |

3.5. Hyperinflationary economies

The Company has subsidiaries in Argentina, which is considered a hyperinflationary economy. For these subsidiaries the accounting policies below are adopted:

Non-monetary items, as well as income and expenses, are adjusted by the changes in the inflation index between the initial recognition and the closing date, so that the balances are stated at current value.

The translation of the balances of the subsidiaries with a hyperinflationary economy to the reporting currency were made at the closing rate of the reporting period for both financial position and income statement balances.

The inflation rates used in 2021 and 2020 were, respectively, 51.65% and 34.04%.

3.6. Business combination

Business combinations are recorded according to the acquisition method, which determines that the cost of an acquisition is measured by the sum of the consideration transferred, assessed based on the fair value on the

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 40 |

acquisition date, and the value of any non-controlling interest in the acquired company. The Company measures the non-controlling interest based on its participation in the net assets identified in the acquired company. Costs directly attributable to the acquisition are recorded as expense when incurred.

Business combinations with related parties are recognized using the acquisition method when the agreements have a substance and at cost when no substance is observed in the transaction.

In the acquisition of a business, Management assesses the acquired assets and liabilities assumed in order to classify and allocate them in accordance with the contractual terms, economic circumstances and relevant conditions on the acquisition date.

Initially, goodwill is measured as the excess of the consideration transferred over the fair value of the net assets acquired (identifiable assets and liabilities assumed, net).

After the initial recognition, goodwill is measured at cost less any accumulated impairment losses. For purposes of testing the recoverable amount, goodwill is allocated to each of the cash-generating units that will benefit from the acquisition.

3.7. Inventories

Inventories are measured at the lower of the average cost of acquisition or production of finished products and the net realizable value. The cost of finished products includes purchased raw materials, labor, production costs, transportation and storage, which are related to all the processes necessary for bringing the products to sales conditions. Write-down to net realizable value due to obsolescence, impaired items, slow-moving and realizable value through sale are evaluated and recorded in each reporting period, as appropriate. Normal production losses are included in the production cost for the respective month, while abnormal losses, if any, are expensed in Cost of sales without movement through inventories.

3.8. Biological assets

The consumable and production biological assets (live animals) and forests are measured at their fair value, using the cost approach technique to live animals and the revenue approach for forests. In determining the fair value of live animals, all losses inherent to the breeding process are already considered.

3.9. Income taxes

In Brazil, it comprises income tax (“IRPJ“) and social contribution on profit (“CSLL“), which are calculated monthly based on taxable profit, after offsetting tax losses and negative social contribution base, limited to 30% of the taxable income, applying the rate of 15% plus an additional 10% for the IRPJ and 9% for the CSLL.

The results obtained from foreign subsidiaries are subject to taxation by the countries where they are based, according to applicable rates and legislation. In Brazil, these results suffer the effects of taxation on universal basis established by the Law No. 12,973 / 14. The Company analyzes the results of each subsidiary for the application of its Income Tax legislation, in order to respect the treaties signed by Brazil and avoid double taxation.

Deferred taxes represent credits and debits on unused tax losses carried forward and negative CSLL base, as well as temporary differences between the tax and accounting bases. Deferred income tax assets and liabilities are classified as non-current. When the Company’s internal studies indicate that the future use of these credits over a 10-year horizon is not probable, the asset is derecognized (note 10.3).

Deferred tax assets and liabilities are presented net if there is enforceable legal right to be offset, and if they are under the responsibility of the same tax authority and under the same taxable entity.

Deferred tax assets and liabilities must be measured at the rates applicable in the period in which the asset is realized or the liability is settled, based on the rates (and tax legislation) that are in force on the financial position date.

In compliance with the interpretation ICPC 22 / IFRIC 23, the Company analyzed relevant tax decisions of higher courts and whether they conflict in any way with the positions adopted by the Company. Regarding the known uncertain tax positions, the Company reviewed the corresponding legal opinions and jurisprudence and did not

| BRF S.A. | 2021 AND 2020 FINANCIAL STATEMENTS | 41 |

identify impacts to be recorded, since it concluded that the tax authorities are not likely to reject the positions adopted.

The Company periodically evaluates the positions assumed in which there are uncertainties about the adopted tax treatment and will set up a provision when applicable.

3.10. Assets held for sale and discontinued operations

Assets held for sale are measured at the lower of the book value and the fair value less selling costs and are not depreciated or amortized. Such items are only classified under this item when its sale is highly probable and they are available for immediate sale in their current conditions.

Losses due to impairment are recorded under Other operating expenses.

The statement of income and cash flows are classified as discontinued operations and presented separately from continued operations of the Company when the operation represents a separate major line of business or geographical area of operations.

The prior periods of the statement of income (loss) and of the statement of cash flows are restated for comparative purposes. The statement of financial position remains as disclosed in prior periods.

3.11. Investments

Investments classified in this group are: i) in associated companies, that are entities over which the Company has significant influence, which is the power to participate in decisions on the investee’s financial and operational policies, but without individual or joint control of these policies; and ii) in joint ventures, in which the control of the business is shared through contractual agreement and decisions about the relevant activities require the unanimous consent of the parties.

Investments are initially recognized at cost and subsequently adjusted using the equity method.

3.12. Property, plant and equipment

Property, plant and equipment are measured by the cost of acquisition, formation, construction or dismantling, less accumulated depreciation. Loans and borrowings costs are recorded as part of the costs of property, plant and equipment in progress, considering the weighted average rate of loans and borrowings effective on the capitalization date.

Depreciation is recognized based on the estimated economic useful life of each asset using the straight-line method. The estimated useful life, residual values and depreciation methods are reviewed annually and the effects of any changes in estimates are accounted for prospectively. Land is not depreciated.

The Company annually performs an impairment analysis for its cash-generating units, which include the balances of property, plant and equipment (note 13).

Gains and losses on disposal of property, plant and equipment are determined by comparing the sale value with the residual book value and are recognized in the statement of income on the date of sale under Other operating income (expense).

3.13. Intangible assets

Acquired intangible assets are measured at cost at initial recognition, while those arising from a business combination are recognized at fair value on the acquisition date. After initial recognition, are presented at cost less accumulated amortization and impairment losses, when applicable. Internally generated intangible assets, excluding development costs, are not capitalized and the expense is recognized in the income statement when incurred.