0001123852 us-gaap:CashAndCashEquivalentsMember us-gaap:FairValueInputsLevel2Member us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember 2019-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

| |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2019 or

|

| |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

| 001-31387 |

| (Commission File Number) |

|

|

| Northern States Power Company |

| (Exact name of registrant as specificed in its charter) |

|

| | | |

| Minnesota | 41-1967505 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 414 Nicollet Mall | Minneapolis | Minnesota | 55401 |

| (Address of principal executive offices) | (Zip Code) |

|

| |

| (612) | 330-5500 |

| (Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act:

|

| | | | |

| Title of each class | | Trading Symbol | | Name of each exchange on which registered |

| N/A | | N/A | | N/A |

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☒ Yes ☐ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act. ☐ Large accelerated filer ☐ Accelerated filer ☒ Non-accelerated filer ☐ Smaller reporting company ☐ Emerging growth company

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes ☒ No

As of Feb. 21, 2020, 1,000,000 shares of common stock, par value $0.01 per share, were outstanding, all of which were held by Xcel Energy Inc., a Minnesota corporation.

DOCUMENTS INCORPORATED BY REFERENCE

The information required by Item 14 of Form 10-K is set forth under the heading “Independent Registered Public Accounting Firm – Audit and Non-Audit Fees” in Xcel Energy Inc.’s definitive Proxy Statement for the 2020 Annual Meeting of Shareholders which definitive Proxy Statement is expected to be filed with the SEC on or about April 6, 2020. Such information set forth under such heading is incorporated herein by this reference hereto.

Northern States Power Company meets the conditions set forth in General Instructions I(1)(a) and (b) of Form 10-K and is therefore filing this form with the reduced disclosure format permitted by General Instruction I(2).

TABLE OF CONTENTS

|

| | |

| PART I | | |

| Item 1 — | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Item 1A — | | |

| Item 1B — | | |

| Item 2 — | | |

| Item 3 — | | |

| Item 4 — | | |

| | | |

PART II

| | |

| Item 5 — | | |

| Item 6 — | | |

| Item 7 — | | |

| Item 7A — | | |

| Item 8 — | | |

| Item 9 — | | |

| Item 9A — | | |

| Item 9B — | | |

| | | |

PART III

| | |

| Item 10 — | | |

| Item 11 — | | |

| Item 12 — | | |

| Item 13 — | | |

| Item 14 — | | |

| | | |

PART IV

| | |

| Item 15 — | | |

| Item 16 — | | |

| | | |

| |

This Form 10-K is filed by NSP-Minnesota. NSP-Minnesota is a wholly owned subsidiary of Xcel Energy Inc. Additional information on Xcel Energy is available in various filings with the SEC. This report should be read in its entirety.

PART I

Definitions of Abbreviations

|

| |

| Xcel Energy Inc.’s Subsidiaries and Affiliates (current and former) |

| NSPM | NSP-Minnesota |

| NSP-Minnesota | Northern States Power Company, a Minnesota corporation |

| NSP System | The electric production and transmission system of NSP-Minnesota and NSP-Wisconsin operated on an integrated basis and managed by NSP-Minnesota |

| NSP-Wisconsin | Northern States Power Company, a Wisconsin corporation |

| PSCo | Public Service Company of Colorado |

| SPS | Southwestern Public Service Company |

| Utility subsidiaries | NSP-Minnesota, NSP-Wisconsin, PSCo and SPS |

| Xcel Energy | Xcel Energy Inc. and its subsidiaries |

|

| |

| Federal and State Regulatory Agencies |

| D.C. Circuit | United States Court of Appeals for the District of Columbia Circuit |

| DOC | Minnesota Department of Commerce |

| DOE | United States Department of Energy |

| DOT | United States Department of Transportation |

| EPA | United States Environmental Protection Agency |

| FERC | Federal Energy Regulatory Commission |

| IRS | Internal Revenue Service |

| MPUC | Minnesota Public Utilities Commission |

| NDPSC | North Dakota Public Service Commission |

| NERC | North American Electric Reliability Corporation |

| NRC | Nuclear Regulatory Commission |

| OAG | Minnesota Office of the Attorney General |

| PHMSA | Pipeline and Hazardous Materials Safety Administration |

| SDPUC | South Dakota Public Utilities Commission |

| SEC | Securities and Exchange Commission |

|

| |

| Electric, Purchased Gas and Resource Adjustment Clauses |

| CIP | Conservation improvement program |

| DSM | Demand side management |

| EIR | Environmental improvement rider |

| FCA | Fuel clause adjustment |

| GUIC | Gas utility infrastructure cost rider |

| PGA | Purchased gas adjustment |

| RDF | Renewable development fund |

| RER | Renewable energy rider |

| RES | Renewable energy standard |

| SEP | State energy policy rider |

| TCR | Transmission cost recovery adjustment |

|

| |

| Other |

| ADIT | Accumulated deferred income taxes |

| AFUDC | Allowance for funds used during construction |

| ALJ | Administrative law judge |

| ARO | Asset retirement obligation |

| ASC | FASB Accounting Standards Codification |

| ASU | FASB Accounting Standards Update |

| C&I | Commercial and Industrial |

| CAPM | Capital Asset Pricing Model |

| CapX2020 | Alliance of electric cooperatives, municipals and investor-owned utilities in the upper Midwest involved in a joint transmission line planning and construction effort |

| CC | Combined cycle |

| CCR | Coal combustion residuals |

| CCR Rule | Final rule (40 CFR 257.50 - 257.107) published by the EPA regulating the management, storage and disposal of CCRs as a nonhazardous waste |

| CEO | Chief executive officer |

| CFO | Chief financial officer |

CO2 | Carbon dioxide |

|

| |

| Corps | U.S. Army Corps of Engineers |

| CT | Combustion turbine |

| CWA | Clean Water Act |

| CWIP | Construction work in progress |

| DCF | Discounted Cash Flows |

| DR | Demand response |

| ELG | Effluent limitations guidelines |

| EMANI | European Mutual Association for Nuclear Insurance |

| ETR | Effective tax rate |

| FASB | Financial Accounting Standards Board |

| FTR | Financial transmission right |

| GAAP | Generally accepted accounting principles |

| GE | General Electric |

| GHG | Greenhouse gas |

| IPP | Independent power producing entity |

| IRP | Integrated Resource Plan |

| ISFSI | Independent spent fuel storage installation |

| ITC | Investment tax credit |

| JOA | Joint operating agreement |

| LNG | Liquefied natural gas |

| MEC | Mankato Energy Center |

| MGP | Manufactured gas plant |

| MISO | Midcontinent Independent System Operator, Inc. |

| Moody’s | Moody’s Investor Services |

| Native load | Customer demand of retail and wholesale customers that a utility has an obligation to serve under statute or long-term contract. |

| NAV | Net asset value |

| NEIL | Nuclear Electric Insurance Ltd. |

| NETO | New England Transmission Owners |

| NOL | Net operating loss |

| O&M | Operating and maintenance |

| Paris Agreement | Establishes a framework for GHG mitigation actions by all countries (“nationally determined contributions”) |

| PI | Prairie Island nuclear generating plant |

| Pipeline Safety Act | Pipeline Safety, Regulatory Certainty, and Job Creation Act |

| PPA | Purchased power agreement |

| PTC | Production tax credit |

| REC | Renewable energy credit |

| ROE | Return on equity |

| ROFR | Right-of-first-refusal |

| RTO | Regional Transmission Organization |

| SAB | Staff Accounting Bulletin |

| SERP | Supplemental executive retirement plan |

| SMMPA | Southern Minnesota Municipal Power Agency |

| Standard & Poor’s | Standard & Poor’s Ratings Services |

| TCJA | 2017 federal tax reform enacted as Public Law No: 115-97, commonly referred to as the Tax Cuts and Jobs Act |

| TO | Transmission owner |

| VaR | Value at Risk |

| VIE | Variable interest entity |

| Westinghouse | Westinghouse Electric Corporation |

|

| |

| Measurements |

| Bcf | Billion cubic feet |

| KV | Kilovolts |

| KWh | Kilowatt hours |

| MMBtu | Million British thermal units |

| MW | Megawatts |

| MWh | Megawatt hours |

|

|

Forward-Looking Statements

|

Except for the historical statements contained in this report, the matters discussed herein are forward-looking statements that are subject to certain risks, uncertainties and assumptions. Such forward-looking statements, assumptions and other statements are intended to be identified in this document by the words “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “objective,” “outlook,” “plan,” “project,” “possible,” “potential,” “should,” “will,” “would” and similar expressions. Actual results may vary materially. Forward-looking statements speak only as of the date they are made, and we expressly disclaim any obligation to update any forward-looking information. The following factors, in addition to those discussed elsewhere in this Annual Report on Form 10-K for the fiscal year ended Dec. 31, 2019 (including risk factors listed from time to time by NSP-Minnesota in reports filed with the SEC, including “Risk Factors” in Item 1A of this Annual Report on Form 10-K hereto), could cause actual results to differ materially from management expectations as suggested by such forward-looking information: operational safety, including our nuclear generation facilities; successful long-term operational planning; commodity risks associated with energy markets and production; rising energy prices and fuel costs; qualified employee work force and third-party contractor factors; ability to recover costs, changes in regulation and subsidiaries’ ability to recover costs from customers; reductions in our credit ratings and the cost of maintaining certain contractual relationships; general economic conditions, including inflation rates, monetary fluctuations and their impact on capital expenditures and the ability of NSP-Minnesota and its subsidiaries to obtain financing on favorable terms; availability or cost of capital; our customers’ and counterparties’ ability to pay their debts to us; assumptions and costs relating to funding our employee benefit plans and health care benefits; our subsidiaries’ ability to make dividend payments; tax laws; effects of geopolitical events, including war and acts of terrorism; cyber security threats and data security breaches; seasonal weather patterns; changes in environmental laws and regulations; climate change and other weather; natural disaster and resource depletion, including compliance with any accompanying legislative and regulatory changes; and costs of potential regulatory penalties.

|

|

Where to Find More Information

|

NSP-Minnesota is a wholly owned subsidiary of Xcel Energy Inc., and Xcel Energy’s website address is www.xcelenergy.com. Xcel Energy makes available, free of charge through its website, its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and all amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable after the reports are electronically filed with or furnished to the SEC. The SEC maintains an internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically at http://www.sec.gov.

|

| | | | | |

| |

| | | | | | |

| Electric customers | 1.5 million | | | NSP-Minnesota was incorporated in 2000 under the laws of Minnesota. NSP-Minnesota conducts business in Minnesota, North Dakota and South Dakota and has electric operations in all three states including the generation, purchase, transmission, distribution and sale of electricity. NSP-Minnesota and NSP-Wisconsin electric operations are managed on the NSP System. NSP-Minnesota also purchases, transports, distributes and sells natural gas to retail customers and transports customer-owned natural gas in Minnesota and North Dakota.

|

| Natural gas customers | 0.5 million | | |

| Total assets | $19.9 billion | | |

| Rate Base | $11.2 billion | | |

| ROE | 9.31% | | |

| Electric generating capacity | 7,712 MW | | |

| Gas storage capacity | 17.1 Bcf | | |

Electric transmission lines (conductor miles)

| 33,528 miles | | |

Electric distribution lines (conductor miles)

| 80,186 miles | | |

| Natural gas transmission lines | 86 miles | | |

| Natural gas distribution lines | 10,518 miles | | |

| | | | | |

NSP-Minnesota had electric sales volume of 41,298 (millions of KWh), 1,497,043 customers and electric revenues of $4,506.6 (millions of dollars) for 2019.

Sales/Revenue Statistics

|

| | | | | | | | |

| | | 2019 | | 2018 |

| KWH sales per retail customer | | 22,405 |

| | 23,511 |

|

| Revenue per retail customer | | $2,368 |

| | $2,414 |

|

| Residential revenue per KWh | |

| 13.22 | ¢ | |

| 13.03 | ¢ |

| Large C&I revenue per KWh | |

| 7.96 | ¢ | |

| 7.69 | ¢ |

| Small C&I revenue per KWh | |

| 10.15 | ¢ | |

| 9.79 | ¢ |

| Total retail revenue per KWh | |

| 10.57 | ¢ | |

| 10.27 | ¢ |

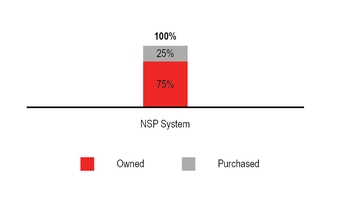

Owned and Purchased Energy Generation — 2019

Electric Energy Sources

Total electric generation by source (including energy market purchases) for the year ended Dec. 31, 2019:

*Distributed generation from the Solar*Rewards® program is not included (approximately 12.3 million KWh for 2019).

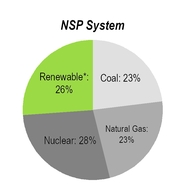

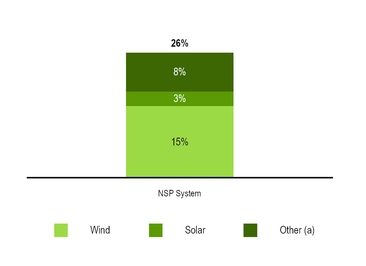

Renewable Energy Sources — NSP System

The NSP System’s renewable energy portfolio includes wind, hydroelectric, biomass and solar power from both owned generating facilities and PPAs. Renewable percentages will vary year over year based on system additions, weather, system demand and transmission constraints.

See Item 2 — Properties for further information.

Renewable energy as a percentage of total energy for 2019:

| |

(a) | Includes biomass and hydroelectric |

Wind Energy Sources

Owned — Owned and operated wind farms with corresponding capacity:

|

| | | | | | |

| 2019 | | 2018 |

| Wind Farms | | Capacity | | Wind Farms | | Capacity |

| 7 | | 1090 MW | | 5 | | 840 MW |

PPAs — Number of PPAs with range: |

| | | | | | |

| 2019 | | 2018 |

| PPAs | | Range | | PPAs | | Range |

| 131 | | 0.7 MW - 205.5 MW | | 132 | | 0.7 MW - 205.5 MW |

Capacity — Wind capacity:

|

| | |

| 2019 | | 2018 |

| 2,780 MW | | 2,550 MW |

Average Cost (Owned) — Average cost per MWh of wind energy from owned generation:

Average Cost (PPAs) — Average cost per MWh of wind energy under existing PPAs:

Wind Energy Development

NSP-Minnesota placed approximately 250 MW of wind into service during 2019:

|

| | |

| Project | | Capacity |

| Foxtail | | 150 MW |

| Lake Benton | | 99 MW |

NSP-Minnesota currently has approximately 1,170 MW of owned wind under development or construction and approximately 450 MW of planned PPAs with an estimated completion date of 2021 or earlier:

|

| | | | |

| Project | | Capacity | | Estimated Completion |

| Freeborn | | 200 MW | | 2020 |

| Blazing Star 1 | | 200 MW | | 2020 |

| Blazing Star 2 | | 200 MW | | 2020 |

Crowned Ridge (a) | | 200 MW | | 2020 |

Jeffers (b) | | 44 MW | | 2020 |

CWN (b) | | 26 MW | | 2020 |

| Dakota Range | | 300 MW | | 2021 |

| Various PPAs | | ~450 MW | | 2020-2021 |

| |

(a) | Build-own-transfer project. |

Solar Energy Sources

Solar energy PPAs: |

| | |

| Type | | Capacity |

| Distributed Generation | | 736 MW |

| Utility-Scale | | 266 MW |

Other Carbon-Free Energy Sources — NSP System

The NSP System’s other carbon-free energy portfolio includes nuclear from owned generating facilities.

See Item 2 — Properties for further information.

Nuclear Energy Sources

The NSP System has two nuclear plants (owned by NSP-Minnesota) with approximately 1,700 MW of total 2019 net summer dependable capacity.

NSP-Minnesota secures contracts for uranium concentrates, uranium conversion, uranium enrichment and fuel fabrication to operate its nuclear plants. The contract strategy involves a portfolio of spot purchases and medium and long-term contracts for uranium concentrates, conversion services and enrichment services with multiple producers and with a focus on diversification and alternate sources to minimize potential impacts caused by supply interruptions due to geographical and world political issues.

Nuclear Fuel Cost

Delivered cost per MMBtu of nuclear fuel consumed for owned electric generation and the percentage of total fuel requirements:

|

| | | | | | | |

| | | Nuclear |

| | | Cost | | Percent |

| 2019 | | $ | 0.81 |

| | 45 | % |

| 2018 | | 0.80 |

| | 45 |

|

Fossil Fuel Energy Sources — NSP System

The NSP System’s fossil fuel energy portfolio includes coal and natural gas power from both owned generating facilities and PPAs.

See Item 2 — Properties for further information.

Coal Energy Sources

NSP System has three coal plants with approximately 2,400 MW of total 2019 net summer dependable capacity.

Approved and proposed coal plant retirements: |

| | | | |

| Approved (2019 to 2027) |

| Year | | Plant | | Capacity |

| 2023 | | Sherco Unit 2 | | 682 MW |

| 2026 | | Sherco Unit 1 | | 680 MW |

|

| | | | |

| Proposed (2028 to 2030) |

| Year | | Plant | | Capacity |

| 2028 | | A.S King | | 511 MW |

| 2030 | | Sherco Unit 3 | | 517 MW |

Coal Fuel Cost

Delivered cost per MMBtu of coal consumed for owned electric generation and the percentage of total fuel requirements:

|

| | | | | | | |

| | | Coal (a) |

| | | Cost | | Percent |

| 2019 | | $ | 2.02 |

| | 36 | % |

| 2018 | | 2.13 |

| | 42 |

|

| |

(a) | Includes refuse-derived fuel and wood for the NSP System. |

Natural Gas Energy Sources

The NSP System has eight natural gas plants with approximately 2,800 MW of total 2019 net summer dependable capacity.

Natural gas supplies, transportation and storage services for power plants are procured to provide an adequate supply of fuel. Remaining requirements are procured through a liquid spot market. Generally, natural gas supply contracts have variable pricing that is tied to natural gas indices. Natural gas supply and transportation agreements include obligations for the purchase and/or delivery of specified volumes or payments in lieu of delivery.

Natural Gas Cost

Delivered cost per MMBtu of natural gas consumed for owned electric generation and the percentage of total fuel requirements:

|

| | | | | | | |

| | | Natural Gas |

| | | Cost | | Percent |

| 2019 | | $ | 3.09 |

| | 19 | % |

| 2018 | | 3.87 |

| | 13 |

|

Capacity and Demand

Uninterrupted system peak demand and occurrence date:

|

| | | | | | | | |

| System Peak Demand (in MW) |

| 2019 | | 2018 |

| 8,774 |

| | July 19 | | 8,927 |

| | June 29 |

Transmission

Transmission lines deliver electricity over long distances from power sources to transmission substations closer to homes and businesses. A strong transmission system ensures continued reliable and affordable service, ability to meet state and regional energy policy goals, and support a diverse generation mix, including renewable energy. NSP-Minnesota owns more than 33,500 conductor miles of transmission lines across its service territory.

During 2019, NSP-Minnesota completed the following transmission projects:

|

| | | | | |

| Project | | Miles | | Size |

| Maple River-Red River | | 5 |

| | 115 KV |

Upcoming transmission projects:

|

| | | | | | | |

| Project | | Miles | | Size | | Completion Date |

| Huntley-Wilmarth | | 50 |

| | 345 KV | | 2021 |

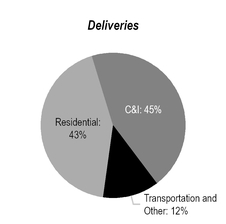

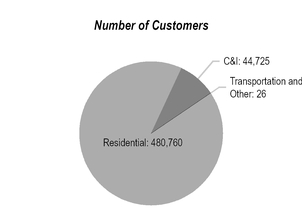

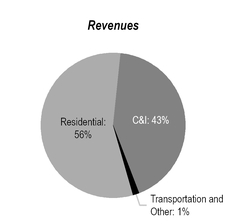

Natural gas operations consist of purchase, transportation and distribution of natural gas to end use residential, C&I and transport customers. NSP-Minnesota had natural gas deliveries of 106,292 (thousands of MMBtu), 525,511 customers and natural gas revenues of $571.3 (millions of dollars) for 2019.

Sales/Revenue Statistics

|

| | | | | | | | |

| | | 2019 | | 2018 |

| MMBtu sales per retail customer | | 176.96 |

| | 172.78 |

|

| Revenue per retail customer | | $ | 1,072.29 |

| | $ | 1,094.53 |

|

| Residential revenue per MMBtu | | 7.04 |

| | 7.29 |

|

| C&I revenue per MMBtu | | 5.12 |

| | 5.42 |

|

| Transportation and other revenue per MMBtu | | 0.59 |

| | 1.09 |

|

Capability and Demand

Natural gas supply requirements are categorized as firm or interruptible (customers with an alternate energy supply).

Maximum daily output (firm and interruptible) and occurrence date:

|

| | | | | | | | |

| 2019 | | 2018 |

| MMBtu | | Date | | MMBtu | | Date |

| 897,615 |

| (a) | Feb. 25 | | 786,751 |

| | Jan. 12 |

| |

(a) | Increase in maximum MMBtu output due to colder winter temperatures in 2019. |

Natural Gas Supply and Costs

NSP-Minnesota actively seeks natural gas supply, transportation and storage alternatives to yield a diversified portfolio, which provides increased flexibility, decreased interruption and financial risk and economical rates. In addition, NSP-Minnesota conducts natural gas price hedging activities approved by its state commissions.

Average delivered cost per MMBtu of natural gas for regulated retail distribution:

NSP-Minnesota has natural gas supply transportation and storage agreements that include obligations for purchase and/or delivery of specified volumes or to make payments in lieu of delivery.

See Item 2 - Properties for further information.

Seasonality

Demand for electric power and natural gas is affected by seasonal differences in the weather. In general, peak sales of electricity occur in the summer months and peak sales of natural gas occur in the winter months. As a result, the overall operating results may fluctuate substantially on a seasonal basis. Additionally, NSP-Minnesota’s operations have historically generated less revenues and income when weather conditions are milder in the winter and cooler in the summer.

Competition

NSP-Minnesota is subject to public policies that promote competition and development of energy markets. NSP-Minnesota’s industrial and large commercial customers have the ability to generate their own electricity. In addition, customers may have the option of substituting other fuels or relocating their facilities to a lower cost region.

Customers have the opportunity to supply their own power with distributed generation including solar generation and in most jurisdictions can currently avoid paying for most of the fixed production, transmission and distribution costs incurred to serve them.

Several states, including Minnesota, have incentives for the development of rooftop solar, community solar gardens and other distributed energy resources. Distributed generating resources are potential competitors to NSP-Minnesota’s electric service business with these incentives and federal tax subsidies.

The FERC has continued to promote competitive wholesale markets through open access transmission and other means. NSP-Minnesota’s wholesale customers can purchase their output from generation resources of competing suppliers or non-contracted quantities and use the transmission systems of Xcel Energy Inc.’s utility subsidiaries on a comparable basis to serve their native load.

FERC Order No. 1000 established competition for construction and operation of certain new electric transmission facilities. State utilities commissions have also created resource planning programs that promote competition for electricity generation resources used to provide service to retail customers.

NSP-Minnesota has franchise agreements with cities subject to periodic renewal; however, a city could seek alternative means to access electric power or gas, such as municipalization. No municipalization activities are occurring presently.

While facing these challenges, NSP-Minnesota believes its rates and services are competitive with alternatives currently available.

|

|

| Public Utility Regulation |

See Item 7 for discussion of public utility regulation.

Environmental Regulation

Our facilities are regulated by federal and state environmental agencies that have jurisdiction over air emissions, water quality, wastewater discharges, solid wastes and hazardous substances. Various company activities require registrations, permits, licenses, inspections and approvals from these agencies. NSP-Minnesota has received necessary authorizations for the construction and continued operation of its generation, transmission and distribution systems. Our facilities have been designed and constructed to operate in compliance with applicable environmental standards and related monitoring and reporting requirements. However, it is not possible to determine when or to what extent additional facilities or modifications of existing or planned facilities will be required as a result of changes to regulations, interpretations or enforcement policies or what effect future laws or regulations may have.

We may be required to incur expenditures in the future for remediation of MGP and other sites if it is determined that prior compliance efforts are not sufficient.

NSP-Minnesota must comply with emission budgets that require the purchase of emission allowances from other utilities.

There are significant present and future environmental regulations to encourage use of clean energy technologies and regulate emissions of GHGs. NSP-Minnesota has undertaken numerous initiatives to meet current requirements and prepare for potential future regulations, reduce GHG emissions and respond to state renewable and energy efficiency goals. If future environmental regulations do not take into consideration investments already made or if additional initiatives or emission reductions are required, substantial costs may be incurred.

In July 2019, the EPA adopted the Affordable Clean Energy rule, which requires states to develop plans for GHG reductions from coal-fired power plants. The state plans, due to the EPA in July 2022, will evaluate and potentially require heat rate improvements at existing coal-fired plants. It is not yet known how these state plans will affect NSP-Minnesota’s existing coal plants, but they could require substantial additional investment, even in plants slated for retirement. NSP-Minnesota believes, based on prior state commission practice, the cost of these initiatives or replacement generation would be recoverable through rates.

NSP-Minnesota seeks to address climate change and potential climate change regulation through efforts to reduce its GHG emissions in a balanced, cost-effective manner.

As of Dec. 31, 2019, NSP-Minnesota had 3,195 full-time employees and eight part-time employees, of which 2,036 were covered under collective-bargaining agreements.

Xcel Energy, which includes NSP-Minnesota, is subject to a variety of risks, many of which are beyond our control. Risks that may adversely affect the business, financial condition, results of operations or cash flows are described below. These risks should be carefully considered together with the other information set forth in this report and future reports that Xcel Energy files with the SEC.

Oversight of Risk and Related Processes

The Board of Directors is responsible for the oversight of material risk and maintaining an effective risk monitoring process. Management and the Board of Directors have responsibility for overseeing the identification and mitigation of key risks.

At a threshold level, NSP-Minnesota maintains a robust compliance program and promotes a culture of compliance beginning with the tone at the top. The risk mitigation process includes adherence to our code of conduct and compliance policies, operation of formal risk management structures and overall business management. NSP-Minnesota further mitigates inherent risks through formal risk committees and corporate functions such as internal audit, and internal controls over financial reporting and legal.

Management identifies and analyzes risks to determine materiality and other attributes such as timing, probability and controllability. Identification and risk analysis occurs formally through risk assessment conducted by senior management, the financial disclosure process, hazard risk procedures, internal audit and compliance with financial and operational controls. Management also identifies and analyzes risk through the business planning process, development of goals and establishment of key performance indicators, including identification of barriers to implementing our strategy. The business planning process also identifies likelihood and mitigating factors to prevent the assumption of inappropriate risk to meet goals.

Management communicates regularly with the Board of Directors and its sole stockholder regarding risk. Senior management presents and communicates a periodic risk assessment to the Board of Directors, providing information on the risks that management believes are material, including financial impact, timing, likelihood and mitigating factors. The Board of Directors regularly reviews management’s key risk assessments, which includes areas of existing and future macroeconomic, financial, operational, policy, environmental and security risks.

Overall, oversight, management and mitigation of risk is an integral and continuous part of the Board of Directors’ governance of NSP-Minnesota. Processes are in place to ensure appropriate risk oversight, as well as identification and consideration of new risks.

Risks Associated with Our Business

Operational Risks

Our natural gas and electric transmission and distribution operations involve numerous risks that may result in accidents and other operating risks and costs.

Our natural gas transmission and distribution activities include inherent hazards and operating risks, such as leaks, explosions, outages and mechanical problems. Our electric generation, transmission and distribution activities include inherent hazards and operating risks such as contact, fire and outages. These risks could result in loss of life, significant property damage, environmental pollution, impairment of our operations and substantial financial losses. We maintain insurance against most, but not all, of these risks and losses. The occurrence of these events, if not fully covered by insurance, could have a material effect on our financial condition, results of operations and cash flows.

Additionally, compliance with existing and potential new regulations related to the operation and maintenance of our natural gas infrastructure could result in significant costs. The PHMSA is responsible for administering the DOT’s national regulatory program to assure the safe transportation of natural gas, petroleum and other hazardous materials by pipelines. The PHMSA continues to develop regulations and other approaches to risk management to assure safety in design, construction, testing, operation, maintenance and emergency response of natural gas pipeline infrastructure. We have programs in place to comply with the PHMSA regulations and systematically monitor and renew infrastructure over time, however, a significant incident or material finding of non-compliance could result in penalties and higher costs of operations.

Our natural gas and electric transmission and distribution operations are dependent upon complex information technology systems and network infrastructure, the failure of which could disrupt our normal business operations, which could have a material adverse effect on our ability to process transactions and provide services.

Our utility operations are subject to long-term planning and project risks.

Most electric utility investments are planned to be used for decades. Transmission and generation investments typically have long lead times and are planned well in advance of when they are brought in-service subject to long-term resource plans. These plans are based on numerous assumptions such as: sales growth, customer usage, commodity prices, economic activity, costs, regulatory mechanisms, customer behavior, available technology and public policy. Our long-term resource plan is dependent on our ability to obtain required approvals, develop necessary technical expertise, allocate and coordinate sufficient resources and adhere to budgets and timelines.

In addition, the long-term nature of both our planning and our asset lives are subject to risk. The electric utility sector is undergoing a period of significant change. For example, increases in energy efficiency, wider adoption of lower cost renewable generation, distributed generation and shifts away from coal generation to decrease carbon emissions and increasing use of natural gas in electric generation driven by lower natural gas prices. Customer adoption of these technologies and increased energy efficiency could result in excess transmission and generation resources, downward pressure on sales growth, as well as stranded costs if NSP-Minnesota is not able to fully recover costs and investments.

Changing customer expectations and technologies are requiring significant investments in advanced grid infrastructure, which increases exposure to technology obsolescence.

Evolving stakeholder preference for lower emission generation sources may pressure our investments in natural gas generation and delivery. The magnitude and timing of resource additions and changes in customer demand may not coincide while customer preference for resource generation may change, which introduces further uncertainty into long-term planning. Additionally, multiple states may not agree as to the appropriate resource mix, which may lead to costs to comply with one jurisdiction that are not recoverable across all jurisdictions served by the same assets.

We are subject to longer-term availability of inputs such as coal, natural gas, uranium and water to cool our facilities. Lack of availability of these resources could jeopardize long-term operations of our facilities or make them uneconomic to operate.

We are subject to commodity risks and other risks associated with energy markets and energy production.

In the event fuel costs increase, customer demand could decline and bad debt expense may rise, which may have a material impact on our results of operations. Despite existing fuel recovery mechanisms, higher fuel costs could significantly impact our results of operations if costs are not recovered. Delays in the timing of the collection of fuel cost recoveries could impact our cash flows.

A significant disruption in supply could cause us to seek alternative supply services at potentially higher costs and supply shortages may not be fully resolved, which could cause disruptions in our ability to provide services to our customers. Failure to provide service due to disruptions may also result in fines, penalties or cost disallowances through the regulatory process. Also, significantly higher energy or fuel costs relative to sales commitments could negatively impact our cash flows and results of operations.

We also engage in wholesale sales and purchases of electric capacity, energy and energy-related products as well as natural gas. In many markets, emission allowances and/or RECs are also needed to comply with various statutes and commission rulings. As a result, we are subject to market supply and commodity price risk. Commodity price changes can affect the value of our commodity trading derivatives. We mark certain derivatives to estimated fair market value on a daily basis. Settlements can vary significantly from estimated fair values recorded and significant changes from the assumptions underlying our fair value estimates could cause earnings variability.

Failure to attract and retain a qualified workforce could have an adverse effect on operations.

Certain specialized knowledge is required of our technical employees for construction and operation of transmission, generation, and distribution assets. Our business strategy is dependent on our ability to recruit, retain and motivate employees. Competition for skilled employees is high in the areas of business operations. Failure to hire and adequately train replacement employees, including the transfer of significant internal historical knowledge and expertise to new employees, or future availability and cost of contract labor may adversely affect the ability to manage and operate our business. We have seen a tightening of supply for engineers and skilled laborers in certain markets and are implementing plans to retain these employees. Inability to attract and retain these employees could adversely impact our results of operations, financial condition or cash flows.

Our operations use third-party contractors in addition to employees to perform periodic and ongoing work.

We rely on third-party contractors to perform operations, maintenance and construction work. Our contractual arrangements with these contractors typically include performance standards, progress payments, insurance requirements and security for performance. Poor vendor performance could impact ongoing operations, restoration operations, our reputation and could introduce financial risk or risks of fines.

We are subject to the risks of nuclear generation.

NSP-Minnesota has two nuclear generation plants, PI and Monticello. Risks of nuclear generation include:

| |

| • | Hazards associated with the use of radioactive material in energy production, including management, handling, storage and disposal; |

| |

| • | Limitations on insurance available to cover losses that may arise in connection with nuclear operations, as well as obligations to contribute to an insurance pool in the event of damages at a covered U.S. reactor; and |

| |

| • | Technological and financial uncertainties related to the costs of decommissioning nuclear plants may cause our funding obligations to change. |

The NRC has authority to impose licensing and safety-related requirements for the operation of nuclear generation facilities, including the ability to impose fines and/or shut down a unit until compliance is achieved. Revised NRC safety requirements could necessitate substantial capital expenditures or an increase in operating expenses. In addition, the Institute for Nuclear Power Operations reviews our nuclear operations and nuclear generation facilities. Compliance with the Institute for Nuclear Power Operations’ recommendations could result in substantial capital expenditures or a substantial increase in operating expenses.

If an incident did occur, it could have a material impact on our results of operations, financial condition or cash flows. Furthermore, non-compliance or the occurrence of a serious incident at other nuclear facilities could result in increased industry regulation, which may increase our compliance costs.

NSP-Wisconsin’s production and transmission system is operated on an integrated basis with our production and transmission system, and NSP-Wisconsin may be subject to risks associated with our nuclear generation.

We are a wholly owned subsidiary of Xcel Energy Inc. Xcel Energy Inc. can exercise substantial control over our dividend policy and business and operations and may exercise that control in a manner that may be perceived to be adverse to our interests.

All of the members of our Board of Directors, as well as many of our executive officers, are officers of Xcel Energy Inc. Our Board of Directors makes determinations with respect to a number of significant corporate events, including the payment of our dividends.

We have historically paid quarterly dividends to Xcel Energy Inc. In 2019, 2018 and 2017 we paid $466.6 million, $456.3 million and $506.6 million of dividends to Xcel Energy Inc., respectively. If Xcel Energy Inc.’s cash requirements increase, our Board of Directors could decide to increase the dividends we pay to Xcel Energy Inc. to help support Xcel Energy Inc.’s cash needs. This could adversely affect our liquidity. The most restrictive dividend limitation for NSP-Minnesota is imposed by our state regulatory commissions. State regulatory commissions indirectly limit the amount of dividends NSP-Minnesota can pay to Xcel Energy Inc., by requiring a minimum equity-to-total capitalization ratio.

See Note 5 to the consolidated financial statements for further information.

Financial Risks

Our profitability depends on our ability to recover costs from our customers and changes in regulation may impair our ability to recover costs from our customers.

We are subject to comprehensive regulation by federal and state utility regulatory agencies, including siting and construction of facilities, customer service and the rates that we can charge customers.

The profitability of our operations is dependent on our ability to recover the costs of providing energy and utility services and earn a return on our capital investment. Our rates are generally regulated and based on an analysis of our costs incurred in a test year. We are subject to both future and historical test years depending upon the regulatory jurisdiction. Thus, the rates we are allowed to charge may or may not match our costs at any given time. Rate regulation is premised on providing an opportunity to earn a reasonable rate of return on invested capital.

There can also be no assurance that our regulatory commissions will judge all our costs to be prudent, which could result in disallowances, or that the regulatory process will always result in rates that will produce full recovery. Overall, management believes prudently incurred costs are recoverable given the existing regulatory framework. However, there may be changes in the regulatory environment that could impair our ability to recover costs historically collected from customers, or we could exceed caps on capital costs (e.g., wind projects) required by commissions and result in less than full recovery.

Changes in the long-term cost-effectiveness or to the operating conditions of our assets may result in early retirements of utility facilities. While regulation typically provides relief for these types of changes, there is no assurance that regulators would allow full recovery of all remaining costs.

In a continued low interest rate environment there has been increased downward pressure on allowed ROE. Conversely, higher than expected inflation or tariffs may increase costs of construction and operations. Also, rising fuel costs could increase the risk that we will not be able to fully recover our fuel costs from our customers.

Adverse regulatory rulings or the imposition of additional regulations could have an adverse impact on our results of operations and materially affect our ability to meet our financial obligations, including debt payments.

Any reductions in our credit ratings could increase our financing costs and the cost of maintaining certain contractual relationships.

We cannot be assured that our current ratings will remain in effect, or that a rating will not be lowered or withdrawn by a rating agency. Significant events including disallowance of costs, significantly lower returns on equity, changes to equity ratios and impacts of tax policy may impact our cash flows and credit metrics, potentially resulting in a change in our credit ratings. In addition, our credit ratings may change as a result of the differing methodologies or change in the methodologies used by the various rating agencies. Any downgrade could lead to higher borrowing costs and could impact our ability to access capital markets. Also, we may enter into contracts that require posting of collateral or settlement of applicable contracts if credit ratings fall below investment grade.

We are subject to capital market and interest rate risks.

Utility operations require significant capital investment. As a result, we frequently need to access capital markets. Capital markets are global and impacted by issues and events throughout the world. Any disruption in capital markets could have a material impact on our ability to fund our operations. Capital market disruption and financial market distress could prevent us from issuing short-term commercial paper, issuing new securities or cause us to issue securities with unfavorable terms and conditions, such as higher interest rates.

Higher interest rates on short-term borrowings with variable interest rates could also have an adverse effect on our operating results. The performance of capital markets impacts the value of assets held in trusts to satisfy future obligations to decommission our nuclear plants and satisfy our defined benefit pension and postretirement benefit plan obligations. These assets are subject to market fluctuations and yield uncertain returns, which may fall below expected returns. A decline in the market value of these assets may increase funding requirements. Additionally, the fair value of the debt securities held in the nuclear decommissioning and/or pension trusts may be impacted by changes in interest rates.

We are subject to credit risks.

Credit risk includes the risk that our customers will not pay their bills, which may lead to a reduction in liquidity and an increase in bad debt expense. Credit risk is comprised of numerous factors including the price of products and services provided, the overall economy and local economies in the geographic areas we serve, including local unemployment rates.

Credit risk also includes the risk that various counterparties that owe us money or product will become insolvent and may breach their obligations. Should the counterparties fail to perform, we may be forced to enter into alternative arrangements. In that event, our financial results could be adversely affected and incur losses.

We may at times have direct credit exposure in our short-term wholesale and commodity trading activity to financial institutions trading for their own accounts or issuing collateral support on behalf of other counterparties. We may also have some indirect credit exposure due to participation in organized markets, such as Southwest Power Pool, Inc., PJM Interconnection, LLC, MISO and Electric Reliability Council of Texas, in which any credit losses are socialized to all market participants.

We have additional indirect credit exposure to financial institutions in the form of letters of credit provided as security by power suppliers under various purchased power contracts. If any of the credit ratings of the letter of credit issuers were to drop below investment grade, the supplier would need to replace that security with an acceptable substitute. If the security were not replaced, the party could be in default under the contract.

As we are a subsidiary of Xcel Energy Inc., we may be negatively affected by events impacting the credit or liquidity of Xcel Energy Inc. and its affiliates.

If either Standard & Poor’s or Moody’s were to downgrade Xcel Energy Inc.’s debt securities below investment grade, it would increase Xcel Energy Inc.’s cost of capital and restrict its access to the capital markets. This could limit Xcel Energy Inc.’s ability to contribute equity or make loans to us, or may cause Xcel Energy Inc. to seek additional or accelerated funding from us in the form of dividends. If such event were to occur, we may need to seek alternative sources of funds to meet our cash needs.

As of Dec. 31, 2019, Xcel Energy Inc. and its utility subsidiaries had approximately $17.4 billion of long-term debt and $1.3 billion of short-term debt and current maturities. Xcel Energy Inc. provides various guarantees and bond indemnities supporting some of its subsidiaries by guaranteeing the payment or performance by these subsidiaries for specified agreements or transactions.

Xcel Energy also has other contingent liabilities resulting from various tax disputes and other matters. Xcel Energy Inc.’s exposure under the guarantees is based upon the net liability of the relevant subsidiary under the specified agreements or transactions. The majority of Xcel Energy Inc.’s guarantees limit its exposure to a maximum amount that is stated in the guarantees.

As of Dec. 31, 2019, Xcel Energy had guarantees outstanding with a maximum stated amount of approximately $2.0 million and immaterial exposure. Xcel Energy also had additional guarantees of $60.4 million at Dec. 31, 2019 for performance and payment of surety bonds for the benefit of itself and its subsidiaries, with total exposure that cannot be estimated at this time. If Xcel Energy Inc. were to become obligated to make payments under these guarantees and bond indemnities or become obligated to fund other contingent liabilities, it could limit Xcel Energy Inc.’s ability to contribute equity or make loans to us, or may cause Xcel Energy Inc. to seek additional or accelerated funding from us in the form of dividends. If such event were to occur, we may need to seek alternative sources of funds to meet our cash needs.

Increasing costs of our defined benefit retirement plans and employee benefits may adversely affect our results of operations, financial condition or cash flows.

We have defined benefit pension and postretirement plans that cover most of our employees. Assumptions related to future costs, return on investments, interest rates and other actuarial assumptions have a significant impact on our funding requirements related to these plans. Estimates and assumptions may change. In addition, the Pension Protection Act changed the minimum funding requirements for defined benefit pension plans. Therefore, our funding requirements and related contributions may change in the future. Also, the payout of a significant percentage of pension plan liabilities in a single year due to high numbers of retirements or employees leaving NSP-Minnesota could trigger settlement accounting and could require NSP-Minnesota to recognize incremental pension expense related to unrecognized plan losses in the year liabilities are paid. Changes in industry standards utilized in key assumptions (e.g., mortality tables) could have a significant impact on future liabilities and benefit costs.

Increasing costs associated with health care plans may adversely affect our results of operations.

Increasing levels of large individual health care claims and overall health care claims could have an adverse impact on our results of operations, financial condition or cash flows. Health care legislation could also significantly impact our benefit programs and costs.

Federal tax law may significantly impact our business.

NSP-Minnesota collects through regulated rates estimated federal, state and local tax payments. Changes to federal tax law may benefit or adversely affect our earnings and customer costs. Tax depreciable lives and the value of various tax credits or the timeliness of their utilization may impact the economics or selection of resources. There could be timing delays before regulated rates provide for realization of tax changes in revenues. In addition, certain IRS tax policies such as tax normalization may impact our ability to economically deliver certain types of resources relative to market prices.

Macroeconomic Risks

Economic conditions impact our business.

Our operations are affected by local, national and worldwide economic conditions, which correlates to customers/sales growth (decline). Economic conditions may be impacted by insufficient financial sector liquidity leading to potential increased unemployment, which may impact customers’ ability to pay their bills which could lead to additional bad debt expense.

Additionally, NSP-Minnesota faces competitive factors, which could have an adverse impact on our financial condition, results of operations and cash flows. Further, worldwide economic activity impacts the demand for basic commodities necessary for utility infrastructure, which may inhibit our ability to acquire sufficient supplies. We operate in a capital intensive industry and federal trade policy could significantly impact the cost of materials we use. There may be delays before these additional material costs can be recovered in rates.

Operations could be impacted by war, terrorism or other events.

Our generation plants, fuel storage facilities, transmission and distribution facilities and information and control systems may be targets of terrorist activities. Any disruption could impact operations or result in a decrease in revenues and additional costs to repair and insure our assets. These disruptions could have a material impact on our financial condition, results of operations or cash flows. The potential for terrorism has subjected our operations to increased risks and could have a material effect on our business. We have already incurred increased costs for security and capital expenditures in response to these risks. The insurance industry has also been affected by these events and the availability of insurance may decrease. In addition, insurance may have higher deductibles, higher premiums and more restrictive policy terms.

A disruption of the regional electric transmission grid, interstate natural gas pipeline infrastructure or other fuel sources, could negatively impact our business, our brand and reputation. Because our facilities are part of an interconnected system, we face the risk of possible loss of business due to a disruption caused by the actions of a neighboring utility.

We also face the risks of possible loss of business due to significant events such as severe storm, severe temperature extremes, wildfires, widespread pandemic, generator or transmission facility outage, pipeline rupture, railroad disruption, operator error, sudden and significant increase or decrease in wind generation or a disruption of work force within our operating systems (or on a neighboring system).

The recent coronavirus outbreak in China is an example of how major catastrophic events throughout the world may disrupt our business. While we are a domestic company, the Company participates in a global supply chain, which includes materials and components that are sourced from China. A prolonged disruption could result in the delay of equipment and materials that may impact our ability to reliably serve our customers.

Disruption due to events such as those noted above could result in a significant decrease in revenues and significant additional costs to repair assets, which could have a material impact on our results of operations, financial condition or cash flows.

NSP-Minnesota participates in biennial grid security and emergency response exercises (GridEx). These efforts, led by the NERC, test and further develop the coordination, threat sharing, and interaction between utilities and various government agencies relative to potential cyber and physical threats against the nation’s electric grid.

A cyber incident or security breach could have a material effect on our business.

We operate in an industry that requires the continued operation of sophisticated information technology, control systems and network infrastructure. In addition, we use our systems and infrastructure to create, collect, use, disclose, store, dispose of and otherwise process sensitive information, including company data, customer energy usage data, and personal information regarding customers, employees and their dependents, contractors and other individuals.

Our generation, transmission, distribution and fuel storage facilities, information technology systems and other infrastructure or physical assets, as well as information processed in our systems (e.g., information regarding our customers, employees, operations, infrastructure and assets) could be affected by cyber security incidents, including those caused by human error. Our industry has been the target of several attacks on operational systems and has seen an increased volume and sophistication of cyber security incidents from international activist organizations, Nation States and individuals. Cyber security incidents could harm our businesses by limiting our generating, transmitting and distributing capabilities, delaying our development and construction of new facilities or capital improvement projects to existing facilities, disrupting our customer operations or causing the release of customer information, all of which would likely receive state and federal regulatory scrutiny and could expose us to liability.

Our generation, transmission systems and natural gas pipelines are part of an interconnected system. Therefore, a disruption caused by the impact of a cyber security incident of the regional electric transmission grid, natural gas pipeline infrastructure or other fuel sources of our third-party service providers’ operations, could also negatively impact our business.

Our supply chain for procurement of digital equipment may expose software or hardware to these risks and could result in a breach or significant costs of remediation. We are unable to quantify the potential impact of cyber security threats or subsequent related actions. Cyber security incidents and regulatory action could result in a material decrease in revenues and may cause significant additional costs (e.g., penalties, third-party claims, repairs, insurance or compliance) and potentially disrupt our supply and markets for natural gas, oil and other fuels.

We maintain security measures to protect our information technology and control systems, network infrastructure and other assets. However, these assets and the information they process may be vulnerable to cyber security incidents, including asset failure or unauthorized access to assets or information. A failure or breach of our technology systems or those of our third-party service providers could disrupt critical business functions and may negatively impact our business, our brand, and our reputation. The cyber security threat is dynamic and evolves continually, and our efforts to prioritize network protection may not be effective given the constant changes to threat vulnerability.

Our operating results may fluctuate on a seasonal and quarterly basis and can be adversely affected by milder weather.

Our electric and natural gas utility businesses are seasonal and weather patterns can have a material impact on our operating performance. Demand for electricity is often greater in the summer and winter months associated with cooling and heating. Because natural gas is heavily used for residential and commercial heating, the demand depends heavily upon weather patterns. A significant amount of natural gas revenues are recognized in the first and fourth quarters related to the heating season. Accordingly, our operations have historically generated less revenues and income when weather conditions are milder in the winter and cooler in the summer. Unusually mild winters and summers could have an adverse effect on our financial condition, results of operations or cash flows.

Public Policy Risks

We may be subject to legislative and regulatory responses to climate change, with which compliance could be difficult and costly.

Legislative and regulatory responses related to climate change and new interpretations of existing laws create financial risk as our facilities may be subject to additional regulation at either the state or federal level in the future. Such regulations could impose substantial costs on our system.

We may be subject to climate change lawsuits. An adverse outcome could require substantial capital expenditures and possibly require payment of substantial penalties or damages. Defense costs associated with such litigation can also be significant and could affect results of operations, financial condition or cash flows if such costs are not recovered through regulated rates.

Although the United States has not adopted any international or federal GHG emission reduction targets, many states and localities may continue to pursue climate policies in the absence of federal mandates. The steps that NSP-Minnesota has taken to date to reduce GHG emissions, including energy efficiency measures, adding renewable generation or retiring or converting coal plants to natural gas, occurred under state-endorsed resource plans, renewable energy standards and other state policies. While those actions likely would have put NSP-Minnesota in a good position to meet federal or international standards being discussed, the lack of federal action does not adversely impact these state-endorsed actions and plans.

If our regulators do not allow us to recover all or a part of the cost of capital investment or the O&M costs incurred to comply with the mandates, it could have a material effect on our results of operations, financial condition or cash flows.

Increased risks of regulatory penalties could negatively impact our business.

The Energy Act increased civil penalty authority for violation of FERC statutes, rules and orders. The FERC can impose penalties of up to $1.3 million per violation per day, particularly as it relates to energy trading activities for both electricity and natural gas. In addition, NERC electric reliability standards and critical infrastructure protection requirements are mandatory and subject to potential financial penalties. Also, the PHMSA, Occupational Safety and Health Administration and other federal agencies have the authority to assess penalties. In the event of serious incidents, these agencies have become more active in pursuing penalties. Some states additionally have the authority to impose substantial penalties. If a serious reliability, cyber or safety incident did occur, it could have a material effect on our results of operations, financial condition or cash flows.

Environmental Risks

We are subject to environmental laws and regulations, with which compliance could be difficult and costly.

We are subject to environmental laws and regulations that affect many aspects of our operations, including air emissions, water quality, wastewater discharges and the generation, transport and disposal of solid wastes and hazardous substances. Laws and regulations require us to obtain permits, licenses, and approvals and to comply with a variety of environmental requirements.

Environmental laws and regulations can also require us to restrict or limit the output of facilities or the use of certain fuels, shift generation to lower-emitting facilities, install pollution control equipment, clean up spills and other contamination and correct environmental hazards. Environmental regulations may also lead to shutdown of existing facilities. Failure to meet requirements of environmental mandates may result in fines or penalties. We may be required to pay all or a portion of the cost to remediate (i.e., clean-up) sites where our past activities, or the activities of other parties, caused environmental contamination.

We are subject to mandates to provide customers with clean energy, renewable energy and energy conservation offerings. It could have a material effect on our results of operations, financial condition or cash flows if our regulators do not allow us to recover the cost of capital investment or the O&M costs incurred to comply with the requirements.

In addition, existing environmental laws or regulations may be revised, and new laws or regulations may be adopted. We may also incur additional unanticipated obligations or liabilities under existing environmental laws and regulations.

We are subject to physical and financial risks associated with climate change and other weather, natural disaster and resource depletion impacts.

Climate change can create physical and financial risk. Physical risks include changes in weather conditions and extreme weather events.

Our customers’ energy needs vary with weather. To the extent weather conditions are affected by climate change, customers’ energy use could increase or decrease. Increased energy use due to weather changes may require us to invest in generating assets, transmission and infrastructure. Decreased energy use due to weather changes may result in decreased revenues.

Climate change may impact a region’s economy, which could impact our sales and revenues. The price of energy has an impact on the economic health of our communities. The cost of additional regulatory requirements, such as regulation of GHG, could impact the availability of goods and prices charged by our suppliers which would normally be borne by consumers through higher prices for energy and purchased goods. To the extent financial markets view climate change and emissions of GHGs as a financial risk, this could negatively affect our ability to access capital markets or cause us to receive less than ideal terms and conditions.

Severe weather impacts our service territories, primarily when thunderstorms, flooding, tornadoes, wildfires and snow or ice storms occur. Extreme weather conditions in general require system backup and can contribute to increased system stress, including service interruptions. Extreme weather conditions creating high energy demand may raise electricity prices, increasing the cost of energy we provide to our customers.

To the extent the frequency of extreme weather events increases, this could increase our cost of providing service. Periods of extreme temperatures could impact our ability to meet demand. Changes in precipitation resulting in droughts or water shortages could adversely affect our operations. Drought conditions also contribute to the increase in wildfire risk from our electric generation facilities. While we carry liability insurance, given an extreme event, if NSP-Minnesota was found to be liable for wildfire damages, amounts that potentially exceed our coverage could negatively impact our results of operations, financial condition or cash flows. Drought or water depletion could adversely impact our ability to provide electricity to customers, cause early retirement of units and increase the price paid for energy. We may not recover all costs related to mitigating these physical and financial risks.

|

|

| ITEM 1B — UNRESOLVED STAFF COMMENTS |

None.

Virtually all of the utility plant property of NSP-Minnesota is subject to the lien of its first mortgage bond indenture.

|

| | | | | | | | |

NSP-Minnesota

Station, Location and Unit | | Fuel | | Installed | | MW (a) | |

| Steam: | | | | | | | |

| A.S. King-Bayport, MN, 1 Unit | | Coal | | 1968 | | 511 |

| |

| Sherco-Becker, MN | | | | | | | |

| Unit 1 | | Coal | | 1976 | | 680 |

| |

| Unit 2 | | Coal | | 1977 | | 682 |

| |

| Unit 3 | | Coal | | 1987 | | 517 |

| (b) |

| Monticello MN, 1 Unit | | Nuclear | | 1971 | | 617 |

| |

| PI-Welch, MN | | | | | | | |

| Unit 1 | | Nuclear | | 1973 | | 521 |

| |

| Unit 2 | | Nuclear | | 1974 | | 519 |

| |

| Various locations, 4 Units | | Wood/Refuse | | Various | | 36 |

| (c) |

| Combustion Turbine: | | | | | | | |

| Angus Anson-Sioux Falls, SD, 3 Units | | Natural Gas | | 1994 - 2005 | | 327 |

| |

| Black Dog-Burnsville, MN, 3 Units | | Natural Gas | | 1987 - 2018 | | 494 |

| |

| Blue Lake-Shakopee, MN, 6 Units | | Natural Gas | | 1974 - 2005 | | 453 |

| |

| High Bridge-St. Paul, MN, 3 Units | | Natural Gas | | 2008 | | 530 |

| |

| Inver Hills-Inver Grove Heights, MN, 6 Units | | Natural Gas | | 1972 | | 282 |

| |

| Riverside-Minneapolis, MN, 3 Units | | Natural Gas | | 2009 | | 454 |

| |

| Various locations, 7 Units | | Natural Gas | | Various | | 10 |

| |

| Wind: | | | | | | | |

| Border-Rolette County, ND, 75 Units | | Wind | | 2015 | | 148 |

| (d) |

| Courtenay Wind-Stutsman County, ND, 100 Units | | Wind | | 2016 | | 190 |

| (d) |

| Foxtail-Dickey County, ND, 75 Units | | Wind | | 2019 | | 150 |

| (d) |

| Grand Meadow-Mower County, MN, 67 Units | | Wind | | 2008 | | 99 |

| (d) |

| Lake Benton-Pipestone County, MN, 44 Units | | Wind | | 2019 | | 99 |

| (d) |

| Nobles-Nobles County, MN, 134 Units | | Wind | | 2010 | | 197 |

| (d) |

| Pleasant Valley-Mower County, MN, 100 Units | | Wind | | 2015 | | 196 |

| (d) |

| | | | | Total | | 7,712 |

| |

| |

(a) | Summer 2019 net dependable capacity. |

| |

(b) | Based on NSP-Minnesota’s ownership of 59%. |

| |

(c) | Refuse-derived fuel is made from municipal solid waste. |

| |

(d) | Values disclosed are the maximum generation levels for these wind units. Capacity is attainable only when wind conditions are sufficiently available (on-demand net dependable capacity is zero). |

Electric utility overhead and underground transmission and distribution lines (measured in conductor miles) at Dec. 31, 2019:

|

| | |

| Conductor Miles | |

| 500 KV | 2,917 |

|

| 345 KV | 13,133 |

|

| 230 KV | 2,203 |

|

| 161 KV | 673 |

|

| 115 KV | 8,045 |

|

| Less than 115 KV | 86,743 |

|

NSP-Minnesota had 346 electric utility transmission and distribution substations at Dec. 31, 2019.

Natural gas utility mains at Dec. 31, 2019:

|

| | |

| Miles | |

| Transmission | 86 |

|

| Distribution | 10,518 |

|

|

|

| ITEM 3 — LEGAL PROCEEDINGS |

NSP-Minnesota is involved in various litigation matters in the ordinary course of business. The assessment of whether a loss is probable or is a reasonable possibility, and whether the loss or a range of loss is estimable, often involves a series of complex judgments about future events. Management maintains accruals for losses probable of being incurred and subject to reasonable estimation. Management is sometimes unable to estimate an amount or range of a reasonably possible loss in certain situations, including but not limited to when (1) the damages sought are indeterminate, (2) the proceedings are in the early stages, or (3) the matters involve novel or unsettled legal theories. In such cases, there is considerable uncertainty regarding the timing or ultimate resolution of such matters, including a possible eventual loss. For current proceedings not specifically reported herein, management does not anticipate that the ultimate liabilities, if any, would have a material effect on NSP-Minnesota’s financial statements. Unless otherwise required by GAAP, legal fees are expensed as incurred.

See Note 10 to the consolidated financial statements, Item 1 and Item 7 for further information.

|

|

ITEM 4 — MINE SAFETY DISCLOSURES

|

None.

PART II

|

|

| ITEM 5 — MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

NSP-Minnesota is a wholly owned subsidiary of Xcel Energy Inc. and there is no market for its common equity securities.

The dividends declared during 2019 and 2018 were as follows:

|

| | | | | | | | |

| (Millions of Dollars) | | 2019 | | 2018 |

| First quarter | | $ | 94.6 |

| | $ | 84.6 |

|

| Second quarter | | 95.3 |

| | 88.7 |

|

| Third quarter | | 94.0 |

| | 184.2 |

|

| Fourth quarter | | 194.3 |

| | 82.7 |

|

|

|

| ITEM 6 — SELECTED FINANCIAL DATA |

This is omitted per conditions set forth in general instructions I(1)(a) and (b) of Form 10-K for wholly owned subsidiaries (reduced disclosure format).

|

|

| ITEM 7 — MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Discussion of financial condition and liquidity for NSP-Minnesota is omitted per conditions set forth in general instructions I(1)(a) and (b) of Form 10-K for wholly owned subsidiaries. It is replaced with management’s narrative analysis and the results of operations for the current year as set forth in general instructions I(2)(a) of Form 10-K for wholly owned subsidiaries (reduced disclosure format).

Non-GAAP Financial Measures

The following discussion includes financial information prepared in accordance with GAAP, as well as certain non-GAAP financial measures such as, electric margin, natural gas margin, and ongoing earnings. Generally, a non-GAAP financial measure is a measure of a company’s financial performance, financial position or cash flows that excludes (or includes) amounts that are adjusted from measures calculated and presented in accordance with GAAP. NSP-Minnesota’s management uses non-GAAP measures for financial planning and analysis, for reporting of results to the Board of Directors, in determining performance-based compensation and communicating its earnings outlook to analysts and investors. Non-GAAP financial measures are intended to supplement investors’ understanding of our performance and should not be considered alternatives for financial measures presented in accordance with GAAP. These measures are discussed in more detail below and may not be comparable to other companies’ similarly titled non-GAAP financial measures.

Electric and Natural Gas Margins

Electric margin is presented as electric revenues less electric fuel and purchased power expenses. Natural gas margin is presented as natural gas revenues less the cost of natural gas sold and transported. Expenses incurred for electric fuel and purchased power and the cost of natural gas are generally recovered through various regulatory recovery mechanisms. As a result, changes in these expenses are generally offset in operating revenues.

Management believes electric and natural gas margins provide the most meaningful basis for evaluating our operations because they exclude the revenue impact of fluctuations in these expenses. These margins can be reconciled to operating income, a GAAP measure, by including other operating revenues, cost of sales-other, O&M expenses, conservation and DSM expenses, depreciation and amortization and taxes (other than income taxes).

Earnings Adjusted for Certain Items (Ongoing Earnings)

Ongoing earnings reflect adjustments to GAAP earnings (net income) for certain items.

We use these non-GAAP financial measures to evaluate and provide details of NSP-Minnesota’s core earnings and underlying performance. We believe these measurements are useful to investors to evaluate the actual and projected financial performance and contribution of NSP-Minnesota. For the years ended Dec. 31, 2019 and Dec. 31, 2018, there were no adjustments to GAAP earnings and therefore GAAP earnings equal ongoing earnings.

2019 Comparison with 2018

NSP-Minnesota’s net income was approximately $542.6 million for 2019, compared with approximately $492.3 million for 2018. The increase in earnings was driven by a higher electric margin resulting from regulatory rate outcomes and capital riders and lower O&M, partially offset by increased depreciation.

Electric Margin