OMB APPROVAL

OMB Number: 3235-0570

Expires: October 31, 2006

Estimated average burden hours per response: 19.3

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-10223

ING Senior Income Fund

(Exact name of registrant as specified in charter)

7337 E. Doubletree Ranch Rd., Scottsdale, AZ | | 85258 |

(Address of principal executive offices) | | (Zip code) |

The Corporation Trust Company, 1209 Orange

Street, Wilmington, DE 19801

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-800-992-0180

Date of fiscal year end: | February 28 |

| |

Date of reporting period: | February 28, 2006 |

Item 1. Reports to Stockholders.

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1):

Annual Report

February 28, 2006

ING Senior Income Fund

E-Delivery Sign-up – details inside

E-Delivery Sign-up – details inside

This report is submitted for general information to shareholders of the ING Funds. It is not authorized for distribution to prospective shareholders unless accompanied or preceded by a prospectus which includes details regarding the funds’ investment objectives, risks, charges, expenses and other information. This information should be read carefully. | |

|

|

|

ING Senior Income Fund |

|

|

ANNUAL REPORT |

|

February 28, 2006 |

|

| | |

|

Table of Contents |

|

Portfolio Managers’ Report | 3 | |

| | |

Report of Independent Public Accounting Firm | 9 | |

| | |

Statement of Assets and Liabilities | 10 | |

| | |

Statement of Operations | 12 | |

| | |

Statements of Changes in Net Assets | 13 | |

| | |

Statement of Cash Flows | 14 | |

| | |

Financial Highlights | 15 | |

| | |

Notes to Financial Statements | 17 | |

| | |

Additional Information | 26 | |

| | |

Portfolio of Investments | 27 | |

| | |

Tax Information | 59 | |

| | |

Trustee and Officer Information | 60 | |

| | |

Advisory Contract Approval Discussion | 65 | |

| | |

| | |

|

|

| | | | |

| | |

| Go Paperless with E-Delivery! |

|

|

Sign up now for on-line prospectuses, fund reports, and proxy statements. In less than five minutes, you can help reduce paper mail and lower fund costs. |

|

Just go to www.ingfunds.com, click on the E-Delivery icon from the home page, follow the directions and complete the quick 5 Steps to Enroll. |

|

You will be notified by e-mail when these communications become available on the internet. Documents that are not available on the internet will continue to be sent by mail. |

|

(THIS PAGE INTENTIONALLY LEFT BLANK)

ING Senior Income Fund

PORTFOLIO MANAGERS’ REPORT |

Dear Shareholders:

ING Senior Income Fund (the “Fund”) is a continuously offered, diversified and closed-end management investment company that seeks to provide investors with a high level of monthly income. The Fund seeks to achieve this objective by investing in a professionally managed portfolio comprised primarily of senior loans.

| | |

| PORTFOLIO CHARACTERISTICS

AS OF FEBRUARY 28, 2006 | |

| | | | |

| Net Assets | | $2,147,009,918 | |

| | | | |

| Total Assets | | $2,664,499,954 | |

| | | | |

| Assets Invested in Senior Loans | | $2,588,497,820 | |

| | | | |

| Senior Loans Represented | | 521 | |

| | | | |

| Average Amount Outstanding per Loan | | $4,968,326 | |

| | | | |

| Industries Represented | | 39 | |

| | | | |

| Average Loan Amount per Industry | | $66,371,739 | |

| | | | |

| Portfolio Turnover Rate | | 82% | |

| | | | |

| Weighted Average Days to Interest Rate Reset | | 41 | |

| | | | |

| Average Loan Final Maturity | | 65 months | |

| | | | |

| Total Leverage as a Percentage of Total Assets | | 14.6% | |

| | | | |

PERFORMANCE SUMMARY

During the year ended February 28, 2006, the Fund’s Class A and Q shares each distributed total dividends from income of $0.78, resulting in an average annualized distribution rate of 5.89%(1) and 5.91%(1), respectively. During the same period, the Fund’s Class B and Class C shares each distributed total dividends from income of $0.70, resulting in an average annualized distribution rate of

5.40%(1) for Class B shares and 5.39%(1) for Class C shares.

The Fund’s total return for the year ended February 28, 2006, for each of the share classes, excluding sales charges, ranged from 4.96% on Class A, 4.37% on Class B, 4.44% on Class C and 4.97% on Class Q. The Fund’s net returns were slightly less than the returns of the S&P/LSTA Leveraged Loan Index (“LLI”), which had a gross return of 5.62%.

MARKET OVERVIEW

The LLI posted a solid 5.62% gross return for the twelve month period ended February 28, 2006, or roughly 2.16% in excess of average one month London Inter-Bank Offered Rate (“LIBOR”). It continues to be favorable times but, by some accounts, very challenging times for loan investors, as market conditions remain highly charged. Demand for loans continues to be exceptionally strong as long-established loan buyers (such as the Fund) and, increasingly, non-traditional investors including hedge funds and high-yield bond investors look to floating rate loans as a hedge against rising rates. During the first quarter of 2006, the number of investor groups actively trading loans was estimated at 235, up from approximately 170 at the end of 2004.

As noted in our last report, increased competition has made sourcing new loan investments more demanding for all active investors and, in turn, has driven average borrowing (or credit) spreads on loans to new lows. Fortunately, on the other side of the equation, the available supply of new loans has generally maintained pace, buoyed by robust merger and acquisition activity, sustained economic strength and low relative borrowing rates. Institutional loan volume surged to $72 billion during the first quarter of 2006, up from $46 billion during the previous calendar quarter,

(1) The distribution rate is calculated by annualizing dividends declared during the period and dividing the resulting annualized dividend by the Fund’s average month-end net asset value (in the case of NAV) or the average month-end NYSE Composite closing price (in the case of Market). The distribution rate is based solely on the actual dividends and distributions, which are made at the discretion of management. The distribution rate may or may not include all investment income and ordinarily will not include capital gains or losses, if any.

3

ING Senior Income Fund

PORTFOLIO MANAGERS’ REPORT (continued) |

and topping the prior high water mark of $52 billion during the first quarter of 20051.

While new deal volume has been quite good, it has also been inconsistent at best and, at times, painfully uneven. When new issuance activity slows down, the pace of borrowing spread re-pricing (lower) inevitably heats up. As a result, credit spreads on new loans have continued on a flat to downward path, and secondary loan prices have remained very firm, even, in some cases, in the face of negative company-specific credit developments. In short, like most other capital markets, loan investors currently reside within a very liquidity-driven environment.

Credit conditions and the direction of short-term interest rates remain the primary focus of loan investors, and paramount to overall loan performance. Default rates continued to grind upward in fiscal 2006, ending the period at 2.08%, versus 1.98% at the end of calendar 2005, but still well shy of the average over the last full credit cycle. Digging more deeply into the default statistics reveals a high concentration in a small number of industries (traditional automotive suppliers and domestic commercial airlines, areas in which the Fund has been significantly underweight for some time).

Generally speaking, the broader U.S. economy remains on solid footing from a Gross Domestic Product and job growth perspective, while inflation, although showing signs of escalating, remains within acceptable ranges. It is, however, that threat of rising wholesale and retail prices that seemingly perpetuates a hawkish stance from the Federal Reserve (“Fed”). While senior loans have been proven an all-weather asset class, they historically have performed exceptionally well in periods of rising short-term interest rates.

|

TOP TEN INDUSTRY SECTORS AS OF

FEBRUARY 28, 2006 AS A

PERCENTAGE OF: |

| | TOTAL

ASSETS | | NET

ASSETS | |

North American Cable | | 9.3 | % | | 11.5 | % | |

Healthcare, Education and Childcare | | 8.5 | % | | 10.5 | % | |

Chemicals, Plastics & Rubber | | 6.9 | % | | 8.6 | % | |

Oil & Gas | | 5.5 | % | | 6.8 | % | |

Printing & Publishing | | 4.8 | % | | 6.0 | % | |

Buildings & Real Estate | | 4.8 | % | | 6.0 | % | |

Utilities | | 4.7 | % | | 5.8 | % | �� |

Leisure, Amusement, Entertainment | | 3.8 | % | | 4.7 | % | |

Automobile | | 3.7 | % | | 4.6 | % | |

Containers, Packaging & Glass | | 3.7 | % | | 4.6 | % | |

| | | | | | | |

Portfolio holdings are subject to change daily. |

|

|

TOP TEN SENIOR LOAN ISSUERS

AS OF FEBRUARY 28, 2006

AS A PERCENTAGE OF: |

| | TOTAL

ASSETS | | NET

ASSETS | |

Charter Communications Operating, LLC | | 2.4 | % | | 3.0 | % | |

Metro-Goldwyn-Mayer Studios, Inc. | | 1.9 | % | | 2.4 | % | |

Georgia-Pacific Corporation | | 1.8 | % | | 2.3 | % | |

Sungard Data Systems, Inc. | | 1.4 | % | | 1.8 | % | |

NRG Energy, Inc. | | 1.4 | % | | 1.8 | % | |

Davita, Inc. | | 1.3 | % | | 1.6 | % | |

Fidelity National Information Solutions, Inc. | | 1.2 | % | | 1.5 | % | |

Huntsman International, LLC | | 1.2 | % | | 1.5 | % | |

Community Health Systems, Inc. | | 1.2 | % | | 1.5 | % | |

Targa Resources, Inc. | | 1.2 | % | | 1.5 | % | |

| | | | | | | |

Portfolio holdings are subject to change daily. |

|

PORTFOLIO OVERVIEW

Performance during fiscal 2006 was favorably impacted by constructive asset selection and the avoidance of defaults. The Fund’s top two individual issuers at period-end, Charter Communications Operating LLC (2.4% of total assets) and MGM Studios, Inc. (1.9% of total assets) were, by a fairly wide margin, the two largest contributors to LLI returns for the fiscal year. Detractors to Fund returns were, individually, not significant.

The Fund’s modest underperformance relative to the LLI can be explained largely by what we have chosen to avoid as a matter of credit discipline. Based on a strategy of emphasizing the better quality subset of the loan universe, we have maintained an intentional

4

ING Senior Income Fund

PORTFOLIO MANAGERS’ REPORT (continued) |

underweight of the lowest-rated and second lien components of the market. We continue to view most second lien loans as high-yield bond substitutes with a generally unfavorable risk/return profile under normal market conditions. We also continue to largely shun individual credits that carry excessive debt leverage (typically born out in the lowest of public credit ratings) and those offering less than traditional covenant protections. Although those types of transactions almost always provide above average yields, we continue to believe that the extra compensation does not, in most cases, justify the level of incremental risk.

There were no significant changes in sector positioning during the period. The North American Cable (9.3% of total assets) and Healthcare (8.5% of total assets) sectors closed out the period as the Fund’s top two sector exposures. We continue to view these industry groups as attractive based on a combination of low secured leverage levels and healthy market multiples (i.e., strong collateral coverage), relative price stability and continuity of demand. The lone material change in the Fund’s top sector positioning was a reduction in the Buildings/Real Estate sector to 4.8% from 6.1% of total assets as of the last reporting period (August 31, 2005), this due to sizeable prepayments of a small number of issuers in this sector.

The Fund remains well diversified. The average individual loan position represented approximately 0.19% of total assets at period-end, down from 0.20% at August 31, 2005, while the average industry sector accounted for roughly 2.49%, essentially unchanged from the prior period.

USE OF LEVERAGE

The Fund seeks to prudently utilize financial leverage in order to increase the yield to shareholders. As of February 28, 2006, the Fund had $389 million outstanding under a $750 million revolving credit facility.

OUTLOOK

As of this writing, there do not appear to be any signs on the investment or economic horizons that would point to a change in current loan market dynamics. Credit conditions are expected to remain reasonably stable (Standard & Poor’s Leveraged Commentary & Data is forecasting an improvement in default rates by year-end), and although proving to be very enigmatic, the “new” Fed has, at least thus far, maintained an inflation fighting (i.e., rate-raising) bias. As such, we see no abatement in the overall demand for floating rate secured loans.

Variables to the equation would include the consistency and quality of new loan supply and, as a direct result of how that supply/demand balance takes shape, the direction of credit spreads. While spreads appeared to have bottomed out near the end of 2005, there are fresh indications that they could be headed modestly lower over the near-term. A positive offset to that development would likely be the continuation of very strong secondary loan valuations.

Our strategy remains unchanged: to deliver attractive-risk adjusted returns and moderate NAV volatility. As such, we remain focused on the better quality subset of the loan universe (i.e., better relative credit ratings, traditional first position collateral packages, and standard covenant protections) and will cede excess returns to maintain that strategy.

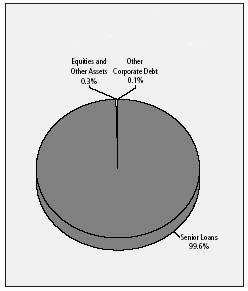

Investment Types |

as of February 28, 2006 |

(as a percent of total investments) |

|

Portfolio holdings are subject to change daily. |

5

ING Senior Income Fund

PORTFOLIO MANAGERS’ REPORT (continued) |

| |

|

| | |

Jeffrey A. Bakalar | | Daniel A. Norman |

Senior Vice President | | Senior Vice President |

Senior Portfolio Manager | | Senior Portfolio Manager |

ING Investment Management Co. | | ING Investment Management Co. |

| | |

| |

|

| | |

ING Senior Income Fund

April 18, 2006

1. Source: Standard & Poor’s Leveraged Commentary & Data

6

ING Senior Income Fund

PORTFOLIO MANAGERS’ REPORT (continued) |

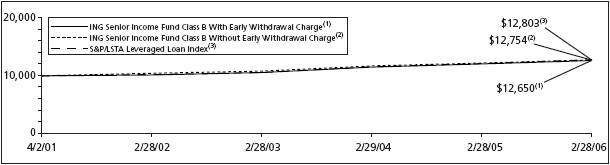

| | Average Annual Total Net Returns for the

Periods Ended February 28, 2006 | |

| | 1 Year | | | | 3 Year | | | | April 2, 2001 | | | December 15, 2000 | |

Including Sales Charge: | | | | | | | | | | |

Class A(1) | | 2.34 | % | | 4.50 | % | | 5.11 | % | | — | | |

Class B(2) | | 1.37 | % | | 5.04 | % | | 4.91 | % | | — | | |

Class C(3) | | 3.44 | % | | 5.68 | % | | 5.11 | % | | — | | |

Class Q | | 4.97 | % | | 6.16 | % | | — | | | 5.56 | % | |

Excluding Sales Charge: | | | | | | | | | | | | | |

Class A | | 4.96 | % | | 6.21 | % | | 5.65 | % | | — | | |

Class B | | 4.37 | % | | 5.64 | % | | 5.08 | % | | — | | |

Class C | | 4.44 | % | | 5.68 | % | | 5.11 | % | | — | | |

Class Q | | 4.99 | % | | 6.16 | % | | — | | | 5.56 | % | |

S&P/LSTA Leveraged Loan Index(4) | | 5.62 | % | | 6.62 | % | | 5.18 | % | | 5.36 | % | |

| | | | | | | | | | | | | | | | | | | |

Based on an initial investment of $10,000, the graph and table above illustrate the total net return of ING Senior Income Fund against the gross return of the LLI. The LLI Index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Fund’s performance is shown both with and without the imposition of sales charges.

Total returns reflect that ING Investments, LLC (the Fund’s Investment Advisor) may have waived, reimbursed or recouped fees and expenses otherwise payable by the Fund.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will fluctuate. Shares, when sold, may be worth more or less than their original cost. The Fund’s future performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month-end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

(1) Reflects deduction of the maximum Class A sales charge of 2.50%. There is no front-end sales charge if you purchase Class A Common Shares in an amount of $1 million or more. However, the shares will be subject to a 1.00% Early Withdrawal Charge (“EWC”) if they are repurchased by the Fund within one year of purchase.

(2) Class B maximum EWC is 3% in the first year, declining to 1% in the fifth year and eliminated thereafter.

(3) Class C maximum EWC is 1% for the first year.

(4) Source: S&P/Loan Syndications and Trading Association. The LLI Index (“LLI”) is an unmanaged total return index that captures accrued interest, repayments, and market value changes. It represents a broad cross section of leveraged loans syndicated in the United States, including dollar-denominated loans to overseas issuers. Standard & Poor’s and the Loan Syndications and Trading Association (“LSTA”) conceived the LLI to establish a performance benchmark for the syndicated leveraged loan industry. An investor cannot invest directly in an index. Since inception performance for the index is shown from March 31, 2001 for Class A, B and C and from December 31, 2000 for Class Q.

7

ING Senior Income Fund

PORTFOLIO MANAGERS’ REPORT (continued) |

|

YIELDS AND DISTRIBUTIONS RATES |

|

| | 30-Day SEC Yields(1) | | Average Annualized Distribution Rates(2) | |

| | Class A | | Class B | | Class C | | Class Q | | Class A | | Class B | | Class C | | Class Q | |

February 28, 2006 | | 5.49 | % | | 5.14 | % | | 5.14 | % | | 5.63 | % | | 5.89 | % | | 5.40 | % | | 5.39 | % | | 5.91 | % | |

August 31, 2005 | | 4.70 | % | | 4.32 | % | | 4.31 | % | | 4.79 | % | | 5.02 | % | | 4.53 | % | | 4.52 | % | | 5.04 | % | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

(1) Yield is calculated by dividing the Fund’s net investment income per share for the most recent thirty days by the net asset value. Yield calculations do not include any commissions or sales charges, and are compounded for six months and annualized for a twelve-month period to derive the Fund’s yield consistent with the Securities Exchange Commission standardized yield formula for open-end investment companies.

(2) Distribution Rates are calculated by annualizing dividends declared during the period (i.e., by dividing the monthly dividend amount by the number of days in the month and multiplying by the number of days in the fiscal year) and then dividing the resulting annualized dividend by the month-ending NAV.

Risk is inherent in all investing. The following are the principal risks associated with investing in the Fund. This is not, and is not intended to be, a description of all risks of investing in the Fund. A more detailed description of the risks of investing in the Fund is contained in the Fund’s current prospectus.

Credit Risk: The Fund invests a substantial portion of its assets in below investment grade senior loans and other below investment grade assets. Below investment grade loans involve a greater risk that borrowers may not make timely payment of the interest and principal due on their loans. They also involve a greater risk that the value of such loans could decline significantly. If borrowers do not make timely payments of the interest due on their loans, the yield on the Fund’s common shares will decrease. If borrowers do not make timely payment of the principal due on their loans, or if the value of such loans decreases, the value of the Fund’s NAV will decrease.

Interest Rate Risk: Changes in short-term market interest rates will directly affect the yield on the Fund’s common shares. If short-term market interest rates fall, the yield on the Fund will also fall. To the extent that the interest rate spreads on loans in the Fund experience a general decline, the yield on the Fund will fall and the value of the Fund’s assets may decrease, which will cause the Fund’s value to decrease. Conversely, when short-term market interest rates rise, because of the lag between changes in such short-term rates and the resetting of the floating rates on assets in the Fund’s portfolio, the impact of rising rates will be delayed to the extent of such lag.

Leverage Risk: The Fund’s use of leverage through borrowings or the issuance of preferred shares can adversely affect the yield on the Fund’s Common Shares. To the extent that the Fund is unable to invest the proceeds from the use of leverage in assets which pay interest at a rate which exceeds the rate paid on the leverage, the yield on the Fund’s Common Shares will decrease. In addition, in the event of a general market decline in the value of assets such as those in which the Fund invests, the effect of that decline will be magnified in the Fund because of the additional assets purchased with the proceeds of the leverage.

No Daily Redemptions: The Fund does not redeem its shares on a daily basis and there is no market for its shares. Shareholders can only redeem their shares once a month, and if redemption requests from all shareholders exceed 5% of the Fund’s total assets in a particular month, the Fund may reduce such requests pro rata and redeem only an amount equal to 5% of its total assets.

8

ING Senior Income Fund

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM |

The Board of Directors and Shareholders of

ING Senior Income Fund

We have audited the accompanying statement of assets and liabilities of ING Senior Income Fund (the “Fund”), including the portfolio of investments, as of February 28, 2006, the related statements of operations and cash flows for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended. These financial statements and financial highlights are the responsibility of management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of February 28, 2006 by correspondence with the custodian and brokers, or by other appropriate auditing procedures. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of ING Senior Income Fund as of February 28, 2006, the results of its operations and its cash flows for the year then ended, the changes in its net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended, in conformity with principles generally accepted in the United States of America

Boston, Massachusetts

April 21, 2006

9

ING Senior Income Fund

STATEMENT OF ASSETS AND LIABILITIES as of February 28, 2006 |

ASSETS: | | | |

Investments in securities at value (Cost $2,571,259,229) | | $ | 2,598,779,418 | |

Cash | | 19,531,638 | |

Receivables: | | | |

Investment securities sold | | 6,011,937 | |

Fund shares sold | | 20,091,727 | |

Interest | | 19,638,619 | |

Reimbursement due from Manager | | 239,283 | |

Prepaid expenses | | 203,440 | |

Prepaid arrangement fees on notes payable | | 3,892 | |

Total assets | | 2,664,499,954 | |

| | | |

LIABILITIES: | | | |

Payable for investment securities purchased | | 120,105,691 | |

Notes payable | | 389,000,000 | |

Accrued interest payable | | 1,735,914 | |

Payable to affilates | | 2,570,218 | |

Income distribution payable | | 2,977,686 | |

Accrued trustees fees | | 16,510 | |

Deferred arrangement fees | | 623,500 | |

Other accrued expenses and liabilities | | 460,517 | |

Total liabilities | | 517,490,036 | |

NET ASSETS | | $ | 2,147,009,918 | |

| | | |

NET ASSETS CONSIST OF: | | | |

Paid-in capital | | $ | 2,126,015,947 | |

Distributions in excess of net Investment Income | | (1,537,786 | ) |

Accumulated net realized loss on investments | | (4,988,432 | ) |

Net unrealized appreciation of investments | | 27,520,189 | |

NET ASSETS | | $ | 2,147,009,918 | |

See Accompanying Notes to Financial Statements

10

ING Senior Income Fund

STATEMENT OF ASSETS AND LIABILITIES as of February 28, 2006 (continued) |

Class A: | | | |

Net assets | | $ | 918,620,500 | |

Shares authorized | | unlimited | |

Par value | | $ | 0.01 | |

Shares outstanding | | 59,029,296 | |

Net asset value and redemption price per share | | $ | 15.56 | |

Maximum offering price per share (2.50%)(1) | | $ | 15.96 | |

| | | | |

Class B: | | | |

Net assets | | $ | 120,253,750 | |

Shares authorized | | unlimited | |

Par value | | $ | 0.01 | |

Shares outstanding | | 7,742,146 | |

Net asset value and redemption price per share(2) | | $ | 15.53 | |

Maximum offering price per share | | $ | 15.53 | |

| | | | |

Class C: | | | |

Net assets | | $ | 923,549,269 | |

Shares authorized | | unlimited | |

Par value | | $ | 0.01 | |

Shares outstanding | | 59,401,816 | |

Net asset value and redemption price per share(2) | | $ | 15.55 | |

Maximum offering price per share | | $ | 15.55 | |

| | | | |

Class Q: | | | |

Net assets | | $ | 184,586,399 | |

Shares authorized | | unlimited | |

Par value | | $ | 0.01 | |

Shares outstanding | | 11,917,850 | |

Net asset value and redemption price per share | | $ | 15.49 | |

Maximum offering price per share | | $ | 15.49 | |

(1) | Maximum offering price is computed at 100/97.50 of net asset value. On purchases of $100,000 or more, the offering price is reduced. |

(2) | Redemption price per share may be reduced for any applicable contingent deferred sales charge. |

See Accompanying Notes to Financial Statements

11

ING Senior Income Fund

STATEMENT OF OPERATIONS for the Year Ended February 28, 2006 |

INVESTMENT INCOME: | | | |

Dividends | | $ | 37,778 | |

Interest | | 141,938,847 | |

Arrangement fees earned | | 937,698 | |

Other | | 2,367,686 | |

Total investment income | | 145,282,009 | |

EXPENSES: | | | |

Investment management fees | | 18,821,167 | |

Administration fees | | 2,352,646 | |

Distribution and service fees: | | | |

Class A | | 2,067,230 | |

Class B | | 1,209,337 | |

Class C | | 6,734,357 | |

Class Q | | 454,630 | |

Transfer agent fees: | | | |

Class A | | 314,432 | |

Class B | | 45,634 | |

Class C | | 339,513 | |

Class Q | | 68,586 | |

Shareholder reporting expense | | 375,750 | |

Interest expense | | 14,211,557 | |

Custodian fees | | 1,058,461 | |

Credit facility fees | | 30,916 | |

Professional fees | | 238,702 | |

Trustees’ fees | | 76,052 | |

Registration fees | | 364,227 | |

Postage expense | | 608,208 | |

Miscellaneous expense | | 92,936 | |

Total expenses | | 49,464,341 | |

Less: | | | |

Net recouped fees | | 178,941 | |

Net expenses | | 49,643,282 | |

Net investment income | | 95,638,727 | |

REALIZED AND UNREALIZED GAIN (LOSS) FROM INVESTMENTS: | | | |

Net realized loss on investments | | (4,748,860 | ) |

Net change in unrealized appreciation on investments | | 3,162,848 | |

Net loss on investments | | (1,586,012 | ) |

Net increase in net assets resulting from operations | | $ | 94,052,715 | |

See Accompanying Notes to Financial Statements

12

ING Senior Income Fund

STATEMENTS OF CHANGES IN NET ASSETS |

| | Year

Ended

February 28, | | Year

Ended

February 28, | |

| | | 2006 | | | | 2005 | | |

INCREASE IN NET ASSETS FROM OPERATIONS: | | | | | |

Net investment income | | $ | 95,638,727 | | $ | 41,435,388 | |

Net realized loss on investments | | (4,748,860 | ) | 4,274,502 | |

Net change in unrealized appreciation

on investments | | 3,162,848 | | 13,321,736 | |

Net increase in net assets resulting

from operations | | 94,052,715 | | 59,031,626 | |

DISTRIBUTIONS TO SHAREHOLDERS: | | | | | |

Net investment income | | | | | |

Class A | | (41,083,708 | ) | (15,392,853 | ) |

Class B | | (5,430,910 | ) | (3,140,818 | ) |

Class C | | (40,253,552 | ) | (17,474,122 | ) |

Class Q | | (9,102,024 | ) | (6,835,055 | ) |

Net realized gain on investments | | | | | |

Class A | | (222,358 | ) | (1,943,784 | ) |

Class B | | (30,632 | ) | (416,134 | ) |

Class C | | (234,761 | ) | (2,526,261 | ) |

Class Q | | (48,368 | ) | (743,837 | ) |

Total distributions | | (96,406,313 | ) | (48,472,864 | ) |

CAPITAL SHARE TRANSACTIONS: | | | | | |

Net proceeds from sale of shares | | 945,527,139 | | 1,640,693,467 | |

Dividends reinvested | | 63,704,837 | | 32,670,018 | |

| | 1,009,231,976 | | 1,673,363,485 | |

Cost of shares repurchased | | (735,409,909 | ) | (477,107,687 | ) |

Net increase in net assets resulting from

capital share transactions | | 273,822,067 | | 1,196,255,798 | |

Net increase in net assets | | 271,468,469 | | 1,206,814,560 | |

NET ASSETS: | | | | | |

Beginning of year | | 1,875,541,449 | | 668,726,889 | |

End of year | | $ | 2,147,009,918 | | $ | 1,875,541,449 | |

Distributions in excess of net investment income

at end of year | | $ | (1,537,786 | ) | $ | (1,298,065 | ) |

| | | | | | | | | | | |

See Accompanying Notes to Financial Statements

13

ING Senior Income Fund

STATEMENT OF CASH FLOWS for the Year Ended February 28, 2006 |

INCREASE (DECREASE) IN CASH Cash Flows From Operating Activities: | | | |

Interest received | | $ | 133,103,682 | |

Dividends received | | 37,778 | |

Facility fees paid | | (34,735 | ) |

Arrangement fee received | | 401,854 | |

Other income received | | 2,454,546 | |

Interest paid | | (12,819,979 | ) |

Other operating expenses paid | | (35,090,915 | ) |

Purchases of investments | | (3,007,883,028 | ) |

Proceeds from disposition of investments | | 2,534,085,579 | |

Net cash used for operating activities | | (385,745,218 | ) |

Cash Flows From Financing Activities: | | | |

Distributions paid to common shareholders | | (31,345,695 | ) |

Proceeds from capital shares sold | | 945,145,844 | |

Disbursements for capital shares repurchased | | (735,409,909 | ) |

Net issuance of notes payable | | 226,000,000 | |

Net cash flows provided by financing activities | | 404,390,240 | |

Net increase in cash | | 18,645,022 | |

Cash at beginning of year | | 886,616 | |

Cash at end of year | | $ | 19,531,638 | |

Reconciliation of Net Increase in Net Assets Resulting from

Operations to Net Cash Used by Operating Activities: | | | |

Net increase in net assets resulting from operations | | $ | 94,052,715 | |

Adjustments to reconcile net increase in net assets resulting from operations to net cash used by operating activities: | | | |

Change in unrealized appreciation on investments | | (3,162,848 | ) |

Net accretion/amortization of discounts on investments | | 123,014 | |

Realized loss on sale of investments | | 4,748,860 | |

Purchases of investments | | (3,007,883,028 | ) |

Proceeds on sale of investments | | 2,534,085,579 | |

Increase in interest receivable | | (8,958,179 | ) |

Increase in prepaid arrangement fees on notes payable | | (3,819 | ) |

Decrease in prepaid expenses and other assets | | 179,301 | |

Decrease in deferred arrangement fees on senior loans | | (535,844 | ) |

Increase in accrued interest payable | | 1,391,578 | |

Increase in reimbursement due from manager | | (239,283 | ) |

Increase in payable to affiliate | | 447,526 | |

Increase in accrued trustee fees | | 11,346 | |

Decrease in accrued expenses | | (2,136 | ) |

Total adjustments | | (479,797,933 | ) |

Net cash used for operating activities | | $ | (385,745,218 | ) |

Non Cash Financing Activities | | | |

Receivable for shares sold | | $ | 20,091,727 | |

Reinvestment of dividends | | $ | 63,704,837 | |

See Accompanying Notes to Financial Statements

14

ING SENIOR INCOME FUND | FINANCIAL HIGHLIGHTS |

Selected data for a share of beneficial interest outstanding throughout each period.

| | Class A | |

| | Year Ended

February 28 or 29, | | April 2,

2001(1) to

February 28, | |

| | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

Per Share Operating Performance: | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 15.59 | | 15.47 | | 14.83 | | 14.92 | | 15.00 | |

Income (loss) from investment operations: | | | | | | | | | | | |

Net investment income | | $ | 0.78 | | 0.55 | | 0.61 | | 0.69 | | 0.81 | |

Net realized and unrealized gain (loss) on investments | | $ | (0.03 | ) | 0.18 | | 0.69 | | (0.09 | ) | (0.09 | ) |

Total income from investment operations | | $ | 0.75 | | 0.73 | | 1.30 | | 0.60 | | 0.72 | |

Less distributions from: | | | | | | | | | | | |

Net investment income | | $ | 0.78 | | 0.56 | | 0.64 | | 0.69 | | 0.80 | |

Net realized gain on investments | | $ | — | | 0.05 | | 0.02 | | — | | — | |

Total distributions | | $ | 0.78 | | 0.61 | | 0.66 | | 0.69 | | 0.80 | |

Net asset value, end of period | | $ | 15.56 | | 15.59 | | 15.47 | | 14.83 | | 14.92 | |

Total Investment Return(2) | | % | 4.96 | | 4.80 | | 8.93 | | 4.15 | | 4.92 | |

Ratios/Supplemental Data: | | | | | | | | | | | |

Net assets, end of period (000’s) | | $ | 918,621 | | 736,740 | | 172,975 | | 11,106 | | 2,411 | |

Average borrowings (000’s)(3) | | $ | 325,044 | | 34,767 | | 20,771 | | 17,655 | | 19,797 | |

Asset coverage per $1,000 of debt | | $ | 6,519 | | 1,251 | | — | * | 689 | | 3,220 | |

Ratios to average net assets after reimbursement/recoupment: | | | | | | | | | | | |

Expenses (before interest and other fees related to revolving credit facility)(4)(5) | | % | 1.50 | | 1.34 | | 1.36 | | 1.42 | | 1.47 | |

Expenses (with interest and other fees related to revolving credit facility)(4)(5) | | % | 2.20 | | 1.45 | | 1.43 | | 1.63 | | 1.73 | |

Net investment income(4)(5) | | % | 4.98 | | 3.49 | | 3.84 | | 4.88 | | 5.58 | |

Ratios to average net assets before reimbursement/recoupment: | | | | | | | | | | | | |

Expenses (before interest and other fees related to revolving credit facility)(4)(5) | | % | 1.48 | | 1.35 | | 1.46 | | 1.57 | | 1.82 | |

Expenses (with interest and other fees related to revolving credit facility)(4)(5) | | % | 2.18 | | 1.46 | | 1.53 | | 1.78 | | 2.07 | |

Net investment income(4)(5) | | % | 5.00 | | 3.48 | | 3.74 | | 4.73 | | 5.26 | |

Portfolio turnover rate% | | 82 | | 82 | | 72 | | 60 | | 65 | |

Shares outstanding at end of period (000’s) | | 59,029 | | 47,252 | | 11,180 | | 749 | | 162 | |

| | | | | | | | | | | | | | | | | | | |

| | Class B | |

| | Year Ended

February 28 or 29, | | April 2,

2001(1) to

February 28, | |

| | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

Per Share Operating Performance: | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 15.57 | | 15.45 | | 14.82 | | 14.92 | | 15.00 | |

Income (loss) from investment operations: | | | | | | | | | | | |

Net investment income | | $ | 0.70 | | 0.47 | ** | 0.53 | | 0.62 | | 0.75 | |

Net realized and unrealized gain (loss) on investments | | $ | (0.04 | ) | 0.18 | ** | 0.69 | | (0.10 | ) | (0.10 | ) |

Total income from investment operations | | $ | 0.66 | | 0.65 | | 1.22 | | 0.52 | | 0.65 | |

Less distributions from: | | | | | | | | | | | |

Net investment income | | $ | 0.70 | | 0.48 | | 0.57 | | 0.62 | | 0.73 | |

Net realized gain on investments | | $ | — | | 0.05 | | 0.02 | | — | | — | |

Total distributions | | $ | 0.70 | | 0.53 | | 0.59 | | 0.62 | | 0.73 | |

Net asset value, end of period | | $ | 15.53 | | 15.57 | | 15.45 | | 14.82 | | 14.92 | |

Total Investment Return(2) | | % | 4.37 | | 4.28 | | 8.33 | | 3.57 | | 4.45 | |

Ratios/Supplemental Data: | | | | | | | | | | | |

Net assets, end of period (000’s) | | $ | 120,254 | | 125,200 | | 62,852 | | 17,648 | | 12,776 | |

Average borrowings (000’s)(3) | | $ | 325,044 | | 34,767 | | 20,771 | | 17,655 | | 19,797 | |

Asset coverage per $1,000 of debt | | $ | 6,519 | | 1,251 | | — | * | 689 | | 3,220 | |

Ratios to average net assets after reimbursement/recoupment: | | | | | | | | | | | |

Expenses (before interest and other fees related to revolving credit facility)(4)(5) | | % | 1.99 | | 1.87 | | 1.87 | | 1.91 | | 1.96 | |

Expenses (with interest and other fees related to revolving credit facility)(4)(5) | | % | 2.69 | | 1.94 | | 1.97 | | 2.09 | | 2.23 | |

Net investment income(4)(5) | | % | 4.45 | | 2.93 | | 3.47 | | 4.12 | | 5.19 | |

Ratios to average net assets before reimbursement/recoupment: | | | | | | | | | | | | |

Expenses (before interest and other fees related to revolving credit facility)(4)(5) | | % | 1.97 | | 2.13 | | 2.22 | | 2.31 | | 2.29 | |

Expenses (with interest and other fees related to revolving credit facility)(4)(5) | | % | 2.67 | | 2.19 | | 2.31 | | 2.49 | | 2.54 | |

Net investment income(4)(5) | | % | 4.47 | | 2.67 | | 3.13 | | 3.72 | | 4.89 | |

Portfolio turnover rate | | % | 82 | | 82 | | 72 | | 60 | | 65 | |

Shares outstanding at end of period (000’s) | | 7,742 | | 8,043 | | 4,068 | | 1,191 | | 856 | |

| | | | | | | | | | | | | | | | | | | |

(1) Commencement of operations.

(2) Total investment returns are not annualized for periods of less than one year and do not include sales load.

(3) Based on the active days of borrowing.

(4) Annualized for periods less than one year.

(5) The Investment Manager has agreed to limit expenses excluding interest, taxes, brokerage commissions, leverage expenses, other investment related costs and extraordinary expenses, subject to possible recoupment by the Investment Manager within three years to the following:

Class A – 0.90% of Managed Assets plus 0.45% of average daily net assets

Class B – 0.90% of Managed Assets plus 1.20% of average daily net assets

Class C – 0.90% of Managed Assets plus 0.95% of average daily net assets

Class Q – 0.90% of Managed Assets plus 0.45% of average daily net assets

* There were no loans outstanding at period end.

** Per share numbers have been calculated using the monthly average share method, which more appropriately represents the per share data for the period.

See Accompanying Notes to Financial Statements

15

ING SENIOR INCOME FUND (CONTINUED) | FINANCIAL HIGHLIGHTS |

Selected data for a share of beneficial interest outstanding throughout each period.

| | Class C | |

| | Year Ended

February 28 or 29, | | April 2,

2001(1) to

February 28, | |

| | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

Per Share Operating Performance: | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 15.58 | | 15.46 | | 14.82 | | 14.92 | | 15.00 | |

Income (loss) from investment operations: | | | | | | | | | | | |

Net investment income | | $ | 0.70 | | 0.47 | | 0.53 | | 0.62 | | 0.75 | |

Net realized and unrealized gain (loss) on investments | | $ | (0.03 | ) | 0.18 | | 0.70 | | (0.10 | ) | (0.10 | ) |

Total income from investment operations | | $ | 0.67 | | 0.65 | | 1.23 | | 0.52 | | 0.65 | |

Less distributions from: | | | | | | | | | | | |

Net investment income | | $ | 0.70 | | 0.48 | | 0.57 | | 0.62 | | 0.73 | |

Net realized gain on investments | | $ | — | | 0.05 | | 0.02 | | — | | — | |

Total distributions | | $ | 0.70 | | 0.53 | | 0.59 | | 0.62 | | 0.73 | |

Net asset value, end of period | | $ | 15.55 | | 15.58 | | 15.46 | | 14.82 | | 14.92 | |

Total Investment Return(2) | | % | 4.44 | | 4.28 | | 8.40 | | 3.57 | | 4.45 | |

Ratios/Supplemental Data: | | | | | | | | | | | |

Net assets, end of period (000’s) | | $ | 923,549 | | 830,584 | | 275,849 | | 32,647 | | 19,391 | |

Average borrowings (000’s)(3) | | $ | 325,044 | | 34,767 | | 20,771 | | 17,655 | | 19,797 | |

Asset coverage per $1,000 of debt | | $ | 6,519 | | 1,251 | | — | * | 689 | | 3,220 | |

Ratios to average net assets after reimbursement/recoupment: | | | | | | | | | | | |

Expenses (before interest and other fees related to revolving credit facility)(4)(5) | | % | 1.99 | | 1.83 | | 1.86 | | 1.91 | | 1.96 | |

Expenses (with interest and other fees related to revolving credit facility)(4)(5) | | % | 2.69 | | 1.94 | | 1.94 | | 2.09 | | 2.23 | |

Net investment income(4)(5) | | % | 4.46 | | 2.88 | | 3.38 | | 4.19 | | 5.20 | |

Ratios to average net assets before reimbursement/recoupment: | | | | | | | | | | | | |

Expenses (before interest and other fees related to revolving credit facility)(4)(5) | | % | 1.97 | | 1.83 | | 1.96 | | 2.06 | | 2.29 | |

Expenses (with interest and other fees related to revolving credit facility)(4)(5) | | % | 2.67 | | 1.95 | | 2.04 | | 2.24 | | 2.54 | |

Net investment income(4)(5) | | % | 4.48 | | 2.87 | | 3.28 | | 4.04 | | 4.89 | |

Portfolio turnover rate | | % | 82 | | 82 | | 72 | | 60 | | 65 | |

Shares outstanding at end of period (000’s) | | 59,402 | | 53,316 | | 17,841 | | 2,202 | | 1,300 | |

| | | | | | | | | | | | | | | | | | | | |

| | Class Q | |

| | Year Ended

February 28 or 29, | |

| | 2006 | | 2005 | | 2004 | | 2003 | | 2002(6) | |

Per Share Operating Performance: | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 15.52 | | 15.41 | | 14.79 | | 14.89 | | 15.30 | |

Income (loss) from investment operations: | | | | | | | | | | | |

Net investment income | | $ | 0.78 | | 0.52 | | 0.63 | | 0.69 | | 0.81 | |

Net realized and unrealized gain (loss) on investments | | $ | (0.03 | ) | 0.20 | | 0.65 | | (0.10 | ) | (0.32 | ) |

Total income from investment operations | | $ | 0.75 | | 0.72 | | 1.28 | | 0.59 | | 0.49 | |

Less distributions from: | | | | | | | | | | | |

Net investment income | | $ | 0.78 | | 0.56 | | 0.64 | | 0.69 | | 0.90 | |

Net realized gain on investments | | $ | — | | 0.05 | | 0.02 | | — | | — | |

Total distributions | | $ | 0.78 | | 0.61 | | 0.66 | | 0.69 | | 0.90 | |

Net asset value, end of period | | $ | 15.49 | | 15.52 | | 15.41 | | 14.79 | | 14.89 | |

Total Investment Return(2) | | % | 4.97 | | 4.75 | | 8.82 | | 4.09 | | 3.73 | |

Ratios/Supplemental Data: | | | | | | | | | | | |

Net assets, end of period (000’s) | | $ | 184,586 | | 183,017 | | 157,051 | | 215,341 | | 215,029 | |

Average borrowings (000’s)(3) | | $ | 325,044 | | 34,767 | | 20,771 | | 17,655 | | 19,797 | |

Asset coverage per $1,000 of debt | | $ | 6,519 | | 1,251 | | — | * | 689 | | 3,220 | |

Ratios to average net assets after reimbursement/recoupment: | | | | | | | | | | | |

Expenses (before interest and other fees related to revolving credit facility)(4)(5) | | % | 1.49 | | 1.34 | | 1.40 | | 1.41 | | 1.43 | |

Expenses (with interest and other fees related to revolving credit facility)(4)(5) | | % | 2.19 | | 1.45 | | 1.54 | | 1.59 | | 1.63 | |

Net investment income(4)(5) | | % | 4.96 | | 3.39 | | 4.17 | | 4.69 | | 5.94 | |

Ratios to average net assets before reimbursement/recoupment: | | | | | | | | | | | | |

Expenses (before interest and other fees related to revolving credit facility)(4)(5) | | % | 1.47 | | 1.34 | | 1.48 | | 1.56 | | 1.70 | |

Expenses (with interest and other fees related to revolving credit facility)(4)(5) | | % | 2.17 | | 1.45 | | 1.62 | | 1.74 | | 1.90 | |

Net investment income(4)(5) | | % | 4.98 | | 3.38 | | 4.09 | | 4.54 | | 5.67 | |

Portfolio turnover rate | | % | 82 | | 82 | | 72 | | 60 | | 65 | |

Shares outstanding at end of period (000’s) | | 11,918 | | 11,789 | | 10,188 | | 14,559 | | 14,439 | |

| | | | | | | | | | | | | | | | | | | |

(1) Commencement of operations.

(2) Total investment returns are not annualized for periods of less than one year and do not include sales load.

(3) Based on the active days of borrowing.

(4) Annualized for periods less than one year.

(5) The Investment Manager has agreed to limit expenses excluding interest, taxes, brokerage commissions, leverage expenses, other investment related costs and extraordinary expenses, subject topossible recoupment by the Investment Manager within three years to the following:

Class A – 0.90% of Managed Assets plus 0.45% of average daily net assets

Class B – 0.90% of Managed Assets plus 1.20% of average daily net assets

Class C – 0.90% of Managed Assets plus 0.95% of average daily net assets

Class Q – 0.90% of Managed Assets plus 0.45% of average daily net assets

(6) Effective March 30, 2001, the Management of the Fund effectuated a reverse stock split of 0.6656 of a Share for one Share. Prior period amounts have been restated to reflect the reverse stock split.

* There were no loans outstanding at period end.

See Accompanying Notes to Financial Statements

16

ING Senior Income Fund

NOTES TO FINANCIAL STATEMENTS as of February 28, 2006 |

NOTE 1 — ORGANIZATION

ING Senior Income Fund (the “Fund”), a Delaware statutory trust, is registered under the Investment Company Act of 1940 as amended, (the “1940 Act”), as a continuously-offered, diversified, closed-end, management investment company. The Fund invests at least 80% of its assets plus the amount of any borrowings, in U.S. dollar denominated, floating rate secured senior loans, which generally are not registered under the Securities Act of 1933 as amended (the “‘33 Act”), but contain certain restrictions on resale and cannot be sold publicly. These loans bear interest (unless otherwise noted) at rates that float periodically at a margin above the London Inter-Bank Offered Rate (“LIBOR”) and other short-term rates. During the period December 15, 2000 through March 30, 2001, the Fund issued 19,933,953 Class Q shares to an affiliate of the Fund’s manager, ING Investments, LLC (the “Investment Manager”) in exchange for $200,000,000. Effective April 2, 2001, the Fund commenced the offering of Class A, Class B, Class C and Class Q shares to the public.

The Fund currently has four classes of shares; A, B, C and Q. Class A shares are subject to a sales charge of up to 2.50%. Class A shares purchased in excess of $1,000,000 are not subject to a sales charge but are subject to an Early Withdrawal Charge (“EWC”) of up to 1% within one year of purchase. Class A shares are issued upon conversion of Class B shares eight years after purchase or through an exchange of Class A shares of certain ING Funds. Class B shares are subject to an EWC of up to 3% over the five-year period after purchase and Class C shares are subject to an EWC of 1% during the first year after purchase.

To maintain a measure of liquidity, the Fund offers to repurchase between 5% and 25% of its outstanding common shares on a monthly basis. This is a fundamental policy that cannot be changed without shareholder approval. The Fund currently anticipates offerings to repurchase 5% of its outstanding common shares each month. The Fund may not repurchase more than 25% in any calendar quarter. Other than these monthly repurchases, no market for the Fund’s common shares is expected to exist. The separate classes of shares differ principally in their distribution fees and shareholder servicing fees. All shareholders bear the common expenses of the Fund and earn income and realized gains/losses from the portfolio pro rata on the average daily net assets of each class, without distinction between share classes. Differences in the per share dividend rates generally result from differences in separate class expenses, including distribution fees and shareholder servicing fees.

Effective January 31, 2005, Class B common shares of the Fund became closed to new investment, provided that (1) Class B common shares of the Fund may be purchased through the reinvestment of dividends issued by the Fund; and (2) subject to the terms and conditions of relevant exchange privileges and as permitted under their respective prospectuses, Class B common shares of the Fund may be acquired through exchange of Class B shares of other funds in the ING mutual funds complex for the Fund’s Class B common shares.

NOTE 2 — SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of the significant accounting policies consistently followed by the Fund in the preparation of its financial statements. The policies are in conformity with U.S. generally accepted accounting principles.

A. Senior Loan and Other Security Valuation. Senior loans held by the Fund are normally valued at the mean of the means of one or more bid and asked quotations obtained from a pricing service or other sources determined by the Board of Trustees to be independent and believed to be reliable. Loans for which reliable market value quotations are not readily available may be valued with reference to another loan or a group of loans for which quotations are more readily available and whose characteristics are comparable to the loan being valued. Under this approach, the comparable loan or loans serve as a proxy for changes in value of the loan being valued. The Fund has engaged an independent pricing service to provide quotations from dealers in loans and to calculate values under the proxy procedure described above.

17

ING Senior Income Fund

NOTES TO FINANCIAL STATEMENTS as of February 28, 2006 (continued) |

NOTE 2 — SIGNIFICANT ACCOUNTING POLICIES (continued)

It is expected that most of the loans held by the Fund will be valued with reference to quotations from the independent pricing service or with reference to the proxy procedure described above. As of February 28, 2006, 99.97% of total investments were valued based on these procedures.

Prices from a pricing service may not be available for all loans and the Investment Manager may believe that the price for a loan derived from market quotations or the proxy procedure described above is not reliable or accurate. Among other reasons, this may be the result of information about a particular loan or borrower known to the Investment Manager that the Investment Manager believes may not be known to the pricing service or reflected in a price quote. In this event, the loan is valued at fair value as determined in good faith under procedures established by the Fund’s Board of Trustees and in accordance with the provisions of the 1940 Act. Under these procedures, fair value is determined by the Investment Manager and monitored by the Fund’s Board of Trustees through its Valuation, Proxy and Brokerage Committee (formerly, Valuation and Proxy Committee).

In fair valuing a loan, consideration is given to several factors, which may include, among others, the following: (i) the characteristics of and fundamental analytical data relating to the loan, including the cost, size, current interest rate, period until the next interest rate reset, maturity and base lending rate of the loan, the terms and conditions of the loan and any related agreements, and the position of the loan in the borrower’s debt structure; (ii) the nature, adequacy and value of the collateral, including the Fund’s rights, remedies and interests with respect to the collateral; (iii) the creditworthiness of the borrower and the cash flow coverage of outstanding principal and interest, based on an evaluation of its financial condition, financial statements and information about the borrower’s business, cash flows, capital structure and future prospects; (iv) information relating to the market for the loan, including price quotations for, and trading in, the loan and interests in similar loans and the market environment and investor attitudes towards the loan and interests in similar loans; (v) the reputation and financial condition of the agent for the loan and any intermediate participants in the loan; (vi) the borrower’s management; and (vii) the general economic and market conditions affecting the fair value of the loan. Securities other than senior loans for which reliable market value quotations are not readily available and all other assets will be valued at their respective fair values as determined in good faith by, and under procedures established by, the Board of Trustees of the Fund. Investments in securities maturing in 60 days or less from the date of valuation are valued at amortized cost, which, when combined with accrued interest, approximates market value. To the extent the Fund invests in other registered companies, the Fund’s NAV is calculated based on the current NAV of the registered investment company in which the Fund invests. The prospectuses for those investment companies explain the circumstances under which they will use fair value pricing and the effects of using fair value pricing.

B. Distributions to Shareholders. The Fund declares and goes ex-dividend daily and pays dividends monthly from net investment income. Distributions from capital gains, if any, are declared and paid annually. The Fund may make additional distributions to comply with the distribution requirements of the Internal Revenue Code. The character and amounts of income and gains to be distributed are determined in accordance with federal income tax regulations, which may differ from U.S. generally accepted accounting principles for investment companies. The Fund records distributions to its shareholders on the ex-dividend date.

C. Security Transactions and Revenue Recognition. Revolver and delayed draw loans are booked on a settlement date basis. Security transactions and senior loans are accounted for on trade date (date the order to buy or sell is executed). Realized gains or losses are reported on the basis of identified cost of securities sold. Interest income is recorded on an accrual basis at the then-current loan rate. The accrual of interest on loans is discontinued when, in the opinion of management, there is an indication that the borrower may be unable to meet payments as they become due. Upon such discontinuance, all unpaid accrued interest is reversed. Cash collections on non-accrual loans are generally applied as a reduction to the recorded investment of the loan. Loans are generally returned to accrual status only after all past due amounts have been received and the borrower has demonstrated sustained performance. Premium amortization and discount accretion are

18

ING Senior Income Fund

NOTES TO FINANCIAL STATEMENTS as of February 28, 2006 (continued) |

NOTE 2 — SIGNIFICANT ACCOUNTING POLICIES (continued)

determined by the effective yield method over the shorter of four years or the actual term of the loan. Arrangement fees received on revolving credit facilities, which represent non-refundable fees or purchase discounts associated with the acquisition of loans, are deferred and recognized using the effective yield method over the shorter of four years or the actual term of the loan. No such fees are recognized on loans which have been placed on non-accrual status. Arrangement fees associated with all other loans, except revolving credit facilities, are treated as discounts and are accreted as described above. Dividend income is recorded on the ex-dividend date.

D. Federal Income Taxes. It is the Fund’s policy to comply with subchapter M of the Internal Revenue Code and related excise tax provisions applicable to regulated investment companies and to distribute substantially all of its net investment income and net realized capital gains to its shareholders. Therefore, no federal income tax provision is required. No capital gain distributions shall be made until any capital loss carryforwards have been fully utilized or expire.

E. Use of Estimates. Management of the Fund has made certain estimates and assumptions relating to the reporting of assets, liabilities, revenues, expenses and contingencies to prepare these financial statements in conformity with accounting principles generally accepted in the United States of America for investment companies. Actual results could differ from these estimates.

NOTE 3 — INVESTMENTS

For the year ended February 28, 2006, the cost of purchases and the proceeds from principal repayment and sales of investments, excluding short-term investments, totaled $2,481,653,064 and $1,937,604,549, respectively. At February 28, 2006, the Fund held senior loans valued at $2,588,497,820 representing 99.6% of its total investments. The market value of these assets is established as set forth in Note 2.

The senior loans acquired by the Fund typically take the form of a direct lending relationship with the borrower acquired through an assignment of another lender’s interest in a loan. The lead lender in a typical corporate loan syndicate administers the loan and monitors collateral. In the event that the lead lender becomes insolvent, enters FDIC receivership or, if not FDIC insured, enters into bankruptcy, the Fund may incur certain costs and delays in realizing payment, or may suffer a loss of principal and/or interest.

Warrants and shares of common stock held in the portfolio were acquired in conjunction with loans held by the Fund. Certain of these shares and warrants are restricted and may not be publicly sold without registration under the ‘33 Act, or without an exemption under the ‘33 Act. In some cases, these restrictions expire after a designated period of time after the issuance of the shares or warrants.

Dates of acquisition and cost or assigned basis of restricted securities are as follows:

| | Date of

Acquisition | | Cost or

Assigned Basis | |

| | | | | |

Decision One Corporation — Common Shares | | 06/03/05 | | $295,535 | |

Galey & Lord, Inc. — Common Shares | | 03/31/04 | | — | |

Murray’s Discount Auto Stores, Inc. — Escrow | | 08/11/03 | | 71 | |

Neoplan USA Corporation — Common Shares | | 08/31/04 | | — | |

Neoplan USA Corporation — Preferred B Shares | | 08/29/03 | | — | |

Neoplan USA Corporation — Preferred C Shares | | 08/29/03 | | 40,207 | |

Neoplan USA Corporation — Preferred D Shares | | 08/29/03 | | 330,600 | |

New World Restaurant Group, Inc. — Warrants | | 02/20/02 | | 20 | |

Norwood Promotional Products, Inc. — Common Shares | | 08/23/04 | | 10,046 | |

Safelite Glass Corporation — Common Shares | | 06/21/01 | | 184,912 | |

Safelite Realty Corporation — Common Shares | | 06/21/01 | | — | |

Total restricted securities excluding senior loans (market value of $7,368,622 was 0.3% of net assets at February 28, 2006). | | | | $861,391 | |

19

ING Senior Income Fund

NOTES TO FINANCIAL STATEMENTS as of February 28, 2006 (continued) |

NOTE 4 — MANAGEMENT AND ADMINISTRATION AGREEMENTS

The Fund has entered into an Investment Management Agreement with the Investment Manager to provide advisory and management services. The Investment Management Agreement compensates the Investment Manager with a fee, computed daily and payable monthly, at an annual rate of 0.80% of the Fund’s average daily gross asset value, minus the sum of the Fund’s accrued and unpaid dividends on any outstanding preferred shares and accrued liabilities (other than liabilities for the principal amount of any borrowings incurred, commercial paper or notes issued by the Fund and the liquidation preference of any outstanding preferred shares) (“Managed Assets”). The Fund is sub-advised by ING Investment Management Co. (“ING IM”). Under the Sub-Advisory Agreement, ING IM is responsible for managing the assets of the Fund in accordance with its investment objective and policies, subject to oversight by the Investment Manager. Both ING IM and the Investment Manager are indirect, wholly-owned subsidiaries of ING Groep N.V. and affiliates of each other.

The Fund has also entered into an Administration Agreement with ING Funds Services, LLC (the “Administrator”), an indirect, wholly-owned subsidiary of ING Groep N.V., to provide administrative services. The Administrator is compensated with a fee, computed daily and payable monthly, at an annual rate of 0.10% of the Fund’s Managed Assets.

NOTE 5 — DISTRIBUTION AND SERVICE FEES

Each share class of the Fund has adopted a Plan pursuant to Rule 12b-1 under the 1940 Act (the “12b-1 Plans”), whereby ING Funds Distributor, LLC (the “Distributor”) is reimbursed or compensated (depending on the class of shares) by the Fund for expenses incurred in the distribution of the Fund’s shares (“Distribution Fees”). Pursuant to the 12b-1 Plans, the Distributor is entitled to a payment each month for actual expenses incurred in the distribution and promotion of the Fund’s shares, including expenses incurred in printing prospectuses and reports used for sales purposes, expenses incurred in preparing and printing sales literature and other such distribution related expenses, including any distribution or Shareholder Servicing Fees (“Service Fees”) paid to securities dealers who executed a distribution agreement with the Distributor. Under the 12b-1 plans, each class of shares of the Fund pays the Distributor a combined Distribution and/or Service Fee based on average daily net assets at the following annual rates:

| Class A | | | | Class B | | | | Class C | | | | Class Q | | |

0.25% | | 1.00% | | 0.75% | | 0.25% | |

During the year ended February 28, 2006, the Distributor waived 0.25% of the Service Fee on Class B shares only.

NOTE 6 — EXPENSE LIMITATIONS

The Investment Manager has voluntarily agreed to limit expenses, excluding interest, taxes, brokerage commissions, leverage expenses, other investment-related costs and extraordinary expenses, to the following:

Class A | | — | | 0.90% of Managed Assets plus 0.45% of average daily net assets |

Class B | | — | | 0.90% of Managed Assets plus 1.20% of average daily net assets |

Class C | | — | | 0.90% of Managed Assets plus 0.95% of average daily net assets |

Class Q | | — | | 0.90% of Managed Assets plus 0.45% of average daily net assets |

As of February 28, 2006, the amounts of waived and reimbursed fees that are subject to possible recoupment by the Investment Manager, and the related expiration dates are as follows:

February 28, | | | |

| 2007 | | | | 2008 | | | | 2009 | | | | Total | | |

$117,524 | | $157,969 | | $— | | $275,493 | |

| | | | | | | | | | | | | | | |

20

ING Senior Income Fund

NOTES TO FINANCIAL STATEMENTS as of February 28, 2006 (continued) |

NOTE 7 — COMMITMENTS

The Fund has entered into a one-year revolving credit agreement, collateralized by assets of the Fund, to borrow up to $750 million maturing April 30, 2006. Borrowing rates under this agreement are based on a commercial paper pass through rate plus 0.25% on the funded portion. A facility fee of 0.15% is charged on the entire facility. There was $389 million of borrowings outstanding at February 28, 2006 at a rate of 4.90%, excluding other fees related to the entire facility. Average borrowings for the year ended February 28, 2006 were $325,043,836 and the average annualized interest rate was 4.37%, excluding other fees related to the entire facility.

NOTE 8 — SENIOR LOAN COMMITMENTS

At February 28, 2006, the Fund had unfunded loan commitments pursuant to the terms of the following loan agreements:

Aftermarket Technology Corporation | | $ | 1,750,000 | |

Baker & Taylor, Inc. | | 1,023,682 | |

Baker Tanks, Inc. | | 510,000 | |

Builders Firstsource, Inc. | | 1,500,000 | |

Dex Media West, LLC | | 935,303 | |

Eastman Kodak Company | | 3,176,471 | |

Federal-Mogul Corporation | | 2,030,000 | |

FSC Acquisition, LLC | | 300,220 | |

Hearthstone Housing Partners II, LLC | | 3,617,647 | |

Hertz Corporation | | 1,000,000 | |

Interstate Bakeries Corporation | | 2,500,000 | |

JohnsonDiversey, Inc. | | 508,666 | |

Kerasotes Theatres, Inc. | | $ | 1,125,000 | |

Navistar International Corporation | | 4,926,024 | |

Owens-Illinois Group, Inc. | | 93 | |

Primedia, Inc. | | 2,439,194 | |

Rural Cellular Corporation | | 66,667 | |

Sears Canada, Inc. | | 4,500,000 | |

Syniverse Holding LLC | | 1,500,000 | |

Trump Entertainment Resorts Holdings L.P. | | 1,741,250 | |

Vertafore, Inc. | | 555,556 | |

Yonkers Racing Corporation | | 991,465 | |

| | $ | 36,697,238 | |

NOTE 9 — TRANSACTIONS WITH AFFILIATES AND RELATED PARTIES

At February 28, 2006, the Fund had the following amounts recorded in payable to affiliates on the accompanying Statement of Assets and Liabilities (see Notes 4 and 5):

| Accrued Investment

Management Fees | | | | Accrued

Administrative Fees | | | | Accrued Distribution

and Service Fees | | | | Total | | |

$1,569,515 | | $196,189 | | $804,514 | | $2,570,218 | |

The Fund has adopted a Retirement Policy covering all independent trustees of the Fund who will have served as an independent trustee for at least five years at the time of retirement. Benefits under this plan are based on an annual rate as defined in the plan agreement, as amended.

NOTE 10 — CUSTODIAL AGREEMENT

State Street Bank and Trust Company (“SSB”) serves as the Fund’s custodian and recordkeeper. Custody fees paid to SSB may be reduced by earnings credits based on the cash balances held by SSB for the Fund. There were no earning credits for the year ended February 28, 2006.

NOTE 11 — SUBORDINATED LOANS AND UNSECURED LOANS

The primary risk arising from investing in subordinated loans or in unsecured loans is the potential loss in the event of default by the issuer of the loans. The Fund may invest up to 10% of its total assets, measured at the time of investment, in subordinated loans and up to 10% of its total assets, measured at the time of investment, in unsecured loans. As of February 28, 2006, the Fund held 0.40% of its total assets in subordinated loans and unsecured loans.

21

ING Senior Income Fund

NOTES TO FINANCIAL STATEMENTS as of February 28, 2006 (continued) |

NOTE 12 — CAPITAL SHARES

Transactions in capital shares and dollars were as follows:

| | Class A Shares | | Class B | |

| | Year

Ended

February 28, | | Year

Ended

February 28, | | Year

Ended

February 28, | | Year

Ended

February 28, | |

| | 2006 | | 2005 | | 2006 | | 2005 | |

Number of Shares | | | | | | | | | |

Shares sold | | 31,514,689 | | 45,019,222 | | 1,200,449 | | 4,821,925 | |

Dividends reinvested | | 1,898,903 | | 788,747 | | 239,725 | | 156,144 | |

Shares redeemed | | (21,636,099 | ) | (9,735,823 | ) | (1,741,409 | ) | (1,002,526 | ) |

Net increase (decrease) in shares outstanding | | 11,777,493 | | 36,072,146 | | (301,235 | ) | 3,975,543 | |

Dollar Amount ($) | | | | | | | | | |

Shares sold | | $ | 489,981,974 | | $ | 698,962,403 | | $ | 18,629,961 | | $ | 74,699,998 | |

Dividends reinvested | | 28,952,268 | | 12,229,952 | | 3,673,529 | | 2,420,379 | |

Shares redeemed | | (336,384,874 | ) | (151,275,068 | ) | (27,037,514 | ) | (15,545,425 | ) |

Net increase (decrease) | | $ | 182,549,368 | | $ | 559,917,287 | | $ | (4,734,024 | ) | $ | 61,574,952 | |

| | Class C | | Class Q | |

| | Year

Ended

February 28, | | Year

Ended

February 28, | | Year

Ended

February 28, | | Year

Ended

February 28, | |

| | 2006 | | 2005 | | 2006 | | 2005 | |

Number of Shares | | | | | | | | | |

Shares sold | | 21,990,018 | | 40,188,013 | | 6,157,327 | | 15,769,611 | |

Dividends reinvested | | 1,896,487 | | 960,495 | | 139,868 | | 202,240 | |

Shares redeemed | | (17,801,097 | ) | (5,673,352 | ) | (6,168,276 | ) | (14,371,320 | ) |

Net increase in shares outstanding | | 6,085,408 | | 35,475,156 | | 128,919 | | 1,600,531 | |

Dollar Amount ($) | | | | | | | | | |

Shares sold | | $ | 341,614,102 | | $ | 623,309,711 | | $ | 95,301,102 | | $ | 243,721,354 | |

Dividends reinvested | | 29,009,463 | | 14,895,319 | | 2,069,577 | | 3,124,368 | |

Shares redeemed | | (276,458,120 | ) | (88,054,810 | ) | (95,529,401 | ) | (222,232,384 | ) |

Net increase | | $ | 94,165,445 | | $ | 550,150,220 | | $ | 1,841,278 | | $ | 24,613,338 | |

NOTE 13 — FEDERAL INCOME TAXES

The amount of distributions from net investment income and net realized capital gains are determined in accordance with federal income tax regulations, which may differ from U.S. generally accepted accounting principles for investment companies. These book/tax differences may be either temporary or permanent. Permanent differences are reclassified within the capital accounts based on their federal tax-basis treatment; temporary differences are not reclassified. Key differences include the treatment of short-term capital gains, foreign currency transactions, and wash sale deferrals. Distributions in excess of net investment income and/or net realized capital gains for tax purposes are reported as distributions of paid-in capital.

The following permanent tax differences have been reclassified as of February 28, 2006:

| Paid-in Capital | | | Undistributed

Net Investment

Income On

Investments | | Accumulated

Net Realized

Gains/(Losses) | |

$ | | $(8,254) | | $8,254 | |

Dividends paid by the Fund from net investment income and distributions of net realized short-term capital gains are, for federal income tax purposes, taxable as ordinary income to shareholders.

The tax composition of dividends and distributions to shareholders was as follows:

Year ended February 28, 2006 | | Year ended February 28, 2005 | |

Ordinary Income | | Long-Term

Capital Gains | | Ordinary Income | | Long-Term

Capital Gains | |

$96,285,686 | | $120,627 | | $47,736,711 | | $736,153 | |

22

ING Senior Income Fund

NOTES TO FINANCIAL STATEMENTS as of February 28, 2006 (continued) |

NOTE 13 — FEDERAL INCOME TAXES (continued)

The tax-basis components of distributable earnings and the expiration dates of the capital loss carryforwards which may be used to offset future realized capital gains for federal income tax purposes as of February 28, 2006 were:

Undistributed

Ordinary Income | | Unrealized

Appreciation/

(Depreciation) | | Post-October

Capital Losses

Deferred | | Capital

Loss

Carryforwards | | | Expiration

Dates | | |

$1,439,900 | | $26,867,090 | | $(1,560,405) | | $(2,774,928) | | 2014 | |

NOTE 14 — INFORMATION REGARDING TRADING OF ING’S US MUTUAL FUNDS

In 2004, ING Investments reported to the Boards of Directors/Trustees (the “Boards”) of the ING Funds that, like many U.S. financial services companies, ING Investments and certain of its U.S. affiliates had received informal and formal requests for information since September 2003 from various governmental and self-regulatory agencies in connection with investigations related to mutual funds and variable insurance products. ING Investments has advised the Boards that it and its affiliates have cooperated fully with each request.

In addition to responding to regulatory and governmental requests, ING Investments reported that management of U.S. affiliates of ING Groep N.V., including ING Investments (collectively, “ING”), on their own initiative, have conducted, through independent special counsel and a national accounting firm, an extensive internal review of trading in ING insurance, retirement, and mutual fund products. The goal of this review was to identify any instances of inappropriate trading in those products by third parties or by ING investment professionals and other ING personnel. ING’s internal review related to mutual fund trading is now substantially completed. ING has reported that, of the millions of customer relationships that ING maintains, the internal review identified several isolated arrangements allowing third parties to engage in frequent trading of mutual funds within ING’s variable insurance and mutual fund products, and identified other circumstances where frequent trading occurred, despite measures taken by ING intended to combat market timing. ING further reported that each of these arrangements has been terminated and fully disclosed to regulators. The results of the internal review were also reported to the independent members of the Board.

ING Investments has advised the Board that most of the identified arrangements were initiated prior to ING’s acquisition of the businesses in question in the U.S. ING Investments further reported that the companies in question did not receive special benefits in return for any of these arrangements, which have all been terminated.

Based on the internal review, ING Investments has advised the Board that the identified arrangements do not represent a systemic problem in any of the companies that were involved.

In September 2005, ING Funds Distributor, LLC (“IFD”), the distributor of certain ING Funds, settled an administrative proceeding with the NASD regarding three arrangements, dating from 1995, 1996 and 1998, under which the administrator to the then-Pilgrim Funds, which subsequently became part of the ING Funds, entered into formal and informal arrangements that permitted frequent trading. Under the terms of the Letter of Acceptance, Waiver and Consent (“AWC”) with the NASD, under which IFD neither admitted nor denied the allegations or findings, IFD consented to the following sanctions: (i) a censure; (ii) a fine of $1.5 million; (iii) restitution of approximately $1.44 million to certain ING Funds for losses attributable to excessive trading described in the AWC; and (iv) agreement to make certification to NASD regarding the review and establishment of certain procedures.

23

ING Senior Income Fund

NOTES TO FINANCIAL STATEMENTS as of February 28, 2006 (continued) |

NOTE 14 — INFORMATION REGARDING TRADING OF ING’S U.S. MUTUAL FUNDS (continued)

In addition to the arrangements discussed above, in 2004 ING Investments reported to the Board that, at that time, these instances include the following, in addition to the arrangements subject to the AWC discussed above:

• Aeltus Investment Management, Inc. (a predecessor entity to ING Investment Management Co.) has identified two investment professionals who engaged in extensive frequent trading in certain ING Funds. One was subsequently terminated for cause and incurred substantial financial penalties in connection with this conduct and the second has been disciplined.

• ReliaStar Life Insurance Company (“ReliaStar”) entered into agreements seven years ago permitting the owner of policies issued by the insurer to engage in frequent trading and to submit orders until 4pm Central Time. In 2001 ReliaStar also entered into a selling agreement with a broker-dealer that engaged in frequent trading. Employees of ING affiliates were terminated and/or disciplined in connection with these matters.

• In 1998, Golden American Life Insurance Company entered into arrangements permitting a broker-dealer to frequently trade up to certain specific limits in a fund available in an ING variable annuity product. No employee responsible for this arrangement remains at the company.