Exhibit 99

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The Board of Directors of Magellan GP, LLC

We have audited the accompanying consolidated balance sheets of Magellan GP, LLC as of December 31, 2008 and 2007. These balance sheets are the responsibility of Magellan GP, LLC’s management. Our responsibility is to express an opinion on these balance sheets based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated balance sheets are free of material misstatement. We were not engaged to perform an audit of Magellan GP, LLC’s internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of Magellan GP, LLC’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the balance sheets, assessing the accounting principles used and significant estimates made by management, and evaluating the overall balance sheet presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the balance sheets referred to above present fairly, in all material respects, the consolidated financial position of Magellan GP, LLC at December 31, 2008 and 2007, in conformity with U.S. generally accepted accounting principles.

/s/ Ernst & Young LLP

Tulsa, Oklahoma

February 26, 2009

MAGELLAN GP, LLC

CONSOLIDATED BALANCE SHEETS

(In thousands)

| | | | | | | | |

| | | December 31, | |

| | | 2007 | | | 2008 | |

| ASSETS | | | | | | | | |

Current assets: | | | | | | | | |

Cash and cash equivalents | | $ | — | | | $ | 33,242 | |

Accounts receivable (less allowance for doubtful accounts of $10 and $462 at December 31, 2007 and 2008, respectively) | | | 62,834 | | | | 37,517 | |

Other accounts receivable | | | 10,696 | | | | 11,073 | |

Affiliate accounts receivable | | | 208 | | | | 376 | |

Inventory | | | 120,462 | | | | 47,734 | |

Energy commodity derivative contracts | | | — | | | | 20,200 | |

Other current assets | | | 10,882 | | | | 15,440 | |

| | | | | | | | |

Total current assets | | | 205,082 | | | | 165,582 | |

Property, plant and equipment | | | 2,603,262 | | | | 2,891,698 | |

Less: accumulated depreciation | | | 455,074 | | | | 529,410 | |

| | | | | | | | |

Net property, plant and equipment | | | 2,148,188 | | | | 2,362,288 | |

Equity investments | | | 24,324 | | | | 23,190 | |

Long-term receivables | | | 7,801 | | | | 7,390 | |

Goodwill | | | 11,902 | | | | 14,766 | |

Other intangibles (less accumulated amortization of $6,743 and $8,290 at December 31, 2007 and 2008, respectively) | | | 7,086 | | | | 5,539 | |

Debt placement costs (less accumulated amortization of $2,170 and $2,937 at December 31, 2007 and 2008, respectively) | | | 6,368 | | | | 7,649 | |

Other noncurrent assets | | | 6,322 | | | | 10,217 | |

| | | | | | | | |

Total assets | | $ | 2,417,073 | | | $ | 2,596,621 | |

| | | | | | | | |

| | |

| LIABILITIES AND OWNER’S EQUITY | | | | | | | | |

Current liabilities: | | | | | | | | |

Accounts payable | | $ | 39,622 | | | $ | 39,441 | |

Affiliate payroll and benefits | | | 23,364 | | | | 18,119 | |

Accrued interest payable | | | 7,197 | | | | 15,077 | |

Accrued taxes other than income | | | 21,039 | | | | 20,151 | |

Environmental liabilities | | | 36,127 | | | | 19,634 | |

Deferred revenue | | | 20,797 | | | | 21,492 | |

Accrued product purchases | | | 43,230 | | | | 23,874 | |

Energy commodity derivatives deposit | | | — | | | | 18,994 | |

Other current liabilities | | | 29,268 | | | | 18,477 | |

| | | | | | | | |

Total current liabilities | | | 220,644 | | | | 195,259 | |

Long-term debt | | | 914,536 | | | | 1,083,485 | |

Long-term affiliate pension and benefits | | | 22,370 | | | | 31,787 | |

Supply agreement deposit | | | 18,500 | | | | — | |

Noncurrent portion of product supply liability | | | 24,348 | | | | — | |

Other deferred liabilities | | | 9,476 | | | | 8,642 | |

Environmental liabilities | | | 21,491 | | | | 22,166 | |

Non-controlling owners’ interests of consolidated subsidiaries | | | 1,131,739 | | | | 1,203,187 | |

Commitments and contingencies | | | | | | | | |

Owner’s equity: | | | | | | | | |

Owner’s equity | | | 58,563 | | | | 69,213 | |

Accumulated other comprehensive loss | | | (4,594 | ) | | | (17,118 | ) |

| | | | | | | | |

Total owner’s equity | | | 53,969 | | | | 52,095 | |

| | | | | | | | |

Total liabilities and owner’s equity | | $ | 2,417,073 | | | $ | 2,596,621 | |

| | | | | | | | |

See accompanying notes.

1

MAGELLAN GP, LLC

NOTES TO CONSOLIDATED BALANCE SHEETS

1. Organization, Description of Business and Basis of Presentation

Organization

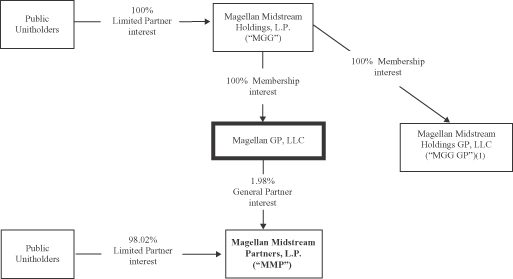

Unless otherwise noted, the terms “we,” “us,” “our” and other similar terms refer to Magellan GP, LLC, a Delaware limited liability company. We were formed in August 2000 to serve as the general partner of Magellan Midstream Partners, L.P. and manage its operations.

Our organizational structure at December 31, 2008 and that of our affiliate entities, as well as how we refer to these entities in our notes to consolidated balance sheets, is provided below:

| (1) | MGG GP holds a non-economic general partner interest in MGG. |

We own an approximate 2% general partner interest in MMP and all of MMP’s incentive distribution rights, and we serve as MMP’s general partner. Because we control MMP, it is included in our consolidated balance sheets (see Note 2—Summary of Significant Accounting Policies – Basis of Presentation). Therefore, theDescription of Business discussion below relates to MMP. The incentive distribution rights of MMP that we own entitle us to receive increasing percentages of MMP’s distributions, up to a maximum of 48%.

We and MMP do not have employees. We and MMP have contracted with MGG GP to provide MMP with all general and administrative services and operating functions required for its operation.

Description of Business

MMP owns a petroleum products pipeline system, petroleum products terminals and an ammonia pipeline system. MMP’s reportable segments offer different products and services and are managed separately because each requires different marketing strategies and business knowledge. During 2008, MMP acquired petroleum products terminals in Bettendorf, Iowa and Wrenshall, Minnesota and a petroleum products terminal in Mt. Pleasant, Texas along with a 76-mile petroleum products pipeline for $38.3 million, plus related liabilities assumed of $2.6 million. The results of these facilities have been included in MMP’s petroleum products pipeline system segment from their respective acquisition dates.

2

MAGELLAN GP, LLC

NOTES TO CONSOLIDATED BALANCE SHEETS—(Continued)

Petroleum Products Pipeline System.MMP’s petroleum products pipeline system includes approximately 8,700 miles of pipeline and 49 terminals that provide transportation, storage and distribution services. MMP’s petroleum products pipeline system covers a 13-state area extending from Texas through the Midwest to Colorado, North Dakota, Minnesota, Wisconsin and Illinois. The products transported on MMP’s pipeline system are primarily gasoline, distillates, LPGs and aviation fuels. Product originates on the system from direct connections to refineries and interconnects with other interstate pipelines for transportation and ultimate distribution to retail gasoline stations, truck stops, railroads, airports and other end-users. MMP has an ownership interest in Osage Pipe Line Company, LLC (“Osage Pipeline”), which owns the 135-mile Osage pipeline that transports crude oil from Cushing, Oklahoma to El Dorado, Kansas and has connections to National Cooperative Refining Association’s refinery in McPherson, Kansas and the Frontier refinery in El Dorado, Kansas. MMP’s petroleum products blending and fractionation operations are also included in the petroleum products pipeline system segment.

Petroleum Products Terminals.Most of MMP’s petroleum products terminals are strategically located along or near third-party pipelines or petroleum refineries. The petroleum products terminals provide a variety of services such as distribution, storage, blending, inventory management and additive injection to a diverse customer group including governmental customers and end-users in the downstream refining, retail, commercial trading, industrial and petrochemical industries. Products stored in and distributed through the petroleum products terminal network include refined petroleum products, blendstocks, crude oils, heavy oils and feedstocks. The terminal network consists of seven marine terminals and 27 inland terminals. Five of MMP’s marine terminal facilities are located along the Gulf Coast and two marine terminal facilities are located on the East Coast. MMP’s inland terminals are located primarily in the southeastern United States.

Ammonia Pipeline System.The ammonia pipeline system consists of a 1,100-mile ammonia pipeline and six company-owned terminals. Shipments on the pipeline primarily originate from ammonia production plants located in Borger, Texas and Enid and Verdigris, Oklahoma for transport to terminals throughout the Midwest. The ammonia transported through the system is used primarily as nitrogen fertilizer.

2. Summary of Significant Accounting Policies

Basis of Presentation.At December 31, 2007 and 2008, our general partner ownership interest in MMP was 1.995% and 1.989%, respectively. In January 2009 our general partner interest changed to 1.983% (see Note 17—Subsequent Events). Our ownership of MMP is derived solely through our general partner ownership interest in MMP.

Our general partner ownership interest in MMP gives us control of MMP as the limited partner interests in MMP: (i) do not have the substantive ability to dissolve MMP, (ii) can remove us as MMP’s general partner only with a supermajority vote of the MMP limited partner units and the MMP limited partner units which can be voted in such an election are restricted, and (iii) do not possess substantive participating rights in MMP’s operations. Therefore, our consolidated balance sheets include the assets and liabilities of MMP. All intercompany transactions have been eliminated.

Use of Estimates.The preparation of our consolidated balance sheets in conformity with accounting principles generally accepted in the United States requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities that exist at the date of our consolidated balance sheets. Actual results could differ from those estimates.

Regulatory Reporting.MMP’s petroleum products pipelines are subject to regulation by the Federal Energy Regulatory Commission (“FERC”), which prescribes certain accounting principles and practices for the annual Form 6 report filed with the FERC that differ from those used in these financial statements. Such differences relate primarily to capitalization of interest, accounting for gains and losses on disposal of property, plant and equipment and other adjustments. MMP follows U.S. generally accepted accounting principles (“GAAP”) where such differences of accounting principles exist.

Cash Equivalents.Cash and cash equivalents include demand and time deposits and other highly marketable securities with original maturities of three months or less when acquired.

3

MAGELLAN GP, LLC

NOTES TO CONSOLIDATED BALANCE SHEETS—(Continued)

Accounts Receivable and Allowance for Doubtful Accounts.Accounts receivable represent valid claims against non-affiliated customers and are recognized when products are sold or services are rendered. MMP extends credit terms to certain customers based on historical dealings and to other customers after a review of various credit indicators. An allowance for doubtful accounts is established for all or any portion of an account where collections are considered to be at risk and reserves are evaluated no less than quarterly to determine their adequacy. Judgments relative to at-risk accounts include the customers’ current financial condition, the customers’ historical relationship with MMP and current and projected economic conditions. Accounts receivable are written off when the account is deemed uncollectible.

Inventory Valuation.Inventory is comprised primarily of refined petroleum products, natural gas liquids, transmix and additives, which are stated at the lower of average cost or market.

Property, Plant and Equipment.Property, plant and equipment consist primarily of pipeline, pipeline-related equipment, storage tanks and processing equipment. Property, plant and equipment are stated at cost except for impaired assets. Impaired assets are recorded at fair value on the last impairment evaluation date for which an adjustment was required. At the time of MGG’s acquisition of general and limited partner interests in MMP on June 17, 2003, we recorded MMP’s property, plant and equipment at 54.6% of their fair values and at 46.4% of their historical carrying values reflecting MGG’s ownership percentages in MMP at that time.

Most of MMP’s assets are depreciated individually on a straight-line basis over their useful lives; however, the individual components of certain assets, such as some of MMP’s older tanks, are grouped together into a composite asset and those assets are depreciated using a composite rate. MMP assigns asset lives based on reasonable estimates when an asset is placed into service. Subsequent events could cause MMP to change its estimates, which would impact the future calculation of depreciation expense. The depreciation rates for most of MMP’s pipeline assets are approved and regulated by the FERC. Assets with the same useful lives and similar characteristics are depreciated using the same rate. The range of depreciable lives by asset category is detailed in Note 4—Property, Plant and Equipment.

The carrying value of property, plant and equipment sold or retired and the related accumulated depreciation is removed from our accounts and any associated gains or losses are recorded on our income statement in the period of sale or disposition.

Expenditures to replace existing assets are capitalized and the replaced assets are retired. Expenditures associated with existing assets are capitalized when they improve the productivity or increase the useful life of the asset. Direct project costs such as labor and materials are capitalized as incurred. Indirect project costs, such as overhead, are capitalized based on a percentage of direct labor charged to the respective capital project. Expenditures for maintenance, repairs and minor replacements are charged to operating expense in the period incurred.

Asset Retirement Obligation. MMP records asset retirement obligations under the provisions of Statement of Financial Accounting Standard (“SFAS”) No. 143,Accounting for Asset Retirement Obligationsand Financial Interpretation (“FIN”) No. 47, Accounting for Conditional Asset Retirement Obligations (as amended). SFAS No. 143 requires the fair value of a liability related to the retirement of long-lived assets be recorded at the time a legal obligation is incurred, if the liability can be reasonably estimated. When the liability is initially recorded, the carrying amount of the related asset is increased by the amount of the liability. Over time, the liability is accreted to its future value, with the accretion recorded to expense. FIN No. 47 clarified that where there is an obligation to perform an asset retirement activity, even though uncertainties exist about the timing or method of settlement, an entity is required to recognize a liability for the fair value of a conditional asset retirement obligation if the fair value of the liability can be determined.

MMP’s operating assets generally consist of underground refined products and ammonia pipelines and related facilities along rights-of-way and above-ground storage tanks and related facilities. MMP’s rights-of-way agreements typically do not require the dismantling, removal and reclamation of the rights-of-way upon permanent removal of the pipelines and related facilities from service. Additionally, management is unable to predict when, or if, MMP’s pipelines, storage tanks and related facilities would become completely obsolete and require decommissioning. Accordingly, except for a $1.5 million liability associated with anticipated tank liner replacements, MMP has recorded no liability or corresponding asset in conjunction with SFAS No. 143 and FIN No. 47 as both the amounts and future dates of when such costs might be incurred are indeterminable.

Equity Investments.MMP accounts for investments greater than 20% in affiliates which it does not control by the equity method of accounting. Under this method, an investment is recorded at its acquisition cost, plus its equity in undistributed earnings or losses since acquisition, less distributions received and less amortization of excess net investment.

4

MAGELLAN GP, LLC

NOTES TO CONSOLIDATED BALANCE SHEETS—(Continued)

Excess net investment is the amount by which MMP’s initial investment exceeded its proportionate share of the book value of the net assets of the investment. MMP amortizes excess net investment over the weighted-average depreciable asset lives of the equity investee as of the date of the equity investment. Equity method investments are evaluated for impairment annually or whenever events or circumstances indicate that there is an other-than-temporary loss in value of the investment. In the event that MMP determines that the loss in value of an investment is other-than-temporary, it would record a charge to earnings to adjust the carrying value to fair value. MMP recorded no equity investment impairments during 2007 or 2008.

Goodwill and Other Intangible Assets.MMP has adopted SFAS No. 142,Goodwill and Other Intangible Assets. In accordance with this Statement, goodwill, which represents the excess of cost over fair value of assets of businesses acquired, is no longer amortized but is evaluated periodically for impairment. Goodwill was $11.9 million and $14.8 million at December 31, 2007 and 2008, respectively. Of our reported goodwill at December 31, 2008, $11.9 million was acquired in transactions involving MMP’s petroleum products terminals segment and $2.9 million was acquired in a transaction involving MMP’s petroleum products pipeline system segment.

The determination of whether goodwill is impaired is based on management’s estimate of the fair value of MMP’s reporting units using a discounted future cash flow (“DFCF”) model as compared to their carrying values. Critical assumptions used in our DFCF model included: (i) time horizon of 20 years, (ii) revenue growth of 1.5% per year and expense growth of 1.5% per year, except G&A costs with an assumed growth of 4.0% per year, (iii) weighted-average cost of capital of 11.5% based on assumed cost of debt of 8.0%, assumed cost of equity of 15.0% and a 50%/50% debt-to-equity ratio, (iv) annual maintenance capital spending growth of 2.5% and (v) 8 times earnings before interest, taxes and depreciation and amortization multiple for terminal value. We selected October 1 as our impairment measurement test date and have determined that our goodwill was not impaired as of October 1, 2007 or 2008. If impairment were to occur, the amount of the impairment would be charged against earnings in the period in which the impairment occurred. The amount of the impairment would be determined by subtracting the implied fair value of the reporting unit goodwill from the carrying amount of the goodwill.

Judgments and assumptions are inherent in management’s estimates used to determine the fair value of MMP’s operating segments. The use of alternate judgments and assumptions could result in the recognition of different levels of impairment charges on our consolidated balance sheets.

Other intangible assets are amortized over their estimated useful lives of 5 years up to 25 years. The weighted-average asset life of MMP’s other intangible assets at December 31, 2008 was approximately 9 years. The useful lives are adjusted if events or circumstances indicate there has been a change in the remaining useful lives. MMP’s other intangible assets are reviewed for impairment whenever events or changes in circumstances indicate that the recoverability of the carrying amount of the intangible asset should be assessed. MMP recognized no impairments for other intangible assets in 2007 or 2008.

Impairment of Long-Lived Assets.MMP has adopted SFAS No. 144,Accounting for the Impairment or Disposal of Long-Lived Assets. In accordance with this Statement, MMP evaluates its long-lived assets of identifiable business activities, other than those held for sale, for impairment when events or changes in circumstances indicate, in management’s judgment, that the carrying value of such assets may not be recoverable. The determination of whether impairment has occurred is based on management’s estimate of undiscounted future cash flows attributable to the assets as compared to the carrying value of the assets. The amount of the impairment recognized is calculated as the excess of the carrying amount of the asset over the fair value of the assets, as determined either through reference to similar asset sales or by estimating the fair value using a discounted cash flow approach.

Long-lived assets to be disposed of through sales that meet specific criteria are classified as “held for sale” and are recorded at the lower of their carrying value or the estimated fair value less the cost to sell. Until the assets are disposed of, an estimate of the fair value is re-determined when related events or circumstances change. We had no significant assets classified as “held for sale” during 2007 or 2008.

Judgments and assumptions are inherent in management’s estimate of undiscounted future cash flows used to determine recoverability of an asset and the estimate of an asset’s fair value used to calculate the amount of impairment to recognize. The use of alternate judgments and assumptions could result in the recognition of different levels of impairment charges in the financial statements.

MMP recorded impairment against the earnings of its petroleum products pipeline system segment of $2.2 million in 2007. Impairments recorded during 2008 were insignificant. The inputs for the valuation models used in determining the fair value of assets impaired during 2007 and 2008 are Level 3—Significant Unobservable Inputs as described in SFAS No. 157,Fair Value Measurements.

5

MAGELLAN GP, LLC

NOTES TO CONSOLIDATED BALANCE SHEETS—(Continued)

Lease Financings.Direct financing leases are accounted for such that the minimum lease payments plus the unguaranteed residual value accruing to the benefit of the lessor is recorded as the gross investment in the lease. The net investment in the lease is the difference between the total minimum lease payment receivable and the associated unearned income.

Debt Placement Costs.Costs incurred for debt borrowings are capitalized as paid and amortized over the life of the associated debt instrument using the effective interest method. When debt is retired before its scheduled maturity date, any remaining placement costs associated with that debt are written off. When MMP increases the borrowing capacity of its revolving credit facility, the unamortized deferred costs associated with the old revolving credit facility, any fees paid to the creditor and any third-party cost incurred are capitalized and amortized over the term of the new revolving credit facility.

Capitalization of Interest.Interest on borrowed funds is capitalized on projects during construction based on the weighted-average interest rate of MMP’s debt. MMP capitalizes interest on all construction projects requiring three months or longer to complete with total costs exceeding $0.5 million.

Pension and Postretirement Medical and Life Benefit Obligations.MGG GP sponsors three pension plans, which cover substantially all of its employees, a postretirement medical and life benefit plan for selected employees and a defined contribution plan. Our affiliate pension and postretirement benefit liabilities represent the funded status of the present value of benefit obligations of these plans.

MGG GP’s pension, postretirement medical and life benefits costs are developed from actuarial valuations. Actuarial assumptions are established to anticipate future events and are used in calculating the expense and liabilities related to these plans. These factors include assumptions management makes with regard to interest rates, expected investment return on plan assets, rates of increase in health care costs, turnover rates and rates of future compensation increases, among others. In addition, subjective factors such as withdrawal and mortality rates are used to develop actuarial valuations. Management reviews and updates these assumptions on an annual basis. The actuarial assumptions that we use may differ from actual results due to changing market rates or other factors. These differences could result in a significant impact to the amount of pension and postretirement medical and life benefit liabilities we have recorded or may record.

Paid-Time Off Benefits.Affiliate liabilities for paid-time off benefits are recognized for all employees performing services for MMP when earned by those employees. MMP recognized affiliate paid-time off liabilities of $8.8 million and $9.8 million at December 31, 2007 and 2008, respectively. These balances represent the remaining vested paid-time off benefits of employees who support MMP. Affiliate liabilities for paid-time off are reflected in the affiliate payroll and benefits balances of the consolidated balance sheets.

Derivative Financial Instruments.MMP accounts for derivative instruments in accordance with SFAS No. 133,Accounting for Financial Instruments and Hedging Activities (as amended), which establishes accounting and reporting standards requiring that derivative instruments be recorded on the balance sheet at fair value as either assets or liabilities.

For those instruments that qualify for hedge accounting, the accounting treatment depends on each instrument’s intended use and how it is designated. Derivative financial instruments qualifying for hedge accounting treatment can generally be divided into two categories: (1) cash flow hedges and (2) fair value hedges. Cash flow hedges are executed to hedge the variability in cash flows related to a forecasted transaction. Fair value hedges are executed to hedge the value of a recognized asset or liability. At inception of a hedged transaction, MMP documents the relationship between the hedging instrument and the hedged item, the risk management objectives and the methods used for assessing and testing correlation and hedge effectiveness. MMP also assesses, both at the inception of the hedge and on an on-going basis, whether the derivatives that are used in its hedging transactions are highly effective in offsetting changes in cash flows or fair value of the hedge item. If MMP determines that a derivative, originally designated as a cash flow or fair value hedge, is no longer highly effective, it discontinues hedge accounting prospectively by including changes in the fair value of the derivative in current earnings. The changes in fair value of derivative financial instruments that either do not qualify for hedge accounting or are not designated a hedging instrument are included in current earnings.

As part of MMP’s risk management process, it assesses the creditworthiness of the financial and other institutions with which it executes financial derivatives. MMP uses, or has used, derivative agreements primarily for fair value hedges of its debt, cash flow hedges of forecasted debt transactions and for forward purchases and forward sales of petroleum products. Such financial instruments involve the risk of non-performance by the counterparty, which could result in material losses to MMP.

6

MAGELLAN GP, LLC

NOTES TO CONSOLIDATED BALANCE SHEETS—(Continued)

MMP uses derivatives to help manage product purchases and sales. Derivatives that qualify for and are designated as normal purchases and sales are accounted for using traditional accrual accounting. As of December 31, 2008, MMP had commitments under forward purchase contracts for product purchases of approximately 0.1 million barrels that will be accounted for as normal purchases totaling approximately $8.4 million and had commitments under forward sales contracts for product sales of approximately 0.2 million barrels that will be accounted for as normal sales totaling approximately $8.8 million.

MMP has entered into New York Mercantile Exchange (“NYMEX”) commodity based futures contracts to hedge against price changes on the petroleum products it expects to sell in the future. These contracts do not qualify as normal sales or for hedge accounting treatment under SFAS No. 133,Accounting for Derivative Instruments and Hedging Activities (as amended); therefore, MMP recognizes gains or losses from these agreements currently in earnings. At December 31, 2008, the fair value of MMP’s NYMEX agreements, representing 0.6 million barrels of petroleum products, was $20.2 million, which we and MMP recognized as energy commodity derivative contracts on our consolidated balance sheets.

MMP has used interest rate derivatives to help manage interest rate risk. For derivatives designated as hedging instruments, MMP reports gains, losses and any ineffectiveness from interest rate derivatives in its results of operations. MMP recognizes the effective portion of cash flow hedges, which hedge against changes in interest rates, as adjustments to other comprehensive income. MMP records the non-current portion of unrealized gains or losses associated with fair value hedges on long-term debt as adjustments to long-term debt with the current portion recorded as adjustments to interest expense. MMP reports the change in fair value of interest rate derivatives that are not designated as hedging instruments currently in earnings.

Deferred Transportation Revenue and Costs.Customers on MMP’s petroleum products pipeline are invoiced for transportation services when their product enters MMP’s system. At each period end, MMP records all invoiced amounts associated with products that have not yet been delivered (in-transit products) as a deferred liability. Additionally, at each period end MMP defers the direct costs it has incurred associated with these in-transit products until delivery occurs. These deferred costs are determined using judgments and assumptions that management considers reasonable.

Equity-Based Incentive Compensation Awards.The compensation committee of our board of directors has issued incentive awards of MMP phantom units without distribution equivalent rights representing limited partner interests in MMP to certain employees of MGG GP who support MMP. We have also issued MMP phantom units with distribution equivalent rights to certain of our directors. These awards are accounted for as prescribed in SFAS No. 123(R),Share-Based Payments.

Under SFAS No. 123(R), MMP classifies unit award grants as either equity or liabilities. Fair value for MMP award grants classified as equity is determined on the grant date of the award and this value is recognized as compensation expense ratably over the requisite service period, which is the vesting period of each unit award. Fair value for MMP equity awards is calculated as the closing price of MMP’s common units representing limited partner interests in it on the grant date reduced by the present value of expected per-unit distributions to be paid by MMP during the requisite service period. MMP unit award grants classified as liabilities are re-measured at fair value on the close of business at each reporting period end until settlement date. Compensation expense for MMP liability awards for each period is the re-measured value of the award grants times the percentage of the requisite service period completed less previously-recognized compensation expense.

Certain MMP unit award grants include performance and other provisions, which can result in payouts to the recipients from zero up to 200% of the amount of the award. Additionally, certain MMP unit award grants are also subject to personal and other performance components which could increase or decrease the number of units to be paid out by 20%. Judgments and assumptions of the final award payouts are inherent in the accruals recorded for unit-based incentive compensation costs. The use of alternate judgments and assumptions could result in the recognition of different levels of unit-based incentive compensation liabilities in our consolidated balance sheets.

Environmental.Environmental expenditures that relate to current or future revenues are expensed or capitalized based upon the nature of the expenditures. Expenditures that relate to an existing condition caused by past operations that do not contribute to current or future revenue generation are expensed. Liabilities are recorded when environmental costs are probable and can be reasonably estimated. Environmental liabilities are recorded on an undiscounted basis except for those instances where the amounts and timing of the future payments are fixed or reliably determinable. MMP uses the risk-free interest rate to discount these liabilities. At

7

MAGELLAN GP, LLC

NOTES TO CONSOLIDATED BALANCE SHEETS—(Continued)

December 31, 2008, expected payments on discounted liabilities were $0.3 million during each year in 2009, 2010 and 2011 and $0.2 million each year in 2012 and 2013 and $4.4 million for all periods thereafter. A reconciliation of our undiscounted environmental liabilities to amounts reported on our consolidated balance sheets is provided in the table below (in thousands). See Note 12—Commitments and Contingencies for a discussion of the changes in our environmental liabilities between December 31, 2007 and December 31, 2008.

| | | | | | | | |

| | | December 31, | |

| | | 2007 | | | 2008 | |

Aggregate undiscounted environmental liabilities | | $ | 63,165 | | | $ | 47,549 | |

Amount of environmental liabilities discounted | | | (5,547 | ) | | | (5,749 | ) |

| | | | | | | | |

Environmental liabilities as reported | | $ | 57,618 | | | $ | 41,800 | |

| | | | | | | | |

Environmental liabilities are recorded independently of any potential claim for recovery. Accruals related to environmental matters are generally determined based on site-specific plans for remediation, taking into account currently available facts, existing technologies and presently enacted laws and regulations. Accruals for environmental matters reflect prior remediation experience and include an estimate for costs such as fees paid to contractors and outside engineering, consulting and law firms. MMP maintains selective insurance coverage, which may cover all or portions of certain environmental expenditures. Receivables are recognized in cases where the realization of reimbursements of remediation costs is considered probable. MMP would sustain losses to the extent of amounts it has recognized as environmental receivables if the counterparties to these transactions become insolvent or are otherwise unable to perform their obligations.

Management has determined that certain costs would have been covered by the indemnifications of MMP by a former affiliate, which have been settled (see Note 12—Commitments and Contingencies). Management makes judgments on what would have been covered by these indemnifications. All costs charged to MMP’s income that would have been covered by these indemnifications are charged directly to MMP’s general partner in determining MMP’s allocation of net income (seeNon-Controlling Owners’ Interests of Consolidated Subsidiaries discussion below).

The determination of the accrual amounts recorded for environmental liabilities include significant judgments and assumptions made by management. The use of alternate judgments and assumptions could result in the recognition of different levels of environmental remediation costs in our consolidated balance sheets.

Non-Controlling Owners’ Interests of Consolidated Subsidiaries (“Non-Controlling Interest”). The non-controlling interest on our balance sheets reflects the outside ownership interest of MMP, which was approximately 98% at December 31, 2007 and 2008. Each quarter, we calculate non-controlling interest expense by multiplying the non-controlling owners’ proportionate ownership of limited partner units in MMP by the limited partners’ allocation of MMP’s net income, less allocations of amounts associated with each period’s amortization of the step-up in basis of the assets and liabilities of MMP. For purposes of calculating non-controlling interest, in periods where distributions exceed net income, MMP’s net income is allocated to its general and limited partners based on their proportionate share of cash distributions for the period, with adjustments made for certain charges which are specifically allocated to MMP’s general partner. However, for periods in which MMP’s net income exceeds its distributions, the net income allocation is adjusted as if the undistributed net income is allocated approximately 2% to the general partner and the remainder to the limited partners.

Income Taxes.We and MMP are partnerships for income tax purposes and therefore are not subject to federal income taxes or state income taxes. The tax on our and MMP’s net income is borne by our respective individual partners through the allocation of taxable income. Net income for financial statement purposes may differ significantly from taxable income of unitholders as a result of differences between the tax basis and financial reporting basis of assets and liabilities and the taxable income allocation requirements under our partnership agreement. The aggregate difference in the basis of our net assets for financial and tax reporting purposes cannot be readily determined because information regarding each partner’s tax attributes in us is not available to us.

8

MAGELLAN GP, LLC

NOTES TO CONSOLIDATED BALANCE SHEETS—(Continued)

Segment Disclosures. Total assets and goodwill for MMP’s operating segments at December 31, 2007 and 2008 is provided below:

| | | | | | | | | | | | |

| | | Petroleum

Products

Pipeline

System | | Petroleum

Products

Terminals | | Ammonia

System | | Total |

December 31, 2007 | | | | | | | | |

Segment assets | | $ | 1,693,466 | | $ | 661,339 | | $ | 32,464 | | $ | 2,387,269 |

Corporate assets | | | | | | | | | | | | 29,804 |

| | | | | | | | | | | | |

Total assets | | | | | | | | | | | $ | 2,417,073 |

| | | | | | | | | | | | |

Goodwill | | $ | — | | $ | 11,902 | | $ | — | | $ | 11,902 |

| | | | | | | | | | | | |

Investment in equity method investee | | $ | 24,324 | | $ | — | | $ | — | | $ | 24,324 |

| | | | | | | | | | | | |

December 31, 2008 | | | | | | | | |

Segment assets | | $ | 1,715,336 | | $ | 778,652 | | $ | 38,581 | | $ | 2,532,569 |

Corporate assets | | | | | | | | | | | | 64,052 |

| | | | | | | | | | | | |

Total assets | | | | | | | | | | | $ | 2,596,621 |

| | | | | | | | | | | | |

Goodwill | | $ | 2,864 | | $ | 11,902 | | $ | — | | $ | 14,766 |

| | | | | | | | | | | | |

Investment in equity method investee | | $ | 23,190 | | $ | — | | $ | — | | $ | 23,190 |

| | | | | | | | | | | | |

New Accounting Pronouncements

In December 2008, the Financial Accounting Standards Board (“FASB”) issued FASB Staff Position (“FSP”) FAS 132(R)-1,Employers’ Disclosures about Postretirement Benefit Plan Assets. This FSP expands the disclosure requirements for employer pension plans and other postretirement benefit plans to include factors that are pertinent to an understanding of investment policies and strategies. The additional disclosure requirements include: (i) for annual financial statements, the fair value of each major category of plan assets separately for pension and other postretirement plans, (ii) a narrative description of the basis used to determine the expected long-term rate of return on asset assumption, (iii) information to enable users of financial statements to assess the inputs and valuation techniques used to develop fair value measurements of plan assets at the annual reporting date, (iv) for fair value measurements using unobservable inputs, disclosure of the effect of the measurements on changes in plan assets for the period. This FSP is effective for fiscal years ending after December 15, 2009, with early application permitted. Provisions of this FSP are not required for earlier periods that are presented for comparative purposes. The adoption of this FSP will not have a material impact on our financial position.

In September 2008, the FASB issued Emerging Issues Task Force (“EITF”) No. 08-6Equity Method Investment Accounting Considerations. This EITF requires entities to measure its equity method investments initially at cost in accordance with SFAS No. 141(R)Business Combinations. Further, the EITF clarified that entities should not separately test an investee’s underlying indefinite-lived intangible asset for impairment; however, they are required to recognize other-than-temporary impairments of an equity method investment in accordance with Accounting Principles Bulletin No. 18,The Equity Method of Accounting for Investments in Common Stock. In addition, entities are required to account for a share issuance by an equity method investee as if the investor had sold a proportionate share of its investment. Any gain or loss to the investor resulting from an investee’s share issuance is to be recognized in earnings. This EITF is effective in fiscal years beginning on or after December 15, 2008, and interim periods within those fiscal years and is to be applied prospectively. Earlier application by an entity that has previously adopted an alternative accounting policy is not permitted. The adoption of this ETIF will not have a material impact on our financial position.

In June 2008, the FASB issued FSP EITF Issue No. 03-6-1,Determining Whether Instruments Granted in Share-Based Payment Transactions are Participating Securities. This FSP clarified that unvested share-based payment awards that contain non-forfeitable rights to distributions or distribution equivalents, whether paid or unpaid, are participating securities as defined in SFAS No. 128,Earnings Per Share and are to be included in the computation of earnings per unit pursuant to the two-class method. This FSP is

9

MAGELLAN GP, LLC

NOTES TO CONSOLIDATED BALANCE SHEETS—(Continued)

effective for financial statements issued after December 15, 2008 and interim periods within those years with prior period earnings per unit data retrospectively adjusted. Early application of this FSP is not permitted. Application of this FSP will not have a material impact on our financial position.

In May 2008, the FASB issued SFAS No. 162,The Hierarchy of Generally Accepted Accounting Principles. This Statement identifies the sources of accounting principles and the framework for selecting the principles to be used in the preparation of financial statements that are presented in conformity with GAAP in the United States. The statement will not change our current accounting practices.

In April 2008, the FASB issued FSP No. FAS 142-3,Determination of the Useful Life of Intangible Assets. This FSP amends the factors that should be considered in developing renewal or extension assumptions used to determine the useful life of a recognized intangible asset under SFAS No. 142,Goodwill and Other Intangible Assets. This FSP also expands the disclosures required for recognized intangible assets. This FSP is effective for financial statements issued for fiscal years beginning after December 15, 2008 and interim periods within those fiscal years. Early adoption is prohibited. Adoption of this FSP will not have a material impact on our financial position.

In March 2008, the FASB issued SFAS No. 161,Disclosures about Derivative Instruments and Hedging Activities. SFAS No. 133,Accounting for Derivative Instruments and Hedging Activitiesestablished, among other things, the disclosure requirements for derivative instruments and for hedging activities. SFAS No. 161 amends SFAS No. 133, requiring qualitative disclosures about objectives and strategies for using derivatives, quantitative disclosures about fair value amounts and gains and losses on derivative instruments, and disclosures about credit-risk-related contingent features in derivative agreements. SFAS No. 161 is effective for financial statements issued for fiscal years and interim periods beginning after November 15, 2008. We do not expect that our adoption of this standard will have a material effect on our financial position.

In February 2008, the FASB issued FSP No. 157-1,Application of FASB Statement No. 157 to FASB Statement No. 13 and Other Accounting Pronouncements That Address Fair Value Measurements for Purposes of Lease Classification or Measurement under Statement 13. FSP No. 157-1 amends SFAS No. 157,Fair Value Measurements, to exclude SFAS No. 13,Accounting for Leases, and other accounting pronouncements that address fair value measurements for purposes of lease classification or measurement under Statement 13. However, this scope exception does not apply to assets acquired and liabilities assumed in a business combination that are required to be measured at fair value under SFAS No. 141(R),Business Combinations, or SFAS No. 141 (revised 2007),Business Combinations, regardless of whether those assets and liabilities are related to leases. This FSP is effective with the initial adoption of SFAS No. 157, which we adopted on January 1, 2007. The adoption of this FSP did not have a material effect on our financial position.

In December 2007, the FASB issued SFAS No. 141(R),Business Combinations. This Statement requires, among other things, that entities; (i) recognize, with certain exceptions, 100% of the fair values of assets acquired, liabilities assumed and non-controlling interests in acquisitions of less than a 100% controlling interest when the acquisition constitutes a change in control of the acquired entity; (ii) measure acquirer shares issued in consideration for a business combination at fair value on the acquisition date; (iii) recognize contingent consideration arrangements at their acquisition-date fair values, with subsequent changes in fair value generally reflected in earnings; (iv) recognize, with certain exceptions, pre-acquisition loss and gain contingencies at their acquisition-date fair values; (v) expense, as incurred, acquisition-related transaction costs; and (vi) capitalize acquisition-related restructuring costs only if the criteria in SFAS No. 146,Accounting for Costs Associated with Exit or Disposal Activities (as amended) are met as of the acquisition date. This Statement is to be applied prospectively to business combinations for which the acquisition date is on or after the beginning of the first annual reporting period beginning on or after December 15, 2008. Early application is prohibited. Our initial adoption of this Statement is not expected to have a material impact on our financial position.

In December 2007, the FASB issued SFAS No. 160,Non-Controlling Interests in Consolidated Financial Statements. This Statement requires, among other things, that: (i) the non-controlling interest be clearly identified and presented in the consolidated statement of financial position within equity, but separate from the parent’s equity; (ii) the amount of consolidated net income attributable to the parent and to the non-controlling interest be clearly identified and presented on the face of the consolidated statement of income; (iii) all changes in a parent’s ownership interest while the parent retains its controlling financial interest in its subsidiary be accounted for consistently (as equity transactions); (iv) when a subsidiary is deconsolidated, any retained non-controlling equity investment in the former subsidiary be initially measured at fair value. The gain or loss on the deconsolidation of the subsidiary is measured using the fair value of any non-controlling equity investment rather than the carrying amount of that retained investment; and (v) sufficient disclosures be made to clearly identify and distinguish between the interests of the parent and the interests of non-controlling owners. SFAS No. 160 is effective for fiscal years, and interim periods within those fiscal years, beginning on or after

10

MAGELLAN GP, LLC

NOTES TO CONSOLIDATED BALANCE SHEETS—(Continued)

December 15, 2008. Early adoption is prohibited. Components of our financial position will be materially impacted as the non-controlling owners’ interests will be reported as a component of equity instead of being reported as a liability.

In February 2007, the FASB issued SFAS No. 159,The Fair Value Option for Financial Assets and Financial Liabilities.This Statement permits entities to choose to measure many financial instruments and certain other items at fair value, with the objective of mitigating volatility in reported earnings caused by measuring related assets and liabilities differently (without being required to apply complex hedge accounting provisions). We can make an election at the beginning of each fiscal year beginning after November 15, 2007 to adopt this statement. We do not plan to adopt this Statement.

In January 2007, the FASB issued Revised Statement 133 Implementation Issue No. G19,Cash Flow Hedges: Hedging Interest Rate Risk for the Forecasted Issuances of Fixed-Rate Debt Arising from a Rollover Strategy.This Implementation Issue clarified that in a cash flow hedge of a variable-rate financial asset or liability, the designated risk being hedged cannot be the risk of changes in its cash flows attributable to changes in the specifically identified benchmark rate if the cash flows of the hedged transaction are explicitly based on a different index. Our adoption of this Implementation Issue did not have a material impact on our financial position.

In January 2007, the FASB issued Statement 133 Implementation Issue No. G26,Cash Flow Hedges: Hedging Interest Cash Flows on Variable-Rate Assets and Liabilities That Are Not Based on a Benchmark Interest Rate.This Implementation Issue clarified, given the guidance in Implementation Issue No. G19, that an entity may hedge the variability in cash flows by designating the hedged risk as the risk of overall changes in cash flows. The effective date of this guidance for us was April 1, 2007. Our adoption of this Implementation Issue did not have a material impact on our financial position.

3. Inventory

Inventory at December 31, 2007 and 2008 was as follows (in thousands):

| | | | | | |

| | | December 31, |

| | | 2007 | | 2008 |

Refined petroleum products | | $ | 65,215 | | $ | 20,917 |

Transmix | | | 32,824 | | | 13,099 |

Natural gas liquids | | | 16,233 | | | 7,534 |

Additives | | | 5,812 | | | 6,184 |

Other | | | 378 | | | — |

| | | | | | |

Total inventories | | $ | 120,462 | | $ | 47,734 |

| | | | | | |

During 2008 MMP recorded a $19.7 million lower-of-average-cost-or-market adjustment to its transmix inventory associated with its product overages and shortages. In addition, during 2008 MMP recorded lower-of-average-cost-or-market adjustments of $6.4 million and $3.0 million to its refined petroleum products inventory and transmix inventory, respectively, associated with its butane blending and fractionation activities.

The decrease in refined petroleum products inventory from 2007 to 2008 was primarily attributable to the sale of refined petroleum products inventory in connection with the assignment of a product supply agreement to a third-party entity effective March 1, 2008 as well as a significant decrease in the prices of products that comprised inventory during 2008.

11

MAGELLAN GP, LLC

NOTES TO CONSOLIDATED BALANCE SHEETS—(Continued)

4. Property, Plant and Equipment

Property, plant and equipment consisted of the following (in thousands):

| | | | | | | | |

| | | December 31, | | Estimated Depreciable |

| | | 2007 | | 2008 | | Lives |

Construction work-in-progress | | $ | 112,891 | | $ | 120,521 | | |

Land and rights-of-way | | | 56,715 | | | 58,847 | | |

Carrier property | | | 1,406,295 | | | 1,470,123 | | 6 – 59 years |

Buildings | | | 15,467 | | | 20,048 | | 20 – 53 years |

Storage tanks | | | 427,159 | | | 515,606 | | 20 – 40 years |

Pipeline and station equipment | | | 224,324 | | | 228,961 | | 3 – 59 years |

Processing equipment | | | 301,134 | | | 405,431 | | 3 – 56 years |

Other | | | 59,277 | | | 72,161 | | 3 – 48 years |

| | | | | | | | |

Total | | $ | 2,603,262 | | $ | 2,891,698 | | |

| | | | | | | | |

Carrier property is defined as pipeline assets regulated by the FERC. Other includes interest capitalized of $22.5 million and $25.4 million at December 31, 2007 and 2008, respectively.

5. Concentration of Risks

MMP transports, stores and distributes petroleum products for refiners, marketers, traders and end-users of those products. The major concentration of MMP’s petroleum products pipeline system’s revenues is derived from activities conducted in the central United States. Transportation and storage revenues are generally secured by warehouseman’s liens. MMP periodically evaluates the financial condition and creditworthiness of its customers and requires additional security as it deems necessary.

The employees assigned to conduct MMP’s operations are employees of MGG GP. As of December 31, 2008, MGG GP employed 1,204 employees.

At December 31, 2008, the labor force of 577 employees assigned to MMP’s petroleum products pipeline system was concentrated in the central United States. Approximately 37% of these employees were represented by the United Steel Workers Union (“USW”). MGG GP’s collective bargaining agreement with the USW was ratified by the union members in February 2009. This agreement expires January 31, 2012. The labor force of 296 employees assigned to MMP’s petroleum products terminals operations at December 31, 2008 is primarily concentrated in the southeastern and Gulf Coast regions of the United States. Approximately 10% of these employees were represented by the International Union of Operating Engineers (“IUOE”) and covered by a collective bargaining agreement that expires in October 2010. On July 1, 2008, MMP assumed operations of its ammonia pipeline from a third-party pipeline company. At December 31, 2008, the labor force of 19 employees assigned to MMP’s ammonia pipeline system was concentrated in the central United States and none of these employees were covered by a collective bargaining agreement.

6. Employee Benefit Plans

MGG GP sponsors two union pension plans for certain employees (“USW plan” and “IUOE plan”) and a pension plan for certain non-union employees (“Salaried plan”), a postretirement benefit plan for selected employees and a defined contribution plan. MMP is required to reimburse MGG GP for all costs for its obligations associated with the pension plans, postretirement plan and defined contribution plan for qualifying individuals assigned to MMP’s operations.

In December 2006, we adopted SFAS No. 158,Employers’ Accounting for Defined Benefit Pension and Other Postretirement Plans. Upon adoption of SFAS No. 158, we recognized the funded status of the present value of the benefit obligation of MGG GP’s pension plans and its postretirement medical and life benefit plan.

12

MAGELLAN GP, LLC

NOTES TO CONSOLIDATED BALANCE SHEETS—(Continued)

The annual measurement date for the aforementioned plans is December 31. The following table presents the changes in affiliate benefit obligations and plan assets for pension benefits and other postretirement benefits for the year ended December 31, 2007 and 2008 (in thousands):

| | | | | | | | | | | | | | | | |

| | | Pension Benefits | | | Other Postretirement

Benefits | |

| | | 2007 | | | 2008 | | | 2007 | | | 2008 | |

Change in affiliate benefit obligation: | | | | | | | | | | | | | | | | |

Affiliate benefit obligation at beginning of year | | $ | 43,849 | | | $ | 42,117 | | | $ | 15,004 | | | $ | 17,069 | |

Service cost | | | 5,765 | | | | 5,473 | | | | 533 | | | | 435 | |

Interest cost | | | 2,539 | | | | 2,698 | | | | 1,026 | | | | 1,029 | |

Plan participants’ contributions | | | — | | | | — | | | | 61 | | | | 108 | |

Actuarial (gain) loss | | | (837 | ) | | | 2,709 | | | | 661 | | | | 1,133 | |

Benefits paid | | | (951 | ) | | | (1,799 | ) | | | (216 | ) | | | (617 | ) |

Pension settlement | | | (8,248 | ) | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | |

Affiliate benefit obligation at end of year | | | 42,117 | | | | 51,198 | | | | 17,069 | | | | 19,157 | |

Change in plan assets: | | | | | | | | | | | | | | | | |

Fair value of plan assets at beginning of year | | | 29,416 | | | | 36,599 | | | | — | | | | — | |

Employer contributions | | | 15,000 | | | | 9,143 | | | | 155 | | | | 509 | |

Plan participants’ contributions | | | — | | | | — | | | | 61 | | | | 108 | |

Actual return on plan assets | | | 1,382 | | | | (5,730 | ) | | | — | | | | — | |

Benefits paid | | | (951 | ) | | | (1,799 | ) | | | (216 | ) | | | (617 | ) |

Pension settlement | | | (8,248 | ) | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | |

Fair value of plan assets at end of year | | | 36,599 | | | | 38,213 | | | | — | | | | — | |

| | | | | | | | | | | | | | | | |

Funded status at end of year | | $ | (5,518 | ) | | $ | (12,985 | ) | | $ | (17,069 | ) | | $ | (19,157 | ) |

| | | | | | | | | | | | | | | | |

Accumulated affiliate benefit obligation | | $ | 31,139 | | | $ | 38,447 | | | | | | | | | |

| | | | | | | | | | | | | | | | |

The amounts included in pension benefits in the previous table combine the union pension plans with the Salaried pension plan. At December 31, 2007, the fair value of MGG GP’s USW and Salaried pension plans’ assets exceeded their respective accumulated benefit obligations and the fair value of the IUOE plan assets was equal to its accumulated benefit obligation. At December 31, 2008, the fair value of the USW plan’s assets exceeded the fair value of the accumulated benefit obligation by $1.8 million and the fair value of the Salaried and IUOE plans’ assets combined were $2.0 million less than the fair value of their accumulated benefit obligation.

Amounts recognized in our consolidated balance sheets were as follows (in thousands):

| | | | | | | | | | | | | | | | |

| | | Pension Benefits | | | Other Postretirement

Benefits | |

| | | 2007 | | | 2008 | | | 2007 | | | 2008 | |

Amounts recognized in consolidated balance sheet: | | | | | | | | | | | | | | | | |

Current accrued benefit cost | | $ | — | | | $ | — | | | $ | (217 | ) | | $ | (355 | ) |

Long-term accrued benefit cost | | | (5,518 | ) | | | (12,985 | ) | | | (16,852 | ) | | | (18,802 | ) |

| | | | | | | | | | | | | | | | |

| | | (5,518 | ) | | | (12,985 | ) | | | (17,069 | ) | | | (19,157 | ) |

Accumulated other comprehensive income: | | | | | | | | | | | | | | | | |

Net actuarial loss | | | 4,980 | | | | 15,970 | | | | 5,384 | | | | 6,209 | |

Prior service cost (credit) | | | 1,876 | | | | 1,569 | | | | (3,829 | ) | | | (2,977 | ) |

| | | | | | | | | | | | | | | | |

Net amount recognized in consolidated balance sheet | | $ | 1,338 | | | $ | 4,554 | | | $ | (15,514 | ) | | $ | (15,925 | ) |

| | | | | | | | | | | | | | | | |

13

MAGELLAN GP, LLC

NOTES TO CONSOLIDATED BALANCE SHEETS—(Continued)

The weighted-average rate assumptions used to determine benefit obligations as of December 31, 2007 and 2008 were as follows:

| | | | | | | | | | | | |

| | | Pension

Benefits | | | Other

Postretirement

Benefits | |

| | | 2007 | | | 2008 | | | 2007 | | | 2008 | |

Discount rate—Salaried plan | | 6.50 | % | | 6.00 | % | | N/A | | | N/A | |

Discount rate—USW plan | | 6.50 | % | | 6.25 | % | | N/A | | | N/A | |

Discount rate—IUOE plan | | 6.50 | % | | 5.75 | % | | N/A | | | N/A | |

Discount rate—Other Postretirement Benefits | | N/A | | | N/A | | | 6.50 | % | | 5.75 | % |

Rate of compensation increase – Salaried plan | | 5.00 | % | | 5.00 | % | | N/A | | | N/A | |

Rate of compensation increase – USW plan | | 4.50 | % | | 4.50 | % | | N/A | | | N/A | |

Rate of compensation increase – IUOE plan | | 5.00 | % | | 5.00 | % | | N/A | | | N/A | |

The non-pension postretirement benefit plans provide for retiree contributions and contain other cost-sharing features such as deductibles and coinsurance. The accounting for these plans anticipates future cost sharing that is consistent with management’s expressed intent to increase the retiree contribution rate generally in line with health care cost increases.

The annual assumed rate of increase in the health care cost trend rate for 2009 is 7.5% decreasing systematically to 4.5% by 2018 for pre-65 year-old participants and 9.0% decreasing systematically to 5.3% by 2018 for post-65 year-old participants. The health care cost trend rate assumption has a significant effect on the amounts reported. As of December 31, 2008, a 1.0% change in assumed health care cost trend rates would have the following effect (in thousands):

| | | | | | |

| | | 1%

Increase | | 1%

Decrease |

Change in postretirement benefit obligation | | $ | 2,827 | | $ | 2,638 |

The expected long-term rate of return on plan assets was determined by combining a review of projected returns, historical returns of portfolios with assets similar to the current portfolios of the union and non-union pension plans and target weightings of each asset classification. MGG GP’s investment objective for the assets within the pension plans is to earn a return which exceeds the growth of its obligations that result from interest and changes in the discount rate, while avoiding excessive risk. Defined diversification goals are set in order to reduce the risk of wide swings in the market value from year to year, or of incurring large losses that may result from concentrated positions. MGG GP evaluates risks based on the potential impact on the predictability of contribution requirements, probability of under-funding, expected risk-adjusted returns and investment return volatility. Funds are invested with multiple investment managers. MGG GP’s target allocation and actual weighted-average asset allocation percentages at December 31, 2007 and 2008 were as follows

| | | | | | | | | | | | |

| | | 2007 | | | 2008 | |

| | | Actual | | | Target | | | Actual (a) | | | Target | |

Equity securities | | 55 | % | | 63 | % | | 30 | % | | 40 | % |

Debt securities | | 29 | % | | 36 | % | | 59 | % | | 59 | % |

Other | | 16 | % | | 1 | % | | 11 | % | | 1 | % |

| (a) | MMP made cash contributions of $15.0 million and $9.1 million to the pension plans in the 2007 and 2008 fiscal years, respectively. Amounts contributed in 2007 and 2008 in excess of benefit payments made were to be invested in debt and equity securities over a twelve-month period, with the amounts that remained uninvested as of December 31, 2007 and 2008 scheduled for investment in accordance with the target. Excluding these uninvested cash amounts, MGG GP’s actual allocation percentages at December 31, 2007 would have been 66% equity securities and 34% debt securities and at December 31, 2008, would have been 33% equity securities and 67% debt securities. In 2009, these uninvested cash amounts will be invested to bring the total asset allocation in line with the target allocation. |

14

MAGELLAN GP, LLC

NOTES TO CONSOLIDATED BALANCE SHEETS—(Continued)

As of December 31, 2008, benefit amounts expected to be paid through December 31, 2018 were as follows (in thousands):

| | | | | | |

| | | Pension

Benefits | | Other

Postretirement

Benefits |

2009 | | $ | 1,922 | | $ | 355 |

2010 | | | 2,084 | | | 439 |

2011 | | | 2,252 | | | 533 |

2012 | | | 2,390 | | | 629 |

2013 | | | 2,400 | | | 714 |

2014 through 2018 | | | 15,884 | | | 4,747 |

Contributions estimated to be paid in 2009 are $7.2 million and $0.4 million for the pension and other postretirement benefit plans, respectively.

7. Related Party Transactions

Under a services agreement, MMP reimburses MGG GP for the costs of employees necessary to conduct its operations and administrative functions. Current affiliate payroll and benefits accruals associated with this agreement at December 31, 2007 and 2008 were $23.4 million and $18.1 million, respectively, and long-term affiliate pension and benefits accrual at December 31, 2007 and 2008 was $22.4 million and $31.8 million, respectively. MMP settles its payroll, payroll-related expenses and non-pension postretirement benefit costs with MGG GP on a monthly basis. MMP funds its long-term affiliate pension liabilities through payments to MGG GP when MGG GP makes contributions to its pension funds.

One of our former independent board members, John P. DesBarres, served as a board member for American Electric Power Company, Inc. (“AEP”) of Columbus, Ohio until December 2008. Mr. DesBarres passed away on December 29, 2008. For the years ended December 31, 2007 and 2008, MMP’s operating expenses included $2.7 million and $2.8 million, respectively, of power costs incurred with Public Service Company of Oklahoma (“PSO”), which is a subsidiary of AEP. MMP had no amounts payable to or receivable from PSO or AEP at December 31, 2007 or December 29, 2008.

Because MMP’s distributions have exceeded target levels as specified in its partnership agreement, we receive approximately 50%, including our approximate 2% general partner interest, of any incremental cash distributed per MMP limited partner unit. As of December 31, 2008, our executive officers collectively owned a beneficial interest in MGG of less than 1%; therefore, our executive officers also indirectly benefit from these distributions. In 2007 and 2008, distributions we received from MMP, based on our general partner interest and incentive distribution rights, totaled $70.3 million and $85.6 million, respectively.

In January 2008, MMP issued 197,433 limited partner units primarily to settle the 2005 unit award grants to certain employees, which vested on December 31, 2007. We did not make an equity contribution associated with this equity issuance and as a result our general partner ownership interest in MMP changed from 1.995% to 1.989%.

In January 2009, MMP issued 210,149 limited partner units primarily to settle the 2007 unit award grants to certain employees, which vested on December 31, 2008. We did not make an equity contribution associated with this equity issuance and a result, our general partner ownership in MMP changed from 1.989% to 1.983%. See Note 17—Subsequent Events for further discussion of this matter.

15

MAGELLAN GP, LLC

NOTES TO CONSOLIDATED BALANCE SHEETS—(Continued)

8. Debt

Consolidated debt at December 31, 2007 and 2008 was as follows (in thousands):

| | | | | | |

| | | December 31, |

| | | 2007 | | 2008 |

Revolving credit facility | | $ | 163,500 | | $ | 70,000 |

6.45% Notes due 2014 | | | 249,634 | | | 249,681 |

5.65% Notes due 2016 | | | 252,494 | | | 253,328 |

6.40% Notes due 2018 | | | — | | | 261,555 |

6.40% Notes due 2037 | | | 248,908 | | | 248,921 |

| | | | | | |

Total Debt | | $ | 914,536 | | $ | 1,083,485 |

| | | | | | |

The face value of MMP’s debt outstanding as of December 31, 2008 was $1,070.0 million. The difference between the face value and carrying value of MMP’s debt outstanding was amounts recognized for discounts incurred on debt issuances and the unamortized portion of gains recognized on derivative financial instruments which had qualified as fair value hedges of MMP’s long-term debt until the hedges were terminated or hedge accounting treatment was discontinued. At December 31, 2008, maturities of MMP’s debt were as follows: $0 in 2009, 2010 and 2011; $70.0 million in 2012; $0 in 2013; and $1.0 billion thereafter. MMP’s debt is non-recourse to us.

Revolving Credit Facility.In September 2007, MMP amended and restated its revolving credit facility to increase the borrowing capacity from $400.0 million to $550.0 million. In addition, the maturity date of the revolving credit facility was extended from May 2011 to September 2012. MMP incurred $0.2 million of legal and other costs associated with this amendment. Borrowings under the facility remain unsecured and incur interest at LIBOR plus a spread that ranges from 0.3% to 0.8% based on MMP’s credit ratings and amounts outstanding under the facility. Borrowings under this facility are used primarily for general purposes, including capital expenditures. As of December 31, 2008, $70.0 million was outstanding under this facility and $3.9 million was obligated for letters of credit. Amounts obligated for letters of credit are not reflected as debt on our consolidated balance sheets. The weighted-average interest rate on borrowings outstanding under the facility at December 31, 2007 and 2008 was 5.4% and 4.8%, respectively. Additionally, a commitment fee is assessed at a rate of 0.05% to 0.125%, depending on MMP’s credit rating. Borrowings outstanding under this facility as of July 14, 2008 of $212.0 million were repaid with the net proceeds from MMP’s debt offering of 10-year senior notes completed in July 2008 (see6.40% Notes due 2018 below).

6.45% Notes due 2014. In May 2004, MMP sold $250.0 million aggregate principal of 6.45% notes due 2014 in an underwritten public offering. The notes were issued for the discounted price of 99.8%, or $249.5 million, and the discount is being accreted over the life of the notes. Including the impact of amortizing the gains realized on the hedges associated with these notes (see Note 9—Derivative Financial Instruments), the effective interest rate of these notes is 6.3%.

5.65% Notes due 2016. In October 2004, MMP issued $250.0 million of 5.65% senior notes due 2016 in an underwritten public offering. The notes were issued for the discounted price of 99.9%, or $249.7 million, and the discount is being accreted over the life of the notes. MMP used an interest rate swap to effectively convert $100.0 million of these notes to floating-rate debt until May 2008 (see Note 9—Derivative Financial Instruments). Including the amortization of the $3.8 million gain realized from terminating that interest rate swap and the amortization of losses realized on pre-issuance hedges associated with these notes, the weighted-average interest rate of these notes at December 31, 2007 and 2008 was 5.5% and 5.7%, respectively. The outstanding principal amount of the notes was increased by $2.7 million at December 31, 2007 for the fair value of the associated swap-to-floating derivative instrument and by $3.5 million at December 31, 2008 for the unamortized portion of the gain recognized upon termination of that swap.

6.40% Notes due 2018. In July 2008, MMP issued $250.0 million of 6.40% notes due 2018 in an underwritten public offering. Net proceeds from the offering, after underwriter discounts of $1.6 million and offering costs of $0.4 million, were $248.0 million. The net proceeds were used to repay the $212.0 million of borrowings outstanding under MMP’s revolving credit facility at that time, and the balance was used for general purposes. In connection with this offering, MMP entered into $100.0 million of interest rate swap agreements to hedge against changes in the fair value of a portion of these notes, effectively converting $100.0 million of these notes to floating-rate debt (see Note 9—Derivative Financial Instruments). These agreements originally expired on July 15, 2018, the

16

MAGELLAN GP, LLC

NOTES TO CONSOLIDATED BALANCE SHEETS—(Continued)

maturity date of the 6.40% notes; however, in December 2008 MMP terminated $50.0 million of these agreements and discontinued hedge accounting on the remaining $50.0 million, resulting in it recognizing gains of $11.7 million. The outstanding principal amount of the notes was increased by $11.7 million at December 31, 2008 for the unamortized portion of those gains. Including the amortization of those gains, the weighted-average interest rate of these notes at December 31, 2008 was 5.9%.

6.40% Notes due 2037. In April 2007, MMP issued $250.0 million of 6.40% notes due 2037 in an underwritten public offering. The notes were issued for the discounted price of 99.6%, or $248.9 million, and the discount is being accreted over the life of the notes. Net proceeds from the offering, after underwriter discounts of $2.2 million and offering costs of $0.3 million, were $246.4 million. The net proceeds were used to repay a portion of other notes that were outstanding at that time. Including the impact of amortizing the gains realized on the interest hedges associated with these notes (see Note 9—Derivative Financial Instruments), the effective interest rate of these notes is 6.3%.

The revolving credit facility described above requires MMP to maintain a specified ratio of consolidated debt to EBITDA of no greater than 4.75 to 1.00. In addition, the revolving credit facility and the indentures under which MMP’s public notes were issued contain covenants that limit MMP’s ability to, among other things, incur indebtedness secured by certain liens or encumber its assets, engage in certain sale-leaseback transactions, and consolidate, merge or dispose of all or substantially all of its assets. MMP was in compliance with these covenants as of December 31, 2008.

The revolving credit facility and notes described above are senior indebtedness.

9. Derivative Financial Instruments

Commodity Derivatives

MMP’s petroleum products blending activities generate gasoline products and MMP can estimate the timing and quantities of sales of these products. MMP uses forward sales agreements to lock in forward sales prices and most of the gross margins realized from its blending activities. MMP accounts for these forward sales agreements as normal sales.

In addition to forward sales agreements, MMP uses NYMEX contracts to lock in forward sales prices. Although these NYMEX agreements represent an economic hedge against price changes on the petroleum products MMP expects to sell in the future, they do not qualify as normal purchases or for hedge accounting treatment under SFAS No. 133,Accounting for Derivative Instruments and Hedging Activities (as amended); therefore, MMP recognizes the change in fair value of these agreements currently in earnings. During 2008, MMP closed its positions on NYMEX contracts associated with the sale of 0.5 million barrels of gasoline, and recognized total gains of $30.7 million as product sales revenues. At December 31, 2008, the fair value of MMP’s open NYMEX contracts, representing 0.6 million barrels of petroleum product, was a gain of $20.2 million, which we and MMP recognized as energy commodity derivative contracts on our consolidated balance sheet. These open NYMEX contracts mature between January 2009 and April 2009. At December 31, 2008, MMP had received $19.0 million in margin cash from these agreements, which we and MMP recorded as energy commodity derivatives deposit on our consolidated balance sheets.

17

MAGELLAN GP, LLC

NOTES TO CONSOLIDATED BALANCE SHEETS—(Continued)

Interest Rate Derivatives

MMP uses interest rate derivatives to help manage interest rate risk. As of December 31, 2008, MMP had two offsetting interest rate swap agreements outstanding:

| | • | | In July 2008, MMP entered into a $50.0 million interest rate swap agreement (“Derivative A”) to hedge against changes in the fair value of a portion of the $250.0 million of 6.40% notes due 2018. Derivative A effectively converted $50.0 million of those notes from a 6.40% fixed rate to a floating rate of six-month LIBOR plus 1.83% and terminates in July 2018. MMP originally accounted for Derivative A as a fair value hedge. On December 8, 2008, in order to capture the economic value of Derivative A at that time, we entered into an offsetting derivative as described below, and discontinued hedge accounting on Derivative A. The $5.4 million fair value of Derivative A at that time was recorded as an adjustment to long-term debt and is being amortized over the remaining life of the 6.40% fixed-rate notes due 2018. The fair value of Derivative A as of December 31, 2008 was $7.5 million, of which $0.3 million was recorded to other current assets and $7.2 million was recorded to noncurrent assets on our consolidated balance sheet. |