Table of Contents

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 20-F

(Mark One)

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

or

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2007

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period to

or

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell report

Commission file number 1-15154

ALLIANZ SE

(Exact name of registrant as specified in its charter)

Federal Republic of Germany

(Jurisdiction of incorporation or organization)

Königinstrasse 28, 80802 Munich, Germany

(Address of principal executive offices)

Burkhard Keese

ALLIANZ SE

Königinstrasse 28, 80802 Munich, Germany

Telephone: +49 89 3800-16596

Facsimile: +49 89 3800-16598

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

| Ordinary Shares (without par value)* | The New York Stock Exchange, Inc. |

| * | Not for trading, but only in connection with the listing of American Depositary Shares, pursuant to the requirements of the New York Stock Exchange. |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock at December 31, 2007:

Ordinary shares, without par value | 452,350,000 shares |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

YES x NO ¨

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

YES ¨ NO x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

YES x NO ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer x | Accelerated filer ¨ | Non-accelerated filer ¨ |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ¨

International Financial Reporting Standards as issued by the International Accounting Standards Board x

Other ¨

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ¨ Item 18 ¨

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

YES ¨ NO x

Table of Contents

Item | Page | |||

| i | ||||

| 1 | ||||

| 2 | ||||

ITEM 1. | 3 | |||

ITEM 2. | 3 | |||

ITEM 3. | 3 | |||

| 3 | ||||

| 5 | ||||

| 5 | ||||

| 6 | ||||

ITEM 4. | 14 | |||

| 14 | ||||

| 16 | ||||

| 17 | ||||

| 18 | ||||

| 28 | ||||

Selected Statistical Information Relating to our Banking Operations | 41 | |||

| 63 | ||||

ITEM 4A. | 68 | |||

ITEM 5. | 69 | |||

| 69 | ||||

| 80 | ||||

| 80 | ||||

| 84 | ||||

| 93 | ||||

| 101 | ||||

Item | Page | |||

| 109 | ||||

| 115 | ||||

| 121 | ||||

| 123 | ||||

| 130 | ||||

Investment Portfolio Impairments, Depreciation and Unrealized Losses | 135 | |||

| 138 | ||||

| 139 | ||||

ITEM 6. | 141 | |||

| 141 | ||||

| 143 | ||||

| 145 | ||||

| 149 | ||||

| 155 | ||||

| 155 | ||||

| 155 | ||||

| 156 | ||||

| 156 | ||||

ITEM 7. | 156 | |||

| 156 | ||||

| 157 | ||||

ITEM 8. | 157 | |||

| 157 | ||||

| 157 | ||||

| 157 | ||||

| 157 | ||||

ITEM 9. | 158 | |||

| 158 | ||||

| 158 | ||||

ITEM 10. | 159 | |||

| 159 | ||||

| 161 |

i

Table of Contents

TABLE OF CONTENTS

Item | Page | |||

| 161 | ||||

| 161 | ||||

| 161 | ||||

| 164 | ||||

| 166 | ||||

ITEM 11. | 167 | |||

| 167 | ||||

Internal Risk CapitalFramework | 168 | |||

| 172 | ||||

| 174 | ||||

| 175 | ||||

| 182 | ||||

| 185 | ||||

| 186 | ||||

| 187 | ||||

| 190 | ||||

ITEM 12. | 190 | |||

ITEM 13. | 190 |

Item | Page | |||

ITEM 14. | Material Modifications to the Rights of Security Holders and Use of Proceeds | 190 | ||

ITEM 15. | 190 | |||

ITEM 16A. | 192 | |||

ITEM 16B. | 192 | |||

ITEM 16C. | 192 | |||

ITEM 16D. | 193 | |||

ITEM 16E. | Purchases of Equity Securities by the Issuer and Affiliated Purchasers | 194 | ||

ITEM 17. | 195 | |||

ITEM 18. | 195 | |||

ITEM 19. | 195 | |||

Index to the Consolidated Financial Statements and Schedules | ||||

ii

Table of Contents

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

In this Annual Report, the terms “we,” “us” and “our” refer to Allianz Societas Europaea (or Allianz SE, and together with its consolidated subsidiaries, the Allianz Group), unless the context requires otherwise.

Unless otherwise indicated, when we use the term “consolidated financial statements,” we are referring to the consolidated financial statements (including the related notes) of Allianz SE as of December 31, 2007 and 2006 and for each of the years in the three-year period ended December 31, 2007, which have been audited by KPMG Deutsche Treuhand-Gesellschaft AG Wirtschaftsprüfungsgesellschaft. The consolidated financial statements of the Allianz Group have been prepared in conformity with International Financial Reporting Standards (“IFRS”), as adopted under European Union (“EU”) regulations in accordance with section 315a of the German Commercial Code (“HGB”). The consolidated financial statements of the Allianz Group have also been prepared in accordance with IFRS as issued by the International Accounting Standard Board (“IASB”). The Allianz Group’s application of IFRSs results in no differences between IFRS as adopted by the EU and IFRS as issued by the IASB. The amounts set forth in some of the tables may not add up to the total amounts given in those tables due to rounding.

References herein to “$”, “U.S.$” and “U.S. Dollar” are to United States Dollars and references to “€” and “Euro” are to the Euro, the single currency established for participants in the third stage of the European Economic and Monetary Union (or EMU), commencing January 1, 1999. We refer to the countries participating in the third stage of the EMU as the “Euro zone.”

For convenience only (except where noted otherwise), some of the Euro figures have been translated into U.S. Dollars at the rate of $1.5369 = €1.00, the noon buying rate in New York for cable transfers in Euros certified by the Federal Reserve Bank of New York for customs purposes on March 10, 2008. These translations do not mean

that the Euro amounts actually represent those U.S. Dollar amounts or could be converted into U.S. Dollars at those rates. See “Key Information—Exchange Rate Information” for information concerning the noon buying rates for the Euro from January 1, 2003 through March 10, 2008.

Unless otherwise indicated, when we use the terms “gross premiums,” “gross premiums written” and “gross written premiums,” we are referring to premiums (whether or not earned) for insurance policies written during a specific period, without deduction for premiums ceded to reinsurers, and when we use the terms “net premiums,” “net premiums written” and “net written premiums,” we are referring to premiums (whether or not earned) for insurance policies written during a specified period, after deduction for premiums ceded to reinsurers. When we use the term “statutory premiums,” we are referring to gross premiums written from sales of life insurance policies as well as gross receipts from sales of unit-linked and other investment-oriented products, in accordance with the statutory accounting practices applicable in the relevant insurer’s home jurisdiction.

Unless otherwise indicated, we have obtained data regarding the relative size of various national insurance markets from annual reports prepared by SIGMA, an independent organization that publishes market research data on the insurance industry. In addition, unless otherwise indicated, insurance market share data are based on gross premiums written and statutory premiums for our Property-Casualty and Life/Health segments, respectively. Data on position and market share within particular countries are based on various third party and/or internal sources as indicated herein.

1

Table of Contents

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This annual report includes “forward-looking statements” within the meaning of the safe harbor provisions of The Private Securities Litigation Reform Act of 1995. These include statements under “Information on the Company,” “Operating and Financial Review and Prospects,” “Quantitative and Qualitative Disclosures About Market Risk” and elsewhere in this annual report relating to, among other things, our future financial performance, plans and expectations regarding developments in our business, growth and profitability, and general industry and business conditions applicable to the Allianz Group. These forward-looking statements can generally be identified by terminology such as “may,” “will,” “should,” “expects,” “plans,” “intends,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” or “continue” or other similar terminology. We have based these forward-looking statements on our current expectations, assumptions, estimates and projections about future events. These forward-looking statements are subject to a number of risks, uncertainties, assumptions and other factors that may cause our actual results, performance or achievements or those of our industry to be materially different from or worse than those expressed or implied by these forward-looking statements. These factors include, without limitation:

| • | general economic conditions, including in particular economic conditions in our core business areas and core markets; |

| • | function and performance of global financial markets, including emerging markets; |

| • | frequency and severity of insured loss events, including terror attacks, environmental and asbestos claims; |

| • | mortality and morbidity levels and trends; |

| • | persistency levels; |

| • | interest rate levels; |

| • | currency exchange rate developments, including the Euro/U.S. Dollar exchange rate; |

| • | levels of additional loan loss provisions; |

| • | further impairments of investments; |

| • | general competitive factors, in each case on a local, regional, national and global level; |

| • | changes in laws and regulations, including in the United States and in the European Union; |

| • | changes in the policies of central banks and/or foreign governments; |

| • | the impact of acquisitions, including related integration and restructuring issues; and |

| • | terror attacks, events of war, and their respective consequences. |

2

Table of Contents

PART I

| ITEM 1. | Identity of Directors, Senior Management and Advisors |

Not applicable.

| ITEM 2. | Offer Statistics and Expected Timetable |

Not applicable.

| ITEM 3. | Key Information |

Selected Consolidated Financial Data

We present below our selected financial data as of and for each of the years in the five-year period ended December 31, 2007. We derived the selected financial data for each of the years in the five-year period ended December 31, 2007 from our audited annual consolidated financial statements, including the notes to those financial statements. All the data should be read in conjunction with our consolidated financial statements and the notes thereto. We prepare our annual audited consolidated financial statements in accordance with IFRS.

Effective January 1, 2006, we implemented certain revisions to our consolidated financial statements to enhance the reader’s understanding of our financial results and to use a more consistent presentation with that of our peers. These revisions reflect certain reclassifications in our consolidated balance sheet and consolidated income statement, changes to our segment reporting, changes to operating profit methodology and changes to our consolidated cash flow statement. Our selected financial data as of and for the years ended December 31, 2005, 2004 and 2003 presented below also reflect these revisions, with the exception of total revenues and operating profit for the year ended December 31, 2003. Total revenues and operating profit for the year ended December 31, 2003 are presented in accordance with our pre-2006 segment reporting structure and operating profit methodology, and accordingly do not reflect the retrospective application of our revised segment reporting structure and operating profit methodology, due to the unreasonable effort or expense required to prepare such information, in particular resulting from the implementation of our new Corporate segment.

3

Table of Contents

| As of or For the Years ended December 31, | 2007 | 2007 | Change from previous year | 2006 | 2005 | 2004 | 2003 | |||||||||||||||||

| $(1) | € | % | € | € | € | € | ||||||||||||||||||

| (in millions, except per share data) | ||||||||||||||||||||||||

Income Statement | ||||||||||||||||||||||||

Total revenues(2) | ||||||||||||||||||||||||

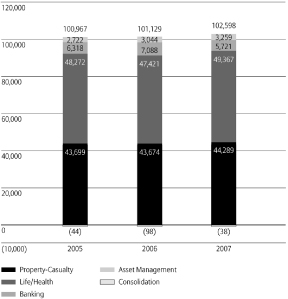

Property-Casualty | € | mn | 68,068 | 44,289 | 1.4 | 43,674 | 43,699 | 42,942 | 43,420 | (3) | ||||||||||||||

Life/Health | € | mn | 75,872 | 49,367 | 4.1 | 47,421 | 48,272 | 45,233 | 42,319 | (3) | ||||||||||||||

Banking | € | mn | 8,793 | 5,721 | (19.3 | ) | 7,088 | 6,318 | 6,576 | 6,704 | (3) | |||||||||||||

Asset Management | € | mn | 5,009 | 3,259 | 7.1 | 3,044 | 2,722 | 2,245 | 2,226 | (3) | ||||||||||||||

Consolidation | € | mn | (58 | ) | (38 | ) | not meaningful |

| (98 | ) | (44 | ) | (47 | ) | (929 | )(3) | ||||||||

Total Group | € | mn | 157,683 | 102,598 | 1.5 | 101,129 | 100,967 | 96,949 | 93,740 | (3) | ||||||||||||||

Operating profit(4) | ||||||||||||||||||||||||

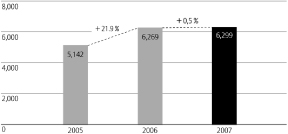

Property-Casualty | € | mn | 9,681 | 6,299 | 0.5 | 6,269 | 5,142 | 4,825 | 2,397 | (3) | ||||||||||||||

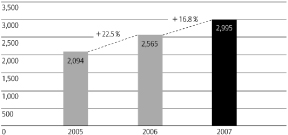

Life/Health | € | mn | 4,603 | 2,995 | 16.8 | 2,565 | 2,094 | 1,788 | 1,265 | (3) | ||||||||||||||

Banking | € | mn | 1,188 | 773 | (45.6 | ) | 1,422 | 704 | 447 | (396 | )(3) | |||||||||||||

Asset Management | € | mn | 2,089 | 1,359 | 5.3 | 1,290 | 1,132 | 839 | 716 | (3) | ||||||||||||||

Corporate | € | mn | (499 | ) | (325 | ) | not meaningful | | (831 | ) | (881 | ) | (870 | ) | — | (3) | ||||||||

Income (loss) before income taxes and minority interests in earnings | € | mn | 17,779 | 11,568 | 12.1 | 10,323 | 7,829 | 5,044 | 3,812 | |||||||||||||||

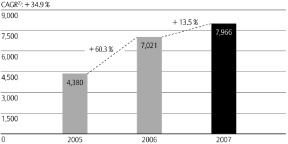

Net income (loss)(5) | € | mn | 12,243 | 7,966 | 13.5 | 7,021 | 4,380 | 2,266 | 2,691 | |||||||||||||||

Balance Sheet | ||||||||||||||||||||||||

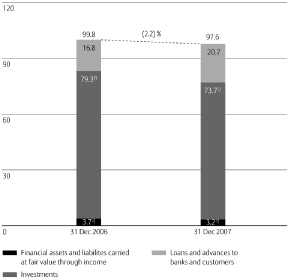

Investments | € | mn | 441,017 | 286,952 | (3.8 | ) | 298,134 | 285,015 | 254,085 | 237,682 | ||||||||||||||

Loans and advances to banks and customers(6) | € | mn | 609,691 | 396,702 | (6.4 | ) | 423,765 | 359,610 | 406,218 | 382,590 | ||||||||||||||

Total assets(6) | € | mn | 1,630,880 | 1,061,149 | (4.4 | ) | 1,110,081 | 1,054,656 | 1,058,612 | 971,076 | ||||||||||||||

Liabilities to banks and customers(6) | € | mn | 517,158 | 336,494 | (10.6 | ) | 376,565 | 333,118 | 377,480 | 337,201 | ||||||||||||||

Reserves for loss and loss adjustment expenses | € | mn | 97,910 | 63,706 | (2.7 | ) | 65,464 | 67,005 | 62,331 | 62,782 | ||||||||||||||

Reserves for insurance and investment contracts(6) | € | mn | 449,150 | 292,244 | 1.8 | 287,032 | 277,647 | 251,497 | 233,896 | |||||||||||||||

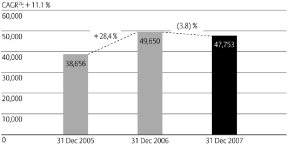

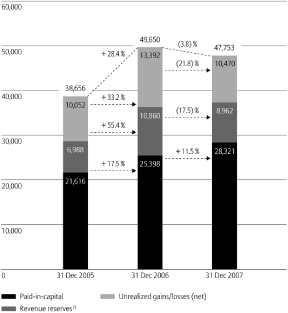

Shareholders’ equity(6) | € | mn | 73,392 | 47,753 | (3.8 | ) | 49,650 | 38,656 | 29,995 | 27,993 | ||||||||||||||

Minority interests(6) | € | mn | 5,576 | 3,628 | (49.5 | ) | 7,180 | 8,386 | 7,696 | 7,266 | ||||||||||||||

Returns | ||||||||||||||||||||||||

Return on equity after income taxes(6)(7) | % | 16.4 | 16.4 | 0.5pts | 15.9 | 12.9 | 7.8 | 11.0 | ||||||||||||||||

Return on equity after income taxes and before goodwill amortization(6)(7) | % | 16.4 | 16.4 | 0.5pts | 15.9 | 12.9 | 11.6 | 16.5 | ||||||||||||||||

Share Information | ||||||||||||||||||||||||

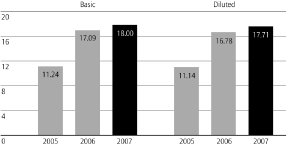

Basic earnings per share | € | 27.66 | 18.00 | 5.3 | 17.09 | 11.24 | 6.19 | 7.96 | ||||||||||||||||

Diluted earnings per share | € | 27.22 | 17.71 | 5.5 | 16.78 | 11.14 | 6.16 | 7.93 | ||||||||||||||||

Weighted average number of shares outstanding | ||||||||||||||||||||||||

Basic | mn | 442.5 | 442.5 | 7.7 | 410.9 | 389.8 | 365.9 | 338.2 | ||||||||||||||||

Diluted | mn | 449.6 | 449.6 | 7.5 | 418.3 | 393.3 | 368.1 | 339.8 | ||||||||||||||||

Shareholders’ equity per share(6) | € | 166 | 108 | (10.7 | ) | 121 | 99 | 82 | 83 | |||||||||||||||

Dividend per share | € | 8.45 | 5.50 | 44.7 | 3.80 | 2.00 | 1.75 | 1.50 | ||||||||||||||||

Dividend payment | € | mn | 3,805 | 2,476 | 50.8 | 1,642 | 811 | 674 | 551 | |||||||||||||||

Share price as of December 31(8) | € | 227.38 | 147.95 | (4.4 | ) | 154.76 | 127.94 | 97.60 | 100.08 | |||||||||||||||

Market capitalization as of December 31 | € | mn | 102,358 | 66,600 | (0.4 | ) | 66,880 | 51,949 | 35,936 | (9) | 36,743 | (9) | ||||||||||||

Other data | ||||||||||||||||||||||||

Employees | 181,207 | 181,207 | 8.8 | 166,505 | 177,625 | 176,501 | 173,750 | |||||||||||||||||

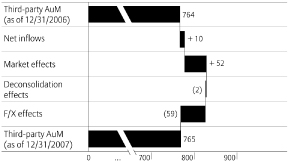

Third-party assets under management as of December 31 | € | mn | 1,175,146 | 764,621 | 0.1 | 763,855 | 742,937 | 584,624 | 564,714 | |||||||||||||||

(1) | Amounts given in Euros have been translated for convenience only into U.S. Dollars at the rate of $1.5369 = €1.00, the noon buying rate in New York for cable transfers in Euros certified by the Federal Reserve Bank of New York for customs purposes on March 10, 2008. |

(2) | Total revenues comprise Property-Casualty segment’s gross premiums written, Life/Health segment’s statutory premiums, Banking segment’s operating revenues and Asset Management segment’s operating revenues. Please refer to “Operating and Financial Review and Prospects—Introduction” for a reconciliation of total revenues to premiums written for the Allianz Group. |

(3) | Total revenues and operating profit for the year ended December 31, 2003 do not reflect the reporting changes effective January 1, 2006. |

(4) | The Allianz Group uses operating profit to evaluate the performance of its business segments. For further information on operating profit, as well as the particular reconciling items between operating profit and net income, see Note 5 to our consolidated financial statements. |

(5) | Effective January 1, 2005, under IFRS, and on a prospective basis, goodwill is no longer amortized. |

(6) | The Allianz Group identified prior period errors through an analysis of various balance sheet accounts (the “Errors”). The Errors resulted primarily from the accounting for the purchase of Dresdner Bank in 2001 and 2002, consolidation of special funds in 2001 and other errors related to minority interest and policyholder participation occurred in combination with mergers. The Errors had the effect of reducing net income by €78 mn in 2006, €42 mn in 2005, and €157 mn for the 4 years from 2001 through 2004. As the majority of the Errors related to the years 2001 through 2004, the Errors from these periods have been accounted for in 2007 by adjusting the opening balance sheet as of January 1, 2005. The Errors for 2005 and 2006 have been corrected through an out-of-period adjustment to net income in 2007. Certain financial instruments that were previously presented on a net presentation are now presented on a gross basis, due to contractual limitations to the right of offset. Partially offsetting these reclassifications from net to gross presentation is a change in the presentation of Collateral paid for securities borrowing transactions and Collateral received for securities lending transactions from gross to net presentation. The net effect is an increase in total assets and total liabilities of €57,610 mn, €66,123 mn, €67,654 mn and €37,274 mn in 2006, 2005, 2004 and 2003, respectively. For further information, see Note 3 to the consolidated financial statements. |

(7) | Based on average shareholders’ equity. Average shareholders’ equity has been calculated based upon the average of the current and preceding year’s shareholders’ equity. |

(8) | Source: Thomson Financial Datastream. |

(9) | Excluding treasury shares. |

4

Table of Contents

The following table sets forth the annual dividends declared in 2007 and paid in prior years per ordinary share and American Depositary Share (or “ADS”) equivalent for 2003 through 2007. The table does not reflect the related tax credits available to German taxpayers. See “Additional Information—German Taxation—Taxation of Dividends.”

| Dividend per ordinary share | Dividend paid per ADS equivalent | |||||||

| € | $ | € | $ | |||||

2003 | 1.50 | 1.82 | 0.150 | 0.182 | ||||

2004 | 1.75 | 2.27 | 0.175 | 0.227 | ||||

2005 | 2.00 | 2.43 | 0.200 | 0.243 | ||||

2006 | 3.80 | 5.13 | 0.380 | 0.513 | ||||

2007(1) | 5.50 | 8.45 | 0.550 | 0.845 | ||||

(1) | Dividend amounts given in Euros have been translated for convenience only into U.S. Dollars at the rate of $1.5369 = €1.00, the noon buying rate in New York for cable transfers in Euros certified by the Federal Reserve Bank of New York for customs purposes on March 10, 2008. See “Presentation of Financial and Other Information.” |

The ability to pay future dividends will depend upon our future earnings, financial condition (including our cash needs), prospects and other factors. You should not assume that any dividends will actually be paid or make any assumptions about the amount of dividends which will be paid in any given year. See “Financial Information—Dividend Policy.”

The table below sets forth, for the periods indicated, information concerning the noon buying rates for the Euro expressed in U.S. Dollars per €1.00. No representation is made that the Euro or U.S. Dollar amounts referred to herein could be or could have been converted into U.S. Dollars or Euros, as the case may be, at any particular rate or at all.

| High | Low | Period average(1) | Period end | |||||

| ($ per €1.00) | ||||||||

2003 | 1.2597 | 1.0361 | 1.1321 | 1.2597 | ||||

2004 | 1.3625 | 1.1801 | 1.2478 | 1.3538 | ||||

2005 | 1.3476 | 1.1667 | 1.2400 | 1.1842 | ||||

2006 | 1.3327 | 1.1860 | 1.2481 | 1.3197 | ||||

2007 | 1.4862 | 1.2904 | 1.3797 | 1.4603 | ||||

September | 1.4219 | 1.3606 | 1.3913 | 1.4219 | ||||

October | 1.4468 | 1.4092 | 1.4349 | 1.4468 | ||||

November | 1.4862 | 1.4435 | 1.4562 | 1.4688 | ||||

December | 1.4759 | 1.4344 | 1.4630 | 1.4603 | ||||

2008 | ||||||||

January | 1.4877 | 1.4574 | 1.4790 | 1.4841 | ||||

February | 1.5187 | 1.4495 | 1.5019 | 1.5187 | ||||

March (until March 10, 2008) | 1.5369 | 1.5195 | 1.5282 | 1.5369 | ||||

(1) | Computed using the average of the noon buying rates for Euros on the last business day of each month during the relevant annual period or on the first and last business days of each month during the relevant monthly period. |

On March 10, 2008, the noon buying rate for the Euro was $1.5369.

5

Table of Contents

You should carefully review the following risk factors together with the other information contained in this annual report before making an investment decision. Our financial position and results of operations may be materially adversely affected by each of these risks. The market price of our ADSs may decline as a result of each of these risks and investors may lose the value of their investment in whole or in part. Additional risks not currently known to us or that we now deem immaterial may also adversely affect our business and your investment.

Interest rate volatility may adversely affect Allianz Group’s results of operations.

Changes in prevailing interest rates (including changes in the difference between the levels of prevailing short-and long-term rates) can affect Allianz Group’s insurance, asset management, banking and corporate results.

Over the past several years, movements in both short- and long-term interest rates have affected the level and timing of recognition of gains and losses on securities held in Allianz Group’s various investment portfolios. An increase in interest rates could substantially decrease the value of Allianz Group’s fixed income portfolio, and any unexpected change in interest rates could materially adversely affect Allianz Group’s bond and interest rate derivative positions. Results of Allianz Group’s asset management business may also be affected by movements in interest rates, as management fees are generally based on the value of assets under management, which fluctuate with changes in the level of interest rates.

The short-term impact of interest rate fluctuations on Allianz Group’s life/health insurance business may be reduced in part by products designed to partly or entirely transfer Allianz Group’s exposure to interest rate movements to the policyholder. While product design reduces Allianz Group’s exposure to interest rate volatility, changes in interest rates will impact this business to the extent they result in changes to current interest income, impact the value of Allianz Group’s fixed income portfolio, and affect the levels of new product sales or surrenders of business in force. In addition,

reductions in the investment income below the rates prevailing at the issue date of the policy, or below the regulatory minimum required rates in countries such as Germany and Switzerland, would reduce or eliminate the profit margins on the life/health insurance business written by Allianz Group’s life/health subsidiaries to the extent the maturity composition of the assets does not match the maturity composition of the insurance obligations they are backing.

In addition, the composition of Allianz Group’s banking assets and liabilities, and any mismatches resulting from that composition, cause the net income of Allianz Group’s banking operations to vary with changes in interest rates. Allianz Group is particularly impacted by changes in interest rates as they relate to different maturities of contracts and the different currencies in which Allianz Group holds interest rate positions. A mismatch with respect to maturity of interest-earning assets and interest-bearing liabilities in any given period can have a material adverse effect on the financial position or results of operations of Allianz Group’s banking business.

Market risks could impair the value of Allianz Group’s portfolio and adversely impact Allianz Group’s financial position and results of operations.

Allianz Group holds a significant equity portfolio, which represented approximately 15% of Allianz Group’s financial assets at December 31, 2007, excluding financial assets and liabilities carried at fair value through income. Fluctuations in equity markets affect the market value and liquidity of these holdings. Allianz Group also has real estate holdings in its investment portfolio, the value of which is likewise exposed to changes in real estate market prices and volatility.

Most of Allianz Group’s assets and liabilities are recorded at fair value, including trading assets and liabilities, financial assets and liabilities designated at fair value through income, and securities available-for-sale. Changes in the value of securities held for trading purposes and financial assets designated at fair value through income are recorded through Allianz Group’s consolidated

6

Table of Contents

income statement. Changes in the market value of securities available-for-sale are recorded directly in Allianz Group’s consolidated shareholders’ equity. Available-for-sale equity and fixed income securities, as well as securities classified as held-to-maturity, are reviewed regularly for impairment, with write-downs to fair value charged to income if there is objective evidence that the cost may not be recovered. See “Operating and Financial Review—Critical Accounting Policies and Estimates” and Note 2 to the consolidated financial statements for further information concerning Allianz Group’s significant accounting and valuation policies.

Allianz Group’s financial condition may be affected by adverse developments in the financial markets

The ability of Allianz Group to meet its financing needs depends on the availability of funds in the international capital markets. The financing of Allianz Group’s activity includes funding through commercial papers and medium term notes. A sustained break-down of such markets could have a materially adverse impact on the cost of funding as well as on the refinancing structure of Allianz Group. Furthermore, the illiquidity or sustained volatility of certain market segments may affect the mark-to-market valuation of certain assets and may lead to valuation losses and an increased risk of counterparty defaults.

Market and other factors could adversely affect goodwill, deferred policy acquisition costs and deferred tax assets; Allianz Group’s deferred tax assets are also potentially impacted by changes in tax legislation.

Business and market conditions may impact the amount of goodwill Allianz Group carries in its consolidated financial statements. As of December 31, 2007, Allianz Group has recorded goodwill in an aggregate amount of €12,453 million, of which €6,165 million relates to its asset management business, €4,433 million relates to its insurance business, €1,714 million relates to its banking business, and €141 million relates to its corporate segment.

As the value of certain parts of Allianz Group’s businesses, including in particular Allianz Group’s

banking and asset management businesses, are significantly impacted by such factors as the state of financial markets and ongoing operating performance, significant declines in financial markets or operating performance could also result in impairment of other goodwill carried by us and result in significant write-downs, which could be material. No impairments were recorded for goodwill in 2007.

The assumptions Allianz Group made with respect to recoverability of deferred policy acquisition costs (“DAC”) are also affected by such factors as operating performance and market conditions. DAC is incurred in connection with the production of new and renewal insurance business and is deferred and amortized generally in proportion to profits or to premium income expected to be generated over the life of the underlying policies, depending on the classification of the product. If the assumptions on which expected profits are based prove to be incorrect, it may be necessary to accelerate amortization of DAC, even to the extent of writing down DAC through impairments, which could materially adversely affect results of operations. No impairments were recorded for DAC in 2007.

As of December 31, 2007, Allianz Group had a total of €4,771 million in net deferred tax assets and €3,973 million in net deferred tax liabilities. The calculation of the respective tax assets and liabilities is based on current tax laws and IFRS and depends on the performance of the Allianz Group as a whole and certain business units in particular. At December 31, 2007, €3,227 million of deferred tax assets depended on the ability to use existing tax-loss carry forwards.

Changes in German or other tax legislation or regulations or an operating performance below currently anticipated levels may lead to a significant impairment of deferred tax assets, in which case Allianz Group could be obligated to write-off certain tax assets. Tax assets may also need to be written- down if certain assumptions of profitability prove to be incorrect, as losses incurred for longer than expected will make the usability of tax assets more unlikely. Any such development may have a material adverse impact on Allianz Group’s results of operations.

7

Table of Contents

Loss reserves for Allianz Group’s property-casualty insurance and reinsurance policies are based on estimates as to future claims payments. Adverse developments relating to claims could lead to further reserve additions and materially adversely impact Allianz Group’s results of operations.

In accordance with industry practice and accounting and regulatory requirements, Allianz Group established reserves for losses and loss adjustment expenses related to its property-casualty insurance and reinsurance businesses, including property-casualty business in run-off. Reserves are based on estimates of future payments that will be made in respect of claims, including expenses relating to such claims. Such estimates are made both on a case-by-case basis, based on the facts and circumstances available at the time the reserves are established, as well as in respect of losses that have been incurred but not reported (“IBNR”) to the Allianz Group. These reserves represent the estimated ultimate cost necessary to bring all pending reported and IBNR claims to final settlement.

Reserves, including IBNR reserves, are subject to change due to a number of variables that affect the ultimate cost of claims, such as changes in the legal environment, results of litigation, changes in medical costs, costs of repairs and other factors such as inflation and exchange rates, and Allianz Group’s reserves for asbestos and environmental and other latent claims are particularly subject to such variables. Allianz Group’s results of operations depend significantly upon the extent to which Allianz Group’s actual claims experience is consistent with the assumptions Allianz Group uses in setting the prices for products and establishing the liabilities for obligations for technical provisions and claims. To the extent that Allianz Group’s actual claims experience is less favorable than the underlying assumptions used in establishing such liabilities, Allianz Group may be required to increase its reserves, which may materially adversely affect its results of operations.

Established loss reserves estimates are periodically adjusted in the ordinary course of settlement, using the most current information available to management, and any adjustments resulting from changes in reserve estimates are reflected in current results of operations. Allianz Group also conducts reviews of various lines of business to consider the adequacy of reserve levels.

Based on current information available to us and on the basis of Allianz Group’s internal procedures, Allianz Group’s management considers that Allianz Group’s reserves are adequate at December 31, 2007. However, because the establishment of reserves for loss and loss adjustment expenses is an inherently uncertain process, there can be no assurance that ultimate losses will not materially exceed the established reserves for loss and loss adjustment expenses and have a material adverse effect on Allianz Group’s results of operations.

Actuarial experience and other factors could differ from that assumed in the calculation of life/health actuarial reserves and pension liabilities.

The assumptions Allianz Group makes in assessing its life/health insurance reserves may differ from what we experience in the future. Allianz Group derive its life/health insurance reserves using “best estimate” actuarial practices and assumptions. These assumptions include the assessment of the long-term development of interest rates, investment returns, the allocation of investments between equity, fixed income and other categories, policyholder bonus rates (some of which are guaranteed), mortality and morbidity rates, policyholder lapses and future expense levels. Allianz Group monitors its actual experience of these assumptions and to the extent that it considers that this experience will continue in the longer term it refines its long-term assumptions. Similarly, estimates of Allianz Group’s own pension obligations necessarily depend on assumptions concerning future actuarial, demographic, macroeconomic and financial markets developments. Changes in any such assumptions may lead to changes in the estimates of life/health insurance reserves or pension obligations.

We have a significant portfolio of contracts with guaranteed investment returns, including endowment and annuity products for the German market as well as certain guaranteed contracts in other markets. The amounts payable by us at maturity of an endowment policy in Germany and in certain other markets include a “guaranteed benefit,” an amount that, in practice, is equal to a legally mandated maximum rate of return on actuarial reserves. If interest rates decline to historically low levels for a long period, we could be required to provide additional funds to Allianz Group’s life/health subsidiaries to support their obligations in respect of products with higher guaranteed returns, or increase reserves in respect of

8

Table of Contents

such products, which could in turn have a material adverse effect on Allianz Group’s results of operations.

In the United States, and to a lesser extent in Europe and Asia we have a portfolio of contracts with guaranteed investment returns indexed to equity markets. We enter into derivative contracts as a means of mitigating the risk of investment returns underperforming guaranteed returns. However, there can be no assurance that the hedging arrangements will satisfy the returns guaranteed to policyholders, which could in turn have a material adverse effect on Allianz Group’s results of operations.

Allianz Group’s financial results may be materially adversely affected by the occurrence of catastrophes.

Portions of Allianz Group’s property-casualty insurance may cover losses from unpredictable events such as hurricanes, windstorms, hailstorms, earthquakes, fires, industrial explosions, freezes, riots, floods and other man-made or natural disasters, including acts of terrorism. The incidence and severity of these catastrophes in any given period are inherently unpredictable.

Although the Allianz Group monitors its overall exposure to catastrophes and other unpredictable events in each geographic region, each of Allianz Group’s subsidiaries independently determines, within the Allianz Group’s limit framework, its own underwriting limits related to insurance coverage for losses from catastrophic events. We generally seek to reduce Allianz Group’s potential losses from these events through the purchase of reinsurance, selective underwriting practices and by monitoring risk accumulation. However, such efforts to reduce exposure may not be successful and claims relating to catastrophes may result in unusually high levels of losses and could have a material adverse effect on Allianz Group’s financial position or results of operations.

We have significant counterparty risk exposure.

We are subject to a variety of counterparty risks, including:

General Credit Risks. Third-parties that owe us money, securities or other assets may not pay or perform under their obligations. These parties include

the issuers whose securities we hold, borrowers under loans made, customers, trading counterparties, counterparties under swaps, credit default and other derivative contracts, clearing agents, exchanges, clearing houses and other financial intermediaries. These parties may default on their obligations to us due to bankruptcy, lack of liquidity, downturns in the economy or real estate values, operational failure or other reasons.

Reinsurers. We transfer our exposure to certain risks in our property-casualty and life/health insurance business to others through reinsurance arrangements. Under these arrangements, other insurers assume a portion of Allianz Group’s losses and expenses associated with reported and unreported losses in exchange for a portion of policy premiums. The availability, amount and cost of reinsurance depend on general market conditions and may vary significantly. Any decrease in the amount of Allianz Group’s reinsurance will increase its risk of loss. When we obtain reinsurance, we are still liable for those transferred risks if the reinsurer cannot meet its obligations. Therefore, the inability of Allianz Group’s reinsurers to meet their financial obligations could materially affect Allianz Group’s results of operations. Although Allianz Group conducts periodic reviews of the financial statements and reputations of its reinsurers, including, and as appropriate, requiring letters of credit, deposits or other financial measures to further minimize its exposure to credit risk, reinsurers may become financially unsound by the time they are called upon to pay amounts due.

Many of our businesses are dependent on the financial strength and credit ratings assigned to us and our businesses by various rating agencies. Therefore, a downgrade in our ratings may materially adversely affect relationships with customers and intermediaries, negatively impact sales of our products and increase our cost of borrowing.

Claims paying ability and financial strength ratings are each a factor in establishing the competitive position of insurers. Our financial strength rating has a significant impact on the individual ratings of key subsidiaries. If a rating of certain subsidiaries falls below a certain threshold, the respective operating business may be significantly impacted. A ratings downgrade, or the potential for such a downgrade, of the Allianz Group

9

Table of Contents

or any of our insurance subsidiaries could, among other things, adversely affect relationships with agents, brokers and other distributors of our products and services, thereby negatively impacting new sales, adversely affect our ability to compete in our markets and increase our cost of borrowing. In particular, in those countries where primary distribution of our products is done through independent agents, such as the United States, future ratings downgrades could adversely impact sales of our life insurance and annuity products. Any future ratings downgrades could also materially adversely affect our cost of raising capital, and could, in addition, give rise to additional financial obligations or accelerate existing financial obligations which are dependent on maintaining specified rating levels.

Rating agencies can be expected to continue to monitor our financial strength and claims paying ability, and no assurances can be given that future ratings downgrades will not occur, whether due to changes in our performance, changes in rating agencies’ industry views or ratings methodologies, or a combination of such factors.

If our asset management business underperforms, it may experience a decline in assets under management and related fee income.

While the assets under management in our asset management segment include a significant amount of funds related to our insurance operations, third-party assets under management, represent the majority. Results of our asset management activities are affected by share prices, share valuation, interest rates and market volatility. In addition, third-party funds are subject to withdrawal in the event our investment performance is not competitive with other asset management firms. Accordingly, fee income from the asset management business might decline if the level of our third-party assets under management were to decline due to investment performance or otherwise.

Increased geopolitical risks following the terrorist attack of September 11, 2001, and any future terrorist attacks, could have a continuing negative impact on our businesses.

After September 11, 2001, reinsurers generally either put terrorism exclusions into their policies or drastically increased the price for such coverage.

Although we have attempted to exclude terrorist coverage from policies we write, this has not been possible in all cases, including as a result of legislative developments such as the Terrorism Risk Insurance Act in the United States. Furthermore, even if terrorism exclusions are permitted in our primary insurance policies, we may still have liability for fires and other consequential damage claims that follow an act of terrorism itself. As a result we may have liability under primary insurance policies for acts of terrorism and may not be able to recover a portion or any of our losses from our reinsurers.

At this time, we cannot assess the future effects of terrorist attacks, potential ensuing military and other responsive actions, and the possibility of further terrorist attacks, on our businesses. Such matters have significantly adversely affected general economic, market and political conditions, increasing many of the risks in our businesses noted in the previous risk factors. This may have a material negative effect on our businesses and results of operations over time.

Changes in existing, or new, government laws and regulations, or enforcement initiatives in respect thereof, in the countries in which we operate may materially impact us and could adversely affect our business.

Our insurance, banking and asset management businesses are subject to detailed, comprehensive laws and regulation as well as supervision in all the countries in which we do business. Changes in existing laws and regulations may affect the way in which we conduct our business and the products we may offer. Changes in regulations relating to pensions and employment, social security, financial services including reinsurance business, taxation, securities products and transactions may materially adversely affect our insurance, banking and asset management businesses by restructuring our activities, imposing increased costs or otherwise.

Regulatory agencies have broad administrative power over many aspects of the financial services business, which may include liquidity, capital adequacy and permitted investments, ethical issues, money laundering, “know your customer” rules, privacy, record keeping, and marketing and selling practices. Banking, insurance and other financial services laws, regulations and policies currently

10

Table of Contents

governing us and our subsidiaries may change at any time in ways which have an adverse effect on our business, and we cannot predict the timing or form of any future regulatory or enforcement initiatives in respect thereof. Also, bank regulators and other supervisory authorities in the EU, the United States and elsewhere continue to scrutinize payment processing and other transactions under regulations governing such matters as money-laundering, prohibited transactions with countries subject to sanctions, and bribery or other anti-corruption measures. If we fail to address, or appear to fail to address, appropriately any of these changes or initiatives, our reputation could be harmed and we could be subject to additional legal risk, including enforcement actions, fines and penalties. Despite our best efforts to comply with applicable regulations, there are a number of risks in areas where applicable regulations may be unclear or where regulators revise their previous guidance or courts overturn previous rulings. Regulators and other authorities have the power to bring administrative or judicial proceedings against us, which could result, among other things, in significant adverse publicity and reputational harm, suspension or revocation of our licenses, cease-and- desist orders, fines, civil penalties, criminal penalties or other disciplinary action that could materially harm our results of operations and financial condition.

Effective January 2005, reinsurance companies in Germany such as Allianz SE are subject to specific legal requirements regarding the assets covering their technical reserves. These assets are required to be appropriately diversified to prevent a reinsurer from relying excessively on any particular asset. The introduction of these requirements anticipated the implementation of EU Reinsurance Directive (2005/68/EC) which was adopted in November 2005. All of the directive’s provisions were implemented in Germany effective June 2, 2007. Although Allianz SE expects to continue to meet the new requirements, there can be no assurances as to the impact on Allianz SE of any future amendments to or changes in the interpretation of the laws and regulations regarding assets covering technical reserves of reinsurance companies, which could require Allianz SE to change the composition of its asset portfolio covering its technical reserves or take other appropriate measures.

In addition, discussions on a new solvency regime for insurance companies in the EU (Solvency II) are ongoing. As those discussions are not yet finalized, its potential future impact for capital requirements can not currently be assessed. For more information, see “Item 11. Quantitative and Qualitative Disclosures about Market Risk – Outlook”.

In addition, changes to tax laws may affect the attractiveness of certain of our products that currently receive favorable tax treatment. Governments in jurisdictions in which we do business may consider changes to tax laws that could adversely affect such existing tax advantages, and if enacted, could result in a significant reduction in the sale of such products.

Our business may be negatively affected by adverse publicity, regulatory actions or litigation with respect to the Allianz Group, other well-known companies and the financial services industry generally.

Adverse publicity and damage to our reputation arising from failure or perceived failure to comply with legal and regulatory requirements, financial reporting irregularities involving other large and well-known companies, increasing regulatory and law enforcement scrutiny of “know your customer”, anti-money laundering and anti-terrorist-financing procedures and their effectiveness, regulatory investigations of the mutual fund, banking and insurance industries, and litigation that arises from the failure or perceived failure by the Allianz Group companies to comply with legal, regulatory and compliance requirements, could result in adverse publicity and reputational harm, lead to increased regulatory supervision, affect our ability to attract and retain customers, maintain access to the capital markets, result in law suits, enforcement actions, fines and penalties or have other adverse effects on us in ways that are not predictable.

Changes in value relative to the Euro of non-Euro zone currencies in which we generate revenues and incur expenses could adversely affect our reported earnings and cash flow.

We prepare our consolidated financial statements in Euro. However, a significant portion of the revenues and expenses from our subsidiaries outside the Euro zone, including in the United States, Switzerland and the United Kingdom, originates in currencies other than the Euro. We expect this trend

11

Table of Contents

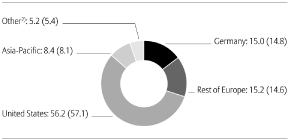

to continue as we expand our business into growing non-Euro zone markets. For the year ended December 31, 2007, approximately 34.2% of our gross premiums written in our property-casualty segment and 27.9% of our statutory premiums in our life/health segment originated in currencies other than the Euro. Furthermore, as of December 31, 2007, 56.1% of the third-party assets under management at the Asset Management segment are in the United States, and 44.2% of the assets in our Banking Operations are located outside of Germany.

As a result, although our non-Euro zone subsidiaries generally record their revenues and expenses in the same currency, changes in the exchange rates used to translate foreign currencies into Euro may adversely affect our results of operations.

While our non-Euro assets and liabilities, and revenues and related expenses, are generally denominated in the same currencies, we do not generally engage in hedging transactions with respect to dividends or cash flows in respect of our non-Euro subsidiaries.

The share price of Allianz SE has been and may continue to be volatile.

The share price of Allianz SE has been volatile in the past and may continue to be volatile due in part to the high volatility in the securities markets generally, and in financial institutions’ shares in particular, as well as developments which impact our financial results. Factors other than our financial results that may affect our share price include but are not limited to: market expectations of the performance and capital adequacy of financial institutions generally; investor perception of as well as the actual performance of other financial institutions; investor perception of the success and impact of our strategy, including the acquisition of Assurances Générales de France S.A. (or “AGF”, and together with its subsidiaries, the “AGF Group”), a downgrade or rumored downgrade of our credit ratings; potential litigation or regulatory action involving the Allianz Group or any of the industries we have exposure to through our insurance, banking and asset management activities; announcements concerning the bankruptcy or other similar reorganization proceedings involving, or any investigations into the accounting practices of, other

insurance or reinsurance companies, banks or asset management companies; and general market volatility.

The benefits that Allianz SE may realize from Allianz AG’s conversion into a European Company (Societas Europaea) and from the completed mergers with RAS S.p.A. and AGF could be materially different from our current expectations.

The benefits that Allianz SE may realize from Allianz AG’s conversion into a European Company (Societas Europaea, SE) and the subsequent reorganization of its European operations, including the acquisition of minority interests in the Italian subsidiary, RAS S.p.A. and its French subsidiary AGF could be materially different from our current expectations. For more information about these transactions and reorganization, see “Information on the Company—Legal Structure—AGF minorities buy-out procedure completed” and “Information on the Company—Important Group Organizational Changes—Reorganization in Italy.” We took these measures to implement a business plan creating strategic synergies and organizational efficiencies, however, our estimates of the benefits that we may realize as a result of these measures involve subjective judgments that are subject to uncertainties. A variety of factors that are partially or entirely beyond our control could cause actual results to be materially different from what we currently expect, and any synergies that we realize from a conversion to an SE and full ownership of these subsidiaries could be materially different from our current expectations.

The Allianz Group has been and may continue to be adversely affected by ongoing turbulence and volatility in the world’s financial markets.

Starting in the second half of 2007, the crisis in the mortgage market in the United States, triggered by a serious deterioration of credit quality, led to a revaluation of credit risks. These conditions have resulted in greater volatility, less liquidity, widening of credit spreads and overall tightening of financial markets throughout the world. In addition, the prices for many types of asset-backed securities (ABS) and other structured products have deteriorated. Although most of Allianz’s insurance operations have not been significantly affected by this crisis, Allianz has been materially impacted as a result of our investment banking operations’ exposures to U.S. mortgage-

12

Table of Contents

related structured investment products, including subprime, midprime and prime residential mortgage-backed securities (RMBS), collateralized debt obligations (CDOs), monoline insurer guarantees, structured investment vehicles (SIVs) and other investments. As a result, in late 2007, we recorded significant negative revaluations on the investment portfolio of our subsidiary, Dresdner Bank. For details regarding the impact of the financial market crisis on the Allianz Group’s 2007 results, please see “Operating and Financial Review and Prospects—Executive Summary—Impact of the financial markets turbulence.”

The valuation of ABS and other affected instruments is a complex process, involving the

consideration of market transactions, pricing models, management judgment and other factors, and is also impacted by external factors such as underlying mortgage default rates, interest rates, rating agency actions and property valuations. While we continue to monitor our exposures in this area, in light of the ongoing market environment and the resulting uncertainties concerning valuations, it is difficult to predict how long these volatile conditions will exist and how the Allianz Group’s markets, business and operations will be affected. Continuation or worsening of the turbulence in the world’s financial markets could have a material adverse effect on the Allianz Group’s financial position, shareholders’ equity and results of operations in future periods.

13

Table of Contents

ITEM 4. Information on the Company

The Allianz Group

Founded in 1890 and with 117 years of experience in the financial services industry, the Allianz Group is committed to providing financial security to a broad base of customers ranging from private individuals to large multinational corporations.

Allianz SE (formerly Allianz Aktiengesellschaft, or Allianz AG) is a European Company (Societas Europaea, or SE) incorporated in the Federal Republic of Germany and organized under the laws of the Federal Republic of Germany and the European Union. Allianz SE is the ultimate parent of the Allianz Group. It was incorporated as Allianz Versicherungs- Aktiengesellschaft in Berlin, Germany on February 5, 1890 and converted to a European Company on October 13, 2006. Our registered office is located at Koeniginstrasse 28, 80802 Munich, Germany, telephone +49 (0) 89 3800-0.

The Allianz Group’s Business Model

As an integrated and globally operating financial services provider we seek to offer our clients considerable value by providing a wide range of insurance and financial products as well as an extensive advisory capacity through our subsidiaries under strong and well-known brands. We operate and manage our activities primarily through four operating segments: Property-Casualty, Life/Health, Banking and Asset Management. We consider ourselves well-positioned to anticipate and successfully respond to competitive forces affecting our various operations.

Property-Casualty & Life/Health insurance operations

We are one of the leading insurance groups in the world and rank number one in the German property-casualty and life insurance markets based on gross premiums written and statutory premiums, respectively.(1) We are also among the largest insurance companies in a number of the other countries in which we operate. Our product portfolio

(1) | Source: As published by Gesamtverband der deutschen Versicherungswirtschaft e.V. (or “GDV“) in 2007. The GDV is a private association representing the German insurance industry. |

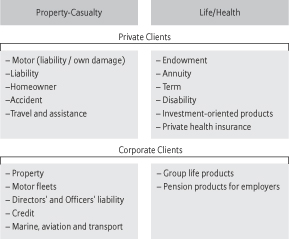

includes a wide array of property-casualty and life/health insurance products for both private and corporate customers.

Product portfolio of the insurance segments

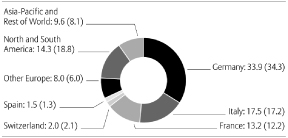

We conduct business in almost every European country, with Germany, Italy and France being our most important markets. We also run operations in the United States and in Central and Eastern Europe as well as in Asia-Pacific.(2)

We distribute our insurance products via a broad network of self-employed agents, brokers, banks and other channels. Increasingly, we distribute our insurance products in cooperation with car manufacturers and dealers in Europe and Asia-Pacific and also have direct distribution operations in Central Europe, India and Australia. The particular distribution channels vary by product and geographic market.

Our more mature insurance markets (e.g. Germany, France, Italy and the United States) are highly competitive. In recent years, we have also experienced increasing competition in emerging markets, as large insurance companies and other financial service providers from more developed countries have entered these markets to participate in their high growth potential. In addition, local institutions have become more experienced and have established strategic relationships, alliances or mergers with our competitors.

(2) | For a more detailed discription of our geographic diversification, please refer to “Global Diversification of our Insurance Business”. |

14

Table of Contents

The investments of most Allianz insurance companies’ are managed internally through specialists within the Allianz Group (Allianz Investment Management).

Allianz SE, the Allianz Group’s parent company, acts on an arm’s length basis as reinsurer for most of our insurance operations and assumed 26.9%, 33.3% and 35.6% of all reinsurance ceded by Allianz Group companies for the years ended December 31, 2007, 2006 and 2005, respectively. Allianz SE also assumes a relatively small amount of reinsurance from external cedents and cedes risk to third-party reinsurers. The Allianz Group has established a pooling arrangement that offers reinsurance coverage to the Group’s subsidiaries against natural catastrophes, which provides the benefit of internal Group diversification.

Banking operations

Our banking activities are primarily conducted through the Dresdner Bank Group (or “Dresdner Bank”), one of the leading commercial banks in Germany(1), accounting for 94.8% of our total Banking segment’s operating revenues in fiscal year 2007 (2006: 96.0%). While Dresdner Bank focuses on selected geographic regions worldwide, Germany is its primary market. Dresdner Bank is present in the world’s major financial centers and operates its banking business mainly through 1,074 (as of December 31, 2007) branch offices, of which 1,019 are located in Germany and 55 outside of Germany.

Dresdner Bank’s focus is on serving the financial needs of private and corporate, as well as multinational and institutional clients according to the following business model.

Business model of Dresdner Bank

(1) | Based on total assets as of December 31, 2007. |

The Private & Corporate Clients division offers integrated financial solutions for private and corporate clients. These solutions are provided by dedicated sales and product units.

The Investment Banking division, known as Dresdner Kleinwort, focuses on German and multinational groups, financial investors and institutions requiring access to the capital markets and to global banking services.

In addition to our bankassurance activities, the distribution of Dresdner Bank products through our German insurance agents network is of increasing importance. By offering both insurance and banking services in 120 (as of December 31, 2007) selected agencies, an innovative and successful distribution channel is evolving.

We are subject to competition from both bank and non-bank institutions that provide financial services and, in some of our activities, also from government agencies. Substantial competition exists among a large number of commercial banks, saving banks, other public sector banks, brokers and dealers, investment banking firms, insurance companies investment advisors, mutual funds and hedge funds that provide the types of banking products and services that our banking operations offer.

Asset Management operations

We are one of the five largest asset managers in the world.(2)

Our business activities in this segment consist of asset management products and services both for third-party investors and for the Allianz Group’s insurance operations.

We serve a comprehensive range of retail and institutional asset management clients. Our institutional customers include corporate and public pension funds, insurance and other financial services companies, governments and charities, and financial advisors.

(2) | Based on total assets under management as of December 31, 2007, own source. |

15

Table of Contents

AGI’s customer and selected product range

Our retail asset management business is primarily conducted under the brand name Allianz Global Investors (“AGI”) through our operating companies worldwide. In our institutional asset management business, we operate under the brand names of our investment management entities, with AGI serving as an endorsement brand. With €725 billion of third-party assets as of December 31, 2007, AGI managed 94.8% (2006: 94.6%) of our total third-party assets on a worldwide basis, which includes fixed income, equity, money market and sector products, as well as alternative investments.

The United States and Germany as well as France, Italy and the Asia-Pacific region represent our primary asset management markets.

Our distribution channels vary by product and geographic market. In Europe and in the United States, AGI markets and services its institutional products through specialized operations and personnel. Retail products in Europe are mostly distributed through proprietary Allianz Group channels. In the United States, AGI’s local asset management operating entities also offer a wide range of retail products. In addition we have committed substantial resources to the expansion of the third-party asset management business in the Asia-Pacific region.

In the asset management business, competition comes from all major international financial institutions and peer insurance companies that also offer asset management products and services, competing for retail and institutional clients.

Corporate segment

Our Corporate segment’s activities include the management and support of Allianz Group’s businesses through its strategy, risk, corporate finance, treasury, financial control, communication, legal, human resources and technology functions. The Corporate segment also includes the Group’s alternative investments coordinated by Allianz Alternative Assets Holding GmbH.

AGF minorities buy-out procedure completed

As of December 31, 2006 Allianz SE owned 57.5% of the share capital and 60.2% of the voting rights of its French-based subsidiary, Assurances Générales de France S.A. (“AGF”). In order to achieve full ownership of AGF, Allianz announced a tender offer for the outstanding AGF shares on January 18, 2007.

The acceptance period for the tender offer started on March 23, 2007 and ended on April 20, 2007. The consideration for one AGF share provided in the offer was 0.25 of an Allianz SE share and €87.50 in cash, which was increased to €88.45 to reflect the dividend per Allianz SE share for 2006 multiplied by 0.25, as Allianz SE shares issued due to the tender offer did not carry the rights to dividends for 2006.

On April 27, 2007 the French stock market authority, the Autorité des Marchés Financiers (“AMF”) announced, that following the closing of the tender offer for the outstanding shares of AGF, Allianz SE (directly and indirectly through its subsidiary Allianz Holding France SAS) held 178,030,698 AGF shares representing 92.18% of AGF’s share capital and voting rights. Taking into account the 6,199,392 treasury shares held by AGF representing 3.21% of the share capital, minority shareholders held 8,895,695 shares representing 4.61% of AGF, less than 5%, the threshold for a subsequent squeeze-out procedure of the AGF share capital and voting rights.

16

Table of Contents

In order to achieve 100% ownership of AGF, Allianz SE and its subsidiary Allianz Holding France SAS subsequently launched a mandatory squeeze-out procedure of the AGF shares still held by minority shareholders. In accordance with the General Regulations of the AMF, and subject to review and prior authorization by the AMF, the squeeze-out was implemented on the basis of a price of €125.00 in cash per AGF share. Additionally, AGF’s minority shareholders also received the 2006 AGF dividend of €4.25 per share.

On July 10, 2007, the Allianz Group completed the squeeze-out procedure for AGF and now holds 100% of the shares of AGF. As a result, the AGF shares are no longer listed on the Paris stock exchange Euronext.

Concurrent with the AGF transaction, and in order to provide the share component of the consideration to AGF shareholders, Allianz completed a capital increase involving the issuance of approximately 16.97 million new Allianz SE shares. The total cash component of the consideration for the acquisition of the outstanding AGF shares amounted to approximately €7.1 billion.

Acquisition in 2007

On February 21, 2007 Sistema and Allianz signed a share purchase agreement, whereby Allianz became a major shareholder of ROSNO Group, one of the four leading insurance companies in Russia. Allianz now holds approximately 97% in ROSNO, which is active in the Property-Casualty, Life/Health and Asset Management business. With this acquisition, we improved our strategic position in Central and Eastern Europe and expect to become by far the most important foreign majority owner of an insurance company in our strategic market Russia.

Squeeze-out of Allianz Lebensversicherungs-AG announced

On January 18, 2008 we announced the start of the squeeze-out process for the remaining shares in Allianz Lebensversicherungs-AG, having reached the required threshold of 95%.

Important Group Organizational Changes(1)

In order to realize the potential for operational and strategic synergies, we continued to pursue the

(1) | Please see Note 4 to our consolidated financial statements for information on changes in the scope of consolidation in the years ended December 31, 2007, 2006 and 2005. |

reorganization projects started in recent years and complemented these with additional new activities:

Reorganization of German Insurance Operations

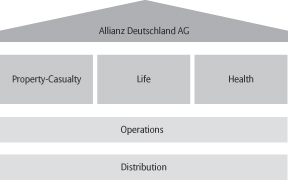

We continued the reorganization of our German insurance operations which was announced in 2005, by consolidating our major insurance subsidiaries under the Allianz SE wholly-owned holding company Allianz Deutschland AG and revising our regional sales and service structure. This process is part of our ongoing effort to simplify structures and reduce complexity within the Allianz Group, enabling us to react to changes in our markets with greater speed, focus and flexibility. Our goal is to create one joint presence of our insurance operations, with customers perceiving Allianz as one unit with comprehensive high quality services geared toward the customer’s needs. The reorganization is part of our strategy to further develop our leading position in the German insurance market.

At the beginning of 2007, we completed negotiations with the works councils, such negotiations being an important prerequisite for the implementation of the new operating model.

The German insurance operations are now organized according to the following business structure.

Business model of Allianz Deutschland AG

We are continuing this reorganization program and expect the reduced complexity to allow us to reduce costs in the long-term.

17

Table of Contents

In the framework of the reorganization back-office functions were lined up based on a shared services approach. This process was already started in 2006 and was further implemented in 2007 according to schedule. In the course of the year 2007 the Allianz north-east service region tested the functionality of the new business model in a pilot phase. In the financial year 2008 the remaining three regions will also be reorganized.

Reorganization in Italy

On October 1, 2007 the integration of Riunione Adriatica di Sicurtà (“RAS”), Lloyd Adriatico and Allianz Subalpina, which are–as a group–the

second largest composite insurer in Italy(1), was completed successfully. The newly formed Allianz S.p.A. is now able to realize the chance to exploit new opportunities for growth. To support this, the brands of the sales networks were reinforced with the Allianz brand, so e.g. the former RAS brand is now called “Allianz RAS”.

(1) | Based on gross premiums written and statutory premiums written; source Italian Insurers Association, ANIA. |

Global Diversification of our Insurance Business1)

As an integrated financial services provider we offer insurance, banking and asset management products and services to more than 80 million customers in over 70 countries. We are one of the leading global services providers of insurance, banking and asset management. Based on our market capitalization2), we are the largest financial institution in Germany.

Germany

In Germany, we have more than 100 years of experience in the insurance business. Today, together with Dresdner Bank and Allianz Global Investors we offer a complete spectrum of financial services.

Operations

We operate in the German market mainly through our insurance companies Allianz Versicherungs-Aktiengesellschaft (“Allianz Sach”), Allianz Lebensversicherungs-Aktiengesellschaft (“Allianz Leben”) and Allianz Private Krankenversicherungs-Aktiengesell-schaft (“Allianz Private Kranken”). In addition, Allianz Beratungs- und Vertriebs-AG serves as a distribution company. All entities are organized under the umbrella of the holding company Allianz Deutschland AG.3) At the end

of 2007, Allianz Deutschland AG had a total of 19.8 million customers.

As the market leader in Germany based on gross premiums written in 20074), Allianz Sach develops and providesproperty-casualty.

Forlife insurance, with Allianz Leben we are also market leader based on statutory premiums in 2007.4) In addition to Allianz Leben, we operate through a variety of smaller operating entities in the German market.

Through Allianz Private Kranken, we are the third-largest privatehealth insurer in Germany based on statutory premiums in 2007.4)

Our German results of operations also include our property-casualty assumed reinsurance business, which is primarily attributable to Allianz SE.

(1) | Please see “ITEM 18. Financial Statements—Notes to the Allianz Group’s Consolidated Financial Statements—Selected subsidiaries and other holding” for a breakdown of selected operating entities. |

(2) | As of March 1, 2008. Source: Deutsche Börse Group. |

(3) | Please see “Information on the Company—Important Group Organizational Changes—Reorganization of German Insurance Operations” for further information. |

(4) | Source: Based on data provided by German Insurance Association, GDV. |

18

Table of Contents

Products & Distributions

We offer products not only for all three insurance lines but also with a clear focus on products combining coverage from life, health and property-casualty insurance designed to better respond to customer needs. In addition we distribute products from Dresdner Bank and Allianz Global Investors Germany.

Our products are distributed mainly through a network of full-time tied agents, while distribution through our new bankagencies and brokers is increasing.

Inproperty-casualty, we offer a wide variety of insurance products for financial coverage for risks to private and business clients. Our main lines of business are motor liability and own damage, accident, general liability and property insurance.

In thelife business, we are active both in the private and commercial markets and offer a comprehensive range of life insurance and related products on both an individual and group basis. The main classes of coverage offered include annuity, endowment and term insurance. In our commercial lines, we offer group life insurance and provide companies with services and solutions in connection with pension arrangements and defined contribution plans.

In thehealth insurance business, we provide a wide range of products, including full private health care coverage for salaried employees and the self-employed, supplementary insurance for individuals insured under statutory health insurance plans, supplementary care insurance and foreign travel medical insurance.

Outlook

In order to strengthen our market position, we intend to further develop our customer-focused organization and aim to provide our clients with more integrated products for every stage of their lives.

For theproperty-casualty business, we see Germany being a rather mature market with a high degree of competition. One of the key challenges is achieving growth while also maintaining an appropriate level of profitability. To deliver all-encompassing service in emergency cases we will further develop our assistance-services for individuals and corporate customers.

For ourlife business, we expect strong growth opportunities as we see an increasing demand for private retirement products and retirement provisions in general.