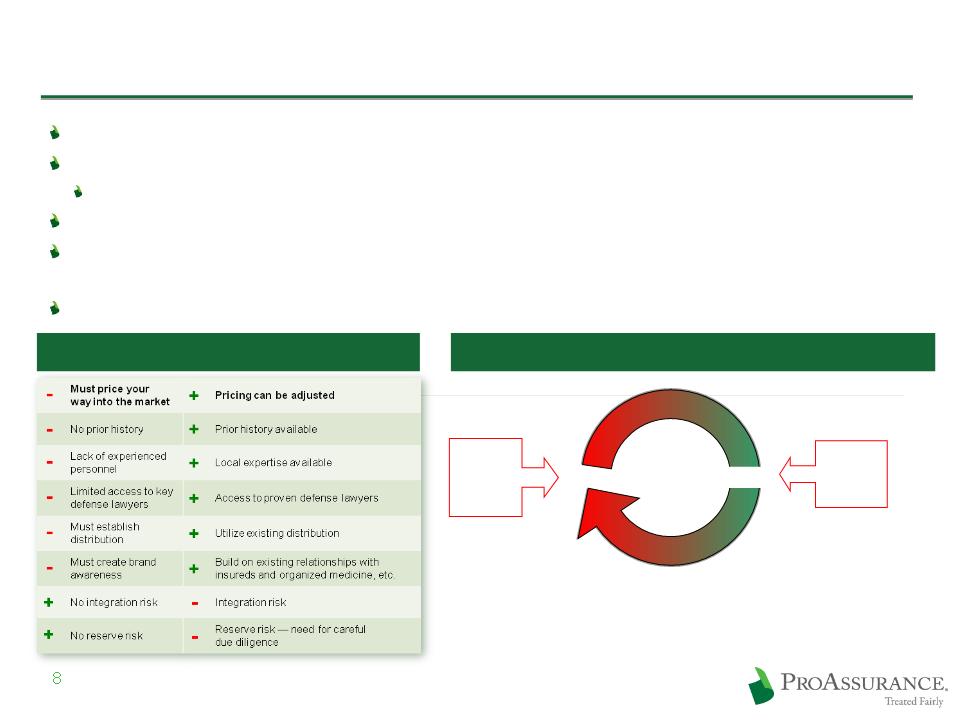

We are skilled at finding M & A opportunities, conducting in-depth due diligence and integrating

resulting acquisitions

2009: Consolidation of:

Mid-Continent General Agency

2009: Consolidation of:

Mid-Continent General Agency

Georgia Lawyers Insurance Co.

Georgia Lawyers Insurance Co.

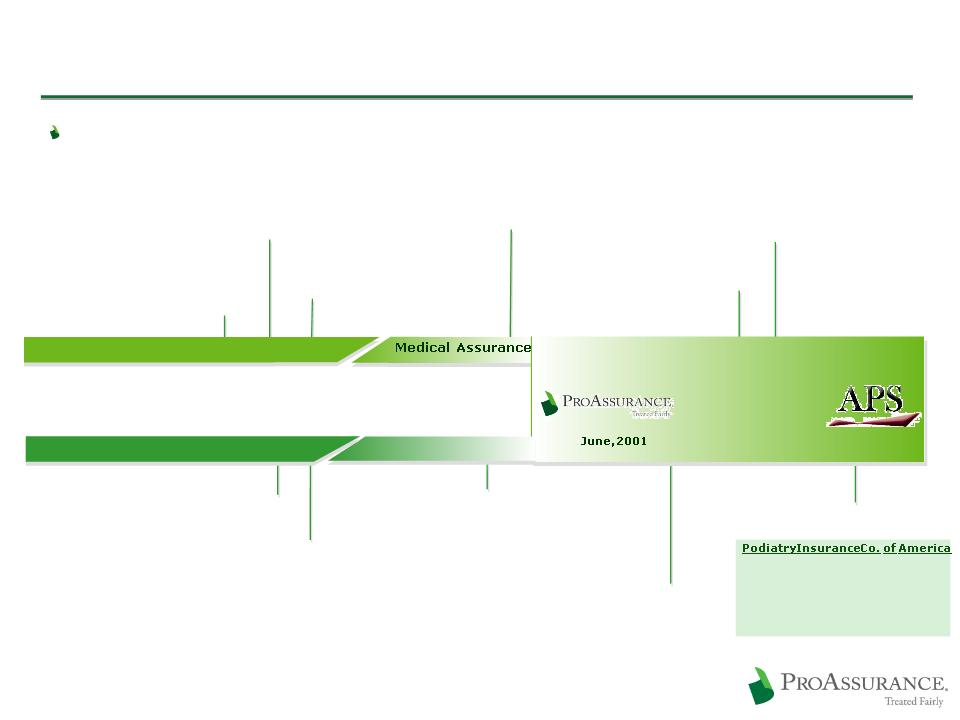

2004: Purchased Selected Renewal Rights from:

OHIC Insurance Company

2004: Purchased Selected Renewal Rights from:

OHIC Insurance Company

We Expect to Continue Growing Through M & A

7

1994: Consolidation of:

West Virginia Hosp. Ins Co.

1994: Consolidation of:

West Virginia Hosp. Ins Co.

1995: Consolidation of;

1995: Consolidation of;

Physicians Ins Co of Indiana

Physicians Ins Co of Indiana

Assumed business of:

Physicians Ins Co of Ohio

Assumed business of:

Physicians Ins Co of Ohio

1996: Consolidation of:

1996: Consolidation of:

Missouri Medical Ins Co

Missouri Medical Ins Co

1995: Assumed business of:

Associated Physicians Ins Co. (IL)

1995: Assumed business of:

Associated Physicians Ins Co. (IL)

1998: Consolidation of:

Physicians Protective Trust Fund (FL)

1998: Consolidation of:

Physicians Protective Trust Fund (FL)

1996: Assumed business of:

American Medical Ins Exchange (IN)

1996: Assumed business of:

American Medical Ins Exchange (IN)

Founding in the 1970s

Founding in the 1970s

1999: Assumed business of:

Medical Defense Associates (MO)

1999: Assumed business of:

Medical Defense Associates (MO)

Mutual Assurance

Physicians Ins. Co. of Michigan

Professionals Group

Creation of:

Creation of:

2005: Consolidation of:

NCRIC Group

2005: Consolidation of:

NCRIC Group

2006: Consolidation of:

PIC Wisconsin Group

2006: Consolidation of:

PIC Wisconsin Group

2007: PRI renewal rights deal

2002: SERTA renewal rights deal

2001: OUM renewal rights deal

2000: DPM Merger

1999: PACO Acquisition

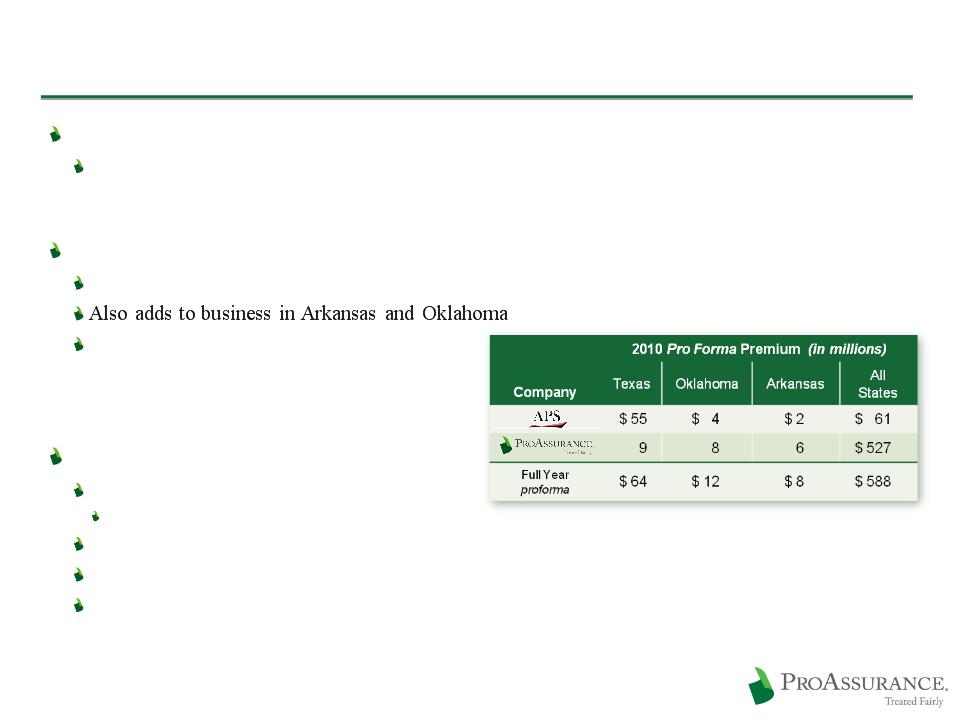

Completed

11/30/10