March 8, 2005

Association of Insurance and Financial Analysts

2005 Mid-Winter Conference

A. Derrill Crowe, M.D.

Edward L. Rand

Frank B. O’Neil

Chairman & CEO

Senior VP, Finance

Investor Relations Officer

Caution Regarding Forward Looking Statements

This presentation contains historical information as well as forward-looking statements that are based

upon our estimates and anticipation of future events, including our proposed transaction with NCRIC

Group, Inc. These estimates and events are subject to certain risks and uncertainties that could cause

actual results to vary materially from the expected results described in the forward-looking statements.

The words “anticipate,” “believe,” “estimate,” “expect,” “hopeful,” “intend,” “may,” “optimistic,”

“preliminary,” “project,” “should,” “will,” and similar expressions, whether used on a slide or in

speakers’ remarks, are intended to identify these forward-looking statements. There are numerous

important factors that could cause our actual results to differ materially from those in the forward-

looking statements. Thus, sentences and phrases that we use to convey our view of future events and

trends are expressly designated as Forward-Looking Statements as are sections of this presentation

clearly identified as giving our outlook on future business. The principal risk factors that may cause

actual results to differ materially from those expressed in the forward-looking statements are described

in various documents we file with the Securities and Exchange Commission, including the most recent

Form 10K for the year ended December 31, and Form 10Q for the most recent quarter. You should also

refer to our Form 8K filed February 28, 2005 for specific Cautions and Risk Factors regarding our

proposed transaction with NCRIC Group.

Financial data for the medical malpractice segment for all periods prior to June, 2001 reflects Medical

Assurance, Inc. data only, except where noted.

1

ProAssurance Overview

PROFESSIONAL LIABILITY

PERSONAL LINES

Overview

2

Market Cap: $1 Billion

Gross Premiums: $790 million

Assets: $3.2 billion

Specialty insurer diversified by

product and geography

Experienced, invested management

73% of Premiums

Fourth Largest Writer of Med Mal

The Industry’s Blue Chip Company

27% of Premiums

Targeting the Michigan Education

Community

Significantly Outperforms Peers

Experienced, Stable Management

12

0

Sr. Vice President / Finance

Ned Rand

Years in

Industry

Years at

Company

Position

Name

22

14

Average

20

10

Sr. Vice President / Claims

Darryl Thomas

25

12

Chief Financial Officer / MEEMIC

Christine Schmitt

17

17

Sr. Vice President / IR

Frank O'Neil

21

21

Chief Accounting Officer

James Morello

30

12

President & CEO - MEEMIC

Lynn Kalinowski

24

8

Chief Financial Officer

Howard Friedman

27

27

Vice Chairman

Paul Butrus

20

6

Sr. Vice President / Marketing

Jeff Bowlby

24

19

President & COO

Victor Adamo

28

28

Chairman & CEO

Derrill Crowe, M.D.

Management is aligned with shareholders–Directors & Officers own 11%

3

Professional Liability

The Core of ProAssurance

4

Creating a Leader Through Acquisitions

1994: Purchased:

West Virginia Hosp. Ins Co.

1995: Acquisition of;

Physicians Ins Co of Indiana

Assumed business of:

Physicians Ins Co of Ohio

1996: Acquisition of:

Missouri Medical Ins Co

1995: Assumed business of:

Associated Physicians Ins Co. (IL)

1998: Consolidation with:

Physicians Protective Trust Fund (FL)

1996: Assumed business of:

American Medical Ins Exchange (IN)

1997: Affiliated with:

MEEMIC

Founding in

the 1970’s

1999: Assumed business of:

Medical Defense Associates (MO)

2004: Purchased Selected Renewal Rights from:

OHIC Insurance Company

Mutual Assurance

Medical Assurance

Physicians Ins. Co. of Michigan

Professionals Group

Merger Created

June, 2001

2005: Proposed Acquisition of:

NCRIC Group

5

Regional Operating Structure

Corporate strategy

applied locally to

underwriting & claims

Local knowledge crucial

to understanding legal

environment

Local presence preserves

long-term customer

relationships

Consolidated Financial Strength With Local Operating Model

States of Origin or Acquisition

Expansion States

Professional Liability

+

+

+

+

+

6

Corporate Headquarters

Claims Offices

Claims / Underwriting Offices

+

Regional Operating Structure

Strengthening our

business model by

merging NCRIC into

our operations

Adds Mid-Atlantic

presence

Consolidated Financial Strength With Local Operating Model

Corporate Headquarters

States of Origin or Acquisition

Expansion States

Professional Liability

Claims Offices

Claims / Underwriting Offices

+

+

+

+

+

NCRIC transaction subject to regulatory approvals and approval by NCRIC shareholders

7

+

NCRIC Transaction

Stock-for-stock transaction to close

early in Q3

Exchange ratio: One NCRIC share

receives 0.25 PRA shares, within collar

Transaction consideration will vary

within a 10% collar

The exchange ratio will float outside

of the 10% collar

8

Strategic Advantages

Ease of Integration

Similar backgrounds and operating models

Transaction is expected to be accretive

in 2005

Strengthens our business in states we

had targeted for growth

Strengthens PRA’s position as the

market leader

9

Insuring physicians,

hospitals, dentists and other

healthcare providers

Majority of insureds are smaller

groups and solo practitioners

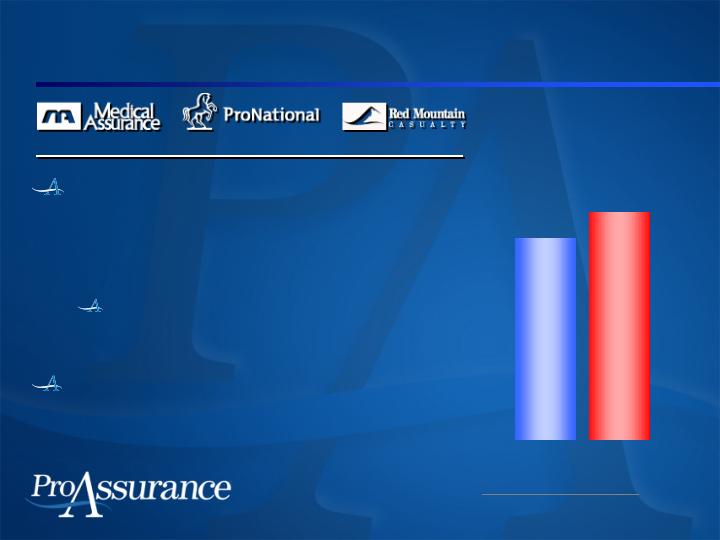

Professional Liability Snapshot

Three Year Average 2001-2003

Statutory Adjusted

Loss Ratio*

Medical Malpractice

*Source:A. M. Best Aggregates & Averages

Medial Malpractice Predominating

US Industry

124.3%

PRA

109.7%

Superior results through careful

underwriting, proper pricing and

effective claims handling

10

$349

$462

$543

$574

2001

2002

2003

2004

Gross Written Premiums*

(millions)

4 Year CAGR:

18.0%

We focus on bottom line results

but have been growing our top

line as well

Confident in current reserve

levels

Rated “A-” by A. M. Best,

S & P and Fitch

Professional Liability Snapshot

11

Market Leadership

Proven M& A capability

NCRIC transaction

We have advantages of size and scope

Ability to raise capital on a stand alone

basis to support growth

$ 198.5 million since 2002

Capital permits cost-effective use of

reinsurance

Professional Liability

12

Market Leadership

Specialty insurance with local operations

Venue-specific claims management

and underwriting knowledge

Proven track record of regional

operating success

Experienced management at all

levels of the organization

Professional Liability

13

Aggressive Claims Defense

Driven from the top of the organization

Our long-term competitive advantage

Aggressive defense of non-meritorious

claims

Cases Tried in 2004: 528

2002: 360; 2003:391

90% of closed claims resolved with no

indemnity payments

Generates lower costs and higher loyalty

Professional Liability

14

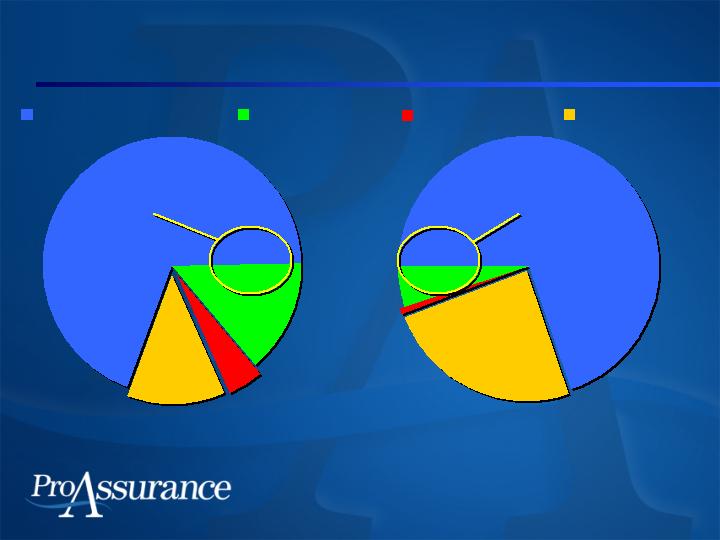

Closed Claim Outcome Comparison

Favorable

Outcomes: 83.3%

Favorable

Outcomes: 74.8%

15

14.0%

4.4%

12.3%

69.3%

24.4%

0.8%

5.1%

69.7%

Dropped or Dismissed

Defense Verdict

Plaintiff Verdict

Settled

ProAssurance 2004

Physician Insurers

Association, 2003

Latest Available Data

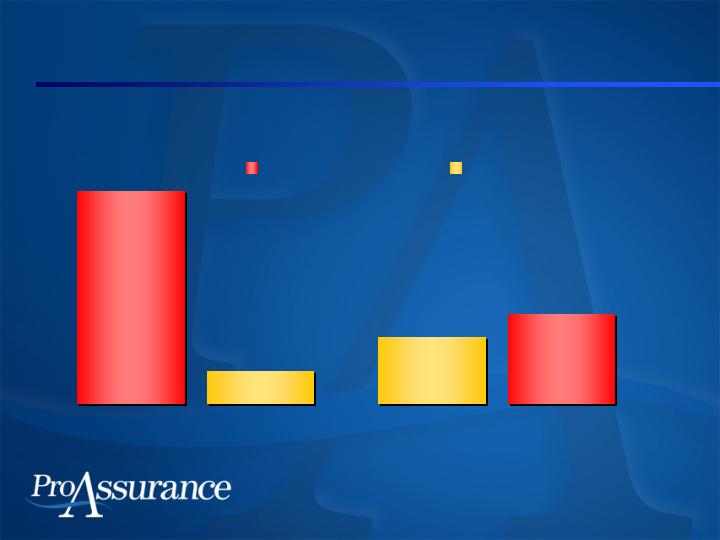

Closed Claim Cost Comparison

Reflects Results in All States with Various Policy Limits

16

$1,018,110

$153,145

$322,544

$430,601

Avg. Verdict

Avg. Settlement

ProAssurance 2004

Physician Insurers

Association, 2003

Latest Available Data

Average Indemnity Comparison

Weighted Average Indemnity Per Closed Claim

Latest Available Data

$63,399

$82,146

17

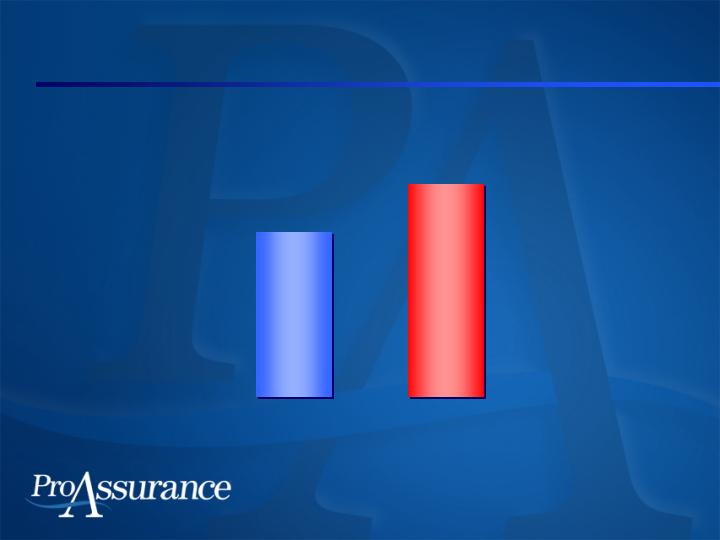

ProAssurance

PIAA 2003

2004

Three-Year Loss Ratio Comparisons

Our focus on

claims defense

allows us to

achieve better

results

Average Statutory Loss Ratio

2001-2003

US Industry

124.3%

PRA

109.7%

LEGAL

INDEMNITY

*Source:A. M. Best Aggregates & Averages

18

53.9%

88.3%

55.8%

36.0%

Medial Malpractice Predominating

Professional Liability Combined Ratio

Financial Overview

PRA PL Only

PL Industry

Source: ProAssurance Statutory Filings and A. M. Best Statutory Results

A. M. Best

Estimate

19

1999

2000

2001

2002

2003

2004

88.2%

109.4%

125.2%

124.5%

111.6%

104.8%

129.7%

133.8%

142.5%

135.2%

128.1%

154.2%

Pricing Remains Strong

Rate increases ensured higher

premium per unit of risk

19% in 2004

28% in 2003

28% in 2002

23% in 2001

Continuous re-underwriting of our book

New insureds balance out non-renewals

Professional Liability

20

Looking Ahead to 2005

Continued growth at adequate rates

Ensures proper margins on each policy

Adding insureds through growth in

existing markets and through M&A

Competitors’ capacity remains

constrained

Growth in Red Mountain Casualty

Our E & S market

21

Looking Ahead to 2005

The fragmented Professional Liability

market will provide acquisition

opportunities

Pursuing opportunistic acquisitions

Success not dependent on acquisitions

Professional Liability

22

ProAssurance will be invited to

participate in any major opportunities

Experienced consolidator

Acquisitions formed our foundation

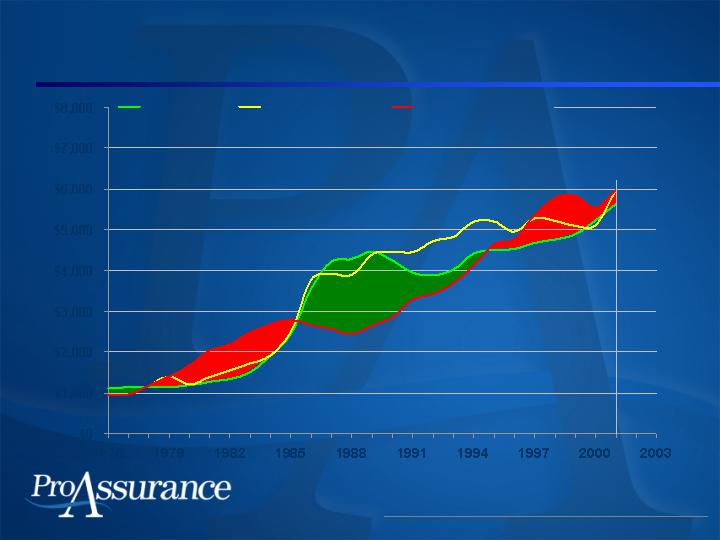

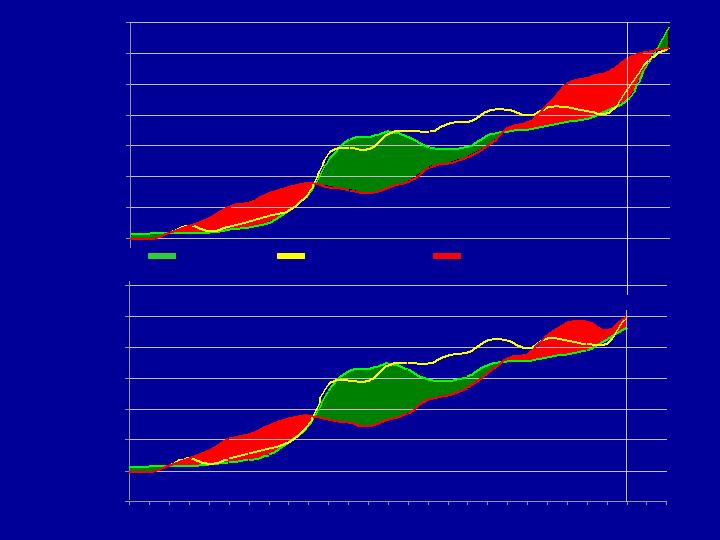

Will History Repeat Itself—Again?

Professional Liability

Millions

Source: A. M. Best Aggregates and Averages 1976 – 2001

At 12/31/2001

23

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

Premium

Initial Reserve

(Estimated)

Developed Loss

(Actual)

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

Medical Malpractice Industry, Net Basis Occurrence and Claims-Made Combined

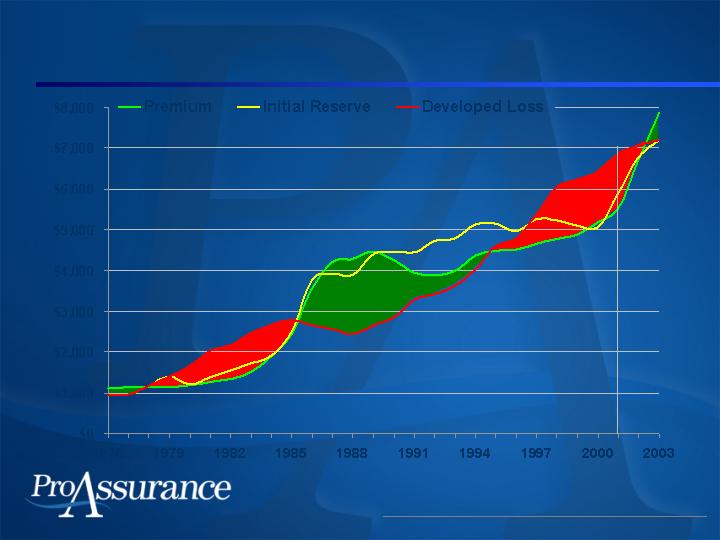

Will History Repeat Itself—Again?

Professional Liability

Millions

(Estimated)

(Actual)

Source: A. M. Best Aggregates and Averages 1976 – 2003

12/31/2001

24

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

Premium

Initial Reserve

Developed Loss

Medical Malpractice Industry, Net Basis Occurrence and Claims-Made Combined

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

Premiums

In Millions

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

At 12/31/2001

Premium

Initial Reserve

Developed Loss

(Estimated)

(Actual)

Looking Ahead: Tort Reform

Federal tort reform faces Senate roadblock

even after Republican gains

State-by-state reforms

Passed in many states (GA,FL, OH, PA, TX & WV)

Long-term effectiveness yet to be proven

No judicial review yet—could be found

unconstitutional

Organizational efforts in many other states

ProAssurance’s business plans do not

depend on tort reform

Professional Liability

26

Personal Lines

The Overlooked Gem

Personal Lines Snapshot

MEEMIC targets teachers and

the educational community

Primarily personal auto (81%)

Also homeowners and boat

Overview

$130

$142

$174

$197

$216

2000

2001

2002

2003

2004

Direct Written Premiums

(millions)

5 Year CAGR:

13.5%

28

Personal Lines Snapshot

Careful underwriting in a

preferred market

Peer-to-peer selling model

provides a solid foundation

Incremental expansion underway

Rated “A-”

Overview

MI Industry

86.9%

MEEMIC

68.2%

*Source: A. M. Best

Statutory Adjusted Loss Ratio*

Private Passenger Auto

Superior Results

Five Year Average 1999-2003

29

MEEMIC’s Importance

2004 accomplishments

Combined ratio of 83.4%

Tenth straight year of underwriting

profitability

Growth in Premiums and

Policyholders

Consistent results

Personal Lines

30

Industry-Leading Results

65.2%

70.3%

64.6%

65.8%

61.3%

23.7%

23.8%

23.1%

22.1%

22.1%

2000

2001

2002

2003

2004

GAAP Combined Ratio

Expense Ratio

Loss Ratio

88.9%

94.1%

87.7%

87.9%

Personal Lines

Source: A. M. Best

83.4%

5 Year Average of 88.4%

31

MEEMIC: Steady Growth

Premiums continue to increase in a

softening market

Up 10% for 2004

Up 13% for 2003

Increasing value of cars and homes

insured

Sustained policyholder growth in all

lines

Personal Lines

32

Financial Overview

The Strength of ProAssurance

33

Financial Highlights

Cash flows at all time high

Consolidated Combined Ratio

below 100 for 2004

Solid bottom line growth

Continued growth

in top line as well

$36.3

$61.3

$177.0

$282.8

$373.5

2000

2001

2002

2003

2004

Merger Created ProAssurance in June 2001

Cash Flow from

Operations

34

Balance Sheet Comparison

in millions

Balance Sheet Strength Sets

ProAssurance Apart

December 31, 2004, Unaudited

35

Total Assets

$

3,240

$

2,879

13%

Cash & Invested Assets

$

2,485

$

2,103

21%

Reserves for Losses

and Loss Adjustment

Expenses

$

2,413

$

2,173

11%

Shareholders’ Equity

$

611

$

546

12%

Y-to-Y

2004

2003

Change

High Quality, Liquid Investment Portfolio

Financial Overview

December 31, 2004, Unaudited

Cash

2%

Equities

1%

Other

2%

Fixed

Securities*

95%

Total = $2.4 billion

* Includes Preferred Stock and Business-Owned Life Insurance

36

Conservative portfolio

No derivatives

Managed by outside advisors

Average fixed maturity duration

of 3.81 years

High quality fixed income

portfolio

Weighted average rating of “AA”

99.5% investment grade

Avg. tax-equivalent yield: 4.72%

Net unrealized gain: $37.5 mln

Affected by recent interest rate

movement

2004 Income Statement

in millions, except per share data

Financial Overview

December 31, 2004, Unaudited

37

Gross Premiums Written

$

573.6

$

216.1

$

789.7

Net Investment Income

75.0

10.9

87.2

Total Revenue

593.9

196.6

794.6

Total Expenses

537.6

153.0

697.1

Net Income

72.8

Professional

Personal

Liability

Lines

Consolidated

Cash from Operations

$

373.5

Net Income/Share (diluted)

$

2.37

2004 Income Statement vs. 2003

in millions, except per share data

Financial Overview

December 31, 2004, Unaudited

38

Gross Premiums Written

$

789.7

$

740.1

7%

Net Investment Income

87.2

73.6

19%

Total Revenue

794.6

709.6

12%

Total Expenses

697.1

659.3

6%

Net Income

$ 72.8

$

38.7

88%

2004

2003

Change

Cash from Operations

$

373.5

$

282.8

32%

Net Income/Share (diluted)

$

2.37

$

1.32

80%

Consistent Growth in Book Value per Share

$3.67

$6.27

$8.56

$11.57

$13.92

$16.02

$18.77

$20.92

1991

1993

1995

1997

1999

2001

2003

2004

Annual stock price performance of

PRA and predecessors is 18.9%

since inception in September, 1991

Financial Overview

39

Key Objective: 12%-14% ROE

ROE targets drive our ultimate consolidated

combined ratio goals

Professional Liability: 96% or lower

Personal Lines: 94% or lower

Combined Ratio History

2005: <99.2% (goal)

2004: 99.2%

2003: 105.1%

2002: 113.0%

2004 Outlook

40

Our Opportunities

41

Leader in medical malpractice industry

Organic growth and M&A expansion

Proven platform with regional operating

approach

Attractive niche personal lines business

Experienced management team focused

on driving returns

Conservative financial position