1

Non-GAAP Measures

Forward Looking Statements

This presentation contains Forward Looking Statements and other information designed

to convey our projections and expectations regarding future results. There are a number

of factors which could cause our actual results to vary materially from those projected in

this presentation. The principal risk factors that may cause these differences are

described in various documents we file with the Securities and Exchange Commission,

such as our current reports on Form 8-K, and our regular reports on Forms 10-Q and 10-

K, particularly in “Item 1A, Risk Factors.” Please review this presentation in

conjunction with a thorough reading and understanding of these risk factors.

to convey our projections and expectations regarding future results. There are a number

of factors which could cause our actual results to vary materially from those projected in

this presentation. The principal risk factors that may cause these differences are

described in various documents we file with the Securities and Exchange Commission,

such as our current reports on Form 8-K, and our regular reports on Forms 10-Q and 10-

K, particularly in “Item 1A, Risk Factors.” Please review this presentation in

conjunction with a thorough reading and understanding of these risk factors.

This presentation contains Non-GAAP measures, and we may reference

Non-GAAP measures in our remarks. A reconciliation of these measures to GAAP

measures is available in our latest quarterly news release, which is available in the

Investor Relations section of our website, www.ProAssurance.com, and in

the related Current Reports on Form 8K disclosing that release.

Non-GAAP measures in our remarks. A reconciliation of these measures to GAAP

measures is available in our latest quarterly news release, which is available in the

Investor Relations section of our website, www.ProAssurance.com, and in

the related Current Reports on Form 8K disclosing that release.

2

ProAssurance: Quick Facts

Market Cap: $1.9 Billion / Equity: $1.3 Billion

Fifth largest writer of medical liability

Writing business in 30 jurisdictions

Approximately 39,000 policyholders

Approximately 33,000 physicians & dentists

Approximately 5,400 attorneys

Majority in small or solo practice

Highly rated by A. M. Best and Fitch

3

ProAssurance: Our Challenges

The soft market

Finding profitable growth opportunities

Maintaining operational discipline in the face of

irrational competitors

irrational competitors

The financial markets

Balancing risk vs. return

Ensuring enduring balance sheet strength

The Soft Market Challenge:

Finding Profitable Growth

Finding Profitable Growth

The Soft Market Challenge:

Finding Profitable Growth

Finding Profitable Growth

5

Finding Profitable Growth

The Challenges

We take a long-term view

We focus on the bottom line

We will reluctantly turn away unprofitable business

We understand Wall Street’s expectation

for top line growth

for top line growth

But not at any price

6

ProAssurance was

formed by the

combination of two

successful companies

with a history of M & A

formed by the

combination of two

successful companies

with a history of M & A

Profitable Growth Through M & A

ProAssurance has been built through M & A

7

Each company brought

multiple transactions

into ProAssurance at

our founding in 2001

multiple transactions

into ProAssurance at

our founding in 2001

Profitable Growth Through M & A

ProAssurance has been built through M & A

8

We have continued to

grow through M & A

grow through M & A

NCRIC in the mid-

Atlantic

Atlantic

PIC-Wisconsin in the

upper Midwest

upper Midwest

Profitable Growth Through M & A

ProAssurance has been built through M & A

9

We carefully evaluate

the medical and legal

climate of each state

before entering

the medical and legal

climate of each state

before entering

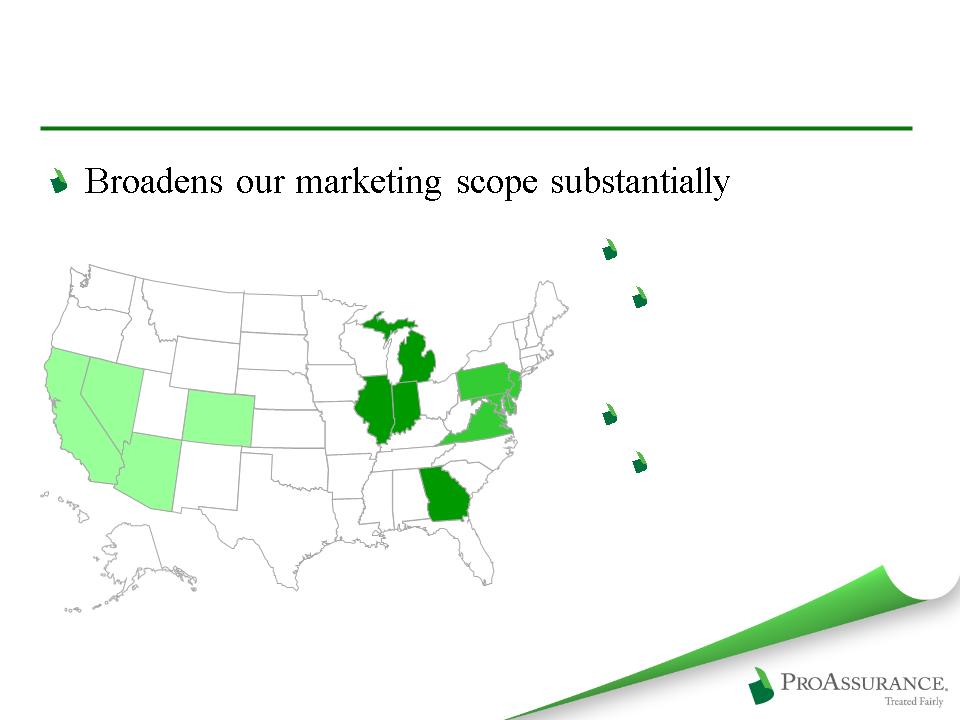

We are the market

leaders in AL, DE, DC,

OH, & WI

leaders in AL, DE, DC,

OH, & WI

Denovo Growth Also Plays a Role

We have added states as opportunities arose

10

New Transactions Strengthen Us

The PICA Group

Leading insurer of podiatric physicians nationwide

Market share: approximately 70%

2007 Premiums: $99 million

Profitable

Well managed

Low integration risk

Joining PRA through a sponsored demutualization

Will operate as a stand-alone subsidiary

11

9,800 DPMs

6,800 other providers

93% Direct

Largest States:

CA, FL, NY, IL, TX

11%

7%

9%

7%

8%

PICA’s Business Profile

PICA’s Business Profile

Adding the PICA Group

Expands our footprint nationwide

Adds ~$99 mln premium and 16,600 insureds

12

New Transactions Strengthen Us

Georgia Lawyers Insurance Company

A leading insurer of Georgia attorneys

2007 Premiums: $5.5 million

Solidifies our presence in the legal professional

liability market

liability market

13

GLIC: 2,700 lawyers

Most small and

mid-size firms

mid-size firms

Existing legal book is

5,400 attorneys in 2,8oo

law firms

5,400 attorneys in 2,8oo

law firms

2007 Premium:

$10.4 million

$10.4 million

Adding Georgia Lawyers Insurance

14

Greyhawk (Phoenix)

AZ, CA, CO, NV,

WA

WA

ProLawyer (Philadelphia)

DE, DC, MD, NJ,

PA, VA

PA, VA

Adding Dedicated Agents for Lawyers

The Soft Market Challenge:

Maintaining Operational Discipline

Maintaining Operational Discipline

The Soft Market Challenge:

Maintaining Operational Discipline

Maintaining Operational Discipline

16

Maintain Operational Discipline

The Challenge

Irrational competitors price their product to protect

their top line and market share

their top line and market share

Mortgaging their future for the status quo

We compete by offering real service and solid

financial security

financial security

17

Our local presence

retains the benefits of

our M & A transactions

through long-term

customer relationships

retains the benefits of

our M & A transactions

through long-term

customer relationships

Efficiencies gained

from consolidated

“back-room” operations

from consolidated

“back-room” operations

Claims / Underwriting Offices

Claims / Underwriting Offices

Operational Discipline: Strategy

Local knowledge remains the key to profitable

professional liability insurance

professional liability insurance

18

Operational Discipline: Strategy

Apply an overall corporate strategy that

recognizes state-by-state differences

recognizes state-by-state differences

Loss trends allowing more aggressive strategies in

long-term markets

long-term markets

Spread risk through geographical

diversification

diversification

Maintain margin

More important than top-line volume

Protect the balance sheet

19

Operational Discipline: Strategy

Charge adequate an adequate premium for

every risk

every risk

Loss-trends drive rates

Retain historical reserving practices

Be prepared when the cycle turns

20

Insureds

Reserves in millions

Strict Underwriting as Claims Peaked.

The Hard Market

The Hard Market

NCRIC

Policyholders

Policyholders

PIC Wis

Policyholders

Policyholders

Market Softening

Maintaining Historical Reserving

21

We try more claims

than any company in

our line of business

than any company in

our line of business

We try more claims

than any company in

our line of business

than any company in

our line of business

Focus on Claims Defense: Our Core

We offer our insureds the

option of an unfettered defense

of their claim

option of an unfettered defense

of their claim

Provides a long-term financial

and marketing advantage

and marketing advantage

A key differentiating factor in

the market as claims data

becomes public

the market as claims data

becomes public

22

Favorable

Outcomes:

83%

Outcomes:

83%

Favorable

Outcomes:

83%

Outcomes:

83%

Favorable

Outcomes:

74%

Outcomes:

74%

Favorable

Outcomes:

74%

Outcomes:

74%

ProAssurance Industry Data

Source: The PIAA

Five Year Average

2003 - 2008

2003 - 2008

Why Claims Strategy Matters

23

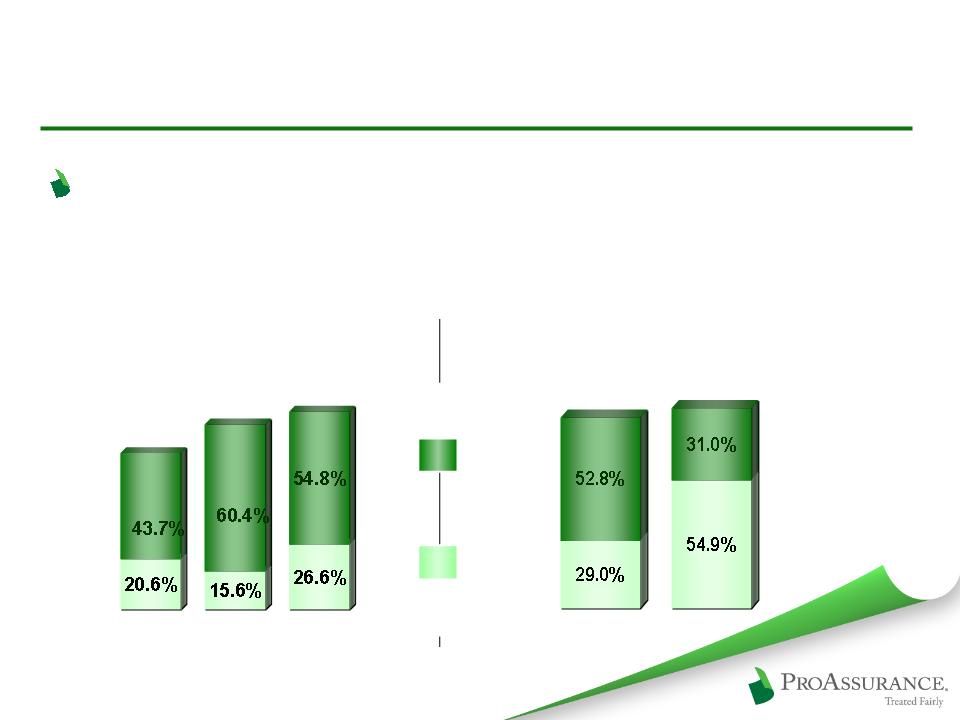

Average Statutory Loss Ratio

2003-2007

Industry

85.9%

85.9%

Legal

Payments

Payments

Loss

Payments

Payments

PRA:

81.8%

81.8%

2005

81.4%

ProAssurance Stand Alone

2005 - - 2007

2006

76.0%

*Source: A. M. Best Aggregates & Averages, Medical Malpractice Predominating

2007

64.3%

Why Claims Strategy Matters

Our ability and willingness to defend claims

allows us to achieve better results

allows us to achieve better results

24

Board / Discipline

Board / Discipline / Med Mal

Med Mal disclosure

legislation proposed

legislation proposed

P

P

P

P

P

The Age of Transparency

25

http://12.150.185.184/dca/simple_search.jsp

The Age of Transparency

The Financial Challenge:

Balancing Risk vs. Return

Balancing Risk vs. Return

The Financial Challenge:

Balancing Risk vs. Return

Balancing Risk vs. Return

27

Navigating the Financial Markets

The Challenges

Balancing risk vs. return

Ensuring enduring balance sheet strength

28

AT

9/30/2008

9/30/2008

Stockholder’s Equity

Stockholder’s Equity

96%

96%

Other

Debt

Debt

4%

Balancing Risk vs. Return

29

$3.5 Billion

$3.5 Billion

Portfolio

Portfolio

Fixed Income: 86%

Fixed Income: 86%

Short Term: 9%

Short Term: 9%

Equity and Other

Investments: 3%

Investments: 3%

Equity and Other

Investments: 3%

Investments: 3%

BOLI: 2%

BOLI: 2%

AT

9/30/2008

9/30/2008

Balancing Risk vs. Return

30

Asset

Backed:

Backed:

28%

State/Muni:

44%

Corporate:

19%

BOLI: 2%

Govt/Agency:7%

AT

9/30/2008

9/30/2008

Portfolio: Fixed Income

$3.1 Billion is Fixed Income

Average fixed maturity

duration: 4.4 years

duration: 4.4 years

Average tax-equivalent

yield: 5.41%

yield: 5.41%

97.6% investment grade

Weighted average: AA

31

AT

9/30/2008

9/30/2008

The Financial Challenge:

Ensuring Balance Sheet Strength

Ensuring Balance Sheet Strength

The Financial Challenge:

Ensuring Balance Sheet Strength

Ensuring Balance Sheet Strength

33

All $ amounts in billions

AT

9/30/2008

9/30/2008

34

Y-T-D 2008 Income Statement Highlights

in millions, except per share data

Gross Premiums Written $ 374 $ 440 -15%

Net Investment Income 122 128 -5%

Operating Income $ 127 $ 118 8%

Operating Income/Diluted Share $ 3.73 $ 3.36 11%

Operating Cash Flow $ 142 $ 207 -31%

September 30, Y-OVER-Y

2008 2007 CHANGE

35

Insurance Leverage

(in millions)

0.9:1

0.9:1

Premiums

to Surplus

to Surplus

Premiums

to Surplus

to Surplus

0.9:1

0.9:1

1:1

1:1

0.7:1

0.7:1

0.5:1

0.5:1

0.5:1

0.5:1

0.3:1

0.3:1

36

Book Value Each Year End for ProAssurance and Predecessor Companies

Stock Price

Book Value

CAGR

Since 1991: 14.4%

As PRA: 12.5%

Steady Growth Throughout The Cycles

CAGR

Since 1991: 15.7%

As PRA: 15.8%

Return

Total: 1331%

5 Yr: 140%

10 Yr: 240%

Summary:

Prepared to Meet the Challenges

Prepared to Meet the Challenges

Summary:

Prepared to Meet the Challenges

Prepared to Meet the Challenges

38

ProAssurance

Concentrating on shareholder value

Growing Book Value per Share

Focused on the long-term

Maintaining leading market position

Protecting the balance sheet

Building strength for the next cycle turn

Evaluating all M & A opportunities

39

ProAssurance

Proven success throughout the cycles

Disciplined pricing and underwriting

Consistent reserving policy

Proven claims strategy

Balance sheet strength

Significant share ownership throughout the

company

company

Demonstrated commitment to a long-term

view of a complicated business

view of a complicated business

40

Appendix: Investments

Appendix: Investments

41

$ in 000’s

Performance by Quarter Q1, 2005 - Q3, 2008

AT

9/30/2008

9/30/2008

Equities & Other Investments

42

AT

9/30/2008

9/30/2008

Portfolio: Municipals $1.4B

Current investment policy

requires investment grade

rating prior to apply the

effect of insurance

requires investment grade

rating prior to apply the

effect of insurance

43

Whole Loan LTV: 59%

Alt-A LTV: 63%

Further Details Provided

on Sub-Prime and

CMBS in our handouts

and today’s 8K

on Sub-Prime and

CMBS in our handouts

and today’s 8K

AT

9/30/2008

9/30/2008

44

AT

9/30/2008

9/30/2008

Further Details Provided

on Sub-Prime and

CMBS in our handouts

and today’s 8K

on Sub-Prime and

CMBS in our handouts

and today’s 8K

Portfolio: Corporate

45

Tax Notes are private

placements guaranteed by

banks & secured by Sec 42 tax

credits

placements guaranteed by

banks & secured by Sec 42 tax

credits

AT

9/30/2008

9/30/2008

Further Details Provided

on Sub-Prime and

CMBS in our handouts

and today’s 8K

on Sub-Prime and

CMBS in our handouts

and today’s 8K

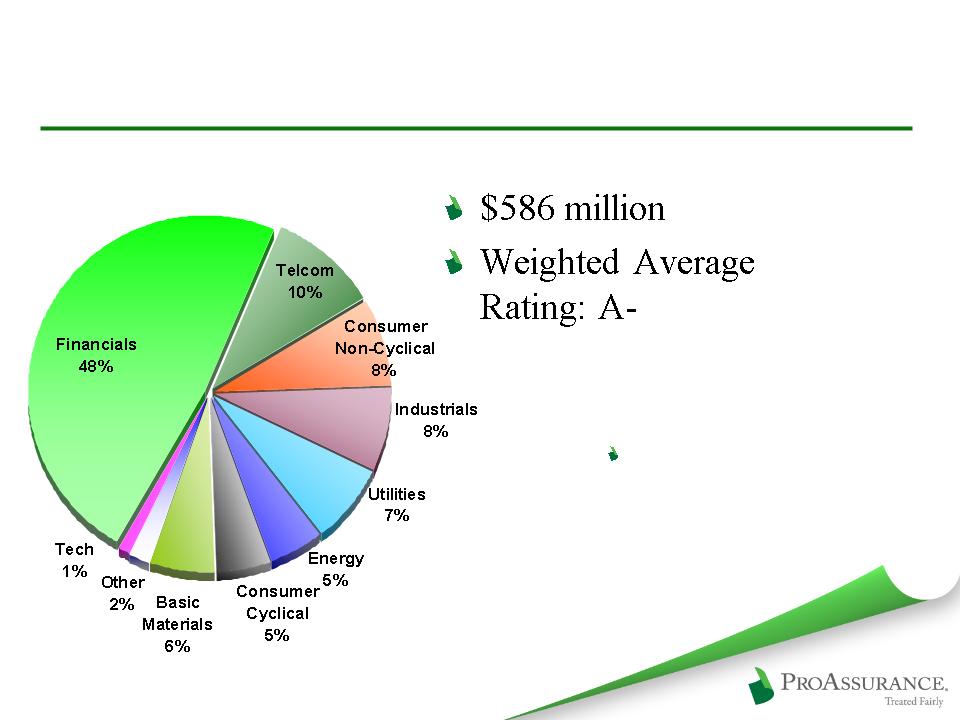

Portfolio: Corporate-Financials

46

AT

9/30/2008

9/30/2008

Portfolio: Treasury/GSE

47

$524 million

Average Rating:

AAA

AAA

AT

9/30/2008

9/30/2008

Portfolio: FRE and FNM

48

AT

9/30/2008

9/30/2008

Portfolio Overview: Short Term

49

AT

9/30/2008

9/30/2008

Portfolio Overview: BOLI

50

At 9/30/08 | Type | Quality |

$8.7Mln | Mortgage-Backed | AA+ avg - LTV 73% |

$6.1Mln | Home Equity | AA avg |

At 09/30/08 | Vintage |

$7.2 Mln | 2004 & Prior |

$4.4 Mln | 2005 |

$2.6 Mln | 2006 |

$0.6 Mln | 2007 |

Portfolio Overview: Sub-Prime

$13.4 million market value in AFS portfolio

$1.4 million market value in high-yield LP

51

At 9/30/08 | Quality |

$191 Mln | AAA |

$2 Mln | AA |

At 9/30/08 | Wtd Avg LTV |

85% | <70% |

15% | <72% |

At 9/30/08 | Credit Support |

80% | >20% |

5% | 15% - 20% |

13% | 10% - 15% |

2% | Less than 10% |

At 9/30/08 | Deal Cumulative Delinquencies |

45% | None |

27% | 0% - 0.5% |

20% | 0.5% - 1.0% |

7% | 1.0% - 2.0% |

1% | 2.0% - 2.2% |

At 9/30/08 | Debt Service Coverage |

78% | >1.5x |

22% | >1.3-1.5x |

Portfolio Overview: CMBS

$193 million in non-agency CMBS

6% of fixed income portfolio

52

AT

9/30/2008

9/30/2008

BofA/ML $25 | NRUC $6 |

Wells/Wach $19 | Depfa ACS $5 |

Morgan Stanley $16 | DeutscheBk $5 |

Citigroup $14 | BONY $5 |

GECC $13 | Unilever Cap $4 |

American Exp $11 | Deere Cap $4 |

JP Morgan $9 | FMCC $3 |

Goldman $8 | Boeing Cap $3 |

Hypotheken Essn $8 | Met Life $3 |

Credit Suisse $7 | Blackrock $3 |

Portfolio: Corporate-Financials

Top 20 Largest Banks & Financials

($ 171 million)

Appendix: Industry History

Appendix: Industry History