March 9-11, 2009

W. Stancil Starnes Chairman and Chief Executive Officer

Edward L. Rand, Jr. Chief Financial Officer

Frank B. O’Neil Investor Relations Officer

Raymond James & Associates

Raymond James & Associates

30th Annual Institutional Investors Conference

30th Annual Institutional Investors Conference

2

Forward Looking Statements

This presentation contains Forward Looking Statements and other information designed

to convey our projections and expectations regarding future results. There are a number

of factors which could cause our actual results to vary materially from those projected in

this presentation. The principal risk factors that may cause these differences are

described in various documents we file with the Securities and Exchange Commission,

such as our current reports on Form 8-K, and our regular reports on Forms 10-Q and 10-

K, particularly in “Item 1A, Risk Factors.” Please review this presentation in

conjunction with a thorough reading and understanding of these risk factors.

to convey our projections and expectations regarding future results. There are a number

of factors which could cause our actual results to vary materially from those projected in

this presentation. The principal risk factors that may cause these differences are

described in various documents we file with the Securities and Exchange Commission,

such as our current reports on Form 8-K, and our regular reports on Forms 10-Q and 10-

K, particularly in “Item 1A, Risk Factors.” Please review this presentation in

conjunction with a thorough reading and understanding of these risk factors.

This presentation contains Non-GAAP measures, and we may reference

Non-GAAP measures in our remarks. A reconciliation of these measures to GAAP

measures is available in our latest quarterly news release, which is available in the

Investor Relations section of our website, www.ProAssurance.com, and in

the related Current Reports on Form 8K disclosing that release.

Non-GAAP measures in our remarks. A reconciliation of these measures to GAAP

measures is available in our latest quarterly news release, which is available in the

Investor Relations section of our website, www.ProAssurance.com, and in

the related Current Reports on Form 8K disclosing that release.

Non-GAAP Measures

3

ProAssurance: Quick Facts

Market Cap: $1.4 Billion / Equity: $1.4 Billion

Fifth largest writer of medical liability

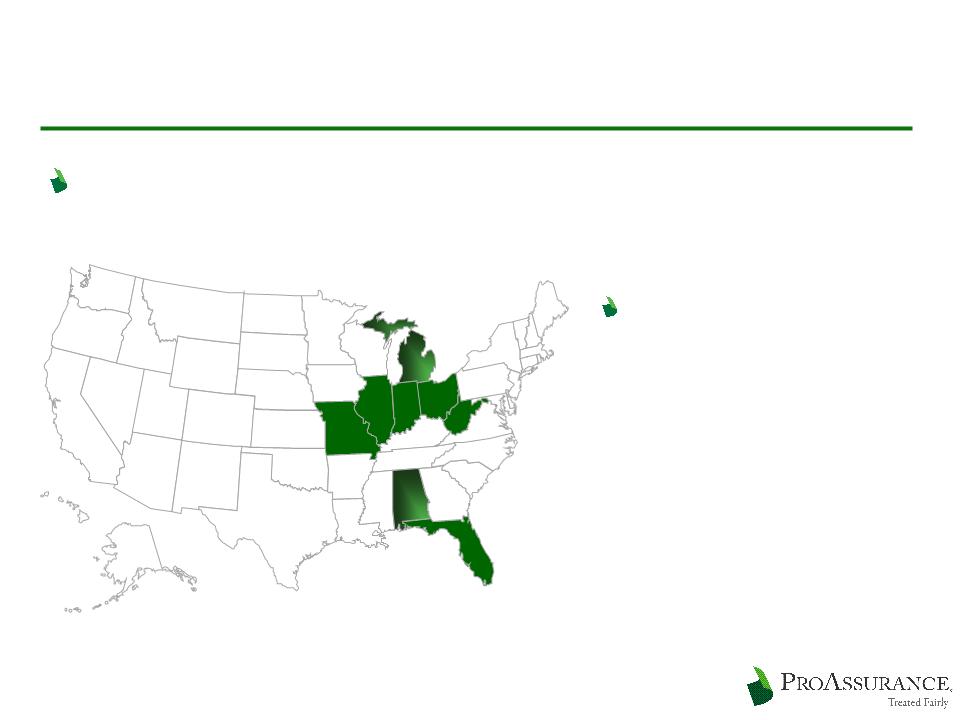

Writing business in 30 jurisdictions

Approximately 39,000 policyholders

32,500 physicians & dentists

8,100 attorneys

Majority in small or solo practice

Highly rated by A. M. Best and Fitch

4

ProAssurance: Long-Term Success

Our Balance Sheet remains strong

Conservative investments

Little debt

Low leverage

Solid stock performance over time

Growing organically and through M & A

Adding over $100 million to our top line in 2009

through M & A

through M & A

Diversifying our risk profile

5

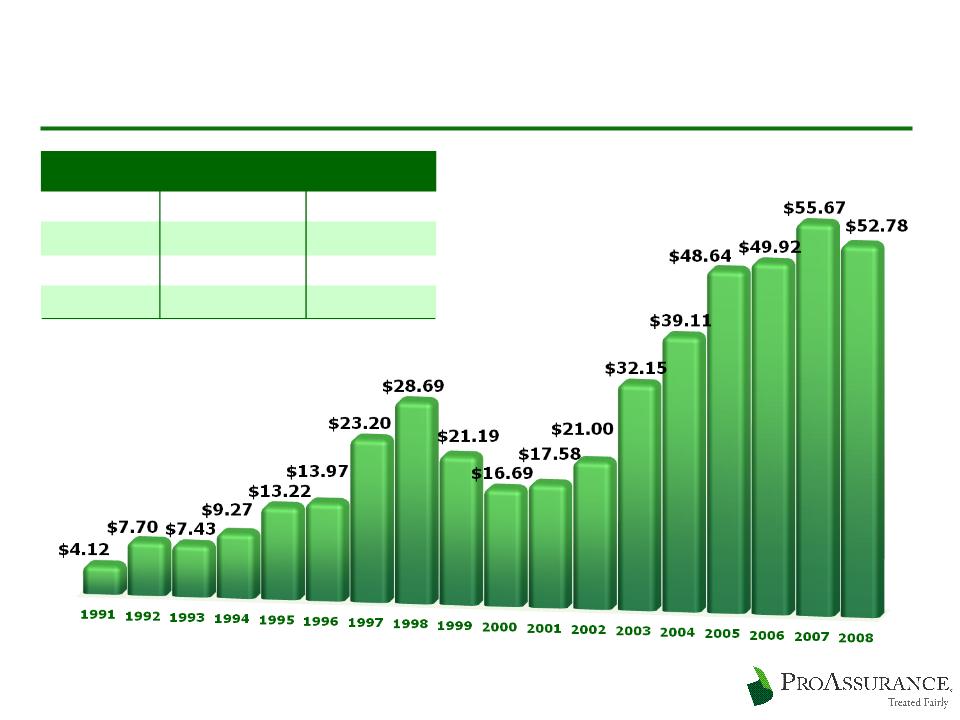

ProAssurance: Long-Term Success

NYSE Closing Price at Each year-End

Stock Price Performance

Cumulative

CAGR

10 year

249%

10%

5 year

135%

6%

1 year

-5%

-5%

6

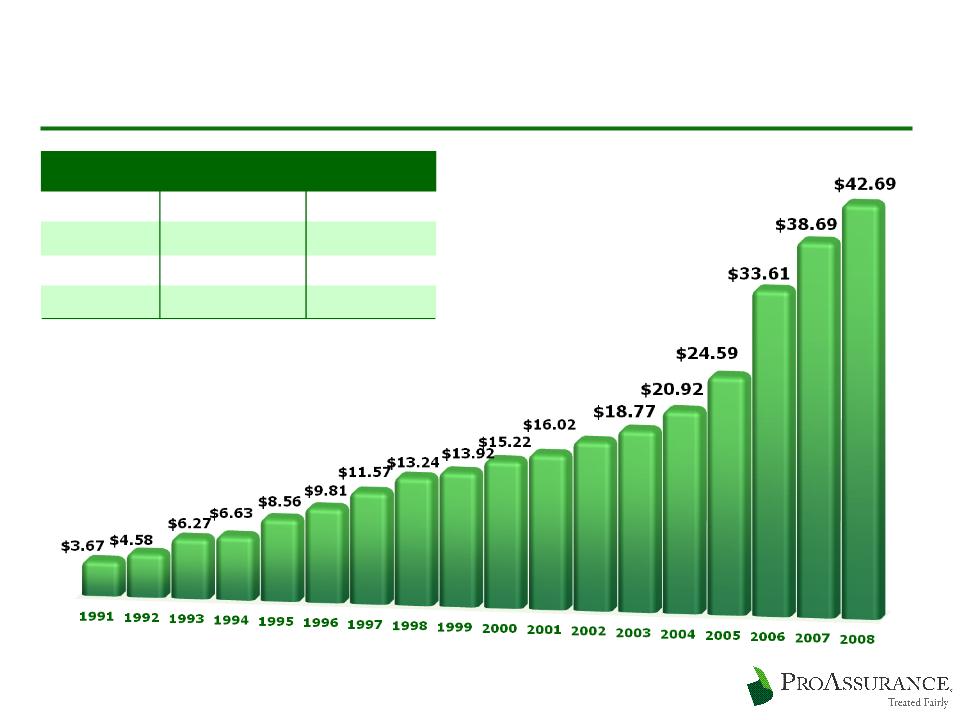

ProAssurance: Long-Term Success

NYSE Closing Price at Each year-End

Book Value Growth

Cumulative

CAGR

10 year

67%

13%

5 year

51%

10%

1 year

10%

10%

7

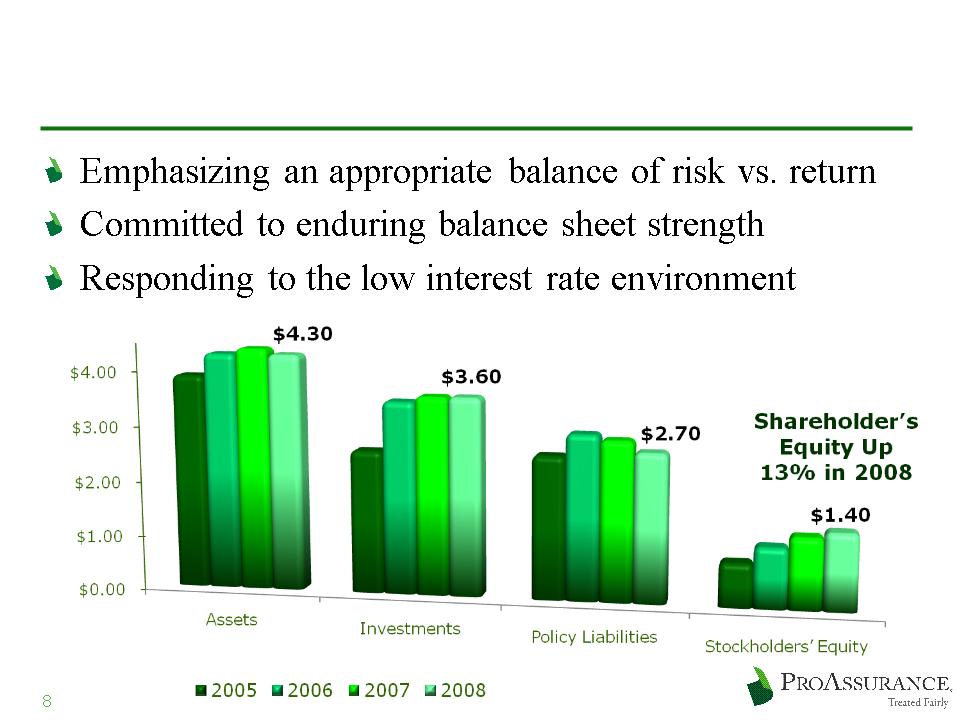

ProAssurance: 2008 Highlights

Increased Shareholders’ Equity

and Book Value per Share

and Book Value per Share

Significantly increased profits

Announced three M&A transactions

Major brand enhancement project

Entering 2009 in a Strong Position

$ amounts

in Billions

in Billions

9

ProAssurance 2008 highlights

in millions, except per share data

Gross Premiums Written $ 472 $ 549 - 14%

Net Investment Income 158 171 - 8%

Total Revenue 567 706 - 20%

Total Expenses 470 561 -16%

Operating Income $ 207 $ 172 20%

Net Income (Includes Investment Losses) $ 178 $ 168 6%

Operating Income/Diluted Share $ 6.07 $ 4.90 24%

Operating Cash Flow $ 165 $ 244 -32%

December 31, Y-OVER-Y

2008 2007 CHANGE

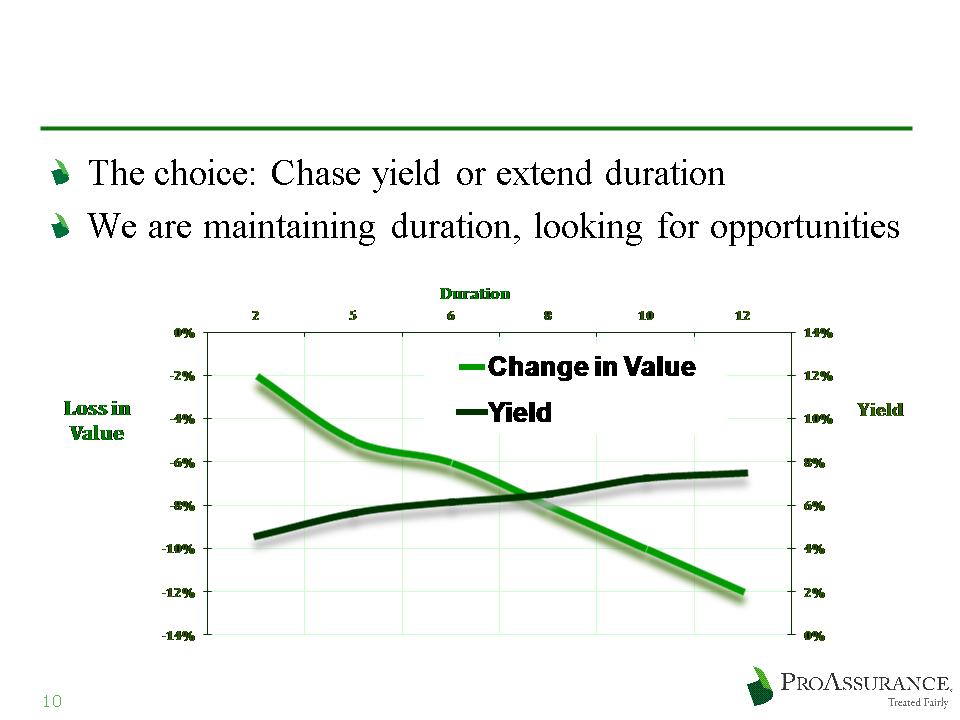

Responding to Low Interest Rates

Loss in value assuming a 100 basis point shift in the yield curve

Yields based on Single A composite corporate debt

11

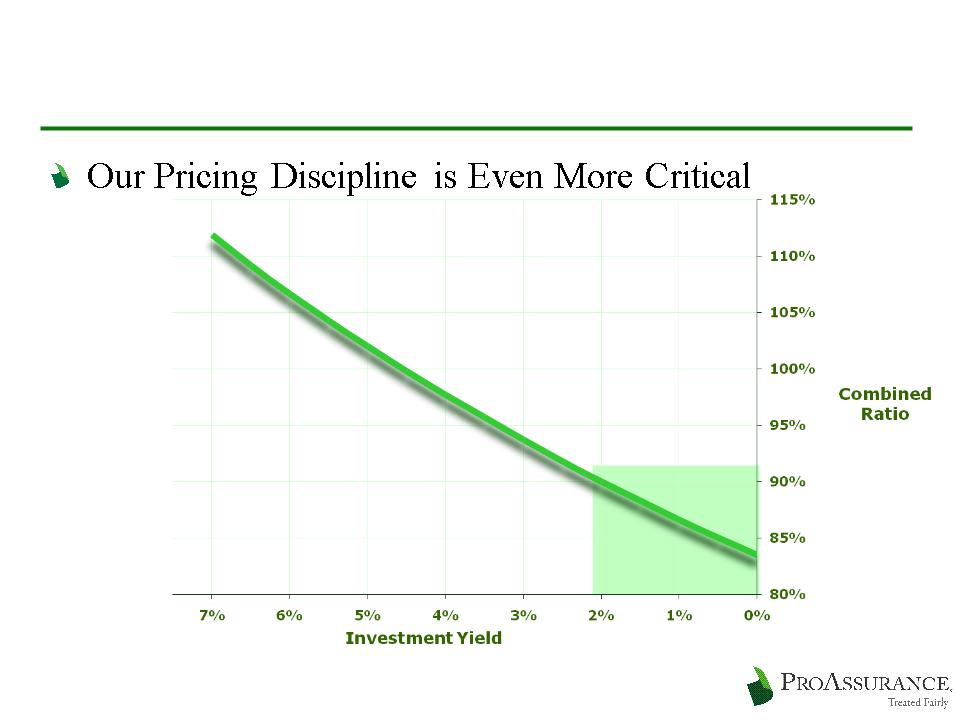

Responding to Low Interest Rates

Loss ratio required

to generate a 13%

after-tax ROE

to generate a 13%

after-tax ROE

Assumes a 1:1 premium to surplus ratio for physicians professional

liability claims-made coverages

liability claims-made coverages

(in millions)

Prepared for an

improving market

improving market

Prudent capital

management

management

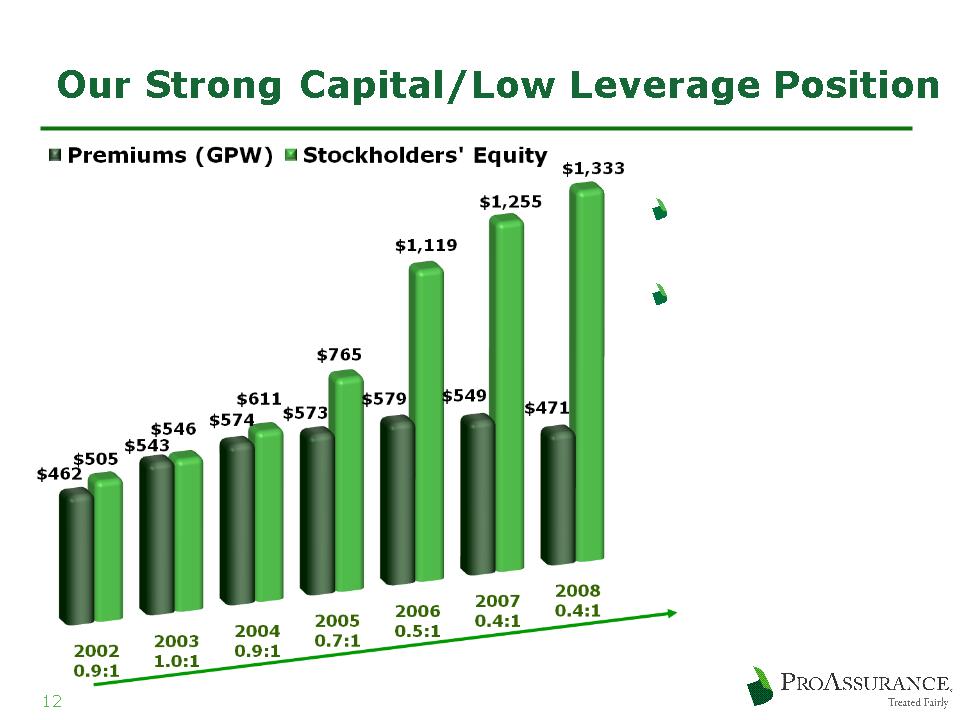

Premiums to Surplus

for Each year

for Each year

13

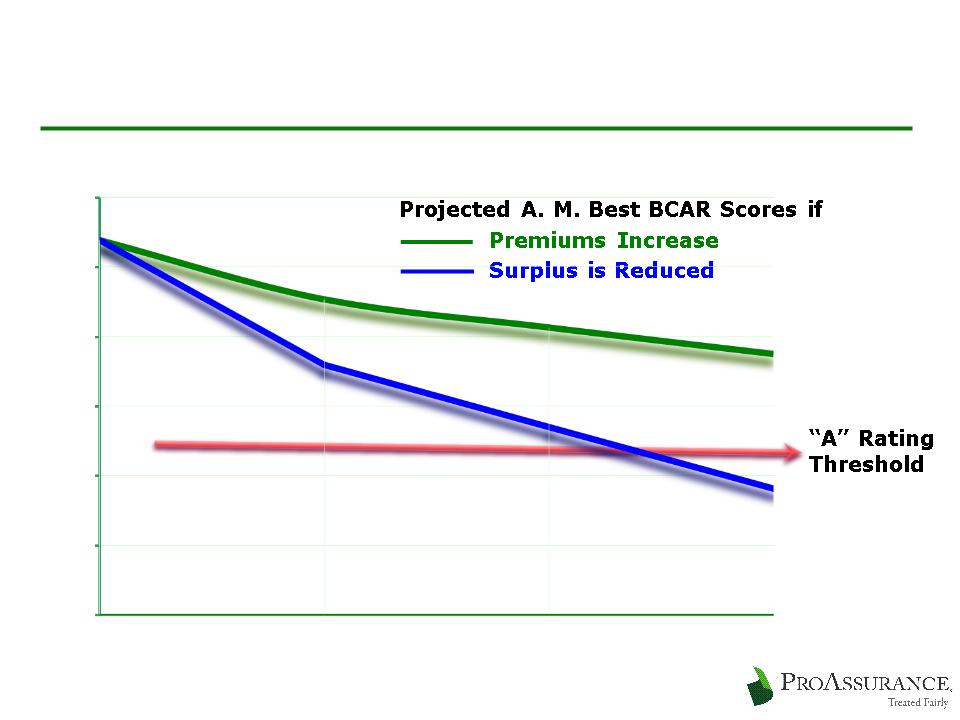

Excess Capital vs. Excess Capacity

14

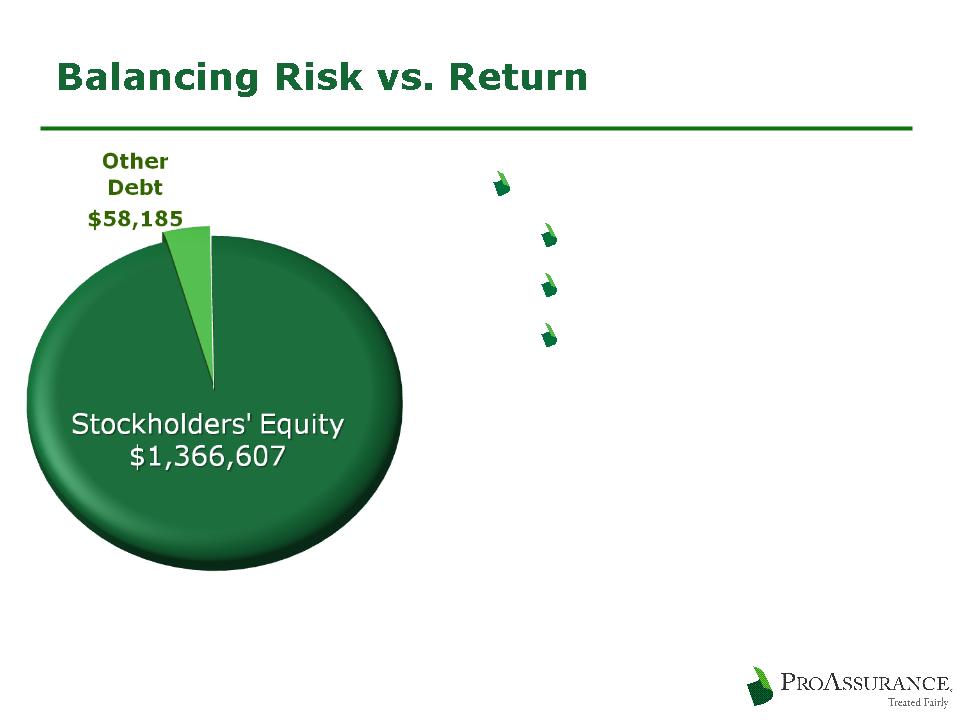

Little Dependence on Debt

Low Debt to Cap Ratio

Little strain on cash flow

Repurchased additional

$22 million of debt in Q4

$22 million of debt in Q4

12/31/2008

Balancing Risk vs. Return

15

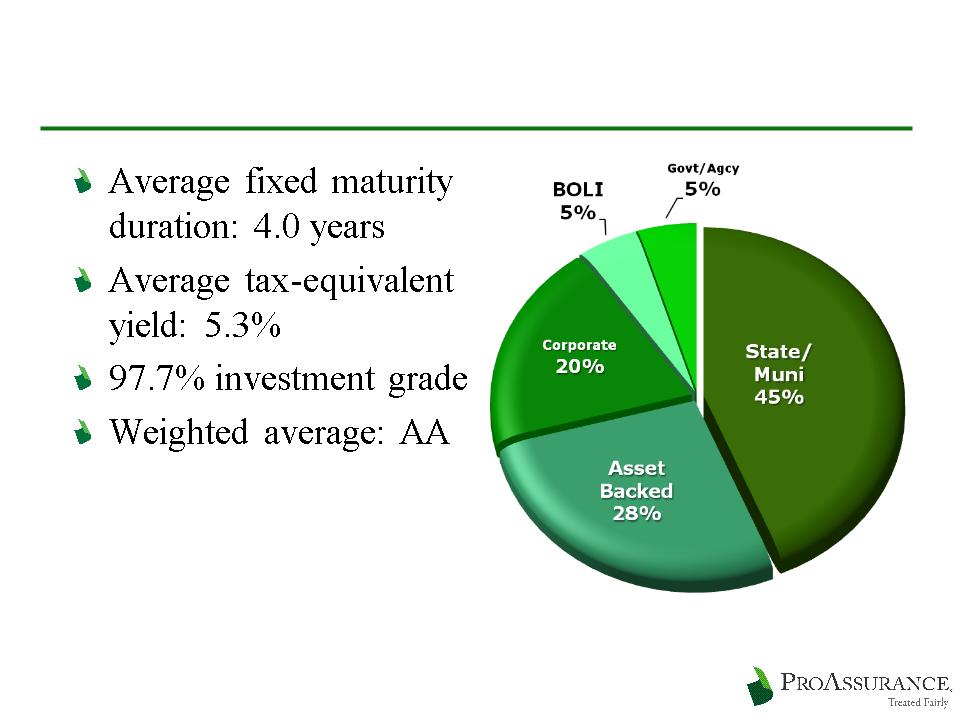

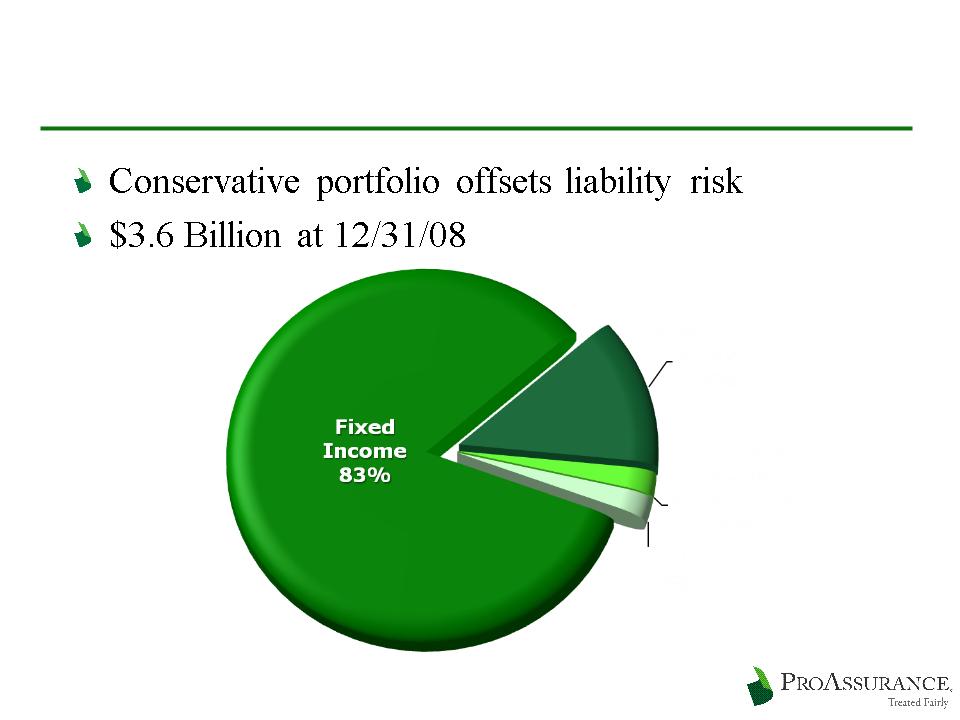

Our conservative investment

philosophy balances

risk and return

philosophy balances

risk and return

We are building cash and short-

term balances as we look to the

future

term balances as we look to the

future

Low equity allocation helps

mute the impact of the volatile

equity markets

mute the impact of the volatile

equity markets

$3.6 Billion

$3.6 Billion

Portfolio

Portfolio

Fixed Income:

83%

83%

Fixed Income:

83%

83%

Short

Term: 13%

Term: 13%

Short

Term: 13%

Term: 13%

Equity and Other

Investments: 2%

Investments: 2%

Equity and Other

Investments: 2%

Investments: 2%

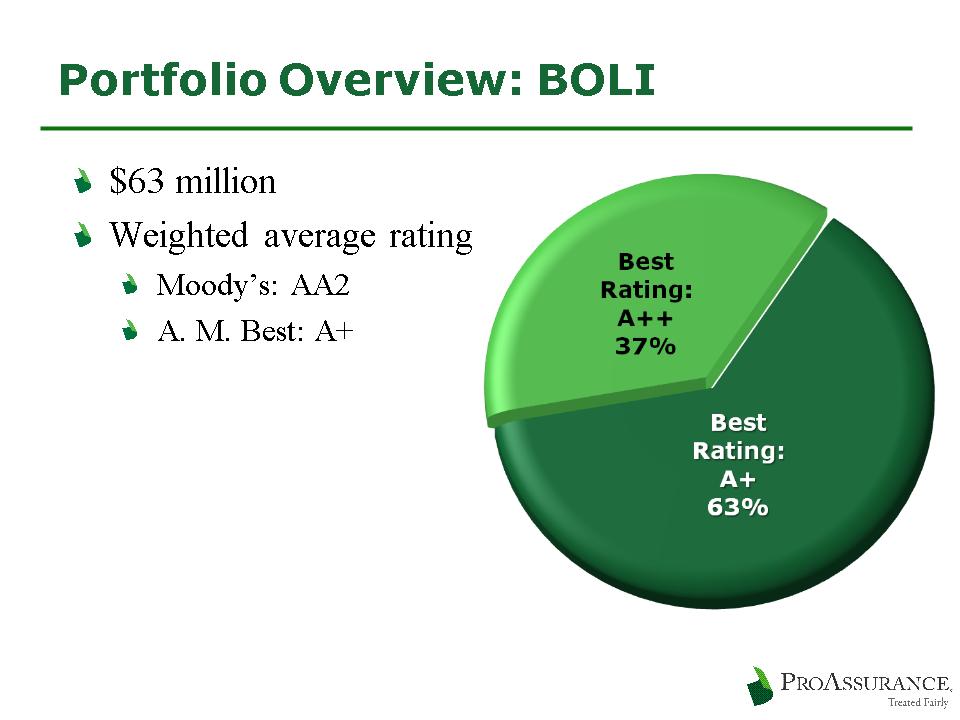

BOLI: 2%

BOLI: 2%

12/31/2008

16

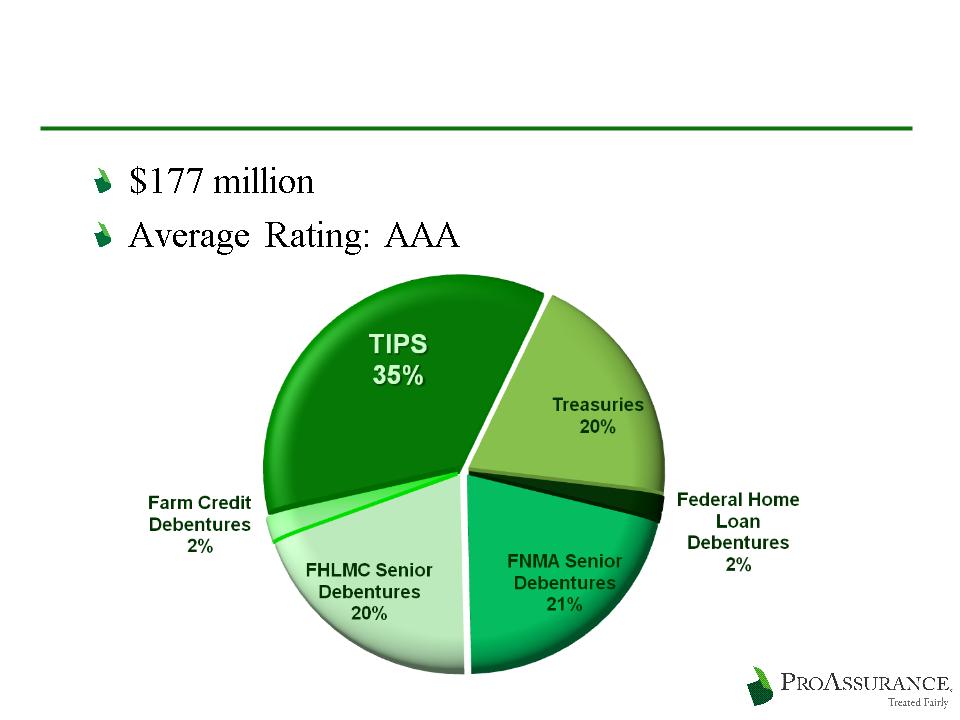

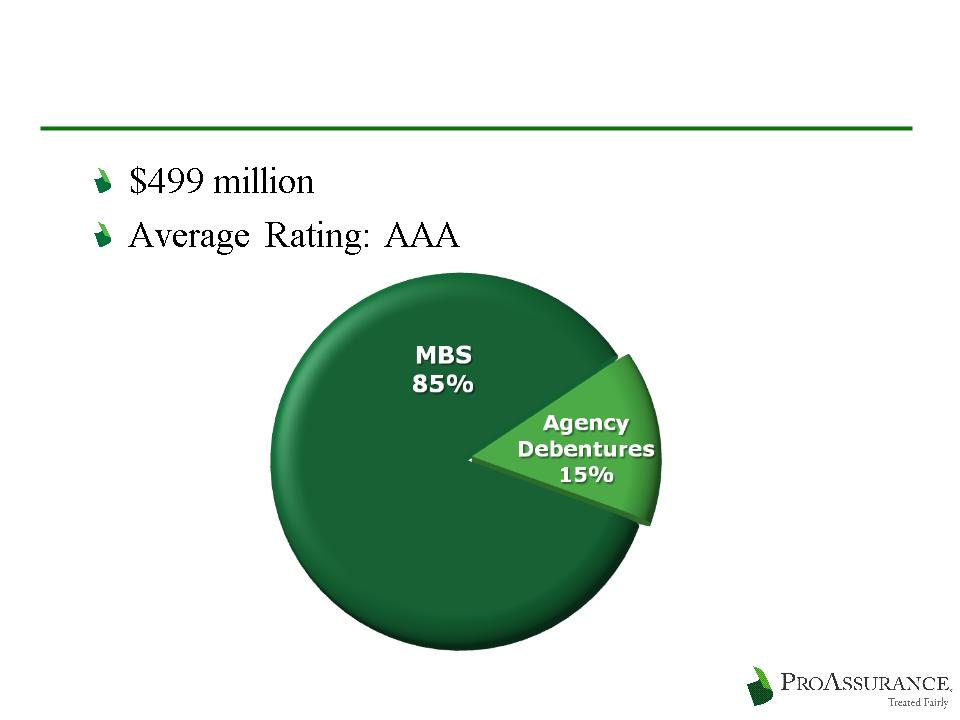

Fixed Income: $3.0 Billion

12/31/2008

19

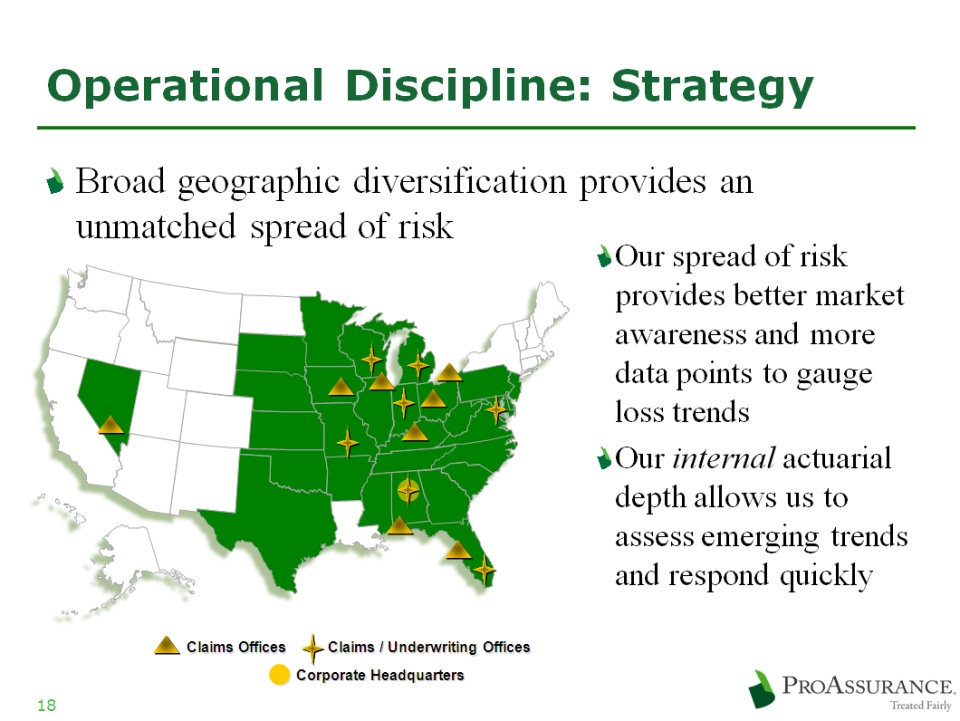

Operation Discipline: Claims

Our balance sheet strength and deep expertise

ensures our insureds have the option of an

uncompromising defense of their claim

ensures our insureds have the option of an

uncompromising defense of their claim

We defend our insureds at trial more often

than any other company in our line

than any other company in our line

Provides a long-term financial and marketing

advantage

advantage

A key differentiating factor in the market

as claims data becomes public

as claims data becomes public

20

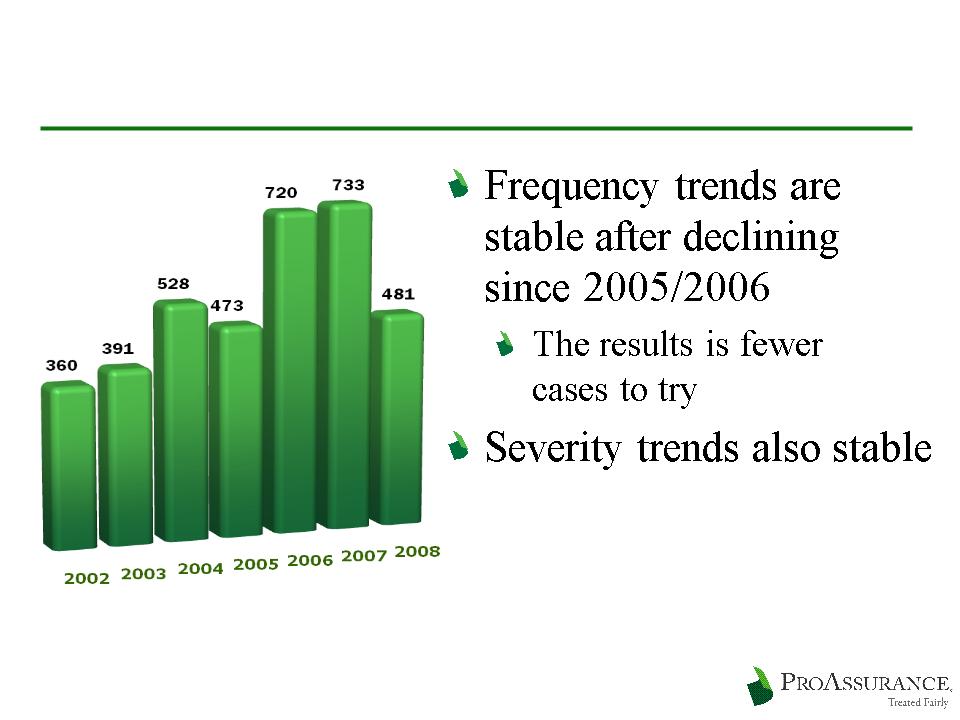

Claims Trends Remain Favorable

ProAssurance Claims Tried

21

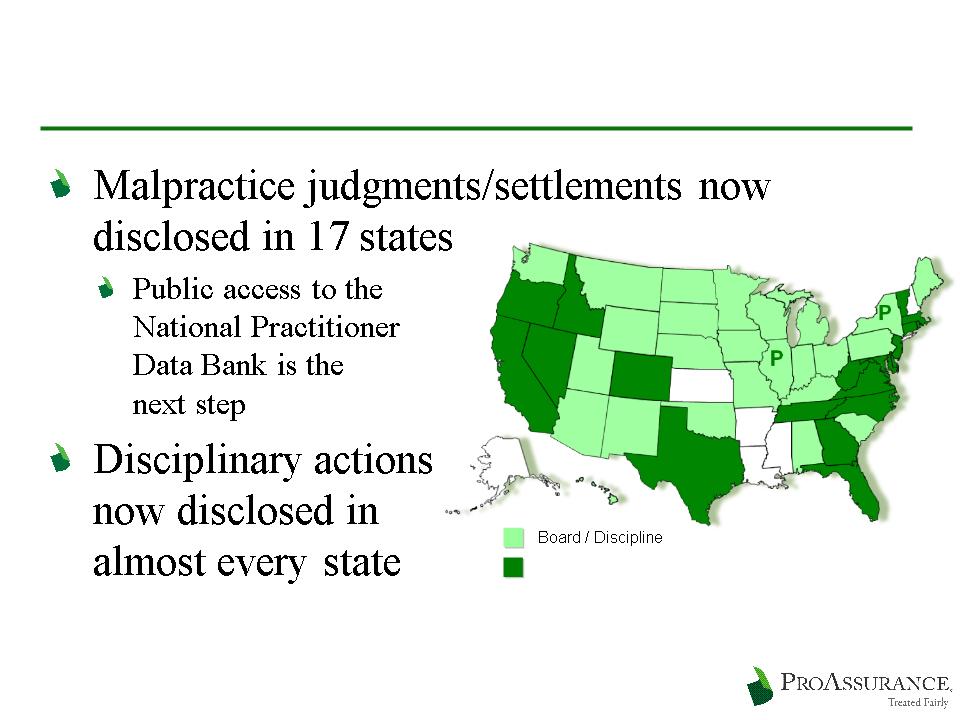

The Age of Transparency

Board / Discipline / Med Mal

Med Mal disclosure

legislation proposed

legislation proposed

P

22

Operational Discipline: Underwriting

Pricing Discipline

Rates on renewing business down less than 10%

from the peak of pricing in 2006

from the peak of pricing in 2006

Rates down 2% in 2007

Rates down 7% in 2008

Use of credits allows us to maintain existing

rate filings

rate filings

Pricing developed using multiple years

Not unduly influenced by current market

conditions

conditions

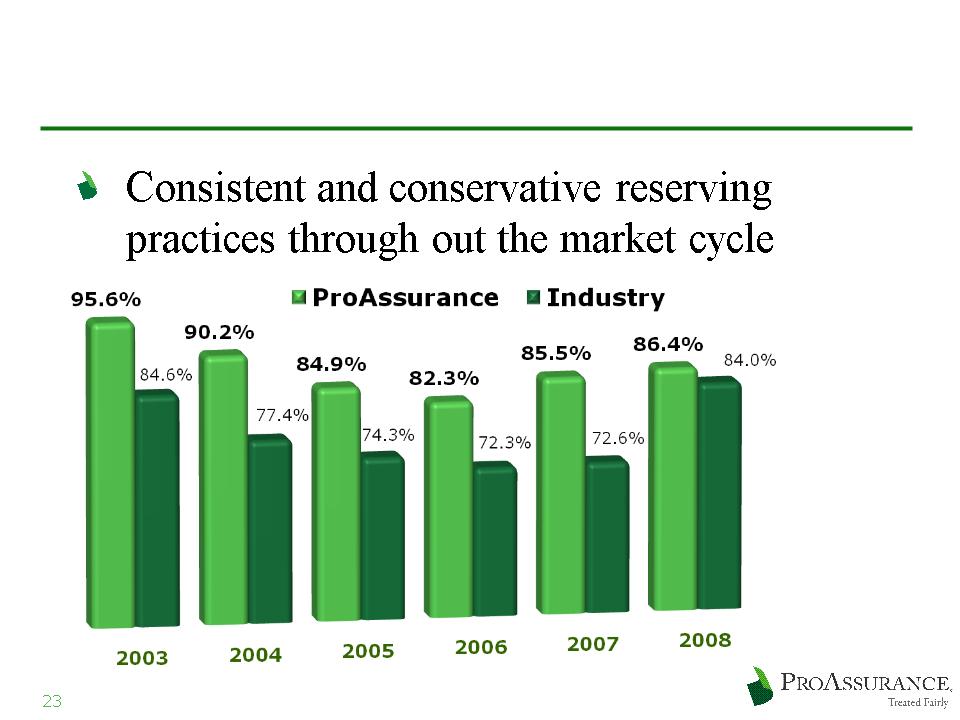

Operational Discipline: Actuarial

Initial Accident Year Loss Ratios

2008 Industry is

A. M. Best Data

Through Q3 2008

A. M. Best Data

Through Q3 2008

24

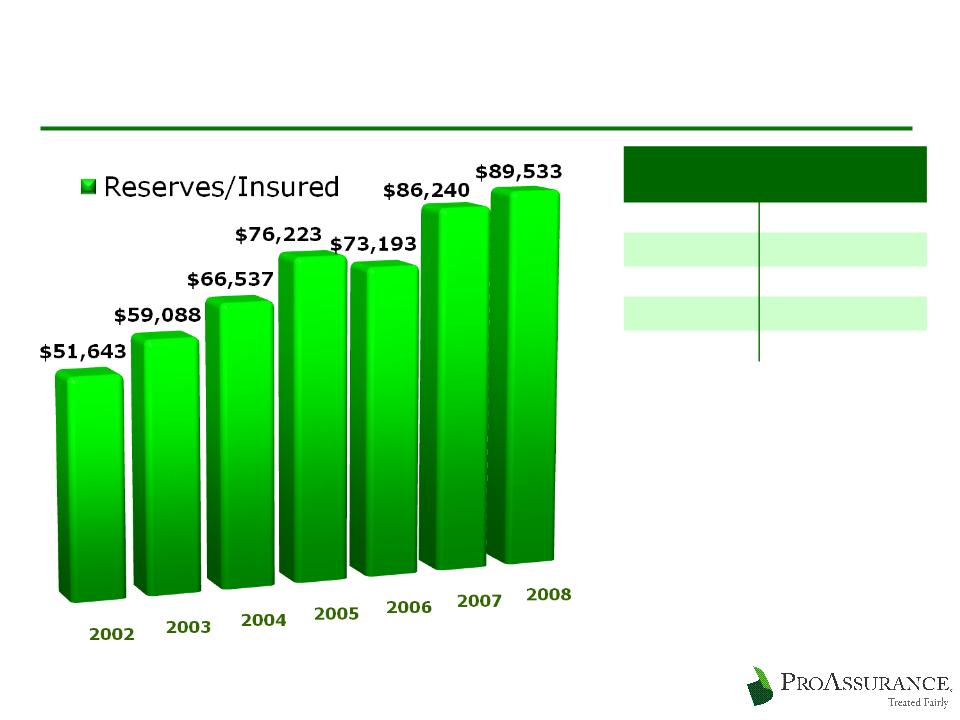

Operational Discipline: Actuarial

Reserve History

(billions)

(billions)

2008

$ 2.7

2007

$ 2.9

2006

$ 2.6

2005

$ 2.2

2004

$ 1.8

25

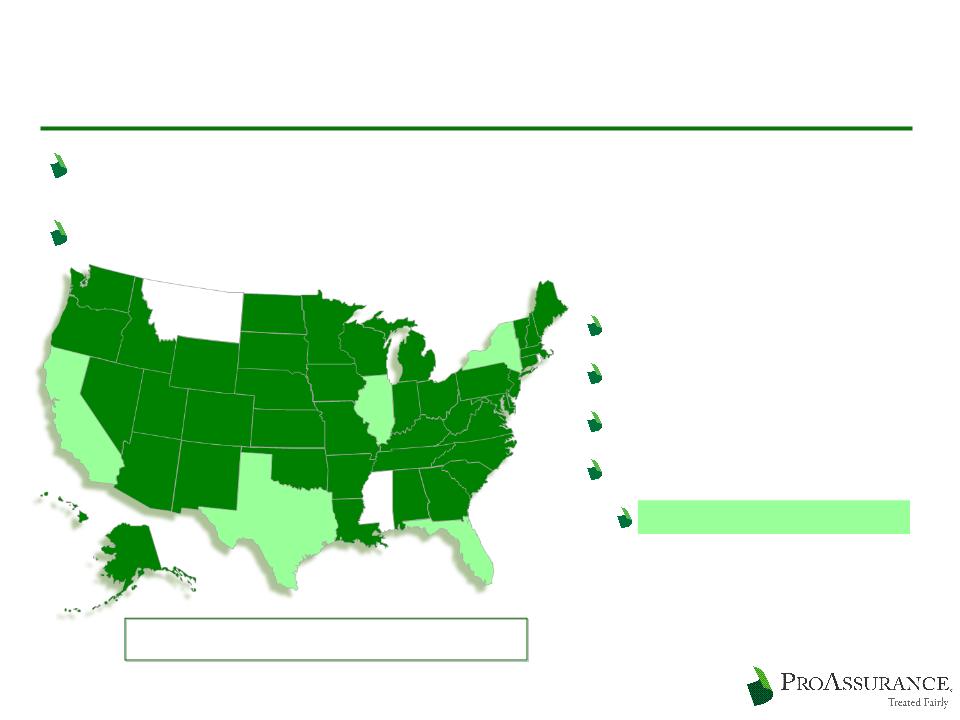

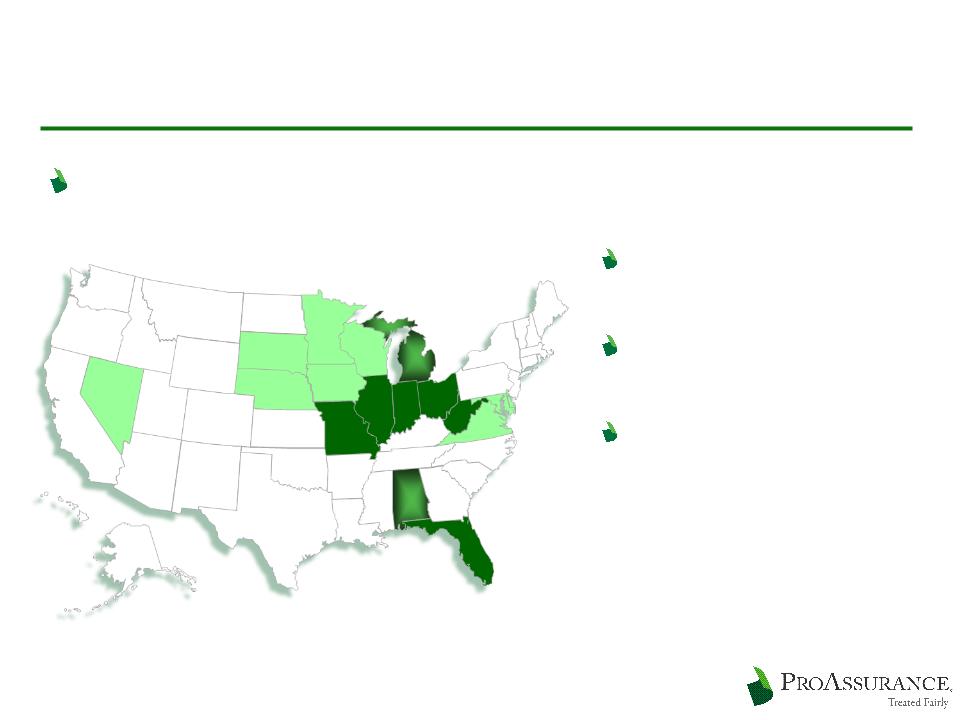

Growth Opportunities in 2009

We have announced three transactions that

diversify and add significant premium

diversify and add significant premium

We are incrementally expanding our footprint

Wyoming and South Carolina

Taking advantage of improving conditions in

selected markets within our footprint

selected markets within our footprint

26

New Transactions to Strengthen Us

The PICA Group

Leading insurer of podiatric physicians nationwide

National market share: approximately 70%

2008 Premiums: $97 million

Profitable

Well managed

Low integration risk

Joining PRA through a sponsored demutualization

27

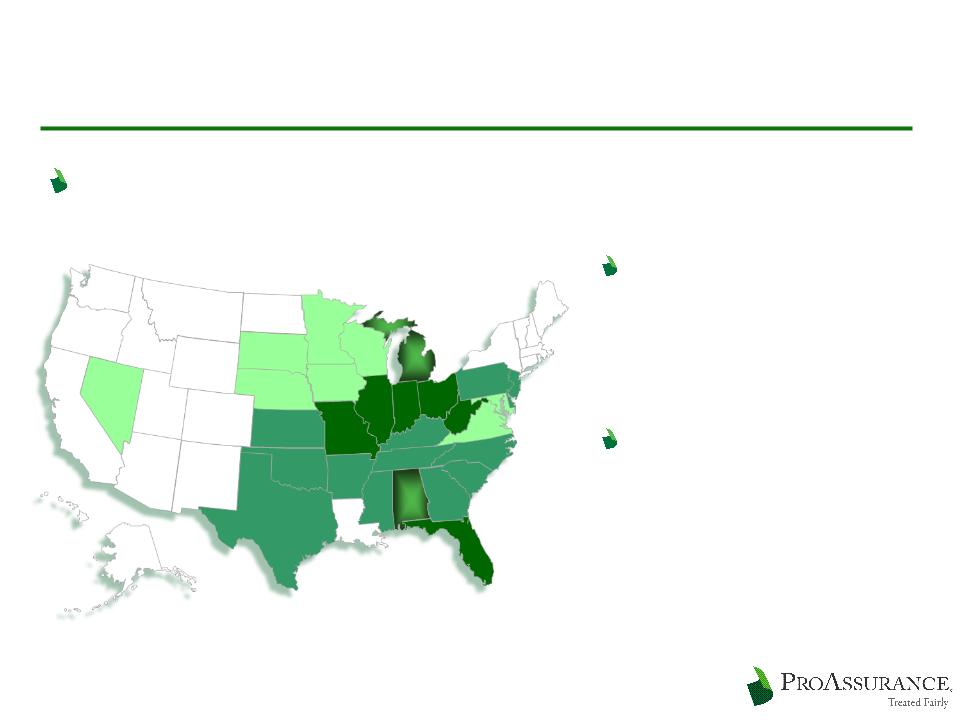

Adding the PICA Group

Expands our footprint nationwide

Adds ~16,600 insureds

9,800 DPMs

6,800 other providers

93% Direct

Largest States:

CA, FL, NY, IL, TX

PICA’s Business Profile

PICA’s Business Profile

11%

7%

9%

7%

8%

28

New Transactions to Strengthen Us

Mid-Continent General Agency

Growing market for ancillary healthcare

professional liability

professional liability

Produced $26 million of premium in 2008

Georgia Lawyers Insurance Company

A leading insurer of Georgia attorneys

2008 Premium: $5.7 million

Solidifies our presence in the legal professional

liability market

liability market

Both drive growth in key areas

Summary:

Successfully Executing a Proven,

Disciplined Strategy

Successfully Executing a Proven,

Disciplined Strategy

Summary:

Successfully Executing a Proven,

Disciplined Strategy

Successfully Executing a Proven,

Disciplined Strategy

30

The Promise of Treat Fairly

Treated Fairly is our brand enhancement initiative

Affirms our existing, enduring commitment to

every stakeholder

every stakeholder

Insureds

Agents

Investors

The public

We run our business as owners who are

rewarded for long-term success

rewarded for long-term success

31

ProAssurance

Concentrating on shareholder value

Growing Book Value per Share

Focused on the long-term

Maintaining leading market position

Protecting the balance sheet

Building strength for the next cycle turn

Evaluating all M & A opportunities

32

ProAssurance

Proven success throughout the cycles

Disciplined pricing and underwriting

Consistent reserving policy

Proven claims strategy

Balance sheet strength

Significant share ownership throughout the

company

company

Demonstrated commitment to a long-term

view of a complicated business

view of a complicated business

Appendix: Claims Data

Appendix: Claims Data

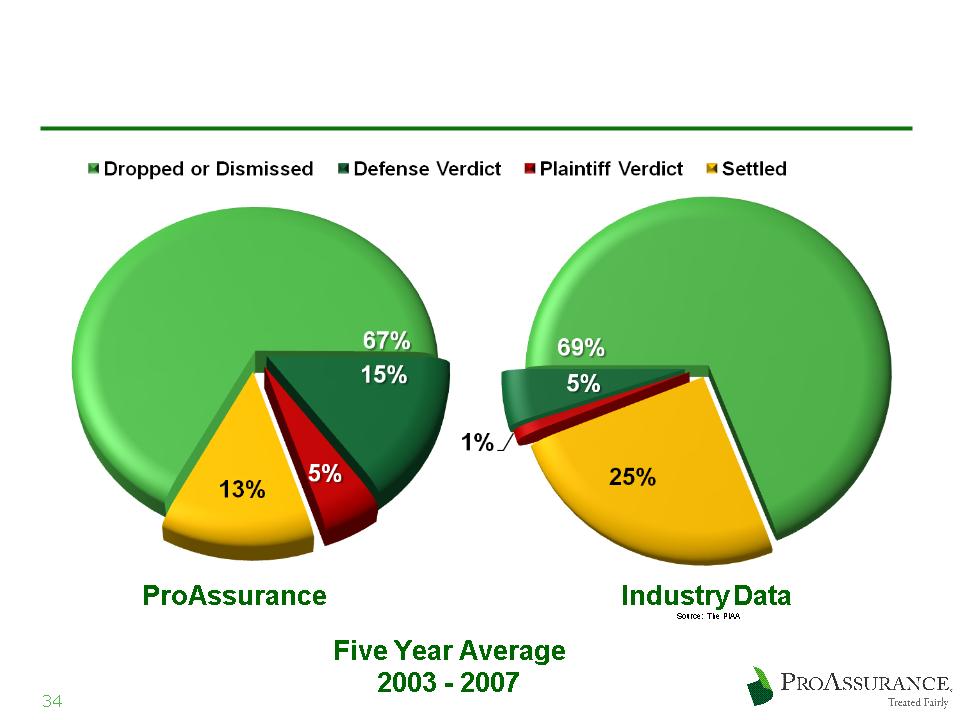

Why Claims Strategy Matters

Favorable

Outcomes:

82%

Outcomes:

82%

Favorable

Outcomes:

82%

Outcomes:

82%

Favorable

Outcomes:

74%

Outcomes:

74%

Favorable

Outcomes:

74%

Outcomes:

74%

Why Claims Strategy Matters

Our ability and willingness to defend claims

allows us to achieve better results

allows us to achieve better results

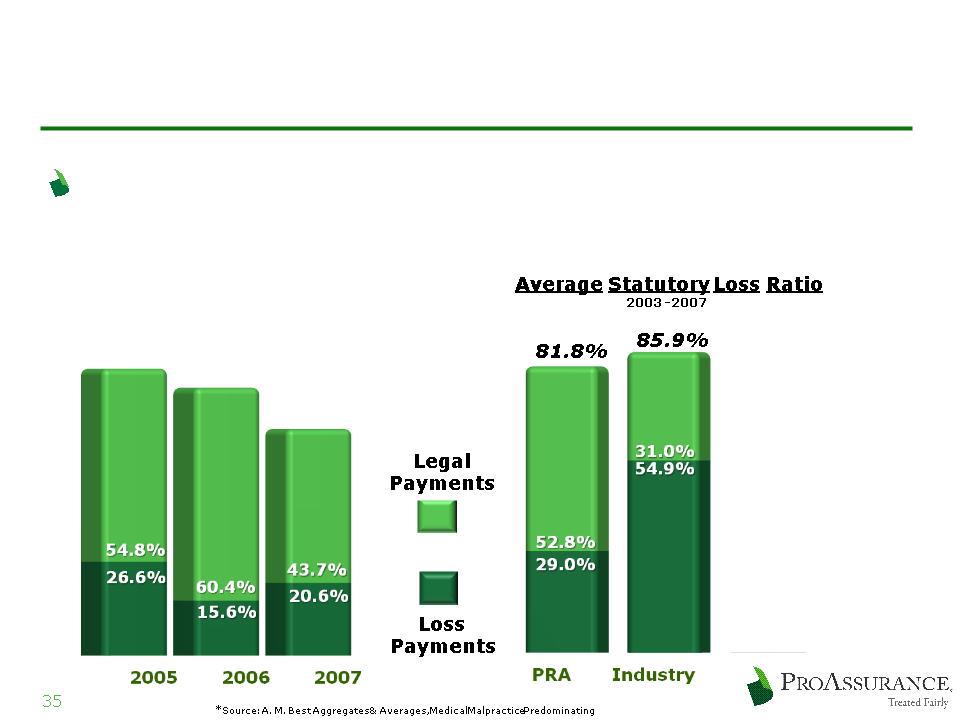

81.4%

ProAssurance Stand Alone

2005 - - 2007

76.0%

64.3%

Appendix: Investments

Appendix: Investments

37

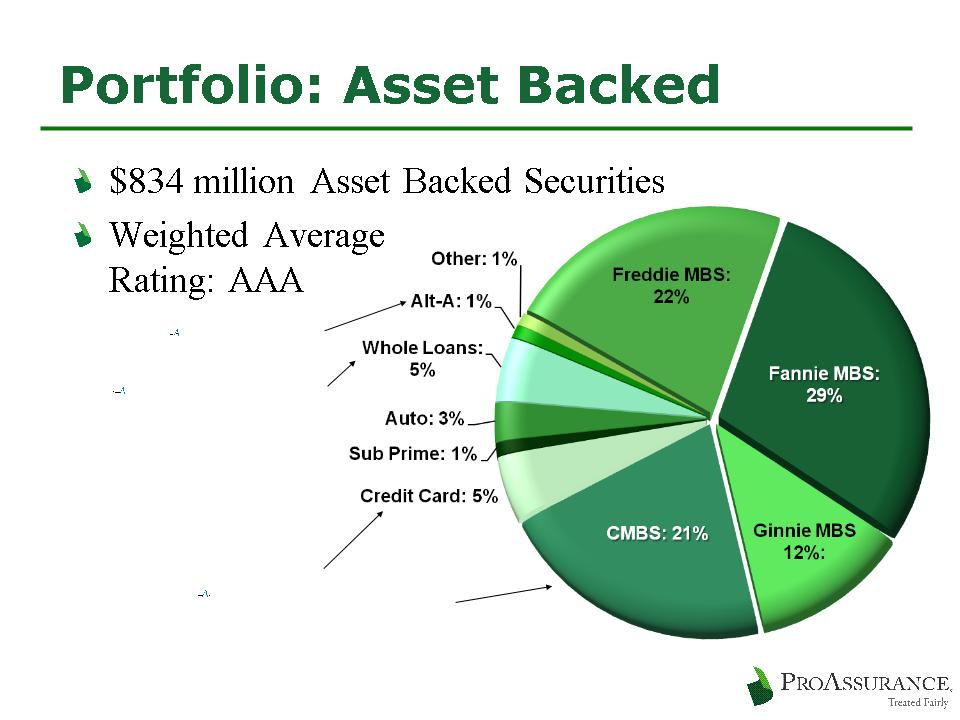

Portfolio Overview

12/31/2008

38

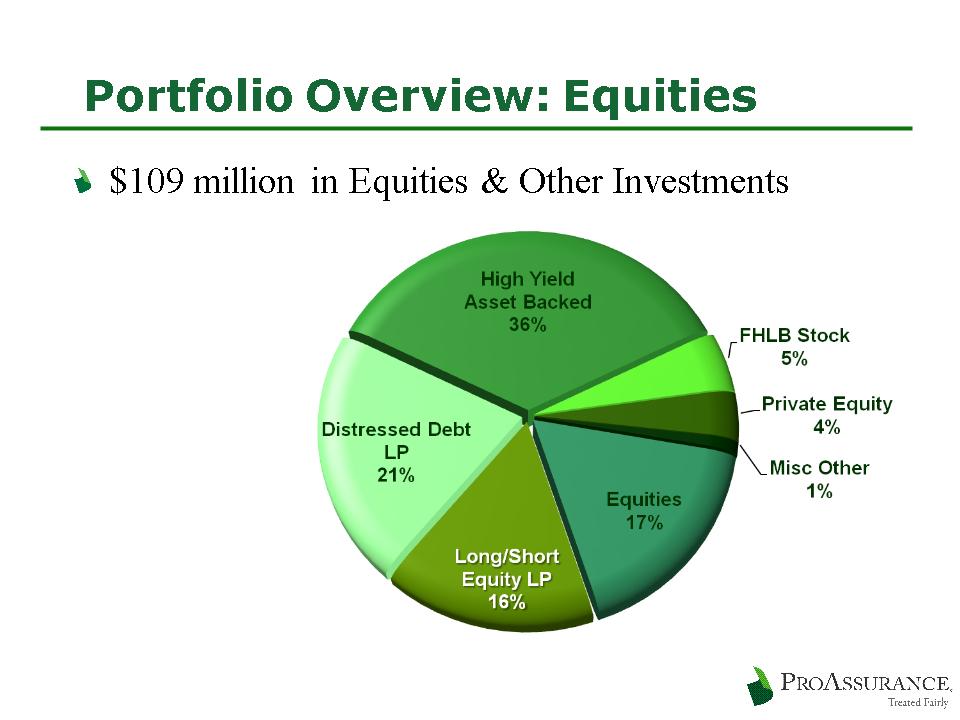

12/31/2008

Equities & Other Investments

$ in 000’s

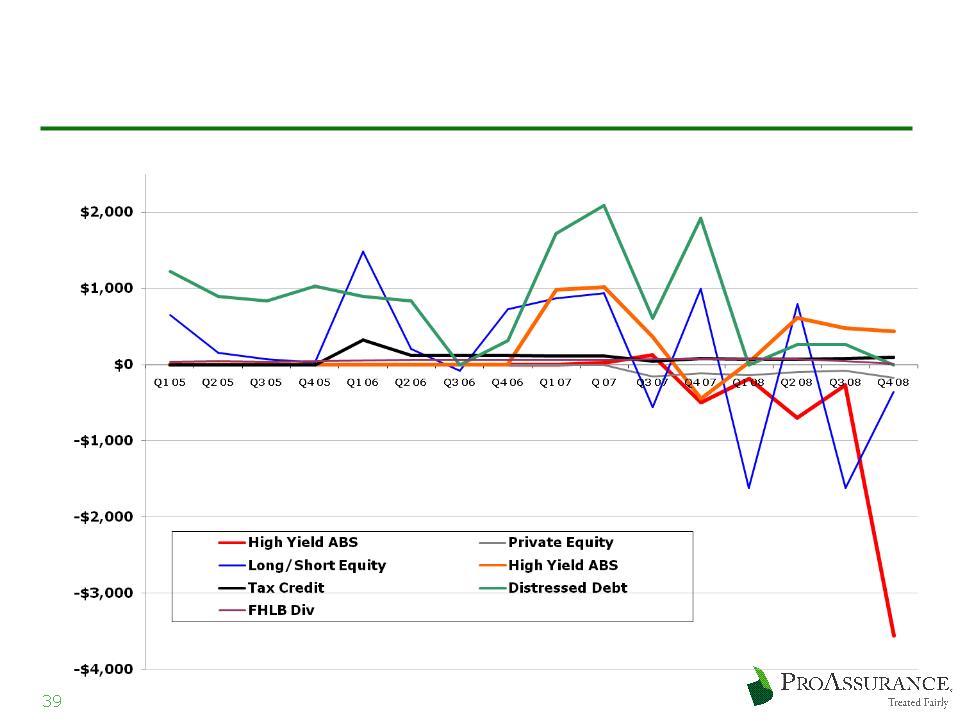

Performance Q1, 2005 - Q4, 2008

40

12/31/2008

41

Alt-A LTV: 62%

Whole Loan LTV: 57%

Further Details Provided on

Sub-Prime and CMBS on

following pages

Sub-Prime and CMBS on

following pages

Bloomberg Data

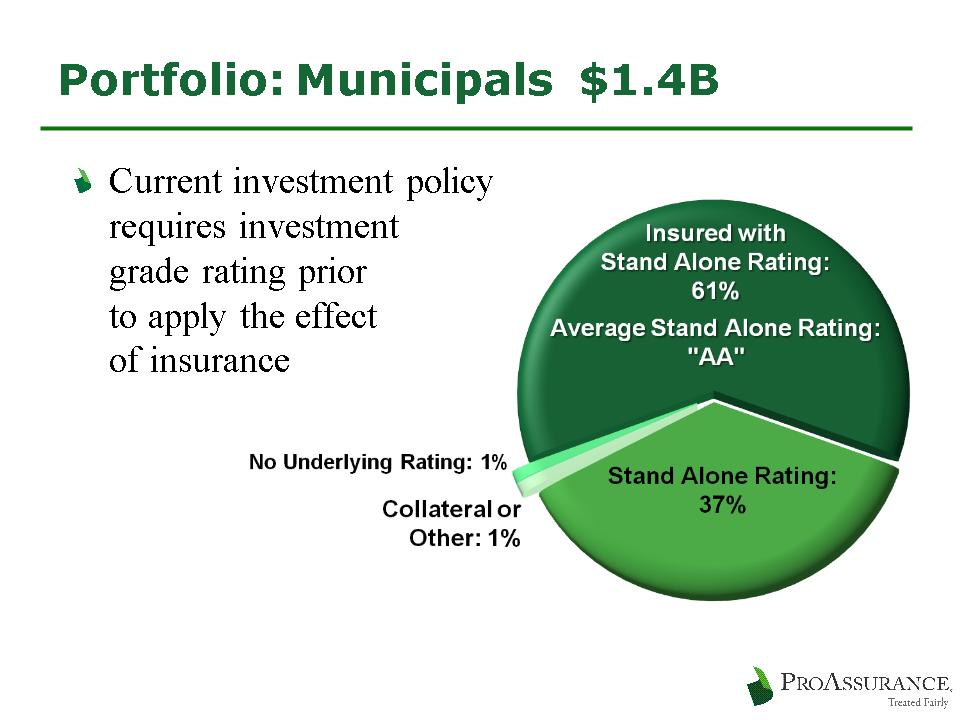

12/31/2008

12/31/2008

42

Portfolio Overview: Sub-Prime

$11.7 million market value in AFS portfolio

$2.5 million unrealized loss)

$5.0 million market value in high-yield LP

rated BB

rated BB

LP’s focus is distressed ABS)

At 12/31/08

Type

Quality

$6.9Mln

Mortgage-Backed

AA+ avg - LTV 72%

$4.7Mln

Home Equity

AA avg

At 12/31/08

Vintage

$6.2 Mln

2004 & Prior

$3.7 Mln

2005

Quality & Vintage information only on direct holdings

12/31/08

12/31/08

43

Portfolio Overview: CMBS

$171 million Fair Value in non-agency CMBS

Book Value: $194 Book Value

6% of fixed income portfolio

At 12/31/08

Quality

$169 Mln

AAA

$2 Mln

AA

At 12/31/08

Wtd Avg LTV

85%

<70%

15%

<72%

At 12/31/08

Credit Support

78%

>20%

7%

15% - 20%

12%

10% - 15%

3%

Less than 10%

At 12/31/08

Deal Cumulative Delinquencies

32%

None

36%

0% - 0.5%

16%

0.5% - - 1.0%

14%

1.0% - - 2.0%

2%

2.0% - - 2.6%

At 12/31/08

Debt Service Coverage

89%

>1.5x

11%

>1.2-1.5x

AT

12/31/2008

12/31/2008

44

12/31/2008

45

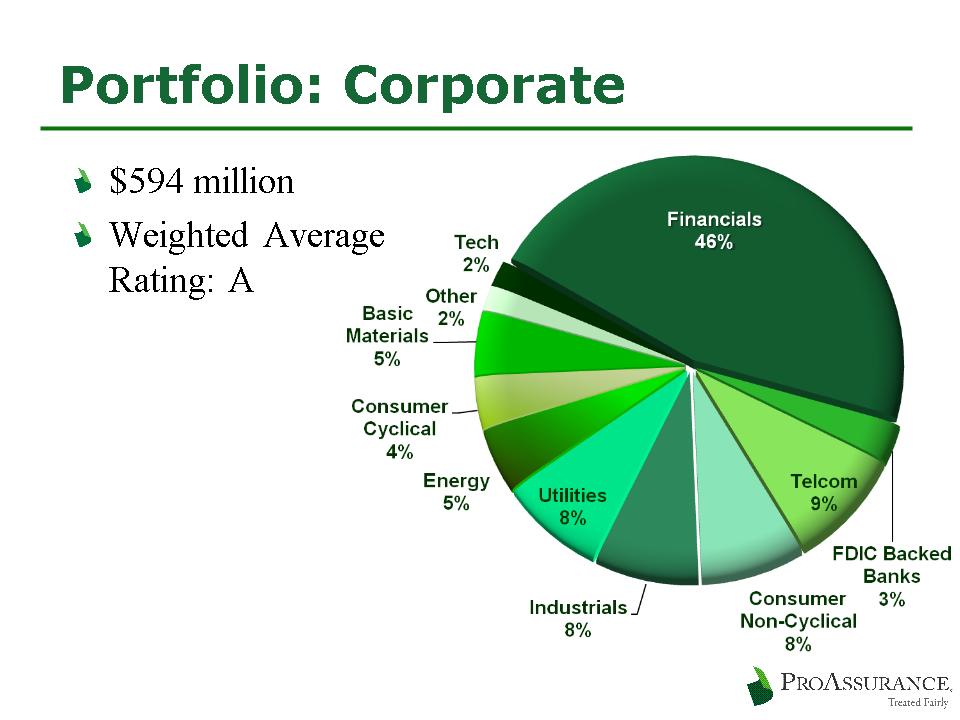

Portfolio: Corporate-Financials

Top 20 Largest Banks/Financials: $ 200 million

$17 mm FDIC

BoA/ML $27 ($1)

Credit Suisse $7

Wells/Wachovia $21

Depfa ACS $5

M Stanley $24 ($4)

DeutscheBk $5

JPM Chase $20 ($10)

BONY $5

GECC $13

Unilever Cap $4

Amer Exp $12

John Deere Cap $4

Citi $11

CIT $4

Goldman $9

Met Life $4

Hypotheken Essn $9

FMCC $4

NRUC $9

CAT Fin $3

FDIC backed listed in parentheses

12/31/2008

46

Portfolio: Treasury/GSE

12/31/2008

47

Portfolio: FRE and FNM

12/31/2008

48

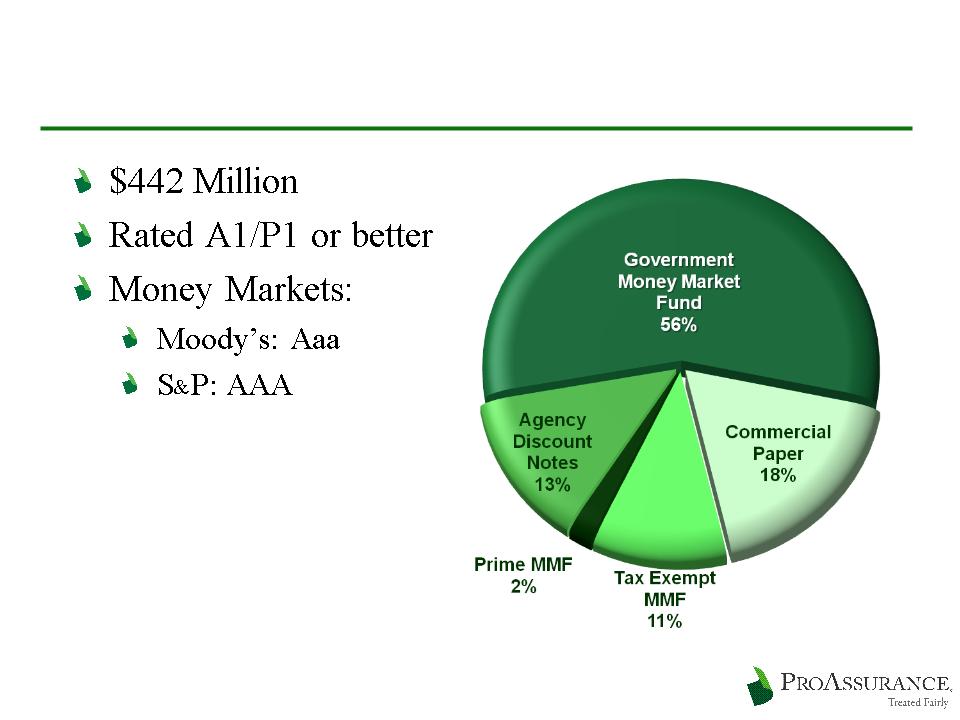

Portfolio Overview: Short Term

12/31/2008

49

12/31/2008

Appendix: Industry History

Appendix: Industry History

51

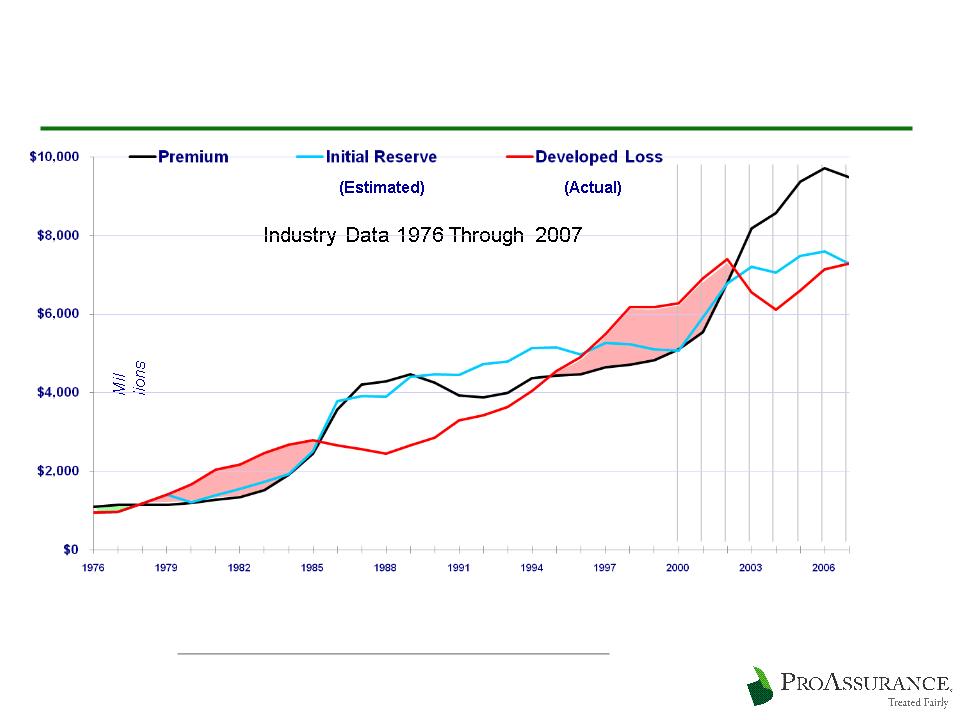

Will History Repeat Itself—Again?

Source: A. M. Best Aggregates and Averages 1976 - 2001

Medical Malpractice Industry, Net Basis Occurrence and Claims-Made Combined

Medical Malpractice Industry, Net Basis Occurrence and Claims-Made Combined

Appendix: M & A History

Appendix: M & A History

53

Profitable Growth Through M & A

ProAssurance has been built through M & A

ProAssurance was

formed by the

combination of two

successful companies

with a history of M & A

formed by the

combination of two

successful companies

with a history of M & A

54

Profitable Growth Through M & A

ProAssurance has been built through M & A

Each company brought

multiple transactions

into ProAssurance at

our founding in 2001

multiple transactions

into ProAssurance at

our founding in 2001

55

Profitable Growth Through M & A

ProAssurance has been built through M & A

We have continued to

grow through M & A

grow through M & A

NCRIC in the mid-

Atlantic

Atlantic

PIC-Wisconsin in the

upper Midwest

upper Midwest

56

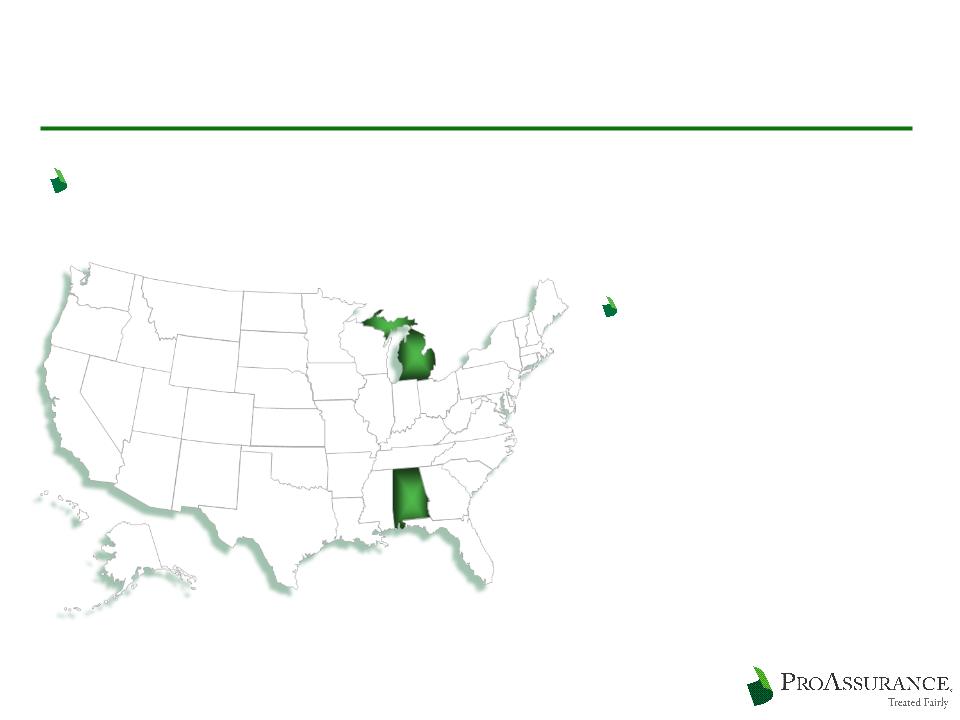

Denovo Growth Also Plays a Role

We have added states as opportunities arose

We carefully evaluate

the medical and legal

climate of each state

before entering

the medical and legal

climate of each state

before entering

We are the market

leaders in AL, DE, DC,

OH, & WI

leaders in AL, DE, DC,

OH, & WI