June 16, 2010

Frank B. O’Neil Investor Relations Officer |

Forward Looking Statements

This presentation contains Forward Looking Statements and other information designed

to convey our projections and expectations regarding future results. There are a number

of factors which could cause our actual results to vary materially from those projected in

this presentation. The principal risk factors that may cause these differences are

described in various documents we file with the Securities and Exchange Commission,

such as our current reports on Form 8-K, and our regular reports on Forms 10-Q and 10-

K, particularly in “Item 1A, Risk Factors.” Please review this presentation in

conjunction with a thorough reading and understanding of these risk factors.

to convey our projections and expectations regarding future results. There are a number

of factors which could cause our actual results to vary materially from those projected in

this presentation. The principal risk factors that may cause these differences are

described in various documents we file with the Securities and Exchange Commission,

such as our current reports on Form 8-K, and our regular reports on Forms 10-Q and 10-

K, particularly in “Item 1A, Risk Factors.” Please review this presentation in

conjunction with a thorough reading and understanding of these risk factors.

This presentation contains Non-GAAP measures, and we may reference

Non-GAAP measures in our remarks. A reconciliation of these measures to GAAP

measures is available in our latest quarterly news release, which is available in the

Investor Relations section of our website, www.ProAssurance.com, and in

the related Current Reports on Form 8K disclosing that release.

Non-GAAP measures in our remarks. A reconciliation of these measures to GAAP

measures is available in our latest quarterly news release, which is available in the

Investor Relations section of our website, www.ProAssurance.com, and in

the related Current Reports on Form 8K disclosing that release.

2

Non-GAAP Measures

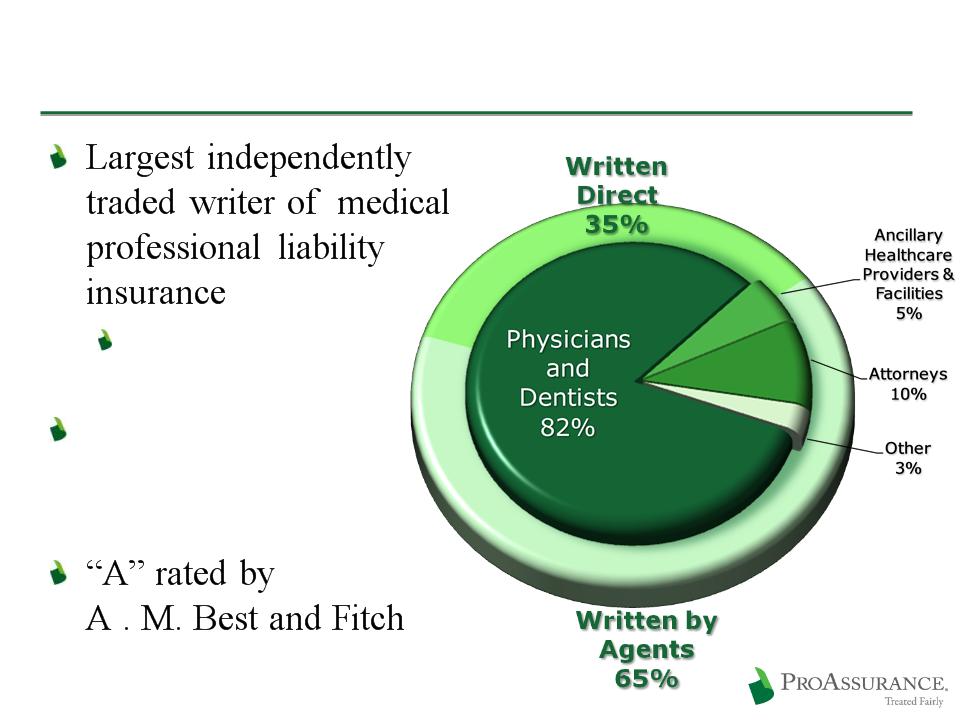

ProAssurance: Quick Facts

Fourth largest

overall writer

overall writer

Insuring 62,500

policyholders

nationwide

policyholders

nationwide

3

Effective & Experienced Management

4

W. Stancil Starnes, J.D. Chairman & Chief Executive Officer sstarnes@proassurance.com (205) 877-4400 Company Tenure: 3 Years Prior MPL Experience: 29 Years Industry & Related Experience: 32 Years Formerly in the private practice of law in MPL defense and complex corporate litigation. | Victor T. Adamo, J.D., CPCU President vadamo@proassurance.com (205) 877-4400 Company Tenure: 25 Years Prior MPL Experience: 5 Years Industry & Related Experience: 30 Years Formerly in the private practice of corporate law. | Jeffrey L. Bowlby, A.R.M. Sr. Vice-President & Chief Marketing Office jbowlby@proassurance.com (517) 347-6306 Company Tenure: 12 Years Prior MPL Experience: - Industry & Related Experience: 26 Years Career-long experience in insurance sales and marketing, most recently as SVP for Marketing with Meadowbrook. |

Howard H. Friedman, F.C.A.S. Sr. Vice-President & Chief Underwriting Officer hfriedman@proassurance.com (205) 802-4796 Company Tenure: 14 Years Prior MPL Experience: 16 Years Industry & Related Experience: 30 Years Career-long experience in MPL company operations and management. Former ProAssurance CFO. | Jeffrey P. Lisenby, J.D. Sr. Vice-President, General Counsel & Secretary jlisenby@proassurance.com (205) 445-2668 Company Tenure: 9 Years Prior MPL Experience: - Industry & Related Experience: 9 Years Formerly in the private practice of law. | Frank B. O’Neil Sr. Vice-President & Chief Communications Officer foneil@proassurance.com (205) 877-4461 Company Tenure: 23 Years Prior MPL Experience: - Industry & Related Experience: 23 Years Formerly a television news executive and anchor. |

Edward L. Rand, Jr., CPA Sr. Vice-President & Chief Financial Officer erand@proassurance.com (205) 802-4718 Company Tenure: 6 Years Prior MPL Experience: - Industry & Related Experience: 18 Years Career-long experience in insurance finance and accounting. Most recently Chief Accounting Officer for Partner Re. | Darryl K. Thomas, J.D. Sr. Vice-President & Chief Claims Officer dthomas@proassurance.com (205) 445-2668 Company Tenure: 12 Years Prior MPL Experience: 10 Years Industry & Related Experience: 22 Years Career-long experience in MPL claims management. | Hayes V. Whiteside, M.D. Sr. Vice-President & Chief Medical Officer hwhiteside@proassurance.com (205) 445-2670 Company Tenure: 6 Years MPL Experience: - Industry & Related Experience: 27 Years Formerly in the private practice of Urology. |

Average executive tenure through VP level is 16 years

Recognition and Rating Highlights

Third straight year as one of the

50 top performing property casualty

insurance companies

50 top performing property casualty

insurance companies

Top 3% of all P&C companies

Affirmed at “A” (Excellent)

by A. M. Best

by A. M. Best

Positive Outlook

by S & P

by S & P

5

Recent Business Highlights

Maintaining our profitability and book value growth

GROWING the top line

Three M&A transactions completed in 2009 -

Provided approximately $100 million in annualized

premium growth

Provided approximately $100 million in annualized

premium growth

Existing markets grew modestly in 2009

Outstanding performance in a challenging

financial market and a demanding line of

insurance

financial market and a demanding line of

insurance

6

How We Define Success

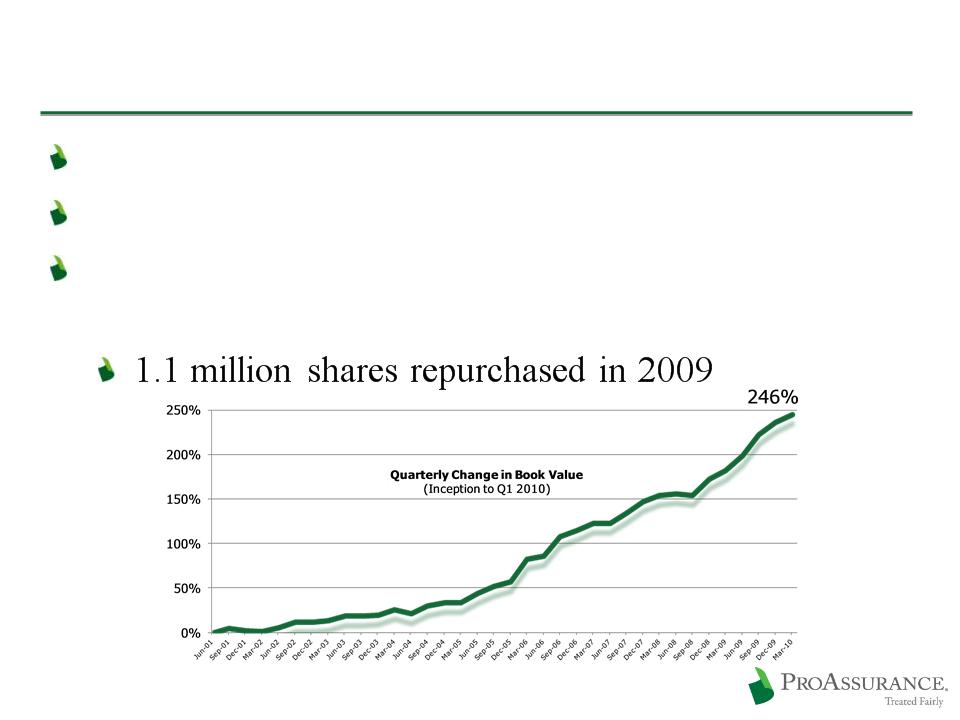

23% Increase in Book Value per Share in 2009

19% Increase in Revenue vs. 2008

28% Increase in Diluted EPS

Top Line Growth in 2009

$28 million of new business in our historical book

Outstanding performance in a challenging

financial market and a demanding line of

insurance

financial market and a demanding line of

insurance

7

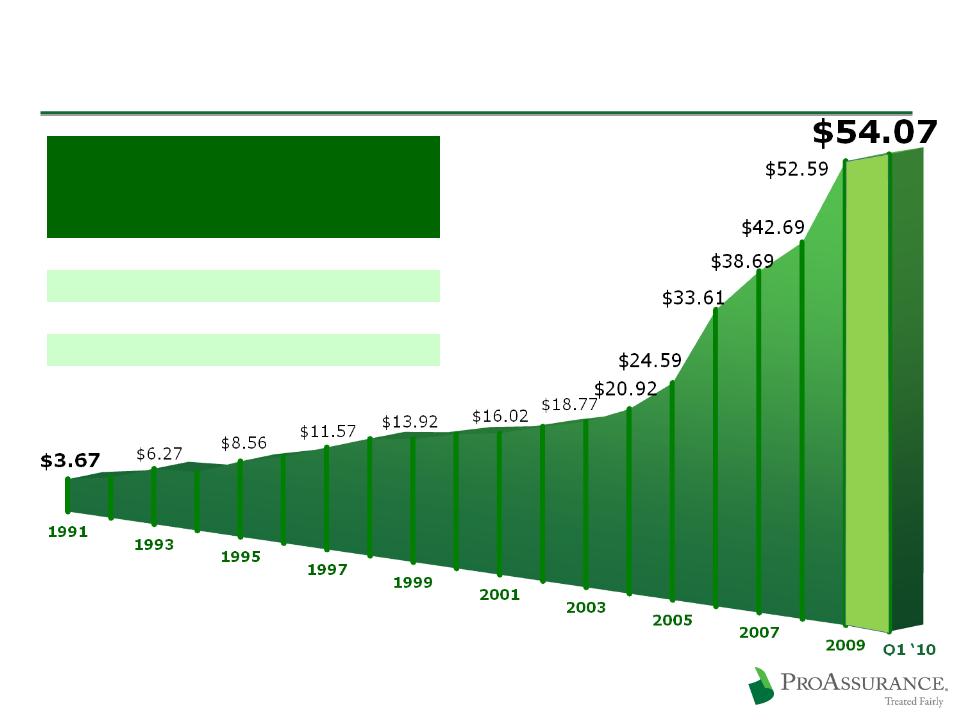

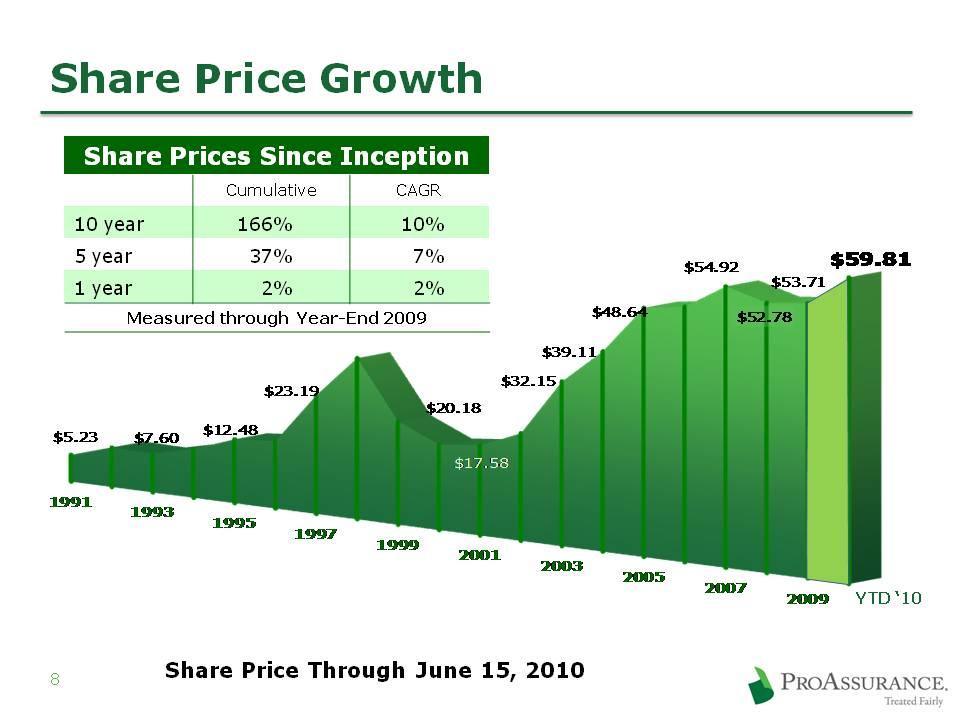

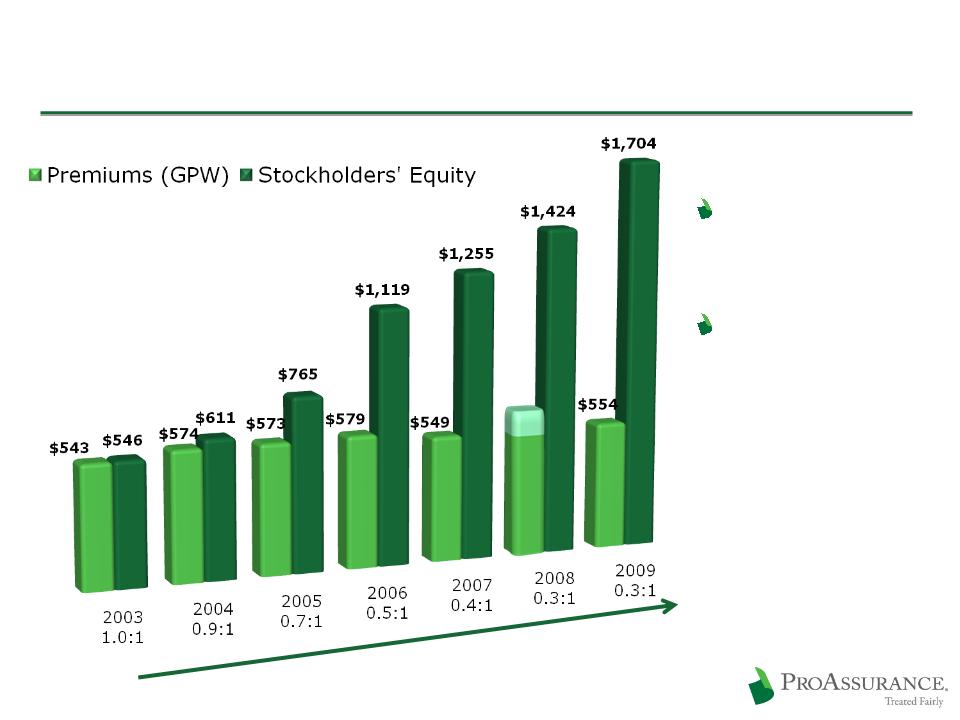

Book Value Growth Through Q1 2010

Book Value Growth EVERY Year Since Inception | ||

Cumulative | CAGR | |

10 year | 278% | 14% |

5 year | 151% | 20% |

1 year | 23% | 23% |

Measured through Year-End 2009 | ||

8

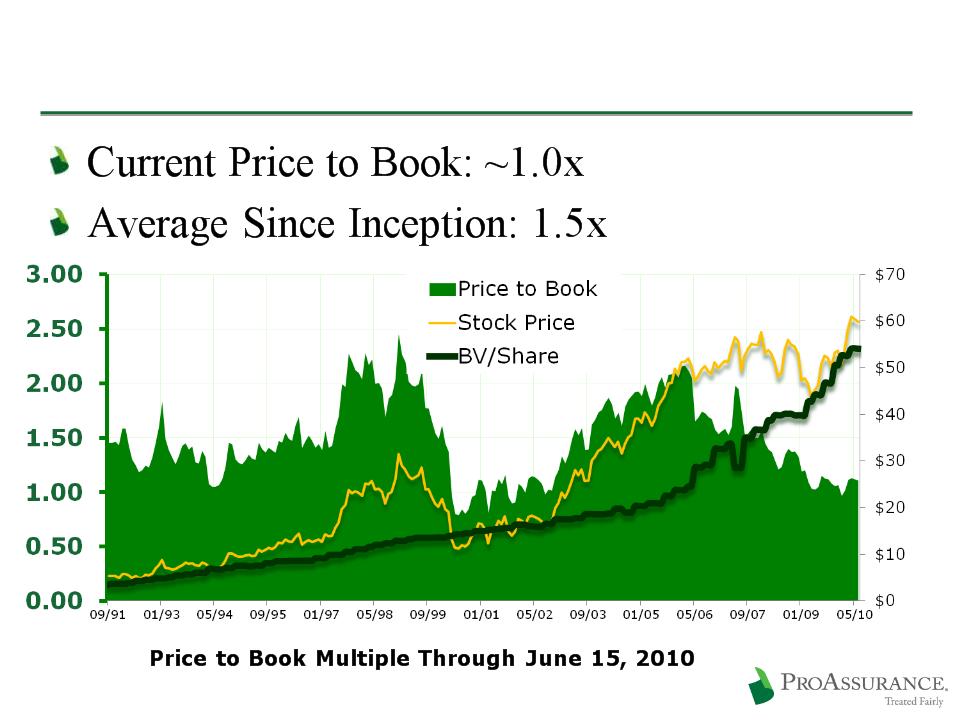

Book Value per Share

Trading Below Historic BV Multiple

10

Key Advantages

Enduring Financial Strength

12

Emphasizing an appropriate balance of risk vs. return

Committed to enduring balance sheet strength

Responding to the low interest rate environment

Stockholder’s Equity Up

Over >16% Since

12/31/07

Over >16% Since

12/31/07

Investments Balance Risk vs. Return

Key Investment Actions in Q1 10

Further reduction of cash and short-

term balances

term balances

Added to corporate bond holdings

CUSIP-level portfolio disclosure

on our website:

www.proassurance.com/investorrelations/supplemental.aspx

on our website:

www.proassurance.com/investorrelations/supplemental.aspx

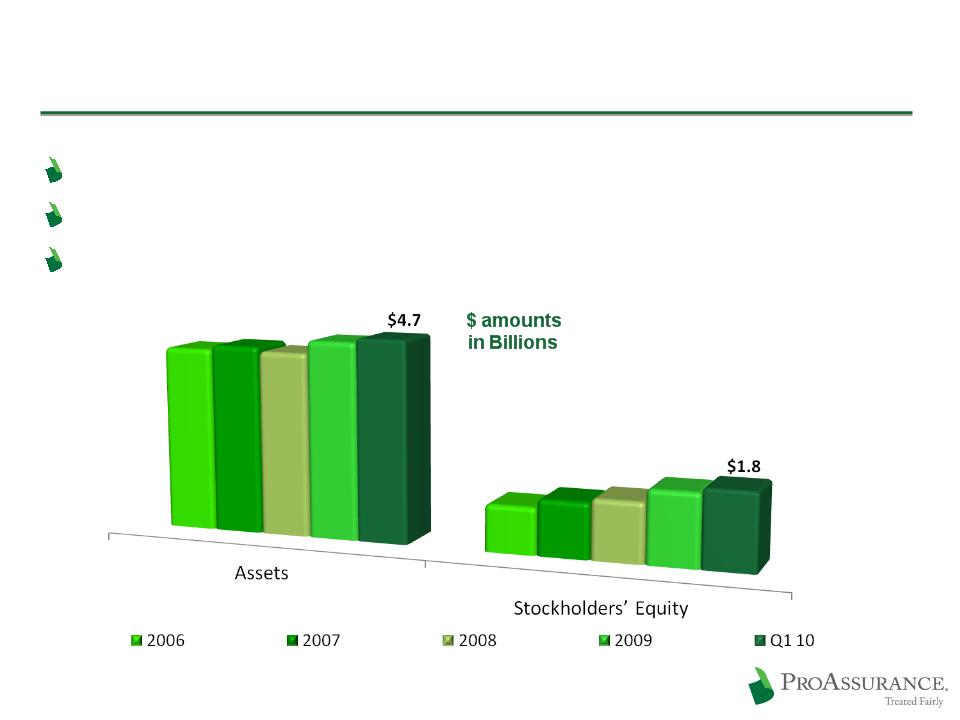

$3.9 Billion

Portfolio

Portfolio

$3.9 Billion

Portfolio

Portfolio

Fixed Income: 90%

Short Term: 4%

Short Term: 4%

Equity and Other Investments: 4%

Equity and Other Investments: 4%

BOLI: 2%

BOLI: 2%

13

3/31/10

Using capital to build through M&A

Preserving capital for future opportunities

Enhancing shareholder value by repurchasing shares

at prices that build Book Value

at prices that build Book Value

Capital Management

15

Source: SNL Financial

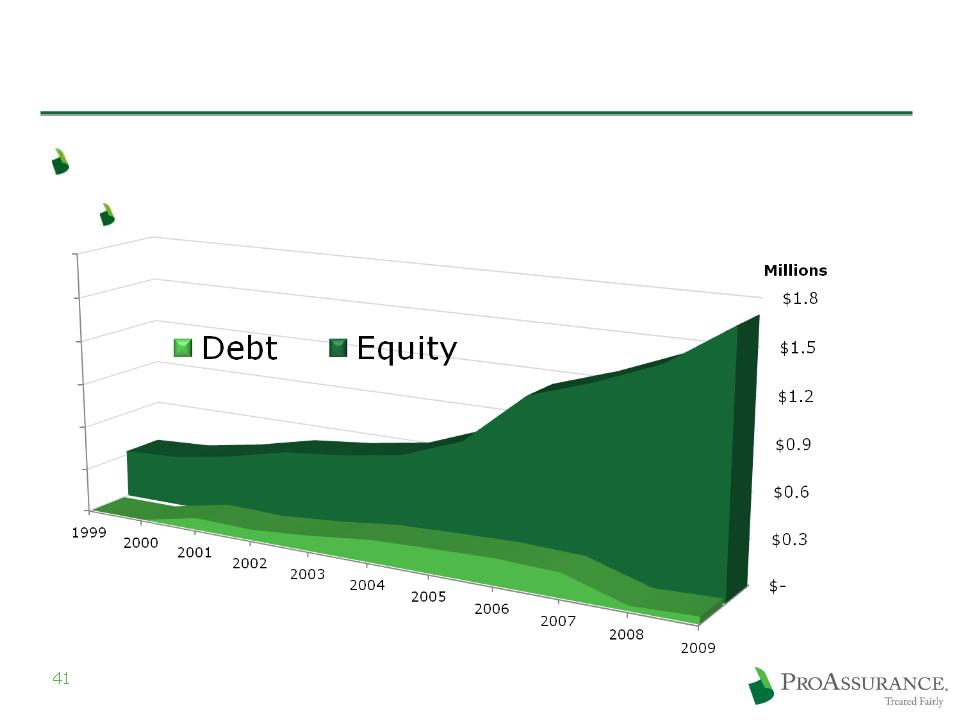

Our Strong Capital/Low Leverage Position

16

(in millions)

Prepared for an

improving market

improving market

Prudent capital

management

management

Premiums to Surplus

for Each year

for Each year

$567

$ 96

$471

($96 mil PICA pro forma in 2008)

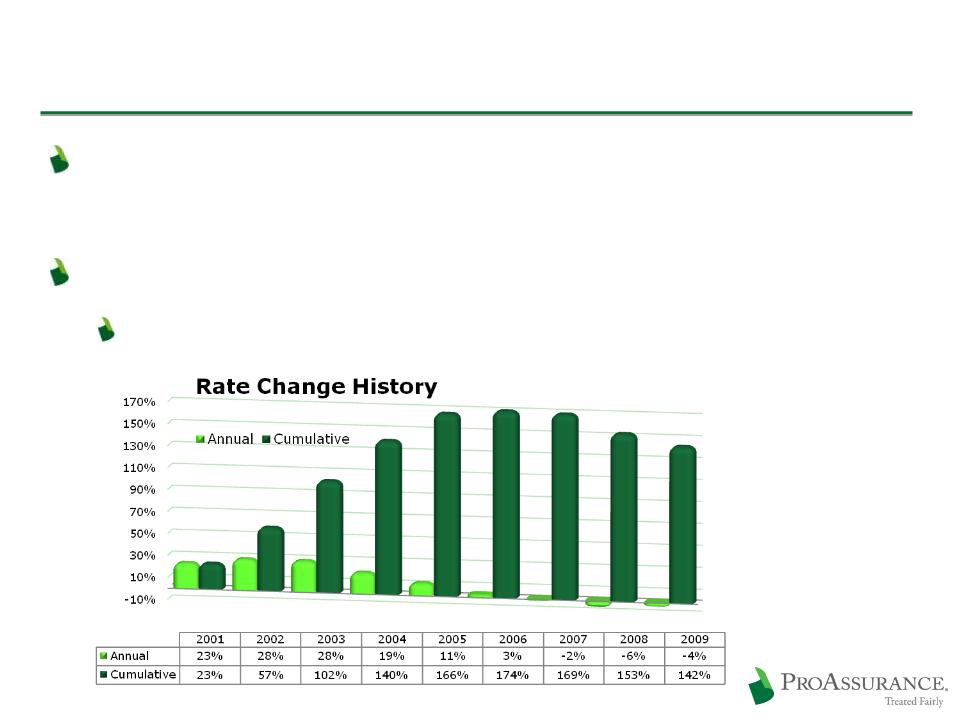

Maintain Profitability Through the Cycle

Ensure pricing discipline

Rates based on loss data across multiple years

Not unduly influenced by current market

conditions

conditions

Using credits allows us to maintain existing

rate filings

rate filings

17

Rate Discussion

Rates on renewing physician business down

less than 12% from peak pricing in 2006

less than 12% from peak pricing in 2006

Recent rate filings are really minor adjustments

Slight increases in Arkansas, Illinois and Indiana

18

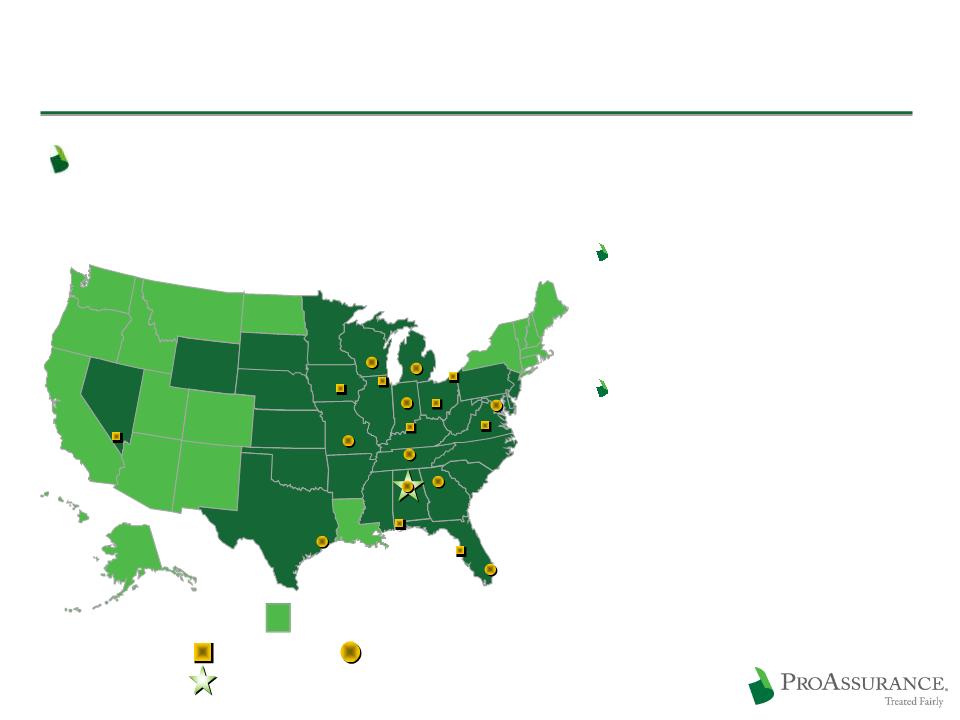

Spread Risk

Broad geographic diversification provides an

unmatched spread of risk

unmatched spread of risk

19

Our spread of risk provides

better market awareness and

more data points to gauge

loss trends

better market awareness and

more data points to gauge

loss trends

Our internal actuarial depth

allows us to assess emerging

trends and respond quickly

allows us to assess emerging

trends and respond quickly

Corporate Headquarters

Corporate Headquarters

Claims Offices

Claims Offices

Claims / Underwriting Offices

Claims / Underwriting Offices

PICA and/or E&S States

PICA and/or E&S States

(Birmingham)

Differentiate In Claims Management

Claims management has always set us apart

We combine financial strength with deep expertise

Give our insureds the option of an uncompromising

defense of their claim

defense of their claim

Allows us to defend our insureds at trial more often

than any other company in our line

than any other company in our line

Provides long-term financial and marketing

advantages

advantages

A key differentiating factor in the market

as claims data becomes public

as claims data becomes public

20

Claims Trends Remain Favorable

Frequency trends are

stable after declining

since 2006

stable after declining

since 2006

The result is fewer

cases to try

cases to try

Severity trends also

stable

stable

Trends are much the

same in states with or

without Tort Reform

same in states with or

without Tort Reform

21

ProAssurance Claims Tried

to a Verdict

to a Verdict

The Ohio Example

Exhaustive, reliable data provided by the Ohio

Department of Insurance

Department of Insurance

Broad range of competitors and business

approaches

approaches

Pricing

Underwriting

Claims handling

22

www.insurance.ohio.gov/Legal/Reports/Documents/MedMal_Closed_Claim_2008.pdf

ProAssurance closes more claims

with NO indemnity payments

with NO indemnity payments

Ohio Closed Claims 2005-2008

Source: Ohio Department of Insurance: www.insurance.ohio.gov/Legal/Reports/Documents/MedMal_Closed_Claim_2008.pdf

ProAssurance closes more claims at trial—offering our

insureds the chance for vindication

insureds the chance for vindication

Ohio Closed Claims 2005-2008

Excludes Trials that Ended with a Directed Verdict

Source: Ohio Department of Insurance: www.insurance.ohio.gov/Legal/Reports/Documents/MedMal_Closed_Claim_2008.pdf

Ohio Closed Claims 2005-2008

Source: Ohio Department of Insurance: www.insurance.ohio.gov/Legal/Reports/Documents/MedMal_Closed_Claim_2008.pdf

Prepare for State Changes

We are prepared, operationally and financially,

if Tort Reforms are struck down in our states

if Tort Reforms are struck down in our states

We never give advance credit for untested

reforms unless required by law or regulation

reforms unless required by law or regulation

Prices are set and reserves established as if there

is no tort reform, until results reflect otherwise

is no tort reform, until results reflect otherwise

26

Maximizing Our Potential

2009: Consolidation of:

Mid-Continent General Agency

Mid-Continent General Agency

2009: Consolidation of:

Mid-Continent General Agency

Mid-Continent General Agency

Georgia Lawyers Insurance Co.

Georgia Lawyers Insurance Co.

2004: Purchased Selected Renewal Rights from:

OHIC Insurance Company

OHIC Insurance Company

2004: Purchased Selected Renewal Rights from:

OHIC Insurance Company

OHIC Insurance Company

Success Through M&A

We’ve built a leading platform through M&A

28

1994: Consolidation of:

West Virginia Hosp. Ins Co.

West Virginia Hosp. Ins Co.

1994: Consolidation of:

West Virginia Hosp. Ins Co.

West Virginia Hosp. Ins Co.

1995: Consolidation of;

1995: Consolidation of;

Physicians Ins Co of Indiana

Physicians Ins Co of Indiana

Assumed business of:

Physicians Ins Co of Ohio

Physicians Ins Co of Ohio

Assumed business of:

Physicians Ins Co of Ohio

Physicians Ins Co of Ohio

1996: Consolidation of:

1996: Consolidation of:

Missouri Medical Ins Co

Missouri Medical Ins Co

1995: Assumed business of:

Associated Physicians Ins Co. (IL)

Associated Physicians Ins Co. (IL)

1995: Assumed business of:

Associated Physicians Ins Co. (IL)

Associated Physicians Ins Co. (IL)

1998: Consolidation of:

Physicians Protective Trust Fund (FL)

Physicians Protective Trust Fund (FL)

1998: Consolidation of:

Physicians Protective Trust Fund (FL)

Physicians Protective Trust Fund (FL)

1996: Assumed business of:

American Medical Ins Exchange (IN)

American Medical Ins Exchange (IN)

1996: Assumed business of:

American Medical Ins Exchange (IN)

American Medical Ins Exchange (IN)

Founding in the 1970’s

Founding in the 1970’s

1999: Assumed business of:

Medical Defense Associates (MO)

Medical Defense Associates (MO)

1999: Assumed business of:

Medical Defense Associates (MO)

Medical Defense Associates (MO)

Mutual Assurance

Physicians Ins. Co. of Michigan

Professionals Group

Creation of:

Creation of:

2005: Consolidation of:

NCRIC Group

NCRIC Group

2005: Consolidation of:

NCRIC Group

NCRIC Group

2006: Consolidation of:

PIC Wisconsin Group

PIC Wisconsin Group

2006: Consolidation of:

PIC Wisconsin Group

PIC Wisconsin Group

2007: PRI renewal rights deal

2002: SERTA renewal rights deal

2001: OUM renewal rights deal

2000: DPM Merger

1999: PACO Acquisition

2009 M & A Transactions

29

2008 Premium: $98 million

Significant growth in our core business

Nationwide geographical expansion

2008 Healthcare Premium: $20 million

Extends our core business

Broadens our medically-related range

Geographical expansion

Broadens our medically-related range

Geographical expansion

2008 Premium: $5.7 million

Adds to our lawyers’ book

Geographical expansion

Affirms our interest in this line

Responding to Changes in HealthCare

Projected sector growth through 20181

Physician’s Assistants 39%

Medical Assistants 36%

Licensed Nurses 34%

Chiropractors 31%

Physicians and Surgeons 22%

Podiatrists 9%

1Bureau of Labor Statistics 2008 to 2018 Projections

30

Keep an Eye on Washington

Effects of Healthcare Reform

No immediate effect—no Tort Reform in the bill

More patients will ultimately require more

physicians and ancillary providers

physicians and ancillary providers

Known: More customers for us

Unknown: Effect on the medical/legal environment

More frustration in the system?

More unexpected outcomes?

Demonstration projects do not provide meaningful

reform or immediate data

reform or immediate data

Signals a desire to leave the tort system in

the hands of each state

the hands of each state

31

Summary

ProAssurance

Producing sustainable shareholder value

Growing Book Value per Share

Finding the right M & A opportunities

Significant share ownership at all levels

Focusing on long-term

Preparing for a changing market

Leveraging financial strength

Protecting the balance sheet

Maintain our leading market position

Building strength for the next cycle turn

33

June 16, 2010

Frank B. O’Neil Investor Relations Officer |

Additional Slides for Meetings

General Information

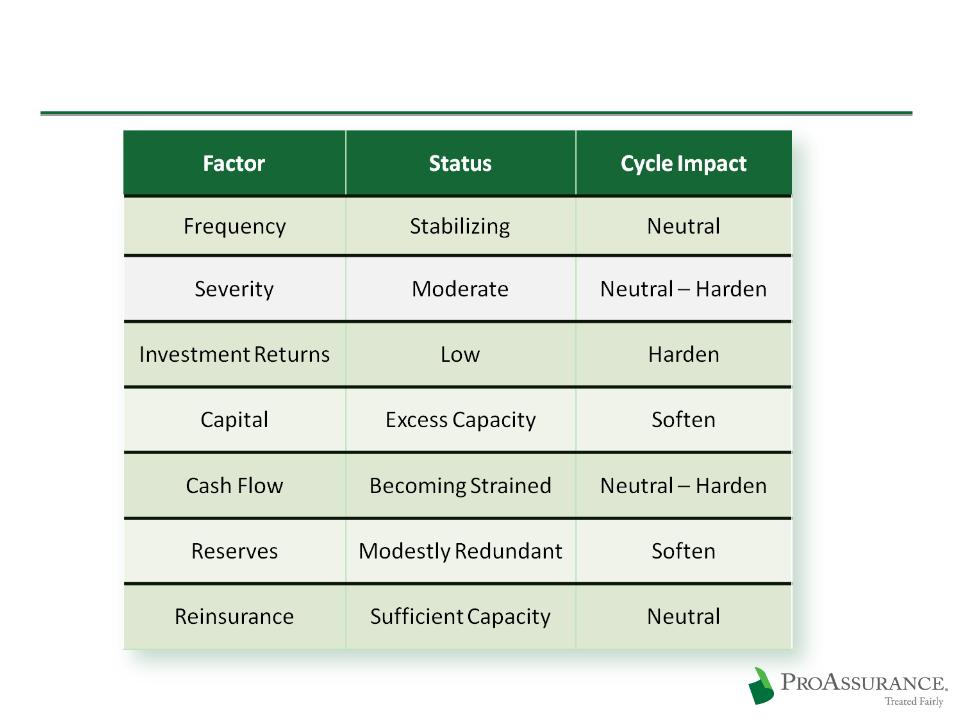

The State of the Market

37

The State of the Market

Prices have been falling yet profitability

remains high

remains high

Continued low interest rates must enforce

discipline sooner or later

discipline sooner or later

Frequency is no longer declining

Only a matter of time before frequency moves

higher

higher

But when?

Severity is trending upward at expected,

manageable rates (4%-5%) in most states

manageable rates (4%-5%) in most states

38

Reserve adequacy

39

Net favorable development continues

We remain confident in current reserve levels

Our levels compare favorably to external

actuarial reviews from Tillinghast and E&Y

actuarial reviews from Tillinghast and E&Y

Excess Capital vs. Excess Capacity

40

Conceptual Model of Projected

A. M. Best BCAR Scores if

A. M. Best BCAR Scores if

Premiums Increase

Surplus is Reduced

Conservative Use of Debt

Low Debt to Cap Ratio

No strain on cash flow

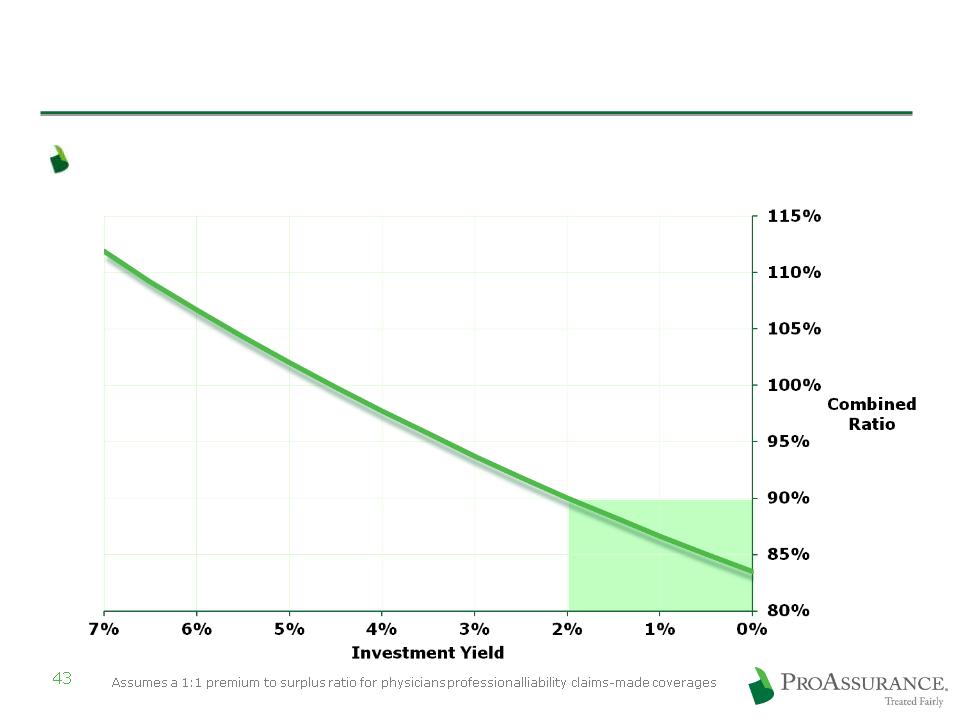

Investments

Investment Income Provides No Cushion

Pricing discipline is even more critical

Combined Ratio

required to generate

a 13% after-tax ROE

required to generate

a 13% after-tax ROE

The Importance of Investment Income

44

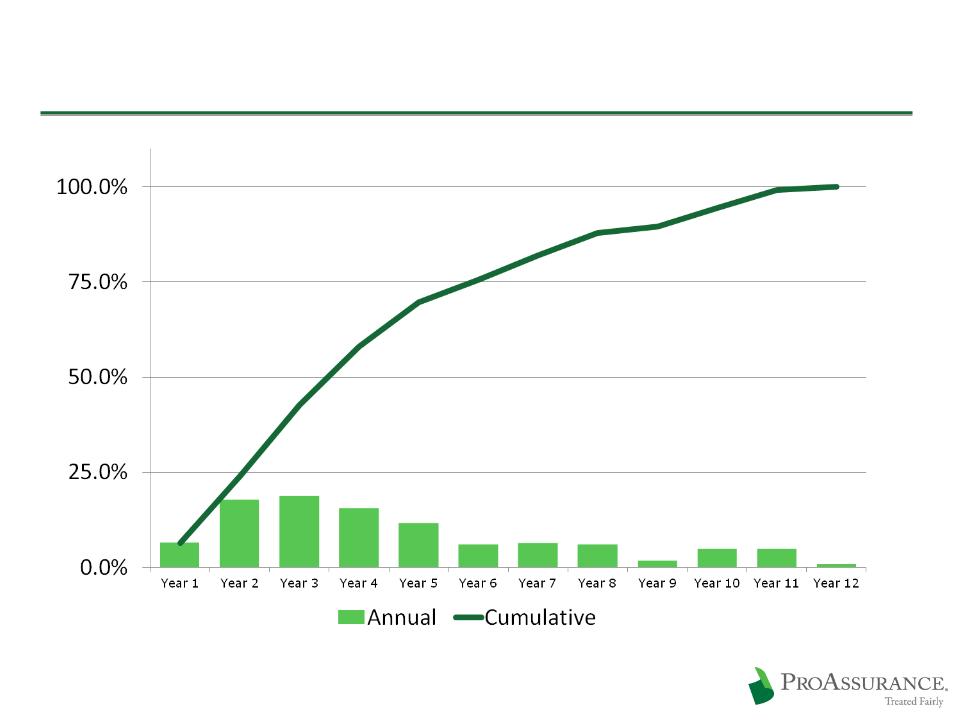

Typical Claims Payout Pattern

The Importance of Investment Income

45

Year

1

1

Year

2

2

Year

3

3

Year

4

4

Year

5

5

Year

6

6

Year

7

7

Year

8

8

Incident

Occurs

Occurs

Discovery

and

Preparation

and

Preparation

Claim

Reported

Reported

Trial

and

Appeals

Appeals

Resolution

5-6 Years

After

Claim

Reported

After

Claim

Reported

Life Cycle of a Typical Claim

No Change to Investment Strategy

Our focus is on protecting the balance sheet and

growing book value

growing book value

We are not extending duration for yield

Main pressures in investments are declining yield and

lower cash balances

lower cash balances

Cash put to work in 2009 as we gained confidence

2009 net realized investment gains: $12.8 million

2008 net realized investment losses: $51 million

Includes $47 million in OTTI

Q1 2010 net realized investment losses: < $1 million

46

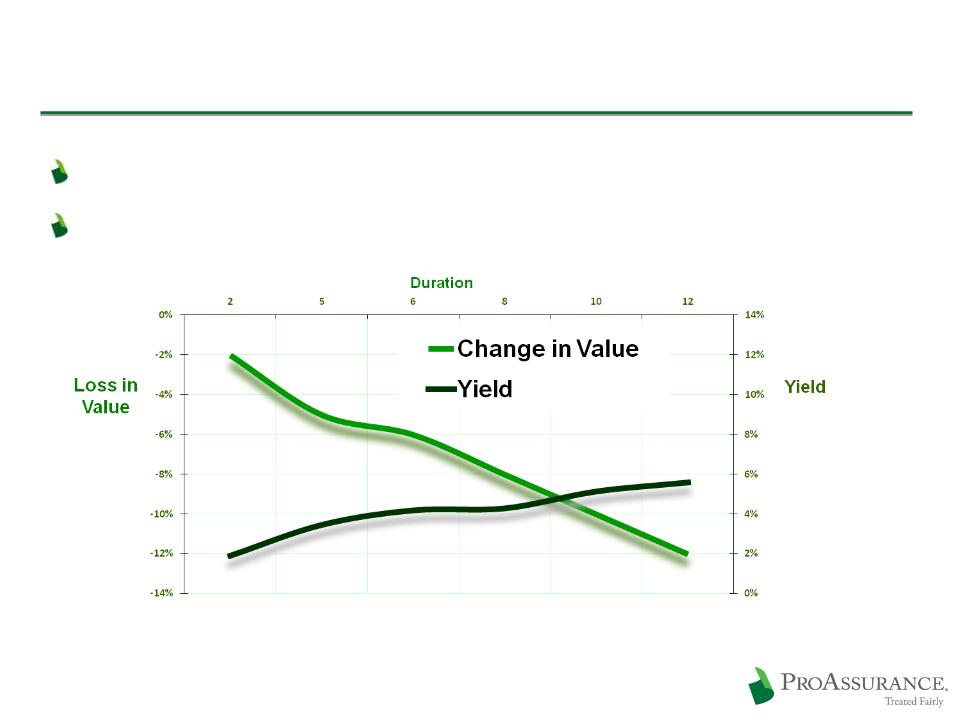

Strategy: Investment Discipline

The choice: Chase yield or extend duration

We are maintaining duration, looking for opportunities

47

Loss in value assuming a 100 basis point shift in the yield curve

Yields based on Single A composite corporate debt

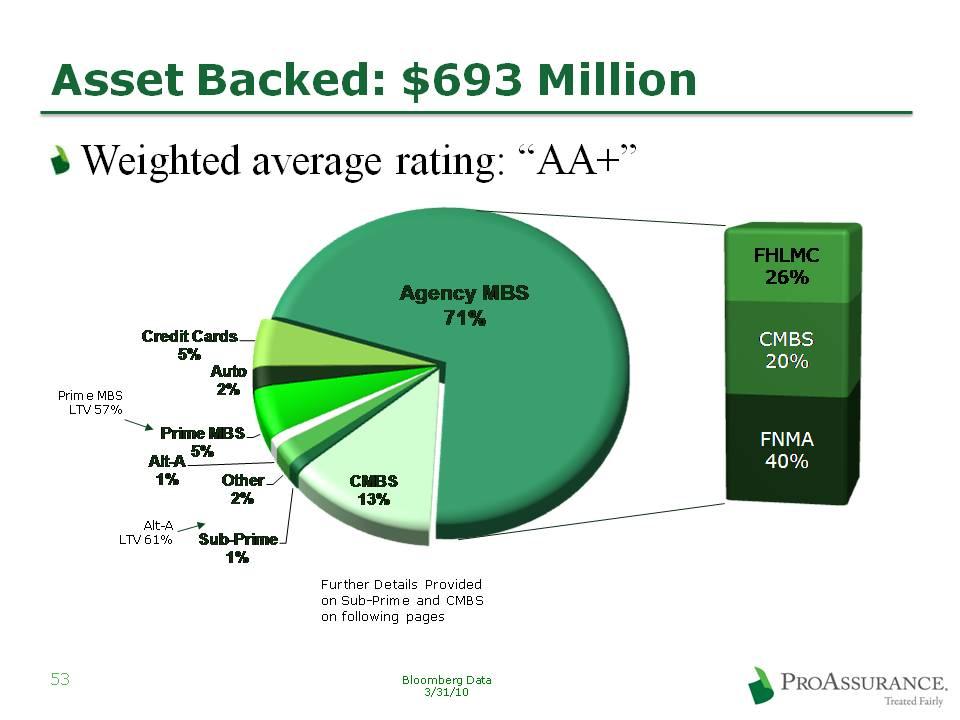

Fixed Income Breakdown

97% investment grade

48

3/31/10

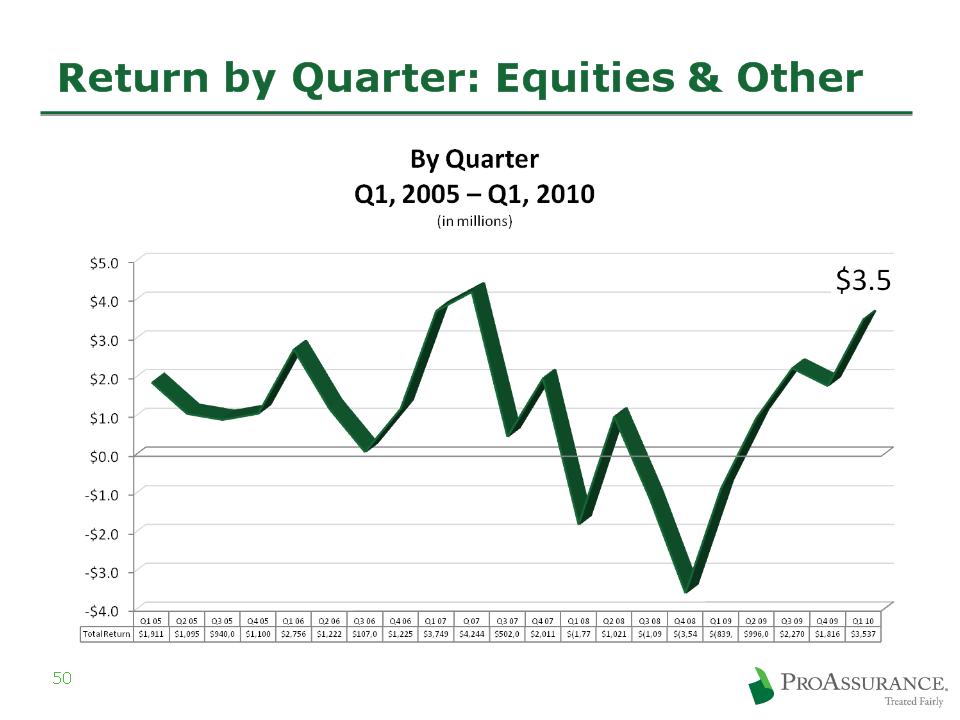

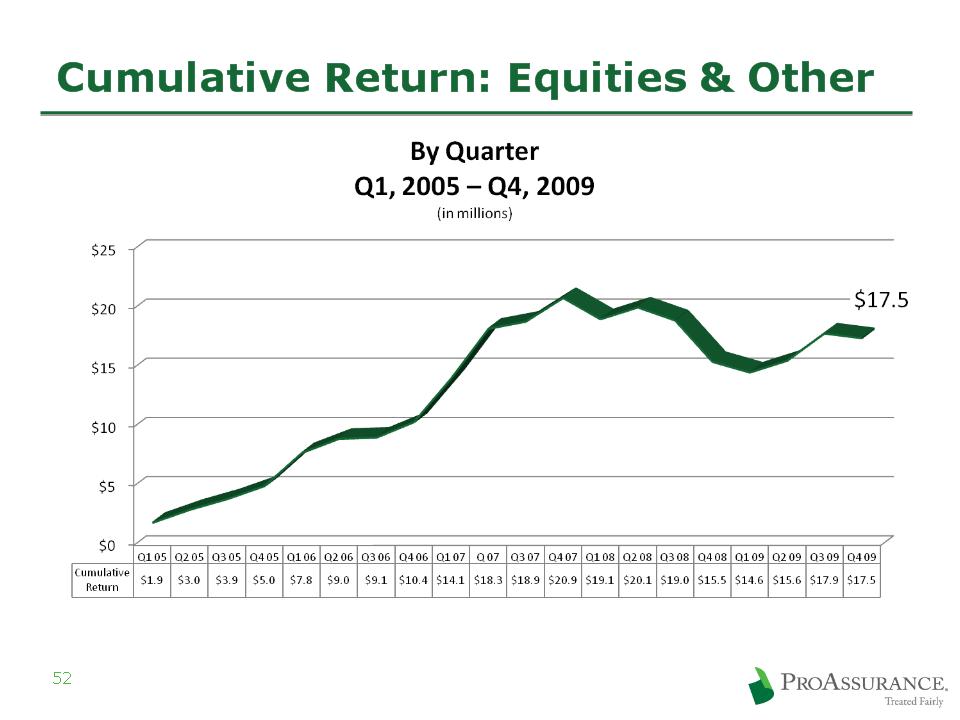

Equities & Other: $160 Million

49

3/31/10

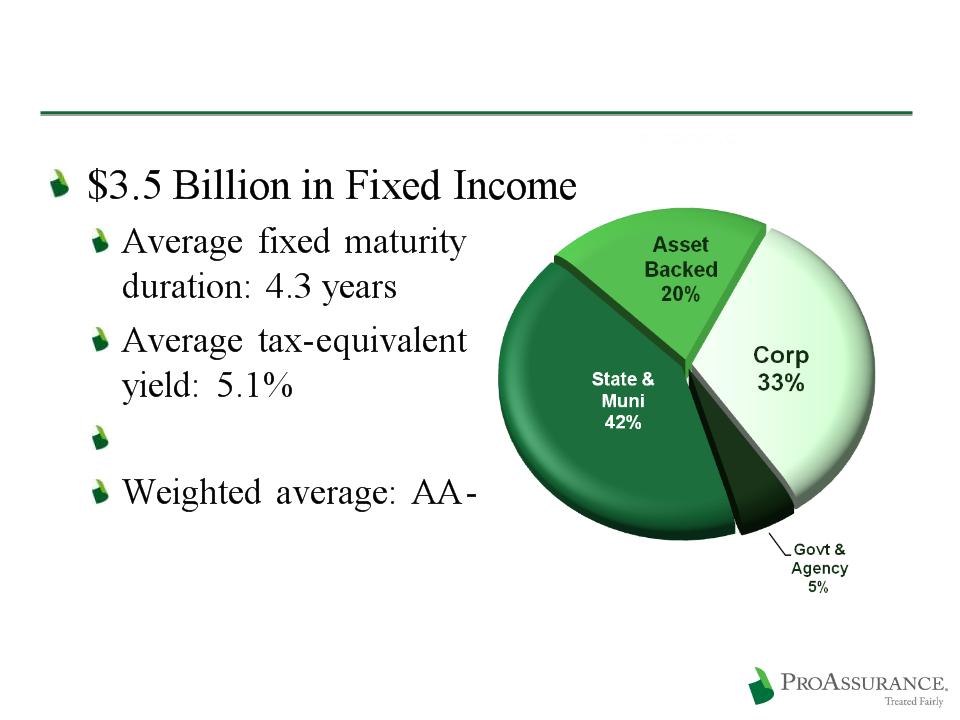

Municipals: $1.5 Billion

53

3/31/10

Investment policy has always required

investment grade rating prior to applying the

effect of insurance

investment grade rating prior to applying the

effect of insurance

Sub-Prime Detail

55

$8.1 million market value in AFS portfolio

$2.5 million unrealized loss

$15.8 million market value in

high-yield LP rated “A”

high-yield LP rated “A”

LP’s focus is distressed ABS

At 3/31/10 | Vintage |

$5.1 Mln | 2004 & Prior |

$3.0 Mln | 2005 |

Quality & Vintage information only on direct holdings at 3/31/10

CMBS Detail

Vintages

2005 & Prior- $65 million

2006- $23 million

Top Property Types

Office: 58% of CMBS portfolio

Retail Anchored: 29% of CMBS portfolio

Mixed Use: 8% of CMBS portfolio

Other: 5% of CMBS Portfolio

56

CMBS Detail

$88 million Fair Value in non-agency CMBS

Book Value: $86 million (2% of fixed income portfolio)

57

At 3/31/2010 | Quality |

$ 83.0 Mln | AAA |

$ 3.0 Mln | AA |

$ 0.7 Mln | A |

$ 0.9 Mln | BB+ |

At 3/31/2010 | Wtd Avg LTV |

14% | <65% |

46% | =65-70% |

21% | <70-75% |

19% | =75-85% |

At 3/31/2010 | Credit Support |

35% | >30% |

47% | 20% - 30% |

12% | 10% - 20% |

6% | Less than 10% |

At 3/31/2010 | Deal Cumulative Delinquencies |

18% | 0.0% - 1.0% |

22% | 1.0% - 3.0% |

10% | 3.0% - 5.0% |

23% | 5.0% - 10.0% |

27% | >10.0% |

At 3/31/2010 | Debt Service Coverage |

80% | =>1.5x |

14% | 1.4x-1.5x |

6% | 1.3x-1.4x |

3/31/10

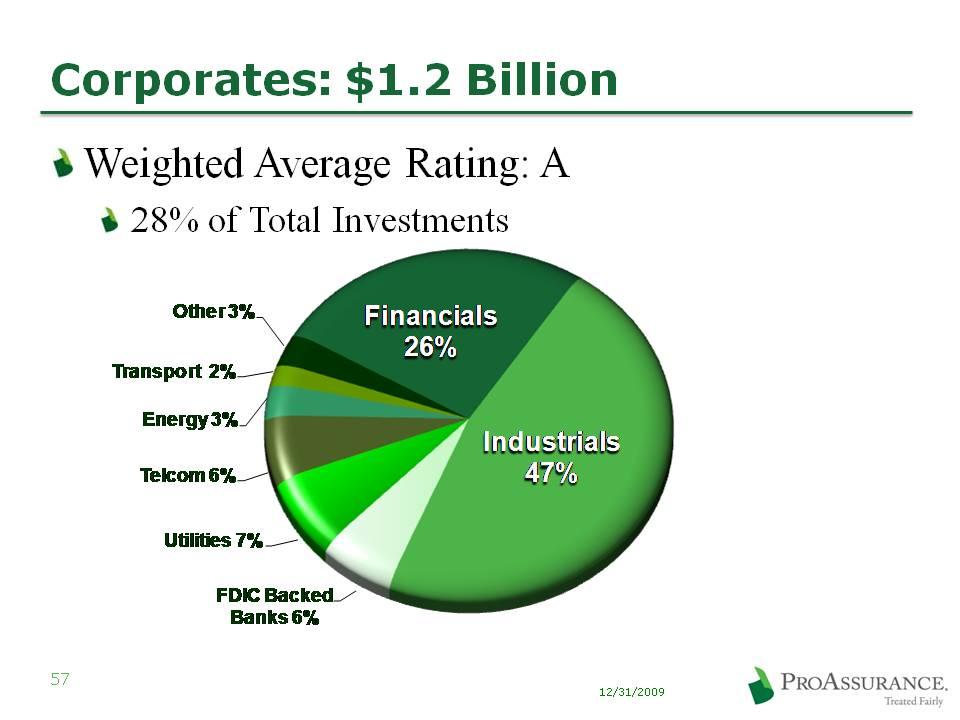

Corporate: Detail on Financials

Top 20 Largest Banks/Financials: $ 269 million

$57 mm FDIC backing

BA $40 ($22) | Eurohypo $8 |

BP Cap $26 | Boeing Cap $7 |

JPM $23 ($14) | US Bank $7 |

GECC $22 ($4) | Credit Suisse $7 |

MS $20 ($6) | PNC $6 ($2) |

Wells $20 | Natl Rural $6 |

GS $18 ($2) | Deutsche Bank $5 |

Amex $16 | Depfa ACS -Covered $5 |

Citi $13 ($5) | FMCC $5 |

BNY $10 | John Deere Cap $5 ($2) |

FDIC backed amounts listed in parentheses | |

59

12/31/2009

Treasury/GSE: $206Million

60

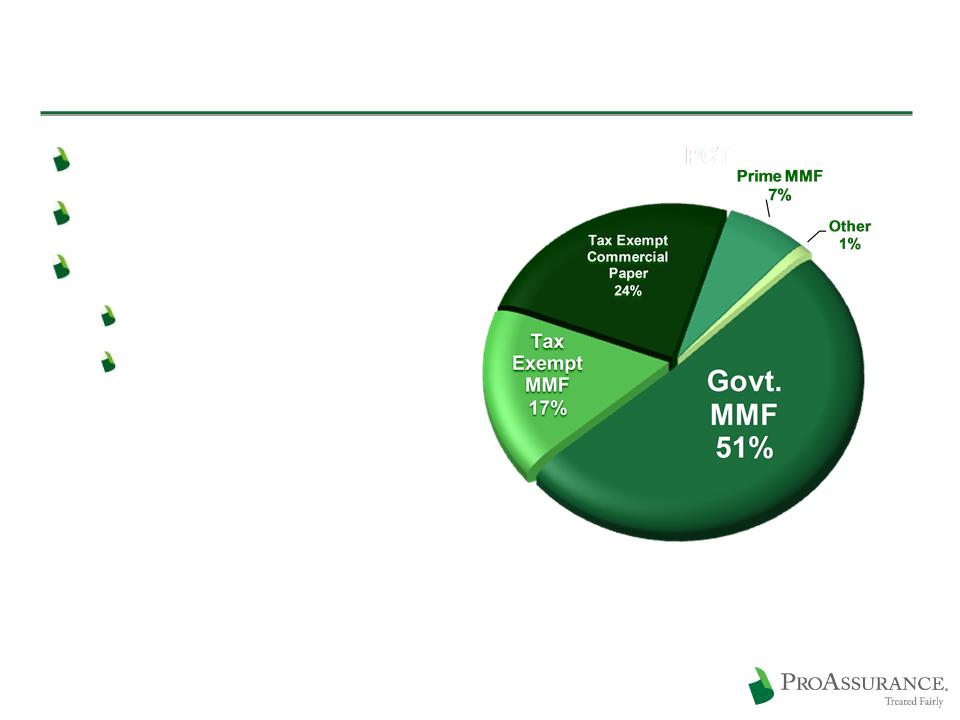

3/31/2010

Portfolio Overview: Short Term

$152 Million

Rated A1/P1 or better

Money Markets:

Moody’s: Aaa

S&P: AAA

61

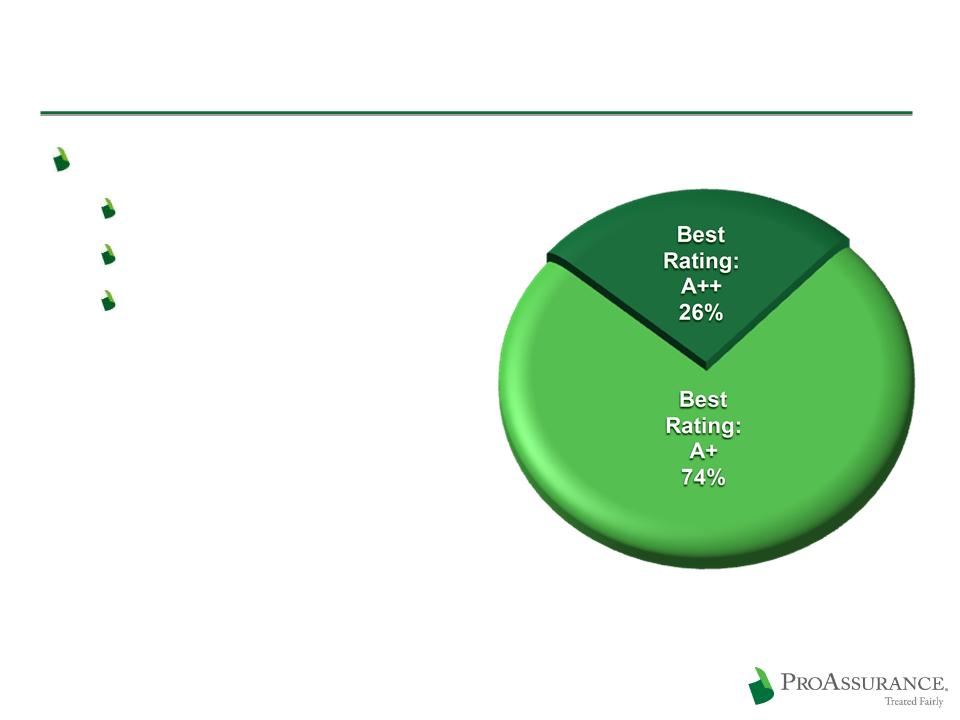

3/31/2010

BOLI: $65 Million

Weighted average rating

Moody’s: AA3

S&P: AA-

A. M. Best: A+

62

3/31/2010

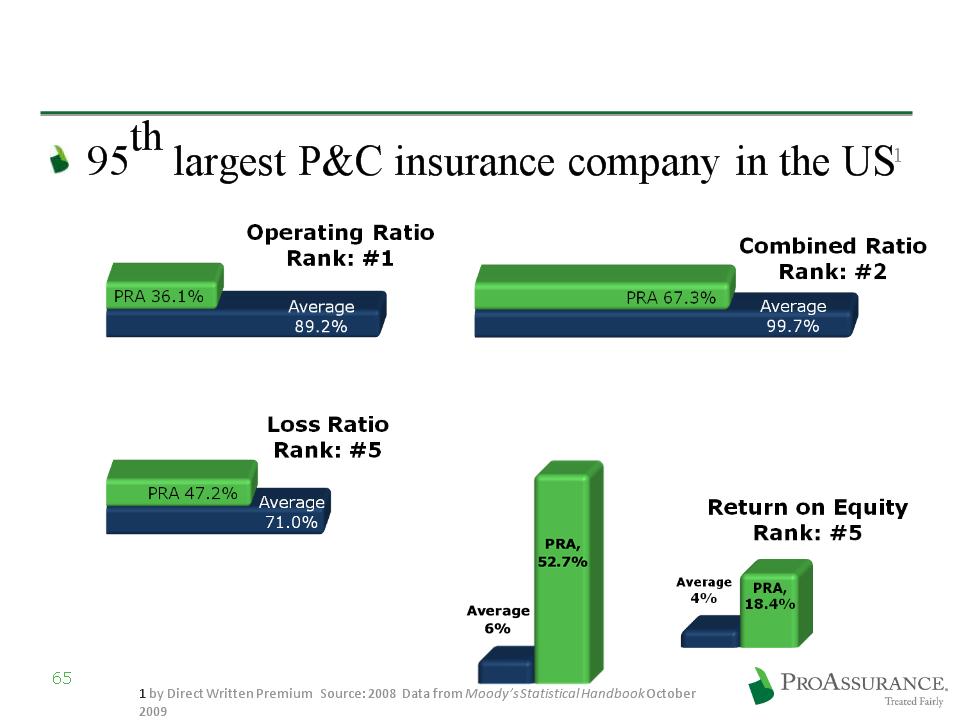

Moody’s 2008 Rankings

Outstanding Performance vs Industry

Moody’s rankings of the top 100 P&C

insurance companies by premium volume

insurance companies by premium volume

64

1 by Direct Written Premium Source: 2008 Data from Moody’s Statistical Handbook October

2009

2009

Category | Ranking |

Direct Written Premiums | 95 |

Operating Ratio | 1 |

Combined Ratio | 2 |

Loss Ratio | 5 |

ROE | 5 |

Moody’s Top 100 Ranking Data

Return on Premium

Rank: #1

Sales & Marketing Highlights

Distribution Sources

We remain primarily agent-driven

Direct in Alabama, Florida and in all states for

Podiatric business

Podiatric business

Dual distribution working in DC and parts of

Missouri

Missouri

67

New Business Acquisition Trends

Profitable new business can be found

New business added in a number of states

Retention is at historical highs

The market is equal parts pricing sanity and

insanity

insanity

68

Retention trends

Retention was 88% in Q1 2010

Retention was 88% overall in 2009

Despite competitors' pricing we are retaining

business

business

69

Competition

We have see no new large scale competitors

Greatest competition is physicians moving into

hospital captives and large clinic alternative risk

transfer programs

hospital captives and large clinic alternative risk

transfer programs

We will address these issues through new products

and new approaches to our business partners

and new approaches to our business partners

Some consolidation among start-ups

Pricing largely a non-factor due to the soft market

70

Terms and Conditions

One-off concessions by many carriers

Tail coverage

Prior acts

Slot rating

71

Lawyers Professional Liability

Historical book performing as expected

MGA’s producing new business as expected in

market previously unserved

market previously unserved

Primarily western US (Greyhawk) and

mid-Atlantic (ProLawyer)

mid-Atlantic (ProLawyer)

72

Reinsurance

Reinsurance Overview

74

No real change in pricing

Somewhat surprising to us

Interest remains high in our program

Aspen, Hannover and Transatlantic lead our

program

program

Solid mix of London, US and Bermudan

companies

companies

Additional Claims Highlights

Loss Trends

Frequency remains at historically low levels

No longer declining

Some signs of frequency returning

Severity is manageable

Fewer cases for us to try

We are trying the same percentage of our

claims inventory

claims inventory

76

77

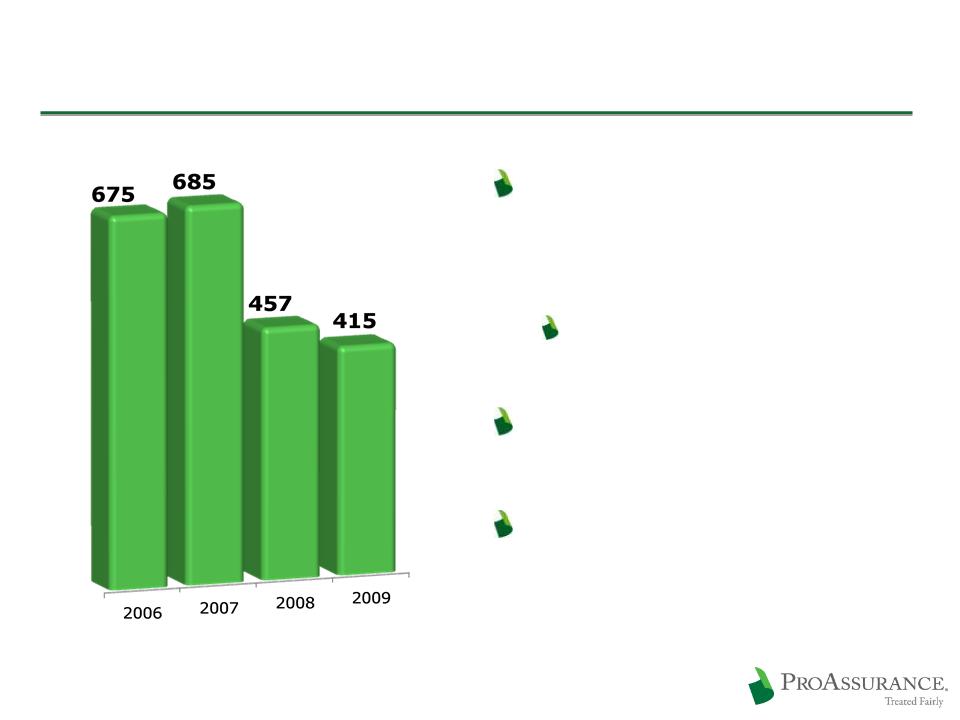

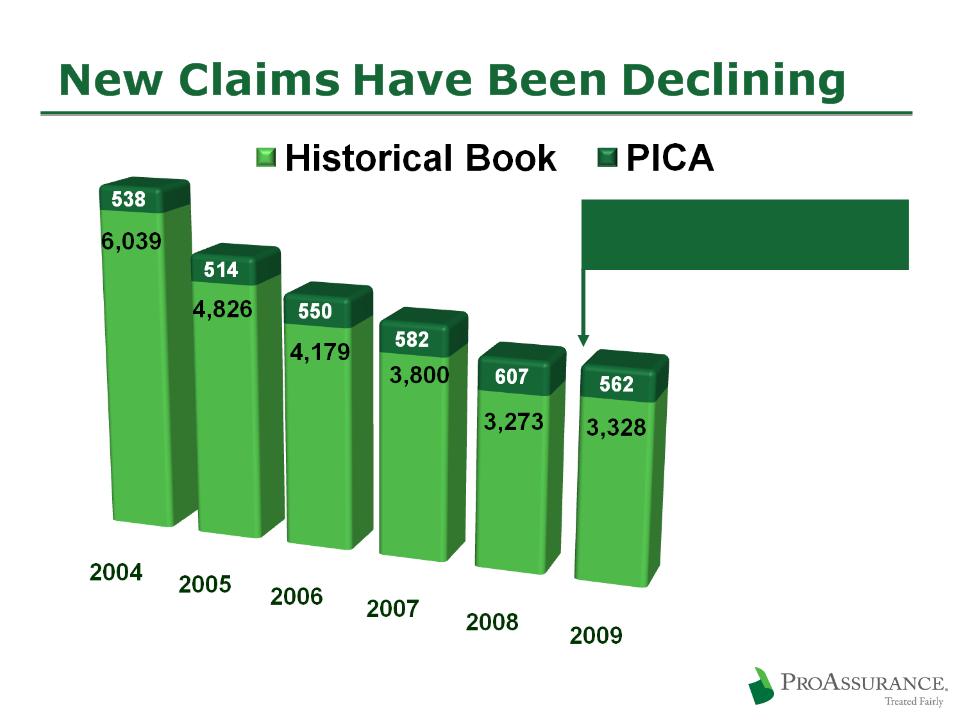

New Claims Opened Each Year

New Claims Opened Each Year

6,577

5,340

4,729

4,382

3,880

Claims are level from

2008 to 2009

2008 to 2009

3,890

No Emerging Claim Hotspots

No unexpected claims trends are emerging by

specialty

specialty

Greater public access to claims outcome data

should fuel renewed attention to claims defense

should fuel renewed attention to claims defense

78

Risk Management Highlights

We Are a Doctor-Focused Company

We value physician input and seek partnerships

with organized medicine

with organized medicine

Endorsed in Alabama, D.C., Indiana and Wisconsin

Physician involvement at all levels of the

organization

organization

Led by Hayes Whiteside, M.D., SVP and Chief

Medical Officer

Medical Officer

We actively participate in national and state tort

reform efforts

reform efforts

80

Risk Management Scope

Approximately 80% of insureds are “touched”

by risk management programs each year

by risk management programs each year

Risk management publications provide

specialty-specific advice

specialty-specific advice

State-specific publications target current event

issues

issues

Risk Resource center provides immediate

access to risk management advice in dynamic

situations

access to risk management advice in dynamic

situations

81