This presentation contains Forward Looking Statements and other information designed to convey

our projections and expectations regarding future results. There are a number of factors which

could cause our actual results to vary materially from those projected in this presentation. The

principal risk factors that may cause these differences are described in various documents we file

with the Securities and Exchange Commission, such as our Current Reports on Form 8-K, and our

regular reports on Forms 10-Q and 10-K, particularly in “Item 1A, Risk Factors.” Please review

this presentation in conjunction with a thorough reading and understanding of these risk factors.

our projections and expectations regarding future results. There are a number of factors which

could cause our actual results to vary materially from those projected in this presentation. The

principal risk factors that may cause these differences are described in various documents we file

with the Securities and Exchange Commission, such as our Current Reports on Form 8-K, and our

regular reports on Forms 10-Q and 10-K, particularly in “Item 1A, Risk Factors.” Please review

this presentation in conjunction with a thorough reading and understanding of these risk factors.

We especially identify statements concerning our transactions involving Medmarc Insurance

Company and Independent Nevada Doctors Insurance Company as Forward Looking Statements

and direct your attention to our news releases issued on June 27, 2012, our Current Report on Form

8K, issued on June 28, 2012 and our 10K, filed on February 19, 2013 for a discussion of

risk factors pertaining to these transactions and subsequent integration into ProAssurance.

Company and Independent Nevada Doctors Insurance Company as Forward Looking Statements

and direct your attention to our news releases issued on June 27, 2012, our Current Report on Form

8K, issued on June 28, 2012 and our 10K, filed on February 19, 2013 for a discussion of

risk factors pertaining to these transactions and subsequent integration into ProAssurance.

This presentation contains Non-GAAP measures, and we may reference Non-GAAP measures in

our remarks and discussions. A reconciliation of these measures to GAAP measures is available in

our latest quarterly news release, which is available in the Investor Relations section of our website,

www.ProAssurance.com, and in the related Current Report on Form 8K disclosing that release.

our remarks and discussions. A reconciliation of these measures to GAAP measures is available in

our latest quarterly news release, which is available in the Investor Relations section of our website,

www.ProAssurance.com, and in the related Current Report on Form 8K disclosing that release.

FORWARD LOOKING STATEMENTS

NON-GAAP MEASURES

YTD 2013 Highlights

Solid profitability with ROE of 11.1%%

Book Value per share now $37.79

2.6% increase since year-end 2012

Mark-to-market effect $(0.40)/share in Q2

Book Value per Share has grown each year since

1991

1991

Recent transactions contributing to our results

with integration proceeding as planned

with integration proceeding as planned

3

ProAssurance Corporate Profile

Specialty liability insurance writer

Healthcare Professional Liability (HCPL)

Only public company writing predominately HCPL

Life sciences and medical devices

Attorney’s professional liability

Market Cap: ~$3.0 billion

Shareholders’ Equity: $2.4 billion

Total Assets: $5.3 billion

Claims-Paying Ratings: “A+” (Superior) by A. M. Best

and “A” by Fitch

and “A” by Fitch

Debt ratings recently upgraded by S&P and Moody’s

4

ProAssurance Business Profile

5

Q2 2013 Policyholders: ~64,600

Q2 2013 Premium: $286 mln

June 30, 2013

Includes Acquisitions

Includes Acquisitions

Tail Premium Allocated by Line

Distribution Channels | |||

HCPL | LPL | Life Sciences | |

Agent / Broker | 67% | 77% | 100% |

Direct | 33% | 23% | -- |

ProAssurance Geographic Profile

Broad geographic diversification

Locally-based decision-making differentiates ProAssurance by

addressing each state’s unique medical/legal challenges

addressing each state’s unique medical/legal challenges

National Footprint

(Birmingham)

Corporate Headquarters

Corporate Headquarters

Claims Offices

Claims Offices

Claims / Underwriting Offices

Claims / Underwriting Offices

Underwriting Offices

Underwriting Offices

6

Seeking Increased Yield But Balancing Risk

We continue to focus on

maintaining a high quality, well

diversified fixed income

portfolio

maintaining a high quality, well

diversified fixed income

portfolio

We have made incremental

changes to obtain higher yields

in blue chip investments

changes to obtain higher yields

in blue chip investments

$4.2 Billion

Portfolio

Portfolio

$4.2 Billion

Portfolio

Portfolio

Fixed Income:

85%

85%

Fixed Income:

85%

85%

Short Term: 2%

Short Term: 2%

Equity and Equity Substitutes: 12%

Equity and Equity Substitutes: 12%

BOLI: 1%

BOLI: 1%

6/30/13

7

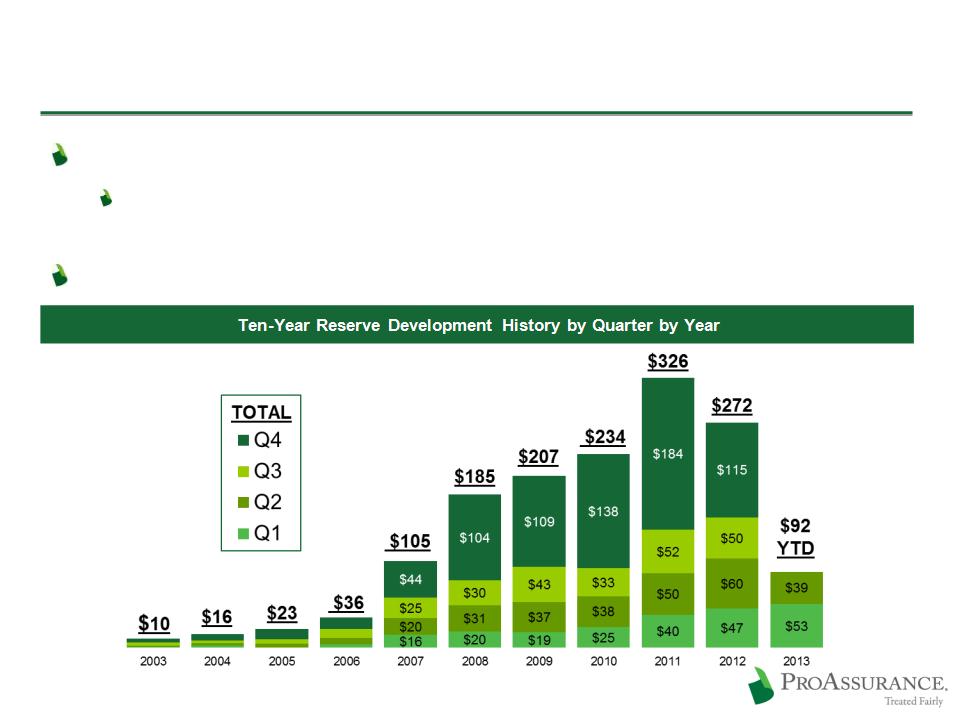

Consistent Approach to Reserves

Recognizing loss trends as they appear

No change in long-term results but potential

volatility quarter-to-quarter

volatility quarter-to-quarter

No change in reserving philosophy or process

8

$ in millions

Management is Experienced & Invested

Effective senior management remains in place—13 years average tenure

Average ProAssurance tenure through the VP level is 16 years, 25 years average industry experience

Management and employees are invested, owning ~5.6 % of ProAssurance stock

W. Stancil Starnes, JD Chairman & Chief Executive Officer Company Tenure: 6 Years Prior MPL Experience: 29 Years Total Industry & Related Experience: 35 Years Formerly in the private practice of law in MPL defense and complex corporate litigation | Jeffrey L. Bowlby, ARM Sr. Vice-President & Chief Marketing Officer Company Tenure: 15 Years Prior MPL Experience: - Total Industry & Related Experience: 29 Years Career-long experience in insurance sales and marketing, most recently as SVP for Marketing with Meadowbrook | Howard H. Friedman, ACAS Sr. Vice-President & Chief Underwriting Officer Company Tenure: 17 Years Prior MPL Experience: 16 Years Total Industry & Related Experience: 33 Years Career-long experience in MPL company operations and management. Former ProAssurance CFO |

Jeffrey P. Lisenby, JD Sr. Vice-President, General Counsel & Secretary Company Tenure: 12 Years Prior MPL Experience: - Total Industry & Related Experience: 12 Years Formerly in the private practice of law | Duncan Y. Manley Vice-President, Operations and Information Systems Company Tenure: 13 Years Prior MPL Experience: 7 Years Total Industry & Related Experience: 20 Years Career-long experience in MPL company operations as an executive and consultant | Frank B. O’Neil Sr. Vice-President & Chief Communications Officer Company Tenure: 26 Years Prior MPL Experience: - Total Industry & Related Experience: 26 Years Formerly a television news executive and anchor |

Mary Todd Peterson President & CEO of Medmarc Company Tenure: 12 Years Prior Industry Experience: 14 Years Total Industry & Related Experience: 26 Years Former Partner with Johnson Lambert and VP Finance & Controller with Acacia | Edward L. Rand, Jr., CPA Sr. Vice-President & Chief Financial Officer Company Tenure: 8 Years Prior MPL Experience: - Total Industry & Related Experience: 20 Years Career-long experience in insurance finance and accounting. Most recently Chief Accounting Officer for Partner Re | Ross E. Taubman, DPM President of PICA Company Tenure: 2 Year Prior MPL Experience: - Total Industry & Related Experience: 28 Years Formerly in the private practice of podiatry. Leader in organized podiatric medicine; former president and Trustee of the American Podiatric Medical Association |

Darryl K. Thomas, JD Hayes V. Whiteside, MD, FACS Sr. Vice-President & Chief Claims Officer Sr. Vice-President & Chief Medical Officer Company Tenure: 18 Years Company Tenure: 9 Years Prior MPL Experience: 10 Years Prior MPL Experience: - Total Industry & Related Experience: 28 Years Total Industry & Related Experience: 29 Years Career-long experience in MPL claims management Formerly in the private practice of Urology | ||

9

Our Commitment to Treated Fairly

Steadfast dedication to in-depth underwriting and

adequate pricing

adequate pricing

Unquestioned financial strength consistently

delivering value for insureds and shareholders

delivering value for insureds and shareholders

An unsurpassed level of customer service

Unwavering dedication to the defense of

non-meritorious lawsuits

non-meritorious lawsuits

Allows our insureds the right to an unfettered defense of

their claims where permitted by law

their claims where permitted by law

10

Driven to Excel / Focused on Shareholder Value

Maintaining profitability

Continuing growth in book value per share

Producing sustainable shareholder value

Focusing on long-term—ready for the market turn

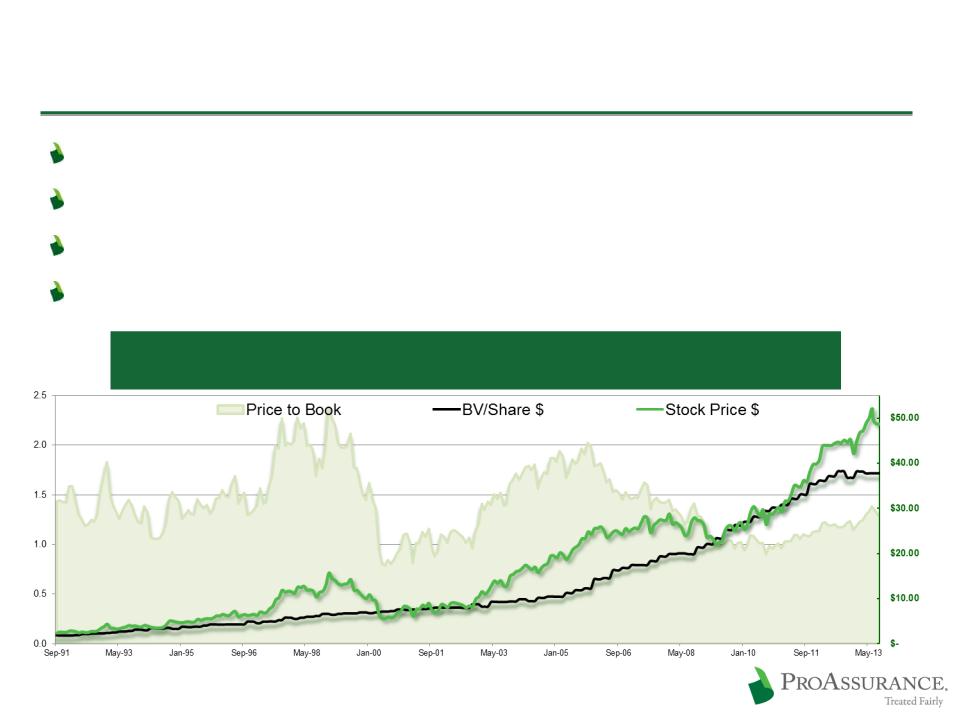

Current Prices Reflect the Solid Value of ProAssurance

Current Price to Q2 2013 Book: 1.3x Average Since Inception: 1.4x

Unadjusted for dividends

Prices Adjusted for 2:1 Stock Split

11

Strategies for Future Success

Our successful experience and deep expertise

uniquely qualify ProAssurance to insure the

widest range of healthcare risks

uniquely qualify ProAssurance to insure the

widest range of healthcare risks

Building a Bridge to the Future

We are uniquely positioned to succeed by serving both

the emerging, complex healthcare market and the

legacy business that will remain

the emerging, complex healthcare market and the

legacy business that will remain

Smaller competitors with less experience and capacity

have decisions to make about their future in this new

healthcare environment

have decisions to make about their future in this new

healthcare environment

13

Legacy business is

largely single-state, solo

and small groups.

A substantial amount of

this business will

remain, but will demand

more from insurers.

largely single-state, solo

and small groups.

A substantial amount of

this business will

remain, but will demand

more from insurers.

The future will be

dominated by large

groups and institutions,

often multi-disciplinary

and multi-state. They

will demand financial

strength and deep

expertise.

dominated by large

groups and institutions,

often multi-disciplinary

and multi-state. They

will demand financial

strength and deep

expertise.

Building a Bridge to the Future

Larger risks demand sophisticated coverages

that span the continuum of healthcare

that span the continuum of healthcare

Broad healthcare liability experience is our

foundation

foundation

Added capacity & capability through M&A

Medmarc, PICA and Mid-Continent

Home

Healthcare

Healthcare

Non-Traditional

Delivery Settings

Delivery Settings

Multi-Specialty

Clinics

Clinics

Hospital & Facility

Centered Care

Centered Care

New delivery

devices,

techniques and

research

devices,

techniques and

research

ProAssurance spans the continuum of care

Traditional

Practices

Practices

14

ProAssurance Will Grow Prudently

We are building the platform that will allow us

to serve the broad spectrum of healthcare

to serve the broad spectrum of healthcare

Prudent leverage of our success and experience

with the addition of specialized expertise

with the addition of specialized expertise

Healthcare-related coverages that compliment our

MPL line

MPL line

ProAssurance is a demonstrated leader in M&A

The MPL market will firm and we are prepared

to grow organically as opportunities arise

to grow organically as opportunities arise

15

ProAssurance’s Successful M&A History

Original

Companies

Companies

Purchased Company

Demutualization

OHIC

HOSPITALS ONLY

HOSPITALS ONLY

2

1

1

1

1

1

1

1

1

3

4

4

1

4

Renewal Rights

Assumed Business

2

2

†

2

3

1

3

3

1

SERTA

16

Strategy for an Evolving Market

Shaped by a healthcare landscape that will

change—with or without federal healthcare

reform

change—with or without federal healthcare

reform

Expanding our capabilities and commitment

across the continuum of healthcare

across the continuum of healthcare

Building on two decades of hospital experience

Recent expansion into products liability for life

sciences and medical devices through M&A

sciences and medical devices through M&A

Enhancing our historical commitment to

individual providers and small groups

individual providers and small groups

17

Positioned to Succeed

ProAssurance has the right combination of geographic scope, broad experience, and

financial strength for success in the new world of healthcare liability

financial strength for success in the new world of healthcare liability

18

SNL 2012 Statutory Data, MPL Writers with Direct Written Premiums >$80 million

Strategy for an Evolving Market

Leverage our reach, expertise and financial

strength with larger accounts

strength with larger accounts

Largest non-profit healthcare

system in the US

system in the US

Now in Michigan, Florida,

Illinois, Indiana and Texas

Illinois, Indiana and Texas

Insuring Ascension-affiliated

physicians through coordinated,

jointly insured programs

physicians through coordinated,

jointly insured programs

Financial involvement of both entities creates incentive to reduce risk

*www.ascensionhealth.org/index.php?option=com_locations&view=locations&Itemid=148

Ascension Health’s Ministry Locations*

19

Strategy for an Evolving Market

Joint physician/hospital insurance products to

address the unique risk tolerance and claims-

handling expectation of each insured

address the unique risk tolerance and claims-

handling expectation of each insured

Partnerships with existing physician-focused

companies to leverage hospital expertise

companies to leverage hospital expertise

Recently announced California venture with

CAP-MPT: CAPAssurance

CAP-MPT: CAPAssurance

Alternative risk and self-insurance mechanisms

Captive insurance, risk sharing programs and

Risk Retention Groups for

specific specialties or regions

Risk Retention Groups for

specific specialties or regions

20

Healthcare Reform

Known: More customers for us

May accelerate the growth of hospital-owned practices and

consolidation into larger groups

consolidation into larger groups

Provides an opportunity for us due to our geographic reach,

long-term experience in hospitals and our financial strength

long-term experience in hospitals and our financial strength

We have enhanced our ability to write new classes of

business through acquisitions

business through acquisitions

May hasten the need for consolidation of smaller insurers

Unknown: Effect on the medical/legal environment

Increased patient frustration with the system

Possibility of more unexpected outcomes

21

Sound Strategy = Consistent Profitability

Captures our focus on long-term excellence

Increased every year we have been public

The Payoff: Consistent Book Value Growth

23

Inception to 6/30/13

CAGR: 16%

CAGR: 16%

Cumulative: 2,171%

10 Year Summary (2003 -2012)

CAGR: 16%

CAGR: 16%

Cumulative: 360%

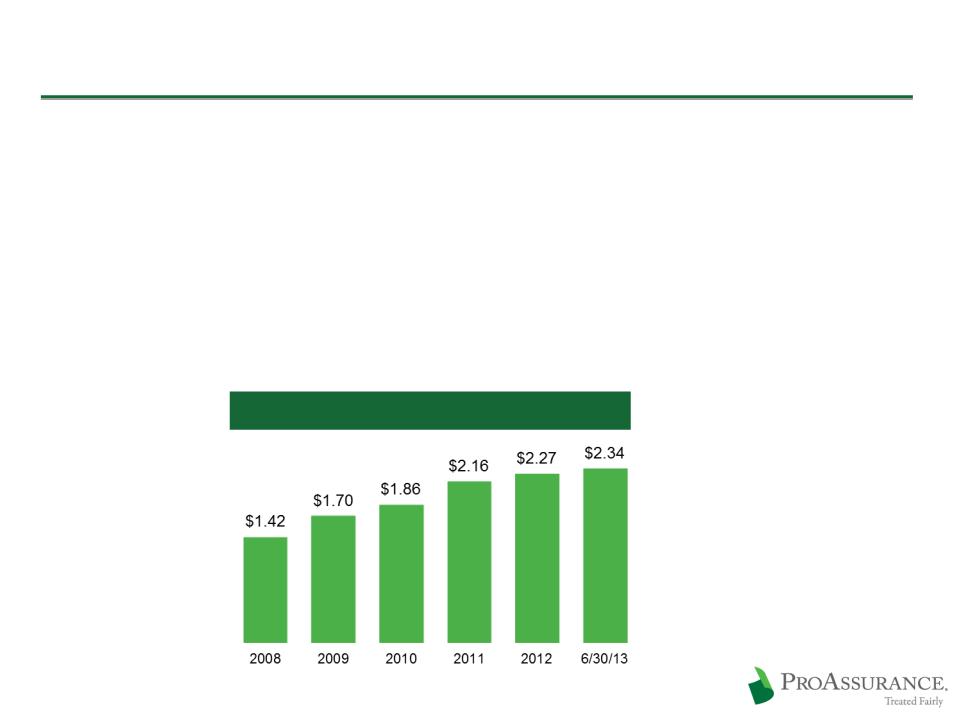

Historical Book Value Per Share

Split Adjusted

Dividends Shown in the Year Declared

Split Adjusted

Dividends Shown in the Year Declared

Reflects all stock splits and includes all dividends in the year declared

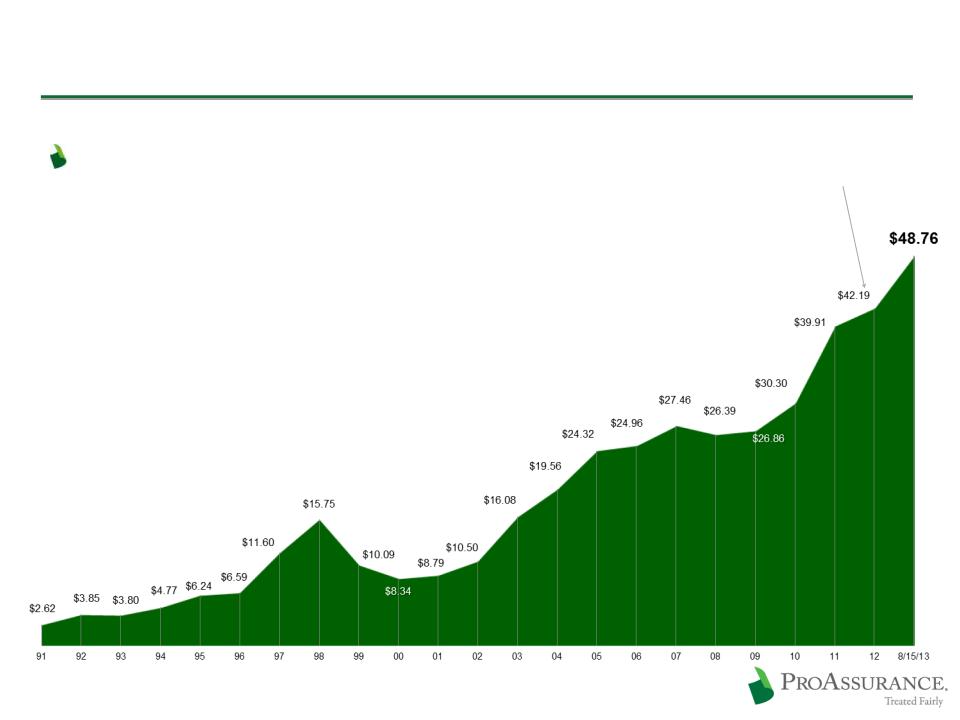

Share price reflects investor confidence in

our business decisions and long-term strategy

our business decisions and long-term strategy

The Payoff: Steady Share Price Increase

24

Historical Share Price

Reflects all stock splits

2012 excludes

$2.50/share

special dividend

$2.50/share

special dividend

Inception to 8/15/13

CAGR: 14%

CAGR: 14%

Cumulative: 1,761%

10 Year Summary (2003-2012)

CAGR: 15%

CAGR: 15%

Cumulative: 302%

Historical Financial Performance

Our disciplined, long-term approach drives

consistent profitability

consistent profitability

$ in millions

Net Income1

Operating Income2

25

1 Includes a gain of $35.5 million in the first quarter of 2013 in connection with our acquisition of Medmarc as a result of the value

of the net assets acquired vs. our purchase price.

of the net assets acquired vs. our purchase price.

2 Excludes the after-tax effects of net realized gains or losses and one-time items that do not reflect normal operating results

YTD 2013 Income Statement Highlights

in millions, except per share data

26

June 30, | Y-OVER-Y Change | ||

2013 | 2012 | ||

Gross Premiums Written | $ 286 | $ 273 | +5% |

Net Investment Result | $ 62 | $ 64 | -3% |

Total Revenues | $ 366 | $ 344 | +6% |

Total Expenses (Includes Loss Costs) | $ 201 | $ 190 | +6% |

Net Income (Includes Realized Investment Gains & Losses and gain on acquisition) | $ 163 | $ 114 | +43% |

Operating Income | $ 105 | $ 108 | -3% |

Net Income per Diluted Share | $2.63 | $1.85 | +42% |

Operating Income per Diluted Share | $1.69 | $1.74 | -3% |

Q2 2013 Income Statement Highlights

in millions, except per share data

27

June 30, | Y-OVER-Y Change | ||

2013 | 2012 | ||

Gross Premiums Written | $ 123 | $ 102 | +21% |

Net Investment Result | $ 30 | $ 32 | -6% |

Total Revenues | $ 171 | $ 164 | +4% |

Total Expenses (Includes Loss Costs) | $ 106 | $ 84 | +26% |

Net Income (Includes Realized Investment Gains & Losses and gain on acquisition) | $ 50 | $ 58 | -14% |

Operating Income | $ 45 | $ 59 | -24% |

Net Income per Diluted Share | $0.81 | $0.95 | -15% |

Operating Income per Diluted Share | $0.72 | $0.96 | -25% |

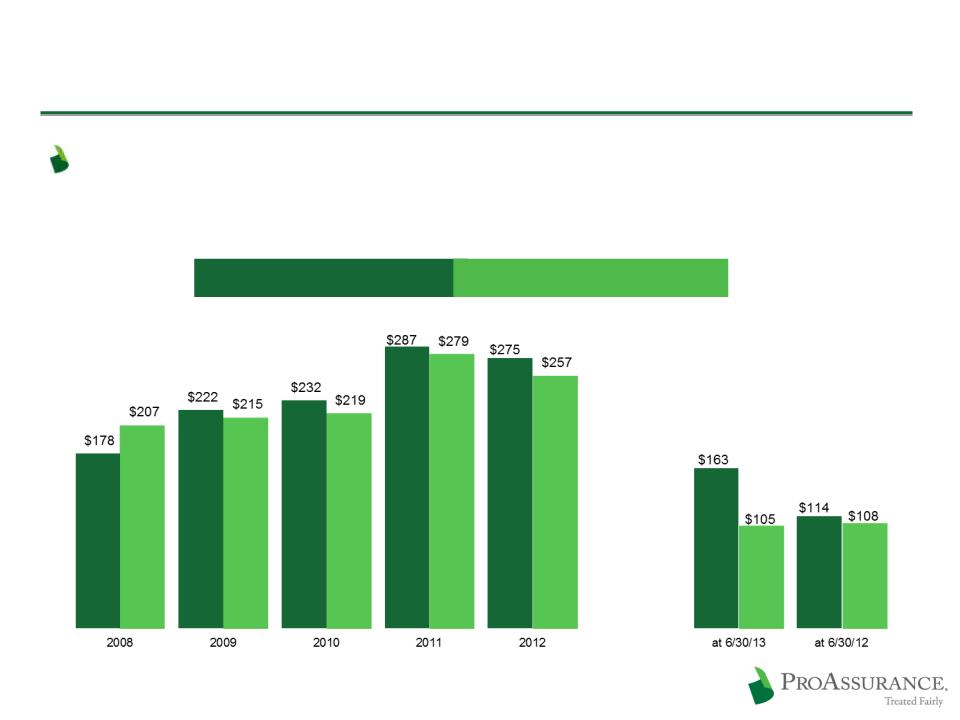

Disciplined Underwriting

Five Year Premium History

28

Consistently writing profitable business to ensure long-

term success

term success

Premium driven by competition, physician consolidation

Loss trends remains favorable

Gross Premiums Written

Net Premiums Earned

YTD 2013 Balance Sheet Highlights

Split adjusted, in billions, except Book Value per share

Shareholders’ Equity $ 2.3 $ 2.3 +3%

Total Investments 4.2 3.9 +6%

Total Assets 5.1 4.9 +5%

Policy Liabilities 2.5 2.3 +7%

6/30/13 12/31/12 CHANGE

Shareholders’ Equity

64% increase since 2008

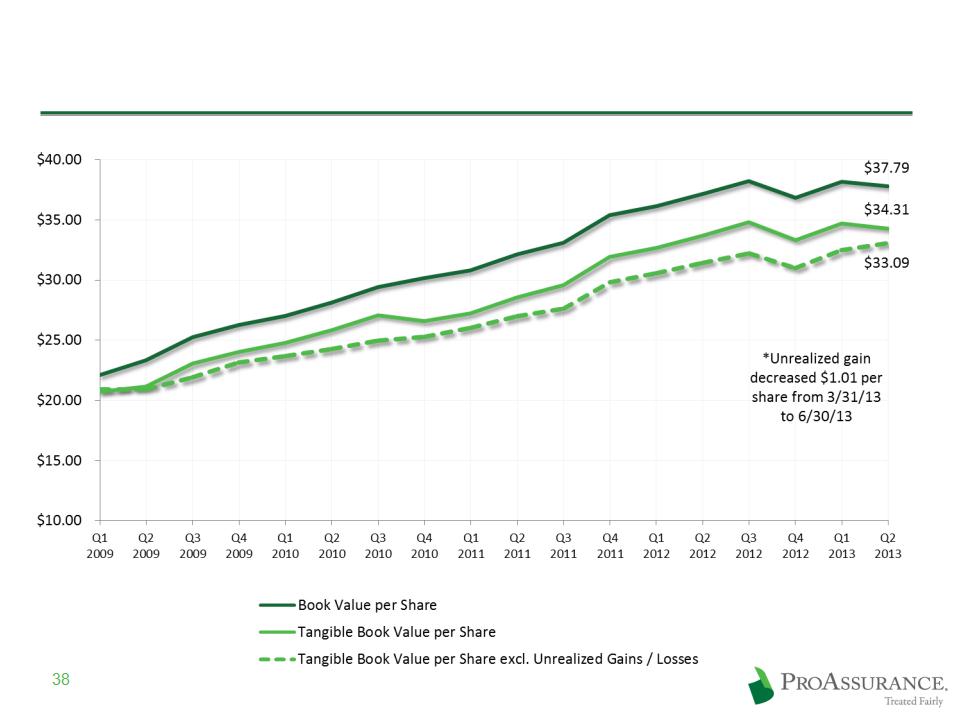

Book Value per Share $ 37.79 $36.85 +3%

29

Long-Term Financial Strength

Our balance sheet is our

top financial priority

top financial priority

Financial strength

differentiates us in

the market

differentiates us in

the market

The claims defense

philosophy that

differentiates us in the

market leverages our

financial strength

philosophy that

differentiates us in the

market leverages our

financial strength

Total Assets

30

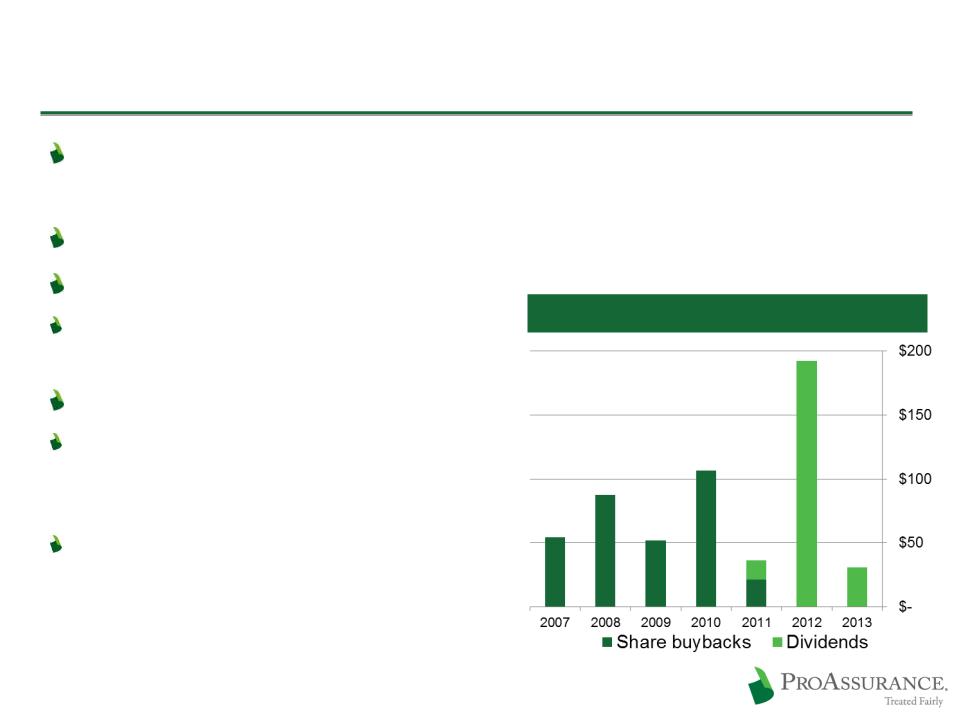

Capital Management Priorities

Balancing our future needs vs. expectations from rating agencies

and investors

and investors

Preferred use is to support growth through M&A or new business

Regular dividend is $1.00/share

~2% yield based on

current share price

current share price

Prudent share repurchase program

$321 million spent to

repurchase 6.1 million shares

since 2005

repurchase 6.1 million shares

since 2005

Repurchasing shares at prices

that enhance shareholder value

and build Book Value

that enhance shareholder value

and build Book Value

31

Returning Capital to Shareholders

$ in millions

Strong capital position us for a firming market

We recognize the effect on ROE

The manner in which

capital is used has an

effect on financial ratings

capital is used has an

effect on financial ratings

Capital Management Priorities

32

Conceptual Model of Projected A. M. Best BCAR Scores if

Excess Capital vs. Excess Capacity

Premiums to Surplus

6/30/13 Premium is annualized

(2x 6/30/13)

(2x 6/30/13)

“A+” Rating

Threshold

Threshold

Capital Management Priorities

No long-term debt

Fully secured by

investments with higher

yields than the

cost of borrowing

investments with higher

yields than the

cost of borrowing

33

Debt to Equity

No Debt Prior to 2001

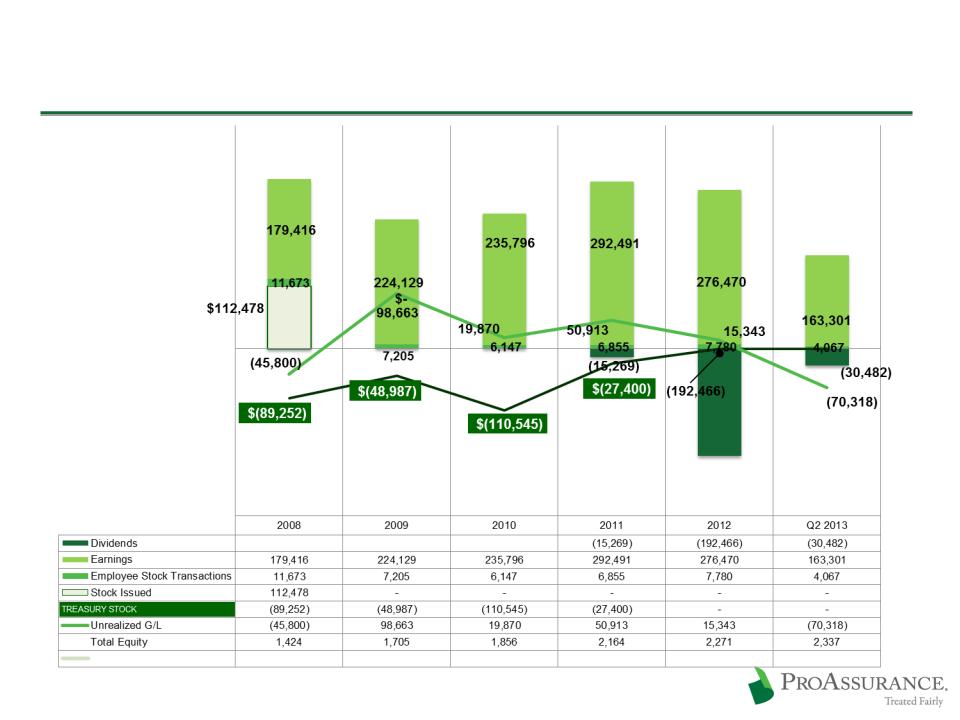

Behind the Numbers

Capital Growth: 2008-Q2 2013

in $000’s except

total equity (000,000’s)

total equity (000,000’s)

* Includes economic cost of holding treasury shares

35

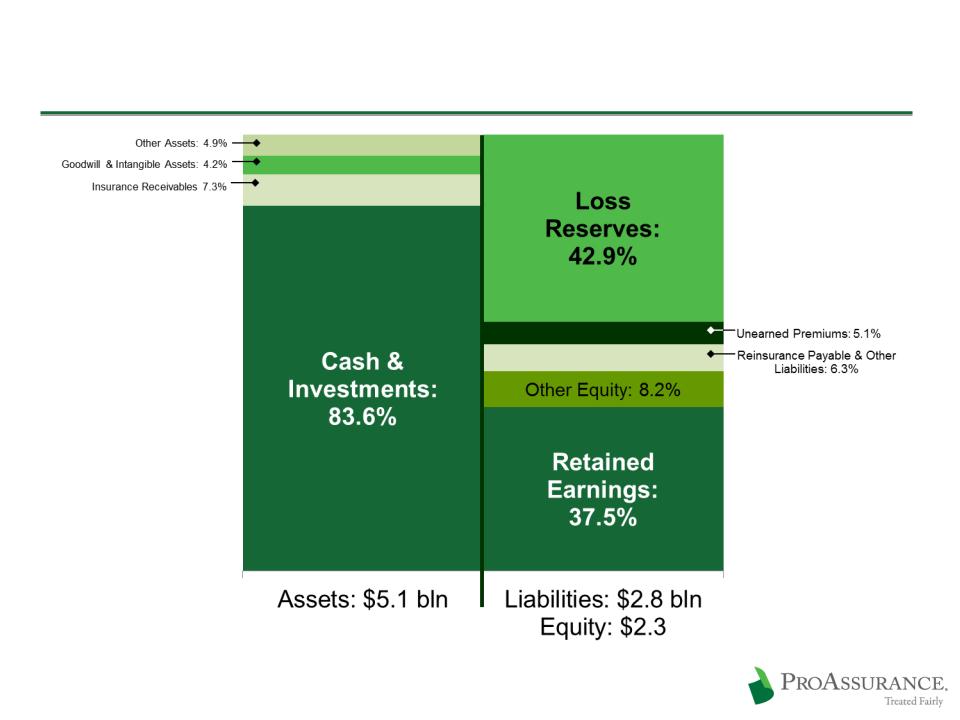

Inside ProAssurance’s Balance Sheet

6/30/13

36

Inside ProAssurance’s Income Statement

6/30/13

37

$35.5 Non-Taxable Gain on Acquisition

Book Value per Share History

Steady Return in an Unfavorable Environment

Long-term ROE target: 12% -14%

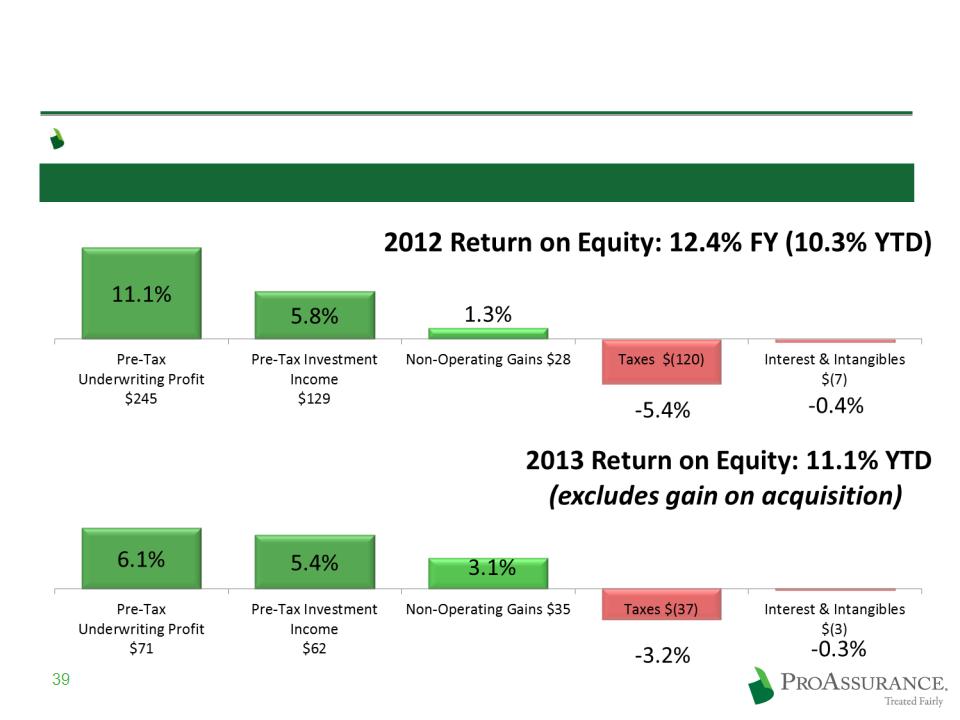

Components of Return on Equity (in millions)

The choice: chase yield or extend duration

We are maintaining duration, looking for

opportunities

opportunities

Pricing discipline becomes even more

critical in a low interest rate environment

critical in a low interest rate environment

Lack of investment yield may be a hard

market catalyst

market catalyst

Return on Equity and Investment Returns

Assumes a 1:1 premium to surplus ratio for physicians

professional liability claims-made coverages

professional liability claims-made coverages

Combined Ratio Required to

Generate a 13% Return on Equity

Generate a 13% Return on Equity

Long-Term ROE Target is 12%-14%

The Yield Trap

Revised to reflect yields at 6/30/13

40

ProAssurance Operational Review

ProAssurance delivers an unparalleled level of

service and financial stability that truly

differentiates our coverage and our Company in an

evolving, competitive market

service and financial stability that truly

differentiates our coverage and our Company in an

evolving, competitive market

Underwriting for Profitability Not Market Share

Underwriting process driven by individual risk

selection and assessment of loss history, areas

of practice, and location

selection and assessment of loss history, areas

of practice, and location

Rates contemplate specific ROE expectations

Frequent rate/loss reviews ensure adequate prices

Rate filings consider the results of the past five to

seven years to ensure a single year does not unduly

influence results

seven years to ensure a single year does not unduly

influence results

Stringent underwriting standards maintain rate

structure and enhance profitability

structure and enhance profitability

42

ProAssurance Pricing History

Peak pricing was in 2006

Improved frequency trends are reflected in recent rate declines

Improvement in frequency has outweighed the steady, manageable rise in severity

Loss trends have improved in states with and without tort reforms

Rate changes (up or down) through 2013 likely will be low-to-mid single digits

MD/DO Rate Change History

PICA excluded to facilitate accurate comparisons over time

43

ProAssurance Retention Remains High

Continued underwriting vigilance is being used today

to ensure future success

to ensure future success

Market share is important, but NOT as important as

profitability

profitability

Retention remains in line with recent quarters

44

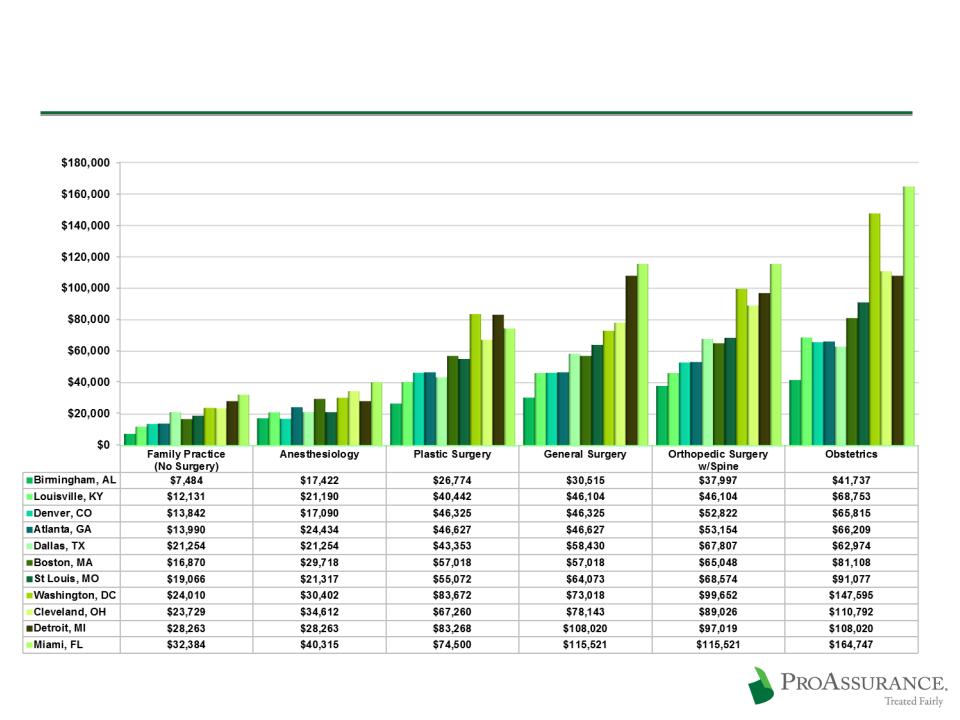

Key State Rate Comparison

Annual Premium for a $1M / $3M Policy

Filed or Approved at 1/01/13

45

Understanding Recent Loss Trends

Frequency stable after

historic declines

historic declines

Lawyers are the gatekeepers

Must weigh the cost of a trial vs.

chances of success

chances of success

Likelihood of success is affected

by many factors

by many factors

Societal perceptions of lawsuits

against physicians

against physicians

Effects of the overall Tort

Reform debate and headlines

across the country

Reform debate and headlines

across the country

Reforms enacted in some states

Better quality of care reduces the

number of medical misadventures

number of medical misadventures

Severity uptrend remains

steady at 2%-3%

steady at 2%-3%

Closely tied to inflation

Primarily medical cost inflation

Jury sentiment in reaction to

headlines has moderated, but

not eliminated, runaway

verdicts in recent years

headlines has moderated, but

not eliminated, runaway

verdicts in recent years

Tort Reforms have limited

non-economic damages in a

number of states

non-economic damages in a

number of states

46

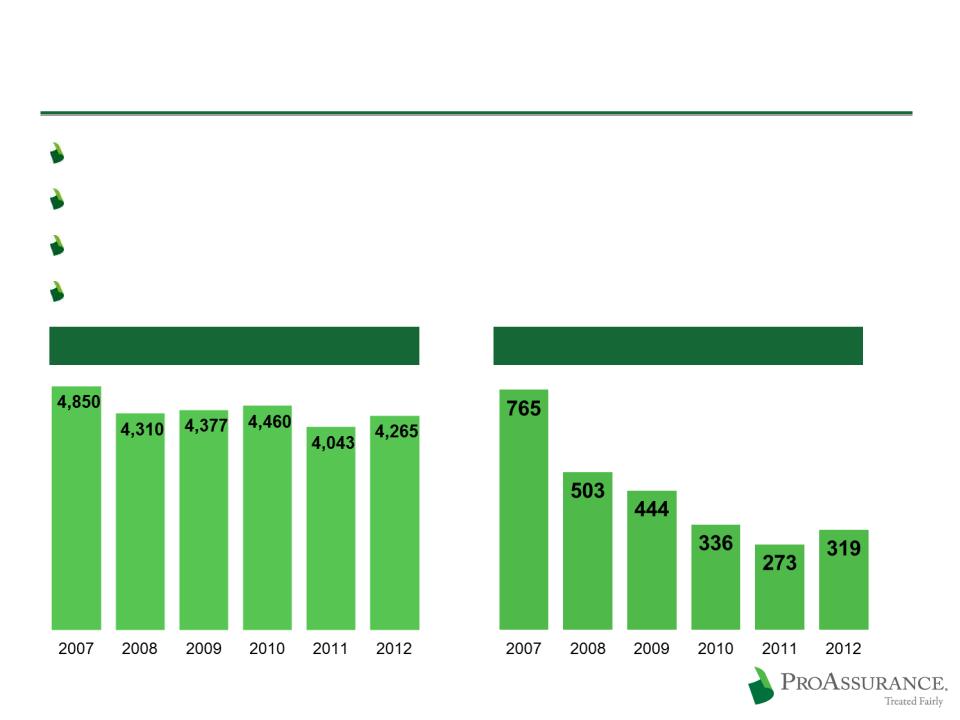

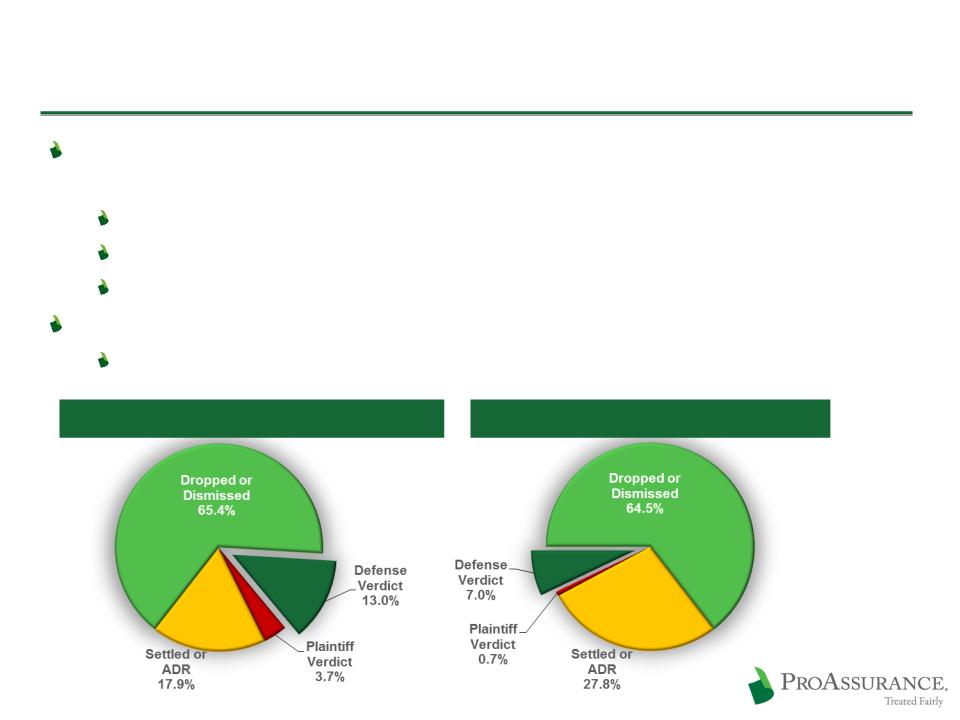

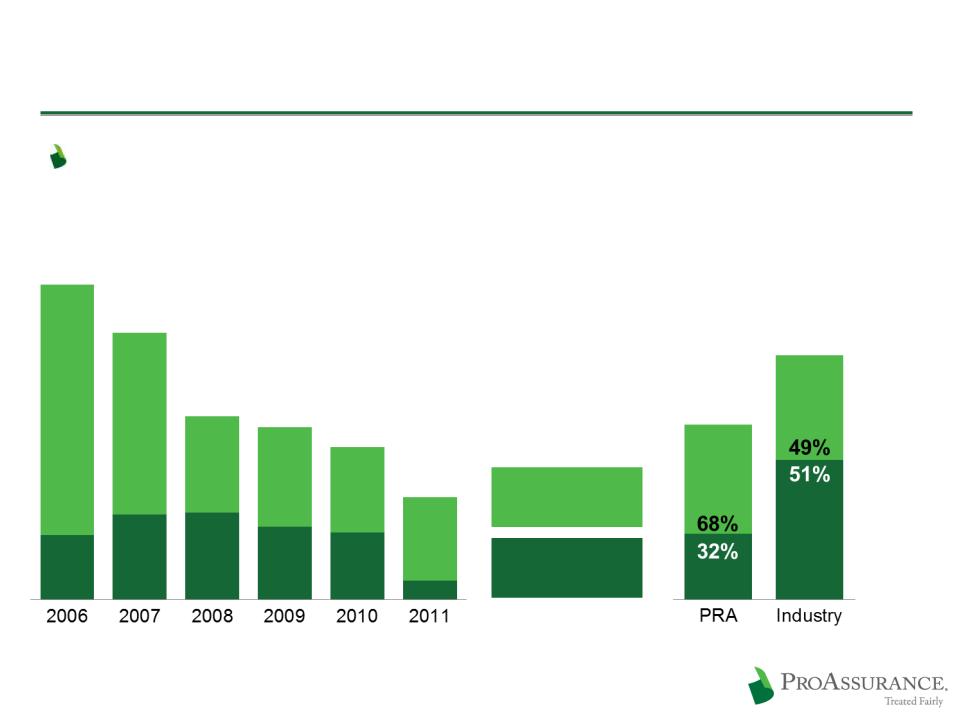

New Claims Opened Each Year

Claims Trends Remain Favorable

Fewer cases to try following significant decline in frequency

Severity trends steady and manageable

No observed effect from the economic downturn

Trends are much the same in states with or without Tort Reform

ProAssurance Claims Tried to a Verdict

47

Differentiate Through Claims Defense

We leverage our financial strength to give our insureds the opportunity for

an uncompromising defense of each claim

an uncompromising defense of each claim

Differentiates our product

Provides long-term financial and marketing advantages

Retains business and deters future lawsuits

Increasingly important as claims data becomes public

Malpractice outcomes now public in 26 states

ProAssurance: 78% No Paid Losses

Industry: 72% No Paid Losses

Source: Preliminary PIAA 2011

Claim Trend Analysis,

ProAssurance Excluded

Claim Trend Analysis,

ProAssurance Excluded

Five Year Average

2007-2011

2007-2011

Source: ProAssurance,

as reported to

PIAA

as reported to

PIAA

48

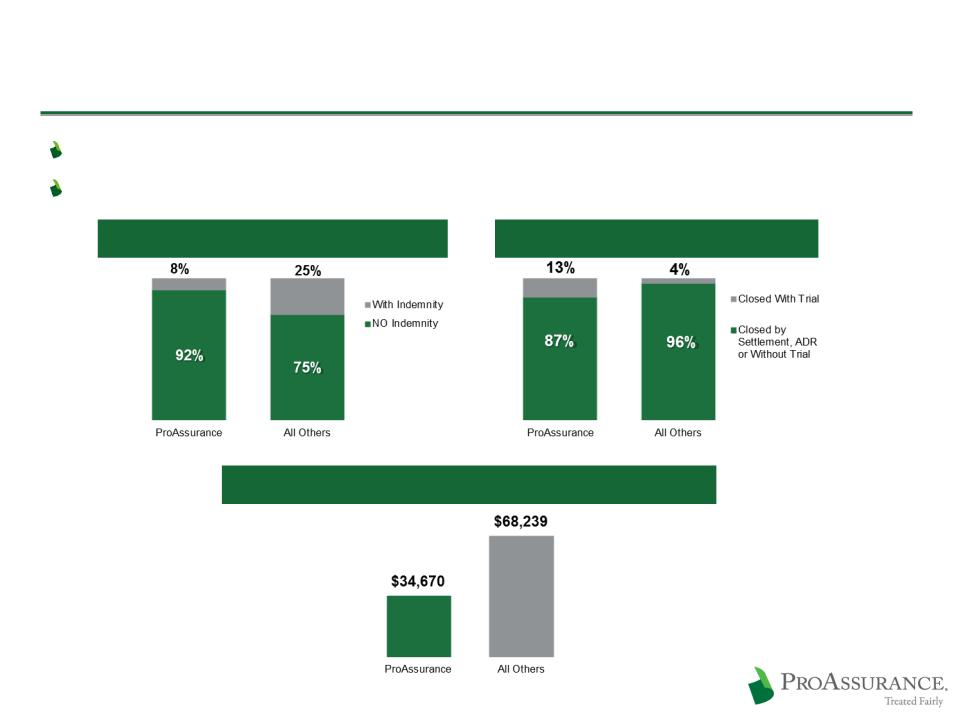

The Ohio Example: 2005 - 2011 Data

Comprehensive, reliable data provided by the Ohio Department of Insurance

Broad range of competitors and business approaches

www.insurance.ohio.gov/Legal/Reports/Documents/2011ClosedClaimReport.pdf

More Claims Closed With No Indemnity

More Claims Defended in Court

2x Lower Average Indemnity Payment per Closed Claim

49

The Bottom Line Benefits of Strong Defense

Our ability and willingness to defend claims allows us

to achieve better results

to achieve better results

Source: Statutory Basis, A.M. Best Aggregates & Averages

Some totals may not agree due to rounding

Some totals may not agree due to rounding

ProAssurance vs. Industry

Average Loss Ratio (2007-2011)

Legal Payments as

a Percentage of

Total Loss Ratio

a Percentage of

Total Loss Ratio

Loss Payments as a

Percentage of Total

Loss Ratio

Percentage of Total

Loss Ratio

64.3%

44.2%

58.9%

42.0%

41.6%

76.0%

36.8%

ProAssurance Stand Alone

Loss Ratio (2006-2011)

Calendar Year

Calendar Year

24.7%

79%

68%

52%

58%

56%

81%

19%

21%

32%

48%

42%

44%

50

51

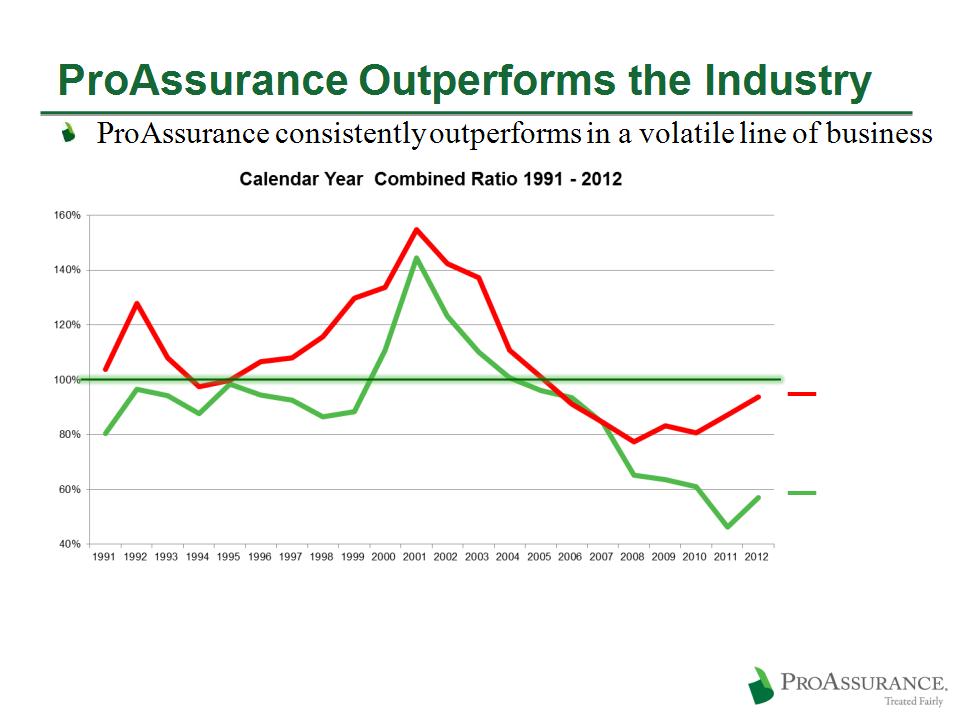

Source: 1991-2011 A.M. Best Aggregates and Averages, Medical Malpractice Lines of Business

2012: Preliminary A. M. Best industry data from special report issued 5/6/13

Five Years: ProAssurance Average: 58.7% / Industry Average: 84.4%

Ten Years: ProAssurance Average: 77.8% / Industry Average: 94.7%

1991-2011: ProAssurance Average: 89.8% / Industry Average: 107.9%

Industry Average

ProAssurance

ProAssurance Outperforms the Industry

2004-2011 A.M. Best Aggregates and Averages, Medical Malpractice Lines of Business

2012: Preliminary SNL Data

Weighted

Average

High/Low

Average

High/Low

Industry

Average

Average

Today’s Healthcare Professional Liability Market

ProAssurance delivers an unparalleled level of

service and financial stability that truly

differentiates our coverage and our Company in an

evolving, competitive market

service and financial stability that truly

differentiates our coverage and our Company in an

evolving, competitive market

HCPL Stands Apart in Insurance

HCPL claims may not be filed for years after an

incident and may take years to resolve: Long-tail

incident and may take years to resolve: Long-tail

Personal lines are short tail

Introduces long periods of uncertainty

Loss trends may change expected severity from time of

initial pricing

initial pricing

Can be mitigated by the use of the claims-made policy form

Can provide a false sense of security for start-ups and

companies seeking to aggregate market share based on price

companies seeking to aggregate market share based on price

Float can be meaningful

HCPL claims are almost always lawsuits

High cost to defend, even if you win

54

The HCPL Market Today

Prolonged period of “benign profitability”

Premiums levels remain well above levels of 2000

Significant policyholder retention by all companies

despite fierce competition

despite fierce competition

No large commercial carriers have entered the market

in a meaningful manner

in a meaningful manner

Significant barriers to entry in underwriting and claims

handling

handling

Psychological barriers exist—failures in the past

No catastrophe exposure

55

The HCPL Market Today

56

The HCPL Market Today

Changes in healthcare delivery are changing the

underlying dynamics

underlying dynamics

Physicians are combining into larger groups

Physician practices are being brought into hospitals through

purchase or affiliation

purchase or affiliation

Hospitals are combining into large networks requiring

greater insurance expertise and greater financial security

greater insurance expertise and greater financial security

Larger companies with geographical reach and

financial strength will have an advantage in attracting

new business and continuing to consolidate

financial strength will have an advantage in attracting

new business and continuing to consolidate

57

The HCPL Market Today

Market remains fragmented even after two

decades of consolidation

decades of consolidation

More than 100 writers

Largest market share is ~8%

87% of top 100 companies have <2%

76% of top 100 companies have <1%

58

ProAssurance’s Standing in HCPL

ProAssurance is the largest independent

publicly-traded writer of HCPL insurance

publicly-traded writer of HCPL insurance

Fourth largest overall writer

DPW: SNL Data 2012

59

Investment Portfolio Detail

ProAssurance remains conservatively

invested, to ensure our ability to keep our

long-term promise of insurance protection

invested, to ensure our ability to keep our

long-term promise of insurance protection

ProAssurance: Investment Profile

$4.2 Billion Overall Portfolio

$3.5 Billion Fixed Income Portfolio

Average duration: 4.0 years

Average tax-equivalent

income yield: Q2 13: 4.3% / Q2 12: 4.5%

income yield: Q2 13: 4.3% / Q2 12: 4.5%

Investment grade: 93%

Weighted average: A+

06/30/13

Tax credit portfolio not reflected in investment

income—provides approximately $17.8 million

in tax credits and $10.9 million in deductions in

2013

income—provides approximately $17.8 million

in tax credits and $10.9 million in deductions in

2013

CUSIP-level portfolio disclosure on our website:

www.proassurance.com/investorrelations/supplemental.aspx

www.proassurance.com/investorrelations/supplemental.aspx

61

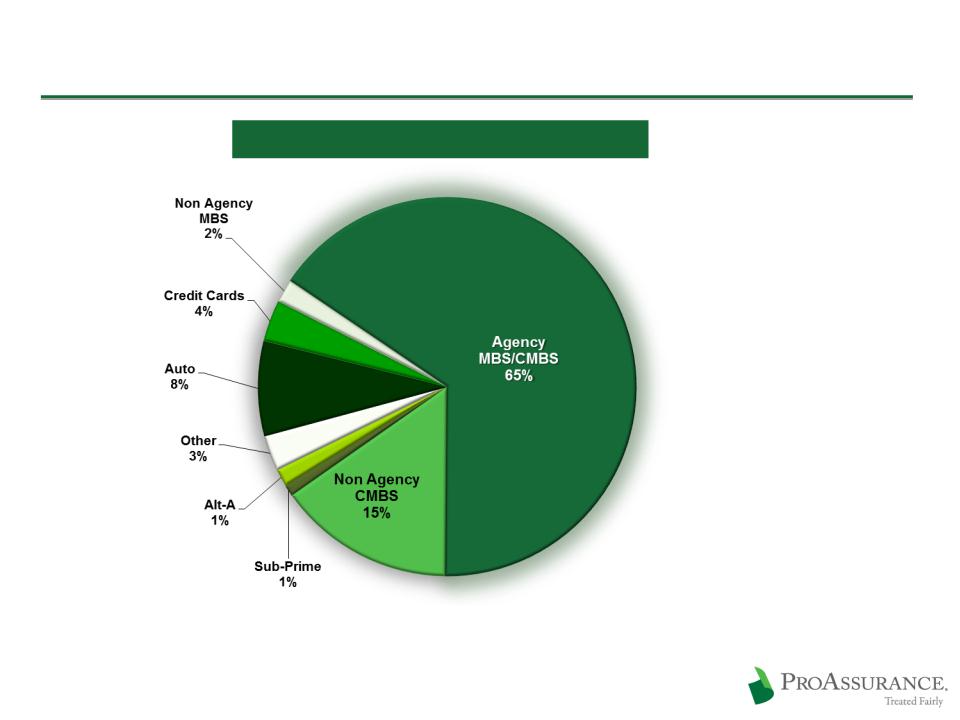

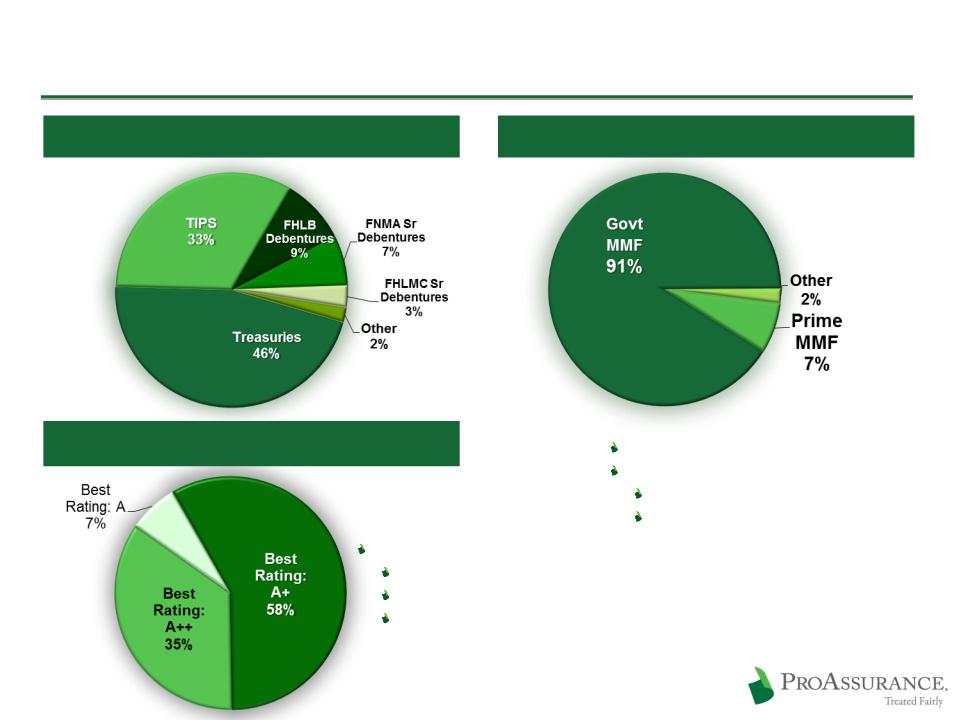

ProAssurance Portfolio Detail: Asset Backed

06/30/13

Subject to Rounding

Asset Backed: $464 Million

Weighted Average Rating: “AA+”

62

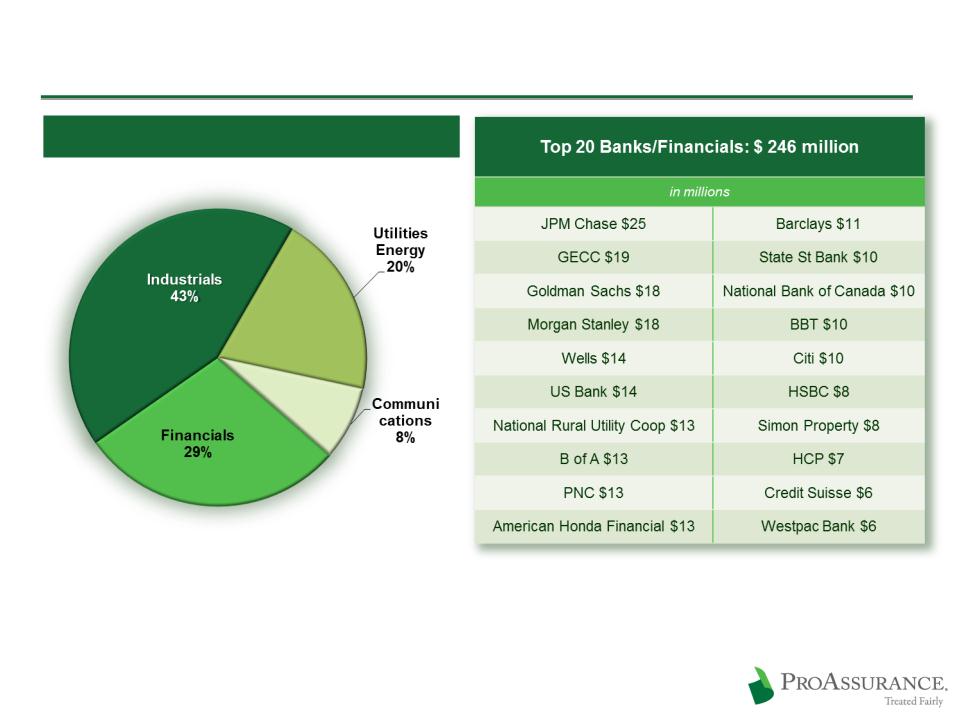

ProAssurance Portfolio Detail: Corporate

Corporates: $1.5 Billion

Weighted Average Rating: A-

6/30/13

63

ProAssurance Portfolio Detail: Municipals

Municipals: $1.3 Billion / Average Rating is AA

Investment policy has always required

investment grade rating prior to applying the

effect of insurance

investment grade rating prior to applying the

effect of insurance

Weighted Average Rating: AA

06/30/13

64

ProAssurance Portfolio Detail: Equities & Other

06/30/13

65

Equities & Other: $482 Million

5.4% TE Book Yield

13% TE IRR

ProAssurance Portfolio Detail: Various

Rated A1/P1 or better

Money Markets:

Moody’s: Aaa

S&P: AAA

Weighted average rating

Moody’s: AA3

S&P: AA-

A. M. Best: A+

Treasury / GSE: $271 Million

Short Term: $87 Million

BOLI: $53 Million

06/3013

66

ProAssurance Transaction Discussion

Medmarc is broadening our product offerings and capabilities in

protecting the delivery of healthcare

protecting the delivery of healthcare

With the acquisition of

Independent Nevada Doctors Insurance Exchange (IND),

ProAssurance becomes the leading

medical professional liability writer in Nevada

Independent Nevada Doctors Insurance Exchange (IND),

ProAssurance becomes the leading

medical professional liability writer in Nevada

Medmarc Transaction Update

A leading products liability writer in medical

technology and life sciences

technology and life sciences

Meaningful legal professional liability book

Acquisition completed effective January 1, 2013

Functioning as an operationally independent

subsidiary

subsidiary

Broad acceptance in Medmarc’s target markets

Coordinated marketing opportunities growing

68

IND Transaction Update

Leading MPL writer in Nevada

Acquisition completed in late November 2012

Integration well underway and proceeding

smoothly

smoothly

New business opportunities evolving as agents

understand the scope and capability of the

combined organizations

understand the scope and capability of the

combined organizations

69