As filed with the Securities and Exchange Commission on November 18, 2022

Commission File No. ______________

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________________

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

__________________________________

JACKSON NATIONAL LIFE INSURANCE COMPANY OF NEW YORK

(Exact Name of registrant as specified in its charter)

__________________________________

| New York | 6311 | 13-3873709 | ||||||||||||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) | ||||||||||||

2900 Westchester Avenue, Purchase, New York 10577

(517) 381-5500

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

__________________________________

Carrie L. Chelko, Esq.

Executive Vice President and General Counsel

Jackson National Life Insurance Company

1 Corporate Way, Lansing, MI 48951

(517) 381-5500

(Name and Address of Agent for Service)

Copy to:

Alison Samborn, Esq.

Associate General Counsel, Insurance Legal

Jackson National Life Insurance Company

1 Corporate Way, Lansing, MI 48951

__________________________________

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: x

If this Form is filed to register addition securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. □

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. □

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. □

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act. □

| Large accelerated filer □ | Accelerated filer □ | Non-accelerated filer x | Smaller reporting company □ | Emerging growth company □ | ||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. □

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

THE INFORMATION IN THE PROSPECTUS IS NOT COMPLETE AND MAY BE CHANGED. WE MAY NOT SELL THE SECURITIES UNTIL THE REGISTRATION STATEMENT FILED WITH THE SECURITIES AND EXCHANGE COMMISSION IS EFFECTIVE. THIS PROSPECTUS IS NOT AN OFFER TO SELL THESE SECURITIES AND IS NOT SOLICITING AN OFFER TO BUY THESE SECURITIES IN ANY STATE WHERE THE OFFER OR SALE IS NOT PERMITTED.

JACKSON MARKET LINK PRO® II

SINGLE PREMIUM DEFERRED INDEX-LINKED ANNUITY

Issued by

Jackson National Life Insurance Company of New York®

The date of this prospectus is __________, 2023. This prospectus contains information about the Contract and Jackson National Life Insurance Company of New York (“Jackson of NY®”) that you should know before investing. This prospectus is a disclosure document and describes all of the Contract’s material features, benefits, rights, and obligations of annuity purchasers under the Contract. The description of the Contract’s material provisions in this prospectus is current as of the date of this prospectus. If certain material provisions under the Contract are changed after the date of this prospectus, in accordance with the Contract, those changes will be described in a supplemented prospectus. It is important that you also read the Contract and endorsements, which may reflect additional non-material variations. Jackson of NY's obligations under the Contract are subject to our financial strength and claims-paying ability. The information in this prospectus is intended to help you decide if the Contract will meet your investment and financial planning needs.

Index-linked annuity contracts are complex insurance and investment vehicles. Before you invest, be sure to discuss the Contract’s features, benefits, risks, and fees with your financial professional in order to determine whether the Contract is appropriate for you based upon your financial situation and objectives. Please carefully read this prospectus and any related documents and keep everything together for future reference.

This prospectus describes the Indexes, Terms, Crediting Methods, and Protection Options that we currently offer under the Contract. We reserve the right to limit the number of Contracts that you may purchase. We also reserve the right to refuse any Premium payment. Please confirm with us or your financial professional that you have the most current prospectus that describe the availability and any restrictions on the Crediting Methods and Protection Options.

The Jackson Market Link Pro II Contract is an individual single Premium deferred registered index-linked annuity Contract issued by Jackson of NY. The Contract provides for the potential accumulation of retirement savings and partial downside protection in adverse market conditions. The Contract is a long-term, tax-deferred annuity designed for retirement or other long-term investment purposes. It is available for use in Non-Qualified plans, Qualified plans, Tax-Sheltered annuities, Traditional IRAs, and Roth IRAs.

Jackson of NY is located at 2900 Westchester Avenue, Purchase, New York, 10577. The telephone number is 1-800-599-5651. Jackson of NY is the principal underwriter for these Contracts. Jackson National Life Distributors LLC (“JNLD”), located at 300 Innovation Drive, Franklin, Tennessee 37067, serves as the distributor of the Contracts.

An investment in this Contract is subject to risk including the possible loss of principal and that loss can become greater in the case of an early withdrawal due to charges and adjustments imposed on those withdrawals. See “Risk Factors” beginning on page 6 for more information.

| Neither the SEC nor any state securities commission has approved or disapproved these securities or passed upon the adequacy of this prospectus. It is a criminal offense to represent otherwise. We do not intend for this prospectus to be an offer to sell or a solicitation of an offer to buy these securities in any state where this is not permitted. | ||

| • Not FDIC/NCUA insured • Not Bank/CU guaranteed • May lose value • Not a deposit • Not insured by any federal agency | ||

| TABLE OF CONTENTS | |||||

| SUMMARY | |||||

| RISK FACTORS | |||||

| Risk of Loss | |||||

| Liquidity | |||||

| Limitations on Transfers | |||||

| Loss of Contract Value | |||||

| No Ownership of Underlying Securities | |||||

| Tracking Index Performance | |||||

| Limits on Investment Return | |||||

| Buffers | |||||

| Elimination, Suspension, Replacements, Substitutions, and Changes to Indexes, Crediting Methods, and Terms | |||||

| Intra-Term Performance Locks | |||||

| Issuing Company | |||||

| Effects of Withdrawals, Annuitization, or Death | |||||

| GLOSSARY | |||||

| THE ANNUITY CONTRACT | |||||

| Owner | |||||

| Annuitant | |||||

| Beneficiary | |||||

| Assignment | |||||

| PREMIUM | |||||

| Minimum Premium | |||||

| Maximum Premium | |||||

| Allocations of Premium | |||||

| Free Look | |||||

| CONTRACT OPTIONS | |||||

| Fixed Account | |||||

| Index Account | |||||

| ADDITIONAL INFORMATION ABOUT THE INDEX ACCOUNT OPTIONS | |||||

| Indexes | |||||

| Protection Options | |||||

| Crediting Methods | |||||

| Cap | |||||

| Performance Trigger | |||||

| Performance Boost | |||||

| TRANSFERS AND REALLOCATIONS | |||||

| Transfer Requests | |||||

| Automatic Reallocation of Fixed Account Value | |||||

| Automatic Reallocation of Index Account Option Value to a New Index Account Option or the Fixed Account | |||||

| Intra-Term Performance Lock | |||||

| End-Term Performance Lock | |||||

| Automatic Rebalancing | |||||

| ACCESS TO YOUR MONEY | |||||

| WITHDRAWAL CHARGE | |||||

Waiver of Withdrawal Charge | |||||

| INCOME PAYMENTS | |||||

| Income Options | |||||

| DEATH BENEFIT | |||||

| Payout Options | |||||

| Pre-Selected Payout Options | |||||

| Spousal Continuation Option | |||||

| Death of Owner On or After the Income Date | |||||

| Death of Annuitant | |||||

| Stretch Contracts | |||||

| TAXES | |||||

| CONTRACT OWNER TAXATION | |||||

| Tax-Qualified and Non-Qualified Contracts | |||||

| Non-Qualified Contracts - General Taxation | |||||

| Non-Qualified Contracts - Aggregation of Contracts | |||||

| Non-Qualified Contracts - Withdrawals and Income Payments | |||||

| Non-Qualified Contracts - Required Distributions | |||||

| Non-Qualified Contracts - 1035 Exchanges | |||||

| Tax-Qualified Contracts - Withdrawals and Income Payments | |||||

| Withdrawals - Roth IRAs | |||||

| Death Benefits | |||||

| Assignment | |||||

| Withholding | |||||

| Annuity Purchases by Nonresident Aliens and Foreign Corporations | |||||

| Definition of Spouse | |||||

| Transfers, Assignments or Exchanges of a Contract | |||||

| Tax Law Changes | |||||

| JACKSON OF NY TAXATION | |||||

| OTHER INFORMATION | |||||

| General Account | |||||

| Unregistered Separate Account | |||||

| Distribution of Contracts | |||||

| Modification of Your Contract | |||||

| Confirmation of Transactions | |||||

| Legal Proceedings | |||||

| JACKSON OF NY | |||||

| CAUTION REGARDING FORWARD-LOOKING STATEMENTS | |||||

| RISKS RELATED TO OUR BUSINESS AND INDUSTRY | |||||

| OUR BUSINESS | |||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS | |||||

| FINANCIAL STATEMENTS | |||||

| APPENDIX A (EXAMPLES OF INTERIM VALUE ADJUSTMENTS UPON WITHDRAWALS, PERFORMANCE LOCK TRANSFERS, AND AUTOMATIC REBALANCING) | A-1 | ||||

SUMMARY

Jackson Market Link Pro II is a Registered Index-Linked Annuity (“RILA”) contract. The Contract is an SEC registered, tax deferred annuity that permits you to link your investment to an Index (or multiple Indexes) over a defined period of time ("term"). If the Index Return is positive, the Contract credits any gains in that Index to your Index Account Option Value, subject to the Crediting Method you choose: a stated Cap Rate, Performance Trigger Rate, or Performance Boost Rate. If the Index Return is negative, the Contract credits losses, which may be absorbed, subject to a Buffer Protection Option.

The Contract currently offers five Indexes that can be tracked in any combination, which allow for the ability to diversify among different asset classes and investment strategies. There is also a one-year Fixed Account available for election.

At the end of an Index Account Option Term, we will credit an Index Adjustment (which may be positive, negative, or equal to zero) based on the Index Return, Crediting Method, and Protection Option of the Index Account Option selected.

Indexes: Each Index is comprised of or defined by certain securities or by a combination of certain securities and other investments. Please refer to the section titled “Indexes” for a description of each of the Indexes offered on this Contract. The Indexes currently offered on the Contract are the S&P 500, Russell 2000, MSCI Emerging Markets, MSCI EAFE, and the MSCI KLD 400 Social Index.

Crediting Methods: Each Crediting Method provides the opportunity to receive an Index Adjustment based on any positive Index Return. The Crediting Methods currently offered on the Contract are the Cap, Performance Trigger, and Performance Boost Crediting Methods. Current Cap Rates, Index Participation Rates, Performance Trigger Rates, Performance Boost Rates, and Performance Boost Cap Rates are provided at the time of application, and to existing owners and financial professionals at any time, upon request.

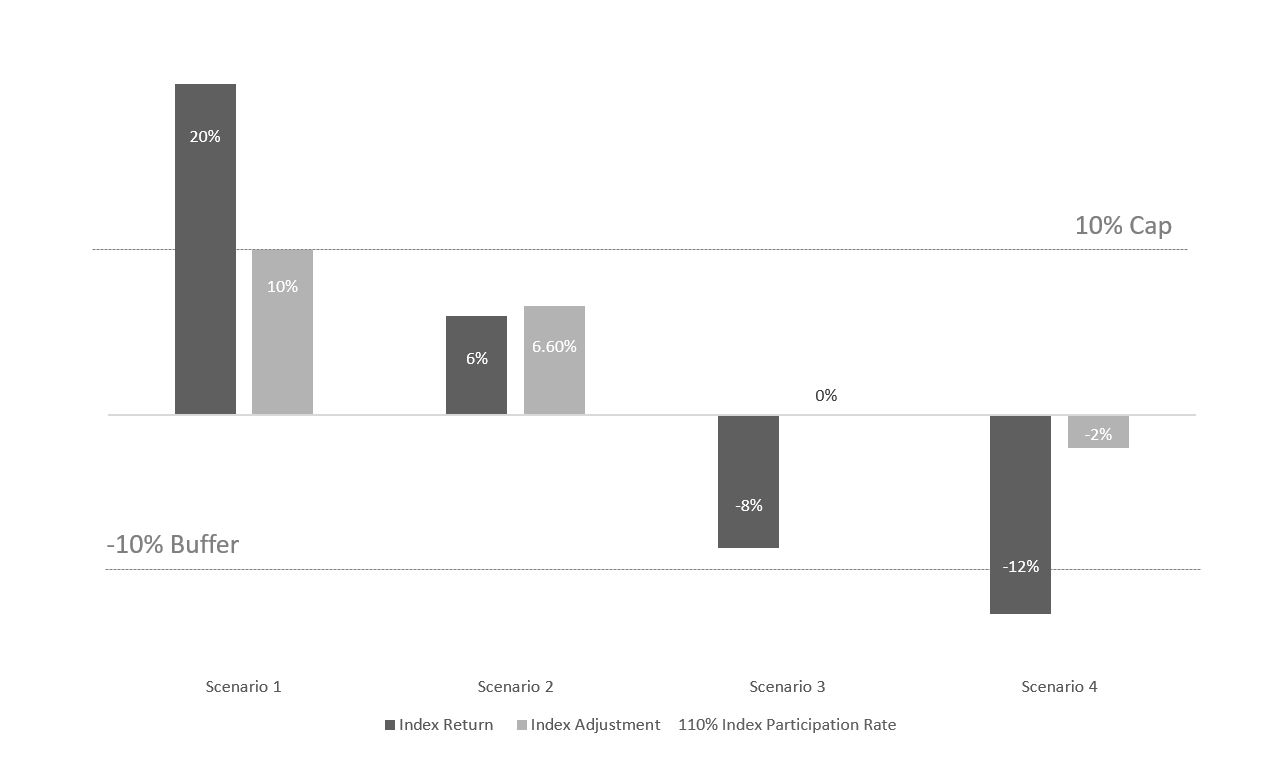

•A Cap Crediting Method provides you the opportunity to receive a positive Index Adjustment equal to the Index Return multiplied by the Index Participation Rate up to a stated Cap Rate if the Index Return is positive at the end of the Index Account Option Term. The Cap Rate is the maximum amount of positive Index Adjustment that you will receive if the Index Return is positive. If the Index Return is less than the stated Cap Rate, you will receive a positive Index Adjustment equal to the Index Return multiplied by the Index Participation Rate. If the Index Return is in excess of the Cap Rate, your positive Index Adjustment will be limited by (and equal to) the Cap Rate. The Index Participation Rate is guaranteed to be at least 100%, and will never serve to reduce an Index Adjustment. An Index Participation Rate or a Cap Rate are not a guarantee of any positive return.

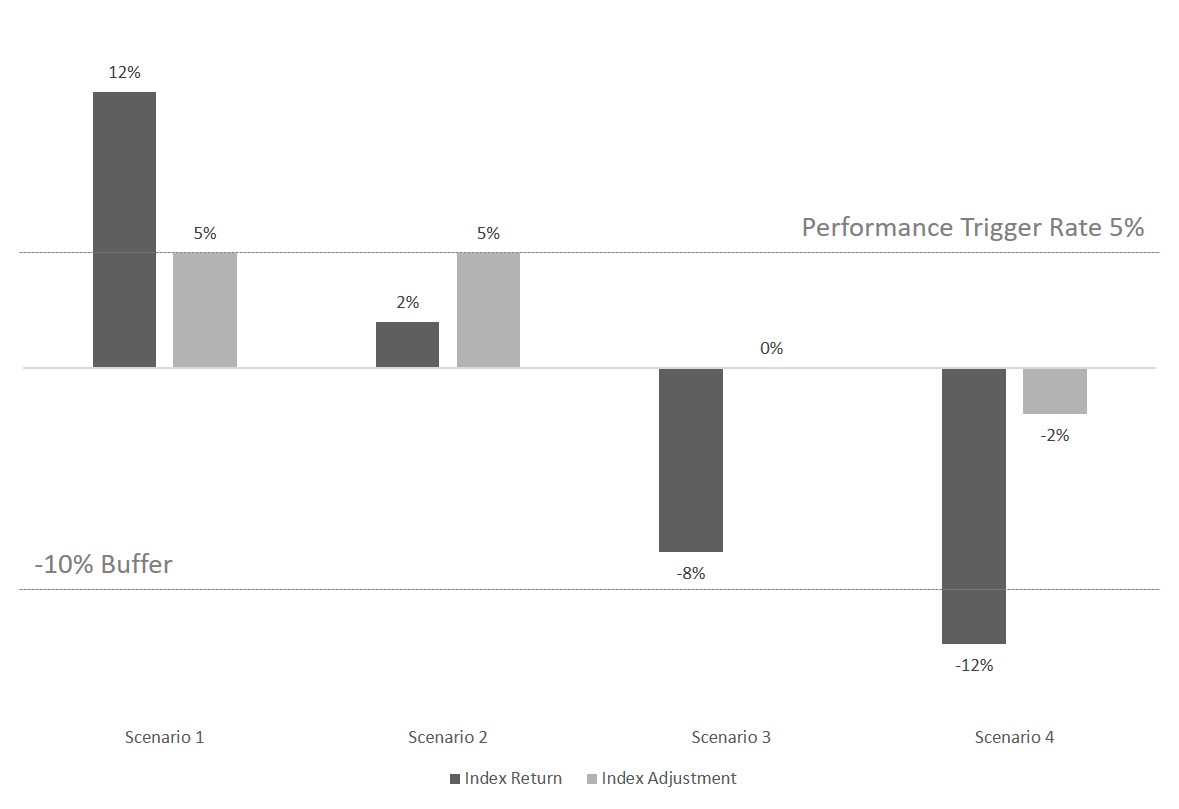

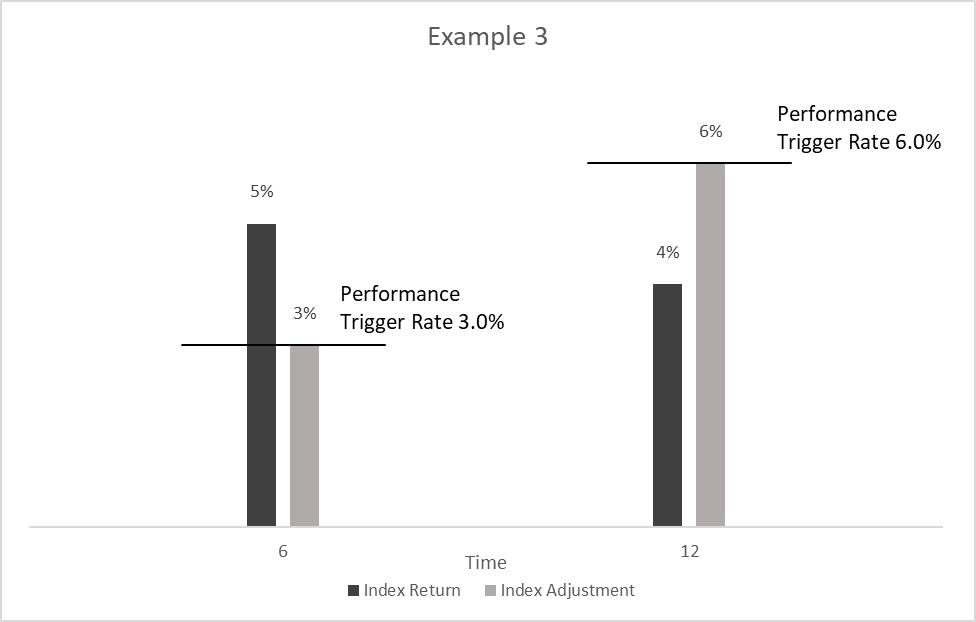

•A Performance Trigger Crediting Method provides you the opportunity to receive a positive Index Adjustment equal to a stated Performance Trigger Rate if the Index Return is flat or positive at the end of the Index Account Option Term. The Performance Trigger Rate equals the positive Index Adjustment that you will receive if the Index Return is flat or positive, regardless of whether the actual Index Return is higher or lower than the stated Performance Trigger Rate. A Performance Trigger Rate is not a guarantee of any positive return.

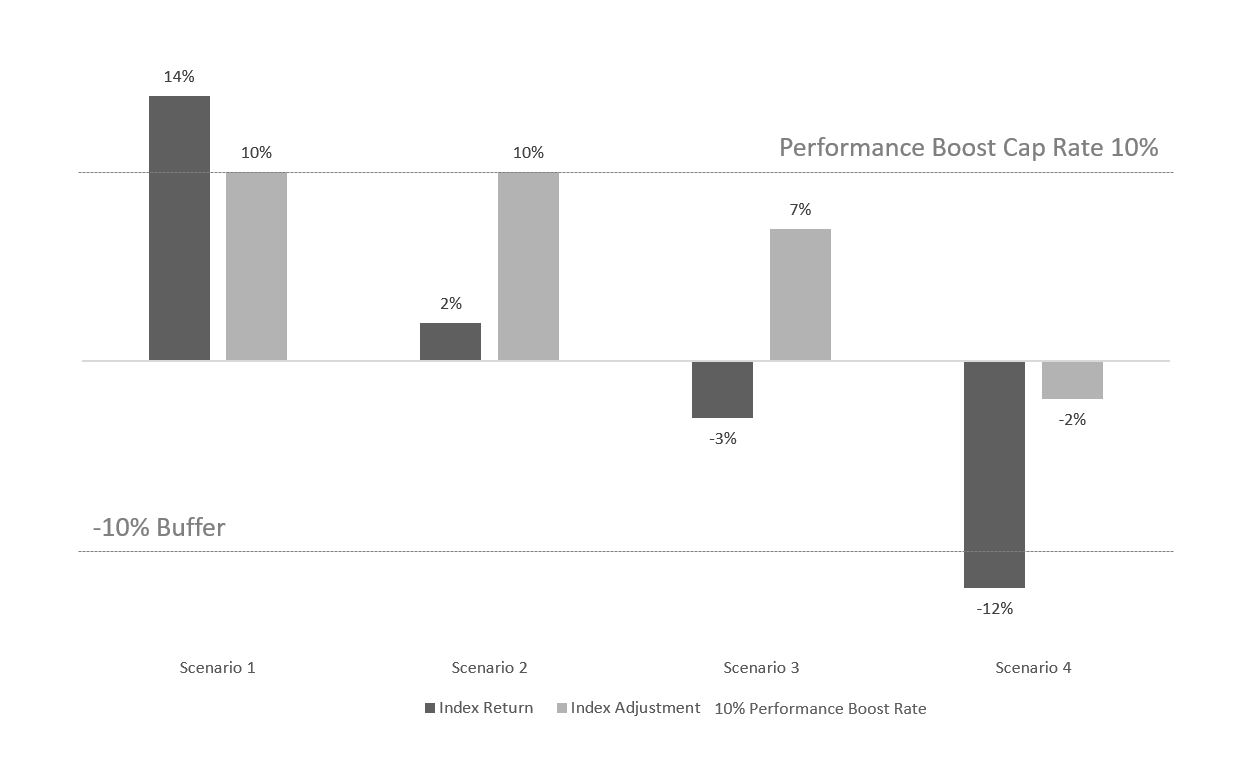

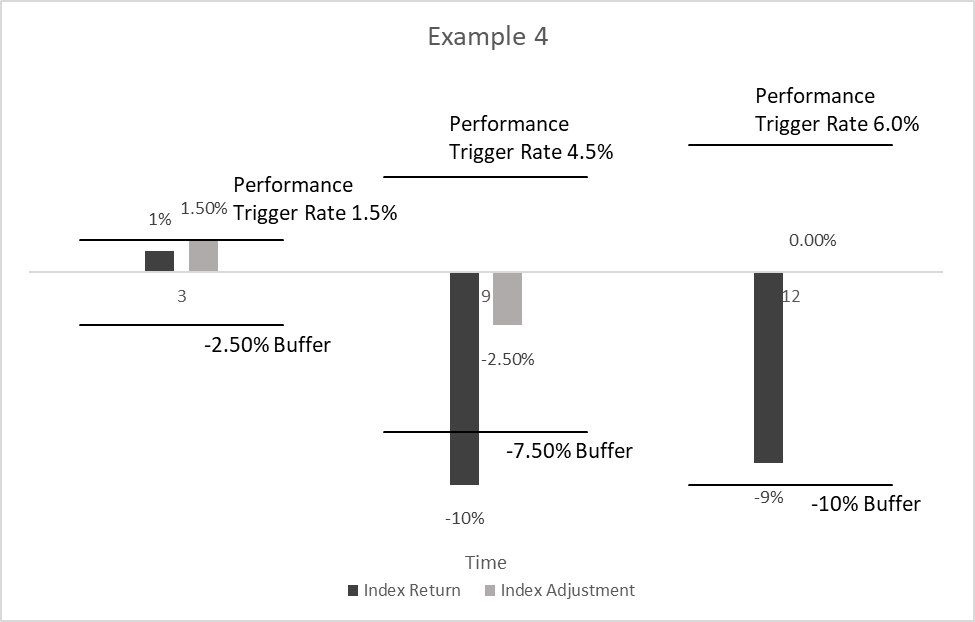

•A Performance Boost Crediting Method provides you the opportunity to receive a positive Index Adjustment equal to Index Return plus the Performance Boost Rate if the Index Return is flat, positive, or negative, but not if the negative return is equal to or in excess of the elected Buffer Protection Option at the end of each Index Account Option Term. Any Index Adjustment credited is limited by a Performance Boost Cap Rate. There are two rates associated with the Performance Boost Crediting Method: the Performance Boost Rate, and the Performance Boost Cap Rate. The Performance Boost Rate is used to boost your Index Adjustment to a value higher than Index Return, and is equal to the Buffer percentage. The Performance Boost Cap Rate limits the amount of positive Index Adjustment you can receive, and is the maximum amount of Index Adjustment that could be credited to an Index Account Option at the end of each Index Account Option Term, expressed as a percentage. The Performance Boost Crediting Method is only available with the Buffer Protection Option. If Index Return is negative in excess of the Buffer, your Index Adjustment will be negative in the amount that the Index Return exceeds the Buffer. A Performance Boost Rate or a Performance Boost Cap Rate are not a guarantee of any positive return.

Protection Options: The Protection Options provide a level of downside protection if the Index Return is negative. We currently offer a Buffer Protection Option. Current Buffer rates are provided at the time of application.

A Buffer protects from loss up to a specific amount (typically 10% or 20%). You only incur a loss if the Index declines more than the stated Buffer percentage. For example, if an Index declines 15% and you chose a 10% Buffer, you would incur a loss of 5% for that Index Account Option Term. Available Buffer rates are guaranteed to be no less than 10% or more than 30%.

1

Index Account Option Terms: The Contract currently offers three term lengths: a 1-Year term, a 3-Year term, and a 6-Year term depending on the Crediting Method and Protection Option you choose.

As of the date of this prospectus, you may currently select the following combination of Crediting Methods, Protection Options, and Index Account Option Terms with any of the available Indexes:

| Crediting Methods | Protection Options* | Term Length | ||||||||||||

| Buffer | 1-Year | 3-Year | 6-Year | |||||||||||

| Cap | 10%, 20% | ü | ü | ü | ||||||||||

| Performance Trigger | 10% | ü | N/A | N/A | ||||||||||

| Performance Boost | 10% | ü | ü | ü | ||||||||||

* Protection Option rates listed above are the rates currently available as of the date of this prospectus. These rates may be changed from time to time, so you should contact your financial professional or the Jackson of NY Customer Care Center for current rate availability.

The available Crediting Method and Protection Option rates are the rates effective as of the first day of an Index Account Option Term. The rate for a particular Index Account Option Term may be higher or lower than the rate for previous or future Index Account Option Terms. At least 30 days prior to any Index Account Option Term Anniversary, we will send you written notice advising you of how you may obtain the available rates for the next Index Account Option Term.

We reserve the right to delete or add Indexes, Crediting Methods, Protection Options, and Index Account Option Terms in the future. At least 30 days prior to the end of your Index Account Option Term, we will send you notice identifying the Indexes, Crediting Methods, Protection Options, or Index Account Option Terms that are available, so that you may tell us how you would like your Index Account Option Value allocated on your Index Account Option Term Anniversary. On your Index Account Option Term Anniversary, your Index Account Option Value will be automatically renewed into the same Index Account Option unless you instruct us to transfer such amount into a different Index Account Option or the Fixed Account, subject to our rules regarding Index Account Option combinations no longer available, or that would extend beyond your Income Date. See "Automatic Reallocation of Index Account Option Value to a New Index Account Option or the Fixed Account" beginning on page 24.

It is possible that an Index may be replaced during an Index Account Option Term. If an Index is replaced during an Index Account Option Term, we will provide you with notice of the substituted Index, and Index Return for the Index Account Option Term will be calculated by adding the Index Return for the original Index from the beginning of the term up until the date of replacement, to the Index Return from the substituted Index starting on the date of replacement through the end of the Index Account Option Term. While any substituted Index will need to be approved by regulators prior to replacing your Index, it is possible that you may experience lower Index Return under a substituted Index than you would have if that Index had not been replaced. For more information about replacing Indexes, please see "Replacing an Index" on page 18. We also reserve the right to remove, add or change the combinations in which we offer Indexes, Crediting Methods, Protection Options and Index Account Option Terms in the future. All Indexes, Crediting Methods, Protection Options, and Index Account Option Terms we currently offer may not be available through every selling broker-dealer.

Fixed Account: You also have the option to invest all or a portion of your Contract Value into a Fixed Account. Amounts allocated to the Fixed Account earn compounded interest at a fixed rate for the duration of the term. Currently, we offer a one-year term for amounts allocated to the Fixed Account and at the end of the one-year term, you will have the option of reallocating those amounts to Index Account Options, or to continue with the amounts in the Fixed Account. The credited interest rate on the Fixed Account is set annually and can be changed as each one-year term resets on the Contract Anniversary, subject to a guaranteed minimum interest rate.

There is also a Short Duration Fixed Account Option, which is a limited-purpose Fixed Account Option only available in connection with Intra-Term Performance Locks and spousal continuation, and may not be independently elected. On each Contract Anniversary, any amounts allocated to the Short Duration Fixed Account Option as part of an Intra-Term Performance Lock, including interest earned on those amounts, will be reallocated into a new Index Account Option identical to the one from which they were originally transferred, subject to availability requirements, unless new allocation instructions have been received by us in Good Order, and will begin a new Index Account Option Term. For more information on availability requirements, see "Automatic Reallocation of Index Account Option Value to a New Index Account Option or the Fixed Account" beginning on page 24. On each Contract Anniversary, any amounts allocated to the Short Duration Fixed Account

2

Option in connection with a spousal continuation adjustment, including interest earned on those amounts, will be reallocated to the 1-year Fixed Account Option unless new allocation instructions have been received by us in Good Order from the spouse continuing the Contract.

Intra-Term Performance Lock: You have the option to lock in Interim Value during each Index Account Option Term on Index Account Options with certain Crediting Methods. This feature allows you to transfer the full Interim Value from your selected Index Account Option into the Short Duration Fixed Account Option, where it will earn the declared Short Duration Fixed Account rate of interest beginning on the the Intra-Term Performance Lock Date until the next Contract Anniversary. An Intra-Term Performance Lock ends the Index Account Option Term for the Index Account Option out of which it is transferred, effectively terminating that Index Account Option. Once an Intra-Term Performance Lock has been processed, it is irrevocable. Intra-Term Performance Lock is not currently available with elections of the Performance Trigger Crediting Method.

Any interest credited to the Contract, whether from allocations to the Index Account Options or the Fixed Account, is backed by the claims-paying ability of Jackson National Life Insurance Company of New York.

You are permitted to make transfers and withdrawals under the terms of the Contract. Transfers among Index Account Options or between Index Account Options and the Fixed Account are permissible only at the end of the Index Account Option Term or Fixed Account term unless you are executing an Intra-Term Performance Lock. Withdrawals taken during the first six years of the Contract may be subject to Withdrawal Charges and withdrawals taken from Index Account Options may be subject to an Interim Value adjustment. Depending on the Crediting Method, Protection Option, Index selected, and the amount of time that has elapsed in the Index Account Option Term, this adjustment could be substantial.

Registered Index-Linked Annuities are long term investments, subject to a potentially substantial loss of principal. Working with a financial professional, you should carefully consider which Indexes, Crediting Methods, and Protection Options (or combinations thereof) are right for you based on your risk tolerance, investment objectives, and other relevant factors. Not all options may be suitable for all investors, including the overall purchase of a RILA.

Contract Overview

| Contract | Individual single premium deferred registered index-linked annuity contract | ||||

| Minimum Premium | $25,000 | ||||

| Issue Ages | 0 - 85 | ||||

| Contract Value | The sum of the Fixed Account Value and the Index Account Value. | ||||

| Index Account Options | Each Index Account Option is defined by an Index, a Crediting Method, a Protection Option, and a Term length. The Crediting Method and Protection Option you choose define the parameters under which the positive or negative Index Adjustment will be credited. | ||||

| Index Account Option Term | Terms currently available under the Contract are 1, 3, and 6 years in length. | ||||

| Index | The Indexes currently offered under the Contract are: - S&P 500 Index - Russell 2000 Index - MSCI EAFE Index - MSCI Emerging Markets Index - MSCI KLD 400 Social Index | ||||

| Crediting Method | The Crediting Methods currently offered under the Contract are: - Cap - Performance Trigger - Performance Boost | ||||

| Protection Options | We currently offer a Buffer Protection Option under the Contract. | ||||

3

| Intra-Term Performance Lock | This feature allows you to lock in your Interim Value prior to the end of your Index Account Option Term on Index Account Options with certain Crediting Methods. If you elect an Intra-Term Performance Lock, your full Interim Value as of the Intra-Term Performance Lock Date will be transferred into the Short Duration Fixed Account Option where it will earn a declared rate of interest for the remainder of the Contract Year. Once an Intra-Term Performance Lock has been processed, it is irrevocable. An Intra-Term Performance Lock ends the Index Account Option Term for the Index Account Option out of which it is transferred, effectively terminating that Index Account Option. Any amounts allocated to the Short Duration Fixed Account Option in connection with an Intra-Term Performance Lock, including interest earned on those amounts, will be reallocated into a new Index Account Option identical to the one from which they were originally transferred, subject to availability requirements, unless new allocation instructions have been received by us in Good Order, and will begin a new Index Account Option Term. Intra-Term Performance Lock is not currently available with elections of the Performance Trigger Crediting Method. For more information, see "Intra-Term Performance Lock" beginning on page 25. | ||||

| Fixed Account | A Contract Option which provides a declared amount of interest over a stated period. | ||||

| Interim Value | The daily value of your Index Account Option on any given Business Day prior to the end of an Index Account Option Term. The Interim Value is calculated using prorated Index Adjustment Factors, where applicable, based on the elapsed portion of the Index Account Option Term. Please note: the Index Participation Rate is never prorated. | ||||

| Transfers | You may request a transfer to or from the Fixed Account and to or from the Index Account Options. You may also request transfers among the available Index Account Options. Transfers among Index Account Options or between Index Account Options and the Fixed Account are permissible only at the end of the Index Account Option Term or Fixed Account term unless you are executing an Intra-Term Performance Lock. The effective date of transfers other than those in connection with an Intra-Term Performance Lock is the first day of the Fixed Account term and/or an Index Account Option Term into which a transfer is made. | ||||

| Access to Your Money | You may withdraw some or all of your money at any time prior to the Income Date. For any withdrawal from an Index Account Option, an Interim Value adjustment as of the date of the withdrawal will apply and may substantially reduce your Index Account Option Value. In addition, a withdrawal taken in excess of the Free Withdrawal amount may be subject to additional Withdrawal Charges. | ||||

| Withdrawal Charge | A percentage charge applied to withdrawals in excess of the Free Withdrawal amount. Withdrawal Charges apply during the first six years of the Contract as follows: Number of Complete Contract Years since Issue Date Withdrawal Charge Percentage 0…………………………………………………..8.00% 1…………………………………………………..8.00% 2…………………………………………………..7.00% 3…………………………………………………..6.00% 4…………………………………………………. 5.00% 5…………………………………………………..4.00% 6 or more………………………………………....…...0.00% For more information about Withdrawal Charges, including details about when you may be entitled to a waiver of Withdrawal Charges, please see the section titled “WITHDRAWAL CHARGE" on page 26. | ||||

| Death Benefit | For Owners 80 or younger at the Issue Date of the Contract, the standard death benefit (known as the Return of Premium death benefit) is the greater of the Contract Value or the Premium you paid into the Contract (reduced proportionately by the percentage reduction in the Index Account Option Value and the Fixed Account Value for each partial withdrawal (including any applicable Withdrawal Charge)). For Owners age 81 or older at the Issue Date of the Contract, the standard death benefit is the Contract Value. | ||||

4

| Income Options | You can choose to begin taking income from your Contract no sooner than 13 months after the Issue Date, or anytime thereafter. All of the Contract Value must be annuitized. Withdrawal Charges (if you begin taking income in the first Contract Year) will apply, and we will use your Interim Value (if you begin taking income on any day other than the Index Account Option Term Anniversary) to calculate your income payments. You may choose from the following annuitization options: - Life Income - Joint Life and Survivor Income - Life Income with Guaranteed Payments for 10 Years or 20 Years - Life Income for a Specified Period Once an income option has been selected, and payments begin, the income option may not be changed. No withdrawals will be permitted once the contract is in the income phase. For more information about income options, please see the section titled "Income Options" on page 29. | ||||

| Charges and Expenses | You will bear the following charges and expenses: - Withdrawal Charges; and - Premium and Other Taxes. | ||||

| Free Look Provision | You may cancel the Contract within a certain time period after receiving it by returning the Contract to us or to the financial professional who sold it to you. This is known as a “Free Look.” We will return your Contract Value and we will not deduct a Withdrawal Charge. Free Looks are subject to Interim Value adjustments. | ||||

5

RISK FACTORS

The purchase of the Contract and the features you elect involve certain risks. You should carefully consider the following factors, in addition to considerations listed elsewhere in this prospectus, prior to purchasing the Contract.

Risk of Loss. An investment in an index-linked annuity is subject to the risk of loss. You may lose money, including the loss of principal.

Liquidity. We designed the Contract to be a long-term investment that you may use to help save for retirement. If you take withdrawals from your Contract during the withdrawal charge period, withdrawal charges may apply. In addition, each time you take a withdrawal, we will recalculate your Index Account Option Value, based on an Interim Value adjustment, which could be positive or negative. In doing so, we use prorated Index Adjustment Factors, where applicable, which serve to reduce any positive Index Adjustment, as well as increase any negative Index Adjustment we credit. Please note: the Index Participation Rate is never prorated. Any negative adjustment could be significant and impact the amount of Contract Value available for future withdrawals. The adjustments and charges that are imposed when amounts are withdrawn before the end of an Index Account Option Term can result in a loss of Contract Value even if the Index Return has been positive. In addition, amounts withdrawn from this Contract may also be subject to taxes and a 10% additional federal tax penalty if taken before age 59½. If you plan on taking withdrawals that will be subject to withdrawal charges and/or taking withdrawals before age 59½, this Contract may not be appropriate for you.

Limitations on Transfers. You can transfer Contract Value among the Index Account Options and the Fixed Account only at designated times (on the Index Account Option Term Anniversary for amounts invested in Index Account Options, and Contract Anniversaries for amounts invested in the Fixed Account). You cannot transfer out of a current Index Account Option to another Index Account Option (or to the Fixed Account) until the Index Account Option Term Anniversary (unless you are executing an Intra-Term Performance Lock) and you cannot transfer out of the Fixed Account to an Index Account Option until the Contract Anniversary. In all cases, the amount transferred can only be transferred to a new Index Account Option or Fixed Account. This may limit your ability to react to market conditions. You should consider whether the inability to reallocate Contract Value during the elected investment terms is consistent with your financial needs and risk tolerance.

In addition, you should understand that for renewals into the same Index Account Option, a new Cap Rate, Index Participation Rate, Performance Trigger Rate, Performance Boost Cap Rate, or Performance Boost Rate will go into effect on the Index Account Option Term Anniversary that coincides with the beginning of the new Index Account Option Term. Such rates could be lower, higher, or equal to your current Crediting Method percentage rate. For more information on how rates are set and communicated, please see the subsection titled "Crediting Methods" under "Additional Information About the Index Account Options".

If we do not receive new instructions at the end of the Index Option Term or prior to a Contract Anniversary to change an allocation, no transfers will occur and your current allocation will remain in place for the next elected term, subject to the availability of your elected Index Account Option. This will occur even if the Fixed Account and/or specific Index Account Option is no longer appropriate for your investment goals. For more information about transfers, please see the section titled "Transfers and Reallocations" on page 24.

Loss of Contract Value. There is a risk of substantial loss of Contract Value (except for amounts allocated to the Fixed Account) due to any negative Index Return that exceeds the Buffer amount. If any negative Index Return exceeds the Buffer you have elected at the end of the Index Account Option Term, you will realize the amount of loss associated with that Protection Option. Buffers are not cumulative, and their protection does not extend beyond the length of any given Index Account Option Term. If you keep amounts allocated to an Index Account Option over multiple Index Account Option Terms in which negative Index Adjustments are made, the total combined loss of Index Account Option Value over those multiple Index Account Option Terms may exceed the stated limit of any applicable Protection Option for a single Index Account Option Term.

No Ownership of Underlying Securities. You have no ownership rights in the securities that comprise an Index. Purchasing the Contract is not equivalent to purchasing shares in a mutual fund that invests in securities comprising the Indexes nor is it equivalent to directly investing in such securities. You will not have any ownership interest or rights in the securities, such as voting rights, or the right to receive dividend payments, or other distributions. Index returns would be higher if they included the dividends from the component securities.

Tracking Index Performance. When you allocate money to an Index Account Option, the value of your investment depends in part on the performance of the applicable Index. The performance of an Index is based on changes in the values of

6

the securities or other investments that comprise or define the Index. The securities comprising or defining the Indexes are subject to a variety of investment risks, many of which are complicated and interrelated. These risks may affect capital markets generally, specific market segments, or specific issuers. The performance of the Indexes may fluctuate, sometimes rapidly and unpredictably. Negative Index Return may cause you to realize investment losses. The historical performance of an Index or an Index Account Option does not guarantee future results. It is impossible to predict whether an Index will perform positively or negatively over the course of a term.

While you will not directly invest in an Index, if you choose to allocate amounts to an Index Account Option, you are indirectly exposed to the investment risks associated with the applicable Index as the Contract performance tracks the Index Return and then your elected Crediting Methods and Protection Option are applied based on that performance. Because each Index is comprised or defined by a collection of equity securities, each Index is exposed to market fluctuations that may cause the value of a security to change, sometimes rapidly and unpredictably.

Limits on Investment Return.

•Cap Rate. If you elect a Cap Crediting Method, the highest possible return that you may achieve on your investment is equal to the Cap Rate, or "Cap". The Cap therefore limits the positive Index Adjustment, if any, that may be credited to your Contract for a given Index Account Option Term. The Caps do not guarantee a certain amount of minimum Index Adjustment credited. Any Index Adjustment based on a Cap Crediting Method may be less than the positive return of the Index. This is because any positive return of the Index that we credit to your Index Account Option Value is subject to a maximum in the form of a Cap, even when the positive Index Return is greater.

•Performance Trigger Rate. If you elect a Performance Trigger Crediting Method, the highest possible return that you may achieve is equal to the Performance Trigger Rate. The Performance Trigger Rate therefore limits the positive Index Adjustment, if any, that may be credited to your Contract for a given Index Account Option Term. The Performance Trigger Rates do not guarantee a minimum Index Adjustment amount. Any Index Adjustment credited for a Performance Trigger Crediting Method may be less than the positive return of the Index. This is because any positive return of the Index that we credit to your Index Account Option Value is always equal to the Performance Trigger Rate, even when the positive Index Return is greater.

•Performance Boost Cap Rate. If you elect a Performance Boost Crediting method, the highest possible return that you may achieve is equal to the Performance Boost Cap Rate. The Performance Boost Cap Rate therefore limits the positive Index Adjustment, if any, that may be credited to your Contract for a given Index Account Option Term. The Performance Boost Cap Rates do not guarantee a minimum Index Adjustment amount. Any Index Adjustment credited for a Performance Boost Crediting Method may be less than the positive return of the Index. This is because any positive return of the Index that we credit to your Index Account Option Value is subject to a maximum in the form of a Performance Boost Cap Rate, even when the positive Index Return is greater. In addition, if the Index Return is negative and equal to or in excess of the elected Buffer, you will not get the benefit of the Performance Boost Rate to increase the value of your Index Adjustment.

Buffers. If you allocate money to an Index Account Option, Index fluctuations may cause an Index Adjustment to be negative at the end of the Index Account Option Term despite the application of the Buffer Protection Option that you elect. If you elect a Buffer, a negative Index Return will result in a negative Index Adjustment if the negative Index Return exceeds the Buffer.

If we credit your Contract with a negative Index Adjustment, your Index Account Option Value will be reduced. Buffers are not cumulative, and their protection does not extend beyond the length of any given Index Account Option Term. Any portion of your Contract Value allocated to an Index Account Option will benefit from the protection of the Buffer for that Index Account Option Term only. A new Buffer will be applied to subsequent Index Account Option Terms. You assume the risk that you will incur a loss and that the amount of the loss could be significant. You also bear the risk that sustained negative Index Return may result in a zero or negative Index Adjustment being credited to your Index Account Option Value over multiple Index Account Option Terms.

If an Index Account Option Value is credited with a negative Index Adjustment for multiple Index Account Option Terms, the total combined loss of Index Account Option Value over those multiple Index Account Option Terms may exceed the stated limit of any applicable Buffer for a single Index Account Option Term.

7

Elimination, Suspension, Replacements, Substitutions, and Changes to Indexes, Crediting Methods, and Terms. We may replace an Index if it is discontinued or if there is a substantial change in the calculation of the Index, or if hedging instruments become difficult to acquire or the cost of hedging becomes excessive. If we substitute an Index, the performance of the new Index may differ from the original Index. If an Index is replaced during an Index Account Option Term, the Index Return for the Index Account Option Term will be calculated by adding the Index Return for the original Index from the beginning of the term up until the date of replacement, to the Index Return from the substituted Index starting on the date of replacement through the end of the Index Account Option Term. A substitution of an Index during an Index Account Option Term will not cause a change in the Crediting Method, Protection Option, or Index Account Option Term length.

Changes to the Cap Rates, Index Participation Rates, Performance Trigger Rates, Performance Boost Rates, and Performance Boost Cap Rates, if any, occur at the beginning of the next Index Account Option Term. We will send you written notice at least 30 days prior to each Index Account Option Term instructing you how to obtain the Cap Rates, Index Participation Rates, Performance Trigger Rates, Performance Boost Rates, and Performance Boost Cap Rates for the next Index Account Option Term. On the Index Account Option Term Anniversary, you may transfer your Index Account Option Value to another Index Account Option or to the Fixed Account without charge. The guaranteed minimum Buffer will not change for the life of your Contract.

We may also add or remove an Index, Index Account Option Term, Crediting Method, or Protection Option during the time that you own the Contract. We will not add any Index, Index Account Option Term, Crediting Method, or Protection Option until the new Index or Crediting Method has been approved by the insurance department in your state. Any addition, substitution, or removal of an Index, Crediting Method, Protection Option, or Index Account Option Term will be communicated to you in writing.

Intra-Term Performance Locks. Because an Intra-Term Performance Lock utilizes Interim Value on the Intra-Term Performance Lock Date, you may receive less on the date you exercise your Intra-Term Performance Lock than you would have had you exercised your Intra-Term Performance Lock on a different date. Because the calculation of Interim Value utilizes pro-rated Index Adjustment Factors, you may receive less than you would have received had you not exercised an Intra-Term Performance Lock and instead remained invested until the end of your Index Account Option Term when you would have realized the full value of your Index Adjustment Factors. Please note: the Index Participation Rate is never prorated. When you exercise an Intra-Term Performance Lock, you must transfer the full Interim Value from the selected Index Account Option to the Short Duration Fixed Account Option, which means you will not get the benefit of any positive Index market performance for the remainder of that Contract Year. Once you have exercised an Intra-Term Performance Lock, the Interim Value transferred to the Short Duration Fixed Account Option will be inaccessible for transfer until the next Contract Anniversary. It is possible that the same combination of options that made up the Index Account Option on which you exercised your Intra-Term Performance Lock may no longer be available or may have different rates once you reach the Contract Anniversary, thus preventing you from being reallocated into an identical Index Account Option. Further, once you have exercised an Intra-Term Performance Lock, it is irrevocable.

Issuing Company. No company other than Jackson of NY has any legal responsibility to pay amounts that Jackson of NY owes under the Contract. The amounts you invest are not placed in a registered separate account, and your rights under the Contract to invested assets and the returns on those assets are subject to the claims paying ability of Jackson of NY. You should review and be comfortable with the financial strength of Jackson of NY for its claims-paying ability.

Effects of Withdrawals, Annuitization, or Death. If any of the following are taken during the Index Account Option Term, they could be subject to Withdrawal Charges as well as an Interim Value adjustment that could reduce your Index Account Option Value: a partial or total withdrawal, Required Minimum Distribution ("RMD"), free look, Intra-Term Performance Lock, income payment, or death benefit payment. Such reduction could be significant. The Interim Value adjustment may result in an Index Adjustment that is less than the Index Adjustment you would have received if you had held the investment until the end of the Index Account Option Term. If you take a withdrawal when the Index Return is negative, your remaining Contract Value may be significantly less than if you waited to take the withdrawal when the Index Return was positive.

All withdrawals, including RMDs, will be taken proportionately from each of your Index Account Options and Fixed Account unless otherwise specified. Withdrawals can also reduce the Death Benefit. Any Return of Premium death benefit will be reduced in a pro-rated amount. Pro rata reductions can be greater than the actual dollar amount of your withdrawal.

In addition, since all withdrawals reduce the Contract Value, withdrawals will also reduce the amount that can be taken as income since such amount is determined by the Contract Value on the Income Date. The Latest Income Date for this contract is age 95.

8

If your Contract Value falls below the minimum contract value remaining as a result of a withdrawal (as stated in your Contract), we may terminate your Contract.

9

GLOSSARY

These terms are capitalized when used throughout this prospectus because they have special meaning. In reading this prospectus, please refer back to this glossary if you have any questions about these terms.

Adjusted Index Return - the percentage change in an Index value measured from the start of an Index Account Option Term to the end of the Index Account Option Term, adjusted based on the elected Cap Rate, Index Participation Rate, Performance Trigger Rate, Performance Boost Rate, Performance Boost Cap Rate, or Buffer.

Annuitant – the natural person on whose life annuity payments for this Contract are based. The Contract allows for the naming of joint Annuitants. Any reference to the Annuitant includes any joint Annuitant.

Beneficiary – the natural person or legal entity designated to receive any Contract benefits upon the Owner’s death. The Contract allows for the naming of multiple Beneficiaries.

Buffer - a Protection Option and an Index Adjustment Factor. A Buffer is the amount of negative Index price change before a negative Index Adjustment is credited to the Index Account Option Value at the end of an Index Account Option Term, expressed as a percentage. A Buffer protects from loss up to a stated amount. You only incur a loss if the Index declines more than the stated Buffer percentage during the Index Account Option Term (though it is possible to incur a loss in excess of the stated Buffer percentage if you make a withdrawal prior to the end of the Index Account Option Term).

Business Day - any day that the New York Stock Exchange is open for business during the hours in which the New York Stock Exchange is open.

Cap Rate ("CR") or Cap - one of three currently available Crediting Methods, and an Index Adjustment Factor. The Cap Rate is the maximum positive Index Adjustment, expressed as a percentage, that will be credited to an Index Account Option under the Cap Crediting Method at the end of each Index Account Option Term after application of the Index Participation Rate.

Contract - the single premium deferred Index-linked annuity contract and any optional endorsements you may have selected.

Contract Anniversary - the Business Day on or immediately following each one-year anniversary of the Issue Date.

Contract Option - one of the options offered by the Company under this Contract. The Contract Options for this product are the Fixed Account and Index Account.

Contract Value - the sum of the allocations to the Fixed Account and the Index Account.

Contract Year - the succeeding twelve months from a Contract’s Issue Date and every anniversary. The first Contract Year (Contract Year 0-1) starts on the Contract’s Issue Date and extends to, but does not include, the first Contract Anniversary. Subsequent Contract Years start on an anniversary date and extend to, but do not include, the next anniversary date.

For example, if the Issue Date is January 15, 2023 then the end of Contract Year 1 would be January 14, 2024, and January 15, 2024, which is the first Contract Anniversary, begins Contract Year 2.

Crediting Method - the general term used to describe a method of crediting the applicable positive Index Adjustment at the end of an Index Account Option Term.

End-Term Performance Lock - a Contract feature that allows for the automatic reallocation of positive Index Adjustments from Index Account Options into the Fixed Account at the end of each Index Account Option Term.

Fixed Account - a Contract Option in which amounts earn a declared rate of interest for a stated period.

Fixed Account Option - An option within the Fixed Account for allocation of Premium or Contract Value defined by its term.

Fixed Account Minimum Interest Rate - the minimum interest rate applied to the Fixed Account, guaranteed for the life of the Contract.

Fixed Account Minimum Value - the minimum guaranteed amount of the Fixed Account Value. The Fixed Account Minimum Value is equal to all amounts allocated to the Fixed Account, reduced by withdrawals (including any applicable Withdrawal Charges) and transfers from the Fixed Account, and taxes, accumulated at the Fixed Account Minimum Interest Rate.

Fixed Account Value - the value of the portion of the Premium allocated to the Fixed Account. The Fixed Account Value is equal to the larger of the Fixed Account Minimum Value or Premium allocated to the Fixed Account, plus interest credited daily at never less than the Fixed Account Minimum Interest Rate for the Contract per annum, less any partial withdrawals including any Withdrawal Charges on such withdrawals, and any amounts transferred out of the Fixed Account.

10

Good Order - when our administrative requirements, including all information, documentation and instructions deemed necessary by us, in our sole discretion, are met in order to issue a Contract or execute any requested transaction pursuant to the terms of the Contract.

Income Date - the date on which Income Payments are scheduled to begin as described in the Income Provisions.

Index - a benchmark used to determine the positive or negative Index Adjustment credited, if any, for a particular Index Account Option.

Index Account - a Contract Option in which amounts are credited positive or negative index-linked interest for a specified period.

Index Account Option - an option within the Index Account for allocation of Premium, defined by its term, Index, Crediting Method, and Protection Option.

Index Account Option Term - the selected duration of an Index Account Option.

Index Account Option Term Anniversary - the Business Day concurrent with or immediately following the end of an Index Account Option Term.

Index Account Option Value - the value of the portion of Premium allocated to an Index Account Option.

Index Account Value - the sum of the Index Account Option Values.

Index Adjustment - an adjustment to Index Account Option Value at the end of each Index Account Option Term, or at the time of withdrawal of Index Account Option Value. Index Adjustments can be positive or negative, depending on the performance of the selected Index, Crediting Method, and Protection Option. The Index Adjustment is equal to the Adjusted Index Return. During an Index Account Option Term, the Index Adjustment is equal to the Adjusted Index Return, further adjusted based on your prorated Index Adjustment Factors, where applicable. Please note: the Index Participation Rate is never prorated.

Index Adjustment Factor(s) - the parameters used to determine the amount of an Index Adjustment. These parameters are specific to the applicable Crediting Method and Protection Option. Cap Rates, Performance Trigger Rates, Performance Boost Rates, Performance Boost Cap Rates, Index Participation Rates, and Buffers are all Index Adjustment Factors.

Index Participation Rate ("IPR") - the percentage applied to any positive Index Return in the calculation of the Index Adjustment for the Cap Crediting Method. The IPR is an Index Adjustment Factor, and is declared at the beginning of the Index Account Option term. The IPR is guaranteed to be at least 100%, and will never serve to decrease an Index Adjustment.

Index Return - the percentage change in an Index value measured from the start of an Index Account Option Term to the end of the Index Account Option Term.

Interim Value - the Index Account Option Value during the Index Account Option Term. The Interim Value is the greater of the Index Account Option Value at the beginning of the term reduced for any withdrawals (including Required Minimum Distributions, income payments, death benefits, and Free Looks) or Intra-Term Performance Locks transferred from the Index Account Option during the term, including any Withdrawal Charges, in the same proportion as the Interim Value was reduced on the date of the withdrawal or Intra-Term Performance Lock, plus the prorated Index Adjustment subject to prorated Index Adjustment Factors, where applicable, or zero. The Index Participation Rate is not prorated. The Interim Value uses applicable prorated Index Adjustment Factors (based on the elapsed portion of the Index Account Option Term), but the Index Participation Rate is not prorated for purposes of calculating Interim Value. The Interim Value is calculated on each date of the Index Account Option Term, and is the amount of Index Account Option Value available for withdrawal or Intra-Term Performance Lock prior to the end of the Index Account Option Term.

Intra-Term Performance Lock- a Contract feature that permits the one-time reallocation of Interim Value from an Index Account Option to the Short Duration Fixed Account Option prior to the end of the Index Account Option Term.

Intra-Term Performance Lock Date - the date Interim Value is reallocated to the Short duration Fixed Account Option in connection with an Intra-Term Performance Lock.

Issue Date - the date your Contract is issued.

Jackson of NY, JNLNY, we, our, or us – Jackson National Life Insurance Company of New York. (We do not capitalize “we,” “our,” or “us” in the prospectus.)

Latest Income Date ("LID") - the date on which you will begin receiving income payments. The Latest Income Date is the Contract Anniversary on which the Owner will be 95 years old, or such date allowed by the Company on a non-discriminatory basis or required by a qualified plan, law or regulation.

11

Owner, you or your – the natural person or legal entity entitled to exercise all rights and privileges under the Contract. Usually, but not always, the Owner is the Annuitant. The Contract allows for the naming of joint Owners. (We do not capitalize “you” or “your” in the prospectus.) Any reference to the Owner includes any joint Owner.

Performance Boost Cap Rate ("PBCR") - an Index Adjustment Factor associated with the Performance Boost Crediting Method. The PBCR is the maximum positive Index Adjustment, expressed as a percentage, that could be credited to an Index Account Option under the Performance Boost Crediting Method at the end of each Index Account Option Term.

Performance Boost Rate ("PBR") - one of three currently available Crediting Methods, and an Index Adjustment Factor. The PBR is the amount that will be added to Index Return, expressed as a percentage, that will increase value of the Index Adjustment that will be credited to an Index Account Option under the Performance Boost Crediting Method at the end of each Index Account Option Term if the performance criteria are met. The Index Adjustment credited under the Performance Boost Crediting Method is limited by the Performance Boost Cap Rate.

Performance Trigger Rate ("PTR") - one of three currently available Crediting Methods, and an Index Adjustment Factor. The PTR is the amount of positive Index Adjustment, expressed as a percentage, that will be credited to an Index Account Option under the Performance Trigger Crediting Method at the end of each Index Account Option Term if the performance criteria are met.

Premium - consideration paid into the Contract by or on behalf of the Owner. The maximum Premium payment you may make without prior approval is $1 million. This maximum amount is subject to further limitations at any time.

Protection Option - the general term used to describe the Buffer Index Adjustment Factor. Protection Options provide varying levels of partial protection against the risk of loss of Index Account Option Value when Index Return is negative.

Remaining Premium - total Premium paid into the Contract, reduced by withdrawals of Premium, including Withdrawal Charges, before withdrawals are adjusted for any applicable charges.

Withdrawal Charge - a charge that is applied to withdrawals in excess of the free withdrawal during the first six years of the Contract, expressed as a percentage of Remaining Premium,

Withdrawal Value - the amount payable upon a total withdrawal of Contract Value. The Withdrawal Value is equal to the Contract Value, subject to any applicable positive or negative Interim Value adjustment, less any applicable Withdrawal Charge.

12

THE ANNUITY CONTRACT

Your Contract is a contract between you, the Owner, and us. The Contract is an individual single Premium deferred index-linked annuity. Your Contract and any endorsements are the formal contractual agreement between you and the Company.

Your Contract is intended to help facilitate your retirement savings on a tax-deferred basis, or other long-term investment purposes, and provides for a death benefit. Purchases under tax-qualified plans should be made for other than tax deferral reasons. Tax-qualified plans provide tax deferral that does not rely on the purchase of an annuity contract. We will not issue a Contract to someone older than age 85.

Your Premium and Contract Value may be allocated to:

•the Fixed Account, in which amounts earn a declared rate of interest for a certain period,

•the Index Account, in which amounts may be allocated to the Index Account Options, which are currently available with a variety of Crediting Methods and term lengths, and certain Protection Options, all of which may be credited with a positive or negative Index Adjustment based upon the performance of a specified Index.

Your Contract, like all deferred annuity contracts, has two phases:

•the accumulation phase, when your Premium may accumulate value based upon the Index Adjustment and/or Fixed Account interest credited, and

•the income phase, when we make income payments to you.

As the Owner, you can exercise all the rights under your Contract. In general, joint Owners jointly exercise all the rights under the Contracts. In some cases, such as telephone and internet transactions, joint Owners may authorize each joint Owner to act individually. On jointly owned Contracts, correspondence and required documents will be sent to the address of record of the first Owner identified in your Contract.

Owner. As Owner, you may exercise all ownership rights under the Contract. Usually, but not always, the Owner is the Annuitant. The Contract allows for the naming of joint Owners. Only two joint Owners are allowed per Contract. Any reference to the Owner includes any joint Owner. Joint Owners have equal ownership rights, and as such, each Owner must authorize any exercise of Contract rights unless the joint Owners instruct us in writing to act upon authorization of an individual joint Owner.

Ownership Changes. To the extent allowed by law, we reserve the right to refuse ownership changes at any time on a non-discriminatory basis, as required by applicable law or regulation. You may request to change the Owner or joint Owner of this Contract by sending a signed, dated request to our Customer Care Center. The change of ownership will not take effect until it is approved by us, unless you specify another date, and will be subject to any payments made or actions taken by us prior to our approval. We will use the oldest Owner's age for all Contract purposes. No person whose age exceeds the maximum issue age allowed by Jackson of NY as of the Issue Date of the Contract may be designated as a new Owner.

Jackson of NY assumes no responsibility for the validity or tax consequences of any ownership change. If you make an ownership change, you may have to pay taxes. We encourage you to seek legal and/or tax advice before requesting any ownership change.

Annuitant. The Annuitant is the natural person on whose life income payments for this Contract are based. If the Contract is owned by a natural person, you may change the Annuitant at any time before you begin taking income payments by sending a written, signed and dated request to the Customer Care Center. If the Contract is owned by a legal entity, we will use the oldest Annuitant's age for all Contract purposes unless otherwise specified in your Contract. Contracts owned by legal entities are not eligible for Annuitant changes. The Annuitant change will take effect on the date you signed the change request, unless you specify otherwise, subject to any payments made or actions taken by us prior to receipt of the request in Good Order. We reserve the right to limit the number of joint Annuitants to two. If the Contract is owned by a legal entity, the Annuitant(s) will be entitled to the benefits of the waivers of Withdrawal Charges for extended care, as described more fully in your Contract.

13

Beneficiary. The Beneficiary is the natural person or legal entity designated to receive any Contract benefits upon the first Owner's death. The Contract allows for the naming of multiple Beneficiaries. You may change the Beneficiary(ies) by sending a written, signed and dated request to the Customer Care Center. If an irrevocable Beneficiary was previously designated, that Beneficiary must consent in writing to any change of Beneficiary(ies). The Beneficiary change will take effect on the date you signed the change request, subject to any payments made or actions taken by us prior to receipt of the request in Good Order.

Assignment. To the extent allowed by law, we reserve the right to refuse assignments at any time on a non-discriminatory basis, as required by applicable law or regulation. You may request to assign this Contract by sending a signed, dated request to our Customer Care Center. The assignment will take effect on the date we approve it, unless you specify another date, subject to any payments made or actions taken by us prior to our approval. Your right to assign the Contract is subject to the interest of any assignee or irrevocable Beneficiary. If the Contract is issued pursuant to a qualified plan, it may not be assigned except under such conditions as may be allowed under the plan and applicable law. Generally, an assignment or pledge of a non-qualified annuity is treated as a distribution.

Jackson of NY assumes no responsibility for the validity or tax consequences of any assignment. We encourage you to seek legal and/or tax advice before requesting any assignment.

PREMIUM

Minimum Premium:

•$25,000 under most circumstances

Maximum Premium:

•The maximum Premium payment you may make without our prior approval is $1 million.

We reserve the right to waive minimum and maximum Premium amounts in a non-discriminatory manner. Our right to restrict Premium to a lesser maximum amount may affect the benefits under your Contract.

Allocations of Premium. You may allocate Premium to any available Indexed Account Option or Fixed Account. Each allocation must be a whole percentage between 0% and 100%. The minimum amount you may allocate to an Indexed Account Option or Fixed Account is $100.

We will issue your Contract and allocate your Premium payment within two Business Days (days when the New York Stock Exchange is open) after we receive your complete Premium payment and all information that we require for the purchase of a Contract in Good Order. We reserve the right to reject a Premium payment that is comprised of multiple payments paid to us over a period of time. If we permit you to make multiple payments as part of your Premium payment, the Contract will not be issued until all such payments are received in Good Order. We reserve the right to hold such multiple payments in a non-interest bearing account until the Issue Date. If we do not receive all information required to issue your Contract, we will contact you to get the necessary information. If for some reason we are unable to complete this process within five Business Days, we will return your money. Each Business Day ends when the New York Stock Exchange closes (usually 4:00 p.m. Eastern time). No Premium will be accepted after the Contract has been issued.

Free Look. You may cancel your Contract by returning it to your financial professional or to us within ten days after receiving it (30 days after receiving it if it was purchased as a replacement Contract). If you cancel your Contract during this period, we will return:

•Premiums paid to the Fixed Account, less

•any withdrawals from the Fixed Account, plus

•the Index Account Value without deduction for any fees and charges.

We will determine the Index Account Value as of the date we receive the Contract. We will pay the applicable free look proceeds within seven days of a request in Good Order. When you exercise a Free Look, amounts returned from Index Account Options are subject to an Interim Value adjustment.

14

CONTRACT OPTIONS

The Contract is divided into two general categories for allocation of your Premium and Contract Value: the Fixed Account, where amounts earn a declared rate of interest for an annually renewable one-year term, and the Index Account, where amounts earn index-linked interest ("Index Adjustment") for a specified term based upon the performance of a selected Index.

Fixed Account. The Fixed Account is an annually renewable account in which amounts you allocate earn a declared rate of interest. Fixed Account interest rates are guaranteed for one year from the date you allocate amounts into the Fixed Account and are subject to change on each Contract Anniversary thereafter. In no event will the interest rate credited to amounts allocated to the Fixed Account be less than the Fixed Account Minimum Interest Rate, as discussed below.

Short Duration Fixed Account Option. The Short Duration Fixed Account Option is a limited-purpose Fixed Account Option that is used for Intra-Term Performance Locks and spousal continuation option adjustments, and cannot be independently elected. Fixed Account interest rates for the Short Duration Fixed Account Option are guaranteed from the date funds are allocated to the Short Duration Fixed Account Option until the next Contract Anniversary. On each Contract Anniversary, any amounts allocated to the Short Duration Fixed Account Option as part of an Intra-Term Performance Lock, including interest earned on those amounts, will be reallocated into a new Index Account Option identical to the one from which they were originally transferred, subject to availability requirements, unless new allocation instructions have been received by us in Good Order, and will begin a new Index Account Option Term. For more information on availability requirements, see "Automatic Reallocation of Index Account Option Value to a New Index Account Option or the Fixed Account" beginning on page 24. On each Contract Anniversary, any amounts allocated to the Short Duration Fixed Account Option in connection with a spousal continuation adjustment, including interest earned on those amounts, will be reallocated to the 1-year Fixed Account Option unless new allocation instructions have been received by us in Good Order from the spouse continuing the Contract.

Fixed Account Value. The Fixed Account Value is equal to (1) the value of Premium and any amounts transferred into the Fixed Account; (2) plus interest credited daily at a rate not less than the Fixed Account Minimum Interest Rate, per annum; (3) less any gross partial withdrawals, including any Withdrawal Charges on such withdrawals; (4) less any amounts transferred out of the Fixed Account. The Fixed Account Value will never be less than the Fixed Account Minimum Value. The Fixed Account Minimum Value is equal to the greater of (a)any allocations to the Fixed Account, plus interest credited daily at never less than the Fixed Account Minimum Interest Rate per annum, less any partial withdrawals after being reduced for any applicable Withdrawal Charge and taxes, or (b) zero.

Rates of Interest We Credit. This Contract guarantees a Fixed Account Minimum Interest Rate that applies to amounts allocated to the 1-year Fixed Account Option as well as the Short Duration Fixed Account Option. The Fixed Account Minimum Interest Rate guaranteed by the Contract will be no less than the minimum non-forfeiture rate. The minimum non-forfeiture rate will be determined by Jackson of NY, pursuant to the requirements outlined by the Standard Nonforfeiture Law for Individual Deferred Annuities. The Fixed Account Minimum Interest Rate is guaranteed for the life of the Contract. In addition, we establish a declared rate of interest ("base interest rate") at the time you allocate any amounts to the Fixed Account, and that base interest rate will apply to that allocation for the entire one-year Fixed Account term. To the extent that the base interest rate that we establish for any allocation is higher than the Fixed Account Minimum Interest Rate, we will credit that allocation with the higher base interest rate. Thus, the declared base interest rate could be greater than the guaranteed Fixed Account Minimum Interest Rate specified in your Contract, but will never cause your allocation to be credited at less than the currently applicable Fixed Account Minimum Interest Rate. On each Contract Anniversary, the base interest rate is subject to change. Different base interest rates apply to the Short Duration Fixed Account Option.

Index Account. Amounts allocated to the Index Account are credited with an Index Adjustment at the end of each Index Account Option Term based upon the performance of the selected Index, Crediting Method, and Protection Option. Your selections from available options make up what are referred to as Index Account Options, which are available with different combinations of Indexes, Protection Options, Crediting Methods, and term lengths. As of the date of this prospectus, the following options are currently available for election with any of the Indexes:

15

| Crediting Methods | Protection Options* | Term Length | ||||||||||||

| Buffer | 1-Year | 3-Year | 6-Year | |||||||||||

| Cap | 10%, 20% | ü | ü | ü | ||||||||||

| Performance Trigger | 10% | ü | N/A | N/A | ||||||||||

| Performance Boost | 10% | ü | ü | ü | ||||||||||

* Protection Option rates listed above are the rates currently available as of the date of this prospectus. These rates may be changed from time to time, so you should contact your financial professional or the Jackson of NY Customer Care Center for current rate availability.

Crediting Method and Protection Option Rates. Available rates for Crediting Methods and Protection Options are the rates effective as of the first day of your Index Account Option Term. The rates for a particular Index Account Option Term may be higher or lower than the rates for previous or future Index Account Option Terms. At least 30 days prior to any Index Account Option Term Anniversary, we will send you written notice advising you of how you may obtain the rates for the next Index Account Option Term. You may also request current rates at any time by contacting your financial professional or the Jackson of NY Customer Care Center. Guaranteed minimum and maximum rates for each Crediting Method and Protection Option are listed below in the sections for each specific Crediting Method and Protection Option.

Index Account Value. The Index Account Value is equal to the sum of all the Index Account Option Values.

Index Account Option Value. When you allocate Contract Value to an Index Account Option for an Index Account Option Term, your investment in the Index Account Option is represented by an Index Account Option Value. Your Index Account Option Value is the portion of your Contract Value allocated to that Index Account Option at any given time. If you allocate Contract Value to multiple Index Account Options at the same time, you will have a separate Index Account Option Value for each Index Account Option in which you are invested. The minimum amount you may allocate to an Index Account Option is $100.

•At the beginning of the Index Account Option Term, your Index Account Option Value is equal to the Premium allocated or Contract Value transferred to the Index Account Option, less any amount transferred out of the Index Account Option.

•During the Index Account Option Term, your Index Account Option Value is equal to the Interim Value, which is equal to the Index Account Option Value at the beginning of the Index Account Option Term, reduced for any partial withdrawals taken from the Index Account Option during the current Index Account Option Term (including any Withdrawal Charges on such withdrawals) in the same proportion that the Interim Value was reduced on the date of any such withdrawal, credited with a positive or negative Index Adjustment. The Index Adjustment credited is subject to prorated Index Adjustment Factors, where applicable, as of the date of the withdrawal. Please note: the Index Participation Rate is not prorated. During the Index Account Option Term, your Interim Value will never be less than zero.

•At the end of the Index Account Option Term, your Index Account Option Value is equal to the Index Account Option Value at the beginning of the Index Option Term reduced for any partial withdrawals taken from the Index Account Option during the current Index Account Option Term (including any Withdrawal Charges on such withdrawals) in the same proportion that the Interim Value was reduced on the date of any such withdrawal, and credited with a positive or negative Index Adjustment. At the end of your Index Account Option Term, your Index Account Option Value will never be less than zero.

16

Index Adjustment. For each Index Account Option to which you allocate Contract Value, at the end of the Index Account Option Term, we will credit your Index Account Option Value with an Index Adjustment. This Index Adjustment can be positive or negative, depending on the performance of the Index and the Crediting Method and Protection Option chosen.

•If the Index Adjustment is positive, your Index Account Option Value will increase by a dollar amount equal to the positive Index Adjustment.

•If the Index Adjustment is negative, your Index Account Option Value will decrease by a dollar amount equal to the negative Index Adjustment.

•If the Index Adjustment is equal to zero, no Index Adjustment will be credited and there will be no adjustment to your Index Account Option Value.

We also credit a positive or negative Index Adjustment during the Index Account Option Term when you exercise an Intra-Term Performance Lock or take a withdrawal. During the term, the Index Adjustment is subject to the prorated Index Adjustment Factors, where applicable, as of the date of the Intra-Term Performance Lock or withdrawal. Please note: the Index Participation Rate is not prorated.