0001129137 amx:MembersOfTheAuditAndCorporatePracticesCommitteeMember 2023-01-01 2023-12-31

As filed with the Securities and Exchange Commission on

April

[

●

] 2024UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM

20-F

☐

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIESEXCHANGE

ACT OF 1934or

☒

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934For the fiscal year ended December 31, 2023 or

or

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934

or

☐

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report

For the transition period from to

Commission file number:

1-16269

AMÉRICA MÓVIL, S.A.B. DE C.V.

(exact name of registrant as specified in its charter)

America Mobile

(translation of registrant’s name into English)

United Mexican States

(jurisdiction of incorporation)Lago Zurich 245, Plaza Carso / Edificio Telcel, Colonia Ampliación Granada, Miguel Hidalgo, 11529, Mexico City, Mexico

(address of principal executive offices)

Daniela Lecuona Torras

Lago Zurich 245, Plaza Carso / Edificio Telcel, Piso 16, Colonia Ampliación Granada, Miguel Hidalgo 11529 Mexico City, Telephone:

(5255) 2581-3700 / Facsimile: (5255) 2581-4422

E-mail:

daniela.lecuona@americamovil.com(name, telephone,

e-mail

and/or facsimile number and address of company contact person)Securities registered pursuant to Section 12(b) of the Act:

TITLE OF EACH CLASS: | TRADING SYMBOL | NAME OF EACH EXCHANGE ON WHICH REGISTERED | ||

| American Depositary Shares, each representing 20 B Shares, without par value | AMX | New York Stock Exchange | ||

| 3.625% Senior Notes Due 2029 | AMX29 | New York Stock Exchange | ||

| 2.875% Senior Notes Dute 2030 | AMX30 | New York Stock Exchanget | ||

| 4.700% Senior Notes Due 2032 | AMX32 | New York Stock Exchange | ||

| 6.375% Senior Notes Due 2035 | AMX35 | New York Stock Exchange | ||

| 6.125% Senior Notes Due 2037 | AMX37 | New York Stock Exchange | ||

| 6.125% Senior Notes Due 2040 | AMX40 | New York Stock Exchange | ||

| 4.375% Senior Notes Due 2042 | AMX42 | New York Stock Exchange | ||

| 4.375% Senior Notes Due 2049 | AMX49 | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

The number of outstanding shares of each of the registrant’s classes of capital or common stock as of December 31, 2023:

62,450 million | B Shares |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | Yes | X | No | |||||

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. | Yes | No | X | |||||

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. | Yes | X | No | |||||

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this Chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). | Yes | X | No | |||||

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act |

X | Large accelerated filer | Accelerated filer | Non-accelerated filer | Emerging growth company |

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. | Yes | X | No | |||||

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. | Yes | No | X | |||||

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). | Yes | No | X | |||||

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing

U.S. GAAP | X | International Financial Reporting Standards as issued by the International Accounting Standards Board | Other | |||||||||

If “other” has been checked in response to the previous question, indicate by check mark which financial statement item | Item | Item | ||||||

the registrant has elected to follow. | 17 | 18 | ||||||

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the | Yes | No | X | |||||

Exchange Act). |

(See Form 20-F Cross Reference Guide on page 98) | ||||

6 | ||||

9 | ||||

| 10 | ||||

| 18 | ||||

| 19 | ||||

| 19 | ||||

| 21 | ||||

23 | ||||

| 24 | ||||

| 26 | ||||

| 34 | ||||

39 | ||||

52 | ||||

| 53 | ||||

| 54 | ||||

| 55 | ||||

| 55 | ||||

| 55 | ||||

| 56 | ||||

| 57 | ||||

62 | ||||

| 63 | ||||

| 67 | ||||

| 69 | ||||

| 72 | ||||

| 73 | ||||

| 75 | ||||

77 | ||||

93 | ||||

| 94 | ||||

| 94 | ||||

| 95 | ||||

| 96 | ||||

| 97 | ||||

| 98 | ||||

| 100 | ||||

103 | ||||

5

We prepared our audited consolidated financial statements included in this annual report in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS”). The selected financial information should be read in conjunction with, and is qualified in its entirety by reference to, our audited consolidated financial statements.

We present our audited consolidated financial statements in Mexican pesos (“Ps.”). This annual report contains translations of various Mexican peso amounts into U.S. dollars at specified rates solely for your convenience. You should not construe these translations as representations that the Mexican peso amounts actually represent the U.S. dollar amounts or could be converted into U.S. dollars at the rate indicated. Unless otherwise indicated, we have translated U.S. dollar amounts from Mexican pesos at the exchange rate of Ps.16.8935 to U.S.$1.00, which was the rate reported by Banco de México on December 29, 2023, as published in the Official Gazette of the Federation (, or “Official Gazette”).

Diario Oficial de la Federación

On August 8, 2022, we completed the

spin-off

of our telecommunications towers and other related passive infrastructure in Latin America outside of Mexico, other than Colombia and our telecommunications towers existing in Peru and in the Dominican Republic prior to thespin-off,

as previously disclosed in our press release furnished on a report on Form6-K

on August 8, 2022. As part of thespin-off

and the associated corporate restructuring, we contributed to Sitios Latinoamérica, S.A.B. de C.V. (“Sitios Latam”) capital stock, assets and liabilities, mainly consisting of the shares of our subsidiaries holding telecommunications towers and other associated infrastructure in Latin America outside of Mexico, other than Colombia and our telecommunications towers existing in Peru and in the Dominican Republic prior to thespin-off.

On February 3, 2023, we completed the sale of all of our telecommunication towers owned by our subsidiary in the Dominican Republic to Sitios Latam for an amount of Ps.2.4 billion. Between March and July, 2023, we completed the sale of all of our telecommunication towers owned by our subsidiary in Peru to Sitios Latam for an amount of Ps.4.0 billion. As a result of thespin-off,

as of our annual report for the fiscal year ended December 31, 2022, the assets and liabilities of Sitios Latam no longerappear in the consolidated financial information included in our annual reports. We maintain commercial relationships with Sitios Latam through our subsidiaries, which are parties to master service agreements for passive infrastructure sharing with Sitios Latam for the use of tower space, property and other equipment. The terms of those agreements for tower space are between five (5) and twelve (12) years, while terms for property and other equipment are usually between five (5) and twenty five (25) years, each with an option to renew.

On October 6, 2022, we combined our Chilean operation, Claro Chile, S.A. (“Claro Chile”), with the Chilean operation of Liberty Latin America, Ltd. (“LLA”), VTR, in order to create Claro Chile, SpA, a 50:50 joint venture (“ClaroVTR”); as a result, Claro Chile ceased to be our wholly owned subsidiary, as previously disclosed in our press release furnished on a report on Form

6-K

on October 6, 2022. In accordance with IFRS 11 Joint Arrangements (“IFRS 11”), ClaroVTR wasclassified

as a joint venture, since we exercise joint control over ClaroVTR with LLA, and all relevant decisions require the consent of both parties. As a result, in accordance with IFRS 5Non-current

Assets Held for Sale and Discontinued Operations (“IFRS 5”), the operations of Claro Chile are classified as discontinued operations for all reporting periods prior to 2023 presented in the consolidated financial information included in this report and are recognized through the equity method from October 6, 2022 onwards. Accordingly, where applicable, results are presented in the profit (loss) after tax from discontinued operations in the consolidated financial information included in this annual report. Operating and financial information presented herein therefore excludes Claro Chile, including for periods prior to the creation of the joint venture. In September 2023, we identified impairment indicators and assessed that there is objective evidence that ClaroVTR is impaired. As a result, an amount of Ps.4.7 billion was recorded as the difference between the recoverable amount of ClaroVTR and its carrying value. Additionally, as of December 31, 2023, we recorded an impairment relating to purchased convertible notes from ClaroVTR totaling Ps.12.2 billion. Both amounts are recorded under “valuation of derivatives, interest cost from labor obligations and other financial items” in our consolidated statements of comprehensive income. See Note 22 to our audited consolidated financial statements.6

FOR THE YEAR ENDED DECEMBER 31, | ||||||||||||||||||||||||||||||||

2021 (2) | 2022 (3)(4) | 2023 | 2023 | |||||||||||||||||||||||||||||

| (in millions of Mexican pesos, except share and per share amounts) | (in millions of U.S. dollars, except share and per share amounts) | |||||||||||||||||||||||||||||||

STATEMENT OF COMPREHENSIVE INCOME DATA: | ||||||||||||||||||||||||||||||||

Operating revenues | Ps. | 830,687 | Ps. | 844,501 | Ps. | 816,013 | U.S. | 48,303 | ||||||||||||||||||||||||

Operating costs and expenses | 506,828 | 514,996 | 496,443 | 29,387 | ||||||||||||||||||||||||||||

Depreciation and amortization | 156,303 | 158,634 | 151,786 | 8,985 | ||||||||||||||||||||||||||||

Operating income | 167,556 | 170,871 | 167,784 | 9,931 | ||||||||||||||||||||||||||||

Net profit for the year from continuing operations | Ps. | 72,090 | Ps. | 88,225 | Ps. | 80,790 | U.S. | 4,782 | ||||||||||||||||||||||||

Net profit (loss) for the year from discontinued operations | 124,236 | - | (6,719 | ) | - | - | ||||||||||||||||||||||||||

Net profit for the year | Ps. | 196,326 | Ps. | 81,506 | Ps. | 80,790 | U.S. | 4,782 | ||||||||||||||||||||||||

NET PROFIT (LOSS) ATTRIBUTABLE FOR THE YEAR TO: | ||||||||||||||||||||||||||||||||

Equity holders of the parent from continuing operations | Ps. | 68,187 | Ps. | 82,878 | Ps. | 76,111 | U.S. | 4,505 | ||||||||||||||||||||||||

Equity holders of the parent from discontinued operations | 124,236 | (6,719 | ) | - | - | |||||||||||||||||||||||||||

Equity holders of the parent | Ps. | 192,423 | Ps. | 76,159 | Ps. | 76,111 | U.S. | 4,505 | ||||||||||||||||||||||||

Non-controlling interests | 3,903 | 5,347 | 4,679 | 277 | ||||||||||||||||||||||||||||

Net profit for the year | Ps. | 196,326 | Ps. | 81,506 | Ps. | 80,790 | U.S. | 4,782 | ||||||||||||||||||||||||

EARNINGS PER SHARE: | ||||||||||||||||||||||||||||||||

Basic and diluted from continuing operations | Ps. | 1.03 | Ps. | 1.30 | Ps. | 1.21 | U.S. | 0.07 | ||||||||||||||||||||||||

Basic and diluted from discontinued operations | Ps. | 1.88 | Ps. | (0.11 | ) | Ps. | - | U.S. | - | |||||||||||||||||||||||

Dividends declared per share (1) | Ps. | 0.40 | Ps. | 0.44 | Ps. | 0.46 | U.S. | 0.03 | ||||||||||||||||||||||||

WEIGHTED AVERAGE NUMBER OF SHARES OUTSTANDING (MILLIONS): | ||||||||||||||||||||||||||||||||

Basic | 65,967 | 63,936 | 63,049 | - | ||||||||||||||||||||||||||||

Diluted | 65,967 | 63,936 | 63,049 | - | ||||||||||||||||||||||||||||

BALANCE SHEET DATA: | ||||||||||||||||||||||||||||||||

Property, plant and equipment, net | Ps. | 731,197 | Ps. | 657,226 | Ps. | 628,651 | U.S. | 37,213 | ||||||||||||||||||||||||

Right of use assets | 90,372 | 121,874 | 113,568 | 6,723 | ||||||||||||||||||||||||||||

Total assets | 1,689,650 | 1,618,099 | 1,564,186 | 92,591 | ||||||||||||||||||||||||||||

Short-term debt and current portion of long-term debt | 145,223 | 102,024 | 160,964 | 9,528 | ||||||||||||||||||||||||||||

Short-term liability related to right-of-use | 27,632 | 32,902 | 24,375 | 1,443 | ||||||||||||||||||||||||||||

Long-term debt | 418,807 | 408,565 | 339,713 | 20,109 | ||||||||||||||||||||||||||||

Long-term liability related to right-of-use | 71,022 | 101,247 | 100,794 | 5,967 | ||||||||||||||||||||||||||||

Capital stock | 96,333 | 95,365 | 95,362 | 5,645 | ||||||||||||||||||||||||||||

Total equity | Ps. | 454,042 | Ps. | 437,829 | Ps. | 421,702 | U.S. | 24,962 | ||||||||||||||||||||||||

NUMBER OF OUTSTANDING SHARES (MILLIONS) (5) : | ||||||||||||||||||||||||||||||||

AA Shares | 20,555 | 20,555 | - | - | ||||||||||||||||||||||||||||

A Shares | 502 | 488 | - | - | ||||||||||||||||||||||||||||

L Shares | 43,633 | 42,282 | - | - | ||||||||||||||||||||||||||||

B Shares | - | - | 62,450 | - | ||||||||||||||||||||||||||||

(1) | Figures for each year provided represent the annual dividend declared at the general shareholders’ meeting for that year. For information on dividends paid per share translated into U.S. dollars, see “Share Ownership and Trading—Dividends” under Part IV of this annual report. |

(2) | On November 23, 2021, we completed the sale of TracFone Wireless, Inc. (“TracFone”) to Verizon Communications Inc. (“Verizon”). As a result of the sale of TracFone, in accordance with IFRS 5, the operations of Tracfone are classified as discontinued operations for the reporting periods prior to 2022 presented in the consolidated financial information included in this annual report. See “Overview—Discontinued Operations” under Part II of this annual report and Note 2 Ac to our audited consolidated financial statements included in this annual report. |

(3) | On July 1, 2022, we completed the sale of the operations of Claro Panama, S.A. (“Claro Panama”) to Cable & Wireless Panama, S.A., an affiliate of LLA. As a result of the sale of Claro Panama, in accordance with IFRS 5, the operations of Claro Panama are classified as discontinued operations for the reporting periods prior to 2023 presented in the consolidated financial information included in this annual report. See “Overview—Discontinued Operations” under Part II of this annual report and Note 2 Ac to our audited consolidated financial statements included in this annual report. |

(4) | As a result of the incorporation of ClaroVTR as a joint venture in 2022, in accordance with IFRS 5, the operations of Claro Chile are classified as discontinued operations for the reporting periods prior to 2023 presented in the consolidated financial information included in this annual report and are recognized through the equity method from October 6, 2022 onwards. See “Overview—Discontinued Operations” under Part II of this annual report and Note 2 Ac to our audited consolidated financial statements included in this annual report. |

(5) | We have not included earnings or dividends on a per American Deposit Share (“ADS”) basis. On December 20, 2022, our shareholders approved the conversion (such conversion, the “Reclassification”) of all of our AA Shares, A Shares and L Shares into a single series of B Shares on a one-for-one |

7

HISTORY AND CORPORATE INFORMATION

América Móvil, S.A.B. de C.V. (“América Móvil,” “we” or the “Company”) is a Sociedad Anónima Bursátil de Capital Variable organized under the laws of Mexico.

We were established in 2000 when Teléfonos de México, S.A.B. de C.V. (“Telmex”), a fixed-line Mexican telecommunications operator privatized in 1990, spun off to us its wireless operations in Mexico and other countries. We have made significant acquisitions throughout Latin America, the United States, the Caribbean and Europe, and we have also expanded our businesses organically.

Our principal executive offices are located at Lago Zurich 245, Plaza Carso / Edificio Telcel, Colonia Ampliación Granada, Miguel Hidalgo, 11529, Mexico City, Mexico. Our telephone number at this location is (5255) 2581-3700.

BUSINESS OVERVIEW

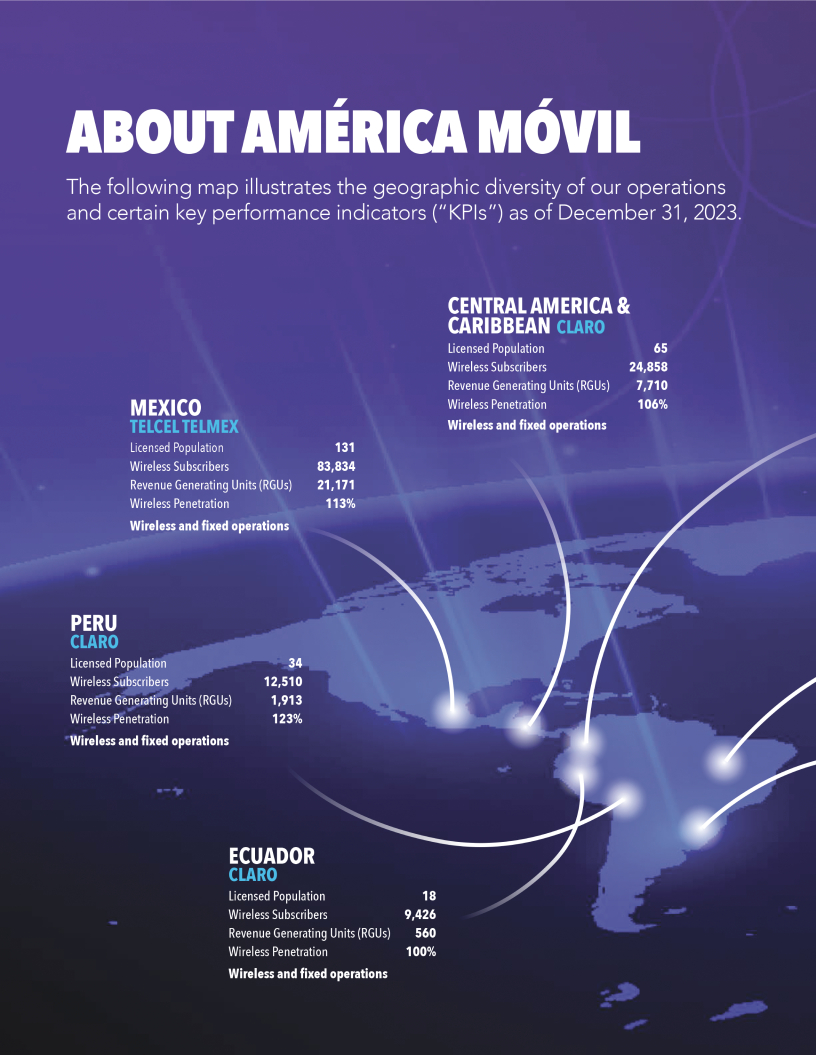

We provide telecommunications services in 22 countries. We are a leading telecommunications services provider in Latin America, ranking first in wireless, fixed-line, broadband and Pay TV services based on the number of RGUs (as defined under “Key Performance Indicators”).

Our largest operations are in Mexico and Brazil, which together account for over half of our total RGUs and where we have the largest market share based on RGUs. We have operations in 15 countries in the Americas and seven countries in Central and Eastern Europe as of December 31, 2023. For a list of our principal subsidiaries, see Note 2 a(ii) to our audited consolidated financial statements and “Additional Information—Exhibit 8.1” under Part VII of this annual report.

We aim to build on our position as a leader in integrated telecommunication services in Latin America and the Caribbean, and to grow in other parts of the world by continuing to expand our subscriber base through the development of our existing businesses and strategic acquisitions when opportunities arise. We have developed world-class integrated telecommunications platforms to offer our customers new services and enhanced communications solutions with higher data speed transmissions at lower prices. We continue investing in our networks to increase coverage and implement new technologies to optimize our network capabilities. See “Operating and Financial Review and Prospects—Overview” under Part II of this annual report for a discussion on the seasonality of our business.

10

11

12

13

KEY PERFORMANCE INDICATORS

Our customers generate revenue for us by purchasing one or more of our services. We refer to each service that a customer purchases as a revenue generating unit (“RGU”). Our management has identified RGUs as a KPI that helps measure the performance of our operations because it allows the Company to assess its performance on a

perservice

basis. Each wireless subscription, which includes prepaid and postpaid subscriptions, is counted as a single RGU, while a single fixed service customer can have multiple RGUs, depending on the services we provide in its respective country. Fixed RGUs consist of fixed voice, fixed data and Pay TV units (which include customers of our Pay TV services and, separately, of certain other digital services). The figures below reflect total wireless subscriptions and fixed RGUs of all our consolidated subsidiaries in the following reportable segments:| • | Mexico Wireless; |

| • | Mexico Fixed; |

| • | Brazil; |

| • | Colombia; |

| • | Southern Cone (Argentina) |

| • | Southern Cone (Paraguay and Uruguay); |

| • | Andean Region (Ecuador and Peru); |

| • | Central America (Costa Rica, El Salvador, Guatemala, Honduras and Nicaragua); |

| • | the Caribbean (the Dominican Republic and Puerto Rico); and |

| • | Europe (Austria, Belarus, Bulgaria, Croatia, North Macedonia, Serbia and Slovenia). |

AS OF DECEMBER 31, | ||||||||||||

2021 | 2022 | 2023 | ||||||||||

| (in thousands) | ||||||||||||

WIRELESS RGUs | ||||||||||||

Mexico | 80,539 | 82,851 | 83,834 | |||||||||

Brazil | 70,541 | 83,260 | 86,951 | |||||||||

Colombia | 35,062 | 37,550 | 39,240 | |||||||||

Southern Cone (Argentina) | 23,407 | 23,875 | 24,928 | |||||||||

Southern Cone (Paraguay and Uruguay) | 2,941 | 3,040 | 3,115 | |||||||||

Andean Region | 20,774 | 21,365 | 21,936 | |||||||||

Central America | 15,753 | 16,673 | 17,266 | |||||||||

Caribbean | 7,020 | 7,345 | 7,592 | |||||||||

Europe | 22,766 | 23,897 | 25,245 | |||||||||

Total Wireless RGUs | 278,803 | 299,856 | 310,106 | |||||||||

FIXED RGUs: | ||||||||||||

Mexico | 21,408 | 20,824 | 21,171 | |||||||||

Brazil | 25,291 | 24,136 | 23,089 | |||||||||

Colombia | 8,876 | 9,248 | 9,440 | |||||||||

Southern Cone (Argentina) | 1,694 | 2,546 | 3,212 | |||||||||

Southern Cone (Paraguay and Uruguay) | 326 | 319 | 337 | |||||||||

Andean Region | 2,444 | 2,608 | 2,473 | |||||||||

Central America | 4,376 | 4,624 | 4,923 | |||||||||

Caribbean | 2,608 | 2,774 | 2,787 | |||||||||

Europe | 6,077 | 6,204 | 6,270 | |||||||||

Total Fixed RGUs | 73,100 | 73,283 | 73,702 | |||||||||

Total RGUs | 351,903 | 373,139 | 383,808 | |||||||||

PRINCIPAL BRANDS

We operate in all of our geographic segments under the Claro brand name, except in Mexico and Europe, where we principally do business under the brand names listed below.

COUNTRY | PRINCIPAL BRANDS | SERVICES AND PRODUCTS | ||

Mexico | Telcel | Wireless voice | ||

| Wireless data | ||||

| Equipment and accessories | ||||

| Telmex Infinitum | Fixed voice | |||

| Fixed data | ||||

| Equipment and accessories | ||||

Europe | A1 | Wireless voice | ||

| Wireless data | ||||

| Fixed voice | ||||

| Fixed data | ||||

| Pay TV | ||||

| Equipment and accessories | ||||

14

SERVICES AND PRODUCTS

We offer, and derive revenues from, a wide range of services and products that vary by market, including wireless voice, wireless data and value-added services, fixed voice, fixed data, broadband and information technology (“IT”) services, Pay TV,(“OTT”) services and sales of equipment and accessories.

over-the-top

Wireless Operations

In 2023, our wireless voice and data operations generated revenues of Ps.418.1 billion, representing 51.2% of our consolidated revenues. As of December 31, 2023, our wireless operations represented approximately 80.8% of our total RGUs, an increase from 80.4%, as of December 31, 2022.

Revenues from wireless voice services primarily include charges from monthly subscriptions, usage charges billed to customers and usage charges billed to other service providers for calls completed on our network. The primary drivers of revenues from monthly subscription charges are the number of total RGU’s and the price of our service packages. The primary drivers of revenues from usage charges are airtime, international and long-distance calls and interconnection fees.

Revenues from wireless data services primarily include charges for data, cloud, internet,OTT services and data center services. Revenues from value-added services, including revenues from VPN services to our corporate clients, also contribute to our results for wireless data services.

machine-to-machine,

VOICE AND DATA.

Our wireless subsidiaries provide voice communication services across the countries in which they operate. We offer international roaming services to our wireless subscribers through a network of cellular service providers with which our wireless subsidiaries have entered into international roaming agreements around the world, and who provide GSM, 3G,

4G-LTE

and 5G roaming services.The voice and data plans are either “postpaid,” where the customer is billed monthly for the previous month, or “prepaid,” where the customer pays in advance for a specified volume of use over a specified period. Postpaid plans increased as a percentage of the wireless base from 38.0% in December 2022 to 39.3% as of December 31, 2023, while prepaid plans represented 60.7% as of December 31, 2023.

Our wireless voice services are offered under a variety of plans to meet the needs of different market segments. In addition, we often bundle wireless data communications services together with wireless voice services. Our

wireless subsidiaries had approximately 310 million wireless voice and data subscriptions as of December 31, 2023.

Prepaid customers typically generate lower levels of usage and are often unwilling or financially ineligible to purchase postpaid plans. Our prepaid plans have been instrumental to increase wireless penetration in Latin America and Eastern Europe to levels similar to those of developed markets. Additionally, prepaid plans entail little to no risk of

non-payment,

as well as lower customer acquisition costs and billing expenses, compared to the average postpaid plan.In general, our average rates per minute of wireless voice (“ARPM”) are very competitive for both prepaid and postpaid plans. ARPM is a measure used widely among companies in the telecommunications industry to compare the rates of voice calls of both prepaid and postpaid plans. Our average rates per minute of wireless voice used in 2023 increased by approximately 9.8% at constant exchange rates relative to 2022. This increase is mainly driven by a decrease in number of voice minutes due to increased data usage.

In addition, the plans we offer our retail customers include selective discounts and promotions that reduce the rates our customers pay.

VALUE-ADDED SERVICES.

As part of our wireless data business, our subsidiaries offer value-added services that include Internet access, messaging and other wireless entertainment and corporate services through GSM/ EDGE, 3G, 4G LTE and 5G networks.

Internet services include roaming capability and wireless Internet connectivity for feature phones, smartphones, tablets and laptops, including data transmission,services, mobile banking, virtual private network (“VPN”) services, video calls and personal communications services (“PCS”).

e-mail

services, instant messaging, content streaming and interactive applications. For example, in Mexico, our website for our wireless services (www.telcel.com) through Radiomóvil Dipsa, S.A. de C.V. (“Telcel”), offers access to a wide range of services and content such as video, music, games and other applications, which our subscribers can access from mobile devices. In addition, we offer other wireless services, including wireless security services, mobile payment solutions,machine-to-machine

Fixed Operations

In 2023, our fixed voice, data, broadband and IT solutions had revenues of Ps.244.5 billion, representing 30.0% of our consolidated revenues. As of December 31, 2023, our

15

fixed operations represented approximately 19.2% of our total RGUs, a decrease from 19.6% as of December 31, 2022.

Revenues from fixed voice services primarily include charges from monthly subscriptions, usage charges billed to customers and usage charges billed to other service providers for calls completed on our network. The primary drivers of revenues from monthly subscription charges are the number of total RGU’s and the price of our service packages. The primary drivers of revenues from usage charges are airtime, international and long-distance calls and interconnection fees.

Revenues from fixed data services primarily include charges for data, cloud, broadband,and data center services. Revenues from IT solutions, including revenues from dedicated links to our corporate clients, also contribute to our results for fixed data services.

machine-to-machine

VOICE.

Our fixed voice services include local, domestic and international long-distance, under a variety of plans to meet the needs of different market segments, specifically tailored to our residential and corporate clients.

DATA.

We offer data services, including data centers, data administration and hosting services to our residential and corporate clients under a variety of plans.

BROADBAND.

We provide residential broadband access through hybrid fiber-coaxial (“HFC”) or fiber-optic cable. These services are typically bundled with voice services and are competitively priced as a function of the desired or available speed. As a complement to these services, we offer a number of products such as home networking and smart home services.

IT SOLUTIONS.

Our subsidiaries provide a number of different IT solutions for small businesses and large corporations; including specific solutions to the industrial, financial, government and tourism sectors, among others.

Pay TV

We offer Pay TV through cable and satellite TV subscriptions to both retail and corporate customers under a variety of plans. As of December 31, 2023, we had approximately 13 million Pay TV RGUs, a decrease of approximately 242 thousand Pay TV RGUs from the prior year.

Pay TV revenues consist primarily of charges from subscription services, additional programming, including

on-demand

programming and advertising.OTT Services

We sell video, audio and other media content that is delivered through the internet directly from the content provider to the viewer or end user. Our most important service is ClaroVideo, an

on-demand

internet streaming video provider with more than 32,000 content titles sold across all the Latin American and Caribbean markets in which we operate. We offer bundled packages of ClaroVideo, which may include:| • | Subscription video on demand, providing unlimited access to our entire catalogue of content titles for a fixed monthly subscription fee; |

| • | Transactional video on demand and electronic sell-through, offering the option to rent or buy new content releases; and |

| • | Add-on services such as subscription and other OTT services through a platform payment system, including access to FOX, HBO, Noggin and Paramount+, among others. |

We also offer an advertised and unlimited music streaming and downloading service in 15 countries in Latin America and Europe through ClaroMúsica, with access to approximately 100 million songs across all music genres.

Sales of Equipment and Accessories

Sales of equipment and accessories, and associated revenues, include the sale of handsets, accessories, IoT devices, and other equipment such as smart devices.

Other Services

Other services, and revenues from such services, include other businesses such as software development, call center services, entertainment content and news, telephone directories, advertising, cybersecurity services, mobile banking and corporate IT solutions.

16

Services and Products by Country

The following table is a summary of our principal services rendered and products produced as of December 31, 2023, in the countries in which we operate.

WIRELESS VOICE, DATA AND VALUE ADDED SERVICES (1) | FIXED VOICE, DATA, BROAD- BAND, AND IT SERVICES (2) | PAY TV | OTT SERVICES (3) | |||||

Argentina | ● | ● | ● | ● | ||||

Austria | ● | ● | ● | ● | ||||

Belarus | ● | ● | ● | ● | ||||

Brazil | ● | ● | ● | ● | ||||

Bulgaria | ● | ● | ● | ● | ||||

Colombia | ● | ● | ● | ● | ||||

Costa Rica | ● | ● | ● | ● | ||||

Croatia | ● | ● | ● | ● | ||||

Dominican Republic | ● | ● | ● | ● | ||||

Ecuador | ● | ● | ● | ● | ||||

El Salvador | ● | ● | ● | ● | ||||

Guatemala | ● | ● | ● | ● | ||||

Honduras | ● | ● | ● | ● | ||||

North Macedonia | ● | ● | ● | ● | ||||

Mexico | ● | ● | ● (4) | |||||

Nicaragua | ● | ● | ● | ● | ||||

Paraguay | ● | ● | ● | ● | ||||

Peru | ● | ● | ● | ● | ||||

Puerto Rico | ● | ● | ● | ● | ||||

Serbia | ● | ● | ||||||

Slovenia | ● | ● | ● | ● | ||||

Uruguay | ● | ● | ||||||

(1) Includes voice communication and international roaming services, interconnection and termination services, SMS, MMS,e-mail, mobile browsing, entertainment and gaming applications.(2 ) Fixed voice includes local calls, national and international long-distance.(3) Includes ClaroVideo and ClaroMúsica.(4) Services provided bynon-concessionaire subsidiaries. |

17

Our networks are one of our main competitive advantages. Today, we own and operate one of the largest integrated platforms based on our covered population across 15 countries in Latin America, and we are expanding our network in Europe.

INFRASTRUCTURE

For the year ended December 31, 2023, our capital expenditures totaled Ps.156.3 billion, which allowed us to increase our network, expand our capacity and upgrade our systems to operate with the latest technologies. With fully convergent platforms, we are able to deliver high-quality voice, video and data products.

As of December 31, 2023, the main components of our infrastructure were comprised of:

• | Cell sites: 110,824 sites with 2G, 3G, 4G and/or 5G technologies across Latin America and Europe. We have been expanding our coverage and improving quality and speed with a number of street cells and indoor solutions. On August 8, 2022, we completed the spin-off to Sitios Latam of our telecommunications towers and other related passive infrastructure in Latin America outside of Mexico, Colombia and our telecommunications towers existing in the Dominican Republic and Peru prior to thespin-off. Between February and July 2023, we completed the sale of all of our telecommunications towers in the Dominican Republic and Peru. See “Acquisitions, Other Investments and Divestitures.” |

| • | Fiber-optic network: More than 1.3 million km. Our network reached approximately 102 million homes. |

• | Submarine cable systems: Capacity in more than 197 thousand km of submarine cables, including the AMX-1 submarine cable that extends 18.3 thousand km and connects the United States to Central and South America with 13 landing points and also the South Pacific Submarine Cable that extends 7.3 thousand km along the Latin American Pacific coast, connecting Guatemala, Ecuador, Peru and Chile with five landing points. Both systems provide international connectivity to all of our subsidiaries in these geographic areas. |

• | Satellites: Five. Star One S.A. (“Star One”) has the most extensive satellite system in Latin America, with a fleet that covers the United States, Mexico, Central America and South America. We use these satellites to supply capacity for DTH services for Claro TV throughout Brazil and in other DTH Operations, as well as cellular backhaul, video broadcast and corporate data networks. |

• | Data centers: 43. We use our data centers to manage a number of cloud solutions, such as Infrastructure as a Service (“IAAS”), Software as a Service (“SAAS”), security solutions and unified communications. |

TECHNOLOGY

Our primary wireless networks use GSM/EDGE, 3G, 4G LTE and 5G technologies, which we offer in most of the countries where we operate. We aim to increase the speed of transmission of our data services and have been expanding our 5G coverage. In 2022, we began our 5G rollout in some countries in the Latin America region. In February 2022, we launched 5G in Mexico through Telcel, which was the largest data infrastructure deployment in Latin America. As of December 31, 2023 we covered close to 50% of the population in Mexico and Brazil with 5G services.

We transmit wireless calls and data through radio frequencies that we use under spectrum licenses. Spectrum is a limited resource, and, as a result, we may face spectrum and capacity constraints on our wireless network. We continue to invest significant capital in expanding our network capacity and reach and to address spectrum and capacity constraints on abasis.

market-by-market

The table below presents a summary of the population covered by our network, by country, as of December 31, 2023.

GENERATION TECHNOLOGY | ||||||||||||||||

GSM | UMTS | LTE | 5G | |||||||||||||

| (% of covered population) | ||||||||||||||||

Argentina | 99.29 | 98.30 | 97.74 | - | ||||||||||||

Austria | 99.99 | 95.20 | 98.67 | 90.50 | ||||||||||||

Belarus | 99.90 | 99.90 | - | - | ||||||||||||

Brazil | 95.38 | 96.74 | 96.60 | 45.82 | ||||||||||||

Bulgaria | 99.83 | 99.92 | 99.44 | 82.64 | ||||||||||||

Colombia | 90.23 | 90.11 | 87.20 | - | ||||||||||||

Costa Rica | 90.74 | 96.74 | 97.01 | - | ||||||||||||

Croatia | 99.00 | 99.00 | 98.90 | 92.30 | ||||||||||||

Dominican Republic | 99.12 | 98.75 | 89.63 | 53.36 | ||||||||||||

Ecuador | 96.03 | 81.80 | 80.83 | - | ||||||||||||

El Salvador | 82.19 | 96.31 | 89.95 | - | ||||||||||||

Guatemala | 88.44 | 90.50 | 88.46 | 28.51 | ||||||||||||

Honduras | 73.93 | 81.87 | 75.08 | - | ||||||||||||

North Macedonia | 99.80 | 99.90 | 99.20 | 99.50 | ||||||||||||

Mexico | 95.44 | 96.56 | 93.96 | 49.46 | ||||||||||||

Nicaragua | 71.75 | 79.36 | 78.49 | - | ||||||||||||

Paraguay | 76.89 | 80.76 | 83.63 | - | ||||||||||||

Peru | 88.03 | 85.15 | 85.52 | 25.70 | ||||||||||||

Puerto Rico | - | 96.95 | 99.26 | 90.65 | ||||||||||||

Serbia | 99.80 | 98.00 | 99.50 | - | ||||||||||||

Slovenia | 99.90 | - | 99.30 | 80.00 | ||||||||||||

Uruguay | 99.52 | 99.23 | 98.65 | - | ||||||||||||

18

We operate in an intensely competitive industry. Competitive factors within our industry include pricing, brand recognition, service and product offerings, customer experience, network coverage and quality, development and deployment of technologies, availability of additional spectrum licenses and regulatory developments.

Our principal competitors differ, depending on the geographical market and the types of service we offer. We compete against other providers of wireless, broadband and Pay TV that operate on a multi-national level, such as AT&T Inc., Teléfonica and Millicom, as well as various providers that operate on a nationwide level, such as Telecom Argentina in Argentina and Telecom Italia in Brazil.

Competition remains intense as a result of saturation in the fixed and wireless market, increased network investment by our competitors, the development and deployment of new technologies, the introduction of new products and services, new market entrants, the availability of additional spectrum, both licensed and unlicensed, and regulatory changes.

The effects of competition on our subsidiaries depend, in part, on the size, service offerings, financial strength and business strategies of their competitors, regulatory developments and the general economic and business climate in the countries in which they operate, including demand growth, interest rates, inflation and exchange rates. The effects could include loss of market share and pressure to reduce rates. See “Regulation” under Part VI and “Risk Factors” under Part III of this annual report.

Geographic diversification has been a key to our financial success, as it has provided for greater stability in our cash flow and profitability and has contributed to our strong credit ratings. In recent years, we have been evaluating the expansion of our operations to regions outside of Latin America. We believe that Europe and other areas beyond Latin America present opportunities for investment in the telecommunications sector that could benefit us and our shareholders over the long term.

We continue to seek ways to optimize our portfolio, including by finding investment opportunities in telecommunications and related companies worldwide, including in markets where we are already present, and we often have several possible acquisitions under consideration. We may pursue opportunities in Latin America or in other areas in the world. Some of the assets that we acquire may require significant funding for capital expenditures. We can give no assurance as to the extent, timing or cost of such investments. We also periodically evaluate opportunities for dispositions, in particular for businesses and in geographies that we no longer consider strategic. Recent developments related to acquisitions, other investments and divestitures include:

| • | In December 2020, our Brazilian subsidiary, Claro S.A. (“Claro Brasil”), together with two other purchasers, won |

a competitive bid to acquire the mobile business owned by Oi Group in Brazil. Pursuant to the transaction, Claro Brasil paid R$3.6 billion for 32.0% of Oi Group’s mobile business. Claro Brasil also committed to enter into long term agreements with Oi Group for the supply of data transmission capacity. This transaction closed on April 20, 2022. The final purchase price for the acquisition was Ps.14.2 billion, net of cash acquired, of which an amount of Ps.1.3 billion was withheld for price adjustment purposes and other conditions, in accordance with the purchase agreement. Additionally, Claro Brasil received Ps.781 million during the twelve months following April 20, 2022, for transition services. On October 4, 2023, Claro Brasil and the two other purchasers reached an agreement on the value of a post-purchase price adjustment, pursuant to which Ps.658 million was paid to Oi Group. The post-purchase price adjustment corresponds to 50% of the Ps.1.3 billion withheld at closing for price adjustment purposes plus interest and monetary correction of Ps.155.7 million. All issues and disputes between the Oi Group, Claro Brasil and the two other purchasers relating to the determination of the acquisition price are now concluded. |

| • | On August 8, 2022, we completed the spin-off of our telecommunications towers and other related passive infrastructure in Latin America outside of Mexico, other than Colombia and our telecommunications towers existing in Peru and in the Dominican Republic prior to |

19

the spin off. As part of the spin-off and the associated corporate restructuring, we contributed to Sitios Latam a portion of our capital stock, assets and liabilities, mainly consisting of the shares of our subsidiaries holding telecommunications towers and other associated infrastructure in Latin America outside of Mexico, other than Colombia and our telecommunications towers existing in Peru and in the Dominican Republic prior to thespin-off. The shares of Sitios Latam began trading on the Mexican Stock Exchange on September 29, 2022. On February 3, 2023, we completed the sale of all of our telecommunications towers owned by our subsidiary in the Dominican Republic to Sitios Latam for an amount of Ps.2.4 billion. Between March and July 2023, we completed the sale of all of our telecommunication towers owned by our subsidiary in Peru to Sitios Latam for an amount of Ps.4.0 billion. In total, 4,592 telecommunications towers were transferred pursuant to these two transactions in 2023. |

| • | On October 6, 2022, we entered into an agreement to combine our Chilean operation, Claro Chile, with the Chilean operations of LLA, VTR, to form a 50:50 joint venture, ClaroVTR, which we previously announced on September 29, 2021. On December 26, 2023, we announced our entry into a transaction agreement (the “Claro Chile Transaction Agreement”) with LLA, ClaroVTR and certain of our and LLA’s affiliates and an amended shareholders agreement to amend ClaroVTR’s governance structure. Pursuant to the Claro Chile Transaction Agreement, we agreed with LLA to, collectively in proportion to our respective shareholding interests or individually, provide additional capital to ClaroVTR, during the calendar year 2023 and through June 30, 2024 in an aggregate amount not to exceed CLP$972.4 billion (Ps.18.7 billion) (the “Commitment”). This Commitment seeks to support the execution of the business plan of ClaroVTR, and CLP$289.3 billion (Ps.5.6 billion) of the Commitment aims to permit the refinancing of certain bank debt guaranteed by the Company and existing at the formation of ClaroVTR. The Claro Chile Transaction Agreement provides us and LLA with an exercisable catch-up right on or before August 1, 2024 to cure any failure to fund our or LLA’s respective portions of the Commitment in order to maintain ClaroVTR as a 50:50 joint venture. As of December 31, 2023, we have purchased notes from ClaroVTR with an aggregate principal amount of CLP$742.1 billion (Ps.14.3 billion) (including the amounts used for the refinancing of bank debt) that are convertible into shares of ClaroVTR. In September 2023, we identified impairment indicators and assessed that there is objective evidence that ClaroVTR is impaired. As a result, an amount of Ps.4.7 billion was recorded as the difference between the recoverable amount of ClaroVTR and its carrying value. Additionally, as of December 31, |

2023, we recorded an impairment relating to purchased convertible notes from ClaroVTR totaling Ps.12.2 billion. Both amounts are recorded in the “valuation of derivatives, interest cost from labor obligations and other financial items” caption of the consolidated statements of comprehensive income in our audited consolidated financial statements. See Note 22 to our audited consolidated financial statements. |

| • | On February 6, 2023, we entered into a definitive agreement with Österreichische Beteiligungs AG (“OBAG”) with respect to OBAG’s and América Móvil’s participations in Telekom Austria AG (“Telekom Austria” or “TKA”) (the “TKA Shareholders Agreement”), which became effective on February 6, 2023. The TKA Shareholders Agreement provides a new 10-year term from February 2, 2023 and ensures América Móvil’s leadership and control over Telekom Austria Group by providing América Móvil with the right to nominate the majority of Telekom Austria Group’s supervisory board members and to nominate the chairman and chief executive officer of Telekom Austria Group’s management board with the decision-making vote over all management decisions. As part of the renewal of the TKA Shareholders Agreement, América Móvil and OBAG agreed to firmly support thespin-off of the mobile towers in most of the countries in which TKA operates, including Austria. In furtherance of the foregoing, we procured a€ 500 million, five-year bullet loan on behalf of EuroTeleSites AG (“EuroTeleSites”), the company designated to own TKA’s towers after thespin-off. On July 6, 2023, EuroTeleSites launched a€ 500 million 5.25% five-year bond. The five-year bullet loan and five-year bond were designed to ensure EuroTeleSite’s full funding at the time of the tower spin-off. Thespin-off of TKA’s tower business, in all countries in which TKA operates, other than Belarus, was approved by the shareholders of TKA in an extraordinary shareholders’ meeting on August 1, 2023. On September 22, 2023, TKA completed thespin-off of its telecommunications towers and other related passive infrastructure in all countries in which TKA operates, other than Belarus, and listed the shares of EuroTeleSites on the Vienna Stock Exchange. As part of thespin-off, TKA contributed to EuroTeleSites net total assets of€ 290 million in the form of capital stock, assets and liabilities, mainly consisting of the shares of TKA’s subsidiary. Both of TKA and EuroTeleSites are indirect subsidiaries of América Móvil over which América Móvil retains a controlling interest. |

For additional information on our acquisitions and investments, see Note 12 to our audited consolidated financial statements included in this annual report.

20

MARKETING

We advertise our services and products through different channels with consistent and distinct branding and targeted marketing. We advertise via print, radio, television, digital media, sports event sponsorships and other outdoor advertising campaigns. In 2023, our efforts were mainly focused on promoting our 5G services, our fiber optic rollout, leveraging the speed and quality of our networks and our fixed bundled offers, which compete on broadband speed and premium content.

We build on the strength of our well-recognized brand names to increase consumer awareness and customer loyalty. Building brand recognition is crucial for our business, and we have managed to position our brands as those of a premium carrier in most countries where we operate. According to the 2023 Brand Finance Telecom 150 report, Claro and Telcel ranked among the top thirty and top fifty strongest brands, respectively, in the telecom sector worldwide. Also, in the Brand Finance Latin America report Claro was named the most valuable telecom brand and ranked as the third most valuable brand in the Latin America region. Kantar BrandZ named Telcel as the most valuable brand in Mexico. In addition, a

year-end

2023 study by Austrian Brand Monitor found that A1, the brand name behind Telekom Austria, ranked number one in the Austrian telecommunications market for brand preference.SALES AND DISTRIBUTION

Our extensive sales and distribution channels help us attract new customers and develop new business opportunities. We primarily sell our services and products through a network of retailers and service centers for retail customers and a dedicated sales force for corporate customers, with more than 380,000 points of sale and more than 3,350 customer service centers. Our subsidiaries also sell their services and products online.

CUSTOMER SERVICE

We give priority to providing our customers with quality customer care and support. We focus our efforts on constantly improving our customers’ experience by leveraging our commercial offerings and our sales and distribution networks. Customers may make inquiries by calling a toll-free telephone number, accessing our subsidiaries’ web sites and social media accounts or visiting one of the customer sales and service centers located throughout the countries we serve.

21

Discontinued Operations

On November 23, 2021, we completed the sale of our U.S. operations to Verizon, as previously disclosed in our press release furnished on a report on Form

6-K

on November 23, 2021. As a result of the sale of TracFone, in accordance with IFRS 5, the operations of TracFone are classified as discontinued operations for the reporting periods prior to 2022 presented in the consolidated financial information included in this annual report. Accordingly, results are presented in the “profit (loss) after tax for the year from discontinued operations” in the consolidated financial information included in this annual report. Operating and financial information presented herein therefore excludes TracFone, including for periods prior to the sale.On July 1, 2022, we completed the sale of our Panamanian operations to Cable & Wireless Panama, S.A., an affiliate of LLA, as previously disclosed in our press release furnished on a report on Form

6-K

on July 1, 2022. As a result of the sale of Claro Panama, in accordance with IFRS 5, the operations of Claro Panama are classified as discontinued operations for the reporting periods prior to 2023 presented in the consolidated financial information included in this annual report. Accordingly, where applicable, results are presented in the “profit (loss) after tax for the year from discontinued operations” in the consolidated financial information included in this annual report. Operating and financial information presented herein therefore excludes Claro Panama, including for periods prior to the sale.On October 6, 2022, we entered into an agreement to combine our Chilean operations with LLA in order to create ClaroVTR, a 50:50 joint venture, as a result of which Claro Chile ceased to be our wholly owned subsidiary, as previously disclosed in our press release furnished on a report on Form

6-K

on October 6, 2022. In accordance with IFRS 11, this transaction was classified as a joint venture, since we exercise joint control over ClaroVTR with LLA, and all relevant decisions require the consent of both parties. As a result of the incorporation of the ClaroVTR as a joint venture, in accordance with IFRS 5, the operations of Claro Chile are classified as discontinued operations for the reporting periods prior to 2023 presented in the consolidated financial information included in this annual report and are recognized through the equity method from October 6, 2022. Accordingly, where applicable, results are presented in the “profit (loss) after tax for the year from discontinued operations” in the consolidated financial information included in this annual report. Operating and financial information presented herein therefore excludes Claro Chile, including for periods prior to the joint venture agreement.Segments

We have operations in 22 countries, which are aggregated for financial reporting purposes into ten reportable segments. Our operations in Mexico are presented in two segments—Mexico Wireless and Mexico Fixed, which consist mainly of Telcel and Telmex, respectively. Our headquarters’ operations are allocated to the Mexico Wireless segment. Our operations in the Southern Cone are presented in two segments, Argentina, and Uruguay and Paraguay. Financial information about our segments is presented in Note 23 to our audited consolidated financial statements included in this annual report.

The factors that drive our financial performance differ in the various countries where we operate, including the competitive landscape, the regulatory environment and economic factors, among others. Accordingly, our results of operations in each period reflect a combination of these effects on our different segments.

Constant Currency Presentation

Our financial statements are presented in Mexican pesos, but our operations outside Mexico account for a significant portion of our operating revenues. Currency variations between the Mexican peso and the currencies of our

non-Mexican

subsidiaries, especially the Euro, U.S. dollar, Brazilian real, Colombian peso and Argentine peso, affect our results of operations as reported in Mexican pesos. In the following discussion regarding our operating results, we include a discussion of the change in the different components of our revenues between periods at constant exchange rates, i.e., using the same exchange rate from the year end of the prior fiscal year to translate the local-currency results of ournon-Mexican

operations for both periods. We believe that this additional information helps investors better understand the performance of ournon-Mexican

operations and their contribution to our consolidated results.All comparisons at constant exchange rates in our consolidated figures exclude Argentina.

Our Argentine subsidiary is subject to the accounting guidelines applicable to hyperinflationary economies, with all the accounting variables expressed in real terms at constant Argentine pesos. Pursuant to IFRS rules, for consolidation purposes in our consolidated financial statements—with no other economy considered hyperinflationary—Argentine peso figures expressed in constant Argentine peso terms at the prevailing prices at the end of a reporting period must be converted into Mexican pesos at the exchange rate observed at the end of such reporting period. Due to hyperinflationary conditions in Argentina and the magnitude of the Argentine peso’s depreciation, the application of the above-referenced norm generates unusual effects. Therefore, we exclude Argentina from all consolidated figures cited at constant exchange rates.

24

Effects of Exchange Rates

Our results of operations are affected by changes in currency exchange rates. In 2023 compared to 2022, the Mexican peso was stronger against several of our operating currencies, including the U.S. Dollar, the Euro, the Brazilian real and the Colombian peso.

Since most of our debt is issued by América Móvil out of Mexico, to the extent that our functional currency, the Mexican peso, appreciates or depreciates against the currencies in which our indebtedness is denominated, we may incur foreign exchange gains or losses that are recorded as foreign currency exchange (loss) gain, net in our consolidated statements of comprehensive income.

Changes in exchange rates also affect the fair value of derivative financial instruments that we use to manage our currency-risk exposure, which are generally not accounted for as hedging instruments. In 2023, the Mexican peso strengthened against the currencies in which most of our indebtedness is denominated, and we recorded net foreign exchange gains of Ps.14.7 billion and net fair value losses on derivatives of Ps.10.3 billion. In 2022, the Mexican peso strengthened against the currencies in which most of our indebtedness is denominated, and we recorded net foreign exchange gains of Ps.20.8 billion and net fair value losses on derivatives of Ps.28.6 billion. See Note 7 to our audited consolidated financial statements included in this annual report.

Effects of Regulation

We operate in a regulated industry. Our results of operations and financial condition have been, and will continue to be, affected by regulatory actions and changes. Significant regulatory developments are presented in more detail in “Regulation” under Part VI and “Risk Factors” under Part III of this annual report.

Comparison of Results of Operations Between 2022 and 2021

Discussions of year-over-year comparisons between 2022 and 2021 that are not included in this report can be found under Part II, “Operating and Financial Review and Prospects” of our Form

20-F

for the fiscal year ended December 31, 2022, as filed on May 1, 2023 (FileNo. 001-16269).

Due to classifying Claro Panama’s and Claro Chile’s operations as discontinued operations for all years prior to 2023 presented in the consolidated financial information included in this report, the year-over-year comparisons presented in our Form20-F

for the fiscal year ended December 31, 2022, as filed on May 1, 2023, may not align with the figures presented herein for the same periods.Composition of Operating Revenues

In 2023, our total operating revenues were Ps.816.0 billion. Our operating revenues are derived from the sale of wireless and fixed voice services, wireless and fixed data services, including OTT services, value-added services and IT solutions, Pay TV, equipment, accessories and other services. For more information, see “Operating and Financial Review and Prospects—Results of Operations” under Part II of this annual report.

Seasonality of our Business

Our business is subject to a certain degree of seasonality, characterized by a higher number of new customers during the fourth quarter of each year. We believe this seasonality is mainly driven by the Christmas shopping season.

General Trends Affecting Operating Results

Our results of operations in 2023 reflected several continuing long-term trends, including:

| • | intense competition, with growing costs for marketing and subscriber acquisition and retention, as well as increasing service prices; |

| • | developments in the telecommunications regulatory environment; |

| • | growing demand for data services over fixed and wireless networks, as well as for smartphones and devices with stronger data service capabilities; |

| • | declining demand for voice services; |

| • | declining demand for traditional Pay TV services; |

| • | increasing capital expenditures linked to higher demand for connectivity; |

| • | our continued strategic focus on our cost savings programs in view of pressures from costs of customer care, the growing size and complexity of our infrastructure and general price inflation; and |

| • | instability in economic conditions caused by political uncertainty, inflation and volatility in financial markets and exchange rates. |

These trends are broadly characteristic of our businesses in all regions in recent years, and they have affected comparable telecommunications providers as well.

25

CONSOLIDATED RESULTS OF OPERATIONS FOR 2023 AND 2022

As described above under “Constant Currency Presentation,” due to hyperinflationary conditions in Argentina, for comparative purposes, our consolidated results of operations at constant exchange rates exclude Argentina.

Operating Revenues

Total operating revenues for 2023 decreased by 3.4%, or Ps.28.5 billion, over 2022. At constant exchange rates, total operating revenues for 2023 increased by 5.1% over 2022. This increase at constant exchange rates principally reflects an increase in mobile service revenues and a favorable trend in fixed services, partially offset by a decrease in fixed voice and Pay TV service revenues.

SERVICE REVENUES.

Service revenues for 2023 decreased by 3.3%, or Ps.23.8 billion, over 2022. At constant exchange rates, service revenues for 2023 increased by 5.2% over 2022. This increase at constant exchange rates principally reflects increases in revenues from our prepaid and postpaid mobile services, broadband and corporate services networks, which were partially offset by a decrease in revenues from our fixed voice and Pay TV services.

SALES OF EQUIPMENT.

Sales of equipment revenues for 2023 decreased by 3.5%, or Ps.4.7 billion, over 2022. At constant exchange rates, sales of equipment revenues for 2023 increased by 4.6% over 2022. This increase at constant exchange rates principally reflects higher sales of smartphones, data-enabled devices and accessories in Brazil, Mexico, Austria, Colombia and Ecuador, which were partially offset by lower sales in Central America and Peru.

Operating Costs and Expenses

TOTAL OPERATING COSTS AND EXPENSES.

Total operating costs and expenses for 2023 decreased by 3.6%, or Ps.18.6 billion, over 2022. At constant exchange rates, total operating costs and expenses for 2023 increased by 4.8% over 2022. This increase in operating costs and expenses at constant exchange rates principally reflects increased costs associated with electric energy, network maintenance, lease space, IT and logistics.

COST OF SALES AND SERVICES.

Cost of sales and services decreased by 4.3%, or Ps.14.1 billion, over 2022. At constant exchange rates, cost of sales and services for 2023 increased by 3.9% over 2022. This increase in costs of sales and services at constant exchange rates principally reflects an increase in sales of

higher-end

smartphones as well as, increased electric energy costs,corporate network, IT services and network maintenance costs. This increase was partially offset by our cost savings program.

COMMERCIAL, ADMINISTRATIVE AND GENERAL EXPENSES.

Commercial, administrative and general expenses for 2023 decreased by 3.6%, or Ps.6.5 billion, over 2022. As a percentage of operating revenues, commercial, administrative and general expenses were 21.2% for 2023, the same as 2022. At constant exchange rates, commercial, administrative and general expenses for 2023 increased by 5.1% over 2022. This increase in commercial, administrative and general expenses at constant exchange rates principally reflects the recognition of certain uncollectible accounts, increased expenses for frequency

rights-of-use

(i.e.,

concessions), improvements to customer service centers and advertising.OTHER EXPENSES.

Other expenses for 2023 increased by Ps.2.0 billion over 2022, principally due to the cost of sales of towers in Peru and the Dominican Republic.

DEPRECIATION AND AMORTIZATION.

Depreciation and amortization for 2023 decreased by 4.3%, or Ps.6.8 billion, over 2022. As a percentage of operating revenues, depreciation and amortization were 18.6% for 2023, a decrease of 0.2% over 2022. At constant exchange rates, depreciation and amortization for 2023 increased by 8.3% over 2022. This increase in depreciation and amortization at constant exchange rates principally reflects higher amortization offor towers owned by Sitios Latam, higher capital expenditures in Brazil, our acquisition of 32.0% of Oi Group’s mobile business in Brazil in April 2022 and amortization of 5G license payments.

rights-of-use

Operating Income

Operating income for 2023 decreased by 1.8%, or Ps.3.1 billion, over 2022. Operating margin (operating income as a percentage of operating revenues) was 20.6% for 2023, which represented an increase of 0.3% over 2022.

Non-Operating

ItemsNET INTEREST EXPENSE.

FOREIGN CURRENCY EXCHANGE GAIN, NET.

We recorded a net foreign currency exchange gain of Ps.14.7 billion for 2023, compared to our net foreign currency exchange gain of Ps.20.8 billion for 2022. This decrease principally reflects the depreciation of certain

26

currencies against the Mexican Peso, in which our indebtedness is denominated, particularly, the U.S. dollar, the euro and the British pound sterling.

VALUATION OF DERIVATIVES, INTEREST COST FROM LABOR OBLIGATIONS AND OTHER FINANCIAL ITEMS, NET.

INCOME TAX.

Our income tax expense in 2023 decreased by 25.0%, or Ps.11.5 billion, over 2022 (excluding income tax for discontinued operations in Panama and Chile). This decrease mainly reflects less profit before income tax due to a decrease in our net foreign currency exchange gains and other effects, including a Ps.12.2 billion impairment of ClaroVTR’s purchased convertible notes, in 2023.

Our effective corporate income tax rate as a percentage of profit before income tax was 29.9% for 2023, compared to 34.3% for 2022. This rate differed from the applicable rate of 30.0% under Mexican law and changed year over year mainly due to the tax effects of higher inflation on several of our subsidiaries, other tax benefits in Brazil and net operating losses in Brazil and in our Mexican fixed line business.

Net Profit

We recorded a net profit of our continuing operations of Ps.80.8 billion for 2023, a decrease of 8.4%, or Ps.7.4 billion, over 2022.

SEGMENT RESULTS OF OPERATIONS

We discuss below the operating results of each reportable segment. Notes 2. z) and 23 to our audited consolidated

financial statements describe how we translate the financial statements of our non-Mexican subsidiaries. Exchange rate changes between the Mexican peso and the currencies in which our subsidiaries operate affect our reported results in Mexican pesos and the comparability of reported results between periods.

The following table sets forth the exchange rates used to translate the results of our most significant non Mexican operations, as expressed in Mexican pesos per foreign currency unit, and the change from the rate used in the prior period. The U.S. dollar is the functional currency in several of the countries or territories in which we or our subsidiaries operate, including Ecuador, Puerto Rico and El Salvador.

MEXICAN PESOS PER FOREIGN CURRENCY UNIT (AVERAGE FOR THE PERIOD) THE YEARS ENDED DECEMBER 31, | ||||||

2022 | 2023 | % CHANGE | ||||

Brazilian real | 3.9045 | 3.5545 | (9.0) | |||

Colombian peso | 0.0048 | 0.0041 | (14.6) | |||

Argentine peso | 0.1586 | 0.0681 | (57.1) (1) | |||

U.S. dollar | 20.1283 | 17.7617 | (11.8) | |||

Euro | 21.2285 | 19.2047 | (9.5) | |||

(1) As of December 31, 2023, the devaluation of the Argentine peso against the Mexican peso is due pri- marily to economic policies established by the new Argentine presidential administration. The stated goals of the policies involve, among other things, the devaluation of the Argentine peso by more than 50 percent against the U.S. dollar. | ||||||

The tables below set forth operating revenues and operating income for each of our segments for the years indicated.

YEAR ENDED DECEMBER 31, 2023 | ||||||||||||||||

OPERATING REVENUES | OPERATING INCOME | |||||||||||||||

(in millions of Mexican pesos) | (as a % of total operating revenues) | (in millions of Mexican pesos) | (as a % of total operat- ing income) | |||||||||||||

Mexico Wireless | Ps. 258,788 | 31.7 | Ps. 84,817 | 50.6 | ||||||||||||

Mexico Fixed | 101,832 | 12.5 | 12,064 | 7.2 | ||||||||||||

Brazil | 166,710 | 20.4 | 25,618 | 15.3 | ||||||||||||

Colombia | 62,718 | 7.7 | 9,959 | 5.9 | ||||||||||||

| Southern Cone (Argentina) | 18,923 | 2.3 | 515 | 0.3 | ||||||||||||

| Southern Cone (Paraguay and Uruguay) | 4,006 | 0.5 | (444 | ) | (0.3 | ) | ||||||||||

Andean Region | 52,992 | 6.5 | 10,639 | 6.3 | ||||||||||||

Central America (1) | 44,064 | 5.4 | 6,956 | 4.1 | ||||||||||||

Caribbean | 38,268 | 4.7 | 7,723 | 4.6 | ||||||||||||

Europe | 100,836 | 12.4 | 15,752 | 9.4 | ||||||||||||

Eliminations | (33,124 | ) | (4.1 | ) | (5,815 | ) | (3.4 | ) | ||||||||

Total | Ps. 816,013 | 100.0 | Ps. 167,784 | 100.0 | ||||||||||||

27

YEAR ENDED DECEMBER 31, 2022 | ||||||||||||||||

OPERATING REVENUES | OPERATING INCOME | |||||||||||||||

| (in millions of Mexican pesos) | (as a% of total operating revenues) | (in millions of Mexican pesos) | (as a% of total operat- ing income) | |||||||||||||

Mexico Wireless | Ps. 245,899 | 29.1 | Ps. 76,709 | 44.9 | ||||||||||||

Mexico Fixed | 99,985 | 11.8 | 16,172 | 9.5 | ||||||||||||

Brazil | 170,880 | 20.2 | 26,666 | 15.6 | ||||||||||||

Colombia | 71,300 | 8.4 | 14,171 | 8.3 | ||||||||||||

| Southern Cone (Argentina) | 34,517 | 4.1 | 2,571 | 1.5 | ||||||||||||

| Southern Cone (Paraguay and Uruguay) | 4,521 | 0.5 | (778 | ) | (0.5 | ) | ||||||||||

Andean Region | 55,498 | 6.6 | 8,262 | 4.8 | ||||||||||||

Central America (1) | 47,215 | 5.6 | 7,540 | 4.4 | ||||||||||||

Caribbean | 42,714 | 5.1 | 10,285 | 6.0 | ||||||||||||

Europe | 105,956 | 12.5 | 16,156 | 9.5 | ||||||||||||

Eliminations | (33,984 | ) | (3.9 | ) | (6,883 | ) | (4.0 | ) | ||||||||

Total | Ps. 844,501 | 100.0 | Ps. 170,871 | 100.0 | ||||||||||||

(1) Excludes Claro Panama. | ||||||||||||||||

INTERPERIOD SEGMENT COMPARISONS

The following discussion addresses the financial performance of each of our reportable segments by comparing results for 2023 and 2022. In the year-over-year comparisons for each segment, we include percentage changes in operating revenues, percentage changes in operating income and operating margin (operating income as a percentage of operating revenues), in each case calculated based on the segment financial information presented in Note 23 to our audited consolidated financial statements.

Each reportable segment includes all income, cost and expense eliminations that occurred between subsidiaries within the reportable segment. The Mexico Wireless segment also includes corporate income, costs and expenses.

For all segments, we also include percentage changes in adjusted segment operating revenues, adjusted segment operating income and adjusted operating margin (adjusted operating income as a percentage of adjusted operating revenues), which consist of segment operating

revenues, segment operating income and segment operating margin, respectively, minus (i) certain intersegment transactions, (ii) for our

non-Mexican

segments, the effects of foreign currency translation and (iii) for the Mexican Wireless segment only, revenues and costs of group corporate activities and other businesses that are allocated to the Mexico Wireless segment. The following discussions provide a quantification of thesenon-IFRS

financial measures, presented herein to the most directly comparable financial measures calculated and presented in accordance with IFRS. We have provided thenon-IFRS

financial measures herein, which are not calculated or presented in accordance with IFRS, as supplemental information and in addition to the financial measures that are calculated and presented in accordance with IFRS.These supplemental

non-IFRS

financial measures are presented because management has evaluated our financial results both including and excluding the adjusted items and believes that the supplementalnon-IFRS

financial measures presented provide additional perspective and insights when analyzing our core operating performance from period to period and trends in our historical operating results. These supplementalnon-IFRS

financial measures should not be considered superior to, as a substitute for or as an alternative to, and should be considered in conjunction with, the IFRS financial measures presented herein.Except for the Southern Cone – Argentina segment, comparisons in the following discussion are calculated using figures in Mexican pesos. For the Southern Cone – Argentina segment only, due to hyperinflationary conditions in Argentina, comparisons in the following discussion are calculated using figures in constant Argentine peso terms, i.e., adjusted for inflation in accordance with International Accounting Standard (“IAS”) 29 Financial Reporting in Hyperinflationary Economies (“IAS 29”), and must be converted into Mexican pesos at the exchange rate observed at the end of the period per IFRS rules, as described above under “Constant Currency Presentation.”

Discussions of year-over-year comparisons between 2022 and 2021 that are not included in this report can be found under Part II, Operating and Financial Review and Prospects of our Form

20-F

for the fiscal year ended December 31, 2022, as filed on May 1, 2023.28

2023 COMPARED TO 2022

Mexico Wireless

The number of prepaid wireless subscriptions for 2023 increased by 0.9% over 2022, and the number of postpaid wireless subscriptions increased by 2.4%, resulting in an increase in the total number of wireless subscriptions in Mexico of 1.2%, or 983 thousand, to approximately 83.8 million as of December 31, 2023.

Segment operating revenues for 2023 increased by 5.2% over 2022. Adjusted segment operating revenues were Ps.239.6 billion in 2023 and Ps.226.2 in 2022, after giving effect to adjustments of Ps.(19.2) billion and Ps.(19.7) billion, respectively, for intersegment transactions and revenues of group corporate activities and other businesses that are allocated to the Mexico Wireless segment. This represents an increase of 5.9% in adjusted segment operating revenues in 2023 as compared to 2022, which principally reflects an increase in mobile services in prepaid and postpaid plans.

Segment operating income for 2023 increased by 10.6% over 2022. Adjusted segment operating income was Ps.98.1 billion in 2023 and Ps.91.1 billion in 2022, after giving effect to adjustments of Ps.13.3 billion and Ps.14.4 billion, respectively, for intersegment transactions and revenues and costs of group corporate activities and other businesses that are allocated to the Mexico Wireless segment. This represents an increase in adjusted segment operating income of 7.7% in 2023 as compared to 2022.

Segment operating margin was 32.8% in 2023, as compared to 31.2% in 2022. Adjusted segment operating margin was 40.9% in 2023, as compared to 40.3% in 2022. This slight increase in segment operating margin for 2023 principally reflects the effects of our cost savings program, partially offset by increases in costs associated with maintenance, customer care and adjustments in wages and salaries.

Mexico Fixed

The number of fixed voice RGUs in Mexico for 2023 decreased by 1.1% over 2022, and the number of broadband RGUs in Mexico increased by 4.6%, resulting in an increase in total fixed RGUs in Mexico of 1.7% over 2022, or 347 thousand, to approximately 21.2 million as of December 31, 2023.

Segment operating revenues for 2023 increased by 1.8% over 2022. Adjusted segment operating revenues were Ps.84.8 billion in 2023 and Ps.83.0 billion in 2022, after giving effect to adjustments of Ps.(17.0) billion and Ps.(16.9) billion for intersegment transactions. This represents an increase of 2.1% in adjusted segment operating revenues in 2023 as compared to 2022, which

principally reflects a stable increase in broadband by 7.2% and corporate network services by 11.3%, which was partially offset by a continued decrease in fixed voice revenues by 1.9% and long distance services by 13.8%.

Segment operating income for 2023 decreased by 25.4% over 2022. Adjusted segment operating (loss) income was Ps.(0.1) billion in 2023 and Ps.4.5 billion in 2022, after giving effect to adjustments of Ps.(12.2) billion and Ps.(11.7) billion, respectively, for intersegment transactions. This represents a decrease of 102.6% in adjusted segment operating income in 2023 as compared to 2022, which principally reflects increases in network maintenance costs, technical expenses and the contractual salary of our employees.

Segment operating margin was 11.8% in 2023, as compared to 16.2% in 2022. Adjusted segment operating margin was (0.1)% in 2023, as compared to 5.4% in 2022. The decrease in segment operating margin for 2023 principally reflects a decrease in revenues from voice services and an increase in network maintenance costs and technical expenses.

Brazil