Hosted by:

Niel Ellerbrook – Chairman, President and CEO

Jerry Benkert – EVP and CFO

Carl Chapman – EVP and COO

Ron Christian –EVP, General Counsel and CAO

First Quarter 2006 Results

Conference Call and Webcast

April 27, 2006 – 3:00 pm ET

Forward-Looking Statements

Statements contained or incorporated by reference in these slides

regarding future events and developments are “forward-looking

statements” within the meaning of Section 27A of the Securities Act of

1933. Forward-looking statements are based on management’s beliefs and

assumptions that derive from information currently known by

management. Because such statements are based on expectations and not

historical facts, actual results may differ materially from those projected in

the particular statements. Readers are cautioned not to place undue

reliance on these forward-looking statements, which speak only as of the

date of this document, or in the case of documents incorporated by

reference, as of the date of those documents.

statements” within the meaning of Section 27A of the Securities Act of

1933. Forward-looking statements are based on management’s beliefs and

assumptions that derive from information currently known by

management. Because such statements are based on expectations and not

historical facts, actual results may differ materially from those projected in

the particular statements. Readers are cautioned not to place undue

reliance on these forward-looking statements, which speak only as of the

date of this document, or in the case of documents incorporated by

reference, as of the date of those documents.

Additional detailed information concerning a number of factors that could

cause actual results to differ materially from the information that is

provided to you here is readily available in our annual report on Form 10-K

filed with the Securities and Exchange Commission on February 16, 2006.

provided to you here is readily available in our annual report on Form 10-K

filed with the Securities and Exchange Commission on February 16, 2006.

Co

Vectren Corporation

ntact:Steven M. Schein

VP – Investor Relations

812-491-4209

sschein@vectren.com

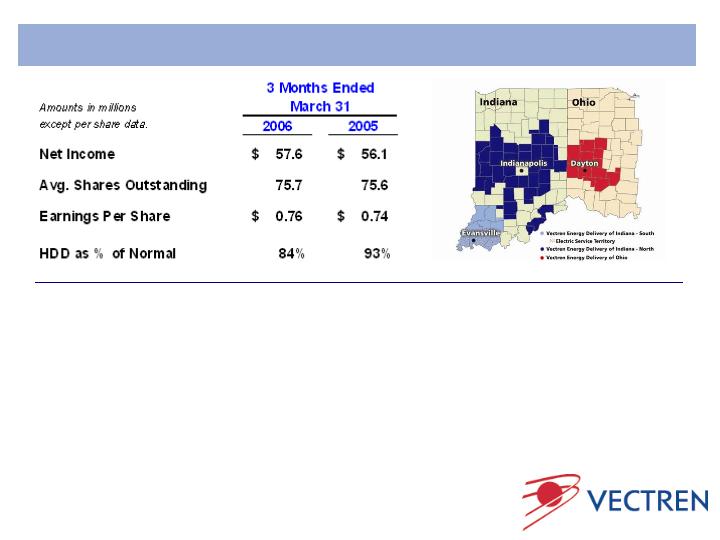

Strong 1st Quarter Results

Ø

Strong business unit performance – Utility and Nonutility

Ø

Warmer than normal weather

–

NTA mitigates weather impact on ~ 60% to 65% of gas heating load

Ø

High gas prices

–

Average cost per Dth for 3 months ended Mar. 31 @ $10.64 compared to $7.29

in same 2005 period.

Ø

Results in line with expectations

–

Synfuels 1st quarter reserve of $0.03 EPS

Vectren Corporation

Vectren North

(Indiana Gas)

Vectren South

(SIGECO) - Gas

Vectren Utility

Holdings Inc.

Vectren Energy

Delivery of Ohio

(VEDO)

(VEDO)

Vectren

Enterprises

Energy

Marketing and

Services

Services

Mining

Operations

Energy

Infrastructure

Services

Services

Vectren South

(SIGECO) –

Elec.

Elec.

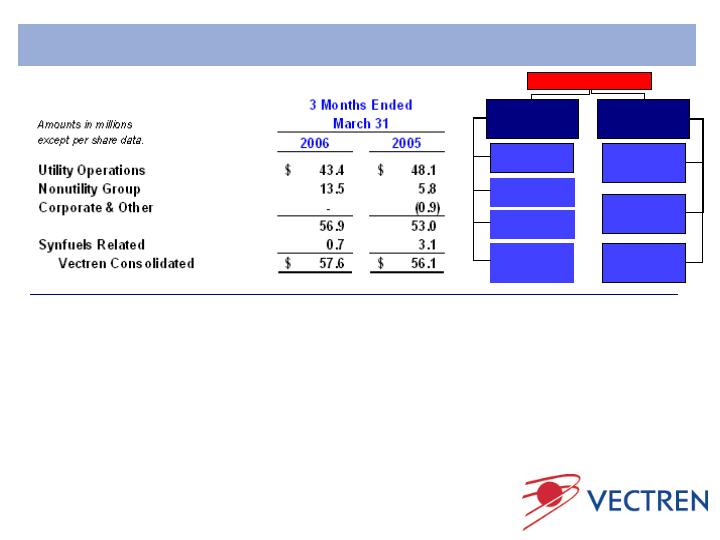

Net Income By Business Unit

Ø

Vectren results excluding synfuels improve $3.9 million ($0.05 per share)

Ø

Utility operations decline $4.7 million

–

Lower volumes of gas sold due to customer response to high energy prices

–

Lower wholesale power results as a result of 2005 mark to market gains

Ø

Nonutility earnings increase $7.7 million

–

Another strong quarter of nonutility earnings growth with each business group

contributing earnings growth over 2005

Positioned for the Future

Ø

$110 Multi-pollutant order received in February

–

Ensures Vectren’s generating fleet will be 100% scrubbed for SO2

and 90% for NOx

Ø

Conservation-oriented rate tariffs and energy efficiency

programs under review

–

Settlement on file and in front of Ohio Commission

–

Indiana settlement dialogue in progress

Ø

ProLiance gas supply agreement approved

–

Extends service agreement to Indiana utilities until 2011

Ø

Exercised option on additional Indiana coal reserves

–

80 million tons of recoverable coal

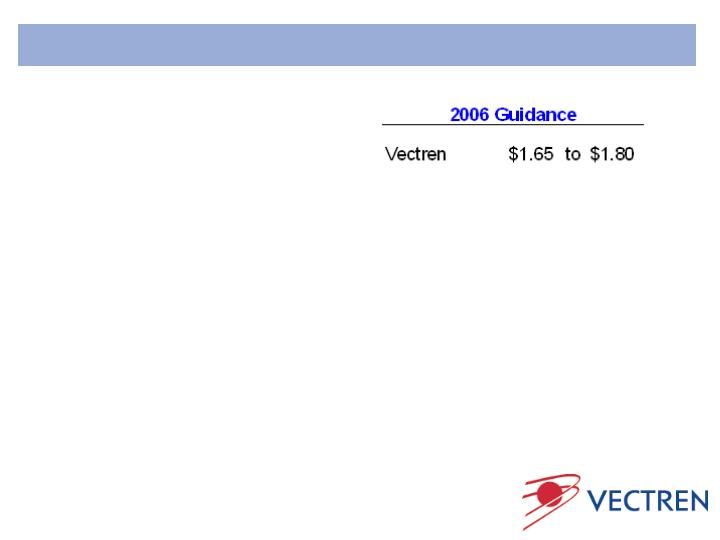

Ø

Earnings guidance for Vectren, inclusive of reduced

synfuels

–

$1.65 to $1.80

Ø

Expected 2006 Synfuels-related contributions

–

$0.04 to $0.05

Utility Operations

Ø

Reduced gas margins result of higher gas prices and

warm weather

Ø

Conservation-oriented tariffs expected to offset

margin loss from customer response to high gas

costs

costs

Ø

Normal Temperature Adjustment (NTA) in Indiana

Ø

2006 mark to market reduced wholesale power

marketing margins $2.7 million

Ø

O & M flat quarter over quarter

Ø

Depreciation reflects increased capital expenditures

Ø

Short-term interest rates slightly higher than

expected

Net Income

3 months ended March 31

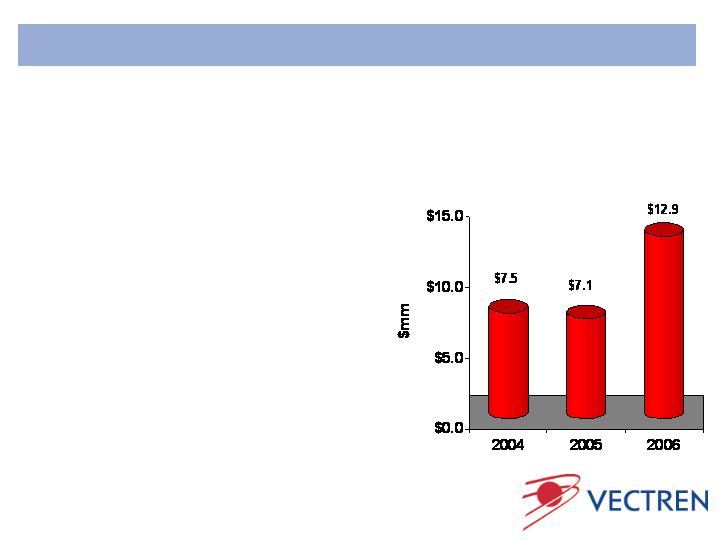

Energy Marketing & Services

Ø

ProLiance – wholesale gas

marketing

–

Volatility in gas prices continued;

margin per Dth increased 80%+

over 2005

over 2005

–

Earnings driven by storage

optimization opportunities

–

Storage transaction volume growth

of 3 Bcf or 10% over 2005

Ø

Source – retail gas marketing

–

Customer count approaching

150,000

–

Conservatively hedged for weather

due to unprecedented gas costs

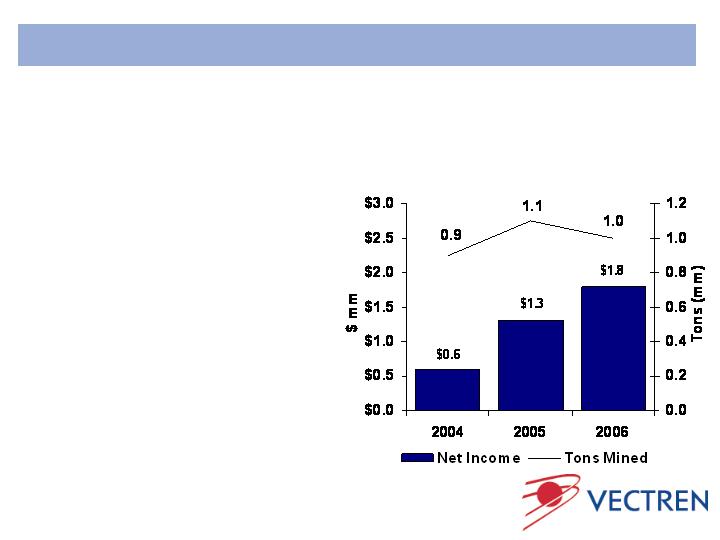

Net Income & Tons Mined

3 Months ended March 31

Coal Mining Operations

Ø

Mining operations reflect

improved pricing and

increased tax benefits from

depletion

increased tax benefits from

depletion

Ø

Operational costs increases

in steel, diesel, and

explosives offset by

increased revenue per ton

explosives offset by

increased revenue per ton

Ø

Slight decline in tons mined

due to timing of highwall

mining

mining

Ø

90+% of 2006 production

contracted at fixed prices

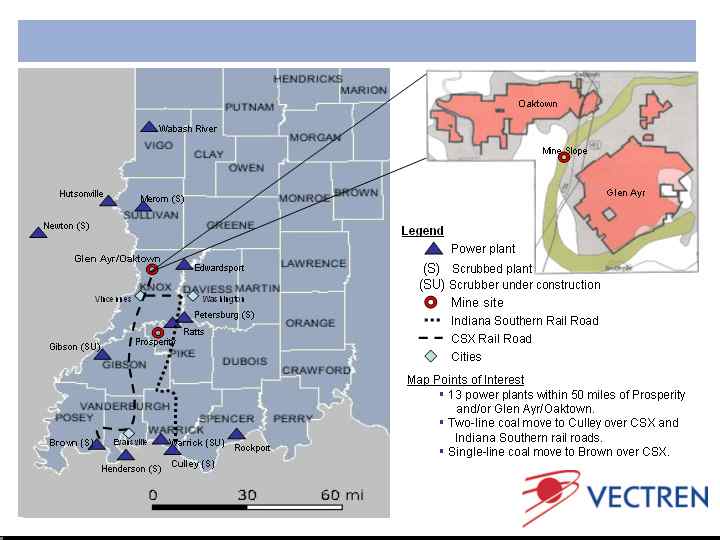

New Mine Project Summary

Ø

Reserves located 8 miles north of Vincennes in Knox County,

Indiana

Ø

Located within 50 miles of 8 coal-fired plants and adjacent to

mainline rail service

Ø

Two mines, 80 million tons

Ø

Projected coal quality: 11,200 BTU; 6 lb Sulfur

Ø

Expect to mine 5 million tons annually

Ø

Creates 425 mining jobs

Ø

Estimated 2 ½ years for land acquisition, permitting, rail access

and mine development

Ø

Replaces 1+ million tons of Cypress Creek coal in 2009

Ø

Mine development and equipment costs estimated at $125 million

Glen Ayr/Oaktown Project – Location Map

§

§

§

Ø

Reliant Services gas

construction

–

Lower seasonal loss of $0.4

million compared to $1.0 million

in 2005

in 2005

–

Improved earnings driven by

Miller Pipeline’s gas construction

division with large pipeline

projects in 1st quarter

division with large pipeline

projects in 1st quarter

–

Additional large pipeline projects

started in the 2nd quarter

–

Currently mobilizing crews to

new territories; geographic

expansion with acquisition of a

small construction company

expansion with acquisition of a

small construction company

–

Expect Q2 YTD profitability

Energy Infrastructure Services

Ø

ESG Performance Contracting

–

Lower seasonal loss of $0.8

million compared to $1.1 million

in 2005

in 2005

–

Q1 2006 ending backlog

increased to $51 million from

$19 million in 2005

$19 million in 2005

–

Over 50% of projects in backlog

are for schools and colleges

which are generally monetized in

the 2nd and 3rd quarters

which are generally monetized in

the 2nd and 3rd quarters

–

Johnson City, TN landfill project

construction in progress for

mid-year operation

mid-year operation

–

Expect Q2 YTD profitability

2006 Synfuels Outlook

Ø

Synfuels tax benefits expire at end of 2007

Ø

Current stock price reflects synfuels sunset

Ø

Credits are expected to phase out ratably with NYMEX prices

from approximately $60 to $74 per barrel

Ø

Approximately one third of expected tax credits are insured in

2006

Ø

Reserved $2.3 million 1st quarter to reflect possible phase

out of tax credits earned in 1st quarter

Ø

Tax legislation is being considered that would eliminate

phase out risk for 2006 but could increase the risk in 2007

Ø

AMT credit carryforward of approximately $47 million

Ø

Investment balance of $7.2 million is not currently impaired

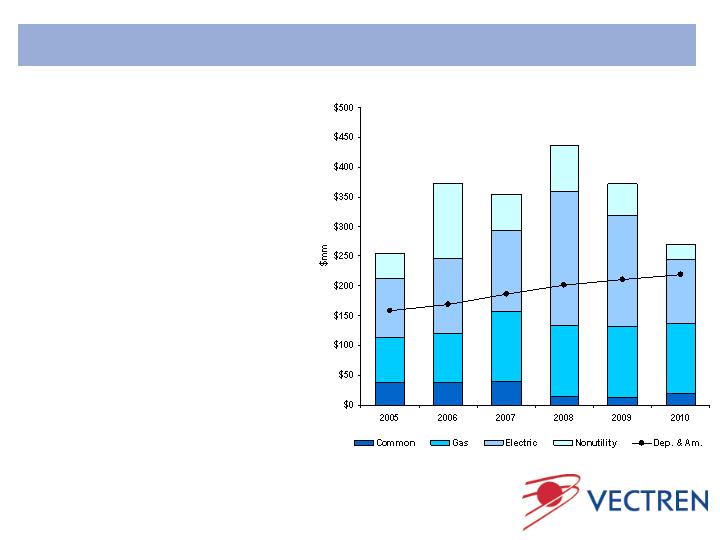

$255

$373

$354

$435

$372

$270

Capital Expenditures and Investments

Major Utility Expenditures

Ø

Environmental Compliance

–

$230 million

Ø

Coal Fired Generation

–

$225 million

Ø

Bare Steel/Cast Iron

–

$170 million

Major Nonutility

Ø

Midstream Assets

Ø

Coal Reserves

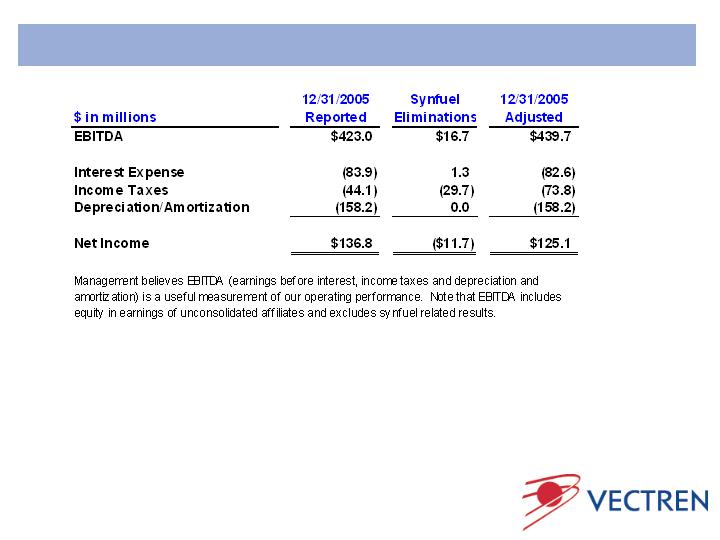

Reconciliation of EBITDA to Net Income

Ø

Enterprise Value at December 31, 2005 @ $3.6 billion

–

Net Debt @ $1.5 billion

–

Market Capitalization @ $2.1 billion

Ø

Enterprise Value to EBITDA @ 8.5x

Ø

Enterprise Value to EBITDA (excluding synfuels) @ 8.2x

Ø

Expected synfuels-related

contribution reduced given

uncertainty

uncertainty

–

$0.04 to $0.05

Ø

Expected earnings excluding

synfuels unchanged

Ø

Most significant assumptions

–

Normal weather

–

High gas costs remain

–

Conservation tariffs achieved

–

Expected conversion of

backlog and construction

revenue at ESG and Reliant

revenue at ESG and Reliant

–

Synfuels uncertainties

2006 EPS Guidance

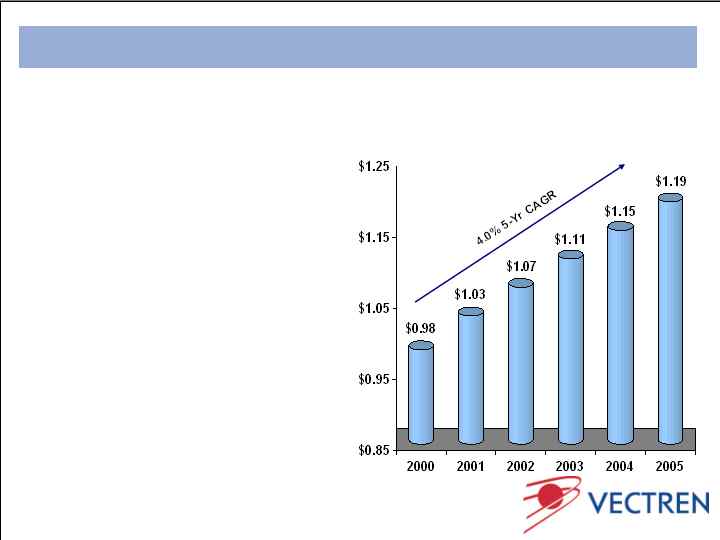

46 Consecutive Years Increased

Dividends Paid

Vectren = Long-term Shareholder Value

Ø

Supportive Regulation

–

Multi-pollutant

–

NTA

–

ProLiance service agreement

–

Conservation-oriented rates

Ø

Consistent Dividend Policy

–

3.4% increase December 2005

–

$1.22 annualized rate

–

55% to 65% target payout

–

85%+ funded from utility

Ø

Long-term growth objectives

–

EPS growth greater than 5%

–

Total return between 9 to 9½%