SUMMARY OF RISK FACTORS

The following summary is a concise description of certain of the material risk factors that you should consider in making your decision to purchase any notes. This summary does not purport to summarize all of the risks that you should consider in making your decision to purchase any notes. You should carefully read the risks factors set forth under “Risk Factors,” as well as the other information contained in this prospectus.

Risks primarily related to the nature of the notes and the structure of the transaction.

The notes are subject to certain risks related to their nature as asset-backed securities and the structure of the transaction, which could lead to payment delays, shortfalls in payments or losses on your notes, including due to factors such as, but not limited to:

| • | the limited pool of receivables and other assets available to make payments on the notes; |

| • | the subordination of certain classes of the notes to other more senior classes of the notes; |

| • | unpredictability of the rate at which the notes will amortize, and the potential acceleration of payments on the notes due to the occurrence of an event of default; and |

| • | the suitability of the notes as investments for investors subject to the EU Securitization Rules or the UK Securitization Rules. |

Risks primarily related to the receivables and economic conditions.

The notes are subject to certain risks related to the receivables and economic conditions, which could lead to payment delays, shortfalls in payments or losses on your notes, including due to factors such as, but not limited to:

| • | the effect of the COVID-19 pandemic, and related measures taken in response to the pandemic, on the obligors of the receivables, on the transaction parties and on the abilities of the transaction parties to perform their respective obligations under the transaction agreements; |

| • | economic developments, geopolitical conditions, public health concerns and other market events; |

| • | discount pricing incentives, marketing incentive programs and other used car market factors that may impact the amounts received upon disposition of the financing vehicles; |

| • | certain contractual terms and low annual percentage rates of the receivables, and the rate of depreciation of the related financed vehicles; |

| • | potential adverse effects of any recalls with respect to the financed vehicles; and |

| • | geographic concentrations of the receivables and extreme weather conditions, public health concerns, natural disasters and other similar events in specific geographic areas. |

Risks primarily related to legal and regulatory matters.

The notes are subject to certain risks related to legal and regulatory matters, which could lead to payment delays, shortfalls in payments or losses on your notes, including due to factors such as, but not limited to:

| • | federal and state consumer protection laws regulating the creation, collection and enforcement of the receivables; |

| • | the regulatory environment in which TMCC operates, and potential litigation or governmental proceedings that could affect the transaction parties; and |

| • | the Servicemembers Civil Relief Act and other similar state laws potentially limiting the ability of the servicer to collect from certain obligors of the receivables. |

Risks primarily related to servicing.

The notes are subject to certain risks related to the servicing of the receivables, which could lead to payment delays, shortfalls in payments or losses on your notes, including due to factors such as, but not limited to:

| • | the ability of the servicer to commingle collections on the receivables for a limited time; |

| • | the potential cost of transferring servicing responsibilities to a successor servicer, in the event of a servicer default; |

| • | the effect of credit ratings-related matters on the servicer; |

| • | the potential that a security breach or cyber-attack could adversely affect TMCC’s business and its ability to service the receivables; |

| • | TMCC’s enterprise data practices are subject to increasingly complex, restrictive, and punitive regulations; and |

| • | TMCC’s servicing activities could be disrupted by a failure or interruption of its information services. |

Risks primarily related to bankruptcy and insolvency of transaction parties and perfection of security interests.

The notes are subject to certain risks related to the potential bankruptcy and insolvency of transaction parties and perfection of security interests, which could lead to payment delays, shortfalls in payments or losses on your notes, including due to factors such as, but not limited to:

| • | the bankruptcy or insolvency of TMCC, the depositor or the issuing entity; |

| • | interests of other persons or competing claims in the receivables or the related financed vehicles could be superior to the interests of the indenture trustee therein; and |

| • | the failure of the servicer to maintain control of the receivables evidenced by electronic contracts. |

General risks relating to the transaction.

The notes are subject to certain general risks applicable to transactions of this nature, which could lead to payment delays, shortfalls in payments or losses on your notes, including due to factors such as, but not limited to:

| • | the complexity of the notes; |

| • | the potential absence of a secondary market for the notes; |

| • | withdrawal or downgrade of the ratings on the notes, potential issuance of unsolicited ratings on the notes, rating agency conflicts of interest and related regulatory scrutiny; |

| • | the retention by the depositor of certain of the notes; and |

| • | limitations on your ability to exercise rights directly, due to the absence of physical notes, and potential delays in receiving payments as the result of the notes being held in book-entry form. |

RISK FACTORS

You should consider the following risk factors in deciding whether to purchase any notes.

Risks Primarily Related to the Nature of the Notes and the Structure of the Transaction

You must rely for repayment only upon payments from the issuing entity’s assets, which may not be sufficient to make full payments on your notes.

The notes represent indebtedness of the issuing entity and will not be insured or guaranteed by the depositor, sponsor, administrator, servicer or any of their respective affiliates, any governmental entity, the trustees or any other person. The only sources of payment on your notes are payments received on the receivables and, to the extent available, any funds on deposit in the accounts of the issuing entity, including amounts on deposit in the reserve account. The amounts deposited in the reserve account will be limited. If the entire reserve account has been used and the available credit enhancement is exhausted, the issuing entity will depend solely on current collections on the receivables to make payments on the notes. The issuing entity will also have the benefit of overcollateralization (including the yield supplement overcollateralization amount) to provide limited protection against low-interest yielding receivables. For additional information, you should refer to “Payments to Noteholders—Credit and Cash Flow Enhancement—Overcollateralization,” “—Yield Supplement Overcollateralization Amount” and “—Reserve Account” in this prospectus. If the assets of the issuing entity are not sufficient to pay interest on and principal of the notes you hold, you will suffer a loss.

Certain events (including some that are not within the control of the issuing entity, the depositor, the sponsor, the administrator, the servicer, the indenture trustee, the owner trustee or of their respective affiliates) may result in events of default under the indenture and cause acceleration of all outstanding notes. If so directed by the holders of notes evidencing not less than a majority of the aggregate principal amount of the notes of the controlling class then outstanding (excluding for such purposes the aggregate outstanding principal amount of any notes held of record or beneficially owned by TMCC, TAFR LLC or any of their affiliates), acting together as a single class, following an event of default resulting in an acceleration of the notes, the indenture trustee will liquidate the assets of the issuing entity only in limited circumstances, and the issuing entity may be required promptly to sell the receivables, liquidate its assets and apply the proceeds to the payment of the notes. Liquidation would be likely to accelerate payment of all notes that are then outstanding. If a liquidation occurs close to the date when any class otherwise would have been paid in full, repayment of that class might be delayed while liquidation of the assets is occurring. The issuing entity cannot predict the length of time that will be required for liquidation of its assets to be completed. In addition, the amounts received from a sale in these circumstances may not be sufficient to pay all amounts owed to the holders of all classes of notes or any class of notes, and you may suffer a loss. This deficiency will be more severe in the case of any notes where the aggregate outstanding principal amount of the notes exceeds the aggregate principal balance of the receivables. Even if liquidation proceeds are sufficient to repay the notes in full, any liquidation that causes principal of a class of notes to be paid before the related final scheduled payment date will involve the prepayment risks described under “—Prepayments on receivables may cause prepayments on the notes, resulting in reduced returns on your investment and reinvestment risk to you” below. Also, an event of default that results in the acceleration of the maturity of the notes will cause priority of payments of the notes to change, as described under “Payments to Noteholders—Payments After Occurrence of Event of Default Resulting in Acceleration” in this prospectus. Therefore, all outstanding notes may be affected by any shortfall in liquidation proceeds. For additional information, you should refer to “—Prepayments on receivables may cause prepayments on the notes, resulting in reduced returns on your investment and reinvestment risk to you” below.

Failure to pay principal on your notes will not constitute an event of default until maturity.

The amount of principal required to be paid to the noteholders will generally be limited to amounts available in the collection account (including amounts transferred to the collection account from the reserve account). Therefore, the failure to pay principal of your notes generally will not result in the occurrence of an event of default until the final scheduled payment date for your notes. For additional information, you should refer to “Description of the Notes—Indenture—Events of Default; Rights Upon Event of Default” in this prospectus.

Payment priorities increase risk of loss or delay in payment to certain classes of notes.

Based on the priorities described under “Payments to Noteholders” in this prospectus, classes of notes that receive principal payments before other classes will be repaid more rapidly than the other classes. Because principal of the notes will be paid sequentially, except in the case of the class A-2 notes, the class A-3 notes and the class A-4 notes after an event of default resulting in an acceleration of the notes, classes of notes that have higher sequential

numerical class designations or higher alphabetical sequential class designations will be outstanding longer and therefore will be exposed to the risk of losses on the receivables during periods after other classes have received most or all amounts payable on their notes, and after which a disproportionate amount of credit enhancement may have been applied and not replenished.

Because of the priority of payment on the notes, the yields of the higher numerically designated classes or higher alphabetically designated classes will be more sensitive to losses on the receivables and the timing of such losses than the lower numerically designated classes and lower alphabetically designated classes. Accordingly, the class A-2 notes will be more sensitive to losses on the receivables and the timing of such losses than the class A-1 notes; the class A-3 notes will be relatively more sensitive to losses on the receivables and the timing of such losses than the class A-1 notes and the class A-2 notes; the class A-4 notes will be relatively more sensitive to losses on the receivables and the timing of such losses than the class A-1 notes, the class A-2 notes and the class A-3 notes; and the class B notes will be relatively more sensitive to losses on the receivables and the timing of such losses than the class A notes. If the actual rate and amount of losses exceed your expectations, and if amounts in the reserve account are insufficient to cover the resulting shortfalls, the yield to maturity on your notes may be lower than anticipated, and you could suffer a loss.

Classes of notes that receive payments of principal earlier than expected are exposed to greater reinvestment risk, and classes of notes that receive payments of principal later than expected are exposed to greater risk of loss. In either case, the yields on your notes could be materially and adversely affected. In addition, the notes are subject to risk because payments of principal and interest on the notes on each payment date are subordinated to the payment of the total servicing fee and certain amounts payable to the indenture trustee, the owner trustee and the asset representations reviewer in respect of fees, expenses and indemnification amounts. This subordination could result in reduced or delayed payments of principal and interest on the notes.

For additional information, you should refer to “—You must rely for repayment only upon payments from the issuing entity’s assets, which may not be sufficient to make full payments on your notes” above.

Prepayments on receivables may cause prepayments on the notes, resulting in reduced returns on your investment and reinvestment risk to you.

If you receive payment of principal on your notes earlier than you expected, you may not be able to reinvest the principal you receive at a rate as high as the rate on your notes. Prepayments on the receivables will shorten the life of the notes to an extent that cannot be predicted. Prepayments may occur for a number of reasons. Some prepayments may be caused by the obligors under the receivables. For example, obligors may: (i) make early payments, since receivables will be prepayable at any time without penalty; (ii) default, resulting in the repossession and sale of the financed vehicle; (iii) damage the vehicle or become unable to pay due to death or disability, resulting in payments to the issuing entity under any existing physical damage, credit life or other insurance; or (iv) sell their vehicles or be delinquent or default on their receivables as a result of a manufacturer recall.

Some prepayments may be caused by the sponsor, the depositor or the servicer. For example, the sponsor and the depositor will make representations and warranties regarding the receivables, and the servicer will agree to take or refrain from taking certain actions with respect to the receivables. If the sponsor or the depositor breaches any such representation or warranty, or if the servicer breaches any such agreement, and such breach is material and cannot be remedied, the breaching party will be required to purchase the affected receivables from the issuing entity. This will result, in effect, in the prepayment of the purchased receivables. The servicer will also have the option to purchase the receivables from the issuing entity on or after the payment date when the aggregate outstanding principal balance of the receivables has declined to 5% or less of the aggregate principal balance of the receivables as of the cutoff date. In addition, an event of default under the indenture could cause your notes to be prepaid.

Additionally, under its current servicing practices, the servicer will modify the terms of any receivable impacted by the Servicemembers Civil Relief Act, as amended, and will be obligated to purchase any such modified receivable by depositing an amount equal to the remaining outstanding principal balance of such impacted receivable into the collection account. The Servicemembers Civil Relief Act provides, and similar laws of many states may provide, relief to obligors who enter active military service (including national guard members) and to obligors in reserve status who are called to active duty after the origination of their receivables. In addition, relief may also be granted to obligors who are dependents of persons eligible for benefits under the Servicemembers Civil Relief Act. Global conflicts and tensions may continue to involve military operations that will increase the number of U.S. citizens who have been called or will be called to active duty. The Servicemembers Civil Relief Act provides, generally, that an obligor who is covered by the Servicemembers Civil Relief Act may not be charged interest on the related receivable in excess of 6% per annum during the period of the obligor’s active duty. The Servicemembers Civil Relief Act also limits the ability of the servicer to repossess the financed vehicle securing a receivable during the related obligor’s period of active duty and, in some cases, may require the servicer to extend the maturity of the receivable, lower the monthly payments and readjust the payment schedule for a period of time after the completion of the obligor’s military service. We do not know how many receivables may be impacted by the Servicemembers Civil Relief Act.

The rate of prepayments on the receivables may be influenced by a variety of economic, social and other factors. The sponsor cannot predict the actual prepayment rates for the receivables, and you will bear any reinvestment risks resulting from a faster or slower rate of payments of the receivables. Increased delinquency and credit losses are significantly influenced by the combined impact of a number of factors, including the effects of changes in a servicer’s servicing operations, lower used vehicle values, continued economic weakness, longer term financing and tiered/risk based pricing. TMCC cannot guarantee that the delinquency and loss levels of the receivables will correspond to the delinquency and loss levels TMCC has experienced in the past on its loan portfolio. There is a risk that delinquencies and losses could increase or decline from historical levels for various reasons including changes in underwriting standards, changes in local, regional or national economies or the impact of other local, national or global events, including public health concerns, such as the COVID-19 Outbreak. For additional information, you should refer to “Weighted Average Lives of the Notes” in this prospectus.

The notes may not be suitable investments for investors subject to the EU Securitization Rules or the UK Securitization Rules, and such rules could have an adverse impact on the value and liquidity of the notes.

TMCC will agree to retain, on an ongoing basis, the SR Retained Interest. In addition, TMCC will agree not to sell, transfer or otherwise surrender all or part of the rights, benefits or obligations arising from the SR Retained Interest or subject it to any credit risk mitigation or hedging, except to the extent permitted by the EU Securitization Rules and the UK Securitization Rules.

However, the securitization transaction described in this prospectus is not being structured to ensure compliance by any person with the transparency requirements in Article 7 of the EU Securitization Regulation or Article 7 of the UK Securitization Regulation. In particular, neither TMCC nor any other party to the transaction described in this prospectus will be required to produce any information or disclosure for purposes of Article 7 of the EU Securitization Regulation or Article 7 of the UK Securitization Regulation, or to take any other action in accordance with, or in a manner contemplated by, such articles.

Prospective investors are responsible for analyzing their own legal and regulatory position and are advised to consult with their own advisors regarding the suitability of the notes for investment and compliance with the EU Securitization Rules, the UK Securitization Rules or any existing or future similar regimes in any relevant jurisdictions. Failure by an EU Affected Investor to comply with any applicable EU Securitization Rules or a UK Affected Investor to comply with the UK Securitization Rules with respect to an investment in the notes may result in the imposition of a penalty regulatory capital charge on that investment or of other regulatory sanctions or measures. The EU Securitization Rules, the UK Securitization Rules and any other changes to the regulation or regulatory treatment of the notes for some or all investors may negatively impact the regulatory position of EU Affected Investors and UK Affected Investors and have an adverse impact on the value and liquidity of the notes.

For more information regarding the EU Securitization Rules and the UK Securitization Rules, see “The Sponsor, Administrator and Servicer––Credit Risk Retention—EU and UK Risk Retention” and “EU Securitization Regulation and UK Securitization Regulation” in this prospectus.

Risks Primarily Related to the Receivables and Economic Conditions

Adverse events arising from the coronavirus outbreak could have an adverse effect on your notes.

An outbreak of infectious disease caused by a coronavirus discovered in late 2019 and related variants (collectively, “COVID-19”) has spread throughout the world, including in the United States (the “COVID-19 Outbreak”). The COVID-19 Outbreak has led, and will likely continue to lead, to disruption and volatility in the global capital markets and in the economies of many nations. In the United States, the COVID-19 Outbreak has caused an unprecedented level of unemployment claims, economic volatility, and resulted in a decline in consumer confidence and spending. The long-term and ultimate impacts of the social, economic and financial disruptions caused by the COVID-19 Outbreak are unknown. The ultimate duration or possible resurgence of the COVID-19 Outbreak or similar public health issues are also uncertain. See “—Economic developments, geopolitical conditions, public health concerns and other market events may adversely affect the liquidity, performance and market value of your notes” below.

The negative economic conditions arising from the COVID-19 Outbreak impacted certain of TMCC’s financial results during fiscal year 2021, including higher provision for credit losses on its retail loan portfolio primarily due to the increase in expected credit losses. It is unclear how many obligors have been and will continue to be adversely affected by the COVID-19 Outbreak, which could have a negative impact on the ability of obligors to make timely payments on the receivables and may result in losses on your notes. To the extent the COVID-19 Outbreak or the related economic uncertainty results in increased delinquencies and defaults by obligors due to financial hardship or otherwise, TMCC may implement a range of responsive actions with respect to obligors and the related receivables. For example, in response to the COVID-19 Outbreak, and for a limited period of time, the servicer temporarily suspended outbound collection activities in states with state-wide stay-at-home orders and repossession activities nationwide, and offered additional extensions to obligors requesting relief. The servicer has since resumed its standard retail loan extension policies, and it has resumed outbound collection activities and repossession activities where legally permissible to do so. For additional information, see “The Sponsor, Administrator and Servicer—Servicing of Motor Vehicle Retail Installment Sales Contracts” in this prospectus.

Because a pandemic such as the COVID-19 Outbreak has not occurred in recent years, and because it is impacting obligors throughout the United States, TMCC’s historical loss and delinquency experience is unlikely to accurately predict the performance of the receivables.

The COVID-19 Outbreak may also have the effect of heightening many of the other risks described in this “Risk Factors” section, such as those related to the ability of obligors to make timely payments on the receivables, used vehicle values, the performance, market value, credit ratings and secondary market liquidity of your notes, and risks of geographic concentration of the obligors. The COVID-19 Outbreak could also adversely affect the ability of the servicer and the other transaction parties to perform their respective obligations under the transaction documents, which could have an adverse effect on the timing and amount of payments on the notes.

Economic developments, geopolitical conditions, public health concerns and other market events may adversely affect the liquidity, performance and market value of your notes.

The United States has in the past experienced, and may in the future experience, a recession or period of economic contraction. During the recession which resulted from the COVID-19 Outbreak, the United States experienced an unprecedented level of unemployment claims, economic volatility, and a decline in consumer confidence and spending. Although the economy has improved in more recent months, it is possible that a higher percentage of obligors will seek protection under bankruptcy or debtor relief laws as a result of financial and economic disruptions related to the COVID-19 Outbreak than is reflected in TMCC’s historical experience. See “—Adverse events arising from the coronavirus outbreak could have an adverse effect on your notes” above. In addition, a deterioration in economic conditions, including elevated unemployment, decreases in home values and lack of available credit may lead to increased delinquency and default rates by obligors, as well as decreased consumer demand for automobiles and declining market values of the automobiles securing the receivables. As a result, delinquencies and credit losses on the receivables could increase, which could result in losses on your notes. In addition, consumer debt levels remain elevated as a result of current economic conditions, and there have been increasing trends in rates of delinquency and default frequency. As consumers assume higher debt levels, delinquencies and losses on the receivables may increase, which could result in losses on your notes.

Events in the global financial markets, including downgrades of sovereign debt, health pandemics, devaluation of currencies by foreign governments and slowing economic growth have in the past caused (and may cause again), a significant reduction in liquidity in the secondary market for asset-backed securities, which could adversely affect the market value of the notes and limit the ability of an investor to sell its notes.

Geopolitical conditions and other market events may impact TMCC and your notes. Restrictive exchange or import controls or other disruptive trade policies, disruption of operations as a result of systemic political or economic instability, adverse changes to tax laws and regulations, social unrest, outbreak of war or expansion of hostilities, health epidemics and other outbreaks, climate-related risk, and acts of terrorism, could each have a material adverse effect on TMCC’s business, results of operations and financial condition.

Any such events could also adversely affect TMCC’s ability to service the receivables and perform its other obligations under the transaction agreements, which could have an adverse effect on your notes.

Additionally, higher future energy and fuel prices could reduce the amount of disposable income that the affected obligors have available to make monthly payments on their automobile finance contracts. Higher energy costs could also cause business disruptions, which could cause unemployment and a deepening economic downturn. Such obligors could potentially become delinquent in making monthly payments or default if they were unable to make payments due to increased energy or fuel bills or unemployment. The issuing entity’s ability to make payments on the notes could be adversely affected if the related obligors were unable to make timely payments.

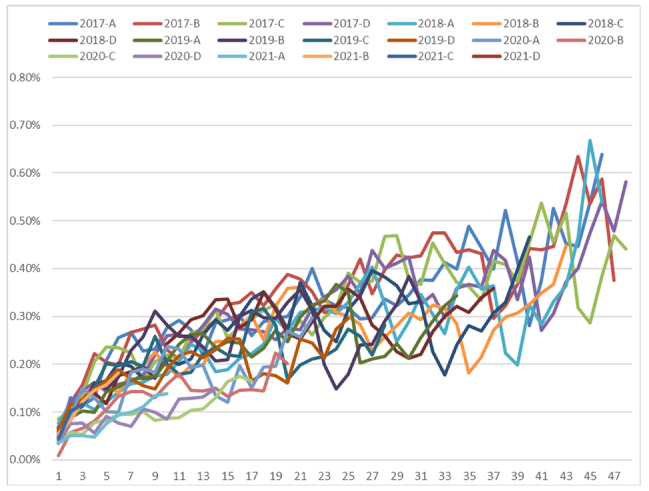

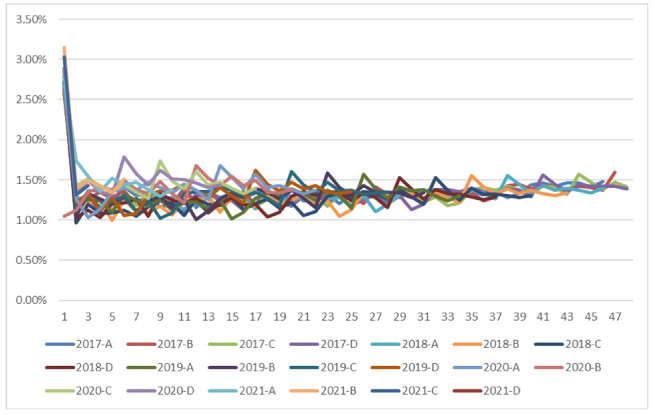

Delinquencies and losses with respect to automobile finance contracts may increase during the term of your notes. These increases in delinquencies and losses may be related to changes in consumer debt levels, increases in interest rates, a rise in the supply of used vehicles, a decrease in prices of used vehicles or the impact of public health concerns (such as the COVID-19 Outbreak). For delinquency and loss information regarding certain automobile loans originated and serviced by TMCC, you should refer to “Delinquencies, Repossessions and Net Losses” and “Static Pools” in this prospectus. Increased delinquencies and losses may lead to decreased collections on the receivables and the issuing entity may not have sufficient available collections to pay amounts due on the notes on any payment date or to pay any class of the notes in full on the related final scheduled payment date.

The amounts received upon disposition of the financed vehicles may be adversely affected by discount pricing incentives, marketing incentive programs and other used car market factors, which may increase the risk of loss on your notes.

The market for used Toyota or Lexus vehicles could be adversely affected by factors such as governmental action, changes in consumer demand, new vehicle incentive programs, new vehicle pricing, new vehicle sales, styling changes (including future plans for new Toyota and Lexus product introductions), recalls, the actual or perceived quality, safety or reliability of Toyota and Lexus vehicles, used vehicle supply (such as an overabundance of used cars, crossover utility vehicles, light-duty trucks and sport utility vehicles in the marketplace), the level of current used vehicle values, fuel prices, increased competition, fluctuations in interest rates, decreased or delayed new vehicle production due to the COVID-19 Outbreak, or other health pandemics, shortage of parts, components or raw materials, natural disasters, supply chain or logistic network interruptions or other events and economic conditions generally. Any such adverse change could result in reduced proceeds upon the liquidation or other disposition of financed vehicles, and therefore could result in reduced proceeds on defaulted receivables. If losses on the receivables exceed the credit enhancement available, you may suffer a loss on your investment.

Discount pricing incentives or other marketing incentive programs on new vehicles by Toyota Motor North America, Inc., TMCC or any of their competitors that effectively reduce the prices of new vehicles may have the effect of reducing demand by consumers for used cars, crossover utility vehicles, light-duty trucks and sport utility vehicles. Additionally, the pricing of used vehicles is affected by the supply and demand for those vehicles, which, in turn, is affected by consumer tastes, economic factors (including the price of gasoline), the introduction and pricing of new vehicle models, the actual or perceived quality, safety or reliability of vehicles and other factors. The reduced demand for used cars, crossover utility vehicles, light-duty trucks and sport utility vehicles resulting from discount pricing incentives or other marketing incentive programs introduced by Toyota Motor North America, Inc., TMCC or any of their competitors or other factors may reduce the prices consumers will be willing to pay for used cars, crossover utility vehicles, light-duty trucks and sport utility vehicles, including the vehicles that secure the receivables. In addition, if programs are implemented by the United States government to stimulate the sale of new vehicles, this may have the effect of further reducing the values of used vehicles. As a result, the proceeds received by the issuing entity upon any repossession of financed vehicles may be reduced and may not be sufficient to pay

the receivables. The servicer manages the market for used Toyota and Lexus vehicles through certain programs, but there can be no assurance that such programs will continue to be successful.

Paid-ahead simple interest contracts may affect the weighted average lives of the notes.

If an obligor on a simple interest contract makes a payment on the contract ahead of schedule (for example, because the obligor intends to go on vacation), the weighted average life of the notes could be affected. This is because the additional scheduled payments will be treated as a principal prepayment and applied to reduce the principal balance of the related contract and the obligor will generally not be required to make any scheduled payments during the period for which it was paid ahead. During this paid ahead period, interest will continue to accrue on the principal balance of the contract, as reduced by the application of the additional scheduled payments, but the obligor’s contract would not be considered delinquent during this period. Furthermore, when the obligor resumes his required payments, the payments so paid may be insufficient to cover the interest that has accrued since the last payment by the obligor. This situation will continue until the regularly scheduled payments are once again sufficient to cover all accrued interest and to reduce the principal balance of the contract. The payment by the issuing entity of the paid ahead principal amount on the notes will generally shorten the weighted average lives of the notes. However, depending on the length of time during which a paid ahead simple interest contract is not amortizing as described above, the weighted average lives of the notes may be extended. TMCC’s portfolio of retail installment sales contracts has historically included simple interest contracts which have been paid ahead by one or more scheduled monthly payments. There can be no assurance as to the number of contracts in the issuing entity which may become paid ahead simple interest contracts as described above or the number or the principal amount of the scheduled payments which may be paid ahead.

There may be potential adverse effects on the servicer, the receivables and your notes in the event any Toyota or Lexus models are subject to recalls.

Toyota Motor North America, Inc. periodically conducts vehicle recalls which could include temporary suspensions of sales and production of certain Toyota and Lexus models. Because TMCC’s business is substantially dependent upon the sale of Toyota and Lexus vehicles, such events could adversely affect TMCC’s business. A decline in values of used Toyota and Lexus vehicles would have a negative effect on residual values and return rates which, in turn, could increase credit losses to TMCC. Further, as described below, under “—The regulatory environment in which TMCC operates could have an adverse effect on TMCC, the depositor and the issuing entity, which could result in losses or delays in payments on your notes,” TMCC and its affiliates have been or may continue to become subject to litigation and governmental investigations and have been or may become subject to fines or other penalties. These factors could affect sales of Toyota and Lexus vehicles and, accordingly, could have a negative effect on TMCC’s business, results of operations and financial condition. If the demand for used Toyota or Lexus vehicles decreases due to recalls or other factors, the resale value of the vehicles related to the receivables may also decrease. As a result, the amount of proceeds received upon the liquidation or other disposition of financed vehicles may decrease. A decrease in the level of sales, including as a result of the actual or perceived quality, safety or reliability of Toyota and Lexus vehicles, or a change in standards of regulatory bodies, will have a negative impact on the level of TMCC’s financing volume, voluntary protection products volume, earnings assets and revenues. The credit performance of TMCC’s dealer and consumer lending portfolios may also be adversely affected. In addition, as a result of any recalls, obligors of related receivables may be more likely to be delinquent in or default on payments on their receivables. If any of these events materially affect collections on the receivables, you may experience delays in payments or principal losses on your notes if the available credit enhancement has been exhausted.

The geographic concentration of the obligors and performance of the receivables may increase the risk of loss on your investment.

The concentration of the receivables in specific geographic areas may increase the risk of loss. A deterioration in economic conditions in the states where obligors reside, including those caused by extreme weather conditions and natural disasters, public health concerns (including pandemics) and other similar events could adversely affect the ability and willingness of obligors to meet their payment obligations under the receivables and may consequently affect the delinquency, loss and repossession experience of the issuing entity with respect to the receivables. An improvement in economic conditions could result in prepayments by the obligors of their payment obligations under the receivables. As a result, you may receive principal payments of your notes earlier than anticipated.

As of the cutoff date, TMCC’s records indicate that, based on the mailing addresses of the obligors of the receivables, approximately 26.90% and 13.70% of the aggregate principal balance of the receivables as of the cutoff date was concentrated in California and Texas, respectively. No other state, based on the mailing addresses of the related obligors, accounts for more than 5.00% of the aggregate principal balance of the receivables as of the cutoff date.

Certain obligors’ ability to make timely payments on the receivables, and the condition of the financed vehicles, may be adversely affected by extreme weather conditions, natural disasters, public health concerns and other similar events.

Extreme weather conditions and natural disasters, such as floods, hurricanes, earthquakes, tornadoes and wildfires (including an increase in the frequency of such conditions and disasters as the result of climate change), public health concerns (including pandemics, such as the COVID-19 Outbreak) and other similar events, could result in substantial business disruptions, economic losses, unemployment, travel restrictions and disruptions caused by directives (such as the stay-at-home requirements) intended to limit the spread of COVID-19, and could have a negative effect on general economic conditions, consumer confidence and general market liquidity. As a result of such events, the obligors’ ability to make timely payments could be adversely affected, and the issuing entity’s ability to make payments on the notes could be adversely affected if obligors are unable to make timely payments on the receivables. In addition, any such events may adversely affect the condition of the financed vehicles. No representation or warranty will be made by TMCC or any other entity regarding the condition of any financed vehicle as of the cutoff date or any other date. Under the terms of the receivables, obligors are required to maintain physical damage insurance. However, there can be no assurance that such insurance has been maintained in all cases or would fully cover any damage to the related financed vehicle. For additional information, you should refer to “Transfer and Servicing Agreements—Insurance on Financed Vehicles” in this prospectus. No prediction can be made, and no assurance may be given, as to the effect of extreme weather conditions, natural disasters, public health concerns (including pandemics, such as the COVID-19 Outbreak) and other similar events on the rate of delinquencies, prepayments and/or losses on the receivables or the market value of your notes. See also “—Adverse events arising from the coronavirus outbreak could have an adverse effect on your notes” above.

The rate of depreciation of certain financed vehicles could exceed the amortization of the outstanding principal balance of the loan on those financed vehicles, which may result in losses.

There can be no assurance that the value of any financed vehicle will be greater than the outstanding principal balance of the related receivable. New vehicles normally experience an immediate decline in value after purchase because they are no longer considered new. As a result, it is highly likely that the principal balance of the related receivable will exceed the value of the related vehicle during the earlier years of a receivable’s term. Defaults during these earlier years are likely to result in losses because the proceeds of repossession are less likely to pay the full amount of interest and principal owed on the receivable. The frequency and amount of losses may be greater for receivables with longer terms, because these receivables tend to have a somewhat greater frequency of delinquencies and defaults and because the slower rate of amortization of the principal balance of a longer term receivable may result in a longer period during which the value of the financed vehicle is less than the remaining principal balance of the receivable. See the tables describing the composition of the receivables under the heading “The Receivables” in this prospectus for the percentage of the aggregate principal balance of the receivables as of the cutoff date consisting of receivables with original scheduled payments greater than 60 months. The frequency and amount of losses may also be greater for obligors with little or no equity in their vehicles because the principal balances for such obligors are likely to be greater for similar loan terms and vehicles than for obligors with a more significant amount of equity in the vehicle. Additionally, although the frequency of delinquencies and defaults tends to be greater for receivables secured by used vehicles, the amount of any loss tends to be greater for receivables secured by new vehicles because of the higher rate of depreciation described above.

You may suffer losses due to receivables with low annual percentage rates.

The receivables include receivables that have APRs that are less than the interest rates on your securities. Obligors with higher APR receivables may prepay at a faster rate than obligors with lower APR receivables. Higher rates of prepayments of receivables with higher APRs may result in the issuing entity holding receivables that will generate insufficient collections to cover delinquencies or chargeoffs on the receivables or to make current payments of interest on or principal of your notes. Similarly, higher rates of prepayments of receivables with higher APRs will decrease the amounts available to be deposited in the reserve account, reducing the protection against losses and shortfalls afforded thereby to the notes. For additional information, you should refer to “Prepayment and Yield

Considerations” and the tables describing the distribution of the receivables by APR under “The Receivables” in this prospectus.

Risks Primarily Related to Legal and Regulatory Matters

Receivables that fail to comply with consumer protection laws may be unenforceable, which may result in losses on your investment.

Numerous federal and state consumer protection laws regulate consumer contracts such as the receivables. Also, some of these laws may provide that the assignee of a consumer contract (such as the issuing entity) is liable to the related obligor for any failure of the contract to comply with these laws. If any of the receivables do not comply with one or more of these laws, the servicer may be prevented from or delayed in collecting payments on such receivables, and the issuing entity, as assignee of the related originator, could be held liable for any applicable penalties or damages. If that happens, payments on your notes could be delayed or reduced.

TMCC and the depositor will make representations and warranties relating to the receivables’ compliance with law and the issuing entity’s ability to enforce the contracts. If the depositor breaches any of these representations or warranties, the issuing entity’s sole remedy (other than the indemnification available to the issuing entity as described below) will be to require the depositor to repurchase the related receivable if such breach materially and adversely affects the interest of the issuing entity in such receivable and such breach has not been cured in all material respects within any applicable cure period. TMCC will have a corresponding obligation to repurchase any such receivable from the depositor. TMCC will also indemnify the depositor for any failure of a receivable to have been originated in compliance with all applicable requirements of law, and the depositor’s right to such indemnification will be assigned to the issuing entity. Any failure by TMCC or the depositor to repurchase any affected receivables, or to indemnify the issuing entity, as applicable, could result in delays or reductions in payments on your notes. For additional information, you should refer to “Certain Legal Aspects of the Receivables—Consumer Finance Regulation” and “Repurchases of Receivables” in this prospectus.

The regulatory environment in which TMCC operates could have an adverse effect on TMCC, the depositor and the issuing entity, which could result in losses or delays in payments on your notes.

The Dodd-Frank Wall Street Reform and Consumer Protection Act, or the “Dodd-Frank Act,” and its implementing regulations have had and may continue to have broad implications for the consumer financial services industry.

As a provider of finance and voluntary protection products and services, TMCC operates in a highly regulated environment. TMCC is subject to state licensing requirements and state and federal laws and regulations. In addition, TMCC is subject to governmental and regulatory examinations, information gathering requests, and investigations from time to time at the state and federal levels. Compliance with applicable law is costly and can affect TMCC’s results of operations. Compliance requires forms, processes, procedures, controls and the infrastructure to support these requirements. Compliance may create operational constraints and place limits on pricing, as the laws and regulations in the financial services industry are designed primarily for the protection of consumers. Changes in laws and regulations could restrict TMCC’s ability to operate its business as currently operated, could impose substantial additional costs or require it to implement new processes, which could adversely affect TMCC’s business, prospects, financial performance or financial condition. The failure to comply with applicable laws and regulations could result in significant statutory civil and criminal fines, penalties, monetary damages, attorney or legal fees and costs, restrictions on TMCC’s ability to operate its business, possible revocation of licenses and damage to TMCC’s reputation, brand and valued customer relationships. Any such costs, restrictions, revocations or damage could adversely affect TMCC’s business, prospects, results of operations or financial condition.

TMCC’s principal consumer finance regulator at the federal level is the Consumer Financial Protection Bureau, or the “CFPB,” which has broad regulatory, supervisory and enforcement authority over TMCC. The CFPB’s supervisory authority allows it, among other things, to conduct comprehensive and rigorous examinations to assess TMCC’s compliance with consumer financial protection laws, which could result in enforcement actions, regulatory fines and mandated changes to TMCC’s business, products, policies and procedures. The CFPB’s rulemaking authority includes the authority to promulgate rules regarding, among other practices, debt collection practices that would apply to third-party collectors and first-party collectors, such as TMCC, and rules regarding consumer credit reporting practices. The timing and impact of these rules on TMCC’s business remain uncertain. In addition, the CFPB has focused on the area of auto finance, particularly with respect to indirect financing arrangements, dealer compensation and fair lending compliance, and has questioned the value and increased scrutiny

of the marketing and sale of certain ancillary or add-on products, including products similar to those financed by TMCC or sold through its affiliates.

The CFPB and the Federal Trade Commission, or the “FTC,” may investigate the products, services and operations of credit providers, including banks and other finance companies engaged in auto finance activities. As a result of such investigations, the CFPB and the FTC have announced various enforcement actions against lenders in the past few years involving significant penalties, consent orders, cease and desist orders and similar remedies that, if applicable to TMCC or the products, services and operations TMCC offers, may require TMCC to cease or alter certain business practices, which could have a material adverse effect on TMCC’s results of operations, financial condition, and liquidity. Supervision and investigations by these agencies may result in monetary penalties, increase TMCC’s compliance costs, require changes in its business practices, affect its competitiveness, impair its profitability, harm its reputation or otherwise adversely affect its business.

At the state level, state regulators are taking a more stringent approach to supervising and regulating providers of financial products and services subject to their jurisdiction. For example, certain states have proposed or enacted rate cap bills that would put limits on the maximum rate of finance charges. As described under “Certain Legal Aspects of the Receivables—Consumer Finance Regulation” and “—Other Federal Regulation” in this prospectus, TMCC may take certain actions relating to certain of the receivables, including modifying their terms or making certain payments to obligors. There can be no assurance that TMCC will take any of these actions or, if it does, whether any of these actions will result in the repurchase of some or all of the affected receivables. For additional information regarding state consumer protection laws and related regulations that may affect TMCC, you should refer to “Certain Legal Aspects of the Receivables—Consumer Finance Regulation” in this prospectus.

If the Federal Deposit Insurance Corporation, or the “FDIC,” were appointed receiver of TMCC, the depositor or the issuing entity under the Orderly Liquidation Authority provisions of the Dodd-Frank Act, the FDIC could repudiate contracts deemed burdensome to the estate, including secured debt. TMCC has structured the transfers of the receivables to the depositor and the issuing entity as a valid and perfected sale under applicable state law and under the U.S. Bankruptcy Code to mitigate the risk of the recharacterization of the sale as a grant of security interest to secure debt of TMCC. Any attempt by the FDIC to recharacterize the transfer of the receivables as a grant of a security interest to secure debt that the FDIC then repudiates would cause delays in payments or losses on the notes. In addition, if the issuing entity were to become subject to the Orderly Liquidation Authority, the FDIC may repudiate the debt of the issuing entity and the noteholders would have a secured claim in the receivership of the issuing entity. Also, if the issuing entity were subject to Orderly Liquidation Authority, the noteholders would not be permitted to accelerate the debt, exercise remedies against the collateral or replace the servicer without the FDIC’s consent for 90 days after the receiver is appointed. As a result of any of these events, delays in payments on the notes would occur and possible reductions in the amount of those payments could occur. For additional information, you should refer to “Certain Legal Aspects of the Receivables—Dodd-Frank Act Orderly Liquidation Authority Provisions” in this prospectus.

No assurances can be given that the liquidation framework for the resolution of “covered financial companies” would not apply to TMCC or its affiliates, including the depositor and the issuing entity. For additional information, you should refer to “Certain Legal Aspects of the Receivables—Dodd-Frank Act Orderly Liquidation Authority Provisions—Potential Applicability to TMCC, the Depositor and the Issuing Entity” in this prospectus.

On March 27, 2020, the Coronavirus Aid, Relief, and Economic Security Act (the “CARES Act”) was signed into law. The CARES Act was extensive and significant legislation adopted to address the COVID-19 Outbreak, and it includes various provisions intended to help consumers, such as new requirements affecting credit reporting, direct payments to workers, and unemployment relief. Portions of the assistance provided by the CARES Act lapsed by the end of 2020. On December 27, 2020, the Consolidated Appropriations Act of 2021 (the “Appropriations Act”) was signed into law, which included a $900 billion economic stimulus package and renewed certain provisions of the CARES Act, including reauthorizing and providing additional funding for several stimulus programs established by the CARES Act. The Appropriations Act also restored the Federal Pandemic Unemployment Compensation program, which provides an additional $300 per week to individuals collecting traditional unemployment compensation. This benefit was available for weeks of unemployment beginning after December 26, 2020 and ending on March 14, 2021. On March 11, 2021, President Biden signed the American Rescue Plan Act of 2021 (the “American Rescue Plan Act”), which included a $1.9 trillion economic stimulus package. The American Rescue Plan Act built upon the CARES Act and the Appropriations Act by extending unemployment benefits through September 6, 2021 (though some states discontinued the additional federal unemployment benefits ahead of this date), providing stimulus checks to certain individuals and families up to

$1,400 per adult and eligible dependent, making the Small Business Administration’s Paycheck Protection Program (the “PPP”) more accessible to businesses and nonprofits, adding additional funding of $7.25 billion to the PPP and providing additional relief to state and local communities.

It is not known how many obligors of the receivables may have been or are receiving benefits under the CARES Act, the Appropriations Act, or the American Rescue Plan Act, or what the effect of any reduction of such benefits may be on the ability of the obligors to meet their payment obligations under the receivables. The potential impact of these acts on TMCC and its affiliates or on the obligors is not yet known. It is possible that compliance with the implementing regulations under such acts may impose costs on, or create operational constraints for, TMCC and may have an adverse impact on the ability of TMCC to effectively service the receivables. Further, Federal, state or local governments, could enact, and in some cases already have enacted, laws, regulations, executive orders or other guidance that allow obligors to stop making scheduled payments on certain obligations for some period of time, require modifications to the related contracts (e.g., waiving accrued interest), or preclude creditors from exercising certain rights or taking certain actions with respect to collateral securing such obligations, including repossession or liquidation of financed vehicles.

Changes to the regulatory environment in which TMCC operates, including, for example, laws or regulations intended to mitigate factors contributing to, or intended to address the potential impacts of, climate change, could have a material adverse effect on TMCC’s business, results of operations and financial condition. Any such changes could also adversely affect TMCC’s ability to service the receivables and perform its other obligations under the transaction agreements, which could have an adverse effect on your notes.

The return on the notes could be reduced by shortfalls due to state laws limiting collections on certain receivables.

Pursuant to federal law and the laws of various states, payments on retail installment sales contracts or installment loans, such as the receivables, by certain members of the military who are on active duty and residents in those states who are called into active duty with the national guard or the reserves by the related governor, will be deferred under certain circumstances. These laws and related regulations may also limit the ability of the servicer to repossess the financed vehicle securing a receivable. As a result of such legislation or regulations, there may be delays or reductions in payment of, and increased losses on the receivables and you may suffer a loss on your notes. We do not know how many receivables may be impacted by such legislation or regulations. For additional information, you should refer to “Certain Legal Aspects of the Receivables—Other Limitations” in this prospectus.

Risks Primarily Related to Servicing

Funds held by the servicer that are intended to be used to make payments on the notes may be exposed to a risk of loss.

The servicer generally may retain all payments and proceeds collected on the receivables during each collection period. The servicer is generally not required to segregate those funds from its own accounts until the funds are deposited in the collection account on or prior to each payment date. Until any collections or proceeds are deposited into the collection account, the servicer will be able to invest those amounts for its own benefit at its own risk. The issuing entity and noteholders are not entitled to any amount earned on the funds held by the servicer. If the servicer does not deposit the funds in the collection account as required on any payment date, the issuing entity may be unable to make the payments owed on your notes.

A servicer default may result in additional costs, increased servicing fees by a substitute servicer or a diminution in servicing performance, including higher delinquencies and defaults, all of which may have an adverse effect on your notes.

If a servicer default occurs, either the indenture trustee or the holders of notes evidencing not less than a majority of the aggregate principal amount of the notes of the controlling class then outstanding, acting together as a single class (excluding for such purposes the aggregate outstanding principal amount of any notes held of record or beneficially owned by TMCC, TAFR LLC or any of their affiliates), may remove the servicer without the consent of the owner trustee or the certificateholders. In the event of the removal of the servicer and the appointment of a successor servicer, we cannot predict the cost of the transfer of servicing to the successor, the ability of the successor to perform the obligations and duties of the servicer under the sale and servicing agreement; or the servicing fees charged by the successor. In addition, the holders of notes evidencing not less than a majority of the aggregate principal amount of the notes of the controlling class then outstanding (excluding for such purposes the aggregate outstanding principal amount of any notes held of record or beneficially owned by TMCC, TAFR LLC or any of

their affiliates), acting together as a single class, have the ability, with some exceptions, to waive defaults by the servicer. Furthermore, the indenture trustee may experience difficulties in appointing a successor servicer and during any transition phase, it is possible that normal servicing activities could be disrupted, resulting in increased delinquencies and/or defaults on the receivables. Additionally, because the servicing fee is based on a percentage of the aggregate outstanding amount of the receivables, the fee the servicer receives each month will be reduced as the size of the pool decreases over time. At some point, if the need arises to obtain a successor servicer, the fee that such successor servicer would earn might not be sufficient to induce a potential successor servicer to agree to service the remaining receivables in the pool, which could result in increased delinquencies and/or defaults on the receivables.

There may be potential adverse effects of credit ratings-related matters on the servicer, which could have an adverse effect on your notes.

Several credit rating agencies rate the long-term corporate credit and/or debt of TMCC and its affiliates. The credit ratings of TMCC depend, in large part, on the existence of the credit support arrangements with Toyota Financial Services Corporation and Toyota Motor Corporation and on the financial condition and results of operations of Toyota Motor Corporation. If these arrangements (or replacement arrangements acceptable to the applicable rating agencies) become unavailable to TMCC, or if the credit ratings of the credit support providers were lowered, TMCC’s credit ratings would be adversely impacted. The cost and availability of financing is influenced by credit ratings, which are intended to be an indicator of the creditworthiness of a particular company, security or obligation.

Credit rating agencies which rate the credit of Toyota Motor Corporation and its affiliates, including TMCC, may qualify or alter ratings at any time. Global economic conditions and other geopolitical factors, including the COVID-19 Outbreak, may directly or indirectly affect such ratings and your notes. Any downgrade in the sovereign credit ratings of the United States or Japan may directly or indirectly have a negative effect on the ratings of Toyota Motor Corporation and TMCC. Downgrades or placement on review for possible downgrades could result in an increase in TMCC’s borrowing costs as well as reduced access to global unsecured debt capital markets. These factors would have a negative impact on TMCC’s competitive position, results of operations and financial condition, which could affect the ability of the servicer to collect on the receivables and therefore result in delays in payments or principal losses on your notes if the available credit enhancement has been exhausted.

A security breach or a cyber-attack affecting TMCC could adversely affect TMCC’s business, results of operations and financial condition, which could have an adverse effect on your notes.

TMCC collects and stores certain personal and financial information from customers, employees, and other third parties. Security breaches or cyber-attacks involving TMCC’s systems or facilities, or the systems or facilities of third-party providers, could expose TMCC to a risk of loss of personal information of customers, employees and third parties or other confidential, proprietary or competitively sensitive information, business interruptions, regulatory scrutiny, actions and penalties, litigation, reputational harm, a loss of confidence, and other financial and non-financial costs, all of which could potentially have an adverse impact on TMCC’s future business with current and potential customers, results of operations and financial condition.

TMCC relies on encryption and other information security technologies licensed from third parties to provide security controls necessary to help in securing online transmission of confidential information pertaining to customers, employees and other aspects of TMCC’s business. Advances in information system capabilities, new discoveries in the field of cryptography or other events or developments may result in a compromise or breach of the technology that TMCC uses to protect sensitive data. A party who is able to circumvent TMCC’s security measures by methods such as hacking, fraud, trickery or other forms of deception could misappropriate proprietary information or cause interruption in TMCC’s operations. TMCC may be required to expend capital and other resources to protect against such security breaches or cyber-attacks or to remediate problems caused by such breaches or attacks. TMCC’s security measures are designed to protect against security breaches and cyber-attacks, but TMCC’s failure to prevent such security breaches and cyber-attacks could subject TMCC to liability, decrease TMCC’s profitability and damage TMCC’s reputation. Even if a failure of, or interruption in, TMCC’s systems or facilities is resolved timely or an attempted cyber incident or other security breach is successfully avoided or thwarted, it may require TMCC to expend substantial resources or to take actions that could adversely affect customer satisfaction or behavior and expose TMCC to reputational harm.

TMCC could also be subjected to cyber-attacks that could result in slow performance and loss or temporary unavailability of TMCC’s information systems. Information security risks have increased because of new

technologies, the use of the internet and telecommunications technologies (including mobile devices) to conduct financial and other business transactions, and the increased sophistication and activities of organized crime, perpetrators of fraud, terrorists, and others. In addition, TMCC may have increased cyber-security risks and increased vulnerability to security breaches and other information technology disruptions as a result of the COVID-19 Outbreak and increased remote work arrangements. TMCC may not be able to anticipate or implement effective preventative measures against all security breaches of these types, especially because the techniques used change frequently and because attacks can originate from a wide variety of sources. The occurrence of any of these events could have a material adverse effect on TMCC’s business, results of operations and financial condition, could adversely affect TMCC’s ability to service the receivables and perform its other obligations under the transaction agreements, and could have an adverse effect on your notes.

TMCC’s enterprise data practices, including the collection, use, sharing, and security of personal and financial information of TMCC’s customers, employees, and third-party individuals, are subject to increasingly complex, restrictive, and punitive regulations.

Under current laws, the failure to maintain compliant data practices could result in consumer complaints and regulatory inquiry, resulting in civil or criminal penalties, as well as brand impact or other harm to TMCC’s business. In addition, increased consumer sensitivity to real or perceived failures in maintaining acceptable data practices could damage TMCC’s reputation and deter current and potential customers from using TMCC’s products and services. For example, well-publicized allegations involving the misuse or inappropriate sharing of personal information have led to expanded governmental scrutiny of practices relating to the safeguarding of personal information and the use or sharing of personal data by companies in the U.S. and other countries. That scrutiny has in some cases resulted in, and could in the future lead to, the adoption of stricter laws and regulations relating to the use and sharing of personal information. For example, some states have enacted and others are considering enacting data protection regimes that grant consumers broad new rights including access to, deletion of, and limiting the sharing of personal information that is collected by businesses and requiring regulated entities to establish measures to identify, manage, secure, track, produce, update and delete personal information. In some jurisdictions, these laws and regulations provide a private right of action that would allow customers to bring suit directly against us for certain violations of these laws and regulations. These types of laws and regulations could prohibit or significantly restrict financial services providers such as TMCC from sharing information among affiliates or with third parties such as vendors, and thereby increase compliance costs, or could restrict TMCC’s use of personal data when developing or offering products or services to customers. These restrictions could inhibit TMCC’s development or marketing of certain products or services, or increase the costs of offering them to customers. Because many of these laws are new, there is little clarity as to their interpretation, as well as a lack of precedent for the scope of enforcement. In addition, these laws are state specific and have specific details that are not uniform state-to-state. The cost of compliance with these laws and regulations will be high and is likely to increase in the future. Any failure or perceived failure to comply with applicable privacy or data protection laws and regulations could result in requirements to modify or cease certain operations or practices, significant liabilities or fines, penalties or other sanctions, which could adversely affect TMCC’s ability to service the receivables and perform its other obligations under the transaction agreements, and could have an adverse effect on your notes.

A failure or interruption of TMCC’s information systems, including in connection with any consolidation of or change in servicing operations, could have an adverse effect on your notes.

TMCC relies on its own information systems and third-party information systems to manage its operations, which creates meaningful operational risk for TMCC. Any failure or interruption of TMCC’s information systems or the third-party information systems on which it relies as a result of inadequate or failed processes or systems, human errors, employee misconduct, catastrophic events, security breaches, acts of vandalism, computer viruses, malware, ransomware, misplaced or lost data, or other events could disrupt TMCC’s normal operating procedures, damage its reputation and have an adverse effect on TMCC’s business, results of operations and financial condition, which could adversely affect TMCC’s ability to service the receivables and perform its other obligations under the transaction agreements, and could have an adverse effect on your notes. These operations risks may be increased as a result of remote work arrangements due to the COVID-19 Outbreak. From time to time, TMCC may update its servicing systems in order to improve operating efficiency, update technology and enhance customer services. For example, TMCC is in the process of implementing a new core servicing system to replace its legacy core servicing system, which includes building a new enterprise integration platform that also accommodates downstream systems. In connection with any such updates, TMCC may experience limited disruptions in servicing activities both during and following roll-out of the new servicing systems or platforms caused by, among other things, periods of system down-time and periods devoted to user training. These and other implementation related difficulties may contribute

to higher delinquencies. It is not possible to predict with any degree of certainty all of the potential adverse consequences that may be experienced, and there can also be no assurance that any such disruptions in servicing activities will not adversely affect TMCC’s ability to service the receivables, which could have an adverse effect on your notes.

Risks Primarily Related to Bankruptcy and Insolvency of Transaction Parties and Perfection of Security Interests

The bankruptcy of TMCC or the depositor could result in losses or delays in payments on your notes.

If TMCC or the depositor were to become subject to bankruptcy proceedings, you could experience losses or delays in the payments on your notes. TMCC will sell the receivables to the depositor, and the depositor will in turn sell the receivables to the issuing entity. However, if TMCC or the depositor were to become subject to a bankruptcy proceeding, the court in the bankruptcy proceeding could conclude that TMCC or the depositor effectively still owns the receivables by concluding that the sale to the depositor by TMCC or the sale to the issuing entity by the depositor was not a “true sale” or that the issuing entity should be consolidated with TMCC or the depositor for bankruptcy purposes. If a court were to reach this conclusion, you could experience losses or delays in payments on the notes as a result of, among other things:

| • | an “automatic stay” which prevents secured creditors from exercising remedies against a debtor in bankruptcy without permission from the court and provisions of the U.S. Bankruptcy Code that permit substitution of collateral in certain circumstances; |

| • | certain tax or government liens on TMCC’s or the depositor’s property (that arose prior to the transfer of a receivable to the issuing entity) having a prior claim on collections before the collections are used to make payments on your notes; and |

| • | the fact that neither the issuing entity nor the indenture trustee has a perfected security interest in (a) one or more of the vehicles securing the receivables or (b) any cash collections held by TMCC or the depositor at the time TMCC or the depositor were to become the subject of a bankruptcy proceeding. |

The depositor will take steps in structuring the transactions described in this prospectus to minimize the risk that a court would consolidate the issuing entity with the depositor for bankruptcy purposes or conclude that the sale of receivables to the issuing entity was not a “true sale.” For additional information, you should refer to “Certain Legal Aspects of the Receivables—Certain Bankruptcy Considerations” in this prospectus.

The bankruptcy of the issuing entity could result in losses or delays in payments on your notes.

If the issuing entity were to become subject to bankruptcy proceedings, you could experience losses or delays in the payments on your notes as a result of, among other things, an “automatic stay,” which prevents secured creditors from exercising remedies against a debtor in bankruptcy without permission from the applicable court, and provisions of the U.S. Bankruptcy Code that permit substitution of collateral in limited circumstances.

The insolvency or bankruptcy of the servicer could delay the appointment of a successor servicer or reduce payments on your notes.

In the event of default by the servicer resulting solely from certain events of insolvency or the bankruptcy of the servicer, the indenture trustee could neither appoint a successor servicer nor prevent the servicer from appointing a sub-servicer, as the case may be, without the consent of the bankruptcy trustee or the bankruptcy court, and delays in the collection of payments on the receivables may occur. Any delay in the collection of payments on the receivables may delay or reduce payments to noteholders.

The issuing entity’s interests in financed vehicles may be unenforceable or defeated.

The certificates of title for vehicles financed by TMCC name TMCC as the secured party. The certificates of title for financed vehicles under contracts assigned to the issuing entity will not be amended to identify the issuing entity as the new secured party because it would be administratively burdensome to do so. However, financing statements showing the transfer to the issuing entity of TMCC’s and the depositor’s interest in the receivables and the transfer to the indenture trustee of the issuing entity’s interest in the receivables will be filed with the appropriate governmental authorities. TMCC, as servicer, will retain the documentation for the receivables and the certificates of title. Because of these arrangements, another person could acquire an interest in the receivables and the financed vehicles that is judged by a court of law to be superior to the issuing entity’s or the indenture trustee’s interest. Examples of these persons are other creditors of the obligor, a subsequent purchaser of a financed vehicle or another lender who finances the vehicle. Some of the ways this could happen are described under “Certain Legal Aspects of

the Receivables” in this prospectus. In some circumstances, either the depositor or the servicer will be required to purchase receivables if a security interest superior to the claims of others has not been properly established and maintained. The details of this obligation are described under “Repurchases of Receivables” in this prospectus.

If the servicer does not maintain control of the receivables evidenced by electronic contracts, the issuing entity may not have a perfected interest in those receivables.