Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 2003

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Transition Period from to

Commission File Number 333-69826

Hornbeck Offshore Services, Inc.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 72-1375844 | 4424 | ||

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | (Primary Standard Industrial Classification Code Number) |

103 Northpark Boulevard, Suite 300

Covington, Louisiana 70433

(985) 727-2000

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Securities registered pursuant to Section 12(b) of the Act:

None.

Securities registered pursuant to Section 12(g) of the Act:

None.

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ¨ No x

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Yes ¨ No ¨ NOT APPLICABLE.

Indicate by check mark whether the Registrant is an accelerated filer (as defined in Exchange Act Rule 12b-2). Yes ¨ No x

The aggregate market value of common stock, par value $.01 per share, held by non-affiliates of the Registrant is not ascertainable as such stock is privately held and there is no public market for such stock. The total number of shares of the Registrant’s common stock, par value $.01 per share, outstanding as of March 5, 2004 was 14,527,814 (after giving effect to a 1-for-2.5 reverse stock split effective on such date)

DOCUMENTS INCORPORATED BY REFERENCE

None.

Table of Contents

HORNBECK OFFSHORE SERVICES, INC. AND SUBSIDIARIES

FORM 10-K

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2003

| 1 | ||

| 1 | ||

| 1 | ||

| 2 | ||

| 6 | ||

| 9 | ||

| 11 | ||

| 12 | ||

| 12 | ||

| 13 | ||

| 17 | ||

| 17 | ||

| 17 | ||

| 17 | ||

| 18 | ||

| 18 | ||

| 18 | ||

| 19 | ||

Item 5—Market for the Registrant’s Common Stock and Related Stockholder Matters | 19 | |

| 19 | ||

Item 7—Management’s Discussion and Analysis of Financial Condition and Results of Operations | 22 | |

| 22 | ||

| 24 | ||

| 26 | ||

| 29 | ||

| 31 | ||

| 32 | ||

| 32 | ||

| 34 | ||

Item 7a—Quantitative and Qualitative Disclosures About Market Risk | 35 | |

| 35 | ||

Item 9—Changes in and Disagreements with Accountants on Accounting and Financial Disclosures | 35 | |

| 35 | ||

| 37 | ||

| 37 | ||

| 37 | ||

| 39 | ||

| 40 | ||

| 40 | ||

| 42 | ||

| 42 | ||

| 43 | ||

| 43 | ||

| 43 | ||

| 44 | ||

| 44 | ||

| 47 | ||

| 48 | ||

i

Table of Contents

| 48 | ||

| 50 | ||

Item 15—Exhibits, Financial Statement Schedules and Reports on Form 8-K | 50 | |

| F-1 | ||

| S-1 | ||

ii

Table of Contents

ITEMS 1 AND 2.—Business and Properties.

Hornbeck Offshore Services, Inc. was incorporated under the laws of the State of Delaware in 1997. In this annual report on Form 10-K, “company,” “we,” “us” and “our” refers to Hornbeck Offshore Services, Inc. and its subsidiaries, except as otherwise indicated. References in this annual report on Form 10-K to “OSVs” mean offshore supply vessels; to “deepwater” mean offshore areas, generally 1,000’ to 5,000’ in depth, and ultra-deepwater areas, generally more than 5,000’ in depth; to “deep well” mean a well drilled to a true vertical depth of 15,000’ or greater; and to “new generation,” when referring to OSVs, mean modern, deepwater-capable vessels subject to the regulations promulgated under the International Convention on Tonnage Measurement of Ships, 1969, which was adopted by the United States and made effective for all U.S.-flagged vessels in 1992.

BUSINESS

We are a leading provider of technologically advanced, new generation OSVs serving the offshore oil and gas industry, primarily in the U.S. Gulf of Mexico and in select international markets. The focus of our OSV business is on complex exploration and production activities, which include deepwater, deep well and other logistically demanding projects. We are also a leading transporter of petroleum products through our tug and tank barge segment serving the energy industry, primarily in the northeastern United States and Puerto Rico.

In the mid-1990s, oil and gas producers began seeking large hydrocarbon reserves at deeper well depths using new, specialized drilling and production equipment. We recognized that the existing fleet of conventional 180’OSVs operating in the U.S. Gulf of Mexico was not designed to support these more complex projects or to operate in the challenging environments in which they were conducted. Therefore, in 1997, we began a program to construct new generation OSVs based upon the proprietary designs of our in-house team of naval architects. Since that time, we have constructed 17 new generation OSVs using these proprietary designs, and expanded our fleet with the acquisitions of a total of six additional new generation OSVs. Our fleet of 23 OSVs is among the youngest fleets in the industry with an average age of approximately three years.

Our OSVs were purposefully designed with the flexibility to meet the diverse needs of our clients in all stages of their exploration and production activities. As a result, all of our OSVs have enhanced capabilities that allow them to more effectively support premium drilling equipment required for deep drilling and related specialty services. In contrast to conventional 180’ OSVs, our vessels have dynamic positioning capability, as well as greater storage and off-loading capacity. We are capable of providing OSV services to our customers anywhere in the world and we are actively pursuing additional contracts in select international markets.

Historically, demand for our OSV services has been primarily driven by the drilling of deep wells, whether in the deepwater or on the U.S. Continental Shelf, and other complex exploration and production projects that require specialized drilling and production equipment. In addition, our new generation OSVs are increasingly in demand by our customers for conventional drilling projects. Customers on such projects are willing to pay more than the prevailing dayrates for conventional 180’ OSVs because of the ability of our OSVs to reduce overall offshore logistics costs for the customer through the vessels’ greater capacities and operating efficiencies.

According to the Minerals Management Service, or MMS, in 2002 the deepwater region accounted for 68% of total U.S. Gulf of Mexico oil production and 38% of total U.S. Gulf of Mexico natural gas production, up substantially from 4% and 1%, respectively, in 1990. In addition, the MMS estimates that deep reservoirs on the Continental Shelf may hold up to 55 tcf of undiscovered natural gas. This potential reserve base compares favorably to the current total of approximately 26 tcf of proven natural gas reserves in the entire U.S. Gulf of Mexico. Our new generation OSVs are also well suited for drilling in logistically demanding projects and frontier areas, where support infrastructure is severely limited.

1

Table of Contents

Our tug and tank barge fleet consists of 12 ocean-going tugs, 16 ocean-going tank barges and one coastwise tanker. We believe our tug and tank barge business complements our OSV business by providing additional revenue and geographic diversification, while allowing us to offer another line of services to integrated oil and gas companies. Demand for our tug and tank barge services is primarily driven by the level of refined petroleum product consumption in the northeastern United States and Puerto Rico, our core operating markets. The Energy Information Administration, or EIA, projects that refined petroleum product consumption in the East Coast region of the United States will increase by an average of 1.7% per year from 2002 to 2010. Demand for refined petroleum products is primarily driven by population growth, the strength of the U.S. economy, seasonal weather patterns, oil prices and competition from alternate energy sources.

The OSV Industry

OSVs primarily serve exploratory and developmental drilling rigs and production facilities and support offshore construction and subsea maintenance activities. OSVs differ from other types of marine vessels in their cargo carrying flexibility and capacity. In addition to transporting deck cargo, such as pipe or drummed material and equipment, OSVs also transport liquid mud, potable and drilling water, diesel fuel, dry bulk cement and personnel between shore bases and offshore rigs and facilities. In general, demand for OSVs, as evidenced by dayrates and utilization rates, is primarily related to offshore oil and natural gas exploration, development and production activity, which in turn is influenced by a number of factors, including oil and natural gas prices and the drilling budgets of offshore exploration and production companies.

OSVs operate worldwide, but are generally concentrated in relatively few offshore regions with high levels of exploration and development activity such as the Gulf of Mexico, the North Sea, Southeast Asia, West Africa, Brazil and the Middle East. While there is some vessel migration between regions, key factors such as mobilization costs, vessel suitability and government statutes prohibiting foreign-flagged vessels from operating in certain waters generally limit such migration.

The U.S. Gulf of Mexico is a critical oil and natural gas supply basin for the United States, accounting for 30% and 25%, respectively, of total U.S. oil and natural gas production in 2002. Offshore oil and natural gas drilling and production in the U.S. Gulf of Mexico occurs on the Continental Shelf and in the deepwater. Drilling activity on the Continental Shelf has historically been limited to shallow wells, or wells with true vertical depths of less than 15,000’. More recently, however, operators have begun to increasingly focus exploratory efforts on deep wells and natural gas reserves located below 15,000’. These deep prospects are largely undeveloped, but are believed to contain significant reserves.

While the shallow waters of the Continental Shelf have been actively explored for decades, relatively few deep wells have been drilled historically due to the high cost associated with these wells. The dry hole cost of a typical Continental Shelf well drilled from 8,000’ to 12,000’ generally ranges from $4 million to $8 million, while the dry hole cost for a deep well drilled in a similar location but to 15,000’ or more can range from $10 million to $25 million. The higher costs associated with the drilling of deep wells can be attributed to, among other things, the need for specialized, high-end drilling rigs and related equipment, greater volumes of downhole materials such as liquid mud, tubular products and cement, and longer drilling times.

Despite the higher costs associated with deep well Continental Shelf drilling, operators, especially those in search of natural gas, have continued to demonstrate interest. This interest is driven by, among other things, the potential for the discovery of significant natural gas reserves. The MMS estimates that there may be up to 55 tcf of undiscovered, conventionally recoverable, deep well natural gas on the Continental Shelf. Moreover, the abundance of existing platforms, production facilities and pipelines on the Continental Shelf allow new deep gas to flow quickly to market. In addition, MMS data indicates that higher natural gas production rates can be expected from wells drilled on the Continental Shelf below 16,000’. Furthermore, the MMS royalty relief programs enacted in 2001, and expanded in August 2003 and again in January 2004, have stimulated interest by reducing the development costs of these deep wells. The combination of these factors partly compensates for the higher drilling costs of deep wells on the Continental Shelf and can allow operators to commercially produce discovered reserves in this market. While drilling on the Continental Shelf has declined, gas production data from 2000 to 2003 provided by IHS Energy, an energy research company, suggests an

2

Table of Contents

increasing focus on deep wells on the Continental Shelf. From 2000 to 2003, gas production from deep wells as a percentage of total wells on the Continental Shelf increased from 22% to 30%.

Recent discoveries of large hydrocarbon reserves in deepwater fields in the Gulf of Mexico and at deeper well depths on the Continental Shelf have resulted in increased developmental and exploratory drilling activities in these areas. The deepwater region of the U.S. Gulf of Mexico is an increasingly important source of oil and natural gas production with many unexplored areas of potential oil and natural gas reserves. According to the 2004 Deepwater and Ultra Deepwater Report of Infield Systems Limited, an international energy research firm, the U.S. Gulf of Mexico had 58 deepwater projects developed between 1999 and 2003, and an additional 79 deepwater projects have been identified for development between 2004 and 2008.

Because oil and natural gas exploration, development and production costs in the shallow well Continental Shelf market are generally lower than those in the deepwater or deep well environments, shallow well drilling activity on the Continental Shelf is typically more sensitive to fluctuations in commodity prices, particularly the price of natural gas. Accordingly, actual or anticipated decreases in oil and natural gas prices generally result in reduced offshore drilling activity and correspondingly lower demand for the conventional 180’ OSVs serving the shallow well Continental Shelf market. This causes a corresponding decline in OSV dayrates and utilization rates in that market. In contrast, the relatively larger capital commitments and longer lead times and investment horizons associated with deepwater, particularly ultra-deepwater, and deep well developments make it less likely that an operator will abandon such projects in response to a short-term decline in oil or natural gas prices. Dayrates and utilization rates for new generation OSVs that serve the deepwater and deep well markets are, therefore, generally less sensitive to short-term commodity price fluctuations and tend to be more stable than dayrates and utilization rates for OSVs serving the shallow well Continental Shelf market.

According to our analysis of the industry and data compiled from various industry sources, including the U.S. Coast Guard, we estimate that the U.S.-flagged OSV fleet currently totals 353 vessels, substantially all of which are located in the Gulf of Mexico. Of this total, 246, or 70% are conventional 180’ OSVs that primarily operate on the Continental Shelf. The remaining 107 vessels are new generation OSVs that primarily operate in the deepwater Gulf of Mexico. However, during soft market conditions in the deepwater, these modern vessels have increasingly migrated at premium dayrates to conventional drilling environments, such as the U.S. Continental Shelf, Mexico and Trinidad & Tobago. Of the conventional OSV fleet, a significant number are currently cold-stacked. Vessels that are cold-stacked have generally been removed from active service by the operator due to lack of demand. In contrast, we believe there are currently no new generation OSVs cold-stacked.

The Market for New Generation OSVs

Complex exploration and production projects require specialized equipment and higher volumes of supplies to meet the more difficult operating environment associated with such offshore developments. In order to better serve these projects and meet customer demands, new generation OSVs, including our entire OSV fleet, are designed with larger capacities, including greater liquid mud and dry bulk cement capacities, as well as larger areas of open deck space than conventional 180’ OSVs. These features are essential to the effective servicing of deepwater drilling projects, which are often distant from shore-based support infrastructure, because they allow a vessel to make fewer trips to supply the liquid mud, drilling water, dry bulk cement and other needs of the customer. In addition, OSVs operating in deepwater environments generally require dynamic positioning, or anchorless station-keeping capability, primarily because customers’ safety procedures preclude OSVs from tying up to deepwater installations, and to enable continued operation in adverse weather conditions. We believe that conventional 180’ OSVs, substantially all of which lack dynamic positioning capability and sufficient on-deck or below-deck cargo capacity, are not capable of operating effectively or economically in the deepwater market. In addition, certain ports have draft or other logistical impediments, which limit the pool of new generation vessels capable of servicing such ports. Our proprietary vessels were designed to work under these shallow draft and logistically demanding conditions.

As a result of recent deepwater and deep well drilling activity, utilization rates for new generation OSVs in the U.S. Gulf of Mexico have averaged approximately 95% over the last two years while the average utilization rate for the conventional 180’ OSV fleet over the same period has been approximately 73%. Additional utilization for new generation OSVs has come from increasing demand for these vessels in support of conventional shelf drilling projects. Moreover, during the same two-year period, average dayrates for new generation OSVs were generally more than double the average dayrates

3

Table of Contents

of conventional 180’ OSVs. Given the recent and expected deepwater and deep well activity, we believe that the supply of new generation OSVs, including vessels currently available and vessels being constructed under announced construction plans, is more than sufficient to meet the current and near term demand for such vessels. Long-term projections of deepwater and deep well activity, however, indicate a potential shortage of new generation OSVs. Furthermore, although U.S.-flagged vessels operating in overseas locations may be remobilized to the U.S. Gulf of Mexico, historically such remobilization has been limited.

Our OSV Business

We currently own and operate a fleet of 23 new generation OSVs. Our in-house engineering team, using our proprietary designs, built 17 of our OSVs expressly to meet the demands of deepwater regions and other complex drilling projects. Our in-house engineering team possesses significant vessel operating experience. Drawing from this experience, we work closely with potential charterers to design vessels specifically to meet their anticipated needs. This is particularly the case when the charterer will operate a project that could have a duration of more than 20 years and require expenditures exceeding $1 billion. All of our vessels have up to three times the dry bulk capacity and deck space, two to ten times the liquid mud capacity and two to four times the deck tonnage compared to conventional 180’ OSVs. The advanced cargo handling systems of our 17 proprietary OSVs allow for dry bulk and liquid cargos to be loaded and unloaded three times faster than conventional 180’ OSVs, while the solid state controls of their engines typically result in a 20% greater fuel efficiency than vessels powered by conventional engines. In addition, our larger classes of proprietary OSV designs, designated by us as our 240 ED and 265 classes, were designed, in part, to supply the substantially greater liquid mud volume and other cargo capacity required for ultra-deepwater drilling. We believe that the customers’ recognition of the superior capabilities of our proprietary OSVs has contributed to our ability to achieve higher dayrates and utilization rates and increased overall operating cost efficiencies than our competitors.

All of our new generation OSVs are equipped with dynamic positioning systems and controllable pitch thrusters, which allow our vessels to maintain position within minimal variance, and state-of-the-art safety, emergency power, fire alarm and fire suppression systems and systems monitoring equipment. The unique hull design and integrated rudder and thruster system of our 17 proprietary OSVs provide for a more maneuverable vessel. These proprietary vessels also have double-bottomed and double-sided hulls that minimize environmental impact in the event of vessel collisions or groundings, solid state controls that minimize visible soot and polluting gases and zero discharge sewage and waste systems that minimize the impact on marine environments. In addition, these 17 vessels are either fully SOLAS (Safety of Life at Sea) certified or SOLAS ready. SOLAS is the international convention that regulates the technical characteristics of vessels for purposes of ensuring international standards of safety for vessels engaged in commerce between international ports. These features allow us to market our proprietary OSVs for service in international waters.

Our technologically advanced, new generation OSVs are also capable of providing specialty services in support of certain of our customers, including well stimulation, remotely operated vehicles, or ROVs, used in oilfield subsea construction and maintenance, underwater inspections, marine seismic operations, and certain non-energy applications such as fiber optics cable installation, military work and containerized cargo transportation. Compared to conventional 180’ OSVs, our OSVs have more dead weight capacity, deck space, and berthing accommodations, improved maneuverability and greater fuel efficiency. We believe these characteristics strengthen demand for our OSVs in specialty situations. Two of our vessels, theHOS Innovatorand theHOS Dominator,currently provide ROV subsea construction and maintenance support for a large oilfield service company under contracts that each have an initial term of three years. TheBJ Blue Rayprovides deepwater well stimulation support services for another large oilfield service company under a contract with a five-year initial term. This vessel was the first U.S.-flagged well stimulation vessel to receive the American Bureau of Shipping WS and DPS2 class notations. We believe theBJ Blue Rayis one of the most technologically sophisticated well stimulation vessels in the world.

On June 26, 2003, we completed the acquisition of five 220’ new generation OSVs from Candy Marine Investment Corporation, an affiliate of Candy Fleet Corporation, or Candy Fleet. Following the completion in July 2003 of a private placement of our common stock and satisfaction of certain other conditions, on August 6, 2003 we acquired an additional 220’ new generation OSV from Candy Fleet. These six vessels complement our existing OSV fleet and have allowed us to expand our service offerings to clients, particularly those drilling wells on the Continental Shelf.

4

Table of Contents

The following table provides information, as of March 1, 2004, regarding our existing fleet of OSVs.

Offshore Supply Vessels(1)

Name | Class | Current Service Function | Built (Acquired) | Deadweight (long tons) | Brake Horsepower | |||||

BJ Blue Ray | 265 | Well Stimulation | November 2001 | 3,756 | 6,700 | |||||

HOS Brimstone | 265 | Supply | June 2002 | 3,756 | 6,700 | |||||

HOS Stormridge | 265 | Supply | August 2002 | 3,756 | 6,700 | |||||

HOS Sandstorm | 265 | Supply | October 2002 | 3,756 | 6,700 | |||||

HOS Bluewater | 240 ED | Supply | March 2003 | 2,850 | 4,000 | |||||

HOS Gemstone | 240 ED | Supply | June 2003 | 2,850 | 4,000 | |||||

HOS Greystone | 240 ED | Supply | September 2003 | 2,850 | 4,000 | |||||

HOS Silverstar | 240 ED | Supply | January 2004(2) | 2,850 | 4,000 | |||||

HOS Innovator | 240 E | ROV Support(3) | April 2001 | 2,380 | 4,500 | |||||

HOS Dominator | 240 E | ROV Support(3) | February 2002 | 2,380 | 4,500 | |||||

HOS Deepwater | 240 | Supply | November 1999 | 2,250 | 4,500 | |||||

HOS Cornerstone | 240 | Supply | March 2000 | 2,250 | 4,500 | |||||

HOS Explorer | 220 | Supply | February 1999 (June 2003) | 1,607 | 3,900 | |||||

HOS Express | 220 | Supply | September 1998 (June 2003) | 1,607 | 3,900 | |||||

HOS Pioneer | 220 | Supply | June 2000 (June 2003) | 1,607 | 4,200 | |||||

HOS Trader | 220 | Supply | November 1997 (June 2003) | 1,607 | 3,900 | |||||

HOS Voyager | 220 | Supply | May 1998 (June 2003) | 1,607 | 3,900 | |||||

HOS Mariner | 220 | Supply | September 1999 August 2003) | 1,607 | 3,900 | |||||

HOS Crossfire | 200 | Supply | November 1998 | 1,750 | 4,000 | |||||

HOS Super H | 200 | Supply | January 1999 | 1,750 | 4,000 | |||||

HOS Brigadoon | 200 | Supply | March 1999 | 1,750 | 4,000 | |||||

HOS Thunderfoot | 200 | Supply | May 1999 | 1,750 | 4,000 | |||||

HOS Dakota | 200 | Supply | June 1999 | 1,750 | 4,000 |

| (1) | We have also bareboat chartered a newly constructed 165’ crewboat, which we named theHOS Hotshot.We have an option to purchase this vessel during the term of the charter. |

| (2) | The vessel was delivered from the shipyard on January 21, 2004 and, after further modifications, commenced service on March 3, 2004 as it was mobilized to Trinidad & Tobago. |

| (3) | The term “ROV” means remotely operated vehicle. |

We have designed and constructed five distinct classes of proprietary OSVs and added a sixth class, through the acquisitions of six OSVs from Candy Fleet, to meet the diverse needs of the offshore oil and gas industry. The following table provides a comparison of certain specifications and capabilities of our new generation OSVs to conventional 180’ OSVs.

5

Table of Contents

| Our Proprietary Design OSV Classes | Acquired OSVs | |||||||||||||

Conventional 180’ OSV(1) | 200 | 240 | 240 E | 240 ED | 265 | 220 | ||||||||

Size | ||||||||||||||

Class length overall (ft.) | 180 | 200 | 240 | 240 | 240 | 265 | 220 | |||||||

Breadth (ft.) | 40 | 54 | 54 | 54 | 54 | 60 | 46 | |||||||

Depth (ft.) | 14 | 18 | 18 | 18 | 20 | 22 | 17 | |||||||

Maximum draft (ft.) | 12 | 13 | 13 | 13 | 14.5 | 16 | 13.7 | |||||||

Deadweight (long tons) | 950 | 1,750 | 2,250 | 2,380 | 2,850 | 3,756 | 1,607 | |||||||

Clear deck area (sq. ft.) | 3,450 | 6,580 | 8,836 | 8,100 | 8,100 | 9,212 | 5,472 | |||||||

Capacity | ||||||||||||||

Fuel capacity (gallons) | 79,400 | 90,000 | 151,800 | 135,100 | 104,210 | 151,800 | 114,490 | |||||||

Fuel pumping rate (gallons per minute) | 275 | 550 | 550 | 550 | 550 | 500 | 380 | |||||||

Drill water capacity (gallons) | 120,000 | 240,000 | 240,000 | 240,000 | 311,000 | 413,000 | 99,000 | |||||||

Dry bulk capacity (cu. ft.) | 4,000 | 7,000 | 8,400 | 8,400 | 6,000 | 10,800 | 8,040 | |||||||

Liquid mud capacity (barrels) | 1,200 | 3,640 | 6,475 | 6,475 | 8,300 | 10,500 | 2,955 | |||||||

Liquid mud pumping rate (gallons per minute) | 250 | 500 | 1,000 | 1,000 | 1,000 | 1,000 | 1,200 | |||||||

Potable water capacity (gallons) | 11,500 | 52,200 | 52,200 | 52,200 | 30,400 | 20,430 | 26,800 | |||||||

Machinery | ||||||||||||||

Main engines (horsepower) | 2,250 | 4,000 | 4,000 | 4,000 | 4,000 | 6,700 | 3,900 | |||||||

Auxiliaries (number) | 2 | 3 | 3 | 3 | 3 | 3 | 2 | |||||||

Total rating (kw) | 200 | 750 | 750 | 750 | 750 | 860 | 250 | |||||||

Bow thruster (horsepower) | 325 | 800 | 1,600 | 1,600 | 1,600 | 2,400 | 530 | |||||||

Type of Pitch | Fixed | Controllable | Controllable | Controllable | Controllable | Controllable | Fixed | |||||||

Stern thruster (horsepower) | None | 300 | 300 | 800 | 800 | 1,600 | 300 | |||||||

Type of Pitch | — | Controllable | Controllable | Controllable | Controllable | Controllable | Fixed | |||||||

Fire fighting (gallons per minute) | None | 1,250 | 2,700 | 2,700 | 2,700 | 2,700 | 2,600 | |||||||

Dynamic positioning(2) | None | DP0,1 | DP1 | DP2 | DP2 | DP2,3 | DP0,1 | |||||||

Crew Requirements | ||||||||||||||

Number of personnel(3) | 5 | 6 | 6 | 7 | 7 | 8 | 6 | |||||||

| (1) | Statistics are for a typical 180’ class vessel. Actual specifications and capabilities may vary from vessel to vessel. |

| (2) | Dynamic positioning permits a vessel to maintain position without the use of anchors. The numbers “0,” “1,” “2” and “3” refer to increasing levels of technical sophistication and system redundancy features. |

| (3) | Regulatory manning requirements; depending on the services provided, operators may man vessels with more crew than required by regulations. |

The Tug and Tank Barge Industry

Introduction. The domestic tank barge industry provides marine transportation of crude oil, petroleum products and petrochemicals by tug and tank barge, and is a critical link in the U.S. petroleum distribution chain. Petroleum products are transported in the northeastern United States through a vast network of terminals, tankers and pipelines. We believe, based upon our analysis of the industry, that in the northeastern United States approximately 430 million barrels of petroleum products are transported annually by tank barges. Additionally, the EIA estimates that in Puerto Rico, our other core area of operation, approximately 70 million barrels of petroleum products are transported annually.

Demand for tug and tank barge services in the northeastern United States is primarily driven by population growth, the strength of the U.S. economy, seasonal weather patterns, oil prices and competition from alternate energy sources. According to the EIA, demand for petroleum products in the northeastern United States is expected to increase approximately 1.7% annually through 2010, which we believe will generate steadily increasing demand for the tank barge industry.

The largest single tank barge market in the northeastern United States is New York Harbor. Imported petroleum products are primarily delivered to New York Harbor as it has the capacity to receive products in cargo lots of 50,000 tons or more per tanker. By contrast, draft limitations in most New England ports and drawbridge limitations in Boston and Portland, Maine limit the average cargo carrying capacity of direct imports into many of the largest New England ports to about 30,000 tons per tanker. As a result, ships importing directly into New England must frequently discharge in multiple ports or terminals or transfer cargos to tank barges. As existing single-hulled tankers are retired due to age or as mandated under the Oil Pollution Act of 1990, or OPA 90, they are typically replaced by larger tankers. These larger-sized tankers are being built to facilitate the importation of crude oil and petroleum products into the United States. The volume of imported crude oil and petroleum products is expected to grow at a compound annual rate of 2.4% through 2025, according to the EIA. As larger petroleum tankers are being built, we believe that direct delivery into New York Harbor will

6

Table of Contents

generate increased tank barge demand for lightering services and further shipment to New England, the Hudson River and Long Island.

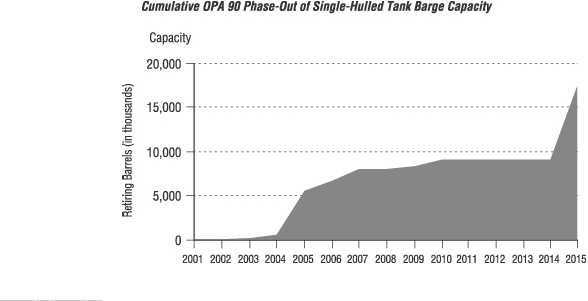

Oil Pollution Act of 1990. OPA 90 mandates that all single-hulled tank vessels operating in U.S. waters be removed from service according to a time schedule. Data provided by a U.S. Coast Guard report dated September 2001 indicates that 5.5 million barrels of single-hulled tank barge capacity would need to be retired by 2005 and an additional 3.5 million barrels by 2010, as mandated by OPA 90. According to the report, this represented on a cumulative basis as of each such retirement date, 22% and 36%, respectively, of the total 24.9 million barrel single- and double-hulled tank barge capacity that existed in 2001. The following chart illustrates the capacity of tank vessels that must be removed from service from 2000 through 2014. We believe that, absent a substantial increase in the number of double-hulled vessels constructed in the industry, this reduction in capacity, assuming steady demand, may favorably impact dayrates and utilization of the remaining tank barges, including our own.

Based on data contained in the United States Coast Guard Report to Congress on the Progress to Replace Single Hull Tank

Vessels with Double Hull Tank Vessels, dated September 2001.

Additionally, OPA 90 requires that owners or operators of tankers operating in U.S. waters submit vessel spill response plans to the U.S. Coast Guard for approval and operate according to the plans upon approval. Our vessel response plans have been approved by the U.S. Coast Guard, and all of our crew members have been trained to comply with these guidelines. For further discussion of OPA 90 see“—Environmental and Other Governmental Regulation”below.

Our Tug and Tank Barge Business

We provide marine transportation, distribution and logistics services in the northeastern United States, Puerto Rico and the U.S. Gulf of Mexico with our fleet of 12 ocean-going tugs and 16 ocean-going tank barges. We provide our services to major oil companies, refineries and oil traders. Generally, a tug and tank barge work together as a“tow”to transport refined or bunker grade petroleum products. Our tank barges carry petroleum products that are typically characterized as either“clean”or“dirty.”Clean products are primarily gasoline, home heating oil, diesel fuel and jet fuel. Dirty products are mainly crude oils, residual crudes and feedstocks, heavy fuel oils and asphalts. Our tugs and tank barges serve the northeastern U.S. coast, primarily New York Harbor, by transporting both clean and dirty petroleum products to and from refineries and distribution terminals.

Our tugs and tank barges also transport both clean and dirty petroleum products from refineries and distribution terminals in Puerto Rico to the Puerto Rico Electric Power Authority and to utilities located on other Caribbean islands. In

7

Table of Contents

addition, we provide ship lightering, bunkering and docking services in these markets and are well positioned to provide such services to the increasing number of new tankers that are too large to make direct deliveries to distribution terminals and refineries.

On May 31, 2001, we acquired nine ocean-going tugs and nine ocean-going tank barges from the Spentonbush/Red Star Group, composed of certain affiliates of Amerada Hess, as well as the business related to these tugs and tank barges, greatly expanding our capacity in the northeastern United States and increasing our market share of the coastwise trade on the U.S. upper east coast. As part of the acquisition, Amerada Hess entered into a long-term contract of affreightment with us pursuant to which Amerada Hess has committed to use us as its exclusive marine logistics provider and transporter of liquid petroleum products by tank barge in the northeastern United States. Under this contract, Amerada Hess has committed to ship a minimum of 45 million barrels annually for an initial period from June 1, 2001 through March 31, 2006 with options to renew for subsequent periods by mutual agreement. Also under the contract, we have the opportunity, on a reasonable commercial efforts basis, to coordinate the marine logistics for Amerada Hess in the southeastern United States, subject to Amerada Hess’s right to cancel within 30 days after December 31 of each year of the contract. The contract of affreightment will provide us with a significant source of revenues over the life of the contract. Our contract of affreightment allows Amerada Hess to reduce its minimum annual cargo volume commitment subject to significant adjustment penalties. Because the tank barge market in the northeastern United States is currently operating at or near capacity, we believe that we would be able to replace through other customers any volumes that Amerada Hess does not transport as contemplated by the contract.

One of our tank barges is double-hulled and is not subject to OPA 90 retirement dates. Ten of our 15 single-hulled tank barges are not required under OPA 90 to be retired or double-hulled until 2015. Of our remaining five single-hulled tank barges, three are required to be retired or modified before 2005 and two in 2009. In recognition of their upcoming retirements, we have recently commenced construction of two double-hulled, ocean-going tank barges that are expected to be delivered in December 2004 and we are evaluating plans for the construction or retrofit of a third tank barge. Our coastwise tanker is not subject to OPA 90 retirement dates. Based on the remaining lives of the majority of our tank barge fleet under OPA 90, we believe we are well positioned to obtain additional customers in the northeastern United States, as a large portion of currently available capacity in that market is required to be removed from service or be substantially reconstructed by 2005.

The following tables provide information, as of March 1, 2004, regarding the tugs, tank barges and the coastwise tanker we own and the two double-hulled tank barges currently under construction.

Ocean-Going Tugs

Name | Gross Tonnage | Length (feet) | Year Built | Brake Horsepower | ||||

Ponce Service | 190 | 107 | 1970 | 3,900 | ||||

Caribe Service | 194 | 111 | 1970 | 3,900 | ||||

Atlantic Service | 198 | 105 | 1978 | 3,900 | ||||

Brooklyn Service | 198 | 105 | 1975 | 3,900 | ||||

Gulf Service | 198 | 126 | 1979 | 3,900 | ||||

Tradewind Service | 183 | 105 | 1975 | 3,200 | ||||

Yabucoa Service | 183 | 105 | 1975 | 3,000 | ||||

Spartan Service | 126 | 102 | 1978 | 3,000 | ||||

Sea Service | 173 | 109 | 1975 | 2,820 | ||||

North Service | 187 | 100 | 1978 | 2,200 | ||||

Bayridge Service | 194 | 100 | 1981 | 2,000 | ||||

Stapleton Service | 146 | 78 | 1966 | 1,530 |

8

Table of Contents

Ocean-Going Tank Barges and Coastwise Tanker

Name | Barrel Capacity | Length (feet) | Year Built | OPA 90 Date(1) | ||||||

Ocean-Going Tank Barges: | ||||||||||

Energy 13501 | 135,000 | est. | 450 | TBD | (2) | N/A | ||||

Energy 11101 | 111,844 | 420 | 1979 | 2009 | ||||||

Energy 11102 | 111,844 | 420 | 1979 | 2009 | ||||||

Energy 11001 | 110,000 | est. | 390 | TBD | (2) | N/A | ||||

Energy 9801 | 97,432 | 390 | 1967 | 2005 | ||||||

Energy 9501 | 94,442 | 346 | 1972 | 2005 | ||||||

Energy 8701 | 86,454 | 360 | 1976 | 2005 | ||||||

Energy 8001(3) | 81,364 | 350 | 1996 | N/A | ||||||

Energy 7002 | 72,693 | 351 | 1971 | 2015 | ||||||

Energy 7001 | 72,016 | 300 | 1977 | 2015 | ||||||

Energy 6505 | 65,710 | 328 | 1978 | 2015 | ||||||

Energy 6504 | 66,333 | 305 | 1958 | 2015 | ||||||

Energy 6503 | 65,145 | 327 | 1988 | 2015 | ||||||

Energy 6502 | 64,317 | 300 | 1980 | 2015 | ||||||

Energy 6501 | 63,875 | 300 | 1974 | 2015 | ||||||

Energy 5501 | 57,848 | 341 | 1969 | 2015 | ||||||

Energy 2201 | 22,556 | 242 | 1973 | 2015 | ||||||

Energy 2202 | 22,457 | 242 | 1974 | 2015 | ||||||

Coastwise Tanker: | ||||||||||

Energy Service 9001(4) | — | 402 | 1992 | N/A |

| TBD: | To be determined. |

| N/A: | OPA 90 limitations are not applicable to this vessel. |

| (1) | Prior to January 1 of the year indicated (except for theEnergy 11101 for which the date is June 1), according to OPA 90, the vessel must be refurbished as a double hull or be retired from service in U.S. waters. For a discussion of OPA 90 see “—Environmental and Other Governmental Regulation” below. |

| (2) | Currently under construction with delivery anticipated in December 2004. |

| (3) | This vessel, formerly known as theT/B Kilchis, is a double-hulled tank barge that was acquired on February 28, 2003. Upon closing, we renamed this vessel theEnergy 8001. |

| (4) | This coastwise tanker, formerly known as theM/V W.K. McWilliams, Jr., acquired on November 15, 2001, is not currently certified to transport petroleum products and, therefore, barrel capacity is not applicable to this vessel. |

Technologically Advanced Fleet of New Generation OSVs. Our technologically advanced, new generation OSVs were designed with the specifications necessary for operations in complex and challenging drilling environments, including deepwater, deep well and other logistically demanding projects. Our new generation OSVs have significantly more capacity and operate more efficiently than conventional 180’ OSVs. While operators are especially concerned with a vessel’s ability to avoid collisions with multi-million dollar drilling rigs or production platforms during adverse weather conditions, they are hesitant to stop operations under such conditions due to the high daily cost of halting such complex operations. Our proprietary vessels incorporate sophisticated technologies and are designed specifically to operate safely in complex exploration and production environments. These technologies include dynamic positioning, roll reduction systems and controllable pitch thrusters, which allow our vessels to maintain position with minimal variance, and our unique cargo handling systems, which permit high volume transfer rates of liquid mud and dry bulk. We believe that we earn higher average dayrates and maintain higher utilization rates than our competitors due to the superior capabilities of our OSVs, our six-year track record of safe and reliable performance and the collaborative efforts of our in-house design team in providing marine engineering solutions to our customers.

Young OSV Fleet with Lower Cost of Ownership. We believe that we operate the youngest fleet of U.S.-flagged OSVs. While the average age of the conventional 180’ U.S.-flagged OSV fleet is approximately 24 years, the average age of our OSV fleet is approximately three years. Newer vessels generally experience less downtime and require significantly less maintenance and scheduled drydocking costs compared to older vessels. The average intermediate drydocking for

9

Table of Contents

recertification for one of our OSVs generally lasts five to ten days in the shipyard and costs approximately $0.3 million. In contrast, the typical drydocking for recertification of a conventional 180’ OSV may last up to 90 days in the shipyard and can cost as much as $1.5 million. We believe that our operation of new, technologically advanced OSVs gives us a competitive advantage in obtaining long-term contracts for our vessels and in attracting and retaining crews. Since we accepted delivery of our first OSV in November 1998, the average utilization rate for our OSVs has been approximately 94%. According to ODS-Petrodata, the U.S. Gulf of Mexico industry average was approximately 73% over the same time period, based on vessels available for service. We expect that our newer, larger, faster and more cost-efficient vessels will remain in high demand as deepwater and other complex and challenging exploration, development and production activities continue to increase globally.

Commitment to Safety and Quality. As part of our commitment to safety and quality, we have voluntarily pursued and received certifications that are not generally held by other companies in our industry. We have formerly maintained certifications to the requirements of the International Standards Organization, or ISO, Standards 9002 and 14000 for quality and environmental management, respectively, with respect to the eight tugs and nine tank barges acquired from the Spentonbush/Red Star Group. We are one of the few OSV companies operating in the U.S. Gulf of Mexico that is approved under the U.S. Coast Guard’s Streamlined Inspection Program in which we and the Coast Guard cooperate to develop training, inspection and compliance processes, with our personnel conducting periodic examinations of vessel systems to the requirements of the vessels’ Coast Guard certifications, and taking corrective actions where necessary. Both of our principal office locations in Covington, Louisiana and Brooklyn, New York, as well as the majority of our vessels, including all of our OSVs and our tugs and tank barges acquired from the Spentonbush/Red Star Group, are also certified under the International Safety Management Code, or ISM Code, developed by the International Maritime Organization to provide internationally recognized standards for the safe management and operation of ships and for pollution prevention. We are currently combining the ISO and ISM certification of our fleetwide operations to standards of the American Bureau of Shipping’s Safety, Quality and Environmental Certification, or ABS SQE, which integrates the elements of these certifications into a single program. Quality, Safety and Environmental Certificates are an increasingly important consideration for both our OSV and tank barge customers due to the environmental and regulatory sensitivity associated with offshore drilling and production activity and waterborne transportation of petroleum products, respectively. We believe that customers recognize our commitment to safety and that our strong reputation and performance history provide us with a competitive advantage.

Leading Market Presence in Core Target Markets. Our 23 OSVs comprise the second largest fleet of technologically advanced, new generation OSVs qualified for work in the U.S. Gulf of Mexico. Currently, 19 of our 23 OSVs operate in that area. We also operate one of the largest fleets of tugs and tank barges for the transportation of petroleum products in Puerto Rico and believe that we are the fourth largest tank barge transporter of petroleum products in New York Harbor. We believe that having scale in our selected markets benefits our customers and provides us with operating efficiencies.

Successful Track Record of Vessel Construction and Acquisitions. Our management has significant naval architecture, marine engineering and shipyard experience. We believe we are unique in the manner in which we design our own vessels and work closely with our contracted shipyards in their construction. We typically source and supply many of the manufactured components (owner-furnished equipment), comprising a large portion of the aggregate cost of a vessel, directly from vendors rather than through the shipyard. In addition to substantial cost savings, we believe our approach enables us to better control the construction process, resulting in a higher quality vessel and an enhanced level of service from these vendors during the applicable warranty periods. We believe that our history of designing and constructing 17 new generation OSVs on time and on budget provides us with a competitive advantage in obtaining contracts for our vessels prior to their actual delivery. Our company has designed its operations and management systems in contemplation of additional growth through new vessel construction and acquisitions. To date, we have successfully completed and integrated four acquisitions involving 13 ocean-going tugs and 13 ocean-going tank barges, one acquisition of a coastwise tanker and two acquisitions involving six 220’ new generation OSVs.

Favorable OPA 90 Fleet Status. Data provided by a U.S. Coast Guard report dated September 2001 indicates that 5.5 million barrels of single-hulled tank barge capacity would need to be retired by 2005 and an additional 3.5 million barrels by 2010, as mandated by OPA 90. According to the report, this represented on a cumulative basis as of each such retirement date, 22% and 36%, respectively, of the total 24.9 million barrel single- and double-hulled tank barge capacity that existed in 2001. Because 10 of our 15 single-hulled tank barges are not required to be replaced or retrofitted with double hulls until 2015, we believe we have a competitive advantage over operators who have a higher percentage of single-hulled tank barges that must be retired or modified to add double hulls before 2010.

10

Table of Contents

Experienced Management Team with Proven Track Record. Our executive management team has an average of 20 years of domestic and international marine transportation industry-related experience. We believe that our team has successfully demonstrated its ability to grow our fleet through new construction and strategic acquisitions and to secure profitable contracts for our vessels in both favorable and unfavorable market conditions. Moreover, our in-house engineering team has significant operating experience that enables us to more effectively design and manage our new vessel construction program, adapt our vessels for specialized purposes, oversee and manage the drydocking process and provide custom marine engineering solutions to our customers. We believe this will continue to result in a lower overall cost of ownership over the life of our vessels compared to our competitors, as well as a competitive advantage in securing contracts for our OSVs as the benefits of our proprietary designs and in-house engineering capabilities are recognized by our customers.

Apply Existing and Develop New Technologies to Meet our Customers’Vessel Needs. Our new generation OSVs are designed to meet the higher capacity and performance needs of our clients’increasingly more complex drilling and production programs. In addition, our proprietary double-hulled tank barges currently under construction are designed to maximize transit speed, improve cargo through-put rates and enhance crew safety features. Our new generation OSVs are equipped with sophisticated propulsion and cargo handling systems, dynamic positioning capabilities and have larger capacities than conventional 180’ OSVs. We are committed to applying existing and developing new technologies to maintain a technologically advanced fleet that will enable us to continue to provide a high level of customer service and meet the developing needs of our customers for OSVs and ocean-going tugs and tank barges, as well as other types of vessels that complement our two business segments. Improvements in exploration and production technologies have enabled operators to pursue larger scale, more complex drilling programs in remote locations and under more challenging operating conditions. We believe that the trend toward increasingly more complex projects will increase the demand for our technologically advanced fleet of new generation OSVs. Oil and natural gas exploration and development activity in these regions has increased recently as a result of several factors, including world-class exploration potential, improvements in exploration and production technologies for deepwater projects, and slowing or declining production from onshore and shallow water fields. We believe that deepwater regions worldwide and deep well drilling on the Continental Shelf will continue to be active areas for exploration and development in the foreseeable future, and that demand for our OSVs, which are uniquely equipped to serve the current and planned drilling programs in these markets, will continue to be strong.

Expand Fleet Through Newbuilds and Strategic Acquisitions. We plan to expand our fleet through construction of new vessels, including construction of new generation OSVs and double-hulled tank barges as market conditions warrant, retrofitting of certain vessels and through strategic acquisitions. Market demand for vessels, including demand for new generation OSVs in domestic and international markets, will be the main determinant of the level and timing of construction of additional vessels. We believe that acquisition opportunities are likely to arise as consolidation continues in our two industry segments. We intend to use our expertise and experience to evaluate and execute strategic acquisitions where the opportunity exists to expand our service offerings in our core markets and create or enhance long-term client relationships. To date, we have completed seven acquisitions involving 33 vessels and have constructed 17 proprietary vessels, with two more expected for delivery in December 2004.

Pursue Optimal Mix of Long-Term and Short-Term Contracts. We seek to balance our portfolio of customer contracts by entering into both long-term and short-term charters. Long-term charters, which contribute to higher utilization rates, provide us with more predictable cash flow. Most of our long-term charters contain annual dayrate escalation provisions. Short-term charters provide the opportunity to benefit from increasing dayrates in favorable market cycles. Currently, seven of our 23 OSVs operate under long-term charters, the initial terms of which range from one to five years. Our contract of affreightment with Amerada Hess for the services of tugs and tank barges in the northeastern United States has an initial term of June 1, 2001 through March 31, 2006. Our other tug and tank barge contracts typically have been renewed annually over the last several years.

Build Upon Existing Customer Relationships. We intend to build upon existing customer relationships by expanding the services we offer to those customers with diversified marine transportation needs. Many integrated oil and gas companies require OSVs to support their exploration and production activities and ocean-going tugs and tank barges to support their refining, trading and retail distribution activities. Moreover, many of our customers that conduct operations internationally have expressed interest in chartering our OSVs in such markets. For example, we are operating three OSVs in Trinidad &

11

Table of Contents

Tobago for a customer with whom we have a long-standing relationship in the U.S. Gulf of Mexico. Currently, four of our new generation OSVs are chartered for use in international markets. Our management team has significant international experience and will continue to evaluate such opportunities.

Optimize Tug and Tank Barge Operations. Due to OPA 90 phase-out requirements of single-hulled barges, the total barrel-carrying capacity of existing tank vessels transporting petroleum products domestically is projected to decline from its current level without a commensurate increase in newbuildings and retrofittings. In addition, the energy industry is increasingly outsourcing its marine transportation requirements and focusing on safety and reliability as a key determinant in awarding new business. We believe that these trends will improve the balance of supply and demand, and result in improved tank barge utilization and dayrates.

Major oil companies, large independent oil and gas exploration, development and production companies and large oil service companies constitute the majority of our customers for our OSV services, while refining, marketing and trading companies constitute the majority of our customers for our tug and tank barge services. The percentage of revenues attributable to a customer in any particular year depends on the level of oil and natural gas exploration, development and production activities undertaken or refined petroleum products or crude oil transported by a particular customer, the availability and suitability of our vessels for the customer’s projects or products and other factors, many of which are beyond our control. For the year ended December 31, 2003, Amerada Hess Corporation accounted for more than 10% of our total revenues. Under the terms of our contract of affreightment with Amerada Hess, we are required to meet certain performance criteria and, if we fail to meet such criteria, Amerada Hess would be entitled to terminate the contract. Our contract of affreightment provides for minimum annual cargo volumes to be transported and allows Amerada Hess to reduce its minimum commitment, subject to significant adjustment penalties. Because the tank barge market in the northeastern United States is currently operating at or near capacity, we believe that we would be able to replace through other customers any volumes that Amerada Hess does not transport as contemplated by the contract. For a discussion of significant customers in prior periods, see note 14 of the notes to our consolidated financial statements.

We enter into a variety of contract arrangements with our customers, including spot and time charters, contracts of affreightment and consecutive voyage contracts. Our contracts are obtained through competitive bidding or, with established customers, through negotiation.

Currently, seven of our 23 OSVs operate under long-term charters. Most of the contracts for our OSVs contain early termination options in favor of the customer; however some have substantial early termination penalties designed to discourage the customers from exercising such options. Similarly, 12 of our 16 tank barges provide services under long-term contracts with initial terms of one year or longer. Since we commenced operations, our OSVs have performed services for approximately 64 different customers, and our tugs and tank barges have performed services for approximately 252 different customers. Because of the variety and number of customers historically using the services of our fleet, and the approximate balance between supply and demand in both the OSV and tug and tank barge markets, we believe that the loss of any one customer would not have a material adverse effect on our business.

Because we have established a reputation for on-time delivery and reliability, charterers have contacted us in certain circumstances to construct vessels to meet their needs. In such circumstances, we have generally contracted these specially designed vessels for three to five years, with renewal options, before construction is completed. Although we will design vessels to meet the specific needs of a charterer, we ensure in our design that customization does not preclude efficient operation of these vessels for other customers, for other purposes or in other situations.

We operate in a highly competitive industry. Competition in the OSV and ocean-going tug and tank barge segments of the marine transportation industry primarily involves factors such as:

| • | quality and capability of the vessels; |

| • | ability to meet the customer’s schedule; |

12

Table of Contents

| • | safety record; |

| • | reputation; |

| • | price; and |

| • | experience. |

The terms of the Jones Act restrict the ability of vessels that are not built in the United States, registered under the laws of the United States and owned and managed by U.S. citizens to compete in the coastwise trade in the United States and Puerto Rico. See“—Environmental and Other Governmental Regulation”for a more detailed discussion of the Jones Act.

We do not anticipate significant competition in the near term from pipelines as an alternative method of petroleum product delivery in the northeastern United States or Puerto Rico. No pipelines are currently under construction that could provide significant competition to tank barges in the northeastern United States or Puerto Rico, nor are any new pipelines likely to be built in the near future due to cost constraints and logistical and environmental requirements.

We believe that approximately 84% of the new generation OSVs currently operating in the U.S. Gulf of Mexico are owned by privately-held companies. We believe we operate the second largest fleet of new generation OSVs in the U.S. Gulf of Mexico. In contrast, approximately 75% of the conventional 180’ OSVs operating on the Continental Shelf of the U.S. Gulf of Mexico are owned by publicly-traded companies. We operate one of the largest tank barge fleets in Puerto Rico and we believe that we are the fourth largest transporter by tank barge of petroleum products in New York Harbor. Most of our competitors in the tug and tank barge industry are privately held.

Although some of our principal competitors are larger and have greater financial resources and, with respect to OSVs, extensive international operations, we believe that our operating capabilities and reputation enable us to compete effectively with other fleets in the market areas in which we operate. In particular, we believe that the relatively young age and advanced features of our OSVs provide us with a competitive advantage. The ages of our OSVs range from one month to 76 months, while the average age of the industry’s conventional 180’ U.S.-flagged OSV fleet is approximately 24 years. Retirement of older vessels has already commenced and we believe that many more of these older vessels will be retired in the next few years. The young age of our fleet, together with the advanced capabilities of our vessels, position us to take advantage of the expanding deepwater, deep well and other logistically demanding exploration and production projects in the U.S. Gulf of Mexico and around the world. In addition, our new generation OSVs are also increasingly in demand by our customers for conventional drilling projects because of the ability of our OSVs to reduce overall offshore logistics costs for the customer through the vessels’ greater capacities and operating efficiencies.

Environmental and Other Governmental Regulation

Our operations are significantly affected by a variety of federal, state, local and international laws and regulations governing worker health and safety and the manning, construction and operation of vessels. Certain U.S. governmental agencies, including the U.S. Coast Guard, the National Transportation Safety Board, the U.S. Customs Service and the Maritime Administration of the U.S. Department of Transportation, have jurisdiction over our operations. In addition, private industry organizations such as the American Bureau of Shipping oversee aspects of our business. The Coast Guard and the National Transportation Safety Board establish safety criteria and are authorized to investigate vessel accidents and recommend improved safety standards.

The U.S. Coast Guard regulates and enforces various aspects of marine offshore vessel operations. Among these are classification, certification, routes, drydocking intervals, manning requirements, tonnage requirements and restrictions, hull and shafting requirements and vessel documentation. Coast Guard regulations require that each of our vessels be drydocked for inspection at least twice within a five-year period.

13

Table of Contents

Under Section 27 of the Merchant Marine Act of 1920, also known as the Jones Act, the privilege of transporting merchandise or passengers for hire in the coastwise trade in U.S. domestic waters is restricted to only those vessels that are owned and managed by U.S. citizens and are built in and registered under the laws of the United States. A corporation is not considered a U.S. citizen unless, among other things:

| • | the corporation is organized under the laws of the United States or of a state, territory or possession of the United States; |

| • | at least 75% of the ownership of voting interests with respect to its capital stock is held by U.S. citizens; |

| • | the corporation’s chief executive officer, president and chairman of the board are U.S. citizens; and |

| • | no more than a minority of the number of directors necessary to constitute a quorum for the transaction of business are non-U.S. citizens. |

We meet all of the foregoing requirements. If we should fail to comply with these requirements, our vessels would lose their eligibility to engage in coastwise trade within U.S. domestic waters. To facilitate compliance, our certificate of incorporation:

| • | limits ownership by non-U.S. citizens of any class of our capital stock (including our common stock) to 20%, so that foreign ownership will not exceed the 25% permitted; |

| • | permits withholding of dividends and suspension of voting rights with respect to any shares held by non-U.S. citizens that exceed 20% |

| • | permits a stock certification system with two types of certificates to aid tracking of ownership; |

| • | permits our board of directors to redeem any shares held by non-U.S. citizens that exceed 20%; and |

| • | permits our board of directors to make such determinations to ascertain ownership and implement such measures as reasonably may be necessary. |

Recently, the Jones Act restrictions have been challenged by interests seeking to facilitate foreign competition for coastwise trade. Historically, their efforts have been defeated by large margins when considered by the U.S. Congress. Industry associations and participants have actively responded to the latest challenges involving the nature, extent and availability of lease-finance alternatives permitted by a 1996 amendment of the Jones Act. Certain foreign interests have attempted to utilize those provisions to operate or propose operation in the U.S. coastwise trade. On February 4, 2004, the United States Coast Guard published a final rule further restricting the lease-finance provisions to prevent their misuse. In the final rule, the Coast Guard noted that Congress’s intent in adopting the 1996 amendment was to broaden the sources of capital for owners of U.S. vessels engaged in coastwise trade by creating new lease-finance options and not to undermine the basic principle of U.S. maritime law that vessels operated in domestic trades must be operated and controlled by U.S. citizens. The final rule grandfathers indefinitely any vessel that received a coastwise endorsement before February 4, 2004 or any vessel built under a construction contract entered into before that date in reliance on a letter ruling from the Coast Guard dated prior to that date. In addition to the final rule, the Coast Guard and the Maritime Administration, on February 4, 2004, published a joint notice of proposed rulemaking that included provisions addressing certain charter-back restrictions intended to further prevent misuse of the lease-finance provisions. Also, the Coast Guard is proposing to limit the grandfathering provisions of the Coast Guard’s final rule to three years instead of having them be indefinite. There can be no assurance that the proposed rulemaking will be adopted as proposed or that, even if adopted with favorable provisions, further efforts to interpret the Jones Act, including these rules, in a manner designed to circumvent the historical protections afforded to U.S. coastwise trade will not continue. Should foreign competition be permitted to enter the U.S. coastwise market, it could have an adverse effect on the U.S. OSV industry and on us.

Our operations are also subject to a variety of federal, state, local and international laws and regulations regarding the discharge of materials into the environment or otherwise relating to environmental protection. The requirements of these laws and regulations have become more complex and stringent in recent years and may, in certain circumstances, impose strict liability, rendering a company liable for environmental damages and remediation costs without regard to negligence or fault on the part of such party. Aside from possible liability for damages and costs including natural resource damages associated with releases of hazardous materials including oil into the environment, such laws and regulations may expose us to liability for the conditions caused by others or even acts of ours that were in compliance with all applicable laws and regulations at the time such acts were performed. Failure to comply with applicable laws and

14

Table of Contents

regulations may result in the imposition of administrative, civil and criminal penalties, revocation of permits, issuance of corrective action orders and suspension or termination of our operations. Moreover, it is possible that changes in the environmental laws, regulations or enforcement policies that impose additional or more restrictive requirements or claims for damages to persons, property, natural resources or the environment could result in substantial costs and liabilities to us. We believe that we are in substantial compliance with currently applicable environmental laws and regulations.

OPA 90 and regulations promulgated pursuant thereto impose a variety of regulations on “responsible parties” related to the prevention of oil spills and liability for damages resulting from such spills. A “responsible party” includes the owner or operator of an onshore facility, pipeline or vessel or the lessee or permittee of the area in which an offshore facility is located. OPA 90 assigns liability to each responsible party for oil removal costs and a variety of public and private damages. Under OPA 90, “tank vessels” of over 3,000 gross tons that carry oil or other hazardous materials in bulk as cargo, a term which includes our tank barges, are subject to liability limits of the greater of $1,200 per gross ton or $10 million. For any vessels, other than “tank vessels,” that are subject to OPA 90, the liability limits are the greater of $500,000 or $600 per gross ton. A party cannot take advantage of liability limits if the spill was caused by gross negligence or willful misconduct or resulted from violation of a federal safety, construction or operating regulation. If the party fails to report a spill or to cooperate fully in the cleanup, the liability limits likewise do not apply. Moreover, OPA 90 imposes on responsible parties the need for proof of financial responsibility to cover at least some costs in a potential spill. We have provided satisfactory evidence of financial responsibility to the U.S. Coast Guard for all of our vessels over 300 tons.

OPA 90 also imposes ongoing requirements on a responsible party, including preparedness and prevention of oil spills, preparation of an oil spill response plan and proof of financial responsibility (to cover at least some costs in a potential spill) for vessels in excess of 300 gross tons. We have engaged the National Response Corporation to serve as our independent contractor for purposes of providing stand-by oil spill response services in all geographical areas of our fleet operations. In addition, our Oil Spill Response Plan has been approved by the U.S. Coast Guard.

OPA 90 requires that all newly-built tank vessels used in the transport of petroleum products be built with double hulls and provides for a phase-out period for existing single hull vessels. Modifying existing vessels to provide for double hulls will be required of all tank barges and tankers in the industry by the year 2015. We are in a favorable position concerning this provision because a significant number of vessels in our fleet of tank barges measure less than 5,000 gross tons. Vessels of such tonnage may continue to operate without double hulls through the year 2015. Under existing legal requirements, therefore, we will be required to modify or replace only five of our tank barges before 2015. Although we are not aware of anything that would lead us to believe this current schedule will change, it remains possible that a change in the law affecting the requirement for double hulls or other aspects of our operations may occur that would require us to modify or replace our existing tank barge fleet earlier than currently anticipated.

The Clean Water Act imposes strict controls on the discharge of pollutants into the navigable waters of the United States. The Clean Water Act also provides for civil, criminal and administrative penalties for any unauthorized discharge of oil or other hazardous substances in reportable quantities and imposes substantial liability for the costs of removal and remediation of an unauthorized discharge. Many states have laws that are analogous to the Clean Water Act and also require remediation of accidental releases of petroleum in reportable quantities. Our OSVs routinely transport diesel fuel to offshore rigs and platforms and also carry diesel fuel for their own use. Our OSVs also transport bulk chemical materials used in drilling activities and liquid mud, which contain oil and oil by-products. In addition, our tank barges are specifically engaged to transport a variety of petroleum products. We maintain vessel response plans as required by the Clean Water Act to address potential oil and fuel spills.

The Comprehensive Environmental Response, Compensation, and Liability Act of 1980, also known as “CERCLA” or “Superfund,” and similar laws impose liability for releases of hazardous substances into the environment. CERCLA currently exempts crude oil from the definition of hazardous substances for purposes of the statute, but our operations may involve the use or handling of other materials that may be classified as hazardous substances. CERCLA assigns strict liability to each responsible party for all response and remediation costs, as well as natural resource damages and thus we could be held liable for releases of hazardous substances that resulted from operations by third parties not under our control or for releases associated with practices performed by us or others that were standard in the industry at the time.

15

Table of Contents

The Resource Conservation and Recovery Act regulates the generation, transportation, storage, treatment and disposal of onshore hazardous and non-hazardous wastes and requires states to develop programs to ensure the safe disposal of wastes. We generate non-hazardous wastes and small quantities of hazardous wastes in connection with routine operations. We believe that all of the wastes that we generate are handled in all material respects in compliance with the Resource Conservation and Recovery Act and analogous state statutes.

LEEVAC Marine, Inc., a predecessor entity to one of our current subsidiaries, was notified in March 1996 regarding the possibility of remediating on a voluntary basis certain waste pits at the SBA Shipyards site in Jennings, Louisiana. This site is not identified as a federal Superfund site. Subsequent to this initial notice, in December 2000, LEEVAC Marine was one of approximately 14 companies that formed a limited liability company, SSIC Remediation, LLC, to address this matter. LEEVAC Marine accrued a $100,000 liability at the time of our formation to cover this expense. Our subsidiary’s current percentage of liability for cleanup efforts within the SSIC Remediation group at this site is estimated at approximately 2.64%, and, to date, it has contributed approximately $34,000 towards this cleanup effort and an additional $17,000 to pay certain costs discussed below, thereby reducing the accrued liability with respect to this matter to $44,600. The $34,000 contribution represents our subsidiary’s current share of a $1.9 million voluntary cleanup plan submitted to the limited liability company’s members by an independent contractor who has agreed to clean up the site in a manner that will meet both state and federal standards. In June 1997, Cari Investment Company, the former parent of LEEVAC Marine, Inc., agreed to indemnify us for certain matters, including those discussed in this paragraph. The indemnity would also be applicable to all liabilities, obligations, damages and expenses related to the SBA Shipyard matter in excess of $100,000. Christian G. Vaccari, who served as our Chairman and Chief Executive Officer until February 2002 and is serving as one of our directors, is a minority shareholder and President, Chief Executive Officer and Chairman of the Board of Cari Investment Company. In July 2002, our subsidiary entered into a contractual agreement whereby it paid an additional $17,000 to SSIC Remediation, LLC in order to limit its exposure to certain future costs incurred by the independent contractor at the site. This limitation on payment of future monies relates primarily to certain legal and administrative costs of SSIC Remediation, LLC and does not bar future payment of monies for potential Superfund cleanup costs or for costs associated with any suits brought by third parties. In late 2002, SSIC Remediation, LLC commenced interim phase remedial activities at the SBA Shipyards site pursuant to a December 9, 2002 “Order and Agreement” that it entered into with EPA. These remedial efforts are on-going at this site.

In addition to laws and regulations affecting us directly, our operations are also influenced by laws, regulations and policies which affect our customers’drilling programs and the oil and natural gas industry as a whole.

The Outer Continental Shelf Lands Act gives the federal government broad discretion to regulate the release of offshore resources of oil and natural gas. Because our operations rely primarily on offshore oil and natural gas exploration, development and production, if the government were to exercise its authority under the Outer Continental Shelf Lands Act to restrict the availability of offshore oil and natural gas leases, such an action would have a material adverse effect on our financial condition and results of operations.

We currently have in place protection and indemnity insurance coverage that includes coverage for pollution incidents in navigable waters of the United States. Our OSVs have $5 million in primary insurance coverage for such offshore pollution incidents, with an additional $100 million in excess umbrella coverage. In addition, our tugs and tank barges have insurance coverage for oil spills with a coverage limit of $1 billion.