STANTEC INC. 2011 FINANCIAL REVIEW

One Team. Integrated Solutions.

STN.TSX.NYSE

AT STANTEC, OUR FOCUS IS ON SUCCESSFULLY IMPLEMENTING OUR BUSINESS STRATEGY TO CONSISTENTLY DELIVER RESULTS FOR OUR CLIENTS, EMPLOYEES, AND SHAREHOLDERS.

From across North America and internationally, we provide our clients integrated design and consulting services in architecture, engineering, interior design, landscape architecture, urban planning, surveying, environmental sciences, economics, project management, and many other disciplines.

In simple terms, the world of Stantec is the water we drink, the routes we travel, the buildings we visit, the industries in which we work, and the neighborhoods we call home.

TABLE OF CONTENTS

4 Stantec At A Glance

8 2011 Financial Summary and Highlights

10 Message to Shareholders

12 Board of Directors

14 Locations

IBC Shareholder Information

Management’s Discussion and Analysis

M-1 Caution Regarding

Forward-Looking Statements

M-3 Executive Summary

M-4 Core Business and Strategy

M-9 Key Performance Drivers

and Capabilities

M-13 Results

M-45 Outlook

M-48 Critical Accounting Estimates,

Developments, and Measures

M-61 Risk Factors

M-72 Controls and Procedures

M-73 Corporate Governance

M-74 Subsequent Event

Consolidated Financial Statements

F-1 Management Report

F-2 Independent Auditors’

Report of Registered Public

Accounting Firm

F-3 Independent Auditors’ Report

on Internal Control Over

Financial Reporting

F-4 Consolidated Statements of

Financial Position

F-5 Consolidated Statements

of Income

F-6 Consolidated Statements

of Comprehensive Income

F-7 Consolidated Statements

of Shareholders’ Equity

F-8 Consolidated Statements

of Cash Flows

F-9 Notes to the Consolidated

Financial Statements

STANTEC INC. 3

STANTEC AT A GLANCE

VISION

To become and remain a top 10 global design firm. Being top 10 means

Recognition for the quality of our work among the top 10 firms in our industry

Working on complex projects for top, long-term clients

Ability to attract and retain highly talented, innovative employees

10 TOP

MISSION

To be One Team providing integrated solutions to create shared value for our clients, employees, shareholders, and communities.

ONE TEAM

STRATEGY

To achieve our vision, we focus on

Positioning Stantec among the top-three service

providers in our geographic locations

Focusing on operational excellence

Providing expertise and value-added services to

our clients with a commitment to excellence in

project execution through an integrated quality

management system

Driving a client-focused culture through cross-selling

efforts and account management strategies

FOUNDATION CLIENTS PEOPLE

The successful implementation of our business strategy results in growth. The three key drivers of our strategic plan are our foundation, our clients, and our people. We create shareholder value through building on our foundation, attracting and retaining the best clients, and

focusing on our people. Based on our successes in those areas, we believe that we are well positioned to realize our vision of becoming and remaining a top 10 global design firm.

4 2011 STANTEC FINANCIAL REVIEW

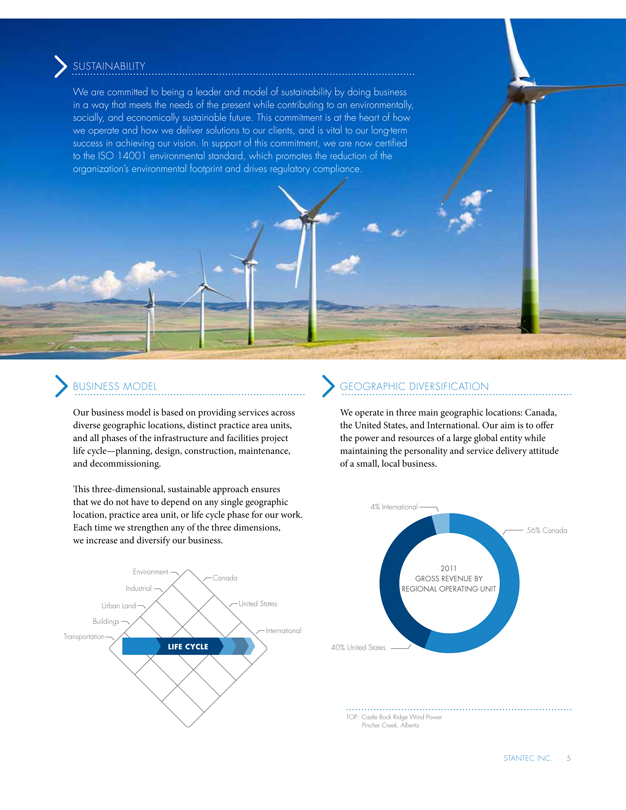

SUSTAINABILITY

We are committed to being a leader and model of sustainability by doing business in a way that meets the needs of the present while contributing to an environmentally, socially, and economically sustainable future. This commitment is at the heart of how we operate and how we deliver solutions to our clients, and is vital to our long-term success in achieving our vision. In support of this commitment, we are now certified to the ISO 14001 environmental standard, which promotes the reduction of the organization’s environmental footprint and drives regulatory compliance.

BUSINESS MODEL

Our business model is based on providing services across diverse geographic locations, distinct practice area units, and all phases of the infrastructure and facilities project life cycle-planning, design, construction management, maintenance, and decommissioning.

This three-dimensional, sustainable approach ensures that we do not have to depend on any single geographic location, practice area unit, or life cycle phase for our work. Each time we strengthen any of the three dimensions, we increase and diversify our business.

GEOGRAPHIC DIVERSIFICATION

We operate in three main geographic locations: Canada, the United States, and International. Our aim is to offer the power and resources of a large global entity while maintaining the personality and service delivery attitude of a small, local business.

Environment

Industrial

Urban Land

Buildings

Transportation

Canada

United States

International

LIFE CYCLE

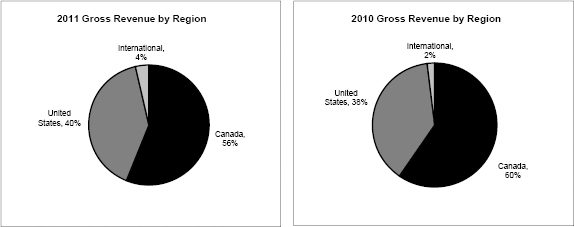

4% International

56% Canada

40% United States

2011 GROSS REVENUE BY

REGIONAL OPERATING UNIT

TOP: Castle Rock Ridge Wind Power

Pincher Creek, Alberta

STANTEC INC. 5

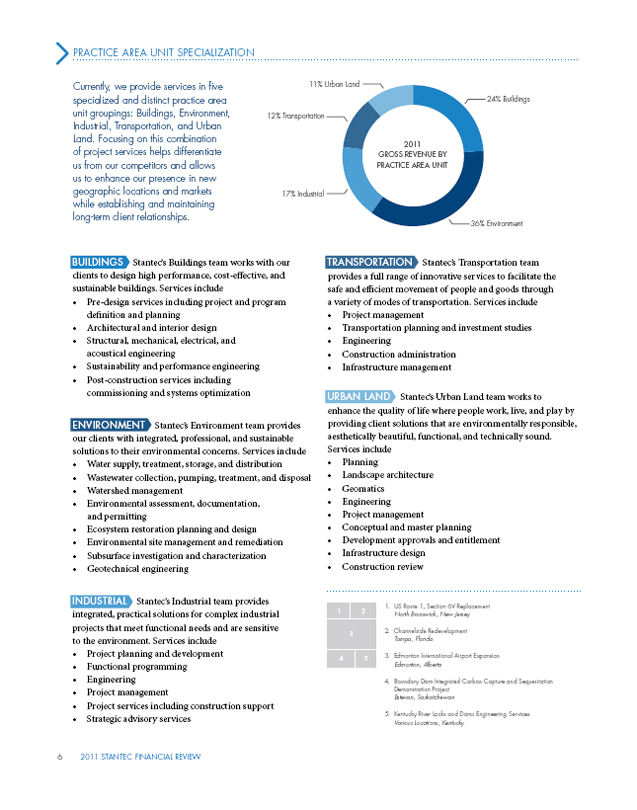

PRACTICE AREA UNIT SPECIALIZATION

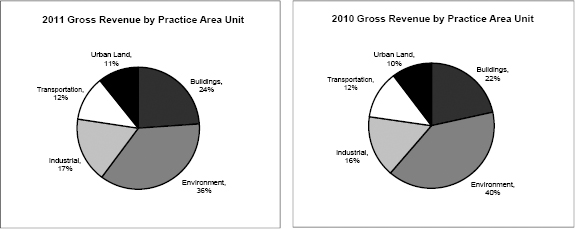

Currently, we provide services in five specialized and distinct practice area unit groupings: Buildings, Environment, Industrial, Transportation, and Urban Land. Focusing on this combination of project services helps differentiate us from our competitors and allows us to enhance our presence in new geographic locations and markets while establishing and maintaining long-term client relationships.

11% Urban Land

12% Transportation

17% Industrial

24% Buildings

36% Environment

2011 GROSS REVENUE BY PRACTICE AREA UNIT

BUILDINGS

Stantec’s Buildings team works with our clients to design high performance, cost-effective, and sustainable buildings. Services include

Pre-design services including project and program definition and planning

Architectural and interior design

Structural, mechanical, electrical, and acoustical engineering

Sustainability and performance engineering

Post-construction services including

commissioning and systems optimization

ENVIRONMENT

Stantec’s Environment team provides

our clients with integrated, professional, and sustainable

solutions to their environmental concerns. Services include

Water supply, treatment, storage, and distribution

Wastewater collection, pumping, treatment, and disposal

Watershed management

Environmental assessment, documentation,

and permitting

Ecosystem restoration planning and design

Environmental site management and remediation

Subsurface investigation and characterization

Geotechnical engineering

INDUSTRIAL Stantec’s Industrial team provides

integrated, practical solutions for complex industrial

projects that meet functional needs and are sensitive

to the environment. Services include

Project planning and development

Functional programming

Engineering

Project management

Project services including construction support

Strategic advisory services

TRANSPORTATION

Stantec’s Transportation team

provides a full range of innovative services to facilitate the

safe and efficient movement of people and goods through

a variety of modes of transportation. Services include

Project management

Transportation planning and investment studies

Engineering

Construction administration

Infrastructure management

URBAN LAND Stantec’s Urban Land team works to

enhance the quality of life where people work, live, and play by

providing client solutions that are environmentally responsible,

aesthetically beautiful, functional, and technically sound.

Services include

Planning

Landscape architecture

Geomatics

Engineering

Project management

Conceptual and master planning

Development approvals and entitlement

Infrastructure design

Construction review

1. US Route 1, Section 6V Replacement

North Brunswick, New Jersey

2. Channelside Redevelopment

Tampa, Florida

3. Edmonton International Airport Expansion

Edmonton, Alberta

4. Boundary Dam Integrated Carbon Capture and Sequestration

Demonstration Project

Estevan, Saskatchewan

5. Kentucky River Locks and Dams Engineering Services

Various Locations, Kentucky

2011 STANTEC FINANCIAL REVIEW

6

STANTEC INC. 7

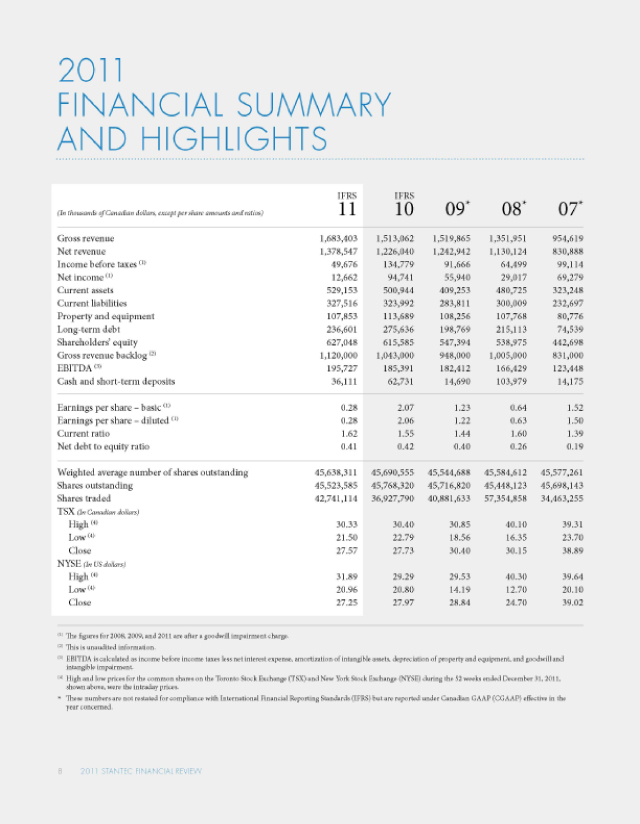

2011

FINANCIAL SUMMARY

AND HIGHLIGHTS

11IFRS 10IFRS 09* 08* 07*

(In thousands of Canadian dollars, except per share amounts and ratios)

Gross revenue 1,683,403 1,513,062 1,519,865 1,351,951 954,619

Net revenue 1,378,547 1,226,040 1,242,942 1,130,124 830,888

Income before taxes (1) 49,676 134,779 91,666 64,499 99,114

Net income (1) 12,662 94,741 55,940 29,017 69,279

Current assets 529,153 500,944 409,253 480,725 323,248

Current liabilities 327,516 323,992 283,811 300,009 232,697

Property and equipment 107,853 113,689 108,256 107,768 80,776

Long-term debt 236,601 275,636 198,769 215,113 74,539

Shareholders’ equity 627,048 615,585 547,394 538,975 442,698

Gross revenue backlog (2) 1,120,000 1,043,000 948,000 1,005,000 831,000

EBITDA (3) 195,727 185,391 182,412 166,429 123,448

Cash and short-term deposits 36,111 62,731 14,690 103,979 14,175

Earnings per share - basic (1) 0.28 2.07 1.23 0.64 1.52

Earnings per share - diluted (1) 0.28 2.06 1.22 0.63 1.50

Current ratio 1.62 1.55 1.44 1.60 1.39

Net debt to equity ratio 0.41 0.42 0.40 0.26 0.19

Weighted average number of shares outstanding 45,638,311 45,690,555 45,544,688 45,584,612 45,577,261

Shares outstanding 45,523,585 45,768,320 45,716,820 45,448,123 45,698,143

Shares traded 42,741,114 36,927,790 40,881,633 57,354,858 34,463,255

TSX (In Canadian dollars)

High (4) 30.33 30.40 30.85 40.10 39.31

Low (4) 21.50 22.79 18.56 16.35 23.70

Close 27.57 27.73 30.40 30.15 38.89

NYSE (In US dollars)

High (4) 31.89 29.29 29.53 40.30 39.64

Low (4) 20.96 20.80 14.19 12.70 20.10

Close 27.25 27.97 28.84 24.70 39.02

(1) The figures for 2008, 2009, and 2011 are after a goodwill impairment charge.

(2) is is unaudited information.

(3) EBITDA is calculated as income before income taxes less net interest expense, amortization of intangible assets, depreciation of property and equipment, and goodwill and intangible impairment.

(4) High and low prices for the common shares on the Toronto Stock Exchange (TSX) and New York Stock Exchange (NYSE) during the 52 weeks ended December 31, 2011, shown above, were the intraday prices.

* These numbers are not restated for compliance with International Financial Reporting Standards (IFRS) but are reported under Canadian GAAP (CGAAP) effective in the year concerned.

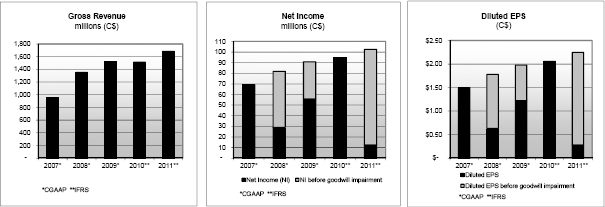

8 2011 STANTEC FINANCIAL REVIEW

GROSS REVENUE

07 08 09 10 11

$0 600 1,200 1,800

EBITDA

07 08 09 10 11

$0 50 100 150 200

NET INCOME

07 08 09 10 11

$0 40 80 120

Net Income Net Income before goodwill impairment

DILUTED EPS

07 08 09 10 11

$0 0.60 1.20 1.80 2.40

EPS-Diluted EPS-Diluted before goodwill impairment

GROSS REVENUE BACKLOG

07 08 09 10 11 $0 400 800 1,200

All charts represent millions of Canadian dollars, except for diluted EPS. 2011 and 2010 numbers are in compliance with IFRS. Prior years are not restated but are reported under CGAAP.

WHY INVEST IN STANTEC?

BECAUSE WE ARE FOCUSED ON DELIVERING RESULTS.

OUR GROSS REVENUE WAS

$1.7 BILLION

(2010 - $1.5 billion)

WE INCREASED EBITDA TO

$195.7 MILLION

(2010 - $185.4 million)

CASH FLOWS FROM OPERATING ACTIVITIES WERE

$114.6 MILLION

(2010 - $111.9 million)

STANTEC INC. 9

MESSAGE TO SHAREHOLDERS

The word that best characterizes Stantec as we move into 2012 is focus. Despite the ongoing challenges of the business environment, we have remained focused on our long-term strategy. We saw 2011 unfold in a way that renewed our commitment to our people, our clients, and our foundation. Through disciplined execution of our strategy, integrated project delivery to global/national and regional/local clients, and through the commitment and expertise of our people, we delivered solid results.

FOCUS ON PERFORMANCE. Once more, we ended the year with a strong balance sheet and an increase in operating cash flows, giving us the flexibility to continue to grow both organically and through acquisitions. At the same time, we achieved revenue growth, our EBITDA increased, and we saw our 58th year of uninterrupted profitability. Thanks to our financial strength and confidence in our ability to generate sustained cash flow, in February 2012, Stantec’s board of directors approved a dividend policy and concurrently declared our first quarterly dividend, payable on April 17, 2012 to shareholders of record on March 30, 2012. The declaration of this dividend reflects the confidence of our board of directors and management in our ability to generate ongoing cash flow from operations, continue to grow revenue, and complete strategic acquisitions while providing enhanced shareholder returns.

FOCUS ON TOP-TIER POSITIONING. We continued to enhance our local strength and expand the depth and breadth of our services in 2011 through the acquisition of five companies, each which have helped strengthen our position as a top-tier firm in our geographic locations. Collectively, these firms added approximately 725 staff to our One Team; strengthened our presence in the US Midwest and Southeast; and expanded our presence to all Canadian provinces and territories with new locations in Nunavut and Yukon. These acquisitions have also helped align our interest in emerging markets such as shale gas, as well as alternate project delivery models which continue to gain traction in the United States.

FOCUS ON OUR CLIENTS. In 2011 we evolved our organizational structure to reflect the sectors in which our clients do business, enabling us to match our expertise accordingly through effective cross-selling. For example, through multidisciplinary collaboration, we won a project to provide architecture; interior design; structural, mechanical, and electrical engineering; surveying; and site development services to assist retailer Target with the rollout of its stores into the Canadian marketplace. We continued to expand our account management program, helping us to strengthen our relationship with key global/national and regional/local clients by meeting more of their service needs. For example, we secured contracts for the Polaris pipeline expansions and Cold Lake pipeline system projects in Alberta with Inter Pipeline Fund. We also secured a long-term

Through disciplined execution of our strategy, integrated project delivery to global/national and regional/local clients, and through the commitment and expertise of our people, we delivered solid results.

10 2011 STANTEC FINANCIAL REVIEW

project with the US Department of Transportation to provide the Federal Highway Administration with technical services in the United States and Canada, established under the Strategic Highway Research Program.

FOCUS ON OPERATIONAL EXCELLENCE. Our core commitment to technical, project management, and client service excellence forms the foundation for the growth and diversity of our Company. Our formal integrated management system provides a disciplined and accountable framework for managing risks, quality outcomes, and regulatory compliance. This integrated management system has been implemented and registered to three internationally recognized ISO standards:

ISO 9001:2008 Quality Management Standard - aligns business processes with strategic objectives, provides a disciplined approach to managing risk, and promotes quality outcomes and management transparency

ISO 14001:2004 Environmental Management Standard - promotes the reduction of the organization’s environmental footprint and drives regulatory compliance

ISO/IEC 20000-1:2005 IT Service Management Standard - promotes the quality, consistency, reliability, and value of information technology services

Our integrated management system, in addition to our strong enterprise system, collectively help us to manage our operations effectively.

In 2011, and every year, we have our committed and hardworking employees to thank. By working together as One Team, they deliver high-quality, integrated, and well-managed projects to our clients and effectively manage our operations. Through their dedication, they help us to execute our long-term strategy and provide us with a reputation for excellence.

Our performance in 2011 was a testament to the strength of our business model, which enabled us to adjust our service delivery to meet the needs of our clients and those of a changing market. As we look to 2012, a year where we anticipate moderate economic recovery, we remain focused on the disciplined execution of our long-term strategy. We are confident that we are well positioned to continue to expand our business to meet our clients’ needs and to take advantage of market opportunities because of the agility of our business model.

In closing, we would like to thank our clients for entrusting us with their projects. The services we provide are essential to helping our clients improve the quality of life in communities across North America and around the world, and we are thankful to our clients for allowing us to work with them as One Team to achieve their project goals, which in turn contributes to our success.

On behalf of Stantec, thank you for your confidence in our strategic direction and for your continued support.

Bob Gomes, P.Eng.

President & CEO

STANTEC INC. 11

BOARD OF DIRECTORS

At Stantec we know the integrity of a company’s board of directors sets the tone for its operations, and we have in place a remarkable group of qualified, knowledgeable directors. All members of our board fulfill their roles guiding the management of the Company’s business and affairs while adhering to sound corporate governance practices in three major areas: stewardship, independence, and expertise.

1. ARAM H. KEITH

Chair of the Board of Directors, Stantec Inc., Irvine, California

2. ROBERT J. GOMES

President & CEO, Stantec Inc.

Edmonton, Alberta

3. DOUGLAS K. AMMERMAN

Director, Stantec Inc.

Laguna Beach, California

4. ROBERT J. BRADSHAW

Director, Stantec Inc.

Toronto, Ontario

5. DAVID L. EMERSON

Director, Stantec Inc.

Vancouver, British Columbia

6. DR. DELORES M. ETTER

Director, Stantec Inc.

Dallas, Texas

7. ANTHONY P. FRANCESCHINI

Director, Stantec Inc.

Edmonton, Alberta

8. SUSAN E. HARTMAN

Director, Stantec Inc.

Evergreen, Colorado

9. IVOR M. RUSTE

Director, Stantec Inc.

Calgary, Alberta

CORPORATE OFFICERS

ARAM H. KEITH

Chair of the Board of Directors

ROBERT J. GOMES

President & CEO

DANIEL J. LEFAIVRE

Senior Vice President & CFO

RICHARD K. ALLEN

Senior Vice President & COO

PAUL J.D. ALPERN

Vice President, Secretary & General Counsel

12. 2011 STANTEC FINANCIAL REVIEW

STANTEC INC. 13

LOCATIONS

CANADA

Calgary, Alberta Edmonton, Alberta Fort McMurray, Alberta Lethbridge, Alberta Medicine Hat, Alberta Red Deer, Alberta Abbotsford, British Columbia Burnaby, British Columbia Kamloops, British Columbia Kelowna, British Columbia Sidney, British Columbia Surrey, British Columbia Vancouver, British Columbia Victoria, British Columbia Winnipeg, Manitoba St. John’s, Newfoundland & Labrador Fredericton, New Brunswick Moncton, New Brunswick Saint John, New Brunswick Yellowknife, Northwest Territories Halifax, Nova Scotia Sydney, Nova Scotia Iqaluit, Nunavut Barrie, Ontario Burlington, Ontario Guelph, Ontario Hamilton, Ontario Kitchener, Ontario London, Ontario Markham, Ontario Mississauga, Ontario North Bay, Ontario Ottawa, Ontario Sudbury, Ontario Toronto, Ontario Windsor, Ontario Charlottetown, Prince Edward Island Montreal, Quebec

Regina, Saskatchewan Saskatoon, Saskatchewan Whitehorse, Yukon

UNITED STATES

Birmingham, Alabama Phoenix, Arizona Tempe, Arizona Tucson, Arizona Bakersfield, California Fresno, California Irvine, California Lafayette, California Long Beach, California Los Angeles, California Los Gatos, California Modesto, California Petaluma, California Redlands, California Rocklin, California Sacramento, California San Diego, California San Francisco, California San Luis Obispo, California Thousand Oaks, California Walnut Creek, California Boulder, Colorado Denver, Colorado Fort Collins, Colorado Washington, District of Columbia Hamden, Connecticut Hartford, Connecticut Fort Myers, Florida Jacksonville, Florida Naples, Florida Orlando, Florida Panama City, Florida Port Charlotte, Florida Sarasota, Florida Tallahassee, Florida Tampa, Florida Atlanta, Georgia Duluth, Georgia Macon, Georgia Chicago, Illinois Springfield, Illinois

Indianapolis, Indiana Waterloo, Iowa Lexington, Kentucky Louisville, Kentucky New Orleans, Louisiana West Monroe, Louisiana Scarborough, Maine Topsham, Maine Boston, Massachusetts Northampton, Massachusetts Westford, Massachusetts Ann Arbor, Michigan Detroit, Michigan Lansing, Michigan Rochester, Minnesota St. Cloud, Minnesota St. Paul, Minnesota White Bear Lake, Minnesota St. Louis, Missouri Las Vegas, Nevada Reno, Nevada Auburn, New Hampshire Mount Laurel, New Jersey Rochelle Park, New Jersey Toms River, New Jersey Albany, New York Binghamton, New York Buffalo, New York Elmira, New York Hauppauge, New York New York, New York Rochester, New York Charlotte, North Carolina Raleigh, North Carolina Winston-Salem, North Carolina Fargo, North Dakota Canton, Ohio Cincinnati, Ohio Cleveland, Ohio Columbus, Ohio Logan, Ohio Sylvania, Ohio

Toledo, Ohio Portland, Oregon Butler, Pennsylvania Philadelphia, Pennsylvania Pittsburgh, Pennsylvania Plymouth Meeting, Pennsylvania State College, Pennsylvania West Chester, Pennsylvania Charleston, South Carolina Nashville, Tennessee Arlington, Texas Dallas, Texas Houston, Texas Salt Lake City, Utah South Burlington, Vermont Leesburg, Virginia Redmond, Washington Seattle, Washington Buckhannon, West Virginia Charleston, West Virginia Green Bay, Wisconsin Madison, Wisconsin Milwaukee, Wisconsin Waupun, Wisconsin

INTERNATIONAL

St. Michael, Barbados London, England Ahmedabad, India Panama City, Panama Guaynabo, Puerto Rico

Abu Dhabi, United Arab Emirates Dubai, United Arab Emirates

14. 2011 STANTEC FINANCIAL REVIEW

STANTEC INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

and

CONSOLIDATED FINANCIAL STATEMENTS

For the Years Ended December 31, 2011, and 2010

MANAGEMENT’S DISCUSSION AND ANALYSIS

February 23, 2012

This discussion and analysis of Stantec Inc.’s operations, financial position, and cash flows for the year ended December 31, 2011, dated February 23, 2012, should be read in conjunction with the Company’s 2011 audited consolidated financial statements and related notes for the year ended December 31, 2011. Our 2011 audited consolidated financial statements are prepared in accordance with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB). The impact of the transition to IFRS on our reported financial position, financial performance, and cash flows, including the nature and effect of significant changes in accounting policies from those used in our consolidated financial statements for the year ended December 31, 2010, are described in the Critical Accounting Estimates, Developments, and Measures section (under the Transition to IFRS subheading) of this Management’s Discussion and Analysis and in note 38 of our December 31, 2011, audited consolidated financial statements. Unless otherwise indicated, comparative figures in this Management’s Discussion and Analysis have been restated to give effect to these changes.

Unless otherwise indicated, all amounts shown below are in Canadian dollars. Additional information regarding the Company, including our Annual Information Form, is available on SEDAR at www.sedar.com and on EDGAR at www.sec.gov. Such additional information is not incorporated by reference and should not be deemed to be made part of this Management’s Discussion and Analysis.

CAUTION REGARDING FORWARD-LOOKING STATEMENTS

Our public communications often include written or verbal forward-looking statements within the meaning of the US Private Securities Litigation Reform Act and Canadian securities laws. Forward-looking statements are disclosures regarding possible events, conditions, or results of operations that are based on assumptions about future economic conditions or courses of action and include future-oriented financial information.

Statements of this type are contained in this report, including the discussion of our goals in the Core Business and Strategy section and of our annual and long-term targets and expectations for our regions and practice areas in the Results and Outlook sections, and may be contained in filings with securities regulators or in other communications. Forward-looking statements may involve, but are not limited to, comments with respect to our objectives for 2012 and beyond, our strategies or future actions, our targets, our expectations for our financial condition or share price, or the results of or outlook for our operations.

We provide forward-looking information for our business in the Core Business and Strategy section as well as the Results (under the Results of Operations—Gross and Net Revenue, and Liquidity and Capital Resources subheadings) and Outlook sections of this report in order to describe the management expectations and targets by which we measure our success and to assist our shareholders in understanding our financial position as at and for the periods ended on the dates presented in this report. Readers are cautioned that this information may not be appropriate for other purposes.

By their nature, forward-looking statements require us to make assumptions and are subject to inherent risks and uncertainties. There is a significant risk that predictions, forecasts, conclusions, projections, and other forward-looking statements will not prove to be accurate. We caution readers of this report not to place undue reliance on our forward-looking statements since a number of factors could cause actual future results, conditions, actions, or events to differ materially from the targets, expectations, estimates, or intentions expressed in these forward-looking statements.

MANAGEMENT’S DISCUSSION AND ANALYSIS

December 31, 2011

STANTEC INC.

M-1

Future outcomes relating to forward-looking statements may be influenced by many factors, including, but not limited to, the following material and known risks, each of which is further described in the Risk Factors section of this report.

| • | Economic downturns could have a negative impact on our business since our clients may curtail investment in infrastructure projects or experience difficulty paying for services performed. |

| • | The professional consulting services industry is highly competitive, which could have a negative impact on our profit margins and market share. |

| • | The nature of our business exposes us to potential liability claims and contract disputes, which may reduce our profits. |

| • | We may be unsuccessful in our goal of growing our business organically, which could lead to a reduction in our market share. |

| • | Changing markets may offer opportunities to provide services through alternate models. Failure to respond to these market demands may result in lost revenues. |

| • | At any given time, a significant portion of our revenue may be derived from a specific geographic region, industry, or sector. Consequently, our business could suffer materially if there were a downturn in that geographic region, industry, or sector. |

| • | Interruption to our systems and network infrastructure could adversely impact our ability to operate. |

| • | We bear the risk of cost overruns in a significant number of our contracts. We may experience reduced profits or, in some cases, losses, under these contracts if costs increase above our estimates. |

| • | Uncertainties associated with an acquisition may cause a loss of employees. |

| • | We may experience difficulties in integrating an acquired entity’s business into our existing operations and so may not realize the anticipated benefits of the acquisition. |

| • | Our backlog is subject to unexpected adjustments and cancellations and is, therefore, an uncertain indicator of future earnings. |

| • | To attain our goal of increasing the size and profitability of our operations, we may pursue and invest in business opportunities outside North America. Unfamiliarity with markets and political environments may impair our ability to increase international revenues. |

| • | Goodwill and intangible assets acquired from our acquisitions represent substantial portions of our total assets. If external market factors such as adverse stock market conditions and a decline in our share price or if our acquired businesses do not perform as expected, we may be required to write down the value of our goodwill and intangible assets, which could have a material adverse effect on earnings. |

| • | One of our primary competitive advantages is our reputation. If our reputation is damaged due to client dissatisfaction, our ability to win additional business may be materially damaged. |

| • | Our employees may face environmental, health, and safety risks and hazards in the workplace resulting in injury or lost time. |

MANAGEMENT’S DISCUSSION AND ANALYSIS

December 31, 2011

STANTEC INC.

M-2

Assumptions

In determining our forward-looking statements, we consider material factors including assumptions about the performance of the Canadian and US economies in 2012 and its effect on our business. The assumptions we made in determining the outlook for each of our practice areas, our annual targets, and our outlook for 2012 are listed in the Outlook section of this report.

The preceding list of factors is not exhaustive. Investors and the public should carefully consider these factors, other uncertainties, and potential events, as well as the inherent uncertainty of forward-looking statements, when relying on these statements to make decisions with respect to our Company. The forward-looking statements contained herein represent our expectations as of February 23, 2012, and, accordingly, are subject to change after such date. Except as may be required by law, we do not undertake to update any forward-looking statement, whether written or verbal, that may be made from time to time. In the case of the ranges of expected performance for fiscal year 2012, it is our current practice to evaluate and, where we deem appropriate, provide updates. However, subject to legal requirements, we may change this practice at any time at our sole discretion.

EXECUTIVE SUMMARY

Core Business and Strategy

| • | Our Company provides professional consulting services in planning, engineering, architecture, interior design, landscape architecture, surveying, project management, environmental sciences, and project economics for infrastructure and facilities projects. |

| • | Our goal is to become and remain a top 10 global design firm, and we focus on providing professional services in the infrastructure and facilities market principally on a fee-for-service basis. |

Key Performance Drivers and Capabilities

| • | Our performance drivers are our foundation, our clients, and our people. Our performance depends on our ability to create shareholder value through building on our foundation—which includes our risk profile, delivery model, services, systems, and processes to support successful project delivery and operational effectiveness— attracting and retaining the best clients, and focusing on our people. |

Results

| • | Continued growth and profitability. Our gross revenue grew 11.3% in 2011 as compared to 2010, and we achieved a 5.3% increase in our EBITDA, which is our net income before interest expense, income taxes, depreciation, amortization, and goodwill and intangible impairment (the terms gross revenue and EBITDA are defined in the Definition of Non-IFRS and Additional IFRS Measures in the Critical Accounting Estimates, Developments, and Measures section of this report). Excluding the impact of a $90.0 million non-cash goodwill impairment charge, net income increased 8.4% to $102.7 million compared to $94.7 million in 2010, and our diluted earnings per share increased 9.2% to $2.25 as compared to $2.06 in 2010. |

| • | Ongoing ability to adapt to challenging economic conditions.We achieved these positive results in a challenging economic environment and competitive landscape. In 2011, we continued to show strong operational performance, demonstrating our ability to adapt our business model to changing markets. |

| • | Growth through acquisition. Acquisitions completed in 2010 and 2011 contributed $183.2 million to the increase in our gross revenue from 2010 to 2011. We completed five acquisitions in 2011. |

MANAGEMENT’S DISCUSSION AND ANALYSIS

December 31, 2011

STANTEC INC.

M-3

| • | Strong balance sheet and liquidity. Our balance sheet remains solid. In 2011, we generated strong cash flows from operations, which we used for operations and acquisition growth. In 2011, we extended the maturity of our $350 million revolving credit facility to August 31, 2015. At December 31, 2011, $259.5 million of our credit facility was available for future acquisitions, working capital needs, and general corporate purposes. To gain additional financial flexibility in 2011, we issued $70 million of 4.332% senior secured notes, due May 10, 2016, and $55 million of 4.757% senior secured notes, due May 10, 2018. |

| • | Dividend policy. Stantec’s board of directors approved a dividend policy on February 15, 2012, and concurrently declared its first quarterly dividend. This reflects our financial strength and confidence in our ability to generate ongoing cash flow from operations, continue to grow revenue, and complete strategic acquisitions while providing enhanced shareholder returns. |

Outlook

| • | We believe that our overall outlook for 2012 is a moderate increase in organic gross revenue, with a targeted 2.0 to 3.0% increase compared to 2011, particularly in geographic locations and practice area units where we are a top-tier service provider. The outlook for each practice area unit in 2012 ranges from stable for our Buildings practice area unit, to stable to moderate organic growth for our Environment, Urban Land, and Transportation practice area units, to moderate organic growth for our Industrial practice area unit. |

Risks

| • | Various risk factors could cause our actual results to differ materially from those projected in the Outlook section and other forward-looking statements in this report. The material, known risks are described in the Risk Factors section of this report. Although the difficult economic environment appears to be slowly improving, related pressures, such as increased competition, margin compressions, project delays, and fiscal rebalancing, are not expected to subside immediately. Pressures and uncertainties related to economic recovery, volatility in the Canadian/US exchange rate, and public infrastructure funding may adversely impact our outlook for 2012. |

CORE BUSINESS AND STRATEGY

Our Company provides professional consulting services in planning, engineering, architecture, interior design, landscape architecture, surveying, project management, environmental sciences, and project economics for infrastructure and facilities projects. By integrating our expertise in these areas across North America and in other international locations, we are able to work as One Team to provide our clients with a vast number of project solutions. This integrated approach enables us to execute our “Global Expertise. Local Strength.” operating philosophy by maintaining a world-class level of expertise, which we supply to our clients through the strength of our local offices.

We focus on providing professional consulting services in the infrastructure and facilities market, principally on a fee-for-service basis, while participating in various models of alternative project delivery. By focusing on a multidisciplinary service delivery, we also support clients throughout the project life cycle—from the initial conceptualization and financial feasibility study to project completion and beyond.

MANAGEMENT’S DISCUSSION AND ANALYSIS

December 31, 2011

STANTEC INC.

M-4

Our goal is to become and remain a top 10 global design firm. In 2009, we developed a new 10-year strategic plan for achieving our goal. From 2010 to 2020, we intend to continue to increase the depth and breadth of our services. We are confident that we can do so because we have built a solid foundation—made up of a robust business strategy, workforce, organizational structure, and systems—to take us into the future. We will remain focused on servicing the North American market while gradually increasing our geographic reach in other markets that are best suited and receptive to our services as these services evolve and mature. Currently, international work outside of North America accounts for 4% of our business. By 2020, we aim to generate up to 10% of our revenue from our international work. During the year, we revised this target from 20% to 10% in light of the current uncertain global economy and our short-term focus on strengthening our presence in the United States.

Our strategy involves balancing organic and acquisition growth. We will continue to focus on organic growth by expanding our existing business through concentrating on cross-selling existing services to our clients, whether global/national or regional/local. Our One Team approach helps us to provide these integrated services to our clients, which—in turn—results in organic growth.

Our strategy for achieving our vision is by:

| • | Positioning ourselves among the top-three service providers in the geographic locations in which we operate |

| • | Focusing on operational excellence |

| • | Providing expertise and value-added services to our clients with a commitment to excellence in project execution through integrated quality management systems |

| • | Driving a client-focused culture through cross-selling efforts and account management strategies |

| • | Mitigating risk by taking on little or no construction risk and through project diversification among many clients and geographic regions through the use of a focused, three-dimensional business model |

Our business model is a key element of our strategy since it allows us to manage risk while continuing to increase our revenue and earnings through geographic diversification and practice area unit specialization and by providing design solutions in all five phases of the infrastructure and facilities project life cycle (planning, design, construction, maintenance, and decommissioning). Because of the diversity of our model, we are generally able to adapt to changes in market conditions, such as the current challenging economy, by offsetting decreased demand for services in one practice area unit with increased demand for services in another practice area unit.

Through our One Team approach to our business and service delivery, under the rules of IFRS we have one reportable segment—Consulting Services—which is an aggregate of our operating segments. Our operating segments are based on our regional geographic areas, and our chief operating decision maker (chief executive officer) assesses our Company’s performance based on financial information available from these geographic areas. In addition, we have practice area units that provide strategic direction, mentoring, and technical support to our operations across our geographic regions.

The following discussion outlines the three main components of our business model.

Geographic Diversification

During the first half of 2010, we operated in four main geographic regions in North America—Canada East, Canada West, the US East, and the US West—and had a few small offices in the Caribbean with a project presence in several other international locations. In the last half of the year, we expanded our international presence through acquisitions, adding offices in the United Kingdom, the United Arab Emirates, and India. To reflect this growth, in the beginning of 2011, we reorganized our operations into three main geographic regions: Canada, the United States, and International.

MANAGEMENT’S DISCUSSION AND ANALYSIS

December 31, 2011

STANTEC INC.

M-5

Our goal in each of our geographic locations is to position ourselves among the top three service providers. We realize this goal in our existing locations primarily by adding services through organic growth and strategic hiring, which is supplemented by acquisitions. Conversely, we achieve our target in new locations principally by acquiring and integrating firms that complement our organization, which is, in turn, supplemented by strategic hiring and organic growth.

Practice Area Unit Specialization

Currently, we provide services in five specialized and distinct practice area unit groupings: Buildings, Environment, Industrial, Transportation, and Urban Land. Focusing on this combination of project services helps differentiate us from our competitors and allows us to enhance our presence in new geographic locations and markets while establishing and maintaining long-term client relationships. Our strategy for strengthening this element of our business model is to expand the depth of our expertise in our current practice areas—a subset of our practice area units—and to selectively add complementary new practice areas to our operations.

In 2011, in order to enhance our focus on clients, we evolved our model to include 14 sectors in which our clients do business to match our expertise accordingly. The 14 sectors are: Airports & Aviation, Bridges, Commercial, Education/Institutional, Healthcare, Industrial Buildings & Facilities, Mining, Oil & Gas, Power & Energy, Roadways, Science & Technology, Transit/Rail, Urban Development, and Water. Clients within these sectors can benefit from the multidisciplinary services provided by multiple practice area units, meaning that Stantec’s One Team can provide integrated solutions to clients in these sectors.

Buildings. We provide architectural and engineering design and consulting services through two practice areas—Architecture and Buildings Engineering—to both private and public sector clients for a wide range of building types and market sectors across North America and internationally. Our core services include project and program definition; facilities planning; architectural and interior design; and structural, mechanical, electrical and acoustical engineering for both new construction and existing buildings. We also offer services in performance engineering and building operating systems, including analyses of exterior envelope, air quality, lighting, and energy efficiencies. Over the past few years, our Buildings practice area unit has also established an industry-wide reputation for leadership in sustainable and integrated design.

Our long-term goal is to become one of the world’s leading practices in the design of the built environment, and to be positioned as a leading firm worldwide for our expertise in our chosen market sectors, while building and maintaining a foundation of local operations that have stature and critical mass in their respective local communities. We believe the needs of aging infrastructure in North America and in our international locations will provide the Buildings practice area unit with growth opportunities that are consistent with the overall growth targets for the Company as a whole. In the short term, the buildings industry in North America is experiencing volatility, increased competition, and uncertainty in funding for public and private sector projects. Nevertheless, over the past year we have secured projects in our principal focus areas of healthcare and educational facility planning and design. Our outlook for 2012 assumes our ability to take advantage of our expanded geographic presence to pursue North American and international opportunities, and we believe we are well positioned to secure Public-Private Partnership (P3) opportunities, which continue to emerge in Canada and appear poised to emerge in the United States.

Environment. We provide solutions for water supply and wastewater treatment for communities and industry; planning and permitting infrastructure projects; ecosystem restorations; and soil-structure interaction evaluations through our Water, Environmental Services, and Geotechnical practice areas. Approximately one third of Environment’s revenue is derived from water supply, treatment, storage, transmission, and distribution; wastewater collection, pumping, treatment, and disposal; and watershed management. We derive the remaining

MANAGEMENT’S DISCUSSION AND ANALYSIS

December 31, 2011

STANTEC INC.

M-6

revenue from the provision of environmental services such as environmental assessments, documentation, and permitting; ecosystem restoration planning and design; environmental site management and remediation; subsurface investigation and characterization; and geotechnical engineering services. Half of our environmental services are provided to clients in the oil and gas, power, and mining sectors as part of regulatory and permitting activities. The other half of our environmental services’ revenue is derived from a range of other development activities in the communities and clients we service.

In 2012 and over the next five years, we will focus on strengthening our Environment practice area unit by continuing to expand its profile and market share throughout North America, primarily to clients in the mining, power, and oil and gas sectors. By 2020, we expect to be a top-tier firm in the water and environmental services sectors in North America. In the oil and gas sector, we aim to be a leading global firm in the environmental review, permitting, and licensing markets and a top-tier provider of liability management services to top energy firms worldwide.

Industrial. We provide consulting and design services to private, public, and government clients through five practice areas: Industrial Buildings & Facilities, Mining, Oil & Gas, Power, and Program & Project Management. Our core services include planning, functional programming, all aspects of engineering project management, and operational and construction support. We also provide specialty services in strategic management consulting and in the management of multibillion-dollar client programs through our Program & Project Management practice area.

In 2011, we experienced substantial growth in Mining, especially in potash. We also experienced growth in Oil & Gas, especially in pipeline terminals and system-assisted gravity drainage, and in Industrial Buildings & Facilities, where large transport and equipment dealers, manufacturers, and servicing companies—both public and private—renewed or constructed facilities. Efforts in Power secured new projects in the area of clean coal, landfill gas combustion, and the evolving business of the Smart Grid.

Over the next five years, we expect to grow organically and to complete acquisitions that complement our existing services in order to become a top-tier service provider in North America and to generate a greater portion of our Industrial revenues internationally. Our goal for 2020 is to develop several of our sectors into top 10 service providers in North America and earn up to 10% of our industrial revenues through international work.

Transportation. We provide transportation consulting and design services, which include project management, planning, engineering, construction administration, and infrastructure management. More specifically, we prepare transportation master plans for communities; conduct transportation investment studies; plan and design airport, transit, rail, and highway facilities; provide administration and support services for the construction of specific projects; and provide ongoing management planning for the upkeep of transportation facilities. In addition, we provide specialized services such as simulation modeling, evaluate the effectiveness of alternative transportation demand and supply management techniques, prepare investment-grade revenue studies for funding transportation projects, provide public consultation and environmental assessment skills to build broad public support for infrastructure plans, and design and implement integrated infrastructure/asset management systems for all types of transportation infrastructure.

Over the next five years, we expect this practice area unit to move from a top 20 position to a top 10 position in North America through continued development of a strong local presence in growing urban areas, which will be supplemented by expertise in specialty skills that, along with a focus on exemplary levels of client service, differentiate us from other local firms offering similar skill sets. For 2020, our goal is to have a top-five Transit/Rail sector, viable Airports & Aviation and Bridges sectors, and a well-diversified Roadways sector that is capable of competing for the largest and most complex projects in most major urban areas across North America.

MANAGEMENT’S DISCUSSION AND ANALYSIS

December 31, 2011

STANTEC INC.

M-7

Public funding is a key element in the growth opportunities in 2012 and beyond for the Transportation practice area unit, and increases in those funds is limited by budget deficit reduction efforts in most jurisdictions. The P3 and other alternative project delivery models are strong in Canada and, despite limitations on public funding, we expect to see increased opportunities in the United States in the next five years. We will continue to monitor developments in alternate project delivery and other funding mechanisms and focus on those geographic areas and subsets of transportation where funding is the most robust.

Urban Land. We provide planning, landscape architecture, geomatics, engineering, and project management solutions—in greenfield, brownfield, and urban developments—principally for land development, municipal, institutional, real estate, and retail and commercial clients through two practice areas: Urban Development and Geomatics. Our core services include, or relate to, conceptual and master planning, development approvals and entitlement, infrastructure design, landscape architecture, construction review, and a wide variety of surveying and geomatics services to support the residential, commercial, and retail land development industries, municipalities, and major colleges and universities.

The Canadian housing market continued to be relatively buoyant in 2011 and our Canadian Urban Land practice area unit is generally performing well. The US housing market was relatively stable in 2011 compared to 2010, and we believe the anticipated economic recovery in the United States will be slow while the Canadian market will remain robust, although growing at a less accelerated pace. Over the next 5 to 10 years, we aim to be a North American leader in providing integrated planning and urban design services as well as geospatial services (geographic information systems, scanning, survey geodetics, and remote sensing).

Life Cycle Solutions

The third element of our business model is the provision of professional services in all five phases of the project life cycle—planning, design, construction, maintenance, and decommissioning. This inclusive approach enables us to deliver services during periods of strong new capital project activity (i.e., design and construction) as well as during periods of lower new capital project expenditures (i.e., maintenance and rehabilitation). Beginning with the planning and design stages, we provide conceptual and detailed design services, conduct feasibility studies, and prepare plans and specifications. During the construction phase, we generally act as the owners’ representative, providing project management, surveying, and resident engineering services. We focus principally on fee-for-service type work and generally do not act as the contractor or take on construction risk. Following project completion, during the maintenance phase, we provide ongoing professional services for maintenance and rehabilitation projects in areas such as facilities and infrastructure management, facilities operations, and performance engineering. Finally, in the decommissioning phase, we provide solutions, recommendations, and remediation strategies for taking facilities out of active service.

Going forward, our strategy is to continue to expand the scope of services we provide in the initial planning stages and during maintenance, enabling us to establish longer-term relationships with clients throughout the project life cycle. Our three-dimensional business model allows us to provide services to many clients and for many projects, ensuring that we do not rely on a few large projects for our revenue and that no single client or project accounts for more than 5% of our business.

MANAGEMENT’S DISCUSSION AND ANALYSIS

December 31, 2011

STANTEC INC.

M-8

KEY PERFORMANCE DRIVERS AND CAPABILITIES

The three key drivers of our strategic plan are our foundation, our clients, and our people. Our performance depends on our ability to create shareholder value through building on our foundation, attracting and retaining the best clients, and focusing on our people. Based on our successes in those areas, we believe that we are well positioned to realize our goal of becoming and remaining a top 10 global design firm.

Foundation

Our foundation includes our risk profile, delivery model, services, systems, and processes to support successful project delivery and operational effectiveness. Some of the ways our Company focuses on these components are through improved communication and engagement within our balanced leadership model; strengthening resources and support for the One Team model in order to promote a quality management culture that is committed to excellence in project execution; and providing outstanding client service while building a culture of cross-selling and fostering organic growth. Some of the important key elements to our foundation are described below.

Operational excellence

To create our shareholder value, we focus strongly on operational excellence, a core component of the Stantec operating model. An example of one of the ways operational excellence is being deployed is the project management framework, which focuses on improving project planning capabilities and tools, and providing a disciplined commitment to quality assurance and peer review requirements. Operational excellence is also structured around operational organization and support, which includes developing more cost-effective methods in which to contract and provide services to our clients, and reporting and compliance, which focuses on providing external stakeholders with information relevant and timely for their decision-making purposes and to comply with applicable regulations. With regard to effective project management and execution, in 2008 we achieved registration with the International Organization for Standardization’s (ISO) 9001:2000 quality management standard, and in 2010, we updated this certification to the ISO 9001:2008 standard. ISO 9001:2008 is a globally recognized set of requirements for establishing effective quality management systems.

Financing

Our success also depends on our continuing ability to finance our growth plan. Adequate financing gives us the flexibility to acquire firms that are appropriate to our vision and complement our business model. Since we became publicly traded on the Toronto Stock Exchange (TSX) in 1994, we have increased our gross revenue at a compound annual rate of 18.9%. To fund such growth, we require cash generated from both internal and external sources. Historically, we have completed acquisitions using mostly cash and notes, while at opportune times raising additional funds through equity issuances to replenish our cash reserves, pay down debt, or strengthen our balance sheet. However, we have not made an equity offering since 2005, but instead have funded our growth with cash generated from our operations. In 2010, as part of our long-term financing strategy, we filed a short-form shelf prospectus with regulatory authorities in Canada and the United States, which allows us to issue, from time to time, up to $300 million in common shares until June 2012. In 2011, we extended the maturity of our existing $350 million revolving credit facility to August 31, 2015. This facility also gives us access to an additional $75 million, subject to approval from our lenders. At December 31, 2011, $259.5 million of the facility was available to fund future activities. In addition, in 2011, we issued $70 million of 4.332% secured notes due May 10, 2016, and $55 million of 4.757% senior secured notes due May 10, 2018, which was used to repay existing debt.

Growth opportunities and integration

Our current markets give us many opportunities to build toward our goal of becoming and remaining a top 10 global design firm. We believe that such growth is necessary in order to enhance the depth of our expertise,

MANAGEMENT’S DISCUSSION AND ANALYSIS

December 31, 2011

STANTEC INC.

M-9

broaden our services, increase our shareholder value, provide more opportunities for our employees, and leverage our information technology systems. Our strategy combines organic growth with the acquisition of firms that believe in our vision and want to be part of our dynamic Company. We are confident that we can continue to take advantage of acquisition opportunities because we operate in an industry sector that includes more than 100,000 firms, most of which are small. According toEngineering News-Record’s2011 report on the top 500 design firms, the largest engineering and architecture companies headquartered in the United States—our principal competitors—generate about US$80 billion in annual fees, approximately 25% of which they earn internationally. Currently, we have approximately a 2% share of these top 500 design firms’ annual fees.

The integration of acquired firms begins immediately following the acquisition closing date and generally takes between six months and two years to complete. It involves the implementation of our Company-wide information technology and financial management systems as well as provision of support services from our corporate and regional offices. This approach allows new staff to focus on their primary responsibility of continuing to serve clients with minimal interruption while taking advantage of our systems and expertise.

Our acquisition and integration program is managed by a dedicated acquisition team that supports, or is responsible for, the tasks of identifying and valuing acquisition candidates, undertaking and coordinating due diligence, negotiating and closing transactions, and integrating employees and systems following an acquisition. This team is complemented and enhanced by other operational staff as appropriate. We measure our success in integrating acquired employees through a post-integration survey and use the survey results to improve future integration activities. In addition, we measure our growth success by monitoring our year-over-year increase in gross revenue that is due to organic and acquisition growth.

Market presence

Key to our success is achieving a certain level of market presence in the geographic locations we serve. Our target is to be among the top three service providers in each of our geographic locations and practice areas. With this level of market presence, we are less likely to be affected by downturns in regional economies. Top-three positioning also gives us increased opportunities to work for the best clients, obtain the best projects, and attract and retain the best employees in a region, which is important for building or maintaining the staff needed to generate consistent performance and to support regional company infrastructure.

Stantec has a clear strength in the Canadian market: currently, we are the second-largest consulting firm in Canada and enjoy top-tier positioning in a majority of our locations and practices. In addition to this market presence, we are now realizing on our growing position in the United States and have taken strong steps to better position ourselves as a national firm. This means that in the next five years, we anticipate tripling the size of our US operations, which will make us a top-tier design firm in North America.

Clients

Another performance driver is our ability to attract and retain top clients. For us, the best clients are those with whom we have long-term relationships and for whom we provide multiple services and complete large and innovative projects. Currently, a majority of our business comes through repeat clients, and our 10 largest clients account for about 10% of our revenue. Our focus is to expand the number of top clients we serve through an account management program designed to increase organic growth by building on relationships with existing clients, and to reflect a stronger balance between global/national and regional/local clients.

Types of clients

Attracting and retaining the best clients relies on providing bundled services over a long period of time. These clients have predictable, sustainable, and profitable revenue streams, and through cross-selling, these clients quickly see the value of not only our Company, but also our people. We believe one of the most powerful ways to

MANAGEMENT’S DISCUSSION AND ANALYSIS

December 31, 2011

STANTEC INC.

M-10

develop a unified culture is through design assignments for global/national clients that require collaboration and coordination across the Company. Some of our acquired firms have brought a client portfolio with them that is global/national in nature. These global/national clients, with programs extending throughout North America and beyond, position Stantec well in our efforts to reflect balance in our client base.

Account Management and Marketing & Business Development

Finding and retaining clients is a key component of our success, and to meet this goal, we develop targeted marketing and business development plans for our top clients. This activity is completed on a geographic and practice area unit basis to identify our top regional/local clients, and on a sector basis for our global/national clients. By strategically ensuring that a quality client base is being created through setting well-defined goals and related action plans, we are able to maintain a focus on both our regional/local and global/national clients. We also continue to expand our account management program to our top regional/local accounts and consider alternate funding strategies to cultivate growth of our global/national accounts.

Based on our success in these areas, we believe that we are well positioned to continue to be one of the principal providers of professional design and consulting services in our geographic regions.

People

Our most important performance driver is our people. Our success depends on having qualified people. To that end, we concentrate on enhancing our health, safety, and environment program (HSE) to best-in-class, improving employee retention, and aligning our internal communications strategy to improve the delivery of our strategic plan to employee and stakeholder audiences.

Employees

Employees create the project solutions we deliver to clients. Consequently, to achieve our goal of becoming and remaining a top 10 global design firm, we must increase our workforce through a combination of organic hiring and acquisitions. One way we measure our success in this area is by total staff numbers. In 2011, our employee numbers increased to approximately 11,100 from 10,700 in 2010. At December 31, 2011, our workforce was made up of about 6,400 professionals, 3,500 technical staff, and 1,200 support personnel.

To attract and retain qualified people, we offer opportunities to be part of “One Team,” working on challenging multidiscipline projects with some of the most talented people in our industry. We are continually strengthening and supporting our people-oriented culture. For example, during 2011, we continued to deliver face-to-face on-demand project management training sessions and invest in health and safety initiatives, such as education and training for supervisors in health and safety rights and responsibilities. In addition, we continued to roll out the leadership development program we launched in 2008 to leaders throughout our regions. Looking forward to 2012, we will continue to assess and develop our leaders at all levels, from our vice presidents to front-line supervisors.

As well, in 2011, revisions were made to our Career Development and Performance Review process to put a greater emphasis on career management, and we are now developing well-defined leadership, knowledge, and project management career streams to support entrepreneurship, innovation, and project execution. Each career path is distinct and requires different skill sets and knowledge that will allow our employees to take responsibility for managing their careers. Training, coaching, and mentoring will continue to be key components in focusing on building both today’s and tomorrow’s team.

We provide a comprehensive, competitive benefits program that attracts and retains the right talent to achieve our operating and strategic goals. We have created an award-winning wellness culture that provides tools and support to help employees and their families improve their health and well-being.

MANAGEMENT’S DISCUSSION AND ANALYSIS

December 31, 2011

STANTEC INC.

M-11

To measure our success in attracting and retaining staff, we use tools such as employee surveys, 360-degree feedback, and exit interviews. The results of these performance metrics help us develop programs and initiatives for improving and maintaining staff engagement. We also track turnover rates for our staff through our business information system.

Our diversified portfolio approach to business generally enables us to redeploy a portion of our workforce when faced with changes in local, regional, or national economies or practice area demand. Although there will always be some areas where it will be difficult to find appropriate staff during certain periods, as we increase in size we become better able to address these issues by using staff from other parts of the Company, either through temporary relocation or work sharing. We are continually improving our ability to work on projects from multiple locations through standardized practices and systems, project collaboration, and web-based technology.

Leadership

Our ability to align the activities of our senior managers with our short- and long-term financial and strategic goals is also an important driver for our success. To this end, in addition to fixed salaries, we provide, on a discretionary basis, short- and long-term compensation designed to reward our senior managers (including our chief financial and chief operating officers, regional operating unit leaders, and practice area unit leaders) for their individual and corporate contributions to meeting our objectives. The short-term compensation consists of an annual employee cash bonus. The total amount available in the annual employee bonus pool is calculated as a percentage of our annual pre-tax, pre-bonus net income, which we believe directly ties the interests of our bonus-eligible employees, including our senior managers, to our financial performance. In determining the awards each year, we balance the managers’ overall contributions to our profitability Company-wide with the performance of their individual business unit, an approach that, in our view, creates a sense of shared responsibility for achieving outstanding business results and meeting our clients’ needs. In 2011, we implemented a restricted share unit incentive plan for our senior vice presidents through which they are granted annually, as part of their bonus, an allotment of restricted share units that they receive after two years as cash equal to the units’ market value. The market value of the units is based on the market value of our shares. We believe that this plan, by its nature, further invests our senior vice presidents in our longer term share performance.

As part of long-term compensation for our key staff, we grant options through our employee share option plan. In 2011, we improved our share option plan by tying the amount of share options available to be granted in a year to key performance metrics such as growth in earnings per share and net pre-tax, pre-bonus net income as a percentage of net revenue. Key staff may be granted options to purchase shares as part of their total compensation, which further aligns their interests with those of our shareholders and encourages them to stay employed with us over the long term. In making the decision to award options to an individual, our chief executive officer (CEO) and senior management team consider the individual’s ability to contribute to our long-term success, along with other factors.

Similarly, our CEO’s compensation package, which is governed by the terms of his employment agreement, includes a base salary; an annual bonus calculated as a percentage of our pre-tax, pre-bonus income; and a prescribed allotment of deferred share units. We require our CEO, senior vice presidents, chief operating officer, and chief financial officer to own a minimum number of shares, representing a specific percentage of their base salary, in the Company. We believe that deferred share units and minimum ownership requirements provide the appropriate incentives for our CEO to achieve a minimum growth rate in our share price, thereby aligning executive compensation with the interests of shareholders.

MANAGEMENT’S DISCUSSION AND ANALYSIS

December 31, 2011

STANTEC INC.

M-12

Since the results of our operations are dependent on the abilities and efforts of the members of our senior management team and other key personnel, our Corporate Governance and Compensation Committee and senior managers regularly review our succession planning measures for management.

RESULTS

Fourth Quarter Results

Our revenue growth in Q4 11 was solid compared to Q4 10. Gross revenue increased 12.6% to $432.0 million from $383.7 million, and our EBITDA increased 9.6% to $46.8 million from $42.7 million. Excluding the impact of a $90.0 million non-cash goodwill impairment charge, our net income increased 4.3% to $24.3 million from $23.3 million and our diluted earnings per share increased 3.9% to $0.53 from $0.51 when comparing Q4 11 to Q4 10 as further explained below.

The following table summarizes our key operating results for Q4 11 on a percentage of net revenue basis and the percentage increase in the dollar amount of these results compared to the same period last year:

| Quarter Ended December 31 | % of Net Revenue | % Increase (Decrease)* | % Increase (Decrease)* without Goodwill Impairment | |||||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

| (In millions of Canadian dollars, except %) | 2011 | 2010 | 2011 | 2010 | 2011 vs. 2010 | 2011 vs. 2010 | ||||||||||||||||||

| ||||||||||||||||||||||||

Gross revenue** | 432.0 | 383.7 | 124.1% | 123.4% | 12.6% | 12.6% | ||||||||||||||||||

Net revenue** | 348.2 | 310.9 | 100.0% | 100.0% | 12.0% | 12.0% | ||||||||||||||||||

Direct payroll costs | 156.3 | 133.4 | 44.9% | 42.9% | 17.2% | 17.2% | ||||||||||||||||||

Gross margin ** | 191.9 | 177.5 | 55.1% | 57.1% | 8.1% | 8.1% | ||||||||||||||||||

Administrative and marketing expenses | 144.4 | 133.7 | 41.5% | 43.0% | 8.0% | 8.0% | ||||||||||||||||||

Depreciation of property and equipment | 7.4 | 7.1 | 2.1% | 2.3% | 4.2% | 4.2% | ||||||||||||||||||

Impairment of goodwill | 90.0 | - | 25.8% | 0.0% | n/m | n/m | ||||||||||||||||||

Amortization of intangible assets | 5.0 | 5.2 | 1.4% | 1.7% | (3.8% | ) | (3.8% | ) | ||||||||||||||||

Net interest expense | 2.2 | 2.3 | 0.6% | 0.7% | (4.3% | ) | (4.3% | ) | ||||||||||||||||

Other net finance expense | 0.7 | 0.6 | 0.3% | 0.2% | 16.7% | 16.7% | ||||||||||||||||||

Share of income from associates | (0.4 | ) | (0.4 | ) | (0.1% | ) | (0.1% | ) | 0.0% | 0.0% | ||||||||||||||

Foreign exchange loss | 0.4 | 0.4 | 0.1% | 0.1% | 0.0% | 0.0% | ||||||||||||||||||

Other expense | - | 0.5 | 0.0% | 0.2% | (100.0% | ) | (100.0% | ) | ||||||||||||||||

Income (loss) before income taxes | (57.8 | ) | 28.1 | (16.6% | ) | 9.0% | (305.7% | ) | 14.6% | |||||||||||||||

Income taxes | 7.9 | 4.8 | 2.3% | 1.5% | 64.6% | 64.6% | ||||||||||||||||||

Net (loss) income for the period | (65.7 | ) | 23.3 | (18.9% | ) | 7.5% | (382.0% | ) | 4.3% | |||||||||||||||

| ||||||||||||||||||||||||

| * | % increase (decrease) calculated based on the dollar change from the comparable period |

| ** | The terms gross and net revenue and gross margin are defined in the Definition of Additional IFRS Measures in the Critical Accounting Estimates, Developments, and Measures section of this report. |

n/m = not meaningful

| Gross Revenue | Q4 11 vs. Q4 10 | |||

| (In millions of Canadian dollars) | ||||

| ||||

Increase in gross revenue due to: | ||||

Acquisition growth | 38.4 | |||

Organic growth | 8.2 | |||

Impact of foreign exchange rates on revenue earned by foreign subsidiaries | 1.7 | |||

| ||||

Total net increase in gross revenue | 48.3 | |||

| ||||

MANAGEMENT’S DISCUSSION AND ANALYSIS

December 31, 2011

STANTEC INC.

M-13

As indicated in the tables above, during Q4 11, our gross revenue increased by $48.3 million, or 12.6%, to $432.0 million compared to $383.7 million for the same period in 2010. Approximately $38.4 million of this increase resulted from an increase in revenue from acquisitions completed in 2011 and 2010, $8.2 million resulted from organic growth, and $1.7 million was due to foreign exchange. The foreign exchange impact was due to the weakening of the Canadian dollar in Q4 11. During Q4 11, the average exchange rate for the Canadian dollar relative to the US dollar was US$0.98 compared to US$0.99 during Q4 10.

The following table summarizes the change in gross revenue by practice area unit in the fourth quarter of 2011 compared to the same period in 2010.

| Practice Area Unit Gross Revenue | Quarter Ended December 31 | |||||||||||||||||||||||

| (In millions of Canadian dollars) | 2011 | 2010 | Total Change | Change Due to Acquisitions | Change Due to Organic Growth | Change Due to Foreign Exchange | ||||||||||||||||||

| ||||||||||||||||||||||||

Buildings | 98.8 | 84.5 | 14.3 | 20.2 | (6.1 | ) | 0.2 | |||||||||||||||||

Environment | 156.7 | 150.2 | 6.5 | 1.2 | 4.5 | 0.8 | ||||||||||||||||||

Industrial | 78.2 | 63.0 | 15.2 | 7.8 | 7.0 | 0.4 | ||||||||||||||||||

Transportation | 48.4 | 47.3 | 1.1 | 1.8 | (1.0 | ) | 0.3 | |||||||||||||||||

Urban Land | 49.9 | 38.7 | 11.2 | 7.4 | 3.8 | - | ||||||||||||||||||

| ||||||||||||||||||||||||

Total Consulting Services | 432.0 | 383.7 | 48.3 | 38.4 | 8.2 | 1.7 | ||||||||||||||||||

| ||||||||||||||||||||||||

Note: Comparative figures have been restated due to a realignment of several practice components between our Buildings, Industrial, Transportation, and Urban Land practice area units.

Organic growth in Q4 11 was positive in all practice area units except for Buildings and a slight decline in Transportation. The Buildings decline was due to the softening markets in the United States, United Kingdom, and Dubai compared to the same period in 2010. The buildings industry experienced increased competition and reduced funding for private and public sector projects. Our organic growth in Q4 11 compared to Q4 10 was mainly due to growth in our Industrial practice area unit. Our Industrial practice had increased activity in the mining and oil and gas sectors, where we are experiencing growth in potash and where improved oil and gas prices are creating greater project opportunities.

Net income during Q4 11 was positively impacted by the increase in gross revenue and a reduction in our administrative and marketing expenses as a percentage of net revenue from 43.0% in Q4 10 to 41.5% in Q4 11. This decrease was primarily due to a decrease in administrative and marketing labor as a percentage of net revenue in Q4 11 compared to Q4 10. Staff time charged to marketing and administrative labor may fluctuate from quarter to quarter because it is influenced by the mix of projects in progress and being pursued during the period, as well as by acquisition integration activities. In Q4 10, we were in the process of integrating the eight acquisitions completed during the second half of 2010 compared to three in the second half of 2011. In the months following the completion of an acquisition, there is usually an increase in staff time charged to administration and marketing due to integration activities including the orientation of newly acquired staff. In addition, due to this increase in acquisition activity in the second half of 2010 compared to 2011, there were more restructuring costs expensed in Q4 10.