MANAGEMENT REPORT – January to September 2013

To our Stockholders

We present the Management Report and the Financial Statements of Itaú Unibanco Holding S.A. (Itaú Unibanco) and its subsidiaries for the period from January to September 2013, in accordance with the regulations established by the Brazilian Corporate Law, the National Monetary Council (CMN), the Central Bank of Brazil (BACEN), the Brazilian Securities and Exchange Commission (CVM), the Superintendency of Private Insurance (SUSEP), and the National Council of Private Insurance (CNSP).

The information included in this material is available in the Investor Relations’ website of Itaú Unibanco: www.itau-unibanco.com.br/ri > Financial Information > Financial Statements > BRGAAP > 2013. Our results may also be accessed on mobile devices and tablets, and through our application “Itaú RI” (APP).

| 1) | ECONOMIC ENVIRONMENT |

In the USA the improvement in the labor market has remained, in spite of the tax squeeze in progress: approximately 180 thousand jobs have been created per month since the beginning of the year. Europe recorded a 0.29% growth in the second quarter of 2013, after six quarters of recession. In spite of the improvement in the developed countries, emerging countries still slow down, even though China has started to record signs of stabilization in the pace of its economy.

In its September meeting, the FED, the US central bank, decided to maintain its monetary incentives. This decision has brought liquidity relief for the emerging markets.

In the domestic scenario, even though the economy posted a good performance in the second quarter, the economic fundamentals point towards a GDP growth between 2.0% and 2.5% in 2013, lower than expected in the beginning of the year.

After the US dollar was traded at a level higher than 2.40 R$/US$ in mid-August, the Real appreciated at the end of the quarter as a result of interventions by BACEN and the FED’s decision to postpone the reduction in incentives, and it is now traded close to the 2.20 R$/US$.

Inflation measured by IPCA fell, but continues to be under pressure. The impact of a more depreciated Real over prices should make up for the decrease in the food inflation and the IPCA should close at about 6% in 2013.

In view of the inflationary pressures, BACEN started a cycle of increases in the Selic rate, which in the beginning of October reached 9.50%.

| 2) | HIGHLIGHTS |

| 2.1) | Corporate Events/Partnerships |

Repurchase of shares –in the third quarter of 2013, we acquired over 14.5 million preferred shares of own issue in the total amount of R$ 406.3 million at the average price of R$ 28.02 per share. In the year-to-date, we acquired 23.5 million preferred shares of own issue at the average price of R$ 28.18. On a voluntary basis and aiming at having transparency with the capital market agents, we monthly disclose the volumes traded and prices practiced in such trading. To obtain further information, please access www.itau-unibanco.com.br/ri > Corporate Governance > Acquisition of Own Shares.

Itaú Unibanco and Fiat Agreement – on August 20 we renewed, for another 10 years, the commercial cooperation agreement we have with Fiat car maker, the leader in sales of vehicles in the Brazilian market. This agreement sets forth the exclusive financing offer in promotional campaigns held by Fiat in connection with the sale of new automobiles and the exclusive use of the Fiat brand in vehicle-financing related activities.

Tax Assessment Notice issued by the Federal Reserve Service of Brazil (RFB) – in August we reported to the market that the RFB had issued a tax assessment notice in the approximate amount of R$ 18 billion related to the Itaú and Unibanco corporate association operation.

RFB disagrees with the type of business organization adopted to unify Itaú’s and Unibanco’s operations. However, the operation format suggested by RFB fails to be supported by the standards applicable to financial institutions in Brazil. Accordingly, we have challenged said tax assessment notice, by claiming that the operations carried out were adequate and that RFB's understanding that there was undue tax gain was flawed. We consider remote the risk of a loss associated to said tax procedure, and this understanding is supported by our lawyers and external advisors.

We reinforce that the operations carried out in 2008 were legitimate, and approved by the management bodies of the involved companies and respective stockholders and subsequently by the applicable authorities, that is, CVM, BACEN and the Administrative Council for Economic Defense (CADE).

| 2.2) | Approval by Regulatory Bodies |

The following were approved in the third quarter of 2013:

| § | IRB – Brasil Resseguros S.A. Stockholders’ Agreement, by SUSEP, in connection with the privatization process; |

| § | Agreement with Banco Citibank S.A. for purchase of Credicard and Citifinancial, by CADE (pending approval by BACEN). |

| 2.3) | Technology |

The civil works of our new data center, under construction in the interior of São Paulo (SP), is progressing as planned and it should be completed in the first quarter of 2014. This new data center will be one of the largest technology centers in the world, with capacity to support the bank’s expanded operations in the coming decades, keeping our commitment to ensure the availability of financial services and always searching for the continuous improvement of quality, agility and satisfaction of our clients.

Our functionalities were made available in our digital channels, with investments dedicated to the improvement and designing of new tools to serve the increasing expansion of these channels, such as internet banking and mobile banking, thus providing quality operations on an expeditious, modern and secure basis. They include:

Biometrics– we made available more advantages for registered clients. Besides withdrawal operations, clients are now able to check current account balances and statements without using a card and password. Biometrics enable carrying out operations with just a fingerprint identification, without the need for typing a password, providing more security and convenience to our clients. To use biometrics, it is enough to register with any Itaú branch.

Itaú Conta Certa (Itaú right account) – in August we launched this new type of current account for Itaú corporate customers, which permits the customization of service packages by choosing the number of deposit slips, credit order documents (DOC), available electronic transfer (TED), and custody of checks, among other, in accordance with their needs. The clients themselves choose, simulate and contract them at any moment, however and whenever they need them, always on the internet.

| 2.4) | Launch |

| Redecard is now Rede – we have built a new brand, a new positioning and a new business strategy. Rede, a plainer and more direct name – meaning network – summarizes the company’s key attributes, evoking technology, agility and modernity, in addition to creating a young and connected personality. The company’s focus was reviewed, and we will continue serving the merchant, but we are also concerned with the end clients and therefore we will make a closer, quicker and more technology-based service available through digital and mobile media. |  |

Accomplishing the purpose of being the main partner of sellers of goods and services that seek to expand their business potential, Rede offers its customers a series of products that follow the latest market trends. These include: Mobile Rede (transaction capture through a device coupled to a smartphone or tablet for card reading, or by entering purchase data and customer's signature) and e-Rede (in only one platform, a quick, efficient, fast and complete solution for online payments using a strong anti-fraud security system).

Approximately 300 people will reinforce the commercial team to support this operation. In the last two years, approximately R$ 500 million were invested in the update and standardization of 75% of all readers (of which 50% are wireless readers – POS). By the end of the first half, there were over 1 million merchants affiliated with Rede and over 1.7 million terminals, spread across 89% of Brazilian cities. Its total transactions exceeded 1.6 billion.

New Hiper Brand– we disclosed the launch of our new credit card brand available for all Brazilian consumers, Hiper, accepted in over one million establishments accredited by Rede throughout the Brazilian territory. Hiper is an evolution from Hipercard, the largest Brazilian card brand, and arrives to serve consumers searching for a product with immediate benefits. The first issuer of this brand will be Itaucard, for both the bank’s account holders and non-account holders. Among the benefits, we highlight the following:

(i) conversion of 120% of the annuity amount into bonus for mobile phone, applicable to all telephony operators working with such bonus system;

(ii) cards with the Itaucard 2.0 concept.

ETF in Chile – in September we launched the first ETF (Exchange Traded Fund) in Chile, namedIt Now IPSA, which replicates the profitability of the most significant 40 shares in the Chilean market. ETF is an investment fund traded on stock exchanges that may be purchased or sold at any moment, like any other company's share. Last year we achieved the right to the exclusive use of the IPSA, IGPA and Inter-10 trademarks for a ten-year period, thus permitting the creation, trading and dealing ETFs of the main indices of the Santiago Stock Exchange.

| 2.5) | Awards and Recognition |

The best of Dinheiro 2013 (as Melhores da Dinheiro 2013) – promoted by Isto É Dinheiro magazine, this ranking awards the best companies of the year by using management criteria, this is: financial sustainability, human resources, innovation and quality, social and environmental responsibility and corporate governance. We also won the banking sector ranking for the seventh time.

Época NEGÓCIOS 360º– organized by Época magazine, this guide is organized in partnership with Dom Cabral Foundation, which carries out a thorough assessment of the largest Brazilian companies by considering as criteria: financial performance, corporate governance, human resources practices, innovation, vision of future and social and environmental responsibility. Once again, we achieved the first place in the bank sector in this guide, which is already in its second edition.

The 1,000 Best Investment Funds of 2013 (1000 Melhores Fundos de Investimento 2013) – promoted by the Exame Guide of Personal Investments, in a survey conducted by the Center of Finance Studies of FGV (GVCef-FGV), we were elected the Best Manager of the Year. This award which highlighted the best managers for retail, high-end clients, companies and institutional investors. Among 1,000 open-end funds analyzed, we were also elected in the Best Manager categories:

| § | Funds in which investors invest between R$ 50,000 and R$ 250,000 (selective retail); |

| § | Interbank rate (DI) and short-term funds; |

| § | Indexed equity funds; and |

| § | Multimarket investment funds. |

Latin American Executive Team 2013 – organized by the Institutional Investor Magazine, thisranking is achieved based on a survey conducted with over 800 managers of investment and pension funds (buy side analysts), brokers and investment banks (sell side analysts) operating in Latin America. It was disclosed on August 20, when we were the winners in six out of the eight ranking categories: Best Investor Relations by the Sell and Buy Sides; the BestCEO by the Sell and Buy Sides; the Best Bank CFO by the Buy Side and the Best Investor Relations Professional by the Buy Side.

Latin America Research Team 2013 – for the first time Itaú BBA was ranked as the number one Research team of Latin America.

Best Cash Management Bank in Brazil – we were recognized for the sixth consecutive year by Euromoney magazine, one of the most important financial market publications.

| 3) | OPERATIONS |

Commercial Banking - Retail

We offer a wide range of banking products and services to a diversified base of individuals and companies, the bank’s account holders and non-account holders. We have over 40 million clients and 32.9 thousand points of service throughout Brazil and abroad, by means of 4.1 thousand branches, 870 service centers (PABs) and over 27.9 thousand ATMs. In addition, we also provide, throughItaú 30 horas, a means of accessing and checking accounts, making payments, investments and other banking transactions, with no need to turn to a manager. Our products portfolio includes loans and a number of investment, insurance, foreign exchange and brokerage options, among others.

In the retail segment, we provide five Itaú Uniclass exclusive services, with dedicated managers, investment advisory services, exclusive cashiers, managerial telephone service and higher credit limits. We offer expert services to our high-end clients by means of Itaú Personnalité and, with over 20 years of experience in wealth management, we provide Itaú Private Bank, the largest private bank in Latin America. To meet the needs of our corporate clients, we provide Itaú Empresas. In which the very small, small and medium-market companies are served through a dedicated structure, with specific products and services.

Wholesale and Investment Banking

Our banking operations in the corporate banking segment are carried out by Itaú BBA, which operates with a multidisciplinary team, with agility to carry out operations that are traditional for a commercial bank and transactions in capital markets, mergers and acquisitions, offering full services to over 3 thousand of the largest business groups of Brazil, Argentina, Chile, Colombia and Peru. It also serves approximately 700 institutional investors, ensuring full coverage for the head offices of international clients through the Europe, New York and Shangai units.

In October we included another 20 thousand clients to the Wholesale Banking. These companies, with yearly revenues over R$ 30 million and which were previously served by our Retail sector, may now count on a more specialized structure, thus achieving a customized service. By means of this structure, we offer the same products and services available for the Corporate segment, including those provided by the Investment Banking for strategic mergers and acquisitions or companies going public.

Insurance

Our insurance business basically operates in the lines of life and accident, extended warranty and property damages for individuals and corporate solutions for legal entities. Focused on streamlining the portfolio of products and the efficiency in the engaging processes, our insurance policies are sold, among other channels, in our branches, via telemarketing, internet, ATMs, self-service terminals, local independent brokers and multinational brokers.

We hold 30% of capital of the Porto Seguro Group, the insurance company leading the residence and automobile insurance segment in Brazil. We have an operating agreement with the Porto Seguro Group to offer and distribute, on an exclusive basis, residence and automobile insurance products to clients in our network in Brazil and Uruguay.

External Units

We are present in 19 countries other than Brazil, in commercial banking and institutional client operations, and investment, corporate and private banking activities. Seven of these countries are in South America, which is our priority in terms of international expansion. Our operations also comprise North America, Central America, Europe, Asia and Middle East. In the period from January to September, our business abroad reached a recurring net income of approximately R$ 1.4 billion, with total assets of R$ 241.4 billion, equivalent to 12.3% and 22.3% of the bank’s total, respectively.

| 4) | PERFORMANCE |

| 4.1) | Indices |

We present below the performance of the main financial indicators:

| % | bps | |||||||||||

| Performance Ratios | September 30, 2013 | September 30, 2012 | Change | |||||||||

| Recurring return on average equity - annualized | 19.8 | 19.4 | 40 | |||||||||

| Return on average equity - annualized | 19.6 | 18.2 | 140 | |||||||||

| Risk-Adjusted Efficiency Ratio(1) | 71.1 | 74.5 | -340 | |||||||||

| Recurring return on average assets - annualized | 1.4 | 1.5 | -10 | |||||||||

| Return on average assets - annualized | 1.4 | 1.5 | -10 | |||||||||

| Nonperforming Loans Index (NPL over 90 days) | 3.9 | 5.1 | -120 | |||||||||

| Basel ratio - economic financial consolidated | 17.5 | 17.5 | 0 | |||||||||

| Fixed assets ratio - financial conglomerate | 49.8 | 45.5 | 430 | |||||||||

(1) Calculated based on international criteria defined in the Management’s Discussion & Analysis Report.

4.2) Income

| R$ billion | % | |||||||||||

| Statement of Income for the Period(1) | Jan to Sep/13 | Jan to Sep/12 | Change(2) | |||||||||

| Gross income from financial operations | 22.6 | 23.9 | -5.1 | |||||||||

| Expenses for allowance for loan losses | (14.4 | ) | (18.0 | ) | -19.9 | |||||||

| Income from recovery of credits written off as loss | 3.6 | 3.5 | 4.8 | |||||||||

| Banking service fees and income from bank charges | 17.5 | 15.1 | 15.8 | |||||||||

| Income from insurance, pension plan and capitalization operations | 2.6 | 2.1 | 24.9 | |||||||||

| Personnel, other administrative and operating expenses | (25.9 | ) | (24.6 | ) | 5.2 | |||||||

| Tax expenses | (3.3 | ) | (3.3 | ) | -0.7 | |||||||

| Income tax and social contribution | (2.8 | ) | (2.5 | ) | 12.3 | |||||||

| Recurring net income | 11.2 | 10.5 | 5.8 | |||||||||

| Net income | 11.0 | 10.1 | 9.4 | |||||||||

| Dividends and interest on capital (net of taxes) | 1.9 | 2.0 | -2.4 | |||||||||

(1) Excludes the non-recurring effects of each period.

(2) Change is calculated based on actual figures.

Net income for the period from January to September 2013 reached R$ 11.0 billion, with annualized return of 19.6% on average equity (18.2% in the same period of the previous year). Recurring net income was R$ 11.2 billion, with annualized return of 19.8%. The increase of 15.8% in banking service fees and income from banking charges, the increase of 24.9% in income from insurance, pension plan and capitalization operations, and the decrease of 19.9% in expenses for allowance for loan losses, as compared to the same period of 2012, contributed to the increased net income. We also highlight the increase of 9.3% in the loan portfolio, and noteworthy are the areas of payroll advance loans, mortgage, corporate and foreign operations, as drivers of income through lower risks and provisions. Gross income from financial operations decreased 5.1% and reflects our strategy to prioritize lower risk portfolios.

The risk-adjusted efficiency ratio reached 71.1% at the end of September, as compared to 74.5% recorded for the same period of 2012.

4.3) Asset Data

| R$ billion | % | |||||||||||

| Balance Sheet | September 30, 2013 | September 30, 2012 | Change(1) | |||||||||

| Total assets | 1,082.8 | 960.2 | 12.8 | |||||||||

| Loan portfolio with endorsements and sureties | 456.6 | 417.6 | 9.3 | |||||||||

| Free, raised and managed own assets | 1,570.3 | 1,349.0 | 16.4 | |||||||||

| Subordinated debt | 54.4 | 48.5 | 12.1 | |||||||||

| Stockholders’ equity | 78.3 | 79.0 | -0.9 | |||||||||

| Referential equity (economic-financial consolidated) | 116.0 | 110.8 | 4.7 | |||||||||

(1) Change is calculated based on actual figures.

| 4.3.1) | Assets |

Total consolidated assets reached R$ 1.08 trillion at the end of September 2013, which represented a growth of 12.8% when compared to the same period of the previous year. Noteworthy is the 17.6% increase in the institution’s liquidity (cash and cash equivalents added to interbank investments, current).

The diversification of our business is reflected in the composition of our funding and loan portfolio, reducing risks to specific segments, which may be more impacted by the volatility in economy, as follows:

| R$ million | % | |||||||||||

| Loan Portfolio | September 30, 2013 | September 30, 2012 | Change | |||||||||

| Brazil | 420,208 | 390,149 | 7.7 | |||||||||

| Individuals | 156,198 | 148,174 | 5.4 | |||||||||

| Credit cards | 43,078 | 36,699 | 17.4 | |||||||||

| Personal credit | 27,293 | 28,195 | -3.2 | |||||||||

| Payroll advance loans | 20,579 | 12,547 | 64.0 | |||||||||

| Vehicles | 42,733 | 54,046 | -20.9 | |||||||||

| Mortgage loan | 22,515 | 16,687 | 34.9 | |||||||||

| Companies | 264,010 | 241,975 | 9.1 | |||||||||

| Corporate | 178,228 | 152,527 | 16.9 | |||||||||

| Very small, small and middle-market companies | 85,782 | 89,448 | -4.1 | |||||||||

| Latin America | 36,354 | 27,454 | 32.4 | |||||||||

| Total with endorsements and sureties | 456,561 | 417,603 | 9.3 | |||||||||

| Corporate – Private securities | 24,455 | 20,030 | 22.1 | |||||||||

| Total with endorsements, sureties and private securities | 481,017 | 437,632 | 9.9 | |||||||||

| Total with endorsements, sureties and private securities (former Vehicles) | 438,284 | 383,587 | 14.3 | |||||||||

On September 30, 2013 the balance of the loan portfolio, including endorsements and sureties, reached R$ 456.6 billion, an increase of 9.3% as compared to September 30, 2012. If we also consider the risks associated to the credits we borrow in the private securities modality, this increase will reach 9.9%. In Brazil, the balance of our loan portfolio to individuals reflects our strategy to prioritize portfolios with lower risks. Highlights:

| Brazil | |

| Individuals | |

Credit Card (Itaucard, Hipercard and partnerships) | We are leaders in the credit card segment in Brazil. From January to September 2013, the transacted amount in debit and credit cards reached R$ 181.5 billion, a 11.8% increase as compared to the same period of 2012. The balance of the loan portfolio reached R$ 43.1 billion, an increase of 17.4% as compared to the same period of the previous year. |

Payroll advance loans | Our payroll advance loans portfolio recorded a 64.0% increase when compared to September 30, 2012. The portfolio reached 4.5% of total achieved by the bank, reaching R$ 20.6 billion Banco Itaú BMG Consignado S.A. started operations in December 2012 and is present throughout the Brazilian territory, reaching R$ 5.6 billion of the estimated R$ 12 billion expected for the next 2 years, when the new institution was announced. |

| Vehicles | In September, we regained leadership in financing granted for brand new vehicles. Since last year, we have reduced the risk in this segment, which enabled us to improve the portfolio quality, with better credit results. We ended this period with a balance of R$ 42.7 billion, 20.9% lower than in the previous period. In the third quarter of 2013, new financing, lease and Finame granted totaled R$ 5.2 billion, a 3.5% increase as compared to the same period of the previous year. |

| Mortgage loans | We are the leaders in mortgage loans to individuals among the Brazilian private banks. Our offer is made by the network of branches, development companies, real estate agencies and partnerships. By the end of September, we had carried out approximately 27.0 thousand mortgage loans, a 34% increase when compared to the same period of the previous year. Mortgage loans reached R$ 32.0 billion, a growth of 33.1% as compared to September 2012, and noteworthy was the 34.9% increase in financing to individuals. |

| Companies | |

| Wholesale Banking | The Corporate portfolio, managed by Itaú BBA, is composed of loans in national and foreign currency, mandatory loans (BNDES onlending, Rural Credit and Mortgage Loans) and guarantees. In the period from January to September, noteworthy are the transactions in foreign currency that posted a 10.6% growth, particularly due exchange devaluation, and mandatory loans, which increase was 28.7% as compared to the same period of the previous year. Among Itaú BBA's activities, derivatives stand out. The focus was on operations hedging the exposures to foreign currencies, interest rates and commodities with clients that export or with prices pegged to the movements of international markets. The volume of operations contracted from January through September 2013 was 33.9% higher than in the same period of the previous year. |

| Latin America | |

| Argentina, Chile, Colombia, Paraguay and Uruguay | Our loan portfolio recorded a significant increase of 32.4% (not considering the effect of exchange variation) in relation to September 2012. We highlight the increase of loan portfolios in the companies segment in Chile, Uruguay and Argentina, which increased 32.7%, 55.4% and 35.1% respectively. In the individuals segment, the 27.1% increase in the Chile portfolio as compared to the same period of the previous year. |

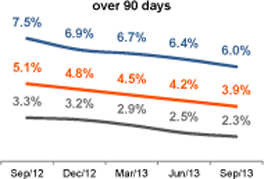

Default

|  |

In line with our credit granting policy, the total default ratio, considering the balance of transactions overdue for over 90 days, reached 3.9% on September 30, 2013, posting a decrease of 120 bps as compared to September 30, 2012. This ratio has recorded the lowest level since Itaú Unibanco merger in 2008, mainly impacted by the change in the credit profile of our portfolio. This ratio reached 6.0% for the individuals and 2.3% for companies’ portfolio at the end of September 2013, dropping 150 and 100 basis points, respectively, in relation to the same period of the previous year.

Short-term default, measured by the balance of transactions overdue from 15 to 90 days, also recorded a decrease in relation to the same period of the previous year. The reduction of 120 bps in the bank’s total portfolio was mainly due to the decrease of 180 bps in the ratio for individuals.

4.3.2) Funding

Free, raised and managed assets totaled R$ 1.57 trillion on September 30, 2013, a 16.4% growth as compared to the same period of 2012. Of this total, 45.9% refer to investment funds, managed portfolios and technical provisions for insurance, pension plan and capitalization, 25.5% to deposits, debentures, and funds from bills, 24.4% to Free assets and other liabilities, and 4.2% to Onlending, interbank deposits and Foreign borrowings through securities.

As compared to September 2012, we recorded a 26.9% increase in demand deposits added to savings deposits, which are funded at a lower cost, showing the attractiveness of our brand. The increase in funding (net of Compulsory deposits and Cash and cash equivalents) provided improvement in the Loan portfolio and funding ratio, reaching 76.5% on September 30, 2013.

4.3.3) Capital Strength

Basel Ratio –At the end of September 2013, the ratio reached 17.5%, remaining unchanged as compared to the same period of 2012, an event that evidences our strength in the capital base.

Rating Agency – in the beginning of October, Moody’s changed the outlook of the Brazilian sovereign rating from positive to stable, based on the following considerations: (i) the main credit metrics are deteriorating; (ii) the economy is going through an extended low-growth period and (iii) deterioration in the reporting quality of government accounts.

As a consequence of this change, the rating agency downgraded from positive to stable the outlook of the ratings (i) of the issuer and long-term deposit on a global scale and local currency (ii) of long-term deposit, senior and subordinated debt in foreign currency of Itaú Unibanco Holding S.A.

Additionally, in view of the reassessment conducted by the agency on the Brazilian government’s capability to provide system support to the financial system, Moody’s downgraded the ratings: (i) of the long-term issuer on a global scale and local currency, and (ii) of long-term programs/senior debt on a global scale and foreign currency of Itaú Unibanco Holding S.A.

For additional information on ratings, access www.itau-unibanco.com.br/ri > Market Opinion > Ratings.

| 4.4) | Services |

| Asset Management | In September 2013, we reached R$ 376.3 billion in assets under management, according to the ANBIMA management ranking, accounting for 15.5% of the market. We posted a 9.6% growth in total, particularly in multimarket funds and DI Funds. In addition to this strong local presence, the area has been expanding to the international field, with professionals strategically allocated, seeking adequate investment opportunities and solutions to global clients. |

| Custody Services | In the custody market, we hold R$ 930.6 billion in assets, according to the ANBIMA management ranking on September, 2013, which represents a 2% increase as compared to the same period of the previous year. In the segment of share bookkeeping services, we account for 63.5% of total companies listed on the BM&FBOVESPA. |

| Kinea | The investments management company controlled by Itaú Unibanco, holder of R$ 5.5 billion in managed assets, ranked among the largest managers in Brazil of real estate funds, hedge funds and private equity. |

| Insurance | The change in retained insurance premiums was 10.9% in the first nine months of the previous year, reaching R$ 4,303 million (not including our share in Porto Seguro, in which we hold 30% of capital). The Individual Life and Accident products were outstanding in the third quarter, with record sales as a result of a campaign in the branch network. The card protection insurance also posted a representative growth both in the opening of accounts and in ATMs, with increases of 122% and 81%, respectively, as compared to the third quarter of 2012. Technical provisions for insurance reached R$ 9.7 billion on September 30, 2013. |

| Pension Plan | The increase in future interest rates in the beginning of the quarter affected fixed-income funds of the pension plan market. Total funding from pension plans totaled R$ 12.8 billion year to date, a 5.2% drop as compared to the same period of the previous year. Revenues from management fees increased 17.3% in the same period, totaling R$ 826.3 million. Technical provisions increased 13.4% in relation to September 2012, totaling R$ 86.0 billion at the end of the period. |

| Capitalization | Technical provisions for capitalization reached R$ 3.0 billion on September 30, 2013, with a 3.2% increase in the twelve-month period. The collection from capitalization securities reached R$ 1.758 million from January to September, a 18.8% increase when compared to the same period of 2012. |

| Consortium | A self-financing system for the installment payment of properties and vehicles, the consortium supplements our product portfolio. As it is a service provision, consortium administration does not give rise to default risk or allocation of loan capital for the institution. Consortium income from January to September 2013 reached R$ 274 million, a growth of 79.8% in relation to the same period of the previous year. |

| Electronic Payment Means (Rede and Hipercard) | Our business is one of the largest in the multi-brand accreditation and merchant acquisition of credit, debt, benefit cards (voucher) and stores (private label) in Brazil. In addition, we carry out the capture, transmission, processing and financial settlement of transactions involving credit and debit cards, factoring, availability of terminals, inquiry on checks, e-commerce, and loyalty programs with partners, and electronic statement, among others. As from the second half of 2013, Rede started to capture transactions from Hipercard. Thus, Hipercard currently has the capture structure and equipment network of Rede in the whole country, increasing its operating efficiency and presence in the domestic level. |

| Investment Banking | Between January and September 2013, our Merger & Acquisition operation, which provided financial advisory to 26 transactions, totaling US$ 9.6 billion, was outstanding. In fixed income, we took part in operations of debentures, promissory notes and securitization, which totaled R$ 10.7 billion in the period from January to September 2013. In international issues of fixed income, we acted as the joint bookrunner of offerings with a total volume of US$ 18.8 billion. In capital markets, we reached the 1st position in the Origination ranking of ANBIMA of September 2013, with a volume of operations of R$ 3.2 billion. |

| 4.5) | Stock Market |

Market value – At the end of the third quarter of 2013, Itaú Unibanco was ranked as the 22ndlargest bank in the world based on the market value criterion (R$ 156.4 billion), according to the Bloomberg ranking.

Traded volume –We daily traded R$ 676.8 million on the stock exchanges where our shares are traded, with a daily average volume of R$ 333.5 million (ITUB3 and ITUB4) on BM&FBOVESPA and R$ 343.3 million (ITUB) on the New York Stock Exchange (NYSE), in the year to date.

Dividends/Interest on Capital –In the year to date, we paid or provided for R$ 1,912.6 million in dividends and interest on capital, net of taxes. Net payout for the last twelve months was 30.7%.

Relations with the market –We took part in 20 conferences and road shows in Brazil and abroad, and held 19 out of the 22 Apimec (Association of Capital Market Analysts and Investment Professionals) meetings scheduled for 2013, thus strengthening our relations with stockholders, analysts and investors of the capital markets. We take the opportunity to strengthen our invitation to our relationship audience for the next Apimec meeting in São Paulo, to be held on November 12.

| R$ | % | |||||||||||

| Shares | September 30, 2013 | September 30, 2012 | Change | |||||||||

| Recurring net income per share(1) | 2.25 | 2.12 | 5.9 | |||||||||

| Net income per share(1) | 2.22 | 2.03 | 9.4 | |||||||||

| Book value per share(1) | 15.79 | 15.89 | -0.6 | |||||||||

| Number of outstanding shares (in thousands)(2) | 4,956,804 | 4,970,068 | -0.3 | |||||||||

| Dividends/Interest on capital, net per share | 0.39 | 0.39 | -0.5 | |||||||||

| Price of preferred share (ITUB4)(2)(3) | 31.56 | 27.85 | 13.3 | |||||||||

| Price of common share (ITUB3)(2)(3) | 30.17 | 24.96 | 20.9 | |||||||||

| Price of preferred share (PN)(3)/Net income per share | 14.19 | 13.70 | 3.6 | |||||||||

| Price of preferred share (PN)(3)/Stockholders’ equity per share | 2.00 | 1.75 | 14.1 | |||||||||

| Market value (in billions) (4)(5) | 156.4 | 138.4 | 13.0 | |||||||||

(1) Calculated based on the weighted average of the number of shares;

(2) The number of outstanding shares and the price of share were adjusted to reflect the 10% bonus on May 20, 2013;

(3) Based on the closing quotation on the last day of the period;

(4) Calculated based on the average quotation of preferred shares on the last day of the period (quotation of average PN multiplied by the number of outstanding shares at the end of the period);

(5) R$ 152,6 billion considering the closing quotation of common and preferred (ON and PN) shares multiplied by total outstanding shares of each type of shares.

| 5) | PEOPLE |

Itaú Unibanco had approximately 94.3 thousand people at the end of the third quarter of 2013, including over 6 thousand employees in foreign units. The employee’s fixed compensation plus charges and benefits totaled R$ 7.8 billion for this period.

We started the selection process for the Trainee Program 2014, which counted this year on 18.3 thousand enrollments. Among those enrolled, we have youths coming from throughout Brazil, in addition to our interns and employees eligible for the program. The final outcome is expected to be disclosed to the candidates in November.

On October 11, 2013 a collective bargaining agreement was signed in connection with the 2013/2014 collective bargaining process, which resulted in an 8% addition to the salaries of banking sector employees, in addition to other benefits.

| 6) | SUSTAINABILITY |

Itaú Unibanco was selected for the 14th consecutive year to make up the Dow Jones Sustainability World Index (DJSI) portfolio, the main sustainability index in the world, in its 2013/2014 edition. Accordingly, it is the only Latin American bank to be part of the index since its creation. In this edition, we achieved the best rate in the banking sector in the criteria “Policies/Anti-crime actions”, “Brand management” and “Financial Stability and Systemic Risk”. The new portfolio includes only eight Brazilian companies, among them two related companies (Itaú Unibanco and Itaúsa). This shows the significance of the corporate sustainability in our organizational culture and long-term vision.

We were elected as one of the companies with the best environmental practices in Brazil in the Época Empresa Verde (Green Company Época) Award (Época magazine), as one of the leading companies in the Empresário Amigo do Esporte 2013 (Entrepreneur Friend of Sport) Award (Ministry of Sport), and we are one of the companies that invested more in this sector under the Sports Incentive Law by supporting sports and para-sports projects.

In this last quarter we published the Itaú Social Welfare 2013 index. Designed by our economy research team, this index takes into consideration human conditions and income distribution in Brazil, in addition to economy conditions.

In the beginning of 2013 we launched the “#issomudaomundo” (change the world) platform, aimed at forging a bond between our purpose of being a transformation agent in the lives of people, our causes and the several projects receiving investments from Itaú in connection with the education, culture, sports and urban mobility pillars. After the Bike Rio, Bike Sampa, Bike PoA and Bike PE (biking in Rio de Janeiro, biking in São Paulo, biking in Porto Alegre and biking in Pernambuco), now comes the time for Bike Salvador (biking in Salvador) in another partnership with the Government of Bahia, which was launched last month.

In October we redesigned the national campaign to encourage reading among children. In this action, adults will be invited to read for children and, to support this invitation, Itaú will offer 4.4 million children’s books free of charge. The purpose is to mobilize society for the importance of reading to a child, showing how this gesture may contribute to ensuring their rights, develop their capacity to learn, and express themselves, in addition to strengthening the affective bond between the child and the adult and developing the taste for reading from an early age. Since 2010, over 30 million books were delivered by the program.

| 7) | INDEPENDENT AUDITORS – CVM Instruction No. 381 |

Procedures adopted by the Company

The policy adopted by Itaú Unibanco Holding S.A., its subsidiaries, and parent company to engage in non-audit related services from our independent auditors is based on the applicable regulations and internationally accepted principles that preserve the auditor’s independence. These principles include the following: (a) an auditor cannot audit his or her own work, (b) an auditor cannot function in the role of management in companies where he or she provides external audit services; and (c) an auditor cannot promote the interests of his or her client.

During the period from January to September 2013, the independent auditors and related parties did not provide non-audit related services in excess of 5% of total external audit fees.

According to CVM Instruction No. 381, we list below the engaged services and related dates:

| § | January 7, March 20, July 31 and August 28 – acquisition of technical material; |

| § | February 28 – review of aspects related to the business continuity program. |

Summary of the Independent Auditors’ justification - PricewaterhouseCoopers

The provision of the above described non-audit related professional services do not affect the independence or the objectivity of the external audit of Itaú Unibanco, its parent and subsidiary/affiliated companies. The policy adopted for providing non-audit related services to Itaú Unibanco is based on principles that preserve the independence of Independent Auditors, all of which were considered in the provision of the referred services, including the approval by the Audit Committee.

| 8) | BACEN - Circular No. 3,068/01 |

Itaú Unibanco hereby represents to have the financial capacity and the intention to hold to maturity securities classified under the line “held-to-maturity securities” in the balance sheet, in the amount of R$ 3,7 billion, corresponding to 1,3% of total securities held.

| 9) | IFRS (International Financial Reporting Standards)/BRGAAP |

We disclosed the consolidated financial statements in accordance with the international financial reporting standards (IFRS), at the same date of this publication, pursuant to CVM/SEP Circular Letter 01/13.

| 10) | ACKNOWLEDGMENTS |

We thank our employees for their determination and skills which have been essential to reaching consistent and differentiated results, and our stockholders and clients for their trust.

(Approved at the Board of Directors' Meeting of October 28, 2013).

ITAÚ UNIBANCO HOLDING S.A.

| BOARD OF DIRECTORS | EXECUTIVE BOARD | |

| Chairman | Chief Executive Officer | |

| Pedro Moreira Salles | Roberto Egydio Setubal | |

| Vice-Chairmen | Executive Vice-Presidents | |

| Alfredo Egydio Arruda Villela Filho | Alfredo Egydio Setubal (*) | |

| Roberto Egydio Setubal | Candido Botelho Bracher | |

| Members | Executive Directors | |

| Alfredo Egydio Setubal | Caio Ibrahim David | |

| Candido Botelho Bracher | Claudia Politanski | |

| Demosthenes Madureira de Pinho Neto | Eduardo Mazzilli de Vassimon | |

| Gustavo Jorge Laboissière Loyola | Ricardo Baldin | |

| Henri Penchas | ||

| Israel Vainboim | ||

| Nildemar Secches | ||

| Pedro Luiz Bodin de Moraes | Directors | |

| Ricardo Villela Marino | Alexsandro Broedel Lopes | |

| Ana Tereza de Lima e Silva Prandini | ||

| Eduardo Hiroyuki Miyaki | ||

| Emerson Macedo Bortoloto | ||

| AUDIT COMMITTEE | Robert George Stribling | |

| President | Rodrigo Luis Rosa Couto | |

| Gustavo Jorge Laboissière Loyola | Rogério Paulo Calderón Peres | |

| Members | ||

| Alkimar Ribeiro Moura | (*) Investor Relations Director | |

| Eduardo Augusto de Almeida Guimarães | ||

| Geraldo Travaglia Filho | ||

| Guy Almeida Andrade | ||

| Luiz Alberto Fiore | ||

| FISCAL COUNCIL | ||

| President | ||

| Iran Siqueira Lima | ||

| Members | ||

| Alberto Sozin Furuguem | Accountant | |

| Luiz Alberto de Castro Falleiros | Reginaldo José Camilo | |

| CRC-1SP – 114.497/O-9 |

ITAÚ UNIBANCO S.A.

| Chief Executive Officer and General Manager | Directors (continued) | |

| Roberto Egydio Setubal | Fernando Barçante Tostes Malta | |

| Fernando Della Torre Chagas | ||

| Executive Vice-Presidents | Fernando José Costa Teles | |

| Alexandre de Barros | Fernando Mattar Beyruti | |

| Alfredo Egydio Setubal | Flávio Delfino Junior | |

| Caio Ibrahim David | Francisco Vieira Cordeiro Neto | |

| Claudia Politanski | Gabriel Amado de Moura | |

| Eduardo Mazzilli de Vassimon | Guilherme Martins Vasconcelos | |

| José Castro Araújo Rudge | Henrique Pinto Echenique | |

| Márcio de Andrade Schettini | João Antonio Dantas Bezerra Leite | |

| Marco Ambrogio Crespi Bonomi | Jorge Luiz Viegas Ramalho | |

| Ricardo Villela Marino | José Félix Valencia Ríos | |

| José Isern | ||

| Executive Directors | José Virgilio Vita Neto | |

| André Sapoznik | Leila Cristiane Barboza Braga de Melo | |

| Carlos Eduardo Monico | Luís Eduardo Gross Siqueira Cunha | |

| Fernando Marsella Chacon Ruiz | Luis Tadeu Mantovani Sassi | |

| Flavio Augusto Aguiar de Souza | Luiz Antonio Nogueira de França | |

| Gustavo Adolfo Funcia Murgel | Luiz Eduardo Loureiro Veloso | |

| Luis Antonio Rodrigues | Luiz Fernando Butori Reis dos Santos | |

| Luís Fernando Staub | Luiz Severiano Ribeiro | |

| Milton Maluhy Filho | Marcello Siniscalchi | |

| Marcelo Boock | ||

| Directors | Marcelo da Costa Lourenço | |

| Adilso Martins de Lima | Marcelo Luis Orticelli | |

| Adriano Cabral Volpini | Marco Antonio Sudano | |

| Alberto Fernandes | Marcos Antônio Vaz de Magalhães | |

| Alexandre Jadallah Aoude | Marcos Vanderlei Belini Ferreira | |

| Alexsandro Broedel Lopes | Mario Luiz Amabile | |

| Álvaro de Alvarenga Freire Pimentel | Messias dos Santos Esteves | |

| Ana Carla Abrão Costa | Osvaldo José Dal Fabbro | |

| Ana Tereza de Lima e Silva Prandini | Paulo Meirelles de Oliveira Santos | |

| Andréa Matteucci Pinotti Cordeiro | Renata Helena de Oliveira Tubini | |

| Carlos Eduardo de Castro | Ricardo Lima Soares | |

| Carlos Eduardo Maccariello | Ricardo Orlando | |

| Carlos Henrique Donegá Aidar | Ricardo Ribeiro Mandacaru Guerra | |

| Carlos Orestes Vanzo | Ricardo Urquijo Lazcano | |

| Cesar Padovan | Roberto Fernando Vicente | |

| Cícero Marcus de Araújo | Rodrigo Luis Rosa Couto | |

| Cintia Carbonieri Araújo | Rogério Carvalho Braga | |

| Claudio César Sanches | Rogério Paulo Calderón Peres | |

| Claudio José Coutinho Arromate | Romildo Gonçalves Valente | |

| Cristiane Magalhães Teixeira Portella | Rooney Silva | |

| Cristina Cestari Spada | Sergio Guillinet Fajerman | |

| Daniel Luiz Gleizer | Sergio Souza Fernandes Júnior | |

| Edilson Pereira Jardim | Wagner Bettini Sanches | |

| Fabiana Pascon Bastos |

| BANCO ITAÚ BBA S.A. | ||

| BOARD OF DIRECTORS | ||

| Chairman | Directors | |

| Roberto Egydio Setubal | Alberto Zoffmann do Espírito Santo | |

| Alexandre Enrico Silva Figliolino | ||

| Vice-Chairmen | André Carvalho Whyte Gailey | |

| Alfredo Egydio Setubal | André Ferrari | |

| Candido Botelho Bracher | Antonio José Calheiros Ribeiro Ferreira | |

| Caio Ibrahim David | ||

| Members | Cristiano Rogério Cagne | |

| Antonio Carlos Barbosa de Oliveira | Eduardo Cardoso Armonia | |

| Caio Ibrahim David | Eduardo Corsetti | |

| Eduardo Mazzilli de Vassimon | Elaine Cristina Zanatta Rodrigues Vasquinho | |

| Henri Penchas | Emerson Savi Junqueira | |

| João Dionísio Filgueira Barreto Amoêdo | Fabio Massashi Okumura | |

| Flávio Delfino Junior | ||

| Gilberto Frussa | ||

| EXECUTIVE BOARD | Ilan Goldfajn | |

| Chief Executive Officer | João Carlos de Gênova | |

| Candido Botelho Bracher | Luiz Felipe Monteiro Arcuri Trevisan | |

| Marcello Peccinini de Chiaro | ||

| Managing Vice-Presidents | Marcelo Ariel Rosenhek | |

| Alberto Fernandes | Marco Antônio Sudano | |

| Daniel Luiz Gleizer | Mário Lúcio Gurgel Pires | |

| Jean-Marc Robert Nogueira Baptista Etlin | Mário Luís Brugnetti | |

| José Roberto Haym | Rodrigo Pastor Faceiro Lima | |

| Thales Ferreira Silva | ||

| Executive Directors | Vanessa Lopes Reisner | |

| Alexandre Jadallah Aoude | ||

| Álvaro de Alvarenga Freire Pimentel | ||

| André Luís Teixeira Rodrigues | ||

| Fernando Fontes Iunes | ||

| José Augusto Durand |

| ITAÚ SEGUROS S.A. | |

| Chief Executive Officer | |

| Fernando José Costa Teles | |

| Directors | |

| Adriano Cabral Volpini | |

| Alexsandro Broedel Lopes | |

| Antonio Eduardo Márquez de Figueiredo Trindade | |

| Cláudio José Coutinho Arromate | |

| Fernando Barçante Tostes Malta (*) | |

| Henrique Pinto Echenique | |

| Mario Luiz Amabile | |

| (*) Elected at O/EGM on August 14, 2013. Awaiting Susep approval. | |

ITAÚ UNIBANCO HOLDING S.A.

Consolidated Balance Sheet (Note 2a)

(In thousands of Reais)

| Assets | Note | 09/30/2013 | 09/30/2012 | |||||||

| Current assets | 793,348,881 | 706,038,456 | ||||||||

| Cash and cash equivalents | 14,466,493 | 13,103,962 | ||||||||

| Interbank investments | 4b and 6 | 192,458,860 | 162,895,073 | |||||||

| Money market | 169,580,802 | 142,631,765 | ||||||||

| Money market – Assets Guaranteeing Technical Provisions - SUSEP | 11b | 3,107,401 | 2,550,201 | |||||||

| Interbank deposits | 19,770,657 | 17,713,107 | ||||||||

| Securities and derivative financial instruments | 4c, 4d and 7 | 203,098,781 | 180,685,791 | |||||||

| Own portfolio | 62,556,363 | 50,363,127 | ||||||||

| Subject to repurchase commitments | 27,293,249 | 29,028,595 | ||||||||

| Pledged in guarantee | 6,976,675 | 6,061,433 | ||||||||

| Securities under resale agreements with free movement | 46,674 | 88,986 | ||||||||

| Deposited with the Central Bank | 12,983,586 | 12,591,352 | ||||||||

| Derivative financial instruments | 7,140,410 | 6,289,799 | ||||||||

| Assets guaranteeing technical provisions - PGBL/VGBL fund quotas | 11b | 79,779,392 | 69,856,629 | |||||||

| Assets guaranteeing technical provisions – other securities | 11b | 6,322,432 | 6,405,870 | |||||||

| Interbank accounts | 73,070,551 | 68,050,957 | ||||||||

| Pending settlement | 6,015,643 | 3,642,547 | ||||||||

| Central Bank deposits | 67,001,420 | 64,359,216 | ||||||||

| National Housing System (SFH) | 1,599 | 1,106 | ||||||||

| Correspondents | 51,889 | 32,654 | ||||||||

| Interbank onlending | - | 15,434 | ||||||||

| Interbranch accounts | 98,045 | 45,053 | ||||||||

| Loan, lease and other credit operations | 8 | 199,763,834 | 190,369,182 | |||||||

| Operations with credit granting characteristics | 4e | 213,468,759 | 205,865,976 | |||||||

| (Allowance for loan losses) | 4f | (13,704,925 | ) | (15,496,794 | ) | |||||

| Other receivables | 107,643,952 | 87,441,291 | ||||||||

| Foreign exchange portfolio | 9 | 52,982,235 | 40,328,553 | |||||||

| Income receivable | 1,599,211 | 1,278,004 | ||||||||

| Transactions with credit card issuers | 4e | 19,978,743 | 17,466,525 | |||||||

| Receivables from insurance and reinsurance operations | 4m I and 11b | 4,636,052 | 3,832,954 | |||||||

| Negotiation and intermediation of securities | 3,281,112 | 2,612,552 | ||||||||

| Sundry | 13a | 25,166,599 | 21,922,703 | |||||||

| Other assets | 4g | 2,748,365 | 3,447,147 | |||||||

| Assets held for sale | 168,304 | 151,515 | ||||||||

| (Valuation allowance) | (47,482 | ) | (42,148 | ) | ||||||

| Unearned premiums of reinsurance | 4m I | 714,658 | 703,734 | |||||||

| Prepaid expenses | 4g and 13b | 1,912,885 | 2,634,046 | |||||||

| Long-term receivables | 274,873,312 | 231,030,307 | ||||||||

| Interbank investments | 4b and 6 | 804,451 | 447,218 | |||||||

| Money market | 387 | 5 | ||||||||

| Interbank deposits | 804,064 | 447,213 | ||||||||

| Securities and derivative financial instruments | 4c, 4d and 7 | 69,011,104 | 53,870,599 | |||||||

| Own portfolio | 42,407,993 | 33,015,876 | ||||||||

| Subject to repurchase commitments | 16,569,334 | 11,117,179 | ||||||||

| Pledged in guarantee | 545,104 | 611,621 | ||||||||

| Derivative financial instruments | 4,722,572 | 4,755,155 | ||||||||

| Assets guaranteeing technical provisions – other securities | 11b | 4,766,101 | 4,370,768 | |||||||

| Interbank accounts - National Housing System (SFH) | 709,581 | 665,268 | ||||||||

| Loan, lease and other credit operations | 8 | 161,623,237 | 141,758,683 | |||||||

| Operations with credit granting characteristics | 4e | 173,570,855 | 153,944,316 | |||||||

| (Allowance for loan losses) | 4f | (11,947,618 | ) | (12,185,633 | ) | |||||

| Other receivables | 40,442,889 | 32,944,074 | ||||||||

| Foreign exchange portfolio | 9 | 6,688 | 621,334 | |||||||

| Sundry | 13a | 40,436,201 | 32,322,740 | |||||||

| Other assets | 4g | 2,282,050 | 1,344,465 | |||||||

| Unearned premiums of reinsurance | 4m I | 269,443 | - | |||||||

| Prepaid expenses | 4g and 13b | 2,012,607 | 1,344,465 | |||||||

| Permanent assets | 14,564,629 | 23,147,466 | ||||||||

| Investments | 4h and 15a Il | 3,067,996 | 3,324,158 | |||||||

| Investments in affiliates and jointly controlled entities | 2,345,214 | 2,365,544 | ||||||||

| Other investments | 996,570 | 1,163,906 | ||||||||

| (Allowance for losses) | (273,788 | ) | (205,292 | ) | ||||||

| Real estate in use | 4i and 15b | 6,108,484 | 5,330,113 | |||||||

| Real estate in use | 3,814,520 | 3,367,455 | ||||||||

| Other fixed assets | 9,862,468 | 9,177,275 | ||||||||

| (Accumulated depreciation) | (7,568,504 | ) | (7,214,617 | ) | ||||||

| Goodwill | 4j and 15b | 44,983 | 10,068,929 | |||||||

| Intangible assets | 4k and 15b | 5,343,166 | 4,424,266 | |||||||

| Acquisition of rights to credit payroll | 1,202,565 | 1,668,789 | ||||||||

| Other intangible assets | 6,092,547 | 4,812,760 | ||||||||

| (Accumulated amortization) | (1,951,946 | ) | (2,057,283 | ) | ||||||

| Total assets | 1,082,786,822 | 960,216,229 | ||||||||

The accompanying notes are an integral part of these financial statements.

ITAÚ UNIBANCO HOLDING S.A.

Consolidated Balance Sheet (Note 2a)

(In thousands of Reais)

| Liabilities | Note | 09/30/2013 | 09/30/2012 | |||||||

| Current liabilities | 596,435,351 | 498,055,041 | ||||||||

| Deposits | 4b and 10b | 192,810,585 | 159,641,813 | |||||||

| Demand deposits | 37,816,640 | 29,817,694 | ||||||||

| Savings deposits | 98,227,575 | 77,413,953 | ||||||||

| Interbank deposits | 7,324,006 | 9,261,769 | ||||||||

| Time deposits | 49,442,364 | 43,148,397 | ||||||||

| Deposits received under securities repurchase agreements | 4b and 10c | 175,113,985 | 134,124,016 | |||||||

| Own portfolio | 73,630,824 | 67,401,791 | ||||||||

| Third-party portfolio | 100,216,519 | 66,487,407 | ||||||||

| Free portfolio | 1,266,642 | 234,818 | ||||||||

| Funds from acceptances and issuance of securities | 4b and 10d | 25,775,077 | 32,853,856 | |||||||

| Real estate, mortgage, credit and similar notes | 19,651,889 | 23,008,711 | ||||||||

| Debentures | 220 | 2,616,549 | ||||||||

| Foreign borrowings through securities | 6,122,968 | 7,228,596 | ||||||||

| Interbank accounts | 7,625,626 | 4,303,979 | ||||||||

| Pending settlement | 5,099,684 | 3,167,626 | ||||||||

| Correspondents | 2,525,942 | 1,136,353 | ||||||||

| Interbranch accounts | 5,365,585 | 4,055,688 | ||||||||

| Third-party funds in transit | 5,330,107 | 4,048,132 | ||||||||

| Internal transfer of funds | 35,478 | 7,556 | ||||||||

| Borrowings and onlending | 4b and 10e | 37,607,335 | 30,292,811 | |||||||

| Borrowings | 25,431,043 | 18,623,732 | ||||||||

| Onlending | 12,176,292 | 11,669,079 | ||||||||

| Derivative financial instruments | 4d and 7h | 5,040,150 | 5,036,698 | |||||||

| Technical provision for insurance, pension plan and capitalization | 4m II and 11a | 11,457,411 | 11,478,348 | |||||||

| Other liabilities | 135,639,597 | 116,267,832 | ||||||||

| Collection and payment of taxes and contributions | 4,430,366 | 4,517,450 | ||||||||

| Foreign exchange portfolio | 9 | 53,308,271 | 40,495,090 | |||||||

| Social and statutory | 16b II | 2,385,194 | 2,335,915 | |||||||

| Tax and social security contributions | 4n 4o and 14c | 7,843,061 | 8,375,074 | |||||||

| Negotiation and intermediation of securities | 6,703,864 | 5,099,896 | ||||||||

| Credit card operations | 4e | 42,172,662 | 38,979,670 | |||||||

| Subordinated debt | 10f | 4,347,233 | 4,631,588 | |||||||

| Sundry | 13c | 14,448,946 | 11,833,149 | |||||||

| Long-term liabilities | 405,164,984 | 381,248,470 | ||||||||

| Deposits | 4b and 10b | 59,468,640 | 72,277,542 | |||||||

| Interbank deposits | 355,763 | 254,083 | ||||||||

| Time deposits | 59,112,877 | 72,023,459 | ||||||||

| Deposits received under securities repurchase agreements | 4b and 10c | 120,022,467 | 111,147,697 | |||||||

| Own portfolio | 91,064,610 | 94,345,489 | ||||||||

| Free portfolio | 28,957,857 | 16,802,208 | ||||||||

| Funds from acceptances and issuance of securities | 4b and 10d | 24,896,558 | 24,190,179 | |||||||

| Real estate, mortgage, credit and similar notes | 14,624,349 | 16,814,606 | ||||||||

| Foreign borrowings through securities | 10,272,209 | 7,375,573 | ||||||||

| Borrowings and onlending | 4b and 10e | 35,693,745 | 26,560,967 | |||||||

| Borrowings | 6,515,533 | 3,370,086 | ||||||||

| Onlending | 29,178,212 | 23,190,881 | ||||||||

| Derivative financial instruments | 4d and 7g | 4,165,030 | 4,088,688 | |||||||

| Technical provision for insurance, pension plan and capitalization | 4m II and 11a | 87,300,193 | 75,802,710 | |||||||

| Other liabilities | 73,618,351 | 67,180,687 | ||||||||

| Foreign exchange portfolio | 9 | 6,794 | 629,586 | |||||||

| Tax and social security contributions | 4n, 4o and 14c | 12,769,661 | 13,041,071 | |||||||

| Subordinated debt | 10f | 50,046,294 | 43,912,152 | |||||||

| Sundry | 13c | 10,795,602 | 9,597,878 | |||||||

| Deferred income | 4p | 1,085,103 | 812,922 | |||||||

| Minority interest in subsidiaries | 16e | 1,841,757 | 1,121,285 | |||||||

| Stockholders' equity | 16 | 78,259,627 | 78,978,511 | |||||||

| Capital | 60,000,000 | 45,000,000 | ||||||||

| Capital reserves | 854,358 | 812,352 | ||||||||

| Revenue reserves | 20,138,600 | 33,503,773 | ||||||||

| Asset valuation adjustment | 4c, 4d and 7d | (815,451 | ) | 1,189,720 | ||||||

| (Treasury shares) | (1,917,880 | ) | (1,527,334 | ) | ||||||

| Total liabilities and stockholders' equity | 1,082,786,822 | 960,216,229 | ||||||||

The accompanying notes are an integral part of these financial statements.

ITAÚ UNIBANCO HOLDING S.A.

Consolidated Statement of Income (Note 2a)

(In thousands of Reais)

| Note | 01/01 to 09/30/2013 | 01/01 to 09/30/2012 | ||||||||

| Income from financial operations | 67,629,290 | 76,334,176 | ||||||||

| Loan, lease and other credit operations | 43,313,370 | 45,900,362 | ||||||||

| Securities and derivative financial instruments | 18,009,052 | 19,557,163 | ||||||||

| Financial income from insurance, pension plan and capitalization operations | 11c | 2,241,423 | 5,314,080 | |||||||

| Foreign exchange operations | 991,670 | 1,001,844 | ||||||||

| Compulsory deposits | 3,073,775 | 4,560,727 | ||||||||

| Expenses of financial operations | (34,242,170 | ) | (37,989,523 | ) | ||||||

| Money market | (29,829,253 | ) | (31,515,987 | ) | ||||||

| Financial expenses on technical provisions for insurance, pension plan and capitalization | 11c | (1,901,022 | ) | (4,803,337 | ) | |||||

| Borrowings and onlending | (2,511,895 | ) | (1,670,199 | ) | ||||||

| Income from financial operations before loan and losses | 33,387,120 | 38,344,653 | ||||||||

| Result of allowance for loan losses | 8d I | (10,739,752 | ) | (14,482,032 | ) | |||||

| Expenses for allowance for loan losses | (14,384,990 | ) | (17,959,140 | ) | ||||||

| Income from recovery of credits written off as loss | 3,645,238 | 3,477,108 | ||||||||

| Gross income from financial operations | 22,647,368 | 23,862,621 | ||||||||

| Other operating revenues (expenses) | (8,501,804 | ) | (10,278,068 | ) | ||||||

| Banking service fees | 13d | 12,228,791 | 10,767,367 | |||||||

| Asset management | 2,641,025 | 2,232,894 | ||||||||

| Current account services | 544,602 | 453,188 | ||||||||

| Credit cards | 5,535,078 | 4,748,607 | ||||||||

| Sureties and credits granted | 1,278,990 | 1,165,739 | ||||||||

| Receipt services | 1,060,583 | 1,051,608 | ||||||||

| Other | 1,168,513 | 1,115,331 | ||||||||

| Income from bank charges | 13e | 5,275,810 | 4,348,110 | |||||||

| Result from insurance, pension plan and capitalization operations | 11c | 2,649,825 | 2,121,522 | |||||||

| Personnel expenses | 13f | (11,236,674 | ) | (10,286,591 | ) | |||||

| Other administrative expenses | 13g | (10,749,334 | ) | (10,549,893 | ) | |||||

| Tax expenses | 4o and 14a II | (3,295,589 | ) | (3,317,217 | ) | |||||

| Equity in earnings of affiliates, jointly controlled entities and other investments | 15a lll | 264,694 | 189,878 | |||||||

| Other operating revenues | 13h | 240,989 | 193,633 | |||||||

| Other operating expenses | 13i | (3,880,316 | ) | (3,744,877 | ) | |||||

| Operating income | 14,145,564 | 13,584,553 | ||||||||

| Non-operating income | 23,828 | (285,951 | ) | |||||||

| Income before taxes on income and profit sharing | 14,169,392 | 13,298,602 | ||||||||

| Income tax and social contribution | 4o and 14a I | (2,842,971 | ) | (2,531,032 | ) | |||||

| Due on operations for the period | (6,648,155 | ) | (6,769,073 | ) | ||||||

| Related to temporary differences | 3,805,184 | 4,238,041 | ||||||||

| Profit sharing – Management Members - Statutory - Law No. 6,404 of 12/15/1976 | (181,748 | ) | (122,972 | ) | ||||||

| Minority interest in subsidiaries | 16e | (94,735 | ) | (542,453 | ) | |||||

| Net income | 11,049,937 | 10,102,145 | ||||||||

| Weighted average of the number of outstanding shares | 16a | 4,968,122,233 | 4,969,731,087 | |||||||

| Net income per share – R$ | 2.22 | 2.03 | ||||||||

| Book value per share - R$ (outstanding at 09/30) | 15.79 | 15.89 | ||||||||

| Supplementary information | ||||||||||

| Exclusion of nonrecurring effects | 2a and 22k | 105,587 | 438,832 | |||||||

| Net income without nonrecurring effects | 11,155,524 | 10,540,977 | ||||||||

| Net income per share – R$ | 2.25 | 2.12 | ||||||||

The accompanying notes are an integral part of these financial statements.

ITAÚ UNIBANCO HOLDING S.A.

Consolidated Statement of Cash Flows

(In thousands of Reais)

| NOTE | 01/01 to 09/30/2013 | 01/01 to 09/30/2012 | ||||||||

| Adjusted net income | 21,053,196 | 27,687,716 | ||||||||

| Net income | 11,049,937 | 10,102,145 | ||||||||

| Adjustments to net income: | 10,003,259 | 17,585,571 | ||||||||

| Granted options recognized | 165,422 | 151,500 | ||||||||

| Adjustment to market value of securities and derivative financial instruments (assets/liabilities) | 7h | 268,713 | (930,095 | ) | ||||||

| Effects of changes in exchange rates on cash and cash equivalents | (1,482,945 | ) | (1,246,762 | ) | ||||||

| Allowance for loan losses | 14,384,990 | 17,959,140 | ||||||||

| Interest and foreign exchange expense from operations with subordinated debt | 3,093,938 | 3,310,483 | ||||||||

| Interest expense from operations with debentures | 41,463 | 132,004 | ||||||||

| Financial expenses on technical provisions for pension plan and capitalization | 1,901,022 | 4,803,337 | ||||||||

| Depreciation and amortization | 15b | 1,731,928 | 1,645,983 | |||||||

| Adjustment to legal liabilities – tax and social security | (814,063 | ) | 634,853 | |||||||

| Adjustment to provision for contingent liabilities | 519,636 | 335,811 | ||||||||

| Deferred taxes | (3,805,184 | ) | (4,238,041 | ) | ||||||

| Equity in earnings of affiliates, jointly controlled entities and other investments | 15a lll | (264,694 | ) | (189,878 | ) | |||||

| Interest and foreign exchange income from available-for-sale securities | (5,684,236 | ) | (3,706,845 | ) | ||||||

| Interest and foreign exchange income from held-to-maturity securities | (336,502 | ) | (401,047 | ) | ||||||

| (Gain) loss from sale of available-for-sale financial assets | 7i | 262,747 | (879,625 | ) | ||||||

| (Gain) loss from sale of investments | (60,430 | ) | (235,252 | ) | ||||||

| (Gain) loss from sale of foreclosed assets | (10,141 | ) | (15,774 | ) | ||||||

| (Gain) loss from sale of fixed assets | (2,416 | ) | 6,641 | |||||||

| Minority interest | 94,735 | 542,453 | ||||||||

| Other | (725 | ) | (93,315 | ) | ||||||

| Change in assets and liabilities | 416,009 | 20,395,014 | ||||||||

| (Increase) decrease in assets | (35,431,267 | ) | (46,859,056 | ) | ||||||

| Interbank investments | (1,823,198 | ) | (28,416,038 | ) | ||||||

| Securities and derivative financial instruments (assets/liabilities) | (2,789,192 | ) | (25,386,620 | ) | ||||||

| Compulsory deposits with the Central Bank of Brazil | (3,300,048 | ) | (643,477 | ) | ||||||

| Interbank and interbranch accounts (assets/liabilities) | 2,043,628 | 35,116,322 | ||||||||

| Loan, lease and other credit operations | (34,272,449 | ) | (30,427,169 | ) | ||||||

| Other receivables and other assets | 2,716,401 | 743,097 | ||||||||

| Foreign exchange portfolio and negotiation and intermediation of securities (assets/liabilities) | 1,993,591 | 2,154,829 | ||||||||

| (Decrease) increase in liabilities | 35,847,276 | 67,254,070 | ||||||||

| Deposits | 9,087,417 | (10,717,067 | ) | |||||||

| Deposits received under securities repurchase agreements | 6,353,523 | 56,453,176 | ||||||||

| Funds for issuance of securities | (2,867,111 | ) | 3,909,068 | |||||||

| Borrowings and onlending | 14,175,873 | 251,718 | ||||||||

| Credit card operations (assets/liabilities) | (3,438,676 | ) | (1,256,209 | ) | ||||||

| Technical provision for insurance, pension plan and capitalization | 3,135,945 | 8,329,215 | ||||||||

| Collection and payment of taxes and contributions | 4,014,553 | 3,661,475 | ||||||||

| Other liabilities | 5,454,869 | 6,645,983 | ||||||||

| Deferred income | (69,117 | ) | (23,289 | ) | ||||||

| Payment of income tax and social contribution | (5,055,257 | ) | (5,611,052 | ) | ||||||

| Net cash provided by (used in) operating activities | 16,413,948 | 42,471,678 | ||||||||

| Interest on capital / dividends received from affiliated companies | 79,154 | 15,577 | ||||||||

| Funds received from sale of available-for-sale securities | 28,553,997 | 15,267,052 | ||||||||

| Funds received from redemption of held-to-maturity securities | 360,937 | 342,820 | ||||||||

| Disposal of assets not for own use | 88,295 | 71,676 | ||||||||

| Disposal of investments | 208,428 | 386,866 | ||||||||

| Sale of fixed assets | 41,863 | 214,731 | ||||||||

| Termination of intangible asset agreements | 63,137 | (643 | ) | |||||||

| Purchase of available-for-sale securities | (22,219,754 | ) | (26,975,859 | ) | ||||||

| Purchase of held-to-maturity securities | (531,438 | ) | (205 | ) | ||||||

| Purchase of investments | (80,038 | ) | (897,123 | ) | ||||||

| Purchase of fixed assets | 15b | (1,707,499 | ) | (1,258,799 | ) | |||||

| Purchase of intangible assets | 15b | (1,239,099 | ) | (1,228,698 | ) | |||||

| Net cash provided by (used in) invesment activities | 3,617,982 | (14,062,605 | ) | |||||||

| Increase in subordinated debt | - | 16,579,927 | ||||||||

| Decrease in subordinated debt | (3,072,536 | ) | (10,321,154 | ) | ||||||

| Increase in debentures | - | 1,500,000 | ||||||||

| Decrease in debentures | (1,610,296 | ) | (54,251 | ) | ||||||

| Change in minority interest | 16e | 362,893 | 348,314 | |||||||

| Acquisition of minority interest in Redecard S.A. | - | (10,807,152 | ) | |||||||

| Granting of stock options | 147,440 | 197,888 | ||||||||

| Purchase of treasury shares | (662,215 | ) | (99,045 | ) | ||||||

| Dividends and interest on capital paid to minority interests | (9,532 | ) | (682,058 | ) | ||||||

| Dividends and interest on capital paid | (5,145,831 | ) | (5,003,160 | ) | ||||||

| Net cash provided by (used in) financing activities | (9,990,077 | ) | (8,340,691 | ) | ||||||

| Net increase (decrease) in cash and cash equivalents | 10,041,853 | 20,068,382 | ||||||||

| Cash and cash equivalents at the beginning of the period | 40,935,830 | 37,616,895 | ||||||||

| Effects of changes in exchange rates on cash and cash equivalents | 1,482,945 | 1,246,762 | ||||||||

| Cash and cash equivalents at the end of the period | 4a and 5 | 52,460,628 | 58,932,039 | |||||||

The accompanying notes are an integral part of these financial statements.

ITAÚ UNIBANCO HOLDING S.A.

Consolidated Statement of Added Value

(In thousands of Reais)

| Note | 01/01 to 09/30/2013 | 01/01 to 09/30/2012 | ||||||||||||||||

| Income | 77,308,781 | 78,996,825 | ||||||||||||||||

| Financial operations | 67,629,290 | 76,334,176 | ||||||||||||||||

| Banking services | 17,504,601 | 15,115,477 | ||||||||||||||||

| Result from insurance, pension plan and capitalization operations | 2,649,825 | 2,121,522 | ||||||||||||||||

| Result of loan losses | 8d | (10,739,752 | ) | (14,482,032 | ) | |||||||||||||

| Other | 264,817 | (92,318 | ) | |||||||||||||||

| Expenses | (38,122,486 | ) | (41,734,400 | ) | ||||||||||||||

| Financial operations | (34,242,170 | ) | (37,989,523 | ) | ||||||||||||||

| Other | (3,880,316 | ) | (3,744,877 | ) | ||||||||||||||

| Inputs purchased from third parties | (8,570,618 | ) | (8,614,088 | ) | ||||||||||||||

| Materials, energy and others | 13g | (262,531 | ) | (298,436 | ) | |||||||||||||

| Third-party services | 13g | (2,427,884 | ) | (2,423,464 | ) | |||||||||||||

| Other | (5,880,203 | ) | (5,892,188 | ) | ||||||||||||||

| Data processing and telecommunications | 13g | (2,661,544 | ) | (2,625,572 | ) | |||||||||||||

| Advertising, promotions and publication | 13g | (729,413 | ) | (674,094 | ) | |||||||||||||

| Installations | (883,292 | ) | (955,478 | ) | ||||||||||||||

| Transportation | 13g | (339,510 | ) | (376,322 | ) | |||||||||||||

| Security | 13g | (408,427 | ) | (384,744 | ) | |||||||||||||

| Travel expenses | 13g | (139,939 | ) | (139,182 | ) | |||||||||||||

| Other | (718,078 | ) | (736,796 | ) | ||||||||||||||

| Gross added value | 30,615,677 | 28,648,337 | ||||||||||||||||

| Depreciation and amortization | 13g | (1,388,241 | ) | (1,217,863 | ) | |||||||||||||

| Net added value produced by the company | 29,227,436 | 27,430,474 | ||||||||||||||||

| Added value received from transfer | 15a lll | 264,694 | 189,878 | |||||||||||||||

| Total added value to be distributed | 29,492,130 | 27,620,352 | ||||||||||||||||

| Distribution of added value | 29,492,130 | 27,620,352 | ||||||||||||||||

| Personnel | 10,198,758 | 34.6 | % | 9,206,415 | 33.3 | % | ||||||||||||

| Compensation | 8,138,992 | 27.6 | % | 7,544,363 | 27.3 | % | ||||||||||||

| Benefits | 1,575,454 | 5.3 | % | 1,126,465 | 4.1 | % | ||||||||||||

| FGTS – government severance pay fund | 484,312 | 1.6 | % | 535,587 | 1.9 | % | ||||||||||||

| Taxes, fees and contributions | 7,358,224 | 24.9 | % | 7,051,397 | 25.5 | % | ||||||||||||

| Federal | 6,695,043 | 22.7 | % | 6,499,197 | 23.5 | % | ||||||||||||

| State | 9,997 | 0.0 | % | 18,290 | 0.1 | % | ||||||||||||

| Municipal | 653,184 | 2.2 | % | 533,910 | 1.9 | % | ||||||||||||

| Return on third parties’ assets - Rent | 790,475 | 2.7 | % | 717,942 | 2.6 | % | ||||||||||||

| Return on own assets | 11,144,672 | 37.8 | % | 10,644,598 | 38.5 | % | ||||||||||||

| Dividends and interest on capital | 2,137,760 | 7.2 | % | 2,201,800 | 8.0 | % | ||||||||||||

| Retained earnings (loss) for the period | 8,912,177 | 30.2 | % | 7,900,345 | 28.6 | % | ||||||||||||

| Minority interest in retained earnings | 94,735 | 0.3 | % | 542,453 | 2.0 | % | ||||||||||||

The accompanying notes are an integral part of these financial statements.

ITAÚ UNIBANCO HOLDING S.A.

Balance Sheet

(In thousands of Reais)

| Assets | Note | 09/30/2013 | 09/30/2012 | |||||||

| Current assets | 12,215,047 | 25,146,990 | ||||||||

| Cash and cash equivalents | 45,720 | 15,773 | ||||||||

| Interbank investments | 4b and 6 | 184,405 | 24,007,541 | |||||||

| Money market | 68,892 | 134,362 | ||||||||

| Interbank deposits | 115,513 | 23,873,179 | ||||||||

| Securities and derivative financial instruments | 4c, 4d and 7 | 11,358,780 | 23,455 | |||||||

| Own portfolio | 11,358,780 | 23,455 | ||||||||

| Other receivables | 621,165 | 1,096,828 | ||||||||

| Income receivable | 15a I | - | 24,736 | |||||||

| Sundry | 13a | 621,165 | 1,072,092 | |||||||

| Other assets – prepaid expenses | 4g | 4,977 | 3,393 | |||||||

| Long-term receivables | 39,086,112 | 21,226,554 | ||||||||

| Interbank invesments – interbank deposits | 4b and 6 | 38,338,051 | 14,571,634 | |||||||

| SECURITIES AND DERIVATIVE FINANCIAL INSTRUMENTS | 4c, 4d and 7 | - | 6,462,126 | |||||||

| Own portfolio | - | 6,462,126 | ||||||||

| Other receivables - sundry | 13a | 748,061 | 192,794 | |||||||

| Permanent assets | 56,004,913 | 57,202,675 | ||||||||

| Investments | 56,004,791 | 57,202,478 | ||||||||

| Investments in subsidiaries | 4h and 15a I | 56,004,791 | 57,202,478 | |||||||

| Real estate in use | 4i | 122 | 197 | |||||||

| Total assets | 107,306,072 | 103,576,219 | ||||||||

| Liabilities | ||||||||||

| Current liabilities | 840,582 | 5,974,293 | ||||||||

| Deposits - interbank deposits | 4b and 10b | 104,110 | 5,154,518 | |||||||

| Funds from acceptance and issuance of securities | 4b and 10d | 18,667 | 18,667 | |||||||

| Other liabilities | 717,805 | 801,108 | ||||||||

| Social and statutory | 16b II | 286,569 | 518,960 | |||||||

| Tax and social security contributions | 4n, 4o and 14c | 151,120 | 85,773 | |||||||

| Subordinated debt | 10f | 247,740 | 150,988 | |||||||

| Sundry | 32,376 | 45,387 | ||||||||

| Long-term liabilities | 19,130,706 | 13,441,549 | ||||||||

| Funds from acceptance and issuance of securities | 4b and 10d | 500,000 | 500,000 | |||||||

| Other liabilities | 18,630,706 | 12,941,549 | ||||||||

| Tax and social security contributions | 4n, 4o and 14c | 1,297,293 | 945,131 | |||||||

| Subordinated debt | 10f | 17,315,721 | 11,979,856 | |||||||

| Sundry | 17,692 | 16,562 | ||||||||

| Stockholders' equity | 16 | 87,334,784 | 84,160,377 | |||||||

| Capital | 60,000,000 | 45,000,000 | ||||||||

| Capital reserves | 854,358 | 812,352 | ||||||||

| Revenue reserves | 29,213,757 | 38,685,639 | ||||||||

| Asset valuation adjustment | 4c, 4d and 7d | (815,451 | ) | 1,189,720 | ||||||

| (Treasury shares) | (1,917,880 | ) | (1,527,334 | ) | ||||||

| Total liabilities and stockholders' equity | 107,306,072 | 103,576,219 | ||||||||

The accompanying notes are an integral part of these financial statements.

ITAÚ UNIBANCO HOLDING S.A.

Statement of Income

(In thousands of Reais)

| Note | 01/01 to 09/30/2013 | 01/01 to 09/30/2012 | ||||||||

| Income from financial operations | 2,524,558 | 2,350,694 | ||||||||

| Securities and derivative financial instruments | 2,524,558 | 2,350,694 | ||||||||

| Expenses of financial operations | (750,676 | ) | (747,201 | ) | ||||||

| Money market | (750,676 | ) | (747,201 | ) | ||||||

| Gross income from financial operations | 1,773,882 | 1,603,493 | ||||||||

| Other operating revenues (expenses) | 5,719,218 | 5,836,411 | ||||||||

| Personnel expenses | (175,727 | ) | (153,606 | ) | ||||||

| Other administrative expenses | (26,703 | ) | (30,420 | ) | ||||||

| Tax expenses | 14a II | (171,431 | ) | (162,726 | ) | |||||

| Equity in earnings of subsidiaries | 15a I | 6,133,477 | 6,233,593 | |||||||

| Other operating revenues (expenses) | (40,398 | ) | (50,430 | ) | ||||||

| Operating income | 7,493,100 | 7,439,904 | ||||||||

| Non-operating income | 18,857 | 18,383 | ||||||||

| Income before taxes on income and profit sharing | 7,511,957 | 7,458,287 | ||||||||

| Income tax and social contribution | 4p | 551,962 | 791,970 | |||||||

| Due on operations for the period | (62,566 | ) | 52,052 | |||||||

| Related to temporary differences | 614,528 | 739,918 | ||||||||

| Profit sharing – Management Members - Statutory - Law No. 6,404 of 12/15/1976 | (10,679 | ) | (2,065 | ) | ||||||

| Net income | 8,053,240 | 8,248,192 | ||||||||

| Weighted average of the number of outstanding shares | 16a | 4,968,122,233 | 4,969,731,087 | |||||||

| Net income per share – R$ | 1.62 | 1.66 | ||||||||

| Book value per share - R$ (outstanding at 09/30) | 17.62 | 16.93 | ||||||||

| Supplementary information | ||||||||||

| Exclusion of nonrecurring effects | 2a and 22k | 105,587 | 438,832 | |||||||

| Net income without nonrecurring effects | 8,158,827 | 8,687,024 | ||||||||

| Net income per share – R$ | 1.64 | 1.75 | ||||||||

The accompanying notes are an integral part of these financial statements.

ITAÚ UNIBANCO HOLDING S.A.

Statement of Changes in Stockholders’ Equity (Note 16)

(In thousands of Reais)

| Capital | Capital reserves | Revenue reserves | Asset valuation adjustment (Note 7d) | Retained earnings | (Treasury shares) | Total | ||||||||||||||||||||||

| Balance at 01/01/2012 | 45,000,000 | 763,413 | 34,422,444 | (139,142 | ) | - | (1,663,562 | ) | 78,383,153 | |||||||||||||||||||

| Purchase of treasury shares | - | - | - | - | - | (99,045 | ) | (99,045 | ) | |||||||||||||||||||

| Granting of stock options | - | (102,561 | ) | 65,176 | - | - | 235,273 | 197,888 | ||||||||||||||||||||

| Granting of options recognized | - | 151,500 | - | - | - | - | 151,500 | |||||||||||||||||||||

| Addition to interest on capital paid on 03/13/2012 - year 2011 | - | - | (1,450 | ) | - | - | - | (1,450 | ) | |||||||||||||||||||